On February 22, 2011, SGO Corporation was established in Delaware USA. On March 14, 2011, SGOCO International purchased 100% of the outstanding shares of common stock of SGO. SGO was founded to market, sell and distribute TROOPS’s high quality products in the U.S. markets. SGO was not operating during 2011 and started to operate in the first quarter of 2012.

SGOCO International directly owns 100% of SGOCO (Fujian) Electronic Co., Ltd. SGOCO (Fujian) is a limited liability company established under the corporate laws of the PRC on July 28, 2011 for the purposes of conducting LCD/LED display product development, branding, marketing and distribution.

On November 15, 2011, we entered into a Sale and Purchase Agreement (“Honesty SPA”) to sell our 100% ownership interest in Honesty Group to Apex, a British Virgin Islands company.

On December 26, 2011, SGOCO International established another wholly owned subsidiary, Beijing SGOCO Image Technology Co. Ltd., a limited liability company under the laws of the PRC to conduct LCD/LED monitor, TV product-related and application-specific product design, brand development and distribution.

On November 14, 2013, SGOCO International established a wholly owned subsidiary, SGOCO (Shenzhen) Technology Co., Ltd., a limited liability company under the laws of the PRC for the purpose of conducting LCD/LED monitor, TV product-related and application-specific product design, brand development and distribution.

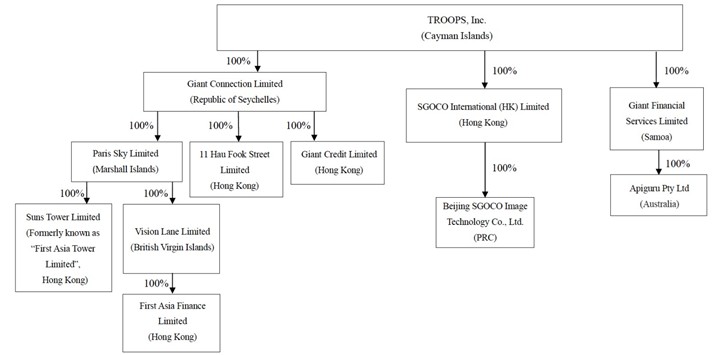

On December 15, 2017, TROOPS formed Giant Connection Limited, a limited liability company registered in Public of Seychelles.

On December 24, 2014, we entered into a Sale and Purchase Agreement (“SPA”) to sell our 100% equity ownership interest in SGOCO (Fujian) to Apex.

On December 28, 2015, SGOCO International entered into a Share Sale and Purchase Agreement for the Sale and Purchase of the entire issued share capital of Boca International Limited with Richly Conqueror Limited, a company incorporated under the laws of the British Virgin Islands. On June 7, 2018 and August 31, 2020, the Group disposed 49% and 51% equity interest of Boca International Limited to Leung Iris Chi Yu and Wong Yiu Tong, respectively.

On April 23, 2017, SGOGO International entered into a Share Sale and Purchase Agreement with Full Linkage Limited pursuant to which SGOCO International acquired all of the issued and outstanding capital stock of CSL. On June 7, 2018 and September 20, 2019, the Group disposed 49% and 51% equity interest of CSL to Leung Iris Chi Yu and Ho Pui Lung, respectively.

On December 15, 2017, TROOPS formed Giant Connection Limited, a limited liability company registered in Public of Seychelles.

On December 22, 2017, Giant Connection Limited, a wholly-owned subsidiary of TROOPS, completed the acquisition of Giant Credit Limited. The principal activity of Giant Credit Limited is money lending in Hong Kong.

On March 8, 2018, Giant Connection Limited, a wholly-owned subsidiary of TROOPS, closed a Share Exchange Agreement with Vagas Lane Limited for the purchase and sale of 11 Hau Fook Street Limited. 11 Hau Fook Street Limited is an investment holding company which owns two properties located at No. 11 Hau Fook Street, Tsim Sha Tsui, Kowloon, Hong Kong.

On June 7, 2018, Giant Connection Limited, a wholly-owned subsidiary of TROOPS, completed the acquisition of Paris Sky Limited. Paris Sky Limited is an investment holding company which, through its wholly owned subsidiary, owns a property located at No. 8 Fui Yiu Kok Street, Tsuen Wan, New Territories, Hong Kong.

On March 12, 2019, the Company’s wholly-owned subsidiary, Paris Sky Limited closed a Share Exchange Agreement for the entire issued share capital of Vision Lane Limited. Vision Lane is a private company incorporated in the British Virgin Islands, and engages in property investment and money lending services in Hong Kong.

On December 23, 2019, the Company entered into a Share Exchange Agreement with Victor Or for the purchase and sale of Giant Financial Services Limited. Giant Financial Services Limited is a private company incorporated in Samoa and provides an online financial marketplace connecting financial institutions and users worldwide via its unique mobile application which features state-of-the-art functions to boost financial accessibility to financial and insurance products and services.