UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2018

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______________ to _______________

Commission File Number: 001-37756

Global Water Resources, Inc.

(Exact Name of Registrant as Specified in its Charter)

Delaware | 90-0632193 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

21410 N. 19th Avenue #220, Phoenix, AZ | 85027 |

(Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (480) 360-7775

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock, par value $0.01 per share | The NASDAQ Stock Market, LLC (NASDAQ Global Select Market) | |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities Act. ☐ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 of Section 15(d) of the Act. ☐ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes ☐ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | x | |||

Non-accelerated filer | ☐ | Smaller reporting company | x | |||

Emerging growth company | x | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes x No

The aggregate market value of the common stock held by non-affiliates of the registrant as of the last business day of the registrant’s most recently completed second fiscal quarter (June 30, 2018) was $185.7 million based upon the closing sale price of the registrant’s common stock as reported on the NASDAQ Global Select Market. As of March 4, 2019, the registrant had 21,471,296 shares of common stock, $0.01 par value per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of this Form 10-K, to the extent not set forth herein, is incorporated herein by reference to the registrant’s definitive proxy statement relating to the 2019 annual meeting of stockholders to be filed with the Securities and Exchange Commission not later than 120 days after the end of the registrant’s fiscal year ended December 31, 2018.

EXPLANATORY NOTE

On April 28, 2016, Global Water Resources, Inc. effected a 100.68 to 1.00 stock split. Certain prior period information has been adjusted to conform to the current year presentation to reflect the stock split. All share and per share amounts presented within the financial statements and management’s discussion and analysis of financial condition and results of operations have been retrospectively adjusted to reflect the impact of the stock split.

TABLE OF CONTENTS

PART I. | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II. | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

PART III. | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV. | ||

Item 15. | ||

Item 16. | ||

FORWARD-LOOKING STATEMENTS

Certain statements in this Annual Report on Form 10-K (this “Form 10-K”) of Global Water Resources, Inc. (the “Company”, “GWRI”, “we”, or “us”) and documents incorporated herein by reference are forward-looking in nature and may constitute “forward-looking information” within the meaning of applicable securities laws. Often, but not always, forward-looking statements can be identified by the words “believes”, “anticipates”, “plans”, “expects”, “intends”, “projects”, “estimates”, “objective”, “goal”, “focus”, “aim”, “should”, “could”, “may”, and similar expressions. These forward‑looking statements include, but are not limited to, statements about our strategies; expectations about future business plans, prospective performance, and opportunities, including potential acquisitions; future financial performance; population and growth projections; technologies; revenues; metrics; operating expenses; market trends, including those in the markets in which we operate; liquidity; cash flows and uses of cash; dividends; amount and timing of capital expenditures; depreciation and amortization; tax payments; hedging arrangements; our ability to repay indebtedness and invest in initiatives; impact and resolutions of legal matters; the impact of tax reform; and the impact of accounting changes and other pronouncements. Forward-looking statements should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not, or the times at or by which, such performance or results will be achieved. Investors are cautioned not to place undue reliance on forward-looking information. A number of factors could cause actual results to differ materially from the results discussed in the forward-looking statements, including, but not limited to, the factors discussed under “Risk Factors” in Item 1A of this Form 10-K and future reports that we file from time to time with the Securities and Exchange Commission (“SEC”). Although the forward-looking statements are based upon what management believes to be reasonable assumptions, investors cannot be assured that actual results will be consistent with these forward-looking statements, and the differences may be material. Except as required by law, we undertake no obligation to publicly release the results of any revision to these forward‑looking statements that may be made to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

PART I

ITEM 1. | BUSINESS |

Overview

We are a water resource management company that owns, operates, and manages water, wastewater, and recycled water utilities in strategically located communities, principally in metropolitan Phoenix, Arizona. We seek to deploy our integrated approach, which we refer to as "Total Water Management," a term we use to mean managing the entire water cycle by owning and operating the water, wastewater, and recycled water utilities within the same geographic areas in order to both conserve water and maximize its total economic and social value. We use Total Water Management to promote sustainable communities in areas where we expect growth to outpace the existing potable water supply. Our model focuses on the broad issues of water supply and scarcity and applies principles of water conservation through water reclamation and reuse. Our basic premise is that the world's water supply is limited and yet can be stretched significantly through effective planning, the use of recycled water, and by providing individuals and communities resources that promote wise water usage practices.

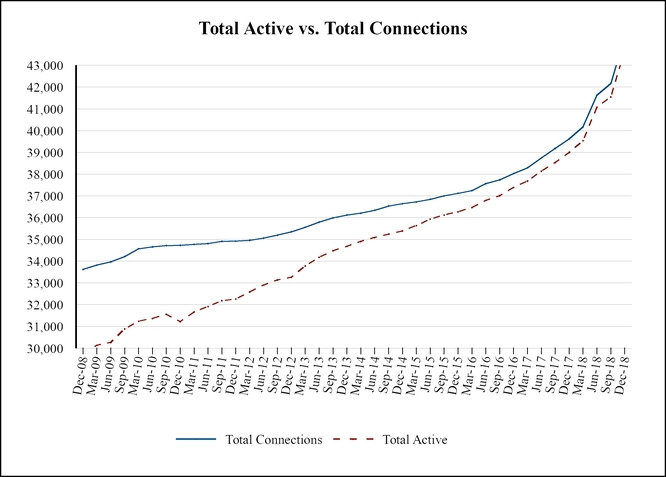

We currently own twelve water and wastewater utilities in strategically targeted communities in metropolitan Phoenix. We currently serve more than 55,000 people in approximately 21,000 homes within our 352 square miles of certificated service areas, which are serviced by seven wholly-owned regulated operating subsidiaries as of December 31, 2018. Approximately 92.8% of our active service connections are customers of our Santa Cruz Water Company, LLC (“Santa Cruz”) and Palo Verde Utilities Company, LLC (“Palo Verde”) utilities, which are located within a single service area. We have grown significantly since our formation in 2003, with total revenues increasing from $4.9 million in 2004 to $35.5 million in 2018, and total service connections increasing from 8,113 as of December 31, 2004 to 44,289 as of December 31, 2018, with regionally planned areas large enough to serve approximately two million service connections.

Our Corporate History

Global Water Resources, LLC (“GWR”) was organized in 2003 to acquire, own, and manage a portfolio of water and wastewater utilities in the southwestern region of the United States (“U.S.”). Global Water Management, LLC (“GWM”) was formed as an affiliated company to provide business development, management, construction project management, operations, and administrative services to GWR and all of its regulated subsidiaries.

-3-

In early 2010, the members of GWR made the decision to raise money through the capital markets, and GWR and GWM were reorganized to form Global Water Resources, Inc., a Delaware corporation. The members established a new entity, GWR Global Water Resources Corp. (“GWRC”), which was incorporated under the Business Corporations Act (British Columbia) on March 23, 2010 to acquire shares of our common stock and to actively participate in our management, business, and operations through its representation on our board of directors and its shared management. On December 30, 2010, GWRC completed its initial public offering in Canada and its common shares were listed on the Toronto Stock Exchange.

On May 3, 2016, GWRC merged with and into the Company (the “Reorganization Transaction”). At the effective time of the merger, holders of GWRC’s common shares received one share of the Company’s common stock for each outstanding common share of GWRC. As a result of the merger, GWRC ceased to exist as a British Columbia corporation and the Company, governed by the corporate laws of the State of Delaware, was the surviving entity. The Reorganization Transaction was conditional upon the concurrent completion of an initial public offering of shares of common stock of the Company in the U.S. (the “U.S. IPO”), which was completed on May 3, 2016.

“Emerging Growth Company” Reporting Requirements

The Company qualifies as an "emerging growth company" as defined in the Jumpstart Our Business Startups Act (the "JOBS Act"). For as long as the Company is deemed to be an emerging growth company, the Company may take advantage of certain exemptions from various regulatory reporting requirements that are applicable to other public companies. Among other things, the Company is not required to (i) provide an auditor's attestation report on the effectiveness of our system of internal control over financial reporting pursuant to Section 404 of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”); (ii) comply with any new rules that may be adopted by the Public Company Accounting Oversight Board ("PCAOB") requiring mandatory audit firm rotation or a supplement to the auditor's report in which the auditor would be required to provide additional information about the audit and the financial statements of the issuer; (iii) comply with any new audit rules adopted by the PCAOB after April 5, 2012 unless the SEC determines otherwise; (iv) comply with any new or revised financial accounting standards applicable to public companies until such standards are also applicable to private companies under Section 102(b)(1) of the JOBS Act; (v) provide certain disclosure regarding executive compensation required of larger public companies; or (vi) hold a nonbinding advisory vote on executive compensation and obtain stockholder approval of any golden parachute payments not previously approved.

As an emerging growth company, the Company has elected to take advantage of the extended transition period for complying with new or revised accounting standards until such standards are also applicable to private companies. As a result of this election, our financial statements may not be comparable with any other public company that is not an emerging growth company (or an emerging growth company that has opted out of using the extended transition provision).

The Company will remain an emerging growth company until the earliest of (i) the last day of the first fiscal year in which our total annual gross revenues exceed $1.07 billion; (ii) the date on which the Company is deemed to be a "large accelerated filer," as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or any successor statute, which would occur if the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter; (iii) the date on which the Company issues more than $1 billion in non-convertible debt during the preceding three-year period; or (iv) the end of the 2021 fiscal year.

U.S. Water Industry Overview

U.S. Water Industry Areas of Business

The U.S. water industry has two main areas of business:

• | Utility Services to Customers. This business includes municipal water and wastewater utilities, which are owned and operated by local governments or governmental subdivisions, and investor-owned water and wastewater utilities. Investor-owned water and wastewater utilities are generally economically regulated, including with respect to rate regulation, by public utility commissions in the states in which they operate. The utility segment is characterized by high barriers to entry, including high capital spending requirements. |

• | General Water Products and Services. This business includes manufacturing, engineering and consulting companies, and numerous other fee-for-service businesses. The activities of these businesses include the building, financing, and operating of water and wastewater utilities, utility repair services, contract operations, laboratory services, manufacturing and distribution of infrastructure and technology components, and other specialized services. At present, and upon the prior sale of the FATHOM™ business and the Loop 303 Contracts (as defined in “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Corporate Transactions” in Part II, Item 7 of this Form 10-K), the Company no longer performs any of these unregulated services. |

-4-

Key Characteristics of the U.S. Water Industry

In the U.S., the water industry is characterized by:

• | Significant Constraints on the Availability of Fresh Water. In Arizona, the Arizona Department of Water Resources estimates that annual water usage is 7 million acre-feet per year. Arizona has the right to use 2.8 million acre-feet from the Colorado River and approximately half of that can be delivered through the Central Arizona Project, a 336 mile diversion canal from the Colorado River to central Arizona. The Colorado River is presently over-allocated, which means that more surface water right allocations have been issued than the actual average annual flow, with allocations being determined based on data from a period during which flows were significantly higher than in recent years. The Central Arizona Project is the only means of transporting Colorado River water into central Arizona. Approximately 41% of the water used in Arizona comes from groundwater. Water in the western U.S. is being pumped from groundwater sources faster than it is replenished naturally, a condition known as overdraft. In areas of water scarcity, such as the arid western U.S., water recycling represents a relatively simple, inexpensive, and energy-efficient means of augmenting water supply as compared to transporting surface water, groundwater, or desalinated water from other locations. Approximately 70% of the water provided by municipalities is currently used for non-potable applications where recycled water could potentially be utilized. |

• | Lack of Technology Utilization to Increase Operating Efficiencies and Decrease Operating Costs. The U.S. water industry has traditionally not taken advantage of advances in technology available to enhance revenue, increase operating efficiencies, and decrease operating costs (including labor and energy costs). Areas of opportunity include automated meter reading, systems management, and administrative functions, such as customer billing and remittance systems. Key drivers for the lack of investment in technology in water and wastewater utilities have been the historical lack of incentives offered or standards imposed by regulators to achieve efficiencies and lower costs and the ownership of the U.S. water utility sector, which largely consists of small, undercapitalized, municipally-owned utilities that lack the financial and technical resources to pursue technology opportunities. |

• | Highly Fragmented Ownership. The utility segment of the U.S. water industry is highly fragmented, with approximately 50,000 water utilities and approximately 16,000 community wastewater utilities, according to the U.S. Environmental Protection Agency ("EPA"). The majority of the approximately 50,000 water utilities are small, serving a population of 500 or less, and 86% of the water utilities serve only 10% of the population. |

• | Large Public Sector Ownership. Municipally-owned utilities provide water and wastewater services for the vast majority of the U.S. population. For homes connected to a community water system, approximately 80% are provided service by municipally-owned utilities. For homes connected to a community wastewater system, about 75% are provided service by municipally-owned utilities. |

• | Aging Infrastructure in Need of Significant Capital Expenditures. Water infrastructure in the U.S. is aging and requires significant investment and stringent focus on cost control to upgrade or replace aging facilities and to provide service to growing populations. Throughout the U.S., utilities are required to make expenditures on the rehabilitation of existing utilities and on the installation of new infrastructure to accommodate growth and make improvements to water quality and wastewater discharges mandated by stricter water quality standards. Water quality standards, first introduced with the Clean Water Act in 1972 and the Safe Drinking Water Act in 1974, are becoming increasingly stringent and numerous. For water, the American Water Works Association estimates investment needs for buried drinking water infrastructure total more than $1 trillion over the next 25 years. The American Society of Civil Engineers estimates capital investment needs to update and grow the nation’s wastewater systems may be as much as $271 billion over the next twenty years. |

Private Sector Opportunities

Municipal water utilities typically fund their capital expenditure needs through user-based water and wastewater rates, municipal taxes, or the issuance of bonds. However, raising large amounts of funds required for capital investment is often challenging for municipal water utilities, which affects their ability to fund capital spending. Many smaller utilities also do not have the in-house technical and engineering resources to manage significant infrastructure or technology-related investments. In order to meet their capital spending challenges and take advantage of technology-related operating efficiencies, many municipalities are examining a combination of outsourcing and partnerships with the private sector or outright privatizations.

• | Outsourcing involves municipally-owned utilities contracting with private sector service providers to provide services, such as meter reading, billing, maintenance, or asset management services. |

• | Public-private partnerships among government, operating companies, and private investors include arrangements, such as design, build, operate contracts; build, own, operate, and transfer contracts; and own, leaseback, and operate contracts. |

-5-

• | Privatization involves a transfer of responsibility for, and ownership of, the utility from the municipality to private investors. |

We believe investor-owned utilities that have greater access to capital are generally more capable of making mandated and other necessary infrastructure upgrades to both water and wastewater utilities, addressing increasingly stringent environmental and human health standards, and navigating a wide variety of regulatory processes. In addition, investor-owned utilities that achieve larger scales are able to spread overhead expenses over a larger customer base, thereby reducing the costs to serve each customer. Since many administrative and support activities can be efficiently centralized to gain economies of scale and sharing of best practices, companies that participate in industry consolidation have the potential to improve operating efficiencies, lower costs, and improve service at the same time.

Our Strategy

We are a water resource management company that provides water, wastewater, and recycled water utility services. We believe we are a leader in Total Water Management practices, such as water scarcity management and advanced water recycling applications. Our long-term goal is to become one of the largest investor-owned operators of integrated water and wastewater utilities in areas of the arid western U.S. where water scarcity management is necessary for long-term economic sustainability and growth.

Our growth strategy involves the elements listed below:

• | acquiring or forming utilities in the path of prospective population growth; |

• | expanding our service areas geographically and organically growing our customer base within those areas; and |

• | deploying our Total Water Management approach into these utilities and service areas. |

We believe this plan can be executed in our current service areas and in other geographic areas where water scarcity management is necessary to support long-term growth and in which regulatory authorities recognize the need for water conservation through water recycling.

Total Water Management is a demand-side-management framework (in that it is a solution intended to drive down demand for renewable supplies versus develop new renewable water supplies) that alleviates the pressures of water scarcity in communities where growth is reasonably expected to outpace potable water supply. Built on an all-encompassing view of the water cycle, Total Water Management promotes sustainable community development through reduced potable water consumption while monetizing the value of water through each stage of delivery, collection, and reuse.

Our business model applies Total Water Management in high growth communities. Components of our Total Water Management approach include:

• | Regional planning to reduce overall design and implementation costs, leveraging the benefits of replicable designs, gaining the benefits of economies of scale, and enhancing the Company’s position as a primary water and wastewater service provider in the region. |

◦ | For example, the Company has secured three separate area-wide Clean Water Act Section 208 Regional Water Quality Management Plans in its major planning areas, covering more than 500 square miles of land. To obtain these plans, a provider must develop, amongst other things, a regional wastewater solution, including plans for engineering, infrastructure location and size, and goals for the management of treated reclaimed water, which the Company successfully demonstrated in obtaining its plans. |

• | Stretching a limited resource by maximizing the use of recycled water, using renewable surface water where available and recharging aquifers with any available excess water. |

◦ | For example, the Company’s water recycling model has been fully implemented in the City of Maricopa. The Company is the water, wastewater, and recycled water provider for the City of Maricopa, which currently has a population of approximately 50,000. A community of this size produces an approximate annual average of 2.6 million gallons of wastewater per day. Because the Company requires developers to take back and utilize recycled water within their communities and invest in “purple pipe” recycled water infrastructure during the initial development of subdivisions, the Company is now able to distribute almost all of the 2.6 million gallons back to the community for beneficial purposes. Approximately 90% of the recycled water goes towards common area non-potable irrigation and for use at a local farm, which allows for the recycled water to naturally recharge into the aquifer. This reduces the total amount of limited ground or |

-6-

surface water that would otherwise be required within the community by over 40%. To date, the Company has reused 7.6 billion gallons of recycled water in the City of Maricopa.

• | Integrating and standardizing water, wastewater, and recycled water infrastructure delivery systems using a separate distribution system of purple pipes to conserve water resources, reduce energy, treatment, and consumable costs (e.g., chemicals, filter media, other general materials, and supplies), provide operational efficiencies, and align the otherwise disparate objectives of water sales and conservation. |

◦ | In addition to the previous example, which related to the requirements for recycled water usage, the separate distribution system of purple pipes, and water conservation achievements, the Company believes that its model results in additional benefits from an economic perspective due to lower use of power and consumables. For every gallon of recycled water that is directly reused while already on land surface, the need to pump additional scarce groundwater and surface water is eliminated. Such additional groundwater and surface water would otherwise need to be treated and distributed in accordance with the Safe Drinking Water Act, which is costly and requires a lot of energy. |

• | Gaining market and regulatory acceptance of broad utilization of recycled water through agreements with developers, strategic relationships with governments, academic research, and publication as industry experts, coupled with public education and community outreach campaigns. |

◦ | For example, the Company has public-private partnerships formally adopted through memorandums of understanding with the City of Maricopa, the City of Casa Grande, and the City of Eloy. Each memorandum of understanding reflects the Company’s intent to deploy Total Water Management. The Company also has 154 infrastructure coordination and financing agreements with landowners or developer entities that include requirements for usage of recycled water and other attributes that support the Company’s Total Water Management model. As discussed above, the Company’s integrated provider model, which is focused on the maximum use of recycled water, underpins its Clean Water Act Section 208 Regional Water Quality Management Plans and Designations of Assured Water Supply. In addition, the Company has won numerous awards for education, outreach, and conservation in the water industry. Further, the Company’s experts have published academic papers regarding Total Water Management, as well as provided insight to industry publications. |

• | Incorporating automated processes, such as supervisory control and data acquisition, automated meter reading, and back-office technologies and “green” billing, which reduce operating costs and manpower requirements, improve system availability and reliability, and improve customer interface. |

◦ | Supervisory Control and Data Acquisition. The Company employs supervisory control and data acquisition in all of its utility systems, which provides continuous monitoring, instantaneous alarming, and historical trending on all key operating assets, including instrumentation and dynamic components (e.g., pumps, motor controlled valves, treatment systems, etc.). This data is reported back to the appropriate operations personnel through a standard industry software known as Wonderware. The benefits of this system include the significantly enhanced ability to: achieve compliance and safety mandates; reduce service outages; troubleshoot systems; provide for remote operations; and allow for proactive maintenance and lower costs related to efficient real-time operations |

◦ | Automated Meter Reading. The Company implements automated meter reading by utilizing the FATHOM™ platform’s Automated Reading Infrastructure technology, with over 99% of all meters being read by such technology. This technology reads each meter numerous times per day (often hourly) and continuously transmits the meter readings back to a centralized data base through a communications tower and cellular transmission units. The data is then presented to the utility, and may be available to customers, through a simple user interface. Reading meters at this frequency provides many benefits to both the utility and the customer. With this data, utilities can better model demand usage, identify system water loss, identify leaks on the customer side of the meter, monitor for abnormal usage, and present interval, hourly, daily, weekly, or monthly usage back to the customers. |

-7-

◦ | Back-Office Technologies and Paperless Billing. The Company employs a series of technologies that allow for the complete automation of the billing and remittance process. The Company also provides its customers with over seven ways to pay, with the majority of options being integrated with the Company’s back-office technologies. In combination with automated meter reading, this suite of technology has minimized the use of human labor and reduced the potential for human error for the entire billing and remittance process, while providing better customer service. |

We believe our Total Water Management-based business model provides us with a significant competitive advantage in high growth, water scarce regions. Based on our experience and discussions with developers, we believe developers prefer our approach because it provides a bundled solution to infrastructure provision and improves housing density in areas of scarce water resources. Developers are also focusing on increased consumer and regulatory demands for environmentally friendly or “green” housing alternatives. Communities prefer the approach because it provides a partnering platform which promotes economic development, reduces their traditional dependence on bond financing and ensures long term water sustainability.

Our competitive advantage facilitates the execution of our growth strategy. Our proven conservation methods lead to successful permitting for more connections in expanded and new service areas.

Our Regulated Utilities

We own and operate regulated water, wastewater and recycled water utilities in communities principally located in metropolitan Phoenix. Our utilities are regulated by the Arizona Corporation Commission (the “ACC”), as described further under “—Regulation—Arizona Regulatory Agencies” below. As of December 31, 2018, our utilities collectively had 43,687 active service connections offering predictable rate-regulated cash flows. Revenues from our regulated utilities accounted for approximately 92.9% of total revenues in 2018. Our utilities currently possess the high-level regional permits that allow us to implement our business model; thus, we believe we are well-positioned for organic growth in our current service areas that are generally located in Arizona’s population growth corridors: Maricopa/Casa Grande, West Valley, and Sun Corridor Region.

A key component of our water utility business is the use of recycled water. Recycled water is highly treated and purified wastewater that is distributed through a separate distribution system of purple pipes for a variety of beneficial, non-potable uses. Recycled water can be delivered for all common area irrigation needs, as well as delivered direct to homes where it can be used for outdoor residential irrigation. Total Water Management model, an integrated approach to the use of potable and non-potable water to manage the entire water cycle, both conserves water and maximizes its total economic value. The application of the Total Water Management model has proven to be effective as a means of water scarcity management that promotes sustainable communities and helps achieve greater dwelling unit density in areas where the availability of sustainable water can be a key constraint on development. Our implementation of the Total Water Management philosophy in Arizona has led to the development of relationships with key regulatory bodies.

-8-

A summary description of our water utilities at December 31, 2018 is set forth in the following table and described in more detail below:

Company | Date of Acquisition (A) or Formation (F) | Service Provided | Square Miles of Service Area (1) | Active Service Connections | Average Monthly Rate Per Service Connection | |||||||||

MARICOPA / CASA GRANDE REGION | ||||||||||||||

Global Water-Santa Cruz Water Company | 2004 (A) | Water | 73 | 20,385 | $ | 57 | ||||||||

Global Water-Palo Verde Utilities Company | 2004 (A) | Wastewater and Recycled Water | 102 | 20,150 | $ | 72 | ||||||||

Global Water - Turner Ranches Irrigation, LLC | 2018 (A) | Water | 7 | 963 | 80 | |||||||||

WEST VALLEY REGION | ||||||||||||||

Water Utility of Greater Tonopah | 2006 (A) | Water | 105 | 341 | $ | 103 | ||||||||

Water Utility of Northern Scottsdale | 2006 (A) | Water | 1 | 87 | $ | 222 | ||||||||

Eagletail Water Company | 2017 (A) | Water | 8 | 56 | $ | 86 | ||||||||

Balterra Sewer Corp | 2008 (A) | Wastewater and Recycled Water | 2 | — | — | |||||||||

Hassayampa Utility Company | 2005 (F) | Wastewater and Recycled Water | 41 | — | — | |||||||||

SUN CORRIDOR REGION | ||||||||||||||

Global Water - Picacho Cove Water Company | 2006 (F) | Water | 2 | — | — | |||||||||

Global Water - Picacho Cove Utilities Company | 2006 (F) | Wastewater and Recycled Water | 2 | — | — | |||||||||

Global Water - Red Rock Utilities, LLC | 2018 (A) | Water, Wastewater and Recycled Water | 9 | 1,705 | 72 | |||||||||

Total | 352 | 43,687 | ||||||||||||

(1) Certified areas may overlap in whole or in part for separate utilities.

Maricopa/Casa Grande Region

The City of Maricopa is located approximately 12 miles south of Phoenix. The relative proximity to a significant urban center, coupled with relatively abundant and inexpensive land, were the key drivers of the real estate boom experienced by this community. In 2005, the City of Maricopa was one of the fastest growing cities in the nation. While growth has slowed nationally since 2007, the City of Maricopa continues to grow, as demonstrated by our addition of 9,920 active service connections (representing approximately 4,900 homes) from December 2009 to December 2018. Development in the area is considered to be affordable and represents one of the few areas within the U.S. where a new home can be purchased from the mid $100,000s.

We operate in this region through Santa Cruz, Palo Verde, Turner Ranches Water and Sanitation Company ("Turner"), and Red Rock Utilities ("Red Rock").

We acquired Santa Cruz and Palo Verde in 2004. Santa Cruz serves 20,385 active service connections as of December 31, 2018 and revenues from Santa Cruz represented approximately 42.5 % and 42.7% of our total revenue for the years ended December 31, 2018 and 2017, respectively. Palo Verde serves 20,150 active service connections as of December 31, 2018 and revenues from Palo Verde represented approximately 52.9% and 52.6% of our total revenue for the years ended December 31, 2018 and 2017, respectively.

The Santa Cruz and Palo Verde service areas include approximately 175 square miles, which we believe provide further opportunities for growth once development returns to these areas and water and wastewater utility services are required. Most of the Santa Cruz and Palo Verde infrastructure is less than fifteen years old. Santa Cruz and Palo Verde provide water and wastewater services, respectively, under an innovative public- private partnership memorandum of understanding with the City of Maricopa in Pinal

-9-

County for approximately 278 square miles of its planning area. We signed a similar memorandum of understanding with the City of Casa Grande to partner in providing water, wastewater, and recycled water services to an approximate 100 square miles of its western region for anticipated growth.

Rate proceedings were completed in 2010 for both Santa Cruz and Palo Verde. In July 2012, these two utilities filed applications with the ACC for increased rates using 2011 as the test year on which the ACC will use to evaluate the utilities’ rates. The rate proceedings were completed in February 2014. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Recent Rate Case Activity”, included in Part II, Item 7 of this Form 10-K, for additional information.

We acquired CP Water Company (“CP Water”) in 2006. CP Water provided water service within parts of Pinal County. CP Water received a Certificate of Convenience and Necessity (“CC&N”) for approximately two square miles of service area in 1984 and currently has 12 active service connections. We acquired this small utility as part of our consolidation strategy to enable the deployment of new integrated infrastructure as development occurs in the corridor between the cities of Maricopa and Casa Grande. CP Water’s service area, customers, and assets have been transferred to Santa Cruz.

We acquired Turner in May 2018. Turner is a non-potable irrigation water utility located in Mesa, Arizona, with approximately seven square miles of service area. Turner serves 963 residential irrigation customers as of December 31, 2018.

West Valley Region

We operate in this region through Water Utility of Greater Tonopah (“Greater Tonopah”), Water Utility of Northern Scottsdale, Inc. (“Northern Scottsdale”), Balterra Sewer Corp (“Balterra”), and Hassayampa Utility Company Inc. (“Hassayampa”), and formerly through Valencia Water Company, Inc. (“Valencia”), Water Utility of Greater Buckeye (“Greater Buckeye”) and Willow Water Valley Co., Inc. (“Willow Valley”).

We acquired Greater Tonopah in 2006. Greater Tonopah serves 341 active service connections as of December 31, 2018. Greater Tonopah has a CC&N for 105 square miles of service area and provides water services to Maricopa County west of the Hassayampa River. The acquisition of Greater Tonopah allowed us to enter into agreements with developers to serve a total of roughly 100,000 home sites plus commercial, schools, parks, and industrial developments.

In November 2017, the Bill and Melinda Gates Investment Group, through an investment vehicle, acquired 20,000 acres in the Belmont development, located in the West Valley Region. Belmont is a mixed use, master planned community and is included within the service area of Greater Tonopah and Hassayampa.

We acquired Northern Scottsdale in 2006. Northern Scottsdale serves 87 active service connections as of December 31, 2018. Northern Scottsdale has a CC&N for one square mile and provides water services to two small subdivisions in Northern Scottsdale.

Rate proceedings were completed in 2010 for Greater Tonopah. Northern Scottsdale completed a rate proceeding in 2008. In July 2012, these five utilities in the West Valley Region filed applications with the ACC for increased rates using 2011 as the test year on which the ACC evaluates the utilities’ rates. The rate proceedings were completed in February 2014. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Recent Rate Case Activity”, included in Part II, Item 7 of this Form 10-K, for additional information.

We acquired Balterra in 2006. Balterra is a wastewater utility and has a CC&N for two square miles in an area in western Maricopa County known as Tonopah. Balterra currently has no active service connections; however, its service area lies directly in the expected path of future growth in the far west valley of metropolitan Phoenix, which we believe should provide opportunities for growth once development commences in this area.

We formed Hassayampa in 2005. Hassayampa is a wastewater utility and has a CC&N for 41 square miles in an area that is contiguous to Balterra. Hassayampa currently has no active service connections; however, like Balterra, its service area lies directly in the path of future growth in the far west valley of metropolitan Phoenix, which we believe should provide opportunities for growth once development commences in this area.

In October 2012, we and our subsidiary, 303 Utilities Company, and the City of Glendale entered into an agreement for future wastewater and recycled water services, advancing our public-private-partnership originally approved by the city council in March 2010. The agreement named 303 Utilities Company as the future wastewater and recycled water provider for a 7,000-acre territory within a portion of Glendale’s western planning area known as the Loop 303 Corridor. The 303 Utilities Company also signed certain wastewater facilities main extension agreements with numerous developers/landowners in the service area to fund the initial design and construction of a wastewater and recycled water utility. In addition, we signed separate offsite water management agreements with these same developers/landowners to provide the coordination, permitting, and engineering work for the related water utility service element of the project. In September 2013, we entered into an agreement to sell the Loop 303 Contracts to a

-10-

third-party. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Corporate Transactions—Sale of Loop 303 Contracts”, included in Part II, Item 7 of this Form 10-K, for additional information.

We formerly operated additional utilities in the West Valley Region through Valencia, Greater Buckeye and Willow Valley. Valencia was consolidated with Greater Buckeye in 2008, and on July 14, 2015, we closed the stipulated condemnation to transfer the operations and assets of Valencia to the City of Buckeye. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Corporate Transactions—Stipulated Condemnation of the Operations and Assets of Valencia”, included in Part II, Item 7 of this Form 10-K, for additional information.

In addition, on May 9, 2016, we closed the sale of Willow Valley to EPCOR Water Arizona Inc. (“EPCOR”). See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Corporate Transactions—Sale of Willow Valley”, included in Part II, Item 7 of this Form 10-K, for additional information.

On May 15, 2017, we acquired Eagletail Water Company ("Eagletail") via merger. Eagletail serves 56 active connections as of December 31, 2018. Eagletail has a CC&N for eight square miles located west of metropolitan Phoenix.

Sun Corridor Region

The Sun Corridor Region is approximately equidistant between Phoenix and Tucson, along the I-10 Corridor.

We operate in this region through Global Water-Picacho Cove Water Company, Global Water-Picacho Cove Utilities Company (collectively, “Picacho Cove”) and Red Rock. We formed Picacho Cove in 2006 to provide water and wastewater services in the City of Eloy and currently have a CC&N for two congruent square miles. The utilities currently have 1,705 active service connections and no facilities.

We acquired Red Rock in October 2018. Red Rock consists of a water and a wastewater utility with service areas in the Pima and Pinal counties of Arizona, with approximately nine square miles of service area. Red Rock serves 859 water customers and 846 sewer customers as of December 31, 2018.

Operations

We treat water to potable standards and also treat, clean, and recycle wastewater for a variety of non-potable uses. A description of these operations follows.

Sources of Water Supply

Our water supplies are primarily derived from groundwater; however, we currently augment these supplies with recycled water and intend to augment them with surface water and increased use of recycled water in the future.

• | Potable Water. Our utilities presently employ groundwater systems for potable water production. Water is brought to the surface from underground aquifers (water levels vary from approximately 60 to 500 feet below land surface depending on the area), disinfected and stored in tanks for distribution to customers. In some instances, individual raw water supplies do not meet the legislative requirements for certain constituents. In those cases, we use well-head, centralized, point-of-use, or blending treatment systems to ensure water quality meets potable standards. |

• | Recycled Water. Recycled water is created by taking wastewater and applying advanced tertiary treatment (i.e., screening, biological reduction, and filtration and disinfection processes) to create a high quality, non-potable water source. Each step is monitored and controlled in order that the stringent requirements for recycled water are continuously met. Recycled water generated by us meets Arizona’s Aquifer Water Quality Standards before it leaves the treatment facility and is recognized as Class A+, the highest quality of recycled water regulated by the Arizona Department of Environmental Quality. Recycled water can be used for irrigation, facilities cooling, and industrial applications and in a residential setting for toilet flushing and lawn watering. |

See “Risk Factors-Operational Factors-There is no guaranteed source of water,” included in Part I, Item 1A of this Form 10-K, for additional information.

Technology

We use sophisticated technology as a principal means of improving our margins. We focus on technological innovations that allow us to deliver high-quality water and customer service with minimal potential for human error, delays, and inefficiencies. The comprehensive technology platform that we use includes supervisory control and data acquisition, automated meter reading, and

-11-

geographical information system technologies, which we use to map and monitor our physical assets and water resources on an automated, real-time basis with fewer people than the standard water utility model requires. Our systems allow us to detect and resolve potential problems promptly, accurately, and efficiently before they become more serious, which both improves customer service and optimizes and extends the efficient performance and life of our assets. The comprehensive technology platform that we use includes automated meter reading technology, which allows us to read water meters remotely rather than physically, improves water resources accounting, allows for identification of high water usage and water theft from disconnected meters. We also use automated voice, internet billing, payment processing, and customer service applications that contribute to additional reduced headcount and a reduction in associated personnel costs.

Decentralized Treatment Facilities

We design and build standard, decentralized facilities that are scaled to the service areas they serve in order to achieve optimum efficiency in providing both water and wastewater services. The replication of our standard facility also improves design, construction, and operating efficiency because we are able to employ similar, proven processes and equipment and technologies at each of our facilities. As a result, our operating efficiency is improved significantly by reducing equipment costs and employee training costs, and our exposure to operational performance risks often associated with larger, custom-built plants is reduced.

Although there has not traditionally been a significant economic incentive or other reward for automation and resource efficiency in our industry, we believe our use of automation in lieu of labor, together with our emphasis on streamlined operations and conservation, will position us well for continued profitable growth and allow us to take advantage of future incentives or rewards that may be available to water utilities that are able to successfully enhance the use of renewable resources.

Regulation

Our water and wastewater utility operations are subject to extensive regulation by U.S. federal, state, and local regulatory agencies that enforce environmental, health and safety requirements, which affect all of our regulated subsidiaries. These requirements include the Safe Drinking Water Act, the Clean Water Act, and the regulations issued under these laws by the EPA. We are also subject to state environmental laws and regulations, such as Arizona’s Aquifer Protection Program and other environmental laws and regulations enforced by the Arizona Department of Environmental Quality, and extensive regulation by the ACC, which regulates public utilities. The ACC also has broad administrative power and authority to set rates and charges, determine service areas and conditions of service, and authorize the issuance of securities as well as authority to establish uniform systems of accounts and approve the terms of contracts with both affiliates and customers.

We are also subject to various federal, state, and local laws and regulations governing the storage of hazardous materials, the management and disposal of hazardous and solid wastes, discharges to air and water, the cleanup of contaminated sites, dam safety, fire protection services in the areas we serve, and other matters relating to the protection of the environment, health, and safety.

We maintain a comprehensive environmental program which addresses, among other things, responsible business practices and compliance with environmental laws and regulations, including the use and conservation of natural resources. Water samples across our water system are analyzed on a regular basis in material compliance with regulatory requirements. We conducted more than 10,600 water quality tests in 2018 at subcontracted laboratory facilities in addition to providing continuous online instrumentations for monitoring parameters such as turbidity and disinfectant residuals and allowing for adjustments to chemical treatment based on changes in incoming water quality. For 2018, we achieved a compliance rate of 99.9% for meeting state and federal drinking water standards and 99.8% for compliance with wastewater requirements, for an overall compliance rating of 99.8%. Compliance with governmental regulations is of utmost importance to us, and considerable time and resources are spent ensuring compliance with all applicable federal, state, and local laws and regulations.

In addition to regulation by governmental entities, our operations may also be affected by civic or consumer advocacy groups. These organizations provide a voice for customers at local and national levels to communicate their service priorities and concerns. Although these organizations may lack regulatory or enforcement authority, they may be influential in achieving service quality and rate improvements for customers.

Safe Drinking Water Act

The federal Safe Drinking Water Act and regulations promulgated thereunder establish minimum national quality standards for drinking water. The EPA has issued rules governing the levels of numerous naturally occurring and man-made chemical and microbial contaminants and radionuclides allowable in drinking water and continues to propose new rules. These rules also prescribe testing requirements for detecting contaminants, the treatment systems that may be used for removing contaminants, and other requirements. Federal and state water quality requirements have become increasingly more stringent, including increased water

-12-

testing requirements, to reflect public health concerns. In Arizona, the requirements of the Safe Drinking Water Act are incorporated by reference into the Arizona Administrative Code.

In order to remove or inactivate microbial organisms, the EPA has promulgated various rules to improve the disinfection and filtration of drinking water and to reduce consumers’ exposure to disinfectants and by-products of the disinfection process.

Contaminants of emerging concern (CECs) are chemicals and other substances that have no regulatory standard, but have been discovered in water or in the environment where they had not previously been detected, or were only present at insignificant levels. We believe contaminants of emerging concern may form the basis for additional regulatory initiatives and requirements in the future. We rely on governmental agencies to establish regulatory standards regarding contaminants of emerging concern and we meet or exceed these standards, when established.

Although it is difficult to project the ultimate costs of complying with the above or other pending or future requirements, we do not expect current requirements under the Safe Drinking Water Act to have a material impact on our operations or financial condition, although it is possible new methods of treating drinking water may be required if additional regulations become effective in the future. In addition, capital expenditures and operating costs to comply with environmental mandates traditionally have been recognized by state public utility commissions as appropriate for inclusion in establishing rates, although rate recovery may be delayed by “regulatory lag”, that is, the delay between the utility’s test year and the issuance of a rate order approving new rates.

Clean Water Act

The federal Clean Water Act regulates discharges of liquid effluents from drinking water and wastewater treatment facilities into waters of the U.S., including lakes, rivers, streams and subsurface, or sanitary sewers. In Arizona, with the exception of Clean Water Act Section 208 Regional Water Quality Management Plans, capacity management and operations and maintenance requirements, and source control requirements, wastewater operations are primarily regulated under the Aquifer Protection Permit program and the Arizona Pollutant Discharge Elimination System program (see below).

The EPA certifies Clean Water Act Section 208 Regional Water Quality Management Plans and Amendments which govern the location of water reclamation facilities and wastewater treatment plants. The EPA’s 40 C.F.R. Pt. 503 bio-solids requirements are reported to the EPA through the Arizona Department of Environmental Quality. While we are not presently regulated to meet source control requirements, we maintain source control through various Codes of Practice that have been accepted by the ACC as enforceable limits on consumer discharges to sanitary sewer systems. We believe we maintain the necessary permits and approvals for the discharges from our water and wastewater facilities.

Arizona Regulatory Agencies

In Arizona, the ACC is the regulatory authority with jurisdiction over water and wastewater utilities. The ACC has exclusive authority to approve rates, mandate accounting treatments, authorize long-term financing programs, evaluate significant capital expenditures and plant additions, examine and regulate transactions between a regulated subsidiary and its affiliated entities, and approve or disapprove reorganizations, mergers, and acquisitions prior to their completion. Additionally, the ACC has statutory authority to oversee service quality and consumer complaints, and approve or disapprove expansion of service areas. The ACC is comprised of five elected members, each serving four year terms. Companies that wish to provide water or wastewater service are granted a CC&N, which allows them to serve customers within a geographic area specified by a legal description of the property. In considering an application for a CC&N, the ACC will determine if the applicant is fit and proper to provide service within a specified area, whether the applicant has sufficient technical, managerial, and financial capabilities to provide the service, and if that service is necessary and in the public interest. Once a CC&N is granted, the utility falls under the ACC’s jurisdiction and must abide by the rules and laws by which a public service corporation operates. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Recent Rate Case Activity,” included in Part II, Item 7 of this Form 10-K, for additional information regarding rate case activity involving the ACC.

-13-

Arizona water and wastewater utilities must also comply with state environmental regulation regarding drinking water and wastewater, including environmental regulations set by Councils of Government (such as the Central Arizona Governments and the Maricopa Association of Governments), the Arizona Department of Environmental Quality, and the Arizona Department of Water Resources. The Central Arizona Governments is the designated management authority for Section 208 of the Clean Water Act for Pinal and Gila Counties and administers the requirements of the Regional Water Quality Management Plans and Amendments at the local level. The Maricopa Association of Governments is the designated management authority for Section 208 of the Clean Water Act for Maricopa County and administers the requirements of the Regional Water Quality Management Plans and Amendments at the local level. The Maricopa County Environmental Services Department has delegated authority for overseeing Arizona Department of Environmental Quality requirements in Maricopa County. The Arizona Department of Environmental Quality regulates water quality and permits water reclamation facilities, discharges of recycled water, re-use of recycled water, and recharge of recycled water. The Arizona Department of Environmental Quality also regulates the clean closure requirements of facilities. In Arizona, the Arizona Department of Environmental Quality has received delegated authority from the EPA for the administration of the Clean Water Act’s National Pollution Discharge Elimination System program. Permits issued by the Arizona Department of Environmental Quality for discharges to waters of the U.S. in Arizona are termed “Arizona Pollutant Discharge Elimination System,” or “AzPDES,” permits. The Arizona Department of Environmental Quality also administers the drinking water quality requirements set by the federal Safe Drinking Water Act within Arizona. Finally, the Arizona Department of Water Resources regulates surface water extraction, groundwater withdrawal, designations and certificates of assured water supply, extinguishment of irrigation grandfathered water rights, groundwater savings facilities, recharge facilities, recharge permits, recovery well permits, storage accounts, and well construction, abandonment, or replacement. We must file periodic reports with the ACC, Arizona Department of Environmental Quality, and Arizona Department of Water Resources.

Within each regulatory organization, we have invested in developing cooperative relationships at all levels, from staff to executives to elected and appointed officials, and have adopted a proactive attitude toward regulatory compliance.

Assured and Adequate Water Supply Regulations

We intend to seek access to renewable water supplies as we grow our water resource portfolio. However, we currently rely almost exclusively (and are likely to continue to rely) on the pumping of groundwater and the generation and delivery of recycled water for non-potable uses to meet future demands in our service areas. Aside from some rights to water through the Central Arizona Project, groundwater (and recycled water derived from groundwater) is the only water supply available to us.

Although we intend to rely on recycled water to help meet water demands in areas, the infrastructure, permits, and customer base necessary to generate and deliver recycled water are not necessarily in place in most of our service areas. In addition, although recycling can extend a limited supply, it does not actually generate a new supply of water. As such, although our proposed generation and delivery of recycled water is likely to help reduce the amount of groundwater that will be required to serve future customers, our ability to serve new customers will remain dependent on its ability to access groundwater. Groundwater is a limited resource in Arizona, and access to new uses of groundwater is closely regulated in the areas served by us. See “Risk Factors—Operational Factors—Inadequate water and wastewater supplies could have a material adverse effect upon our ability to achieve the customer growth necessary to increase our revenues,” included in Part I, Item 1A of this Form 10-K, for additional information.

Nearly all of our service areas are located in “Active Management Areas,” areas within which the use of groundwater is regulated by the Arizona Department of Water Resources in order to manage ongoing problems with groundwater overdraft. The Phoenix, Prescott, and Tucson Active Management Areas are legally mandated to achieve “safe yield” by 2025 or sooner. However, we do not expect any of these Active Management Areas to achieve their safe yield goals. Safe yield requires groundwater pumping to not draw down the groundwater aquifers, or “over-draft,” as all pumping is offset or replaced within the Active Management Area from a renewable supply. The Pinal Active Management Area, which encompasses our major service areas near Maricopa, is managed to allow development of non-irrigation uses and to preserve existing agricultural economies in the Active Management Area for as long as feasible, consistent with the necessity to preserve future water supplies for non-irrigation uses.

-14-

Under Arizona’s assured water supply laws and regulations, a new subdivision inside an Active Management Area must demonstrate that it has an “assured water supply” to the satisfaction of the Arizona Department of Water Resources before the developer is permitted to sell lots. Demonstration of an assured water supply requires, among other things, that an applicant demonstrate that water supplies will be physically, continuously, and legally available to satisfy the water needs of the proposed use for at least 100 years. A developer may make an independent showing of an assured water supply (resulting in a Certificate of Assured Water Supply for a subdivision) or may obtain a written commitment for service from a designated water supplier, such as a privately owned water company or a municipal water supplier. Under the latter approach, the water supplier must demonstrate satisfaction of assured water supply requirements for the developments within its service areas (resulting in a Designation of Assured Water Supply for the provider). At present, we have obtained a Designation of Assured Water Supply in the Maricopa/Casa Grande service territory (Santa Cruz) for approximately 22,900 acre-feet of groundwater use. A Designation of Assured Water Supply is subject to periodic review and renewal by the Arizona Department of Water Resources, and can be increased as demand grows within the service territory, subject to the physical availability of water. A recent physical availability determination for Santa Cruz suggests that, over time, its Designation of Assured Water Supply could potentially be increased to approximately 45,000 acre-feet once sufficient increased demand is established in the area, assuming that water is still physically available by that time (i.e., the groundwater has not been committed to users in surrounding areas). Under our high efficiency Total Water Management model, which is intended to achieve much lower per-unit potable water use rates than would be expected for average developments, 45,000 acre-feet could be sufficient water supply for approximately 180,000 homes per year.

In our West Valley service territory (Greater Tonopah), we expect to receive a Designation of Assured Water Supply in the future. Assuming implementation of our high-efficiency Total Water Management model throughout the service area, this could be a sufficient water supply for approximately 250,000 homes. There is no assurance that the Arizona Department of Water Resources would add any additional acre-feet to any of our Designations of Assured Water Supply in the future.

In our other service areas, we rely upon a Certificate of Assured Water Supply obtained by developers to demonstrate an assured water supply, or will apply for a Designation of Assured Water Supply in the future when required.

Outside of Arizona’s Active Management Areas, the “adequate water supply” program requires a determination of whether there is an adequate water supply—similar to an assured water supply—but it does not necessarily foreclose development when the showing cannot be made. Unless the county government has voted to make the requirement mandatory, a development (outside of Active Management Areas) that cannot demonstrate access to an adequate water supply is generally required only to disclose this fact, although as a practical matter few developments have proceeded on this basis. In addition, whether a water provider to such a development has access to an adequate water supply is nevertheless relevant to its business.

Other Environmental, Health and Safety (including Water Quality) Matters

Our operations also involve the use, storage and disposal of hazardous substances and wastes. For example, our water and wastewater treatment facilities store and use chlorine and other chemicals and generate wastes that require proper handling and disposal under applicable environmental regulations. We could also incur remedial costs in connection with any environmental contamination relating to our operations or facilities, releases or our off-site disposal of wastes. Although we are not aware of any material cleanup or decontamination obligations, the discovery of contamination or the imposition of such obligations arising under relevant federal, state and local laws and regulations in the future could result in additional costs. Our facilities and operations also are subject to requirements under the U.S. Occupational Safety and Health Act and similar laws in Arizona.

Our compliance with all of the environmental, health and safety (including water quality) requirements described above may be subject to inspections and enforcement measures by federal, state and local agencies.

Security

Due to security, vandalism, terrorism and other risks, we take precautions to protect our employees and the water delivered to our customers. In 2002, federal legislation was enacted that resulted in new regulations concerning security of water facilities, including submitting vulnerability assessment studies to the federal government. We have complied with EPA regulations concerning vulnerability assessments and have made filings to the EPA as required. Vulnerability assessments are conducted regularly to evaluate the effectiveness of existing security controls and serve as the basis for further capital investment in security for the facility. Information security controls are deployed or integrated to prevent unauthorized access to company information systems, assure the continuity of business processes dependent upon automation, ensure the integrity of our data and support regulatory and legislative compliance requirements. In addition, communication plans have been developed as a component of our procedures. While we do not make public comments on the details of our security programs, we have been in contact with federal, state, and local law enforcement agencies to coordinate and improve the security of our water delivery systems and to safeguard our water supply.

-15-

Competition

As an owner and operator of regulated utilities, we do not face competition within our existing service areas because Arizona law provides the holder of a CC&N for water and wastewater service with an exclusive right to provide that service within the certificated area, as against other public service corporations. In addition, the high cost of constructing water and wastewater systems in an existing market creates a barrier to entry. We do, however, face competition from other water and wastewater utilities for new service areas and with respect to the acquisition of smaller utilities. We believe our principal competitors for new service areas and acquisitions in Arizona are EPCOR Water Arizona Inc., Arizona Water Company, and Liberty Utilities. We believe competition for new service areas and acquisitions is based on relationships with municipalities and developers, experience in making acquisitions, the ability to finance and obtain regulatory approval, quality and breadth of products and services, the ability to integrate both water and wastewater services, and emplace conservation practices throughout the service areas, price, speed, and ease of implementation.

If we seek to extend our services outside Arizona, we will face competition from other regional or national water utilities for these opportunities.

Although we believe we compete effectively in our regulated businesses, our competitors may have more resources and experience than we have and may therefore have a competitive advantage.

Segment Reporting

We currently operate in one geographic region within the State of Arizona, wherein each operating utility operates within the same regulatory environment, and is operated as one reportable segment. We do not have any customers that contribute more than 10% to our revenues or revenue streams. For additional information, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Segment Reporting” in Part II, Item 7 of this Form 10-K.

Seasonality

Customer demand for our water during the warmer months is generally greater than other times of the year due primarily to additional consumption of water in connection with irrigation systems, swimming pools, cooling systems, and other outside water use. Throughout the year, and particularly during typically warmer months, demand may vary with temperature, as well as the timing and overall levels of rainfall. In the event that temperatures during the typically warmer months are cooler than normal, or if there is more rainfall than normal, the customer demand for our water may decrease and therefore, adversely affect our revenues. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Factors Affecting our Results of Operations—Weather and Seasonality,” included in Part II, Item 7 of this Form 10-K, for additional information.

Employees

As of December 31, 2018, we employed 50 full-time individuals and one part-time employee. Currently, none of our employees participate in collective bargaining agreements, and we consider our employee relations to be good.

Available Information

We maintain an Internet website at www.gwresources.com. Our Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act are accessible through our website, free of charge, as soon as reasonably practicable after these reports are filed electronically with the SEC. To access these reports, go to our website at www.gwresources.com. The foregoing information regarding our website is provided for convenience and the content of our website is not deemed to be incorporated by reference in this report filed with the SEC. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at www.sec.gov.

-16-

ITEM 1A. | RISK FACTORS |

Regulatory and Legislative Factors

We are subject to regulation by the Arizona Corporation Commission and our financial condition depends upon our ability to recover costs in a timely manner from customers through regulated rates.

We are subject to comprehensive regulation by several federal, state and local regulatory agencies that significantly influence our business, liquidity and results of operations and our ability to fully recover costs from utility customers in a timely manner. The Arizona Corporation Commission (“ACC”) is the regulatory authority with jurisdiction over water and wastewater utilities. The ACC has exclusive authority to approve rates, mandate accounting treatments, authorize long-term financing programs, evaluate significant capital expenditures and plant additions, examine and regulate transactions between a regulated subsidiary and its affiliated entities, and approve or disapprove reorganizations, mergers, and acquisitions prior to their completion. Additionally, the ACC has statutory authority to oversee service quality and consumer complaints, and approve or disapprove expansion of service areas. The ACC is comprised of five elected members, each serving four year terms. Our profitability is affected by the rates we may charge and the timeliness of recovering costs incurred through our rates. Accordingly, our financial condition and results of operations are dependent upon the satisfactory resolution of any rate proceedings and ancillary matters which may come before the ACC. In addition, the ACC may reopen prior decisions and modify otherwise final orders under certain circumstances. Decisions made by the ACC could have a material adverse impact on our financial condition, results of operations and cash flows.

We have significant obligations under Infrastructure Coordination and Financing Agreements (“ICFAs”), yet funds from our ICFAs are dependent on development activities by developers which we do not control and are also subject to certain regulatory requirements.

In the past, we extended water and wastewater infrastructure financing to developers and builders through ICFAs. These agreements are contracts with developers or builders in which we coordinate and fund the construction of water, wastewater, and recycled water facilities that will be owned and operated by our regulated subsidiaries in advance of completion of developments in the area. Our investment can be considerable, as we phase-in the construction of facilities in accordance with a regional master plan, as opposed to a single development. Developers and builders pay us agreed-upon fees upon the occurrence of specified development events for their development projects. The ACC requires us to record a portion of the funds we receive under ICFAs as contributions in aid of construction (“CIAC”), which are funds or property provided to a utility under the terms of a collection main extension agreement and/or service connection tariff, the value of which are not refundable. Amounts received as CIAC reduce our rate base once expended on utility plants.

The developer is not required to pay the bulk of the agreed-upon fees until a development receives platting approval. Accordingly, we cannot always accurately predict or control the timing of the collection of our fees. If a developer encounters difficulties, such as during a real estate market downturn, that result in a complete or partial abandonment of the development or a significant delay in its completion, we will have planned, built, and invested in infrastructure that will not be supported by development and will not generate either payments under the applicable ICFA or cash flows from providing services. As a result, our return on our investment and cash flow stream could be adversely affected.

In August 2013, we entered into a settlement agreement with ACC staff, the Residential Utility Consumers Office, the City of Maricopa, and the other parties to a rate case, which established the policy by which ICFA fees will be treated going forward. The settlement also prohibits us from entering into new ICFAs. In February 2014, the rate case proceedings were completed and the ACC issued Rate Decision No. 74364, approving the settlement agreement. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Recent Rate Case Activity,” included in Part II, Item 7 of this Form 10-K, for additional information.

New or stricter regulatory standards or other governmental actions could increase our regulatory compliance and operating costs, which could cause our profitability to suffer, particularly if we are unable to increase our rates to offset such costs.