UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-22147

PowerShares India Exchange-Traded Fund Trust

(Exact name of registrant as specified in charter)

3500 Lacey Road

Downers Grove, IL 60515

(Address of principal executive offices) (Zip code)

Daniel E. Draper

President

3500 Lacey Road

Downers Grove, IL 60515

(Name and address of agent for service)

Registrant’s telephone number, including area code: 800-983-0903

Date of fiscal year end: October 31

Date of reporting period: October 31, 2017

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

The Registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

| October 31, 2017 |

2017 Annual Report to Shareholders

| PIN | PowerShares India Portfolio | |

|

|

2 |

|

|

|

3 |

|

| PIN | Manager’s Analysis | |

| PowerShares India Portfolio (PIN) |

|

|

4 |

|

PowerShares India Portfolio (PIN) (continued)

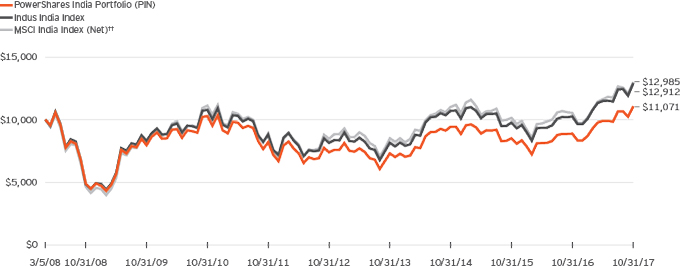

Growth of a $10,000 Investment Since Inception†

Fund Performance History as of October 31, 2017

| Index | 1 Year |

3 Years Average |

3 Years Cumulative |

5 Years Average |

5 Years Cumulative |

Fund Inception† | ||||||||||||||||||||||||||

| Average Annualized |

Cumulative | |||||||||||||||||||||||||||||||

| Indus India Index | 25.86 | % | 6.39 | % | 20.41 | % | 9.64 | % | 58.42 | % | 2.68 | % | 29.12 | % | ||||||||||||||||||

| MSCI India Index (Net)†† | 23.20 | 5.61 | 17.79 | 8.93 | 53.39 | 2.74 | 29.85 | |||||||||||||||||||||||||

| Fund | ||||||||||||||||||||||||||||||||

| NAV Return | 24.46 | 5.48 | 17.35 | 8.42 | 49.78 | 1.06 | 10.71 | |||||||||||||||||||||||||

| Market Price Return | 24.89 | 5.36 | 16.96 | 8.53 | 50.60 | 0.84 | 8.42 | |||||||||||||||||||||||||

|

|

5 |

|

Consolidated Schedule of Investments(a)

PowerShares India Portfolio (PIN)

October 31, 2017

See accompanying Notes to Consolidated Financial Statements which are an integral part of the financial statements.

|

|

6 |

|

Consolidated Statement of Assets and Liabilities

October 31, 2017

| PowerShares India Portfolio (PIN) |

||||

| Assets: | ||||

| Investments in securities, at value |

$ | 292,602,834 | ||

| Foreign currencies, at value |

61,975 | |||

| Receivables: |

||||

| Dividends |

389,514 | |||

| Other assets |

3,123 | |||

|

|

|

|||

| Total Assets |

293,057,446 | |||

|

|

|

|||

| Liabilities: | ||||

| Payables: |

||||

| Accrued unitary management fee |

187,316 | |||

|

|

|

|||

| Total Liabilities |

187,316 | |||

|

|

|

|||

| Net Assets | $ | 292,870,130 | ||

|

|

|

|||

| Net Assets Consist of: | ||||

| Shares of beneficial interest |

$ | 253,863,951 | ||

| Undistributed net investment income |

— | |||

| Undistributed net realized gain (loss) |

(84,650,316 | ) | ||

| Net unrealized appreciation |

123,656,495 | |||

|

|

|

|||

| Net Assets | $ | 292,870,130 | ||

|

|

|

|||

| Shares outstanding (unlimited amount authorized, $0.01 par value) |

11,450,000 | |||

| Net asset value |

$ | 25.58 | ||

|

|

|

|||

| Market price |

$ | 25.62 | ||

|

|

|

|||

| Investments in securities, at cost |

$ | 168,946,568 | ||

|

|

|

|||

| Foreign currencies, at cost |

$ | 61,802 | ||

|

|

|

|||

See accompanying Notes to Consolidated Financial Statements which are an integral part of the financial statements.

|

|

7 |

|

Consolidated Statement of Operations

For the year ended October 31, 2017

| PowerShares India Portfolio (PIN) |

||||

| Investment Income: | ||||

| Dividend income |

$ | 5,765,041 | ||

| Interest income |

3,816 | |||

|

|

|

|||

| Total Income |

5,768,857 | |||

|

|

|

|||

| Expenses: | ||||

| Unitary management fee |

2,242,596 | |||

| Tax expense |

32,101 | |||

|

|

|

|||

| Total Expenses |

2,274,697 | |||

|

|

|

|||

| Net Investment Income |

3,494,160 | |||

|

|

|

|||

| Realized and Unrealized Gain (Loss) on Investments: | ||||

| Net realized gain (loss) from: |

||||

| Investment securities |

36,040,739 | |||

| Foreign currencies |

(1,146,244 | ) | ||

|

|

|

|||

| Net realized gain |

34,894,495 | |||

|

|

|

|||

| Net change in unrealized appreciation from: |

||||

| Investment securities |

7,957,267 | |||

| Foreign currencies |

518 | |||

|

|

|

|||

| Net change in unrealized appreciation |

7,957,785 | |||

|

|

|

|||

| Net realized and unrealized gain |

42,852,280 | |||

|

|

|

|||

| Net increase in net assets resulting from operations |

$ | 46,346,440 | ||

|

|

|

|||

See accompanying Notes to Consolidated Financial Statements which are an integral part of the financial statements.

|

|

8 |

|

Consolidated Statement of Changes in Net Assets

For the years ended October 31, 2017 and 2016

| PowerShares India Portfolio (PIN) | ||||||||

| 2017 | 2016 | |||||||

| Operations: | ||||||||

| Net investment income |

$ | 3,494,160 | $ | 4,570,140 | ||||

| Net realized gain |

34,894,495 | 3,521,497 | ||||||

| Net change in unrealized appreciation |

7,957,785 | 4,850,576 | ||||||

|

|

|

|

|

|||||

| Net increase in net assets resulting from operations |

46,346,440 | 12,942,213 | ||||||

|

|

|

|

|

|||||

| Distributions to Shareholders from: | ||||||||

| Net investment income |

(3,226,186 | ) | (4,357,432 | ) | ||||

|

|

|

|

|

|||||

| Shareholder Transactions: | ||||||||

| Proceeds from shares sold |

— | 32,350,629 | ||||||

| Value of shares repurchased |

(172,852,926 | ) | (93,843,525 | ) | ||||

| Transaction fees |

556,329 | 268,067 | ||||||

|

|

|

|

|

|||||

| Net increase (decrease) in net assets resulting from shares transactions |

(172,296,597 | ) | (61,224,829 | ) | ||||

|

|

|

|

|

|||||

| Increase (Decrease) in Net Assets |

(129,176,343 | ) | (52,640,048 | ) | ||||

|

|

|

|

|

|||||

| Net Assets: | ||||||||

| Beginning of year |

422,046,473 | 474,686,521 | ||||||

|

|

|

|

|

|||||

| End of year |

$ | 292,870,130 | $ | 422,046,473 | ||||

|

|

|

|

|

|||||

| Changes in Shares Outstanding: | ||||||||

| Shares sold |

— | 1,750,000 | ||||||

| Shares repurchased |

(8,850,000 | ) | (5,050,000 | ) | ||||

| Shares outstanding, beginning of year |

20,300,000 | 23,600,000 | ||||||

|

|

|

|

|

|||||

| Shares outstanding, end of year |

11,450,000 | 20,300,000 | ||||||

|

|

|

|

|

|||||

See accompanying Notes to Consolidated Financial Statements which are an integral part of the financial statements.

|

|

9 |

|

PowerShares India Portfolio (PIN)

| For the Year Ended October 31, | ||||||||||||||||||||

| 2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||||||||

| Per Share Operating Performance | ||||||||||||||||||||

| Net asset value at beginning year |

$ | 20.79 | $ | 20.11 | $ | 22.47 | $ | 17.54 | $ | 17.94 | ||||||||||

| Net investment income(a) |

0.27 | 0.22 | 0.17 | 0.22 | 0.19 | |||||||||||||||

| Net realized and unrealized gain (loss) |

4.76 | 0.67 | (2.41 | ) | 4.89 | (0.49 | ) | |||||||||||||

| Total from investment operations |

5.03 | 0.89 | (2.24 | ) | 5.11 | (0.30 | ) | |||||||||||||

| Distributions to shareholders from: |

||||||||||||||||||||

| Net investment income |

(0.28 | ) | (0.22 | ) | (0.15 | ) | (0.19 | ) | (0.16 | ) | ||||||||||

| Transaction fees(a) |

0.04 | 0.01 | 0.03 | 0.01 | 0.06 | |||||||||||||||

| Net asset value at end of year |

$ | 25.58 | $ | 20.79 | $ | 20.11 | $ | 22.47 | $ | 17.54 | ||||||||||

| Market price at end of year(b) |

$ | 25.62 | $ | 20.76 | $ | 19.91 | $ | 22.58 | $ | 17.28 | ||||||||||

| Net Asset Value, Total Return(c) | 24.52 | % | 4.57 | % | (9.88 | )% | 29.30 | % | (1.29 | )% | ||||||||||

| Market Value, Total Return(c) | 24.89 | % | 5.47 | % | (11.21 | )% | 31.66 | % | (2.20 | )% | ||||||||||

| Ratios/Supplemental Data: | ||||||||||||||||||||

| Net assets at end of year (000’s omitted) |

$ | 292,870 | $ | 422,046 | $ | 474,687 | $ | 566,343 | $ | 374,555 | ||||||||||

| Ratio to average net assets of: |

||||||||||||||||||||

| Expenses |

0.79 | % | 0.80 | % | 0.82 | % | 0.85 | % | 0.82 | % | ||||||||||

| Net investment income |

1.22 | % | 1.15 | % | 0.78 | % | 1.14 | % | 1.08 | % | ||||||||||

| Portfolio turnover rate(d) |

27 | % | 39 | % | 68 | % | 49 | % | 117 | % | ||||||||||

| (a) | Based on average shares outstanding. |

| (b) | The mean between the last bid and ask prices. |

| (c) | Net asset value total return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, and redemption on the last day of the period. Net asset value total return includes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset value and returns for shareholder transactions. Market price total return is calculated assuming an initial investment made at the market price at the beginning of the period, reinvestment of all dividends and distributions at market price during the period and sale at the market price on the last day of the period. Total investment return calculated for a period of less than one year is not annualized. |

| (d) | Portfolio turnover rate is not annualized and does not include securities received or delivered from processing creations or redemptions. |

See accompanying Notes to Consolidated Financial Statements which are an integral part of the financial statements.

|

|

10 |

|

Notes to Consolidated Financial Statements

PowerShares India Exchange-Traded Fund Trust

October 31, 2017

Note 1. Organization

PowerShares India Exchange-Traded Fund Trust (the “Trust”) was organized as a Massachusetts business trust on August 3, 2007 and is authorized to have multiple series of portfolios. The Trust is an open-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). As of October 31, 2017, the Trust offered one portfolio, the PowerShares India Portfolio (PIN), an exchange-traded index fund (the “Portfolio”). The Portfolio carries out its investment strategy by investing substantially all of its assets in PowerShares Mauritius, a wholly-owned subsidiary organized in Mauritius (the “Subsidiary”). The Subsidiary invests at least 90% of its total assets in securities that comprise the Indus India Index (the “Underlying Index”), as well as American Depositary Receipts (“ADRs”) and Global Depositary Receipts (“GDRs”) based on securities in the Underlying Index. Invesco PowerShares Capital Management LLC (the “Adviser”) serves as the investment adviser to both the Portfolio and the Subsidiary (collectively the “Fund”). Through such investment structure, the Fund expects to obtain benefits from a tax treaty between Mauritius and India (the “Tax Treaty”). To obtain benefits under the Tax Treaty, the Subsidiary must meet certain tests and conditions, including the establishment of Mauritius tax residence.

The Portfolio’s shares (“Shares”) are listed on NYSE Arca, Inc. The market price of a Share may differ to some degree from the Fund’s net asset value (“NAV”). Unlike conventional mutual funds, the Fund issues and redeems Shares on a continuous basis, at NAV, only in a large specified number of Shares, each called a “Creation Unit.” Creation Units are issued and redeemed principally in exchange for the deposit or delivery of cash. Except when aggregated in Creation Units by Authorized Participants, Shares are not individually redeemable securities of the Fund.

The investment objective of the Fund is to seek to track the investment results (before fees and expenses) of its respective Underlying Index.

Note 2. Significant Accounting Policies

The following is a summary of the significant accounting policies followed by the Fund in preparation of its consolidated financial statements.

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance in accordance with Financial Accounting Standards Board Accounting Standards Codification Topic 946, Financial Services—Investment Companies.

A. Security Valuation

Securities, including restricted securities, are valued according to the following policies:

A security listed or traded on an exchange (except convertible securities) is valued at its last sales price or official closing price as of the close of the customary trading session on the exchange where the security is principally traded, or lacking any sales or official closing price on a particular day, the security may be valued at the closing bid price on that day. Securities traded in the over-the-counter market are valued based on prices furnished by independent pricing services or market makers. When such securities are valued by an independent pricing service they may be considered fair valued. Futures contracts are valued at the final settlement price set by an exchange on which they are principally traded. Listed options are valued at the mean between the last bid and asked prices from the exchange on which they are principally traded. Options not listed on an exchange are valued by an independent source at the mean between the last bid and asked prices. For purposes of determining NAV per Share, futures and option contracts generally are valued 15 minutes after the close of the customary trading session of the New York Stock Exchange (“NYSE”).

Investments in open-end and closed-end registered investment companies that do not trade on an exchange are valued at the end of day NAV per share. Investments in open-end and closed-end registered investment companies that trade on an exchange are valued at the last sales price or official closing price as of the close of the customary trading session on the exchange where the security is principally traded.

Debt obligations (including convertible securities) and unlisted equities are fair valued using an evaluated quote provided by an independent pricing service. Evaluated quotes provided by the pricing service may be determined without exclusive reliance on quoted prices, and may reflect appropriate factors such as institution-size trading in similar groups of securities, developments related to specific securities, dividend rate (for unlisted equities), yield (for debt obligations), quality, type of issue, coupon rate (for debt obligations), maturity (for debt obligations), individual trading characteristics and other market data. Securities with a demand feature exercisable within one to seven days are valued at par. Pricing services generally value debt obligations assuming orderly transactions of institutional round lot size, but the fund may hold or transact in the same securities in smaller, odd lot sizes. Odd lots often trade at lower prices than institutional round lots. Debt obligations are subject to interest rate and credit risks. In addition, all debt obligations involve some risk of default with respect to interest and/or principal payments.

|

|

11 |

|

Foreign securities’ (including foreign exchange contracts’) prices are converted into U.S. dollar amounts using the applicable exchange rates as of the close of the London world markets. If market quotations are available and reliable for foreign exchange-traded equity securities, the securities will be valued at the market quotations. Because trading hours for certain foreign securities end before the close of the NYSE, closing market quotations may become unreliable. If between the time trading ends on a particular security and the close of the customary trading session on the NYSE, events occur that the Adviser determines are significant and make the closing price unreliable, the Fund may fair value the security. If the event is likely to have affected the closing price of the security, the security will be valued at fair value in good faith using procedures approved by the Board of Trustees. Adjustments to closing prices to reflect fair value may also be based on a screening process of an independent pricing service to indicate the degree of certainty, based on historical data, that the closing price in the principal market where a foreign security trades is not the current value as of the close of the NYSE. Foreign securities’ prices meeting the approved degree of certainty that the price is not reflective of current value will be priced at the indication of fair value from the independent pricing service. Multiple factors may be considered by the independent pricing service in determining adjustments to reflect fair value and may include information relating to sector indices, ADRs and domestic and foreign index futures. Foreign securities may have additional risks including exchange rate changes, potential for sharply devalued currencies and high inflation, political and economic upheaval, the relative lack of issuer information, relatively low market liquidity and the potential lack of strict financial and accounting controls and standards.

Securities for which market prices are not provided by any of the above methods may be valued based upon quotes furnished by independent sources. The last bid price may be used to value equity securities. The mean between the last bid and asked prices is used to value debt obligations, including corporate loans.

Securities for which market quotations are not readily available or became unreliable are valued at fair value as determined in good faith following procedures approved by the Board of Trustees. Issuer specific events, market trends, bid/asked quotes of brokers and information providers and other market data may be reviewed in the course of making a good faith determination of a security’s fair value.

The Fund may invest in securities that are subject to interest rate risk, meaning the risk that the prices will generally fall as interest rates rise and, conversely, the prices will generally rise as interest rates fall. Specific securities differ in their sensitivity to changes in interest rates depending on their individual characteristics. Changes in interest rates may result in increased market volatility, which may affect the value and/or liquidity of certain Fund investments.

Valuations change in response to many factors, including the historical and prospective earnings of the issuer, the value of the issuer’s assets, general economic conditions, interest rates, investor perceptions and market liquidity. Because of the inherent uncertainties of valuation, the values reflected in the consolidated financial statements may materially differ from the value received upon actual sale of those investments.

B. Other Risks

Index Risk. Unlike many investment companies, the Fund does not utilize investing strategies that seek returns in excess of its Underlying Index. Therefore, the Fund would not necessarily buy or sell a security unless that security is added or removed, respectively, from its Underlying Index, even if that security generally is underperforming.

Authorized Participant Concentration Risk. Only an authorized participant (“AP”) may engage in creation or redemption transactions directly with a Fund. Each Fund has a limited number of institutions that may act as APs on an agency basis (i.e., on behalf of other market participants). Such market makers have no obligation to submit creation or redemption orders; consequently, there is no assurance that market makers will establish or maintain an active trading market for the Shares. In addition, to the extent that APs exit the business or are unable to proceed with creation and/or redemption orders with respect to a Fund and no other AP is able to step forward to create or redeem Creation Units, that Fund’s Shares may be more likely to trade at a premium or discount to NAV and possibly face trading halts and/or delisting.

Non-Diversified Fund Risk. Because the Fund is non-diversified and can invest, through the Subsidiary, a greater portion of its assets in securities of individual issuers than diversified funds, changes in the market value of a single investment could cause greater fluctuations in share price than would occur in a diversified fund. This may increase the Fund’s volatility and cause the performance of a relatively small number of issuers to have a greater impact on the Fund’s performance.

Non-Correlation Risk. The Fund’s return may not match the return of its Underlying Index for a number of reasons. For example, the Fund incurs operating expenses not applicable to its Underlying Index, and incurs costs in buying and selling securities, especially when rebalancing the Fund’s securities holdings to reflect changes in the composition of its Underlying Index. Because the Fund issues and redeems Creation Units principally for cash, it will incur higher costs in buying and selling securities than if it issued and redeemed Creation Units principally in-kind. In addition, the performance of the Fund and its Underlying Index may vary due to asset valuation differences and differences between the Fund’s portfolio and its Underlying Index resulting from legal restrictions, cost or liquidity constraints.

|

|

12 |

|

Equity Risk. Equity risk is the risk that the value of the securities the Subsidiary holds will fall due to general market and economic conditions, perceptions regarding the industries in which the issuers of securities the Subsidiary holds participate or factors relating to specific companies in which the Subsidiary invests. For example, an adverse event, such as an unfavorable earnings report, may depress the value of securities the Subsidiary holds; the price of securities may be particularly sensitive to general movements in the stock market; or a drop in the stock market may depress the price of most or all of the securities the Subsidiary holds. In addition, securities of an issuer in the Subsidiary’s portfolio may decline in price if the issuer fails to make anticipated dividend payments because, among other reasons, the issuer of the security experiences a decline in its financial condition.

Currency Risk. The Fund, through the Subsidiary, invests in Indian rupee-denominated equity securities of Indian issuers. Because the Fund’s NAV is determined in U.S. dollars, the Fund’s NAV could decline if the Indian rupee depreciates against the U.S. dollar, even if the value of the Subsidiary’s holdings, measured in Indian rupees, increases.

Indian Securities Risk. Investment in Indian securities involves risks in addition to those associated with investments in securities of issuers in more developed countries, which may adversely affect the value of the Fund’s assets. Such heightened risks include, among others, political and legal uncertainty, greater government control over the economy, currency fluctuations or blockage and the risk of nationalization or expropriation of assets. In addition, religious and border disputes persist in India. Certain restrictions on foreign investment may decrease the liquidity of the Fund’s portfolio or inhibit the Fund’s ability to track the Underlying Index. The Fund’s investment in securities of issuers located or operating in India as well as its ability to track the Underlying Index may be limited or prevented at times, due to the limits on foreign ownership imposed by the Reserve Bank of India.

Regulatory Risk. The Adviser is a qualified foreign institutional investor (“FII”) with the Securities and Exchange Board of India (“SEBI”), and the Subsidiary is registered as a sub-account with the SEBI in order to obtain certain benefits relating to the Fund’s ability to make and dispose of investments. There can be no assurances that the Indian regulatory authorities will continue to grant such qualifications, and the loss of such qualifications could adversely impact the ability of the Fund to make investments in India.

The Subsidiary’s investments will be made in accordance with investment restrictions prescribed under the FII regulation. If new policy announcements or regulations in India are made which require retrospective changes in the structure or operations of the Fund, these may adversely impact the performance of the Fund.

Cash Transaction Risk. Unlike most exchange-traded funds (“ETFs”), the Fund currently intends to effect creations and redemptions principally for cash, rather than principally in-kind because of the nature of the Subsidiary’s investments. As such, investments in the Shares may be less tax efficient than investments in conventional ETFs.

Subsidiary Investment Risk. Changes in the laws of India and/or Mauritius could prevent the Subsidiary from operating as intended and/or from continuing to qualify as a Mauritius resident for tax purposes and negatively affect the Fund and its shareholders. Additionally, changes in the provisions of the Tax Treaty could result in the imposition of various taxes on the Subsidiary by India, thereby reducing the return to the Fund on its investments. The governments of India and Mauritius have entered into a protocol, amending the Tax Treaty to phase out the capital gains tax exemption on shares of Indian companies. No assurance can be given that the terms of such amendment will not be subject to interpretation and/or renegotiation.

Tax Risk. The Fund expects that the Subsidiary may be eligible to receive favorable tax treatment pursuant to the Tax Treaty. However, if India and Mauritius were to further re-negotiate the Tax Treaty, any change could result in the imposition of withholding and other taxes on the Subsidiary by India, which would reduce the Fund’s return.

Indian tax authorities recently have adopted an aggressive position towards claims of tax exemptions available under tax treaties, and often challenge claims for various reasons.

General anti-avoidance rules (“GAAR”) were implemented in India for the financial year beginning April 1, 2017. The Indian tax authorities may disregard any arrangement whose main purpose is to obtain a tax benefit. If any such arrangement were determined, tax benefits may be eliminated, thereby adversely affecting the Fund’s or the Subsidiary’s business and financial conditions.

C. Taxes

The Fund intends to comply with the provisions of the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”), applicable to regulated investment companies and to distribute substantially all of the Fund’s taxable earnings to its shareholders. As such, the Fund will not be subject to federal income taxes on otherwise taxable income (including net realized gains) that is distributed to the shareholders. Therefore, no provision for federal income taxes is recorded in the consolidated financial statements. Under the applicable foreign tax laws, a withholding tax may be imposed on interest, dividends and capital gains at various rates.

The Fund recognizes the tax benefits of uncertain tax positions only when the position is more likely than not to be sustained. Management has analyzed the Fund’s uncertain tax positions and concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions. Management is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next 12 months.

|

|

13 |

|

Income and capital gain distributions are determined in accordance with federal income tax regulations, which may differ from accounting principles generally accepted in the United States of America (“GAAP”). These differences are primarily due to differing book and tax treatments for in-kind transactions, losses deferred due to wash sales and passive foreign investment company adjustments, if any.

The Fund files U.S. federal tax returns and tax returns in certain other jurisdictions. Generally, the Fund is subject to examinations by such taxing authorities for up to three years after the filing of the return for the tax period.

On May 10, 2016, India and Mauritius signed a protocol amending their Tax Treaty. With this protocol, Mauritius entities are subject to a 15% short-term capital gains tax in India on the sale of shares of Indian resident companies purchased on or after April 1, 2017. The protocol grandfathers shares acquired on or before March 31, 2017, so that gains on these shares will remain exempt from taxation irrespective of their date of disposal. In addition, during a transition period from April 1, 2017 through March 31, 2019, the tax rate will be limited to 50% of the domestic tax rate in India on such gains, subject to fulfillment of conditions in the Limitation of Benefits article of the Tax Treaty. Gains arising on shares acquired on or after April 1, 2017, and transferred on or after April 1, 2019 will be taxed fully in India as per the India tax laws. It is important to note that the amendments to the capital gains article in the protocol relates to the taxation of shares only and would not affect the taxation of other “securities.” The protocol could reduce the return to the Fund on its investments made on or after April 1, 2017 and the return received by Fund shareholders.

The Fund has obtained a tax residence certificate from the Mauritian authorities and believes such certification is determinative of its resident status for Tax Treaty purposes. A fund that is a tax resident in Mauritius under the Tax Treaty, but has no branch or permanent establishment in India, will not be subject to capital gains tax in India on the sale of securities but will be subject to Indian withholding tax on interest earned on Indian debt securities at a rate of 20.6% to 21.63%, depending on the nature of the underlying debt security. Interest arising in India and paid to a resident in Mauritius may be taxed in India, but the tax cannot exceed 7.5% of the gross amount of interest if the Mauritian resident is the beneficial owner of the interest income. Dividends from Indian companies are paid to the Fund free of Indian tax. With respect to Mauritian taxes, the Fund is subject to income tax in Mauritius on its net income at 15%. However, the Fund is entitled to a foreign tax credit equivalent to the higher of the actual foreign tax suffered and 80% of the Mauritius tax on its foreign source income. A company holding at least 5% of the share capital of an Indian company and receiving dividends may claim a credit for the tax paid by the Indian company on its profits out of which dividends were distributed including the Dividend Distribution Tax. Consequently, for the current period, the Fund is expected to be subject to a maximum effective rate of tax of 3% in Mauritius on its net dividend and interest income. Further, the Fund is not subject to taxes on capital gains in Mauritius.

There is no assurance that the terms of the Tax Treaty will not be subject to additional renegotiation or a different interpretation of the Tax Treaty in the future or that the Subsidiary will continue to be deemed a tax resident by Mauritius, allowing favorable tax treatment. Any change in the provisions of this Tax Treaty or in its applicability to the Subsidiary could result in the imposition of withholding and other taxes on the Subsidiary by India, which would reduce the return to the Fund on its investment.

D. Investment Transactions and Investment Income

Investment transactions are accounted for on a trade date basis. Realized gains and losses from the sale or disposition of securities are computed on the specific identified cost basis. Interest income is recorded on the accrual basis from settlement date. Pay-in-kind interest income and non-cash dividend income received in the form of securities in-lieu of cash are recorded at the fair value of the securities received. Dividend income (net of withholding tax, if any) is recorded on the ex-dividend date. Realized gains, dividends and interest received by the Fund may give rise to withholding and other taxes imposed by foreign countries. Tax conventions between certain countries and the United States may reduce or eliminate such taxes.

The Fund may periodically participate in litigation related to Fund investments. As such, the Fund may receive proceeds from litigation settlements. Any proceeds received are included in the Consolidated Statement of Operations as realized gain (loss) for investments no longer held and as unrealized gain (loss) for investments still held.

Brokerage commissions and mark ups are considered transaction costs and are recorded as an increase to the cost basis of securities purchased and/or a reduction of proceeds on a sale of securities. Such transaction costs are included in the determination of net realized and unrealized gain (loss) from investment securities reported in the Consolidated Statement of Operations and the Consolidated Statement of Changes in Net Assets and the net realized and unrealized gains (losses) on securities per share in the Financial Highlights. Transaction costs are included in the calculation of the Fund’s NAV and, accordingly, they reduce the Fund’s total returns. These transaction costs are not considered operating expenses and are not reflected in net investment income reported in the Consolidated Statement of Operations and the Consolidated Statement of Changes in Net Assets, or the net investment income per share and the ratios of expenses and net investment income reported in the Financial Highlights, nor are they limited by any expense limitation arrangements between the Fund and the Adviser.

E. Country Determination

For the purposes of making investment selection decisions and presentation in the Consolidated Schedule of Investments, the Adviser may determine the country in which an issuer is located and/or credit risk exposure based on various factors. These factors include the

|

|

14 |

|

laws of the country under which the issuer is organized, where the issuer maintains a principal office, the country in which the issuer derives 50% or more of its total revenues and the country that has the primary market for the issuer’s securities, as well as other criteria. Among the other criteria that may be evaluated for making this determination are the country in which the issuer maintains 50% or more of its assets, the type of security, financial guarantees and enhancements, the nature of the collateral and the sponsor organization. Country of issuer and/or credit risk exposure has been determined to be the United States of America, unless otherwise noted.

F. Expenses

The Fund has agreed to pay an annual unitary management fee to the Adviser. Out of the unitary management fee, the Adviser has agreed to pay for substantially all expenses of the Fund and Subsidiary, including the cost of transfer agency, custody, fund administration, legal, audit and other services, except for advisory fees, distribution fees, if any, brokerage expenses, taxes, interest, acquired fund fees and expenses, if any, litigation expenses and other extraordinary expenses.

To the extent the Fund invests in other investment companies, the expenses shown in the accompanying consolidated financial statements reflect the expenses of the Fund and do not include any expenses of the investment companies in which it invests. The effects of such investment companies’ expenses are included in the realized and unrealized gain or loss on the investments in the investment companies.

G. Dividends and Distributions to Shareholders

The Fund declares and pays dividends from net investment income, if any, to its shareholders quarterly and records such dividends on ex-dividend date. Generally, the Fund distributes net realized taxable capital gains, if any, annually in cash and records them on ex-dividend date. Such distributions on a tax basis are determined in conformity with income tax regulations, which may differ from GAAP. Distributions in excess of tax basis earnings and profits, if any, are reported in the Fund’s consolidated financial statements as a tax return of capital at fiscal year-end.

H. Accounting Estimates

The preparation of the financial statements on a consolidated basis in accordance with GAAP requires management to make estimates and assumptions that affect the reported amounts and disclosures in the consolidated financial statements, including estimates and assumptions related to taxation. Actual results could differ from those estimates. In addition, the Fund monitors for material events or transactions that may occur or become known after the period end date and before the date the consolidated financial statements are released to print. All inter-company accounts and transactions have been eliminated in consolidation.

I. Foreign Currency Translations

Foreign currency is valued at the close of the NYSE based on quotations posted by banks and major currency dealers. Portfolio securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollar amounts at date of valuation. Purchases and sales of portfolio securities (net of foreign taxes withheld on disposition) and income items denominated in foreign currencies are translated into U.S. dollar amounts on the respective dates of such transactions. The Fund does not separately account for the portion of the results of operations resulting from changes in foreign exchange rates on investments and the fluctuations arising from changes in market prices of securities held. The combined results of changes in foreign exchange rates and the fluctuation of market prices on investments (net of estimated foreign tax withholding) are included with the net realized and unrealized gain or loss from investments in the Consolidated Statement of Operations. Reported net realized foreign currency gains or losses arise from (1) sales of foreign currencies, (2) currency gains or losses realized between the trade and settlement dates on securities transactions, and (3) the difference between the amounts of dividends, interest, and foreign withholding taxes recorded on the Fund’s books and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign currency gains and losses arise from changes in the fair values of assets and liabilities, other than investments in securities at fiscal period end, resulting from changes in exchange rates.

The Fund may invest in foreign securities, which may be subject to foreign taxes on income, gains on investments or currency repatriation, a portion of which may be recoverable. Foreign taxes, if any, are recorded based on the tax regulations and rates that exist in the foreign markets in which the Fund invests.

Note 3. Investment Advisory Agreement and Other Agreements

The Trust has entered into an Investment Advisory Agreement with the Adviser on behalf of the Fund, pursuant to which the Adviser has overall responsibility for the selection and ongoing monitoring of the Fund’s investments, managing the Fund’s business affairs and providing certain clerical, bookkeeping and other administrative services.

As compensation for its services, the Fund accrues daily and pays monthly to the Adviser an annual unitary management fee of 0.78% of the Fund’s average daily net assets. Out of the unitary management fee, the Adviser has agreed to pay for substantially all expenses of the Fund and Subsidiary, including the cost of transfer agency, custody, fund administration, legal, audit and other services, except for advisory fees, distribution fees, if any, brokerage expenses, taxes, interest, acquired fund fees and expenses, if any, litigation expenses and other extraordinary expenses.

|

|

15 |

|

The Trust has entered into a Distribution Agreement with Invesco Distributors, Inc. (the “Distributor”), which serves as the distributor of Creation Units for the Fund. The Distributor does not maintain a secondary market in the Shares. The Fund is not charged any fees pursuant to the Distribution Agreement. The Distributor is an affiliate of the Adviser.

The Adviser has entered into a licensing agreement for the Fund with Indus Advisors LLC (the “Licensor”). The Underlying Index name trademark is owned by the Licensor. The trademark has been licensed to the Adviser for use by the Fund. The Fund is entitled to use the Underlying Index pursuant to the Trust’s sub-licensing agreement with the Adviser. The Fund is not sponsored, endorsed, sold or promoted by the Licensor, and the Licensor makes no representation regarding the advisability of investing in the Fund. The Fund is not a party to the licensing agreement.

The Trust has entered into service agreements whereby Brown Brothers Harriman & Co. serves as the administrator, custodian, fund accountant and transfer agent for the Fund.

Note 4. Additional Valuation Information

GAAP defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date, under current market conditions. GAAP establishes a hierarchy that prioritizes the inputs to valuation methods, giving the highest priority to readily available unadjusted quoted prices in an active market for identical assets (Level 1) and the lowest priority to significant unobservable inputs (Level 3), generally when market prices are not readily available or are unreliable. Based on the valuation inputs, the securities or other investments are tiered into one of three levels. Changes in valuation methods may result in transfers in or out of an investment’s assigned level:

| Level 1 — | Prices are determined using quoted prices in an active market for identical assets. |

| Level 2 — | Prices are determined using other significant observable inputs. Observable inputs are inputs that other market participants may use in pricing a security. These may include quoted prices for similar securities, interest rates, prepayment speeds, credit risk, yield curves, loss severities, default rates, discount rates, volatilities and others. |

| Level 3 — | Prices are determined using significant unobservable inputs. In situations where quoted prices or observable inputs are unavailable (for example, when there is little or no market activity for an investment at the end of the period), unobservable inputs may be used. Unobservable inputs reflect the Fund’s own assumptions about the factors market participants would use in determining fair value of the securities or instruments and would be based on the best available information. |

As of October 31, 2017, all securities in the Fund were valued based on Level 2 inputs, except for the Short-Term Instruments—Time Deposits which were valued based on Level 1 inputs (see the Consolidated Schedule of Investments for security categories). The level assigned to the securities valuations may not be an indication of the risk or liquidity associated with investing in those securities. Because of the inherent uncertainties of valuation, the values reflected in the consolidated financial statements may materially differ from the value received upon actual sale of those investments.

The Fund’s policy is to recognize transfers in and out of the valuation levels as of the end of the reporting period. For the year ended October 31, 2017, there were transfers from Level 1 to Level 2 of $261,807,757, due to foreign fair value adjustments.

Note 5. Distributions to Shareholders and Tax Components of Net Assets

Tax Character of Distributions to Shareholders Paid During the Fiscal Years Ended October 31, 2017 and 2016:

| 2017 | 2016 | |||||||

| Ordinary Income | $ | 3,226,186 | $ | 4,357,432 | ||||

Tax Components of Net Assets at Fiscal Year-end:

| Undistributed Ordinary Income |

Net Unrealized Appreciation— Investments |

Net Unrealized Appreciation— Foreign Currencies |

Capital Loss Carryforward |

Shares of Beneficial Interest |

Total Net Assets |

|||||||||||||||||

| $ | — | $ | 103,974,741 | $ | 229 | $ | (64,968,791 | ) | $ | 253,863,951 | $ | 292,870,130 | ||||||||||

The differences between book-basis and tax-basis unrealized appreciation (depreciation) is due to differences in the timing of recognition of gains and losses on investments for tax and book purposes. The Fund’s net unrealized appreciation difference is attributable primarily to wash sales.

Capital loss carryforwards are calculated and reported as of a specific date. Results of transactions and other activity after that date may affect the amount of capital loss carryforward actually available for the Fund to utilize. Capital losses generated in years beginning after December 22, 2010 can be carried forward for an unlimited period, whereas previous losses expire in eight tax years. Capital losses with an expiration period may not be used to offset capital gains until all net capital losses without expiration date have been

|

|

16 |

|

utilized. Capital loss carryforwards with no expiration date will retain their character as either short-term or long-term capital losses instead of as short-term capital losses as under prior law. The ability to utilize capital loss carryforwards in the future may be limited under the Internal Revenue Code and related regulations based on the results of future transactions.

The Fund had capital loss carryforwards as of October 31, 2017, which expire as follows:

| Capital Loss Carryforward* | ||||||||||||

| Expiration |

Short-Term | Long-Term | Total | |||||||||

| October 31, 2018 | $ | 2,587,911 | $ | — | $ | 2,587,911 | ||||||

| October 31, 2019 | 15,322,005 | — | 15,322,005 | |||||||||

| Not subject to expiration | 30,697,840 | 16,361,035 | 47,058,875 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total capital loss carryforward | $ | 48,607,756 | $ | 16,361,035 | $ | 64,968,791 | ||||||

|

|

|

|

|

|

|

|||||||

| * | Capital loss carryforwards as of the date listed above are reduced for limitations, if any, to the extent required by the Internal Revenue Code and may be further limited depending upon a variety of factors, including the realization of net unrealized gains or losses as of the date of any reorganization. |

Note 6. Investment Transactions

For the fiscal year ended October 31, 2017, the cost of securities purchased and proceeds from sales of securities (other than short-term securities, if any) were $78,413,692 and $251,181,518, respectively.

At October 31, 2017, the aggregate cost of investments, including any derivatives, on a tax basis includes adjustments for financial reporting purposes, as of the most recently completed federal income tax reporting year-end:

| Aggregate unrealized appreciation of investments | $ | 138,012,343 | ||

| Aggregate unrealized (depreciation) of investments | (34,037,602 | ) | ||

|

|

|

|||

| Net unrealized appreciation of investments | $ | 103,974,741 | ||

|

|

|

|||

| Cost of investments for tax purposes is $188,628,093. |

Note 7. Reclassification of Permanent Differences

Primarily as a result of differing book/tax treatment of investment activity, undistributed net realized gain (loss) was increased by $3,557,723 and undistributed net investment income and shares of beneficial interest were decreased by $267,974 and $3,289,749, respectively. These reclassifications had no effect on the net assets of the Fund.

Note 8. Trustees’ and Officer’s Fees

Trustees’ and Officer’s Fees include amounts accrued by the Fund to pay remuneration to each Trustee who is not an “interested person” as defined in the 1940 Act (an “Independent Trustee”), any Trustee who is not an affiliate of the Adviser or Distributor (or any of their affiliates) and who is otherwise an “interested person” of the Trust under the 1940 Act (an “Unaffiliated Trustee”) and an Officer of the Trust. The Adviser, as a result of the Fund’s unitary management fee, pays for such compensation. The Trustee who is an “interested person” of the Trust does not receive any Trustees’ fees.

The Trust has adopted a deferred compensation plan (the “Plan”). Under the Plan, each Independent Trustee or Unaffiliated Trustee who has executed a Deferred Fee Agreement (a “Participating Trustee”) may defer receipt of all or a portion of his compensation (“Deferral Fees”). Such Deferral Fees are deemed to be invested in select PowerShares Funds. The Deferral Fees payable to the Participating Trustee are valued as of the date such Deferral Fees would have been paid to the Participating Trustee. The value increases with contributions or with increases in the value of the Shares selected, and the value decreases with distributions or with declines in the value of the Shares selected. Obligations under the Plan represent unsecured claims against the general assets of the Fund.

Note 9. Capital

Shares are created and redeemed by the Fund only in Creation Units of 50,000 Shares. Only Authorized Participants are permitted to purchase or redeem Creation Units from the Fund. Unlike most ETFs, the Fund currently effects creations and redemptions principally in exchange for the deposit or delivery of cash, rather than principally in exchange for the deposit or delivery of a basket of securities (“Deposit Securities”). If an in-kind transaction is permitted, there will be a balancing cash component to equate the transaction to the NAV per Share of the Fund on the transaction date. However, cash in an amount equivalent to the value of certain securities may be substituted for any otherwise permitted in-kind transaction, generally when the securities are not available in sufficient quantity for delivery, not eligible for trading by the Authorized Participant or as a result of other market circumstances.

To the extent that the Fund permits transactions in exchange for Deposit Securities, the Fund may issue Shares in advance of receipt of Deposit Securities subject to various conditions, including a requirement to maintain on deposit with the Trust cash at least equal to 105% of the market value of the missing Deposit Securities. In accordance with the Trust’s Participant Agreement, Creation Units will be issued to an Authorized Participant, notwithstanding the fact that the corresponding Deposit Securities have not been received in part or in whole, in reliance on the undertaking of the Authorized Participant to deliver the missing Deposit Securities as soon as

|

|

17 |

|

possible, which undertaking shall be secured by the Authorized Participant’s delivery and maintenance of collateral consisting of cash in the form of U.S. dollars in immediately available funds having a value (marked-to-market daily) at least equal to 105%, which the Adviser may change from time to time, of the value of the missing Deposit Securities.

Certain transaction fees may be charged by the Fund for creations and redemptions, which are treated as increases in capital.

Transactions in the Fund’s Shares are disclosed in detail in the Consolidated Statement of Changes in Net Assets.

Note 10. Indemnifications

Under the Trust’s organizational documents, its Officers and Trustees are indemnified against certain liabilities arising out of the performance of their duties to the Fund. Also, under the Subsidiary’s organizational documents, the directors and officers of the Subsidiary are indemnified against certain liabilities that may arise out of the performance of their duties to the Fund and/or the Subsidiary, respectively. Each Independent Trustee and Unaffiliated Trustee is also indemnified against certain liabilities arising out of the performance of his duties to the Trust pursuant to an Indemnification Agreement between such trustee and the Trust. Additionally, in the normal course of business, the Trust enters into contracts with service providers that contain general indemnification clauses. The Trust’s maximum exposure under these arrangements is unknown, as this would involve, future claims that may be made against the Trust that have not yet occurred. However, based on experience, the Trust believes the risk of loss to be remote.

Note 11. Subsequent Event

The Trust entered into service agreements with The Bank of New York Mellon, a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BYNM”), pursuant to which BNYM serves as the administrator, custodian, fund accountant and transfer agent for the Fund beginning November 1, 2017.

|

|

18 |

|

Report of Independent Registered Public Accounting Firm

To the Board of Trustees of PowerShares India Exchange-Traded Fund Trust and Shareholders of the PowerShares India Portfolio

In our opinion, the accompanying consolidated statement of assets and liabilities, including the consolidated schedule of investments, and the related consolidated statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the consolidated financial position of the PowerShares India Portfolio and its subsidiary (constituting PowerShares India Exchange-Traded Fund Trust, hereafter collectively referred to as the “Fund”) as of October 31, 2017, the results of their operations for the year then ended, the changes in their net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These consolidated financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities as of October 31, 2017 by correspondence with the custodian, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Chicago, IL

December 26, 2017

|

|

19 |

|

As a shareholder of the PowerShares India Exchange-Traded Fund Trust (the “Fund”), you incur a unitary management fee. In addition to the unitary management fee, a shareholder may pay distribution fees, if any, brokerage expenses, taxes, interest, litigation expenses and other extraordinary expenses (including acquired fund fees and expenses, if any). The expense example below is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held through the six-month period ended October 31, 2017.

Actual Expenses

The first line in the following table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expense Paid During the Six-Month Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line in the following table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annualized rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only, and do not reflect any transactional costs such as sales charges and brokerage commissions. Therefore, the second line in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value May 1, 2017 |

Ending Account Value October 31, 2017 |

Annualized Expense Ratio Six-Month Period |

Expenses Paid During the Six-Month Period(1) |

|||||||||||||

| Actual | $ | 1,000.00 | $ | 1,117.70 | 0.75 | % | $ | 4.02 | ||||||||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,021.41 | 0.75 | 3.83 | ||||||||||||

| (1) | Expenses are calculated using the annualized expense ratio, which represents the ongoing expenses as a percentage of net assets for the six-months ended October 31, 2017. Expenses are calculated by multiplying the Fund’s annualized expense ratio by the average account value for the period, then multiplying the result by 184/365. Expense ratios for the most recent six-month period may differ from expense ratios based on the annualized data in the Financial Highlights. |

|

|

20 |

|

Form 1099-DIV, Form 1042-S and other year-end tax information provide shareholders with actual calendar year amounts that should be included in their tax returns. Shareholders should consult their tax advisers.

The following distribution information is being provided as required by the Internal Revenue Code or to meet a specific state’s requirement.

The Fund designates the following amounts or, if subsequently determined to be different, the maximum amount allowable for its fiscal year ended October 31, 2017:

| Qualified Dividend Income* |

Dividends-Received Deduction* | |||||||||

| 100.00 | % | 0.00 | % | |||||||

| * | The above percentages are based on ordinary income dividends paid to shareholders during the Fund’s fiscal year. |

|

|

21 |

|

The Independent Trustees, the Unaffiliated Trustees, the Non-Independent Trustees and the executive officers of the Trust, their term of office and length of time served, their principal business occupations during at least the past five years, the number of portfolios in the Fund Complex overseen by each Trustee and the other directorships, if any, held by a Trustee are shown below.

The Trustees and Officers information is current as of October 31, 2017.

The Independent Trustees of the Trust, their term of office and length of time served, their principal business occupations during at least the past five years, the number of portfolios in the Fund Complex (as defined below) overseen by each Independent Trustee and the other directorships, if any, held by each Independent Trustee are shown below.

| Name, Address and Year of Birth of Independent Trustees |

Position(s) Held with Trust |

Term of Office and Length of Time Served* |

Principal Occupation(s) During Past 5 Years |

Number of Portfolios in Fund Complex** Overseen by Independent Trustees |

Other Directorships Held by Independent Trustees During the Past 5 Years | |||||

| Ronn R. Bagge—1958 c/o Invesco PowerShares Capital Management LLC 3500 Lacey Road, Suite 700 Downers Grove, IL 60515 |

Chairman of the Nominating and Governance Committee and Trustee | Chairman of the Nominating and Governance Committee and Trustee since 2008 | Founder and Principal, YQA Capital Management LLC (1998-Present); formerly Owner/CEO of Electronic Dynamic Balancing Co., Inc. (high-speed rotating equipment service provider). | 154 | None | |||||

| Todd J. Barre—1957 c/o Invesco PowerShares Capital Management LLC 3500 Lacey Road, Suite 700 Downers Grove, IL 60515 |

Trustee | Since 2010 | Assistant Professor of Business, Trinity Christian College (2010-2016); formerly Vice President and Senior Investment Strategist (2001-2008), Director of Open Architecture and Trading (2007-2008), Head of Fundamental Research (2004-2007) and Vice President and Senior Fixed Income Strategist (1994-2001), BMO Financial Group/Harris Private Bank. | 154 | None | |||||

| Marc M. Kole—1960 c/o Invesco PowerShares Capital Management LLC 3500 Lacey Road, Suite 700 Downers Grove, IL 60515 |

Chairman of the Audit Committee and Trustee | Chairman of the Audit Committee and Trustee since 2008 | Senior Director of Finance, By The Hand Club for Kids (2015-Present); formerly: Chief Financial Officer, Hope Network (social services) (2008-2012); Assistant Vice President and Controller, Priority Health (health insurance) (2005-2008); Senior Vice President of Finance, United Healthcare (2004-2005); Chief Accounting Officer, Senior Vice President of Finance, Oxford Health Plans (2000-2004); Audit Partner, Arthur Andersen LLP (1996-2000). | 154 | None | |||||

| * | This is the date the Independent Trustee began serving the Trust. Each Trustee serves an indefinite term, until his successor is elected. |

| ** | Fund Complex includes all open-end funds (including all of their portfolios) advised by the Adviser. At October 31, 2017, the Fund Complex consisted of the Trust’s 1 portfolio and four other exchange-traded fund trusts with 153 portfolios advised by the Adviser. |

|

|

22 |

|

Trustees and Officers (continued)

| Name, Address and Year of Birth of Independent Trustees |

Position(s) Held with Trust |

Term of Office and Length of Time Served* |

Principal Occupation(s) During Past 5 Years |

Number of Portfolios in Fund Complex** Overseen by Independent Trustees |

Other Directorships Held by Independent Trustees During the Past 5 Years | |||||

| Yung Bong Lim—1964 c/o Invesco PowerShares Capital Management LLC 3500 Lacey Road, Suite 700 Downers Grove, IL 60515 |

Chairman of the Investment Oversight Committee and Trustee | Chairman of the Investment Oversight Committee since 2014; Trustee since 2013 | Managing Partner, RDG Funds LLC (2008-Present); formerly, Managing Director, Citadel LLC. (1999-2007). | 154 | None | |||||

| Gary R. Wicker—1961 c/o Invesco PowerShares Capital Management LLC 3500 Lacey Road, Suite 700 Downers Grove, IL 60515 |

Trustee | Since 2013 | Senior Vice President of Global Finance and Chief Financial Officer at RBC Ministries (publishing company) (2013-Present); formerly, Executive Vice President and Chief Financial Officer, Zondervan Publishing (a division of Harper Collins/NewsCorp) (2007-2012); Senior Vice President and Group Controller (2005-2006), Senior Vice President and Chief Financial Officer (2003-2004), Chief Financial Officer (2001-2003), Vice President, Finance and Controller (1999-2001) and Assistant Controller (1997-1999), divisions of The Thomson Corporation (information services provider). | 154 | None | |||||

| Donald H. Wilson—1959 c/o Invesco PowerShares Capital Management LLC 3500 Lacey Road, Suite 700 Downers Grove, IL 60515 |

Chairman of the Board and Trustee | Chairman since 2012; Trustee since 2008 | Chairman and Chief Executive Officer, Stone Pillar Advisors, Ltd. (2010-Present); President and Chief Executive Officer, Stone Pillar Investments, Ltd. (2016-Present); formerly, Chairman, President and Chief Executive Officer, Community Financial Shares, Inc. and Community Bank—Wheaton/Glen Ellyn (subsidiary) (2013-2015); Chief Operating Officer, AMCORE Financial, Inc. (bank holding company) (2007-2009); Executive Vice President and Chief Financial Officer, AMCORE Financial, Inc. (2006-2007); Senior Vice President and Treasurer, Marshall & Ilsley Corp. (bank holding company) (1995-2006). | 154 | None | |||||

| * | This is the date the Independent Trustee began serving the Trust. Each Trustee serves an indefinite term, until his successor is elected. |

| ** | Fund Complex includes all open-end funds (including all of their portfolios) advised by the Adviser. At October 31, 2017, the Fund Complex consisted of the Trust’s 1 portfolio and four other exchange-traded fund trusts with 153 portfolios advised by the Adviser. |

|

|

23 |

|

Trustees and Officers (continued)

The Unaffiliated Trustee, his term of office and length of time served, his principal business occupations during the past five years, the number of portfolios in the Fund Complex (as defined below) overseen by the Unaffiliated Trustee and the other directorships, if any, held by the Unaffiliated Trustee are shown below.

| Name, Address and Year of Birth of Unaffiliated Trustee |

Position(s) Held with Trust |

Term of Office and Length of Time Served* |

Principal Occupation(s) During Past 5 Years |

Number of Portfolios in Fund Complex** Overseen by Unaffiliated Trustee |

Other Directorships Held by Unaffiliated Trustee During the Past 5 Years | |||||

| Philip M. Nussbaum—1961 c/o Invesco PowerShares Capital Management LLC 3500 Lacey Road, Suite 700 Downers Grove, IL 60515 |

Trustee | Since 2008 | Chairman, Performance Trust Capital Partners (2004-Present). | 154 | None |

| * | This is the date the Unaffiliated Trustee began serving the Trust. The Unaffiliated Trustee serves an indefinite term, until his successor is elected. |

| ** | Fund Complex includes all open-end funds (including all of their portfolios) advised by the Adviser. At October 31, 2017, the Fund Complex consisted of the Trust’s 1 portfolio and four other exchange-traded fund trusts with 153 portfolios advised by the Adviser. |

|

|

24 |

|

Trustees and Officers (continued)

The Interested Trustee and the executive officers of the Trust, their term of office and length of time served, their principal business occupations during the past five years, the number of portfolios in the Fund Complex (as defined below) overseen by the Interested Trustee and the other directorships, if any, held by the Interested Trustee are shown below.

| Name, Address and Year of Birth of Interested Trustee |

Position(s) Held with Trust |

Term of Office and Length of Time Served* |

Principal Occupation(s) During Past 5 Years |

Number of Portfolios in Fund Complex** Overseen by Interested Trustee |

Other Directorships Held by Interested Trustee During the Past 5 Years | |||||

| Kevin M. Carome—1956 Invesco Ltd. Two Peachtree Pointe, 1555 Peachtree St., N.E., Suite 1800 Atlanta, GA 30309 |

Trustee | Since 2010 | Senior Managing Director, Secretary and General Counsel, Invesco Ltd. (2007-Present); Director, Invesco Advisers, Inc. (2009-Present); Director (2006-Present) and Executive Vice President (2008-Present), Invesco Group Services, Inc., Invesco Holding Company (US), Inc. and Invesco North American Holdings, Inc.; Director, Invesco Holding Company Limited (2007-Present); Executive Vice President (2008-Present), Invesco Investments (Bermuda) Ltd.; Manager, Horizon Flight Works LLC, Director and Executive Vice President, Invesco Finance, Inc. and Director, Invesco Finance PLC (2011-Present); Director and Secretary (2012-Present), Invesco Services (Bahamas) Private Limited; and Director and Executive Vice President (2014-Present), INVESCO Asset Management (Bermuda) Ltd.; formerly, Director and Chairman, INVESCO Funds Group, Inc., Senior Vice President, Secretary and General Counsel, Invesco Advisers, Inc. (2003-2006); Director, Invesco Investments (Bermuda) Ltd. (2008-2016); Senior Vice President and General Counsel, Liberty Financial Companies, Inc. (2000-2001); General Counsel of certain investment management subsidiaries of Liberty Financial Companies, Inc. (1998-2000); Associate General Counsel, Liberty Financial Companies, Inc. (1993-1998); Associate, Ropes & Gray LLP. | 154 | None |

| * | This is the date the Interested Trustee began serving the Trust. The Interested Trustee serves an indefinite term, until his successor is elected. |

| ** | Fund Complex includes all open-end funds (including all of their portfolios) advised by the Adviser. At October 31, 2017, the Fund Complex consisted of the Trust’s 1 portfolio and four other exchange-traded fund trusts with 153 portfolios advised by the Adviser. |

|

|

25 |

|

Trustees and Officers (continued)

| Name, Address and Year of Birth of Executive Officers |

Position(s) Held with Trust |

Length of Time Served* |

Principal Occupation(s) During Past 5 Years | |||

| Daniel E. Draper—1968 Invesco PowerShares Capital Management LLC 3500 Lacey Road, Suite 700 Downers Grove, IL 60515 |

President and Principal Executive Officer |

Since 2015 | President and Principal Executive Officer, PowerShares Exchange-Traded Fund Trust, PowerShares Exchange-Traded Fund Trust II, PowerShares India Exchange-Traded Fund Trust, PowerShares Actively Managed Exchange-Traded Fund Trust and PowerShares Actively Managed Exchange-Traded Commodity Fund Trust (2015-Present); Chief Executive Officer and Principal Executive Officer (2016-Present) and Managing Director (2013-Present), Invesco PowerShares Capital Management LLC; Senior Vice President, Invesco Distributors, Inc. (2014-Present); formerly, Vice President, PowerShares Exchange-Traded Fund Trust, PowerShares Exchange-Traded Fund Trust II, PowerShares India Exchange-Traded Fund Trust, PowerShares Actively Managed Exchange-Traded Fund Trust (2013-2015) and PowerShares Actively Managed Exchange-Traded Commodity Fund Trust (2014-2015); Managing Director, Credit Suisse Asset Management (2010-2013) and Lyxor Asset Management/Societe Generale (2007-2010). | |||

| Steven M. Hill—1964 Invesco PowerShares Capital Management LLC 3500 Lacey Road, Suite 700 Downers Grove, IL 60515 |

Vice President and Treasurer |

Since 2013 | Vice President and Treasurer, PowerShares Exchange-Traded Fund Trust, PowerShares Exchange-Traded Fund Trust II, PowerShares India Exchange-Traded Fund Trust, PowerShares Actively Managed Exchange-Traded Fund Trust (2013-Present) and PowerShares Actively Managed Exchange-Traded Commodity Fund Trust (2014-Present); Head of Global ETF Administration, Invesco PowerShares Capital Management LLC (2011-Present); Principal Financial and Accounting Officer—Investment Pools, Invesco PowerShares Capital Management LLC (2015-Present); formerly, Senior Managing Director and Chief Financial Officer, Destra Capital Management LLC and its subsidiaries (2010-2011); Chief Financial Officer, Destra Investment Trust and Destra Investment Trust II (2010-2011); Senior Managing Director, Claymore Securities, Inc. (2003-2010); and Chief Financial Officer, Claymore sponsored mutual funds (2003-2010). | |||

| Peter Hubbard—1981 Invesco PowerShares Capital Management LLC 3500 Lacey Road, Suite 700 Downers Grove, IL 60515 |

Vice President | Since 2009 | Vice President, PowerShares Exchange-Traded Fund Trust, PowerShares Exchange-Traded Fund Trust II, PowerShares India Exchange-Traded Fund Trust, PowerShares Actively Managed Exchange-Traded Fund Trust (2009-Present) and PowerShares Actively Managed Exchange-Traded Commodity Fund Trust (2014-Present); Vice President and Director of Portfolio Management, Invesco PowerShares Capital Management LLC (2010-Present); formerly, Vice President of Portfolio Management, Invesco PowerShares Capital Management LLC (2008-2010); Portfolio Manager, Invesco PowerShares Capital Management LLC (2007-2008); Research Analyst, Invesco PowerShares Capital Management LLC (2005-2007); Research Analyst and Trader, Ritchie Capital, a hedge fund operator (2003-2005). | |||

| Sheri Morris—1964 Invesco Management Group, Inc. 11 Greenway Plaza, Suite 1000 Houston, TX 77046 |

Vice President | Since 2012 | President and Principal Executive Officer, The Invesco Funds (2016-Present); Treasurer, The Invesco Funds (2008-Present); Vice President, Invesco Advisers, Inc. (formerly known as Invesco Institutional (N.A.), Inc.) (registered investment adviser) (2009-Present) and Vice President, PowerShares Exchange-Traded Fund Trust, PowerShares Exchange-Traded Fund Trust II, PowerShares India Exchange-Traded Fund Trust, PowerShares Actively Managed Exchange-Traded Fund Trust (2012-Present) and PowerShares Actively Managed Exchange-Traded Commodity Fund Trust (2014-Present); formerly, Vice President and Principal Financial Officer, The Invesco Funds (2008-2016); Treasurer, PowerShares Exchange-Traded Fund Trust, PowerShares Exchange-Traded Fund Trust II, PowerShares India Exchange-Traded Fund Trust and PowerShares Actively Managed Exchange-Traded Fund Trust (2011-2013); Vice President, Invesco Aim Advisers, Inc., Invesco Aim Capital Management, Inc. and Invesco Aim Private Asset Management, Inc.; Assistant Vice President and Assistant Treasurer, The Invesco Funds and Assistant Vice President, Invesco Advisers, Inc., Invesco Aim Capital Management, Inc. and Invesco Aim Private Asset Management, Inc. | |||

| * | This is the period for which the Officers began serving the Trust. Each Officer serves an indefinite term, until his or her successor is elected. |

|

|

26 |

|

Trustees and Officers (continued)

| Name, Address and Year of Birth of Executive Officers |

Position(s) Held with Trust |

Length of Time Served* |

Principal Occupation(s) During Past 5 Years | |||

| Anna Paglia—1974 Invesco PowerShares Capital Management LLC 3500 Lacey Road, Suite 700 Downers Grove, IL 60515 |

Secretary | Since 2011 | Secretary, PowerShares Exchange-Traded Fund Trust, PowerShares Exchange-Traded Fund Trust II, PowerShares India Exchange-Traded Fund Trust, PowerShares Actively Managed Exchange-Traded Fund Trust (2011-Present) and PowerShares Actively Managed Exchange-Traded Commodity Fund Trust (2014-Present); Head of Legal (2010-Present) and Secretary (2015-Present), Invesco PowerShares Capital Management LLC (2010-Present); Manager and Assistant Secretary, Invesco Indexing LLC (2017-Present); formerly, Partner, K&L Gates LLP (formerly, Bell Boyd & Lloyd LLP) (2007-2010); Associate Counsel at Barclays Global Investors Ltd. (2004-2006). | |||

| Rudolf E. Reitmann—1971 Invesco PowerShares Capital Management LLC 3500 Lacey Road, Suite 700 Downers Grove, IL 60515 |

Vice President | Since 2013 | Vice President, PowerShares Exchange-Traded Fund Trust, PowerShares Exchange-Traded Fund Trust II, PowerShares India Exchange-Traded Fund Trust, PowerShares Actively Managed Exchange-Traded Fund Trust (2013-Present) and PowerShares Actively Managed Exchange-Traded Commodity Fund Trust (2014-Present); Head of Global Exchange Traded Funds Services, Invesco PowerShares Capital Management LLC (2013-Present). | |||

| David Warren—1957 Invesco Canada Ltd. 5140 Yonge Street, Suite 800 Toronto, Ontario M2N 6X7 |