As filed with the Securities and Exchange Commission on November 19, 2012

Registration No. 333-182599

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

PROSPER MARKETPLACE, INC.

(Exact name of registrant as specified in its charter)

|

Delaware

|

6199

|

73-1733867

|

|

(State or other jurisdiction of incorporation or organization)

|

(Primary Standard Industrial Classification Code Number

|

(I.R.S. Employer Identification Number)

|

111 Sutter Street, 22nd Floor

San Francisco, CA 94104

(415) 593-5400

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Sachin Adarkar, Esq.

General Counsel

111 Sutter Street, 22nd Floor

San Francisco, CA 94104

(415) 593-5400

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Keir D. Gumbs, Esq.

Covington & Burling LLP

1201 Pennsylvania Avenue, NW

Washington, DC 20004

(202) 662-6000

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 as amended (the “Securities Act”), check the following box. T

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

o

|

Accelerated filer

|

o

|

|

|

Non-accelerated filer

|

o (Do not check if a smaller reporting company)

|

Smaller reporting company

|

T

|

CALCULATION OF REGISTRATION FEE

|

Title of Securities being Registered

|

Proposed Maximum

Aggregate

Offering Price

|

Amount of

Registration

Fee(1)

|

||

|

Borrower Payment Dependent Notes

|

$300,000,000

|

$1

|

(1) Pursuant to Rule 415(a)(6) under the Securities Act of 1933, we are carrying over to this registration statement $300,000,000 of unsold securities from registration #333-147019 filed on October 10, 2007, for which the filing fee of $15,350 was previously paid. No additional filing fee is being paid with this registration statement because no additional securities are being registered. In accordance with Rule 415(a)(6), the offering of securities on the earlier registration statement will be deemed terminated as of the effective date of this registration statement.

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED NOVEMBER 19, 2012

$300,000,000 Borrower Payment Dependent Notes

This is a public offering to lender members of Prosper Marketplace, Inc., or Prosper, of up to $300,000,000 in principal amount of Borrower Payment Dependent Notes, or “Notes.”

We will issue the Notes in a series, with each series of Notes dependent for payment on payments we receive on a specific borrower loan described in a listing posted on our peer-to-peer online credit platform, which we refer to as our “platform.” All listings on our platform are posted by individual consumer borrower members of Prosper requesting individual consumer loans, which we refer to as “borrower loans.”

Important terms of the Notes include the following, each of which is described in detail in this prospectus:

|

·

|

Our obligation to make payments on a Note will be limited to an amount equal to the lender member’s pro rata share of amounts we receive with respect to the corresponding borrower loan for that Note, net of any servicing fees. We do not guarantee payment of the Notes or the corresponding borrower loans.

|

|

·

|

The Notes are special, limited obligations of Prosper only and are not obligations of the borrowers under the corresponding borrower loans.

|

|

·

|

The Notes will bear interest from the date of issuance, have a fixed rate, be payable monthly and have an initial maturity of one, three or five years from issuance. We may add additional Note terms from time to time.

|

|

·

|

A lender member’s recourse will be extremely limited in the event that borrower information is inaccurate for any reason.

|

We will offer Notes to our lender members at 100% of their principal amount. The Notes will be offered only through our website, and there will be no underwriters or underwriting discounts.

The Notes will be issued in electronic form only and will not be listed on any securities exchange. The Notes will not be transferable except through the Folio Investing Note Trader platform, or the “Note Trader Platform,” operated and maintained by FOLIOfn Investments, Inc., a registered broker-dealer. There can be no assurance, however, that a market for Notes will develop on the Note Trader platform. Therefore, lender members must be prepared to hold their Notes to maturity.

This offering is highly speculative and the Notes involve a high degree of risk. Investing in the Notes should be considered only by persons who can afford the loss of their entire investment. See “Risk Factors” on page 22.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is _____, 2012

PROSPER MARKETPLACE, INC.

TABLE OF CONTENTS

|

ii

|

|

|

iii

|

|

|

1

|

|

|

4

|

|

|

9

|

|

|

20

|

|

|

22

|

|

|

23

|

|

|

23

|

|

|

23

|

|

|

25

|

|

|

26

|

|

|

36

|

|

|

43

|

|

|

43

|

|

|

44

|

|

|

48

|

|

|

49

|

|

|

50

|

|

|

55

|

|

|

55

|

|

|

55

|

|

|

55

|

ABOUT THIS PROSPECTUS

This prospectus describes our offering of our Borrower Payment Dependent Notes, or “Notes.” This prospectus is part of a registration statement filed with the Securities and Exchange Commission, which we refer to as the “SEC.” This prospectus, and the registration statement of which it forms a part, speak only as of the date of this prospectus. We will supplement this registration statement from time to time as described below.

Unless the context otherwise requires, we use the terms “Prosper,” “the Company,” “our company,” “we,” “us” and “our” in this prospectus to refer to Prosper Marketplace, Inc., a Delaware corporation.

The offering described in this prospectus is a continuous offering pursuant to Rule 415 under the Securities Act of 1933, as amended (the “Securities Act”). We offer Notes continuously, and sales of Notes through our platform occur on a daily basis. Before we post a borrower loan request on our website and thereby offer the series of Notes corresponding to that borrower loan, as described in “About Prosper,” we prepare a supplement to this prospectus, which we refer to as a “listing report.” In that listing report, we provide information about the series of Notes offered for sale on our website that correspond to the posted member loan, as well as information about any other series of Notes then being offered for sale on our website. No later than two business days after the date the bidding period for a loan listing ends and a series of Notes is sold, we will file another prospectus supplement with the SEC, which we refer to as a “sales report”, describing all borrower loan information set forth on the bidding page for that series of Notes in tabular form, as well as the aggregate principal balance, bidding history, maturity date and interest rate for that series of Notes. These prospectus supplements will provide information about the series of Notes offered for sale on our website that will correspond to the information contained in the corresponding borrower loan listing for that series of Notes. The listing and sales reports are also posted to our website.

We will prepare prospectus supplements to update this prospectus for other purposes, such as to disclose changes to the terms of our offering of the Notes, provide quarterly updates of our financial and other information included in this prospectus and disclose other material developments. We will file these prospectus supplements with the SEC pursuant to Rule 424(b) and post them on our website. When required by SEC rules, such as when there is a “fundamental change” in our offering or the information contained in this prospectus, or when an annual update of our financial information is required by the Securities Act or SEC rules, we will file post-effective amendments to the registration statement of which this prospectus forms a part, which will include either a prospectus supplement or an entirely new prospectus to replace this prospectus. We currently anticipate that post-effective amendments will be required, among other times, when we change material terms of the Notes offered through our platform.

The Notes are not available for offer and sale to residents of every state. Our website will indicate the states where residents may purchase Notes. We will post on our website any special suitability standards or other conditions applicable to purchases of Notes in certain states that are not otherwise set forth in this prospectus.

WHERE YOU CAN FIND MORE INFORMATION

We have filed a registration statement on Form S-1 with the SEC in connection with this offering. In addition, we are required to file annual, quarterly and current reports and other information with the SEC. You may read and copy the registration statement and any other documents we have filed at the SEC’s Public Reference Room at 100 F Street, N.E., Room 1580, Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the Public Reference Room. Our SEC filings are also available to the public at the SEC’s Internet site at http://www.sec.gov.

This prospectus is part of the registration statement and does not contain all of the information included in the registration statement and the exhibits, schedules and amendments to the registration statement. Some items are omitted in accordance with the rules and regulations of the SEC. For further information with respect to us and the Notes, we refer you to the registration statement and to the exhibits and schedules to the registration statement filed as part of the registration statement. Whenever a reference is made in this prospectus to any of our contracts or other documents, the reference may not be complete and, for a copy of the contract or document, you should refer to the exhibits that are a part of the registration statement.

We “incorporate” into this prospectus information we filed with the SEC in our Annual Report on Form 10-K/A (“Annual Report”) for the fiscal year ended December 31, 2011 filed on November 14, 2012, our Quarterly Report on Form 10-Q for the period ended September 30, 2012 filed on November 7, 2012, our Quarterly Report on Form 10-Q for the period ended June 30, 2012 filed on August 9, 2012, our Quarterly Report on Form 10-Q for the period ended March 31, 2012 filed on May 15, 2012 (“Quarterly Reports”), our Current Report on Form 8-K filed on March 7, 2012, our Current Report on Form 8-K filed on March 15, 2012 and our Current Report on Form 8-K filed on June 25, 2012 (“Current Reports”). This means that we disclose important information to you by referring you to our Annual Report for the fiscal year ended December 31, 2011, our Quarterly Report for the period ended September 30, 2012 and our Current Reports on Form 8-K filed on March 7, 2012, March 15, 2012 and June 25, 2012, which are available on our website, www.prosper.com . The information incorporated by reference is considered to be part of this prospectus. Information contained in this prospectus automatically updates and supersedes previously filed information.

You may request a copy of our Annual Report, Quarterly Reports and our Current Reports, which will be provided to you at no cost, by writing, telephoning or emailing us. Requests should be directed to Customer Support, 111 Sutter St, 22nd Floor, San Francisco, CA 94104; telephone number (415) 593-5400; or emailed to support@prosper.com. In addition, our Annual Reports and Quarterly Reports are available on our website, www.prosper.com.

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus. You should read the following summary together with the more detailed information appearing in this prospectus, including our financial statements and related notes, and the risk factors beginning on page 22, before deciding whether to purchase our Notes.

Prosper provides a peer-to-peer online credit platform, which we refer to as our “platform,” that enables its borrower members to borrow money and its lender members to purchase Notes issued by Prosper, the proceeds of which facilitate the funding of specific loans made to borrower members.

About the Platform

Our platform is an online marketplace that permits our lender members to bid on loan listings and purchase Notes from Prosper that are dependent for payment on payments we receive on the corresponding borrower loans described in the listings. All listings on our platform are posted by individual consumer members of Prosper requesting individual consumer loans, which we refer to as “borrower listings” or “listings” and “borrower loans,” respectively. We refer to Prosper’s individual borrower members as “borrowers.”

Each listing sets forth the desired loan amount, interest rate and corresponding yield percentage, the minimum amount of total bids required for the loan to fund, the Prosper Rating and estimated loss rate for the listing, debt-to-income ratio, certain credit information from the borrower’s credit report, the borrower’s numerical credit score range, the borrower’s self-reported annual income range, occupation and employment status, and the borrower’s group affiliation, if any.

Prosper sets the interest rates for borrower loans based on Prosper Ratings, as well as additional factors, such as estimated loss rates, loan terms, group affiliations, the general economic environment and competitive conditions. The yield percentage on each series of Notes is equal to the interest rate on the related borrower loan, minus Prosper’s servicing fee, currently set at 1%, which Prosper may extend in the future to between 1% and 3%.

Apart from the credit score range and information obtained from a credit report, such as number of accounts delinquent, public records, and other such borrower credit information, none of the information regarding the borrower’s income, financial status, or self-reported credit history is verified by Prosper. Such information is self-reported and should not be relied on by lender members in making investment decisions. Borrower listings may include the borrower’s narrative description of why the loan is being requested and the borrower’s financial situation. Borrowers are identified by a Prosper screen name but are not permitted to disclose in listings their identity or contact information. Listings are displayed publicly on our platform, although certain information is only viewable by members.

Each listing will be assigned a proprietary credit rating by Prosper, referred to as the “Prosper Rating.” The Prosper Rating is a letter that indicates the level of risk associated with a listing and corresponds to an estimated average annualized loss rate range for the listing. There are currently seven Prosper Ratings, represented by seven letter scores, but this, as well as the loss ranges associated with each, may change over time as the marketplace dictates. The estimated loss rate for each listing is based on two scores: a consumer reporting agency score and an in-house custom score calculated using the historical performance of previous borrower loans with similar characteristics. We will use these two scores to determine an estimated loss rate for each listing, which correlates to a Prosper Rating. This new rating system allows Prosper to maintain consistency when assigning a rating to a listing. See “About Prosper” for more information.

The Notes. Our lender members will have the opportunity to buy Borrower Payment Dependent Notes issued by Prosper, which are dependent for payment on payments we receive on the corresponding borrower loans.

Lender members access our platform and, by bidding on a loan listing, make purchase commitments for Notes that are dependent for payment on payments we receive on the corresponding borrower loan for that listing. By making a bid on a listing, a lender member is committing to purchase from Prosper a Note in the principal amount of the lender’s winning bid. The lender members who purchase the Notes will designate that the sale proceeds be applied to facilitate the funding of the corresponding borrower loan. The Notes will be special, limited obligations of Prosper only and not obligations of any borrower.

The Notes are unsecured and holders of the Notes do not have a security interest in the corresponding borrower loans or the proceeds of those corresponding borrower loans. If Prosper were to become subject to a bankruptcy or similar proceeding, the holder of a Note would generally have a general unsecured claim against Prosper that may or may not be limited in recovery to such borrower payments. To limit the risk of Prosper’s insolvency, Prosper has granted the trustee under the indenture for the Notes, referred to as the “indenture trustee,” a security interest in Prosper’s right to payment under, and all proceeds received by Prosper on, the corresponding borrower loans and in the bank account in which the borrower loan payments are deposited. The indenture trustee may exercise its legal rights to the collateral only if an event of default has occurred under the indenture, which would include Prosper becoming subject to a bankruptcy or similar proceeding. See “Risk Factors—Risks Related to Prosper, Our Platform and Our Ability to Service the Notes.”

Prosper will pay principal and interest on each series of Notes in an amount equal to each such Note’s pro rata portion of the principal and interest payments, if any, Prosper receives on the corresponding borrower loan, net of Prosper’s servicing fee, currently set at 1%, which Prosper may extend in the future to between 1% and 3%. Prosper will pay lender members any other amounts Prosper receives on each corresponding borrower loan, including late fees and prepayments, subject to the servicing fee, except that Prosper will not pay to lender members any non-sufficient funds fees for failed borrower payments or collection fees we or a third-party collection agency charge.

Under the lender member registration agreement, in the event of a material default under a series of Notes due to verifiable identity theft of the named borrower’s identity, Prosper will repurchase the Notes from the lender members. In the event we breach any of our other representations and warranties in the lender registration agreement pertaining to the Notes, and such breach materially and adversely affects a series of Notes, we will either indemnify the lender members, repurchase that series of Notes or cure the breach. See “About Prosper.”

Borrower Loans. Our platform allows our borrower members to request loans by posting listings on the platform indicating a requested loan amount. All borrower loans are unsecured obligations of individual borrower members with a fixed interest rate set by Prosper and a loan term currently set at one, three or five years, which Prosper may extend in the future to between three months to seven years. The minimum and maximum principal amounts for borrower loans are currently $2,000 and $25,000, respectively, but in the future Prosper may permit borrowers to request loans in principal amounts between $500 and $35,000. Lender members may access our platform and bid by indicating that they are willing to purchase Notes relating to the borrower loan in the principal amounts of their respective bids. If at the end of the bidding period the listing has received bids equal to or exceeding the minimum amount required for the loan to fund, a loan will be made to the borrower in an amount equal to the total amount of all winning bids, at the interest rate set by Prosper.

All borrower loans will be funded by WebBank, a Federal Deposit Insurance Corporation (“FDIC”) insured, Utah-chartered industrial bank. After funding a loan, WebBank sells and assigns the loan to Prosper, without recourse to WebBank, in exchange for the principal amount of the borrower loan. WebBank has no obligation to purchasers of the Notes. For all borrower loans, Prosper verifies the borrower member’s identity against data from consumer reporting agencies and other identity and anti-fraud verification databases. Borrower listings are posted without our obtaining any documentation of the borrower’s ability to afford the loan. In limited instances, we verify the income, employment, occupation or other information provided by Prosper borrower members in listings. This verification is normally done after the listing has been created and bidding is substantially complete, but before the loan is funded, and therefore the results of our verification are not reflected in the borrower listings.

Borrower loans will be serviced by Prosper. Prosper refers borrower loans that become more than 30 days past-due to a third party collection agency for collection proceedings. For loans that were originated between November 2005 and July 12, 2009, as of December 31, 2011, 11,826 loans or 41% of all borrower loans ever funded have been referred to a collection agency for collection proceedings, and 43% have been greater than 30 days past due at any time; 40% have been greater than 60 days past due at any time. For loans that were originated between July 13, 2009 and December 31, 2011, as of December 31, 2011, 1,461 loans or 8% of all borrower loans ever funded have been referred to a collection agency for collection proceedings and 7% have been greater than 30 days past due at any time; 6% have been greater than 60 past due at any time. See “About Prosper.”

Quick Invest. Our loan search tool, Quick Invest, allows lender members to identify Notes that meet their investment criteria. A lender using Quick Invest is asked to indicate (i) the Prosper Rating or Ratings she wishes to use as search criteria, (ii) the total amount she wishes to invest and (iii) the amount she wishes to invest per Note. Quick Invest then compiles a basket of Notes for her consideration that meet her search criteria. If the pool of Notes that meet her criteria exceeds the total amount she wishes to invest, Quick Invest selects Notes from the pool based on how far the listings corresponding to the Notes have progressed through our loan verification process, i.e. , Notes from the pool that correspond to listings for which we have completed our loan verification process will be selected first. If the pool of Notes that meet the lender member’s criteria and for which we have completed loan verification still exceeds the amount she wishes to invest, Quick Invest selects Notes from that pool based on the principle of first in, first out, i.e. , the Notes from the pool with the corresponding listings that were posted on our website earliest will be selected first. If the member’s search criteria include multiple Prosper Ratings, Quick Invest divides the lender’s basket into equal portions, one portion representing each Prosper Rating selected. To the extent available Notes with these Prosper Ratings are insufficient to fill the lender’s order, the lender is advised of this shortfall and given an opportunity either to reduce the size of her order or to modify her search criteria to make her search more expansive. Our Auto Quick Invest feature allows lender members (i) to have Quick Invest searches run on their designated criteria automatically each time new listings are posted on our platform, and (ii) to place bids on any Notes identified by each such search. See “About Prosper.”

Prosper Funding LLC. On February 17, 2012, the Company formed Prosper Funding LLC, a Delaware limited liability company (“PFL”). The Company is the sole member of PFL. PFL has been organized and will be operated in a manner that is intended to minimize the likelihood that it will (i) become subject to bankruptcy proceedings or (ii) be substantively consolidated with the Company, and thus have its assets subject to claims by the Company’s creditors, in the event the Company becomes subject to a bankruptcy proceeding. The Company intends to restructure its platform so borrower loans are held by PFL and PFL issues and sells the borrower payment dependent notes tied to the loans. On March 7, 2012, PFL filed a registration statement on Form S-1 with the SEC for a continuous offering and sale of such notes. After PFL’s registration statement is declared effective, but before PFL commences offering notes pursuant to such registration statement, the Company intends for PFL to assume all outstanding Notes issued by the Company. PFL has not commenced operations as of the date of this prospectus.

Corporate Information

We were incorporated in the State of Delaware in March 2005, and our principal executive offices are located at 111 Sutter Street, 22nd Floor, San Francisco, California 94104. Prosper’s telephone number at this location is (415) 593-5400. Prosper’s website address is www.prosper.com. The information contained on our website is not incorporated by reference into this prospectus.

From the launch of our platform in February of 2006 until October 16, 2008, the operation of our platform differed from the structure described in this prospectus and we did not offer Notes. Instead, our platform allowed lender members to purchase, and take assignment of, borrower loans directly. Under that structure the borrower loans were evidenced by individual promissory notes in the amount of each lender member’s winning bid, which notes were thereafter sold and assigned to each lender member with a winning bid, subject to our right to service the borrower loans. In addition, we previously assigned one of seven letter credit grades based on the borrower’s credit score and displayed the borrower’s credit grade in the listing posted on our platform. Commencing July 13, 2009, each listing was assigned a Prosper Rating, which is derived from two scores: a consumer reporting agency score and an in-house custom score calculated using the historical performance of previous borrower loans with similar characteristics.

From October 16, 2008 until July 13, 2009 except for a brief period between April 28, 2009 and May 8, 2009 during which our wholly owned subsidiary Prosper Loans Marketplace, Inc. conducted an intrastate offering under Section 3(a)(11) of the Securities Act to California residents only and no securities were issued, we did not offer lender members the opportunity to make any purchases on our platform. During this time, we also did not accept new lender registrations or allow new loan purchase commitments from existing lender members. We continued to service all borrower loans originated on the platform on or before October 16, 2008, and lender members were able to access their accounts, monitor their borrower loans and withdraw available funds without charge. We also limited the borrowing side of our platform during this period. Borrowers could still request loans, but those loan requests were forwarded to companies that had a pre-existing relationship with Prosper that could make or facilitate a loan to the borrower.

Our historical financial results and much of the discussion in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” reflects the structure of our lending platform and our operations prior to July 13, 2009. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our Annual Report for the fiscal year ended December 31, 2011, pages 73-83, which is incorporated by reference in this prospectus.

THE OFFERING

|

Issuer

|

Prosper Marketplace, Inc.

|

|

|

Securities offered

|

Prosper Borrower Payment Dependent Notes, or “Notes,” issued in series, with each series dependent for payment on payments Prosper receives on a specific borrower loan.

|

|

|

Offering price

|

100% of principal amount of each Note.

|

|

|

Initial maturity date

|

Maturities are for one, three or five years and match the maturity date of the corresponding borrower loan. Prosper may in the future extend available loan terms to between three months to seven years, at which time the Notes will have terms between three months and seven years.

|

|

|

Final maturity date / Extension of maturity date

|

The final maturity date of each Note is the date that is one year after the initial maturity date. Each Note will mature on the initial maturity date, unless any principal or interest payments in respect of the corresponding borrower loan remain due and payable to Prosper upon the initial maturity date, in which case the maturity of the Note will be automatically extended to the final maturity date. If there are any amounts under the corresponding borrower loan still due and owing to us after the final maturity date, we will have no further obligation to make payments on the Notes of the series even if we receive payments on the corresponding borrower loan after the final maturity date. However, because we may, in our sole discretion and subject to our servicing standard, amend, modify, sell to a third-party debt purchaser or charge-off the borrower loan at any time after the 31st day of its delinquency, and because we generally charge-off a loan after it becomes more than 120 days past due, a borrower loan may never reach the final maturity date.

|

|

|

Interest rate

|

Each series of Notes will have a stated, fixed interest rate equal to its yield percentage determined by Prosper, which is the interest rate for the corresponding borrower loan, net of servicing fees.

|

|

|

Setting interest rate for Notes

|

Interest rates vary among the Notes, but each series of Notes that corresponds to a single borrower loan will have the same interest rate. Prosper sets the interest rates for borrower loans based on their Prosper Ratings, as well as additional factors such as estimated loss rates, loan terms, group affiliations, the economic environment and competitive conditions. The interest rate on each Note is equal to the interest rate on the corresponding borrower loan, net of servicing fees. See “About Prosper.”

|

|

Payments on the Notes

|

We will pay principal and interest on any Note a lender member purchases in an amount equal to the lender member’s pro rata portion of the principal and interest payments, if any, we receive on the corresponding borrower loan, net of servicing fees and other charges. See “—Servicing Fees and Other Charges.” Each Note will provide for monthly payments over a term equal to the corresponding borrower loan. The payment dates for the Notes will fall on the sixth day after the due date for each installment of principal and interest on the corresponding borrower loan. See “Summary of Material Agreements—Indenture as Form of Notes” for more information.

|

|

|

Borrower loans

|

Lender members will designate Prosper to apply the proceeds from the sale of each series of Notes to Prosper’s purchase of the corresponding borrower loan from WebBank. Each borrower loan is a fully amortizing consumer loan made by WebBank to an individual Prosper borrower member. Borrower loans currently have a term of one, three or five years, but Prosper may in the future extend available loan terms to between three months to seven years. Borrower members may request loans within specified minimum and maximum principal amounts (currently between $2,000 and $25,000, but which may increase to between $500 and $35,000), which are subject to change from time to time. WebBank subsequently sells and assigns the borrower loan to Prosper without recourse to WebBank in exchange for the principal amount of the borrower loan. Borrower loans are repayable in monthly installments and are unsecured and unsubordinated. Borrower loans may be repaid at any time by Prosper borrower members without prepayment penalty. Prosper verifies the borrower member’s identity against data from consumer reporting agencies and other identity and anti-fraud verification databases. Borrower listings are posted without our obtaining any documentation of the borrower member’s ability to afford the loan. In limited instances, we verify the income, employment, occupation or other information provided by Prosper borrower members in listings. This verification is normally done after the listing has been created and bidding is substantially completed, but before the loan has funded, and therefore the results of our verification are not reflected in the listings. Prosper is responsible for servicing the borrower loans. See “About Prosper” for more information.

Borrower members are able to use the loan proceeds for any purpose other than buying, carrying or trading in securities or buying or carrying any part of an investment contract security and they warrant and represent that they will not use the proceeds for any such purpose.

|

|

|

Security Interest—Ranking

|

The Notes will not be contractually senior or contractually subordinated to any other indebtedness of Prosper. All Notes will be unsecured special, limited obligations of Prosper. The Notes do not restrict Prosper’s incurrence of other indebtedness or the grant or imposition of liens or security interests on the assets of Prosper, and holders of the Notes do not have a security interest in the corresponding borrower loan or the proceeds of that loan. Accordingly, in the event of a bankruptcy or similar proceeding of Prosper, the relative rights of a holder of a Note, as compared to the holders of unsecured indebtedness of Prosper, are uncertain. To limit the risk of Prosper’s insolvency, Prosper has granted the indenture trustee a security interest in Prosper’s right to payment under, and all proceeds received by Prosper on, the corresponding borrower loans and in the bank account in which the borrower loan payments are deposited. The indenture trustee may exercise its legal rights to the collateral only if an event of default has occurred under the indenture, which would include Prosper becoming subject to a bankruptcy or similar proceeding. Only the indenture trustee, not the holders of the Notes, has a security interest in the above collateral. See “Risk Factors—Risks Related to Prosper, Our Platform and Our Ability to Service the Notes” for more information.

|

|

Servicing fees and Other

Charges

|

We receive a servicing fee equal to an annualized rate currently set at 1% of the outstanding principal balance of the corresponding borrower loan, but which Prosper may extend in the future to between 1% and 3%, which we deduct from each lender member’s share of the borrower loan payments we receive. Any change to our servicing fee will apply only to Notes offered and sold after the date of the change. Listings set forth the servicing fee charged by Prosper. Because servicing fees reduce the effective yield to lenders, the yield percentage displayed in listings is net of servicing fees.

Any non-sufficient funds fees charged to a borrower’s account will be retained by Prosper as additional servicing compensation. If a borrower loan enters collection, either Prosper or the collection agency will charge a collection fee of between 17% and 40% of any amounts that are obtained, in addition to any legal fees incurred in the collection effort. The collection fee will vary dependent upon the collection agency used. The collection fees charged by the various collection agencies can be accessed through hyperlinks from the bidding page on our platform. These fees will correspondingly reduce the amounts of any payments lender members receive on the Notes and are not reflected in the yield percentage displayed in listings.

We will pay lender members any late fees we receive on borrower loans.

|

|

|

Use of proceeds

|

We will use the proceeds of each series of Notes to purchase the corresponding borrower loan obtained by the borrower member.

|

|

|

Electronic form and transferability

|

The Notes will be issued in electronic form only and will not be listed on any securities exchange. The Notes will not be transferable except through the Folio Investing Note Trader platform operated and maintained by FOLIO fn Investments, Inc., a registered broker-dealer. There can be no assurance that a market for the Notes will develop on the Note Trader platform and, therefore, lender members must be prepared to hold their Notes to maturity. See “About Prosper” for more information.

|

|

|

U.S. federal income tax consequences

|

Although the matter is not free from doubt, we intend to treat the Notes as our debt instruments that have original issue discount (“OID”) for U.S. federal income tax purposes. Accordingly, if you hold a Note, you will be required to include OID currently as ordinary interest income for U.S. federal income tax purposes (which may be in advance of interest payments on the Note) if the Note has a maturity date of more than one year, regardless of your regular method of tax accounting. If the Note has a maturity of one year or less, (1) if you are a cash-method taxpayer, in general, you will not have to include OID currently in income on your Note unless you elect to do so, and (2) if you are an accrual-method taxpayer, in general, you will have to include OID currently in income on your Note. You should consult your own tax advisor regarding the U.S. federal, state, local and non-U.S. tax consequences of the purchase, ownership, and disposition of the Notes (including any possible differing treatments of the Notes). See “Material U.S. Federal Income Tax Considerations” for more information.

|

|

|

Financial suitability

|

To purchase Notes, lender members located in Idaho, Maine, New Hampshire, Oregon, Virginia and Washington must meet one or more of the following suitability requirements:

|

| a. | (i) You must have an annual gross income of at least $70,000; (ii) your net worth must be at least $70,000; and (iii) the total amount of Notes you purchase cannot exceed 10% of your net worth; or | ||

|

b.

|

(i) Your net worth must be at least $250,000; and (ii) the total amount of Notes you purchase cannot exceed 10% or your net worth. |

| Lender members that are residents of California must meet one or more of the following suitability requirements: | |||

|

a.

|

(i) You must have had an annual gross income of at least $85,000 during the last tax year; (ii) you must have a good faith belief that your annual gross income for the current tax year will be at least $85,000; and (iii) the total amount of Notes you purchase cannot exceed 10% of your net worth; or | ||

|

b.

|

(i) Your net worth must be at least $200,000; and (ii) the total amount of Notes you purchase cannot exceed 10% or your net worth; or | ||

| c. | (i) Your net investment in Notes cannot exceed $2,500; and (ii) the total amount of Notes you purchase cannot exceed 10% or your net worth. | ||

|

For purposes of these suitability requirements, you and your spouse are considered to be a single person. In addition, the following definitions apply:

"annual gross income" means the total amount of money you earn each year, before deducting any amounts for taxes, insurance, retirement contributions or any other payments or expenses;

"net worth" means the total value of all your assets, minus the total value of all your liabilities. The value of an asset is equal to the price at which you could reasonably expect to sell it. In calculating your net worth, you should only include assets that are liquid, meaning assets that consist of cash or something that could be quickly and easily converted into cash, such as a publicly-traded stock. You shouldn't include any illiquid assets, such as homes, home furnishings or cars;

"net investment" means the principal amount of Notes purchased, minus principal payments received on the Notes.

Lender members should be aware that we may apply more restrictive financial suitability standards or maximum investment limits to residents of certain states. If established, before making commitments to purchase Notes, each lender member will be required to represent and warrant that he or she meets these minimum financial suitability standards and maximum investment limits. See “Financial Suitability Requirements” for more information.

|

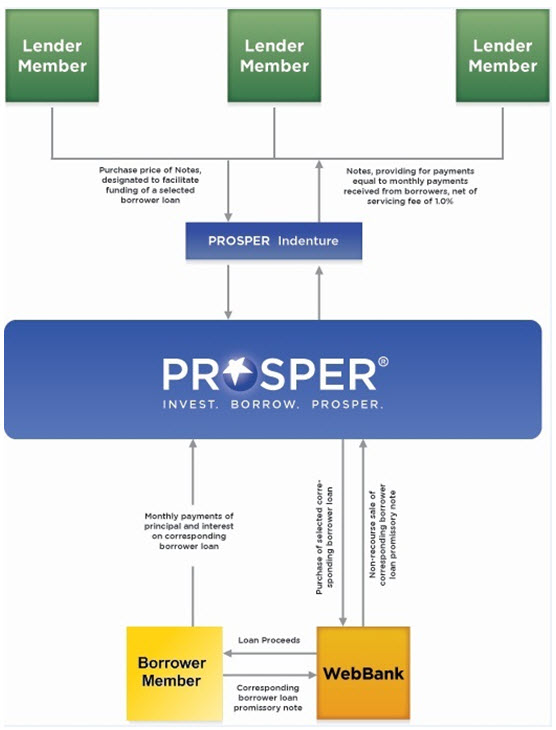

The following diagram illustrates the basic structure of our platform for a single series of Notes. This graphic does not demonstrate many details of our platform, including the effect of prepayments, late payments, late fees or collection fees. See “About Prosper” for more information.

QUESTIONS AND ANSWERS

|

Q:

|

Who is Prosper?

|

|

A:

|

Prosper provides a peer-to-peer online credit platform that enables its borrower members to borrow money and its lender members to purchase Notes issued by Prosper, the proceeds of which facilitate the funding of specific loans made to borrower members.

|

|

Q:

|

What is our platform?

|

|

A:

|

Our platform is an online marketplace that permits our lender members to bid on listings and purchase Notes from Prosper that are dependent for payment on payments we receive on the corresponding borrower loans described in the listings. All listings on our platform are posted by individual consumer members of Prosper requesting individual consumer loans, which we refer to as “borrower listings” or “listings” and “borrower loans,” respectively. Each listing sets forth the desired loan amount, borrower interest rate, lender yield percentage, and other information.

|

|

Q:

|

Who is WebBank?

|

|

A:

|

WebBank is an FDIC-insured, Utah-chartered industrial bank that is authorized or permitted to make loans in the states where borrower members reside, and makes all borrower loans originated through our platform.

|

|

Q:

|

What is a borrower listing?

|

|

A:

|

A borrower listing is a request by a borrower member for a borrower loan in a specified amount. In addition to the borrower’s requested loan amount and interest rate, which is set by Prosper, each listing will show the lender’s yield percentage, which will equal the borrower’s interest rate, net of servicing fees, the minimum amount of total bids required for the loan to fund, and the Prosper Rating and estimated loss rate for the listing. The listing will also show the borrower’s numerical credit score range, debt-to-income ratio, summary information from the borrower’s credit report, and self-reported occupation, employment status and range of income information, and may also include the borrower’s narrative description of why the loan is being requested and the borrower’s financial situation. The specific numerical credit score we receive for a borrower from the credit reporting agency is not displayed or disclosed to anyone (including the borrower). A listing may also contain questions asked by lender members about the listing and the borrower member’s responses to those questions. Borrower members are only identified by a Prosper screen name in their listings, and are not permitted to disclose their identity or contact information. Listings may only be created by individuals registered as borrowers on our platform. Listings are displayed publicly on our platform, although certain information is only viewable by registered members.

|

|

Q:

|

What are borrower loans?

|

|

A:

|

Borrower loans are unsecured obligations of individual borrower members with an interest rate determined by Prosper. Borrower loans currently have a term of one, three or five years, but we may in the future extend available loan terms to between three months to seven years. Each borrower loan is originated through our platform, funded by WebBank and sold and assigned to Prosper after it is made in exchange for the principal amount of the corresponding borrower loan. Borrower members may request loans within specified minimum and maximum principal amounts, currently $2,000 and $25,000, respectively, but in the future Prosper may permit borrowers to request loans in principal amounts between $500 and $35,000. Borrower loans are repayable in monthly installments and are unsecured and unsubordinated. Borrower loans may be repaid at any time by borrower members without prepayment penalty. A borrower loan will be made to a borrower member only if the borrower’s listing has received bids equal to or exceeding the minimum amount required for the loan to fund.

|

|

Q:

|

Do lender members make loans directly to borrower members?

|

|

A:

|

No. Lender members do not make loans directly to borrower members. Instead, lender members purchase Notes issued by Prosper, the proceeds of which are designated by the lender members who purchase the Notes to facilitate the funding of the corresponding borrower loan. We use all proceeds we receive from issuances of the Notes to purchase the borrower loans. Even though lender members do not make loans directly to Prosper borrower members, the lender members will nevertheless be wholly dependent on the borrowers for repayment of the Notes. If a borrower defaults on the payment obligations under a borrower loan, Prosper will not have any obligation to make payments to the holders of Notes dependent for payment on that borrower loan.

|

|

Q:

|

Who are our lender members?

|

|

A:

|

Our lender members are individuals and institutions that have the opportunity to buy our Notes. Lender members must register on our website. Any natural person at least 18 years of age who is a U.S. resident with a bank account and a social security number or any institution with a taxpayer identification number can be a lender member and place bids on our platform. During lender registration, potential lender members must agree to a credit profile authorization statement for identification purposes, a tax withholding statement and the terms and conditions of the Prosper website, and must enter into a lender registration agreement with Prosper, which will govern the terms under which a lender member may purchase Notes from Prosper. In order to bid on a listing, a lender member must have funds on deposit in a Prosper funding account in at least the amount of the lender member’s bid.

|

|

Q:

|

Who are borrower members?

|

Any natural person at least 18 years of age who is a U.S. resident in a state where loans through the platform are available, has a bank account and a social security number, and has registered with Prosper and passed our anti-fraud and identity verification process may be a borrower member. Prosper currently allows borrower members to post listings on our platform regardless of their income. Prosper reserves the right to restrict access to our platform by setting minimum credit or other guidelines for borrowers. Currently, a borrower must have a credit score of at least 640 (before October 16, 2008, the minimum was 520) in order to post a listing on our platform, except that the minimum is 600 for borrower members who (1) had previously obtained a Prosper loan and paid off the loan in full, or (2) are seeking a second loan and are otherwise eligible for a second loan. In the future, Prosper may allow borrowers with a credit score below 640 to post listings as long as bids are made primarily from friends and family.

|

Q:

|

What is a bid?

|

|

A:

|

A bid on a listing is a lender member’s commitment to purchase a Note in the principal amount of the lender member’s bid. Lender members “bid” the amount they are willing to commit to the purchase of a Note that is dependent for payment on payments we receive on the borrower loan described in the listing. A lender who wishes to bid on a listing must have funds in the amount of the bid in the Lender member’s funding account at the time the bid is made. Currently, a bid may be between $25 and the full amount of the requested loan amount described in the listing. Once a bid is placed, it is irrevocable, and the amount of the bid may not be withdrawn from the lender member’s funding account, unless the bidding period expires without the listing having received enough bids to be funded.

|

|

Q:

|

What are our Borrower Payment Dependent Notes?

|

|

A:

|

Our lender members may purchase Borrower Payment Dependent Notes, or “Notes,” from Prosper. We will issue the Notes in a series, with each series dependent for payment on payments we receive on a specific borrower loan. The proceeds of each series of Notes are used to purchase the borrower loan upon which that series of Notes is dependent for payment. Each series of Borrower Notes will have a stated interest rate equal to the final yield percentage, as determined by Prosper. The interest rate on the Note will be lower than the interest rate on the corresponding borrower loan because the yield percentage is net of Prosper’s fee for servicing the corresponding borrower loan. We will pay each Note holder principal and interest on the Note in an amount equal to the pro rata portion of the principal and interest payments, if any, we receive on the corresponding borrower loan, net of our servicing fee currently set at 1%, which Prosper may extend in the future to between 1% and 3%. We will also pay the Note holder any other amounts we receive on the borrower loans, including late fees and prepayments, subject to our servicing fee, if any, except that we will not pay the Note holder any non-sufficient funds fees or collection fees we or a third-party collection agency charge. The Notes are special, limited obligations of Prosper only and not the borrowers. The Notes will be unsecured and do not represent an ownership interest in the corresponding borrower loans.

|

|

Q:

|

How are interest rates and payments calculated on the Notes?

|

|

A:

|

The interest rate on a Note is the yield percentage that corresponds to the interest rate determined by Prosper for the related borrower loan. Prosper sets the interest rates for borrower loans based on Prosper Ratings, as well as additional factors, such as estimated loss rates, loan terms, group affiliations, the general economic environment and competitive conditions. The yield percentage on each series of Notes is equal to the interest rate on the related borrower loan, minus Prosper’s servicing fee, currently set at 1%, which Prosper may extend in the future to between 1% and 3%. Payments are in an amount sufficient to amortize the Note amount over the term of the Note at the interest rate set forth in the Note.

|

|

Q:

|

What is Quick Invest?

|

|

A:

|

Our loan search tool, Quick Invest, allows lenders to identify Notes that meet their investment criteria. A lender using Quick Invest is asked to indicate (i) the Prosper Rating or Ratings she wishes to use as search criteria, (ii) the total amount she wishes to invest and (iii) the amount she wishes to invest per Note. Quick Invest then compiles a basket of Notes for her consideration that meet her search criteria. If the pool of Notes that meet her criteria exceeds the total amount she wishes to invest, Quick Invest selects Notes from the pool based on how far the listings corresponding to the Notes have progressed through our loan verification process, i.e. , Notes from the pool that correspond to listings for which we have completed our loan verification process will be selected first. If the pool of Notes that meet the lender member’s criteria and for which we have completed loan verification still exceeds the amount she wishes to invest, Quick Invest selects Notes from that pool based on the principle of first in, first out, i.e. , the Notes from the pool with the corresponding listings that were posted on our website earliest will be selected first. If the member’s search criteria include multiple Prosper Ratings, Quick Invest divides her basket into equal portions, one portion representing each Prosper Rating selected. To the extent available Notes with these Prosper Ratings are insufficient to fill the lender’s order, the lender is advised of this shortfall and given an opportunity either to reduce the size of her order or to modify her search criteria to make her search more expansive Our Auto Quick Invest feature allows lender members (i) to have Quick Invest searches run on their designated criteria automatically each time new listings are posted on our platform, and (ii) to place bids on any Notes identified by each such search. See “About Prosper.”

|

|

Q:

|

How does the bidding process work for borrower listings?

|

|

A:

|

A bid on a borrower listing is a lender member’s binding commitment to purchase a Note in the principal amount of the lender member’s bid, should the listing receive bids equal to or exceeding the minimum amount required for the loan to fund. Lender members bid the amount they are willing to commit to purchase a Note dependent for payment on payments we receive on the borrower loan described in the listing. After a listing is posted, lender members can place bids on that listing until the listing has received bids totaling the requested loan amount. Once the listing has received bids totaling the requested loan amount, those bids are the “winning bids” and no further bids can be placed. The maximum length of the bidding period is 14 days. If the listing does not receive bids equal to or exceeding the minimum amount by the close of the fourteenth day after the listing is posted, the listing will terminate and will not be funded.

|

|

Q:

|

Is partial funding of loans permitted?

|

|

A:

|

Yes. When a borrower member creates a loan listing, she may opt for partial funding, which means her loan can be funded if it receives bids for 70% or more of the amount requested. Each loan listing will indicate whether the borrower has opted for partial funding as well as the minimum amount of total bids required for the loan to fund. We may change the percentage threshold for partial funding, which is currently set at 70%, from time to time. Any such change will be disclosed on our website and will only affect listings created after we have implemented such change. See “About Prosper” for more information.

|

|

Q:

|

How does Prosper set interest rates for borrower loans?

|

|

A:

|

Prosper has an interest rate committee, consisting of members of our management team, that meets regularly to set the interest rates for borrower loans. The committee sets rates based on Prosper Ratings, as well as additional factors, such as estimated loss rates, loan terms, group affiliations, the general economic environment and competitive conditions. A table listing the current rates set by the committee is posted on our website. The committee meets to review this table on at least a monthly basis, but may meet more frequently as changes in market conditions and the general economic environment dictate. The yield percentage on each series of Notes is equal to the interest rate on the related borrower loan, minus Prosper’s servicing fee, currently set at 1%, which Prosper may extend in the future to between 1% and 3%. The interest rate set by Prosper for each loan listing, as well as the yield percentage for the corresponding Notes, will be set forth on the listing, as posted on our website, and will also be included in the listing report filed by Prosper for that listing. See “About Prosper” for more information.

|

|

Q:

|

How are the Notes being offered?

|

|

A:

|

We are offering the Notes directly to lender members only through our website for a purchase price of 100% of the principal amount of the Notes. We are not using any underwriters, and there will be no underwriting discounts.

|

|

Q:

|

Will I receive a certificate for my Notes?

|

|

A:

|

No. The Notes are issued only in electronic form. This means that each Note will be stored on our website. You can view a record of the Notes you own and the form of your Notes online and print copies for your records by visiting your secure, password-protected webpage in the “My Account” section of our website.

|

|

Q:

|

Will the Notes be listed on an exchange?

|

|

A:

|

No. The notes will not be listed on any securities exchange.

|

|

Q:

|

Will I be able to sell my Notes?

|

|

A:

|

The Notes will not be transferable except through the Note Trader platform operated and maintained by FOLIOfn Investments, Inc., a registered broker-dealer . There can be no assurance that a market for Notes will develop on the Note Trader platform and, therefore, lender members must be prepared to hold their Notes to maturity. See “About Prosper” for more information.

|

|

Q:

|

Does Prosper verify the listing information provided by borrower members?

|

|

A:

|

We verify the identity of every borrower who obtains a loan through our platform using a combination of documentary and non-documentary methods. We ask each borrower to submit a copy of her current driver’s license, passport or other government-issued, photo identification card, which we authenticate using third-party reference materials. In addition, we compare the information contained in the credit report we obtain for the borrower from a consumer reporting agency with the information contained in the borrower’s application. We also run the borrower’s application information through a fraud database. Finally, we require the borrower to submit bank statements, cancelled checks or other documentary evidence to verify the accuracy of her bank account information. For the small number of borrowers who do not have a current, government-issued photo identification card, we may rely on the other screening processes described above to verify their identity. But we obtain and authenticate photo identification from the great majority of our borrowers, and perform the other processes described above for all borrowers who obtain a loan. If we are unable to verify the identity of a borrower in the manner described above, we will cancel the borrower’s loan listing or pending loan.

|

In addition to identity verification, we verify income and employment information for a subset of our borrowers based on a proprietary algorithm. The intention of this algorithm is to identify instances where the borrower’s self-reported income is highly determinative of the borrower’s Prosper Rating. The algorithm gives greatest weight to Prosper Rating, loan amount, stated income, and debt-to-income ratio. For the period from July 14, 2009 through December 31, 2011, we verified employment and/or income on approximately 47% of the loans we originated on a unit basis (8,904 out of 19,059) and approximately 67% of our originations on a dollar basis ($75,308,364 out of $113,074,405). If a borrower fails to provide satisfactory information in response to an income or employment verification inquiry, we (a) request additional information from the borrower, (b) cancel the borrower’s listing or (c) refuse to proceed with the funding of the borrower loan.

Where we choose to verify a borrower’s income or employment information, the verification is normally done after the borrower’s listing has already been posted. This allows Prosper to focus its verification efforts on the listings most likely to fund, and increases the percentage of funded loans that are subject to verification. When we identify inaccurate employment or income information in a borrower’s application or listing that has resulted in the borrower obtaining a different Prosper Rating or interest rate for her loan than she would have obtained if she had provided the correct information, we cancel the listing. If we identify inaccurate information in the borrower’s listing that does not trigger cancellation of the listing, we do not update the listing to include the corrected information. Our participation in funding loans on the platform from time to time has had, and will continue to have, no effect on our income and employment verification process, the selection of loan requests verified or the frequency of income and employment verification. Please see “About Prosper” for further information.

|

Q:

|

Will lender members have access to financial statements, financial histories or any other financial information of the borrower members?

|

|

A:

|

No. Lender members do not have access to financial statements, financial histories or any other financial information of the borrower members. Borrower members may elect to provide financial information in their listing description, or in response to lender members’ questions, but such information is not verified.

|

|

Q:

|

Are the Notes secured by any collateral?

|

|

A:

|

No. All Notes will be unsecured special, limited obligations of Prosper. The Notes do not restrict Prosper’s incurrence of other indebtedness or the grant or imposition of liens or security interests on the assets of Prosper, and holders of the Notes do not have a security interest in the corresponding borrower loan or the proceeds of that loan. To limit the risk of Prosper’s insolvency, Prosper has granted the indenture trustee a security interest in Prosper’s right to payment under, and all proceeds received by Prosper on, the corresponding borrower loans and in the bank account in which the borrower loan payments are deposited. The indenture trustee may exercise its legal rights to the collateral only if an event of default has occurred under the indenture, which would include Prosper becoming subject to a bankruptcy or similar proceeding. Only the indenture trustee, not the holders of the Notes, has a secured claim to the above collateral.

|

|

Q:

|

Does Prosper or WebBank participate in the platform as a lender member?

|

|

A:

|

From time to time, Prosper may fund portions of loan requests on its platform and hold any related Notes it purchases for its own account. Any Prosper bid on a loan will be made public in the same manner in which bids by other bidders are made public. In addition, loans upon which Prosper bids will be identified to other bidders in a manner that is intended to make Prosper’s direct participation in the bidding clear. Prosper will participate in loans on its platform on the same terms and conditions as other potential lenders on the platform. In some cases, Prosper’s participation in a loan may cause the loan to fund, and in some cases, fund faster, than it would fund in the absence of Prosper’s participation. The amount that Prosper may choose to fund of any particular loan may vary significantly and Prosper reserves the right to fund up to the entire amount of a given loan request. WebBank does not participate in our platform as a lender member. The directors or executive officers of Prosper have in the past and may in the future participate in their individual capacities as lender members on our platform. WebBank is the originating lender on all borrower loans made through our platform, and then sells and assigns the borrower loans to Prosper.

|

|

Q:

|

Do lender members need to be licensed as a consumer lender or finance company?

|

|

A:

|

Our platform is designed and structured in a manner such that the activities performed by lender members on our platform do not trigger state lending or finance company licensing requirements. States that have lending or finance company licensing laws normally require a lending license for persons who engage in the business of making loans. All borrower loans originated on our platform are made by WebBank, and WebBank is the named lender on all promissory notes representing borrower loans. Prosper performs its identity and anti-fraud verification process on all borrower loans and services the borrower loans. WebBank is the originating lender and has authority to make borrower loans in all states where loans through the platform are available. Persons who register as lender members do not lend money, but rather purchase Notes issued by Prosper. The proceeds of the sale of Notes are not disbursed to borrowers. See “Government Regulation—Regulation and Consumer Protection Laws” for more information and “Risk Factors—Risks Inherent in Investing in the Notes” for more information.

|

|

Q:

|

Can borrower members have more than one loan outstanding at any one time?

|

|

A:

|

Yes. Borrower members may have up to two borrower loans originated through the platform outstanding at any one time, provided that the aggregate outstanding principal balance of both borrower loans does not exceed the then-current maximum allowable loan amount for borrower loans (currently $25,000, but which may increase to $35,000 in the future). If a borrower member with a loan originated through the platform outstanding posts a listing for a second loan through the platform, the listing will disclose that the borrower member has a loan originated through the platform outstanding. Currently, to be eligible to obtain a second borrower loan while an existing loan is outstanding, the borrower member must satisfy additional criteria. See “About Prosper” for more information.

|

|

Q:

|

How much money can lender members bid on our platform?

|

|

A:

|

Our platform currently allows lender members to bid as little as $25 and as much as the full amount of any particular listing, up to an aggregate amount of $5,000,000 for individuals and $50,000,000 for institutions.

|

|

Q:

|

What is a Prosper Rating?

|

|

A:

|

Each listing will be assigned a proprietary credit rating by Prosper, referred to as the Prosper Rating. The Prosper Rating is a letter that indicates the level of risk associated with a listing and corresponds to an estimated average annualized loss rate range. There are currently seven Prosper Ratings, represented by seven letter scores, but this, as well as the loss ranges associated with each, may change over time as the marketplace dictates. The Prosper Rating will be derived from two scores: a consumer reporting agency score and an in-house custom score calculated using the historical performance of previous borrower loans with similar characteristics. The use of these two scores will determine an estimated loss rate for each listing, which correlates to a Prosper Rating. This rating system allows Prosper to maintain consistency when assigning a rating to each listing. See “About Prosper” for more information.

|

|

Q:

|

Under what circumstances is Prosper required to offer to repurchase the Notes or indemnify lender members?

|

|

A.

|

Under the lender registration agreement, in the event of a material default under a series of Notes due to verifiable identity theft of the named borrower’s identity, Prosper will repurchase the Notes and credit the lender members’ accounts with the remaining unpaid principal balance of the Notes. The determination of whether verifiable identity theft has occurred is in our sole discretion. In the event we breach any of our other representations and warranties in the lender registration agreement pertaining to the Notes, and such breach materially and adversely affects a series of Notes, we will either indemnify the lender members, repurchase the series of Notes or cure the breach. The limited circumstances where this may occur include (1) the failure of the corresponding borrower loan to materially comply at origination with applicable federal and state law, (2) the listing corresponding to the Note contains a Prosper score different from the score calculated by Prosper for that listing, or (3) Prosper incorrectly applying its formula to determine the Prosper score, resulting in a Prosper Rating different from the Prosper Rating that should have appeared in the listing. Prosper is not, however, under any obligation to cure, indemnify or repurchase a series of Notes because of the Prosper score or Prosper Rating for any other reason. See “About Prosper.”

|

|

Q:

|

Why did Prosper revise its credit grading system?

|

|

A:

|

We revised our credit grading system prior to the relaunch of our platform in July 2009. The goal of the Prosper Rating system is to have our ratings align with loss rate tiers, rather than simply with credit score tiers, to facilitate understanding among lender members and to maintain consistency across listings.

|

|

Q:

|

What is a debt-to-income ratio?

|

|

A:

|

Part of a borrower’s credit profile displayed in listings is a debt-to-income ratio (or DTI). DTI is a measurement of the borrower’s ability to take on additional debt. This number takes into consideration how much debt the borrower has or will have, including the borrower loan. The DTI is expressed as a percentage and is calculated by dividing the borrower’s monthly income into his or her monthly debt payments, including the debt resulting from the borrower loan being requested. Debt amounts are taken from the borrower’s credit report without verification and exclude monthly housing payments. The borrower’s income is self-reported and not verified by Prosper.

|

|

Q:

|

How do lender members receive payments on the Notes?

|

|

A:

|

All payments on the Notes are processed through our platform. If and when we make a payment on a Note, the payment will be deposited in the lender member’s Prosper account. Lender members may elect to have available balances in their Prosper account transferred to their bank account at any time, subject to normal execution times for such transfers (generally 2-3 days).

|

|

Q:

|

What are the fees and charges withheld from borrower loan payments and retained by Prosper?

|

|

A:

|

Servicing fees charged by Prosper are deducted from loan payments received on borrower loans, and reduce the lenders’ effective yield. This reduction will be automatically taken into account by our platform in calculating the yield percentage displayed in listings. See “About the Loan Platform—Loan Servicing and Collection” for more information.

|

Any non-sufficient funds fees charged to a borrower’s account will be retained by Prosper and will not be remitted to you. If collection action is taken in respect of a borrower loan, Prosper or the collection agency will charge a collection fee of between 17% and 40% of any amounts that are obtained, in addition to any legal fees incurred in the collection effort. The collection fee will vary dependent upon the collection agency used. In addition, any legal fees incurred in connection with collection efforts will be deducted from any borrower loan payments Prosper receives. These fees will correspondingly reduce the amounts of any payments lender members receive on the Notes. You will receive all other amounts Prosper receives on borrower loans, including late fees and prepayments, subject to our servicing fees.

|

Q:

|

What happens if a borrower misses a payment or does not repay the borrower loan?

|

|

A:

|

Borrowers who miss payments face the same consequences as they would if they missed payments on any similar form of bank or other commercial credit obligation, including in most cases the reporting of late payments to consumer reporting agencies. Borrowers may also incur late fees for missed or delinquent payments, to the extent allowed by applicable law. Late fees collected by Prosper on borrower loans are passed on to the lender members who own the Notes dependent for payment on that borrower loan.

|

|

Q:

|

What guarantees do lender members have that a Note will be paid?

|

|

A:

|

There are no guarantees that a Note will be paid. See “Risk Factors—Risks Related to Borrower Default” for more information.

|

|

Q:

|

Can lender members collect on late payments themselves?

|

|

A:

|

No. Under the lender registration agreement, each lender member agrees that under no circumstances may a lender member attempt collection of a late payment, or any amounts owing on a borrower loan corresponding to their Note, themselves. Lender members must depend on Prosper or third-party collection agents to pursue collection on delinquent borrower loans. If collection action must be taken in respect of a borrower loan, Prosper or the collection agency will charge a collection fee of between 17% and 40% of any amounts that are obtained, in addition to any legal fees incurred in the collection effort. These fees will correspondingly reduce the amounts of any payments lender members receive on the Notes.

|

We are obligated to use commercially reasonable efforts to service and collect borrower loans, in good faith, accurately and in accordance with industry standards customary for servicing loans such as the borrower loans. When a borrower’s payment is late on a borrower loan, we communicate directly with the borrower to encourage repayment. We normally refer borrower loans that become more than 30 days past-due to a nationally-licensed collection agency, which makes further attempts to collect delinquent amounts and have the borrowers bring the account current. We may, in our sole discretion and subject to our servicing standard, refer a borrower loan to a collection agency, elect to initiate legal action to collect a borrower loan or sell a borrower loan to a third party debt buyer at any time. We may also work with the borrower member to structure a new payment plan for the borrower loan without the consent of any holder of the Notes corresponding to the borrower loan. Borrower loans that become more than 120 days past due are charged off. Depending on market conditions, we either sell charged off loans to an unaffiliated third party debt purchaser or continue to collect on those accounts, and we may in our discretion institute legal proceedings to collect the debt. In servicing borrower loans we may, in our discretion, utilize affiliated or unaffiliated third party loan servicers, collection agencies or other agents or contractors. We report loan delinquencies and charge-offs to consumer reporting agencies, which negatively impacts the borrower’s credit file. Borrowers whose loans are charged off are not permitted to post any further listings on our platform. See “About Prosper” for more information.

|

Q:

|

What happens if a borrower repays early?

|

|

A:

|