UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2018

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-37481

PERSHING GOLD CORPORATION

(Exact Name of Registrant as Specified in its Charter)

| NEVADA | 26-0657736 | |

| (State of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

| 1658 Cole Boulevard | ||

| Building 6 - Suite 210 | ||

| Lakewood, Colorado | 80401 | |

| (Address of principal executive offices) | (Zip Code) |

(720) 974-7254

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock, $0.0001 par value |

Nasdaq Stock Market LLC (Nasdaq Global Market) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12-b-2 of the Exchange Act). (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | ||

| Non-accelerated filer x | Smaller reporting company x | ||

| Emerging growth company ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates as of June 30, 2018 was approximately $34.7 million, based on the closing price of the registrant’s common stock of $1.84 per share on the Nasdaq Global Market on June 29, 2018.

The number of shares of common stock outstanding on April 1, 2019 was 33,686,921.

DOCUMENTS INCORPORATED BY REFERENCE

None.

References to “the Company,” “our,” “we,” or “us” mean Pershing Gold Corporation and, unless otherwise specified, its subsidiaries. Many of the terms used in our industry are technical in nature. We have included a glossary of some of these terms below.

FORWARD-LOOKING STATEMENTS

Some information contained in or incorporated by reference into this annual report on Form 10-K may contain forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995. These statements include statements relating to our plans to undergo a merger with Americas Silver Corporation, future management of Pershing Gold by Americas Silver Corporation, our shareholders’ investment in Americas Silver Corporation upon consummation of the merger, Americas Silver Corporation’s ability to finance and operate Relief Canyon Mine and return value to our shareholders, the conclusions of a feasibility study and related studies, the timing of any gold production, our mineralized material estimate, further permitting and development efforts required to advance the Relief Canyon Mine to various phases of production, expectations and the timing and budget for exploration and future development of our Relief Canyon properties, our planned expenditures for 2019, our estimates of the cost of future permitting changes and additional bonding requirements, future exploration plans, the estimated preliminary internal economics for the Relief Canyon Mine, our expected cash needs, our ability to fund our business with our current cash reserves based on our currently planned activities and statements concerning our financial condition, our plans with respect to future financing options, our anticipation of future environmental impacts, business and operating strategies, and operating and legal risks.

We use the words “anticipate,” “continue,” “likely,” “estimate,” “expect,” “may,” “could,” “will,” “project,” “should,” “believe” and similar expressions to identify forward-looking statements. Statements that contain these words discuss our future expectations and plans, or state other forward-looking information. Although we believe the expectations and assumptions reflected in those forward-looking statements are reasonable, we cannot assure you that these expectations and assumptions will prove to be correct. Our actual results could differ materially from those expressed or implied in these forward-looking statements as a result of various factors described in this annual report on Form 10-K, including:

| · | Risks relating to the planned merger with Americas Silver Corporation, regulatory approval, management of Pershing Gold by Americas Silver Corporation, Americas Silver Corporation’s ability to finance and operate the Relief Canyon Mine, determining the feasibility and economic viability of commencing mining, our ability to fund future exploration costs or purchase additional equipment, and our ability to obtain or amend the necessary permits, consents, or authorizations needed to advance expansion of the deposit or recommissioning of the gold processing facility; |

| · | Risks related to the Relief Canyon properties other than the Relief Canyon Mine, including our ability to advance gold exploration, discover any deposits of gold or other minerals which can be mined at a profit, maintain our unpatented mining claims and millsites, commence mining, obtain and maintain any necessary permits, consents, or authorizations needed to continue exploration, and raise the necessary capital to finance exploration and potential expansion; |

| · | Our ability to acquire additional mineral targets; |

| · | Our ability to obtain additional external funding; |

| · | Our ability to achieve any meaningful revenue; |

| · | Our ability to engage or retain geologists, engineers, consultants and other key management and mining personnel necessary to successfully operate and grow our business; |

| · | The volatility of the market price of our common stock or our intention not to pay any cash dividends in the foreseeable future; |

| · | Changes in any federal, state or local laws and regulations or possible challenges by third parties or contests by the federal government that increase costs of operation or limit our ability to explore on certain portions of our property; |

| 2 |

| · | Decreases in the market price for gold and economic and political events affecting the market prices for gold and other minerals which may be found on our exploration properties; and |

| · | The factors set forth under “Risk Factors” in Item 1A of this annual report on Form 10-K. |

Many of these factors are beyond our ability to control or predict. Although we believe that the expectations reflected in our forward-looking statements are based on reasonable assumptions, such expectations may prove to be materially incorrect due to known and unknown risk and uncertainties. You should not unduly rely on any of our forward-looking statements. These statements speak only as of the date of this annual report on Form 10-K. Except as required by law, we are not obligated to publicly release any revisions to these forward-looking statements to reflect future events or developments. All subsequent written and oral forward-looking statements attributable to us and persons acting on our behalf are qualified in their entirety by the cautionary statements contained in this section and elsewhere in this annual report on Form 10-K.

GLOSSARY OF SELECTED MINING TERMS

The following is a glossary of selected mining terms used in this annual report on Form 10-K that may be technical in nature:

“Base metal” means a classification of metals usually considered to be of low value and higher chemical activity when compared with the precious metals (gold, silver, platinum, etc.). This nonspecific term generally refers to the high-volume, low-value metals copper, lead, tin, and zinc.

“Deposit” means an informal term for an accumulation of mineral ores.

“Doré” means a mixture of gold and silver that is produced from the refinery furnace.

“Exploration stage” means a U.S. Securities and Exchange Commission descriptive category applicable to public mining companies engaged in the search for mineral deposits and ore reserves and which are not either in the mineral development or the ore production stage.

“Feasibility study” means an engineering study designed to define the technical, economic, and legal viability of a mining project with a high degree of reliability.

“Formation” means a distinct layer of sedimentary rock of similar composition.

“Grade” means the metal content of ore, usually expressed in troy ounces per ton (2,000 pounds) or in grams per ton or metric tonnes that contain 2,204.6 pounds or 1,000 kilograms.

“Heap leach” means a mineral processing method involving the crushing and stacking of an ore on an impermeable liner upon which solutions are sprayed to dissolve metals, i.e. gold, copper, etc.; the solutions containing the metals are then collected and treated to recover the metals.

“Lode” means a classic vein, ledge, or other rock in place between definite walls.

“Millsite” means a specific location of five acres or less on public lands that are non-mineral in character. Millsites may be located in connection with a placer or lode claim for mining and milling purposes or as an independent/custom mill site that is independent of a mining claim.

“Mineralization” means the concentration of metals within a body of rock.

| 3 |

“Mining” means the process of extraction and beneficiation of mineral reserves or mineral deposits to produce a marketable metal or mineral product. Exploration continues during the mining process and, in many cases, mineral reserves or mineral deposits are expanded during the life of the mine operations as the exploration potential of the deposit is realized.

“Mining claim” means a mining interest giving its holder the right to prospect, explore for and exploit minerals within a defined area.

“Net smelter return royalty” means a defined percentage of the gross revenue from a resource extraction operation, less a proportionate share of transportation, insurance, and smelting/refining costs.

“Open pit” means a mine working or excavation open to the surface.

“Ore” means material containing minerals that can be economically extracted.

“Outcrop” means that part of a geologic formation or structure that appears at the surface of the earth.

“Precious metal” means any of several relatively scarce and valuable metals, such as gold, silver, and the platinum-group metals.

“Probable reserves” means reserves for which quantity and grade and/or quality are computed from information similar to that used for proven reserves, but the sites for inspection, sampling and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven reserves, is high enough to assume continuity between points of observation.

“Production stage” means a project that is actively engaged in the process of extraction and beneficiation of mineral reserves or mineral deposits to produce a marketable metal or mineral product.

“Proven reserves” means reserves for which (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and/or quality are computed from the results of detailed sampling and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of reserves are well-established.

“Reclamation” means the process of returning land to another use after mining is completed.

“Recovery” means that portion of the metal contained in the ore that is successfully extracted by processing, expressed as a percentage.

“Reserves” means that part of a mineral deposit that could be economically and legally extracted or produced at the time of reserve determination.

“Sampling” means selecting a fractional part of a mineral deposit for analysis.

“Sediment” means solid fragmental material that originates from weathering of rocks and is transported or deposited by air, water, or ice, or that accumulates by other natural agents, such as chemical precipitation from solution or secretion by organisms, and that forms in layers on the Earth’s surface at ordinary temperatures in a loose, unconsolidated form.

“Sedimentary” means formed by the deposition of sediment.

“Unpatented mining claim” means a mineral claim staked on federal or, in the case of severed mineral rights, private land (where the U.S. government has retained ownership of the locatable minerals) to which a deed from the U.S. government has not been received by the claimant. Unpatented claims give the claimant the exclusive right to explore for and to develop the underlying minerals and the right to use the surface for such purpose. However, the claimant does not own title to either the minerals or the surface, and the claim must include a discovery of valuable minerals to be valid and is subject to the payment of annual claim maintenance fees that are established by the governing authority of the land on which the claim is located.

| 4 |

“Vein” means a fissure, fault or crack in a rock filled by minerals that have traveled upwards from some deep source.

“Waste” means rock lacking sufficient grade and/or other characteristics of ore.

PART I

ITEMS 1 AND 2: BUSINESS AND PROPERTIES

Overview

We are a gold and precious metals exploration company pursuing exploration, development and mining opportunities primarily in Nevada. We are currently focused on exploration at our Relief Canyon properties in Pershing County in northwestern Nevada and, if economically feasible, commencing mining at the Relief Canyon Mine. None of our properties contain proven and probable reserves under SEC Industry Guide 7, and our activities on all of our properties are exploratory in nature.

Our principal offices are located in Lakewood, Colorado at 1658 Cole Boulevard, Building No. 6, Suite 210, Lakewood, Colorado 80401 and we have an exploration office at 1055 Cornell Avenue, Lovelock, Nevada 89419. Our telephone number is 720-974-7254. We maintain a website at www.pershinggold.com, which contains information about us. Our website and the information contained in and connected to it are not part of this annual report on Form 10-K.

Merger Agreement

On September 28, 2018, we entered into an Agreement and Plan of Merger with Americas Silver Corporation (“Americas Silver”) and R Merger Sub, Inc., a wholly-owned subsidiary of Americas Silver (“Merger Sub”), which agreement was amended on March 1, 2019 (as amended, the “Merger Agreement”). Under the terms of the Merger Agreement, we will merge with and into Merger Sub, with Pershing Gold Corporation being the surviving corporation and becoming a wholly-owned subsidiary of Americas Silver (the “Merger”).

In connection with the Merger, our common stockholders will be issued 0.715 Americas Silver common shares for each share of our common stock (the “Common Stock Exchange Ratio”). Holders of our Series E Convertible Preferred Stock (“Series E Preferred Stock”) have been given the option to (a) convert their shares of Series E Preferred Stock into our common shares immediately before the closing and exchange those common shares for Americas Silver common shares at the Common Stock Exchange Ratio, or (b) exchange their Series E Preferred Stock for non-voting preferred stock of Americas Silver (“Americas Silver Preferred Shares”) at a ratio of 461.440 Americas Silver preferred shares for each share of Series E Preferred Stock (the “Preferred Stock Exchange Ratio”).

On January 9, 2019, the Merger was approved by (i) preferred shareholders holding at least 75% of our preferred shares, voting as a separate class, and (ii) a majority of the voting shares held by our common shareholders and preferred shareholders, voting together as a single class. The issuance of the Americas Silver shares in connection with the Merger was also approved by Americas Silver’s shareholders on January 9, 2019.

Completion of the Merger will be subject to the satisfaction of other customary closing conditions, including, among others, the receipt of certain regulatory approvals necessary for the completion of the Merger. On April 1, 2019, the Committee of Foreign Investment in the United States (“CFIUS”) completed its review of the Merger and CFIUS determined that there are no unresolved national security concerns with respect to the transaction.

The Merger Agreement contains certain termination rights for both us and Americas Silver, including in the event that the Merger is not consummated by June 1, 2019.

| 5 |

Convertible Debenture

Concurrent with the execution of the Merger Agreement, we entered into a Convertible Secured Debenture with Americas Silver (the “Debenture”), effective October 1, 2018, that allows us to borrow up to $4,000,000 from Americas Silver. The interest rate is 16% per year on the amount drawn, accrued and compounded monthly. The loan will mature on June 1, 2019, or September 1, 2019 if we have exercised an option to extend maturity. As of April 1, 2019 we had drawn approximately $2.78 million on the Debenture and accrued interest of approximately $133,000.

Corporate Structure

We were incorporated in Nevada on August 2, 2007 under the name Excel Global, Inc., and we changed our name to Pershing Gold Corporation on February 27, 2012.

We operate our business directly and also through our wholly-owned subsidiary, Gold Acquisition Corp., a Nevada corporation. Gold Acquisition Corp. owns and is conducting exploration on the Relief Canyon Mine property in northwestern Nevada. Pershing Gold Corporation owns directly and is conducting exploration on the Relief Canyon properties adjacent to the Relief Canyon Mine property, which we refer to as the Relief Canyon expansion properties. We also have a subsidiary, Pershing Royalty Company, that holds royalty interests in 17 unpatented mining claims in Pershing County, and in 192 claims in Lander County, Nevada, and a wholly-owned subsidiary, Blackjack Gold Corporation, formed for potential purchases of exploration targets.

Business Strategy

Our business strategy is to acquire and advance precious metals exploration properties. We seek properties with known mineralization that are in an advanced stage of exploration and have previously undergone drilling but are under-explored, which we believe we can advance to increase value. We are currently focused on exploration of the Relief Canyon properties and, if economically feasible, commencing mining at the Relief Canyon Mine. We also periodically review other strategic opportunities, focused primarily in Nevada.

Relief Canyon Mine Property

We acquired the Relief Canyon Mine property in August 2011. The property then consisted of approximately 1,100 acres of unpatented mining claims and millsites and included three open pit mines and a processing plant that could be used to process material from the Relief Canyon Mine or from other mining operations. We refer to this property as the “Relief Canyon Mine” property.

We significantly expanded our Relief Canyon property position in 2012 with the acquisition of approximately 23,000 additional acres of unpatented mining claims and leased and subleased lands around the Relief Canyon Mine and south of the Relief Canyon Mine. We refer to this expanded property position as the “Relief Canyon properties.” In early 2015, we acquired 74 mining claims near the Relief Canyon Mine on which the processing facilities are located that we had previously leased from Newmont USA Ltd. (“Newmont”), and we entered into a new mining lease directly with the owner of approximately 1,600 acres of fee land that we had previously subleased from Newmont pursuant to a Mining Lease and Sublease dated June 15, 2006 (“2006 Lease Agreement”). Newmont was granted a 2% net smelter return on the claims and fee lands that were subject to the 2015 transaction; in June 2018 Newmont assigned this royalty interest to Maverix Metals (Nevada) Inc. (“Maverix”). In 2018, we exercised a right of first offer (“ROFO”) to purchase all of Newmont’s right, title, and interest in, to, and under the 2006 Lease Agreement. By exercise of the ROFO and the closing of a Purchase and Sale Agreement dated August 27, 2018 (“2018 PSA”), between the Company and Newmont, we acquired all of the assets then held under the 2006 Lease Agreement and it terminated. Assets acquired under the 2018 PSA include (i) 81 unpatented lode claims, (ii) 320 acres of private minerals (subject to an underlying 2.125% NSR royalty payable to New Nevada Resources, LLC); (iii) assignment of a Mining Lease dated effective December 31, 2014 between New Nevada Resources, LLC and New Nevada Lands, LLC (collectively “New Nevada”), covering approximately 2,458.88 acres of private lands subject to a 2.5% NSR royalty payable to New Nevada, and other customary terms and conditions. Most of the Relief Canyon Mine properties are subject to a 2% net smelter return royalty payable to either RG Royalties, LLC, a subsidiary of Royal Gold, Inc. or Maverix. In March 2017, we entered into a mining sublease with Newmont covering 960 acres of fee land leased by Newmont from New Nevada, which further consolidated our land holdings in the Pershing Pass area south of the Relief Canyon Mine. In June 2018 Newmont assigned its rights in and to the 2017 mining sublease, and to the underlying New Nevada lease (partial), with respect to the subleased 960 acres to Maverix, with Maverix now the sub-lessor. In January 2019 the Company and Maverix amended the mining sublease to recognize the Company and Maverix as the current parties to the sublease, amend the work commitment schedule, and various notice and reporting requirements.

| 6 |

Since we acquired the Relief Canyon Mine property in 2011, we have drilled a total of 550 drill holes totaling approximately 325,000 feet at the Relief Canyon properties. Our exploration efforts have been focused primarily on expanding the known Relief Canyon Mine deposit. Our 2011-2013 exploration drilling programs expanded the deposit. We began a drilling program in 2014 which we completed in early 2015. In this program, we drilled a total of 134 core holes, totaling approximately 74,000 feet, for the purpose of extending and upgrading the current deposit. The 2014 drill results included some gold intercepts at significantly higher grades than the average historic grade of the Relief Canyon Mine deposit of approximately one gram of gold per ton. We conducted the 2015 drilling program from May 2015 through December 2015, which demonstrated that the high-grade zone in the North Target Area has continued south under the North Pit and that the higher-grade L Zone of the Relief Canyon Mine deposit is geologically open to the west, south and southwest. In November 2016, we completed Phase 1 of our 2016 drilling program, which included 22 core holes, totaling approximately 15,000 feet. In November 2016, we commenced Phase 2 drilling and completed this drilling in December 2016, which included nine core holes totaling approximately 8,000 feet. During 2017, we drilled an additional 15 holes, totaling approximately 5,800 feet at our Blackjack Project Area, located approximately nine miles south of the Relief Canyon Mine. The 2018 drilling program focused on four target areas of the Relief Canyon properties: the West Step-out area, the North East Pit, the Main Zone, and the South East Lightbulb Pit. The budget for the 2018 drilling program was approximately $2.7 million, and included 38 core holes with 31,000 feet completed.

Feasibility Study and Mineralized Material Estimate

On May 24, 2018, Mine Development Associates of Reno, Nevada (“MDA”) completed a feasibility study on the Relief Canyon Mine. The feasibility study included an estimate of mineralized material at the Relief Canyon Mine deposit, calculated at a cut-off grade of 0.005 ounces of gold per ton for oxide material, 0.01 ounces of gold per ton for mixed material and 0.02 ounces of gold per ton for sulfide material. Silver grades were only available for a portion of the deposit. The database used for the mineralized material estimate described below includes 419 core holes and 676 reverse circulation holes for a total of 482,755 feet, of which 415 core holes and 89 reverse circulation holes were drilled by us from 2011 to September 2016.

| Tons | Average gold grade (ounces per ton) |

|||||

| 41,876,000 | 0.019 | |||||

| Tons | Average silver grade (ounces per ton) |

|||||

| 17,576,000 | 0.117 | |||||

“Mineralized material” as used in this annual report on Form 10-K, although permissible under the Securities and Exchange Commission (“SEC”) Guide 7, does not indicate “reserves” by SEC standards. We cannot be certain that any part of the Relief Canyon deposit will ever be confirmed or converted into SEC Industry Guide 7 compliant “reserves.” Investors are cautioned not to assume that all or any part of the mineralized material will be confirmed or converted into SEC Industry Guide 7 compliant reserves or that mineralized material can be economically or legally extracted. In addition, in this annual report on Form 10-K we also modify our estimates made in compliance with National Instrument 43-101 to conform to SEC Industry Guide 7 for reporting in the United States. Mineralized material is substantially equivalent to measured and indicated mineral resources as disclosed for reporting purposes in Canada, except that the SEC only permits issuers to report “mineralized material” in tonnage and average grade without reference to contained ounces.

The feasibility study indicated the possibility of a viable mine and recommended that work should continue on advancing the project to a production decision. The recommended advancement work would include additional drilling to improve the knowledge of the deposit, and obtaining silver assays for continuous mineralized intervals from past core drilling and new drilling so that more silver values can be added to the economic analysis for the mine.

| 7 |

Permitting

We have all of the state and federal permits necessary to start mining and heap-leach processing operations at the Relief Canyon Mine. We have planned a two-phase permitting and development scenario for the project. Phase I, which has been fully authorized under our permits, is the re-purposing of previously approved disturbance and creating new surface disturbance for expanded mining to a pit bottom elevation of 5,080 feet, partial backfilling of the Phase I pit to approximately 20 feet above the historical groundwater elevation to eliminate a pit lake, expanded exploration operations, full build-out of the heap leach pad to accommodate leaching of the Phase I ore, and construction of a new waste rock storage facility. Phase II would include additional mine expansion activities and would allow mining further below the water table. We used the mine plan in the May 2018 feasibility study as the basis for the Phase II permit applications, which were submitted in June 2018.

Production Decision and Financing

While we have begun initial land clearing in preparation for potential construction at the Relief Canyon Mine, we have not yet secured sufficient financing to, and our board of directors has not yet decided to, bring the mine into production at this time. Although the Relief Canyon Mine currently has an available leach pad and processing facility and we have senior mine and processing personnel in place, we would be required to obtain mining equipment (which could be through purchase, lease, contract mining or a combination of these), hire employees for the mine and the processing plant, purchase materials and supplies, commence mining, leaching and processing activities, and continue these activities as well as the corporate activities currently conducted for a number of months until sufficient positive cash flow is produced by gold sales to fund all of these activities.

In order to commence mining at Relief Canyon, based on the estimates contained in the feasibility study, we currently expect to incur capital expenditures and working capital expenditures of approximately $38 million. This estimate is exclusive of general and administrative expenses and other exploration costs that will be incurred by us. This estimate assumes that we would utilize a contract miner to mine ore at the pit and deliver it to the crusher.

There are no assurances that we will be successful in raising sufficient financing to commence production at Relief Canyon. Moreover, if the Merger with Americas Silver closes, the ultimate decision on when or if to put the mine into production will be made by the Americas Silver board of directors.

Relief Canyon Properties

Location, Access and Facilities

The Relief Canyon properties are located about 100 miles northeast of Reno, Nevada. The nearest town is Lovelock, Nevada, approximately 15 miles west-southwest of the Relief Canyon Mine property, which can be reached from both Reno and Lovelock on U.S. Interstate 80. The Relief Canyon Mine property is reached from Lovelock by travelling approximately seven miles northeast on I-80 to the Coal Canyon Exit (Exit No. 112), then about 10 miles southeast on Coal Canyon Road (State Route 857, a paved road maintained by Pershing County) to Packard Flat, and then north on a gravel road for two miles. All of the Relief Canyon properties can be accessed by unpaved roads from the Relief Canyon Mine property.

Through our wholly-owned subsidiary, Gold Acquisition Corp., we own 254 unpatented mining claims and 120 millsite claims, and lease approximately 1,600 acres of fee land, at the Relief Canyon Mine property. The Relief Canyon Mine property includes the Relief Canyon Mine and gold processing facility, currently on care and maintenance status. The Relief Canyon Mine includes three open pit mines, heap leach pads comprised of six cells, two solution ponds and a cement block constructed adsorption desorption-recovery (“ADR”) solution processing circuit. The ADR type process plant consists of four carbon columns, an acid wash system, a stripping vessel, and electrowinning cells. The process facility was completed in 2008 and Firstgold Corp. produced a small amount of gold there in 2009. See “Relief Canyon Properties – Property History.” The facilities are generally in good condition.

| 8 |

When the Relief Canyon Mine was in production in the late 1980s and early 1990s, previous operators used conventional heap leach processing methods in which ore removed from the open pit mines was crushed, stacked on heap leach pads and sprinkled with a dilute sodium cyanide solution to dissolve gold and silver from the ore. The “pregnant” gold and silver bearing solution was piped to the gold recovery plant and processed using a conventional ADR gold and silver recovery system. In the ADR system, the pregnant solution flowed through a series of carbon columns where the gold and silver were adsorbed onto activated carbon. The next step in the process involved stripping the gold from the gold-bearing carbon in electrowinning cells and then recovering the gold in an on-site refinery. The resulting doré was then sent to a third party facility for further processing into saleable gold and silver products. Following removal of the gold and silver, the cyanide solution was recycled to the heap leach pads in a closed-loop system.

We plan to add mercury pollution control equipment to the process plant to allow for onsite stripping of the gold-bearing carbon. If we elect not to add the mercury pollution control equipment we could ship gold-laden carbon from the carbon columns to a third-party refinery for further processing.

Adequate line power is available to the site to operate the existing process facility and ancillary facilities. There is a backup generator onsite that could provide the required power for the heap leach pumping system in the event of power outages. Another generator will be used to provide power for the crushing and conveying system. Sufficient water rights to operate the Relief Canyon Mine and the processing and ancillary facilities have been appropriated with two operating and permitted wells.

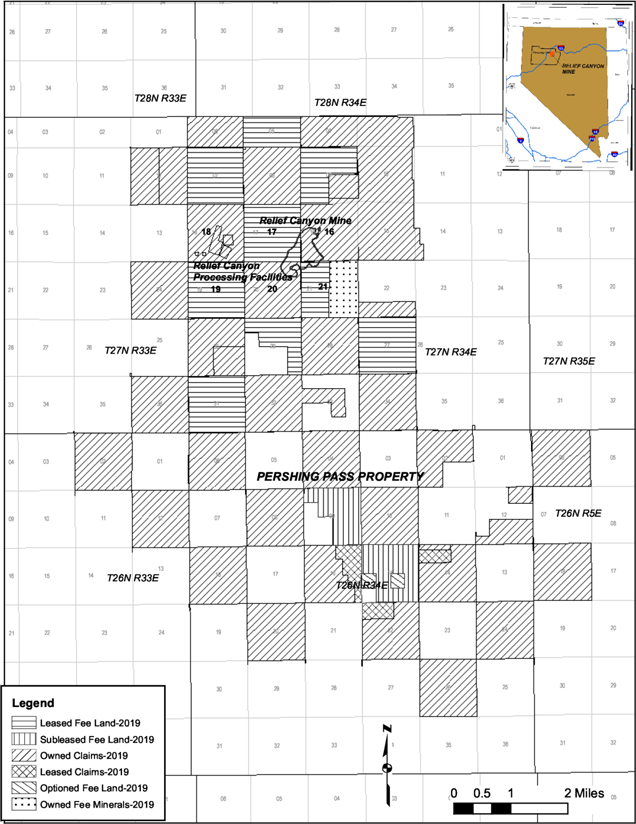

The maps below show the location of the Relief Canyon properties:

| 9 |

Figure 1: Relief Canyon properties, excluding the Coal Canyon project

| 10 |

Figure 2: Coal Canyon Project

| 11 |

Rock Formation and Mineralization

The Relief Canyon properties are located in Pershing County, Nevada at the southern end of the Humboldt Range. The range is underlain by a sequence of late Paleozoic to Mesozoic aged volcanic and sedimentary rocks. Gold-bearing rocks at the Relief Canyon properties are primarily developed within breccia zones along the contact between the Grass Valley and Cane Springs Formations.

Property History

Gold was first discovered on the property by the Duval Corp. in 1979. Subsequent exploration was performed by various companies including Lacana Mining, Santa Fe Gold Corp., and Pegasus Gold Inc., and gold was produced from the property during the late 1980s and early 1990s. Firstgold Corp. acquired the property in 1995, explored periodically from 1995 until 2009, and produced a small amount of gold in 2009. Firstgold Corp. filed for bankruptcy protection in January 2010, and in August 2011, pursuant to an order of the bankruptcy court, we (through our wholly owned subsidiary, Gold Acquisition Corp.) purchased 100% of the Relief Canyon Mine property and related assets.

Title and Ownership Rights

Our property rights currently total approximately 29,000 acres and are comprised of approximately 1,137 owned unpatented mining claims, 120 owned millsite claims, 62 leased unpatented mining claims, and 6,586 acres of leased, 960 acres of subleased private lands, and 320 acres of owned private minerals. In January 2015, we acquired certain mining claims from Newmont, entered into a new mining lease on private, or fee, lands that we previously subleased from Newmont, and amended the 2006 Minerals Lease and Sublease with Newmont with respect to certain other portions of the Relief Canyon properties. The above summary of property units, and Map Figure 2 below also reflect the land status changes resulting from the Company’s 2018 exercise of its right of first offer (“ROFO”) to purchase all of Newmont’s right, title, and interest in, to, and under the 2006 Lease Agreement. By exercise of the ROFO and the closing of a Purchase and Sale Agreement dated August 27, 2018, between the Company and Newmont, the Company acquired all of the assets then held under the 2006 Lease Agreement and the Agreement terminated. These transactions, which did not increase the size of our Relief Canyon property position, aare described below. In March 2017, we entered into a mining sublease with Newmont covering 960 acres of fee land leased by Newmont from New Nevada, which further consolidated our land holdings in the Pershing Pass area south of the Relief Canyon Mine. In June 2018 Newmont assigned its rights in and to the 2017 mining sublease, and to the underlying New Nevada lease (partial) with respect to the subleased 960 acres to Maverix, with Maverix now the sub-lessor. In January 2019 the Company and Maverix amended the mining sublease to recognize the Company and Maverix as the current parties to the sublease, and to amend the work commitment schedule and various notice and reporting requirements. We also control options to purchase two 40 acre parcels of fee land in the same vicinity. In December 2017, we entered into two mining leases in the Coal Canyon area, which is west of the Relief Canyon Mine, leasing an additional 43 unpatented claims, and 1,899 acres of fee land, as further described below under the heading “Coal Canyon Project”.

In order to maintain ownership of the unpatented mining claims and millsites at the Relief Canyon properties, we are required to make annual claim maintenance payments of $155 per mining claim or millsite to the Bureau of Land Management (the “BLM”), and to record in the county records an affidavit of payment of claim maintenance fees and notice of intent to hold and pay state and county recording fees of $12.00 per claim or millsite. Our total property maintenance costs for all of the unpatented mining claims and millsites for the Relief Canyon properties in 2018 was approximately $307,000, and we expect our land holding costs to be approximately $327,000 in 2019, which covers the cost of maintaining the additionally acquired claims, new leases covering both claims and fee lands, as noted herein, and an increase in the BLM claim maintenance fee which is anticipated to be adjusted for inflation in 2019.

January 2015 Acquisition

In January 2015, we acquired 74 unpatented mining claims totaling approximately 1,300 acres that we had previously leased from Newmont. We also entered into a new mining lease directly with New Nevada Resources, LLC and New Nevada Lands, LLC for approximately 1,600 acres of fee, or private, land that we had previously subleased from Newmont. The new lease has a primary term of twenty years that can be extended for so long thereafter as mining, development or processing operations are being conducted on the land on a continuous basis. The lease contains customary terms and conditions, including annual advance royalty payments commencing at $1.00 per acre and increasing after five years by the greater of five percent or an amount determined from the Consumer Price Index, and a 2.5% net smelter returns production royalty.

| 12 |

The claims that we acquired from Newmont and the fee land subject to our new lease are located near, and include portions of, the pit and the land on which the Relief Canyon Mine property processing facilities are located. These areas are shown in the map above as owned claims and leased fee. These properties also include lands to the south and west of the current mine pits that we believe are prospective for potential expansion of the Relief Canyon Mine deposit, and lands that could in the future be used for new or expanded mine support facilities, including potential waste rock storage. As a result of these transactions, the claims we purchased from Newmont and the private lands we leased from New Nevada Resources, LLC and New Nevada Lands, LLC are no longer subject to Newmont’s joint venture rights discussed below.

2018 Exercise Right of First Refusal – June 15, 2006 Lease Agreement

In 2018, we exercised the ROFO to purchase all of Newmont’s right, title, and interest in and under the Minerals Lease & Sublease dated June 15, 2006 between Newmont and Pershing Gold (as successor in interest), as amended (the “2006 Lease Agreement”) for $1,100,000. By exercise of the ROFO, and the closing of a Purchase and Sale Agreement dated August 27, 2018 (the “2018 PSA”) between us and Newmont, we acquired all of the assets then held under the 2006 Lease Agreement and the agreement terminated. By termination of the 2006 Lease Agreement, the area of interest established by the agreement also terminated. Assets acquired under the 2018 PSA include (i) 81 unpatented lode claims, (ii) 320 acres of private minerals (subject to an underlying 2.125% NSR royalty payable to New Nevada Resources, LLC); (iii) assignment of a Mining Lease dated effective December 31, 2014, between New Nevada Resources, LLC and New Nevada Lands, LLC (collectively “Owner”), covering approximately 2,458.88 acres of private lands subject to a 2.5% NSR royalty payable to Owner, and other customary terms and conditions under the Mineral Lease agreement; and (iv) termination of the 2006 Lease Agreement in its entirety, without any further force or effect.

Coal Canyon Project

In December 2017, we entered into two mining leases at Coal Canyon, which is west of the Relief Canyon Mine (see Figure 2, above). One such mining lease with Good Springs Exploration, LLC and Clancy Wendt (collectively “Lessor”) covers 43 unpatented mining claims which added 800 acres to our property holdings. The lease contains customary terms and conditions, with a primary term of ten years, which may be extended by us, annual advance royalty payments to Lessor starting at $20,000 per year, capping at $50,000, which payments are recoupable against a 3% net smelter return royalty, which royalty can be reduced by one percent of net smelter return for a payment of $1 million, and also includes a conditional purchase option for $350,000.

A second mining lease with Owner covers 1,899 acres of fee land. The lease contains customary terms and conditions, with a primary term of twenty years, which may be extended by us, with annual advance royalty payments to Owner starting at $10 per acre capping at $25 per acre, which payments are recoupable against a 3% net smelter return royalty. This royalty can be reduced by one percent of net smelter return in exchange for a payment of $1 million, and also includes a conditional purchase option at a price of $500 per acre.

Royalties

As currently defined by exploration drilling, most of the Relief Canyon deposit is located on property that is subject to a 2% net smelter return royalty, with a portion of the deposit located on property subject to net smelter return royalties totaling 4.5%. The rest of the property is subject, under varying circumstances, to net smelter return royalties ranging from 2% to 5%.

The map below shows the royalties payable on the properties on which the current Relief Canyon Mine pits and processing facilities are located and the surrounding properties we now own or lease directly from New Nevada Resources, LLC and New Nevada Lands, LLC, as the result of the January 2015 and January 2018 transactions with Newmont (Maverix), New Nevada Resources, LLC and New Nevada Lands, LLC described above.

| 13 |

Pershing Pass Property

With the various noted property additions, the Pershing Pass property consists of over 765 unpatented mining claims (746 owned, 19 leased) covering approximately 12,900 acres and a mining lease covering approximately 635 acres of fee land. The Pershing Pass property includes approximately 490 unpatented lode mining claims covering approximately 9,700 acres that we acquired from Silver Scott Mines in March 2012 and approximately 283 unpatented lode mining claims covering about 5,660 acres owned directly by Victoria Resources (US) Inc., a wholly-owned subsidiary of Victoria Gold Corp., prior to our purchase (collectively, “Victoria”). Victoria has reserved a 2% net smelter return royalty on the 221 claims that are located outside the area of interest related to the prior 2006 Lease Agreement, which area of interest was terminated by the 2018 ROFO exercise, discussed above. The Pershing Pass property also includes 17 unpatented mining claims acquired from a third party in April 2012 subject to a 2% net smelter return royalty, 17 unpatented mining claims that we located in mid-2012, and approximately 635 acres of private lands that we leased in December 2012. The primary term of the lease is ten years, ending in December 2022, which may be extended as long as mineral exploration, development or mining work continues on the property. Production from the private lands covered by the lease is subject to a 2% net smelter return royalty on all metals produced other than gold, and to a royalty on gold indexed to the gold price, ranging from 2% at gold prices of less than $500 per ounce to 3.5% at gold prices over $1,500 per ounce. Prior to one year after commencement of commercial production, we can repurchase up to 3% of the royalty on gold production at the rate of $600,000 for each 1%. The Blackjack Project Area is located within the Pershing Pass property.

| 14 |

In September 2013, we entered into a lease agreement and purchase option for 19 unpatented mining claims (approximately 400 acres) in the Pershing Pass property. The lease grants us exclusive rights to conduct mineral exploration, development and mining and an exclusive option to purchase the claims. The primary term of the lease is ten years, which may be extended as long as mineral exploration, development, or mining work continues on the property. Production from the lease is subject to a 1% net smelter return royalty on precious metals and a one-half percent net smelter royalty on all other metals produced from the lease. Pursuant to a 2011 Deed of Royalty, the claims are also subject to an additional 2% net smelter return royalty on precious metals and a one percent net smelter royalty on all other metals (a total 3% on precious metals – 1.5% on other metals). Prior to production, we are required to pay a $10,000 annual advance minimum royalty payment to Nevada Select Royalties, Inc. The advance minimum royalty remains at $10,000 per year until September 2023 when the advance royalty payment increases to $12,500 per year. The advance royalty payment increases to $15,000 per year in September 2028 and then $20,000 per year in September 2033. The advance minimum royalty payments are due on or before the anniversary dates of the lease agreement. If we decide to exercise the purchase option, which is exercisable at any time, we can acquire the 19 unpatented mining claims for $250,000.

Maverix Pershing Pass Sublease

The March 2017 mining sublease with Newmont added 960 acres of fee land to our property holdings at Pershing Pass. In June 2018, Newmont assigned its rights in and to the 2017 mining sublease, and to the underlying 2014 New Nevada lease (partial), with respect to the subleased 960 acres, to Maverix, with Maverix now being the sub-lessor. In January 2019, the Company and Maverix amended the mining sublease to recognize the Company and Maverix as the current parties to the sublease, amend the work commitment schedule, and amend various notice and reporting requirements. Under the terms of the sublease, we have the exclusive right to prospect, explore for, develop, and mine minerals on these areas. The sublease has an initial term of ten years and may be extended by us until December 3, 2034 and so long thereafter as any mining, development, or processing operations are being conducted continuously. The subleased fee lands are owned by New Nevada Resources, LLC (“NNR”) and New Nevada Lands, LLC (“NNL”), and leased by Maverix under a December 2014 Mining Lease. The underlying 2014 lease contains customary terms and conditions, with a primary term of twenty years, which may be extended by us, and annual advance royalty payments to NNR and NNL, which payments are recoupable against a 2.125% net smelter return royalty payable to NNR and NNL.

The sublease calls for us to make minimum work expenditures for the first four years of the sublease, followed by annual advance minimum royalty payments to Maverix to maintain the sublease in good standing. The sublease may be terminated any time after we have spent $500,000 toward a required $1.5 million work commitment within the first two years of the sublease. Otherwise, upon termination we must pay Maverix the difference between $500,000 and the costs already incurred by us towards the required work commitment. As of December 31, 2018, the most recent cost reporting date, the Company can credit approximately $270,000 in exploration expenditures already incurred against the $1.5 million work commitment. The sublease creates a 2.0% net smelter return royalty on all minerals, excluding industrial minerals, which have a 0.875% net smelter return produced from the subleased fee lands in favor of Maverix. The Maverix 2.0% net smelter return is in addition to the 2.125% net smelter return payable to NNR and NNL. The sublease also creates a 2.0% net smelter return royalty in favor of Maverix on minerals (excepting industrial minerals) produced from our claims located in Section 10 and 16 adjacent to the subleased fee lands.

Environmental Permitting Requirements

Various levels of governmental controls and regulations address, among other things, the environmental impact of mineral mining and exploration operations and establish requirements for reclamation of mineral mining and exploration properties after exploration operations have ceased. With respect to the regulation of mineral mining and exploration, legislation and regulations in various jurisdictions establish performance standards, air and water quality emission limits and other design or operational requirements for various aspects of the operations, including health and safety standards. Legislation and regulations also establish requirements for reclamation and rehabilitation of mining properties following the cessation of operations and may require that some former mining properties be managed for long periods of time after mining activities have ceased.

Our activities are subject to various levels of federal and state laws and regulations relating to protection of the environment, including requirements for closure and reclamation of mineral exploration properties. Some of the laws and regulations include the Clean Air Act, the Clean Water Act, the Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA”), the Emergency Planning and Community Right-to-Know Act, the Endangered Species Act, the Federal Land Policy and Management Act, the National Environmental Policy Act, the Resource Conservation and Recovery Act, and related state laws in Nevada. Additionally, much of our property is subject to the federal General Mining Law of 1872, which regulates how mining claims on federal lands are located and maintained.

| 15 |

The State of Nevada, where we focus our mineral exploration efforts, requires mining projects to obtain a Nevada State Reclamation Permit pursuant to the Mined Land Reclamation Act (the “Nevada MLR Act”), which establishes reclamation and financial assurance requirements for all mining operations in the state. New and expanding facilities are required to provide a reclamation plan and financial assurance to ensure that the reclamation plan is implemented upon completion of operations. The Nevada MLR Act also requires reclamation plans and permits for exploration projects that will result in more than five acres of surface disturbance on private lands.

We have an approved Plan of Operations from the BLM and a Reclamation Permit from the Nevada Division of Environmental Protection (“NDEP”) that authorizes mining, mineral processing and exploration drilling at the Relief Canyon Mine property. In March 2015, we submitted requests to the BLM and the NDEP to amend the Plan of Operations and the Reclamation Permit to allow us to expand the mine. In August 2016, the BLM approved our Environmental Assessment and Plan of Operations Modification, authorizing us to expand the pit boundary, deepen the pit, build a new waste rock storage area and heap leach pads, and increase the permissible drilling areas around the existing pits at the Relief Canyon Mine property. In December 2016, the NDEP approved our reclamation permit. Like the Plan of Operations, the state reclamation permit authorizes expansion and deepening of the pit, building new waste rock and heap leach facilities, and increases the permitted area of drilling. We estimate the annual cost of holding these permits to total approximately $40,000. NDEP issued the Water Pollution Control Permit Major Modification and Renewal, the Class I Air Quality Operating Permit to Construct, and the revised Class II air quality operating permits in February 2017. In 2017, we submitted minor modifications to BLM and NDEP for the Plan of Operations, the Reclamation Permit, and the Water Pollution Control Permit to optimize the configuration of the mining, heap leach pad, and ancillary facilities. As of December 2018, the agencies have approved the modified permit applications.

With the approval of the Environmental Assessment, the 2015 Plan of Operations Modification, and the 2017 Plan of Operations Modification, we were required to increase our reclamation bond with BLM and the NDEP from approximately $5.6 million to approximately $12.5 million, which is currently approximately $80,000 in excess of the current requirement to cover reclamation of land disturbed in our exploration and mining operations. This bond is provided through third-party insurance underwriters, collateralized by approximately 30% of the $12.5 million bond amount, or about $3.7 million.

Approximately $12.4 million of our reclamation bond with BLM and the NDEP covers both exploration and mining at the Relief Canyon Mine property, including the three open pit mines and associated waste rock disposal areas, the mineral processing facilities, ancillary facilities, and the exploration roads and drill pads, with an additional $22,000 covering generative exploration properties located away from the Relief Canyon Mine. The remaining approximately $80,000 can be used to satisfy, or partially satisfy, future bonding requirements for exploration or mining. Our preliminary estimate of the likely amount of additional financial assurance for future exploration is approximately $100,000, although we expect periodic increases due to effects of inflation.

Additional permitting would be required in the future for the Phase II operations to mine further below the water table. BLM may require an Environmental Impact Statement to evaluate the impacts associated with mining below the water table. In fiscal year 2018, we spent approximately $750,000 for the continuation of studies for expansion below the water table and preparing and submitting the amended plan of operations modification.

As discussed above, we have an authorized Plan of Operations from the BLM and a Reclamation Permit from the NDEP, which authorized expansion of the pit, mineral processing, and our 2018 drilling program. We may need to secure a new or modified NDEP Reclamation Permit in order to conduct exploration activities on some of the private lands subleased from Newmont. We plan to apply for additional required permits to conduct our exploration programs as necessary. These permits would be obtained from the BLM, the NDEP or both agencies. Obtaining such permits will require the posting of additional bonds for subsequent reclamation of disturbances caused by exploration. Delays in the granting of permits or permit amendments are not uncommon, and any delays in the granting of permits may adversely affect our exploration activities.

| 16 |

Our current exploration permit costs are minimal, although future exploration activities may require amendments to these permits. We have Notices of Intent from BLM for exploration drilling on our unpatented mining claims in the Pershing Pass area of the Relief Canyon expansion properties, located to the south of the Relief Canyon Mine property and for the Coal Canyon Property, located to the west of the Relief Canyon Mine property. A Notice of Intent includes information regarding the company submitting the notice, maps of the proposed disturbance, equipment to be utilized, the general schedule of operations, a calculation of the total disturbance anticipated, and a detailed reclamation plan and budget. We have provided a $10,500 reclamation bond for the Pershing Pass Notice of Intent and a $11,200 reclamation bond for the Coal Canyon Notice of Intent to ensure reclamation of our exploration activities on public lands based on the estimated third-party costs to reclaim and re-vegetate the disturbed acreage. It is not necessary to file a Notice of Intent prior to work on private land. Measurement of land disturbance is cumulative, and once five acres total of public lands have been disturbed and remain unreclaimed in one project area, a Plan of Operations must be filed and approved by the BLM before additional work can take place, and a Reclamation Permit must be obtained from the NDEP. Both the Plan of Operations and the NDEP Reclamation Permit require a cash bond and a reclamation plan. Future exploration at Pershing Pass or Coal Canyon could require a Plan of Operations and a NDEP Reclamation Permit.

We do not anticipate discharging water into active streams, creeks, rivers and lakes because there are no bodies of water near the Relief Canyon project area. We also do not anticipate disturbing any endangered species or archaeological sites or causing damage to our property. Re-contouring and re-vegetation of disturbed surface areas would be completed pursuant to the applicable permits. The cost of reclamation work varies according to the degree of physical disturbance. It is difficult to estimate the future cost of compliance with environmental laws since the full nature and extent of our future activities cannot be determined at this time.

Other Exploration

We conducted generative exploration on the Relief Canyon expansion properties in 2012 and 2013. Since then, we have generated geological mapping over approximately three-quarters of our broader land holdings and conducted other exploratory work, including exploratory drilling at three targets in the expansion properties: Buffalo, Buffalo Pediment and the Blackjack Project Area. We intend to continue to focus our expenditures on the Relief Canyon Mine property. Because the Relief Canyon expansion properties are at an early stage of exploration, it would take significant time to perform sufficient exploration drilling to determine whether these properties contain mineable reserves that could be put into production in the future. Although we are not currently planning to resume exploration efforts with respect to the Relief Canyon expansion properties, we may in the future increase our exploration efforts depending on results and available funding.

We intend to continue to acquire additional mineral targets in Nevada and elsewhere in locations where we believe we have the potential to quickly expand and advance known mineralization and the potential to discover new deposits. If, through our exploration program, we discover an area that potentially may be profitably mined for gold, we would focus on determining whether that is feasible, including further delineation of the location, size and economic feasibility of a potential orebody. We will require external funding to pursue our exploration programs. There is no assurance we will be able to raise capital on acceptable terms or at all.

Employees

We currently have 19 full-time employees. We believe that our relations with our employees are good. In the future, if our activities grow, we may hire personnel on an as-needed basis. For the foreseeable future, we plan to engage geologists, engineers and other consultants as necessary.

Competition

We compete with other exploration companies for the acquisition of a limited number of exploration rights, and many of the other exploration companies possess greater financial and technical resources than we do. The mineral exploration industry is highly fragmented, and we are a very small participant in this sector. Many of our competitors explore for a variety of minerals and control many different properties around the world. Many of them have been in business longer than we have and have established more strategic partnerships and relationships. We also compete with other exploration companies for the acquisition and retention of skilled technical personnel.

| 17 |

Our competitive position depends upon our ability to acquire and explore new and existing gold properties. However, there is significant competition for properties suitable for gold exploration. Failure to achieve and maintain a competitive position could adversely impact our ability to obtain the financing necessary for us to acquire gold properties. As a result, we may be unable to continue to acquire interests in attractive properties on terms that we consider acceptable. We will be subject to competition and unforeseen limited sources of supplies in the industry in the event spot shortages arise for supplies such as explosives, and certain equipment such as drill rigs, bulldozers and excavators that we will need to conduct exploration. If we are unsuccessful in securing the products, equipment and services we need we may have to suspend our exploration plans until we are able to secure them.

Market for Gold

In the event that gold is produced from our property, we believe that wholesale purchasers for the gold would be readily available. Readily available wholesale purchasers of gold and other precious metals exist in the United States and throughout the world. Among the largest are Handy & Harman, Engelhard Industries and Asahi Refining. Historically, these markets are liquid and volatile. In 2018 and through March 22, 2019, the London Fix AM high and low gold fixes were $1,360.25 and $1,176.70 per troy ounce, respectively, which represents an approximate 0.6% increase and 2.4% increase in gold prices as compared to the high and low gold price in 2017, respectively. Wholesale purchase prices for precious metals can be affected by a number of factors, all of which are beyond our control, including but not limited to:

| · | fluctuation in the supply of, demand and market price for gold; |

| · | mining activities of our competitors; |

| · | sale or purchase of gold by central banks and for investment purposes by individuals and financial institutions; |

| · | interest rates; |

| · | currency exchange rates; |

| · | inflation or deflation; |

| · | fluctuation in the value of the United States dollar and other currencies; and |

| · | political and economic conditions of major gold or other mineral-producing countries. |

Gold ore is typically mined and leached to produce pregnant solutions, which are processed through a series of steps to recover gold and produce doré. Doré is then sold to refiners and smelters for the value of the minerals that it contains, less the cost of further refining and smelting. Refiners and smelters then sell the gold on the open market through brokers who work for wholesalers including the major wholesalers listed above.

| ITEM 1A: | RISK FACTORS |

Our investors should consider the following risk factors carefully, in addition to the other information contained in, or incorporated by reference into, this annual report on Form 10-K.

| 18 |

Risks Related to Our Business

We do not know if our properties contain any gold or other minerals that can be mined at a profit.

The properties on which we have the right to explore for gold and other minerals do not contain SEC Industry Guide 7 compliant mineral reserves and we do not know if any deposits of gold or other minerals can be mined at a profit. Whether a gold or other mineral deposit can be mined at a profit depends upon many factors. Some but not all of these factors include: the particular attributes of the deposit, such as size, grade and proximity to infrastructure; operating costs and capital expenditures required to start mining a deposit; the availability and cost of financing; the price of the gold or other minerals which is highly volatile and cyclical; and government regulations, including regulations relating to prices, taxes, royalties, land use, importing and exporting of minerals and environmental protection. We are also obligated to pay production royalties on certain of our mineral production, including a net smelter royalty of 2% on production from most of our Relief Canyon Mine property, with a portion of the deposit located on property subject to net smelter return royalties totaling 4.5%, which would increase our costs of production and make our ability to operate profitably more difficult. We are also obligated to pay a net smelter royalty of up to 5% on production from some of our claims and lands.

We are an exploration stage company and have conducted exploration activities only since 2011. We reported a net loss for the year ended December 31, 2018, and expect to incur operating losses for the foreseeable future.

Our evaluation of our Relief Canyon Mine property is primarily based on historical production data and on new exploration data that we have developed since 2011, supplemented by historical exploration data. Our plans for recommencing mining and processing activities at the Relief Canyon Mine property are still being developed, as are our exploration programs on the Relief Canyon expansion properties. Accordingly, we are not yet in a position to precisely estimate expected amounts of minerals, yields or values or evaluate the likelihood that our business will be successful. We have not earned any revenues from mining operations. The likelihood of success must be considered in light of the problems, expenses, difficulties, complications and delays encountered in connection with the exploration of the mineral properties and commencement of mining activities that we plan to undertake. These potential problems include, but are not limited to, unanticipated problems relating to exploration, costs and expenses that may exceed current estimates and the requirement for external funding to continue our business. Prior to completion of our exploration stage, we anticipate that we will incur increased operating expenses without realizing any revenues. We reported a net loss of approximately $14.2 million for the year ended December 31, 2018. We expect to incur significant losses into the foreseeable future. Our monthly burn rate for all costs during 2018 was approximately $1.1 million, including $0.8 million for general and administrative costs (including all employee salaries, public company expenses, consultants, and land holdings costs) and $0.3 million for exploration activities. To pursue the commencement of mining and processing at Relief Canyon, additional external financing would be required. If we are unable to raise external funding, and eventually generate significant revenues from our claims and properties, we will not be able to earn profits or continue operations. We have no production history upon which to base any assumption as to the likelihood that we will prove successful, and it is uncertain that we will generate any operating revenues or ever achieve profitable operations. If we are unsuccessful in addressing these risks, our business will most likely fail.

Exploring for gold and other minerals is inherently speculative, involves substantial expenditures, and is frequently non-productive.

Mineral exploration (currently our only business), and gold exploration in particular, is a business that by its nature is very speculative. We may not be able to establish mineral reserves on our properties or be able to mine any gold or any other minerals on a profitable basis. Few properties that are explored are ultimately developed into producing mines. Unusual or unexpected geological conditions, fires, flooding, explosions, cave-ins, landslides and the inability to obtain suitable or adequate machinery, equipment or labor are just some of the many risks involved in mineral exploration programs and the subsequent development of gold deposits.

The mining industry is capital intensive and we may be unable to raise necessary funding.

We spent approximately $13.7 million on our business and exploration during the year ended December 31, 2018. In addition to anticipated G&A and exploration costs in 2019, in order to commence mining at Relief Canyon, based on the estimates contained in the feasibility study, it would require capital expenditures and working capital expenditures of approximately $38 million. To pursue the commencement of production at Relief Canyon, additional external financing would be required. Such additional financing could include streaming, royalty financing, forward sale arrangements, debt offerings (including convertible debt), additional equity financing or other alternatives. In addition, even if we do not decide to pursue the commencement of production at Relief Canyon, we will be required to raise additional funds in order to finance our operations. We may be unable to secure additional financing on terms acceptable to us, or at all. Our inability to raise additional funds would prevent us from achieving our business objectives and would have a negative impact on our business, financial condition, results of operations and the value of our securities. If we raise additional funds by issuing additional equity or convertible debt securities, the ownership of existing stockholders may be diluted and the securities that we may issue in the future may have rights, preferences or privileges senior to those of the current holders of our common stock. Such securities may also be issued at a discount to the market price of our common stock, resulting in possible further dilution to the book value per share of common stock. If we raise additional funds by issuing debt, we could be subject to debt covenants that could place limitations on our operations and financial flexibility.

| 19 |

Unanticipated problems or delays may negatively affect our ability to commence mining and processing activities at Relief Canyon.

If we were to decide to pursue the commencement of mining and processing activities at Relief Canyon, additional external financing would be required. Although the Relief Canyon Mine currently has an available leach pad and processing facility and we have senior mine and processing personnel in place, we would be required to obtain mining equipment (which could be through purchase, lease, contract mining or a combination of these), hire employees for the mine and the processing plant, purchase materials and supplies, commence mining, leaching and processing activities, and continue these activities as well as the corporate activities currently conducted for a number of months until sufficient positive cash flow is produced by gold sales to fund all of these ongoing activities. We may suffer significant delays or cost overruns as a result of a variety of factors, such as increases in the prices of materials, mining or processing problems, unanticipated variations in mined materials, shortages of workers or materials, transportation constraints, adverse weather, equipment failures, fires, damage to or destruction of property and equipment, environmental problems, unforeseen difficulties or labor issues, any of which could delay or prevent us from commencing or ramping up mining and processing. If our start-up were prolonged or delayed or our costs were higher than anticipated, we could be unable to obtain sufficient funds to cover the additional costs, and our business could experience a substantial setback. Prolonged problems could have a material adverse effect on our business, consolidated financial condition or results of operations and threaten our viability.

We must make annual lease payments, advance royalty and royalty payments and claim maintenance payments or we will lose our rights to our property.

We are required under the terms of the leases covering some of our property interests to make annual lease payments and advance royalty and royalty payments each year. We are also required to make annual claim maintenance payments to the BLM and pay a fee to Pershing County in order to maintain our rights to explore and, if warranted, to develop our unpatented mining claims. If we fail to meet these obligations, we will lose the right to explore for gold and other minerals on our property. Our total annual property maintenance costs payable to the BLM and Pershing County for all of the unpatented mining claims and millsites in the Relief Canyon area in 2018 were approximately $220,000, and we expect our annual maintenance costs to be approximately $220,000 in 2019. Our lease payments, advance royalty and royalty payments and claim maintenance payments are described above under “Business and Properties” on page 5.

| 20 |

Our business is subject to extensive environmental regulations that may make exploring, mining or related activities prohibitively expensive, and which may change at any time.

All of our operations are subject to extensive environmental regulations that can substantially delay exploration and mine development and make exploration and mine development expensive or prohibit it altogether. We may be subject to potential liabilities associated with the pollution of the environment and the disposal of waste products that may occur as the result of exploring and other related activities on our properties, including our plan to process gold at our processing facility. We may have to pay to remedy environmental pollution, which may reduce the amount of money that we have available to use for exploration, mine development, or other activities, and adversely affect our financial position. If we are unable to fully remedy an environmental problem, we might be required to suspend operations or to enter into interim compliance measures pending the completion of the required remedy. If a decision is made to mine our properties and we retain any operational responsibility for doing so, our potential exposure for remediation may be significant, and this may have a material adverse effect upon our business and financial position. We have not purchased insurance for potential environmental risks (including potential liability for pollution or other hazards associated with the disposal of waste products from our exploration activities) and such insurance may not be available to us on reasonable terms or at a reasonable price. All of our exploration and, if warranted, development activities will be subject to regulation under one or more local, state and federal environmental impact analyses and public review processes. It is possible that future changes in applicable laws, regulations and permits or changes in their enforcement or regulatory interpretation could have significant impact on some portion of our business, which may require our business to be economically re-evaluated from time to time. These risks include, but are not limited to, the risk that regulatory authorities may increase bonding requirements beyond our financial capability. Inasmuch as posting of bonding in accordance with regulatory determinations is a condition to the right to operate under specific federal and state operating permits, increases in bonding requirements could prevent operations even if we are in full compliance with all substantive environmental laws. We have been required to post a substantial bond under various laws relating to mining and the environment and may in the future be required to post a larger bond to pursue additional activities. For example, we must provide BLM and the NDEP additional financial assurance (reclamation bonds) to guarantee reclamation of any new surface disturbance required for drill roads, drill sites, or mine expansion. In February 2018, we increased the amount of our reclamation bond with BLM and the NDEP to approximately $12.5 million. Approximately $12.4 million of our reclamation bond covers both exploration and mining at the Relief Canyon Mine property, including the three open pit mines and associated waste rock disposal areas, the mineral processing facilities, ancillary facilities, and the exploration roads and drill pads. Approximately $22,000 covers exploration on the Relief Canyon expansion properties. The reclamation bond was collateralized by approximately 30% of the $12.5 million bond amount, or about $3.7 million. Approximately $80,000 of the reclamation bond remains available for future mining or exploration operations. Our preliminary estimate of the likely amount of additional financial assurance for future exploration is approximately $100,000, although we expect periodic increases due to effects of inflation.

The government licenses and permits which we need to explore on our property may take too long to acquire or cost too much to enable us to proceed with exploration. In the event that we conclude that the Relief Canyon Mine deposit can be profitably mined, or we discover other commercially exploitable deposits, we may face substantial delays and costs associated with securing the additional government licenses and permits that could preclude our ability to develop the mine.