UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended May 31, 2014

[ ] TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from [ ] to [ ]

Commission file number 000-53461

MANTRA VENTURE GROUP LTD.

(Exact name of registrant as specified in its charter)

| Nevada | 26-0592672 |

| (State or other jurisdiction of incorporation or | (I.R.S. Employer Identification No.) |

| organization) | |

| 1562 128th Street, Surrey, British Columbia, Canada | V4A 3T7 |

| (Address of principal executive offices) | (Zip Code) |

| Registrant's telephone number, including area code: | (604) 560-1503 |

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange On Which Registered |

| N/A | N/A |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.00001 par value

(Title of class)

Indicate by check mark if the registrant is a well-known

seasoned issuer, as defined in Rule 405 the Securities Act.

Yes

[ ] No [X]

Indicate by check mark if the registrant is not required to

file reports pursuant to Section 13 or Section 15(d) of the Act

Yes

[ ] No [X]

Indicate by check mark whether the registrant: (1) has filed

all reports required to be filed by Section 13 or 15(d) of the Securities

Exchange Act of 1934 during the preceding 12 months (or for such shorter period

that the registrant was required to file such reports) and (2) has been subject

to such filing requirements for the last 90 days.

Yes

[X] No [ ]

Indicate by check mark whether the registrant has submitted

electronically and posted on its corporate Website, if any, every Interactive

Data File required to be submitted and posted pursuant to Rule 405 of Regulation

S-K (§229.405 of this chapter) during the preceding 12 months (or for such

shorter period that the registrant was required to submit and post such files).

Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [ ] |

| Non-accelerated filer [ ] | Smaller reporting company [X] |

Indicate by check mark whether the registrant is a shell

company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No

[X]

The aggregate market value of Common Stock held by non-affiliates of the Registrant on November 29, 2013 was $2,138,003 based on a $0.10 average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock as of the latest practicable date.

70,692,692 common shares as of September 12, 2014.

DOCUMENTS INCORPORATED BY REFERENCE

None.

Table of Contents

3

PART I

Item 1. Business

FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements. These statements relate to future events or our future financial performance. In some cases, you can identify forward-looking statements by terminology such as “may”, “will”, “should”, “expects”, “plans”, “anticipates”, “believes”, “estimates”, “predicts”, “potential” or “continue” or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors that may cause our or our industry's actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable laws, including the securities laws of the United States, we do not intend to update any of the forward-looking statements so as to conform these statements to actual results.

In this annual report, unless otherwise specified, all dollar amounts are expressed in United States dollars. All references to “US$” refer to United States dollars and all references to “common stock” refer to the common shares in our capital stock.

As used in this annual report, the terms “we”, “us”, “our” and “our company” mean Mantra Venture Group Ltd. and our wholly owned subsidiaries Carbon Commodity Corporation, Mantra China Inc., Mantra China Limited, Mantra Media Corp., Mantra NextGen Power Inc., and Mantra Wind Inc., as well as our majority owned subsidiary Climate ESCO Ltd. and Mantra Energy Alternatives Ltd., unless otherwise indicated.

Description of Business

We were incorporated in Nevada on January 22, 2007. On December 8, 2008 we continued our corporate jurisdiction out of the state of Nevada and into the Province of British Columbia, Canada. Our principal offices are located at 1562 128th Street, Surrey, British Columbia, Canada, V4A 3T7. Our telephone number is (604) 560-1503. Our fiscal year end is May 31.

We are building a portfolio of companies and technologies that mitigate negative environmental and health consequences that arise from the production of energy and the consumption of resources.

Our mission is to develop and commercialize alternative energy technologies and services to enable the sustainable consumption, production and management of resources on residential, commercial and industrial scales. To carry out our business strategy we intend to acquire or license from third parties technologies that require further development before they can be brought to market. We also intend to develop such technologies ourselves, and we anticipate that to complete commercialization of some technologies we will enter into joint ventures, partnerships, or other strategic relationships with third parties who have expertise that we may require. We also plan to enter into formal relationships with consultants, contractors, retailers and manufacturers who specialize in the areas of environmental sustainability in order to carry out our online retail strategy.

We are a development stage company that has only recently begun generating revenue from our operations. At this time we own a technology for the electro-reduction of carbon dioxide and have the exclusive world license for a mixed-reactant fuel cell. Since our inception, we have incurred operational losses and we have completed several rounds of financing to fund our operations.

4

We carry on our business through our subsidiary, Mantra Energy Alternatives Ltd. (“MEA”), through which we identify, acquire, develop and market technologies related to alternative energy production, greenhouse gas emissions reduction and resource consumption reduction;

We also have a number of inactive subsidiaries which we plan to engage in various business activities in the future.

Effective June 19, 2012, our company’s subsidiary, MEA, entered into a service contract with PowerTech Labs Inc., whereby PowerTech assisted MEA in the evaluation and the development of our ERC(electro-reduction of carbon dioxide) system. As compensation, PowerTech was paid $171,000 plus the cost of materials. The carbon enrichment unit proved successful at the proof-of-concept scale, and the bench-scale version was then designed and built. This unit, too, proved successful in its goal of enriching a dilute (roughly 20%) stream of carbon dioxide to over 80%. The program has now been completed.

On October 28, 2008, we entered into a convertible debenture with StichtingAdministratiekantoor Carlos Bijl for a principal amount of $150,000 and an annual interest rate of 10%. Stichting started an action in the Supreme Court of British Columbia for non-payment of the convertible debenture.

We entered into a settlement agreement with Stichting dated July 16, 2012, pursuant to which:

- the due date of the Convertible Debenture would be extended to April 11, 2013;

- within 5 business days we were to pay $43,890 representing net interest to and including September 30, 2012, less $15,000 we forwarded to Stichting on February 16, 2012;

- commencing on October 31, 2012 we were to pay accrued monthly interest at 10% per annual until April 11, 2013 (this amount has been paid);

- we were to pay a $10,000 premium on the $150,000 principal of the convertible debenture payable by April 11, 2013.

We entered into an agreement dated April 29, 2013 with Stichting to amend the settlement agreement, pursuant to which:

- the due date of the convertible debenture was extended from April 11, 2013 to September 15, 2013;

- upon execution of the amendment to the settlement agreement, we paid $6,836 in full satisfaction of future interest payable on the convertible debenture from April 1, 2013 to September 15, 2013; and

- we granted to Stichting options to purchase up to 100,000 common shares of our company, exercisable for a period of 24 months from the time of grant and at the exercise price of $0.12 per common share.

On November 15, 2013, we entered into a second settlement agreement amendment with Stichting, pursuant to which we agreed to pay interest of $4,438 and commencing February 1, 2014, to make monthly payments of $10,000 on the outstanding principal and interest. Our company has made monthly payments for a total of $50,000 as at May 31, 2014.

On July 31, 2012, our subsidiary, MEA, entered into a master services agreement with Tekion (Canada), Inc. MEA’s ERC technology converts carbon dioxide (CO2) in stack gases to a formate salt which can then be further processed into formic acid or used to operate a fuel cell to generate power. MEA engaged PowerTech Labs to do further engineering on the system. In order to get this technology to commercialization, Tekion proposed a program that ran parallel to the PowerTech program to help Mantra with some of the critical issues regarding this process. The program has now been completed.

Also on July 31, 2012, MEA entered into a statement of work with Tekion setting out the work summary, deliverables, budgets and timelines in several stages, which have now all been completed.

On January 8, 2013, our company entered into an employment agreement with our officer and director, Larry Kristof, whereby Larry Kristof has agreed to provide services as chief executive officer of our company for a period of two years. As compensation, pursuant to the terms of the employment agreement, Larry Kristof will receive an annual salary of $60,000, payable in equal monthly installments. The employment agreement may be terminated by Larry Kristof, for any reason, by providing at least three month’s advance written notice to our company.

5

Also on January 8, 2013, our company’s subsidiary, MEA, entered into an employment agreement with Larry Kristof, whereby Larry Kristof has agreed to provide services as chief executive officer of MEA for a period of two years. As compensation, pursuant to the terms of the employment agreement, Larry Kristof will receive an annual salary of $60,000, payable in equal monthly installments. The employment agreement may be terminated by Larry Kristof, for any reason, by providing at least three month’s advance written notice to our company.

On March 13, 2013, we entered into a letter of engagement with BC Research Inc. pursuant to which we engaged BC Research to design and engineer a proposed demonstration unit of our company’s ERC technology. The scope of work will include determining power requirements for the planned ERC unit, and producing an equipment list, a functional description of equipment and specification, electrical drawings, a drawing package for potential suppliers, and a simplified 3D model of the system. The objective of the engagement is to determine the fabrication and operating costs of the demonstration unit to within a 25% variance. It is estimated that completion of the planned work will be achieved within 15 weeks from the date of our company’s purchase order and payment of a CDN$30,000 retainer. Our company compensated BC Research based on its customary hourly rates. BC Research completed this project at a cost of $161,759and our company retains all intellectual property resulting from the services performed.

Concurrently with the engagement of B.C. Research, our company, through our subsidiary, MEA, has entered into a sublease agreement with B.C. Research, dated as at February 25, 2013, for the sublease of a workshop and office space of approximately 600 square feet located in Burnaby, British Columbia. The term of the sublease continued until March 1, 2014 at a cost of CDN$18,720 (CDN$1,560 monthly). The sublease has not been renewed. We moved out of the facility on May 31, 2014 and now lease our own laboratory space in Vancouver, British Columbia at a cost of approximately $3,600 per month.

On May 7, 2013, we entered into a director agreement with Patrick Dodd. As compensation under the director agreement, our company granted stock options to Mr. Dodd to purchase up to 200,000 shares of our common stock at a price of $0.10 per share. The stock options shall terminate for exercise the earlier of May 7, 2015 or 180 calendar days after resignation of Mr. Dodd as director, in which case, 100,000 stock options shall remain available to Mr. Dodd at an exercise price of $0.10 until November 7, 2015. On March 1, 2014, we amended this agreement which granted Mr. Dodd options to purchase 150,000 common shares of our company at $0.02 per common share. On August 25, 2014, Mr. Dodd notified us and provided payment for the exercise of the options.

Collaboration with Alstom (Switzerland) Ltd.

On June 24, 2013, through our majority owned subsidiary, MEA our company entered into an agreement with Alstom (Switzerland) Ltd. concerning the joint research and development projects relating to (1) a pilot plant for the conversion of carbon dioxide to formate at a Lafarge cement plant (the “Lafarge pilot project”); and (2) the development of processes for the conversion of carbon dioxide to other valuable chemicals.

Pursuant to the agreement with Alstom, MEA and Alstom will co-operate in one or more research and development projects related to MEA’s ERC technology. Prospective projects will be associated with the development of technologies and processes for the conversion of CO2 to chemical products and the investigation of the feasibility of scale-up and commercialization of these processes. Prior to undertaking any research and development project under the agreement, MEA and Alstom will mutually agree to special terms and conditions governing the purpose, aims and objectives of any such project, including technical descriptions, the designation of work phases and project managers, and the allocation of responsibilities and costs between the parties. The commencement of any work phase for any project will be at the sole discretion of Alstom.

Intellectual Property Management

MEA and Alstom also will establish an intellectual property committee to oversee and manage all intellectual property issues and activities resulting from the agreement, including the protection of any new intellectual property. Each party will have exclusive right and discretion to prosecute all patents and patent applications resulting from its work on any project. The parties will jointly prosecute any intellectual property in jointly-owned results. Alstom will have the additional option under the agreement to acquire an exclusive license to intellectual property created by MEA under the agreement, and to a license to MEA’s ERC technology as may be reasonably required to exploit intellectual property assumed by Alstom. The agreement does not affect ownership of any underlying intellectual property of either party.

6

Lafarge Pilot Project and Carbon Dioxide to Alternative Products

The agreement with Alstom will remain valid for 5 years or the completion of the last active project, whichever last occurs, and may be extended at any time by the written agreement of both parties. The first joint research and development project under the agreement is the Lafarge pilot project, which plans for the design, construction, and installation of a pilot plant for the conversion of 100 kg/day carbon dioxide to formate, followed by a commercialization scale-up study. Alstom’s contribution to the Lafarge pilot plant project will be approximately CDN$250,000 for in-kind services. A second integrated research and development project will study carbon dioxide conversion to alternative chemical products by electrochemical reduction, with a focus on catalyst materials and lifetime. Alstom’s contribution to the alternative products project will be approximately CDN$190,375 for Phase 1. For Phases 2 through 4 Alstom’s planed, but not committed, contribution is estimated at CDN$456.125 and the final amount of Phase 5 will be determined. Mantra and Alstom are actively seeking external funding to support the execution of the projects.

On July 1, 2013, we entered into a consulting agreement with BC0798465 Ltd., whereby BC0798465 Ltd. agreed to provide Mr. Colin Oloman for consulting services to our scientific advisory board for an indefinite term. In consideration for such consulting services, we have agreed to compensate BC0798465 Ltd. for Mr. Oloman’s services at CDN$150 per hour and 300,000 options to acquire 300,000 common shares of our capital stock, previously registered on a Form S-8 registration statement, filed with the United States Securities and Exchange Commission on November 24, 2009, at a purchase price of $0.20 per share for a period of two years.

On October 10 and October 17, 2013, our company’s subsidiary, MEA, entered into employment agreements with Amin Aziznia and Sona Kazemi, whereby Mr. Aziznia and Mrs. Kazemi have each agreed to perform services as senior process engineers of MEA for a term of one year. As compensation for services rendered, Mr. Aziznia and Mrs. Kazemi shall each receive base gross remuneration of $65,000 per annum with an increase to $70,000 per annum subject to receipt by MEA of an Industrial Research and Development Fellowship from the Natural Sciences and Engineering Research Council of Canada (the “NSERC IRDF Grant”). The compensation is payable in twelve equal monthly installments. In addition, we have agreed to grant to each of Mr. Aziznia and Ms. Kazemi, 100,000 stock options to acquire up to 100,000 common shares of our company at a purchase price of $0.10 per share. The options will, when granted, be non-transferrable, vest immediately and expire upon the earlier of 24 months, or upon termination of the employment agreements. The agreements would terminate if MEA did not receive the NSERC IRDF Grant. The NSERC IRDF Grants have been granted and are effective as of August 1, 2014.

On March 1, 2014, we entered into an agreement with Small Cap Invest Ltd., a Frankfurt-based financial service company. Serving as a contractor, Small Cap Invest will develop investor and public relations across Europe, and use an impressive breadth of experience to ultimately facilitate the penetration and development of Mantra’s technologies in European markets.

On March 13, 2014, we entered into a consulting agreement with DC Consulting LLC (“DCC”), dated effective March 13, 2014, whereby DCC has agreed to provide our company with various services including management consulting, business advisory, shareholder information and public relations which commenced March 17, 2014 and terminates on March 16, 2015. The agreement provides for a monthly cash payment in the amount of $7,250 per month and the issuance of 25,000 shares of our company’s common stock upon execution of the agreement and 20,000 shares of our company’s common stock per month for months 2 to 12.

Effective March 25, 2014, our company, through our subsidiary MEA, entered into letter of engagement with BC Research Inc. pursuant to which BC Research has undertaken to design, engineer and build our company’s ERC demonstration unit. Based in Vancouver, British Columbia, BC Research is the technology commercialization and innovation center of NORAM Engineering and Constructors Ltd., a globally active firm which provides innovative solutions and engineering and equipment packages to the chemical, pulp and paper, minerals processing and electrochemical industries.

7

The BC Research facility houses a wet chemical laboratory and over 10,000 square feet of pilot plant space, and is where our company is performing its ongoing research and development work on ERC. Pursuant to the letter of engagement BC Research (in collaboration with NORAM) has been engaged to engineer, design and build our company’s ERC demonstration unit for the estimated cost of CDN$360,000 (approximately $326,000). Engineering and design services for the project will be provided primarily by NORAM engineers and scientists. Our company has delivered the first payment installment of CDN$190,000 to BC Research and project work has commenced and is estimated to take approximately 24 weeks. We may terminate the agreement at any time and will retain all prior-owned and new intellectual property related to the project.

On August 22, 2014, we entered into an agreement with Green Baron Ventures Inc., doing business as Evergreen Marketing, Inc. Pursuant to the terms of this agreement, Green Baron is to provide us with investor relation services. In exchange for the service provided by Green Baron, we compensated Green Baron with a total of USD$3,500 and of 12,000 common shares of our company.

Electro Reduction of Carbon Dioxide (“ERC”)

On November 2, 2007, through our subsidiary, Mantra Energy, we entered into a technology assignment agreement with 0798465 BC Ltd. whereby we acquired 100% ownership in and to a certain chemical process for the electro-reduction of carbon dioxide as embodied by and described in the following patent cooperation treaty application:

| Country |

Application

Number |

File Date |

Status |

| Patent Cooperation Treaty (PCT) | W02207 | 10/13/2006 | PCT |

On January 14, 2014, our company and Mantra Energy, received acceptance of our primary ERC patent application in Australia. This patent application covers the reactor and process for the electrochemical conversion of carbon dioxide to chemical products, and is a crucial component of Mantra's intellectual property portfolio. The Australian patent was officially issued on May 1, 2014.

As of the date of this annual report, we have been awarded the following patents:

| Country | Patent Number | Patent Date | Name of Patent |

| India | 251493 | March 20, 2012 | “An Electrochemical Process for Reducing of Carbon Dioxide” |

| China | ZL 2006 8 0037810.8 | May 8, 2013 | “Continuous Co-Current Electrochemical Reduction of Carbon Dioxide” |

| Australia | 2012202601 | May 1, 2014 | “Continuous Co-Current Electrochemical Reduction of Carbon Dioxide” |

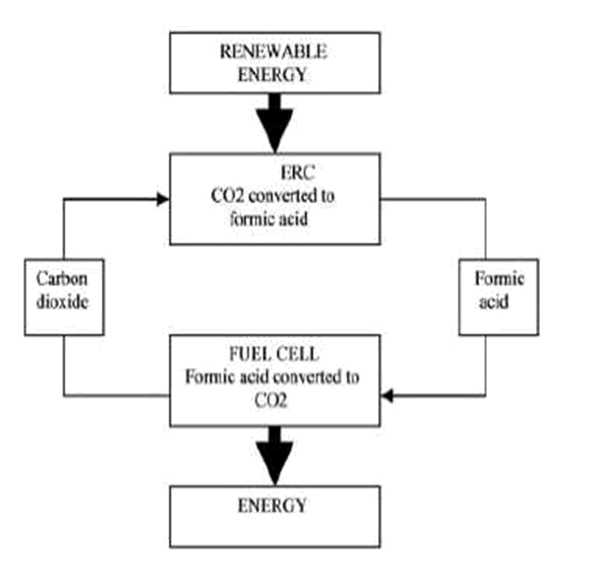

The reactor at the core of the chemical process, referred to as the electrochemical reduction of carbon dioxide (CO2), or ERC, has been proven functional through small scale prototype trials and limited scale-up trials. ERC offers a possible solution to reduce the impact of CO2 on Earth’s environment by converting CO2 into chemicals with a broad range of commercial applications, including a fuel for a next generation of fuel cells. Powered by electricity, the ERC process combines captured carbon dioxide with water to produce materials, such as formic acid, formate salts, oxalic acid and methanol, that are conventionally obtained from the thermo-chemical processing of fossil fuels. However, while thermo-chemical reactions must be driven at relatively high temperatures that are normally obtained by burning fossil fuels, ERC operates at near ambient conditions and is driven by electric energy that can be taken from an electric power grid supplied by hydro, wind, solar or nuclear energy.

8

In a fuel cell a fuel is oxidized and an oxidant reduced, resulting in the production of an electric current to drive and external load. Because ERC can be used to produce such a fuel from CO2, a regenerative fuel cell cycle can be developed using the technology in conjunction with an appropriate fuel cell. As shown in the figure, this concept can be used to provide energy storage, whereby clean electricity produced by intermittent renewable resources can be stored and its supply correlated with demand.

ERC has been shown to produce a range of compounds, including formic acid, formate salts, oxalic acid, and methanol. The efficiency for generation of each compound depends on the experimental conditions, most importantly the material of the cathode, which catalyzes the electrochemical reactions.

Until appropriate cathodes are found some products of CO2 reduction (methanol, for instance) are obtained at efficiencies too low for practical use. Other products can be generated on known cathodes with high current yields that could support valuable practical processes. For example, formic acid has been obtained on tin cathodes with current yields above 80%. Formate salts and sodium bicarbonate are obtained at similarly high yields.

9

ERC Development to Date

We have retained one of the creators of the technology, Professor Colin Oloman, as a member of our scientific advisory board, to further develop the carbon dioxide reduction process to achieve optimal results on a consistent basis. On June 1, 2008, we entered into a technology development and support agreement with Kemetco Research Inc., an integrated science, technology and innovation company. Pursuant to that agreement, we had established a research and development facility for the ERC in Vancouver, British Columbia, staffed by a dedicated research team provided by Kemetco. The use of the research and development facility by our company ended in 2010.

In October of 2008, we completed our first ERC prototype reactor capable of processing 1 kilogram of CO2 per day. In order to facilitate the testing and development of this reactor, we entered into an agreement with Kemetco on January 29, 2010. The agreement was intended to govern the development and testing of our prototype reactor for a period of 10 months and contemplated costs of approximately $250,000 including labor and materials purchases. On March 18, 2010 we entered into another agreement with Kemetco which amended and replaced the January 29, 2010 agreement. Under the terms of the January 29, 2010 agreement, we agreed to proceed with the testing and development of our ERC prototype reactor for a period of 5 months at an estimated cost of approximately $125,000. We have not renewed our agreement with Kemetco and have not been involved with Kemetco since approximately May 2010.

Pictured Above, Design for Bench Scale ERC Reactor

We anticipate that commercialization of ERC will require us to develop reactors capable of processing not less than 100 tons of CO2 per day; however, there is no guarantee that we will successfully produce reactors of that size. Production of commercially viable ERC reactors will depend on continued research and development, successful testing of small scale ERC reactors, and securing of additional financing. This testing is underway in our research facilities, and is complemented by the parallel engineering of a scaled-up demonstration plant by BC Research Inc.

10

Established and Emerging Market for ERC and its Chemical Products:

The technology behind ERC can be applied to any scale commercial venture which outputs CO2 into the atmosphere, though it is expected to be most effective when applied to large scale stationary sources. We anticipate that, once fully commercialized, we will be able to offer ERC as a CO2 management system to various industry including steel, cement, fermentation processes, power generation and pulp and paper.

As described, the ERC process can be used to produce a variety of different chemical products from CO2. The first products that Mantra is targeting are formic acid and its salts. These products have existing markets as commodity chemicals and sell for between $1,000 and $1,500 per tonne, with global consumption being in excess of 600,000 tonnes per year. Formic acid and its salts are used in a variety of industrial applications, including silage preservation, leather tanning, textiles production, oil well drilling, and de-icing, and show enormous potential for market expansion through their use in chemical energy storage.

However, if the ERC process reaches market acceptance as a way to deal with CO2 emissions from industryfacilities, it will likely lead to supply of formic acid in excess of current market demand. We have identified several potential future applications for formic acid, which may lead to an expansion in current market demand. The applications we have identified and are currently focusing on are energy storage and steel pickling.

Energy Storage

Formic acid and its salts have been recognized as excellent energy carriers. They have high volumetric and gravimetric energy densities compared to conventional storage technologies such as batteries, and as liquids are much easier to store and distribute than gaseous hydrogen. By liberating energy from them using direct fuel cells, these chemicals can be used to produce electricity on demand, and as such can be used for energy storage. Their use in energy storage applications would vastly increase the market for formic acid and its salts, as the value of energy storage market is expected to surpass $20 billion in the coming years.

Steel Pickling

Steel pickling is part of the finishing process in the production of certain steel products in which oxide and scale are removed from the surface of strip steel, steel wire, and other forms of steel, by dissolution in acid. A solution of either hydrochloric acid (HCl) or sulfuric acid is generally used to treat carbon steel products, while a combination of hydrofluoric and nitric acids is often used for stainless steel. Approximately one quarter of the HCl produced in the U.S. is used for pickling steel (American Chemistry, 2003), consuming an estimated 5Mt/year. As an organic acid, formic acid would be a very attractive replacement for HCl in the steel pickling process. Formic acid has many potential advantages over HCl in this application, including: less iron lost from the steel surface, improvement in final surface quality, and the elimination of corrosion inhibiting and neutralizing rinse processes to prevent rust development. In addition, formic acid is both bio-degradable and reusable which would allow water used in the picking process to be recycled more easily.

Competition

There are several existing alternative methods to ERC which convert CO2 into useful products. Other methodsinclude, for example:

- Thermo-chemical reactions to produce carbon monoxide, formic acid, methane or methanol;

- Bio-chemical reactions to produce methane;

- Photo-chemical reactions to produce carbon monoxide, formaldehyde or formic acid; and

- Photo-electro-chemical reaction to produce carbon monoxide and possibly methane & methanol.

Some thermo-chemical methods are established commercial industrial processes (e.g. production of methanol from CO2) however, like ERC, most of these alternative methods of CO2 conversion are still at the level of laboratory research and development projects. These alternative methods typically suffer from the following problems:

11

- Low reaction rate and low CO2 space velocity make it too costly and time consuming to process industrial quantities of CO2 ;

- Low selectivity for specified product(s) makes it harder to control product yield;

- High operating temperature and pressure requires large quantities of fossil fuels to power reaction; and

- Highly expensive and cumbersome hydrogen (H2) is required as a feed reactant.

Based on scholarship and test results to date, we believe that, compared with alternative methods of CO2 conversion, ERC, when converting CO2 to formate or formic acid, has several notable advantages including the following:

- Medium reaction rate allows for commercially viable CO2 processing times;

- Medium CO2 space velocity gives the ability to treat comparatively large volumes of CO2 ;

- High product selectivity for formate and formic acid;

- Low operating temperature and pressure make it possible to rely on renewable sources of electricity instead of fossil fuels; and

- Hydrogen (H2) is not required as feed reactant.

In addition to these advantages, we consider most developers of CO2 utilization technologies to not be directly competitive with Mantra. This is because a) the supply of CO2 from industrial sources is very large, allowing for multiple technologies to be successful commercially, and b) most technologies generate different products from CO2 than those produced by Mantra, and thus will not be competitors in the sale of chemical products.

However, because ERC has not yet been tested at a commercially viable scale, there is no guarantee that any of the advantages cited by us will translate into actual competitive advantages for ERC over competing methods for CO2 conversion at an industrial scale. Also, like other competing methods, ERC suffers from fast cathode deterioration, and we must successfully isolate or develop a better ERC cathode in order to gain a competitive advantage in this regard. We have had success developing methods for improving the activity and extending the lifetime of the cathode at the bench scale and expect these methods to translate into significant process improvements as ERC is scaled up.

Our competition consists of a number of small companies capable of competing effectively in the alternative energy market as well as several large companies that possess substantially greater financial and other resources than we do. Many of these competitors are substantially larger and better funded than us, and have significantly longer histories of research, operation and development. Our competitors include technology providers or energy producers using biomass combustion, biomass anaerobic digestion, geothermal, solar, wind, new hydro and other renewable energy sources. In addition, we will face well-established competition from electric utilities and other energy companies in the traditional energy industry who have substantially greater financial resources than we do.

Our competitors may be able to offer more competitively priced and more widely available energy products than ours and they also may have greater resources than us to create or develop new technologies and products.

Therefore, there is no assurance that we will be successful in competing with existing and emerging competitors in the alternative energy industry or traditional energy industry.

We plan to identify business opportunities with interested parties and potential customers by networking and participating in conferences and exhibitions related to greenhouse gas emissions reduction and alternative energy sources and technologies. The strategic and geographic focus of our business is currently the North American market. We believe that one of our competitive advantages is our online carbon reduction marketplace which brings energy/carbon reduction products and service providers into direct contact with consumers and enables the facilitation of business contacts. The focus of our online carbon reduction marketplace is not on business-to-business carbon trading, as is the case with many of our competitors.

While our competitors may be operating similar business models, we plan to build our competitive position in the industry by:

- filling our Scientific Advisory Board with skilled and proficient professionals;

12

- developing and acquiring technologies to establish sustainable fuel supply chains;

- providing a comprehensive range of services; and

- providing marketing and promotion services to generate public awareness and enhance the reputation of sustainability initiatives.

However, since we are a newly-established company, we face the same problems as other start-up companies in other industries. Our competitors may develop similar technologies to ours and use the same methods as we do, and they may generally be able to respond more quickly to new or emerging technologies and changes in legislation and industry regulation. Additionally, our competitors may devote greater resources to the development, promotion and sale of their technologies or services than we do. Increased competition could also result in loss of key personnel, reduced margins or loss of market share, any of which could harm our business.

Government Regulations

Some aspects of our intended operations will be subject to a variety of federal, provincial, state and local laws, rules and regulations in North America and worldwide relating to, among other things, worker safety and the use, storage, discharge and disposal of environmentally sensitive materials. For example, we are subject to the Resource Conservation Recovery Act (“RCRA”), the principal federal legislation regulating hazardous waste generation, management and disposal.

Under some of the laws regulating the use, storage, discharge and disposal of environmentally sensitive materials, an owner or lessee of real estate may be liable for the costs of removing or remediating certain hazardous or toxic substances located on or in, or emanating from, such property, as well as related costs of investigation and property damage. Laws of this nature often impose liability without regard to whether the owner or lessee knew of, or was responsible for, the presence of the hazardous or toxic substances. These laws and regulations may require the removal or remediation of pollutants and may impose civil and criminal penalties for violations. Some of the laws and regulations authorize the recovery of natural resource damages by the government, injunctive relief and the imposition of stop, control, remediation and abandonment orders. The costs arising from compliance with environmental and natural resource laws and regulations may increase operating costs for both us and our potential customers. We are also subject to safety policies of jurisdictional-specific Workers Compensation Boards and similar agencies regulating the health and safety of workers.

In addition to the forgoing, in the future our U.S., Canadian and global operations may be affected by regulatory and political developments at the federal, state, provincial and local levels including, but not limited to, restrictions on offset credit trading, the verification of offset projects and related offset credits, price controls, tax increases, the expropriation of property, the modification or cancellation of contract rights, and controls on joint ventures or other strategic alliances.

We are not aware of any material violations of environmental permits, licenses or approvals issued with respect to our operations. We expect to comply with all applicable laws, rules and regulations relating to our intended business. At this time, we do not anticipate any material capital expenditures to comply with environmental or various regulations and requirements.

While our intended projects or business activities have been designed to produce environmentally friendly green energy or other alternative products for which no specific regulatory barriers exist, any regulatory changes that impose additional restrictions or requirements on us or on our potential customers could adversely affect us by increasing our operating costs and decreasing potential demand for our technologies, products or services, which could have a material adverse effect on our results of operations.

Research and Development Expenditures

During the year ended May 31, 2014 we spent $396,278 on research and development. For the last two fiscal years, we have spent $824,952 on research and development. We anticipate that we will incur $4,200,000 in expenses on research and development (including wages and commercialization efforts) for ERC as well as other technologies we may acquire over the next 12 months.

13

Employees

As of September 8, 2013, we had 2 employees engaged in administrative duties, website development and marketing. Larry Kristof is employed by both our company and by our subsidiary Mantra Energy Alternatives Ltd., as chief executive officer. Our employees were engaged on a full-time basis. Additionally, we have retained a number of consultants for legal, accounting and investor relations services.

As of August 30, 2014, we had 7 employees at our research facilities in Vancouver, British Columbia, including: Patrick Dodd, Amin Aziznia, Sona Kazem, Piotr Forysinski, Christina Gyenge, and two undergraduate students. These employees are engaged in research and development activities to improve our company’s technologies and are employed on a full time basis.

Intellectual Property

We acquired the process for the “Continuous Co-Current Electrochemical Reduction of Carbon Dioxide”, or the ERC technology, on November 2, 2007 pursuant to a technology assignment agreement with 0798465 BC Ltd. According to the agreement, we paid 0798465 BC Ltd. 40,000 common shares at a fair market value of $0.25 per share and 250,000 options to purchase our common shares at an exercise price of $0.25 per share until October 31, 2012. The process for the ERC technology was developed by Dr. Colin Oloman and Dr. Hui Li at the University of British Columbia's Clean Energy Research Center in Vancouver, British Columbia. They filed the initial patent application for the invention under the Patent Cooperation Treaty in 2006. We acquired all right and title in and to the ERC technology as embodied by and described in the following Patent Cooperation Treaty application:

| Country |

Application

Number |

File Date |

Status |

| Patent Cooperation Treaty (PCT) |

W02207 |

10/13/2006 |

PCT(1)

|

| (1) |

The Patent Cooperation Treaty, an international patent law treaty, provides a unified procedure for filing patent applications to protect inventions in each of its contracting states. |

The Patent Cooperation Treaty filing was made with a Receiving Office in 2006 and a written opinion was issued by International Searching Authority regarding the patentability of the invention which is the subject of the application. Finally, the examination and grant procedures will be handled by the relevant national or regional authorities. On March 31, 2008 we initiated the national patent process. We plan to begin the national patent process initially in Europe, Japan and China. The national phases for other countries, particularly the U.S. and Canada, will be initiated in the near future.

On January 14, 2014, our company and Mantra Energy, received acceptance of our primary ERC patent application in Australia. This patent application covers the reactor and process for the electrochemical conversion of carbon dioxide to chemical products, and is a crucial component of Mantra's intellectual property portfolio. The Australian patent was officially issued on May 1, 2014.

As of the date of this annual report, we have been awarded the following patents:

14

| Country | Patent Number | Patent Date | Name of Patent |

| India |

251493 |

March 20, 2012 |

“An Electrochemical Process for Reducing of Carbon Dioxide” |

| China |

ZL 2006 8 0037810.8 |

May 8, 2013 |

“Continuous Co- Current Electrochemical Reduction of Carbon Dioxide” |

| Australia |

2012202601 |

May 1, 2014 |

“Continuous Co- Current Electrochemical Reduction of Carbon Dioxide” |

We have not filed for protection of our trademark. We own the copyright of our logo and all of the contents of our website, www.mantraenergy.com.

REPORTS TO SECURITY HOLDERS

We intend to furnish our shareholders annual reports containing financial statements audited by our independent auditors and to make available quarterly reports containing unaudited financial statements for each of the first three quarters of each year.

The public may read and copy any materials that we file with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The address of that site is www.sec.gov.

Item 1A. Risk Factors

As a “smaller reporting company”, we are not required to provide the information required by this Item.

Item 1B. Unresolved Staff Comments

As a “smaller reporting company”, we are not required to provide the information required by this Item.

Item 2. Description of Property

Our principal executive offices are located at 1562 128th Street, Surrey, British Columbia, Canada V4A 3T7. Our telephone number is (604) 560-1503. The office is approximately 1,200 square feet in size and is leased for a term of twenty four months. The lease began on June 1, 2014 and will end in June 2016. Currently we pay approximately $1,300 per month for our office space in Surrey.

Our research facilities are located at 202-3590 West 41st Avenue, Vancouver, British Columbia, Canada, V6N 3E6. The telephone number is (604) 267-4005. The facility is approximately 1,400 square feet in size and is leased for a term of two years beginning on July 1, 2014. Currently we pay approximately $3,600 per month in rent.

15

Item 3. Legal Proceedings

On May 23, 2012, a former employee of our company delivered a Notice of Application seeking against our company for approximately $55,000. The hearing of that Application took place on July 31, 2012, at which time the former employee obtained judgment in the approximate amount of $55,000. Our company did not defend the amount of the judgment and the amount is included in accounts payable, but claims a complete set-off on the basis that the former employee retains 1,000,000 shares of common stock of our company as security for payment of the outstanding consulting fees owed to him.

On August 31, 2012, our company commenced a separate action against the former employee seeking a return of the 1,000,000 shares of common stock and a stay of execution of the judgment. That application is pending and has not yet been heard or determined by the court. The payment of the judgment claim of approximately $55,000 is dependent upon whether the former employee will first return the 1,000,000 shares of common stock noted above. The probable outcome of our company’s claim for the return of the shares cannot yet be determined.

Item 4. Mine Safety Disclosures

Not applicable.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common stock is not traded on any stock exchange in the United States and Canada and there is no established public trading market for our common stock. Our common stock is quoted on the OTC Bulletin Board, under the trading symbol MVTG. The market for our stock is highly volatile. We cannot assure you that there will be a market in the future for our common stock. OTC Bulletin Board securities are not listed and traded on the floor of an organized national or regional stock exchange. Instead, OTC Bulletin Board securities transactions are conducted through a telephone and computer network connecting dealers in stocks. OTC Bulletin Board stocks are traditionally smaller companies that do not meet the financial and other listing requirements of a regional or national stock exchange.

On February 18, 2008, our common shares began trading on the Frankfurt Stock Exchange under the symbol EDV 5MV. The Frankfurt Stock Exchange is located in Frankfurt, Germany.

The following table reflects the high and low bid information for our common stock obtained from Stockwatch on the OTC Bulletin Board and reflects inter-dealer prices, without retail mark-up, markdown or commission, and may not necessarily represent actual transactions.

Quarter Ended |

High ($) |

Low ($) |

| May 31, 2014 | 0.744 | 0.18 |

| February 28, 2014 | 0.18 | 0.0471 |

| November 30, 2013 | 0.15 | 0.072 |

| August 31, 2013 | 0.19 | 0.10 |

| May 31, 2013 | 0.23 | 0.1 |

| February 28, 2013 | 0.3 | 0.131 |

| November 30, 2012 | 0.24 | 0.1139 |

| August 31, 2012 | 0.12 | 0.06 |

| May 31, 2012 | 0.1199 | 0.032 |

16

Our common shares are issued in registered form. Island Stock Transfer, Roosevelt Office Center, 15500 Roosevelt Boulevard, Suite 301, Clearwater, Florida 33760 (Telephone: (727) 289-0010) is the registrar and transfer agent for our common shares.

Holders

As of September 12, 2014, there were approximately 181 holders of record of our common stock. As of such date, 70,692,692 shares of our common stock were issued and outstanding.

Dividends

To date, we have not paid any dividends on our common shares and we do not expect to declare or pay any dividends on our common shares in the foreseeable future. Payment of any dividends will depend upon future earnings, if any, our financial condition, and other factors as deemed relevant by our board of directors.

Equity Compensation Plans

On November 24, 2009, we registered a 2009 Stock Compensation Plan and a 2009 Stock Option Plan which permits our company to grant up to an aggregate of 3,500,000 options to acquire shares of common stock, to directors, officers, employees and consultants of our company.

Recent Sales of Unregistered Securities; Use of Proceeds from Registered Securities

We did not sell any equity securities which were not registered under the Securities Act during the year ended May 31, 2014 that were not otherwise disclosed on our quarterly reports on Form 10-Q or our current reports on Form 8-K filed during the year ended May 31, 2014.

Purchase of Equity Securities

We did not purchase any of our shares of common stock or other securities during our fiscal year ended May 31, 2014.

Item 6. Selected Financial Data

As a “smaller reporting company” we are not required to provide the information required by this Item.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

The following discussion should be read in conjunction with our consolidated financial statements, including the notes thereto, appearing elsewhere in this Annual Report. The discussions of results, causes and trends should not be construed to imply any conclusion that these results or trends will necessarily continue into the future.

Results of Operations

Results of Operations for the Years Ended May 31, 2014 and 2013

The following summary of our results of operations should be read in conjunction with our audited financial statements for the years ended May 31, 2014 and 2013.

17

Our operating results for the years ended May 31, 2014 and 2013 are summarized as follows:

| Year Ended | ||||||

| May 31, | ||||||

| 2014 | 2013 | |||||

| Revenue | $ | 274,584 | $ | 3,027 | ||

| Cost of goods sold | $ | – | $ | 2,500 | ||

| Operating Expenses | $ | (1,568,122 | ) | $ | (1,374,699 | ) |

| Other Income (Expense) | $ | (59,222 | ) | $ | (45,959 | ) |

| Net Loss | $ | (1,352,760 | ) | $ | (1,420,131 | ) |

Revenues

Our revenues for the year ended May 31, 2014 were $274,584, compared to our revenues for the year ended May 31, 2013, which were $3,027, representing approximately a 8,971% increase. During the year ended May 31, 2014, we started generating research and development services revenue.

Operating Expenses

Our operating expenses for the year ended May 31, 2014 and May 31, 2013 are outlined in the table below:

| Year Ended | ||||||

| May 31, | ||||||

| 2014 | 2013 | |||||

| Business development | $ | 40,300 | $ | 18,907 | ||

| Consulting and advisory | $ | 342,307 | $ | 120,787 | ||

| Depreciation and amortization | $ | 25,771 | $ | 30,872 | ||

| Foreign exchange loss (gain) | $ | (88,728 | ) | $ | (13,942 | ) |

| General and administrative | $ | 132,674 | $ | 48,452 | ||

| License fees | $ | 40,000 | $ | 30,459 | ||

| Management fees | $ | 184,463 | $ | 312,586 | ||

| Professional fees | $ | 168,354 | $ | 159,705 | ||

| Public listing costs | $ | 24,405 | $ | 15,400 | ||

| Rent | $ | 57,853 | $ | 22,623 | ||

| Research and development | $ | 396,278 | $ | 428,674 | ||

| Shareholder communications and awareness | $ | 7,382 | $ | 40,035 | ||

| Travel and promotion | $ | 199,327 | $ | 119,906 | ||

| Wages and benefits | $ | 37,736 | $ | 40,235 | ||

The increase in operating expenses for the year ended May 31, 2014, compared to the same period in fiscal 2013, was mainly due to increases in business development, consulting and advisory fees, general and administrative expenses, license fees, professional fees, public listing costs, rent, and travel and promotion expenses offset by a significant decrease in management fees and increase in foreign exchange gain. The increase in our expenses was the result of an overall increase in business activity which corresponded with increase revenues and investment in our Company. The increase in activity in part related to our establishment of a new research and development facility in Vancouver, British Columbia, and to expenses incurred in connection with our collaboration with NORAM Engineering and BC Research Inc. for the ERC Pilot Plant Project, The increase in foreign exchange gain was largely the result of the relative increase in the value during fiscal 2014 of the U.S. Dollar against the Canadian Dollar: our revenues are largely in U.S. Dollars and a substantial amount of our expenses are paid in Canadian Dollars.

Our general and administrative expenses consist of office occupation expenses, communication expenses (cellular, internet, fax and telephone), bank charges, foreign exchange, courier, postage costs and office supplies. Our professional fees include legal, accounting, and auditing fees. Business development, consulting and advisory costs include fees paid, shares issued and options granted to contractors and advisory board members.

Liquidity and Financial Condition

As of May 31, 2014, our total current assets were $1,600,174 and our total current liabilities were $1,252,130 and we had working capital of $348,044 compared to a working capital deficit of $1,126,556 as at May 31, 2013.

18

We have suffered recurring losses from operations. The continuation of our company is dependent upon our company attaining and maintaining profitable operations and raising additional capital as needed. In this regard we have historically raised additional capital through equity offerings and loan transactions.

Cash Flows

| Year Ended | Year Ended | |||||

| May 31, | May 31, | |||||

| 2014 | 2013 | |||||

| Net Cash Used in Operating Activities | $ | (1,302,235 | ) | $ | (1,353,630 | ) |

| Net Cash Used In Investing Activities | $ | (78,808 | ) | $ | (64,884 | ) |

| Net Cash Provided by Financing Activities | $ | 2,287,542 | $ | 1,228,301 | ||

| Cash increase during the year | $ | 906,499 | $ | (190,213 | ) |

The increase in cash that we experienced during fiscal 2014 as compared to fiscal 2013 was due primarily to the increase during fiscal 2014 of cash received from the sale of our common stock. We expect that our total expenses will increase over the next year as we increase our business operations. We have not been able to reach the break-even point since our inception and have had to rely on outside capital resources. We do not anticipate making significant revenues for the next year. Over the next 12 months, we plan to primarily concentrate on commercializing our ERC technology and associated projects.

| Description |

Estimated expenses ($) |

| Research and Development | 500,000 |

| Consulting Fees | 250,000 |

| Commercialization of ERC | 3,000,000 |

| Shareholder communication and awareness | 200,000 |

| Professional Fees | 300,000 |

| Wages and Benefits | 200,000 |

| Management Fees | 150,000 |

| Total | 5,100,000 |

In order to fully carry out our business plan, we need additional financing of approximately $5,100,000 for the next 12 months. In order to improve our liquidity, we intend to pursue additional equity financing from private placement sales of our equity securities or shareholders’ loans. We do not presently have sufficient financing to undertake our planned business activities. Issuances of additional shares will result in dilution to our existing shareholders.

We currently do not have any arrangements in place for the completion of any further private placement financings and there is no assurance that we will be successful in completing any further private placement financings. If we are unable to achieve the necessary additional financing, then we plan to reduce the amounts that we spend on our business activities and administrative expenses in order to be within the amount of capital resources that are available to us.

Off-Balance Sheet Arrangements

We have no significant off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in our financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that are material to our stockholders.

Inflation

The effect of inflation on our revenue and operating results has not been significant.

19

Critical Accounting Policies

Our consolidated financial statements are impacted by the accounting policies used and the estimates and assumptions made by management during their preparation. A complete summary of these policies is included in note 2 of the notes to our financial statements. We have identified below the accounting policies that are of particular importance in the presentation of our financial position, results of operations and cash flows, and which require the application of significant judgment by management.

Basis of Presentation/Principles of Consolidation

These consolidated financial statements and related notes are presented in accordance with accounting principles generally accepted in the United States. These consolidated financial statements include the accounts of our company and our subsidiaries, Carbon Commodity Corporation, Climate ESCO Ltd., Mantra Energy Alternatives Ltd., Mantra China Inc., Mantra China Limited, Mantra Media Corp., Mantra NextGen Power Inc., and Mantra Wind Inc. All the subsidiaries are wholly-owned with the exception of Climate ESCO Ltd., which is 64.84% owned and Mantra Energy Alternatives Ltd., which is 89.09% owned. All inter-company balances and transactions have been eliminated.

Use of Estimates

The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Our company regularly evaluates estimates and assumptions related to allowance for doubtful accounts, the estimated useful lives and recoverability of long-lived assets, valuation of inventory, equity component of convertible debt, stock-based compensation, and deferred income tax asset valuation allowances. Our company bases our estimates and assumptions on current facts, historical experience and various other factors that we believe to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities and the accrual of costs and expenses that are not readily apparent from other sources. The actual results experienced by our company may differ materially and adversely from our company’s estimates. To the extent there are material differences between the estimates and the actual results, future results of operations will be affected.

Accounts Receivable

Our company recognizes allowances for doubtful accounts to ensure accounts receivable are not overstated due to the inability or unwillingness of its customers to make required payments. The allowance is based on historical bad debt expense, the age of receivable and the specific identification of receivables our company considers at risk.

Intangible Assets

Intangible assets consist of patents and are stated at cost and have a definite life. Intangible assets are amortized over their estimated useful lives. Our company periodically evaluates the reasonableness of the useful lives of these assets. Once these assets are fully amortized, they are removed from the accounts. These assets are reviewed for impairment or obsolescence when events or changes in circumstances indicate that the carrying amount may not be recoverable. If impaired, intangible assets are written down to fair value based on discounted cash flows or other valuation techniques. Our company has no intangibles with indefinite lives.

Long-lived Assets

In accordance with ASC 360, “Property, Plant and Equipment”, our company tests long-lived assets or asset groups for recoverability when events or changes in circumstances indicate that their carrying amount may not be recoverable. Circumstances which could trigger a review include, but are not limited to: significant decreases in the market price of the asset; significant adverse changes in the business climate or legal factors; accumulation of costs significantly in excess of the amount originally expected for the acquisition or construction of the asset; current period cash flow or operating losses combined with a history of losses or a forecast of continuing losses associated with the use of the asset; and current expectation that the asset will more likely than not be sold or disposed significantly before the end of its estimated useful life. Recoverability is assessed based on the carrying amount of the asset and its fair value, which is generally determined based on the sum of the undiscounted cash flows expected to result from the use and the eventual disposal of the asset, as well as specific appraisal in certain instances. An impairment loss is recognized when the carrying amount is not recoverable and exceeds fair value.

20

Technology Development Revenue Recognition

Our company performs research and development services. Our company recognizes revenue under research contracts when a contract has been executed, the contract price is fixed and determinable, delivery of services or products has occurred, and collectability of the contract price is considered reasonably assured and can be reasonably estimated. Revenue is based on direct labor hours expended at contract billing rates plus other billable direct costs.

Research and Development Costs

Research and development costs are expensed as incurred.

Stock-based Compensation

Our company records stock-based compensation in accordance with ASC 718, “Compensation – Stock Compensation”, using the fair value method. All transactions in which goods or services are the consideration received for the issuance of equity instruments are accounted for based on the fair value of the consideration received or the fair value of the equity instrument issued, whichever is more reliably measurable.

Our company uses the Black-Scholes option pricing model to calculate the fair value of stock-based awards. This model is affected by our company’s stock price as well as assumptions regarding a number of subjective variables. These subjective variables include, but are not limited to our company’s expected stock price volatility over the term of the awards, and actual and projected employee stock option exercise behaviors. The value of the portion of the award that is ultimately expected to vest is recognized as an expense in the consolidated statement of operations over the requisite service period.

Recent Accounting Pronouncements

Our company has limited operations and is considered to be in the development stage. In the year ended May 31, 2014, our company has elected to early adopt Accounting Standards Update No. 2014-10, Development Stage Entities (Topic 915): Elimination of Certain Financial Reporting Requirements. The adoption of this ASU allows our company to remove the inception to date information and all references to development stage.

We do not expect the adoption of any other recently issued accounting pronouncements to have a significant impact on our results of operations, financial position or cash flow.

Item 7A. Quantitative and Qualitative Disclosures about Market Risk

As a “smaller reporting company”, we are not required to provide the information required by this Item.

Item 8. Financial Statements and Supplementary Data

21

MANTRA VENTURE GROUP LTD.

Consolidated financial

statements

May 31, 2014

(Expressed in U.S. dollars)

0

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Stockholders of

Mantra

Venture Group Ltd.

We have audited the accompanying consolidated balance sheet of Mantra Venture Group Ltd. (“the Company”) as of May 31, 2014 and the related consolidated statements of operations, stockholders’ equity (deficit) and cash flows for the year then ended. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion the financial statements referred to above present fairly, in all material respects, the financial position of Mantra Venture Group Ltd. as of May 31, 2014, and the results of their operations and cash flows for the year then ended in conformity with U.S. generally accepted accounting principles.

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 1 to the consolidated financial statements, the Company has not generated significant revenue and has an accumulated deficit of $9,314,295 as of May 31, 2014 which raises substantial doubt about its ability to continue as a going concern. Management’s plans concerning these matters are also described in Note 1. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

/s/ Sadler, Gibb & Associates, LLC

Salt Lake City, UT

September 15, 2014

F-1

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Stockholders of

Mantra

Venture Group Ltd.

We have audited the accompanying consolidated balance sheet of Mantra Venture Group Ltd. (the “Company”) as of May 31, 2013, and the related consolidated statements of operations, stockholders’ equity (deficit), and cash flows for the year then ended. These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. An audit includes consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of the Company as of May 31, 2013, and the results of its operations and its cash flows for the year then ended, in conformity with accounting principles generally accepted in the United States.

The accompanying consolidated financial statements have been prepared assuming the Company will continue as a going concern. As discussed in Note 1 to the financial statements, the Company has not generated significant revenues, has a working capital deficit, and has incurred operating losses since inception. These factors raise substantial doubt about the Company’s ability to continue as a going concern. Management’s plans in regard to these matters are also discussed in Note 1 to the financial statements. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

/s/ SATURNA GROUP CHARTERED ACCOUNTANTS LLP

Saturna Group Chartered Accountants LLP

Vancouver, Canada

September 11, 2013

F-2

MANTRA VENTURE GROUP LTD.

Consolidated balance sheets

(Expressed in U.S. dollars)

| May 31, | May 31, | |||||

| 2014 | 2013 | |||||

| $ | $ | |||||

| ASSETS | ||||||

| Current assets | ||||||

| Cash | 931,886 | 25,387 | ||||

| Amounts receivable | 163,591 | 19,915 | ||||

| Prepaid expenses and deposits | 504,697 | 34,521 | ||||

| Total current assets | 1,600,174 | 79,823 | ||||

| Restricted cash | 27,374 | 28,750 | ||||

| Property and equipment | 94,231 | 70,771 | ||||

| Intangible assets | 29,547 | |||||

| Total assets | 1,751,326 | 179,344 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY (DEFICIT) | ||||||

| Current liabilities | ||||||

| Accounts payable and accrued liabilities | 715,053 | 571,805 | ||||

| Due to related parties | 159,994 | 173,424 | ||||

| Loans payable | 204,176 | 253,227 | ||||

| Obligations under capital lease | 8,246 | 7,826 | ||||

| Convertible debentures | 164,660 | 200,097 | ||||

| Total current liabilities | 1,252,129 | 1,206,379 | ||||

| Loans payable | – | 31,346 | ||||

| Obligations under capital lease | 19,856 | 29,177 | ||||

| Convertible debentures (net of discount of $175,360) | 16,640 | – | ||||

| Total liabilities | 1,288,625 | 1,266,902 | ||||

| Stockholders’ equity (deficit) | ||||||

| Mantra Venture Group Ltd. stockholders’ deficit | ||||||

| Preferred

stock Authorized: 20,000,000 shares, par value $0.00001 Issued and outstanding: Nil shares |

– | – | ||||

| Common

stock Authorized: 100,000,000 shares, par value $0.00001 Issued and outstanding: 69,157,322 (May 31, 2013 – 55,226,276) shares |

692 | 552 | ||||

| Additional paid-in capital | 9,679,880 | 6,875,939 | ||||

| Subscriptions receivable | (1,791 | ) | – | |||

| Common stock subscribed | 216,391 | 115,662 | ||||

| Accumulated deficit | (9,314,295 | ) | (8,023,639 | ) | ||

| Total Mantra Venture Group Ltd. stockholders’ equity (deficit) | 580,877 | (1,031,486 | ) | |||

| Non-controlling interest | (118,176 | ) | (56,072 | ) | ||

| Total stockholders’ deficit | 462,701 | (1,087,558 | ) | |||

| Total liabilities and stockholders’ equity (deficit) | 1,751,326 | 179,344 |

(The accompanying notes are an integral part of these consolidated financial statements)

F-3

MANTRA VENTURE GROUP LTD.

Consolidated statements of operations

(Expressed in U.S.

dollars)

| Year ended | Year ended | |||||

| May 31, | May 31, | |||||

| 2014 | 2013 | |||||

| $ | $ | |||||

| Revenue | 274,584 | 3,027 | ||||

| Cost of goods sold | – | 2,500 | ||||

| Gross profit | 274,584 | 527 | ||||

| Operating expenses | ||||||

| Business development | 40,300 | 18,907 | ||||

| Consulting and advisory | 342,307 | 120,787 | ||||

| Depreciation and amortization | 25,772 | 30,872 | ||||

| Foreign exchange loss (gain) | (88,728 | ) | (13,942 | ) | ||

| General and administrative | 132,673 | 48,452 | ||||

| License fees | 40,000 | 30,459 | ||||

| Management fees | 184,463 | 312,586 | ||||

| Professional fees | 168,354 | 159,705 | ||||

| Public listing costs | 24,405 | 15,400 | ||||

| Rent | 57,853 | 22,623 | ||||

| Research and development | 396,278 | 428,674 | ||||

| Shareholder communications and awareness | 7,382 | 40,035 | ||||

| Travel and promotion | 199,327 | 119,906 | ||||

| Wages and benefits | 37,736 | 40,235 | ||||

| Total operating expenses | 1,568,122 | 1,374,699 | ||||

| Loss before other income (expense) | (1,293,538 | ) | (1,374,172 | ) | ||

| Other income (expense) | ||||||

| Accretion of discounts on convertible debentures | (26,557 | ) | (2,998 | ) | ||

| Gain on settlement of debt | 11,503 | 497 | ||||

| Interest expense | (44,168 | ) | (43,458 | ) | ||

| Total other income (expense) | (59,222 | ) | (45,959 | ) | ||

| Net loss for the period | (1,352,760 | ) | (1,420,131 | ) | ||

| Less: net loss attributable to the non-controlling interest | 62,104 | 85,962 | ||||

| Net loss attributable to Mantra Venture Group Ltd. | (1,290,656 | ) | (1,334,169 | ) | ||

| Net loss per share attributable to Mantra Venture Group Ltd. common shareholders, basic and diluted | (0.02 | ) | (0.03 | ) | ||

| Weighted average number of shares outstanding used in the calculation of net loss attributable to Mantra Venture Group Ltd. per common share | 59,096,396 | 51,052,620 |

(The accompanying notes are an integral part of these consolidated financial statements)

F-4

MANTRAVENTUREGROUPLTD.

Consolidated statements of stockholder’s equity (deficit)

For the

years ended May 31, 2014 and 2013

| Common Stock | Additional | Common | Common stock | Total | ||||||||||||||||||||

| paid-in | stock | subscriptions | Accumulated | Non-controlling | stockholders’ | |||||||||||||||||||

| Amount | capital | subscribed | receivable | deficit | interest | equity (deficit) | ||||||||||||||||||

| Number | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||

| Balance, May 31, 2012 | 45,623,806 | 456 | 5,675,442 | 144,916 | (94,708 | ) | (6,689,470 | ) | (8,297 | ) | (971,661 | ) | ||||||||||||

| Stock Issued for Cash | ||||||||||||||||||||||||

| Stock issued at $0.03 per share pursuant to the exercise of stock options | 250,000 | 3 | 7,497 | – | – | – | – | 7,500 | ||||||||||||||||

| Stock issued at $0.05 per share pursuant to the exercise of stock options | 200,000 | 2 | 9,998 | – | – | – | – | 10,000 | ||||||||||||||||

| Units issued at $0.015 per share | 1,333,333 | 13 | 19,987 | (20,000 | ) | – | – | – | – | |||||||||||||||

| Units issued at $0.05 per share | 826,000 | 8 | 41,292 | (41,300 | ) | – | – | – | – | |||||||||||||||

| Units issued at $0.10 per share | 2,125,000 | 21 | 212,479 | (20,000 | ) | – | – | – | 192,500 | |||||||||||||||

| Units issued at $0.12 per share | 3,325,001 | 33 | 398,967 | – | – | – | – | 399,000 | ||||||||||||||||

| Units issued at $0.17 per share | 1,543,136 | 16 | 262,318 | – | – | – | – | 262,334 | ||||||||||||||||

| Stock Issued by Subsidiary | ||||||||||||||||||||||||

| Stock issued at Cdn$1.00 per share | – | – | 185,067 | – | – | – | 22,664 | 207,731 | ||||||||||||||||

| Share subscriptions for previously issued shares received by subsidiary | – | – | – | – | 94,708 | – | 8,292 | 103,000 | ||||||||||||||||