Table of Contents

Filed Pursuant to Rule 424(b)(4)

Registration No. 333-213334

6,000,000 Shares

Class A Common Stock

This is an initial public offering of shares of Class A common stock of Apptio, Inc.

Following this offering, we will have two classes of authorized common stock, Class A common stock and Class B common stock. All shares of our capital stock outstanding prior to this offering will convert into shares of our Class B common stock. The rights of the holders of Class A common stock and Class B common stock will be identical, except with respect to voting and conversion rights. Each share of Class A common stock will be entitled to one vote per share. Each share of Class B common stock will be entitled to ten votes per share and is convertible into one share of Class A common stock. Outstanding shares of Class B common stock will represent approximately 98% of the voting power of our outstanding capital stock immediately following the closing of this offering.

Prior to this offering, there has been no public market for the Class A common stock. The initial public offering price per share is $16.00. Our Class A common stock has been approved for listing on The NASDAQ Global Market under the symbol “APTI.”

We are an “emerging growth company” as defined under the federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements for this and future filings.

Investing in our Class A common stock involves risks. See the section of this prospectus captioned “Risk Factors” beginning on page 14 to read about factors you should consider before buying shares of the Class A common stock.

Neither the Securities and Exchange Commission nor any regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

| Initial public offering price |

$ | 16.00 | $ | 96,000,000 | ||||

| Underwriting discount |

$ | 1.12 | $ | 6,720,000 | ||||

| Proceeds, before expenses, to us |

$ | 14.88 | $ | 89,280,000 | ||||

To the extent that the underwriters sell more than 6,000,000 shares of Class A common stock, the underwriters have the option to purchase up to an additional 900,000 shares from us at the initial public offering price less the underwriting discount.

The underwriters expect to deliver the shares against payment in New York, New York on September 28, 2016.

| Goldman, Sachs & Co. | J.P. Morgan | BofA Merrill Lynch |

| Barclays | Jefferies | RBC Capital Markets | Pacific Crest Securities a division of KeyBanc Capital Markets |

Prospectus dated September 22, 2016

Table of Contents

Table of Contents

| Page |

| 1 |

| 14 |

| 44 |

| 46 |

| 47 |

| 48 |

| 50 |

| 52 |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

55 |

| 87 |

| 106 |

| 115 |

| 130 |

| 134 |

| 137 |

| 144 |

| MATERIAL U.S. FEDERAL INCOME AND ESTATE TAX CONSEQUENCES TO NON-U.S. HOLDERS OF CLASS A COMMON STOCK |

147 |

| 151 |

| 156 |

| 156 |

| 156 |

| F-1 |

Through and including October 17, 2016 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

We have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date.

-i-

Table of Contents

This summary highlights selected information contained elsewhere in this prospectus and is qualified in its entirety by the more detailed information and financial statements included elsewhere in this prospectus. It does not contain all of the information that may be important to you and your investment decision. You should carefully read this entire prospectus, including the matters set forth under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and related notes.

Overview

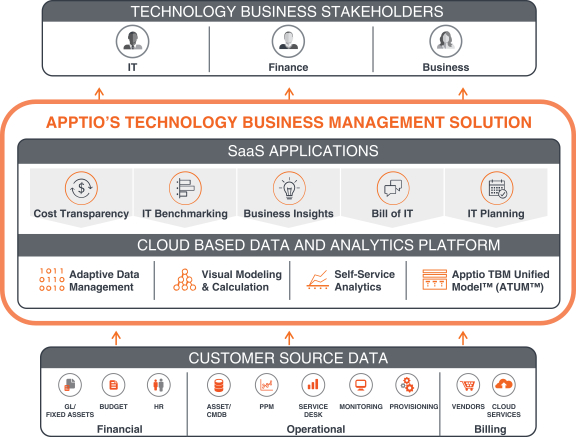

We are the leading provider of Technology Business Management, or TBM, solutions. We pioneered the TBM software category to provide the strategic business management system for the CIO because IT needed a data-driven system comparable to those leveraged by other enterprise functions such as sales, human resources and finance. Our cloud-based platform and SaaS applications enable IT leaders to analyze, optimize and plan technology investments, and to benchmark their financial and operational performance against peers. We empower IT leaders to transform IT into a service provider, to navigate the cloud transition, and to shift technology resources to drive more business innovation.

Our TBM solutions consist of a powerful, cloud-based platform and a suite of SaaS applications: Cost Transparency, IT Benchmarking, Business Insights, Bill of IT and IT Planning. Our data and analytics platform leverages proprietary modeling capabilities, powerful self-service analytics and planning workflows to enable customers to make actionable, data-driven strategic and operational decisions. Our platform automatically aggregates, cleanses and establishes relationships across large amounts of customer data from disparate sources and maps the data into our standard IT operating model. Our solutions are the business system of record for our customers’ IT organizations.

Our growing customer base, which includes over 40% of the FORTUNE 100, spans a broad spectrum of industries, including financial services, professional services, technology, energy, consumer goods, manufacturing, healthcare, media, retail and transportation, as well as federal and state government agencies. We offer our solutions on a subscription basis, with subscription fees based on spend managed by our applications and the number of applications or capabilities for which the customer has subscribed. Our customers’ annual IT spend ranges from less than $10 million to billions of dollars.

We formed the Technology Business Management Council, or TBM Council, as a separate non-profit entity in 2012 to foster the growth of the TBM category. The TBM Council has become the leading community for CIOs, IT professionals and IT finance professionals dedicated to advancing the discipline of managing the business of IT, with over 2,900 members. This community establishes industry-endorsed best practices for TBM and helps create a powerful network effect for TBM solutions.

We had total revenue of $73.8 million, $106.6 million and $129.3 million in 2013, 2014 and 2015, respectively, reflecting a year-over-year increase of 45% and 21% in 2014 and 2015, respectively. For 2013, 2014 and 2015, our net losses were $23.7 million, $32.9 million and $41.0 million, respectively, as we focused on growing our business.

-1-

Table of Contents

Industry Background

Digitalization of business processes has increasingly made technology a strategic priority for enterprises of all sizes and across industries. Rapid innovation in technology, particularly the emergence of cloud computing, is simultaneously increasing the complexity of technology decision making and fundamentally transforming the way IT services are delivered. To gain and maintain a competitive advantage, IT leaders must focus more time and resources on transforming their IT business, and less time managing legacy infrastructure and applications.

In today’s world, IT professionals must not only measure and manage traditional infrastructure, but also a wide array of modern IT options, such as cloud computing and IT purchased directly by business units. IT leaders are faced with the need to evaluate hybrid approaches to IT, using a mixture of public cloud, private cloud and owned infrastructure solutions in order to best suit their application, workload and business needs.

The challenge with traditional approaches to managing IT is that technology and business leaders do not always have the data and analytics to understand how technology spending and services align to business priorities. The IT function has historically lacked the insight into costs, capacity, and utilization necessary to make data-driven decisions. However, business and IT leaders desire the ability to make fast decisions, drive innovation and adopt new technology to drive better business results, while also demanding better control, cost management and asset utilization. In order to be aligned on objectives, business and IT leaders need data and analytical solutions to drive optimal business results. The benefits the cloud provides in agility and cost are driving greater urgency by IT leaders to adopt solutions enabling them to understand their existing infrastructure and make decisions on how their infrastructure needs evolve as part of an ongoing transition.

Given these factors, we believe that there is significant pent up demand for a single system of record to manage the business of IT.

Our Opportunity

We believe the total addressable market for TBM solutions is large and largely unpenetrated. The total addressable market for our solutions is driven by global IT spend, which Gartner, an independent technology industry and market research firm, expects to be $2.7 trillion in 2016, which is the sum of all enterprise IT spending by vertical industry market worldwide.1 Subscription fees for our applications are based primarily on the customer’s annual costs being managed by our applications and the number of applications or capabilities for which the customer has subscribed. We typically sell a subset of the five applications we offer so that customers can realize a rapid time to value from a targeted implementation, and seek to sell additional applications over time. Assuming full deployment of all of our current applications, subscription fees typically range from 0.1% to 0.5% of a customer’s annual IT spend. With a reasonable expectation of our ability to penetrate the market, we believe that the current total addressable market for our existing TBM solutions is approximately $6 billion.

We also believe that, with the development of additional capabilities and applications, our platform can be extended to other areas of customers’ businesses. In fact, our solutions are currently deployed by several customers to address a variety of non-IT, enterprise business management use cases in shared services such as legal, human resources and facilities and for analyzing operational

| 1 | See Gartner note (1) in the section of this prospectus captioned “Special Note Regarding Forward Looking Statements.” |

-2-

Table of Contents

metrics, and we believe that enterprise business management use cases such as these represent future market opportunities. If we are successful in our strategy of developing and selling additional applications beyond our current offerings, we believe that our market opportunity will expand.

Our Technology Business Management Solutions

We provide the business system of record used by our customers’ IT organizations to analyze, optimize and plan investments, and benchmark their financial and operational performance against peers. Our TBM solutions consist of a powerful, cloud-based platform and a suite of SaaS applications that empower IT leaders to understand, communicate and transform IT to drive greater value from technology investments.

Key elements of our solutions include:

| • | Adaptive Data Management. Our purpose-built, cloud-based data and analytics platform aggregates, cleanses and correlates large amounts of customer data from a wide variety of disparate sources. Our typical customer starts with a handful of data sources and has the option to integrate data from hundreds of sources ranging from general ledger data, human resources data, billing data, and service management and other operational data. |

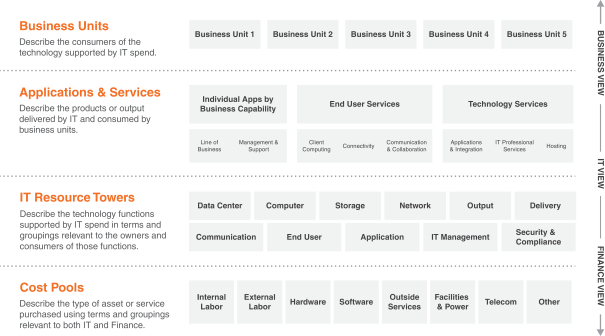

| • | Standard IT Operating Model and Taxonomy. Our platform is underpinned by a flexible framework that provides a standard model for how IT costs are captured, categorized and allocated to IT services and business services. |

| • | Visual Modeling and Powerful Calculation Engine. Our visual modeling capabilities allow users to intuitively build and manage the financial and operational model of their IT organization. |

| • | Intuitive, Self-Service Analytics. Our analytics interface is powerful, yet easy to use by a broad range of IT and business users. |

| • | Modular Applications. Our platform currently includes five SaaS applications that can be deployed in a modular fashion: Cost Transparency, IT Benchmarking, Business Insights, Bill of IT and IT Planning. |

Our platform provides the following benefits:

| • | Increase the Value of IT. Our solutions deliver transparency and actionable insights to IT leaders, enabling them to manage IT in the context of the business. As a result, our solutions enable IT leaders to change their IT organizations from a reactive cost center to a proactive service provider and increase the return on business investments through initiatives such as application rationalization and infrastructure optimization. |

| • | Understand and Communicate IT Costs. Our solutions provide IT and business leaders with a business system of record that gives a comprehensive, transparent and up-to-date view of the costs of IT services associated with specific business functions and services. With this insight, IT leaders can work with business leaders to evaluate different IT options, such as cloud versus owned infrastructure and custom-built or purchased versus SaaS applications, and make better, data-driven decisions. |

-3-

Table of Contents

| • | Optimize IT Investments to Drive Better Business Results. Our solutions enable IT professionals to more efficiently manage existing IT investments and focus incremental effort and spend on innovating and expanding technology investments where they can drive the most value for the business. In addition, our solutions, with their dynamic analytics, key performance indicators, and benchmarking capabilities, allow professionals to optimize investments on an ongoing basis, unlike initiatives based on the advice of consultants or internally developed legacy business processes held together by spreadsheets. |

| • | Plan IT Investments. IT professionals can collaborate with the business to understand their demand for IT services, and then plan efficiently and predictably to meet these demands. |

| • | Transform IT into a Service Provider. Our solutions enable IT to be delivered as a service regardless of whether it is provided by internal resources, cloud providers or other external service providers. Using our solutions, IT leaders can provide transparency into total and unit costs of alternatives and are able to correlate costs to expected value. This empowers business leaders with real, data-driven choices to better align IT and business objectives. |

Our Competitive Strengths

The following strengths are key to our success:

| • | TBM Category Creation and Thought Leadership. We pioneered the TBM category and are its market and thought leader. We believe our efforts and position at the center of the TBM ecosystem allow us to benefit from a network effect, accelerating market adoption of TBM solutions and customer acquisition. |

| • | High Profile Reference Accounts and CIO Engagement. We currently have over 325 customers across various industries, with over 40% of the FORTUNE 100 using our solutions. Our high profile customers and CIO engagement leads to enhanced credibility and better lead generation and conversion. |

| • | Deep IT Business Process Expertise. We have a deep and unique understanding of the role of IT, IT business processes and how IT can maximize business value. We embed this expertise into our purpose-built solutions and these efforts allow us to deliver a compelling value proposition to customers. |

| • | Unique Data Set. We have built a large and unique aggregated data set of customer IT spend across a spectrum of industries, geography and amount of spend. We believe that this data set is the most extensive, granular and up-to-date data set of its kind. This allows us to deliver solutions that provide unique benchmarking capabilities. As our customer base continues to grow, our data set will become deeper and richer, increasing its value. |

| • | Unbiased Approach. Our focus on TBM allows us to provide customers an unbiased assessment of IT solutions offered by providers of infrastructure, applications and services. We believe this has led to deep customer trust. Customers need not be concerned that we have a competing agenda and seek to drive technology decisions that will benefit us economically. |

-4-

Table of Contents

| • | Proven, Enterprise Class Cloud-Based Platform. Our solutions are cloud-based, allowing us to provide enterprise-class software solutions that are regularly updated and highly scalable to customers around the globe. |

Our Growth Strategy

We are pursuing the following strategies to grow our business:

| • | Expand Our Customer Base. We believe the market for TBM solutions is large, growing and under-penetrated. We intend to leverage our strong brand, leadership position, high-profile customer base from a wide range of industries and experienced sales team to target customers with a wide range of IT spend and across industries. |

| • | Further Maximize Our Existing Customer Base. Many customers initially subscribe for a subset of the applications we offer so they can realize rapid time to value by reducing costs or shifting technology investments to where they will be most productive. We seek to generate additional revenue from customers by selling subscriptions to other existing or newly developed applications and modules, and expanding the use of our solutions to additional business units. |

| • | Continue to Foster the IT Leader Community. We will continue to support the TBM Council and leverage our leadership position in a large and growing IT leader community to increase awareness and adoption of TBM solutions. Our relationship with the TBM Council helps us introduce a growing body of CIOs and other leaders to the advantages of TBM and to our solutions, and continues to create a network effect as members exchange information, ideas and experiences with TBM. |

| • | Continue to Deliver Innovative Products. We have made, and will continue to make, significant investments in product development to enhance the capabilities of our existing applications and expand the number of applications on our extensible platform to address customers’ evolving needs. |

| • | Leverage Our Unique Position to Deliver Valuable Benchmarking Data. Over time, we believe there will be substantial opportunities to leverage our large, unique and growing aggregated data set by embedding data insights in our solutions or by selling data to customers or third parties on a standalone basis. |

| • | Expand Internationally. We have a growing presence in Europe and Australia. We believe that there is significant opportunity for our TBM solutions outside of the United States, and we intend to expand our direct sales force and third-party relationships to further penetrate these and other regions. |

| • | Expand into Enterprise Business Management. Many shared services groups, such as legal, facilities and human resources, face similar challenges to IT in making data-driven decisions and lack a software solution to help them do so. We believe a substantial market exists for enterprise business management outside of the IT organization. |

-5-

Table of Contents

Risks Associated with Our Business

Our business is subject to numerous risks and uncertainties, including those highlighted in the section of this prospectus captioned “Risk Factors” immediately following this prospectus summary. Some of these risks are:

| • | We have a history of losses, our revenue growth rate may decline and we expect our costs to increase. As our costs increase, we may not be able to generate sufficient revenue to achieve or maintain profitability in the future. |

| • | The TBM market is relatively new and increasingly competitive and if the market fails to further develop or we are unable to compete effectively, our business, results of operations, financial condition and growth prospects will be harmed. |

| • | If we fail to acquire new customers, convince our existing customers to adopt our solutions, renew their subscriptions and purchase additional subscriptions, or to adapt our solutions to changing market dynamics and customer preferences, or to achieve increased market acceptance of our TBM solutions, our business, results of operations, financial condition and growth prospects will be harmed. |

| • | We have a limited operating history, which makes it difficult to predict our future operating results. Our quarterly operating results may fluctuate and be unpredictable, and because we recognize revenue from subscriptions ratably over the term of the agreement, near-term changes in sales may not be reflected immediately in our operating results. |

| • | We may not achieve anticipated revenue growth from expanding our sales force or from our development efforts, if at all. |

| • | The market in which we participate is increasingly competitive, and if we do not compete effectively, our operating results could be harmed. |

Corporate Information

We were incorporated in Delaware in October 2007. Our principal executive offices are located at 11100 NE 8th Street, Suite 600, Bellevue, Washington 98004. Our telephone number is (866) 470-0320. Our website address is www.apptio.com. Information contained on, or that can be accessed through, our website does not constitute part of this prospectus and inclusions of our website address in this prospectus are inactive textual references only.

Unless the context indicates otherwise, as used in this prospectus, the terms “Apptio,” “the Company,” “we,” “us” and “our” refer to Apptio, Inc. and its subsidiaries, Apptio Europe Limited, Apptio GmbH, Apptio Nordic ApS, Apptio NL B.V., Apptio Pty Ltd and Apptio Technology Canada Ltd. We use “APPTIO®”, “APPTIO TBM UNIFIED MODEL®”, “ATUM®”, the Dissolving Circle Logo Design and other marks as trademarks in the United States and other countries. This prospectus contains references to our trademarks and to those belonging to other entities. Solely for convenience, trademarks and trade names referred to in this prospectus, including logos, artwork and other visual displays, may appear without the ® or ™ symbols, but such references are not intended to indicate in any way that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names. We do not intend our use or display of other entities’ trade names or trademarks to imply a relationship with, or endorsement or sponsorship of us by, any other entity.

-6-

Table of Contents

Additionally, we are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act, or the JOBS Act, and therefore we may take advantage of certain exemptions from various public company reporting requirements, including not being required to have our internal control over financial reporting audited by our independent registered public accounting firm pursuant to Section 404 of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and any golden parachute payments. In addition, the JOBS Act provides that an “emerging growth company” can delay adopting new or revised accounting standards until such time as those standards apply to private companies. We have elected to avail ourselves of this exemption and, therefore, we will not be subject to the same implementation timing of new or revised accounting standards as other public companies that are not “emerging growth companies” until these standards apply to private companies unless we elect to early adopt as permitted by the relevant guidance for private companies.

-7-

Table of Contents

| Class A common stock offered by us |

6,000,000 shares. |

| Class A common stock to be outstanding after this offering |

6,000,000 shares (or 6,900,000 shares if the underwriters exercise their option to purchase additional shares in full). |

| Class B common stock to be outstanding after this offering |

31,285,839 shares. |

| Total Class A common stock and Class B common stock to be outstanding after this offering |

37,285,839 shares. |

| Option to purchase additional shares of Class A common stock from us |

900,000 shares. |

| Use of proceeds |

We estimate that the net proceeds from the sale of shares of Class A common stock in this offering will be approximately $86.0 million (or approximately $99.4 million if the underwriters exercise their option to purchase additional shares in full), based upon the initial price to public of $16.00 per share, and after deducting underwriting discounts and commissions and estimated offering expenses payable by us. |

We intend to use the net proceeds from this offering to repay $20.2 million principal and pre-payment fees for amounts borrowed under our credit facilities, and the remainder for working capital and other general corporate purposes, including making investments in our sales, marketing, professional services and product development organizations. Additionally, we may choose to expand our current business through acquisitions of or investments in other complementary businesses, technologies, or other assets. However, we currently have no agreements or commitments with respect to any such acquisitions or investments. See the section of this prospectus captioned “Use of Proceeds” for additional information.

| Voting rights |

Shares of Class A common stock are entitled to one vote per share. |

| Shares of Class B common stock are entitled to 10 votes per share. |

| Holders of Class A common stock and Class B common stock will generally vote together as a single class, unless otherwise required by law or our certificate of incorporation. The holders of our outstanding Class B common stock will hold approximately 98% of the voting power of our outstanding capital stock following this offering. Our executive officers and directors and their related parties, which include funds affiliated with Madrona Venture Group and Shasta Ventures, and the other holder of 5% or more of our common stock, will |

-8-

Table of Contents

| collectively beneficially own shares representing 66.2% of the voting power of our outstanding capital stock following this offering. Consequently, the holders of Class B common stock will have the ability to control the outcome of matters submitted to our stockholders for approval, including the election of our directors and the approval of any change in control transaction. See the sections of this prospectus captioned “Principal Stockholders” and “Description of Capital Stock” for additional information. |

| Trading symbol |

“APTI”. |

Prior to the closing of this offering, we had one class of common stock. Upon the closing of this offering, we will have authorized a new class of Class A common stock and a new class of Class B common stock. All currently outstanding shares of common stock and convertible preferred stock (including shares issuable upon the exercise of the warrants described below) will convert into shares of new Class B common stock. In addition, all currently outstanding options to purchase shares of capital stock will become exercisable for shares of new Class B common stock.

The number of shares of common stock to be outstanding following this offering is based on 31,285,839 shares of common stock outstanding as of June 30, 2016, and excludes:

| • | 11,394,824 shares of Class B common stock issuable upon exercise of options outstanding as of June 30, 2016, at a weighted-average exercise price of $9.28 per share; |

| • | 551,548 shares of Class B common stock reserved for future issuance under our 2007 Stock Plan as of June 30, 2016. Our 2007 Stock Plan has been terminated and no further awards will be granted under it; |

| • | 222,920 shares of Class B common stock reserved for future issuance under our 2011 Executive Equity Incentive Plan as of June 30, 2016. Our 2011 Executive Equity Incentive Plan has been terminated and no further awards will be granted under it; |

| • | an aggregate of 4,550,000 shares of Class A common stock reserved for future issuance under our 2016 Equity Incentive Plan and 2016 Employee Stock Purchase Plan, each of which became effective on the business day immediately prior to the date of effectiveness of the registration statement of which this prospectus forms a part; and |

| • | 75,214 shares of Class B common stock issuable upon the exercise of warrants outstanding as of June 30, 2016 at a weighted-average exercise price of $9.52 per share, after conversion of the convertible preferred stock. |

Unless otherwise indicated, other than in our consolidated financial statements, this prospectus reflects and assumes the following:

| • | the reclassification of outstanding common stock into an equivalent number of shares of newly authorized Class B common stock, which will occur immediately prior to the closing of this offering, and the authorization of Class A common stock; |

-9-

Table of Contents

| • | the conversion of all outstanding shares of convertible preferred stock into an aggregate of 18,239,475 shares of Class B common stock immediately prior to the closing of this offering; |

| • | the filing of the certificate of incorporation immediately prior to the closing of this offering; and |

| • | no exercise by the underwriters of their option to purchase up to an additional 900,000 shares of Class A common stock. |

-10-

Table of Contents

Summary Consolidated Financial Data

We derived the following summary consolidated statements of operations data for the years ended December 31, 2014 and 2015 from audited consolidated financial statements appearing elsewhere in this prospectus. We derived the following summary consolidated statement of operations data for the year ended December 31, 2013 from audited consolidated financial statements not included in this prospectus. We derived the following summary consolidated statements of operations data for the six months ended June 30, 2015 and 2016 and the summary consolidated balance sheet data as of June 30, 2016 from unaudited consolidated financial statements appearing elsewhere in this prospectus. In the opinion of management, the unaudited consolidated financial statements reflect all adjustments, which include normal recurring adjustments, necessary for a fair presentation of the financial statements. Historical results are not necessarily indicative of the results that may be expected in the future and the results for the six months ended June 30, 2016 are not necessarily indicative of the results that may be expected for the full year or any other period. The summary financial data set forth below should be read together with the financial statements and the related notes to those statements, as well as the sections of this prospectus captioned “Selected Consolidated Financial Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

| Year Ended December 31, | Six Months Ended June 30, |

|||||||||||||||||||

| 2013 | 2014 | 2015 | 2015 | 2016 | ||||||||||||||||

| (in thousands, except per share amounts) |

||||||||||||||||||||

| Consolidated Statements of Operations Data |

||||||||||||||||||||

| Revenue: |

||||||||||||||||||||

| Subscription |

$ | 54,206 | $ | 78,719 | $ | 99,924 | $ | 47,242 | $ | 61,681 | ||||||||||

| Professional services |

19,562 | 27,896 | 29,327 | 14,913 | 13,941 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total revenue |

73,768 | 106,615 | 129,251 | 62,155 | 75,622 | |||||||||||||||

| Cost of revenue: |

||||||||||||||||||||

| Subscription(1) |

8,325 | 14,686 | 23,457 | 11,142 | 13,039 | |||||||||||||||

| Professional services(1) |

19,034 | 25,731 | 25,720 | 13,036 | 12,712 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total cost of revenue(1) |

27,359 | 40,417 | 49,177 | 24,178 | 25,751 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross profit |

46,409 | 66,198 | 80,074 | 37,977 | 49,871 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating expenses: |

||||||||||||||||||||

| Research and development(1) |

17,804 | 23,099 | 30,553 | 14,674 | 17,057 | |||||||||||||||

| Sales and marketing(1) |

43,415 | 60,775 | 71,337 | 33,274 | 35,956 | |||||||||||||||

| General and administrative(1) |

8,597 | 14,245 | 17,763 | 7,698 | 10,684 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total operating expenses |

69,816 | 98,119 | 119,653 | 55,646 | 63,697 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Loss from operations |

(23,407 | ) | (31,921 | ) | (39,579 | ) | (17,669 | ) | (13,826 | ) | ||||||||||

| Other income (expense): |

||||||||||||||||||||

| Interest (expense) income and other, net |

(51 | ) | 2 | (18 | ) | 19 | (434 | ) | ||||||||||||

| Foreign exchange loss |

(163 | ) | (697 | ) | (1,301 | ) | (607 | ) | (407 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Loss before provision for income taxes |

(23,621 | ) | (32,616 | ) | (40,898 | ) | (18,257 | ) | (14,667 | ) | ||||||||||

| Provision for income taxes |

(114 | ) | (256 | ) | (109 | ) | (149 | ) | (214 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net loss |

$ | (23,735 | ) | $ | (32,872 | ) | $ | (41,007 | ) | $ | (18,406 | ) | $ | (14,881 | ) | |||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net loss per share attributable to common stockholders, basic and diluted |

$ | (2.11 | ) | $ | (2.72 | ) | $ | (3.24 | ) | $ | (1.47 | ) | $ | (1.14 | ) | |||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Weighted-average shares used to compute net loss per share attributable to common stockholders, basic and diluted |

11,256 | 12,080 | 12,653 | 12,485 | 13,016 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Pro forma net loss per share attributable to common stockholders, basic and diluted(2) |

$ | (1.33 | ) | $ | (0.48 | ) | ||||||||||||||

|

|

|

|

|

|||||||||||||||||

| Weighted-average shares used to compute pro forma net loss per share attributable to common stockholders, basic and diluted(2) |

30,893 | 31,256 | ||||||||||||||||||

|

|

|

|

|

|||||||||||||||||

-11-

Table of Contents

| (1) | Includes stock-based compensation expense as follows: |

| Year Ended December 31, | Six Months Ended June 30, |

|||||||||||||||||||

| 2013 | 2014 | 2015 | 2015 | 2016 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Cost of revenue: |

||||||||||||||||||||

| Subscription |

$ | 75 | $ | 220 | $ | 482 | $ | 196 | $ | 332 | ||||||||||

| Professional services |

314 | 609 | 738 | 395 | 367 | |||||||||||||||

| Research and development |

836 | 1,465 | 2,283 | 1,160 | 1,267 | |||||||||||||||

| Sales and marketing |

1,047 | 2,006 | 2,477 | 1,210 | 1,441 | |||||||||||||||

| General and administrative |

789 | 1,466 | 1,835 | 894 | 1,008 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total stock-based compensation |

$ | 3,061 | $ | 5,766 | $ | 7,815 | $ | 3,855 | $ | 4,415 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (2) | See Note 8 of the notes to our consolidated financial statements included in this prospectus for an explanation of the method used to calculate basic and diluted net loss per share and pro forma net loss per share attributable to common stockholders and the weighted-average number of shares used in the computation of the per share amounts. |

| As of June 30, 2016 | ||||||||||||

| Actual | Pro Forma(1) | Pro Forma As Adjusted(2) |

||||||||||

| (in thousands) | ||||||||||||

| Consolidated Balance Sheet Data |

||||||||||||

| Cash and cash equivalents |

$ | 42,052 | $ | 42,052 | $ | 107,832 | ||||||

| Working capital, excluding deferred revenue |

71,965 | 71,965 | 138,292 | |||||||||

| Total assets |

107,485 | 107,485 | 173,265 | |||||||||

| Deferred revenue, current and non-current |

82,184 | 82,184 | 82,184 | |||||||||

| Long-term debt, current and non-current, net of debt issuance costs |

19,432 | 19,432 | — | |||||||||

| Preferred stock warrant liability |

406 | — | — | |||||||||

| Convertible preferred stock |

133,809 | — | — | |||||||||

| Accumulated deficit |

(183,652 | ) | (183,652 | ) | (184,420 | ) | ||||||

| Total stockholders’ (deficit) equity |

(151,931 | ) | (17,716 | ) | 67,496 | |||||||

| (1) | Reflects (a) the automatic conversion of all outstanding shares of our convertible preferred stock as of June 30, 2016 into an aggregate of 18,239,475 shares of Class B common stock which conversion will occur immediately prior to the closing of this offering, as if such conversion had occurred on June 30, 2016; and (b) the conversion of warrants to purchase 27,321 shares of convertible preferred stock into warrants to purchase 27,321 shares of Class B common stock. |

| (2) | Gives effect to (a) the pro forma adjustments set forth above, (b) the sale and issuance by us of 6,000,000 shares of Class A common stock in this offering at the initial price to public of $16.00 per share, after deducting underwriting discounts and commissions and estimated offering expenses payable by us and (c) the application of such proceeds as described in the section of this prospectus captioned “Use of Proceeds.” |

-12-

Table of Contents

Non-GAAP Financial Measures

In addition to our results determined in accordance with U.S. generally accepted accounting principles, or GAAP, we believe the following non-GAAP measure is useful in evaluating our business performance. We regularly review the liquidity measure set forth below.

| Year Ended December 31, | Six Months Ended June 30, |

|||||||||||||||||||

| 2013 | 2014 | 2015 | 2015 | 2016 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Other Non-GAAP Financial Data: |

||||||||||||||||||||

| Free cash flow(1) |

$ | (15,480 | ) | $ | (24,276 | ) | $ | (18,234 | ) | $ | (8,071 | ) | $ | (3,729 | ) | |||||

| (1) | We define free cash flow as net cash used in operating activities, plus purchases of property and equipment. |

We believe free cash flow facilitates period-to-period comparisons of liquidity. We consider free cash flow to be an important measure because it measures the amount of cash we generate from our operations after our capital expenditures and reflects changes in working capital. We use free cash flow in conjunction with traditional GAAP measures as part of our overall assessment of our liquidity, including the preparation of our annual operating budget and quarterly forecasts, to evaluate the effectiveness of our business strategies and to communicate with our board of directors concerning our liquidity.

Our definitions may differ from the definitions used by other companies and therefore comparability may be limited. In addition, other companies may not publish these or similar metrics. Thus, our free cash flow should be considered in addition to, not as a substitute for, or in isolation from, measures prepared in accordance with GAAP.

We compensate for these limitations by providing investors and other users of our financial information reconciliations of free cash flow to the related GAAP financial measure, net cash used in operating activities. We encourage investors and others to review our financial information in its entirety, not to rely on any single financial measure and to view free cash flow in conjunction with the related GAAP financial measure.

The following table provides a reconciliation of net cash used in operating activities to free cash flow.

| Year Ended December 31, | Six Months Ended June 30, |

|||||||||||||||||||

| 2013 | 2014 | 2015 | 2015 | 2016 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Net cash used in operating activities |

$ | (11,264 | ) | $ | (17,957 | ) | $ | (10,591 | ) | $ | (3,312 | ) | $ | (1,409 | ) | |||||

| Plus: purchases of property and equipment |

(4,216 | ) | (6,319 | ) | (7,643 | ) | (4,759 | ) | (2,320 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Free cash flow |

$ | (15,480 | ) | $ | (24,276 | ) | $ | (18,234 | ) | $ | (8,071 | ) | $ | (3,729 | ) | |||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

-13-

Table of Contents

Investing in our Class A common stock involves a high degree of risk. Before making an investment decision, you should carefully consider the risks and uncertainties described below, which we believe are the material risks associated with our business and this offering. Our business, financial condition, operating results or growth prospects could be harmed by any of these risks. In that event, the trading price of our Class A common stock could decline due to any of these risks, and you may lose all or part of your investment. In assessing these risks, you should also refer to all of the other information contained in this prospectus, including our financial statements and related notes.

Risks Related to Our Business and Industry

We have a history of losses and we expect our revenue growth rate to decline. As our costs increase, we may not be able to generate sufficient revenue to achieve or maintain profitability in the future.

We incurred net losses of $23.7 million, $32.9 million and $41.0 million in 2013, 2014 and 2015, respectively, and $18.4 million and $14.9 million in the six months ended June 30, 2015 and 2016, respectively. We had an accumulated deficit of $183.7 million at June 30, 2016. We expect that our revenue growth rate will decline over time. We may not be able to generate sufficient revenue to achieve or sustain profitability. We expect to continue to incur losses for the foreseeable future and we expect our costs to increase in future periods as we expend substantial financial and other resources on, among other things:

| • | sales and marketing, including a continued expansion of our direct sales organization which will require time before these investments generate sales results; |

| • | hiring of additional employees for our research and development team to support growth, our technology and datacenter infrastructure, enhancements to our cloud architecture, improved disaster recovery protection, increasing security, compliance and operations expenses, and expenses related to required certifications and third-party attestations; |

| • | other software development, including enhancements and modifications related to our business applications, including investments in our software development team; |

| • | international expansion in an effort to increase our customer base and sales; |

| • | continued growth of the customer success team; and |

| • | general and administration, including significantly increasing expenses in accounting and legal related to the increase in the sophistication and resources required for public company compliance and other work arising from the growth and maturity of the company. |

These expenditures may not result in additional revenue or the growth of our business. If we fail to continue to grow revenue or to achieve or sustain profitability, the market price of our Class A common stock could decline.

We have a limited operating history, which makes it difficult to evaluate our prospects and future operating results.

We were incorporated in 2007 and introduced our first solution in 2008. Our limited operating history makes our ability to forecast future operating results difficult and subjects us to a number of uncertainties, including our ability to plan and model future growth. Our revenue grew 46%, 45% and

-14-

Table of Contents

21% in 2013, 2014 and 2015, respectively, compared to the prior year, and by 22% in the six months ended June 30, 2016 compared to the same period in the prior year; however, our historical revenue growth is not necessarily indicative of our future performance. Our revenue growth is expected to decline in future periods due to a number of reasons, which may include the maturation of our business, increase in overall revenue over time, slowing demand for our applications, increasing competition, a decrease in the growth of the markets in which we compete, or if we fail, for any reason, to continue to capitalize on growth opportunities, a decrease in our renewal rates, or a decline in available opportunities as a result of our increased market penetration in one or more of our markets.

We have encountered and will continue to encounter risks and uncertainties frequently experienced by growing companies in rapidly changing industries, such as determining appropriate investments of our limited resources, market adoption of our current and future applications, competition from other companies, acquiring and retaining customers, hiring, integrating, training and retaining skilled personnel, developing new applications, determining prices and contract terms for our applications, and unforeseen expenses and challenges in forecasting accuracy. If our assumptions regarding these risks and uncertainties, which we use to plan our business, are incorrect or change, or if we do not address these risks successfully, our prospects, operating results and business could be harmed.

If the TBM market fails to develop, or we are unable to maintain our leadership within that market category, our business, results of operations, financial condition and growth prospects could be harmed.

Our business model depends upon the development and adoption of the market for TBM solutions and our leadership within that market category. We derive and expect to continue to derive for some period of time the majority of revenue and cash flows from our core TBM solutions. The TBM market is relatively new and is evolving rapidly, and overall market acceptance of the importance of TBM and our solutions is critical to our continued success. If the market for TBM solutions does not continue to grow, or grows more slowly than we expect, or if the market for TBM solutions does not develop as we anticipate, our operating results would be harmed. In addition, successful market adoption will depend in part on our ability to correctly anticipate, identify and build the key features, functions, reports, metric selection, and packaging that is most useful and attractive to the market, all while maintaining sufficient flexibility with the platform as needed to accommodate customer-specific needs.

We derive, and expect to continue to derive, substantially all of our revenue and operating cash flows from TBM solutions and related professional services. If we fail to adapt our solutions to changing market dynamics and customer preferences or to achieve increased market acceptance of our TBM solutions, our business, results of operations, financial condition, and growth prospects would be harmed.

We derive, and expect to continue to derive, substantially all of our revenue and cash flows from TBM solutions and related professional services. As such, the market acceptance of TBM solutions is critical to our success. Demand for our TBM solutions is affected by a number of factors, many of which are beyond our control, such as continued market acceptance of our solutions by customers for existing and new use cases, the timing of development and release of new applications, features, and functionality introduced by our competitors, technological change, and growth or contraction in our addressable market. Although we may expand our efforts in the marketplace beyond the TBM category, there can be no certainty that any such expansion will generate returns capable of offsetting the costs associated with any such expansion. You should consider our business and prospects based on our current solutions within the TBM category and, and in light of the various challenges we and TBM as a category face, including those discussed in this “Risk Factors” section.

-15-

Table of Contents

Our business model heavily depends on the acquisition of new customers, adoption by current customers of our solutions, renewals of their subscriptions and the purchase of additional subscriptions from us.

In order to maintain or improve our operating results, we depend on the acquisition of new customers, the adoption of additional applications by existing customers and the decision by existing and new customers to renew their subscriptions upon the expiration of their current contract term. Our contracts typically vary in length between one and three years and our customers have no obligation to renew their subscriptions after the expiration of their initial subscription periods. Our customers may elect not to renew, may seek to renew for lower subscription amounts or for shorter contract lengths and may choose to renew for the same or fewer applications and modules over time. Our renewal rates may decline or fluctuate as a result of a number of factors, including leadership changes within our customers resulting in loss of sponsorship, limited customer resources, pricing changes by us or our competitors, adoption and utilization of our solutions by our customers, customer satisfaction with our applications, the acquisition of our customers by other companies, procurement or budgetary decisions from legislative or other regulatory bodies, and deteriorating general economic conditions. To the extent our customer base continues to grow, renewals and the subscriptions to additional applications and modules by renewing customers will become an increasingly important part of our results. If our customers do not renew their subscriptions for our applications, or decrease the amount they spend with us, revenue will decline and our business will be harmed.

Because our recent growth has resulted in the rapid expansion of our business, we do not have a long history upon which to base forecasts of customer renewal rates, customer upgrade rates or future revenue. As a result, our future operating results may be significantly below the expectations of investors, which could harm the market price of our Class A common stock.

If we fail to effectively develop and expand our sales and marketing capabilities, our ability to increase our customer base and increase acceptance of our TBM solutions could be harmed.

To increase the number of customers and increase the market acceptance of our solutions, we will need to expand our sales and marketing operations, including our domestic and international sales force. We will continue to dedicate significant resources to sales and marketing programs. We believe that there is significant competition for direct sales personnel with the sales skills and technical knowledge that we require. Our ability to achieve significant revenue growth in the future will depend, in large part, on our success in recruiting, training and retaining a sufficient number of direct sales personnel. New hires require significant training and time before they achieve full productivity, particularly in new sales territories. Our recent hires and planned hires may not become as productive as quickly as we would like, and we may be unable to hire or retain sufficient numbers of qualified individuals in the future in the markets where we do business. The effectiveness of our sales and marketing has also varied over time and, together with the effectiveness of any partners or resellers we may engage, may vary in the future. Our business will be harmed if our efforts do not generate a correspondingly significant increase in revenue. We may not achieve anticipated revenue growth from expanding our sales force if we are unable to hire, develop and retain talented sales personnel, if our new sales personnel are unable to achieve desired productivity levels in a reasonable period of time, or if our sales and marketing programs are not effective.

-16-

Table of Contents

We may experience quarterly fluctuations in our operating results due to a number of factors, which makes our future results difficult to predict and could cause our operating results to fall below expectations.

Our quarterly operating results have fluctuated in the past and we expect them to fluctuate in the future due to a variety of factors, many of which are outside of our control. As a result, our past results may not be indicative of our future performance, and comparing our operating results on a period-to-period basis may not be meaningful. In addition to the other risks described in this prospectus, factors that may affect our quarterly operating results include:

| • | changes in spending on TBM solutions by our current or prospective customers; |

| • | pricing our applications effectively so that we are able to attract and retain customers without compromising our operating results; |

| • | attracting new customers and increasing existing customers’ use of our solutions; |

| • | unexpected sales and transaction execution delays; |

| • | customer renewal rates and the amounts for which agreements are renewed; |

| • | awareness of our brand; |

| • | changes in the competitive dynamics of our market, including consolidation among competitors or customers and the introduction of new applications or capabilities; |

| • | changes to the commission plans, quotas and other compensation-related metrics for our sales representatives; |

| • | the amount and timing of payment for operating expenses, particularly research and development, sales and marketing expenses and employee benefit expenses; |

| • | our ability to manage our existing business and future growth, including increases in the number of customers for our solutions and the introduction and adoption of our solutions in the United States and globally; |

| • | unforeseen costs and expenses related to the expansion of our business, operations and infrastructure, including disruptions in our hosting network infrastructure and privacy and data security; |

| • | the level of international sales and the pricing of sales; |

| • | foreign currency exchange rate fluctuations; and |

| • | general economic and political conditions in our domestic and international markets. |

We may not be able to accurately forecast the amount and mix of future subscriptions, size or duration of contracts, revenue and expenses and, as a result, our operating results may fall below our estimates or the expectations of public market analysts and investors. If our revenue or operating results fall below the expectations of investors, or below any estimates we may provide, the market price of our Class A common stock could decline.

-17-

Table of Contents

We target sales efforts at enterprise customers and the length, cost and uncertainty associated with sales cycles may result in fluctuations in our operating results and our failure to achieve the expectations of investors.

We target sales efforts at enterprises and face long sales cycles, complex customer requirements, substantial upfront sales costs, and a relatively low and difficult to predict volume of sales on a quarter-by-quarter basis. This makes it difficult to predict with certainty our sales and related operating performance in any given period. Our typical sales cycle is approximately six months, but is variable and difficult to predict and can be longer. Customers often undertake a prolonged evaluation of our solutions, including assessing their own readiness, scoping the professional services involved, and comparing our solutions to products offered by our competitors and their ability to solve the problem internally. Moreover, our customers often begin to deploy our solutions on a limited basis, but nevertheless demand extensive configuration, integration services and pricing concessions, which increase our upfront investment in the sales effort with no guarantee that these customers will deploy our solutions widely enough across their organization to justify our substantial upfront investment. Adherence to our financial plan in part depends on a predictable growth rate in the acquisition of new customers that represent high annual contract value, while additional growth and enhanced predictability in part depends on an increased volume of new customers with a relatively lower annual contract value. Our financial performance and the predictability of our quarterly financial results may be harmed by intermittent failures to secure the higher value enterprise agreements, or increase the volume of transactions overall, according to our forecasts, and depends in large part on the successful execution of our direct sales team. In addition, because of the relatively small and tightly knit nature of the community of IT leaders within the enterprises that we sell into, our business is vulnerable to negative feedback or opinions even if held by a few influential leaders within this community.

Additionally, our quarterly sales cycles are generally more heavily weighted toward the end of the quarter with an increased volume of sales in the last few weeks of the quarter. This could negatively impact the timing of recognized revenue and billings, cash collections and delivery of professional services in subsequent periods. Furthermore, the concentration of contract negotiations in the last few weeks of the quarter could require us to expend more in the form of compensation for additional sales, legal and finance employees and contractors. Compression of sales activity to the end of the quarter also greatly increases the likelihood that sales cycles will extend beyond the quarter in which they are forecasted to close for some sizeable transactions, which will harm forecasting accuracy and adversely impact billings and new customer acquisition metrics for the quarter in which they are forecasted to close.

Because we recognize revenue from subscriptions ratably over the term of the agreement, near-term changes in sales may not be reflected immediately in our operating results.

We offer our applications primarily through multi-year subscription agreements, which typically vary in length between one and three years. All subscription fees that are billed in advance of service are recorded in deferred revenue. Subscription revenue is recognized ratably over the subscription term. As a result, most of the revenue that we report in each period is derived from the recognition of deferred revenue relating to subscriptions entered into during previous periods. A decline in new or renewed subscriptions in any one quarter is not likely to have a material impact on results for that quarter. However, declines would negatively affect revenue and deferred revenue balances in future periods, and the effect of significant downturns in sales and market acceptance of our applications, and potential changes in our rate of renewals, may not be fully reflected in our results of operations until future periods. Our subscription model also makes it difficult for us to rapidly increase our total revenue through additional sales in any period, as revenue from new customers is recognized over the applicable subscription term.

-18-

Table of Contents

Because we expense commissions associated with subscriptions to our applications immediately upon the execution of a subscription agreement with a customer, our operating income in any period may not be indicative of our financial health and future performance.

We expense commissions paid to sales personnel in the period in which we enter into an agreement for the subscription to our applications. In contrast, we recognize the revenue associated with a subscription to our applications ratably over the related subscription period. Although we believe higher sales is a positive indicator of the long-term health of our business, higher sales increases our operating expenses and could decrease earnings in any particular period. Thus, we may report poor operating results due to higher sales commissions in a period in which we experience strong sales of our applications. Alternatively, we may report better operating results due to the reduction of sales commissions in a period in which we experience a slowdown in sales. Therefore, you should not necessarily rely on our operating income during any one quarter as an indication of our financial health and potential future performance.

If we fail to attract and retain additional qualified personnel we may be unable to execute our business strategy.

To execute our business strategy, we must attract and retain highly qualified personnel. In particular, we compete with many other companies for software developers with high levels of experience in designing, developing and managing cloud-based software, as well as for skilled product development, marketing, sales and operations professionals, and we may not be successful in attracting and retaining the professionals we need, in particular in the Seattle, Washington area where we are headquartered. We have experienced, and we expect to continue to experience, difficulty in hiring and retaining highly skilled employees with appropriate qualifications which may, among other things, impede our ability to execute our software development and sales strategies. Many of the companies with which we compete for experienced personnel are more well known and have greater resources than we do. In addition, in making employment decisions, particularly in the software industry, job candidates often consider the value of the stock options or other equity incentives they are to receive in connection with their employment. If the price of our stock declines, or experiences significant volatility, our ability to attract or retain qualified employees will be adversely affected. If we fail to attract new personnel or fail to retain and motivate our current personnel, our growth prospects could be harmed.

The market in which we participate is increasingly competitive, and if we do not compete effectively, our operating results could be harmed.

The market for TBM solutions is relatively new and rapidly evolving. In many cases, our primary competition is the use of legacy spreadsheet-based business processes, or occasionally we encounter either custom software developed, or general purpose business intelligence solutions repurposed, by in-house IT and finance departments of our potential customers to meet specific business needs. As we look to sell our solutions to potential customers with existing internal solutions, we must convince internal stakeholders that our TBM solutions are superior to the legacy solutions that the organization has previously adopted. If we are unable to effectively convince internal stakeholders at our prospective customers to abandon their legacy solutions, our business, results of operations, financial condition and cash flows could be materially and adversely affected.

Larger companies, such as VMware and ServiceNow, provide a suite of products and services that includes TBM capabilities. These competitors have greater name recognition, much longer operating histories, more and better-established customer relationships, larger sales forces, larger marketing and software development budgets and significantly greater resources than we do. These large vendors commonly have an enterprise-wide license agreement in place with the Fortune 2000 enterprise company customer base and are able to leverage that license to easily transact for their

-19-

Table of Contents

services. In some cases, these large vendors may be willing to provide their competing software for free as part of enterprise-wide agreements that include other products or services, which has resulted in pricing pressures and lost sales. Further, such large vendors frequently benefit from existing system integrator and other go-to-market relationships that facilitate their sales and marketing efforts, and that can be easily redirected to competition with us in the TBM market. In addition, certain of our competitors may be able to respond more quickly and effectively than we can to new or changing opportunities, technologies, standards, or customer requirements, or simply accelerate product development and improvements at greater velocity.

Several specialized companies target the TBM market through solutions that are tailored to a specific TBM use case or industry. Some of our principal competitors in these situations offer their products or services at a lower price, which has resulted in pricing pressures and lost sales. Potential customers with discrete and immediate needs that may be addressed by these niche solutions may choose to deploy these solutions instead of an offering from our integrated suite of TBM solutions. If we fail to compete effectively against these more specific, niche providers of TBM solutions, our business will be harmed.

We expect competition to intensify in the future. We expect that the large software vendors who currently do not have an offering in the TBM category, some of which operate in adjacent product categories today, may in the future bring such a solution to market through product development, acquisitions or other means. Such vendors would potentially benefit from the same advantages described above regarding our existing larger competitors, but perhaps on an even greater scale. Also, a simpler solution could gain traction in the market and acceptance by medium sized businesses, which may result in downward pressure on our pricing and potentially a decrease in market share and market opportunity for us.

If we fail to adapt and respond effectively to rapidly changing technology, evolving industry standards and changing customer needs or requirements, our solutions may become less competitive.

Our success depends on our ability to adapt and enhance our solutions. To attract new customers and increase revenue from existing customers, we need to continue to enhance and improve our solutions, capabilities and enhancements to meet customer needs at prices that our customers are willing to pay. Such efforts will require adding new functionality and responding to technological advancements, which will increase our research and development costs. If we are unable to develop solutions that address customers’ needs, or enhance and improve our offerings in a timely manner, we may not be able to maintain or increase market acceptance of our solutions. Further, many of our existing and potential future competitors expend a considerably greater amount of funds on their research and development programs, and those that do not may be acquired by larger companies that would allocate greater resources to competitors’ research and development programs. If we fail to maintain adequate research and development resources or compete effectively with the research and development programs of our competitors our business could be harmed. Our ability to grow is also subject to the risk of future disruptive technologies. If new technologies emerge that are able to deliver TBM solutions at lower prices, more efficiently, more conveniently or more securely, such technologies could adversely affect our ability to compete.

We may not receive significant revenue from our current development efforts for several years, if at all.

Developing software applications is expensive and the investment in product development often involves a long return on investment cycle. We have made and expect to continue to make significant investments in development and related product opportunities. Accelerated product

-20-

Table of Contents

introductions and short product life cycles require high levels of expenditures that could adversely affect our operating results if not offset by revenue increases. We believe that we must continue to dedicate a significant amount of resources to our development efforts to maintain our competitive position. However, we may not receive significant revenue from these investments for several years, if at all.

Our planned further expansion of our business outside the United States exposes us to risks associated with international operations.

Our growth strategy involves the further expansion of our operations and customers located outside of the United States. In 2015 and for the six months ended June 30, 2016, 22% and 24%, respectively, of our revenue was derived from customers located outside North America, primarily from customers in Europe. A key element of our growth strategy is to expand our international operations and develop a worldwide customer base. While we have initiated efforts to expand our business into Asia-Pacific through a limited presence in Australia and Singapore, our investment may never be recouped. Our current international operations and future initiatives will involve a variety of risks, including:

| • | the need to make significant investments in people, solutions and infrastructure, typically well in advance of revenue generation; |

| • | the need to localize and adapt our application for specific countries, including translation into foreign languages and associated expenses; |

| • | potential changes in public or customer sentiment regarding cloud-based services or the ability of non-local enterprises to provide adequate data protection, particularly in the European Union; |

| • | technical or latency issues in delivering our applications; |

| • | dependence on certain third parties, including resellers with whom we do not have extensive experience; |

| • | the lack of reference customers and other marketing assets in regional markets that are new or developing for us, as well as other adaptations in our market generation efforts that we may be slow to identify and implement; |

| • | unexpected changes in regulatory requirements, taxes or trade laws; |

| • | differing labor regulations, especially in the European Union, where labor laws are generally more advantageous to employees as compared to the United States, including deemed hourly wage and overtime regulations in these locations; |

| • | challenges inherent in efficiently managing an increased number of employees over large geographic distances, including the need to implement appropriate systems, policies, benefits and compliance programs; |

| • | difficulties in maintaining our company culture with a dispersed and distant workforce; |

| • | difficulties in managing a business in new markets with diverse cultures, languages, customs, legal systems, alternative dispute systems and regulatory systems; |

-21-

Table of Contents

| • | currency exchange rate fluctuations and the resulting effect on our revenue and expenses, and the cost and risk of entering into hedging transactions if we choose to do so in the future; |

| • | limitations on our ability to reinvest earnings from operations in one country to fund the capital needs of our operations in other countries; |

| • | limited or insufficient intellectual property protection; |

| • | political instability or terrorist activities; |

| • | requirements to comply with foreign privacy and information security laws and regulations and the risks and costs of non-compliance; |

| • | likelihood of potential or actual violations of domestic and international anticorruption laws, such as the U.S. Foreign Corrupt Practices Act and the U.K. Bribery Act, or of U.S. and international export control and sanctions regulations, which likelihood may increase with an increase of sales or operations in foreign jurisdictions and operations in certain industries; |

| • | requirements to comply with U.S. export control and economic sanctions laws and regulations and other restrictions on international trade; |

| • | likelihood that the United States and other governments and their agencies impose sanctions and embargoes on certain countries, their governments and designated parties, which may prohibit the export of certain technology, products, and services to such persons; and |

| • | adverse tax burdens and foreign exchange controls that could make it difficult to repatriate earnings and cash should we desire to do so. |

Our limited experience in operating our business internationally increases the risk that any potential future expansion efforts that we may undertake will not be successful. If we invest substantial time and resources to expand our international operations and are unable to do so successfully and in a timely manner, our business and operating results will be harmed.

Increased sales to customers outside the United States and/or paid for in currency other than the U.S. dollar exposes us to potential currency exchange losses.

As our international sales and operations increase, so too will the number and significance of transactions, including intercompany transactions, occurring in currencies other than the U.S. dollar. In addition, our international subsidiaries may begin to maintain or accumulate assets that are denominated in currencies other than the functional operating currencies of these entities. Accordingly, changes in the value of foreign currencies relative to the U.S. dollar can affect our revenue and operating results due to transactional and translational remeasurement that is reflected in our earnings. We do not currently maintain a program to hedge transactional exposures in foreign currencies. However, in the future, we may use derivative instruments, such as foreign currency forward and option contracts, to hedge certain exposures to fluctuations in foreign currency exchange rates. The use of such hedging activities may not offset any or more than a portion of the adverse financial effects of unfavorable movements in foreign exchange rates over the limited time the hedges are in place. Moreover, the use of hedging instruments may introduce additional risks if we are unable to structure effective hedges with such instruments. Additionally, our license fees are largely based on our customers’ anticipated spend managed by our solutions expressed in U.S. dollars, which fee construct may increase the exposure of our revenue to currency fluctuations.

-22-

Table of Contents

If we fail to manage our rapid growth effectively or our business does not grow as we expect, our operating results may suffer.

Our employee base and operations have grown substantially in a relatively short period of time. Our full-time employee base grew from 628 employees as of June 30, 2015 to 694 employees as of June 30, 2016. Our growth has placed, and will continue to place, a significant strain on our operational, financial and management infrastructure. We anticipate further increases in headcount will be required to support increases in our application offerings and continued expansion. To manage this growth effectively, we must continue to improve operational, financial and management systems and controls by, among other things:

| • | effectively attracting, training and integrating a large number of new employees, particularly technical personnel and members of our management and sales teams; |

| • | further improving key business systems, processes and IT infrastructure to support our business needs; |

| • | enhancing information and communication systems to ensure that employees are well-coordinated and can effectively communicate with each other and customers; and |

| • | improving internal control over financial reporting and disclosure controls and procedures to ensure timely and accurate reporting of operational and financial results. |