00014239020001414475falsefalse20232023FYFY11111http://fasb.org/us-gaap/2023#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2023#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2023#PropertyPlantAndEquipmentNethttp://fasb.org/us-gaap/2023#PropertyPlantAndEquipmentNethttp://fasb.org/us-gaap/2023#AccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2023#AccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationsCurrenthttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationsCurrenthttp://fasb.org/us-gaap/2023#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2023#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationshttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationshttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligations http://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationsCurrenthttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligations http://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationsCurrenthttp://fasb.org/us-gaap/2023#AccruedLiabilitiesCurrent http://fasb.org/us-gaap/2023#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2023#AccruedLiabilitiesCurrent http://fasb.org/us-gaap/2023#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2023#AccruedLiabilitiesCurrent http://fasb.org/us-gaap/2023#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2023#AccruedLiabilitiesCurrent http://fasb.org/us-gaap/2023#OtherLiabilitiesNoncurrent00014239022023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMember2023-01-012023-12-3100014239022023-06-30iso4217:USD00014239022024-02-14xbrli:shares0001423902wes:ServiceFeeBasedMember2023-01-012023-12-310001423902wes:ServiceFeeBasedMember2022-01-012022-12-310001423902wes:ServiceFeeBasedMember2021-01-012021-12-310001423902wes:ServiceProductBasedMember2023-01-012023-12-310001423902wes:ServiceProductBasedMember2022-01-012022-12-310001423902wes:ServiceProductBasedMember2021-01-012021-12-310001423902us-gaap:ProductMember2023-01-012023-12-310001423902us-gaap:ProductMember2022-01-012022-12-310001423902us-gaap:ProductMember2021-01-012021-12-310001423902us-gaap:ProductAndServiceOtherMember2023-01-012023-12-310001423902us-gaap:ProductAndServiceOtherMember2022-01-012022-12-310001423902us-gaap:ProductAndServiceOtherMember2021-01-012021-12-3100014239022022-01-012022-12-3100014239022021-01-012021-12-31iso4217:USDxbrli:shares0001423902srt:AffiliatedEntityMember2023-01-012023-12-310001423902srt:AffiliatedEntityMember2022-01-012022-12-310001423902srt:AffiliatedEntityMember2021-01-012021-12-3100014239022023-12-3100014239022022-12-310001423902srt:NaturalGasLiquidsReservesMember2023-12-310001423902srt:NaturalGasLiquidsReservesMember2022-12-310001423902srt:AffiliatedEntityMember2023-12-310001423902srt:AffiliatedEntityMember2022-12-310001423902wes:CommonUnitsMember2020-12-310001423902us-gaap:GeneralPartnerMember2020-12-310001423902us-gaap:NoncontrollingInterestMember2020-12-3100014239022020-12-310001423902wes:CommonUnitsMember2021-01-012021-12-310001423902us-gaap:GeneralPartnerMember2021-01-012021-12-310001423902us-gaap:NoncontrollingInterestMember2021-01-012021-12-310001423902us-gaap:NoncontrollingInterestMemberwes:ChipetaProcessingLimitedLiabilityCompanyMember2021-01-012021-12-310001423902wes:ChipetaProcessingLimitedLiabilityCompanyMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:NoncontrollingInterestMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMember2021-01-012021-12-310001423902wes:CommonUnitsMemberwes:OccidentalMember2021-01-012021-12-310001423902wes:OccidentalMember2021-01-012021-12-310001423902wes:CommonUnitsMember2021-12-310001423902us-gaap:GeneralPartnerMember2021-12-310001423902us-gaap:NoncontrollingInterestMember2021-12-3100014239022021-12-310001423902wes:CommonUnitsMember2022-01-012022-12-310001423902us-gaap:GeneralPartnerMember2022-01-012022-12-310001423902us-gaap:NoncontrollingInterestMember2022-01-012022-12-310001423902us-gaap:NoncontrollingInterestMemberwes:ChipetaProcessingLimitedLiabilityCompanyMember2022-01-012022-12-310001423902wes:ChipetaProcessingLimitedLiabilityCompanyMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:NoncontrollingInterestMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMember2022-01-012022-12-310001423902wes:CommonUnitsMemberwes:OccidentalMember2022-01-012022-12-310001423902wes:OccidentalMember2022-01-012022-12-310001423902wes:CommonUnitsMember2022-12-310001423902us-gaap:GeneralPartnerMember2022-12-310001423902us-gaap:NoncontrollingInterestMember2022-12-310001423902wes:CommonUnitsMember2023-01-012023-12-310001423902us-gaap:GeneralPartnerMember2023-01-012023-12-310001423902us-gaap:NoncontrollingInterestMember2023-01-012023-12-310001423902us-gaap:NoncontrollingInterestMemberwes:ChipetaProcessingLimitedLiabilityCompanyMember2023-01-012023-12-310001423902wes:ChipetaProcessingLimitedLiabilityCompanyMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:NoncontrollingInterestMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMember2023-01-012023-12-310001423902wes:CommonUnitsMember2023-12-310001423902us-gaap:GeneralPartnerMember2023-12-310001423902us-gaap:NoncontrollingInterestMember2023-12-310001423902wes:ThirdPartiesMember2023-01-012023-12-310001423902wes:ThirdPartiesMember2022-01-012022-12-310001423902wes:ThirdPartiesMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:ServiceFeeBasedMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:ServiceFeeBasedMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:ServiceFeeBasedMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:ServiceProductBasedMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:ServiceProductBasedMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:ServiceProductBasedMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:ProductMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:ProductMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:ProductMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:ProductAndServiceOtherMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:ProductAndServiceOtherMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:ProductAndServiceOtherMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMember2021-01-012021-12-310001423902srt:AffiliatedEntityMemberwes:WesternMidstreamOperatingLPMember2023-01-012023-12-310001423902srt:AffiliatedEntityMemberwes:WesternMidstreamOperatingLPMember2022-01-012022-12-310001423902srt:AffiliatedEntityMemberwes:WesternMidstreamOperatingLPMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMember2023-12-310001423902wes:WesternMidstreamOperatingLPMember2022-12-310001423902wes:WesternMidstreamOperatingLPMembersrt:NaturalGasLiquidsReservesMember2023-12-310001423902wes:WesternMidstreamOperatingLPMembersrt:NaturalGasLiquidsReservesMember2022-12-310001423902srt:AffiliatedEntityMemberwes:WesternMidstreamOperatingLPMember2022-12-310001423902srt:AffiliatedEntityMemberwes:WesternMidstreamOperatingLPMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:CommonUnitsMember2020-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:NoncontrollingInterestMember2020-12-310001423902wes:WesternMidstreamOperatingLPMember2020-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:CommonUnitsMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:NoncontrollingInterestMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:NoncontrollingInterestMemberwes:ChipetaProcessingLimitedLiabilityCompanyMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:ChipetaProcessingLimitedLiabilityCompanyMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:CommonUnitsMemberwes:OccidentalMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:OccidentalMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:CommonUnitsMemberwes:WesternMidstreamPartnersLPMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:WesternMidstreamPartnersLPMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:CommonUnitsMember2021-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:NoncontrollingInterestMember2021-12-310001423902wes:WesternMidstreamOperatingLPMember2021-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:CommonUnitsMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:NoncontrollingInterestMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:NoncontrollingInterestMemberwes:ChipetaProcessingLimitedLiabilityCompanyMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:ChipetaProcessingLimitedLiabilityCompanyMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:CommonUnitsMemberwes:OccidentalMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:OccidentalMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:CommonUnitsMemberwes:WesternMidstreamPartnersLPMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:WesternMidstreamPartnersLPMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:CommonUnitsMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:NoncontrollingInterestMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:CommonUnitsMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:NoncontrollingInterestMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:NoncontrollingInterestMemberwes:ChipetaProcessingLimitedLiabilityCompanyMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:ChipetaProcessingLimitedLiabilityCompanyMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:CommonUnitsMemberwes:WesternMidstreamPartnersLPMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:WesternMidstreamPartnersLPMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:CommonUnitsMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:NoncontrollingInterestMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:ThirdPartiesMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:ThirdPartiesMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:ThirdPartiesMember2021-01-012021-12-310001423902wes:WesternMidstreamPartnersLPMemberwes:WesternMidstreamOperatingLPMember2023-01-012023-12-31xbrli:pure0001423902wes:OperatedMemberwes:NaturalGasGatheringSystemMember2023-12-31wes:unit0001423902wes:NaturalGasGatheringSystemMemberwes:OperatedInterestMember2023-12-310001423902wes:NaturalGasGatheringSystemMemberwes:NonOperatedInterestMember2023-12-310001423902us-gaap:EquityMethodInvesteeMemberwes:NaturalGasGatheringSystemMember2023-12-310001423902wes:OperatedMemberwes:NaturalGasTreatingFacilitiesMember2023-12-310001423902wes:OperatedInterestMemberwes:NaturalGasTreatingFacilitiesMember2023-12-310001423902wes:OperatedMemberus-gaap:NaturalGasProcessingPlantMember2023-12-310001423902us-gaap:NaturalGasProcessingPlantMemberwes:OperatedInterestMember2023-12-310001423902us-gaap:EquityMethodInvesteeMemberus-gaap:NaturalGasProcessingPlantMember2023-12-310001423902wes:OperatedMemberwes:NaturalGasLiquidsPipelineMember2023-12-310001423902us-gaap:EquityMethodInvesteeMemberwes:NaturalGasLiquidsPipelineMember2023-12-310001423902wes:OperatedMembernaics:ZZ4862102023-12-310001423902us-gaap:EquityMethodInvesteeMembernaics:ZZ4862102023-12-310001423902wes:OperatedMembernaics:ZZ4861102023-12-310001423902wes:OperatedInterestMembernaics:ZZ4861102023-12-310001423902us-gaap:EquityMethodInvesteeMembernaics:ZZ4861102023-12-310001423902us-gaap:ConsolidatedEntitiesMemberwes:ChipetaProcessingLimitedLiabilityCompanyMember2023-01-012023-12-310001423902wes:SpringfieldPipelineLimitedLiabilityCompanyMemberwes:ProportionateConsolidationMember2023-01-012023-12-310001423902wes:MarcellusInterestMemberwes:ProportionateConsolidationMember2023-01-012023-12-310001423902us-gaap:EquityMethodInvesteeMemberwes:MiVidaJointVentureLimitedLiabilityCompanyMember2023-12-310001423902us-gaap:EquityMethodInvesteeMemberwes:FrontRangePipelineLLCMember2023-12-310001423902wes:RedBluffExpressPipelineLimitedLiabilityCompanyMemberus-gaap:EquityMethodInvesteeMember2023-12-310001423902wes:MontBelvieuJointVentureMemberus-gaap:EquityMethodInvesteeMember2023-12-310001423902us-gaap:EquityMethodInvesteeMemberwes:RendezvousMember2023-12-310001423902wes:TexasExpressPipelineLLCMemberus-gaap:EquityMethodInvesteeMember2023-12-310001423902wes:TexasExpressGatheringLLCMemberus-gaap:EquityMethodInvesteeMember2023-12-310001423902us-gaap:EquityMethodInvesteeMemberwes:WhitethornPipelineCompanyLimitedLiabilityCompanyMember2023-12-310001423902wes:SaddlehornPipelineCompanyLimitedLiabilityCompanyMemberus-gaap:EquityMethodInvesteeMember2023-12-310001423902wes:PanolaPipelineCompanyLimitedLiabilityCompanyMemberus-gaap:EquityMethodInvesteeMember2023-12-310001423902wes:WhiteCliffsMemberus-gaap:EquityMethodInvesteeMember2023-12-310001423902wes:ChipetaProcessingLimitedLiabilityCompanyMember2023-12-310001423902wes:WesternMidstreamOperatingLPMember2023-12-310001423902wes:LeasesRevenueMember2023-01-012023-12-310001423902wes:LeasesRevenueMember2022-01-012022-12-310001423902wes:LeasesRevenueMember2021-01-012021-12-310001423902wes:CustomersMember2023-12-310001423902wes:CustomersMember2022-12-3100014239022024-01-012023-12-3100014239022025-01-012023-12-3100014239022026-01-012023-12-3100014239022027-01-012023-12-3100014239022028-01-012023-12-3100014239022029-01-012023-12-310001423902wes:MeritageMidstreamServicesIILLCMember2023-10-132023-10-130001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes6Point35PercentDue2029Memberus-gaap:SeniorNotesMember2023-12-310001423902wes:MeritageMidstreamServicesIILLCMember2023-01-012023-12-310001423902wes:MeritageMidstreamServicesIILLCMember2023-12-310001423902wes:MeritageMidstreamServicesIILLCMember2022-01-012022-12-310001423902wes:CactusIIPipelineLimitedLiabilityCompanyMember2022-12-310001423902wes:CactusIIPipelineLimitedLiabilityCompanyMember2022-01-012022-12-310001423902wes:CactusIIPipelineLimitedLiabilityCompanyMember2022-10-012022-12-310001423902wes:RanchWestexJointVentureLimitedLiabilityCompanyMember2022-10-012022-12-310001423902wes:RanchWestexJointVentureLimitedLiabilityCompanyMember2022-01-012022-12-310001423902wes:FortUnionInvestmentMember2020-12-310001423902wes:BisonMember2021-01-012021-12-310001423902wes:BisonMember2020-10-012020-12-310001423902wes:BisonMember2021-04-012021-06-300001423902wes:WesternMidstreamPartnersLPMember2023-01-012023-12-3100014239022021-01-012021-03-3100014239022021-04-012021-06-3000014239022021-07-012021-09-3000014239022021-10-012021-12-3100014239022022-01-012022-03-3100014239022022-04-012022-06-3000014239022022-07-012022-09-3000014239022022-10-012022-12-3100014239022023-01-012023-03-3100014239022023-04-012023-06-3000014239022023-07-012023-09-3000014239022023-10-012023-12-310001423902wes:WesternMidstreamOperatingLPMember2021-01-012021-03-310001423902wes:WesternMidstreamOperatingLPMember2021-04-012021-06-300001423902wes:WesternMidstreamOperatingLPMember2021-07-012021-09-300001423902wes:WesternMidstreamOperatingLPMember2021-10-012021-12-310001423902wes:WesternMidstreamOperatingLPMember2022-01-012022-03-310001423902wes:WesternMidstreamOperatingLPMember2022-04-012022-06-300001423902wes:WesternMidstreamOperatingLPMember2022-07-012022-09-300001423902wes:WesternMidstreamOperatingLPMember2022-10-012022-12-310001423902wes:WesternMidstreamOperatingLPMember2023-01-012023-03-310001423902wes:WesternMidstreamOperatingLPMember2023-04-012023-06-300001423902wes:WesternMidstreamOperatingLPMember2023-07-012023-09-300001423902wes:WesternMidstreamOperatingLPMember2023-10-012023-12-310001423902wes:OccidentalMemberwes:WesternMidstreamPartnersLPMember2023-12-310001423902wes:OccidentalMemberwes:WesternMidstreamPartnersLPMember2023-01-012023-12-310001423902wes:PublicMemberwes:WesternMidstreamPartnersLPMember2023-12-310001423902wes:PublicMemberwes:WesternMidstreamPartnersLPMember2023-01-012023-12-310001423902wes:OccidentalMemberus-gaap:LimitedPartnerMember2021-03-012021-03-3100014239022022-11-020001423902wes:PublicMember2023-01-012023-12-310001423902wes:OccidentalMember2023-01-012023-12-310001423902wes:PublicMember2022-01-012022-12-310001423902wes:OccidentalMember2022-01-012022-12-3100014239022020-11-300001423902wes:PublicMember2021-01-012021-12-310001423902wes:OccidentalMember2021-01-012021-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:OccidentalMember2023-01-012023-12-310001423902srt:AffiliatedEntityMemberwes:ServiceFeeBasedMember2023-01-012023-12-310001423902srt:AffiliatedEntityMemberwes:ServiceFeeBasedMember2022-01-012022-12-310001423902srt:AffiliatedEntityMemberwes:ServiceFeeBasedMember2021-01-012021-12-310001423902srt:AffiliatedEntityMemberwes:ServiceProductBasedMember2023-01-012023-12-310001423902srt:AffiliatedEntityMemberwes:ServiceProductBasedMember2022-01-012022-12-310001423902srt:AffiliatedEntityMemberwes:ServiceProductBasedMember2021-01-012021-12-310001423902srt:AffiliatedEntityMemberus-gaap:ProductMember2023-01-012023-12-310001423902srt:AffiliatedEntityMemberus-gaap:ProductMember2022-01-012022-12-310001423902srt:AffiliatedEntityMemberus-gaap:ProductMember2021-01-012021-12-310001423902srt:AffiliatedEntityMemberwes:WesternMidstreamOperatingLPMember2023-01-012023-12-310001423902srt:AffiliatedEntityMemberwes:WesternMidstreamOperatingLPMember2022-01-012022-12-310001423902srt:AffiliatedEntityMemberwes:WesternMidstreamOperatingLPMember2021-01-012021-12-310001423902wes:NaturalGasMember2023-01-012023-12-310001423902wes:NaturalGasMember2022-01-012022-12-310001423902wes:NaturalGasMember2021-01-012021-12-310001423902wes:CrudeOilandNGLsMember2023-01-012023-12-310001423902wes:CrudeOilandNGLsMember2022-01-012022-12-310001423902wes:CrudeOilandNGLsMember2021-01-012021-12-310001423902us-gaap:PublicUtilitiesInventoryWaterMember2023-01-012023-12-310001423902us-gaap:PublicUtilitiesInventoryWaterMember2022-01-012022-12-310001423902us-gaap:PublicUtilitiesInventoryWaterMember2021-01-012021-12-310001423902srt:AffiliatedEntityMemberwes:IncentivePlansMember2022-01-012022-12-310001423902srt:AffiliatedEntityMemberwes:IncentivePlansMember2021-01-012021-12-310001423902srt:AffiliatedEntityMember2021-01-012021-03-310001423902srt:AffiliatedEntityMember2021-03-310001423902wes:WhiteCliffsMember2021-12-310001423902wes:WhiteCliffsMember2022-01-012022-12-310001423902wes:WhiteCliffsMember2022-12-310001423902wes:RendezvousMember2021-12-310001423902wes:RendezvousMember2022-01-012022-12-310001423902wes:RendezvousMember2022-12-310001423902wes:MontBelvieuJointVentureMember2021-12-310001423902wes:MontBelvieuJointVentureMember2022-01-012022-12-310001423902wes:MontBelvieuJointVentureMember2022-12-310001423902wes:TexasExpressGatheringLLCMember2021-12-310001423902wes:TexasExpressGatheringLLCMember2022-01-012022-12-310001423902wes:TexasExpressGatheringLLCMember2022-12-310001423902wes:TexasExpressPipelineLLCMember2021-12-310001423902wes:TexasExpressPipelineLLCMember2022-01-012022-12-310001423902wes:TexasExpressPipelineLLCMember2022-12-310001423902wes:FrontRangePipelineLLCMember2021-12-310001423902wes:FrontRangePipelineLLCMember2022-01-012022-12-310001423902wes:FrontRangePipelineLLCMember2022-12-310001423902wes:WhitethornPipelineCompanyLimitedLiabilityCompanyMember2021-12-310001423902wes:WhitethornPipelineCompanyLimitedLiabilityCompanyMember2022-01-012022-12-310001423902wes:WhitethornPipelineCompanyLimitedLiabilityCompanyMember2022-12-310001423902wes:CactusIIPipelineLimitedLiabilityCompanyMember2021-12-310001423902wes:SaddlehornPipelineCompanyLimitedLiabilityCompanyMember2021-12-310001423902wes:SaddlehornPipelineCompanyLimitedLiabilityCompanyMember2022-01-012022-12-310001423902wes:SaddlehornPipelineCompanyLimitedLiabilityCompanyMember2022-12-310001423902wes:PanolaPipelineCompanyLimitedLiabilityCompanyMember2021-12-310001423902wes:PanolaPipelineCompanyLimitedLiabilityCompanyMember2022-01-012022-12-310001423902wes:PanolaPipelineCompanyLimitedLiabilityCompanyMember2022-12-310001423902wes:MiVidaJointVentureLimitedLiabilityCompanyMember2021-12-310001423902wes:MiVidaJointVentureLimitedLiabilityCompanyMember2022-01-012022-12-310001423902wes:MiVidaJointVentureLimitedLiabilityCompanyMember2022-12-310001423902wes:RanchWestexJointVentureLimitedLiabilityCompanyMember2021-12-310001423902wes:RanchWestexJointVentureLimitedLiabilityCompanyMember2022-01-012022-12-310001423902wes:RanchWestexJointVentureLimitedLiabilityCompanyMember2022-12-310001423902wes:RedBluffExpressPipelineLimitedLiabilityCompanyMember2021-12-310001423902wes:RedBluffExpressPipelineLimitedLiabilityCompanyMember2022-01-012022-12-310001423902wes:RedBluffExpressPipelineLimitedLiabilityCompanyMember2022-12-310001423902wes:WhiteCliffsMember2023-01-012023-12-310001423902wes:WhiteCliffsMember2023-12-310001423902wes:RendezvousMember2023-01-012023-12-310001423902wes:RendezvousMember2023-12-310001423902wes:MontBelvieuJointVentureMember2023-01-012023-12-310001423902wes:MontBelvieuJointVentureMember2023-12-310001423902wes:TexasExpressGatheringLLCMember2023-01-012023-12-310001423902wes:TexasExpressGatheringLLCMember2023-12-310001423902wes:TexasExpressPipelineLLCMember2023-01-012023-12-310001423902wes:TexasExpressPipelineLLCMember2023-12-310001423902wes:FrontRangePipelineLLCMember2023-01-012023-12-310001423902wes:FrontRangePipelineLLCMember2023-12-310001423902wes:WhitethornPipelineCompanyLimitedLiabilityCompanyMember2023-01-012023-12-310001423902wes:WhitethornPipelineCompanyLimitedLiabilityCompanyMember2023-12-310001423902wes:SaddlehornPipelineCompanyLimitedLiabilityCompanyMember2023-01-012023-12-310001423902wes:SaddlehornPipelineCompanyLimitedLiabilityCompanyMember2023-12-310001423902wes:PanolaPipelineCompanyLimitedLiabilityCompanyMember2023-01-012023-12-310001423902wes:PanolaPipelineCompanyLimitedLiabilityCompanyMember2023-12-310001423902wes:MiVidaJointVentureLimitedLiabilityCompanyMember2023-01-012023-12-310001423902wes:MiVidaJointVentureLimitedLiabilityCompanyMember2023-12-310001423902wes:RedBluffExpressPipelineLimitedLiabilityCompanyMember2023-01-012023-12-310001423902wes:RedBluffExpressPipelineLimitedLiabilityCompanyMember2023-12-310001423902us-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOtherMember2023-01-012023-12-310001423902us-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOtherMember2022-01-012022-12-310001423902us-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOtherMember2021-01-012021-12-310001423902us-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOtherMember2023-12-310001423902us-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOtherMember2022-12-310001423902us-gaap:LandMember2023-12-310001423902us-gaap:LandMember2022-12-310001423902us-gaap:PipelinesMember2023-12-310001423902us-gaap:PipelinesMember2022-12-310001423902us-gaap:GasGatheringAndProcessingEquipmentMember2023-12-310001423902us-gaap:GasGatheringAndProcessingEquipmentMember2022-12-310001423902us-gaap:NaturalGasProcessingPlantMember2023-12-310001423902us-gaap:NaturalGasProcessingPlantMember2022-12-310001423902srt:MinimumMemberwes:TransportationPipelinesAndEquipmentMember2023-12-310001423902srt:MaximumMemberwes:TransportationPipelinesAndEquipmentMember2023-12-310001423902wes:TransportationPipelinesAndEquipmentMember2023-12-310001423902wes:TransportationPipelinesAndEquipmentMember2022-12-310001423902wes:ProducedWaterDisposalSystemMember2023-12-310001423902wes:ProducedWaterDisposalSystemMember2022-12-310001423902us-gaap:AssetUnderConstructionMember2023-12-310001423902us-gaap:AssetUnderConstructionMember2022-12-310001423902srt:MinimumMemberus-gaap:OtherCapitalizedPropertyPlantAndEquipmentMember2023-12-310001423902srt:MaximumMemberus-gaap:OtherCapitalizedPropertyPlantAndEquipmentMember2023-12-310001423902us-gaap:OtherCapitalizedPropertyPlantAndEquipmentMember2023-12-310001423902us-gaap:OtherCapitalizedPropertyPlantAndEquipmentMember2022-12-310001423902wes:RockiesAssetsMember2023-01-012023-12-310001423902us-gaap:IncomeApproachValuationTechniqueMemberus-gaap:FairValueMeasurementsNonrecurringMemberwes:RockiesAssetsMemberus-gaap:FairValueInputsLevel3Member2023-12-310001423902wes:DJBasinComplexMember2021-01-012021-12-310001423902wes:GatheringandProcessingReportingUnitMember2023-12-310001423902wes:TransportationReportingUnitMember2023-12-310001423902wes:DJBasinComplexProcessingPlantsMember2023-12-310001423902wes:DelawareBasinMidstreamLimitedLiabilityCompanyMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotesFloatingRateDue2023Memberus-gaap:SeniorNotesMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotesFloatingRateDue2023Memberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:CommercialPaperMemberwes:CommercialPaperProgram1Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:FairValueInputsLevel2Memberus-gaap:CommercialPaperMemberus-gaap:MarketApproachValuationTechniqueMemberwes:CommercialPaperProgram1Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:FinanceLeaseLiabilityShortTermMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:FinanceLeaseLiabilityShortTermMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:FinanceLeaseLiabilityShortTermMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:FinanceLeaseLiabilityShortTermMember2022-12-310001423902us-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2023-12-310001423902us-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes3Point100PercentDue2025Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorNotes3Point100PercentDue2025Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes3Point100PercentDue2025Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorNotes3Point100PercentDue2025Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes3Point950PercentDue2025Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorNotes3Point950PercentDue2025Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes3Point950PercentDue2025Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorNotes3Point950PercentDue2025Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes4Point650PercentDue2026Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorNotes4Point650PercentDue2026Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes4Point650PercentDue2026Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorNotes4Point650PercentDue2026Member2022-12-310001423902wes:SeniorNotes4Point500PercentDue2028Memberwes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMember2023-12-310001423902wes:SeniorNotes4Point500PercentDue2028Memberwes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2023-12-310001423902wes:SeniorNotes4Point500PercentDue2028Memberwes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMember2022-12-310001423902wes:SeniorNotes4Point500PercentDue2028Memberwes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes4Point750PercentDue2028Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorNotes4Point750PercentDue2028Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes4Point750PercentDue2028Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorNotes4Point750PercentDue2028Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes6Point35PercentDue2029Memberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes6Point35PercentDue2029Memberus-gaap:SeniorNotesMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes6Point35PercentDue2029Memberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes4Point50PercentDue2030Memberus-gaap:SeniorNotesMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes4Point50PercentDue2030Memberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes4Point50PercentDue2030Memberus-gaap:SeniorNotesMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes4Point50PercentDue2030Memberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes6Point15PercentDue2033Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorNotes6Point15PercentDue2033Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes6Point15PercentDue2033Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorNotes6Point15PercentDue2033Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes5Point450PercentDue2044Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorNotes5Point450PercentDue2044Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes5Point450PercentDue2044Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorNotes5Point450PercentDue2044Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes5Point300PercentDue2048Memberus-gaap:SeniorNotesMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes5Point300PercentDue2048Memberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes5Point300PercentDue2048Memberus-gaap:SeniorNotesMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes5Point300PercentDue2048Memberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes5Point500PercentDue2048Memberus-gaap:SeniorNotesMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes5Point500PercentDue2048Memberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes5Point500PercentDue2048Memberus-gaap:SeniorNotesMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes5Point500PercentDue2048Memberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes5Point250PercentDue2050Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorNotes5Point250PercentDue2050Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes5Point250PercentDue2050Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorNotes5Point250PercentDue2050Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:RevolvingCreditFacilityMemberwes:SeniorRevolvingCreditFacility1Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorRevolvingCreditFacility1Member2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:RevolvingCreditFacilityMemberwes:SeniorRevolvingCreditFacility1Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:SeniorRevolvingCreditFacility1Member2022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:FinanceLeaseLiabilityLongTermMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:FinanceLeaseLiabilityLongTermMember2023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:FinanceLeaseLiabilityLongTermMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMemberwes:FinanceLeaseLiabilityLongTermMember2022-12-310001423902wes:LongTermDebtObligationsMember2023-12-310001423902wes:LongTermDebtObligationsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2023-12-310001423902wes:LongTermDebtObligationsMember2022-12-310001423902wes:LongTermDebtObligationsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MarketApproachValuationTechniqueMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:RevolvingCreditFacilityMemberwes:SeniorRevolvingCreditFacility1Member2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes4PercentDue2022Memberus-gaap:SeniorNotesMember2022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes4PercentDue2022Memberus-gaap:SeniorNotesMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes3Point100PercentDue2025Member2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:FinanceLeaseLiabilityMember2022-01-012022-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:RevolvingCreditFacilityMemberwes:SeniorRevolvingCreditFacility1Member2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:CommercialPaperMemberwes:CommercialPaperProgram1Member2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes6Point35PercentDue2029Memberus-gaap:SeniorNotesMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes6Point15PercentDue2033Member2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotesFloatingRateDue2023Memberus-gaap:SeniorNotesMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes3Point100PercentDue2025Member2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes3Point950PercentDue2025Member2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes4Point650PercentDue2026Member2023-01-012023-12-310001423902wes:SeniorNotes4Point500PercentDue2028Memberwes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMemberwes:SeniorNotes4Point750PercentDue2028Member2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:SeniorNotes4Point50PercentDue2030Memberus-gaap:SeniorNotesMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberwes:FinanceLeaseLiabilityMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:SeniorNotesMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMembersrt:MinimumMemberus-gaap:RevolvingCreditFacilityMemberwes:PercentageMarginAboveAdjustedTermSOFRMemberwes:SeniorRevolvingCreditFacility1Member2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:RevolvingCreditFacilityMemberwes:PercentageMarginAboveAdjustedTermSOFRMembersrt:MaximumMemberwes:SeniorRevolvingCreditFacility1Member2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:RevolvingCreditFacilityMemberwes:SeniorRevolvingCreditFacility1Memberwes:AlternateBaseRatePercentageAboveFederalFundsEffectiveRateMember2023-01-012023-12-310001423902wes:AlternateBaseRatePercentageAboveAdjustedTermSOFRMemberwes:WesternMidstreamOperatingLPMemberus-gaap:RevolvingCreditFacilityMemberwes:SeniorRevolvingCreditFacility1Member2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMembersrt:MinimumMemberus-gaap:RevolvingCreditFacilityMemberwes:SeniorRevolvingCreditFacility1Memberus-gaap:BaseRateMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:RevolvingCreditFacilityMembersrt:MaximumMemberwes:SeniorRevolvingCreditFacility1Memberus-gaap:BaseRateMember2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMembersrt:MinimumMemberus-gaap:RevolvingCreditFacilityMemberwes:SeniorRevolvingCreditFacility1Member2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:RevolvingCreditFacilityMembersrt:MaximumMemberwes:SeniorRevolvingCreditFacility1Member2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:CommercialPaperMembersrt:MaximumMemberwes:CommercialPaperProgram1Member2023-01-012023-12-310001423902wes:WesternMidstreamOperatingLPMemberus-gaap:CommercialPaperMembersrt:WeightedAverageMemberwes:CommercialPaperProgram1Member2023-01-012023-12-310001423902wes:WesternGasPartners2017LongTermIncentivePlanMember2023-12-310001423902wes:WesternMidstreamPartnersLP2021LongTermIncentivePlanMember2023-12-310001423902wes:WesternMidstreamPartnersLP2021LongTermIncentivePlanMember2021-03-220001423902wes:TimeVestedMemberwes:ExecutiveLongTermIncentivePlansMember2023-01-012023-12-310001423902wes:MarketAwardMemberwes:ExecutiveLongTermIncentivePlansMember2023-01-012023-12-310001423902us-gaap:PerformanceSharesMemberwes:ExecutiveLongTermIncentivePlansMember2023-01-012023-12-310001423902srt:MinimumMember2023-01-012023-12-310001423902srt:MaximumMember2023-01-012023-12-310001423902wes:LongTermIncentivePlansMember2023-01-012023-12-310001423902wes:LongTermIncentivePlansMember2022-01-012022-12-310001423902wes:LongTermIncentivePlansMember2021-01-012021-12-310001423902wes:NonExecutiveLongTermIncentivePlansMember2023-01-012023-12-310001423902wes:IndependentDirectorLongTermIncentivePlansMember2023-01-012023-12-310001423902wes:TimeVestedMember2022-12-310001423902wes:TimeVestedMember2021-12-310001423902wes:TimeVestedMember2020-12-310001423902wes:TimeVestedMember2023-01-012023-12-310001423902wes:TimeVestedMember2022-01-012022-12-310001423902wes:TimeVestedMember2021-01-012021-12-310001423902wes:TimeVestedMember2023-12-310001423902wes:MarketAwardMember2022-12-310001423902wes:MarketAwardMember2021-12-310001423902wes:MarketAwardMember2020-12-310001423902wes:MarketAwardMember2023-01-012023-12-310001423902wes:MarketAwardMember2022-01-012022-12-310001423902wes:MarketAwardMember2021-01-012021-12-310001423902wes:MarketAwardMember2023-12-310001423902us-gaap:PerformanceSharesMember2022-12-310001423902us-gaap:PerformanceSharesMember2021-12-310001423902us-gaap:PerformanceSharesMember2020-12-310001423902us-gaap:PerformanceSharesMember2023-01-012023-12-310001423902us-gaap:PerformanceSharesMember2022-01-012022-12-310001423902us-gaap:PerformanceSharesMember2021-01-012021-12-310001423902us-gaap:PerformanceSharesMember2023-12-310001423902wes:MarcellusInterestSystemsPanolaMontBelvieuJVWhitethornAndSaddlehornMemberus-gaap:SubsequentEventMember2024-02-212024-02-21

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2023

Or

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

| | |

| WESTERN MIDSTREAM PARTNERS, LP |

| WESTERN MIDSTREAM OPERATING, LP |

| (Exact name of registrant as specified in its charter) |

| | | | | | | | | | | |

| Commission file number: | State or other jurisdiction of incorporation or organization: | I.R.S. Employer Identification No.: |

| Western Midstream Partners, LP | 001-35753 | Delaware | 46-0967367 |

| Western Midstream Operating, LP | 001-34046 | Delaware | 26-1075808 |

| | | | | | | | | | | | | | | | | | | | |

| Address of principal executive offices: | Zip Code: | Registrant’s telephone number, including area code: |

| Western Midstream Partners, LP | 9950 Woodloch Forest Drive, Suite 2800 | The Woodlands, | Texas | 77380 | (346) | 786-5000 |

| Western Midstream Operating, LP | 9950 Woodloch Forest Drive, Suite 2800 | The Woodlands, | Texas | 77380 | (346) | 786-5000 |

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | |

| Title of each class | Trading symbol | Name of exchange

on which registered |

| Western Midstream Partners, LP | Common units | WES | New York Stock Exchange |

| Western Midstream Operating, LP | None | None | None |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| | | | | | | | | | | | | | |

| Western Midstream Partners, LP | Yes | þ | No | ¨ |

| Western Midstream Operating, LP | Yes | þ | No | ¨ |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

| | | | | | | | | | | | | | |

| Western Midstream Partners, LP | Yes | ¨ | No | þ |

| Western Midstream Operating, LP | Yes | ¨ | No | þ |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| | | | | | | | | | | | | | |

| Western Midstream Partners, LP | Yes | þ | No | ¨ |

| Western Midstream Operating, LP | Yes | þ | No | ¨ |

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

| | | | | | | | | | | | | | |

| Western Midstream Partners, LP | Yes | þ | No | ¨ |

| Western Midstream Operating, LP | Yes | þ | No | ¨ |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | |

| | | | | |

| Western Midstream Partners, LP | Large Accelerated Filer | Accelerated Filer | Non-accelerated Filer | Smaller Reporting Company | Emerging Growth Company |

| þ | ☐ | ☐ | ☐ | ☐ |

| Western Midstream Operating, LP | Large Accelerated Filer | Accelerated Filer | Non-accelerated Filer | Smaller Reporting Company | Emerging Growth Company |

| ☐ | ☐ | þ | ☐ | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

| | | | | |

| Western Midstream Partners, LP | ¨ |

| Western Midstream Operating, LP | ¨ |

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

| | | | | |

| Western Midstream Partners, LP | ☑ |

| Western Midstream Operating, LP | ☐ |

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

| | | | | |

| Western Midstream Partners, LP | ☐ |

| Western Midstream Operating, LP | ☐ |

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

| | | | | |

| Western Midstream Partners, LP | ☐ |

| Western Midstream Operating, LP | ☐ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| | | | | | | | | | | | | | |

| Western Midstream Partners, LP | Yes | ☐ | No | þ |

| Western Midstream Operating, LP | Yes | ☐ | No | þ |

The aggregate market value of the registrant’s common units representing limited partner interests held by non-affiliates of the registrant on June 30, 2023, based on the closing price as reported on the New York Stock Exchange.

| | | | | |

| Western Midstream Partners, LP | $5.1 billion |

| Western Midstream Operating, LP | None |

Common units outstanding as of February 14, 2024:

| | | | | |

| Western Midstream Partners, LP | 380,483,668 |

| Western Midstream Operating, LP | None |

DOCUMENTS INCORPORATED BY REFERENCE

None

| | | | | | | | | | | |

| Auditor Name | Auditor Location | Auditor Firm ID |

| Western Midstream Partners, LP | KPMG LLP | Houston, Texas | 185 |

| Western Midstream Operating, LP | KPMG LLP | Houston, Texas | 185 |

FILING FORMAT

This annual report on Form 10-K is a combined report being filed by two separate registrants: Western Midstream Partners, LP and Western Midstream Operating, LP. Western Midstream Operating, LP is a consolidated subsidiary of Western Midstream Partners, LP that has publicly traded debt, but does not have any publicly traded equity securities. Information contained herein related to any individual registrant is filed by such registrant solely on its own behalf. Each registrant makes no representation as to information relating exclusively to the other registrant.

Part II, Item 8 of this annual report includes separate financial statements (i.e., consolidated statements of operations, consolidated balance sheets, consolidated statements of equity and partners’ capital, and consolidated statements of cash flows) for Western Midstream Partners, LP and Western Midstream Operating, LP. The accompanying Notes to Consolidated Financial Statements, which are included under Part II, Item 8 of this annual report, and Management’s Discussion and Analysis of Financial Condition and Results of Operations, which is included under Part II, Item 7 of this annual report, are presented on a combined basis for each registrant, with any material differences between the registrants disclosed separately.

TABLE OF CONTENTS

| | | | | | | | |

| Item | | Page |

| | |

| 1 and 2. | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| 1A. | | |

| 1B. | | |

| 1C. | | |

| 3. | | |

| 4. | | |

| | |

| 5. | | |

| | |

| | |

| | |

| 7. | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| 7A. | | |

| 8. | | |

| 9. | | |

| 9A. | | |

| 9B. | | |

| 9C. | | |

| | | | | | | | |

| Item | | Page |

| | |

| 10. | | |

| 11. | | |

| 12. | | |

| 13. | | |

| 14. | | |

| | |

| 15. | | |

| 16. | | |

COMMONLY USED ABBREVIATIONS AND TERMS

References to “we,” “us,” “our,” “WES,” “the Partnership,” or “Western Midstream Partners, LP” refer to Western Midstream Partners, LP (formerly Western Gas Equity Partners, LP) and its subsidiaries. The following list of abbreviations and terms are used in this document:

| | | | | | | | |

| Defined Term | | Definition |

| Anadarko | | Anadarko Petroleum Corporation and its subsidiaries, excluding our general partner, which became a wholly owned subsidiary of Occidental upon closing of the Occidental Merger on August 8, 2019. |

| Barrel, Bbl, Bbls/d, MBbls/d | | 42 U.S. gallons measured at 60 degrees Fahrenheit, barrels per day, thousand barrels per day. |

| Board | | The board of directors of WES’s general partner. |

| Cactus II | | Cactus II Pipeline LLC, in which we held a 15% interest that we sold in November 2022 (see Note 3—Acquisitions and Divestitures in the Notes to Consolidated Financial Statements under Part II, Item 8 of this Form 10-K). |

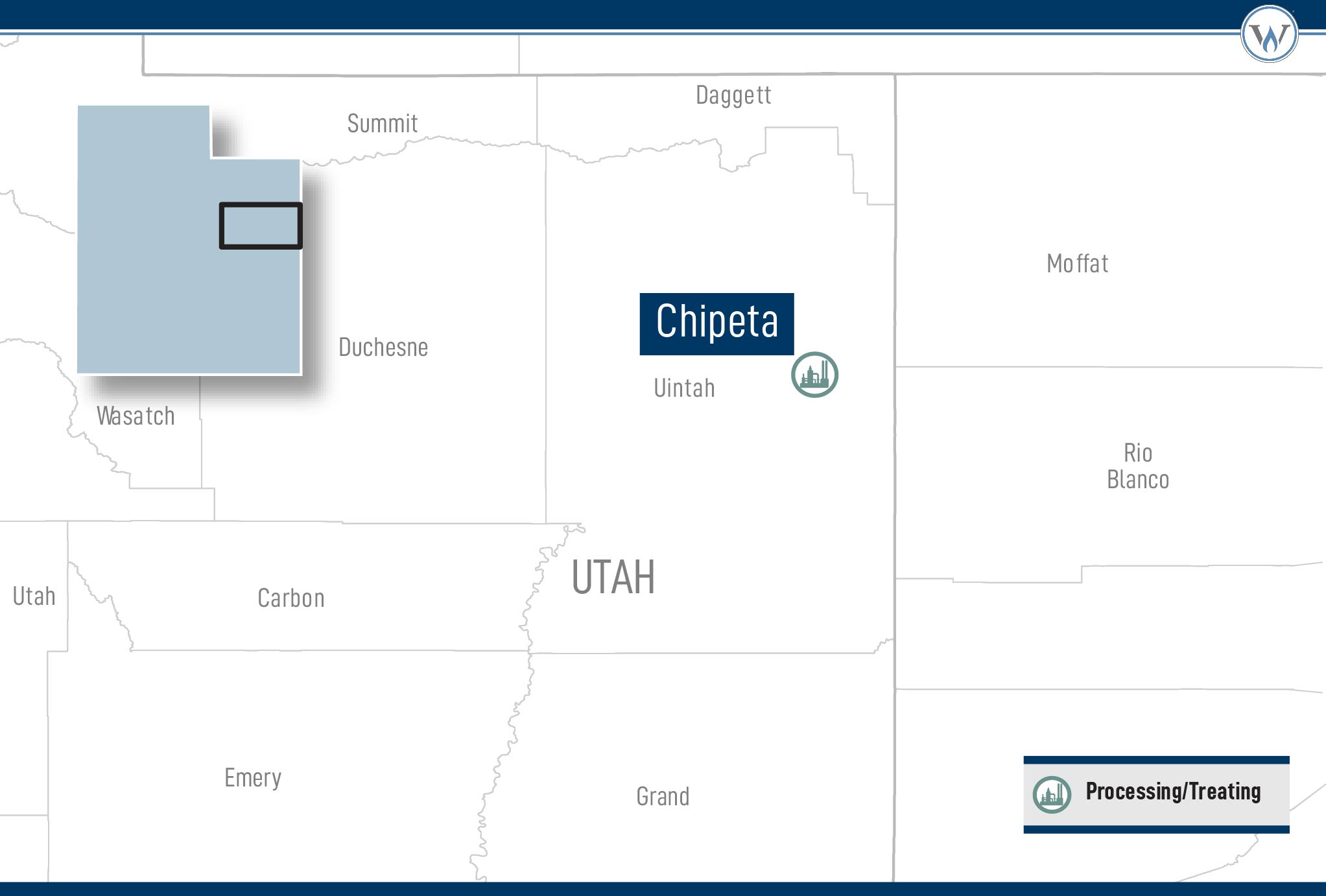

| Chipeta | | Chipeta Processing, LLC, in which we are the managing member of and own a 75% interest. |

| Chipeta LLC agreement | | Chipeta’s limited liability company agreement, as amended and restated as of July 23, 2009. |

| Condensate | | A natural-gas liquid with a low vapor pressure compared to drip condensate, mainly composed of propane, butane, pentane, and heavier hydrocarbon fractions. |

| DBM water systems | | Produced-water gathering and disposal systems in West Texas. |

| Delivery point | | The point where hydrocarbons are delivered by a processor or transporter to a producer, shipper, or purchaser, typically the inlet at the interconnection between the gathering or processing system and the facilities of a third-party processor or transporter. |

| DJ Basin complex | | The Platte Valley, Fort Lupton, Wattenberg, Lancaster, and Latham processing plants, and the Wattenberg gathering system. |

| EBITDA | | Earnings before interest, taxes, depreciation, and amortization. For a definition of “Adjusted EBITDA,” see Reconciliation of Non-GAAP Financial Measures under Part II, Item 7 of this Form 10-K. |

| Equity-investment throughput | | Our share of average throughput from investments accounted for under the equity method of accounting. |

| Exchange Act | | The Securities Exchange Act of 1934, as amended. |

| Floating-Rate Senior Notes due 2023 | | WES Operating’s floating-rate Senior Notes due 2023, which were fully repaid in January 2023. |

| FERC | | The Federal Energy Regulatory Commission. |

| FRP | | Front Range Pipeline LLC, in which we own a 33.33% interest. |

| GAAP | | Generally accepted accounting principles in the United States. |

| General partner | | Western Midstream Holdings, LLC, the general partner of the Partnership. |

| Imbalance | | Imbalances result from (i) differences between gas and NGLs volumes nominated by customers and gas and NGLs volumes received from those customers and (ii) differences between gas and NGLs volumes received from customers and gas and NGLs volumes delivered to those customers. |

| Marcellus Interest | | The 33.75% interest in the Larry’s Creek, Seely, and Warrensville gas-gathering systems and related facilities located in northern Pennsylvania. |

| Mcf, MMcf, MMcf/d | | Thousand cubic feet, million cubic feet, million cubic feet per day. |

| Meritage | | Meritage Midstream Services II, LLC, which was acquired by the Partnership on October 13, 2023. |

| MIGC | | MIGC, LLC. |

| Mi Vida | | Mi Vida JV LLC, in which we own a 50% interest. |

| MLP | | Master limited partnership. |

| Mont Belvieu JV | | Enterprise EF78 LLC, in which we own a 25% interest. |

| Natural-gas liquid(s) or NGL(s) | | The combination of ethane, propane, normal butane, isobutane, and natural gasolines that, when removed from natural gas, become liquid under various levels of pressure and temperature. |

| NYSE | | New York Stock Exchange. |

| Occidental | | Occidental Petroleum Corporation and, as the context requires, its subsidiaries, excluding our general partner. |

| Occidental Merger | | Occidental’s acquisition by merger of Anadarko pursuant to the Occidental Merger Agreement, which closed on August 8, 2019. |

| | | | | | | | |

| Defined Term | | Definition |

| OTTCO | | Overland Trail Transmission, LLC. |

| Panola | | Panola Pipeline Company, LLC, in which we own a 15% interest. |

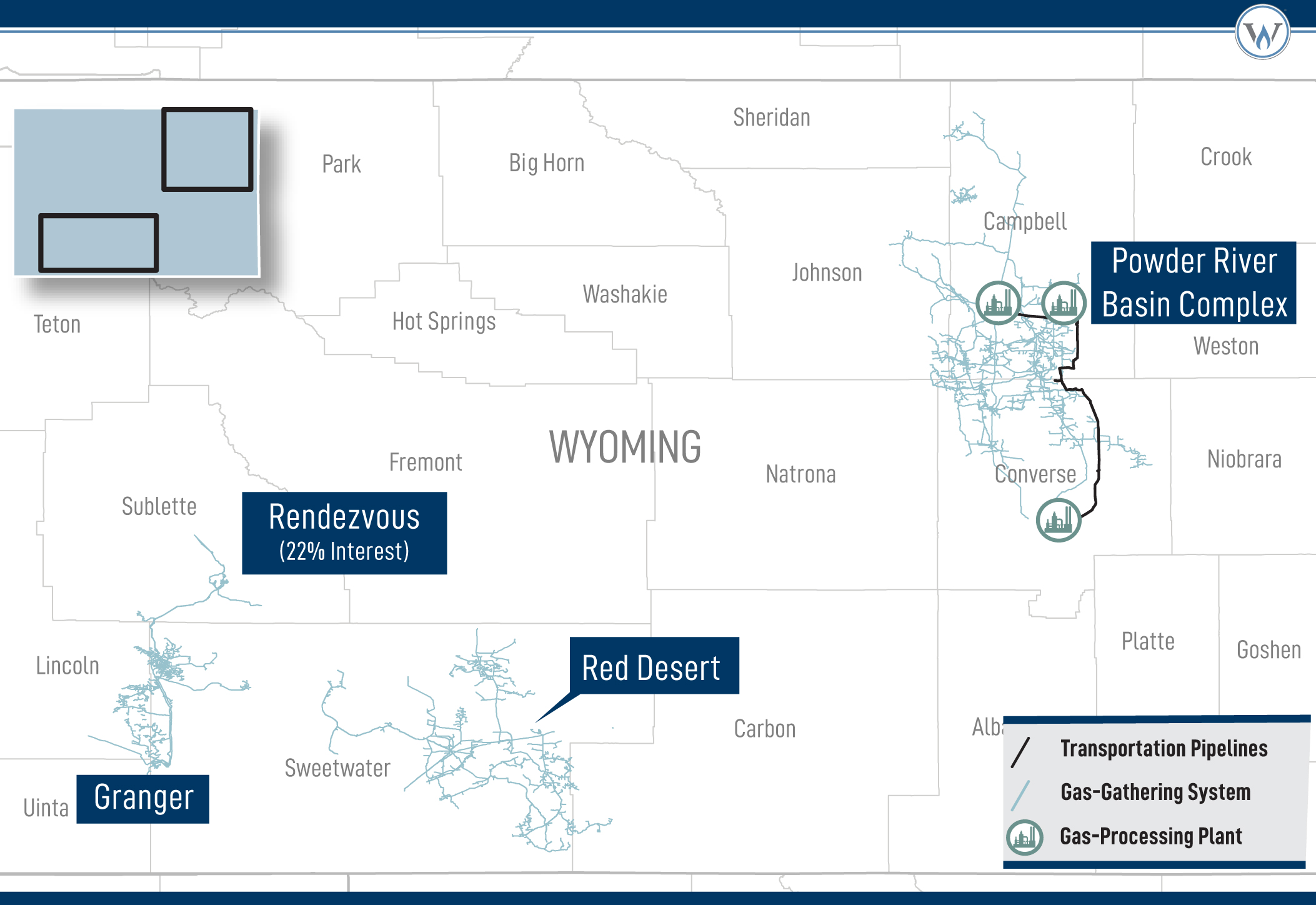

| Powder River Basin complex | | The Hilight system and assets acquired from Meritage, which includes a gathering system, processing plants, and the Thunder Creek NGL pipeline (see Note 3—Acquisitions and Divestitures in the Notes to Consolidated Financial Statements under Part II, Item 8 of this Form 10-K). |

| Produced water | | Byproduct associated with the production of crude oil and natural gas that often contains a number of dissolved solids and other materials found in oil and gas reservoirs. |

| Ranch Westex | | Ranch Westex JV LLC, in which we owned a 50% interest through August 2022, and a 100% interest thereafter (see Note 3—Acquisitions and Divestitures in the Notes to Consolidated Financial Statements under Part II, Item 8 of this Form 10-K). |

| RCF | | WES Operating’s $2.0 billion senior unsecured revolving credit facility. |

| Red Bluff Express | | Red Bluff Express Pipeline, LLC, in which we own a 30% interest. |

| Red Desert complex | | The Red Desert gathering lines and related facilities. |

| Related parties | | Occidental, the Partnership’s equity interests (see Note 7—Equity Investments in the Notes to Consolidated Financial Statements under Part II, Item 8 of this Form 10-K), and the Partnership and WES Operating for transactions that eliminate upon consolidation. |

| Rendezvous | | Rendezvous Gas Services, LLC, in which we own a 22% interest. |

| Residue | | The natural gas remaining after the unprocessed natural-gas stream has been processed or treated. |

| Saddlehorn | | Saddlehorn Pipeline Company LLC, in which we own a 20% interest. |

| SEC | | U.S. Securities and Exchange Commission. |

| Services Agreement | | That certain amended and restated Services, Secondment, and Employee Transfer Agreement, dated as of December 31, 2019, by and among Occidental, Anadarko, and WES Operating GP. |

| Springfield system | | The Springfield gas-gathering system and Springfield oil-gathering system. |

| Stabilization | | The process to reduce the volatility of a liquid hydrocarbon stream by separating very light hydrocarbon gases, methane and ethane in particular, from heavier hydrocarbon components. This process reduces the volatility of the liquids during transportation and storage. |

| Tailgate | | The point at which processed natural gas and/or natural-gas liquids leave a processing facility for end-use markets. |

| TEG | | Texas Express Gathering LLC, in which we own a 20% interest. |

| TEP | | Texas Express Pipeline LLC, in which we own a 20% interest. |

| WES Operating | | Western Midstream Operating, LP, formerly known as Western Gas Partners, LP, and its subsidiaries. |

| WES Operating GP | | Western Midstream Operating GP, LLC, the general partner of WES Operating. |

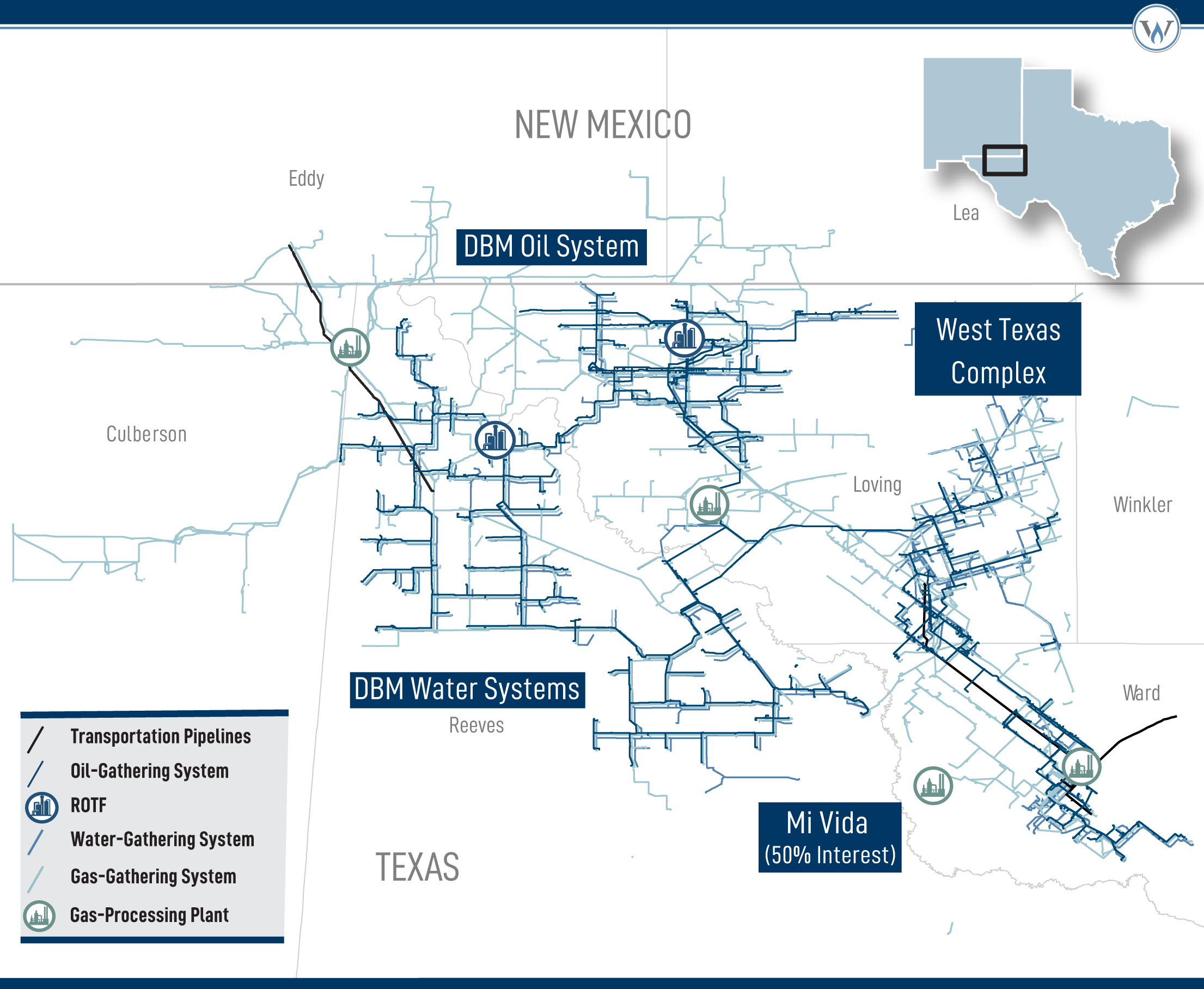

| West Texas complex | | The Delaware Basin Midstream complex and DBJV and Haley systems. |

| WGRAH | | WGR Asset Holding Company LLC, a subsidiary of Occidental. |

| White Cliffs | | White Cliffs Pipeline, LLC, in which we own a 10% interest. |

| Whitethorn LLC | | Whitethorn Pipeline Company LLC, in which we own a 20% interest. |

| Whitethorn | | A crude-oil and condensate pipeline, and related storage facilities, owned by Whitethorn LLC. |

| $1.25 billion Purchase Program | | The $1.25 billion buyback program ending December 31, 2024. The common units may be purchased from time to time in the open market at prevailing market prices or in privately negotiated transactions. |

| $250.0 million Purchase Program | | The $250.0 million buyback program ending December 31, 2021. As of December 31, 2021, the entire $250.0 million authorized program had been fulfilled. |

PART I

Items 1 and 2. Business and Properties

GENERAL OVERVIEW

WES and WES Operating. WES is a Delaware master limited partnership formed in September 2012. Our common units are publicly traded on the NYSE under the symbol “WES.” Our general partner is a wholly owned subsidiary of Occidental. WES Operating is a Delaware limited partnership formed by Anadarko in 2007 to acquire, own, develop, and operate midstream assets. WES owns, directly and indirectly, a 98.0% limited partner interest in WES Operating, and directly owns all of the outstanding equity interests of WES Operating GP, which holds the entire non-economic general partner interest in WES Operating.

WES’s assets include assets owned and ownership interests accounted for by us under the equity method of accounting, through our 98.0% partnership interest in WES Operating, as of December 31, 2023 (see Note 7—Equity Investments in the Notes to Consolidated Financial Statements under Part II, Item 8 of this Form 10-K).

We are engaged in the business of gathering, compressing, treating, processing, and transporting natural gas; gathering, stabilizing, and transporting condensate, NGLs, and crude oil; and gathering and disposing of produced water. In our capacity as a natural-gas processor, we also buy and sell natural gas, NGLs, and condensate on behalf of ourselves and our customers under certain contracts.

Our gathering systems transport raw, or untreated, natural gas from our customers’ wellheads or production facilities to a central location for treating and processing. During processing, unwanted contaminants are removed and natural gas is separated into pipeline quality natural gas, or residue gas, and a mixed NGLs stream that are then transported and marketed to end-use markets or for additional processing. Our crude-oil assets gather raw, high and low vapor-pressure oil at the well site to be processed at oil stabilization facilities before being delivered to crude-oil terminals, storage facilities, long-haul crude-oil pipelines, and refineries. In addition, our produced-water gathering and disposal systems provide the link between well sites or nearby collection points and disposal facilities that (i) remove hydrocarbon products and other sediments from the produced water and re-inject the produced water utilizing permitted disposal wells in compliance with applicable regulations or (ii) sell the produced water to third parties to be treated and recycled.

Available information. We electronically file our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and other documents with the SEC under the Exchange Act. From time to time, we may also file registration and related statements with the SEC pertaining to equity or debt offerings.

We provide access free of charge to all of these SEC filings, as soon as reasonably practicable after filing or furnishing such materials with the SEC, on our website located at www.westernmidstream.com. The public may also obtain such reports from the SEC’s website at www.sec.gov.

Our Corporate Governance Guidelines, Code of Ethics and Business Conduct, Partner Code of Conduct, and the charters of the Audit Committee, the Special Committee, the ESG Committee, and the Compensation Committee of our Board are available on our website. We will also provide, free of charge, a copy of any of our governance documents listed above upon written request to our general partner’s secretary at our principal executive office. Our principal executive office is located at 9950 Woodloch Forest Drive, Suite 2800, The Woodlands, TX 77380. Our telephone number is 346-786-5000.

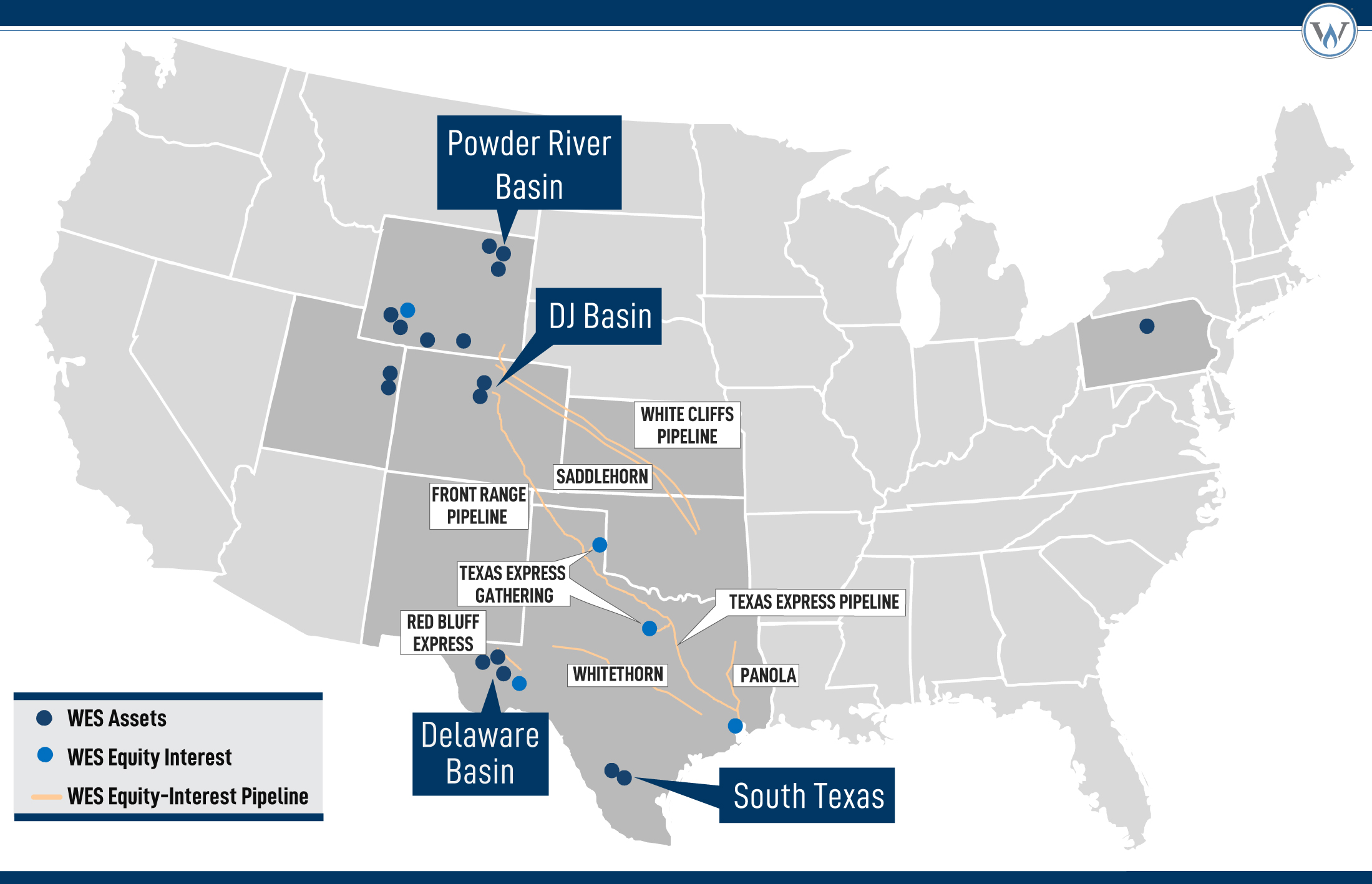

ASSETS AND AREAS OF OPERATION

As of December 31, 2023, our assets and investments consisted of the following:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Wholly

Owned and

Operated | | Operated

Interests | | Non-Operated

Interests | | Equity

Interests | | |

Gathering systems (1) | | 18 | | | 2 | | | 3 | | | 1 | | | |

| Treating facilities | | 38 | | | 3 | | | — | | | — | | | |

| Natural-gas processing plants/trains | | 24 | | | 3 | | | — | | | 3 | | | |

| NGLs pipelines | | 3 | | | — | | | — | | | 5 | | | |

| Natural-gas pipelines | | 6 | | | — | | | — | | | 1 | | | |

| Crude-oil pipelines | | 3 | | | 1 | | | — | | | 3 | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

_________________________________________________________________________________________

(1)Includes the DBM water systems.

These assets and investments are located in Texas, New Mexico, the Rocky Mountains (Colorado, Utah, and Wyoming), and North-central Pennsylvania. The following table provides information regarding our assets by geographic region, as of and for the year ended December 31, 2023:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Area | | Asset Type | | Miles of Pipeline (1) | | Compression (1) (2) | | Processing or Treating Capacity (MMcf/d) (1) | | Processing, Treating, or Disposal Capacity (MBbls/d) (1) | | Average Throughput for Natural-Gas Assets (MMcf/d) (3) | | Average Throughput for Crude-Oil and NGLs Assets (MBbls/d) (3) | | Average Throughput for Produced-Water Assets (MBbls/d) (3) |

| | | | | | | |

| | | Horsepower | | % Electric Driven | | | | | |

| Texas / New Mexico | | Gathering, Processing, Treating, and Disposal | | 4,280 | | 896,951 | | 33 | % | | 2,040 | | 2,448 | | 2,050 | | | 289 | | | 1,029 | |

| | Transportation | | 1,978 | | — | | | — | | | — | | | — | | | 324 | | | 220 | | | — | |

| Rocky Mountains | | Gathering, Processing, and Treating | | 7,147 | | 673,362 | | | 50 | % | | 3,160 | | | 221 | | | 1,986 | | | 71 | | | — | |

| | Transportation | | 2,243 | | — | | | — | | | — | | | — | | | 113 | | | 85 | | | — | |

| North-central Pennsylvania | | Gathering | | 146 | | 15,180 | | | — | % | | — | | | — | | | 120 | | | — | | | — | |

| Total | | | | 15,794 | | 1,585,493 | | | 39 | % | | 5,200 | | | 2,669 | | | 4,593 | | | 665 | | | 1,029 | |

_________________________________________________________________________________________

(1)All system metrics are presented on a gross basis and include owned and leased compressors at certain facilities. Includes horsepower associated with liquid pump stations. Includes bypass capacity at the DJ Basin and West Texas complexes.

(2)Excludes compression horsepower for transportation.

(3)Includes throughput for all assets owned and ownership interests accounted for by us under the equity method of accounting. For further details see Properties below.

Our operations are organized into a single operating segment that engages in gathering, compressing, treating, processing, and transporting natural gas; gathering, stabilizing, and transporting condensate, NGLs, and crude oil; and gathering and disposing of produced water. See Part II, Item 8 of this Form 10-K for disclosure of revenues and operating income (loss) for the years ended December 31, 2023, 2022, and 2021, and total assets for the years ended December 31, 2023 and 2022.

ACQUISITIONS AND DIVESTITURES

Meritage. In October 2023, we closed on the acquisition of Meritage for $885.0 million (subject to certain customary post-closing adjustments) funded with cash, including proceeds from our $600.0 million senior note issuance in September 2023 and borrowings on the RCF.

Cactus II. In November 2022, we sold our 15.00% interest in Cactus II to two third parties for $264.8 million, which includes a $1.8 million pro-rata distribution through closing. Total proceeds were received during the fourth quarter of 2022, resulting in a net gain on sale of $109.9 million that was recorded as Gain (loss) on divestiture and other, net in the consolidated statements of operations.

Ranch Westex. In September 2022, we acquired the remaining 50% interest in Ranch Westex from a third party for $40.1 million. Subsequent to the acquisition, (i) we are the sole owner and operator of the asset, (ii) Ranch Westex is no longer accounted for under the equity method of accounting, and (iii) the Ranch Westex processing plant is included as part of the operations of the West Texas complex.

See Note 3—Acquisitions and Divestitures and Note 13—Debt and Interest Expense under Part II, Item 8 of this Form 10-K.

STRATEGY

Our primary business objective is to create long-term value for our unitholders through continued delivery of profitable operations and return of capital to stakeholders over time. Our foundational principles of operational excellence, superior customer service, and sustainable operations influence our decision making and long-term strategy. To accomplish our primary business objective, we intend to execute the following strategy:

•Capitalizing on core assets and organic growth opportunities. We intend to grow certain of our systems organically over time by meeting our customers’ midstream service needs that arise from drilling activity in our areas of operation. We continually pursue economically attractive organic business development and expansion opportunities in existing or new areas of operation that allow us to leverage our infrastructure, operating expertise, and customer relationships, to meet new or increased demand of our services.

•Controlling our operating, capital, and administrative costs. We intend to maintain our focus on generating efficiencies between our commercial, engineering, and operations teams, as well as optimizing and maximizing the operability of our existing assets to realize cost and capital savings. We expect to continue to drive operational efficiencies and sustainable cost savings throughout the organization.

•Optimizing the return of cash to stakeholders. We intend to operate our assets and make strategic capital decisions that optimize our leverage levels consistent with investment-grade metrics in our sector while returning additional excess cash flow to stakeholders that enhances overall return.

•Generating stable cash flows. We intend to continue generating low-volatility cash flows through commodity-price cycles by pursuing fee-based contracts with risk-reducing protections in place, such as minimum-volume commitments and cost-of-service provisions.

COMPETITIVE STRENGTHS

We believe that we are well positioned to successfully execute our strategy and achieve our primary business objective because of the following competitive strengths:

•Substantial presence in basins with historically strong producer economics. Our core operating areas are in the Delaware, DJ, and Powder River Basins, which historically have seen robust producer activity and are considered to have some of the most favorable producer returns for onshore North America. Our assets in these areas are capable of servicing hydrocarbon production that contains natural gas, crude oil, condensate, and NGLs. Our systems in the Delaware Basin also include significant produced-water takeaway capacity, which makes us a uniquely positioned, full-service midstream provider in the basin.

•Well-positioned and well-maintained assets. We believe that our large-scale asset portfolio, located in geographically diverse areas of operation, provides us with opportunities to expand and attract additional volumes to our systems from multiple productive reservoirs. Moreover, our portfolio consists of high-quality, well-maintained assets for which we have implemented modern processing, treating, measurement, and operating technologies. We believe our forward-looking facility designs enable customers to reduce their environmental impact and enhance operational efficiency.

•Sustainability and safety. Our culture of safety and focus on protecting the environment inform decision making throughout the organization. We strive to minimize emissions by thoughtfully designing, constructing, and operating our assets, and collaborating with state and federal regulatory agencies and environmental groups, producers, and industry partners to reduce or offset emissions in our operations. Through our company-wide safety initiatives, we are committed to the safe and efficient delivery of energy for our customers, with an emphasis on true care and concern for each other, a standardized safety training program, and significant investments in asset integrity.

•Commodity-price and volumetric-risk mitigation. We believe a substantial majority of our cash flows are protected from direct exposure to commodity-price volatility, as 95% of our wellhead natural-gas volume (excluding equity investments) and 100% of our crude-oil and produced-water throughput (excluding equity investments) were serviced under fee-based contracts for the year ended December 31, 2023. This type of contract provides us with a relatively stable revenue stream that is not subject to direct commodity-price risk, except to the extent that (i) actual recoveries differ from contractual recoveries under certain of our processing agreements or (ii) we retain and sell drip condensate that is recovered during the gathering of natural gas from the wellhead or production facility. In addition, we mitigate volumetric risk through minimum-volume commitments and cost-of-service contract structures. For the year ended December 31, 2023, we had approximately 2.6 Bcf/d for our natural-gas assets (excluding equity investments), approximately 465 MBbls/d for our crude-oil and NGLs assets (excluding equity investments), and approximately 860 MBbls/d for our produced-water assets that were supported by either minimum-volume commitments with associated deficiency payments or cost-of-service commitments.

•Liquidity to pursue expansion and acquisition opportunities. We believe our operating cash flows, borrowing capacity, long-dated debt maturity profile, long-term relationships, and reasonable access to capital markets provide us with the liquidity to competitively pursue acquisition and expansion opportunities and to execute our strategy across capital-market cycles. As of December 31, 2023, there was $1.4 billion in effective borrowing capacity under the RCF after taking into account the $613.9 million of outstanding commercial paper borrowings, for which we maintain availability under the RCF as support for our commercial paper program.

•Affiliation with Occidental. We continue to optimize our assets by sizing and planning growth initiatives in a manner that highlights the strength of our asset portfolio to service Occidental’s upstream development plans. Our relationship with Occidental enables us to pursue more capital-efficient projects that enhance the overall value of our business. See WES and WES Operating’s Relationship with Occidental Petroleum Corporation below.

We plan to effectively leverage our competitive strengths to successfully implement our business strategy. However, our business involves numerous risks and uncertainties that may prevent us from achieving our primary business objective. For a more complete description of the risks associated with our business, read Risk Factors under Part I, Item 1A of this Form 10-K.

WES AND WES OPERATING’S RELATIONSHIP WITH OCCIDENTAL PETROLEUM CORPORATION

The officers of our general partner manage our operations and activities under the direction and supervision of the Board of our general partner, which is a wholly owned subsidiary of Occidental. Occidental is among the largest independent oil and gas exploration and production companies in the world. Occidental’s upstream oil and gas business explores for, develops, and produces crude oil and condensate, NGLs, and natural gas.

As of December 31, 2023, Occidental held (i) 185,181,578 of our common units, representing a 47.7% limited partner interest in us, (ii) through its ownership of the general partner, 9,060,641 general partner units, representing a 2.3% general partner interest in us, and (iii) a 2.0% limited partner interest in WES Operating through its ownership of WGRAH, which is reflected as a noncontrolling interest within our consolidated financial statements. As of December 31, 2023, Occidental held 48.8% of our outstanding common units.

For the year ended December 31, 2023, 59% of Total revenues and other, 34% of our throughput for natural-gas assets (excluding equity-investment throughput), 86% of our throughput for crude-oil and NGLs assets (excluding equity-investment throughput), and 78% of our throughput for produced-water assets were attributable to production owned or controlled by Occidental. While Occidental is our contracting counterparty, these arrangements with Occidental include not just Occidental-produced volumes, but also, in some instances, the volumes of other working-interest owners of Occidental who rely on our facilities and infrastructure to bring their volumes to market. In addition, Occidental provides dedications, minimum-volume commitments with associated deficiency payments, and/or cost-of-service commitments under certain of our contracts.

Historically, we sold a significant amount of our natural gas and NGLs to Anadarko Energy Services Company (“AESC”), Occidental’s marketing affiliate. In addition, we purchased natural gas from AESC pursuant to purchase agreements. While we still have some marketing agreements with affiliates of Occidental, on January 1, 2021, we began marketing and selling substantially all our crude oil and residue gas, and a majority of our NGLs, directly to third parties.

Pursuant to the Services Agreement entered into on December 31, 2019, Occidental has performed certain centralized corporate functions for the Partnership and WES Operating. Most of the administrative and operational services previously provided by Occidental fully transitioned to the Partnership by December 31, 2021, with certain limited transition services remaining in place pursuant to the terms of the Services Agreement.

Although we believe our relationship with Occidental enables us to pursue more capital-efficient projects that enhance the overall value of our business, it is also a source of potential conflicts. For example, Occidental is not restricted from competing with us. See Risk Factors under Part I, Item 1A and Certain Relationships and Related Transactions, and Director Independence under Part III, Item 13 of this Form 10-K for more information.

PROPERTIES

The following sections describe in more detail the services provided by our assets in our areas of operation as of December 31, 2023.

GATHERING, PROCESSING, TREATING, AND DISPOSAL

Overview - Texas and New Mexico

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Location | | Asset | | Type | | Processing / Treating Plants | | Processing / Treating Capacity (MMcf/d) (1) | | Processing / Treating / Disposal Capacity (MBbls/d) | | | | Compression Horsepower (2) | | Gathering Systems | | Pipeline Miles (3) |

| West Texas / New Mexico | | West Texas complex (4) | | Gathering, Processing, & Treating | | 15 | | | 1,640 | | | 53 | | | | | 624,074 | | | 3 | | | 1,914 | |

| West Texas | | DBM oil system (5) | | Gathering & Treating | | 16 | | | — | | | 310 | | | | | 12,648 | | | 1 | | | 654 | |

| West Texas | | DBM water systems | | Gathering & Disposal | | — | | | — | | | 1,825 | | | | | 92,395 | | | 5 | | | 799 | |

| West Texas | | Mi Vida (6) | | Processing | | 1 | | | 200 | | | — | | | | | 20,000 | | | — | | | — | |

| East Texas | | Mont Belvieu JV (7) | | Processing | | 2 | | | — | | | 170 | | | | | — | | | — | | | — | |

| South Texas | | Brasada complex | | Gathering, Processing, & Treating | | 3 | | | 200 | | | 15 | | | | | 29,400 | | | 1 | | | 58 | |

| South Texas | | Springfield system (8) | | Gathering & Treating | | 3 | | | — | | | 75 | | | | | 118,434 | | | 2 | | | 855 | |