UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

OR

For the fiscal year ended

OR

OR

Date of event requiring this shell company report

For the transition period from to

Commission file number:

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

People’s Republic of

(Address of principal executive offices)

Tel:

E-mail:

Fax: +

People’s Republic of

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Ticker Symbol(s) | Name of Each Exchange on Which Registered | ||

| The | ||||

| (The |

| * | Not for trading, but only in connection with the listing on The NASDAQ Global Select Market of American depositary shares, each representing 20 ordinary shares. |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the Issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ☐ | ||

| Non-accelerated filer ☐ | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards † provided pursuant to Section 13(a) of the Exchange Act. ☐

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Indicate by check mark whether

the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control

over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that

prepared or issued its audit report.

If securities are registered

pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing

reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| International Financial Reporting Standards as issued Other ☐ | ||

| by the International Accounting Standards Board ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

Yes ☐ No ☐

TABLE OF CONTENTS

- i -

INTRODUCTION

In this annual report, unless the context otherwise requires:

| ● | “ADSs” refer to our American depositary shares, each of which represents 20 ordinary shares; | |

| ● | “China” or “PRC” refers to the People’s Republic of China, including the special administrative regions of Hong Kon and Macau (“Hong Kong ASR” and “Macao SAR”), and only when this annual report refers to specific laws and regulations adopted by the PRC, reference to “China” or the “PRC” excludes Taiwan, Hong Kong SAR and Macau SAR). Unless the context otherwise indicates, the legal and operational risks associated with operating in China discussed in this annual report also apply to any operations we may now or in the future carry out in Hong Kong SAR or Macau; | |

| ● | “consolidated VIEs” refer to Shenzhen Xinbao Investment Management Co., Ltd. (“Xinbao Investment”), Fanhua RONS (Beijing) Technologies Co., Ltd. (“Fanhua RONS Technologies”) and their subsidiaries; | |

| ● | “customer” refers to policyholder or our insurance company partner which we define as customer under ASC 606; and | |

| ● | “HK$” and “HK dollars” refer to the legal currency of Hong Kong SAR; | |

| ● | “Parent” refers to Fanhua Inc., a Cayman Islands holding company; | |

| ● | “provinces” of China refer to the 23 provinces, the four municipalities directly administered by the central government (Beijing, Shanghai, Tianjin and Chongqing), the five autonomous regions (Xinjiang, Tibet, Inner Mongolia, Ningxia and Guangxi), excluding, solely for the purpose of this annual report, Taiwan, Hong Kong SAR and Macau SAR; | |

| ● | “RMB” or “Renminbi” refers to the legal currency of China; | |

| ● | “shares” or “ordinary shares” refer to our ordinary shares, par value US$0.001 per share; | |

| ● | “US$” or “U.S. dollars” refers to the legal currency of the United States; and | |

| ● | “we,” “us,” “our company,” “the Company”, “our” or “Fanhua” refers to Fanhua Inc., formerly known as CNinsure Inc. and its subsidiaries and, in the context of describing its operations and consolidated financial information, its variable interest entities which are its consolidated affiliated entities, if applicable. As described elsewhere in this annual report, we do not own the VIEs, and the results of the VIEs’ operations only accrue to us through contractual arrangements between the VIEs, the VIEs’ nominee shareholders, and certain of our subsidiaries. Accordingly, in appropriate contexts we will describe the VIEs’ activities separately from those of our directly and indirectly owned subsidiaries, and our use of the terms “we,” “us,” and “our” may not include the VIEs in those contexts. |

- ii -

Unless otherwise noted, all translations from Renminbi to U.S. dollars and from U.S. dollars to Renminbi in this annual report are made at a rate of RMB7.0999 to US$1.00, the exchange rate in effect as of December 29, 2023 as set forth in the H.10 statistical release of the Board of Governors of the Federal Reserve System. We make no representation that any Renminbi or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or Renminbi, as the case may be, at any particular rate, or at all. All discrepancies in any table between the amounts identified as total amounts and the sum of the amounts listed therein are due to rounding.

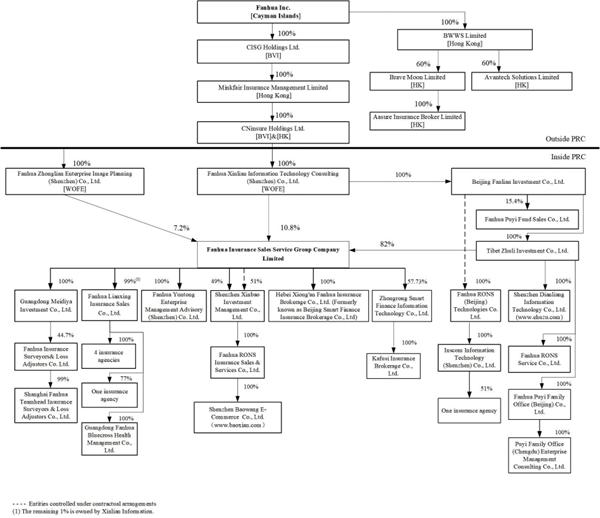

Our Corporate Structure

Fanhua Inc. is a Cayman Islands holding company primarily operating in China through (i) its PRC subsidiaries, including Fanhua Zhonglian Enterprise Image Planning (Shenzhen) Co., Ltd., or Zhonglian Enterprise, and Fanhua Xinlian Information Technology Consulting (Shenzhen) Co., Ltd., or Xinlian Information, and their subsidiaries in which we hold equity ownership interests, and (ii) contractual arrangements among (x) our wholly-owned PRC subsidiaries Fanhua Insurance Sales Service Group Company Limited, or Fanhua Group Company and Beijing Fanlian Investment Co., Ltd., or Fanlian Investment, (y) the consolidated VIEs, namely, Shenzhen Xinbao Investment Management Co., Ltd., or Xinbao Investment, and Fanhua RONS (Beijing) Technologies Co., Ltd., or Fanhua RONS Technologies, two limited liability companies established under PRC law, and (z) the individual nominee shareholders of the consolidated VIEs. Fanhua Inc. holds 49% equity interests in Xinbao Investment. Investors in the ADSs thus are not purchasing, and may never directly hold all equity interests in the consolidated VIEs. PRC laws, regulations, and rules restrict and impose conditions on direct foreign investment in certain types of business, and we therefore operate these businesses in China through the consolidated VIEs. For a summary of these contractual arrangements, see “Item 4. Information on the Company—C. Organizational Structure.” As used in this annual report, “we”, “us”, or “our” refers to Fanhua Inc. and its subsidiaries.

Our corporate structure is subject to risks relating to our contractual arrangements with Xinbao Investment, Fanhua RONS Technologies and their individual nominee shareholders. If the PRC government finds these contractual arrangements non-compliant with the restrictions on direct foreign investment in the relevant industries, or if the relevant PRC laws, regulations, and rules or the interpretation thereof change in the future, we could be subject to severe penalties or be forced to relinquish our interests in the consolidated VIEs or forfeit our rights under the contractual arrangements. Fanhua Inc. and investors in the ADSs face uncertainty about potential future actions by the PRC government, which could affect the enforceability of our contractual arrangements with Xinbao Investment and Fanhua RONS Technologies and, consequently, significantly affect the financial condition and results of operations of Fanhua Inc. If we are unable to claim our right to control the assets of the consolidated VIEs, the ADSs may decline in value or become worthless. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure.”

We face various legal and operational risks and uncertainties relating to doing business in China. We operate our business primarily in China, and are subject to complex and evolving PRC laws and regulations. For example, we face risks relating to regulatory approvals in connection with a future offering of our securities to foreign investors, oversight on cybersecurity and data privacy, and the expanding efforts in anti-monopoly enforcement. Uncertainties in the PRC legal system and the interpretation and enforcement of PRC laws and regulations could limit the legal protection available to you and us, hinder our ability to offer or continue to offer the ADSs, result in a material adverse effect on our business operations, and damage our reputation, which might further cause the ADSs to significantly decline in value or become worthless. See “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China.”

- iii -

FORWARD-LOOKING INFORMATION

This annual report contains forward-looking statements that reflect our current expectations and views of future events. These forward-looking statements are made under the “safe-harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. Known and unknown risks, uncertainties, and other factors, may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements. These statements involve known and unknown risks, uncertainties, and other factors, including those listed under “Item 3. Key Information—D. Risk Factors,” that may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements.

You can identify these forward-looking statements by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “likely to,” “potential,” “continue” or other similar expressions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. These forward-looking statements include, but are not limited to, statements about our goals and growth strategies, our future business development, financial condition and results of operations, our expectations regarding demand for and market acceptance of our products and services, and assumptions underlying or related to any of the foregoing.

Although we believe that our expectations expressed in these forward-looking statements are reasonable, our expectations may later be found to be incorrect. Our actual results could be materially different from our expectations. Moreover, we operate in an evolving environment. New risk factors and uncertainties emerge from time to time, and it is not possible for our management to predict all risk factors and uncertainties, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

You should not place undue reliance on these forward-looking statements. The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events. You should read this annual report and the documents that we refer to in this annual report and exhibits to this annual report completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements.

- iv -

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not Applicable.

Item 2. Offer Statistics and Expected Timetable

Not Applicable.

Item 3. Key Information

The Consolidated VIEs and China Operations

Fanhua Inc. is a Cayman Islands holding company primarily operating in China through (i) its PRC subsidiaries, including Zhonglian Enterprise and Xinlian Information, and their subsidiaries in which we hold equity ownership interests, and (ii) contractual arrangements among (x) our wholly-owned PRC subsidiary Fanhua Group Company and Fanlian Investment, (y) the consolidated VIEs, Xinbao Investment and Fanhua RONS Technologies, limited liability companies established under PRC law, and (z) the individual nominee shareholders of the consolidated VIEs. Fanhua Inc. holds 49% equity interests in Xinbao Investment. Investors in the ADSs thus are not purchasing, and may never directly hold all equity interests in the consolidated VIEs. PRC laws, regulations, and rules restrict and impose conditions on direct foreign investment in certain types of business, and we therefore operate these businesses in China through the consolidated VIEs.

We commenced a restructuring in August 2021 to re-establish the VIE structure for our online insurance business where our direct equity interests in Xinbao Investment were reduced from 100% to 49% and the remaining 51% was nominally held by an employee of the Company on behalf of the Company. The restructuring completed in December 2021. Concurrently, our wholly-owned PRC subsidiary, Fanhua Group Company, entered into contractual arrangements with Xinbao Investment and the individual nominee shareholder. These agreements include:(i) a technology consulting and service agreement, which enables us to receive all of the economic benefits of Xinbao investment and its subsidiaries, (ii) a loan agreement, powers of attorney and an equity pledge agreement, which provide us with effective control over Xinbao Investment, and (iii) an exclusive purchase option agreement, which provides us with the option to purchase part of the equity interests in Xinbao Investment.

On June 24, 2022, our wholly owned subsidiary Fanlian Investment transferred all of the equity interests in Fanhua RONS Technologies to Mr. Peng Ge, our chief financial officer to hold the shares of Fanhua RONS Technologies nominally on behalf of the Company. Concurrently, Fanlian Investment entered into contractual arrangements with Fanhua RONS Technologies and Mr. Ge. The contractual arrangements are substantially similar to those among Fanhua Group Company, Xinbao Investment and its individual nominee shareholder.

For more details of the restructuring and the contractual arrangements, see “Item 4. Information on the Company—C. Organizational Structure.”

In the opinion of the Company’s PRC legal counsel, (i) the ownership structure relating to the consolidated VIEs of the Company is in compliance with existing PRC laws and regulations; (ii) the contractual arrangements with the consolidated VIEs and the individual shareholders are legal, valid and binding obligation of such party, and enforceable against such party in accordance with their respective terms; and (iii) the execution, delivery and performance of the consolidated VIEs and its shareholders do not result in any violation of the provisions of the articles of association and business licenses of the consolidated VIEs, and any violation of any current PRC laws and regulations.

However, control through these contractual arrangements may be less effective than direct ownership, and we could face heightened risks and costs in enforcing these contractual arrangements, because there are substantial uncertainties regarding the interpretation and application of current and future PRC laws, regulations, and rules relating to these contractual arrangements, and these contractual arrangements have not been tested in a court of law. If the PRC government finds such agreements non-compliant with relevant PRC laws, regulations, and rules, or if these laws, regulations, and rules or the interpretation thereof change in the future, we could be subject to severe penalties or be forced to relinquish our interests in Xinbao Investment and Fanhua RONS Technologies or forfeit our rights under the contractual arrangements. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—If the PRC government finds that the contractual arrangements that establish the structure for operating part of our China business does not comply with applicable PRC laws and regulations, we could be subject to severe penalties.” and “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—We rely on contractual arrangements with our consolidated VIEs, Xinbao Investment and Fanhua RONS Technologies, and their shareholders to conduct a small part of our China operations, which may not be as effective in providing operational control as direct ownership, and these contractual arrangements have not been tested in a court of law.”

- 1 -

The following diagram illustrates the corporate structure of us and the consolidated VIEs, including the names, places of incorporation and the proportion of ownership interests in our and the consolidated VIEs’ significant subsidiaries and their respective subsidiaries as of March 31, 2024:

The diagram above omits the names of subsidiaries that are immaterial individually and in the aggregate. For a complete list of our subsidiaries as of March 31, 2024, see Exhibit 8.1 to this annual report.

Permissions and Licenses for Our Operations in PRC

We conduct our business primarily through our subsidiaries, the VIEs, and their subsidiaries in China. As of the date of this annual report, our subsidiaries, the VIEs, and their subsidiaries in China have obtained the requisite licenses and permits from the PRC government authorities that are material for our operations in China, including, among others, the business license, insurance distribution licenses, insurance broker licenses and insurance claims adjusting licenses. The business license is a permit issued by China’s State Administration for Market Regulation that allows a company to conduct specific business within the government’s geographical jurisdiction. Insurance distribution licenses, insurance broker licenses and insurance claims adjusting licenses are issued by the National Financial Regulatory Administration or NFRA or by Hong Kong SAR Insurance Authority, allowing enterprises to engage in insurance agency, brokerage or claims adjusting services, respectively. Theses licenses are the only permissions and approvals that our PRC subsidiaries are required to obtain to conduct our business in China. However, there can be no assurance that we will be able to obtain, renew and/or convert all of the approvals, licenses, and permits required for our existing business operations upon their expiration in a timely manner or duly complete necessary registration or filings with the relevant governmental authorities for any of our new business.

- 2 -

The following chart sets forth a summary of the licenses and permissions obtained by the principal PRC subsidiaries and VIEs as of the date of this annual report:

| S.N. | License/Permit | Subsidiary/VIE | Government Agency | Date of Grant | Date of Expiration | |||||

| 1 | National Insurance Distribution License | Fanhua Insurance Sales Service Group Co., Ltd. |

China Banking and Insurance Regulatory Commission (“CBIRC”) Guangdong Branch |

July 15, 2022 | Long-term Validity | |||||

| 2 | National Insurance Distribution License | Fanhua Lianxing Insurance Sales Co., Ltd. |

CBIRC Sichuan Branch | May 16, 2022 | Long-term Validity | |||||

| 3 | National Insurance Distribution License | Fanhua RONS Insurance Sales & Services Co., Ltd. |

CBIRC Shenzhen Branch |

September 10, 2021 | Long-term Validity | |||||

| 4 | Regional Insurance Distribution License | Shanghai Fanhua Guosheng Insurance Agency Co., Ltd. |

CBIRC Shanghai Branch |

June 12, 2023 | Long-term Validity | |||||

| 5 | Regional Insurance Distribution License | Hunan Fanhua Insurance Agency Co., Ltd. |

CBIRC Hunan Branch | April 17, 2023 | Long-term Validity | |||||

| 6 | Regional Insurance Distribution License | Zhejiang Fanhua Tongchuang Insurance Agency Co., Ltd. |

CBIRC Zhejiang Branch |

April 24, 2022 | Long-term Validity | |||||

| 7 | Regional Insurance Distribution License | Liaoning Fanhua Gena Insurance Agency Co., Ltd. |

NFRA Liaoning Branch | August 31, 2023 | Long-term Validity | |||||

| 8 | Regional Insurance Distribution License | Jiangsu Fanhua Lianchuang Insurance Agency Co., Ltd. |

NFRA Jiangsu Branch | March 14, 2024 | Long-term Validity | |||||

| 9 | Regional Insurance Distribution License | Jilin Zhongji Shi’an Insurance Agency Co., Ltd. |

CBIRC Jilin Branch | September 24, 2003 | Long-term Validity | |||||

| 10 | National Insurance Broker License | Kafusi Insurance Brokerage Co., Ltd. |

CBIRC Guangdong Branch |

December 28, 2022 | August 14, 2025 | |||||

| 11 | National Insurance Broker License | Hebei Xiong’an Fanhua Insurance Brokerage Co., Ltd. |

NFRA Hebei Branch | September 7, 2023 | October 1, 2024 | |||||

| 12 | Insurance Claims Adjusting License | Shanghai Fanhua Teamhead Insurance Surveyors & Loss Adjustors Co., Ltd. |

NFRA Shanghai Branch | N/A | Long-term Validity | |||||

| 13 | Insurance Claims Adjusting License | Fanhua Insurance Surveyors & Loss Adjustors Co., Ltd. |

NFRA Shenzhen Branch |

N/A | Long-term Validity | |||||

| 14 | Insurance Broker License in Hong Kong SAR | Aasure Insurance Broker Limited |

Hong Kong SAR Insurance Authority |

November 30, 2021 | November 29, 2024 | |||||

| 15 | Insurance Broker License in Hong Kong SAR | Minkfair Insurance Management Co.,Ltd. |

Hong Kong SAR Insurance Authority |

April 27, 2020 | N/A | |||||

| 16 | Value-added Telecommunication Business Operation Permit for ICP services | Fanhua RONS Insurance Sales & Service Co. Ltd. |

Ministry of Industry and Information Technology |

August 9, 2022 | August 9, 2027 | |||||

| 17 | Value-added Telecommunication Business Operation Permit for ICP services | Fanhua RONS (Beijing) Technology Co., Ltd. |

Ministry of Industry and Information Technology |

December 8, 2022 | December 8, 2027 |

- 3 -

The PRC government has issued statements and regulatory actions relating to areas such as approvals on offshore offerings, anti-monopoly regulatory actions, and oversight on cybersecurity and data privacy. For example, on February 17, 2023, the China Securities Regulatory Commission (the “CSRC”) released the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Enterprises (the “New Overseas Listing Rules”) with five interpretive guidelines, which took effect on March 31, 2023. We may be required to make filings with the CSRC for applicable securities offerings. In connect with our pending registration statement on Form F-3, as advised by our PRC legal counsel, Hai Run Law Firm, (i) although we are required to complete the filing procedure three days after the completion of the overseas offering, no relevant PRC laws or regulations in effect require that we obtain permission from any PRC authorities to issue securities to foreign investors, and we have not received any inquiry, notice, warning, sanction, or any regulatory objection to this offering from the China Securities Regulatory Commission (“CSRC”), the Cyberspace Administration of China (“CAC”), or any other PRC authorities that have jurisdiction over our operations; (ii) we are not required to obtain permissions from the CSRC; (iii) we are not required to file for a cybersecurity review with the CAC; and finally (iv) we have not received or were denied such requisite permissions by any other PRC authority.

Nonetheless, applicable laws and regulations may be tightened, and new laws or regulations may be introduced to impose additional government approval, license, and permit requirements. If we inadvertently conclude that such permissions and approvals relating to the operations of our business are not required, fail to obtain and maintain such approvals, licenses or permits required for our business, or fail to respond to changes in the applicable laws, regulations, interpretations and regulatory environment, we could be subject to liabilities, monetary penalties and even operational disruption, which may materially and adversely affect our business, operating results, and our financial condition. For more detailed information, see “Item 3. Key Information - D. Risk Factors - Risks Relating to Doing Business in China.”

Implication of The Holding Foreign Companies Accountable Act (the “HFCA Act”)

Our auditor, Deloitte Touche Tohmatsu Certified Public Accountants LLP, is located in mainland China. Our financial statements contained in this annual report on Form 20-F for the fiscal year ended December 31, 2023 have been audited by Deloitte Touche Tohmatsu Certified Public Accountants LLP, or Deloitte, an independent registered public accounting firm that is headquartered in Mainland China and is on such lists.

Pursuant to the Holding Foreign Companies Accountable Act, which was enacted on December 18, 2020 and further amended by the Consolidated Appropriations Act, 2023 signed into law on December 29, 2022, or the HFCA Act, if the SEC determines that we have filed audit reports issued by a registered public accounting firm that has not been subject to inspections by the Public Company Accounting Oversight Board, or the PCAOB, for two consecutive years, the SEC shall prohibit our shares or ADSs from being traded on a national securities exchange or in the over-the-counter trading market in the United States. Trading in our securities on U.S. markets, including the Nasdaq Global Select Market, will be prohibited under the HFCA Act if the PCAOB determines that it is unable to inspect or investigate completely our auditor for two consecutive years.

- 4 -

On December 16, 2021, the PCAOB issued the HFCA Act Determination Report to notify the SEC of its determinations that the PCAOB was unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong SAR, or the 2021 Determinations, including our auditor. On December 29, 2022, the Consolidated Appropriations Act, 2023 was signed into law, which, among others, amended the HFCA Act to reduce the number of consecutive years an issuer can be identified as a Commission-Identified Issuer before the SEC must impose an initial trading prohibition on the issuer’s securities from three years to two. Therefore, once an issuer is identified as a Commission-Identified Issuer for two consecutive years, the SEC is required under the HFCA Act to prohibit the trading of the issuer’s securities on a national securities exchange and in the over-the-counter market.

On May 26, 2022, we were conclusively identified by the Commission as a Commission-Identified Issuer under the Holding Foreign Company Accountable Act, or the HFCA Act. On December 15, 2022, the PCAOB issued a report that vacated its December 16, 2021 determination and removed mainland China and Hong Kong SAR from the list of jurisdictions where it was unable to inspect or investigate completely registered public accounting firms. Therefore, our auditor is currently able to be fully inspected and investigated by the PCAOB. Accordingly, until such time as the PCAOB issues any new determination, our securities are not subject to a trading prohibition under the HFCA Act.

Each year, the PCAOB determines whether it can inspect and investigate completely audit firms in mainland China and Hong Kong SAR, among other jurisdictions. If the PCAOB determines in the future that it no longer has full access to inspect and investigate completely accounting firms in mainland China and Hong Kong SAR and we use an accounting firm headquartered in one of these jurisdictions to issue an audit report on our financial statements filed with the SEC, we would be identified as a Commission-Identified Issuer following the filing of the annual report on Form 20-F for the relevant fiscal year. In accordance with the HFCA Act, our securities would be prohibited from being traded on a national securities exchange or in the over-the-counter trading market in the United States if we are identified as a Commission-Identified Issuer for two consecutive years in the future. There can be no assurance that we would not be identified as a Commission-Identified Issuer for any future fiscal year, and if we were so identified for two consecutive years, we and our investors may be deprived of the benefits of such PCAOB inspections. The inability of the PCAOB to conduct inspections of auditors in China makes it more difficult to evaluate the effectiveness of our independent registered public accounting firm’s audit procedures or quality control procedures as compared to auditors outside of China that are subject to the PCAOB inspections, which could cause investors and potential investors in our securities to lose confidence in the audit procedures and reported financial information and the quality of our financial statements. If we fail to meet the new listing standards specified in the HFCA Act, we could face possible delisting from the Nasdaq, cessation of trading in the “over-the-counter” market, deregistration from the Commission and/or other risks, which may materially and adversely affect, or effectively terminate, our ADSs trading in the United States.

Fund Flows between Fanhua Inc., its Subsidiaries and the Consolidated VIEs

Under PRC law, we may provide funding to our PRC subsidiaries only through capital contributions or loans, and to the consolidated VIEs only through loans, subject to the satisfaction of applicable government registration and approval requirements. We rely on dividends and other distributions from our PRC subsidiaries to satisfy part of our liquidity requirement. Under the contractual arrangements among Fanhua Group Company, the consolidated VIEs, and the shareholders of the consolidated VIEs, Fanhua Group Company is entitled to all of the economic benefits of the consolidated VIEs and its subsidiaries in the form of service fees. For risks relating to the fund flows of our China operations, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—We rely principally on dividends and other distributions on equity paid by our subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our subsidiaries to make payments to us could have a material adverse effect on our ability to conduct our business.”

Assets Transfer Occurred Between Fanhua Inc., its Subsidiaries and the Consolidated VIEs

Under the Contractual Arrangements, Fanhua Group Company and Fanlian Investment provide consultation and training services to the consolidated VIEs and are entitled to receive service fees from the consolidated VIEs in exchange. The Contractual Arrangements provide that the consolidated VIEs shall pay a quarterly fee calculated primarily based on a percentage of its revenues.

- 5 -

Technology consulting and service agreements were entered into between (i) Fanhua Group Company and (ii) Xinbao Investment and each of its subsidiaries on March 1, 2022 and consulting and service agreements were entered into between (i) Fanlian Investment and (ii) Fanhua RONS Technologies and each of its subsidiaries. No service fees have been incurred in 2023. The cash flows occurred between our subsidiaries and the consolidated VIEs included the following: (1) cash received by the VIEs from our subsidiaries as inter-company advances amounted to RMB89.8 million, RMB43.0 million, and RMB39.4 million for the years ended December 31, 2021, 2022 and 2023, respectively; and (2) net commissions received by our subsidiaries from the VIEs offset by technology services paid by our subsidiaries to the VIEs amounted to RMB16.2 million, RMB94.9 million, and RMB56.7 million for the years ended December 31, 2021, 2022 and 2023, respectively.

Dividends or Distributions on Our ADSs or Ordinary Shares Made to the U.S. Investors and Their Tax Consequences

Our board of directors has discretion as to whether to distribute dividends, subject to applicable laws. Although Fanhua Inc. has previously paid dividends on a quarterly basis, the amount and form of future dividends will depend on, among other things, our future results of operations and cash flow, our capital requirements and surplus, the amount of distributions, if any, received by us from our subsidiaries, our financial condition, contractual restrictions and other factors deemed relevant by our board of directors. See “Item 8. Financial Information—A. Consolidated Statements and Other Financial Information—Dividend Policy.”

In addition, subject to the passive foreign investment company rules discussed in detail under “Item 10. Additional Information—E. Taxation—United States Federal Income Taxation—Passive Foreign Investment Company”, the gross amount of any distribution that we make to investors with respect to our ADSs or ordinary shares (including any amounts withheld to reflect PRC or other withholding taxes) will be taxable as a dividend, to the extent paid out of our current or accumulated earnings and profits, as determined under United States federal income tax principles. Furthermore, if we are considered a PRC tax resident enterprise for tax purposes, any dividends we pay to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax. See “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—Our global income or the dividends we receive from our PRC subsidiaries may be subject to PRC tax under the EIT Law, which could have a material adverse effect on our results of operations.” For further discussion on PRC and United States federal income tax considerations of an investment in the ADSs, see “Item 10—Additional Information—E. Taxation.”

Restrictions on Foreign Exchange and the Ability to Transfer Cash between Entities, Across Borders and to U.S. Investors

Our cash dividends were paid in U.S. dollars. The PRC government imposes controls on the convertibility of Renminbi into foreign currencies and, in certain cases, the remittance of currency out of China. The majority of our income is received in Renminbi and shortages in foreign currencies may restrict our ability to pay dividends or other payments, or otherwise satisfy our foreign-currency-denominated obligations, if any. Under existing PRC foreign exchange regulations, payments of current account items, including profit distributions, interest payments and expenditures from trade-related transactions, can be made in foreign currencies without prior approval from SAFE as long as certain procedural requirements are met. Approval from appropriate government authorities is required if Renminbi is converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of loans denominated in foreign currencies. The PRC government may, at its discretion, impose restrictions on access to foreign currencies for current account transactions and if this occurs in the future, we may not be able to pay dividends in foreign currencies to our shareholders.

Relevant PRC laws and regulations permit the PRC companies to pay dividends only out of their retained earnings, if any, as determined in accordance with PRC accounting standards and regulations. Additionally, our PRC subsidiaries and the consolidated VIEs can only distribute dividends upon approval of the shareholders after they have met the PRC requirements for appropriation to the statutory reserves. As a result of these and other restrictions under the PRC laws and regulations, our PRC subsidiaries and the consolidated VIEs are restricted to transfer a portion of their net assets to us either in the form of dividends, loans or advances. Even though we currently do not require any such dividends, loans or advances from our PRC subsidiaries and the consolidated VIEs for working capital and other funding purposes, we may in the future require additional cash resources from our PRC subsidiaries and the consolidated VIEs due to changes in business conditions, to fund future acquisitions and developments, or merely pay dividends to or distributions to our shareholders.

- 6 -

Financial Information Related to the VIEs

The following tables set forth the summary consolidated balance sheets data as of December 31, 2022 and 2023 of the Parent, our wholly-owned foreign subsidiary (“WOFEs”), or Fanhua Group Company and Fanlian Investment, that are the primary beneficiaries of the VIEs under accounting principles generally accepted in the United States, or U.S. GAAP (the “Primary Beneficiaries of VIEs”), our other subsidiaries and the consolidated VIEs and their subsidiaries, and the summary of the consolidated statement of income and cash flows for the years ended December 31, 2022 and 2023. Our consolidated financial statements are prepared and presented in accordance with U.S. GAAP. Our and the consolidated VIEs’ historical results are not necessarily indicative of results expected for future periods. You should read this information together with our consolidated financial statements and the related notes and “Item 5. Operating and Financial Review and Prospects” included elsewhere in this annual report.

| As of December 31, 2023 | ||||||||||||||||||||||||

| Parent | Consolidated VIEs and their subsidiaries | WOFEs | Other Subsidiaries | Eliminating adjustments | Consolidated total | |||||||||||||||||||

| (RMB in thousands) | ||||||||||||||||||||||||

| Assets | ||||||||||||||||||||||||

| Cash and cash equivalents | 23,595 | 7,517 | 816 | 489,610 | — | 521,538 | ||||||||||||||||||

| Restricted cash | — | 24,049 | — | 56,417 | — | 80,466 | ||||||||||||||||||

| Short term investments | — | — | 2,593 | 925,677 | — | 928,270 | ||||||||||||||||||

| Accounts receivable, net | — | 18,518 | — | 261,415 | — | 279,933 | ||||||||||||||||||

| Contract assets, net | — | 9,271 | — | 1,061,658 | — | 1,070,929 | ||||||||||||||||||

| Other receivables, net | 20 | 1,830 | 69,446 | 40,438 | — | 111,734 | ||||||||||||||||||

| Amounts due from internal companies | 450,913 | 134,730 | 1,326,721 | 3,164,514 | (5,076,878 | ) | — | |||||||||||||||||

| Investments in subsidiaries and the VIEs and VIEs’ subsidiaries | 3,010,729 | — | 1,555,719 | 64,000 | (4,630,448 | ) | — | |||||||||||||||||

| Right-of-use assets, net | — | 3,330 | 15,377 | 117,349 | — | 136,056 | ||||||||||||||||||

| Property, plant, and equipment, net | — | 1,995 | 760 | 88,904 | — | 91,659 | ||||||||||||||||||

| Other non-current assets | 13,461 | 30,332 | 123,213 | 68,746 | — | 235,752 | ||||||||||||||||||

| Deferred tax assets | — | 3,000 | — | 37,735 | — | 40,735 | ||||||||||||||||||

| Intangible assets, net | — | 10,930 | — | 47,386 | — | 58,316 | ||||||||||||||||||

| Other assets | — | 59,101 | 45 | 436,350 | — | 495,496 | ||||||||||||||||||

| Total assets | 3,498,718 | 304,603 | 3,094,690 | 6,860,199 | (9,707,326 | ) | 4,050,884 | |||||||||||||||||

| Liabilities | ||||||||||||||||||||||||

| Short-term loan | — | — | — | 164,300 | — | 164,300 | ||||||||||||||||||

| Accounts payable | — | 2,020 | — | 249,229 | 251,249 | |||||||||||||||||||

| Accrued commissions | — | 2,050 | — | 554,893 | — | 556,943 | ||||||||||||||||||

| Other payables and accrued expenses | 3,238 | 3,864 | 803 | 178,094 | — | 185,999 | ||||||||||||||||||

| Amounts due to internal companies | 1,423,072 | 116,547 | 2,110,964 | 1,489,340 | (5,139,923 | ) | — | |||||||||||||||||

| Income tax payable | — | 7,416 | 852 | 91,992 | — | 100,260 | ||||||||||||||||||

| Deferred tax liabilities | — | 4,118 | — | 145,033 | — | 149,151 | ||||||||||||||||||

| Operating lease liability | — | 3,236 | 17,249 | 107,990 | — | 128,475 | ||||||||||||||||||

| Accrued payroll | 1,146 | 8,173 | 3,094 | 81,892 | — | 94,305 | ||||||||||||||||||

| Other liabilities | — | 22,736 | 32,822 | 12,183 | — | 67,741 | ||||||||||||||||||

| Insurance premium payable | — | 14,817 | — | 126 | — | 14,943 | ||||||||||||||||||

| Total liabilities | 1,427,456 | 184,977 | 2,165,784 | 3,075,072 | (5,139,923 | ) | 1,713,366 | |||||||||||||||||

| Total net assets | 2,071,262 | 119,626 | 928,906 | 3,785,127 | (4,567,403 | ) | 2,337,518 | |||||||||||||||||

- 7 -

| As of December 31, 2022 | ||||||||||||||||||||||||

| Parent | Consolidated VIEs and their subsidiaries | WOFEs | Other Subsidiaries | Eliminating adjustments | Consolidated total | |||||||||||||||||||

| (RMB in thousands) | ||||||||||||||||||||||||

| Assets | ||||||||||||||||||||||||

| Cash and cash equivalents | 38,512 | 38,169 | 112,399 | 378,445 | — | 567,525 | ||||||||||||||||||

| Restricted cash | — | 27,115 | — | 53,571 | — | 80,686 | ||||||||||||||||||

| Short term investments | 27,619 | — | — | 320,135 | — | 347,754 | ||||||||||||||||||

| Accounts receivable, net | — | 21,380 | — | 372,220 | — | 393,600 | ||||||||||||||||||

| Contract assets, net | — | — | — | 659,788 | — | 659,788 | ||||||||||||||||||

| Other receivables, net | — | 1,951 | 181,086 | 48,012 | — | 231,049 | ||||||||||||||||||

| Amounts due from internal companies | 417,613 | 208,630 | 943,158 | 3,056,014 | (4,625,415 | ) | — | |||||||||||||||||

| Investment in an affiliate | 4,035 | — | — | — | — | 4,035 | ||||||||||||||||||

| Investments in subsidiaries and the VIEs and VIEs’ subsidiaries | 2,520,667 | — | 1,178,977 | 64,000 | (3,763,644 | ) | — | |||||||||||||||||

| Right-of-use assets, net | — | 5,273 | 13,074 | 126,739 | — | 145,086 | ||||||||||||||||||

| Property, plant, and equipment, net | — | 2,322 | 1,289 | 94,848 | — | 98,459 | ||||||||||||||||||

| Other non-current assets | — | — | 11,400 | — | 11,400 | |||||||||||||||||||

| Deferred tax assets | — | 5,000 | — | 15,402 | — | 20,402 | ||||||||||||||||||

| Other assets | — | 1,755 | 387,545 | 140,432 | — | 529,732 | ||||||||||||||||||

| Total assets | 3,008,446 | 311,595 | 2,817,528 | 5,341,006 | (8,389,059 | ) | 3,089,516 | |||||||||||||||||

| Liabilities | ||||||||||||||||||||||||

| Short-term loan | — | — | — | 35,679 | — | 35,679 | ||||||||||||||||||

| Accounts payable | — | 8,600 | — | 353,752 | — | 362,352 | ||||||||||||||||||

| Accrued commissions | — | — | — | 267,349 | — | 267,349 | ||||||||||||||||||

| Other payables and accrued expenses | 3,599 | 3,267 | 2,597 | 164,863 | — | 174,326 | ||||||||||||||||||

| Amounts due to internal companies | 1,381,444 | 170,839 | 2,102,968 | 972,406 | (4,627,657 | ) | — | |||||||||||||||||

| Income tax payable | — | 7,509 | 852 | 121,663 | — | 130,024 | ||||||||||||||||||

| Deferred tax liabilities | — | — | — | 102,455 | — | 102,455 | ||||||||||||||||||

| Operating lease liability | — | 4,955 | 14,107 | 117,432 | — | 136,494 | ||||||||||||||||||

| Accrued payroll | — | 10,941 | 4,853 | 80,485 | — | 96,279 | ||||||||||||||||||

| Other tax liabilities | — | 26,147 | — | 10,500 | — | 36,647 | ||||||||||||||||||

| Insurance premium payable | — | 16,571 | — | 9 | — | 16,580 | ||||||||||||||||||

| Total liabilities | 1,385,043 | 248,829 | 2,125,377 | 2,226,593 | (4,627,657 | ) | 1,358,185 | |||||||||||||||||

| Total net assets | 1,623,403 | 62,766 | 692,151 | 3,114,413 | (3,761,402 | ) | 1,731,331 | |||||||||||||||||

- 8 -

| For the year ended December 31, 2023 | ||||||||||||||||||||||||

| Parent | Consolidated VIEs and their subsidiaries | WOFEs | Other subsidiaries | Eliminating adjustments (1) | Consolidated total | |||||||||||||||||||

| (RMB in thousands) | ||||||||||||||||||||||||

| Total net revenues | — | 168,965 | — | 3,156,708 | (127,284 | ) | 3,198,389 | |||||||||||||||||

| Third-party revenues | — | 122,880 | — | 3,075,509 | — | 3,198,389 | ||||||||||||||||||

| Intra-Group revenues | — | 46,085 | — | 81,199 | (127,284 | ) | — | |||||||||||||||||

| Total operating costs and expenses | (24,645 | ) | (182,156 | ) | (29,953 | ) | (2,891,099 | ) | 125,289 | (3,002,564 | ) | |||||||||||||

| Third-party operating costs and expenses | (24,645 | ) | (100,956 | ) | (29,953 | ) | (2,847,010 | ) | — | (3,002,564 | ) | |||||||||||||

| Intra-Group operating costs and expenses | — | (81,200 | ) | — | (44,089 | ) | 125,289 | — | ||||||||||||||||

| Income (loss) from operations | (24,645 | ) | (13,191 | ) | (29,953 | ) | 265,609 | (1,995 | ) | 195,825 | ||||||||||||||

| Interest income, net | 1,201 | 1,182 | 7,934 | (4,627 | ) | — | 5,690 | |||||||||||||||||

| Investment income | 10,359 | — | 21,105 | 17,642 | — | 49,106 | ||||||||||||||||||

| Gains from fair value change of a short term investment | 6,650 | — | — | 96,217 | — | 102,867 | ||||||||||||||||||

| Others, net | — | 409 | 4,355 | (8,434 | ) | — | (3,670 | ) | ||||||||||||||||

| Share of income from subsidiaries and the VIEs and VIEs’ subsidiaries | 285,595 | — | 194,973 | — | (480,568 | ) | — | |||||||||||||||||

| Share of income of affiliates, net of impairment | 1,317 | — | — | (2,634 | ) | — | (1,317 | ) | ||||||||||||||||

| Income tax expenses | — | (1,485 | ) | — | (57,917 | ) | — | (59,402 | ) | |||||||||||||||

| Net income | 280,477 | (13,085 | ) | 198,414 | 305,856 | (482,563 | ) | 289,099 | ||||||||||||||||

| For the year ended December 31, 2022 | ||||||||||||||||||||||||

| Parent | Consolidated VIEs and subsidiaries | WOFEs | Other subsidiaries | Eliminating adjustments (1) | Consolidated total | |||||||||||||||||||

| (RMB in thousands) | ||||||||||||||||||||||||

| Total net revenues | — | 165,270 | — | 2,747,360 | (131,016 | ) | 2,781,614 | |||||||||||||||||

| Third-party revenues | — | 141,086 | — | 2,640,528 | — | 2,781,614 | ||||||||||||||||||

| Intra-Group revenues | — | 24,184 | — | 106,832 | (131,016 | ) | — | |||||||||||||||||

| Total operating costs and expenses | (11,318 | ) | (173,131 | ) | (36,227 | ) | (2,523,279 | ) | 131,016 | (2,612,939 | ) | |||||||||||||

| Third-party operating costs and expenses | (11,062 | ) | (67,789 | ) | (36,126 | ) | (2,497,962 | ) | — | (2,612,939 | ) | |||||||||||||

| Intra-Group operating costs and expenses | (256 | ) | (105,342 | ) | (101 | ) | (25,317 | ) | 131,016 | — | ||||||||||||||

| Income (loss) from operations | (11,318 | ) | (7,861 | ) | (36,227 | ) | 224,081 | — | 168,675 | |||||||||||||||

| Interest income | 5 | 388 | 11,606 | 1,675 | — | 13,674 | ||||||||||||||||||

| Investment income | — | — | 6,600 | 11,209 | — | 17,809 | ||||||||||||||||||

| Others, net | 17,495 | 578 | (149 | ) | (21,747 | ) | — | (3,823 | ) | |||||||||||||||

| Share of income from subsidiaries and the VIEs and VIEs’ subsidiaries | 96,432 | — | 156,578 | — | (253,010 | ) | — | |||||||||||||||||

| Share of income of affiliates, net of impairment | (2,342 | ) | — | — | (67,254 | ) | — | (69,596 | ) | |||||||||||||||

| Income tax expenses | — | 2,759 | (2,906 | ) | (40,869 | ) | — | (41,016 | ) | |||||||||||||||

| Net income | 100,272 | (4,136 | ) | 135,502 | 107,095 | (253,010 | ) | 85,723 | ||||||||||||||||

Note:

| (1) | The elimination mainly represents (i) the intercompany service fee related to agency services for distributing life insurance products and non-life insurance products on behalf of insurance companies provide by consolidated affiliated entities to subsidiaries and (ii) the intercompany service fee related to technology services provided by our consolidated variable interest entities to our subsidiaries. |

- 9 -

| For the year ended December 31, 2021 | ||||||||||||||||||||||||

| Parent | Consolidated VIE and its subsidiaries | WOFEs | Other subsidiaries | Eliminating adjustments (1) | Consolidated total | |||||||||||||||||||

| (RMB in thousands) | ||||||||||||||||||||||||

| Total net revenues | — | 16,267 | — | 3,268,763 | (13,916 | ) | 3,271,114 | |||||||||||||||||

| Third-party revenues | — | 16,267 | — | 3,254,847 | — | 3,271,114 | ||||||||||||||||||

| Intra-Group revenues | — | — | — | 13,916 | (13,916 | ) | — | |||||||||||||||||

| Total operating costs and expenses | (331 | ) | (15,730 | ) | (37,677 | ) | (2,929,387 | ) | 13,916 | (2,969,209 | ) | |||||||||||||

| Third-party operating costs and expenses | (331 | ) | (1,814 | ) | (37,677 | ) | (2,929,387 | ) | — | (2,969,209 | ) | |||||||||||||

| Intra-Group operating costs and expenses | — | (13,916 | ) | — | — | 13,916 | — | |||||||||||||||||

| Income (loss) from operations | (331 | ) | 537 | (37,677 | ) | 339,376 | — | 301,905 | ||||||||||||||||

| Interest income | 2 | 60 | 374 | 2,535 | — | 2,971 | ||||||||||||||||||

| Investment income | — | — | 21,767 | 11,131 | — | 32,898 | ||||||||||||||||||

| Others, net | — | 90 | 12,014 | 21,210 | — | 33,314 | ||||||||||||||||||

| Share of income from subsidiaries and the VIE and VIE’s subsidiaries | 254,526 | — | 300,599 | — | (555,125 | ) | — | |||||||||||||||||

| Share of loss of affiliates | (3,208 | ) | — | — | (17,365 | ) | — | (20,573 | ) | |||||||||||||||

| Income tax expenses | — | (172 | ) | 1,760 | (92,162 | ) | — | (90,574 | ) | |||||||||||||||

| Net income | 250,989 | 515 | 298,837 | 264,725 | (555,125 | ) | 259,941 | |||||||||||||||||

Note:

| (1) | The elimination mainly represents the intercompany service fee related to agency services for distributing life insurance products and P&C insurance products on behalf of insurance companies provide by consolidated affiliated entities to subsidiaries. |

| For the year ended December 31, 2023 | ||||||||||||||||||||||||

| Parent | Consolidated VIEs and subsidiaries | WOFEs | Other subsidiaries | Eliminating adjustments | Consolidated total | |||||||||||||||||||

| (RMB in thousands) | ||||||||||||||||||||||||

| Cash flows from operating activities: | (36,520 | ) | (52,983 | ) | 6,620 | 184,670 | — | 101,787 | ||||||||||||||||

| Net cash (used in) provided by transactions with external parties | (36,520 | ) | 3,754 | 6,620 | 127,933 | — | 101,787 | |||||||||||||||||

| Net cash (used in) provided by transactions with internal companies | — | (56,737 | ) | — | 56,737 | — | — | |||||||||||||||||

| Cash flows from investing activities: | 20,092 | (20,095 | ) | 384,002 | (177,970 | ) | (451,849 | ) | (245,820 | ) | ||||||||||||||

| Net cash provided by (used in) transactions with external parties | 30,097 | (20,095 | ) | 384,002 | (639,824 | ) | — | (245,820 | ) | |||||||||||||||

| Net cash provided by (used in) transactions with internal companies | (10,005 | ) | — | — | 461,854 | (451,849 | ) | — | ||||||||||||||||

| Cash flows from financing activities: | (29,044 | ) | 39,359 | (502,207 | ) | 137,731 | 451,849 | 97,688 | ||||||||||||||||

| Net cash used in transactions with external parties | (29,044 | ) | — | — | 126,732 | — | 97,688 | |||||||||||||||||

| Net cash provided by (used in) transactions with internal companies | — | 39,359 | (502,207 | ) | 10,999 | 451,849 | — | |||||||||||||||||

- 10 -

| For the year ended December 31, 2022 | ||||||||||||||||||||||||

| Parent | Consolidated VIEs and subsidiaries | WOFEs | Other subsidiaries | Eliminating adjustments | Consolidated total | |||||||||||||||||||

| (RMB in thousands) | ||||||||||||||||||||||||

| Cash flows from operating activities: | 7,339 | 3,822 | (12,794 | ) | 139,385 | — | 137,752 | |||||||||||||||||

| Net cash (used in) provided by transactions with external parties | 7,339 | 98,715 | (12,794 | ) | 44,492 | — | 137,752 | |||||||||||||||||

| Net cash (used in) provided by transactions with internal companies | — | (94,893 | ) | — | 94,893 | — | — | |||||||||||||||||

| Cash flows from investing activities: | 227,321 | (16,214 | ) | (34,333 | ) | (1,006,158 | ) | 701,822 | (127,562 | ) | ||||||||||||||

| Net cash provided by (used in) transactions with external parties | 917,101 | (16,214 | ) | (34,333 | ) | (994,116 | ) | — | (127,562 | ) | ||||||||||||||

| Net cash provided by (used in) transactions with internal companies | (689,780 | ) | — | — | (12,042 | ) | 701,822 | — | ||||||||||||||||

| Cash flows from financing activities: | (321,712 | ) | 43,032 | (52,476 | ) | 1,012,607 | (701,822 | ) | (20,371 | ) | ||||||||||||||

| Net cash used in transactions with external parties | (321,712 | ) | — | — | 301,341 | — | (20,371 | ) | ||||||||||||||||

| Net cash provided by (used in) transactions with internal companies | — | 43,032 | (52,476 | ) | 711,266 | (701,822 | ) | — | ||||||||||||||||

| For the year ended December 31, 2021 | ||||||||||||||||||||||||

| Parent | Consolidated VIE and its subsidiaries | WOFEs | Other subsidiaries | Eliminating adjustments | Consolidated total | |||||||||||||||||||

| (RMB in thousands) | ||||||||||||||||||||||||

| Cash flows from operating activities: | (784 | ) | 32,674 | (7,013 | ) | 101,321 | — | 126,198 | ||||||||||||||||

| Net cash (used in) provided by transactions with external parties | (784 | ) | 48,923 | (7,013 | ) | 85,072 | — | 126,198 | ||||||||||||||||

| Net cash (used in) provided by transactions with internal companies | — | (16,249 | ) | — | 16,249 | — | — | |||||||||||||||||

| Cash flows from investing activities: | 201,339 | (73,430 | ) | (283,323 | ) | 261,650 | 344,163 | 450,399 | ||||||||||||||||

| Net cash provided by (used in) transactions with external parties | 43,757 | — | (283,323 | ) | 689,965 | — | 450,399 | |||||||||||||||||

| Net cash provided by (used in) transactions with internal companies | 157,582 | (73,430 | ) | — | (428,315 | ) | 344,163 | — | ||||||||||||||||

| Cash flows from financing activities: | (242,518 | ) | — | 501,745 | (175,362 | ) | (344,163 | ) | (260,298 | ) | ||||||||||||||

| Net cash used in transactions with external parties | (242,518 | ) | — | — | (17,780 | ) | — | (260,298 | ) | |||||||||||||||

| Net cash provided by (used in) transactions with internal companies | — | — | 501,745 | (157,582 | ) | (344,163 | ) | — | ||||||||||||||||

- 11 -

Filing Procedures Required from the PRC Authorities for Offering Securities to Foreign Investors

Under applicable laws of mainland China, we and our mainland China subsidiaries may be required to complete certain filing procedures with the China Securities Regulatory Commission, or the CSRC, in connection with future offering and listing in an overseas market, including our follow-on offerings, issuance of convertible bonds, offshore relisting after going-private transactions, and other equivalent offering activities. If we fail to complete such filing procedures for any future offshore offering or listing, including our follow-on offerings, issuance of convertible bonds, offshore relisting after going-private transactions, and other equivalent offering activities, we may face sanctions by the CSRC or other mainland China regulatory authorities, which may include fines and penalties on our operations in mainland China, limitations on our operating privileges in mainland China, restrictions on or delays to our future financing transactions offshore, or other actions that could have a material and adverse effect on our business, financial condition, results of operations, reputation and prospects, as well as the trading price of our ADSs. In addition, we are required to file a report to the CSRC after the occurrence and public disclosure of certain material corporate events, including but not limited to, change of control and voluntary or mandatory delisting. For more detailed information, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The approval of and filing with the CSRC or other PRC government authorities may be required in connection with our future offshore offerings, capital raising activities and acquisitions or other trading arrangements of domestic enterprises conducted by China-based issuers, and also may be required to go through cybersecurity review under the new laws and the draft laws and regulations of mainland China, and, if required, we cannot predict whether or for how long we will be able to obtain such approval or complete such filing or other regulatory procedures.”

Summary of Risk Factors

Investing in the ADSs involves a high degree of risk. You should carefully consider the risks described under “Item 3. Key Information—D. Risk Factors” and other information contained in this annual report on Form 20-F, before you decide whether to purchase the ADSs. Below please find a summary of the principal risks and uncertainties we face, organized under relevant headings:

Risks Related to Our Business and Industry

| ● | We may not be successful in implementing our new strategic initiatives, which may have an adverse impact on our business and financial results; |

| ● | If and when our contracts with insurance companies are suspended or changed, our business and operating results will be materially and adversely affected; |

| ● | If we fail to attract and retain productive agents, especially entrepreneurial agents, and qualified claims adjustors, our business and operating results could be materially and adversely affected; | |

| ● | If our digitalization initiatives are not successful, our business and results of operations may be materially and adversely affected; | |

| ● | Regulations on online insurance distribution are evolving rapidly. If we are unable to adapt to regulatory changes and keep compliant, our business and results of operations may be materially and adversely affected; | |

| ● | All of our personnel engaging in insurance agency, or claims adjusting activities are required under relevant PRC regulations to register with the NFRA’s Insurance Intermediaries Regulatory Information System. If our sales personnel fail to finish practice registration, our business may be materially and adversely affected; |

| ● | Material changes in the regulatory environment could change the competitive landscape of our industry or require us to change the way we do business. The administration, interpretation and enforcement of the laws and regulations currently applicable to us could change rapidly. If we fail to comply with applicable laws and regulations, we may be subject to civil and criminal penalties or lose the ability to conduct our business; | |

| ● | Our business could be negatively impacted if we are unable to adapt our services to regulatory changes in China; |

| ● | We may be unsuccessful in identifying suitable acquisition candidates, completing acquisitions, integrating acquired companies or the acquired companies may not perform to our expectations, which could adversely affect our growth; | |

| ● | Competition in our industry is intense and, if we are unable to compete effectively with both existing and new market participants, we may lose customers, and our financial results may be negatively affected; and |

| ● | Because the commission and fee we earn on the sale of insurance products is based on premiums, commission and fee rates set by insurance companies, any decrease in these premiums, commission or fee rates may have an adverse effect on our results of operations. |

- 12 -

Risks Related to Our Corporate Structure

| ● | Fanhua Inc. is a Cayman Islands holding company primarily operating in China through its subsidiaries and contractual arrangements with Xinbao Investment and Fanhua RONS Technologies. Investors in the ADSs thus are not purchasing, and may never directly hold, all equity interests in the consolidated VIEs. There are substantial uncertainties regarding the interpretation and application of current and future PRC laws, regulations, and rules relating to such agreements that establish the VIE structure for the majority of our and the consolidated VIEs’ operations in China, including potential future actions by the PRC government, which could affect the enforceability of our contractual arrangements with Xinbao Investment and Fanhua RONS Technologies and, consequently, significantly affect the financial condition and results of operations of Fanhua Inc. If the PRC government finds such agreements non-compliant with relevant PRC laws, regulations, and rules, or if these laws, regulations, and rules or the interpretation thereof change in the future, we could be subject to severe penalties or be forced to relinquish our interests in Xinbao Investment and Fanhua RONS Technologies or forfeit our rights under the contractual arrangements; |

| ● |

The PRC government has significant authority to exert influence on the China operations of an offshore holding company, such as us. Therefore, investors in the ADSs and the business of us and the consolidated VIEs face potential uncertainty from the PRC government’s policy. Changes in China’s economic, political or social conditions, or government policies could materially and adversely affect our and the consolidated VIE’s business, financial condition, and results of operations; | |

| ● | We and the consolidated VIEs are subject to extensive and evolving legal development, non-compliance with which, or changes in which, may materially and adversely affect our and the consolidated VIEs’ business and prospects, and may result in a material change in our and the consolidated VIEs’ operations and/or the value of our ADSs or could significantly limit or completely hinder our and the consolidated VIEs’ ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline or be worthless; | |

| ● | It is unclear whether we and the consolidated VIEs will be subject to the oversight of the Cyberspace Administration of China and how such oversight may impact us. Our and the consolidated VIEs’ business could be interrupted or we and the consolidated VIEs could be subject to liabilities which may materially and adversely affect the results of our and the consolidated VIEs’ operation and the value of your investment; | |

| ● | The PRC government’s oversight over our and the consolidated VIEs’ business operations could result in a material adverse change in our and the consolidated VIEs’ operations and the value of our ADSs; | |

| ● | Any failure by the VIEs or their respective shareholders to perform their obligations under our Contractual Arrangements with them would have an adverse effect on our business; and | |

| ● | We rely on contractual arrangements to conduct a small part of our China operations, which may not be as effective in providing operational control as direct ownership. |

Risks Related to Doing Business in China

| ● |

The approval of and filing with the CSRC or other PRC government authorities may be required in connection with our future offshore offerings, capital raising activities and acquisitions or other trading arrangements of domestic enterprises conducted by China-based issuers, we must file with the CSRC within three business days after the issuance, and also may be required to go through cybersecurity review under the new laws and the draft laws and regulations of mainland China, and, if required, we cannot predict whether or for how long we will be able to obtain such approval or complete such filing or other regulatory procedures; |

- 13 -

| ● | Uncertainties in the PRC legal system and the interpretation and enforcement of PRC laws and regulations could limit the legal protections available to you and us, significantly limit or completely hinder our ability to offer or continue to offer our ADSs, cause significant disruption to our and the consolidated VIE’s business operations, and severely damage our and the consolidated VIEs’ reputation, which would materially and adversely affect our and the consolidated VIEs’ financial condition and results of operations and cause our ADSs to significantly decline in value or become worthless. In addition, rules and regulations in China can change quickly with little advance notice, therefore, our assertions and beliefs of the risks imposed by the Chinese legal and regulatory system cannot be certain; | |

| ● | A downturn in the Chinese or global economy could have a material adverse effect on our business; | |

| ● | Governmental control of currency conversion may affect the value of your investment; | |

| ● | The PRC Enterprise Income Tax Law may increase the enterprise income tax rate applicable to some of our PRC subsidiaries, which could have a material adverse effect on our result of operations; |

| ● | Our global income or the dividends we receive from our PRC subsidiaries may be subject to PRC tax under the EIT Law, which could have a material adverse effect on our results of operations; | |

| ● | We rely principally on dividends and other distributions on equity paid by our subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our subsidiaries to make payments to us could have a material adverse effect on our ability to conduct our business; and | |

| ● | PRC regulations relating to the establishment of offshore special purpose companies by PRC residents and employee stock options granted by overseas-listed companies may increase our administrative burden, restrict our overseas and cross-border investment activity, or otherwise adversely affect us. If our shareholders who are PRC residents, or our PRC employees who are granted or exercise stock options, fail to make any required registrations or filings under such regulations, we may be unable to distribute profits and may become subject to liability under PRC laws. We may also face regulatory uncertainties that could restrict our ability to adopt additional equity compensation plans for our directors and employees and other parties under PRC law. |

Risks Related to Our ADSs

| ● | If the PCAOB determines in the future that it no longer has full access to inspect and investigate completely accounting firms in mainland China and Hong Kong SAR, we and our investors may be deprived with the benefits of such inspections, which could cause investors and potential investors in the ADSs to lose confidence in the audit procedures and reported financial information and the quality of our financial statements; | |

| ● | Our ADSs may be prohibited from trading in the United States under the HFCA Act in the future if the PCAOB is unable to inspect or investigate completely auditors located in China. The delisting of the ADSs, or the threat of their being delisted, may materially and adversely affect the value of your investment; | |

| ● | The trade price of our ADSs may be volatile; | |

| ● | We may need additional capital, and the sale of additional ADSs or other equity securities could result in additional dilution to our shareholders; and | |

| ● | Substantial future sales or perceived potential sales of our ordinary shares, ADSs or other equity securities in the public market could cause the price of our ADSs to decline. |

- 14 -

| A. | [Reserved] |

| B. | Capitalization and Indebtedness |

Not Applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not Applicable.

| D. | Risk Factors |

Risks Related to Our Business and Industry

We may not be successful in implementing our new strategic initiatives, which may have an adverse impact on our business and financial results.

In late 2020, we launched new strategic initiatives with focus on (i) building a career-based and professional insurance advisor team with profound insurance knowledge and capabilities to provide family financial asset allocation services to the emerging middle-class and mass-affluent individuals and families and empowering all independent agents and agencies in China to become more efficient and professionalized; (ii) developing digital toolkits and enhancing digital operation capabilities to empower independent agents and increase agent productivity and (iii) offering an open platform to all independent agents and agencies whereby they can have access to compliance support, industry leading IT infrastructure, digital technologies, better products and service offerings, and the library of resources and knowhow to improve their training and skillsets to strengthen their competitiveness in the market. There is no assurance that we will be able to implement these strategic initiatives in accordance with our expectations, which may result in an adverse impact on our business and financial results.

If and when our contracts with insurance companies are suspended or changed, our business and operating results will be materially and adversely affected.

We primarily act as agents for insurance companies in distributing their products to retail customers. We also provide claims adjusting services principally to insurance companies. Our relationships with the insurance companies are governed by agreements between us and the insurance companies. We have entered into strategic partnership agreements with most of our major insurance company partners for the distribution of life, property and casualty insurance products and the provision of claims adjusting services at the corporate headquarters level. While this approach allows us to obtain more favorable terms from insurance companies by combining the sales volumes and service fees of all of our subsidiaries and branches operating insurance agency and claims adjusting businesses, it also means that the termination of a major contract could have a material adverse effect on our business. Under the framework of the headquarter-to-headquarter agreements, our subsidiaries and branches operating insurance agency and claims adjusting businesses generally also enter into contracts at a local level with the respective provincial, city and district branches of the insurance companies. Generally, each branch of these insurance companies has independent authority to enter into contracts with our relevant subsidiaries and branches, and the termination of a contract with one branch has no significant effect on our contracts with the other branches. See “Item 4. Information on the Company—B. Business Overview—Insurance Company Partners.” These contracts establish, among other things, the scope of our authority, the pricing of the insurance products we distribute and our fee rates. These contracts typically have a term of one year, and certain contracts can be terminated by the insurance companies with little advance notice. Moreover, before or upon expiration of a contract, the insurance company that is a party to that contract may agree to renew it only with changes in material terms, including the amount of commissions and fees we receive, which could reduce our revenues to be generated from that contract.

- 15 -

For the year ended December 31, 2023, our top five insurance company partners were Sinatay Life Insurance Co., Ltd., or Sinatay, Aeon Life Insurance Co., Ltd., or Aeon, Li An Life Insurance Co., Ltd., or Li An, Huaxia Life Insurance Co., Ltd., or Huaxia,and Ping An Property & Casualty Insurance Company of China, or Ping An by net revenues. Among these top five partners, each of Sinatay and Aeon accounted for more than 10% of our total net revenues individually in 2023, with Sinatay accounting for 15.3%, Aeon accounting for 10.3%, Lian accounting for 7.5%, Huaxia accounting for 6.1%, and Ping An accounting for 6.0%, respectively.

If we fail to attract and retain productive agents, especially entrepreneurial agents, and qualified claims adjustors, our business and operating results could be materially and adversely affected.

A substantial portion of our sales of insurance products are conducted through our individual sales agents. Some of these sales agents are significantly more productive than others in generating sales. In recent years, some entrepreneurial management staff or senior sales agents of major insurance companies in China have chosen to leave their employers or principals and become independent agents. We refer to these individuals as entrepreneurial agents. An entrepreneurial agent is usually able to assemble and lead a team of sales agents. We have been actively recruiting and will continue to recruit entrepreneurial agents to join our distribution and service network as our sales agents. Entrepreneurial agents have been instrumental to the development of our life insurance business. In addition, we rely primarily on our in-house claims adjustors to provide claims adjusting services. Because claims adjustment requires technical skills, the technical competence of claims adjustors is essential to establishing and maintaining our brand image and relationships with our customers.

As of December 31, 2023, we had 87,851 registered sales agents and 2,303 claims adjustors. Out of the registered sales agents, 45,358 were performing agents, who are defined as sales agents that have sold at least one insurance policy in 2023, and among these performing agents, 15,726 of them sold at least one regular life insurance policy in 2023. If we are unable to attract and retain the core group of highly productive sales agents, particularly entrepreneurial agents, and qualified claims adjustors, our business could be materially and adversely affected. Competition for sales personnel and claims adjustors from insurance companies and other insurance intermediaries may also force us to increase the compensation of our sales agents, and claims adjustors, which would increase operating costs and reduce our profitability.

If our digitalization initiatives are not successful, our business and results of operations may be materially and adversely affected.