UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

___________________________________________________________

FORM 6-K

___________________________________________________________

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 under

the Securities Exchange Act of 1934

For the quarterly period ended September 30, 2020

Commission file number 1-33867

___________________________________________________________

TEEKAY TANKERS LTD.

(Exact name of Registrant as specified in its charter)

___________________________________________________________

Suite 2000, 550 Burrard Street, Bentall 5, Vancouver, BC V6C 2K2 Canada

(Address of principal executive office)

___________________________________________________________

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F ý Form 40-F ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1).

Yes ¨ No ý

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7).

Yes ¨ No ý

TEEKAY TANKERS LTD.

REPORT ON FORM 6-K FOR THE QUARTERLY PERIOD ENDED SEPTEMBER 30, 2020

INDEX

| PAGE | ||||||||

| Item 1. | ||||||||

| Item 2. | ||||||||

PART I – FINANCIAL INFORMATION

ITEM 1 – FINANCIAL STATEMENTS

TEEKAY TANKERS LTD. AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF (LOSS) INCOME (note 1)

(in thousands of U.S. Dollars, except share and per share amounts)

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||||||||||||

| $ | $ | $ | $ | |||||||||||||||||||||||

Voyage charter revenues (note 3) | ||||||||||||||||||||||||||

Time-charter revenues (note 3) | ||||||||||||||||||||||||||

Other revenues (notes 3 and 4) | ||||||||||||||||||||||||||

| Total revenues | ||||||||||||||||||||||||||

| Voyage expenses | ( | ( | ( | ( | ||||||||||||||||||||||

Vessel operating expenses (note 13b) | ( | ( | ( | ( | ||||||||||||||||||||||

| Time-charter hire expenses | ( | ( | ( | ( | ||||||||||||||||||||||

| Depreciation and amortization | ( | ( | ( | ( | ||||||||||||||||||||||

General and administrative expenses (note 13b) | ( | ( | ( | ( | ||||||||||||||||||||||

| Write-down and loss on sale of assets (note 15) | ( | ( | ||||||||||||||||||||||||

Restructuring charge (note 17) | ( | ( | ||||||||||||||||||||||||

| (Loss) income from operations | ( | ( | ||||||||||||||||||||||||

| Interest expense | ( | ( | ( | ( | ||||||||||||||||||||||

| Interest income | ||||||||||||||||||||||||||

Realized and unrealized (loss) gain on derivative instruments (note 8) | ( | ( | ( | |||||||||||||||||||||||

| Equity income | ||||||||||||||||||||||||||

Other (expense) income (note 9) | ( | |||||||||||||||||||||||||

| Net (loss) income before income tax | ( | ( | ( | |||||||||||||||||||||||

Income tax (expense) recovery (note 10) | ( | ( | ( | |||||||||||||||||||||||

| Net (loss) income | ( | ( | ( | |||||||||||||||||||||||

Per common share amounts (note 14) | ||||||||||||||||||||||||||

| - Basic (loss) earnings per share | $ | ( | $ | ( | $ | $ | ( | |||||||||||||||||||

| - Diluted (loss) earnings per share | $ | ( | $ | ( | $ | $ | ( | |||||||||||||||||||

Weighted-average number of Class A and Class B common stock outstanding (note 14) | ||||||||||||||||||||||||||

| - Basic | ||||||||||||||||||||||||||

| - Diluted | ||||||||||||||||||||||||||

Related party transactions (note 13) | ||||||||||||||||||||||||||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

1

TEEKAY TANKERS LTD. AND SUBSIDIARIES

UNAUDITED CONSOLIDATED BALANCE SHEETS (notes 1 and 2)

(in thousands of U.S. Dollars)

| As at | As at | |||||||||||||

| September 30, 2020 | December 31, 2019 | |||||||||||||

$ | $ | |||||||||||||

| ASSETS | ||||||||||||||

| Current | ||||||||||||||

| Cash and cash equivalents | ||||||||||||||

Restricted cash – current (note 16) | ||||||||||||||

| Accounts receivable | ||||||||||||||

Assets held for sale (note 15) | ||||||||||||||

Due from affiliates (note 13c) | ||||||||||||||

Current portion of derivative assets (note 8) | ||||||||||||||

| Bunker and lube oil inventory | ||||||||||||||

| Prepaid expenses | ||||||||||||||

| Accrued revenue | ||||||||||||||

| Total current assets | ||||||||||||||

Restricted cash – long-term (note 16) | ||||||||||||||

Vessels and equipment | ||||||||||||||

At cost, less accumulated depreciation of $496.4 million (2019 - $537.1 million) (note 6) | ||||||||||||||

Vessels related to finance leases, at cost, less accumulated depreciation of $126.9 million (2019 - $143.7 million) (note 7) | ||||||||||||||

Operating lease right-of-use assets (note 7) | ||||||||||||||

| Total vessels and equipment | ||||||||||||||

| Investment in and advances to equity-accounted joint venture | ||||||||||||||

Derivative assets (note 8) | ||||||||||||||

| Other non-current assets | ||||||||||||||

| Intangible assets at cost, less accumulated amortization of $3.6 million (2019 - $3.2 million) | ||||||||||||||

| Goodwill | ||||||||||||||

| Total assets | ||||||||||||||

| LIABILITIES AND EQUITY | ||||||||||||||

| Current | ||||||||||||||

| Accounts payable | ||||||||||||||

Accrued liabilities (notes 13c and 17) | ||||||||||||||

Short-term debt (note 5) | ||||||||||||||

Due to affiliates (note 13c) | ||||||||||||||

Liabilities associated with assets held for sale (note 15) | ||||||||||||||

Current portion of derivative liabilities (note 8) | ||||||||||||||

Current portion of long-term debt (note 6) | ||||||||||||||

Current obligations related to finance leases (note 7) | ||||||||||||||

Current portion of operating lease liabilities (note 7) | ||||||||||||||

| Other current liabilities | ||||||||||||||

| Total current liabilities | ||||||||||||||

Long-term debt (note 6) | ||||||||||||||

Long-term obligations related to finance leases (note 7) | ||||||||||||||

Long-term operating lease liabilities (note 7) | ||||||||||||||

Derivative liabilities (note 8) | ||||||||||||||

Other long-term liabilities (note 10) | ||||||||||||||

| Total liabilities | ||||||||||||||

Commitments and contingencies (notes 5, 6, 7, and 8) | ||||||||||||||

| Equity | ||||||||||||||

Common stock and additional paid-in capital (585.0 million shares authorized, 29.1 million Class A and 4.6 million Class B shares issued and outstanding as of September 30, 2020 and 585.0 million shares authorized, 29.0 million Class A and 4.6 million Class B shares issued and outstanding as at December 31, 2019) (note 12) | ||||||||||||||

| Accumulated deficit | ( | ( | ||||||||||||

| Total equity | ||||||||||||||

| Total liabilities and equity | ||||||||||||||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

2

TEEKAY TANKERS LTD. AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF CASH FLOWS (note 1)

(in thousands of U.S. Dollars)

| Nine Months Ended September 30, | ||||||||||||||

| 2020 | 2019 | |||||||||||||

| $ | $ | |||||||||||||

| Cash, cash equivalents and restricted cash provided by (used for) | ||||||||||||||

| OPERATING ACTIVITIES | ||||||||||||||

| Net income (loss) | ( | |||||||||||||

| Non-cash items: | ||||||||||||||

| Depreciation and amortization | ||||||||||||||

Write-down and loss on sale of assets (note 15) | ||||||||||||||

Unrealized loss on derivative instruments (note 8) | ||||||||||||||

| Equity income | ( | ( | ||||||||||||

Income tax (recovery) expense (note 10) | ( | |||||||||||||

| Other | ||||||||||||||

| Change in operating assets and liabilities | ||||||||||||||

| Expenditures for dry docking | ( | ( | ||||||||||||

| Net operating cash flow | ||||||||||||||

| FINANCING ACTIVITIES | ||||||||||||||

Proceeds from short-term debt (note 5) | ||||||||||||||

Proceeds from long-term debt, net of issuance costs (note 6) | ||||||||||||||

Scheduled repayments of long-term debt (note 6) | ( | ( | ||||||||||||

Prepayments of long-term debt (note 6) | ( | ( | ||||||||||||

Prepayments of short-term debt (note 5) | ( | ( | ||||||||||||

Proceeds from financing related to sales and leaseback of vessels (note 8) | ||||||||||||||

Scheduled repayments of obligations related to finance leases (note 7) | ( | ( | ||||||||||||

| Other | ( | ( | ||||||||||||

| Net financing cash flow | ( | ( | ||||||||||||

| INVESTING ACTIVITIES | ||||||||||||||

Proceeds from sale of assets (net of cash sold of $2.1 million) (note 15) | ||||||||||||||

| Expenditures for vessels and equipment | ( | ( | ||||||||||||

| Loan repayments from equity-accounted joint venture | ||||||||||||||

| Net investing cash flow | ( | |||||||||||||

| Increase in cash, cash equivalents and restricted cash | ||||||||||||||

| Cash, cash equivalents and restricted cash, beginning of the period | ||||||||||||||

| Cash, cash equivalents and restricted cash, end of the period | ||||||||||||||

Supplemental cash flow information (note 16)

The accompanying notes are an integral part of the unaudited consolidated financial statements.

3

TEEKAY TANKERS LTD. AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY (note 1)

(in thousands of U.S. Dollars, except share amounts)

Common Stock and Additional Paid-in Capital | ||||||||||||||||||||||||||||||||

Thousands of Common Shares # | Class A Common Shares $ | Class B Common Shares $ | Accumulated Deficit $ | Total $ | ||||||||||||||||||||||||||||

| Balance as at December 31, 2019 | ( | |||||||||||||||||||||||||||||||

| Net income | — | — | — | |||||||||||||||||||||||||||||

Equity-based compensation (note 12) | — | — | ||||||||||||||||||||||||||||||

| Balance as at March 31, 2020 | ( | |||||||||||||||||||||||||||||||

| Net income | — | — | — | |||||||||||||||||||||||||||||

Equity-based compensation (note 12) | — | — | ||||||||||||||||||||||||||||||

| Balance as at June 30, 2020 | ( | |||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | ( | |||||||||||||||||||||||||||

Equity-based compensation (note 12) | — | — | — | |||||||||||||||||||||||||||||

| Balance as at September 30, 2020 | ( | |||||||||||||||||||||||||||||||

Common Stock and Additional Paid-in Capital | ||||||||||||||||||||||||||||||||

Thousands of Common Shares # | Class A Common Shares $ | Class B Common Shares $ | Accumulated Deficit $ | Total $ | ||||||||||||||||||||||||||||

| Balance as at December 31, 2018 | ( | |||||||||||||||||||||||||||||||

| Net income | — | — | — | |||||||||||||||||||||||||||||

Equity-based compensation (note 12) | — | — | ||||||||||||||||||||||||||||||

| Balance as at March 31, 2019 | ( | |||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | ( | |||||||||||||||||||||||||||

Equity-based compensation (note 12) | — | — | ||||||||||||||||||||||||||||||

| Balance as at June 30, 2019 | ( | |||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | ( | |||||||||||||||||||||||||||

Equity-based compensation (note 12) | — | — | — | |||||||||||||||||||||||||||||

| Balance as at September 30, 2019 | ( | |||||||||||||||||||||||||||||||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

4

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

1.Basis of Presentation

The unaudited interim consolidated financial statements (or unaudited consolidated financial statements) have been prepared in accordance with United States generally accepted accounting principles (or GAAP). These unaudited consolidated financial statements include the accounts of Teekay Tankers Ltd., its wholly-owned subsidiaries, equity-accounted joint venture and any variable interest entities (or VIEs) of which it is the primary beneficiary (collectively, the Company). The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts reported in the unaudited consolidated financial statements and accompanying notes. Actual results could differ from those estimates.

Certain information and footnote disclosures required by GAAP for complete annual financial statements have been omitted and, therefore, these unaudited consolidated financial statements should be read in conjunction with the Company’s audited consolidated financial statements for the year ended December 31, 2019, filed on Form 20-F with the U.S. Securities and Exchange Commission (or the SEC) on April 15, 2020. In the opinion of management, these unaudited consolidated financial statements reflect all adjustments, consisting solely of a normal recurring nature, necessary to present fairly, in all material respects, the Company’s unaudited consolidated financial position, results of operations, and cash flows for the interim periods presented. The results of operations for the interim periods presented are not necessarily indicative of those for a full fiscal year. Intercompany balances and transactions have been eliminated upon consolidation.

In March 2020, the World Health Organization declared the outbreak of a novel coronavirus (or COVID-19) as a pandemic. Given the dynamic nature of these circumstances, the full extent to which the COVID-19 pandemic may have direct or indirect impact on the Company's business and the related financial reporting implications cannot be reasonably estimated at this time, although the pandemic could materially affect the Company's business, results of operations and financial condition in the future. COVID-19 has resulted and may continue to result in a significant decline in global demand for oil. As the Company's business includes the transportation of crude oil and refined petroleum products on behalf of customers, any significant decrease in demand for the cargo the Company transports could adversely affect demand for the Company's vessels and services. Spot tanker rates have come under pressure since mid-May 2020 as a result of record OPEC+ oil production cuts and lower production from other oil producing countries, which reduced crude exports, and the unwinding of floating storage. COVID-19 has also been a contributing factor to the decline in short-term charter rates and the increase in certain crewing-related costs, which has had an impact on our cash flows, and was a contributing factor to the write-down of certain tankers during the nine months ended September 30, 2020 as described in Note 15 - Write-down and Loss on Sale of Assets and the reduction in certain tax accruals as described in Note 10 - Income Tax (Expense) Recovery.

Voyage Charter Revenues and Expenses

Voyage expenses incurred that are recoverable from the Company's customers in connection with its voyage charter contracts are reflected in voyage charter revenues and voyage expenses. The Company recast prior periods to reflect this presentation. This had the impact of increasing both voyage charter revenues and voyage expenses by $5.1 million and $15.5 million for the three and nine months ended September 30, 2019, respectively.

Reverse Stock Split

The per share amounts for all periods presented have been adjusted to reflect a one-for-eight reverse stock split completed in November 2019.

2. Recent Accounting Pronouncements

In June 2016, the Financial Accounting Standards Board (or FASB) issued Accounting Standards Update 2016-13, Financial Instruments - Credit Losses: Measurement of Credit Losses on Financial Instruments (or ASU 2016-13). ASU 2016-13 introduces a new credit loss methodology, which requires earlier recognition of potential credit losses, while also providing additional transparency about credit risk. This new credit loss methodology utilizes a lifetime "expected credit loss" measurement objective for the recognition of credit losses for loans, held-to-maturity debt securities and other receivables at the time the financial asset is originated or acquired. The expected credit losses are subsequently adjusted each period for changes in expected lifetime credit losses. This methodology replaces multiple existing impairment methods under previous GAAP for these types of assets, which generally required that a loss be incurred before it was recognized. The Company adopted this update on January 1, 2020. The adoption of ASU 2016-13 did not have a material impact on the Company's unaudited consolidated financial statements.

In December 2019, the FASB issued ASU 2019-12 - Income Taxes (Topic 740) Simplifying the Accounting for Income Taxes (or ASU 2019-12), as part of its initiative to reduce complexity in the accounting standards. The amendments in ASU 2019-12 eliminate certain exceptions related to the approach for intraperiod tax allocation, the methodology for calculating income taxes in an interim period and the recognition of deferred tax liabilities for outside basis differences, among other changes. The guidance becomes effective for annual reporting periods beginning after December 15, 2020 and interim periods within those fiscal years with early adoption permitted. The Company is currently evaluating the effect of adopting this new guidance.

5

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

3. Revenue

The Company’s primary source of revenue is from chartering its vessels (Aframax tankers, Suezmax tankers and Long Range 2 (or LR2) tankers) to its customers. The Company utilizes two primary forms of contracts, consisting of voyage charters and time-charters.

The extent to which the Company employs its vessels on voyage charters versus time charters is dependent upon the Company’s chartering strategy and the availability of time charters. Spot market rates for voyage charters are volatile from period to period, whereas time charters provide a stable source of monthly revenue. The Company also provides ship-to-ship support services, which include managing the process of transferring cargo between seagoing ships positioned alongside each other, either stationary or underway, as well as commercial management services to third-party owners of vessels. Prior to April 30, 2020, the Company managed liquefied natural gas (or LNG) terminals and procured LNG-related goods for terminal owners and other customers. For descriptions of these types of contracts, see Item 18 - Financial Statements: Note 3 in the Company’s audited consolidated financial statements filed with its Annual Report on Form 20-F for the year ended December 31, 2019. On April 30, 2020, the Company completed the sale of the non-US portion of its ship-to-ship support services business, as well as its LNG terminal management business (see note 15).

The following table contains a breakdown of the Company's revenue by contract type for the three and nine months ended September 30, 2020 and September 30, 2019. All revenue is part of the Company's tanker segment, except for revenue for the non-US portion of the ship-to-ship support services and LNG terminal management, consultancy, procurement, and other related services, which are part of the Company's previously existing ship-to-ship transfer segment. The Company’s lease income consists of the revenue from its voyage charters and time-charters.

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||

$ | $ | $ | $ | ||||||||||||||||||||

| Voyage charter revenues | |||||||||||||||||||||||

| Suezmax | |||||||||||||||||||||||

| Aframax | |||||||||||||||||||||||

| LR2 | |||||||||||||||||||||||

| Full service lightering | |||||||||||||||||||||||

| Total | |||||||||||||||||||||||

| Time-charter revenues | |||||||||||||||||||||||

| Suezmax | |||||||||||||||||||||||

| Aframax | |||||||||||||||||||||||

| LR2 | |||||||||||||||||||||||

| Total | |||||||||||||||||||||||

| Other revenues | |||||||||||||||||||||||

| Ship-to-ship support services | |||||||||||||||||||||||

| Commercial management | |||||||||||||||||||||||

| LNG terminal management, consultancy, procurement and other | |||||||||||||||||||||||

| Total | |||||||||||||||||||||||

| Total revenues | |||||||||||||||||||||||

6

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

Charters-out

As at September 30, 2020, 11 (December 31, 2019 - five ) of the Company’s vessels operated under fixed-rate time charter contracts, three of which are scheduled to expire in 2020, six of which are scheduled to expire in 2021 and two of which are scheduled to expire in 2022. As at September 30, 2020, the minimum scheduled future revenues to be received by the Company under these time charters were approximately $31.6 million (remainder of 2020), $41.7 million (2021) and $5.2 million (2022) (December 31, 2019 - $40.0 million (2020)). The hire payments should not be construed to reflect a forecast of total charter hire revenue for any of the periods. Future hire payments do not include hire payments generated from new contracts entered into after September 30, 2020, from unexercised option periods of contracts that existed on September 30, 2020 or from variable consideration, if any, under contracts. In addition, future hire payments presented above have been reduced by estimated off-hire time for required periodic maintenance and do not reflect the impact of revenue sharing arrangements whereby time-charter revenues are shared with other revenue sharing arrangement participants. Actual amounts may vary given future events such as unplanned vessel maintenance.

Contract Liabilities

As at September 30, 2020, the Company had $3.1 million (December 31, 2019 - $7.5 million) of advanced payments recognized as contract liabilities that are expected to be recognized as time-charter revenues in subsequent periods and which currently are included in other current liabilities on the Company's unaudited consolidated balance sheets.

4. Segment Reporting

On April 30, 2020, the Company completed the sale of the non-US portion of its ship-to-ship support services business, as well as its LNG terminal management business. Following the sale, the Company's remaining ship-to-ship support operations were integrated into the Company's tanker business. As a result, effective April 30, 2020, the Company has one reportable segment. The Company’s segment information for all periods prior to the sale and reorganization has been retroactively adjusted whereby the remaining ship-to-ship support operations have been reallocated from the ship-to-ship transfer segment to the tanker segment. Consequently, the Company’s tanker segment now consists of the operation of all of its tankers, including the operations from those tankers employed on full service lightering contracts, and the US based ship-to-ship support service operations that the Company retained, including its lightering support services provided as part of full service lightering operations. The Company’s ship-to-ship transfer segment consisted of the Company’s non-US lightering support services, LNG terminal management, consultancy, procurement, and other related services which were sold as of April 30, 2020. Segment results are evaluated based on (loss) income from operations. The accounting policies applied to the reportable segments are the same as those used in the preparation of the Company’s unaudited consolidated financial statements.

The following tables include results for the Company’s revenues and (loss) income from operations by segment for the nine months ended September 30, 2020 and three and nine months ended September 30, 2019. No results are included for the three months ended September 30, 2020 as the Company only had one reportable segment during that period.

| Three Months Ended September 30, 2019 | ||||||||||||||||||||||||||

| Tanker Segment | Ship-to-Ship Transfer Segment | Total | ||||||||||||||||||||||||

| $ | $ | $ | ||||||||||||||||||||||||

Revenues (1) | ||||||||||||||||||||||||||

| Voyage expenses | ( | ( | ||||||||||||||||||||||||

| Vessel operating expenses | ( | ( | ( | |||||||||||||||||||||||

| Time-charter hire expenses | ( | ( | ||||||||||||||||||||||||

| Depreciation and amortization | ( | ( | ( | |||||||||||||||||||||||

General and administrative expenses (2) | ( | ( | ( | |||||||||||||||||||||||

| Loss from operations | ( | ( | ( | |||||||||||||||||||||||

| Equity income | ||||||||||||||||||||||||||

7

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

| Nine Months Ended September 30, 2020 | ||||||||||||||||||||||||||

| Tanker Segment | Ship-to-Ship Transfer Segment | Total | ||||||||||||||||||||||||

| $ | $ | $ | ||||||||||||||||||||||||

Revenues (1) | ||||||||||||||||||||||||||

| Voyage expenses | ( | ( | ||||||||||||||||||||||||

| Vessel operating expenses | ( | ( | ( | |||||||||||||||||||||||

| Time-charter hire expenses | ( | ( | ||||||||||||||||||||||||

| Depreciation and amortization | ( | ( | ( | |||||||||||||||||||||||

General and administrative expenses (2) | ( | ( | ( | |||||||||||||||||||||||

| (Loss) gain on sale of assets and write-down of assets | ( | ( | ||||||||||||||||||||||||

| Restructuring charge | ( | ( | ||||||||||||||||||||||||

| Income from operations | ||||||||||||||||||||||||||

| Equity income | ||||||||||||||||||||||||||

| Nine Months Ended September 30, 2019 | ||||||||||||||||||||||||||

| Tanker Segment | Ship-to-Ship Transfer Segment | Total | ||||||||||||||||||||||||

| $ | $ | $ | ||||||||||||||||||||||||

Revenues (1) | ||||||||||||||||||||||||||

| Voyage expenses | ( | ( | ||||||||||||||||||||||||

| Vessel operating expenses | ( | ( | ( | |||||||||||||||||||||||

| Time-charter hire expenses | ( | ( | ||||||||||||||||||||||||

| Depreciation and amortization | ( | ( | ( | |||||||||||||||||||||||

General and administrative expenses (2) | ( | ( | ( | |||||||||||||||||||||||

| Income from operations | ||||||||||||||||||||||||||

| Equity income | ||||||||||||||||||||||||||

(1)Revenues earned from the ship-to-ship transfer segment are reflected in Other Revenues in the Company's unaudited consolidated statements of (loss) income.

(2)Includes direct general and administrative expenses and indirect general and administrative expenses (allocated to each segment based on estimated use of corporate resources).

| As at | |||||||||||

| December 31, 2019 | |||||||||||

| $ | |||||||||||

Tanker | |||||||||||

Ship-to-Ship Transfer | |||||||||||

| Cash and cash equivalents | |||||||||||

| Consolidated total assets | |||||||||||

8

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

5. Short-Term Debt

6. Long-Term Debt

| As at | As at | ||||||||||

| September 30, 2020 | December 31, 2019 | ||||||||||

| $ | $ | ||||||||||

| Revolving Credit Facilities due through 2024 | |||||||||||

| Term Loans due through 2023 | |||||||||||

| Total principal | |||||||||||

| Less: unamortized discount and debt issuance costs | ( | ( | |||||||||

| Total debt | |||||||||||

| Less: current portion | ( | ( | |||||||||

| Long-term portion | |||||||||||

As at September 30, 2020, the Company had one revolving credit facility (or the 2020 Revolver) (December 31, 2019 - two revolving facilities), which, as at such date, provided for aggregate borrowings of up to $485.6 million, of which $330.6 million was undrawn (December 31, 2019 - $371.5 million, of which $30.4 million was undrawn). Interest payments are based on LIBOR plus a margin, which was 2.40 % as at September 30, 2020 (December 31, 2019 - ranged from 2.00 % to 2.75 %). The total amount available under the 2020 Revolver decreases by $47.2 million (remainder of 2020), $91.4 million (2021), $80.4 million (2022), $65.3 million (2023) and $201.3 million (2024). As at September 30, 2020, the Company also had one term loan (or the 2020 Term Loan) outstanding (December 31, 2019 - three ), which totaled $67.4 million (December 31, 2019 - $221.7 million). Interest payments are based on LIBOR plus a margin, which was 2.25 % as at September 30, 2020 (December 31, 2019 - based on a combination of a fixed rate of 5.40 % and variable rates based on LIBOR plus margins, which ranged from 0.30 % to 2.00 %). The term loan reduces in quarterly payments and has a balloon repayment due at maturity in 2023. The 2020 Revolver and 2020 Term Loan are further described below.

In January 2020, the Company entered into the 2020 Revolver, which is scheduled to mature in December 2024, and which had an outstanding balance of $155.0 million as at September 30, 2020. The 2020 Revolver was used to repay a portion of the $455.3 million previously outstanding under two previous revolving credit facilities of the Company, which were scheduled to mature in 2021 and 2022, and under two term loan facilities, which were scheduled to mature in 2020 and 2021. The 2020 Revolver is collateralized by 31 of the Company's vessels, together with other related security. The 2020 Revolver requires that the Company maintain a minimum hull coverage ratio of 125 % of the total outstanding drawn balance for the facility period. Such requirement is assessed on a semi-annual basis with reference to vessel valuations compiled by two or more agreed upon third parties. Should the ratio drop below the required amount, the lender may request that the Company either prepay a portion of the loan in the amount of the shortfall or provide additional collateral in the amount of the shortfall, at the Company's option. As at September 30, 2020, the hull coverage ratio was 483 %. A decline in the tanker market could negatively affect the ratio. In addition, the Company is required to maintain a minimum liquidity (cash, cash equivalents and undrawn committed revolving credit lines with at least six months to maturity) of $35.0 million and at least 5 % of the Company's total consolidated debt and obligations related to finance leases.

9

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

In August 2020, the Company entered into the 2020 Term Loan, which is scheduled to mature in August 2023, and which had an outstanding balance of $67.4 million as at September 30, 2020. The 2020 Term Loan was used to repay a portion of the $85.1 million previously outstanding under one previous term loan facility, which was scheduled to mature in 2021. The 2020 Term Loan is collateralized by four of the Company's vessels, together with other related security. The 2020 Term Loan requires that the Company maintain a minimum hull coverage ratio of 125 % of the total outstanding principal balance for the loan period. Such requirement is assessed on a semi-annual basis with reference to vessel valuations compiled by two or more agreed upon third parties. Should the ratio drop below the required amount, the lender may request that the Company either prepay a portion of the loan in the amount of the shortfall or provide additional collateral in the amount of the shortfall, at the Company's option. As at September 30, 2020, the hull coverage ratio was 182 %. A decline in the tanker market could negatively affect the ratio. In addition, the Company is required to maintain a minimum liquidity (cash, cash equivalents and undrawn committed revolving credit lines with at least six months to maturity) of $35.0 million and at least 5 % of the Company's total consolidated debt and obligations related to finance leases.

As of the date these unaudited consolidated financial statements were issued, the Company was in compliance with all covenants in respect of the 2020 Revolver and the 2020 Term Loan.

The weighted-average interest rate on the Company’s long-term debt as at September 30, 2020 was 2.6 % (December 31, 2019 - 3.7 %). This rate does not reflect the effect of the Company’s interest rate swap agreement (note 8).

The aggregate annual long-term debt principal repayments required to be made by the Company under the 2020 Revolver and the 2020 Term Loan subsequent to September 30, 2020, are $2.8 million (remainder of 2020), $11.2 million (2021), $11.2 million (2022), $42.2 million (2023) and $155.0 million (2024).

7. Operating Leases and Obligations Related to Finance Leases

Operating Leases

The Company charters-in vessels from other vessel owners on time-charter contracts, whereby the vessel owner provides use and technical operation of the vessel for the Company. A time charter-in contract is typically for a fixed period of time, although in certain cases, the Company may have the option to extend the charter. The Company typically pays the owner a daily hire rate that is fixed over the duration of the charter. The Company is generally not required to pay the daily hire rate during periods the vessel is not able to operate.

As at September 30, 2020, minimum commitments to be incurred by the Company under time charter-in contracts were approximately $8.9 million (remainder of 2020), $10.5 million (2021) and $1.5 million (2022).

Obligations Related to Finance Leases

| As at | As at | ||||||||||

| September 30, 2020 | December 31, 2019 | ||||||||||

| $ | $ | ||||||||||

| Total obligations related to finance leases | |||||||||||

| Less: current portion | ( | ( | |||||||||

| Long-term obligations related to finance leases | |||||||||||

From 2017 to 2019, the Company completed sale-leaseback financing transactions with financial institutions relating to 16 of the Company's vessels. Under these arrangements, the Company transferred the vessels to subsidiaries of the financial institutions (collectively, the Lessors) and leased the vessels back from the Lessors on bareboat charters ranging from 9 - to 12 -year terms. The Company is obligated to purchase eight of the vessels upon maturity of their respective bareboat charters. The Company also has the option to purchase each of the 16 vessels at various times starting between July 2020 and November 2021 until the end of their respective lease terms. In October 2020, the Company completed the purchases of two of these vessels for a total cost of $29.6 million and in November 2020, the Company declared purchase options to acquire two more of these vessels for a total cost of $56.7 million with an expected completion date of May 2021 (see note 19).

The bareboat charters related to these vessels require that the Company maintain a minimum liquidity (cash, cash equivalents and undrawn committed revolving credit lines with at least six months to maturity) of $35.0 million and at least 5.0 % of the Company's consolidated debt and obligations related to finance leases.

10

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

two years and 90 % of the total outstanding principal balance thereafter. As at September 30, 2020, these ratios ranged from 87 % to 104 % (December 31, 2019 - ranged from 106 % to 123 %).

Such requirements are assessed annually or quarterly with reference to vessel valuations compiled by one or more agreed upon third parties. As of the date these unaudited consolidated financial statements were issued, the Company was in compliance with all covenants in respect of its obligations related to finance leases.

The weighted-average interest rate on the Company’s obligations related to finance leases as at September 30, 2020 was 7.6 % (December 31, 2019 - 7.6 %).

As at September 30, 2020, the Company's total remaining commitments related to the financial liabilities of these vessels were approximately $559.7 million (December 31, 2019 - $601.7 million), including imputed interest of $163.6 million (December 31, 2019 - $186.9 million), repayable from 2020 through 2030, as indicated below:

| Commitments | ||||||||

| Year | September 30, 2020 | |||||||

| Remainder of 2020 | ||||||||

| 2021 | ||||||||

| 2022 | ||||||||

| 2023 | ||||||||

| 2024 | ||||||||

| Thereafter | ||||||||

8. Derivative Instruments

Interest rate swap agreement

The Company uses derivative instruments in accordance with its overall risk management policies. The Company enters into interest rate swap agreements which exchange a receipt of floating interest for a payment of fixed interest to reduce the Company’s exposure to interest rate variability on its outstanding floating-rate debt. The Company has not designated, for accounting purposes, its interest rate swap as a cash flow hedge of its U.S. Dollar LIBOR-denominated borrowings.

In January 2020, the Company completed a refinancing of certain long-term debt facilities (note 6). As a result of this refinancing, the Company extinguished all of its then existing interest rate swaps. In March 2020, the Company entered into a new interest rate swap which is scheduled to mature in December 2024. The following summarizes the Company's interest rate swap agreement as at September 30, 2020:

| Interest Rate | Notional Amount | Fair Value /Carrying Amount of Liability | Remaining Term | Fixed Swap Rate | |||||||||||||||||||||||||

| Index | $ | $ | (years) | (%) (1) | |||||||||||||||||||||||||

| LIBOR-Based Debt: | |||||||||||||||||||||||||||||

| U.S. Dollar-denominated interest rate swap agreement | LIBOR | ( | |||||||||||||||||||||||||||

(1)Excludes the margin the Company pays on its variable-rate long-term debt, which, as of September 30, 2020, ranged from 2.25 % to 2.40 %.

11

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

The Company is potentially exposed to credit loss in the event of non-performance by the counterparty to the interest rate swap agreements in the event that the fair value results in an asset being recorded. In order to minimize counterparty risk, the Company only enters into interest rate swap agreements with counterparties that are rated A– or better by Standard & Poor’s or A3 or better by Moody’s at the time transactions are entered into.

Forward freight agreements

The Company uses forward freight agreements (or FFAs) in non-hedge-related transactions to increase or decrease its exposure to spot market rates, within defined limits. Net gains and losses from FFAs are recorded within realized and unrealized (loss) gain on derivative instruments in the Company's unaudited consolidated statements of (loss) income.

The following table presents the location and fair value amounts of derivative instruments, segregated by type of contract, on the Company’s unaudited consolidated balance sheets.

| Current portion of derivative assets | Derivative assets | Accounts receivable | Current portion of derivative liabilities | Derivative liabilities | |||||||||||||||||||||||||

$ | $ | $ | $ | $ | |||||||||||||||||||||||||

| As at September 30, 2020 | |||||||||||||||||||||||||||||

| Interest rate swap agreement | ( | ( | |||||||||||||||||||||||||||

| Forward freight agreements | ( | ||||||||||||||||||||||||||||

| ( | ( | ||||||||||||||||||||||||||||

| As at December 31, 2019 | |||||||||||||||||||||||||||||

| Interest rate swap agreements | |||||||||||||||||||||||||||||

| Forward freight agreements | ( | ||||||||||||||||||||||||||||

| ( | |||||||||||||||||||||||||||||

Realized and unrealized gains (losses) relating to the interest rate swaps and FFAs are recognized in earnings and reported in realized and unrealized (loss) gain on derivative instruments in the Company’s unaudited consolidated statements of (loss) income as follows:

| Three Months Ended | Three Months Ended | ||||||||||||||||||||||

| September 30, 2020 | September 30, 2019 | ||||||||||||||||||||||

| Realized losses | Unrealized gains (losses) | Total | Realized gains | Unrealized (losses) gains | Total | ||||||||||||||||||

| $ | $ | $ | $ | $ | $ | ||||||||||||||||||

| Interest rate swap agreements | ( | ( | ( | ||||||||||||||||||||

| Forward freight agreements | ( | ( | ( | ||||||||||||||||||||

| ( | ( | ( | |||||||||||||||||||||

| Nine Months Ended | Nine Months Ended | ||||||||||||||||||||||

| September 30, 2020 | September 30, 2019 | ||||||||||||||||||||||

| Realized gains (losses) | Unrealized losses | Total | Realized gains | Unrealized (losses) gains | Total | ||||||||||||||||||

| $ | $ | $ | $ | $ | $ | ||||||||||||||||||

| Interest rate swap agreements | ( | ( | ( | ( | |||||||||||||||||||

| Forward freight agreements | ( | ( | ( | ||||||||||||||||||||

| ( | ( | ( | ( | ||||||||||||||||||||

12

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

9. Other (Expense) Income

The components of other (expense) income are as follows:

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

| Foreign exchange (loss) gain | ( | ||||||||||||||||||||||

| Other income | |||||||||||||||||||||||

| Total | ( | ||||||||||||||||||||||

10. Income Tax (Expense) Recovery

The following table reflects changes in uncertain tax positions relating to freight tax liabilities, which are recorded in other long-term liabilities and accrued liabilities on the Company's unaudited consolidated balance sheets:

| Nine Months Ended 30 September | |||||||||||

2020 $ | 2019 $ | ||||||||||

| Balance of unrecognized tax benefits as at January 1 | |||||||||||

| Increases for positions related to the current year | |||||||||||

| Changes for positions taken in prior years | ( | ||||||||||

| Settlements with tax authority | ( | ||||||||||

| Decreases related to statute of limitations | ( | ||||||||||

| Balance of unrecognized tax benefits as at September 30 | |||||||||||

Included in the Company's current income tax expense are provisions for uncertain tax positions relating to freight taxes. In the nine months ended September 30, 2020, the Company obtained further legal advice regarding the applicable tax rate in respect of freight taxes in a certain jurisdiction and subsequently secured an agreement in principle with a tax authority relating to an outstanding uncertain tax liability. The agreement in principle was based in part on an initiative of the tax authority in response to the COVID-19 global pandemic, which included the waiver of interest and penalties on unpaid taxes. Based on this and other clarifications of tax regulations, the Company reversed $15.2 million of freight tax liabilities as at June 30, 2020. In August 2020, the Company made a tax payment of $7.7 million to this jurisdiction with respect to open tax years up to and including 2019, with the remaining balance of tax accrual for 2020 recorded in accrued liabilities on the Company's unaudited consolidated balance sheet as of September 30, 2020.

The Company does not presently anticipate that its provisions for these uncertain tax positions will significantly increase in the next 12 months; however, this is dependent on the jurisdictions in which vessel trading activity occurs. The Company reviews its freight tax obligations on a regular basis and may update its assessment of its tax positions based on available information at that time. Such information may include legal advice as to applicability of freight taxes in relevant jurisdictions. Freight tax regulations are subject to change and interpretation; therefore, the amounts recorded by the Company may change accordingly.

11. Financial Instruments

Fair Value Measurements

For a description of how the Company estimates fair value and for a description of the fair value hierarchy levels, see Item 18 - Financial Statements: Note 14 to the Company’s audited consolidated financial statements filed with its Annual Report on Form 20-F for the year ended December 31, 2019.

13

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

The following table includes the estimated fair value and carrying value of those assets and liabilities that are measured at fair value on a recurring and non-recurring basis, as well as the estimated fair value of the Company’s financial instruments that are not accounted for at the fair value on a recurring basis.

| September 30, 2020 | December 31, 2019 | |||||||||||||||||||||||||||||||

Fair Value Hierarchy Level | Carrying Amount Asset / (Liability) $ | Fair Value Asset / (Liability) $ | Carrying Amount Asset / (Liability) $ | Fair Value Asset / (Liability) $ | ||||||||||||||||||||||||||||

| Recurring: | ||||||||||||||||||||||||||||||||

| Cash, cash equivalents and restricted cash | Level 1 | |||||||||||||||||||||||||||||||

Derivative instruments (note 8) | ||||||||||||||||||||||||||||||||

Interest rate swap agreements (1) | Level 2 | ( | ( | |||||||||||||||||||||||||||||

Forward freight agreements (1) | Level 2 | ( | ( | ( | ( | |||||||||||||||||||||||||||

| Non-recurring: | ||||||||||||||||||||||||||||||||

Operating lease right-of-use assets (note 15) | Level 2 | — | — | |||||||||||||||||||||||||||||

Vessels and equipment (3) (note 15) | Level 2 | — | — | |||||||||||||||||||||||||||||

Vessels related to finance leases (3) (note 15) | Level 2 | — | — | |||||||||||||||||||||||||||||

| Other: | ||||||||||||||||||||||||||||||||

Short-term debt (note 5) | Level 2 | ( | ( | ( | ( | |||||||||||||||||||||||||||

| Advances to equity-accounted joint venture | (2) | (2) | (2) | |||||||||||||||||||||||||||||

Long-term debt, including current portion (note 6) | Level 2 | ( | ( | ( | ( | |||||||||||||||||||||||||||

Obligations related to finance leases, including current portion (note 7) | Level 2 | ( | ( | ( | ( | |||||||||||||||||||||||||||

Assets held for sale (note 15) | Level 2 | |||||||||||||||||||||||||||||||

(1)The fair value of the Company’s interest rate swap agreements and FFAs at September 30, 2020 and December 31, 2019 exclude accrued interest income and expenses which are recorded in accounts receivable and accrued liabilities, respectively, on the unaudited consolidated balance sheets.

(2)The advances to its equity-accounted joint venture, together with the Company’s investment in the equity-accounted joint venture, form the net aggregate carrying value of the Company’s interests in the equity-accounted joint venture in these unaudited consolidated financial statements. The fair values of the individual components of such aggregate interests as at September 30, 2020 and December 31, 2019 were not determinable.

12. Capital Stock and Equity-Based Compensation

The authorized capital stock of the Company at September 30, 2020 was 100.0 million shares of Preferred Stock (December 31, 2019 - 100.0 million shares), with a par value of $0.01 per share (December 31, 2019 - $0.01 per share), 485.0 million shares of Class A common stock (December 31, 2019 - 485.0 million shares), with a par value of $0.01 per share (December 31, 2019 - $0.01 per share), and 100.0 million shares of Class B common stock (December 31, 2019 - 100.0 million shares), with a par value of $0.01 per share (December 31, 2019 - $0.01 per share). A share of Class A common stock entitles the holder to one vote per share while a share of Class B common stock entitles the holder to five votes per share, subject to a 49 % aggregate Class B common stock voting power maximum. As of September 30, 2020, the Company had 29.1 million shares of Class A common stock (December 31, 2019 – 29.0 million), 4.6 million shares of Class B common stock (December 31, 2019 – 4.6 million) and no shares of preferred stock (December 31, 2019 – nil ) issued and outstanding.

During the three and nine months ended September 30, 2020, the Company recorded $0.4 million and $1.3 million (2019 - $0.2 million and $0.9 million), respectively, of expenses related to restricted stock units and stock options in general and administrative expenses. During the nine months ended September 30, 2020, a total of 78.3 thousand restricted stock units (2019 - 53.8 thousand) with a market value of $1.3 million (2019 - $0.5 million) vested and were paid to the grantees by issuing 44.8 thousand shares (2019 - 34.1 thousand shares) of Class A common stock, net of withholding taxes.

14

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

13. Related Party Transactions

Management Fee - Related and Other

a.The Company's operations are conducted in part by its subsidiaries, which receive services from Teekay's wholly-owned subsidiary, Teekay Shipping Ltd. (or the Manager) and its affiliates. The Manager provides various services under a long-term management agreement (the Management Agreement). Commencing October 1, 2018, the Company elected to receive vessel management services for its owned and leased vessels (other than certain former Tanker Investments Ltd. (or TIL) vessels, which are technically managed by a third party) from its wholly-owned subsidiaries and no longer contracts these services from the Manager.

b.Amounts received and (paid) by the Company for related party transactions for the periods indicated were as follows:

| Three Months Ended | Nine Months Ended | ||||||||||||||||

| September 30, 2020 | September 30, 2019 | September 30, 2020 | September 30, 2019 | ||||||||||||||

| $ | $ | $ | $ | ||||||||||||||

Vessel operating expenses - technical management fee (i) | ( | ( | |||||||||||||||

Strategic and administrative service fees (ii) | ( | ( | ( | ( | |||||||||||||

Secondment fees (iii) | ( | ( | ( | ( | |||||||||||||

LNG service revenues (iv) | ( | ||||||||||||||||

Technical management fee revenue (v) | |||||||||||||||||

Service revenues (vi) | |||||||||||||||||

(i)The cost of ship management services provided by a third party has been presented as vessel operating expenses on the Company's unaudited consolidated statements of (loss) income. The Company paid such third party technical management fees to the Manager in relation to certain former TIL vessels.

(ii)The Manager’s strategic and administrative service fees have been presented in general and administrative expenses, except for fees related to technical management services, which have been presented in vessel operating expenses on the Company’s unaudited consolidated statements of (loss) income. The Company’s executive officers are employees of Teekay or subsidiaries thereof, and their compensation (other than any awards under the Company’s long-term incentive plan) is set and paid by Teekay or such other subsidiaries. The Company compensates Teekay for time spent by its executive officers on the Company’s management matters through the strategic portion of the management fee.

(iii)The Company pays secondment fees for services provided by some employees of Teekay. Secondment fees have been presented in general and administrative expenses, except for fees related to technical management services, which have been presented in vessel operating expenses on the Company's unaudited consolidated statements of (loss) income.

(iv)In November 2016, the Company's ship-to-ship transfer business signed an operational and maintenance subcontract with Teekay LNG Bahrain Operations L.L.C., an entity wholly-owned by Teekay LNG Partners L.P., for the Bahrain LNG Import Terminal. The terminal is owned by Bahrain LNG W.I.L., a joint venture for which Teekay LNG Operating L.L.C., an entity wholly-owned by Teekay LNG Partners L.P., has a 30 % interest. The sub-contract ended in April 2019.

(v)The Company receives reimbursements from Teekay for the provision of technical management services. These reimbursements have been presented in general and administrative expenses on the Company's unaudited consolidated statements of (loss) income.

c.The Manager and other subsidiaries of Teekay collect revenues and remit payments for expenses incurred by the Company’s vessels. Such amounts, which are presented on the Company’s unaudited consolidated balance sheets in "due from affiliates" or "due to affiliates," as applicable, are without interest or stated terms of repayment. In addition, $12.2 million and $7.9 million were payable as crewing and manning costs as at September 30, 2020 and December 31, 2019, respectively, and such amounts are included in accrued liabilities in the unaudited consolidated balance sheets. These crewing and manning costs will be payable as reimbursement to the Manager once they are paid by the Manager to the vessels' crew.

d.In October 2018, the Company established a new RSA structure under TTCL and subsequently began transitioning the Company's RSA activities from TTOL to TTCL. Pursuant to a service agreement with the Teekay Aframax RSA prior to the change in structure, from time to time, the Company hired vessels to perform full service lightering services. During the three and nine months ended September 30, 2019, the Company recognized nil and $2.0 million, respectively, related to vessels that were chartered-in from the RSA to assist with full service lightering operations. These amounts have been presented in voyage expenses on the Company's unaudited consolidated statements of (loss) income.

15

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

14. (Loss) Earnings Per Share

The net (loss) earnings available for common shareholders and (loss) earnings per common share are presented in the table below:

| Three Months Ended | Nine Months Ended | ||||||||||||||||||||||

| September 30, 2020 | September 30, 2019 | September 30, 2020 | September 30, 2019 | ||||||||||||||||||||

| $ | $ | ||||||||||||||||||||||

| Net (loss) income | ( | ( | ( | ||||||||||||||||||||

| Weighted average number of common shares - basic | |||||||||||||||||||||||

| Dilutive effect of stock-based awards | |||||||||||||||||||||||

| Weighted average number of common shares - diluted | |||||||||||||||||||||||

| (Loss) earnings per common share: | |||||||||||||||||||||||

| – Basic | ( | ( | ( | ||||||||||||||||||||

| – Diluted | ( | ( | ( | ||||||||||||||||||||

Stock-based awards that have an anti-dilutive effect on the calculation of diluted earnings per common share are excluded from this calculation. In the periods where a loss attributable to shareholders has been incurred, all stock-based awards are anti-dilutive. For the three and nine months ended September 30, 2020, 0.2 million and 0.1 million restricted stock units, respectively, had anti-dilutive effects on the calculation of diluted earnings per common share. For the three and nine months ended September 30, 2020, options to acquire 0.2

15. Write-down and Sale of Assets

During the three and nine months ended September 30, 2020, the carrying values of five 43.5

During the three and nine months ended September 30, 2020, the Company recorded write-downs of $1.4 million and $2.1 million, respectively, on its operating lease right-of-use assets, which were written-down to their estimated fair value, based on prevailing charter rates for comparable periods, due to a reduction in these charter rates.

The Company's unaudited consolidated statements of (loss) income for the nine months ended September 30, 2020 includes a gain of $3.1 million relating to the completion of the sale of the non-US portion of its ship-to-ship support services business, as well as its LNG terminal management business for proceeds of $27.1 million, including an adjustment of $1.1 million for the final amounts of cash and other working capital present on the closing date. Of the total proceeds, $14.3 million was received in May 2020 and the remaining $12.7 million was received in July 2020.

During the nine months ended September 30, 2020, the Company completed the sale of three Suezmax tankers, two of which were classified as held for sale on the Company's unaudited consolidated balance sheet as at December 31, 2019, with an aggregate loss on sales of $2.6 million.

16

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

16. Supplemental Cash Flow Information

Total cash, cash equivalents and restricted cash, including cash, cash equivalents and restricted cash held for sale are as follows:

| As at | As at | As at | As at | ||||||||||||||||||||

| September 30, 2020 | December 31, 2019 | September 30, 2019 | December 31, 2018 | ||||||||||||||||||||

$ | $ | $ | $ | ||||||||||||||||||||

Cash and cash equivalents | |||||||||||||||||||||||

Restricted cash – current | |||||||||||||||||||||||

Restricted cash – long-term | |||||||||||||||||||||||

| Cash and cash equivalents held for sale | |||||||||||||||||||||||

| Restricted cash held for sale - current | |||||||||||||||||||||||

The Company maintains restricted cash deposits relating to certain FFAs (note 8) and leasing arrangements (note 7).

Non-cash items related to operating lease right-of-use assets and operating lease liabilities are as follows:

| For the nine months ended | |||||||||||||||||||||||

| September 30, 2020 | September 30, 2019 | ||||||||||||||||||||||

| $ | $ | ||||||||||||||||||||||

| Leased assets obtained in exchange for new operating lease liabilities | |||||||||||||||||||||||

17. Restructuring Charge

During the three and nine months ended September 30, 2020, the Company recognized restructuring charges of $1.4

As at September 30, 2020 and December 31, 2019, restructuring liabilities of $1.4 million and nil , respectively, were recognized in accrued liabilities on the unaudited consolidated balance sheets.

18. Liquidity

Based on the Company's liquidity as at the date these unaudited consolidated financial statements were issued, and from the expected cash flows from Company's operations over the following year, the Company estimates that it will have sufficient liquidity to continue as a going concern for at least a one-year period following the issuance of these unaudited consolidated financial statements.

19. Subsequent Events

On October 19 and 22, 2020, the Company completed the purchases of two Aframax tankers previously under the sale-leaseback arrangement described in note 7 for a total cost of $29.6 million, using available cash.

On November 13, 2020, the Company declared purchase options to acquire two Suezmax tankers for a total cost of $56.7 million, as part of the repurchase options under the sale-leaseback arrangements described in note 7. The Company expects to complete the purchase and delivery of these vessels in May 2021.

17

TEEKAY TANKERS LTD. AND SUBSIDIARIES

September 30, 2020

PART I - FINANCIAL INFORMATION

ITEM 2 – MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations should be read in conjunction with the unaudited consolidated financial statements and accompanying notes contained in Item 1 – Financial Statements of this Report on Form 6-K and with our audited consolidated financial statements contained in Item 18 – Financial Statements and Management’s Discussion and Analysis of Financial Condition and Results of Operations in Item 5 – Operating and Financial Review and Prospects of our Annual Report on Form 20-F for the year ended December 31, 2019.

OVERVIEW

Our business is to own and operate crude oil and product tankers, and we employ a chartering strategy that seeks to capture upside opportunities in the tanker spot market while using fixed-rate time charters to reduce potential downside risks. As an adjacency to these core competencies, we also provide full service lightering (or FSL) services. In early 2020, we entered into an agreement to sell the non-US portion of our ship-to-ship (or STS) business, and our LNG terminal management business, as described below, which sale closed on April 30, 2020. As at September 30, 2020, our fleet consisted of 60 vessels, including seven in-chartered vessels, and one 50%-owned Very Large Crude Carrier (or VLCC). The following table summarizes our fleet as at September 30, 2020:

| Owned and Leased Vessels | Chartered-in Vessels | Total | |||||||||

| Fixed-rate: | |||||||||||

| Suezmax Tankers | 8 | — | 8 | ||||||||

| Aframax Tankers | 2 | — | 2 | ||||||||

LR2 Product Tanker (1) | 1 | — | 1 | ||||||||

Total Fixed-Rate Fleet (2) | 11 | — | 11 | ||||||||

| Spot-rate: | |||||||||||

| Suezmax Tankers | 18 | — | 18 | ||||||||

Aframax Tankers (3) | 15 | 2 | 17 | ||||||||

LR2 Product Tankers (1)(3) | 8 | 2 | 10 | ||||||||

VLCC Tanker (4) | 1 | — | 1 | ||||||||

Total Spot Fleet (5) | 42 | 4 | 46 | ||||||||

| STS Support Vessels | — | 3 | 3 | ||||||||

| Total Teekay Tankers Fleet | 53 | 7 | 60 | ||||||||

1.Long Range 2 (or LR2) product tankers.

2. Three charter-out contracts are scheduled to expire in 2020, six charter-out contracts are scheduled to expire in 2021 and two charter-out contracts are scheduled to expire in 2022.

3. One Aframax tanker is currently time-chartered in for a period of 60 months expiring in 2021, one Aframax tanker is currently time-chartered in for a period of 24 months expiring in 2021 with an option to extend for one year, and two LR2 tankers are currently time-chartered in for periods of 24 months expiring in 2021, each with an option to extend for one year.

4. VLCC owned through a 50/50 joint venture. As at September 30, 2020, the VLCC was trading on spot voyage charters in a pooling arrangement managed by a third party.

5. As at September 30, 2020, a total of 37 of our owned, leased and chartered-in vessels, as well as 18 vessels not in our fleet owned by third parties, were subject to revenue sharing agreements (or RSAs).

18

ITEMS YOU SHOULD CONSIDER WHEN EVALUATING OUR RESULTS

There are a number of factors that should be considered when evaluating our historical financial performance and assessing our future prospects, and we use a variety of financial and operational terms and concepts when analyzing our results of operations. These items can be found in "Item 5 – Operating and Financial Review and Prospects" in our Annual Report on Form 20-F for the year ended December 31, 2019.

SIGNIFICANT DEVELOPMENTS IN 2020

Novel Coronavirus (COVID-19) Pandemic

The novel coronavirus pandemic is dynamic, and its ultimate scope, duration and effects on us, our customers and suppliers and our industry are uncertain.

COVID-19 has resulted and may continue to result in a significant decline in global demand for oil. As our business includes the transportation of crude oil and refined petroleum products on behalf of our customers, any significant decrease in demand for the cargo we transport could adversely affect demand for our vessels and services.

For the nine months ended September 30, 2020, we did not experience any material business interruptions as a result of the COVID-19 pandemic. COVID-19 has been a contributing factor to the decline in spot tanker rates and short-term time charter rates since mid-May 2020 and has also increased certain crewing-related costs, which has had an impact on our cash flows, and was a contributing factor to the write-down of certain tankers as described in "Item 1 - Financial Statements: Note 15 - Write-down and Loss on Sale of Assets" and the reduction of certain tax accruals as described in "Item 1 - Financial Statements: Note 10 - Income Tax (Expense) Recovery" of this report. We are continuing to monitor the potential impact of the pandemic on us, including monitoring counterparty risk associated with our vessels under contract, and monitoring the impact on vessel impairment and have introduced a number of measures to protect the health and safety of our crews on our vessels, as well as our onshore staff.

Effects of the current pandemic may include, among others: deterioration of worldwide, regional or national economic conditions and activity and of demand for oil, including due to a potential slowdown in oil demand due to a current resurgence of COVID-19 cases in many regions and the potential for renewed restrictions and lockdowns over the winter months; operational disruptions to us or our customers due to worker health risks and the effects of new regulations, directives or practices implemented in response to the pandemic (such as travel restrictions for individuals and vessels and quarantining and physical distancing); potential delays in (a) the loading and discharging of cargo on or from our vessels, (b) vessel inspections and related certifications by class societies, customers or government agencies, (c) maintenance, modifications or repairs to, or dry docking of, our existing vessels due to worker health or other business disruptions, and (d) the timing of crew changes; reduced cash flow and financial condition, including potential liquidity constraints; potential reduced access to capital as a result of any credit tightening generally or due to continued declines in global financial markets; potential reduced ability to opportunistically sell any of our vessels on the second-hand market, either as a result of a lack of buyers or a general decline in the value of second-hand vessels; potential decreases in the market values of our vessels and any related impairment charges or breaches relating to vessel-to-loan financial covenants; and potential deterioration in the financial condition and prospects of our customers or business partners.

Given the dynamic nature of the pandemic, the duration of any potential business disruption and the related financial impact cannot be reasonably estimated at this time and could materially affect our business, results of operations and financial condition. Please read “Item 3 - Key Information - Risk Factors” in our Annual Report on Form 20-F for the year ended December 31, 2019 for additional information about the potential risks of COVID-19 on our business.

IMO 2020 Low Sulfur Fuel Regulation

Effective January 1, 2020, the International Maritime Organization (or IMO) imposed a 0.50% m/m (mass by mass), global limit for sulfur in fuel oil used on board ships. To comply with this new regulatory standard, ships may utilize different fuels containing low or zero sulfur or utilize exhaust gas cleaning systems, known as “scrubbers”. We have taken, and continue to take, steps to comply with the 2020 sulfur limit. Detailed plans to address this changeover were prepared and have been successfully implemented. At present, we have not installed any scrubbers on our fleet. We have transitioned to burning compliant low sulfur fuel from January 1, 2020. The initial transition to low sulfur fuel did not have a significant impact on our operating results. The future fuel price spread between high sulfur fuel and low sulfur fuel is uncertain; however, the use of compliant low sulfur fuel is anticipated to result in an increase in voyage expenses. We expect that we will be able to recover fuel price increases from the charterers of our vessels through higher revenues from voyage charters.

Sale of Non-US Ship-to-Ship Business

In January 2020, we reached an agreement to sell the non-US portion of our STS business, as well as our LNG terminal management business for approximately $27.1 million, including an adjustment for the final amounts of cash and other working capital present on the closing date. The sale closed on April 30, 2020, resulting in a gain on sale of approximately $3.1 million. Of the total proceeds, $14.3 million was received in May 2020 and the remaining $12.7 million was received in July 2020.

19

New Loan Facilities

In January 2020, we entered into a new $532.8 million long-term revolving credit facility to refinance 31 vessels which is scheduled to mature at the end of 2024. The proceeds from the new debt facility, which was drawn down in February 2020, were used to repay a portion of the $455 million then outstanding under our prior two revolving facilities, which were scheduled to mature in 2021 and 2022, and two term loan facilities, which were scheduled to mature in 2020 and 2021.

In August 2020, we entered into a new $67.4 million term loan debt facility to refinance four vessels, which is scheduled to mature in 2023. The proceeds were used to repay a portion of the $85.1 million then outstanding under one previous term loan facility, which was scheduled to mature in 2021. Following completion of the refinancing, Teekay no longer guarantees any of our debt facilities.

Vessel Purchases

On October 19 and 22, 2020, we completed the purchases of two Aframax tankers previously under the sale-leaseback arrangements described in "Item 1 - Financial Statements: Note 7 - Operating Leases and Obligations Related to Finance Leases" of this report, for a total cost of $29.6 million, using available cash.

On November 13, 2020, we declared purchase options to acquire two Suezmax tankers for a total cost of $56.7 million, as part of the repurchase options under the sale-leaseback arrangements described in "Item 1 - Financial Statements: Note 7 - Operating Leases and Obligations Related to Finance Leases" of this report. We expect to complete the purchase and delivery of these vessels in May 2021.

Vessel Sales

During the first quarter of 2020, we completed the sale of three Suezmax tankers in separate transactions for a combined sales price of approximately $60.9 million. Two Suezmax tankers were delivered in February 2020, and one Suezmax tanker was delivered in March 2020.

Time Chartered-out Vessels

Between March and May 2020, we entered into time charter-out contracts for five Suezmax tankers and one LR2 tanker with one-year terms at average daily rates of $45,600 and $29,000 respectively, and two Aframax tankers with one to two-year terms at an average daily rate of $25,600. All charter-out contracts commenced between April and June 2020.

In September 2020, we entered into a time charter-out contract for one Aframax tanker with a one-year term at a daily rate of $18,700. This charter-out contract commenced in October 2020.

20

RESULTS OF OPERATIONS

There are a number of factors that should be considered when evaluating our historical financial performance and assessing our future prospects, and we use a variety of financial and operational terms and concepts when analyzing our results of operations. These can be found in "Item 5 – Operating and Financial Review and Prospects" in our Annual Report on Form 20-F for the year ended December 31, 2019.

In accordance with GAAP, we report gross revenues in our unaudited consolidated statements of (loss) income and include voyage expenses among our operating expenses. However, ship-owners base economic decisions regarding the employment of their vessels upon anticipated “time-charter equivalent” (or TCE) rates, which represent net revenues (or revenue less voyage expenses) divided by revenue days, and industry analysts typically measure bulk shipping freight rates in terms of TCE rates. This is because under time charter-out contracts the customer usually pays the voyage expenses, while under voyage charters the ship-owner usually pays the voyage expenses, which typically are added to the hire rate at an approximate cost. Accordingly, the discussion of revenue below focuses on net revenues and TCE rates (both of which are non-GAAP financial measures) where applicable.

Summary

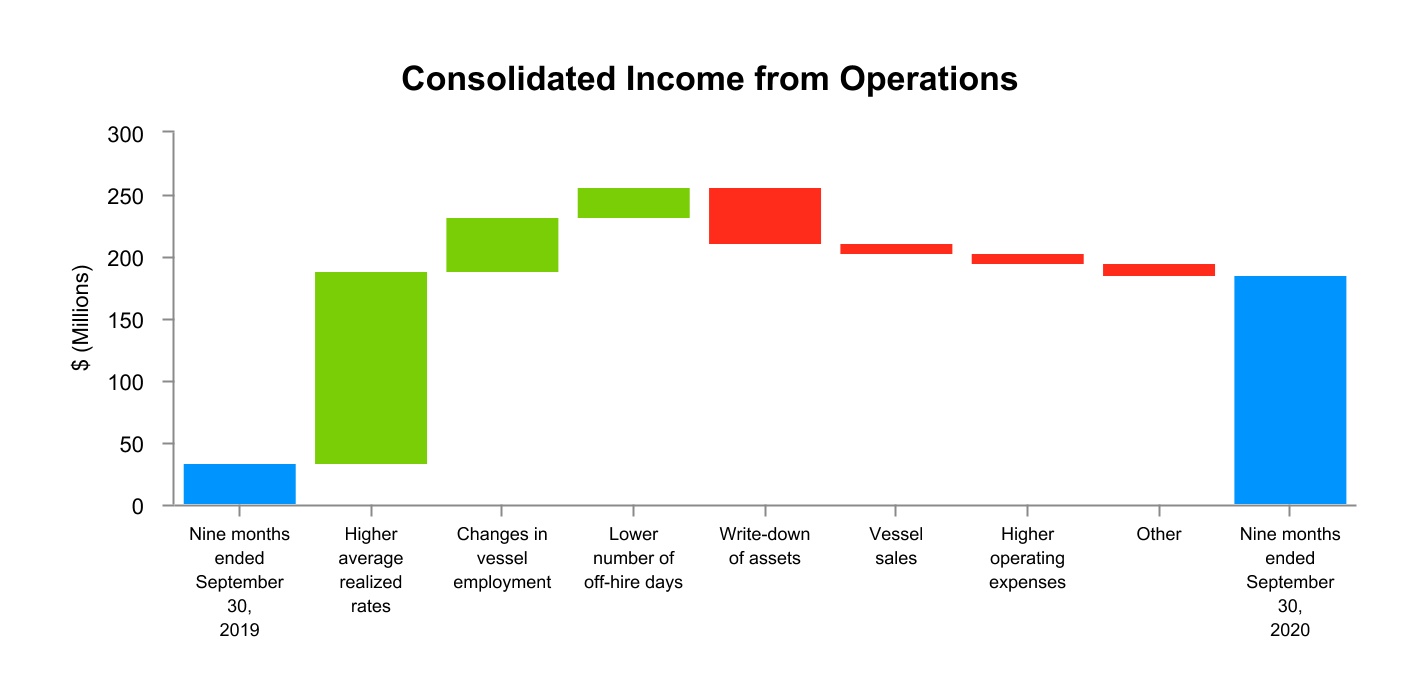

Our consolidated income from vessel operations increased to $183.9 million for the nine months ended September 30, 2020, compared to $32.3 million in the same period last year. The primary reasons for this increase are as follows:

•an increase of $154.9 million due to higher overall average realized spot TCE rates earned by our Suezmax tankers, Aframax tankers and LR2 product tankers, higher earnings from our FSL dedicated vessels, as well as a higher extension rate from one time-charter out contract;

•a net increase of $43.5 million due to a higher number of vessels on time-charter out contracts earning higher rates compared to spot rates for the first three quarters of 2019, partially offset by early exit fees related to our vessels leaving the RSAs to commence time-charter out contracts in the second quarter of 2020; and

•an increase of $24.3 million due to fewer off-hire days related to dry dockings and off-hire bunker expenses compared to the same period in the prior year;

partially offset by

•a decrease of $45.6 million due to the impairment of five Aframax tankers and four right-of-use assets due to the lower near-term tanker market outlook, a reduction of charter rates as a result of the current economic environment, and lower vessel values;

•a decrease of $8.5 million due to the sale of one Suezmax tanker in the fourth quarter of 2019 and three Suezmax tankers in the first quarter of 2020; and

•a decrease of $8.0 million primarily due to increased crewing related costs resulting from the COVID-19 global pandemic, a higher amount of repair and maintenance activities, and higher insurance premiums.

21

On April 30, 2020, we completed the sale of the non-US portion of our STS support services business, as well as our LNG terminal management business. Following this sale, we have only one reportable segment. For periods prior to the sale, we managed our business and analyzed and reported our results of operations on the basis of two reportable segments: the tanker segment and the STS transfer segment. The segment information for all periods has been adjusted to be consistent with the segment presentation after the sale. Please read “Item 1 - Financial Statements: Note 4 - Segment Reporting” of this report.

Details of the changes to our results of operations for each of our segments for the three and nine months ended September 30, 2020, compared to the three and nine months ended September 30, 2019 are provided below.

Three and Nine Months Ended September 30, 2020 versus Three and Nine Months Ended September 30, 2019

Tanker Segment

Our tanker segment consists of crude oil and product tankers that (i) are subject to long-term, fixed-rate time-charter contracts (which have an original term of one year or more), (ii) operate in the spot tanker market, or (iii) are subject to time-charters that are priced on a spot market basis or are short-term, fixed-rate contracts (which have original terms of less than one year), including those employed on FSL contracts. In addition, our tanker segment also includes our US based STS support services.

The following table presents the operating results of our tanker segment for the three and nine months ended September 30, 2020 and 2019, and compares net revenues, a non-GAAP financial measure, for those periods to revenues, the most directly comparable GAAP financial measure:

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||||||||||||||

| (in thousands of U.S. Dollars, except percentage changes) | 2020 | 2019 | % Change | 2020 | 2019 | % Change | |||||||||||||||||||||||||||||

| Revenues | 170,240 | 182,429 | (6.7)% | 751,640 | 608,815 | 23.5% | |||||||||||||||||||||||||||||

| Less: Voyage expenses | (57,777) | (92,866) | (37.8)% | (238,576) | (293,263) | (18.6)% | |||||||||||||||||||||||||||||

| Net revenues | 112,463 | 89,563 | 25.6% | 513,064 | 315,552 | 62.6% | |||||||||||||||||||||||||||||

| Vessel operating expenses | (46,336) | (44,322) | 4.5% | (137,263) | (137,461) | (0.1)% | |||||||||||||||||||||||||||||

| Time-charter hire expenses | (9,070) | (10,637) | (14.7)% | (28,245) | (30,877) | (8.5)% | |||||||||||||||||||||||||||||