Securities Act Registration No. 333-147324

Investment Company Act Registration No. 811-22143

| UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM |

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | [X] |

| Pre-Effective Amendment No. __ | [ ] |

| Post-Effective Amendment No. 38 | [X] |

| And/or | |

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 | [X] |

| Amendment No. 39 | [X] |

(Exact Name of Registrant as Specified in Charter)

| 2691 Route 9, Suite 102 | |

| Malta, NY | 12020 |

| (Address of Principal Executive Offices) | (Zip Code) |

| Registrant’s Telephone Number, including Area Code: (518) 371-3450 Gerard S.E. Heffernan Walthausen Funds 2691 Route 9, Suite 102 Malta, NY 12020 (Name and Address of Agent for Service) Copies to: JoAnn S. Strasser Thompson Hine, LLP 41 South High Street, Suite 1700 Columbus, Ohio 43215 |

| It is proposed that this filing will become effective (check appropriate box) | ||

| [ ] | Immediately upon filing pursuant to paragraph (b) | |

| [X] | on | |

| [ ] | 60 days after filing pursuant to paragraph (a)(1) | |

| [ ] | on (date) pursuant to paragraph (a)(1) | |

| [ ] | on 75 days after filing pursuant to paragraph (a)(2) | |

| [ ] | on (date) pursuant to paragraph (a)(2) of Rule 485. | |

| If appropriate, check the following box: | ||

| [ ] | this post-effective amendment designates a new effective date for a previously | |

| filed post-effective amendment. | ||

PART A

WALTHAUSEN SMALL CAP VALUE FUND

INSTITUTIONAL CLASS TICKER

INVESTOR CLASS TICKER

For Investors Seeking Long-Term Capital Appreciation

PROSPECTUS

As with all mutual funds, the Securities and Exchange Commission has not approved or disapproved of these securities, nor has the Commission determined that this Prospectus is complete or accurate. Any representation to the contrary is a criminal offense.

| Table of Contents | |

| Summary Section | 1 |

| Investment Objective | 1 |

| Fees and Expenses of the Fund | 1 |

| The Principal Investment Strategy of the Fund | 2 |

| The Principal Risks of Investing in the Fund | 2 |

| Performance | 3 |

| Management | 4 |

| Purchase and Sale of Fund Shares | 4 |

| Tax Information | 4 |

| Payments to Broker-Dealers and Other Financial Intermediaries | 4 |

| Cybersecurity | 4 |

| Investment Objective, Principal Investment Strategy, | |

| Related Risks, and Disclosure of Portfolio Holdings | 5 |

| Investment Objective | 5 |

| Principal Investment Strategy of the Fund | 5 |

| The Investment Selection Process Used by the Fund | 5 |

| The Principal Risks of Investing in the Fund | 6 |

| Portfolio Holdings Disclosure | 7 |

| Management | 7 |

| The Investment Advisor | 7 |

| Shareholder Information | 8 |

| Pricing of Fund Shares | 8 |

| Customer Identification Program | 9 |

| Investing in the Fund | 9 |

| Investments Made Through Brokerage Firms or Other Financial Institutions | 9 |

| Minimum Investments | 9 |

| Types of Account Ownership | 10 |

| Instructions For Opening and Adding to an Account | 10 |

| Telephone and Wire Transactions | 11 |

| Tax-Deferred Plans | 11 |

| Types of Tax-Deferred Accounts | 12 |

| Automatic Investment Plans | 12 |

| Instructions For Selling Fund Shares | 13 |

| Additional Redemption Information | 14 |

| Shareholder Communications | 15 |

| Dividends and Distributions | 15 |

| Share Classes | 15 |

| Market Timing | 15 |

| Taxes | 16 |

| Other Fund Service Providers | 17 |

| Privacy Policy | 18 |

| Financial Highlights | 19 |

• The Walthausen Small Cap Value Fund seeks long-term capital appreciation.

The following table describes the expenses and fees that you may pay if you buy and hold shares of the Fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below.

| Institutional | Investor | |

| Class | Class | |

| Sales Charge (Load) Imposed on Purchases | ||

| Deferred Sales Charge (Load) | ||

| Sales Charge (Load) Imposed on Reinvested Dividends | ||

| Annual Fund Operating Expenses (expenses that you pay each | ||

| year as a percentage of the value of your investment) | ||

| Management Fees | ||

| Distribution 12b-1 Fees | ||

| Other Expenses | ||

| Total Annual Fund Operating Expenses | ||

| Fee Waiver / Expense Reimbursement (1) | ( |

( |

| Total Annual Fund Operating Expenses After Fee Waiver |

| (1) |

The following example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The example also assumes that your investment has a 5% annual return each year and that the Fund’s operating expenses remain the same each year. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| Walthausen Small Cap Value Fund | One Year | Three Years | Five Years | Ten Years |

| Institutional Class | $ |

$ |

$ |

$ |

| Investor Class | $ |

$ |

$ |

$ |

Prospectus 1

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was

The Fund invests primarily in common stocks of small capitalization companies that the Advisor believes have the potential for capital appreciation. Small capitalization companies are defined as those with market capitalizations of $2 billion or less at the time of purchase. Under normal circumstances, the Fund will invest at least 80% of its net assets plus any borrowing for investment purposes in common stocks of small capitalization companies, as defined above. The Fund emphasizes a “value”*investment style, investing in companies that appear under-priced according to certain financial measurements of their worth or business prospects.

As with all mutual funds, there is the risk that you could lose some or all of your investment in the Fund.

Risks of Investing in Small Capitalization Companies

The Fund invests in the stocks of small capitalization companies, which may subject the Fund to additional risks. The earnings and prospects of these companies are generally more volatile than larger companies and small capitalization companies may experience higher failure rates than do larger companies.

Risks in General

Domestic economic growth and market conditions, interest rate levels, and political events are among the factors affecting the securities markets in which the Fund invests. There is risk that these and other factors may adversely affect the Fund’s performance.

Additionally, unexpected local, regional or global events, such as war; acts of terrorism; financial, political or social disruptions; natural, environmental or man-made disasters; the spread of infectious illnesses or other public health issues (such as COVID-19); and recessions and depressions could have a significant impact on the Fund and its investments and may impair market liquidity. Such events can cause investor fear, which can adversely affect the economies of nations, regions and the market in general, in ways that cannot necessarily be foreseen.

Risks of Investing in Common Stocks

Overall stock market risks may affect the value of the Fund. Factors such as domestic economic growth and market conditions, interest rate levels, and political events affect the securities markets.

Value Investing Risk

Value investing attempts to identify companies selling at a discount to their intrinsic value. Value investing is subject to the risk that a company’s intrinsic value may never be fully realized by the market or that a company judged by the Advisor to be undervalued may actually be appropriately priced.

Sector Risk

Sector risk is the possibility that all stocks within the same group of industries will decline in price due to sector-specific market or economic developments. The Fund may be overweight in certain sectors at various times.

Prospectus 2

Investment Management Risk

The Advisor’s strategy may fail to produce the intended results.

The as of was for the Investor Class.

() + ()

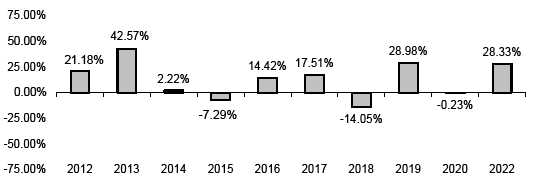

FOR THE PERIODS ENDED 12/31/21 |

1 Year | 5 Years | 10 Years |

| WALTHAUSEN SMALL CAP VALUE FUND | |||

| Investor Class | |||

| Return Before Taxes | |||

| Return After Taxes on Distributions | |||

| Return After Taxes on Distributions and Sale of Fund Shares | |||

| Institutional Class* Return Before Taxes | - | - | |

| Russell 2000 Value Index (does not reflect deductions for fees, | |||

| expenses or taxes) | |||

| * |

Prospectus 3

Management

Investment Advisor

Walthausen & Co., LLC (the “Advisor”)

Portfolio Manager

Gerard S.E. Heffernan has managed the Fund since March 2018. Mr. Heffernan is a Portfolio Manager and Managing Director of the Advisor.

Purchase and Sale of Fund Shares

The minimum initial and subsequent investment amounts for various types of accounts offered by the Fund are shown below.

| Institutional Class | Initial | Additional |

| Regular Account | $100,000 | $1,000 |

| Automatic Investment Plan | $100,000 | $1,000 |

| IRA Account | $100,000 | $1,000 |

| Investor Class | Initial | Additional |

| Regular Account | $2,500 | $100 |

| Automatic Investment Plan | $2,500 | $100 |

| IRA Account | $2,500 | $100 |

Investors may purchase or redeem Fund shares on any business day through a financial intermediary, by mail (Walthausen Funds, c/o Ultimus Fund Solutions, LLC, P.O. Box 46707, Cincinnati, Ohio 45246-0707), by wire, or by telephone at 1-888-925-8428.

Tax Information

The Fund’s distributions are taxable, and will be taxed as ordinary income or capital gains, unless you are investing through a tax-deferred arrangement, such as a 401(k) plan or an individual retirement account. Such tax-deferred arrangements may be taxed later upon withdrawal of monies from those arrangements.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase the Fund through a broker-dealer or other financial intermediary (such as a financial advisor), the Fund and/or its investment advisor may pay the intermediary a fee as compensation for the services it provides, which may include performing sub-accounting services, delivering Fund documents to shareholders and providing information about the Fund. These payments may create a conflict of interest by influencing the financial intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

Cybersecurity

The computer systems, networks and devices used by the Fund and its service providers to carry out routine business operations employ a variety of protections designed to prevent damage or interruption from computer viruses, network failures, computer and telecommunication failures, infiltration by unauthorized persons and security breaches. Despite the various protections utilized by the Fund and its service providers, systems, networks, or devices potentially can be breached. The Fund and its shareholders could be negatively impacted as a result of a cybersecurity breach.

Prospectus 4

Cybersecurity breaches can include unauthorized access to systems, networks, or devices; infection from computer viruses or other malicious software code; and attacks that shut down, disable, slow, or otherwise disrupt operations, business processes, or website access or functionality. Cybersecurity breaches may cause disruptions and impact the Fund’s business operations, potentially resulting in financial losses; interference with the Fund’s ability to calculate its NAV; impediments to trading; the inability of the Fund, the Advisor, and other service providers to transact business; violations of applicable privacy and other laws; regulatory fines, penalties, reputational damage, reimbursement or other compensation costs, or additional compliance costs; as well as the inadvertent release of confidential information.

Similar adverse consequences could result from cybersecurity breaches affecting issuers of securities in which the Fund invests; counterparties with which the Fund engages in transactions; governmental and other regulatory authorities; exchange and other financial market operators, banks, brokers, dealers, insurance companies, and other financial institutions (including financial intermediaries and service providers for the Fund’s shareholders); and other parties. In addition, substantial costs may be incurred by these entities in order to prevent any cybersecurity breaches in the future.

Investment Objective, Principal Investment Strategy, Related Risks, and Disclosure of Portfolio Holdings

Investment Objective

• The Fund seeks long-term capital appreciation.

The Principal Investment Strategy of the Fund

The Fund invests primarily in common stocks of small capitalization companies that the Advisor believes have the potential for capital appreciation. Small capitalization companies are defined as those with market capitalizations of $2 billion or less at the time of purchase. Under normal circumstances, the Fund will invest at least 80% of its net assets plus any borrowing for investment purposes in common stocks of small capitalization companies, as defined above. The Fund emphasizes a “value”*investment style, investing in companies that appear under-priced according to certain financial measurements of their worth or business prospects. The Board of Trustees can change this policy without shareholder approval. The Fund will notify you in writing at least 60 days before implementing any change to this policy.

The Fund may invest in other securities as described in the Statement of Additional Information, which is available upon request.

The Investment Selection Process Used by the Fund

The Advisor searches for securities by using a proprietary valuation model to identify companies that are trading at a discount to intrinsic value. The starting universe is small capitalization companies defined as those with market capitalizations of $2 billion or less. Once investment ideas meet screening criteria, the Advisor studies public filings and constructs detailed models to project earnings and cash flows. The Advisor frequently contacts company management and/or industry experts to develop a clearer understanding of each investment idea. Final investment decisions are based on the Advisor’s internally prepared models and valuation metrics.

The Advisor may sell a security when it reaches the Advisor’s appraised value, when there is a more attractively priced company as an alternative, when the fundamentals of the business have changed, or when the Advisor determines that management of the company is not enhancing shareholder value. These portfolio reviews are conducted continuously through close monitoring of stock prices, changes in the economy, and corporate developments.

Prospectus 5

For temporary defensive purposes, the Fund may hold cash or cash-equivalents and invest without limit in obligations of the U.S. Government and its agencies, money market funds and money market securities, including high-grade commercial paper, certificates of deposit, repurchase agreements and short-term debt securities. Under these circumstances, the Fund may not participate in stock market advances or declines to the same extent it would had it remained more fully invested in common stocks.

The Principal Risks of Investing in the Fund

As with all mutual funds, there is the risk that you could lose some or all of your investment in the Fund.

Risks of Investing in Small Capitalization Companies

The Fund invests in the stocks of small capitalization companies, which may subject the Fund to additional risks. The earnings and prospects of these companies are generally more volatile than larger companies. Small capitalization companies may experience higher failure rates than do larger companies. The trading volume of securities of small capitalization companies is normally less than that of larger companies and, therefore, may disproportionately affect their market price, tending to make them fall more in response to selling pressure than is the case with larger companies. Small capitalization companies may have limited markets, product lines or financial resources and may lack management experience.

Risks in General

An investment in the Fund is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Domestic economic growth and market conditions, interest rate levels, and political events are among the factors affecting the securities markets of the Fund’s investments. There is risk that these and other factors may adversely affect the Fund’s performance. You should consider your own investment goals, time horizon, and risk tolerance before investing in the Fund. An investment in the Fund may not be appropriate for all investors and is not intended to be a complete investment program. You may lose money by investing in the Fund.

Additionally, unexpected local, regional or global events, such as war; acts of terrorism; financial, political or social disruptions; natural, environmental or man-made disasters; the spread of infectious illnesses or other public health issues; and recessions and depressions could have a significant impact on the Fund and its investments and may impair market liquidity. Such events can cause investor fear, which can adversely affect the economies of nations, regions and the market in general, in ways that cannot necessarily be foreseen. The increasing interconnectivity between global economies and financial markets increases the likelihood that events or conditions in one region or financial market may adversely impact issuers in a different country, region or financial market. These risks may be magnified if certain events or developments adversely interrupt the global supply chain; in these and other circumstances, such risks might affect companies worldwide. As a result, local, regional or global events such as war, acts of terrorism, the spread of infectious illness or other public health issues, recessions or other events could have a significant negative impact on global economic and market conditions. The COVID-19 global pandemic and the aggressive responses taken by many governments or voluntarily imposed by private parties, including closing borders, restricting international and domestic travel, and imposing prolonged quarantines or similar restrictions, as well as the closure of, or operational changes to, many retail and other businesses, has had negative impacts, and in many cases severe negative impacts, on markets worldwide. It is not known how long such impacts, or any future impacts of other significant events described above, will or would last, but there could be a prolonged period of global economic slowdown, which may be expected to impact the Fund and its investments.

Risks of Investing in Common Stocks

The Fund invests primarily in common stocks, which subjects the Fund and its shareholders to the risks associated with common stock investing. These risks include the financial risk of selecting individual companies that do not perform as anticipated, the risk that the stock markets in which the

Prospectus 6

Fund invests may experience periods of turbulence and instability, and the general risk that domestic and global economies may go through periods of decline and cyclical change. Many factors affect the performance of each company that the Fund invests in, including the strength of the company’s management or the demand for its product or services. You should be aware that a company’s share price may decline as a result of poor decisions made by management or lower demand for the company’s products or services. In addition, a company’s share price may also decline if its earnings or revenues fall short of expectations.

There are overall stock market risks that may also affect the value of the Fund. Over time, the stock markets tend to move in cycles, with periods when stock prices rise generally and periods when stock prices decline generally. The value of the Fund’s investments may increase or decrease more than the stock markets in general.

Value Investing Risk

Value investing attempts to identify companies selling at a discount to their intrinsic value. Value investing is subject to the risk that a company’s intrinsic value may never be fully realized by the market or that a company judged by the Advisor to be undervalued may actually be appropriately priced.

Sector Risk

Sector risk is the possibility that stocks within the same group of industries will decline in price due to sector-specific market or economic developments. If the Advisor invests a significant portion of its assets in a particular sector, the Fund is subject to the risk that companies in the same sector are likely to react similarly to legislative or regulatory changes, adverse market conditions and/or increased competition affecting that market segment. The sectors in which the Fund may be overweighted will vary.

Investment Management Risk

The Advisor’s strategy may fail to produce the intended results.

Portfolio Holdings Disclosure

A description of the Fund’s policies and procedures with respect to the disclosure of the Fund’s portfolio securities is available in the Fund’s Statement of Additional Information (“SAI”).

Management

The Investment Advisor

Walthausen & Co., LLC, 2691 Route 9, Suite 102, Malta, NY 12020, is the investment advisor of the Fund and has responsibility for the management of the Fund's affairs, under the supervision of the Fund's Board of Trustees. The Fund's investment portfolio is managed on a day-to-day basis by Gerard S.E. Heffernan CFA. Mr. Heffernan is a Portfolio Manager and Managing Director of the Advisor. Mr. Heffernan joined the Advisor in February 2018. His involvement in the investment industry spans over 25 years, including 15 years at Lord Abbett & Co., where he was a partner and portfolio manager specializing in small cap value equities. From June 2013 until February 2018, he was self-employed managing his own portfolio. Mr. Heffernan received a B.S. in Business Administration from Villanova University.

Prospectus 7

The Fund’s Statement of Additional Information provides information about the portfolio managers’ compensation, other accounts managed by the portfolio managers, and the portfolio managers’ ownership of Fund shares. A discussion regarding the basis for the Board of Trustees’ approval of the Management Agreement between the Fund and the Advisor is available in the Annual Report to Shareholders for the fiscal year ended January 31, 2022.

Under the Management Agreement, the Advisor, at its own expense and without reimbursement from the Trust, furnishes office space and all necessary office facilities, equipment and executive personnel necessary for managing the assets of the Fund. For the fiscal year ended January 31, 2022, the Advisor received an investment management fee at an annual rate equal to 1.00% of the average daily net assets of the Fund. Under a Services Agreement with the Fund, the Advisor receives an additional fee of 0.45% of the Fund’s average daily net assets up to $100 million, 0.25% of the Fund’s average daily net assets between $100 million and $500 million, and 0.15% of such assets in excess of $500 million and is obligated to pay the operating expenses of the Fund excluding management fees, brokerage fees and commissions, taxes, borrowing costs (such as (a) interest and (b) dividend expenses on securities sold short), the cost of acquired funds and extraordinary expenses. The Advisor has contractually agreed to waive Services Agreement fees and Management fees to the extent necessary to maintain total annual operating expenses of the Institutional Class Shares and Investor Class Shares, excluding brokerage fees and commissions, taxes, borrowing costs (such as (a) interest and (b) dividend expenses on securities sold short), the cost of acquired funds and extraordinary expenses at 0.98% and 1.21% respectively, of its average daily net assets through May 31, 2023. The Advisor may not terminate the fee waiver before May 31, 2023. The Trustees may terminate the expense waiver upon notice to the Advisor.

The Advisor (not the Fund) may pay certain financial institutions (which may include banks, brokers, securities dealers and other industry professionals) a fee for providing distribution related services and/or for performing certain administrative servicing functions for Fund shareholders to the extent these institutions are allowed to do so by applicable statute, rule or regulation. The Fund may purchase securities issued by these financial institutions or their affiliates, however, the portfolio manager is prohibited from considering the services provided by the financial institution in making a decision whether to purchase or sell the securities of the financial institution or its affiliates.

An investment in the Fund is not a deposit or obligation of any bank, is not endorsed or guaranteed by any bank, and is not insured by the Federal Deposit Insurance Corporation (“FDIC”) or any other government agency. You may lose money by investing in the Fund.

Shareholder Information

Pricing of Fund Shares

The price you pay for a share of the Fund, and the price you receive upon selling or redeeming a share of the Fund, is called the Fund’s net asset value (“NAV”). The NAV is calculated by taking the total value of the Fund’s assets, subtracting its liabilities, and then dividing by the total number of shares outstanding, rounded to the nearest cent: NAV = Total Assets (Class) - Liabilities (Class) / Number of Shares Outstanding (Class)

The NAV is generally calculated on each day the New York Stock Exchange is open as of the close of trading on the Exchange (normally 4:00 p.m. Eastern time). The New York Stock Exchange is generally open every day other than weekends and holidays. All purchases, redemptions or reinvestments of Fund shares will be priced at the next NAV calculated after your order is received in proper form by the Fund’s Transfer Agent, Ultimus Fund Solutions. If you purchase shares directly from the Fund, your order must be placed with the Transfer Agent prior to the close of the trading of the New York Stock Exchange in order to be confirmed for that day’s NAV. The Fund’s assets generally are valued at their market value. Certain short-term securities may be valued at amortized cost, which approximates market value. If market prices are not available or, in the Advisor’s opinion, market

Prospectus 8

prices do not reflect fair value, or if an event occurs after the close of trading (but prior to the time the NAV is calculated) that materially affects fair value, the Advisor may value the Fund’s assets at their fair value according to written policies approved by the Fund’s Board of Trustees. For example, if trading in a portfolio security is halted and does not resume before the Fund calculates its NAV, the Advisor may need to price the security using the Fund’s fair value pricing guidelines. Without a fair value price, short term traders could take advantage of the arbitrage opportunity and dilute the NAV of long term investors. Fair valuation of a Fund’s portfolio securities can serve to reduce arbitrage opportunities available to short term traders, but there is no assurance that fair value pricing policies will prevent dilution of the Fund’s NAV by short term traders. The Fund may use pricing services to determine market value.

Customer Identification Program

IMPORTANT INFORMATION ABOUT PROCEDURES FOR OPENING A NEW ACCOUNT

To help the government fight the funding of terrorism and money laundering activities, Federal law requires all financial institutions to obtain, verify, and record information that identifies each person who opens an account. This means that, when you open an account, we will ask for your name, address, date of birth, and other information that will allow us to identify you. We may also ask for identifying documents, and may take additional steps to verify your identity. We may not be able to open an account or complete a transaction for you until we are able to verify your identity.

Investing in the Fund

You may purchase shares directly through the Fund’s transfer agent or through a brokerage firm or other financial institution that has agreed to sell the Fund’s shares. If you are investing directly in the Fund for the first time, you will need to establish an account by completing a Shareholder Account Application (To establish an IRA, complete an IRA Application). To request an application, call toll-free 1-888-925-8428.

Investments Made Through Brokerage Firms or Other Financial Institutions

If you invest through a brokerage firm or other financial institution, the policies and fees may be different than those described here. Financial advisors, financial supermarkets, brokerage firms, and other financial institutions may charge transaction and other fees and may set different minimum investments or limitations on buying or selling shares. Consult a representative of your financial institution if you have any questions. The Fund is deemed to have received your order when the brokerage firm or financial institution receives the order, and your purchase will be priced at the next calculated NAV. Your financial institution is responsible for transmitting your order in a timely manner.

| Minimum Investments | ||

| Institutional Class | Initial | Additional |

| Regular Account | $100,000 | $1,000 |

| Automatic Investment Plan | $100,000 | $1,000 |

| IRA Account | $100,000 | $1,000 |

| Investor Class | Initial | Additional |

| Regular Account | $2,500 | $100 |

| Automatic Investment Plan | $2,500 | $100 |

| IRA Account | $2,500 | $100 |

The Fund reserves the right to change the amount of these minimums from time to time or to waive them in whole or in part for certain accounts. Investment minimums may be higher or lower to investors purchasing shares through a brokerage firm or other financial institution.

Prospectus 9

All purchases must be made in U.S. dollars and checks must be drawn on U.S. banks. No cash, money orders, travelers checks, credit cards, credit card checks, third party checks or other checks deemed to be high-risk checks will be accepted. You will be charged an annual account maintenance fee of $15 for each tax-deferred account you have with the Fund. A $20 fee will be charged against your account for any payment check returned to the transfer agent or for any incomplete electronic fund transfer, or for insufficient funds, stop payment, closed account or other reasons. If a check does not clear your bank or the Fund is unable to debit your predesignated bank account on the day of purchase, the Fund reserves the right to cancel the purchase. If your purchase is canceled, you will be responsible for any losses or fees imposed by your bank and losses that may be incurred as a result of a decline in the value of the canceled purchase. The Fund (or Fund’s agent) has the authority to redeem shares in your account(s) to cover any losses due to fluctuations in share price. Any profit on such cancellation will accrue to the Fund. Your investment in the Fund should be intended to serve as a long-term investment vehicle. The Fund is not designed to provide you with a means of speculating on the short-term fluctuations in the stock market. The Fund reserves the right to reject any purchase request that it regards as disruptive to the efficient management of the Fund, which includes investors with a history of excessive trading. The Fund also reserves the right to stop offering shares at any time.

Types of Account Ownership

You can establish the following types of accounts by completing a Shareholder Account Application:

• Individual or Joint Ownership

Individual accounts are owned by one person. Joint accounts have two or more owners.

• A Gift or Transfer to Minor

(UGMA or UTMA) An UGMA/UTMA account is a custodial account managed for the benefit of a minor. To open an UGMA or UTMA account, you must include the minor’s social security number on the application.

• Trust

An established trust can open an account. The names of each trustee, the name of the trust and the date of the trust agreement must be included on the application.

• Business Accounts

Corporation and partnerships may also open an account. The application must be signed by an authorized officer of the corporation or a general partner of a partnership.

• IRA Accounts

See “Tax-Deferred Plans” on page 11.

Instructions For Opening and Adding to an Account

TO OPEN AN ACCOUNT

By Mail

Complete and sign the Shareholder Application or an IRA Application

Make your check payable to Walthausen Funds

• For IRA accounts, please specify the year for which the contribution is made.

TO ADD TO AN ACCOUNT

By Mail

Complete the investment slip that is included with your account statement, and write your account number on your check. If you no longer have your investment slip, please reference your name, account number, and address on your check.

Prospectus 10

Mail the application and check to:

Walthausen Funds

c/o Ultimus Fund Solutions, LLC

P.O. Box 46707

Cincinnati, Ohio 45246-0707

By overnight courier, send to:

Walthausen Funds

c/o Ultimus Fund Solutions, LLC

255 Pictoria Drive, Suite 450

Cincinnati, Ohio 45246

Mail the slip and the check to:

Walthausen Funds

c/o Ultimus Fund Solutions, LLC

P.O. Box 46707

Cincinnati, Ohio 45246-0707

TO OPEN AN ACCOUNT

By Wire

Call 1-888-925-8428 for instructions and prior to wiring to the Fund.

TO ADD TO AN ACCOUNT

By Wire

Call 1-888-925-8428 for instructions and prior to wiring to the Fund.

Telephone and Wire Transactions

With respect to all transactions made by telephone, the Fund and its transfer agent will employ reasonable procedures to confirm that instructions communicated by telephone are genuine. Such procedures may include, among others, requiring some form of personal identification prior to acting upon telephone instructions, providing written confirmation of all such transactions, and/or tape recording all telephone instructions. If reasonable procedures are followed, then neither the Fund nor the transfer agent will be liable for any loss, cost, or expense for acting upon an investor’s telephone instructions or for any unauthorized telephone redemption. In any instance where the Fund’s transfer agent is not reasonably satisfied that instructions received by telephone are genuine, neither the Fund nor the transfer agent shall be liable for any losses which may occur because of delay in implementing a transaction.

If you purchase your initial shares by wire, the transfer agent first must have received a completed account application and issued an account number to you. The account number must be included in the wiring instructions as set forth on the previous page. The transfer agent must receive your account application to establish shareholder privileges and to verify your account information. Payment of redemption proceeds may be delayed and taxes may be withheld unless the Fund receives a properly completed and executed account application.

Shares purchased by wire will be purchased at the NAV next determined after the transfer agent receives your wired funds and all required information is provided in the wire instructions. If the wire is not received by 4:00 p.m. Eastern time, the purchase will be effective at the NAV next calculated after receipt of the wire.

Tax-Deferred Plans

If you are eligible, you may set up one or more tax-deferred accounts. A tax-deferred account allows you to defer income taxes due on your investment income and capital gains. A contribution to certain of these plans may also be tax deductible. Tax-deferred accounts include retirement plans described below. Distributions from these plans are generally subject to an additional tax if withdrawn prior to age 59 1/2 or used for a nonqualifying purpose. Investors should consult their tax adviser or legal counsel before selecting a tax-deferred account.

Prospectus 11

U.S. Bank, N.A. serves as the custodian for the tax-deferred accounts offered by the Fund. You will be charged an annual account maintenance fee of $15 for each tax-deferred account you have with the Fund. You may pay the fee by check or have it automatically deducted from your account (usually in December). The custodian reserves the right to change the amount of the fee or to waive it in whole or part for certain types of accounts.

Types of Tax-Deferred Accounts

• Traditional IRA

An individual retirement account. Your contribution may or may not be deductible depending on your circumstances. Assets can grow tax-deferred and distributions are taxable as income.

• Roth IRA

An IRA with non-deductible contributions, tax-free growth of assets, and tax-free distributions for qualified distributions.

• Spousal IRA

An IRA funded by a working spouse in the name of a non-earning spouse.

• SEP-IRA

An individual retirement account funded by employer contributions. Your assets grow tax-deferred and distributions are taxable as income.

• Keogh or Profit Sharing Plans

These plans allow corporations, partnerships and individuals who are self-employed to make tax-deductible contributions for each person covered by the plans.

• 403(b) Plans

An arrangement that allows employers of charitable or educational organizations to make voluntary salary reduction contributions to a tax-deferred account.

• 401(k) Plans

Allows employees of corporations of all sizes to contribute a percentage of their wages on a tax-deferred basis. These accounts need to be established by the trustee of the plan.

Automatic Investment Plans

By completing the Automatic Investment Plan section of the account application, you may make automatic monthly or quarterly investments ($100 minimum per purchase) in the Fund from your bank or savings account. Your initial investment minimum is $2,500 if you select this option. Shares of the Fund may also be purchased through direct deposit plans offered by certain employers and government agencies. These plans enable shareholders to have all or a portion of their payroll or Social Security checks transferred automatically to purchase shares of the Fund.

FOR INVESTING

Automatic Investment Plan

For making automatic investments from a designated bank account.

Payroll Direct Deposit Plan

For making automatic investments from your payroll check.

Dividend Reinvestment

All income dividends and capital gains distributions will be automatically reinvested in shares of the Fund unless you indicate otherwise on the account application or in writing.

Prospectus 12

Instructions For Selling Fund Shares

You may sell all or part of your shares on any day that the New York Stock Exchange is open for trading. Your shares will be sold at the next NAV per share calculated after your order is received in proper form by the transfer agent. The proceeds of your sale may be more or less than the purchase price of your shares, depending on the market value of the Fund’s securities at the time of your sale. Your order will be processed promptly and you will generally receive the proceeds within seven days after the Fund receives your properly completed request. The Fund typically expects to pay redemptions from cash, cash equivalents, proceeds from the sale of fund shares, from the sale of portfolio securities, and then from borrowing from a bank line of credit. These redemption payment methods will be used in regular and stressed market conditions. The Fund will not mail any proceeds unless your investment check has cleared the bank, which may take up to fifteen calendar days. This procedure is intended to protect the Fund and its shareholders from loss. If the dollar or share amount requested is greater than the current value of your account, your entire account balanced will be redeemed. If you choose to redeem your account in full, any automatic services currently in effect for the account will be terminated unless you indicate otherwise in writing. You will be charge a $20 fee for wire redemptions.

TO SELL SHARES

By Mail

Write a letter of instruction that includes:

Mail your request to:

Walthausen Funds

c/o Ultimus Fund Solutions, LLC

P.O. Box 46707

Cincinnati, Ohio 45246-0707

By overnight courier, send to:

Walthausen Funds

c/o Ultimus Fund Solutions, LLC

255 Pictoria Drive, Suite 450

Cincinnati, Ohio 45246

By Telephone

For specific information on how to redeem your account, and to determine if a signature guarantee or other documentation is required, please call toll-free in the U.S. 1-888-925-8428.

Prospectus 13

Additional Redemption Information

Signature Guarantees

Signature guarantees are designed to protect both you and the Fund from fraud. A signature guarantee of each account owner is required to redeem shares in the following situations:

Signature guarantees can be obtained from most banks, savings and loan associations, trust companies, credit unions, broker/dealers, and member firms of a national securities exchange. Call your financial institution to see if they have the ability to guarantee a signature. A notary public cannot provide signature guarantees.

The Fund reserves the right to require a signature guarantee under other circumstances or to delay a redemption when permitted by Federal Law. For more information pertaining to signature guarantees, please call 1-888-925-8428.

Corporate, Trust and Other Accounts

Redemption requests from corporate, trusts, and other accounts may require documents in addition to those described above, evidencing the authority of the officers, trustees or others. In order to avoid delays in processing redemption requests for these accounts, you should call the Transfer Agent at 1-888-925-8428 to determine what additional documents are required.

Address Changes

To change the address on your account, call the transfer agent at 1-888-925-8428 or send a written request signed by all account owners. Include the account number(s) and name(s) on the account and both the old and new addresses. Certain options may be suspended for a period of 15 days following an address change.

Transfer of Ownership

In order to change the account registration or transfer ownership of an account, additional documents will be required. In order to avoid delays in processing these requests, you should call the transfer agent at 1-888-925-8428 to determine what additional documents are required.

Redemption Initiated by the Fund

Because there are certain fixed costs involved with maintaining your account, the Fund may require you to redeem all of your shares if your account balance falls below $500. After your account balance falls below the minimum balance, you will receive a notification from the Fund indicating its intent to close your account along with instructions on how to increase the value of your account to the minimum amount within 60 days. If your account balance is still below $500 after 60 days, the Fund may close your account and send you the proceeds. This minimum balance requirement does not apply to accounts using automatic investment plans, to IRAs, and to other tax-sheltered investment accounts. The right of redemption by the Fund will not apply if the value of your account balance falls below $500 because of market performance. All shares of the Fund are also subject to involuntary redemption if the Board of Trustees determines to liquidate the Fund. Any involuntary redemption will create a capital gain or loss, which may have tax consequences about which you should consult your tax adviser.

Prospectus 14

Shareholder Communications

Account Statements

Every quarter, shareholders of the Fund will automatically receive regular account statements. You will also be sent a yearly statement detailing the tax characteristics of any dividends and distributions you have received.

Confirmations

Confirmation statements will be sent after each transaction that affects your account balance or account registration.

Regulatory Mailings

Financial reports will be sent at least semi-annually. Annual reports will include audited financial statements. To reduce expenses, one copy of each report will be mailed to each taxpayer identification number even though the investor may have more than one account in the Fund.

Dividends and Distributions

The Fund intends to pay distributions on an annual basis and expects that distributions will consist primarily of capital gains. You may elect to reinvest income dividends and capital gain distributions in the form of additional shares of the Fund or receive these distributions in cash. Dividends and distributions from the Fund are automatically reinvested in the Fund, unless you elect to have dividends paid in cash. Reinvested dividends and distributions receive the same tax treatment as those paid in cash. If you are interested in changing your election, you may call the transfer agent at 1-888-925-8428 or send a written notification to:

Walthausen Funds

c/o Ultimus Fund Solutions, LLC

P.O. Box 46707

Cincinnati, Ohio 45246-0707

Share Classes

Institutional Class

Institutional Class shares of the Fund are sold at NAV. Institutional Class shares require a minimum initial investment of $100,000.

Investor Class

Investor Class shares of the Fund are sold at NAV. Investor shares require a minimum initial investment of $2,500.

Market Timing

The Fund discourages market timing. Market timing is an investment strategy using frequent purchases, redemptions, and/or exchanges in an attempt to profit from short-term market movements. Market timing may result in dilution of the value of Fund shares held by long term shareholders, disrupt portfolio management, and increase Fund expenses for all shareholders. The Board of Trustees also has adopted a policy directing the Fund to reject any purchase order with respect to one investor, a related group of investors or their agent(s), where it detects a pattern of purchases and sales of the Fund that indicates market timing or trading that it determines is abusive. This policy applies uniformly to all Fund shareholders. While the Fund attempts to deter market timing, there is no assurance that it will be able to identify and eliminate all market timers. For example, certain accounts called “omnibus accounts” include multiple shareholders. Omnibus accounts typically provide the Fund with a net purchase or redemption request on any given day where purchasers of

Prospectus 15

Fund shares and redeemers of Fund shares are netted against one another and the identity of individual purchasers and redeemers whose orders are aggregated are not known by the Fund. The netting effect often makes it more difficult for the Fund to detect market timing, and there can be no assurance that the Fund will be able to do so. The Fund may invest in foreign securities, and small capitalization companies, and therefore may have additional risks associated with market timing. Because the Fund may invest in securities that are, among other things, priced on foreign exchanges, thinly traded, traded infrequently or relatively illiquid, the Fund has the risk that the current market price for the securities may not accurately reflect current market values. This can create opportunities for market timing by shareholders. For example, securities trading on overseas markets present time zone arbitrage opportunities when events affecting portfolio security values occur after the close of the overseas market, but prior to the close of the U.S. market. A shareholder may seek to engage in short-term trading to take advantage of these pricing differences, and therefore could dilute the value of Fund shares held by long term shareholders, disrupt portfolio management and increase Fund expenses for all shareholders.

Taxes

Fund dividends and distributions are taxable to most investors (unless your investment is in an IRA or other tax-advantaged account). Dividends paid by the Fund out of net ordinary income and distributions of net short-term capital gains are taxable to the shareholders as ordinary income. Distributions by the Fund of net long-term capital gains to shareholders are generally taxable to the shareholders at the applicable long-term capital gains rate, regardless of how long the shareholder has held shares of the Fund.

Redemptions of shares of the Fund are taxable events which you may realize as a gain or loss. The amount of the gain or loss and the rate of tax will depend mainly upon the amount paid for the shares, the amount received from the sale, and how long the shares were held.

The Fund’s distributions may be subject to federal income tax whether received in cash or reinvested in additional shares. In addition to federal taxes, you may be subject to state and local taxes on distributions. For taxable years beginning after December 31, 2012, an additional 3.8% Medicare tax may be imposed on distributions you receive from the Fund and on gains from selling, redeeming or exchanging your shares. Because everyone’s tax situation is unique, always consult your tax professional about federal, state, and local tax consequences of an investment in the Fund.

Prospectus 16

Other Fund Service Providers

Distributor

Foreside Fund Services, LLC

Custodian

U.S. Bank, N.A.

Fund Administrator

Premier Fund Solutions, Inc.

Independent Registered Public Accounting Firm

Cohen & Company, Ltd.

Investment Advisor

Walthausen & Co., LLC

Legal Counsel

Thompson Hine LLP

Transfer Agent

Ultimus Fund Solutions, LLC

Prospectus 17

| PRIVACY POLICY |

The following is a description of the Fund’s policies regarding disclosure of nonpublic personal information that you provide to the Fund or that the Fund collects from other sources. In the event that you hold shares of the Fund through a broker-dealer or other financial intermediary, the privacy policy of your financial intermediary would govern how your nonpublic personal information would be shared with unaffiliated third parties.

Categories of Information the Fund Collects. The Fund collects the following non-public personal information about you:

• Information the Fund receives from you on or in applications or other forms, correspondence, or conversations (such as your name, address, phone number, social security number, assets, income and date of birth); and

• Information about your transactions with the Fund, its affiliates, or others (such as your account number and balance, payment history, parties to transactions, cost basis information, and other financial information).

Categories of Information the Fund Discloses. The Fund does not disclose any non-public personal information about their current or former shareholders to unaffiliated third parties, except as required or permitted by law. The Fund is permitted by law to disclose all of the information it collects, as described above, to its service providers (such as the Fund’s custodian, administrator and transfer agent) to process your transactions and otherwise provide services to you.

Confidentiality and Security. The Fund restricts access to your nonpublic personal information to those persons who require such information to provide products or services to you. The Fund maintains physical, electronic, and procedural safeguards that comply with federal standards to guard your nonpublic personal information.

Prospectus 18

Financial Highlights

The financial highlights table is intended to help you understand the Fund’s financial performance for the past five years. Certain information reflects financial results for a single Fund share. The total returns in the table represent the rate you would have earned (or lost) on an investment in the Fund (assuming reinvestment of all dividends and distributions). The financial information has been audited by Cohen & Company, Ltd., the Fund’s independent registered public accounting firm, whose report, along with the Fund’s financial statements, is included in the Fund’s annual report, which is available upon request.

| Financial Highlights - Investor Class | |||||||||||||||

| Selected data for a share outstanding throughout the period: | 2/1/2021 | 2/1/2020 | 2/1/2019 | 2/1/2018 | 2/1/2017 | ||||||||||

| to | to | to | to | to | |||||||||||

| 1/31/2022 | 1/31/2021 | 1/31/2020 | 1/31/2019 | 1/31/2018 | |||||||||||

| Net Asset Value - | |||||||||||||||

| Beginning of Period | $ | 20.49 | $ | 18.80 | $ | 18.71 | $ | 23.87 | $ | 22.12 | |||||

| Net Investment Income (Loss) (a) | (0.00 | ) + | 0.05 | 0.07 | (0.02 | ) | (0.07 | ) | |||||||

| Net Gain (Loss) on Investments (Realized and Unrealized) (b) | 5.12 | 1.83 | 0.43 | (2.74 | ) | 2.99 | |||||||||

| Total from Investment Operations | 5.12 | 1.88 | 0.50 | (2.76 | ) | 2.92 | |||||||||

| Distributions (From Net Investment Income) | - | + | (0.19 | ) | (0.02 | ) | - | - | |||||||

| Distributions (From Capital Gains) | (7.38 | ) | - | (0.39 | ) | (2.40 | ) | (1.17 | ) | ||||||

| Total Distributions | (7.38 | ) | (0.19 | ) | (0.41 | ) | (2.40 | ) | (1.17 | ) | |||||

| Proceeds from Redemption Fee (e) | - | + | - | + | - | + | - | + | - | + | |||||

| Net Asset Value - | |||||||||||||||

| End of Period | $ | 18.23 | $ | 20.49 | $ | 18.80 | $ | 18.71 | $ | 23.87 | |||||

| Total Return (c) | 23.66 | % | 10.04 | % | 2.55 | % | (10.27 | )% | 13.22 | % | |||||

| Ratios/Supplemental Data | |||||||||||||||

| Net Assets - End of Period (Thousands) | $ | 64,007 | $ | 71,784 | $ | 177,627 | $ | 422,206 | $ | 621,122 | |||||

| Before Reimbursement | |||||||||||||||

| Ratio of Expenses to Average Net Assets | 1.38 | % | 1.35 | % | 1.30 | % | 1.27 | % | 1.26 | % | |||||

| Ratio of Net Investment Income (Loss) to Average Net Assets | -0.17 | % | 0.16 | % | 0.27 | % | -0.09 | % | -0.32 | % | |||||

| After Reimbursement (d) | |||||||||||||||

| Ratio of Expenses to Average Net Assets | 1.21 | % | 1.21 | % | 1.21 | % | 1.27 | % | 1.26 | % | |||||

| Ratio of Net Investment Income (Loss) to Average Net Assets | -0.00 | % + | 0.30 | % | 0.36 | % | -0.09 | % | -0.32 | % | |||||

| Portfolio Turnover Rate | 71.40 | % | 65.91 | % | 56.71 | % | 45.51 | % | 45.20 | % |

+ Amount calculated is less than +/-$0.005/0.005%.

(a) Per share amounts were calculated using the average shares method.

(b) Realized and unrealized gains and losses per share in this caption are balancing amounts necessary to

reconcile the change in net asset value for the period and may not reconcile with the aggregate gains and

losses in the Statement of Operations due to share transactions for the period.

(c) Total return represents the rate that the investor would have earned or lost on an investment in the

Fund assuming reinvestment of dividends.

(d) Effective December 31, 2018, the Advisor has agreed to waive a portion of its service fees and manage-

ment fees.

(e) Prior to June 1, 2021, shares were subject to a redemption fee of 2% if redeemed after holding them for

90 days or less.

Prospectus 19

| Financial Highlights - Institutional Class | ||||||||||||

| Selected data for a share outstanding throughout the period: | 2/1/2021 | 2/1/2020 | 2/1/2019 | 12/31/2018* | ||||||||

| to | to | to | to | |||||||||

| 1/31/2022 | 1/31/2021 | 1/31/2020 | 1/31/2019 | |||||||||

| Net Asset Value - | ||||||||||||

| Beginning of Period | $ | 20.53 | $ | 18.83 | $ | 18.70 | $ | 16.71 | ||||

| Net Investment Income (Loss) (a) | 0.05 | 0.09 | 0.11 | - | + | |||||||

| Net Gain (Loss) on Investments (Realized and Unrealized) (b) | 5.14 | 1.84 | 0.43 | 1.99 | ||||||||

| Total from Investment Operations | 5.19 | 1.93 | 0.54 | 1.99 | ||||||||

| Distributions (From Net Investment Income) | (0.12 | ) | (0.23 | ) | (0.02 | ) | - | |||||

| Distributions (From Capital Gains) | (7.38 | ) | - | (0.39 | ) | - | ||||||

| Total Distributions | (7.50 | ) | (0.23 | ) | (0.41 | ) | - | |||||

| Proceeds from Redemption Fee (e) | - | + | - | + | - | + | - | |||||

| Net Asset Value - | ||||||||||||

| End of Period | $ | 18.22 | $ | 20.53 | $ | 18.83 | $ | 18.70 | ||||

| Total Return (c) | 23.92 | % | 10.33 | % | 2.80 | % | 11.91 | %** | ||||

| Ratios/Supplemental Data | ||||||||||||

| Net Assets - End of Period (Thousands) | $ | 36,005 | $ | 96,863 | $ | 132,207 | $ | 7,741 | ||||

| Before Reimbursement | ||||||||||||

| Ratio of Expenses to Average Net Assets | 1.38 | % | 1.35 | % | 1.30 | % | 1.37 | %*** | ||||

| Ratio of Net Investment Income (Loss) to Average Net Assets | -0.20 | % | 0.15 | % | 0.23 | % | -0.23 | %*** | ||||

| After Reimbursement (d) | ||||||||||||

| Ratio of Expenses to Average Net Assets | 0.98 | % | 0.98 | % | 0.98 | % | 0.98 | %*** | ||||

| Ratio of Net Investment Income (Loss) to Average Net Assets | 0.20 | % | 0.52 | % | 0.55 | % | 0.16 | %*** | ||||

| Portfolio Turnover Rate | 71.40 | % | 65.91 | % | 56.71 | % | 45.51 | %** | ||||

* Commencement of Class.

** Not Annualized.

*** Annualized.

+ Amount calculated is less than $0.005/0.005%.

(a) Per share amounts were calculated using the average shares method.

(b) Realized and unrealized gains and losses per share in this caption are balancing amounts necessary to

reconcile the change in net asset value for the period and may not reconcile with the aggregate gains and

losses in the Statement of Operations due to share transactions for the period.

(c) Total return represents the rate that the investor would have earned or lost on an investment in the Fund

assuming reinvestment of dividends.

(d) Effective December 31, 2018, the Advisor has agreed to waive a portion of its service fees and manage-

ment fees.

(e) Prior to June 1, 2021, shares were subject to a redemption fee of 2% if redeemed after holding them for

90 days or less.

Prospectus 20

This page intentionally left blank

Prospectus 21

Where To Go For Information

For shareholder inquiries please, call toll-free in the U.S. at 1-888-925-8428. You will also find more information about the Fund on our website at www.walthausenfunds.com or in the following documents:

Statement of Additional Information

The Statement of Additional Information is on file with the Securities and Exchange Commission ("SEC"), contains additional and more detailed information about the Fund and is incorporated into this Prospectus by reference. The Fund publishes Shareholder Reports (annual and semiannual reports) that contain additional information about the Fund’s investments. In the Fund’s annual report, you will find a discussion of the market conditions and investment strategies that significantly affected the Fund’s performance during its last fiscal year.

You may obtain the SAI and Shareholder Reports without charge by contacting the Fund at 1-888-925-8428 or on our Internet site at: www.walthausenfunds.com. If you purchased shares through a Financial Intermediary, you may also obtain these documents, without charge, by contacting your Financial Intermediary.

Shareholder Reports and other information about the Fund is available on the EDGAR Database on the SEC's Internet site at http://www.sec.gov, and copies of this information may be obtained, after paying a duplicating fee, by electronic request at the following e-mail address: publicinfo@sec.gov.

Walthausen Funds SEC file number 811-22143

WALTHAUSEN SMALL CAP VALUE FUND

2691 Route 9, Suite

102 Malta, NY 12020

WALTHAUSEN FOCUSED SMALL CAP VALUE FUND

INSTITUTIONAL CLASS TICKER

For Investors Seeking Long-Term Capital Appreciation

PROSPECTUS

June 1, 2022

As with all mutual funds, the Securities and Exchange Commission has not approved or disapproved of these securities, nor has the Commission determined that this Prospectus is complete or accurate. Any representation to the contrary is a criminal offense.

| Table of Contents | |

| Summary Section | 1 |

| Investment Objective | 1 |

| Fees and Expenses of the Fund | 1 |

| The Principal Investment Strategy of the Fund | 2 |

| The Principal Risks of Investing in the Fund | 2 |

| Performance | 3 |

| Management | 4 |

| Purchase and Sale of Fund Shares | 4 |

| Tax Information | 4 |

| Payments to Broker-Dealers and Other Financial Intermediaries | 4 |

| Cybersecurity | 4 |

| Investment Objective, Principal Investment Strategy, | |

| Related Risks, and Disclosure of Portfolio Holdings | 5 |

| Investment Objective | 5 |

| The Principal Investment Strategy of the Fund | 5 |

| The Investment Selection Process Used by the Fund | 5 |

| The Principal Risks of Investing in the Fund | 6 |

| Portfolio Holdings Disclosure | 7 |

| Management | 8 |

| The Investment Advisor | 8 |

| Shareholder Information | 9 |

| Pricing of Fund Shares | 9 |

| Customer Identification Program | 9 |

| Investing in the Fund | 9 |

| Investments Made Through Brokerage Firms or Other Financial Institutions | 9 |

| Minimum Investments | 10 |

| Types of Account Ownership | 10 |

| Instructions For Opening and Adding to an Account | 11 |

| Telephone and Wire Transactions | 11 |

| Tax-Deferred Plans | 12 |

| Types of Tax-Deferred Accounts | 12 |

| Automatic Investment Plans | 13 |

| Instructions For Selling Fund Shares | 13 |

| Additional Redemption Information | 14 |

| Shareholder Communications | 15 |

| Dividends and Distributions | 15 |

| Share Classes | 16 |

| Market Timing | 16 |

| Taxes | 16 |

| Other Fund Service Providers | 17 |

| Privacy Policy | 18 |

| Financial Highlights | 19 |

• The Walthausen Focused Small Cap Value Fund seeks long-term capital appreciation.

The following table describes the expenses and fees that you may pay if you buy and hold shares of the Fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below.

| Institutional | |

| Class | |

| Sales Charge (Load) Imposed on Purchases | |

| Deferred Sales Charge (Load) | |

| Sales Charge (Load) Imposed on Reinvested Dividends | |

| Annual Fund Operating Expenses (expenses that you pay each | |

| year as a percentage of the value of your investment) | |

| Management Fees | |

| Distribution 12b-1 Fees | |

| Other Expenses | |

| Total Annual Fund Operating Expenses | |

| Fee Waiver / Expense Reimbursement (1) | ( |

| Total Annual Fund Operating Expenses After Fee Waiver |

| (1) |

The following example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The example also assumes that your investment has a 5% annual return each year and that the Fund’s operating expenses remain the same each year. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| Walthausen Focused Small Cap Value Fund | One Year | Three Years | Five Years | Ten Years |

| Institutional Class | $ |

$ |

$ |

$ |

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was

Prospectus 1

The Fund invests primarily in common stocks of small capitalization companies that Walthausen & Co., LLC (the "Advisor") believes have the potential for capital appreciation. The Advisor invests in small capitalization companies with market capitalizations below that of the largest member of the Russell 2000 Index at the time of purchase. As of April 30, 2022, the capitalization of the largest member of the Russell 2000 Index was $15.1 billion. The Fund typically invests in 30 to 50 companies. Under normal circumstances, the Fund will invest at least 80% of its net assets (plus any borrowings for investment purposes) in U.S. common stocks of small capitalization companies, as defined above. The Fund emphasizes a "value" investment style, investing in companies that appear underpriced according to certain financial measurements of their worth or business prospects. Financial measures which are used to assess value are Price to Book ratio and Enterprise Value to EBITDA (Earnings before interest, taxes, depreciation and amortization) ratio and other widely used valuation metrics. Those ratios are compared to similar metrics for the market and comparable securities. The Advisor defines Enterprise Value as the market value of a company's equity, debt and unfunded pension claims, less cash. EBITDA is a company's earnings before interest, taxes, depreciation and amortization.

The Advisor may sell a company when the company reaches the Advisor's projection of the stock's future target price, as determined by applying the Advisor's understanding of historical valuation metrics, when there is a more attractively priced company as an alternative, when the fundamentals of the business have changed, or when the Advisor determines that management of the company is not enhancing shareholder value. These portfolio reviews are conducted continuously through close monitoring of stock prices, changes in the economy, and corporate developments.

As with all mutual funds, there is the risk that you could lose some or all of your investment in the Fund.

Risks of Investing in Small Capitalization Companies

The Fund invests in the stocks of small capitalization companies, which may subject the Fund to additional risks. The earnings and prospects of these companies are generally more volatile than larger companies and small capitalization companies may experience higher failure rates than do larger companies.

Risks in General

Domestic economic growth and market conditions, interest rate levels, and political events are among the factors affecting the securities markets in which the Fund invests. There is risk that these and other factors may adversely affect the Fund’s performance.

Additionally, unexpected local, regional or global events, such as war; acts of terrorism; financial, political or social disruptions; natural, environmental or man-made disasters; the spread of infectious illnesses or other public health issues (such as COVID-19); and recessions and depressions could have a significant impact on the Fund's investments and could impair market liquidity. Such events can cause investor fear, which can adversely affect the economies of nations, regions and the market in general, in ways that cannot necessarily be foreseen.

Risks of Investing in Common Stocks

Overall stock market risks may affect the value of the Fund. Factors such as domestic economic growth and market conditions, interest rate levels, and political events affect the securities markets.

Prospectus 2

Value Investing Risk

Value investing attempts to identify companies selling at a discount to a projected future value. Value investing is subject to the risk that a company's intrinsic value may never be fully realized by the market or that a company judged by the Adviser to be undervalued may actually be appropriately priced.

Sector Risk

Sector risk is the possibility that all stocks within the same group of industries will decline in price due to sector-specific market or economic developments. The Fund may be overweight in certain sectors at various times.

Investment Management Risk

The Advisor’s strategy may fail to produce the intended results.

The as of was for the Institutional Class.

() + ()

FOR THE PERIODS ENDED 12/31/21 |

1 Year | 5 Years | 10 Years |

| WALTHAUSEN FOCUSED SMALL CAP VALUE FUND | |||

| (Institutional Class) | |||

| Return Before Taxes | |||

| Return After Taxes on Distributions | |||

| Return After Taxes on Distributions and Sale of Fund Shares | |||

| Russell 2000 Value Index (does not reflect deductions for fees, | |||

| expenses or taxes) | |||

Prospectus 3

Management

Investment Advisor

Walthausen & Co., LLC (the “Advisor”)

Portfolio Managers

Gerard S.E. Heffernan has managed the Fund since March 2018. Mr. Heffernan is a Portfolio Manager and Managing Director of the Advisor.

Purchase and Sale of Fund Shares

The minimum initial and subsequent investment amounts for various types of accounts offered by the Fund are shown below.

| Institutional Class | Initial | Additional |

| Regular Account | $10,000 | $1,000 |

| Automatic Investment Plan | $10,000 | $1,000 |

| IRA Account | $5,000 | $500 |

Investors may purchase or redeem Fund shares on any business day through a financial intermediary, by mail (Walthausen Funds, c/o Ultimus Fund Solutions, LLC, P.O. Box 46707, Cincinnati, Ohio 45246-0707), by wire, or by telephone at 1-888-925-8428.

Tax Information

The Fund’s distributions are taxable, and will be taxed as ordinary income or capital gains, unless you are investing through a tax-deferred arrangement, such as a 401(k) plan or an individual retirement account. Such tax-deferred arrangements may be taxed later upon withdrawal of monies from those arrangements.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase the Fund through a broker-dealer or other financial intermediary (such as a financial advisor), the Fund and/or its investment adviser may pay the intermediary a fee as compensation for the services it provides. These payments may create a conflict of interest by influencing the financial intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

Cybersecurity

The computer systems, networks and devices used by the Fund and its service providers to carry out routine business operations employ a variety of protections designed to prevent damage or interruption from computer viruses, network failures, computer and telecommunication failures, infiltration by unauthorized persons and security breaches. Despite the various protections utilized by the Fund and its service providers, systems, networks, or devices potentially can be breached. The Fund and its shareholders could be negatively impacted as a result of a cybersecurity breach.

Prospectus 4

Cybersecurity breaches can include unauthorized access to systems, networks, or devices; infection from computer viruses or other malicious software code; and attacks that shut down, disable, slow, or otherwise disrupt operations, business processes, or website access or functionality. Cybersecurity breaches may cause disruptions and impact the Fund’s business operations, potentially resulting in financial losses; interference with the Fund’s ability to calculate its NAV; impediments to trading; the inability of the Fund, the Advisor, and other service providers to transact business; violations of applicable privacy and other laws; regulatory fines, penalties, reputational damage, reimbursement or other compensation costs, or additional compliance costs; as well as the inadvertent release of confidential information.

Similar adverse consequences could result from cybersecurity breaches affecting issuers of securities in which the Fund invests; counterparties with which the Fund engages in transactions; governmental and other regulatory authorities; exchange and other financial market operators, banks, brokers, dealers, insurance companies, and other financial institutions (including financial intermediaries and service providers for the Fund’s shareholders); and other parties. In addition, substantial costs may be incurred by these entities in order to prevent any cybersecurity breaches in the future.

Investment Objective, Principal Investment Strategy, Related Risks, and Disclosure of Portfolio Holdings

Investment Objective

• The Fund seeks long-term capital appreciation.

The Principal Investment Strategy of the Fund

The Fund invests primarily in common stocks of small capitalization companies that Walthausen & Co., LLC (the "Advisor") believes have the potential for capital appreciation. The Advisor invests in small capitalization companies with market capitalizations below that of the largest member of the Russell 2000 Index at the time of purchase. As of April 30, 2022, the capitalization of the largest member of the Russell 2000 Index was $15.1 billion. The Fund typically invests in 30 to 50 companies. Under normal circumstances, the Fund will invest at least 80% of its net assets (plus any borrowings for investment purposes) in U.S. common stocks of small capitalization companies, as defined above. The Fund emphasizes a "value" investment style, investing in companies that appear underpriced according to certain financial measurements of their worth or business prospects. Financial measures which are used to assess value are Price to Book ratio and Enterprise Value to EBITDA (Earnings before interest, taxes, depreciation and amortization) ratio and other widely used valuation metrics. Those ratios are compared to similar metrics for the market and comparable securities. The Advisor defines Enterprise Value as the market value of a company's equity, debt and unfunded pension claims, less cash. EBITDA is a company's earnings before interest, taxes, depreciation and amortization. The Fund may invest in other securities as described in the Statement of Additional Information, which is available upon request.

The Investment Selection Process Used by the Fund

The Advisor uses a process with multiple steps to review the universe of small capitalization companies from various angles to identify a diversified pool of quality candidates. The methods used by the Adviser to search for candidates include: a proprietary scoring system that focuses on finding companies on the cusp of positive change, demonstrated by characteristics such as an acceleration in revenues, an inflection to expanding profit margins, cash flow and/or earnings growth, or an event that will reduce company debt; a screen to identify stocks that are trading at the low end of their historical valuation; tracking insider transactions for indications that management is confident of future prospects; attending investor conferences and corporate analyst events to learn details of corporate plans. The Advisor's detailed analysis involves a review of relevant regulatory filings including 10Ks, 10Qs and proxy statements and analysis of available information including credit agreements, indus-

Prospectus 5

try publications, and news articles. The Advisor uses this information to understand the business and build financial models. Models are constructed using consistent formats that allow the Advisor to find pertinent information enabling it to compare each candidate to other companies that the Advisor has also analyzed. In constructing the models, the two critical areas for the Advisor are the cash flow statement and balance sheet because they allow the Advisor to evaluate a company's sustainable free cash flow. Given the importance that the Advisor places on a company's cash flow, the analysts pay particular attention to the accounting footnotes contained within. The portfolio managers and analysts develop a detailed projection of future earnings, cash flow and balance sheet to assist in developing an investment rational or thesis along with detailed price targets and an examination of risks inherent in the investment.

The Advisor may sell a company when the company reaches the Advisor's projection of the stock's future target price, as determined by applying the Advisor's understanding of historical valuation metrics, when there is a more attractively priced company as an alternative, when the fundamentals of the business have changed, or when the Advisor determines that management of the company is not enhancing shareholder value. These portfolio reviews are conducted continuously through close monitoring of stock prices, changes in the economy, and corporate developments.