000142820512/312024Q1FALSE0.20.08330.200014282052024-01-012024-03-310001428205us-gaap:SeriesCPreferredStockMember2024-01-012024-03-310001428205us-gaap:CommonStockMember2024-01-012024-03-3100014282052024-04-24xbrli:shares00014282052024-03-31iso4217:USD00014282052023-12-310001428205us-gaap:AgencySecuritiesMember2024-03-310001428205us-gaap:RelatedPartyMemberus-gaap:AgencySecuritiesMemberarr:BUCKLERSecuritiesLLCMember2024-03-310001428205us-gaap:AgencySecuritiesMember2023-12-310001428205us-gaap:RelatedPartyMemberus-gaap:AgencySecuritiesMemberarr:BUCKLERSecuritiesLLCMember2023-12-310001428205us-gaap:RelatedPartyMemberarr:BUCKLERSecuritiesLLCMember2024-03-310001428205us-gaap:RelatedPartyMemberarr:BUCKLERSecuritiesLLCMember2023-12-31iso4217:USDxbrli:sharesxbrli:pure0001428205us-gaap:SeriesCPreferredStockMember2023-01-012023-12-310001428205us-gaap:SeriesCPreferredStockMember2023-12-310001428205us-gaap:SeriesCPreferredStockMember2024-03-310001428205us-gaap:RelatedPartyMemberarr:BUCKLERSecuritiesLLCMember2024-01-012024-03-310001428205us-gaap:RelatedPartyMemberarr:BUCKLERSecuritiesLLCMember2023-01-012023-03-3100014282052023-01-012023-03-310001428205us-gaap:AgencySecuritiesMember2024-01-012024-03-310001428205us-gaap:AgencySecuritiesMember2023-01-012023-03-310001428205us-gaap:USTreasurySecuritiesMember2024-01-012024-03-310001428205us-gaap:USTreasurySecuritiesMember2023-01-012023-03-310001428205us-gaap:PreferredStockMember2022-12-310001428205us-gaap:CommonStockMember2022-12-310001428205us-gaap:AdditionalPaidInCapitalMember2022-12-310001428205us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2022-12-310001428205us-gaap:RetainedEarningsMember2022-12-310001428205us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-3100014282052022-12-310001428205us-gaap:RetainedEarningsMember2023-01-012023-03-310001428205us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-03-310001428205us-gaap:CommonStockMember2023-01-012023-03-310001428205us-gaap:AdditionalPaidInCapitalMember2023-01-012023-03-310001428205us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2023-01-012023-03-310001428205us-gaap:PreferredStockMember2023-03-310001428205us-gaap:CommonStockMember2023-03-310001428205us-gaap:AdditionalPaidInCapitalMember2023-03-310001428205us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2023-03-310001428205us-gaap:RetainedEarningsMember2023-03-310001428205us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-03-3100014282052023-03-310001428205us-gaap:PreferredStockMember2023-12-310001428205us-gaap:CommonStockMember2023-12-310001428205us-gaap:AdditionalPaidInCapitalMember2023-12-310001428205us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2023-12-310001428205us-gaap:RetainedEarningsMember2023-12-310001428205us-gaap:RetainedEarningsMember2024-01-012024-03-310001428205us-gaap:CommonStockMember2024-01-012024-03-310001428205us-gaap:AdditionalPaidInCapitalMember2024-01-012024-03-310001428205us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2024-01-012024-03-310001428205us-gaap:PreferredStockMember2024-03-310001428205us-gaap:CommonStockMember2024-03-310001428205us-gaap:AdditionalPaidInCapitalMember2024-03-310001428205us-gaap:AccumulatedDistributionsInExcessOfNetIncomeMember2024-03-310001428205us-gaap:RetainedEarningsMember2024-03-310001428205us-gaap:AccumulatedOtherComprehensiveIncomeMember2024-03-310001428205us-gaap:RelatedPartyMemberarr:BUCKLERSecuritiesLLCMemberus-gaap:USTreasurySecuritiesMember2024-01-012024-03-310001428205us-gaap:RelatedPartyMemberarr:BUCKLERSecuritiesLLCMemberus-gaap:USTreasurySecuritiesMember2023-01-012023-03-310001428205us-gaap:RelatedPartyMemberarr:BUCKLERSecuritiesLLCMember2024-03-3100014282052023-09-292023-09-290001428205us-gaap:RepurchaseAgreementsMember2024-03-310001428205us-gaap:RepurchaseAgreementsMemberarr:BUCKLERSecuritiesLLCMember2024-03-310001428205us-gaap:RepurchaseAgreementsMemberarr:BUCKLERSecuritiesLLCMember2023-12-31arr:dealer0001428205us-gaap:FairValueMeasurementsRecurringMemberus-gaap:AgencySecuritiesMemberus-gaap:FairValueInputsLevel1Member2024-03-310001428205us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:AgencySecuritiesMember2024-03-310001428205us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:AgencySecuritiesMember2024-03-310001428205us-gaap:FairValueMeasurementsRecurringMemberus-gaap:AgencySecuritiesMember2024-03-310001428205us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2024-03-310001428205us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2024-03-310001428205us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2024-03-310001428205us-gaap:FairValueMeasurementsRecurringMember2024-03-310001428205us-gaap:FairValueMeasurementsRecurringMemberus-gaap:AgencySecuritiesMemberus-gaap:FairValueInputsLevel1Member2023-12-310001428205us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:AgencySecuritiesMember2023-12-310001428205us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:AgencySecuritiesMember2023-12-310001428205us-gaap:FairValueMeasurementsRecurringMemberus-gaap:AgencySecuritiesMember2023-12-310001428205us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2023-12-310001428205us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001428205us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001428205us-gaap:FairValueMeasurementsRecurringMember2023-12-310001428205arr:TBAAgencySecuritiesMember2024-03-310001428205arr:TBAAgencySecuritiesMember2023-12-310001428205arr:TobeAnnouncedAgencySecuritiesMember2024-03-310001428205arr:TobeAnnouncedAgencySecuritiesMember2023-12-31arr:counterparty0001428205us-gaap:MaturityUpTo30DaysMemberus-gaap:MortgageBackedSecuritiesIssuedByUSGovernmentSponsoredEnterprisesMember2024-03-310001428205us-gaap:MaturityUpTo30DaysMemberus-gaap:MortgageBackedSecuritiesIssuedByUSGovernmentSponsoredEnterprisesMember2024-01-012024-03-310001428205us-gaap:MortgageBackedSecuritiesIssuedByUSGovernmentSponsoredEnterprisesMemberarr:Maturity31To90DaysMember2024-03-310001428205us-gaap:MortgageBackedSecuritiesIssuedByUSGovernmentSponsoredEnterprisesMemberarr:Maturity31To90DaysMember2024-01-012024-03-310001428205us-gaap:MortgageBackedSecuritiesIssuedByUSGovernmentSponsoredEnterprisesMember2024-03-310001428205us-gaap:MortgageBackedSecuritiesIssuedByUSGovernmentSponsoredEnterprisesMember2024-01-012024-03-310001428205us-gaap:MaturityUpTo30DaysMemberus-gaap:MortgageBackedSecuritiesIssuedByUSGovernmentSponsoredEnterprisesMember2023-12-310001428205us-gaap:MaturityUpTo30DaysMemberus-gaap:MortgageBackedSecuritiesIssuedByUSGovernmentSponsoredEnterprisesMember2023-01-012023-06-3000014282052023-01-012023-06-300001428205us-gaap:RepurchaseAgreementsMember2023-12-310001428205us-gaap:BorrowingsMemberarr:BUCKLERSecuritiesLLCMemberarr:CounterpartyConcentrationRiskMember2024-01-012024-03-310001428205us-gaap:BorrowingsMemberarr:BUCKLERSecuritiesLLCMemberarr:CounterpartyConcentrationRiskMember2023-01-012023-12-310001428205arr:BUCKLERSecuritiesLLCMemberus-gaap:StockholdersEquityTotalMemberarr:CounterpartyConcentrationRiskMember2024-01-012024-03-310001428205arr:BUCKLERSecuritiesLLCMemberus-gaap:StockholdersEquityTotalMemberarr:CounterpartyConcentrationRiskMember2023-01-012023-12-310001428205us-gaap:BorrowingsMemberarr:CounterpartyConcentrationRiskMember2024-03-310001428205us-gaap:BorrowingsMemberarr:ThreeRepurchaseAgreementCounterpartiesMemberarr:CounterpartyConcentrationRiskMember2024-01-012024-03-310001428205arr:RepurchaseAgreementBorrowingsMemberarr:ThreeRepurchaseAgreementCounterpartiesMemberarr:CounterpartyConcentrationRiskMember2024-01-012024-03-310001428205us-gaap:BorrowingsMemberarr:CounterpartyConcentrationRiskMember2023-12-310001428205us-gaap:BorrowingsMemberarr:ThreeRepurchaseAgreementCounterpartiesMemberarr:CounterpartyConcentrationRiskMember2023-01-012023-12-310001428205arr:RepurchaseAgreementBorrowingsMemberarr:ThreeRepurchaseAgreementCounterpartiesMemberarr:CounterpartyConcentrationRiskMember2023-01-012023-12-310001428205us-gaap:InterestRateSwapMember2024-03-310001428205us-gaap:InterestRateSwapMember2023-12-310001428205us-gaap:InterestRateSwapMember2024-01-012024-03-310001428205us-gaap:InterestRateSwapMember2023-01-012023-03-310001428205us-gaap:EurodollarFutureMember2024-01-012024-03-310001428205us-gaap:EurodollarFutureMember2023-01-012023-03-310001428205arr:TobeAnnouncedAgencySecuritiesMember2024-01-012024-03-310001428205arr:TobeAnnouncedAgencySecuritiesMember2023-01-012023-03-310001428205arr:InterestRateSwapLessThan3YearsMember2024-03-310001428205arr:InterestRateSwapLessThan3YearsMember2024-01-012024-03-310001428205arr:InterestRateSwapBetween3and5YearsMembersrt:MinimumMember2024-03-310001428205arr:InterestRateSwapBetween3and5YearsMembersrt:MaximumMember2024-03-310001428205arr:InterestRateSwapBetween3and5YearsMember2024-03-310001428205arr:InterestRateSwapBetween3and5YearsMember2024-01-012024-03-310001428205arr:InterestRateSwapBetween5and7YearsMembersrt:MinimumMember2024-03-310001428205arr:InterestRateSwapBetween5and7YearsMembersrt:MaximumMember2024-03-310001428205arr:InterestRateSwapBetween5and7YearsMember2024-03-310001428205arr:InterestRateSwapBetween5and7YearsMember2024-01-012024-03-310001428205arr:InterestRateSwapGreaterThanOrEqualTo7YearsMember2024-03-310001428205arr:InterestRateSwapGreaterThanOrEqualTo7YearsMember2024-01-012024-03-310001428205arr:InterestRateSwapLessThan3YearsMember2023-12-310001428205arr:InterestRateSwapLessThan3YearsMember2023-01-012023-12-310001428205arr:InterestRateSwapBetween3and5YearsMembersrt:MinimumMember2023-12-310001428205arr:InterestRateSwapBetween3and5YearsMembersrt:MaximumMember2023-12-310001428205arr:InterestRateSwapBetween3and5YearsMember2023-12-310001428205arr:InterestRateSwapBetween3and5YearsMember2023-01-012023-12-310001428205arr:InterestRateSwapBetween5and7YearsMembersrt:MinimumMember2023-12-310001428205arr:InterestRateSwapBetween5and7YearsMembersrt:MaximumMember2023-12-310001428205arr:InterestRateSwapBetween5and7YearsMember2023-12-310001428205arr:InterestRateSwapBetween5and7YearsMember2023-01-012023-12-310001428205arr:InterestRateSwapGreaterThanOrEqualTo7YearsMember2023-12-310001428205arr:InterestRateSwapGreaterThanOrEqualTo7YearsMember2023-01-012023-12-3100014282052023-01-012023-12-310001428205arr:SecuredOvernightFinancingRateSOFRMember2024-03-310001428205us-gaap:FederalFundsEffectiveSwapRateMember2024-03-310001428205us-gaap:InterestRateSwapMember2024-03-310001428205arr:SecuredOvernightFinancingRateSOFRMember2023-12-310001428205us-gaap:FederalFundsEffectiveSwapRateMember2023-12-310001428205us-gaap:InterestRateSwapMember2023-12-310001428205arr:TBAAgencySecurities30Year6.0Member2023-12-310001428205arr:TBAAgencySecuritiesMember2023-12-310001428205us-gaap:LimitedLiabilityCompanyMember2024-03-310001428205srt:AffiliatedEntityMemberarr:FeeWaiverAdjustmentEveryMonthThereafterMember2023-02-142023-02-140001428205arr:TransactionsCaseMember2024-01-012024-03-31arr:lawsuit0001428205arr:TransactionsCaseMember2016-04-242016-04-24arr:defendant0001428205arr:TransactionsCaseMember2016-04-252016-04-250001428205arr:The2009StockIncentivePlanMember2024-03-310001428205arr:The2009StockIncentivePlanMemberus-gaap:RestrictedStockUnitsRSUMember2023-12-310001428205arr:The2009StockIncentivePlanMemberus-gaap:RestrictedStockUnitsRSUMember2024-01-012024-03-310001428205arr:The2009StockIncentivePlanMemberus-gaap:RestrictedStockUnitsRSUMember2024-03-310001428205arr:BoardofDirectorsMember2024-01-012024-03-310001428205us-gaap:PreferredStockMember2024-03-310001428205us-gaap:PreferredStockMember2023-12-310001428205us-gaap:CommonStockMember2024-03-310001428205us-gaap:CommonStockMember2023-12-310001428205arr:PreferredCATMSalesAgreementMemberus-gaap:SeriesCPreferredStockMember2020-01-290001428205arr:PreferredCATMSalesAgreementMemberus-gaap:SeriesCPreferredStockMember2024-03-310001428205arr:PreferredCATMSalesAgreementMemberus-gaap:SeriesCPreferredStockMember2023-12-3100014282052022-07-260001428205arr:A2021CommonStockATMSalesAgreementMember2021-05-142021-05-140001428205arr:A2021CommonStockATMSalesAgreementMember2021-05-140001428205arr:A2021CommonStockATMSalesAgreementMember2021-11-122021-11-120001428205arr:A2021CommonStockATMSalesAgreementMember2022-06-092022-06-090001428205arr:A2021CommonStockATMSalesAgreementMember2022-11-042022-11-040001428205arr:A2021CommonStockATMSalesAgreementMember2023-01-172023-01-170001428205us-gaap:CommonStockMemberarr:A2021CommonStockATMSalesAgreementMember2023-01-012023-07-310001428205arr:A2023CommonStockATMSalesAgreementMember2023-07-262023-07-260001428205arr:A2023CommonStockATMSalesAgreementMember2023-07-260001428205us-gaap:CommonStockMemberarr:A2023CommonStockATMSalesAgreementMember2023-01-012023-12-310001428205us-gaap:CommonStockMemberarr:CommonStockRepurchaseProgramMember2024-01-012024-03-310001428205us-gaap:CommonStockMemberarr:A2021CommonStockATMSalesAgreementMember2023-01-012023-12-310001428205us-gaap:CommonStockMemberarr:A2021CommonStockATMSalesAgreementMember2023-12-310001428205us-gaap:CommonStockMemberarr:A2023CommonStockATMSalesAgreementMember2023-12-310001428205us-gaap:CommonStockMember2023-01-012023-12-310001428205us-gaap:SubsequentEventMemberus-gaap:SeriesCPreferredStockMember2024-04-292024-04-290001428205us-gaap:SubsequentEventMemberus-gaap:SeriesCPreferredStockMember2024-05-152024-05-150001428205us-gaap:SubsequentEventMember2024-04-292024-04-290001428205us-gaap:SubsequentEventMember2024-05-152024-05-150001428205us-gaap:SeriesCPreferredStockMember2024-01-292024-01-290001428205us-gaap:SeriesCPreferredStockMember2024-02-272024-02-270001428205us-gaap:SeriesCPreferredStockMember2024-03-272024-03-270001428205us-gaap:CommonStockMember2024-01-302024-01-300001428205us-gaap:CommonStockMember2024-02-282024-02-280001428205us-gaap:CommonStockMember2024-03-282024-03-280001428205us-gaap:CapitalLossCarryforwardMember2019-12-310001428205us-gaap:CapitalLossCarryforwardMember2021-12-310001428205us-gaap:CapitalLossCarryforwardMember2022-12-310001428205us-gaap:CapitalLossCarryforwardMember2023-12-310001428205srt:AffiliatedEntityMemberarr:ArmourManagementAgreementMember2024-01-012024-03-310001428205srt:AffiliatedEntityMember2024-01-012024-03-310001428205arr:ARMOURManagementFeesMember2024-01-012024-03-310001428205arr:ARMOURManagementFeesMember2023-01-012023-03-310001428205arr:ManagementFeesWaivedMember2024-01-012024-03-310001428205arr:ManagementFeesWaivedMember2023-01-012023-03-310001428205arr:ManagementFeeExpenseMember2024-01-012024-03-310001428205arr:ManagementFeeExpenseMember2023-01-012023-03-310001428205srt:AffiliatedEntityMemberarr:OtherExpensesReimbursedMember2024-01-012024-03-310001428205srt:AffiliatedEntityMemberarr:OtherExpensesReimbursedMember2023-01-012023-03-310001428205srt:AffiliatedEntityMemberus-gaap:RestrictedStockUnitsRSUMember2024-01-012024-03-310001428205srt:AffiliatedEntityMember2023-01-012023-03-310001428205us-gaap:RelatedPartyMemberarr:BUCKLERSecuritiesLLCMember2023-12-310001428205us-gaap:RelatedPartyMemberarr:BUCKLERSecuritiesLLCMember2023-01-012023-03-310001428205us-gaap:RelatedPartyMemberarr:BUCKLERSecuritiesLLCMember2024-01-012024-03-310001428205us-gaap:RelatedPartyMemberarr:BUCKLERSecuritiesLLCMember2023-03-200001428205arr:RequiredRegulatoryCapitalRequirementofRelatedPartyMemberarr:BUCKLERSecuritiesLLCMember2024-03-310001428205us-gaap:RelatedPartyMemberarr:RequiredRegulatoryCapitalRequirementofRelatedPartyMemberarr:BUCKLERSecuritiesLLCMember2024-01-012024-03-310001428205arr:UncommittedRevolvingCreditFacilityAndSecurityAgreementMember2021-02-220001428205us-gaap:RelatedPartyMemberarr:UncommittedRevolvingCreditFacilityAndSecurityAgreementMember2021-02-222021-02-220001428205us-gaap:RelatedPartyMemberarr:BUCKLERSecuritiesLLCMember2023-01-012023-12-310001428205us-gaap:RelatedPartyMemberarr:BUCKLERSecuritiesLLCMemberus-gaap:USTreasurySecuritiesMember2023-01-012023-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

| | | | | |

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly Period Ended March 31, 2024

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

ARMOUR RESIDENTIAL REIT, INC.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Maryland | 001-34766 | 26-1908763 |

| (State or other jurisdiction of incorporation or organization) | (Commission File Number) | (I.R.S. Employer Identification No.) |

3001 Ocean Drive, Suite 201, Vero Beach, FL 32963

(Address of principal executive offices)(zip code)

(772) 617-4340

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of Each Class | | Trading symbols | | Name of Exchange on which registered |

| Preferred Stock, 7.00% Series C Cumulative Redeemable | | ARR-PRC | | New York Stock Exchange |

| Common Stock, $0.001 par value | | ARR | | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer" "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☒ Accelerated filer ☐ Non-accelerated filer ☐ Smaller reporting company ☐ Emerging growth company ☐

If an emerging growth company, indicate by a check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The number of outstanding shares of the Registrant’s common stock as of April 24, 2024 was 48,751,806.

ARMOUR Residential REIT, Inc.

TABLE OF CONTENTS

| | | | | |

| |

Item 1. Financial Statements | |

| |

| |

| |

| |

Item 1. Legal Proceedings | |

Item IA. Risk Factors | |

| |

Item 3. Defaults Upon Senior Securities | |

Item 4. Mine Safety Disclosures | |

Item 5. Other Information | |

| |

| |

1

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

ARMOUR Residential REIT, Inc.

CONSOLIDATED BALANCE SHEETS (UNAUDITED)

(in thousands, except per share)

| | | | | | | | | | | | | | |

| | March 31, 2024 | | December 31, 2023 |

| Assets | | | | |

| Cash and cash equivalents | | $ | 221,297 | | | $ | 221,888 | |

| Cash collateral posted to counterparties | | 38,220 | | | 36,970 | |

| Investments in securities, at fair value | | | | |

Agency Securities (including pledged securities of $10,304,605 ($6,167,891 with BUCKLER) at March 31, 2024 and $10,599,340 ($5,400,138 with BUCKLER) at December 31, 2023) | | 10,905,877 | | | 11,159,754 | |

| | | | |

Receivable for unsettled sales (including pledged securities of $35,948 at March 31, 2024) | | 35,948 | | | — | |

| Derivatives, at fair value | | 959,727 | | | 877,412 | |

| Accrued interest receivable | | 46,209 | | | 47,111 | |

| Prepaid and other | | 1,020 | | | 1,260 | |

| | | | |

| Total Assets | | $ | 12,208,298 | | | $ | 12,344,395 | |

| Liabilities and Stockholders’ Equity | | | | |

| Liabilities: | | | | |

Repurchase agreements, net (including $4,865,218 and $4,667,483, respectively with BUCKLER) | | $ | 8,654,063 | | | $ | 9,647,982 | |

| Obligations to return securities received as collateral, at fair value | | 1,101,625 | | | 350,273 | |

| Cash collateral posted by counterparties | | 927,360 | | | 860,130 | |

| Payable for unsettled purchases | | 199,683 | | | 171,513 | |

| Derivatives, at fair value | | 3,328 | | | 5,036 | |

Accrued interest payable- repurchase agreements (including $29,071 and $12,345, respectively with BUCKLER) | | 49,884 | | | 26,509 | |

| Accrued interest payable- U.S. Treasury Securities sold short | | 11,869 | | | 5,049 | |

| Accounts payable and other accrued expenses | | 13,373 | | | 6,719 | |

| Total Liabilities | | $ | 10,961,185 | | | $ | 11,073,211 | |

| | | | |

Commitments and contingencies (Note 8 and Note 14) | | | | |

| | | | |

| Stockholders’ Equity: | | | | |

Preferred stock, $0.001 par value, 50,000 shares authorized; 7.00% Series C Cumulative Preferred Stock; 6,847 shares issued and outstanding ($25.00 per share liquidation preference) | | 7 | | | 7 | |

Common stock, $0.001 par value, 90,000 shares authorized; 48,752 shares and 48,799 shares issued and outstanding at March 31, 2024 and December 31, 2023, respectively. | | 49 | | | 49 | |

| Additional paid-in capital | | 4,317,875 | | | 4,318,155 | |

| Cumulative distributions to stockholders | | (2,258,874) | | | (2,220,567) | |

| Accumulated net loss | | (811,944) | | | (826,460) | |

| | | | |

| Total Stockholders’ Equity | | $ | 1,247,113 | | | $ | 1,271,184 | |

| Total Liabilities and Stockholders’ Equity | | $ | 12,208,298 | | | $ | 12,344,395 | |

See financial statement notes (unaudited).

2

ARMOUR Residential REIT, Inc.

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (LOSS) (UNAUDITED)

(in thousands, except per share)

| | | | | | | | | | | | | | | | | | |

| | | | For the Three Months Ended March 31, |

| | | | | | 2024 | | 2023 |

| Interest Income: | | | | | | | | |

Interest Income (including $0 and $973, respectively with BUCKLER) | | | | | | $ | 141,480 | | | $ | 118,458 | |

Interest expense (including $70,790 and $49,609, respectively with BUCKLER) | | | | | | (136,149) | | | (106,245) | |

| Net Interest Income | | | | | | $ | 5,331 | | | $ | 12,213 | |

| Other Income (Loss): | | | | | | | | |

| Realized loss on sale of available for sale Agency Securities (reclassified from Comprehensive Income (Loss)) | | | | | | — | | | (7,471) | |

| | | | | | | | |

| Gain (loss) on Agency Securities, trading | | | | | | (137,749) | | | 120,366 | |

| Gain (loss) on U.S. Treasury Securities | | | | | | 10,922 | | | (11,854) | |

| | | | | | | | |

Gain (loss) on derivatives, net (1) | | | | | | 156,448 | | | (134,400) | |

| Total Other Income (Loss) | | | | | | $ | 29,621 | | | $ | (33,359) | |

| Expenses: | | | | | | | | |

| Management fees | | | | | | 9,803 | | | 9,244 | |

| Compensation | | | | | | 1,437 | | | 1,159 | |

| Other operating | | | | | | 10,846 | | | 1,460 | |

| Total Expenses | | | | | | $ | 22,086 | | | $ | 11,863 | |

| Less management fees waived | | | | | | (1,650) | | | (1,650) | |

| Total Expenses after fees waived | | | | | | $ | 20,436 | | | $ | 10,213 | |

| Net Income (Loss) | | | | | | $ | 14,516 | | | $ | (31,359) | |

| Dividends on preferred stock | | | | | | (2,995) | | | (2,995) | |

| Net Income (Loss) available (related) to common stockholders | | | | | | $ | 11,521 | | | $ | (34,354) | |

|

| Net Income (Loss) | | | | | | $ | 14,516 | | | $ | (31,359) | |

| Reclassification adjustment for realized loss on sale of available for sale Agency Securities | | | | | | — | | | 7,471 | |

| | | | | | | | |

| Net unrealized gain on available for sale Agency Securities | | | | | | — | | | 4,056 | |

| Other Comprehensive Income | | | | | | — | | | 11,527 | |

| Comprehensive Income (Loss) | | | | | | $ | 14,516 | | | $ | (19,832) | |

| Dividends on preferred stock | | | | | | (2,995) | | | (2,995) | |

| Comprehensive Income (Loss) available (related) to common stockholders | | | | | | $ | 11,521 | | | $ | (22,827) | |

| | | | | | | | |

Net Income (Loss) per share available (related) to common stockholders (Note 11): | | | | | | | | |

| Basic | | | | | | $ | 0.24 | | | $ | (0.95) | |

| Diluted | | | | | | $ | 0.24 | | | $ | (0.95) | |

| Dividends declared per common share | | | | | | $ | 0.72 | | | $ | 1.40 | |

| Weighted average common shares outstanding: | | | | | | | | |

| Basic | | | | | | 48,770 | | | 36,917 | |

| Diluted | | | | | | 48,988 | | | 36,917 | |

(1) Interest income and expense related to our interest rate swap contracts is recorded in gain (loss) on derivatives, net on the consolidated statements of operations and comprehensive income (loss). For additional information, see financial statement Note 7.

See financial statement notes (unaudited).

3

ARMOUR Residential REIT, Inc.

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY (UNAUDITED)

(in thousands)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

|

| | Shares | | Par | | | | | | | | | | |

| | Preferred Stock | | Common Stock | | Preferred Stock | | Common Stock | | Additional Paid-in Capital | | Cumulative Distributions to Stockholders | | Accumulated Net Loss | | Accumulated Other Comprehensive Income (Loss) | | Total Stockholders'Equity |

| Balance, December 31, 2022 | | 6,847 | | | 32,582 | | | $ | 7 | | | $ | 33 | | | $ | 3,874,757 | | | $ | (1,992,361) | | | $ | (758,537) | | | $ | (11,527) | | | 1,112,372 | |

| Comprehensive income (loss) | | — | | | — | | | — | | | — | | | — | | | — | | | (31,359) | | | 11,527 | | | (19,832) | |

| | | | | | | | | | | | | | | | | | |

| Issuance of common stock, net | | — | | | 5,973 | | | — | | | 6 | | | 181,199 | | | — | | | — | | | — | | | 181,205 | |

| Stock based compensation, net of withholding requirements | | — | | | 14 | | | — | | | — | | | 692 | | | — | | | — | | | — | | | 692 | |

| Common stock repurchased | | — | | | (169) | | | — | | | — | | | (4,305) | | | — | | | — | | | — | | | (4,305) | |

| Preferred stock dividends | | — | | | — | | | — | | | — | | | — | | | (2,995) | | | — | | | — | | | (2,995) | |

| Common stock dividends | | — | | | — | | | — | | | — | | | — | | | (52,004) | | | — | | | — | | | (52,004) | |

| Balance, March 31, 2023 | | 6,847 | | | 38,400 | | | $ | 7 | | | $ | 39 | | | $ | 4,052,343 | | | $ | (2,047,360) | | | $ | (789,896) | | | $ | — | | | $ | 1,215,133 | |

|

| Balance, December 31, 2023 | | 6,847 | | | 48,799 | | | $ | 7 | | | $ | 49 | | | $ | 4,318,155 | | | $ | (2,220,567) | | | $ | (826,460) | | | $ | — | | | $ | 1,271,184 | |

| Comprehensive income | | — | | | — | | | — | | | — | | | — | | | — | | | 14,516 | | | — | | | 14,516 | |

| | | | | | | | | | | | | | | | | | |

| Issuance of common stock, net | | — | | | 1 | | | — | | | — | | | 11 | | | — | | | — | | | — | | | 11 | |

| Stock based compensation, net of withholding requirements | | — | | | 22 | | | — | | | — | | | 1,053 | | | — | | | — | | | — | | | 1,053 | |

| Common stock repurchased | | — | | | (70) | | | — | | | — | | | (1,344) | | | — | | | — | | | — | | | (1,344) | |

| Preferred stock dividends | | — | | | — | | | — | | | — | | | — | | | (2,995) | | | — | | | — | | | (2,995) | |

| Common stock dividends | | — | | | — | | | — | | | — | | | — | | | (35,312) | | | — | | | — | | | (35,312) | |

| Balance, March 31, 2024 | | 6,847 | | | 48,752 | | | $ | 7 | | | $ | 49 | | | $ | 4,317,875 | | | $ | (2,258,874) | | | $ | (811,944) | | | $ | — | | | $ | 1,247,113 | |

See financial statement notes (unaudited).

4

ARMOUR Residential REIT, Inc.

CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

(in thousands)

| | | | | | | | | | | | | | |

| | For the Three Months Ended March 31, |

| | 2024 | | 2023 |

| Cash Flows From Operating Activities: | | | | |

| Net Income (Loss) | | $ | 14,516 | | | $ | (31,359) | |

| Adjustments to reconcile net income (loss) to net cash and cash collateral posted to counterparties provided by operating activities: | | | | |

| Net amortization of premium on Agency Securities | | 436 | | | 1,122 | |

| Net amortization of U.S. Treasury Securities | | — | | | 132 | |

| Realized loss on sale of Agency Securities, available for sale | | — | | | 7,471 | |

| (Gain) Loss on Agency Securities, trading | | 137,749 | | | (120,366) | |

| (Gain) Loss on U.S. Treasury Securities | | (10,922) | | | 11,854 | |

| Stock based compensation | | 1,053 | | | 692 | |

| Changes in operating assets and liabilities: | | | | |

| (Increase) Decrease in accrued interest receivable | | 914 | | | (21,424) | |

| (Increase) Decrease in prepaid and other assets | | 240 | | | (4,889) | |

| Change in derivatives, at fair value | | (84,023) | | | 184,119 | |

| Increase in accrued interest payable- repurchase agreements | | 23,375 | | | 19,735 | |

| Increase in accrued interest payable- U.S. Treasury Securities sold short | | 6,820 | | | 5,242 | |

| Increase in accounts payable and other accrued expenses | | 6,654 | | | 1,890 | |

| Net cash and cash collateral posted to counterparties provided by operating activities | | $ | 96,812 | | | $ | 54,219 | |

| Cash Flows From Investing Activities: | | | | |

Purchases of Agency Securities (includes $232,478 and $57,039 with BUCKLER, respectively) | | (422,542) | | | (5,317,154) | |

Purchases of U.S. Treasury Securities (includes $0 and $155,857 with BUCKLER, respectively) | | (97,003) | | | (619,373) | |

| Principal repayments of Agency Securities | | 182,548 | | | 148,523 | |

| Proceeds from sales of Agency Securities | | 347,896 | | | 1,052,878 | |

Proceeds from sales of U.S. Treasury Securities (includes $0 and $154,875 with BUCKLER, respectively) | | 859,277 | | | 613,852 | |

Disbursements on reverse repurchase agreements (includes $(1,805,375) and $(24,678) with BUCKLER, respectively) | | (2,425,876) | | | (24,678) | |

Receipts from reverse repurchase agreements (includes $1,254,000 and $224,579 with BUCKLER, respectively) | | 1,667,250 | | | 224,579 | |

| Increase in cash collateral posted by counterparties | | 67,230 | | | (110,089) | |

| Proceeds from subordinated loan due from BUCKLER | | — | | | 105,000 | |

| Net cash and cash collateral posted to counterparties provided by (used in) investing activities | | $ | 178,780 | | | $ | (3,926,462) | |

| Cash Flows From Financing Activities: | | | | |

| | | | |

| Issuance of common stock, net of expenses | | 1 | | | 181,205 | |

Proceeds from repurchase agreements (including $13,324,607 and $16,786,834, respectively with BUCKLER) | | 23,129,610 | | | 27,517,265 | |

Principal repayments on repurchase agreements (including $(12,575,496) and $(15,003,184), respectively with BUCKLER) | | (23,364,903) | | | (23,625,686) | |

| Series C Preferred stock dividends paid | | (2,995) | | | (2,995) | |

| Common stock dividends paid | | (35,302) | | | (52,004) | |

| Common stock repurchased | | (1,344) | | | (4,305) | |

| Net cash and cash collateral posted to counterparties provided by (used in) financing activities | | $ | (274,933) | | | $ | 4,013,480 | |

| (Continued) |

5

ARMOUR Residential REIT, Inc.

CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

(in thousands)

| | | | | | | | | | | | | | |

| | For the Three Months Ended March 31, |

| | 2024 | | 2023 |

| | | | |

| Net increase in cash and cash collateral posted to counterparties | | 659 | | | 141,237 | |

| Cash and cash collateral posted to counterparties - beginning of period | | 258,858 | | | 118,090 | |

| Cash and cash collateral posted to counterparties - end of period | | $ | 259,517 | | | $ | 259,327 | |

| Supplemental Disclosure: | | | | |

| Cash paid during the period for interest | | $ | 136,718 | | | $ | 107,680 | |

| Non-Cash Investing Activities: | | | | |

| Receivable for unsettled sales | | $ | 35,948 | | | $ | — | |

| Payable for unsettled purchases | | $ | (199,683) | | | $ | — | |

| Net unrealized gain (loss) on available for sale Agency Securities | | $ | — | | | $ | 4,056 | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

See financial statement notes (unaudited).

6

ARMOUR Residential REIT, Inc.

FINANCIAL STATEMENT NOTES (UNAUDITED)

(in thousands, except per share)

Note 1 - Organization and Nature of Business Operations

References to "we," "us," "our," or the "Company" are to ARMOUR Residential REIT, Inc. ("ARMOUR") and its subsidiaries. References to "ACM" are to ARMOUR Capital Management LP, a Delaware limited partnership. ARMOUR owns a 10.8% equity interest in BUCKLER Securities LLC ("BUCKLER"). BUCKLER is a Delaware limited liability company and a FINRA-regulated broker-dealer, controlled by ACM. Refer to the Glossary of Terms for definitions of capitalized terms and abbreviations used in this report. U.S. dollar amounts are presented in thousands, except per share amounts or as otherwise noted.

ARMOUR is an externally managed Maryland corporation incorporated in 2008. The Company is managed by ACM, an investment advisor registered with the Securities and Exchange Commission (the "SEC"), (see Note 8 - Commitments and Contingencies and Note 14 - Related Party Transactions). We have elected to be taxed as a real estate investment trust ("REIT") under the Internal Revenue Code of 1986, as amended (the "Code"). Our qualification as a REIT depends on our ability to meet, on a continuing basis, various complex requirements under the Code relating to, among other things, the sources of our gross income, the composition and values of our assets, our distribution levels and the concentration of ownership of our capital stock. We believe that we are organized in conformity with the requirements for qualification as a REIT under the Code and our manner of operations enables us to meet the requirements for taxation as a REIT for federal income tax purposes. As a REIT, we will generally not be subject to federal income tax on the REIT taxable income that we currently distribute to our stockholders. If we fail to qualify as a REIT in any taxable year and do not qualify for certain statutory relief provisions, we will be subject to federal income tax at regular corporate rates. Even if we qualify as a REIT for U.S. federal income tax purposes, we may still be subject to some federal, state and local taxes on our income.

At March 31, 2024 and December 31, 2023, we invested in mortgage backed securities ("MBS"), issued or guaranteed by a United States ("U.S.") Government-sponsored entity ("GSE"), such as the Federal National Mortgage Association ("Fannie Mae"), the Federal Home Loan Mortgage Corporation ("Freddie Mac"), or a government agency such as Government National Mortgage Administration ("Ginnie Mae") (collectively, "Agency Securities"). Our Agency Securities consist primarily of fixed rate loans. The remaining are either backed by hybrid adjustable rate or adjustable rate loans. From time to time we have also invested in U.S. Treasury Securities and money market instruments.

Note 2 - Basis of Presentation and Consolidation

The accompanying unaudited consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States ("GAAP") for interim financial information and with the instructions to Form 10-Q and Rule 10-01 of Regulation S-X promulgated by the SEC. Accordingly, the condensed financial statements do not include all of the information and footnotes required by GAAP for complete financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary for a fair presentation have been included. Operating results for the three months ended March 31, 2024 are not necessarily indicative of the results that may be expected for the calendar year ending December 31, 2024. These unaudited consolidated financial statements should be read in conjunction with the audited financial statements and notes thereto included in our annual report on Form 10-K for the year ended December 31, 2023.

The unaudited consolidated financial statements include the accounts of ARMOUR Residential REIT, Inc. and its subsidiaries. All intercompany accounts and transactions have been eliminated. The preparation of the consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Significant estimates affecting the accompanying consolidated financial statements include the valuation of MBS, including an assessment of the allowance for credit losses, and derivative instruments. Certain prior year amounts have been reclassified to conform to the current year's presentation.

7

ARMOUR Residential REIT, Inc.

FINANCIAL STATEMENT NOTES (UNAUDITED)

(in thousands, except per share)

All per share amounts, common shares outstanding and stock-based compensation amounts for all periods presented reflect our one-for-five reverse stock split (the “Reverse Stock Split”), which was effective September 29, 2023. No other reclassifications have been made to previously reported amounts.

Note 3 - Summary of Significant Accounting Policies

Cash and cash equivalents

Cash and cash equivalents includes cash on deposit with financial institutions. We may maintain deposits in federally insured financial institutions in excess of federally insured limits. However, management believes we are not exposed to significant credit risk due to the financial position and creditworthiness of the depository institutions in which those deposits are held.

Cash Collateral Posted To/By Counterparties

Cash collateral posted to/by counterparties represents cash posted by us to counterparties or posted by counterparties to us as collateral. Cash collateral posted to/by counterparties may include collateral for interest rate swap contracts, interest rate swaptions, basis swap contracts, futures contracts, repurchase agreements on our MBS and our Agency Securities purchased or sold on a to-be-announced basis ("TBA Agency Securities").

The interest earned or paid on cash collateral posted to/by counterparties is recorded in gain on derivatives, net in the consolidated statements of operations and comprehensive income.

Investments in Securities, at Fair Value

Our investments in securities are generally classified as either available for sale or trading securities. Management determines the appropriate classifications of the securities at the time they are acquired and evaluates the appropriateness of such classifications at each balance sheet date.

Trading Securities are reported at their estimated fair values with gains and losses included in Other Income (Loss) as a component of the consolidated statements of operations and comprehensive income (loss).

Available for Sale Securities represented investments that we intended to hold for extended periods of time and were reported at their estimated fair values with unrealized gains and losses excluded from earnings and reported as part of comprehensive income (loss). During the first quarter of 2023, we sold the remaining balance of our Available for Sale Securities which resulted in a realized loss of $(7,471).

Receivables and Payables for Unsettled Sales and Purchases

We account for purchases and sales of securities on the trade date, including purchases and sales for forward settlement. Receivables and payables for unsettled trades represent the agreed trade price multiplied by the outstanding balance of the securities at the balance sheet date.

Accrued Interest Receivable and Payable

Accrued interest receivable includes interest accrued between payment dates on securities and interest on unsettled sales of securities. Accrued interest payable includes interest on unsettled purchases of securities and interest on repurchase agreements, net. At certain times, we may have interest payable on U.S. Treasury Securities sold short.

Repurchase Agreements, net

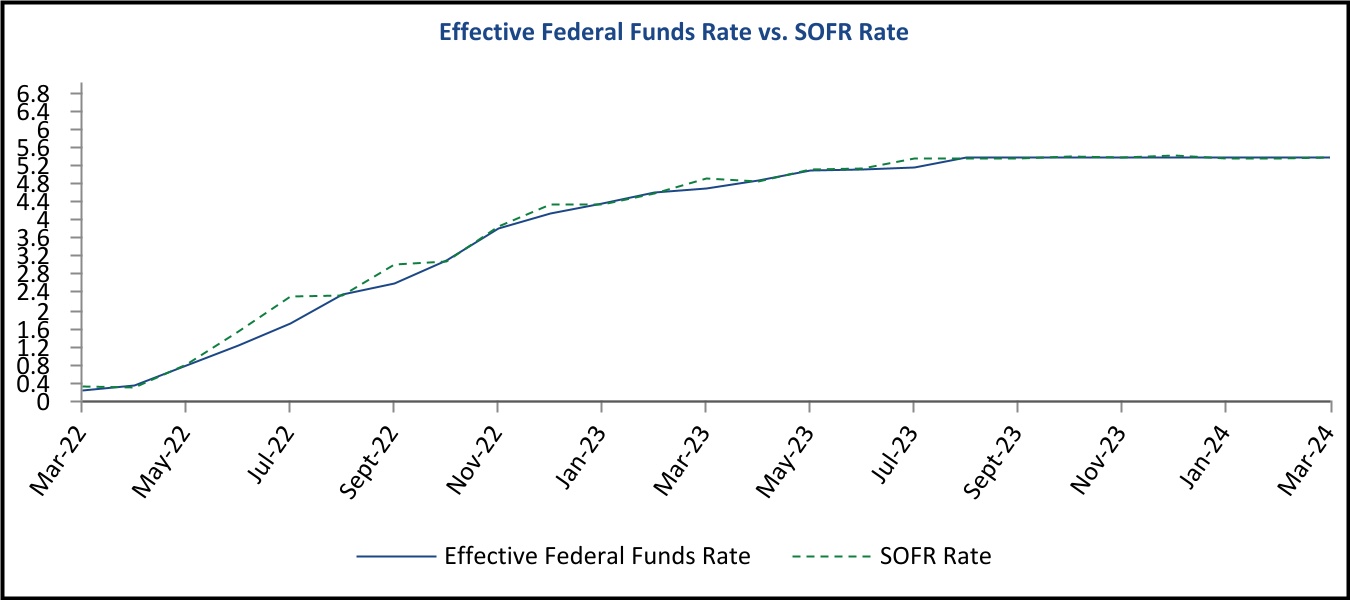

We finance the acquisition of the majority of our MBS through the use of repurchase agreements. Our repurchase agreements are secured by our MBS and bear interest rates that have moved in close relationship to the Federal Funds Effective Rate ("Federal Funds Rate") and the Secured Overnight Funding Rate ("SOFR"). Under these repurchase

8

ARMOUR Residential REIT, Inc.

FINANCIAL STATEMENT NOTES (UNAUDITED)

(in thousands, except per share)

agreements, we sell MBS to a lender and agree to repurchase the same MBS in the future for a price that is higher than the original sales price. The difference between the sales price that we receive and the repurchase price that we pay represents interest paid to the lender, which accrues over the life of the repurchase agreement. A repurchase agreement operates as a financing arrangement under which we pledge our MBS as collateral to secure a loan which is equal in value to a specified percentage of the estimated fair value of the pledged collateral. We retain beneficial ownership of the pledged collateral. At the maturity of a repurchase agreement, we are required to repay the loan and concurrently receive back our pledged collateral from the lender or, with the consent of the lender, we may renew such agreement at the then prevailing interest rate. The repurchase agreements may require us to pledge additional assets to the lender in the event the estimated fair value of the existing pledged collateral declines or take back certain pledged collateral if values increase.

In addition to the repurchase agreement financing discussed above, at certain times, we have entered into reverse repurchase agreements with certain of our repurchase agreement counterparties. Under a typical reverse repurchase agreement, we purchase U.S. Treasury Securities from a borrower in exchange for cash and agree to sell the same securities in the future in exchange for a price that is higher than the original purchase price. The difference between the purchase price originally paid and the sale price represents interest received from the borrower. Reverse repurchase agreement receivables and repurchase agreement liabilities are presented net when they meet certain criteria, including being with the same counterparty, being governed by the same master repurchase agreement ("MRA"), settlement through the same brokerage or clearing account and maturing on the same day. At March 31, 2024 and December 31, 2023, we had $1,112,563 ($905,313 of which were with BUCKLER) and $353,937 (all of which were with BUCKLER), respectively, in reverse repurchase agreements which are recorded in repurchase agreements, net on our consolidated balance sheet.

Obligations to Return Securities Received as Collateral, at Fair Value

We also sell to third parties the U.S. Treasury Securities received as collateral for reverse repurchase agreements and recognize the resulting obligation to return said U.S. Treasury Securities as a liability on our consolidated balance sheet. Interest is recorded on the repurchase agreements, reverse repurchase agreements and U.S. Treasury Securities on an accrual basis and presented as net interest expense. Both parties to the transaction have the right to make daily margin calls based on changes in the fair value of the collateral received and/or pledged. At March 31, 2024 and December 31, 2023, we had obligations to return securities received as collateral associated with our reverse repurchase agreements of $1,101,625 and $350,273, respectively.

Derivatives, at Fair Value

We recognize all derivatives individually as either assets or liabilities at fair value on our consolidated balance sheets. All changes in the fair values of our derivatives are reflected in our consolidated statements of operations and comprehensive income (loss). We designate derivatives as hedges for tax purposes and any unrealized derivative gains or losses would not affect our distributable net taxable income. These transactions may include interest rate swap contracts, interest rate swaptions, basis swap contracts and futures contracts.

We also may utilize forward contracts for the purchase or sale of TBA Agency Securities. We account for TBA Agency Securities as derivative instruments if it is reasonably possible that we will not take or make physical delivery of the Agency Security upon settlement of the contract. We account for TBA dollar roll transactions as a series of derivative transactions. We may also purchase and sell TBA Agency Securities as a means of investing in and financing Agency Securities (thereby increasing our “at risk” leverage) or as a means of disposing of or reducing our exposure to Agency Securities (thereby reducing our “at risk” leverage). We agree to purchase or sell, for future delivery, Agency Securities with certain principal and interest terms and certain types of collateral, but the particular Agency Securities to be delivered are not identified until shortly before the TBA settlement date. We may also choose, prior to settlement, to move the settlement of these securities out to a later date by entering into an offsetting short or long position (referred to as a “pair off”), net settling the paired off positions for cash, and simultaneously purchasing or selling a similar TBA Agency Security for a later settlement date. This transaction is commonly referred to as a “dollar roll.” When it is reasonably possible that we will pair off a TBA Agency Security, we account for that contract as a derivative.

9

ARMOUR Residential REIT, Inc.

FINANCIAL STATEMENT NOTES (UNAUDITED)

(in thousands, except per share)

Revenue Recognition

Interest income is earned and recognized on Agency Securities based on their unpaid principal amounts and their contractual terms. We record interest payable for interest received on securities sold during the period between the trade date and settlement date and interest receivable for purchases during the period between the trade date and settlement date. Premiums and discounts associated with the purchase of Multi-Family MBS, which are generally not subject to prepayment, are amortized or accreted into interest income over the contractual lives of the securities using a level yield method. Premiums and discounts associated with the purchase of other Agency Securities are amortized or accreted into interest income over the actual lives of the securities, reflecting actual prepayments as they occur. Purchase and sale transactions (including TBA Agency Securities) are recorded on the trade date to the extent it is probable that we will take or make timely physical delivery of the related securities. Gains or losses realized from sales of available for sale securities are reclassified into income from Comprehensive Income (Loss) and are determined using the specific identification method.

Interest income on U.S. Treasury Securities is recognized based on their unpaid principal amounts and their contractual terms. Recognition of interest income commences on the settlement date of the purchase transaction and continues through the settlement date of the sale transaction.

Comprehensive Income (Loss)

Comprehensive Income (loss) is comprised of net income (loss) and all changes to the statements of stockholders’ equity, except those due to investments by stockholders, changes in additional paid-in capital and distributions to stockholders.

Note 4 - Fair Value of Financial Instruments

Our valuation techniques for financial instruments use observable and unobservable inputs. Observable inputs reflect readily obtainable data from third-party sources, while unobservable inputs reflect management’s market assumptions. The Accounting Standards Codification Topic No. 820, "Fair Value Measurement," classifies these inputs into the following hierarchy:

Level 1 Inputs - Quoted prices for identical instruments in active markets.

Level 2 Inputs - Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations whose inputs are observable or whose significant value drivers are observable.

Level 3 Inputs - Prices determined using significant unobservable inputs. Unobservable inputs may be used in situations where quoted prices or observable inputs are unavailable (for example, when there is little or no market activity for an investment at the end of the period). Unobservable inputs reflect management’s assumptions about the factors that market participants would use in pricing an asset or liability and would be based on the best information available.

At the beginning of each quarter, we assess the assets and liabilities that are measured at fair value on a recurring basis to determine if any transfers between levels in the fair value hierarchy are needed.

The following describes the valuation methodologies used for our assets and liabilities measured at fair value, as well as the general classification of such instruments pursuant to the valuation hierarchy. Any transfers between levels are assumed to occur at the beginning of the reporting period.

10

ARMOUR Residential REIT, Inc.

FINANCIAL STATEMENT NOTES (UNAUDITED)

(in thousands, except per share)

Investments in Securities

Fair value for our investments in securities are based on obtaining a valuation for each security from third-party pricing services and/or dealer quotes. The third-party pricing services use common market pricing methods that may include pricing models that may incorporate such factors as coupons, prepayment speeds, spread to the Treasury curves and interest rate swap curves, duration, periodic and life caps and credit enhancement. If the fair value of a security is not available from the third-party pricing services or such data appears unreliable, we obtain pricing indications from up to three dealers who make markets in similar securities. Management reviews pricing used to ensure that current market conditions are properly reflected. This review includes, but is not limited to, comparisons of similar market transactions or alternative third-party pricing services, dealer pricing indications and comparisons to a third-party pricing model. Fair values obtained from the third-party pricing services for similar instruments are classified as Level 2 securities if the inputs to the pricing models used are consistent with the Level 2 definition. If quoted prices for a security are not reasonably available from the third-party pricing service, but dealer pricing indications are, the security will be classified as a Level 2 security. If neither is available, management will determine the fair value based on characteristics of the security that we receive from the issuer and based on available market information and classify it as a Level 3 security. U.S. Treasury Securities are classified as Level 1, as quoted unadjusted prices are available in active markets for identical assets.

Derivatives

The fair values of our interest rate swap contracts, interest rate swaptions and basis swap contracts are valued using information provided by third-party pricing services that incorporate common market pricing methods that may include current interest rate curves, forward interest rate curves and market spreads to interest rate curves and are classified as Level 2. We estimate the fair value of TBA Agency Securities based on similar methods used to value our Agency Securities and they are classified as Level 2. Management compares the pricing information received to dealer quotes to ensure that the current market conditions are properly reflected. Futures contracts are traded on the Chicago Mercantile Exchange ("CME") which requires the use of daily mark-to-market collateral and they are classified as Level 1.

The following tables provide a summary of our assets and liabilities that are measured at fair value on a recurring basis at March 31, 2024 and December 31, 2023.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| March 31, 2024 | | Level 1 | | Level 2 | | Level 3 | | Balance |

| Assets at Fair Value: | | | | | | | | |

| Agency Securities | | $ | — | | | $ | 10,905,877 | | | $ | — | | | $ | 10,905,877 | |

| | | | | | | | |

| Derivatives | | $ | — | | | $ | 959,727 | | | $ | — | | | $ | 959,727 | |

| Liabilities at Fair Value: | | | | | | | | |

| Derivatives | | $ | — | | | $ | 3,328 | | | $ | — | | | $ | 3,328 | |

| | | | | | | | |

| December 31, 2023 | | Level 1 | | Level 2 | | Level 3 | | Balance |

| Assets at Fair Value: | | | | | | | | |

| Agency Securities | | $ | — | | | $ | 11,159,754 | | | $ | — | | | $ | 11,159,754 | |

| | | | | | | | |

| Derivatives | | $ | — | | | $ | 877,412 | | | $ | — | | | $ | 877,412 | |

| Liabilities at Fair Value: | | | | | | | | |

| Derivatives | | $ | — | | | $ | 5,036 | | | $ | — | | | $ | 5,036 | |

There were no transfers of assets or liabilities between the levels of the fair value hierarchy during the three months ended March 31, 2024 or for the year ended December 31, 2023.

Excluded from the tables above are financial instruments, including cash and cash equivalents, cash collateral posted to/by counterparties, receivables, payables, borrowings under repurchase agreements, net and obligations to return securities received as collateral, which are presented in our consolidated financial statements at cost, which approximates

11

ARMOUR Residential REIT, Inc.

FINANCIAL STATEMENT NOTES (UNAUDITED)

(in thousands, except per share)

fair value. The estimated fair value of these instruments is measured using "Level 1" or "Level 2" inputs at March 31, 2024 and December 31, 2023.

Note 5 - Investments in Securities

As of March 31, 2024 and December 31, 2023, our securities portfolio consisted of $10,905,877 and $11,159,754 of investment securities, at fair value, respectively. We also had $0 and $305,039 of TBA Agency Securities, at fair value, which were reported at net carrying value of $(175) and $1,816, respectively, at March 31, 2024 and December 31, 2023. TBA Securities are reported in Derivatives, at fair value on our consolidated balance sheets (see Note 7 - Derivatives). The net carrying value of our TBA Agency Securities represents the difference between the fair value of the underlying Agency Security in the TBA contract and the cost basis or the forward price to be paid or received for the underlying Agency Security.

During the first quarter of 2023, we sold the remaining balance of our Available for Sale Securities which resulted in a realized loss of $(7,471).

The tables below present the components of the carrying value and the unrealized gain or loss position of our investments in securities at March 31, 2024 and December 31, 2023.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| March 31, 2024 | | Principal Amount | | Amortized Cost | | Gross Unrealized Loss | | Gross Unrealized Gain | | Fair Value |

| | | | | | | | | | |

| Agency Securities, trading | | $ | 11,195,462 | | | $ | 11,164,626 | | | $ | (275,166) | | | $ | 16,417 | | | $ | 10,905,877 | |

| | | | | | | | | | |

| | | | | | | | | | |

| December 31, 2023 | | | | | | | | | | |

| | | | | | | | | | |

| Agency Securities, trading | | 11,278,161 | | | 11,283,380 | | | (176,660) | | | 53,034 | | | 11,159,754 | |

| | | | | | | | | | |

The following table summarizes the weighted average lives of our investments in securities at March 31, 2024 and December 31, 2023.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | March 31, 2024 | | December 31, 2023 |

| Weighted Average Life | | Fair Value | | Amortized Cost | | Fair Value | | Amortized Cost |

| | | | | | | | |

| ≥ 1 year and < 3 years | | — | | | — | | | 202,508 | | | 195,904 | |

| ≥ 3 years and < 5 years | | 433,799 | | | 428,438 | | | 2,757,464 | | | 2,747,842 | |

| ≥ 5 years | | 10,472,078 | | | 10,736,188 | | | 8,199,782 | | | 8,339,634 | |

| Totals | | $ | 10,905,877 | | | $ | 11,164,626 | | | $ | 11,159,754 | | | $ | 11,283,380 | |

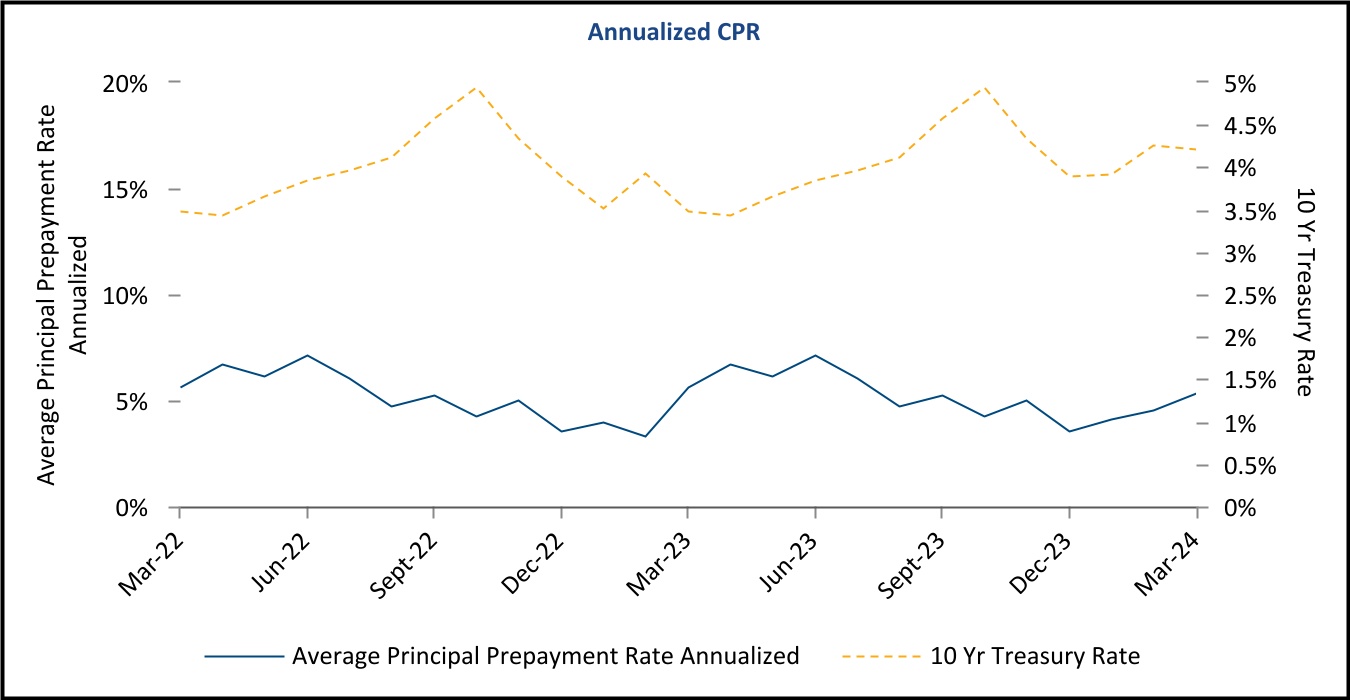

We use a third-party model to calculate the weighted average lives of our investments in securities. Weighted average life is calculated based on expectations for estimated prepayments for the underlying mortgage loans of our investments in securities. These estimated prepayments are based on assumptions such as interest rates, current and future home prices, housing policy and borrower incentives. The weighted average lives of our investments in securities at March 31, 2024 and December 31, 2023 in the tables above are based upon market factors, assumptions, models and estimates from the third-party model and also incorporate management’s judgment and experience. The actual weighted average lives of these securities could be longer or shorter than estimated.

Note 6 - Repurchase Agreements, net

At March 31, 2024, we had active MRAs with 31 counterparties and had $8,654,063 in outstanding borrowings with 14 of those counterparties. At December 31, 2023, we had MRAs with 39 counterparties and had $9,647,982 in outstanding borrowings with 14 counterparties.

12

ARMOUR Residential REIT, Inc.

FINANCIAL STATEMENT NOTES (UNAUDITED)

(in thousands, except per share)

The following tables represent the contractual repricing regarding our repurchase agreements to finance MBS purchases at March 31, 2024 and December 31, 2023. Our repurchase agreements require excess collateral, known as a “haircut.” At March 31, 2024, the average haircut percentage was 2.90% compared to 2.74% at December 31, 2023. The haircut for our repurchase agreements vary by counterparty and therefore, the changes in the average haircut percentage will vary with the changes in our counterparty repurchase agreement balances.

| | | | | | | | | | | | | | | | | | | | |

| March 31, 2024 | | Balance | | Weighted Average Contractual Rate | | Weighted Average Maturity in days |

| | | | | | |

≤ 30 days (1) | | $ | 6,287,337 | | | 5.49 | % | | 19 |

| > 30 days to ≤ 90 days | | 2,366,726 | | | 5.47 | % | | 35 |

| | | | | | |

| | | | | | |

| Total or Weighted Average | | $ | 8,654,063 | | | 5.48 | % | | 24 |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

(1)Net of reverse repurchase agreements of $1,112,563 ($905,313 of which were with BUCKLER). Obligations to return securities received as collateral of $1,101,625 associated with the reverse repurchase agreements are all due within 30 days.

| | | | | | | | | | | | | | | | | | | | |

| December 31, 2023 | | Balance | | Weighted Average Contractual Rate | | Weighted Average Maturity in days |

| | | | | | |

≤ 30 days (1) | | $ | 9,647,982 | | | 5.54 | % | | 12 |

| Total or Weighted Average | | $ | 9,647,982 | | | 5.54 | % | | 12 |

(1)Net of reverse repurchase agreements of $353,937 (all of which were with BUCKLER). Obligations to return securities received as collateral of $350,273 associated with the reverse repurchase agreements all matured in January 2024.

The following table presents information about the gross and net securities purchased and sold under our repurchase agreements, net on the accompanying consolidated balance sheets at March 31, 2024 and December 31, 2023.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| March 31, 2024 | | | | | | | | Gross Amounts Not Offset | | |

| | Gross Amounts | | Gross Amounts offset in the Consolidated Balance Sheet | | Net Amounts Presented in the Consolidated Balance Sheet | | Financial Instruments (1) | | Cash Collateral | | Total Net |

| Assets | | | | | | | | | | | | |

| Reverse Repurchase Agreements | | $ | 1,112,563 | | | $ | (1,112,563) | | | $ | — | | | $ | — | | | $ | — | | | $ | — | |

| Totals | | $ | 1,112,563 | | | $ | (1,112,563) | | | $ | — | | | $ | — | | | $ | — | | | $ | — | |

| | | | | | | | | | | | |

| Liabilities | | | | | | | | | | | | |

| Repurchase Agreements | | $ | (9,766,626) | | | $ | 1,112,563 | | | $ | (8,654,063) | | | $ | 8,654,063 | | | $ | — | | | $ | — | |

| Totals | | $ | (9,766,626) | | | $ | 1,112,563 | | | $ | (8,654,063) | | | $ | 8,654,063 | | | $ | — | | | $ | — | |

13

ARMOUR Residential REIT, Inc.

FINANCIAL STATEMENT NOTES (UNAUDITED)

(in thousands, except per share)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| December 31, 2023 | | | | | | | | Gross Amounts Not Offset | | |

| | Gross Amounts | | Gross Amounts offset in the Consolidated Balance Sheet | | Net Amounts Presented in the Consolidated Balance Sheet | | Financial Instruments (1) | | Cash Collateral | | Total Net |

| Assets | | | | | | | | | | | | |

| Reverse Repurchase Agreements | | $ | 353,937 | | | $ | (353,937) | | | $ | — | | | $ | — | | | $ | — | | | $ | — | |

| Totals | | $ | 353,937 | | | $ | (353,937) | | | $ | — | | | $ | — | | | $ | — | | | $ | — | |

| | | | | | | | | | | | |

| Liabilities | | | | | | | | | | | | |

| Repurchase Agreements | | $ | (10,001,919) | | | $ | 353,937 | | | $ | (9,647,982) | | | $ | 9,647,982 | | | $ | — | | | $ | — | |

| Totals | | $ | (10,001,919) | | | $ | 353,937 | | | $ | (9,647,982) | | | $ | 9,647,982 | | | $ | — | | | $ | — | |

(1)The fair value of securities pledged against our repurchase agreements was $10,304,605 and $10,599,340 at March 31, 2024 and December 31, 2023, respectively.

Our repurchase agreements require that we maintain adequate pledged collateral. A decline in the value of the MBS pledged as collateral for borrowings under repurchase agreements could result in the counterparties demanding additional collateral pledges or liquidation of some of the existing collateral to reduce borrowing levels. We manage this risk by maintaining an adequate balance of available cash and unpledged securities. An event of default or termination event under the standard MRA would give our counterparty the option to terminate all repurchase transactions existing with us and require any amount due to be payable immediately. In addition, certain of our MRAs contain a restriction that prohibits our leverage from exceeding twelve times our stockholders’ equity as well as termination events in the case of significant reductions in equity capital. We also may receive cash or securities as collateral from our derivative counterparties which we may use as additional collateral for repurchase agreements. Certain interest rate swap contracts provide for cross collateralization and cross default with repurchase agreements and other contracts with the same counterparty.

At March 31, 2024 and December 31, 2023, BUCKLER accounted for 56.2% and 48.4%, respectively, of our aggregate borrowings and had an amount at risk of 9.4% and 8.1%, respectively, of our total stockholders' equity with a weighted average maturity of 27 days and 12 days, respectively, on repurchase agreements, net (see Note 14 - Related Party Transactions).

In addition, at March 31, 2024, we had 3 repurchase agreement counterparties that individually accounted for over 5% of our aggregate borrowings. In total, these counterparties accounted for approximately 21.0% of our repurchase agreement borrowings outstanding at March 31, 2024. At December 31, 2023, we had 4 repurchase agreement counterparties that individually accounted for over 5% of our aggregate borrowings. In total, these counterparties accounted for 27.2% of our repurchase agreement borrowings at December 31, 2023.

Note 7 - Derivatives

We enter into derivative transactions to manage our interest rate risk and agency mortgage rate exposures. We have agreements with our derivative counterparties that provide for the posting of collateral based on the fair values of our derivatives. Through this margin process, either we or our counterparties may be required to pledge cash or securities as collateral. Collateral requirements vary by counterparty and change over time based on the fair value, notional amount and remaining term of the contracts. Certain contracts provide for cross collateralization and cross default with repurchase agreements and other contracts with the same counterparty.

Interest rate swap contracts are designed to lock in long-term average funding costs for repurchase agreements associated with our assets in an attempt to maximize earnings from our assets. Such transactions are based on assumptions about prepayments which, if not realized, will cause transaction results to differ from expectations. Interest rate swaptions

14

ARMOUR Residential REIT, Inc.

FINANCIAL STATEMENT NOTES (UNAUDITED)

(in thousands, except per share)

generally provide us the option to enter into an interest rate swap agreement at a certain point of time in the future with a predetermined notional amount, stated term and stated rate of interest in the fixed leg and interest rate index on the floating leg. Basis swap contracts allow us to exchange one floating interest rate basis for another, thereby allowing us to diversify our floating rate basis exposures.

All of our interest rate contracts have floating leg interest rate indexes of either the Federal Funds Rate or SOFR. The Federal Funds Rate is published daily by the New York Federal Reserve and is a measure of unsecured borrowings by depository institutions from other depository institutions or GSEs. SOFR is published daily by the New York Federal Reserve and is the average overnight rate for borrowings secured by U.S. Treasury securities. We enter into interest rate swap contracts either directly with a counterparty (a “bilateral” contract) or through a centrally-cleared swap contract. In a bilateral contract, we exchange margin collateral with the counterparty and have exposure to counterparty risk. In a centrally-cleared contract, we exchange margin collateral with a Futures Clearing Merchant, with whom we have opened an account. Our counterparty risk is limited to the clearing exchange itself. All of our centrally-cleared swaps are cleared by the CME. In general, centrally-cleared interest rate swap contracts require us to post higher initial margin than bilateral contracts.

Futures contracts are traded on the CME which requires the use of daily mark-to-market collateral and the CME provides substantial credit support. The collateral requirements of the CME require us to pledge assets under a bi-lateral margin arrangement, including either cash or Agency Securities and these requirements may vary and change over time based on the market value, notional amount and remaining term of the futures contracts. In the event we are unable to meet a margin call under one of our futures contracts, the counterparty to such agreement may have the option to terminate or close-out all of the outstanding futures contracts with us. In addition, any close-out amount due to the counterparty upon termination of the counterparty’s transactions would be immediately payable by us pursuant to the applicable agreement.

TBA Agency Securities are forward contracts for the purchase (“long position”) or sale (“short position”) of Agency Securities at a predetermined price, face amount, issuer, coupon and stated maturity on an agreed-upon future date. The specific Agency Securities delivered into the contract upon the settlement date, published each month by the Securities Industry and Financial Markets Association, are not known at the time of the transaction. We may enter into TBA Agency Securities as a means of hedging against short-term changes in interest rates. We may also enter into TBA Agency Securities as a means of acquiring or disposing of Agency Securities and we may from time to time utilize TBA dollar roll transactions to finance Agency Security purchases. We estimate the fair value of TBA Agency Securities based on similar methods used to value our Agency Securities.

We have netting arrangements in place with all derivative counterparties pursuant to standard documentation developed by ISDA. We are also required to post or hold cash collateral based upon the net underlying market value of our open positions with the counterparty. A decline in the value of the open positions with the counterparty could result in the counterparties demanding additional collateral pledges or liquidation of some of the existing collateral to reduce borrowing levels. We manage this risk by maintaining an adequate balance of available cash and unpledged securities. An event of default or termination event under the standard ISDA would give our counterparty to the applicable agreement the right to terminate the agreement. In addition, certain of our ISDAs contain a restriction that prohibits our leverage from exceeding twelve times our stockholders’ equity as well as termination events in the case of significant reductions in equity capital.

15

ARMOUR Residential REIT, Inc.

FINANCIAL STATEMENT NOTES (UNAUDITED)

(in thousands, except per share)

The following tables present information about the potential effects of netting our derivatives if we were to offset the assets and liabilities on the accompanying consolidated balance sheets. We currently present these financial instruments at their gross amounts and they are included in Derivatives, at fair value on the accompanying consolidated balance sheets at March 31, 2024 and December 31, 2023.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | Gross Amounts Not Offset | | |

| Assets | | Gross Amounts(1) | | Financial

Instruments | | Cash Collateral | | Total Net |

| March 31, 2024 | | | | | | | | |

Interest rate swap contracts (2) | | $ | 959,586 | | | $ | (3,012) | | | $ | (888,814) | | | $ | 67,760 | |

| | | | | | | | |

| TBA Agency Securities | | 141 | | | (141) | | | — | | | — | |

| Totals | | $ | 959,727 | | | $ | (3,153) | | | $ | (888,814) | | | $ | 67,760 | |

| | | | | | | | |

| December 31, 2023 | | | | | | | | |

Interest rate swap contracts (2) | | $ | 875,596 | | | $ | (5,036) | | | $ | (821,089) | | | $ | 49,471 | |

| TBA Agency Securities | | 1,816 | | | (1,816) | | | — | | | — | |

| Totals | | $ | 877,412 | | | $ | (6,852) | | | $ | (821,089) | | | $ | 49,471 | |

(1)See Note 4 - Fair Value of Financial Instruments for additional discussion.

(2)Includes $18,781 and $6,104 of centrally-cleared interest rate swap contracts, respectively.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | Gross Amounts Not Offset | | |

| Liabilities | | Gross Amounts(1) | | Financial

Instruments | | Cash Collateral | | Total Net |

| March 31, 2024 | | | | | | | | |

Interest rate swap contracts (2) | | $ | (3,012) | | | $ | 3,012 | | | $ | — | | | $ | — | |

| | | | | | | | |

| TBA Agency Securities | | (316) | | | 141 | | | (327) | | | (502) | |

| Totals | | $ | (3,328) | | | $ | 3,153 | | | $ | (327) | | | $ | (502) | |

| | | | | | | | |

| December 31, 2023 | | | | | | | | |

Interest rate swap contracts (2) | | $ | (5,036) | | | $ | 5,036 | | | $ | — | | | $ | — | |

| TBA Agency Securities | | — | | | 1,816 | | | (2,070) | | | (254) | |

| Totals | | $ | (5,036) | | | $ | 6,852 | | | $ | (2,070) | | | $ | (254) | |

(1)See Note 4 - Fair Value of Financial Instruments for additional discussion.

(2)Includes $(3,012) and $(5,036) of centrally-cleared interest rate swap contracts, respectively.

16

ARMOUR Residential REIT, Inc.

FINANCIAL STATEMENT NOTES (UNAUDITED)

(in thousands, except per share)

The following table represents the information regarding our derivatives which are included in Gain on derivatives, net in the accompanying consolidated statements of operations and comprehensive income (loss) for the three months ended March 31, 2024 and March 31, 2023.

| | | | | | | | | | | | | | | | | | |

| | | | | Income (Loss) Recognized |

| | | | For the Three Months Ended March 31, |

| Derivatives | | | | | | 2024 | | 2023 |

Interest rate swap contracts (1) | | | | | | $ | 160,709 | | | $ | (126,414) | |

| Futures contracts | | | | | | — | | | (10,829) | |

| TBA Agency Securities | | | | | | (4,261) | | | 2,843 | |

| Total Gain on Derivatives, net | | | | | | $ | 156,448 | | | $ | (134,400) | |

(1)Includes $25,046 and $(29,096) of centrally-cleared interest rate swap contracts for the three months ended March 31, 2024 and March 31, 2023, respectively.

The following tables present information about our derivatives at March 31, 2024 and December 31, 2023. We did not have any TBA Agency Securities at March 31, 2024.

| | | | | | | | | | | | | | | | | | | | |

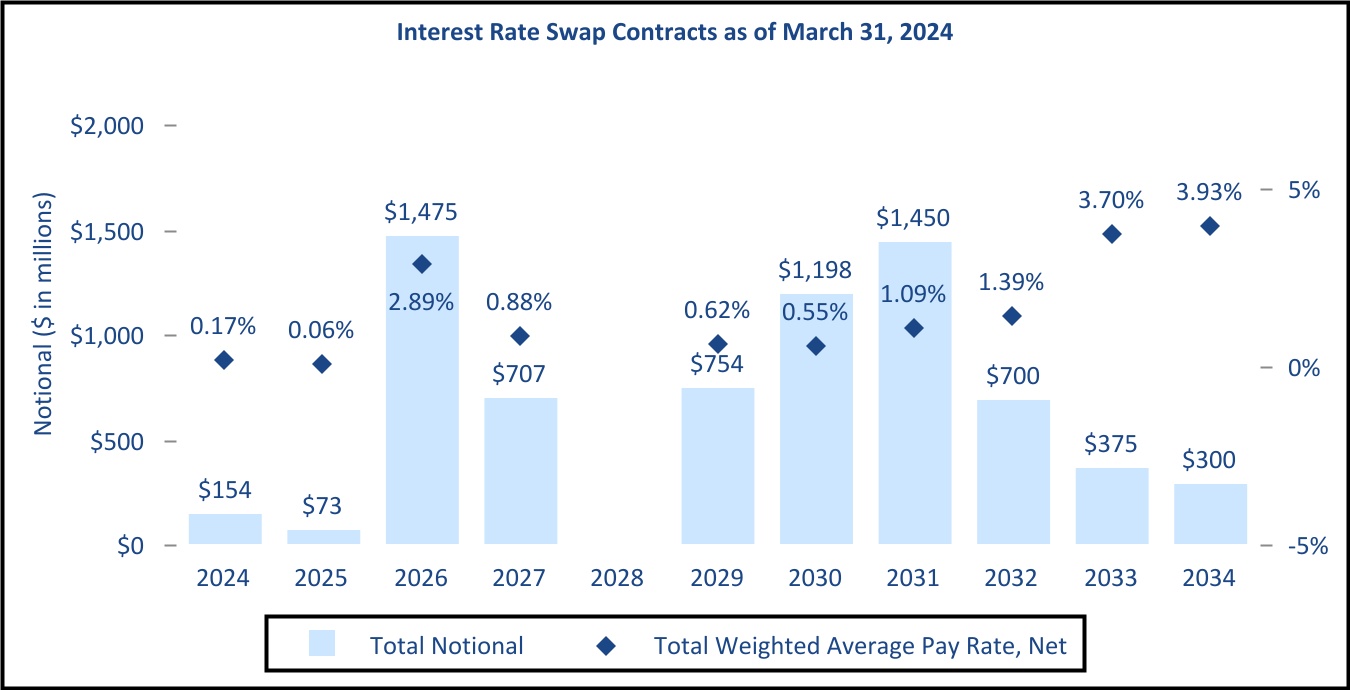

Interest Rate Swap Contracts (1) | | Notional Amount | | Weighted Average Remaining Term (Months) | | Weighted Average Rate |

| March 31, 2024 | | | | | | |

< 3 years | | $ | 1,859,000 | | | 24 | | 2.34 | % |

≥ 3 years and < 5 years | | 550,000 | | | 38 | | 1.06 | % |

≥ 5 years and < 7 years | | 3,202,000 | | | 77 | | 0.79 | % |

≥ 7 years | | 1,575,000 | | | 104 | | 2.37 | % |

| | | | | | |

Total or Weighted Average (2) | | $ | 7,186,000 | | | 66 | | 1.56 | % |

| | | | | | |

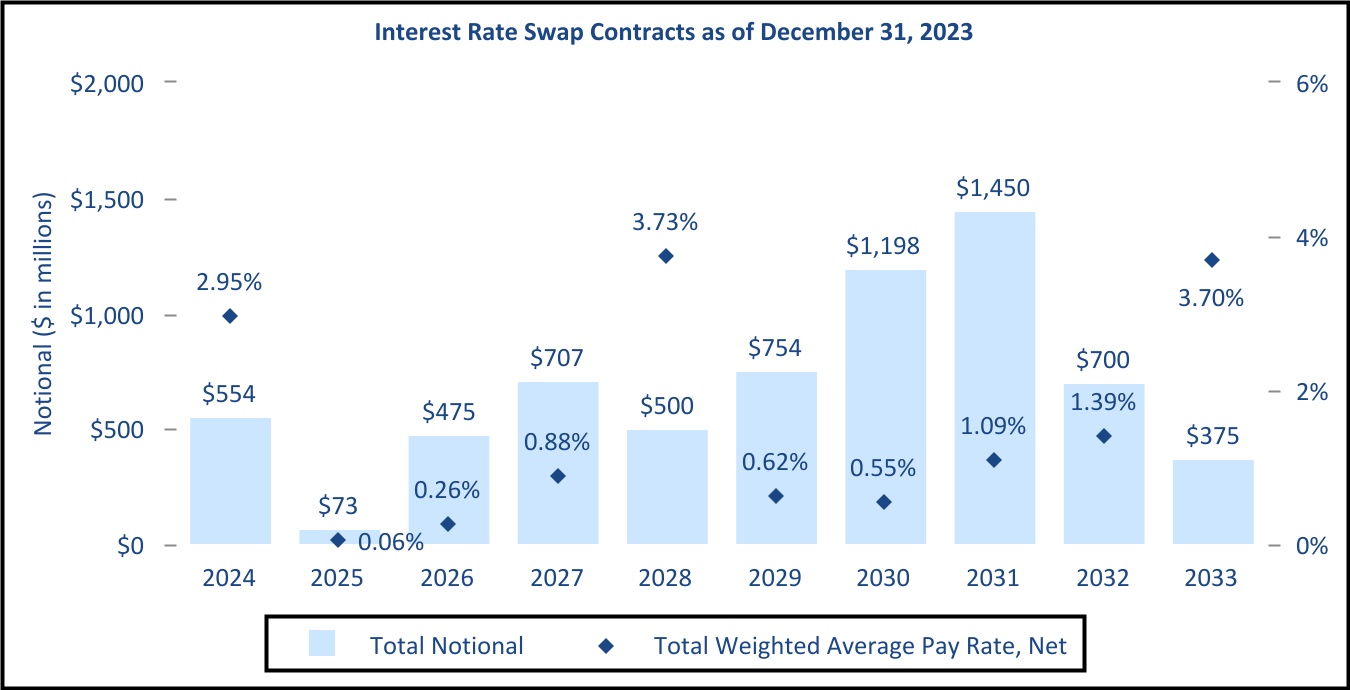

| December 31, 2023 | | | | | | |

< 3 years | | $ | 1,102,000 | | | 18 | | 1.60 | % |

≥ 3 years and < 5 years | | 1,207,000 | | | 45 | | 2.06 | % |

≥ 5 years and < 7 years | | 1,952,000 | | | 75 | | 0.58 | % |

≥ 7 years | | 2,525,000 | | | 95 | | 1.56 | % |

Total or Weighted Average (3) | | $ | 6,786,000 | | | 68 | | 1.37 | % |

(1)Pay Fixed/Receive Variable.

(2)Of this amount, $1,875,000 notional are SOFR based swaps, the last of which matures in 2034; and $5,311,000 notional are Fed Funds based swaps, the last of which matures in 2032. Of this amount, $1,675,000 notional are centrally-cleared interest rate swap contracts, the last of which matures in 2034.

(3)Of this amount, $1,475,000 notional are SOFR based swaps, the last of which matures in 2033; and $5,311,000 notional are Fed Funds based swaps, the last of which matures in 2032. Of this amount, $1,275,000 notional are centrally-cleared interest rate swap contracts, the last of which matures in 2033.

17

ARMOUR Residential REIT, Inc.

FINANCIAL STATEMENT NOTES (UNAUDITED)

(in thousands, except per share)

| | | | | | | | | | | | | | | | | | | | |

| TBA Agency Securities | | Notional Amount | | Cost Basis | | Fair Value |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| December 31, 2023 | | | | | | |

| | | | | | |

30 Year Long, 6.0% | | 300,000 | | | 303,223 | | | 305,039 | |

Totals (1) | | $ | 300,000 | | | $ | 303,223 | | | $ | 305,039 | |

Note 8 - Commitments and Contingencies

Management

The Company is managed by ACM, pursuant to a management agreement (see also Note 14 - Related Party Transactions). The management agreement entitles ACM to receive management fees payable monthly in arrears. Currently, the monthly management fee is 1/12th of the sum of (a) 1.5% of gross equity raised up to $1.0 billion plus (b) 0.75% of gross equity raised in excess of $1.0 billion. Gross equity raised includes the total amounts of paid in capital relating to both our common and preferred stock, before deduction of brokerage commissions and other costs of capital raising. Amounts paid to stockholders to repurchase stock, before deduction of brokerage commissions and costs, reduces gross equity raised. Dividends specifically designated by the Board as liquidation dividends will reduce the amount of gross equity raised. To date, the Board has not so designated any of the dividends paid by the Company. Realized and unrealized gains and losses do not affect the amount of gross equity raised. At March 31, 2024, the effective management fee, prior to management fees waived, was 0.93% based on gross equity raised of $4,230,648.