|

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

|

|

|

|

FORM 10-K

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the Fiscal Year Ended: December 31, 2013

or

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the Transition Period from to

Commission File No. 001-35366

|

|

|

|

CORONADO BIOSCIENCES, INC.

(Exact Name of Registrant as Specified in its Charter)

|

Delaware

|

20-5157386

|

|

||

|

|

(State or Other Jurisdiction of

|

(I.R.S. Employer

|

||

|

|

Incorporation or Organization)

|

Identification No.)

|

||

|

|

|

|

||

|

24 New England Executive Park, Suite 105

|

|

|

||

|

Burlington, MA

|

01803

|

|

||

|

(Address of Principal Executive Offices)

|

(Zip Code)

|

|

||

Registrant’s telephone number, including area code: (781) 652-4500

Securities registered pursuant to Section 12(b) of the Act:

|

(Title of Class)

|

|

(Name of exchange on which registered)

|

|

Common Stock, par value $0.001 per share

|

|

NASDAQ Capital Market

|

Securities registered pursuant to section 12(g) of the Act:

None.

|

|

|

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

¨

|

Accelerated filer

|

x

|

|

|

|

|

|

|

Non-accelerated filer

|

¨ (Do not check if a smaller reporting company)

|

Smaller reporting company

|

¨

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

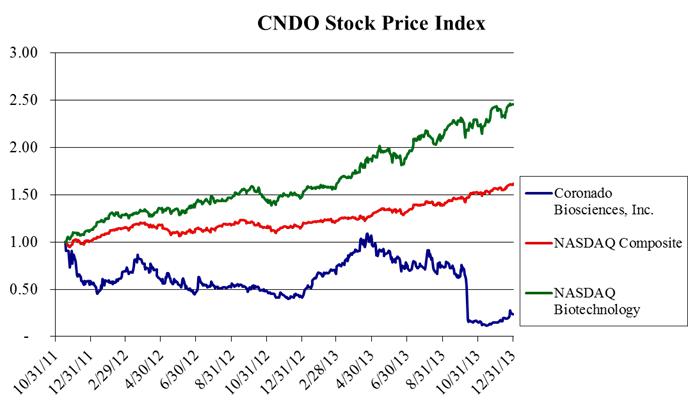

The aggregate market value of the voting stock held by non-affiliates of the registrant as of the last business day of the registrant’s most recently completed second fiscal quarter: $162,039,807 based upon the closing sale price of our common stock of $8.60 on that date. Common stock held by each officer and director and by each person known to own in excess of 5% of outstanding shares of our common stock has been excluded in that such persons may be deemed to be affiliates. The determination of affiliate status in not necessarily a conclusive determination for other purposes.

As of March 12, 2014, there were 44,086,387 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for its 2014 Annual Meeting of Stockholders currently scheduled to be held on June 16, 2014 are incorporated by reference into Part III hereof.

CORONADO BIOSCIENCES, INC.

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

|

|

|

|

Page

|

|

|

|

|

|

|

PART I

|

|

1

|

|

|

Item 1.

|

Business

|

|

1

|

|

Item 1A.

|

Risk Factors

|

|

19

|

|

Item 1B.

|

Unresolved Staff Comments

|

|

30

|

|

Item 2.

|

Properties

|

|

31

|

|

Item 3.

|

Legal Proceedings

|

|

31

|

|

Item 4.

|

Mine Safety Disclosures

|

|

31

|

|

|

|

|

|

|

PART II

|

|

32

|

|

|

Item 5.

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

|

32

|

|

Item 6.

|

Selected Consolidated Financial Data

|

|

34

|

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

|

34

|

|

Item 7A.

|

Quantitative and Qualitative Disclosures About Market Risk

|

|

45

|

|

Item 8.

|

Financial Statements and Supplementary Data

|

|

45

|

|

Item 9.

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

|

45

|

|

Item 9A.

|

Controls and Procedures

|

|

45

|

|

Item 9B.

|

Other Information

|

|

46

|

|

|

|

|

|

|

PART III

|

|

47

|

|

|

Item 10.

|

Directors, Executive Officers and Corporate Governance

|

|

47

|

|

Item 11.

|

Executive Compensation

|

|

47

|

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

|

47

|

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence

|

|

48

|

|

Item 14.

|

Principal Accountant Fees and Services

|

|

48

|

|

|

|

|

|

|

PART IV

|

|

49

|

|

|

Item 15.

|

Exhibits and Financial Statement Schedules

|

|

49

|

CAUTIONARY NOTE REGARDING FORWARD LOOKING STATEMENTS

Statements in this Annual Report on Form 10-K that are not descriptions of historical facts are forward-looking statements that are based on management’s current expectations and are subject to risks and uncertainties that could negatively affect our business, operating results, financial condition and stock price. We have attempted to identify forward-looking statements by terminology including “anticipates,” “believes,” “can,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “might,” “plans,” “potential,” “predicts,” “should,” or “will” or the negative of these terms or other comparable terminology. Factors that could cause actual results to differ materially from those currently anticipated include those set forth under “Item 1A. Risk Factors” including, in particular, risks relating to:

| · | our growth strategy; |

| · | the results of research and development activities; |

| · | uncertainties relating to preclinical and clinical testing; |

| · | financing and strategic agreements and relationships; |

| · | the early stage of products under development; |

| · | our need for substantial additional funds and uncertainties relating to financings; |

| · | our ability to attract, integrate and retain key personnel; |

| · | our ability to manufacture our product; |

| · | government regulation; |

| · | patent and intellectual property matters; |

| · | dependence on third party manufacturers; and |

| · | competition. |

We expressly disclaim any obligation or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in our expectations or any changes in events, conditions or circumstances on which any such statement is based, except as required by law.

PART I

|

Item 1.

|

Business.

|

Overview

Since inception, we have been a biopharmaceutical company involved in the development of novel immunotherapy agents for the treatment of autoimmune diseases and cancer, namely CNDO-201 or Trichuris suis ova (“TSO”) and CNDO-109, as more fully described below. As part of our growth strategy, we plan to identify, evaluate and potentially in-license, acquire or invest in pharmaceutical and biotechnology products, technologies and/or companies. We may also from time to time consider financing existing or later-acquired products, technologies or companies through partnerships, joint ventures, direct financings, and/or public or private spin-outs. We believe these activities will diversify our product development and, over time, may enhance shareholder value through potential royalty, milestone and equity payments, fees as well as potential product revenues.

TSO

CNDO-201 is a biologic comprising the microscopic eggs of the porcine whipworm, which we believe could be used for the treatment of a range of autoimmune diseases, such as Crohn’s disease or CD, ulcerative colitis or UC, multiple sclerosis or MS, autism, psoriasis and Type 1 diabetes or T1D.

In February 2012, we announced positive results from our Phase 1 clinical trial of TSO in 36 patients with CD. The trial was a sequential dose-escalation, double-blind, placebo-controlled study to examine safety and tolerability. TSO was shown to be safe and well tolerated, with no serious treatment-related adverse events reported. To date, a number of investigator-sponsored clinical trials have been conducted using TSO in patients suffering from CD, UC, MS, autism and psoriasis. These studies also demonstrated that TSO is safe and well tolerated.

| 1 | ||

In August 2012, we initiated in the United States a Phase 2 randomized, double-blind, placebo-controlled clinical trial of TSO, known as TRUST-I, designed to evaluate the safety and efficacy of TSO in CD. The study enrolled 250 patients with moderate-to-severe CD to receive either 7500 ova (N=125) or placebo (N=125) once every two weeks for 12 weeks. In October 2013, we reported that the TRUST-I study did not meet its primary endpoint of improving response, defined as a 100-point decrease in the CD Activity Index (“CDAI”), nor the key secondary endpoint of remission, defined as achieving CDAI < 150 points. In the overall patient population, response rate of patients on TSO did not separate from that of placebo. The randomization was stratified by disease activity as measured by CDAI. In the pre-defined subset analysis in patients with baseline CDAI > 290 (N=121), TSO showed a non-significant improved response. The lack of overall response was driven by a higher-than-expected placebo response rate in patients with CDAI < 290. TSO was safe and well-tolerated, and adverse events were balanced between the TSO and the placebo group. The most common adverse event reported was abdominal pain and occurred in 11% of both TSO and placebo groups.

In November 2013, Dr. Falk Pharma GmbH (“Falk”), our development partner, informed us that an independent data monitoring committee (“IDMC”) had conducted a second interim analysis of data from approximately 240 patients who had completed 12 weeks of treatment in Falk’s Phase 2 clinical trial in Europe evaluating TSO in CD. The committee recommended that the trial be stopped due to lack of efficacy and noted no safety concerns. Falk adopted the committee’s recommendations and discontinued the study. The Falk trial, also known as the TRUST-II study, is a double-blind, randomized, placebo-controlled, multi-center Phase 2 study to evaluate the efficacy and safety of three different dosages of oral TSO in patients with active CD.

We have the exclusive rights to TSO in North America, South America and Japan (the “Coronado Territories”) under a sublicense agreement with Ovamed GmbH, or Ovamed, as well as a manufacturing and supply agreement with Ovamed to provide us with our clinical and commercial requirements of TSO. In December 2012, we signed the Second Amendment and Agreement to our sublicense agreement with Ovamed, which provides us the exclusive right to manufacture TSO for the Coronado Territories in exchange for certain consideration to Ovamed. We anticipate in the near term continuing to purchase TSO supplies from Ovamed, as a result of the outcome of TRUST-I. We are currently evaluating our TSO manufacturing plans.

In March 2012, we entered into a Collaboration Agreement with Ovamed and Falk, Ovamed’s sublicensee in Europe for gastroenterology indications, under which we agreed to collaborate in the development of TSO for CD. Under the Collaboration Agreement, Falk granted us exclusive rights and licenses under certain Falk patent rights, pre-clinical data and clinical data from Falk’s clinical trials of TSO in CD, including Falk’s ongoing Phase 2 clinical trial, for use in North America, South America and Japan. We granted Falk exclusive rights and licenses to data from our clinical trials of TSO in CD for use in Europe. A steering committee comprised of our representatives and representatives of Falk and Ovamed is overseeing the clinical development program for CD, under which we and Falk will each be responsible for clinical testing on approximately 50% of the total number of patients required for regulatory approval of TSO for CD in the United States and Europe and will share in certain pre-clinical development costs.

On February 22, 2013, we and Freie Universität Berlin (“FU Berlin”) entered into a Research Agreement to, among other things identify and evaluate secretory proteins from TSO. The duration of the project is expected to be four years, during which time the Company will pay FU Berlin a total maximum amount of approximately $853,000 in research fees, commencing February 2013 and ending January 2017. Through December 31, 2013, we paid approximately $183,000 in research fees. We also entered into several license agreements regarding intellectual property that may result from this research. (See Note 14 of Notes to Consolidated Financial Statements.)

In December 2013, we announced that we submitted an Investigational New Drug (“IND”) application to the U.S. Food and Drug Administration (“FDA”) to begin a Phase 2 clinical study of TSO for the treatment of moderate-to-severe chronic plaque psoriasis. We also held a pre-IND meeting with the FDA regarding TSO for the treatment of autism.

CNDO-109

CNDO-109 is a biologic that activates the immune system’s natural killer, or NK, cells to seek and destroy cancer cells. We intend to study CNDO-109 initially in patients that have been diagnosed with acute myeloid leukemia, or AML. Preclinical studies have demonstrated that CNDO-109 activated NK cells directly kill cells that cause hematologic malignancies including myeloid leukemia and multiple myeloma, as well as breast, prostate and ovarian cancers. Eight patients with high-risk AML received CNDO-109 activated NK cells in a recent Phase 1 investigator-sponsored trial. Although the primary endpoint of the Phase 1 clinical trial was safety, based on the data obtained from this Phase 1 study, we believe early efficacy was observed. The clinical investigators observed that the majority of patients experienced a longer complete remission than their previous complete remission. In February 2012, we filed an Investigational New Drug application, or IND, for a multi-center Phase 1/2 clinical trial in patients with relapsed AML. In November 2012, we initiated this trial. In June 2012, the FDA granted orphan drug designation to CNDO-109 activated NK cells for the treatment of AML and, in September 2012, the U.S. Patent and Trademark Office granted the first U.S. patent covering CNDO-109. In February 2014, a second key patent directed to compositions comprising these activated NK cells was granted. We have exclusive worldwide rights to develop and market CNDO-109 under a license agreement with the University College London Business PLC, or UCLB. In 2013, we enrolled three patients in the Phase 1/2 trial, which is on-going.

| 2 | ||

Industry

Immunology Therapeutics Markets

Autoimmune diseases represent a diverse collection of diseases in terms of their demographic profile and primary clinical manifestations. The phenotypic commonality between them, however, is the damage, driven by a dysfunctional immune system, to tissues and organs that arises from the loss of tolerance or recognition of “self.” Autoimmune disorders include inflammatory bowel disease, or IBD, such as CD and UC, MS, autism, psoriasis, and T1D.

According to a 2012 Decision Resources report, in the United States and Japan, the estimated prevalence of CD was 534,000 patients, UC was 669,000 patients and MS was 485,000 patients. Autism statistics from the U.S. Centers for Disease Control and Prevention, or CDC, identify around 1 in 88 American children as on the autism spectrum–a ten-fold increase in prevalence in 40 years. According to the National Psoriasis Foundation, psoriasis is the most prevalent autoimmune disease in the United States affecting as many as 7.5 million Americans. According to the 2011 National Diabetes Foundation Fact Sheet (released January 26, 2011 by the American Diabetes Association), nearly 26 million Americans have diabetes and between 5-10% or up to 2.5 million have T1D. Prevalence rates for all autoimmune disorders are expected to continue to rise in the next several years. Each of these diseases is believed to be associated with an excessive inflammatory response and dysfunctional immune system, including abnormal activity of T regulatory (“Treg”) cells.

CD is characterized by inflammation of the gastrointestinal tract that causes painful and debilitating symptoms. Most patients with CD experience relapses, and no current therapy is completely effective in preventing acute flares. Although immunosuppressants and TNF-inhibitors are effective maintenance therapies, according to an article published in Alimentary Pharmacology & Therapeutics in 2011, fewer than 50% of patients maintain long-term remission with these drugs. According to a 2007 article in Surgical Clinics of North America, a significant percentage of CD patients require surgery during their lifetime despite available therapies. Therefore, we believe the greatest unmet need is for more effective maintenance therapies that are also safe for long-term use.

The etiology and pathophysiology of UC are not fully understood, but research appearing in several industry publications, including Inflammatory Bowel Disease (2006) and the World Journal of Gastroenterology (2006), strongly suggests that genetic susceptibility and environmental factors, coupled with an abnormal immune response, contribute to the development of the disease. Despite significant advances in the understanding of genetic susceptibility and its role in IBD, novel, targeted therapies for the treatment of UC have yet to be identified. We believe the need for safe and more effective maintenance therapies with sustained long-term efficacy are the greatest unmet need in the management of UC.

MS is an autoimmune inflammatory disease of the central nervous system that is characterized by progressive neuronal loss that manifests clinically as worsening physical disability. The key pathophysiological hallmark of MS is the loss of myelin, a layer of lipids and proteins produced by cells called oligodendrocytes that wrap around the neuron and act like an insulating sheath to facilitate electrical conduction along the nerve. Destruction of myelin by an inflammatory cascade leads to neuronal degeneration. As a result, we believe that there is a substantial unmet need for effective treatments for chronic progressive MS as well as a need for therapies that are more conveniently delivered (e.g., oral agents and less-frequently administered injectable drugs).

Autism is a disorder of neural development characterized by impaired social interaction, impaired social communication, and restricted and repetitive behavior. The diagnostic criteria require that symptoms become apparent before a child is three years old. Autism affects information processing in the brain by altering how nerve cells and their synapses connect and organize. How this occurs is not well understood. It is one of three recognized disorders in the autism spectrum, the other two being Aspberger syndrome, which lacks delays in cognitive development and language, and pervasive development disorder, not otherwise specified, which is diagnosed when the full set of criteria for autism or Asperger syndrome are not met. Increasingly, researchers are looking at the role of the immune system in autism. Intervention can involve behavioral treatments, medicines or both. There are no FDA-approved medicines for treating all three core symptoms of autism, but there are two drugs for treating the irritability associated with autism (risperidone – Risperdal; and aripiprazole—Abilify).

Psoriasis (psoriasis vulgaris) is a chronic inflammatory skin disease characterized by red, scaly, raised plaques. The disease process is driven by T-cell infiltration and associated elevation in cytokine levels leading to increased cell division and aberrant differentiation, resulting in the psoriatic phenotype. While many patients with mild disease are able to control psoriasis symptoms with topical medications alone, patients with moderate to severe disease usually require treatment with systemic agents to achieve good clearance. These systemic agents are usually well tolerated, but can have potentially significant side effects including organ toxicity, infection, malignancy, and teratogenicity that limit their usefulness in the long-term management of psoriasis.

Diabetes mellitus is the condition defined by the body’s inability to regulate blood glucose (sugar) levels. There are two major types of diabetes, T1D and type 2 diabetes, or T2D. T1D, also called juvenile diabetes or insulin-dependent diabetes, is a disorder of the body’s immune system. T1D occurs when the body’s immune system attacks and destroys the beta cells in the pancreas. These cells are located within small islands of endocrine cells called the pancreatic islets. Beta cells normally produce insulin, a hormone that helps the body move the glucose contained in food into cells throughout the body, which use it for energy. But when the beta cells are destroyed, no insulin can be produced, and the glucose stays in the blood instead, where it can cause serious damage to all the organ systems of the body. Insulin is currently the major treatment for people with T1D, and exists as short, medium and long-acting version. A relatively small number of people also use Symlin (pramlintide acetate) injections to help normalize their blood sugar.

| 3 | ||

Oncology Therapeutics Markets

The American Cancer Society estimates that over 1.6 million people in the United States are expected to be diagnosed with cancer in 2012, excluding basal and squamous cell skin cancers and in situ carcinomas (other than urinary bladder carcinomas). This is an increase of approximately 33% from the estimated number of new cancer diagnoses in 2000. We believe this rate is unlikely to decrease in the foreseeable future as the causes of cancer are multiple and poorly understood.

Despite continuous advances every year in the field of cancer research, we believe there remains a significant unmet medical need in the treatment of cancer, as the overall five-year survival rate for a cancer patient diagnosed between 2001 and 2007 still averages only 67% according to the American Cancer Society. According to that same source, cancer is the second leading cause of mortality in the United States after heart disease. The American Cancer Society estimates that approximately one in four deaths in the United States is due to cancer.

AML is one of the most deadly and most common types of acute leukemia in adults. According to a 2011/2012 Decision Resources report, there are over 43,000 cases worldwide, primarily afflicting elderly and relapsed and refractory populations. Once diagnosed with AML, patients typically receive induction and consolidation chemotherapy, with the majority achieving complete remission. However, about 70–80% of patients who achieve first complete remission will relapse, and the overall five-year survival rate is less than 25%.

One of the main treatments for cancer is chemotherapy. While chemotherapy is the most widely used class of anti-cancer agents, individual chemotherapeutic agents often show limited efficacy because tumors maintain complex machinery to repair the DNA damage to tumor cells caused by chemotherapy. Solutions to this problem include combination chemotherapy, but while combination chemotherapy has been intensively studied, it offers only limited hope for improvement as a result of additive toxicities. The limitations inherent in chemotherapy are mirrored by limitations in other therapeutic modalities for cancer, including radiation therapy, targeted therapies and surgical intervention. Each of these therapies either has high levels of toxicity and/or potentially severe adverse events, which in turn frequently limit the amount of treatment that can be administered to a patient.

As a result, we believe that there is a significant unmet medical need for alternatives to existing chemotherapy drugs that do not have the associated toxicities of traditional chemotherapy drugs.

Our Existing Product Candidates

TSO

TSO is a biologic product candidate for the treatment of autoimmune diseases. We currently plan to investigate TSO for the treatment of CD, UC, MS, autism spectrum disorder, and plaque psoriasis.

Background

The rationale for performing research with helminths initially was based on the hygiene hypothesis postulating that multiple exposures to parasites and pathogens in childhood can protect an individual from allergic and autoimmune disease later in life, whereas individuals raised in a more sanitary environment are more likely to develop autoimmune diseases and allergies. These hypotheses and several studies suggest that exposure to helminth parasites which have followed human evolution may protect against and treat autoimmune disorders. This hygiene hypothesis is based on epidemiologic findings of an inverse relationship between autoimmune diseases and helminthic colonization. According to articles published in the New England Journal of Medicine in 2002 and Inflammatory Bowel Disease in 2009, the incidence of autoimmune disease is highest in the developed world and in temperate climates, with positive correlations noted among persons of higher socioeconomic status and high levels of domestic hygiene experienced in childhood.

Furthermore, the incidence of autoimmune disease has increased over the past several decades, while the prevalence of helminths in the United States and Europe has steadily declined during the same time period. These findings have led to the hypothesis that eliminating intestinal helminths in the industrialized world has eliminated a natural T regulatory cell mechanism that prevents excessive T-cell activation such as occurs in IBD as well as in other immune-mediated diseases such as MS and allergies.

The immunologic basis for helminth therapy is derived from experimental animal and human data demonstrating that these organisms alter immune responses beyond those directed against the worms. In animal models, helminths blunt Th1 responses and promote Th2 responses associated with increased production of IL-4 and IL-3. Helminthic colonization in humans can result in diminished Th1 immune responses to challenges with unrelated antigens, as well as increased production of immunomodulatory molecules such as IL-10, transforming growth factor (“TGF”)-ß, and regulatory T-cells. Thus, as noted in the National Review of Immunology in 2007, genetically susceptible persons who are never exposed to helminths may lack a strong Th2 immune response and develop a poorly regulated and destructive intestinal Th1 response, leading to chronic colitis or ileitis.

The study of TSO as it relates to autoimmune disease originates from the work of Dr. Joel V. Weinstock, currently the Chief of the Division of Gastroenterology/Hepatology at Tufts New England Medical Center in Boston. Dr. Weinstock’s research has centered on the evolutionary role of the parasitic helminth, or worm, infections in the prevention of inflammatory diseases. Dr. Weinstock is a consultant of our Company . Certain of his colleagues, namely David Elliott, M.D., Ph.D., and William Sanborn, M.D. are also consultants of our Company.

| 4 | ||

TSO was chosen as an appropriate helminth for therapeutic application due to its ability to colonize in humans briefly without invading or infecting the host. Although not a human parasite, T. suis resembles the human whipworm T. trichuris and is able to colonize in a human host for several weeks before being eliminated from the body without the need for antihelminthic therapy. As reported TSO has potential for being a natural immune system modulator without significant risk of causing disease in humans. Mature T. suis produce ova that exit the porcine host with the stool, however, we believe ova are not infective until incubating in the soil for several weeks, thereby preventing direct host-to-host transmission. We believe that no human diseases have been associated with exposure to T. suis or TSO.

Third Party Clinical Trials

A number of studies have been performed by independent investigators in small samples of patients across a range of diseases with an immune component. These studies evaluated the safety, tolerability and efficacy of TSO treatment.

The first phase I trial was reported in 2003 (Summers, American Journal of Gastroenterology), and included seven patients with refractory IBD (four patients with active CD and three patients with UC). Patients received a single dose of 2500 live TSO orally with 30 ml of Gatorade (Gatorade, Chicago, IL). After a treatment and observation period of at least 12 weeks, two patients with CD and two patients with UC were given additional doses of 2500 ova at three-week intervals in a maintenance period. Efficacy was assessed by improvement in the common clinical indices used to describe disease activity. During the treatment and observation period, all patients improved clinically without any adverse clinical events or laboratory abnormalities. Three of the four patients with CD entered remission while the fourth patient experienced a clinical response. Patients with UC experienced a reduction of the Clinical Colitis Activity Index to 57% of baseline. According to the IBD Quality of Life Index (Irvine et al., 1994), six of seven patients (86%) achieved remission by 8.3 weeks following their dose. The benefit derived from the initial dose was temporary, with the mean length of remission for the six patients who attained it approximately eight weeks. During the one-year maintenance period, multiple doses caused no adverse effects and sustained clinical improvement was observed in each of the four patients treated every three weeks for >28 weeks. While the benefit of treatment appeared temporary with a single dose, it was prolonged with maintenance therapy every three weeks for more than 1 year.

An open label, single-arm, phase II trial was conducted by Summers (Gut, 2005), with 29 patients with active CD. Over a period of 24 weeks, subjects returned every three weeks to drink the TSO suspended in a commercial drink. Dosing of all other inflammatory bowel disease medications was held constant. Disease activity was monitored by CDAI (Best et al., 1976). Remission was defined as a decrease in CDAI to less than 150 while a response was defined as a decrease in CDAI of greater than 100 points. Most patients responded and achieved remission. At week 12, the response rate was 75.9% and 19 of 29 patients (65.5%) showed complete remission. By week 24, the response rate was 79.3% and at this point 21 of 29 patients (72.4%) were in remission. Gender, patient age, disease duration, smoking status, or disease location had no influence on the frequency of response or remission. There was a trend for patients using immunosuppressive drugs to improve to a greater degree than those not using these agents.

A 12-week, randomized, two-arm, placebo-controlled double-blinded single center study was conducted by Summers and Elliot (Gastroenterology, 2005, and Current Opinions in Gastroenterology, 2005), with 54 patients with active UC; this study was followed by a 12-week crossover phase for patients who had not responded during the initial treatment period. The Ulcerative Colitis Disease Activity Index (“UCDAI”) (Walmsley et al., 1998) that assesses four variables assessed disease activity: stool frequency, severity of bleeding, mucosal appearance, and the physician's overall assessment of the disease activity, were used to assess efficacy. Active disease was defined by an UCDAI >four. Patients were treated with either TSO 2500 or matching placebo for up to 12 weeks. Improvement was defined as a decrease in UCDAI of at least four points. Clinical remission was defined by an UCDAI <2. After 12 weeks of treatment, 43.3% of patients treated with TSO achieved response compared to 16.7% in the placebo group (p=0.04, intention-to-treat analysis). Post hoc exploratory analyses of clinically relevant end points were performed by using the 4 components of the UCDAI (frequency of diarrhea, blood in stool, mucosal appearance, and overall assessment of clinical response). With the intention-to-treat analysis, ova-treated patients had significant improvements in stool frequency (p=0.0011), blood in the stool (p=0.0413), mucosal appearance (p<0.001), and overall assessment (p=0.0011) compared with their baseline values. The mean UCDAI decreased from 8.77 ± 0.35 to 6.1 ± 0.61 (p=0.0004) over the 12-week study. The placebo-treated subjects showed significant improvement only in stool frequency (p=0.0488). Their mean UCDAI decreased from 8.75 ± 0.46 to 7.5 ± 0.66 (p=0.1167).

The trial included a second 12-week double-blind crossover phase. Patients who were given placebo for the first 12 weeks and who were not in remission (n=17) were switched to T. suis for a second 12 week interval. Patients who initially received TSO and did not achieve remission (n=15) switched to placebo. At the end of the second phase, 56.3% of patients given TSO responded, whereas only 13.3% improved on placebo (p=0.02) (Elliott personal communication). Combining data from both 12-week periods indicated response rates of 47.8% with ova and 15.4% with placebo (p=0.002).

| 5 | ||

In a study reported in the Multiple Sclerosis Journal in 2011, Dr. John Fleming and his colleagues at the University of Wisconsin studied five subjects with newly diagnosed, treatment-naïve, relapsing–remitting multiple sclerosis, or RRMS. The patients were given 2500 TSO orally every two weeks for three months in a baseline versus treatment controlled trial. The study showed that the mean number of new gadolinium- enhancing magnetic resonance imaging, or MRI, lesions (n-Gdþ) fell from 6.6 at baseline to 2.0 at the end of TSO administration, and two months after TSO was discontinued, the mean number of n-Gdþ rose to 5.8 new lesions. No significant adverse effects were observed. In preliminary immunological investigations, increases in the serum level of the cytokines IL-4 and IL-10 were noted in four of the five subjects. These first five patients represented the first part of a 2-part study (known as HINT-1 and HINT-2). Additional patients are currently being studied for up to 10 months. Results from this second cohort are expected in the first half of 2014.

In studies presented by Dr. John Fleming and by Professor Per Soelberg Soerensen at the American Academy of Neurology in New Orleans on April 25, 2012, TSO was observed to be safe and well tolerated in MS patients, suggesting that TSO would be safe to use in indications other than IBD. Abstracts for these studies, entitled “Temporal Changes in MRI Activity, Inflammation, Immunomodulation, and Gene Expression in Relapsing-Remitting Multiple Sclerosis Subjects Treated with Helminth Probiotic Trichuris Suis” (Fleming) and “Trichuris Suis Ova Therapy for Relapsing Multiple Sclerosis—A Safety Study” (Soerenson) are available on the American Academy of Neurology 2012 Annual Meeting website.

In March 2012, we signed a Collaboration Agreement with Falk and Ovamed for the development of TSO for CD. Under the Collaboration Agreement, Falk granted us exclusive rights and licenses under certain Falk patent rights, pre-clinical data and clinical data from Falk’s clinical trials of TSO in CD, including Falk’s ongoing Phase 2 clinical trial, for use in North America, South America and Japan. We granted Falk exclusive rights and licenses to data from our clinical trials of TSO in CD for use in Europe. Under the agreement, we agreed to pay Falk (i) a total of €5 million (approximately $6.5 million) after receipt of certain pre-clinical and clinical data, of which €2.5 million (approximately $3.4 million) was paid in 2012 and the remaining €2.5 million is expected to be paid in the first half of 2014 upon receipt of the Clinical Study Report (“CSR”) and (ii) a royalty of 1% of net sales of TSO in North America, South America and Japan. A steering committee comprised of our representatives and representatives of Falk and Ovamed is overseeing the clinical development program for CD, under which we and Falk will each be responsible for clinical testing on approximately 50% of the total number of patients required for regulatory approval of TSO for CD in the United States and Europe and will share in certain pre-clinical development costs.

In November 2013, we received from Falk a notification that their independent data monitoring committee had conducted an interim analysis (blinded to Falk) of clinical data from approximately 240 patients in Falk’s Phase 2 clinical trial in Europe evaluating TSO in CD. The study was a double-blind, randomized, placebo-controlled, multi-center trial to evaluate the efficacy and safety of three different dosages of oral TSO in patients with active CD. The committee noted no safety concerns but recommended that the study be stopped due to a lack of efficacy. Falk adopted the committee’s recommendations and discontinued the study.

In December 2013, Eric Hollander, clinical Professor of Psychiatry and Behavioral Sciences at Albert Einstein College of Medicine of Yeshiva University and Director of the Autism and Obsessive Compulsive Spectrum Program at Montefiore Medical Center and Einstein, presented interim data from his pilot study of oral TSO (Trichuris suis ova or CNDO-201) to treat autism at the American College of Neuropsychopharmacology Annual Meeting in Hollywood, Florida. The study is a double-blind, randomized, placebo-controlled, cross-over study and enrolled 10 high-functioning adult autism spectrum disorder patients who were able to give informed consent to participate in the study and who had a history of allergies and/or a family history of immune-inflammatory illness. They were treated for 12 weeks with either TSO or placebo, followed by a four-week washout phase and then 12 weeks of placebo or TSO. The TSO dosage used in the study was 2,500 ova once every two weeks. In the first five patients that completed the study, there was a statistically significant separation from placebo in favor of TSO on three measures of disease: the Montefiore-Einstein Rigidity Scale, the Repetitive Behavior Scale-Revised Sameness Scale, and the Social Responsiveness Scale -Repetitive Behaviors Scale. The treatment was well tolerated. The study is still ongoing and final results are expected in the middle of 2014.

There are also additional ongoing or proposed investigator-initiated clinical trials evaluating TSO in various indications, including UC, MS, autism, and psoriasis. We publicly announced the start of two new trials in 2012, one at the New York University School of Medicine (“NYU”), with Drs. Michael Poles, P’ng Loke and Martin Wolff in UC, and the other at Montefiore in New York City, with Dr. Eric Hollander in autism. We also issued a statement about the agreement with the National Institute of Health’s Allergy and Immunology Department, NIAID in UC, with the principal investigator being Dr. Steven Hanauer, Chicago. All three trials are investigator initiated, but we will provide TSO and have worked closely with the investigators to develop protocols and data management tools. We will continue to work with these sites throughout the trials as part of our overall clinical strategy for TSO. In the first quarter of 2013, we announced the start of an open-label trial in psoriasis, and named the first site of three sites, Mt. Sinai School of Medicine. We intend to support certain of these investigator-initiated trials by providing product supply and, in some cases, grants.

| 6 | ||

Our Clinical Trial Program

In February 2012, we announced positive results from our Phase 1 clinical trial of TSO in patients with CD and the full study results were presented in May 2012 by Dr. David Elliott, Professor and Director of the Gastroenterology and Hepatology Division at the University of Iowa, as a poster at the 8th International Congress on Autoimmunity in Granada, Spain. The Phase 1 clinical trial was a multi-center, sequential dose-escalation, double-blind, placebo-controlled study. The primary objective of the study was to evaluate the safety and tolerability of TSO. The trial enrolled 36 patients with CD ranging in age from 20 to 54 with an equal distribution of male and female patients in three single dose cohorts of orally administered 500, 2500 and 7500 ova. Each cohort had twelve patients, with nine patients receiving TSO and three receiving placebo. Primary safety assessments were determined at day 14 post-dose.

Overall, TSO was found to be safe and well tolerated across all three dose levels tested. There were only two adverse events (metallic taste and sour taste) that were considered to be study drug related as assessed by the investigators, one reported in the 7,500 ova dose group and the other in a patient receiving placebo, respectively. All other reported events were assessed as unrelated to study drug and were self-limiting. Mild gastrointestinal side effects such as nausea (in one placebo-treated patient and two TSO-treated patients) and diarrhea and/or abdominal pain (in two TSO-treated patients) were reported. Safety laboratory values were assessed throughout the study and no clinically significant adverse trends were observed and no laboratory- related adverse events were reported. There were no serious adverse events reported and no patient discontinued the study prematurely.

In August 2012, we initiated our TRUST-I trial, a phase 2 clinical trial of TSO designed to evaluate the safety and efficacy of TSO (7500 ova) given once every two weeks for 12 weeks, in approximately 220 patients with CD.

In October 2013, we reported that the TRUST-I study did not meet its primary endpoint of improving response (where response was defined as a 100-point decrease in the CDAI), nor the key secondary endpoint of remission (defined as achieving CDAI < 150 points). In the overall patient population, response rate of patients on TSO did not separate from that of placebo. The lack of overall response was driven by a higher-than-expected placebo response rate. TSO was safe and well-tolerated, and adverse events were balanced between the TSO and the placebo group. The most common adverse event reported was abdominal pain and occurred in 11% of patients in each treatment group.

In December 2013, we announced that we had submitted an IND application to the FDA to begin a Phase 2 clinical study of TSO for the treatment of moderate to severe chronic plaque psoriasis. We also conducted a pre-IND meeting with the FDA regarding TSO for the treatment of autism.

In addition to the studies described above, we may conduct pilot studies and support certain investigator initiated clinical trials of TSO in these and other autoimmune diseases.

Manufacturing

To date, we have contracted with Ovamed to produce and supply us with all of our requirements of TSO. Ovamed’s contractor inoculates young pathogen-free pigs with T. suis from a master ova bank and harvests the ova which are incubated to maturity and are processed to remove any viruses and other pathogens. Ova then are processed and extensively tested to assure uniformity. They are then used to repopulate the master ova bank and are processed further by Ovamed into a final formulation of the drug product that is a clear, tasteless and odorless liquid. Ovamed manufacturing is conducted at one facility in Germany, which has received Good Manufacturing Practice, or GMP, certification by the European Medicines Agency, or EMA. Ovamed’s manufacturing operations are subject to FDA and EMA standards. See “Government Regulation and Product Approval”.

In December 2012, we entered into the Second Amendment amending certain provisions of our exclusive sublicense agreement and our manufacturing and supply agreement and providing for certain additional agreements with Ovamed. Pursuant to the Second Amendment, our exclusive license from Ovamed in the Coronado Territory was amended to include an exclusive license to make and have made product containing TSO for the Coronado Territory and Ovamed’s exclusive supply rights in the Coronado Territory will terminate once we establish an operational manufacturing facility in the United States. The Ovamed License now terminates 15 years from first commercial sale in the United States, subject to earlier termination under certain circumstances.

In exchange, we agreed to pay Ovamed a total of $1,500,000 in three equal installments of $500,000 in each of December 2014, 2015, and 2016. Additionally, in lieu of product supply payments that would have been payable to Ovamed as the exclusive supplier, we will pay Ovamed a manufacturing fee for product manufactured and sold by us. The manufacturing fee will consist of the greater of (i) a royalty on net sales of product manufactured by us or (ii) a specified amount per unit, known as the Transfer Fee Component. The Manufacturing Fee is subject to certain adjustments and credits and we have a right to reduce the Transfer Fee Component by paying Ovamed an agreed amount within ten business days following FDA approval of a Biologics License Application approving the manufacturing, marketing and commercial sale of Product in the United States and an additional amount within ninety days after the end of the first calendar year in which net sales in the Territory exceed an agreed amount.

Simultaneously with the execution of the Second Amendment, Ovamed assigned to us a five-year property lease in Woburn, MA for space in which we initially planned establish a TSO manufacturing facility. Ovamed agreed to assist us in establishing the Woburn facility and the Second Amendment contemplates that we and Ovamed would act as second source suppliers to each other at agreed transfer prices pursuant to a Second Source Agreement to be negotiated between us. In 2013, we substantially completed the build out of the office area in the Woburn facility. However, based upon TRUST-I results in October 2013, we are currently evaluating our TSO manufacturing plans. It will take approximately one year to complete the manufacturing site and will require an incremental investment from Coronado. Once complete, the Woburn facility will be required to meet GMP standards and will be subject to FDA and other regulatory authorities’ inspections, which could take approximately 12 months from the decision to proceed.

| 7 | ||

CNDO-109

CNDO-109 is a lysate (disrupted CTV-1 cells, cell membrane fragments, cell proteins and other cellular components) that activates donor Natural Killer (NK) cells. CTV-1 is a leukemic cell line re-classified as a T-cell acute lymphocytic leukemia, or ALL. We acquired exclusive worldwide rights to develop and commercialize CNDO-109 activated NK cells for the treatment of cancer from UCLB.

Background

Standard therapy for patients with advanced cancer include chemotherapy, or therapies that are toxic to the cells, that suppress the immune system and carry significant risks of life-threatening infections and other toxicities in the absence of hope for cure. Despite effective cancer therapies that induce clinical responses, including complete remissions, minimal residual disease, or MRD, a term referring to disease that is undetectable by conventional morphologic methods, often remains and serves as a source of cancer recurrence. For years, scientists have studied ways to enhance the patient’s immune system to target cancer cells, maintain remission and possibly even eradicate all cancer cells in the body, including MRD. Researchers believe that a cure for cancer might be possible if immunotherapy is successfully applied to the treatment of cancer.

The most common immunotherapy studied to date involves the use of targeted humanized monoclonal antibodies such as rituximab (anti-CD20) or trastuzumab (anti-HER2/neu). These antibodies bind targets that are over-expressed on cancer cells and promote cell death by a number of immune mechanisms, including antibody dependent cell-mediated cytotoxicity, or ADCC. In ADCC, the most common mechanism of tumor killing, the antibody tags the cancer cell and recruits the cells from the patient’s immune system to attack the tumor. Immune cells recruited by the antibody to kill the cancer include granulocytes, macrophages and NK cells.

Another common therapy that activates the innate immune system involves the administration of high dose Interleukin-2, or IL-2. Through binding to the IL-2 receptor, IL-2 activates NK cells to attack cancer cells. After high-dose IL-2 therapy, NK cells are activated to search out and kill cancer cells. Unfortunately, the use of IL-2 therapy is limited because of its severe side effects, which include severe life-threatening infusion reactions and induction of autoimmune disease.

The importance of NK cells in the host system’s defense against cancer was recognized by Dr. Mark Lowdell at the Royal Free Hospital in London and others when they noted that patients who could mount an immune response to their AML became long-term survivors after chemotherapy. Researchers identified that a key to the successful immune response of the patient’s immune systems was the NK cell. Dr. Lowdell determined that activated NK cells were the key to eliminating AML cells and that NK cells require two signals to kill a tumor cell—a priming signal followed by a trigger signal. NK cells that can be activated by certain cancer cells provide both signals resulting in killing the cancer cell. Cancer cells that cannot be killed only trigger one signal and therefore are considered resistant to NK cells. NK cells which have not been primed cannot respond to the trigger. The “priming signal” can be provided by either cytokines, such as high dose IL-2 or IL-15 or by CNDO-109. In contrast to IL-2 or IL-15, NK cells activated by CNDO-109 retain their activated state after freezing and thawing. This allows commercialization of the process since the NK cells can be activated with CNDO-109 and prepared at a central manufacturing facility under GMP conditions and shipped to the clinical center as a frozen patient-specific dose, ready for infusion. The results of the research conducted by Dr. Lowdell and his colleagues were published in the British Journal of Haematology in 2002 and The Journal of Immunology in 2007 and all inventions and related intellectual property that arose from such research are covered by our license agreement with UCL Business PLC, or UCLB. Dr. Lowdell is a consultant to us.

Although AML is the prototype tumor lysed by CNDO-109 activated NK cells, CNDO-109 activated NK cells are expected to be active against many cancer types. Based on in vitro preclinical efficacy studies of CNDO-109 conducted by Dr. Lowdell at the Royal Free Hospital in London using human specimens of breast cancer, prostate and ovarian cancer, we expect CNDO-109 to be active against tumors that have been successfully treated by high dose IL-2 therapy such as renal cell carcinoma and melanoma.

The treatment of patients with CNDO-109 activated NK cells involves several steps. The activated NK cells are infused into the patient after resting NK cells are incubated with CNDO-109 for at least four hours. Preparation of CNDO-109 activated NK cells takes about 24 hours from start to finish. If the source of the NK cells being used is someone other than the patient, “an allogeneic donor,” the patient will need some form of immunosuppression to allow the CNDO-109 activated NK cells to persist long enough to eradicate MRD. Preliminary data on a small number of patients from the UK Phase 1 clinical trial demonstrated that CNDO-109 activated NK cells can remain active for weeks.

| 8 | ||

Completed Clinical Trial

An investigator-initiated Phase 1 clinical trial of CNDO-109 activated haploidentical NK cells was conducted at the Royal Free Hospital in London in eight patients with high risk (i.e. chemo-sensitive relapsed/refractory) AML who were not eligible for a stem cell transplant. The results of this trial were presented at the ASH Annual Meeting in December 2011. Although the primary endpoint of the Phase 1 clinical trial was safety, the results demonstrated that the majority of AML patients experienced a longer complete remission after receiving CNDO-109 activated NK cells than their previous complete remission. This finding is notable since the duration of each successive complete remission is generally shorter than the last.

Our Clinical Program

We submitted an IND for the CNDO-109 activated NK cell product in the United States in February 2012 using data from UCLB’s Phase 1 clinical trial in the United Kingdom. We initiated a Phase 1/2 clinical trial in the United States in November 2012 using CNDO-109 to activate NK cells to treat AML patients in first complete remission (CR1) who are deemed a high risk to relapse. In Phase 1/2 oncology clinical trials, dose limiting toxicity stopping rules are commonly applied. The CNDO-109 Phase 1/2 trial is subject to a set of dose-limiting toxicities, or DLTs, that could suspend or stop dose escalation by predetermined criteria, including allergic reactions, prolonged aplasia or other organ toxicities of a serious nature. In 2013, we enrolled three patients in the Phase 1/2 trial, which is on going. To date, no DLTs have been observed. We are also considering participation in a Phase 1/2 multiple myeloma trial using autologous NK cells, which we believe may initiate in 2014 and selected pilot Phase 1 clinical trials in other tumor types, including breast, prostate and ovarian cancer, with both allogeneic and autologous cells.

Manufacturing

The manufacturing process for CNDO-109 activated NK cells is currently under development. We have produced a master cell bank and a working cell bank of CTV-1 cells in collaboration with BioReliance Corp. Manufacture and testing of CNDO-109 activated NK cells for our ongoing Phase 1/2 clinical trial is being conducted by Progenitor Cell Therapy, LLC or PCT. We have entered into master service agreements with both companies as well as a supply agreement with PCT. The master service agreements provide the general framework for the relationships, with specific terms to be established in connection with particular projects. Indirectly, we also rely on Miltenyi Biotec GmbH to provide the equipment and reagents necessary for the identification and selection of NK cells.

Strategic Alliances and Commercial Agreements

TSO

Sublicense Agreement with Ovamed GmbH

In January 2011, in connection with our acquisition of the assets of Asphelia Pharmaceuticals, Inc. (“Asphelia”) relating to TSO, Asphelia assigned the Exclusive Sublicense Agreement, dated December 2005, between Asphelia and Ovamed, as amended, and the Ovamed License and Manufacturing and Supply Agreement, dated March 2006, between Asphelia and Ovamed, as amended, otherwise known as the Ovamed Supply Agreement, to us and we assumed Asphelia’s obligations under these agreements. Under the Ovamed License, we received an exclusive sublicense, with a right to grant additional sublicenses to third parties, under Ovamed’s patent rights and know-how to use and sell products encompassing TSO in North America, South America and Japan. Ovamed’s patent rights arise, in turn, from an exclusive license granted in 2005 by the University of Iowa Research Foundation, or UIRF, to Ovamed covering inventions and related intellectual property rights that arose as a result of research relating to TSO performed by Dr. Weinstock and his colleagues while employed by the University of Iowa. In November 2011, we entered into an agreement with UIRF and Ovamed primarily amending certain diligence provisions of the UIRF license agreement with Ovamed and obtaining certain rights in the event of an Ovamed breach of this license.

Under the Ovamed License, we are required to make milestone payments to Ovamed totaling up to approximately $5.45 million, of which $3.0 million has been paid, primarily upon the achievement of various regulatory milestones for the first product that incorporates TSO, and additional milestone payments upon the achievement of regulatory milestones relating to subsequent indications. In the event that TSO is commercialized, we are obligated to pay to Ovamed royalties equal to 4% of net sales. Additionally, we are obligated to pay to Ovamed a percentage of certain consideration we receive from sublicensees (ranging from 10% to 20% of such consideration depending on the stage of clinical development at the time of the sublicense), as well as an annual license maintenance fee of $250,000 and reimbursement of patent costs. We are responsible for all clinical development and regulatory activities and costs relating to licensed products in North America, South America and Japan. Either party may also terminate the agreement under certain customary conditions of breach and we have the right to terminate the Ovamed License with 30 days prior notice.

In January 2011, as part of the purchase price for the Asphelia assets, we paid Ovamed an aggregate of approximately $3.4 million in satisfaction of Asphelia’s agreement to pay Ovamed for certain development costs, the annual license maintenance fee and patent reimbursement costs.

Under the Ovamed Supply Agreement, Ovamed agreed to manufacture and supply us with and we are required to purchase from Ovamed our clinical and commercial requirements of TSO at pre-determined prices. The Ovamed Supply Agreement currently expires in March 2014 but will automatically renew for successive one-year periods, unless we give 12 months’ prior notice of our election not to renew. The Ovamed Supply Agreement is subject to early termination by either party under certain customary conditions of breach and by us in the event of specified failures to supply or regulatory or safety failures.

| 9 | ||

In December 2012, we entered into the Second Amendment amending certain provisions of our exclusive sublicense agreement and our manufacturing and supply agreement and providing for certain additional agreements with Ovamed. Pursuant to the Second Amendment, our exclusive license from Ovamed in the Coronado Territory was amended to include an exclusive license to make and have made product containing TSO for the Coronado Territory and Ovamed’s exclusive supply rights in the Coronado Territory will terminate once we establish an operational manufacturing facility in the United States. The Ovamed License now terminates 15 years from first commercial sale in the United States, subject to earlier termination under certain circumstances.

As part of the Second Amendment, we agreed to pay Ovamed a total of $1,500,000 in three equal installments of $500,000 in each of December 2014, 2015, and 2016. Additionally, in lieu of product supply payments that would have been payable to Ovamed as the exclusive supplier, we will pay Ovamed a manufacturing fee for product manufactured and sold by us. The manufacturing fee will consist of the greater of (i) a royalty on net sales of product manufactured by us or (ii) a specified amount per unit (the “Transfer Fee Component”). The Manufacturing Fee is subject to certain adjustments and credits and we have a right to reduce the Transfer Fee Component by paying Ovamed an agreed amount within ten business days following FDA approval of a Biologics License Application approving the manufacturing, marketing and commercial sale of Product in the United States and an additional amount within ninety days after the end of the first calendar year in which net sales in the Territory exceed an agreed amount.

Simultaneously with the execution of the Second Amendment, Ovamed assigned to us a five-year property lease in Woburn, MA for space in which we initially planned to establish a TSO manufacturing facility. Ovamed agreed to assist us in establishing the Woburn facility and the Second Amendment contemplates that we and Ovamed would act as second source suppliers to each other at agreed transfer prices pursuant to a Second Source Agreement to be negotiated between us. In 2013, we substantially completed the build out of the office area in the Woburn facility. However, based upon TRUST-I results in October 2013, we are currently evaluating our TSO manufacturing plans. It will take approximately one year to complete the manufacturing site and will require an incremental investment from Coronado. Once complete, the Woburn facility will be required to meet GMP standards and will be subject to FDA and other regulatory authorities’ inspections, which could take approximately 12 months from the decision to proceed.

Collaboration Agreement with Ovamed and Falk

In December 2011, we entered into a binding Terms of Agreement with Falk and Ovamed under which we agreed to enter into collaboration agreement relating to the development of TSO for CD. In March 2012, the parties entered into the Collaboration Agreement, under which Falk granted us exclusive rights and licenses under certain Falk patent rights, pre-clinical data, and clinical data from Falk’s clinical trials of TSO in CD, including the ongoing Falk Phase 2 clinical trial, for use in North America, South America and Japan. In exchange, we granted Falk exclusive rights and licenses to our pre-clinical data and data from clinical trials of TSO in CD for use in Europe.

In addition, we agreed to pay Falk a total of €5 million after receipt of certain preclinical and clinical data, half of was paid in 2012 and half of which is expected to be paid in 2014, and contingent upon Falk delivering the Final Clinical Study Report, or CSR, and a royalty equal to 1% of net sales of TSO in North America, South America and Japan.

Under the Collaboration Agreement, a Steering Committee comprised of our representatives and representatives of Falk and Ovamed will oversee the TSO development program for CD, under which we and Falk will each be responsible for clinical testing on approximately 50% of the total number of patients required for regulatory approval of TSO for CD in the United States and Europe and will share in certain pre-clinical development costs. Due to TRUST-I results in mid-October 2013, the Steering Committee agreed to postpone pre-clinical development activities until the evaluation of TRUST-II results in the second quarter of 2014.

The Collaboration Agreement may be terminated by either Falk or us under certain conditions including if the other party fails to cure a material breach under the agreement, subject to prior notice and the opportunity to cure, if the other party is subject to bankruptcy proceedings or if the terminating party terminates all development of TSO.

Research Agreement with FU Berlin

On February 22, 2013, the Company and Freie Universität Berlin, or FU Berlin, entered into a Research Agreement to, among other things, identify and evaluate secretory proteins from Trichuris suis, which we refer to as the Project. The duration of the Project is expected to be four years, during which the Company will pay FU Berlin a total maximum amount of approximately €648,000, or approximately $853,000, in research fees and FU Berlin will periodically produce written progress reports on the Project. The Research Agreement terminates on the later of the date that the last payment or report is due, subject to early termination by either party upon three months written notice for cause or without cause. If the Company terminates the Research Agreement, the Company must pay FU Berlin a termination fee comprised primarily of unpaid research fees due on the first payment date after which termination occurred (subject to adjustment), except where termination is due to a breach by FU Berlin which it fails to cure within 60 days notice or due to FU Berlin’s bankruptcy.

| 10 | ||

On February 22, 2013, the Company and FU Berlin also entered into a Joint Ownership and Exclusive License Agreement or JOELA, pursuant to which the Company agreed to jointly own all intellectual property arising from the Project, which we refer to as the Joint Intellectual Property. FU Berlin also granted the Company (a) an exclusive worldwide license (including the right to sublicense) to its interest in the Joint Intellectual Property and its know-how related to the Project, which we refer to as the Licensed IP, and (b) the right to commercialize products that, without the licenses granted under the JOELA, would infringe the Licensed IP. FU Berlin retains the non-exclusive and non-transferable right to use the Licensed IP for its own internal, academic purposes. Pursuant to the JOELA, the Company must pay FU Berlin a total maximum amount of approximately €3,830,000, or approximately $4,982,000, in potential milestone payments, based primarily on the achievement of clinical development and regulatory milestones, and royalties on potential net sales of products ranging from 1% to 2.5%. The JOELA continues until the last-to-expire patent in any country, subject to early termination by either party without penalty if the other party breaches the JOELA and the breach is not cured within 60 days after receiving notice of the breach or if a party is in bankruptcy. The Company also has the right to terminate the JOELA after giving FU Berlin 60 days written notice of a regulatory action that affects the safety, efficacy or marketability of the Licensed Products or if the Company cannot obtain sufficient materials to conduct trials, or upon 180 days written notice for any reason.

In connection with the Research Agreement and JOELA, the Company entered into a License and Sublicense Agreement, or LSA, with Ovamed, on February 22, 2013, pursuant to which the Company licensed is rights to the Joint Intellectual Property and sublicensed its rights to the Licensed IP to Ovamed in all countries outside North America, South America and Japan, which we refer to as the Ovamed Territory. Pursuant to the LSA, Ovamed would pay the Company a total maximum amount of approximately €1,025,000, or approximately $1,333,000 based primarily on the achievement of regulatory milestones, and royalties on potential net sales of products ranging from 1% to 2.5%, subject to adjustment, in each case equal to the comparable payments due under the JOELA. The LSA continues until the last-to-expire patent in any country in the Ovamed Territory, subject to early termination by either party upon the same terms as in the JOELA.

On February 22, 2013, Coronado, Ovamed and FU Berlin entered into a Letter Agreement to amend a Material Transfer Agreement dated May 14, 2012 by and between Ovamed and FU Berlin. The Letter Agreement provides that Ovamed will retain a 10% interest in FU Berlin’s rights to the Joint Intellectual Property in the Ovamed Territory. It also grants Ovamed certain rights if FU Berlin terminates the JOELA due to the Company’s breach, including the right to have the JOELA survive and the Company’s rights and obligations thereunder assigned to Ovamed.

In 2013, the Company made two payments totaling approximately $183,000 to FU Berlin in accordance with the term of the Research Agreement.

License Agreement with UCLB

In November 2007, we entered into a license agreement with UCLB under which we received an exclusive, worldwide license to develop and commercialize CNDO-109 to activate NK cells for the treatment of cancer and related conditions. Pursuant to a September 2009 amendment, we also received a non-exclusive license, without the right to sublicense, to certain clinical data solely for use in the IND for CNDO-109. Under a May 2012 amendment, additional patent rights and rights to certain additional inventions were added to the license agreement.

In consideration for the license, we will be required to make future milestone payments totaling up to approximately $22 million contingent upon the achievement of various milestones related to regulatory events for the first three indications for which CNDO-109 is developed. In March 2012, we recognized our obligation to pay UCLB a $250,000 milestone related to the filing of an IND for CNDO-109. In the event that CNDO-109 is commercialized, we will be obligated to pay to UCLB royalties ranging from 3% to 5% of net sales of the product or, if commercialized by a sublicensee, a percentage of certain consideration we receive from such sublicensee (ranging from 20% to 30% of such consideration depending on the stage of clinical development at the time of the sublicense). Under the terms of the agreement, we must use diligent and reasonable efforts to develop and commercialize CNDO-109 activated NK cells worldwide and may grant sublicenses to third parties without the prior approval of UCLB. In September 2012, the U.S. Patent and Trade Office granted the first U.S. patent directed to CNDO-109. Foreign counterparts to this patent claim have been granted in India and Australia. In June 2012, we were notified by the FDA that CNDO-109 was granted orphan drug designation. In February 2014, a second key patent directed to compositions comprising these activated NK cells was granted. We have exclusive worldwide rights to develop and market CNDO-109 under a license agreement with the University College London Business PLC, or UCLB

We have entered into consulting agreements with Dr. Mark Lowdell and UCL Consultants Limited (a wholly- owned subsidiary of UCLB) that provide for Dr. Lowdell to provide various services to us relating to our CNDO-109 program.

| 11 | ||

Services Agreement with PCT

In April 2010 and as amended in September 2012, we entered into a Master Contract Services Agreement with Progenitor Cell Therapy (“PCT”) pursuant to which PCT may provide consulting, preclinical, laboratory and/or clinical research-related services, product/process development services, manufacturing services and other services to us in connection with the CNDO-109 development program. PCT is currently performing services related to the manufacturing of CNDO-109. We pay for services under the agreement pursuant to statements of work entered into from time to time. Any product resulting from the services performed or product improvement, inventions or discoveries, including new uses for product resulting from the services performed and related patent rights which arise as a result of the services performed by PCT under the agreement are owned solely and exclusively by and assigned to us. Through December 31, 2013, we have entered into statements of work with PCT aggregating $2.7 million.

In February 2013, we entered into a Master Contract Services Agreement with WuXi AppTec, pursuant to which WuXi AppTec will provide product development, manufacturing and testing services related to CNDO-109. We pay for services under the agreement pursuant to statements of work entered into from time to time. Through December 31, 2013, we have entered into statements of work with WuXi AppTec aggregating $0.9 million.

Intellectual Property

General

Our goal is to obtain, maintain and enforce patent protection for our product candidates, formulations, processes, methods and any other proprietary technologies, preserve our trade secrets, and operate without infringing on the proprietary rights of other parties, both in the United States and in other countries. Our policy is to actively seek to obtain, where appropriate, the broadest intellectual property protection possible for our current product candidates and any future product candidates, proprietary information and proprietary technology through a combination of contractual arrangements and patents, both in the United States and abroad. However, patent protection may not afford us with complete protection against competitors who seek to circumvent our patents.

We also depend upon the skills, knowledge, experience and know-how of our management and research and development personnel, as well as that of our advisors, consultants and other contractors. To help protect our proprietary know-how, which is not patentable, and for inventions for which patents may be difficult to enforce, we currently rely and will in the future rely on trade secret protection and confidentiality agreements to protect our interests. To this end, we require all of our employees, consultants, advisors and other contractors to enter into confidentiality agreements that prohibit the disclosure of confidential information and, where applicable, require disclosure and assignment to us of the ideas, developments, discoveries and inventions important to our business.

TSO

Under the Ovamed License, we have exclusive rights to United States Patent Nos. 6,764,838, 7,250,173 and 7,833,537, owned by the University of Iowa and licensed by UIRF to Ovamed. These patents claim, respectively, methods of producing a pharmaceutical composition comprising an helminthic parasite preparation, pharmaceutical compositions suitable for oral administration comprising an isolated and purified T. suis helminthic parasite preparation, and methods of treating inflammatory bowel disease, including CD and UC, in an individual by the administration of a helminthic parasite preparation obtained from a group of helminthic parasites. These patents are scheduled to expire in December 2018, except for the ‘537 patent, which is set to expire approximately nine months later. Under the patent term restoration provisions of the patent laws, we may choose to restore a portion of the term of one of these patents, or any other relevant patents that may be granted prior to marketing approval of TSO, to recover at least a portion of the delays associated with obtaining regulatory approval. We also have exclusive rights through the Ovamed License under a second patent family owned by UIRF, which is directed to methods of using helminthic parasite preparations to treat patients with a Th1 or Th2 related autoimmune disease. Any patents that mature from this second patent family would not expire until at least November 2023.

Under the Collaboration Agreement, we have an exclusive license in North America and Japan to Falk’s interest in two patent families: one directed to a process for the preparation of the pharmaceutical product comprised of viable eggs of parasitic helminths and another directed to a method of determining biological activity of embryonated Trichuris eggs. Applications for patents are pending in the United States, Canada and Japan for both patent families.

Our success for preserving market exclusivity for our product candidates relies on our ability to obtain and maintain a regulatory period of data exclusivity over an approved biologic, currently 12 years from the date of marketing approval, and to preserve effective patent coverage. Once any regulatory period of data exclusivity expires, depending on the status of our patent coverage, we may not be able to prevent others from marketing and selling products that are biosimilar to or interchangeable with our product candidates. We are also dependent upon the diligence of third parties, which control the prosecution of pending domestic and foreign patent applications and maintain granted domestic and foreign patents.

In addition to any regulatory exclusivity we may be able to obtain, we also seek to protect additional intellectual property rights such as trade secrets and know-how, including commercial manufacturing processes and proprietary business practices.

| 12 | ||

CNDO-109

We have exclusive rights to International Patent Application No. PCT/GB2006/000960 and all pending United States and foreign counterpart applications including granted U.S. Patents No. 8,257,970 and 8,637,308 and the corresponding national phase applications granted in Australia and India and filed in Canada, Europe and Japan, directed to the stimulation of natural killer cells and related CNDO-109 compositions and methods including methods for the treatment of cancer and other conditions. This patent family has been in-licensed on an exclusive basis from UCLB. This CNDO-109 patent has an expiration date of January 2029 in the absence of any patent term extension.