As filed with the Securities and Exchange Commission on February 11, 2022

Registration Statement No. __________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter) |

| 6199 | ||||

(State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

1 Lincoln Street

Boston, MA 02111

Phone: (781) 925-1700

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Coreen Kraysler

Chief Financial Officer

1 Lincoln Street

Boston, MA 02111

Phone: (781) 925-1700

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

Copies to:

Richard A. Friedman, Esq. Greg Carney, Esq. |

Oded Har-Even,

Esq. Angela Gomes, Esq. |

| Sheppard Mullin Richter & Hampton, LLP | Sullivan & Worcester LLP |

| 30 Rockefeller Plaza | 1633 Broadway |

| New York, NY 10112 | New York, NY 10019 |

| Phone: (212) 653-8700 | Phone: (212) 660-5002 |

Approximate date of proposed sale to public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on the Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier registration statement for the same offering: ☐

Indicate by check mark whether registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act of 1934, as amended.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to Section 8(a) may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION | DATED FEBRUARY 11, 2022 |

Shares

Common Stock

Netcapital Inc.

This is a firm commitment public offering of shares of common stock, par value $0.001 per share, or common stock, of Netcapital Inc. We are offering an aggregate of shares of our common stock, $0.001 par value per share, based on an assumed public offering price of $ per share (which is based on the last reported sales price of our common stock on , 2022).

Our common stock is presently quoted on the OTCQX under the symbol “NCPL”. We have applied to have our common stock listed on The Nasdaq Capital Market under the symbol “NCPL”. No assurance can be given that our application will be approved. If our application is not approved, we will not consummate this offering. On February 9, 2021, the last reported sale price for our common stock on the OTCQX was $11.65 per share.

Investing in our securities involves a high degree of risk. See “Risk Factors” beginning on page 9 of this prospectus for a discussion of information that should be considered in connection with an investment in our securities. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||||||

| Public offering price | $ | $ | ||||||||||

| Underwriting discounts and commissions(1) | $ | $ | ||||||||||

| Proceeds to us, before expenses(2) | $ | $ | ||||||||||

| (1) | Underwriting discounts and commissions do not include a non-accountable expense allowance equal to 1.0% of the gross proceeds initial public offering price payable to the underwriters. We refer you to “Underwriting” beginning on page 54 for additional information regarding underwriters’ compensation. |

| (2) | The amount of offering proceeds to us presented in this table does not give effect to any exercise of the: (i) over-allotment option (if any) we have granted to the Representative as described below or (ii) warrants to purchase shares of our common stock, or the Representative’s Warrants, to be issued to ThinkEquity LLC, or ThinkEquity or the Representative. |

We have granted a 45-day option to the Representative to purchase up to additional shares of our common stock, solely to cover over-allotments, if any.

The underwriters expect to deliver our shares to purchasers in the offering on or about , 2022.

ThinkEquity

The date of this prospectus is , 2022

TABLE OF CONTENTS

| SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS | v | ||

| BASIS OF PRESENTATION | v | ||

| PROSPECTUS SUMMARY | 1 | ||

| THE OFFERING | 6 | ||

| RISK FACTORS | 9 | ||

| USE OF PROCEEDS | 20 | ||

| MARKET FOR OUR COMMON STOCK | 20 | ||

| DIVIDEND POLICY | 21 | ||

| CAPITALIZATION | 21 | ||

| DILUTION | 22 | ||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 23 | ||

| OUR BUSINESS | 28 | ||

| LEGAL PROCEEDINGS | 37 | ||

| MANAGEMENT | 37 | ||

| EXECUTIVE COMPENSATION | 42 | ||

| CERTAIN RELATIONSHIPS AND RELATED PARTY TRANSACTIONS | 44 | ||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 46 | ||

| SHARES ELIGIBLE FOR FUTURE SALE | 48 | ||

| DESCRIPTION OF SECURITIES | 50 | ||

| UNDERWRITING | 54 | ||

| LEGAL MATTERS | 61 | ||

| EXPERTS | 61 | ||

| WHERE YOU CAN FIND MORE INFORMATION | 61 | ||

| INDEX TO FINANCIAL STATEMENTS | F-1 |

You should rely only on information contained in this prospectus. We have not, and the underwriters have not, authorized anyone to provide you with additional information or information different from that contained in this prospectus. We are not making an offer of these securities in any state or other jurisdiction where the offer is not permitted. The information in this prospectus may only be accurate as of the date on the front of this prospectus regardless of time of delivery of this prospectus or any sale of our securities.

No person is authorized in connection with this prospectus to give any information or to make any representations about us, the common stock hereby or any matter discussed in this prospectus, other than the information and representations contained in this prospectus. If any other information or representation is given or made, such information or representation may not be relied upon as having been authorized by us. This prospectus does not constitute an offer to sell, or a solicitation of an offer to buy our common stock in any circumstance under which the offer or solicitation is unlawful. Neither the delivery of this prospectus nor any distribution of our common stock in accordance with this prospectus shall, under any circumstances, imply that there has been no change in our affairs since the date of this prospectus.

Neither we nor the Underwriter have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. You are required to inform yourself about, and to observe any restrictions relating to, this offering and the distribution of this prospectus. |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains express or implied forward-looking statements that are based on our management’s beliefs and assumptions and on information currently available to our management. Statements regarding our future results of operations and financial position, business strategy and plans and objectives of management for future operations. All statements, other than statements of historical fact, contained in this prospectus and in any related prospectus supplement are forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as “may,” “could,” “will,” “would,” “should,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “intend,” “predict,” “seek,” “contemplate,” “project,” “continue,” “potential,” “ongoing” or the negative of these terms or other comparable terminology.

Forward-looking statements are subject to significant business, economic and competitive risks, uncertainties and contingencies, many of which are difficult to predict and beyond our control, which could cause our actual results to differ materially from the results expressed or implied in such forward-looking statements. These and other risks, uncertainties and contingencies are described elsewhere in this prospectus, including under “Risk Factors,” and in the documents incorporated by reference herein, and include the following factors:

| · | capital requirements and the availability of capital to fund our growth and to service our existing debt; | |

| · | difficulties executing our growth strategy, including attracting new issuers and investors; | |

| · | our anticipated use of the net proceeds from this offering; | |

| · | economic uncertainties and business interruptions resulting from the coronavirus COVID-19 global pandemic and its aftermath; | |

| · | as restrictions related to the coronavirus COVID-19 global pandemic are removed and face-to-face economic activities normalize, it may be difficult for us to maintain the recent sales gains that we have experienced; | |

·

|

all the risks of acquiring one or more complementary businesses, including identifying a suitable target, completing comprehensive due diligence uncovering all information relating to the target, the financial stability of the target, the impact on our financial condition of the debt we may incur in acquiring the target, the ability to integrate the target’s operations with our existing operations, our ability to retain management and key employees of the target, among other factors attendant to acquisitions of small, non-public operating companies; | |

| · | difficulties in increasing revenue per issuer; | |

| · | challenges related to hiring and training fintech employees at competitive wage rates; | |

| · | difficulties in increasing the average number of investments made per investor; | |

| · | shortages or interruptions in the supply of quality issuers; | |

| · | our dependence on a small number of large issuers to generate revenue; | |

| · | negative publicity relating to any one of our issuers; | |

| · | competition from other online capital portals with significantly greater resources than we have; | |

| · | changes in investor tastes and purchasing trends; | |

| · | our inability to manage our growth; | |

| · | our inability to maintain an adequate level of cash flow, or access to capital, to meet growth expectations; | |

| · | changes in senior management, loss of one or more key personnel or an inability to attract, hire, integrate and retain skilled personnel; | |

| · | labor shortages, unionization activities, labor disputes or increased labor costs, including increased labor costs resulting from the demand for qualified employees; | |

| · | our vulnerability to increased costs of running an online portal on Amazon Web Services; | |

| · | our vulnerability to increasing labor costs; | |

| · | the impact of governmental laws and regulation; | |

| · | failure to obtain or maintain required licenses; | |

| · | changes in economic or regulatory conditions and other unforeseen conditions that prevent or delay the development of a secondary trading market for shares of equity that are sold on our online portal; | |

| · | inadequately protecting our intellectual property or breaches of security of confidential user information; and | |

| · | our expectations regarding having our securities listed on The Nasdaq Capital Market. |

These forward-looking statements speak only as of the date of this prospectus. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained in this prospectus after we distribute this prospectus, whether as a result of any new information, future events or otherwise.

TRADEMARKS AND TRADE NAMES

This prospectus includes trademarks that are protected under applicable intellectual property laws and are the Company’s property [or the property of one of the Company’s subsidiaries. This prospectus also contains trademarks, service marks, trade names and/or copyrights of other companies, which are the property of their respective owners. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that the owner will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names.

INDUSTRY AND MARKET DATA

Unless otherwise indicated, information contained in this prospectus concerning the Company’s industry and the markets in which it operates, including market position and market opportunity, is based on information from management’s estimates, as well as from industry publications and research, surveys and studies conducted by third parties. The third-party sources from which the Company has obtained information generally state that the information contained therein has been obtained from sources believed to be reliable, but the Company cannot assure you that this information is accurate or complete. The Company has not independently verified any of the data from third-party sources nor has it verified the underlying economic assumptions relied upon by those third parties. Similarly, internal company surveys, industry forecasts and market research, which the Company believes to be reliable, based upon management’s knowledge of the industry, have not been verified by any independent sources. The Company’s internal surveys are based on data it has collected over the past several years, which it believes to be reliable. Management estimates are derived from publicly available information, its knowledge of the industry, and assumptions based on such information and knowledge, which management believes to be reasonable and appropriate. However, assumptions and estimates of the Company’s future performance, and the future performance of its industry, are subject to numerous known and unknown risks and uncertainties, including those described under the heading “Risk Factors” in this prospectus and those described elsewhere in this prospectus, and the other documents the Company files with the U.S. Securities and Exchange Commission, or SEC, from time to time. These and other important factors could result in its estimates and assumptions being materially different from future results. You should read the information contained in this prospectus completely and with the understanding that future results may be materially different and worse from what the Company expects. See the information included under the heading “Special Note Regarding Forward-Looking Statements.”

v

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus and does not contain all the information that you should consider in making your investment decision. Before deciding to invest in our securities, you should read this entire prospectus carefully, including the sections of this prospectus entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and related notes contained elsewhere in this prospectus. Unless the context otherwise requires, references in this prospectus to the “Company,” “we,” “us,” and “our” refer to Netcapital, Inc. and its subsidiaries.

Company Overview

Netcapital Inc. is a fintech company with a scalable technology platform that allows private companies to raise capital online from accredited and non-accredited investors. We give all investors the opportunity to access investments in private companies. Our model is disruptive to traditional private equity investing and is based on Title III, Reg CF of the JOBS Act. We generate fees from listing private companies on our portals. Our consulting group, Netcapital Advisors, provides marketing and strategic advice in exchange for equity positions. The Netcapital funding portal is registered with the SEC, is a member of the Financial Industry Regulatory Authority, or FINRA, a registered national securities association, and provides investors with opportunities to invest in private companies.

Our Business

We provide private company investment access to accredited retail and non-accredited retail investors through our online portal (www.netcapital.com). The Netcapital funding portal charges a $5,000 engagement fee and a 4.9% success fee for capital raised at closing. In addition, the portal generates fees for other ancillary services, such as rolling closes. Netcapital Advisors generates fees and equity stakes from consulting in select portfolio and non-portfolio clients. We generated revenues of $1,825,009 with costs of service of $46,080 in the six months ended October 31, 2021 for a gross profit of $1,778,929 in the six months ended October 31, 2021 as compared to revenues of $2,943,486 with costs of service of $714,224 in the six-months ended October 31, 2020 for a gross profit of $1,779,762 in the six months ended October 31, 2020. We generated revenues of $4,723,001 with costs of service of $759,158 in the year ended April 30, 2021 for a gross profit of $3,961,841 in the year ended April 30, 2021 as compared to revenues of 1,753,558 with costs of service of $11,105 in the year ended April 30, 2020 for a gross profit of $1,742,453 in the year ended April 30, 2020.

Funding Portal

Netcapital.com is an SEC-registered funding portal that enables private companies to raise capital online, while investors are able to invest from anywhere in the world, at any time, with just a few clicks. Securities offerings on the portal are accessible through individual offering pages, where companies include product or service details, market size, competitive advantages, and financial documents. Companies can accept investment from anyone, including friends, family, customers, employees, etc.

In addition to access to the funding portal, Netcapital provides the following services:

● a fully automated onboarding process;

● automated filing of required regulatory documents;

● compliance review;

● custom-built offering page on our portal website;

● third party transfer agent and custodial services;

● email marketing to our proprietary list of investors;

● rolling closes, which provide potential access to liquidity before final close date of offering; and

● assistance with annual filings.

● direct access to our team for ongoing support.

1

Consulting Business

The company's consulting group, Netcapital Advisors helps companies at all stages to raise capital. Netcapital Advisors provides strategic advice, technology consulting and digital marketing services to assist with fundraising campaigns on the Netcapital platform. The company also acts as an incubator and accelerator, taking equity stakes in select disruptive start-ups.

Netcapital Advisors’ services include:

● incubation of technology start-ups;

● investor introductions;

● digital marketing;

● website design, software and software development;

● message crafting, including pitch decks, offering pages, and ad creation;

● strategic advice; and

● technology consulting.

Regulatory Overview

In an effort to enhance economic growth and to democratize access to private investment opportunities, Congress finalized the Jumpstart Our Business Startups Act, or JOBS Act, in 2016. Title III of the JOBS Act enabled early-stage companies to offer and sell securities to the general public for the first time. The SEC then adopted Regulation Crowdfunding, or Reg CF, in order to implement the JOBS Act’s crowdfunding provisions.

Reg CF has several important features that changed the landscape for private capital raising and investment. For the first time, this regulation:

| ● | Allowed the general public to invest in private companies, no longer limiting early-stage investment opportunities to less than 10% of the population; |

| ● | Enabled private companies to advertise their securities offerings to the public (general solicitation); and |

| ● | Conditionally exempted securities sold under Section 4(a)(6) from the registration requirements of the Securities and Exchange Act of 1934, as amended, or the Exchange Act. |

Our Market

Established by the JOBS Act, the funding portal industry remains in its infancy. Title III of the JOBS Act outlines Reg CF, which traditionally allowed private companies to raise up to $1.07 million from all Americans. In March 2021, regulatory enhancements by the SEC went into effect and increased the limit to $5 million. These amendments increased the offering limits for Reg CF, Regulation A and Regulation D, Rule 504 offerings as follows; Reg CF increased to $5 million, Regulation D, Rule 504 moved to $10 million from $5 million; Regulation A Tier 2 rose to $75 million from $50 million.

Reg CF private company investments accounted for approximately $490 million in 2021, according to KingsCrowd, versus $205 million during 2020. We believe a significant opportunity exists to disrupt private capital markets via the Netcapital portal.

Private capital markets reached $7.4 trillion at the end of 2020, per Morgan Stanley, and this number is expected to reach $13 trillion over the next five years. Within this market, private equity represents the largest share, with assets in excess of $3 trillion and a 10-year CAGR of 10%. Since 2000, global private equity, or PE, net asset value has increased almost tenfold, nearly three times faster than the size of the public equity market. Both McKinsey and Boston Consulting Group predict that this strong growth will continue, as investors allocate increasing amounts to private equity, due to historically higher returns and lower volatility than public markets.

2

Our Technology

The Netcapital platform is a scalable, real-time, transaction processing engine that runs without human intervention, 24 hours a day, seven days a week. For companies raising capital, the technology provides fully automated onboarding with integrated regulatory filings. Funds are collected from investors and held in escrow until the offering closes.

For entrepreneurs, the technology facilitates access to capital at low cost. For investors, the platform provides access to investments in private, early-stage companies that were previously unavailable to the general public. Both entrepreneurs and investors can track and view their investments through their dashboard on netcapital.com. The platform currently has almost 100,000 users.

Scalability was demonstrated in November 2021, when the platform processed more than 2,000 investments in less than two hours, totaling more than $2 million.

Our infrastructure is designed in a way that can horizontally scale to meet our capacity needs. Using Ansible playbooks and Amazon AMIs, we are able to automate the creation and launch of our production web and application programming interface, or API, endpoints in order to replicate them as needed behind load balancers (ELBs).

Additionally, all of our public facing endpoints live behind CloudFlare to ensure protection from large scale traffic fluctuations (including DDoS attacks).

Our main database layer is built on Amazon RDS and features a Multi-AZ deployment that can also be easily scaled up or down as needed. General queries are cached in our API layer, and we monitor to optimize very complex database queries that are generated by the API. Additionally, we cache the most complex queries (such as analytics data) in our NoSQL (Mongo) data store for improved performance.

Most of our central processing unit, or CPU, intensive data processing happens asynchronously through a worker/jobs system managed by AWS ElastiCache’s Redis endpoint. This component can be easily fine-tuned for any scale necessary.

We license the technology from our affiliate, Netcapital Systems LLC.

Competitive Advantages

We believe we provide the lowest cost solution for digital capital raising versus our peer group (StartEngine Crowdfunding, Inc., Wefunder Inc. and Republic Core LLC). Our access and onboarding of new clients are superior due to our facilitated technology platforms. Our network is rapidly expanding as a result of our enhanced marketing and broad distribution to reach new investors.

Our competitors include StartEngine Crowdfunding, Inc., Wefunder,Inc. and Republic Core LLC . Given the rapid growth in the industry and its potential to disrupt the multi-billion dollar private capital market, there is sufficient room for multiple players.

Our Strategy

Two major tailwinds are driving accelerated growth in the shift to digital fundraising: the COVID-19 pandemic and the increase in funding limits under Reg CF. The pandemic drove a rapid need to bring as many processes as possible online. With travel restrictions in place and most people in lockdown, entrepreneurs were no longer able to fundraise in person and have increasingly turned to online capital raising through funding portals.

3

There are numerous industry drivers and tailwinds that complement investor demand for access to investments in private companies. To capitalize on these, our strategy is to:

| ● | Generate New Investor Accounts. Growing the number of investor accounts on our platform is a top priority. Investment dollars continue to flow through our platform are the key revenue driver. When issuers advertise their offerings, they are generating new investor accounts for us at no cost to Netcapital. We plan to supplement our issuers' spend on advertising by increasing our digital marketing spend as well, which may include virtual conferences going forward. |

| ● | Hire Additional Business Development Staff. We seek to hire additional business development staff that is technology advanced and financially passionate about capital markets to handle our growing backlog of potential customers. |

| ● | Increase the Number of Companies on Our Platform via Marketing. When a new company lists on our platform, they bring their customers, supporters, and brand ambassadors as new investors to Netcapital. We plan to increase our marketing budget to help grow our portal and advisory clients. |

| ● | Invest in Technology. Technology is critical to everything that we do. We plan to invest in developing innovative technologies that enhance our platform and allow us to pursue additional service offerings. For example, we plan on developing a dedicated mobile app in 2022 to make our platform more accessible. |

| ● | Incubate and accelerate our advisory portfolio clients. The advisory portfolio and our equity interests in select advisory clients represent potential upside for our shareholders. We seek to grow this model of advisory clients. |

| ● | Expand Internationally. We believe there is a significant opportunity to expand into Europe and Asia as an appetite abroad grows for U.S. stocks. |

| ● | Open ATS/Secondary Transfer Feature. Lack of liquidity is a key issue for investors in private companies as private markets lack a liquidity feature in our targeted market. We plan to open a Secondary Transfer Feature to provide potential liquidity to investors who participate in our primary offerings on the Netcapital platform. |

| ● | New Verticals Represent a Compelling Opportunity. We operate in a regulated market supported by the JOBS Act. We may pursue expanding our model to include Regulation A and Regulation D offerings. |

Our Management

Netcapital’s management team is experienced in finance, technology, entrepreneurship, and marketing.

Our Chairman and Chief Executive Officer, or CEO, Dr. Cecilia Lenk, was formerly Vice President of Technology and Digital Design at Decision Resources Inc., a global company serving the biopharmaceutical market, where she oversaw the implementation of new technologies, products, and business processes. Prior to joining Decision Resources, she founded a technology firm that built a patented platform for online research. She has a Ph.D. in Biology from Harvard University and a B.A. (with honors) in Environmental Engineering from Johns Hopkins University.

Coreen Kraysler, CFA, is our Chief Financial Officer, or CFO. With over 30 years of investment experience, she was formerly a Senior Vice President and Principal at Independence Investments, where she managed several 5-star rated mutual funds and served on the Investment Committee. She also worked at Eaton Vance as a Vice President, Equity Analyst on the Large and Midcap Value teams. She received a B.A. in Economics and French, cum laude from Wellesley College and a Master of Science in Management from MIT Sloan.

Jason Frishman is the founder and Chief Executive Officer of our funding portal subsidiary, Netcapital Funding Portal Inc. Mr. Frishman founded netcapital.com to help reduce the systemic inefficiencies early-stage companies face in securing capital. He currently holds advisory positions at leading organizations in the financial technology ecosystem and has spoken as an external expert at Morgan Stanley, University of Michigan, YPO, and others. Mr. Frishman has a background in the life sciences and previously conducted research in medical oncology at the Dana Farber Cancer Institute and cognitive neuroscience at the University of Miami, where he graduated summa cum laude with a B.S. in Neuroscience.

4

Corporate Information

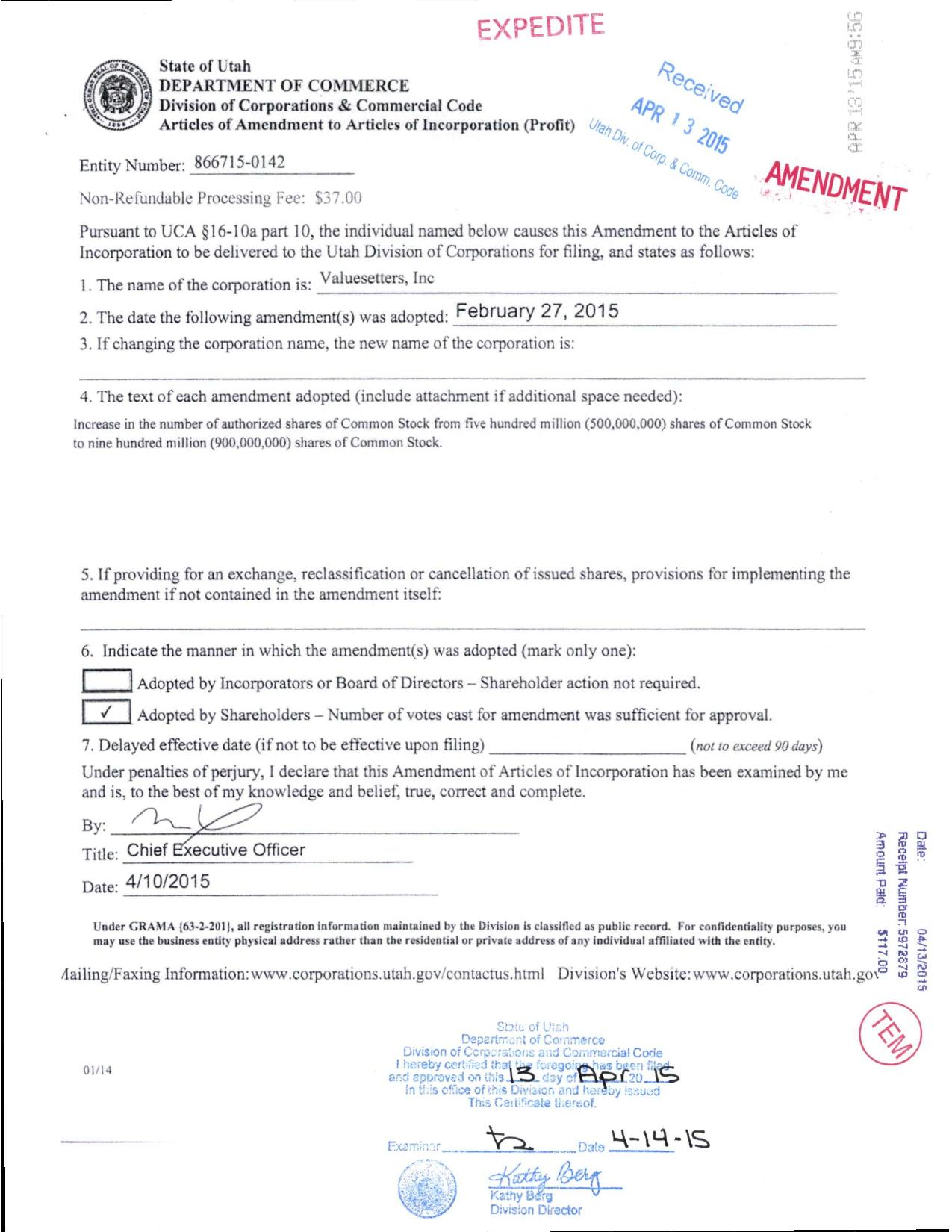

The Company was incorporated in Utah in 1984 as DBS Investments, Inc., or DBS. DBS merged with Valuesetters L.L.C. in December 2003 and changed its name to Valuesetters, Inc. In November 2020, the Company purchased Netcapital Funding Portal Inc. from Netcapital Systems, LLC and changed the name of the Company from Valuesetters, Inc. to Netcapital Inc.

Our principal executive offices are located at State Street Financial Center, One Lincoln Street, Boston, Massachusetts and our telephone number is 781-925-1700. We maintain a website at www.netcapitalinc.com. Information contained on or accessible through our website is not, and should not be considered, part of, or incorporated by reference into, this prospectus and you should not consider any information contained on, or that can be accessed through, our website as part of this prospectus in deciding whether to purchase our securities.

Implications of Being a Smaller Reporting Company

We have elected to take advantage of certain of the reduced disclosure obligations in this prospectus and may elect to take advantage of other reduced reporting requirements in future filings. As a result, the information that we provide to our stockholders may be different than you might receive from other public reporting companies in which you hold equity interests.

We are a “smaller reporting company,” meaning that the market value of our stock held by non-affiliates plus the proposed aggregate amount of gross proceeds to us as a result of this offering is less than $700 million and our annual revenue was less than $100 million during the most recently completed fiscal year. We may continue to be a smaller reporting company after this offering if either (i) the market value of our common stock held by non-affiliates is less than $250 million or (ii) our annual revenue was less than $100 million during the most recently completed fiscal year and the market value of our stock held by non-affiliates is less than $700 million. As a smaller reporting company, we may continue to rely on exemptions from certain disclosure requirements that are available to smaller reporting companies. Specifically, as a smaller reporting company we may choose to present only the two most recent fiscal years of audited financial statements in our Annual Report on Form 10-K and, similar to emerging growth companies, smaller reporting companies have reduced disclosure obligations regarding executive compensation.

Recent Developments

February 2022 Private Placement of Convertible Notes

On February 9, 2022, we issued and sold in a private placement $300,000 of unsecured convertible promissory notes, or the February 2022 Notes. These notes bear interest at a rate of 8% per annum and have a maturity date of February 9, 2023. In addition, these February 2022 Notes shall automatically convert simultaneously with the closing of a Qualified Equity Financing (as defined below) into a number of securities sold in the Qualified Equity Financing equal to the quotient obtained by dividing (a) an amount equal to the amount of the February 2022 Notes outstanding on the closing date of such Qualified Equity Financing by (b) a conversion price equal to the lesser of (1) $10.00 and (2) 80% of the price per shares paid for securities sold in such Qualified Equity Financing upon the closing of such Qualified Equity Financing . A “Qualified Equity Financing” means the offer and sale for cash by us of any of our equity securities with the principal purpose of raising capital and that results in aggregate gross proceeds to us of at least $5,000,000 and “Subsequent Round Securities” means the equity securities sold in the Qualified Equity Financing. We intend to use the net proceeds for working capital and general corporate purposes. The February 2022 Notes were issued under the exemption from registration provided by Section 4(a)(2) and/or Rule 506 of the Securities Act of 1933, as amended. Upon the closing of this offering the February 2022 Notes will convert into shares of our Common Stock.

July 2021 Private Placement

In July 2021, the Company completed an offering for gross proceeds of $1,592,400 in conjunction with the sale of restricted shares of common stock at a price of $9.00 per share. A total of 176,934 shares of common stock were issued.

5

THE OFFERING

| Securities offered by us: | An aggregate of shares of our common stock at a price of $ per share. |

| Common stock outstanding before the offering | 2,865,610 shares of common stock. |

| Common stock to be outstanding after the offering(1) | shares of common stock. If the Representative’s over-allotment option is exercised in full, the total number of shares of common stock outstanding immediately after this offering would be . |

| Option to purchase additional shares | We have granted the Representative a 45-day option to purchase up to additional shares of our common stock to cover allotments, if any. |

| Use of proceeds | We intend to use the net proceeds of this offering for research and development activities, sales and marketing, and for general working capital purposes and potential acquisitions of other companies, products or technologies, though no such acquisitions are currently contemplated. In addition, we may use up to $1,500,000 for the retirement of indebtedness, of which (i) $1,000,000 constitutes indebtedness having an 8% interest rate and a maturity date of April 30, 2023 and (ii) $500,000 constitutes indebtedness having a 3.75% interest rate and a maturity date of June 2050. See “Use of Proceeds” on page 20. |

| Risk factors | Investing in our securities is highly speculative and involves a high degree of risk. You should carefully consider the information set forth in the “Risk Factors” section beginning on page 9 before deciding to invest in our securities. |

| Trading symbol | Our common stock is currently quoted on the OTCQX under the trading symbol “NCPL”. We have applied to list our common stock on Nasdaq under the same symbol upon our satisfaction of the exchange’s initial listing criteria. No assurance can be given that our listing application will be approved. If our listing application is not approved by Nasdaq, we will not consummate this offering. |

| Lock-up Agreements | We and our directors, officers and holders of 5% or more of our outstanding shares as of the date of this prospectus have agreed with the underwriters not to offer for sale, issue, sell, contract to sell, pledge or otherwise dispose of any of our common stock or securities convertible into common stock for a period of six (6) months from the date of the closing date of this offering in the case of the Company’s directors and officers and three (3) months from the date of this offering in the case of the company and 5% or greater holders. See “Underwriting” section on page 54. |

6

| (1) | The number of shares of our common stock to be outstanding after this offering is based on 2,896,844 shares of our common stock outstanding as of February 10, 2022 and excludes the following : |

| · | 28,000 shares of common stock reserved for future issuance under our 2021 Equity Incentive Plan. | |

| · | [ ] shares of common stock issuable upon exercise of warrants with a weighted average exercise price of $[ ] per share; | |

| · | 39,901 shares of common stock issuable upon conversion of $388,642 outstanding liabilities due in conjunction with the acquisition of Netcapital Funding Portal Inc.; | |

| 272,000 shares of common stock issuable upon exercise of outstanding options with an exercise price of $10.50 per share; | ||

| [ ] shares of the Company’s common stock underlying unsecured convertible notes; and | ||

| · | [ ] shares of the Company’s common stock underlying the Warrants and Representative’s Warrants. |

Except as otherwise indicated herein, all information in this prospectus reflects or assumes:

| · | no exercise of the outstanding options or warrants described above; and | |

| · | no exercise of the underwriters’ option to purchase up to an additional shares of common stock to cover over-allotments, if any. |

7

SELECTED HISTORICAL CONSOLIDATED FINANCIAL DATA

The following table presents our selected historical consolidated financial data for the periods indicated. The selected historical consolidated financial data for the years ended April 30, 2021 and 2020 are derived from our audited financial statements. The summary historical financial data for the three-month periods ended October 31, 2021 and 2020 are derived from our unaudited financial statements.

Historical results are included for illustrative and informational purposes only and are not necessarily indicative of results we expect in future periods, and results of interim periods are not necessarily indicative of results for the entire year. The data presented below should be read in conjunction with, and are qualified in their entirety by reference to, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the notes thereto included elsewhere in this prospectus.

| Year Ended | Year Ended | 6 Months Ended | ||||||||||||||

| Income Statement Data: |

April 30, 2021 |

April 30, 2020 |

October 31, 2021 |

October 31, 2020 | ||||||||||||

| Sales | $ | 4,721,003 | $ | 1,753,558 | $ | 1,825,009 | $ | 2,493,486 | ||||||||

| Cost of operations | $ | 5,122,504 | $ | 606,336 | $ | 3,226,328 | $ | 2,386,631 | ||||||||

| Income (loss) from operations | $ | (401,501 | ) | $ | 1,147,222 | $ | (1,401,220 | ) | $ | 106,855 | ||||||

| Interest expense | $ | (87,333 | ) | $ | (18,879 | ) | $ | (70,271 | ) | $ | (23,564 | ) | ||||

| Other income (expense)(4) | $ | 2,571,494 | $ | (175,952 | ) | $ | 3,275,745 | $ | — | |||||||

| Income (loss) before income taxes | $ | 2,082,660 | $ | 424,851 | $ | 1,804,254 | $ | 60,893 | ||||||||

| Benefit (provision) for income taxes | $ | (613,000 | ) | $ | (129,000 | ) | $ | (621,000 | ) | $ | 22,398 | |||||

| Net income (loss) | $ | 1,469,660 | $ | 604,851 | $ | 1,183,254 | $ | 60,893 | ||||||||

| Per Share Data: | ||||||||||||||||

| Net income (loss) per share – basic | 1.18 | 1.50 | 0.48 | 0.15 | ||||||||||||

| Net income (loss) per share – diluted | 0.89 | 1.50 | 0.47 | 0.15 | ||||||||||||

| Weighted average shares outstanding - basic | 1,250,002 | 402,284 | 2,462,251 | 415,726 | ||||||||||||

| Weighted average shares outstanding - diluted | 1,647,295 | 402,284 | 2,497,808 | 415,726 | ||||||||||||

|

Consolidated Statement of Cash Flow Data: |

||||||||||||||||

| Cash (used in) operating activities | $ | (3,250,868 | ) | $ | (3,604 | ) | $ | (1,898,126 | ) | $ | (1,941,012 | ) | ||||

| Net cash provided by (used in) investing activities | $ | 242,025 | $ | — | $ | (247,166 | ) | $ | — | |||||||

| Net cash provided by (used in) financing activities | $ | 5,471,596 | $ | (4,300 | ) | $ | 612,299 | $ | 2,385,800 | |||||||

| Balance Sheet Data: | April 30, 2021 | October 31, 2021 (Actual) |

October 31, 2021 (As Adjusted) | |||||||

| Cash | $ | 2,473,959 | $ | 940,966 | ||||||

| Equity securities at fair value(2) | $ | 6,298,008 | $ | 9,623,753 | ||||||

| Total assets | $ | 25,715,928 | $ | 28,284,919 | ||||||

| Total debt(3) | $ | 5,328,784 | $ | 5,328,784 | ||||||

| Total stockholders’ equity | $ | 25,715,928 | $ | 20,501,783 | ||||||

| (1) | We have an April 30 fiscal year end. |

|

(2) |

Investments are monitored for any changes in observable prices from orderly transactions. |

| (3) | Total debt includes three Small Business Administration, or SBA, loans and a secured loan of $1,000,000 covering substantially all of the Company’s assets. |

| (4) | The result of price changes in the fair value of equity securities is the largest component of other income. |

8

RISK FACTORS

Investing in our securities involves a high degree of risk. You should carefully consider the risks described below, together with the other information contained in this prospectus, including our financial statements and the related notes appearing at the end of this prospectus, before making your decision to invest in our securities. We cannot assure you that any of the events discussed in the risk factors below will not occur. These risks could have a material and adverse impact on our business, results of operations, financial condition and cash flows and, if so, our prospects would likely be materially and adversely affected. If any of such events were to happen, the trading price of our securities in any market that may develop for our securities could decline and you could lose all or part of your investment.

Risks Related to Our Business and Growth Strategy

We have a limited operating history and our profits have been generated primarily by unrealized gains from equity securities we own in other companies. Although we have been profitable, the likelihood of our success must be considered in light of the problems, expenses, difficulties, complications and delays frequently encountered by a small developing company.

We were incorporated in the State of Utah in April 1984. Although we have reported earnings in the year ended April 30, 2021 and the six months ended October 31, 2021, the majority of our earnings came from unrealized gains in equity securities that we own. These securities have observable prices but are not liquid. Furthermore, the likelihood of our success must be considered in light of the problems, expenses, difficulties, complications and delays frequently encountered by a small developing company starting a new business enterprise and the highly competitive environment in which we will operate. Since we have a limited operating history, we cannot assure you that our business will maintain profitability.

We have substantial customer concentration, with a limited number of customers accounting for a substantial portion of our revenues.

We currently derive a significant portion of our revenues from a limited number of customers. During the six months ended October 31, 2021, sales to two customers individually totaled approximately $500,000 and $400,000, and approximately $900,000 in the aggregate, or approximately 75% of our total revenues for the period. For the year ended April 30, 2021, we had one customer that constituted 30% of our revenues, a second customer that constituted 15% of our revenues, a third customer that constituted 14% of our revenues, and a fourth customer that accounted for 11% of our revenues. For the year ended April 30, 2020, we had one customer that constituted 47% of our revenues, a second customer that constituted 31% of our revenues, and a third customer that accounted for 13% of our revenues. There are inherent risks whenever a large percentage of total revenues are concentrated with a limited number of customers. It is not possible for us to predict the future level of demand for our services that will be generated by these customers or new customers, or the future demand for the products and services of these customers or new customers. If any of these customers experience declining or delayed sales due to market, economic or competitive conditions, we could be pressured to reduce the prices we charge for our products which could have an adverse effect on our margins and financial position and could negatively affect our revenues and results of operations and/or trading price of our common stock.

We operate in a regulatory environment that is evolving and uncertain.

The regulatory framework for online capital formation or crowdfunding is very new. The regulations that govern our operations have been in existence for a very few years. Further, there are constant discussions among legislators and regulators with respect to changing the regulatory environment. New laws and regulations could be adopted in the United States and abroad. Further, existing laws and regulations may be interpreted in ways that would impact our operations, including how we communicate and work with investors and the companies that use our services and the types of securities that our clients can offer and sell on our platform.

We operate in a highly regulated industry.

We are subject to extensive regulation and failure to comply with such regulation could have an adverse effect on our business. Further, our subsidiary Netcapital Funding Portal Inc is registered as a funding portal. As a funding portal we have to comply with stringent regulations, and the operation of our funding portal is frequently subject to examination, constraints on its business, and in some cases fines. In addition, some of the restrictions and rules applicable to our subsidiary could adversely affect and limit some of our business plans.

Our funding portal’s service offerings are relatively new in an industry that is still quickly evolving.

The principal securities regulations that we work with, Rule 506(c) and Reg CF, have only been in effect in their current form since 2013 and 2016, respectively. Our ability to continue to penetrate the market remains uncertain as potential issuer companies may choose to use different platforms or providers (including, in the case of Rule 506(c) and Regulation A, using their own online platform), or determine alternative methods of financing. Investors may decide to invest their money elsewhere. Further, our potential market may not be as large, or our industry may not grow as rapidly as anticipated. Success will likely be a factor of investing in the development and implementation of marketing campaigns, repeat business from both issuer companies and investors, and favorable changes in the regulatory environment.

We have an evolving business model.

Our business model is one of innovation, including continuously working to expand our product lines and services to our clients. For example, we are evaluating an expansion into the transfer agent and broker-dealer space as well as our foray into becoming an alternative trading system. It is unclear whether these services will be successful. Further, we continuously try to offer additional types of services, and we cannot offer any assurance that any of them will be successful. From time to time, we may also modify aspects of our business model relating to our service offerings. We cannot offer any assurance that these or any other modifications will be successful or will not result in harm to the business. We may not be able to manage growth effectively, which could damage our reputation, limit our growth, and negatively affect our operating results.

9

We may be liable for misstatements made by issuers.

Under the Securities Act and the Securities Exchange Act of 1934 (the “Exchange Act”), issuers making offerings through our funding portal may be liable for inappropriate disclosures, including untrue statements of material facts or for omitting information that could make the statements misleading. This liability may also extend in Reg CF offerings to funding portals, such as our subsidiary. Even though due diligence defenses may be available, there can be no assurance that if we were sued, we would prevail. Further, even if we do succeed, lawsuits are time consuming and expensive, and being a party to such actions may cause us reputational harm that would negatively impact our business. Moreover, even if we are not liable or a party to a lawsuit or enforcement action, some of our clients have been and will be subject to such proceedings. Any involvement we may have, including responding to document production requests, may be time-consuming and expensive as well.

Our compliance is focused on U.S. laws and we have not analyzed foreign laws regarding the participation of non-U.S. residents.

Some of the investment opportunities posted on our platform are open to non-U.S. residents. We have not researched all the applicable foreign laws and regulations, and we have not set up our structure to be compliant with foreign laws. It is possible that we may be deemed in violation of those laws, which could result in fines or penalties as well as reputational harm. Any violation of foreign laws may limit our ability in the future to assist companies in accessing money from those investors, and compliance with those laws and regulations may limit our business operations and plans for future expansion.

Our cash flow is reliant on one main type of service.

Most of our cash-flow generating services are variants on one type of service: providing a platform for online capital formation. Our revenues are therefore dependent upon the market for online capital formation. As such, any downturn in the market could have a material adverse effect of our business and financial condition.

We depend on key personnel and face challenges recruiting needed personnel.

Our future success depends on the efforts of a small number of key personnel, including the founder of our subsidiary, Netcapital Funding Portal Inc. and Chief Executive Officer, and our compliance, engineering and marketing teams. Our software engineer team, as well as our compliance team and our marketing team are critical to continually innovate and improve our products while operating in a highly regulated industry. In addition, due to the specialized expertise required, we may not be able to recruit the individuals needed for our business needs. There can be no assurance that we will be successful in attracting and retaining the personnel we require to operate and be innovative.

We are vulnerable to hackers and cyber attacks.

As an internet-based business, we may be vulnerable to hackers who may access the data of our investors and the issuer companies that utilize our platform. Further, any significant disruption in service on our funding portal platform or in our computer systems could reduce the attractiveness of our platform and result in a loss of investors and companies interested in using our platform. Further, we rely on a third-party technology provider to provide some of our back-up technology as well as act as our escrow agent. Any disruptions of services or cyber-attacks either on our technology provider, escrow agent, or on us could harm our reputation and materially negatively impact our financial condition and business.

Our funding portal relies on one escrow agent to hold investment commitments for issuers.

We currently rely on Boston Private Bank to provide all escrow services related to offerings on our platform. Any change in this relationship will require us to find another escrow agent and escrow bank. This change may cause us delays as well as additional costs in transitioning our technology. We are not allowed to operate our funding portal business without a qualified third-party escrow bank. There are a limited number of banks that provide this service. As such, if our relationship with our escrow agent is terminated, we may have difficulty finding a replacement which could have a material adverse effect on our business and results of operations.

Our strategy to purchase a portion of early-stage companies may provide us with investments that have no liquidity.

It is our strategy to sometimes purchase, at an affordable price, part or all of early-stage companies and cross pollinate the ideas, technology and expertise within these companies to enhance the operations, profits and market share of all the entities. That strategy may result in us diverting management attention and advisory resources to do work for early-stage companies that pay for the work with equity, which becomes impaired in value or never becomes a liquid asset. For all of these early-stage companies, the future liquidity and value of our investments cannot be guaranteed, and no market may exist for us to generate gains from our investments in early-stage companies.

Our business depends on the reliability of the infrastructure that supports the Internet and the viability of the Internet.

The growth of Internet usage has caused frequent interruptions and delays in processing and transmitting data over the Internet. There can be no assurance that the Internet infrastructure or the Company’s own network systems will continue to be able to support the demands placed on it by the continued growth of the Internet, the overall online securities industry or that of our customers.

The Internet’s viability could be affected if the necessary infrastructure is not sufficient, or if other technologies and technological devices eclipse the Internet as a viable channel.

End-users of our software depend on Internet Service Providers (“ISPs”), online service providers and our system infrastructure for access to the Internet sites that we operate. Many of these services have experienced service outages in the past and could experience service outages, delays and other difficulties due to system failures, stability or interruption. As a result, we may not be able to meet a level of service that we have promised to our subscribers, and we may be in breach of our contractual commitments, which could materially adversely affect our business, revenues, operating results and financial condition.

10

We are dependent on general economic conditions.

Our business model is dependent on investors investing in the companies presented on our platforms. Investment dollars are disposable income. Our business model is thus dependent on national and international economic conditions. Adverse national and international economic conditions may reduce the future availability of investment dollars, which would negatively impact our revenues and possibly our ability to continue operations. It is not possible to accurately predict the potential adverse impacts on the Company, if any, of current economic conditions on its financial condition, operating results and cash flow.

We face significant market competition.

We facilitate online capital formation. Though this is a new market, we compete against a variety of entrants in the market as well likely new entrants into the market. Some of these follow a regulatory model that is different from ours and might provide them competitive advantages. New entrants could include those that may already have a foothold in the securities industry, including some established broker-dealers. Further, online capital formation is not the only way to address helping start-ups raise capital, and the Company has to compete with a number of other approaches, including traditional venture capital investments, loans and other traditional methods of raising funds and companies conducting crowdfunding raises on their own websites. Additionally, some competitors and future competitors may be better capitalized than us, which would give them a significant advantage in marketing and operations.

Moreover, as we continue to expand our offerings, including providing administrative services to issuers and transfer agent services, we will continue to face headwinds and compete with companies that are more established and/or have more financial resources than we do and/or new entrants bringing disruptive technologies and/or ideas.

Intense competition could prevent us from increasing our market share and growing our revenues.

We compete with a number of public and private companies and most of our competitors have significant financial resources and occupy entrenched positions in the market with name-brand recognition. We also face challenges from new Internet sites that aim to attract subscribers who seek to play interactive games or invest in public or private securities. Such companies may be able to attract significantly more subscribers because of new marketing ideas and user interface concepts.

Increased competition from current and future competitors may in the future materially adversely affect our business, revenues, operating results and financial condition.

We will require our secured lender to cooperate with us and, among other things, not demand repayments of principal and interest until the business is capable of making such payments.

We owed our secured lender, or the Lender, $1,000,000, or the Loan, as of October 31, 2021. Our Lender holds a term note bearing interest at an annual rate of 8%. We have not paid interest on the note and it accrues each month. We have a loan and security agreement, or the Loan, with the Lender for a maximum amount of $1,250,000. The maturity date of our loan from the Lender is April 30, 2023. We intend to pay off the Loan using a portions of the net proceeds from this offering.

To secure the payment of all obligations to the Lender, the Company granted to the Lender a continuing security interest and first lien on all of the assets of the Company.

In connection with the Loan, the Company has agreed to certain restrictive covenants, including, among others, that the Company may not convey, sell lease, transfer or otherwise dispose of any part of its business or property, except as permitted in the agreement, dissolve, liquidate or merge with any other party unless, in the case of a merger, the Company is the surviving entity, incur any indebtedness except as defined in the agreement, create or allow a lien on any of its assets or collateral that has been pledged to the Lender, make any loans to any person, except for prepaid items or deposits incurred in the ordinary course of business, or make any material capital expenditures. If we default on our loan obligations with the Lender, it could exercise their rights and remedies under the applicable agreements, which could include seizing all of our assets. Any such action would have a material adverse effect on our business and prospects.

The Loan contains numerous restrictive covenants which limit management’s discretion to operate our business.

In order to obtain Loan, we agreed to certain covenants that place significant restrictions on, among other things, our ability to incur additional indebtedness, to create liens or other encumbrances, to make certain payments and investments, and to sell or otherwise dispose of assets and merge or consolidate with other entities. Any failure to comply with the covenants included in the Loan could result in an event of default, which could trigger an acceleration of the related debt. If we were unable to repay the debt upon any such acceleration, the Lender could seek to foreclose on our assets in an effort to seek repayment under the loans. If the Lender was successful, we would be unable to conduct our business as it is presently conducted and our ability to generate revenues and fund our ongoing operations would be materially adversely affected.

11

We may require additional financing in the future to fund our operations.

We may need additional capital in the future to continue to execute our business plan. Therefore, we will be dependent upon additional capital in the form of either debt or equity to continue our operations. At the present time, we do not have arrangements to raise all of the needed additional capital, and we will need to identify potential investors and negotiate appropriate arrangements with them. Our ability to obtain additional financing will be subject to a number of factors, including market conditions, our operating performance and investor sentiment. If we are unable to raise additional capital when required or on acceptable terms, we may have to significantly delay, scale back or discontinue our operations.

Raising additional capital may cause dilution to our stockholders, restrict our operations or require us to relinquish certain rights.

We may seek additional capital through a combination of equity offerings, debt financings, strategic collaborations and alliances or licensing arrangements. To the extent that we raise additional capital through the sale of equity, convertible debt securities or other equity-based derivative securities, your ownership interest will be diluted and the terms may include liquidation or other preferences that adversely affect your rights as a stockholder. Any indebtedness we incur could involve restrictive covenants, such as limitations on our ability to incur additional debt, acquire or license intellectual property rights, declare dividends, make capital expenditures and other operating restrictions that could adversely impact our ability to conduct our business. Furthermore, the issuance of additional securities, whether equity or debt, by us, or the possibility of such issuance, may cause the market price of our common stock to decline. If we raise additional funds through strategic collaborations and alliances or licensing arrangements with third parties, we may have to relinquish valuable rights to future therapeutic candidates or otherwise agree to terms unfavorable to us, any of which may have a material adverse effect on our business, operating results and prospects. Adequate additional financing may not be available to us on acceptable terms, or at all. If we are unable to raise additional funds when needed, we may be required to delay, limit, reduce or terminate our product development or future commercialization efforts or grant rights to develop and market our future therapeutic candidates that we would otherwise prefer to develop and market ourselves.

Our debt level could negatively impact our financial condition, results of operations and business prospects.

As of February 9, 2022, we continue to have approximately $5,328,784 of indebtedness outstanding and we have borrowed money on three occasions from the SBA. Our level of debt could have significant consequences to our shareholders, including the following:

- requiring the dedication of a substantial portion of cash flow from operations to make payments on debt, thereby reducing the availability of cash flow for working capital, capital expenditures and other general business activities;

- requiring a substantial portion of our corporate cash reserves to be held as a reserve for debt service, limiting our ability to invest in new growth opportunities;

- limiting the ability to obtain additional financing in the future for working capital, capital expenditures, acquisitions and general corporate and other activities;

- limiting the flexibility in planning for, or reacting to, changes in the business and industry in which we operate;

- increasing our vulnerability to both general and industry-specific adverse economic conditions;

- putting us at a competitive disadvantage vs. less leveraged competitors; and

- increasing vulnerability to changes in the prevailing interest rates.

Our ability to make payments of principal and interest, or to refinance our indebtedness, depends on our future performance, which is subject to economic, financial, competitive and other factors. Our business may not generate sufficient cash flow in the future to service our debt because of factors beyond our control, including but not limited to our ability to market our products and expand our operations. If we are unable to generate sufficient cash flows, we may be required to adopt one or more alternatives, such as restructuring debt or obtaining additional equity capital on terms that may be onerous or highly dilutive. Our ability to refinance our indebtedness will depend on the capital markets and our financial condition at such time. We may not be able to engage in any of these activities or engage in these activities on desirable terms, which could result in a default on our debt obligations. We intend to repay this indebtedness with the proceeds raised in this offering.

12

We may make acquisitions or form joint ventures that are unsuccessful.

Our ability to grow is partially dependent on our ability to successfully acquire other companies, which creates substantial risk. In order to pursue a growth by acquisition strategy successfully, we must identify suitable candidates for these transactions; however, because of our limited funds, we may not be able to purchase those companies that we have identified as potential acquisition candidates. Additionally, we may have difficulty managing post-closing issues such as the integration into our corporate structure. Integration issues are complex, time consuming and expensive and, without proper planning and implementation, could significantly disrupt our business, including, but not limited to, the diversion of management's attention, the loss of key business and/or personnel from the acquired company, unanticipated events, and legal liabilities.

Our future growth depends on our ability to develop and retain customers.

Our future growth depends to a large extent on our ability to effectively anticipate and adapt to customer requirements and offer services that meet customer demands. If we are unable to attract new customers and/or retain new customers, our business, results of operations and financial condition may be materially adversely affected.

We will need to attract, train and retain additional highly qualified senior executives and technical and managerial personnel in the future.

We continue to seek technical and managerial staff members, although we have limited resources to compensate them until we have raised additional capital or developed a business that generates consistent cash flow from operations. We believe it is important to negotiate with potential candidates and, if appropriate, engage them on a part-time basis or on a project basis and compensate them at least partially, with stock-based compensation, when appropriate. There is a high demand for highly trained and managerial staff members. If we are not able to fill these positions, it may have an adverse effect on our business.

Major health epidemics, such as the outbreak caused by the COVID-19 pandemic, and other outbreaks or unforeseen or catastrophic events could continue to disrupt and adversely affect our operations, financial condition and business.

Public health epidemics or outbreaks could adversely impact our business. In July 2021, the global tally of confirmed cases of the coronavirus-borne illness COVID-19 exceeded 180 million. The extent to which the coronavirus impacts our operations will depend on future developments, which are highly uncertain and cannot be predicted with confidence, including the duration of the outbreak, new information which may emerge concerning the severity of the coronavirus and the emergence of variants, among others. In particular, the spread and treatment of the coronavirus globally could adversely impact our operations and could have an adverse impact on our business and our financial results. To date, our business has not been impacted by COVID-19 but it could be in the future.

We may make acquisitions or form joint ventures that are unsuccessful.

Our ability to grow is partially dependent on our ability to successfully acquire other companies, which creates substantial risk. In order to pursue a growth by acquisition strategy successfully, we must identify suitable candidates for these transactions; however, because of our limited funds, we may not be able to purchase those companies that we have identified as potential acquisition candidates. Additionally, we may have difficulty managing post-closing issues such as the integration into our corporate structure. Integration issues are complex, time consuming and expensive and, without proper planning and implementation, could significantly disrupt our business, including, but not limited to, the diversion of management's attention, the loss of key business and/or personnel from the acquired company, unanticipated events, and legal liabilities.

We may not be able to protect all of our intellectual property.

Our profitability may depend in part on our ability to effectively protect our proprietary rights, including obtaining trademarks for our brand names, protecting our products and websites, maintaining the secrecy of our internal workings and preserving our trade secrets, as well as our ability to operate without inadvertently infringing on the proprietary rights of others. There can be no assurance that we will be able to obtain future protections for our intellectual property or defend our current trademarks and future trademarks and patents. Further, policing and protecting our intellectual property against unauthorized use by third parties is time-consuming and expensive, and certain countries may not even recognize our intellectual property rights. There can also be no assurance that a third party will not assert infringement claims with respect to our products or technologies. Any litigation for both protecting our intellectual property or defending our use of certain technologies could have material adverse effect on our business, operating results and financial condition, regardless of the outcome of such litigation.

13

Our revenues and profits are subject to fluctuations.

It is difficult to accurately forecast our revenues and operating results, and these could fluctuate in the future due to a number of factors. These factors may include adverse changes in: number of investors and amount of investors’ dollars, the success of world securities markets, general economic conditions, our ability to market our platform to companies and investors, headcount and other operating costs, and general industry and regulatory conditions and requirements. The Company's operating results may fluctuate from year to year due to the factors listed above and others not listed. At times, these fluctuations may be significant and could impact our ability to operate our business.

Natural disasters and other events beyond our control could materially adversely affect us.

Natural disasters or other catastrophic events may cause damage or disruption to our operations, international commerce and the global economy, and thus could have a strong negative effect on us. Our business operations are subject to interruption by natural disasters, fire, power shortages, pandemics and other events beyond our control. Although we maintain crisis management and disaster response plans, such events could make it difficult or impossible for us to deliver our services to our customers and could decrease demand for our services. Since the spring of 2020, large segments of the U.S. and global economies were impacted by COVID-19, a significant portion of the U.S. population were subject to “stay at home” or similar requirements. The extent of the impact of COVID-19 on our operational and financial performance will depend on certain developments, including the duration and spread of the outbreak, impact on our customers (both issuers using our services and investors investing on our platform) and our sales cycles, impact on our customer, employee or industry events, and effect on our vendors, all of which are uncertain and cannot be predicted. At this point, the extent to which COVID-19 may impact our financial condition or results of operations is uncertain. To date, the COVID-19 outbreak, has significantly impacted global markets, U.S. employment numbers, as well as the business prospects of many small business (our potential clients). A significant part of our business model is based on receiving a percentage of the investments made through our platform and services. Further, we are dependent on investments in our offerings to fund our business. However, to date, other than working remotely, COVID-19 has not had a negative impact on the Company. While our business has not yet been impacted by COVID-19, to the extent COVID-19 continues and limits investment capital or personally impacts any of our key employees, it may have significant impact on our results and operations.

Acquisitions may have unanticipated consequences that could harm our business and our financial condition.

Any acquisition that we pursue, whether successfully completed or not, involves risks, including:

| • | material adverse effects on our operating results, particularly in the fiscal quarters immediately following the acquisition as the acquired restaurants are integrated into our operations; | |

| • | risks associated with entering into markets or conducting operations where we have no or limited prior experience; | |

| • | problems retaining key personnel; | |

| • | potential impairment of tangible and intangible assets and goodwill acquired in the acquisition; | |

| • | potential unknown liabilities; | |

| • | difficulties of integration and failure to realize anticipated synergies; and | |

| • | disruption of our ongoing business, including diversion of management’s attention from other business concerns. |

Future acquisitions may be accomplished through a cash purchase transaction, the issuance of our equity securities or a combination of both, could result in potentially dilutive issuances of our equity securities, the incurrence of debt and contingent liabilities and impairment charges related to goodwill and other intangible assets, any of which could harm our business and financial condition.

If we do not effectively protect our customers’ credit and debit card data, or other personal information, we could be exposed to data loss, litigation, liability and reputational damage.

In connection with credit and debit card sales, we transmit confidential credit and debit card information by way of secure online networks. Although we use private networks, third parties may have the technology or know-how to breach the security of the customer information transmitted in connection with credit and debit card sales, and our security measures and those of our technology vendors may not effectively prohibit others from obtaining improper access to this information. If a person were able to circumvent these security measures, he or she could destroy or steal valuable information or disrupt our operations. Any security breach could expose us to risks of data loss, litigation and liability and could seriously disrupt our operations and any resulting negative publicity could significantly harm our reputation.

14

Failure to recognize, respond to and effectively manage the accelerated impact of social media could adversely impact our business.