UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended August 31, 2012

or

[ ] TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to __________

Commission File Number 000-53461

MANTRA VENTURE GROUP LTD.

(Exact name of registrant as specified in its charter)

| British Columbia | 26-0592672 |

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) |

| #562 – 800 15355 24th Avenue, Surrey, British Columbia, Canada | V4A 2H9 |

| (Address of principal executive offices) | (Zip Code) |

(604) 560-1503

(Registrant’s telephone

number, including area code)

N/A

(Former name, former address and

former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all

reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the

registrant was required to file such reports), and (2) has been subject to such

filing requirements for the past 90 days.

[X] YES [

] NO

Indicate by check mark whether the registrant has submitted

electronically and posted on its corporate Web site, if any, every Interactive

Data File required to be submitted and posted pursuant to Rule 405 of Regulation

S-T (§232.405 of this chapter) during the preceding 12 months (or for such

shorter period that the registrant was required to submit and post such

files).

[X] YES [ ] NO

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a small reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [ ] |

| Non-accelerated filer [ ] (Do not check if a smaller reporting company) |

Smaller reporting company [X] |

Indicate by check mark whether the registrant is a shell company

(as defined in Rule 12b-2 of the Exchange Act

[ ]

YES [X] NO

APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY

PROCEEDINGS DURING THE PRECEDING FIVE YEARS

Check whether the registrant has filed all documents and reports

required to be filed by Sections 12, 13 or 15(d) of the Exchange Act after the

distribution of securities under a plan confirmed by a court.

[ ]

YES [ ] NO

APPLICABLE ONLY TO CORPORATE ISSUERS

Indicate the number of shares outstanding of each of the

issuer’s classes of common stock, as of the latest practicable date.

47,783,139 common shares issued and outstanding as of October 22,

2012.

Table of Contents

2

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements

The unaudited interim consolidated financial statements of Mantra Venture Group Ltd. (“we”, “us”, “our” and “our company”) follow. All currency references in this report are in US dollars unless otherwise noted.

3

MANTRA VENTURE GROUP LTD.

(A development stage

company)

Consolidated financial statements

August 31, 2012

(Expressed

in U.S. dollars)

(unaudited)

| Index | |

| Consolidated balance sheets | F–1 |

| Consolidated statements of operations | F–2 |

| Consolidated statements of cash flows | F–3 |

| Notes to the consolidated financial statements | F–4 |

4

MANTRA VENTURE GROUP LTD.

(A development stage

company)

Consolidated balance sheets

(Expressed in U.S. dollars)

| August 31, | May 31, | |||||

| 2012 | 2012 | |||||

| $ | $ | |||||

| (unaudited) | ||||||

| ASSETS | ||||||

| Current assets | ||||||

| Cash | 238,629 | 215,600 | ||||

| Amounts receivable | 30,812 | 16,120 | ||||

| Inventory | – | 2,500 | ||||

| Prepaid expenses and deposits | 97,239 | 40,140 | ||||

| Total current assets | 366,680 | 274,360 | ||||

| Property and equipment (Note 3) | 56,312 | 22,966 | ||||

| Total assets | 422,992 | 297,326 | ||||

| LIABILITIES AND STOCKHOLDERS’ DEFICIT | ||||||

| Current liabilities | ||||||

| Accounts payable and accrued liabilities | 542,886 | 536,888 | ||||

| Due to related parties (Note 4) | 215,432 | 244,455 | ||||

| Loans payable (Note 5) | 236,486 | 227,347 | ||||

| Obligations under capital lease (Note 6) | 3,923 | – | ||||

| Convertible debentures (Note 7) | 200,000 | 200,000 | ||||

| Total current liabilities | 1,198,727 | 1,208,690 | ||||

| Loans payable (Note 5) | 55,870 | 60,297 | ||||

| Obligations under capital lease (Note 6) | 18,176 | – | ||||

| Total liabilities | 1,272,773 | 1,268,987 | ||||

| Going concern (Note 1) | ||||||

| Commitments and contingencies (Note 11) | ||||||

| Subsequent event (Note 12) | ||||||

| Stockholders’ deficit | ||||||

| Mantra Venture Group Ltd. stockholders’ deficit | ||||||

| Preferred

stock Authorized: 20,000,000 shares, par value $0.00001 Issued and outstanding: Nil shares |

– | – | ||||

| Common

stock Authorized: 100,000,000 shares, par value $0.00001 Issued and outstanding: 47,783,139 (May 31, 2012 – 45,623,806) shares |

478 | 456 | ||||

| Additional paid-in capital | 5,736,720 | 5,675,442 | ||||

| Common stock subscribed (Note 8) | 437,915 | 144,916 | ||||

| Common stock subscriptions receivable (Note 8) | – | (94,708 | ) | |||

| Deficit accumulated during the development stage | (7,034,226 | ) | (6,689,470 | ) | ||

| Total Mantra Venture Group Ltd. stockholders’ deficit | (859,113 | ) | (963,364 | ) | ||

| Non-controlling interest | 9,332 | (8,297 | ) | |||

| Total stockholders’ deficit | (849,781 | ) | (971,661 | ) | ||

| Total liabilities and stockholders’ deficit | 422,992 | 297,326 |

(The accompanying notes are an integral part of these consolidated financial statements)

F-1

MANTRA VENTURE GROUP LTD.

(A development stage

company)

Consolidated statements of operations

(Expressed in U.S.

dollars)

(unaudited)

| Accumulated from | |||||||||

| January 22, | |||||||||

| Three months | Three months | 2007 (date of | |||||||

| ended | ended | inception) to | |||||||

| August 31, | August 31, | August 31, | |||||||

| 2012 | 2011 | 2012 | |||||||

| $ | $ | $ | |||||||

| Revenue | 3,027 | 550 | 38,812 | ||||||

| Cost of goods sold | 2,500 | 490 | 14,973 | ||||||

| Gross profit | 527 | 60 | 23,839 | ||||||

| Operating expenses | |||||||||

| Business development | 6,665 | 1,243 | 339,171 | ||||||

| Consulting and advisory | 22,111 | 128,760 | 878,949 | ||||||

| Depreciation and amortization | 5,825 | 7,195 | 156,459 | ||||||

| Foreign exchange loss (gain) | 16,845 | (1,949 | ) | 55,978 | |||||

| General and administrative | 12,278 | 6,070 | 440,129 | ||||||

| License fees | – | – | 53,052 | ||||||

| Management fees (Note 5) | 78,000 | 48,000 | 1,205,270 | ||||||

| Professional fees | 38,602 | 39,130 | 928,397 | ||||||

| Public listing costs | 3,480 | 1,881 | 225,980 | ||||||

| Rent | 4,500 | 8,671 | 225,683 | ||||||

| Research and development | 89,787 | – | 519,589 | ||||||

| Shareholder communications and awareness | 34,719 | – | 676,197 | ||||||

| Travel and promotion | 37,019 | 3,739 | 462,987 | ||||||

| Wages and benefits | – | – | 739,509 | ||||||

| Website development/corporate branding | – | – | 195,451 | ||||||

| Write-down of intangible assets | – | – | 37,815 | ||||||

| Write-down of inventory | – | – | 12,455 | ||||||

| Total operating expenses | 349,831 | 242,740 | 7,153,071 | ||||||

| Loss before other income (expense) | (349,304 | ) | (242,680 | ) | (7,129,232 | ) | |||

| Other income (expense) | |||||||||

| Accretion of discounts on convertible debentures | – | – | (45,930 | ) | |||||

| Gain on settlement of debt | – | 3,250 | 21,835 | ||||||

| Government grant income | – | – | 118,324 | ||||||

| Interest expense | (8,816 | ) | (6,452 | ) | (111,283 | ) | |||

| Loss on disposal of property and equipment | – | – | (14,999 | ) | |||||

| Total other income (expense) | (8,816 | ) | (3,202 | ) | (32,053 | ) | |||

| Net loss for the period | (358,120 | ) | (245,882 | ) | (7,161,285 | ) | |||

| Less: net loss attributable to the non-controlling interest | 13,364 | 18,560 | 127,059 | ||||||

| Net loss attributable to Mantra Venture Group Ltd. | (344,756 | ) | (227,322 | ) | (7,034,226 | ) | |||

| Net loss per share attributable to Mantra Venture Group

Ltd. common shareholders, basic and diluted |

(0.01 | ) | (0.01 | ) | |||||

| Weighted average number of shares outstanding used in

the calculation of net loss attributable to Mantra Venture Group Ltd. per common share |

47,102,480 | 40,900,539 |

(The accompanying notes are an integral part of these consolidated financial statements)

F-2

MANTRA VENTURE GROUP LTD.

(A development stage

company)

Consolidated statements of cash flows

(Expressed in U.S.

dollars)

(unaudited)

| Accumulated from | |||||||||

| Three Months | Three Months | January 22, 2007 | |||||||

| Ended | Ended | (date of inception) to | |||||||

| August 31, | August 31, | August 31, | |||||||

| 2012 | 2011 | 2012 | |||||||

| $ | $ | $ | |||||||

| Operating activities | |||||||||

| Net loss for the period | (358,120 | ) | (245,882 | ) | (7,161,285 | ) | |||

| Adjustments to reconcile

net loss to net cash used in

operating activities: |

|||||||||

| Accretion of discounts on convertible debentures | – | – | 45,930 | ||||||

| Depreciation and amortization | 5,825 | 7,195 | 156,459 | ||||||

| Foreign exchange loss | 12,957 | 166 | 6,530 | ||||||

| Gain on settlement of debt | – | (3,250 | ) | (21,835 | ) | ||||

| Loss on disposal of property and equipment | – | – | 14,999 | ||||||

| Stock-based compensation | – | 78,500 | 1,586,325 | ||||||

| Write-down of intangible assets | – | – | 37,815 | ||||||

| Write-down of inventory | – | – | 12,455 | ||||||

| Changes in operating assets and liabilities: | |||||||||

| Amounts receivable | (14,692 | ) | (8,059 | ) | (30,812 | ) | |||

| Inventory | 2,500 | (90 | ) | (12,455 | ) | ||||

| Prepaid expenses and deposits | (57,099 | ) | 2,954 | (97,239 | ) | ||||

| Other assets | – | – | (12,000 | ) | |||||

| Accounts payable and accrued liabilities | 5,998 | 27,092 | 1,016,594 | ||||||

| Deferred revenue | – | 3,100 | – | ||||||

| Due to related parties | (38,023 | ) | 30,863 | 206,432 | |||||

| Net cash used in operating activities | (440,654 | ) | (107,411 | ) | (4,252,087 | ) | |||

| Investing activities | |||||||||

| Purchase of property and equipment | (8,406 | ) | – | (185,905 | ) | ||||

| Proceeds from sale of property and equipment | – | – | 900 | ||||||

| Net cash used in investing activities | (8,406 | ) | – | (185,005 | ) | ||||

| Financing activities | |||||||||

| Proceeds from loans payable | – | 34,690 | 201,571 | ||||||

| Repayment of loan payable | (7,609 | ) | – | (7,609 | ) | ||||

| Repayment of capital lease obligation | (302 | ) | – | (302 | ) | ||||

| Proceeds from issuance of convertible debentures | – | – | 250,000 | ||||||

| Proceeds from issuance of common stock

and subscriptions received |

480,000 | 55,528 | 4,232,061 | ||||||

| Net cash provided by financing activities | 472,089 | 90,218 | 4,675,721 | ||||||

| Change in cash | 23,029 | (17,193 | ) | 238,629 | |||||

| Cash, beginning of period | 215,600 | 39,101 | – | ||||||

| Cash, end of period | 238,629 | 21,908 | 238,629 | ||||||

| Non-cash investing and financing activities: | |||||||||

| Property and equipment financed under capital lease | 21,765 | – | 21,765 | ||||||

| Shares issued to settle debt | – | 22,750 | 409,372 | ||||||

| Shares issued and stock options granted for

acquisition of intangible assets |

– | – | 37,815 | ||||||

| Supplemental disclosures: | |||||||||

| Interest paid | – | – | – | ||||||

| Income taxes paid | – | – | – |

(The accompanying notes are an integral part of these consolidated financial statements)

F-3

MANTRA VENTURE GROUP LTD.

(A development stage

company)

Notes to the consolidated financial statements

Year ended August

31, 2012

(Expressed in U.S. dollars)

(unaudited)

| 1. |

Basis of Presentation | |

|

The accompanying consolidated interim financial statements of Mantra Venture Group Ltd. (the “Company”) should be read in conjunction with the consolidated financial statements and accompanying notes filed with the U.S. Securities and Exchange Commission in the Company’s Annual Report on Form 10-K for the fiscal year ended May 31, 2012. In the opinion of management, the accompanying financial statements reflect all adjustments of a recurring nature considered necessary to present fairly the Company’s financial position and the results of its operations and its cash flows for the periods shown. The preparation of financial statements in accordance with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the amounts reported. Actual results could differ materially from those estimates. The results of operations and cash flows for the periods shown are not necessarily indicative of the results to be expected for the full year. These consolidated financial statements have been prepared on a going concern basis, which implies the Company will continue to realize its assets and discharge its liabilities in the normal course of business. The Company has yet to acquire commercially exploitable energy related technology, has not generated significant revenues since inception, and is unlikely to generate earnings in the immediate or foreseeable future. The continuation of the Company as a going concern is dependent upon the continued financial support from its shareholders, the ability of management to raise additional equity capital through private and public offerings of its common stock, and the attainment of profitable operations. As at August 31, 2012, the Company has a working capital deficit of $832,047, has not generated significant revenues, and has accumulated losses of $7,034,226 since inception. These factors raise substantial doubt regarding the Company’s ability to continue as a going concern. These consolidated financial statements do not include any adjustments to the recoverability and classification of recorded asset amounts and classification of liabilities that might be necessary should the Company be unable to continue as a going concern. | ||

| 2. |

Summary of Significant Accounting Policies | |

|

(a) |

Principles of Consolidation | |

|

These consolidated financial statements are expressed in US dollars. These consolidated financial statements include the accounts of the Company and its subsidiaries, Carbon Commodity Corporation, Climate ESCO Ltd., Mantra Energy Alternatives Ltd., Mantra China Inc., Mantra China Limited, Mantra Media Corp., Mantra NextGen Power Inc., and Mantra Wind Inc. All the subsidiaries are wholly-owned with the exception of Climate ESCO Ltd., which is 64.84% owned and Mantra Energy Alternatives Ltd., which is 91.95% owned. All inter-company balances and transactions have been eliminated. | ||

|

(b) |

Recent Accounting Pronouncements | |

|

The Company has implemented all new accounting pronouncements that are in effect and that may impact its financial statements and does not believe that there are any other new accounting pronouncements that have been issued that might have a material impact on its financial position or results of operations. | ||

| 3. |

Property and Equipment | |

| May 31, | |||||||||||||

| August 31, 2012 | 2012 | ||||||||||||

| Accumulated | Net carrying | Net carrying | |||||||||||

| Cost | depreciation | value | value | ||||||||||

| $ | $ | $ | $ | ||||||||||

| Computer | 1,702 | 237 | 1,465 | 1,607 | |||||||||

| Office furniture and equipment | 48,847 | 43,043 | 5,804 | 8,000 | |||||||||

| Research equipment | 53,793 | 43,083 | 10,710 | 13,359 | |||||||||

| Vehicle under capital lease | 39,171 | 838 | 38,333 | – | |||||||||

| 143,513 | 87,201 | 56,312 | 22,966 |

F-4

MANTRA VENTURE GROUP LTD.

(A development stage

company)

Notes to the consolidated financial statements

Year ended August

31, 2012

(Expressed in U.S. dollars)

(unaudited)

|

4. |

Related Party Transactions | ||

|

|

|

|

|

|

(a) |

During the three months ended August 31, 2012, the Company incurred management fees of $18,000 (2011 - $18,000) to the President of the Company. | ||

|

|

|

|

|

|

(b) |

During the three months ended August 31, 2012, the Company incurred management fees of $15,000 (2011 - $18,000) to the President of the Company. | ||

|

|

|

|

|

|

(c) |

During the three months ended August 31, 2012, the Company incurred management fees of $20,000 (2011 - $15,000) to a director of the Company. | ||

|

|

|

|

|

|

(d) |

As at August 31, 2012, the Company owes $27,823 (May 31, 2012 - $42,033) to the spouse of the President of the Company which is non-interest bearing, unsecured, and due on demand. | ||

|

|

|

|

|

|

(e) |

As at August 31, 2012, the Company owes $29,018 (May 31, 2012 - $22,444) to two directors of the Company, which is non-interest bearing, unsecured, and due on demand. | ||

|

|

|

|

|

|

(f) |

As at August 31, 2012, the Company owes a total of $158,591 (May 31, 2012 - $179,978) to the President of the Company and a company controlled by the President of the Company which is non-interest bearing, unsecured, and due on demand. | ||

|

|

|

|

|

|

5. |

Loans Payable | ||

|

|

|

|

|

|

(a) |

As at August 31, 2012, the amount of $64,217 (Cdn$63,300) (May 31, 2012 - $61,106, (Cdn$63,300)) is owed to a non-related party which is non-interest bearing, unsecured, and due on demand. | ||

|

|

|

|

|

|

(b) |

As at August 31, 2012, the amount of $10,000 (May 31, 2012 - $10,000) is owed to a non-related party, which bears interest at 10% per annum, is unsecured, and due on demand. | ||

|

|

|

|

|

|

(c) |

As at August 31, 2012, the amount of $30,638 (Cdn$30,200) (May 31, 2012 – $29,183, (Cdn$30,200)) is owed to a non-related party, which is non-interest bearing, unsecured, and due on demand. | ||

|

|

|

|

|

|

(d) |

As at August 31, 2012, the amount of $17,500 (May 31, 2012 - $17,500) is owed to a non-related party which is non-interest bearing, unsecured, and due on demand. | ||

|

|

|

|

|

|

(e) |

As at August 31, 2012, the amount of $15,000 (May 31, 2012 - $15,000) is owed to a non-related party which is non-interest bearing, unsecured, and due on demand. | ||

|

|

|

|

|

|

(f) |

As at August 31, 2012, the amount of $19,169 (Cdn$18,895) (May 31, 2012 – $18,225 (Cdn$18,895)) is owed to a non-related party, which is non-interest bearing, unsecured, and due on demand. | ||

|

|

|

|

|

|

(g) |

As at August 31, 2012, the amounts of $7,500 and $37,537 (Cdn$37,000) (May 31, 2012 - $7,500 and $35,820, (Cdn$37,000)) is owed to a non-related party which is non-interest bearing, unsecured, and due on demand. | ||

|

|

|

|

|

|

(h) |

On January 19, 2012, the Company entered into a settlement agreement to settle a $50,000 convertible debenture and $122,535 in accounts payable and accrued interest with the debt holder. Pursuant to the agreement, the debt holder agreed to reduce the debt to Cdn$100,000 on the condition that the Company pays the amount of Cdn$2,500 per month for 40 months, beginning March 1, 2012 and continuing on the first day of each month thereafter. As at August 31, 2012, $86,305 (May 31, 2012 - $88,820) is owed, of which $30,434 (Cdn$30,000) (May 31, 2012 - $28,523 (Cdn$30,000)) is due over the next twelve months. | ||

|

|

|

|

|

|

(i) |

As at August 31, 2012, the amount of $4,490 (May 31, 2012 - $4,490) is owed to a non-related party which is non-interest bearing, unsecured, and due on demand. | ||

F-5

MANTRA VENTURE GROUP LTD.

(A development stage

company)

Notes to the consolidated financial statements

Year ended August

31, 2012

(Expressed in U.S. dollars)

(unaudited)

| 6. |

Obligations Under Capital Lease |

|

On July 31, 2012, the Company entered into an agreement to lease a vehicle for 3 years. The vehicle lease is classified as a capital lease. The following is a schedule by years of future minimum lease payments under capital leases together with the present value of the net minimum lease payments as of August 31, 2012: |

| Year ending May 31: | $ | |||

| 2013 | 4,866 | |||

| 2014 | 6,489 | |||

| 2015 | 6,489 | |||

| 2016 | 10,212 | |||

| Net minimum lease payments | 28,056 | |||

| Less: amount representing interest payments | (5,957 | ) | ||

| Present value of net minimum lease | 22,099 | |||

| Less: current portion | (3,923 | ) | ||

| Long-term portion | 18,176 |

| 7. |

Convertible Debentures |

|

In October 2008, the Company issued three convertible debentures for total proceeds of $250,000 which bear interest at 10% per annum, are unsecured, and due one year from date of issuance. The unpaid amount of principal and accrued interest can be converted at any time at the holder’s option into 625,000 shares of the Company’s common stock at a price of $0.40 per share. The Company also issued 250,000 detachable, non- transferable share purchase warrants. Each share purchase warrant entitles the holder to purchase one additional share of the Company’s common stock for a period of two years from the date of issuance at an exercise price of $0.50 per share. | |

|

In accordance with ASC 470-20, “Debt with Conversion and Other Options”, the Company determined that the convertible debentures contained no embedded beneficial conversion feature as the convertible debentures were issued with a conversion price higher than the fair market value of the Company’s common shares at the time of issuance. | |

|

In accordance with ASC 470-20, “Debt with Conversion and Other Options”, the Company allocated the proceeds of issuance between the convertible debt and the detachable share purchase warrants based on their relative fair values. Accordingly, the Company recognized the fair value of the share purchase warrants of $45,930 as additional paid-in capital and an equivalent discount against the convertible debentures. The Company has recorded accretion expense of $45,930, increasing the carrying value of the convertible debentures to $250,000. | |

|

On January 19, 2012, the Company entered into a settlement agreement with one of the debenture holders to settle a $50,000 convertible debenture and $122,535 in accounts payable and accrued interest with the debt holder. Pursuant to the agreement, the debt holder agreed to reduce the debt to Cdn$100,000 on the condition that the Company pays the amount of Cdn$2,500 per month for 40 months, beginning March 1, 2012 and continuing on the first day of each month thereafter. | |

|

On July 18, 2012, the Company entered into a settlement agreement with the $150,000 debenture holder. Pursuant to the settlement agreement, the due date of the convertible debenture with a principal amount of $150,000 was extended to April 11, 2013, and the Company paid $43,890 of interest. In addition, commencing on October 31, 2012, the Company will pay accrued monthly interest at 10% per annum until April 11, 2013 when the Company will pay a $10,000 premium and the $150,000 outstanding principal. | |

|

The Company evaluated the modification and determined that the creditor did not grant a concession. In addition, as the present value of the future cash flows was less than 10% different than the cash flows of the original debt, it was determined that the original and new debt instruments are not substantially different. As a result, the modification was not treated as an extinguishment of the debt and no gain or loss is recognized. A new effective interest rate was calculated based on the carrying amount of the original instrument and the revised cash flows. |

F-6

MANTRA VENTURE GROUP LTD.

(A development stage

company)

Notes to the consolidated financial statements

Year ended August

31, 2012

(Expressed in U.S. dollars)

(unaudited)

| 8. |

Common Stock | |

| (a) |

As at August 31, 2012, the Company’s subsidiary, Climate ESCO Ltd., had received subscriptions for 210,000 shares of common stock at $0.10 per share for proceeds of $21,000, which is included in common stock subscribed net of the non-controlling interest portion of $7,384. | |

| (b) |

As at August 31, 2012, the Company had received subscriptions for 11,150,000 shares of common stock and 6,150,000 share purchase warrants to purchase one additional share of common stock at an exercise price of $0.15 per share expiring on the earlier of two years or five business days after the Company’s common stock trades at least one time per day on the FINRA Over the Counter Bulletin Board at a price at or above $0.30 per share for seven consecutive trading days for proceeds of $165,000, of which $70,000 was included in common stock subscribed as at May 31, 2012. | |

| (c) |

During the three months ended August 31, 2012, the Company’s subsidiary, Mantra Energy Alternatives Ltd., received the proceeds of $103,000 which was receivable as at May 31, 2012. In addition, the subsidiary received subscriptions for 282,000 shares of common stock at $1.00 per share for proceeds of Cdn$282,000 which is included in common stock subscribed net of the non-controlling interest portion of $22,701. | |

| (d) |

On June 29, 2012, the Company issued 1,333,333 shares of common stock at $0.015 per share for proceeds of $20,000, which was included in common stock subscribed as at May 31, 2012. | |

| (e) |

On July 9, 2012, the Company issued 826,000 shares of common stock at $0.05 per share for total proceeds of $41,300, which was included in common stock subscribed as at May 31, 2012. | |

| 9. |

Share Purchase Warrants | |

|

The following table summarizes the continuity of share purchase warrants: | ||

| Weighted | |||||||

| average | |||||||

| exercise | |||||||

| Number of | price | ||||||

| warrants | $ | ||||||

| Balance, May 31, 2012 | 7,745,992 | 0.20 | |||||

| Expired | (1,092,317 | ) | 0.20 | ||||

| Balance, August 31, 2012 | 6,653,675 | 0.20 |

As at August 31, 2012, the following share purchase warrants were outstanding:

| Exercise | ||||||||||||

| Number of | price | |||||||||||

| warrants | $ | Expiry date | ||||||||||

| 1,562,500 | 0.20 | October 22, 2012 | ||||||||||

| 275,000 | 0.20 | December 10, 2012 | ||||||||||

| 400,000 | 0.20 | December 25, 2012 | ||||||||||

| 1,048,125 | 0.20 | January 27, 2013 | ||||||||||

| 185,000 | 0.20 | March 28, 2013 | ||||||||||

| 25,000 | 0.20 | August 11, 2013 | ||||||||||

| 2,037,500 | 0.20 | August 31, 2013 | ||||||||||

| 1,120,550 | 0.20 | March 9, 2014 | ||||||||||

| 6,653,675 |

F-7

MANTRA VENTURE GROUP LTD.

(A development stage

company)

Notes to the consolidated financial statements

Year ended August

31, 2012

(Expressed in U.S. dollars)

(unaudited)

| 10. |

Stock Options |

|

The following table summarizes the continuity of the Company’s stock options: |

| Weighted | Weighted | ||||||||||||

| average | average | Aggregate | |||||||||||

| exercise | remaining | intrinsic | |||||||||||

| Number | price | contractual life | value | ||||||||||

| of options | $ | (years) | $ | ||||||||||

| Outstanding and exercisable, May 31, 2012 and August 31, 2012 | 1,300,000 | 0.10 | 0.78 | 84,000 |

Additional information regarding stock options as of August 31, 2012, is as follows:

| Exercise | ||||||||||||

| Number of | price | |||||||||||

| options | $ | Expiry date | ||||||||||

| 250,000 | 0.25 | November 1, 2012 | ||||||||||

| 500,000 | 0.10 | March 31, 2013 | ||||||||||

| 250,000 | 0.03 | April 3, 2014 | ||||||||||

| 200,000 | 0.05 | April 11, 2013 | ||||||||||

| 100,000 | 0.06 | May 1, 2014 | ||||||||||

| 1,300,000 |

| 11. |

Commitments and Contingencies | ||

| (a) |

On September 2, 2009, the Company entered into an agreement with a company to acquire a worldwide, exclusive license for the Mixed Reactant Flow-By Fuel Cell technology. The term of the agreement is for twenty years or the expiry of the last patent licensed under the agreement, whichever is later. The Company agreed to pay the licensor the following license fees: | ||

|

an initial license fee of Cdn$10,000 payable in two installments: Cdn$5,000 upon execution of the agreement (paid) and Cdn$5,000 within thirty days of September 2, 2009 (accrued); | |||

|

a further license fee of Cdn$15,000 (accrued) to be paid within ninety days of September 2, 2009; and | |||

|

an annual license fee, payable annually on the anniversary of the date of the agreement as follows: | |||

| September 1, 2010 | Cdn$10,000 (accrued) |

| September 1, 2011 | Cdn$20,000 (accrued) |

| September 1, 2012 | Cdn$30,000 |

| September 1, 2013 | Cdn$40,000 |

| September 1, 2014 and each successive anniversary |

Cdn$50,000 |

|

The Company is to pay the licensor a royalty calculated as 2% of the gross revenue and 15% of any and all consideration directly or indirectly received by the Company from the grant of any sublicense rights. The Company will pay interest at a rate of 1% per month on any amounts past due. In addition, the Company is responsible for the timely payment of all future costs relating to patent expenses and any new or useful art, process, machine, manufacture or composition of matter arising out of any licensor improvements or joint improvements licensed under this agreement and identified by the licensor as potentially patentable. The Company must also invest a minimum of Cdn$250,000 in research and development directly associated with the technology. | ||

| (b) |

On April 3, 2012, the Company entered into a consulting agreement with a company controlled by a director of the Company. Pursuant to the agreement, the Company issued 250,000 stock options and will pay $5,000 per month until April 3, 2013. | |

| (c) |

On April 4, 2012, the Company entered into a consulting agreement. Pursuant to the agreement, the Company will pay the consultant $4,500 for three months of consulting services commencing April 4, 2012 and $2,500 per month for consulting services after the initial three month term. |

F-8

MANTRA VENTURE GROUP LTD.

(A development stage

company)

Notes to the consolidated financial statements

Year ended August

31, 2012

(Expressed in U.S. dollars)

(unaudited)

| 11. |

Commitments and Contingencies (continued) | |

| (d) |

On April 11, 2012, the Company entered into a consulting agreement. Pursuant to the agreement, the Company issued the consultant 200,000 stock options and will pay the consultant $3,000 per month for a period of one year. | |

| (e) |

On May 23, 2012, a former employee of the Company delivered a Notice of Application seeking judgment against the Company for approximately $55,000. The hearing of that Application took place on July 31, 2012, at which time the former employee obtained judgment in the approximate amount of $55,000. The Company did not defend the amount of the judgment and the amount is included in accounts payable, but claims a complete set-off on the basis that the former employee retains 1,000,000 shares of common stock of the Company as security for payment of the outstanding consulting fees owed to him. On August 31, 2012, the Company commenced a separate action against the former employee seeking a return of the 1,000,000 shares of common stock and a stay of execution of the judgment. That application is pending and has not yet been heard or determined by the court. The payment of the judgment claim of approximately $55,000 is dependent upon whether the former employee will first return the 1,000,000 shares of common stock noted above. The probable outcome of the Company’s claim for the return of the shares cannot yet be determined. | |

| (f) |

On June 19, 2012, the Company entered into a service contract with a consultant to provide consulting services until February 19, 2013 for consideration of $171,000 plus the cost of materials. | |

| 12. |

Subsequent Event | |

|

On September 15, 2012, the Company entered into a consulting agreement. Pursuant to the agreement, the Company will pay the consultant $9,500 per month for six months of services and grant 200,000 stock options exercisable at $0.10 per share expiring on the earlier of September 15, 2014 or on the termination of the agreement. | ||

F-9

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

FORWARD LOOKING STATEMENTS

This quarterly report contains forward-looking statements. These statements relate to future events or our future financial performance. In some cases, you can identify forward-looking statements by terminology such as "may", "should", "expects", "plans", "anticipates", "believes", "estimates", "predicts", "potential" or "continue" or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors that may cause our or our industry's actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

Our unaudited financial statements are stated in United States Dollars (US$) and are prepared in accordance with United States Generally Accepted Accounting Principles. The following discussion should be read in conjunction with our financial statements and the related notes that appear elsewhere in this quarterly report. The following discussion contains forward-looking statements that reflect our plans, estimates and beliefs. Our actual results could differ materially from those discussed in the forward looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those discussed below and elsewhere in this quarterly report.

In this quarterly report, unless otherwise specified, all dollar amounts are expressed in United States dollars. All references to "US$" refer to United States dollars and all references to "common stock" refer to the common shares in our capital stock.

As used in this quarterly report, the terms "we", "us", "our" and "our company" mean Mantra Venture Group Ltd. and our wholly owned subsidiaries Carbon Commodity Corporation, Mantra Energy Alternatives Ltd., Mantra China Inc., Mantra China Limited, Mantra Media Corp., Mantra NextGen Power Inc., and Mantra Wind Inc., as well as our majority owned subsidiary Climate ESCO Ltd., unless otherwise indicated.

Business Overview

We were incorporated in Nevada on January 22, 2007. On December 8, 2008 we continued our corporate jurisdiction out of the state of Nevada and into the Province of British Columbia, Canada. Our principal offices are located at #562 – 800 15355 24th Avenue, Surrey, British Columbia, Canada, V4A 2H9. Our telephone number is (604) 560-1503. Our fiscal year end is May 31.

We are building a portfolio of companies and technologies that mitigate negative environmental and health consequences that arise from the production of energy and the consumption of resources.

Our mission is to develop and commercialize alternative energy technologies and services to enable the sustainable consumption, production and management of resources on residential, commercial and industrial scales. We plan to develop or acquire technologies and services which include electrical power system monitoring technology, wind farm electricity generation, online retail of environmental sustainability solutions through a carbon reduction marketplace, and media solutions to promote awareness of corporate actions that support the environment. To carry out our business strategy we intend to acquire or license from third parties technologies that require further development before they can be brought to market. We also intend to develop such technologies ourselves, and we anticipate that to complete commercialization of some technologies we will enter into joint ventures, partnerships, or other strategic relationships with third parties who have expertise that we may require. We also plan to enter into formal relationships with consultants, contractors, retailers and manufacturers who specialize in the areas of environmental sustainability in order to carry out our online retail strategy.

5

We are a development stage company that has only recently begun operations. We have generated only nominal revenues from our intended business activities, and we do not expect to generate significant revenues in the next 12 months. Other than our invention for the electro-reduction of carbon dioxide, we have not yet developed or acquired any commercially exploitable technology. Since our inception, we have incurred operational losses and we have completed several rounds of financing to fund our operations.

We carry on our business through our subsidiaries as follows:

- Mantra Energy Alternatives Ltd., through which we identify, acquire, develop and market technologies related to alternative energy production, greenhouse gas emissions reduction and resource consumption reduction;

- Mantra Media Corp., through which we offer promotional and marketing services to companies in the sustainability sector or those seeking to adopt sustainable practices; and

- Climate ESCO Ltd., majority owned, through which we distribute and install LED lighting solutions.

We also have a number of inactive subsidiaries which we plan to engage in various business activities in the future.

On February 20, 2012, we entered into a director agreement with Tommy David Unger. As compensation, under the director agreement, we granted stock options to Mr. Unger to purchase up to 500,000 shares of our common stock at a price of $0.01 per share. These options are non-transferrable, vest immediately and expire the earlier of 24 months, or upon the termination of the consulting agreement.

On February 29, 2012, our wholly owned subsidiary, Mantra Energy Alternatives Ltd., entered into subscription agreements with a number of non-US investors for the sale of 3,200,000 shares of Mantra Energy at a price of CAD $1.00 per share, for total proceeds of CAD $3,200,000. Upon the closing of this financing, our company will hold 6,000,000 shares of Mantra Energy out of a total of 9,200,000 issued and outstanding.

On April 3, 2012, we entered into a consulting agreement with BC0848571 Ltd., a company controlled by Tommy David Unger, a director of our company, whereby Mr. Unger has agreed to provide consulting services as our company’s vice president of corporate finance for a period of twelve (12) months. In consideration for agreeing to provide such consulting services by Mr. Unger, we have agreed to pay a salary of $5,000 per month and to grant 250,000 options to acquire 250,000 shares of our common stock at a purchase price of $0.03 per share. These options are non-transferrable, vest immediately and expire the earlier of 24 months, or upon the termination of the consulting agreement.

Effective June 19, 2012, our company’s subsidiary, Mantra Energy, entered into a service contract with PowerTech Labs Inc., whereby PowerTech will assist Manta Energy in the evaluation and the development of our ERC System under specific terms and conditions for a period ending February 19, 2013. As compensation, PowerTech will be paid $171,000 plus the cost of materials as further described in the service contract.

On October 28, 2008, we entered into a convertible debenture with StichtingAdministratiekantoor Carlos Bijl (“Bijl”) for a principal amount of $150,000 and an annual interest rate of 10%. Bijl started an action in the Supreme Court of British Columbia for non-payment of the convertible debenture.

6

On July 18, 2012, we entered into a settlement agreement with Bijl dated July 16, 2012, pursuant to which:

- the due date of the convertible debenture would be extended to April 11, 2013;

- within 5 business days we pay $43,890.41 representing net interest to and including September 30, 2012, less $15,000 we forwarded to Bijl on February 16, 2012;

- commencing on October 31, 2012 we will pay accrued monthly interest at 10% per annual until April 11, 2013;

- we will pay a $10,000 premium on the $150,000 principal of the convertible debenture when we satisfy it on April 11, 2013.

On July 31, 2012, Mantra Energy Alternatives Ltd. (“Mantra Energy”), a subsidiary of Mantra Venture Group Ltd., entered into a Master Services Agreement with Tekion (Canada), Inc. Mantra Energy’s ERC technology converts CO2 in stack gases to a formate salt which can then be further processed into formic acid or used to operate a fuel cell to generate power. Mantra Energy has engaged Powertech Labs to do further engineering on the system. In order to get this technology to commercialization, Tekion has proposed a program that will run in parallel to the Powertech program to help Mantra with some of the critical issues regarding this process.

Pursuant to the terms of the Master Services Agreement, Tekion will provide services to Mantra Energy as follows:

| 1. |

Mantra Energy will authorize provision of services from time to time by the execution of a Statement of Work (“SOW”). |

| 2. |

Tekion shall provide Mantra Energy with the deliverables, and on the terms, as specified in the SOW. |

| 3. |

Mantra Energy shall not be liable for any deliverable to be provided by Tekion unless and until the same is decided by Mantra Energy as being in compliance with the functions, features, capabilities, components, aspects, qualities and capacities described in any specification agreed to by the parties relating to deliverables. Mantra Energy shall not unreasonably withhold its acceptance of any such deliverable. |

| 4. |

Mantra Energy agrees to pay Tekion in the manner specified in each SOW. In addition, Mantra Energy will be responsible for and shall reimburse Tekion for any reasonable travel or other business consulting related expenses incurred by Tekion which directly relate to fulfilling a SOW, including, without limitation, air and other travel (including car rental) and lodging expenses, internet access while travelling, copying and reproduction and related expenses and cellular phone charges, including long distance, roaming and other related cellular phone charges. |

Also on July 31, 2012, Mantra Energy entered into a SOW with Tekion setting out the work summary, deliverables, budgets and timelines in several stages as follows:

Stage 1 – Baseline electrode/membrane materials

selection.

Budgeted Cost: $ 49,900 +

materials

Timeline: 8 weeks

Stage 2a – Reactor

scale-up

Budgeted Cost: $ 74,850 +

materials

Timeline: 12 weeks (parallel

with Stages 1, 2b)

Stage 2b – Improving catalyst functionality (if

required)

Budgeted Cost: $ 62,375 +

materials

Timeline: 10 weeks (parallel

with Stage 2a)

Stage 3 – Single cell

characterization

Budgeted Cost: $

49,900 + materials

Timeline: 4 weeks

7

Stage 4 – Conceptual 100 kg/day pilot plant design

Budgeted Cost:$ 24,950 +

materials

Timeline: 4 weeks

Mantra Energy provided an upfront payment to Tekion of $50,000 on the signing of the SOW.

Electro Reduction of Carbon Dioxide (“ERC”)

On November 2, 2007, through our subsidiary, Mantra Energy Alternatives Ltd., we entered into a technology assignment agreement with 0798465 BC Ltd. whereby we acquired 100% ownership in and to a certain chemical process for the electro-reduction of carbon dioxide as embodied by and described in the following patent cooperation treaty application:

| Country |

Application Number |

File Date |

Status |

| Patent Cooperation Treaty (PCT) |

W02207 |

10/13/2006 |

PCT |

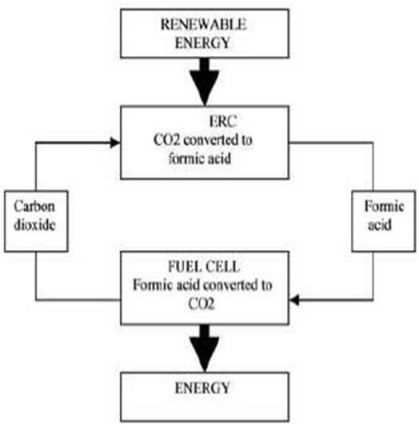

The reactor at the core of the chemical process, referred to as the electrochemical reduction of carbon dioxide, or ERC, has been proven functional through small scale prototype trials. ERC offers a possible solution to reduce the impact of carbon dioxide (CO2) on Earth’s environment by converting CO2 into chemicals with a broad range of commercial applications, including a fuel for a next generation of fuel cells. Powered by electricity, the ERC process combines captured carbon dioxide with water to produce materials, such as formic acid, formate salts, oxalic acid and methanol, that are conventionally obtained from the thermo-chemical processing of fossil fuels. However, while thermo-chemical reactions must be driven at relatively high temperatures that are normally obtained by burning fossil fuels, ERC operates at near ambient conditions and is driven by electric energy that can be taken from an electric power grid supplied by hydro, wind, solar or nuclear energy.

In fuel cells liquid fuels are indirectly burned with air to form carbon dioxide and water, while generating electricity. This process is known as electrochemical combustion or electrooxidation. The complementary nature of ERC and electrooxidation makes it possible to use ERC in a regenerative fuel cell cycle, where carbon dioxide is converted to a fuel that is consumed in a fuel cell to regenerate carbon dioxide. As shown in the figure, the net energy input required in this cycle could be supplied from a renewable or non-fossil fuel source.

8

ERC has been shown to produce a range of compounds, including formic acid, formate salts, oxalic acid, and methanol. The efficiency for generation of each compound depends on the experimental conditions, most importantly the material of the cathode, which catalyses the electrochemical reactions.

Until appropriate cathodes are found some products of CO2 reduction (methanol, for instance) are obtained at efficiencies too low for practical use. Other products can be generated on known cathodes with high current yields that could support valuable practical processes. For example, formic acid has been obtained on tin cathodes with current yields above 80%. Formate salts and sodium bicarbonate are obtained at similarly high yields.

ERC Development to Date

We have retained one of the creators of the technology, Professor Colin Oloman, as a member of our scientific advisory board, to further develop the carbon dioxide reduction process to achieve optimal results on a consistent basis. On June 1, 2008, we entered into a technology development and support agreement with Kemetco Research Inc., an integrated science, technology and innovation company. Pursuant to that agreement, we have established a research and development facility for the ERC in Vancouver, British Columbia, staffed by a dedicated research team provided by Kemetco.

In October of 2008, we completed our first ERC prototype reactor capable of processing 1 kilogram of CO2 per day. In order to facilitate the testing and development of this reactor, we entered into an agreement with Kemetco on January 29, 2010. The agreement was intended to govern the development and testing of our prototype reactor for a period of 10 months and contemplated costs of approximately $250,000 including labor and materials purchases. On March 18, 2010 we entered into another agreement with Kemetco which amended and replaced the January 29, 2010 agreement. Under the terms of the latest agreement, we have agreed to proceed with the testing and development of our ERC prototype reactor for a period of 5 months at an estimated cost of approximately $125,000.

9

In October of 2008, we completed our first ERC prototype reactor capable of processing 1 kilogram of CO2 per day. In order to facilitate the testing and development of this reactor, we entered into an agreement with Kemetco on January 29, 2010. The agreement was intended to govern the development and testing of our prototype reactor for a period of 10 months and contemplated costs of approximately $250,000 including labor and materials purchases. On March 18, 2010 we entered into another agreement with Kemetco which amended and replaced the January 29, 2010 agreement. Under the terms of the latest agreement, we have agreed to proceed with the testing and development of our ERC prototype reactor for a period of 5 months at an estimated cost of approximately $125,000.

Pictured Above, Design for Bench Scale ERC Reactor

We anticipate that commercialization of ERC will require us to develop reactors capable of processing not less than 100 tons of CO2 per day; however, there is no guarantee that we will successfully produce reactors of that size. Production of commercially viable ERC reactors will depend on continued research and development, successful testing of small scale ERC reactors, and securing of additional financing. At the conclusion of our current agreement and development program with Kemetco, an assessment will be made of the project’s progress and the next phase to be conducted.

Established and Emerging Market for ERC and By-Products:

The technology behind ERC can be applied to any scale commercial venture which outputs CO2 into the atmosphere. We anticipate that, once fully commercialized, we will be able to offer ERC as a CO2 management system to various industry including steel, power generation and lumber.

The existing applications of ERC by-products include use as feedstock preservatives, de-icing solutions, and baking soda, among others. Sodium Formate and Formic Acid, two of the main by-products of ERC, currently have an average market value of $1,200/ton, with more than 600,000 tons of formic acid produced annually (Li, 2006). Their applications are diverse, including feedstock preservatives, de-icing solutions, cleaning solutions and baking soda to name a few. The market for formic acid has experienced continual growth and demand over the past several years, mainly attributed to the following: European and developing country demand for formic acid in silage, rising raw materials, energy and logistics costs; and animal feed preservative and Asian demand for formic acid in leather, rubber, food and pharmaceutical industries. The average market price of formic acid is expected to increase by as much as 20% in 2012. (Dunia Frontier Consultants, 2008).

10

However, if the ERC process reaches market acceptance as a way to deal with CO2 emissions from industry facilities, it will likely lead to supply of formic acid in excess of current market demand. We have identified several potential future applications for formic acid, which may lead to an expansion in current market demand. The application we have identified and are currently focusing on is steel pickling.

Steel Pickling

Steel Pickling is part of the finishing process in the production of certain steel products in which oxide and scale are removed from the surface of strip steel, steel wire, and other forms of steel, by dissolution in acid. A solution of either Hydrochloric Acid (HCl) or Sulfuric Acid is generally used to treat carbon steel products, while a combination of Hydrofluoric and Nitric Acids is often used for stainless steel. Approximately ¼ of the HCI produced in the U.S. is used for pickling steel (American Chemistry, 2003), consuming an estimated 5Mt/year. As an organic acid, Formic Acid would be a very attractive replacement for Hydrochloric Acid (HCI) in the steel pickling process. Formic Acid has many potential advantages over HCI in this application, including: less iron lost from the steel surface, improvement in final surface quality, and the elimination of corrosion inhibiting and neutralizing rinse processes to prevent rust development. In addition, Formic Acid is both bio-degradable and reusable which would allow water used in the picking process to be recycled more easily.

Results of Operations for the Three Month Periods Ended August 31, 2012 and August 31, 2011.

Revenues

The following summary of our results of operations should be read in conjunction with our financial statements for the quarter ended August 31, 2012 which are included herein.

Our operating results for three month periods ended August 31, 2012 and August 31, 2011 are summarized as follows:

| Difference Between | |||||||||

| Three Month Period | |||||||||

| Ended | |||||||||

| Three Months | Three Months | August 31, 2012 | |||||||

| Ended | Ended | and | |||||||

| August 31, 2012 | August 31, 2011 | August 31, 2011 | |||||||

| ($) | ($) | ($) | |||||||

| Revenue | 3,027 | 550 | 2,477 | ||||||

| Cost of goods sold | 2,500 | 490 | 2,010 | ||||||

| Operating expenses | 349,831 | 242,740 | 107,091 | ||||||

| Other expense | 8,816 | 3,202 | 5,614 | ||||||

| Net Loss | (358,120 | ) | (245,882 | ) | (112,238 | ) |

We have had limited operational history since our inception on January 22, 2007. From our inception on January 22, 2007 to August 31, 2012 we have generated $38,812 in revenues. For the three months ended August 31, 2012 we generated $3,027 in revenues compared to revenues of $550 generated during the same period in 2011. From January 22, 2007 (inception) to August 31, 2012, we have an accumulated deficit of $7,034,226. We anticipate that we will incur substantial losses over the next year and our ability to generate additional revenues in the next 12 months remains uncertain.

Expenses

Our operating expenses for the three month periods ended August 31, 2012 and August 31, 2011 are summarized as follows:

11

| Three Months Ended | ||||||

| August 31, | August 31, | |||||

| 2012 | 2011 | |||||

| ($) | ($) | |||||

| Business development | 6,665 | 1,243 | ||||

| Consulting and advisory | 22,111 | 128,760 | ||||

| Depreciation and amortization | 5,825 | 7,195 | ||||

| Foreign exchange loss (gain) | 16,845 | (1,949 | ) | |||

| General and administrative | 12,278 | 6,070 | ||||

| Management fees | 78,000 | 48,000 | ||||

| Professional fees | 38,602 | 39,130 | ||||

| Public listing costs | 3,480 | 1,881 | ||||

| Rent | 4,500 | 8,671 | ||||

| Research and development | 89,787 | Nil | ||||

| Shareholder communications and awareness | 34,719 | Nil | ||||

| Travel and promotion | 37,019 | 3,739 | ||||

For the three months ended August 31, 2012, we incurred total expenses of $349,831 compared to total operating expenses for the three months ended August 31, 2011 of $242,740. The $107,091 increase is primarily due to increased foreign exchange loss, general and administrative expenses, management fees, public listing costs, research and development, shareholder communications and awareness and travel and promotion.

Net Loss

Since our inception on January 22, 2007 to August 31, 2012, we have incurred a net loss of $7,161,285. For the three months ended August 31, 2012 we have incurred a net loss of $348,120 compared to a net loss of $245,882 for the same period in 2011. Our net loss per share for the three months ended August 31, 2012 was $0.01, compared to $0.01 for the same period in 2011.

Liquidity and Capital Resources

| Working Capital | ||||||

| At | ||||||

| August 31, | May 31, | |||||

| 2012 | 2012 | |||||

| Current Assets | $ | 366,680 | $ | 274,360 | ||

| Current Liabilities | $ | 1,198,727 | $ | 1,208,690 | ||

| Working Capital Deficit | $ | (832,047 | ) | $ | (934,330 | ) |

| Cash Flows | January 22, | ||||||||

| Three Months | Three Months | 2007 | |||||||

| Ended | Ended | (Inception) to | |||||||

| August 31, | August 31, | August 31, | |||||||

| 2012 | 2011 | 2012 | |||||||

| Net Cash Used in Operating Activities | $ | (440,654 | ) | $ | (107,411 | ) | $ | (4,252,087 | ) |

| Net Cash Used In Investing Activities | $ | (8,406 | ) | $ | Nil | $ | (185,005 | ) | |

| Net Cash Provided by Financing Activities | $ | 472,089 | $ | 90,218 | $ | 4,675,721 | |||

| Change In Cash | $ | 23,029 | $ | (17,193 | ) | $ | 238,629 |

As of August 31, 2012, we had $238,629 cash in our bank accounts and a working capital deficit of $832,047. As of August 31, 2012 we had total assets of $422,992 and total liabilities of $1,272,773.

12

From January 22, 2007 (date of inception) to August 31, 2012, we raised net proceeds of $4,232,061 in cash from the issuance of common stock and share subscriptions received, $201,571 from loans payable and $250,000 from proceeds from the issuance of convertible debentures offset by repayment of loans payable of $7,609 and repayment of capital lease obligations of $302 for a total of $4,675,721 of cash provided by financing activities for the period.

We received net cash of $472,089 from financing activities for the three months ended August 31, 2012 compared to $90,218 for the same period in 2011. During the period in 2012 we raised cash from the issuance of our common stock and share subscriptions received. In the comparable period, we also raised cash in the same manner.

We used net cash of $440,654 in operating activities for the three months ended August 31, 2012 compared to $107,411 for the same period in 2011. We used net cash of $4,252,087 in operating activities for the period from January 22, 2007 (date of inception) to August 31, 2012.

We used cash of $8,406 in investing activities for the three months ended August 31, 2012 compared to $nil for the same period in 2011.

During the three months ended August 31, 2012 we had a net increase of $23,029 in our cash position compared to a net decrease of $17,193 for the same period in 2011. Our monthly cash requirements for the three month period ended August 31, 2012 was approximately $146,885 compared to $35,803 for the same period in 2011. At our current cash position and if this cash requirement continues, we do not have sufficient cash to cover our expenses for one month.

We expect that our total expenses will increase over the next year as we increase our business operations. We have not been able to reach the break-even point since our inception and have had to rely on outside capital resources. We do not anticipate making significant revenues for the next year. Over the next 12 months, we plan to primarily concentrate on commercializing our ERC technology and associated projects.

| Description |

Estimated expenses ($) |

| Research and Development | 2,200,000 |

| Consulting Fees | 250,000 |

| Commercialization of ERC | 1,300,000 |

| Shareholder communication and awareness | 200,000 |

| Professional Fees | 300,000 |

| Wages and Benefits | 200,000 |

| Management Fees | 150,000 |

| Total | 4,600,000 |

In order to fully carry out our business plan, we need additional financing of approximately $4,600,000 for the next 12 months. In order to improve our liquidity, we intend to pursue additional equity financing from private placement sales of our equity securities or shareholders’ loans. We do not presently have sufficient financing to undertake our planned business activities. Issuances of additional shares will result in dilution to our existing shareholders.

We currently do not have any arrangements in place for the completion of any further private placement financings and there is no assurance that we will be successful in completing any further private placement financings. If we are unable to achieve the necessary additional financing, then we plan to reduce the amounts that we spend on our business activities and administrative expenses in order to be within the amount of capital resources that are available to us.

13

Off-Balance Sheet Arrangements

We have no significant off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that is material to stockholders.

Inflation

The effect of inflation on our revenue and operating results has not been significant.

Critical Accounting Policies

Our consolidated financial statements are impacted by the accounting policies used and the estimates and assumptions made by management during their preparation. A complete summary of these policies is included in note 2 of the notes to our financial statements. We have identified below the accounting policies that are of particular importance in the presentation of our financial position, results of operations and cash flows, and which require the application of significant judgment by management.

Use of Estimates

The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Our company regularly evaluates estimates and assumptions related to allowance for doubtful accounts, the estimated useful lives and recoverability of long-lived assets, valuation of inventory, stock-based compensation, and deferred income tax asset valuation allowances. Our company bases its estimates and assumptions on current facts, historical experience and various other factors that it believes to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities and the accrual of costs and expenses that are not readily apparent from other sources. The actual results experienced by our company may differ materially and adversely from our company’s estimates. To the extent there are material differences between the estimates and the actual results, future results of operations will be affected.

Long-lived Assets

In accordance with ASC 360, “Property, Plant and Equipment”, our company tests long-lived assets or asset groups for recoverability when events or changes in circumstances indicate that their carrying amount may not be recoverable. Circumstances which could trigger a review include, but are not limited to: significant decreases in the market price of the asset; significant adverse changes in the business climate or legal factors; accumulation of costs significantly in excess of the amount originally expected for the acquisition or construction of the asset; current period cash flow or operating losses combined with a history of losses or a forecast of continuing losses associated with the use of the asset; and current expectation that the asset will more likely than not be sold or disposed significantly before the end of its estimated useful life. Recoverability is assessed based on the carrying amount of the asset and its fair value, which is generally determined based on the sum of the undiscounted cash flows expected to result from the use and the eventual disposal of the asset, as well as specific appraisal in certain instances. An impairment loss is recognized when the carrying amount is not recoverable and exceeds fair value.

Stock-based Compensation

Our company records stock-based compensation in accordance with ASC 718, “Compensation – Stock Compensation”, using the fair value method. All transactions in which goods or services are the consideration received for the issuance of equity instruments are accounted for based on the fair value of the consideration received or the fair value of the equity instrument issued, whichever is more reliably measurable.

Our company uses the Black-Scholes option pricing model to calculate the fair value of stock-based awards. This model is affected by our company’s stock price as well as assumptions regarding a number of subjective variables. These subjective variables include, but are not limited to our company’s expected stock price volatility over the term of the awards, and actual and projected employee stock option exercise behaviors. The value of the portion of the award that is ultimately expected to vest is recognized as an expense in the consolidated statement of operations over the requisite service period.

Recent Accounting Pronouncements

Our company has implemented all new accounting pronouncements that are in effect and that may impact its financial statements and does not believe that there are any other new accounting pronouncements that have been issued that might have a material impact on its financial position or results of operations.

14

Item 3. Quantitative and Qualitative Disclosures About Market Risk

As a “smaller reporting company”, we are not required to provide the information required by this Item.

Item 4. Controls and Procedures

Evaluation of Disclosure Controls and Procedures

We maintain disclosure controls and procedures that are designed to ensure that information required to be disclosed in our reports filed under the Securities Exchange Act of 1934, as amended, is recorded, processed, summarized and reported within the time periods specified in the Securities and Exchange Commission's rules and forms, and that such information is accumulated and communicated to our management, including our chief executive officer and chief financial officer (our principal executive officer, principal financial officer and principal accounting officer) to allow for timely decisions regarding required disclosure.

As of the end of our quarter covered by this report, we carried out an evaluation, under the supervision and with the participation of our chief executive officer and chief financial officer (our principal executive officer, principal financial officer and principal accounting officer), of the effectiveness of the design and operation of our disclosure controls and procedures. Based on the foregoing, our chief executive officer and chief financial officer (our principal executive officer, principal financial officer and principal accounting officer) concluded that our disclosure controls and procedures were not effective as of the end of the period covered by this quarterly report.

Changes in Internal Controls

During the period covered by this report there were no changes in our internal control over financial reporting that materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

PART II – OTHER INFORMATION

Item 1. Legal Proceedings

On May 23, 2012, a former employee of our company delivered a Notice of Application seeking judgment against our company for approximately $55,000. The hearing of that Application took place on July 31, 2012, at which time the former employee obtained judgment in the approximate amount of $55,000. Our company did not defend the amount of the judgment and the amount is included in accounts payable, but claims a complete set-off on the basis that the former employee retains 1,000,000 shares of common stock of our company as security for payment of the outstanding consulting fees owed to him.

On August 31, 2012, our company commenced a separate action against the former employee seeking a return of the 1,000,000 shares of common stock and a stay of execution of the judgment. That application is pending and has not yet been heard or determined by the court. The payment of the judgment claim of approximately $55,000 is dependent upon whether the former employee will first return the 1,000,000 shares of common stock noted above. The probable outcome of our company’s claim for the return of the shares cannot yet be determined.

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds

On June 29, 2012, we issued 1,333,333 shares of common stock at $0.015 per share for proceeds of $20,000, which was included in common stock subscribed as at May 31, 2012. We have issued all of the shares to one non-US persons relying on Regulation S of the Securities Act of 1933.

On July 9, 2012, we issued 826,000 shares of common stock at $0.05 per share for total proceeds of $41,300, which was included in common stock subscribed as at May 31, 2012. We have issued all of the shares to six non-US persons relying on Regulation S of the Securities Act of 1933.

15

Item 3. Defaults Upon Senior Securities

None.

Item 4. Mine Safety Disclosures

Not applicable.

Item 5. Other Information

None.

Item 6. Exhibits

| Exhibit | |

| Number | Exhibit Description |

| (2) | Plan of acquisition, reorganization, arrangement, liquidation or succession |

| 2.1 |

Plan of Conversion of Mantra Venture Group Ltd. from a Nevada Corporation into a British Columbia Corporation dated October 29, 2008. (incorporated by reference to our Current Report on Form 8-K filed with the SEC on November 4, 2008) |

| (3) |

Articles of Incorporation, Bylaws |

| 3.1 |

Articles of Conversion of Mantra Venture Group Ltd. dated October 28, 2008 (incorporated by reference to our Current Report on Form 8-K filed with the SEC on November 4, 2008) |

| 3.2 |

British Columbia Table 1 Articles adopted on December 4, 2008 (incorporated by reference to our Current Report on Form 8-K filed with the SEC on December 12, 2008) |

| 3.3 |

British Columbia Notice of Articles (incorporated by reference to our Current Report on Form 8-K filed with the SEC on December 12, 2008) |

| (10) |

Material Contracts |

| 10.1 |

Revolving Line of Credit Agreement with Larry Kristof dated October 15, 2008 (incorporated by reference to our Quarterly Report on Form 10-Q filed with the SEC on January 14, 2009) |

| 10.2 |

Sponsorship and Proposed Equity Capital Raise Agreement with M Partners Inc. dated December 4, 2008. (incorporated by reference to our Current Report on Form 8-K filed with the SEC on December 11, 2008) |

| 10.3 |

Contractor Proposal Agreement with Kemetco Research Inc. on January 29, 2009. (incorporated by reference to our Current Report on Form 8-K filed with the SEC on February 4, 2009) |

| 10.4 |

Option Agreement entered into with Synergy BioMetals Recovery Systems Inc. on February 27, 2009. (incorporated by reference to our Current Report on Form 8-K filed with the SEC on March 2, 2009) |

| 10.5 |

Extension of Option Agreement with Synergy BioMetals Recovery Systems Inc. on May 1, 2009. (incorporated by reference to our Annual Report on Form 18-K filed with the SEC on September 15, 2009) |

| 10.6 |

Contractor Proposal Agreement with Kemetco Research Inc. on March 18, 2009. (incorporated by reference to our Current Report on Form 8-K filed with the SEC on March 26, 2009) |

| 10.7 |

Development Agreement with 3M dated October 28, 2009. (incorporated by reference to our Current Report on Form 8-K filed with the SEC on November 6, 2009) |

16

| Exhibit | |

| Number | Exhibit Description |

| 10.8 | Technology Development Cooperation Agreement with Korean Southern Power Co., Ltd. and KC Cottrell Co., Ltd. on August 16, 2010 (incorporated by reference to our Current Report on Form 8-K filed with the SEC on August 17, 2010) |

|

|

|

| 10.9 | Director Agreement with Tommy David Unger dated February 20, 2012 (incorporated by reference to our Current Report on Form 8-K filed with the SEC on February 28, 2012) |

|

|

|

| 10.10 | Subscription Agreement with Mantra Energy Alternatives Ltd. dated February 29, 2012 (incorporated by reference to our Current Report on Form 8-K filed with the SEC on March 9, 2012) |

|

|

|

| 10.11 | Consulting Agreement with BC0848571 Ltd. dated April 3, 2012 (incorporated by reference to our Current Report on Form 8-K filed with the SEC on April 11, 2012) |

|

|

|

| 10.12 | Service Contract with Powertech Labs Inc. dated June 19, 2012 (incorporated by reference to our Current Report on Form 8-K filed with the SEC on June 25, 2012) |

|

|

|

| 10.13 | Settlement Agreement with StichtingAdministratiekantoor Carlos Bijl dated July 16, 2012 (incorporated by reference to our Current Report on Form 8-K filed with the SEC on July 23, 2012) |

|

|

|

| 10.14 | Master Services Agreement between our subsidiary, Mantra Energy Alternatives Ltd., and Tekion (Canada), Inc. dated July 31, 2012 (incorporated by reference to our Current Report on Form 8-K filed with the SEC on August 30, 2012) |

|

|

|

| 10.15 | Statement of Work between our subsidiary, Mantra Energy Alternatives Ltd., and Tekion (Canada), Inc. dated July 31, 2012 (incorporated by reference to our Current Report on Form 8-K filed with the SEC on August 30, 2012) |

|

|

|

| (14) | Code of Ethics |

|

|

|

| 14.1 | Code of Ethics and Business Conduct (incorporated by reference to our Registration Statement on Form S-1 filed with the SEC on February 26, 2008) |

|

|

|

| (21) | List of Subsidiaries |

|

|

|

| 21.1 | Carbon Commodity Corporation |

| Climate ESCO Ltd. |

|

| Mantra Energy Alternatives Ltd. |

|

| Mantra China Inc. |

|

| Mantra China Limited |

|

| Mantra Media Corp. |

|

| Mantra NextGen Power Inc. |

|

| Mantra Wind Inc. |

|

| (31) | (i) Rule 13a-14(a)/ 15d-14(a) Certifications (ii) Rule 13a-14(d)/ 15d-14(d) Certifications |

|

|

|

| 31.1* | |

|

|

|

| (32) | Section 1350 Certifications |

|

|

|

| 32.1* | |

|

|

|

| (99) | Additional Exhibits |

|

|

|

| 99.1 | Audit Committee Charter adopted April 20, 2010 (incorporated by reference to our Annual Report on Form 10-K filed with the SEC on September 14, 2010) |

17

| Exhibit | |

| Number | Exhibit Description |

| (101)** | Interactive Data Files |

| 101.INS | XBRL Instance Document |

| 101.SCH | XBRL Taxonomy Extension Schema Document. |

| 101.CAL | XBRL Taxonomy Extension Calculation Linkbase Document. |

| 101.DEF | XBRL Taxonomy Extension Definition Linkbase Document. |

| 101.LAB | XBRL Taxonomy Extension Label Linkbase Document. |

| 101.PRE | XBRL Taxonomy Extension Presentation Linkbase Document. |

| * |

Filed herewith. |

| ** |

Furnished herewith. Pursuant to Rule 406T of Regulation S-T, the Interactive Data Files on Exhibit 101 hereto are deemed not filed or part of any registration statement or prospectus for purposes of Sections 11 or 12 of the Securities Act of 1933, are deemed not filed for purposes of Section 18 of the Securities and Exchange Act of 1934, and otherwise are not subject to liability under those sections. |

18

SIGNATURES

In accordance with the requirements of the Exchange Act, the registrant caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Mantra Venture Group Ltd. | |

| (Registrant) | |

| Date: October 22, 2012 | /s/ Larry Kristof |

| Larry Kristof | |

| President, Chief Executive Officer, Chief Financial | |

| Officer, Secretary, Treasurer and Director | |

| (Principal Executive Officer, Principal Financial Officer | |

| and Principal Accounting Officer) |

19