UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Form 10-Q

(Mark One)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

FOR THE QUARTERLY PERIOD ENDED MARCH 31, 2022 OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

FOR THE TRANSITION PERIOD FROM TO

Commission File Number: 001-35107

(Exact name of Registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(Address of principal executive offices) (Zip Code)

(212 ) 515-3200

(Registrant’s telephone number, including area code)

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | ||||||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ||||||||||||||||||||

| ☐ | ||||||||||||||||||||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

As of May 7, 2022, there were 1,000 shares of common stock of the Registrant outstanding.

| TABLE OF CONTENTS | ||||||||

| Page | ||||||||

| PART I | ||||||||

| ITEM 1. | ||||||||

| ITEM 2. | ||||||||

| ITEM 3. | ||||||||

| ITEM 4. | ||||||||

| PART II | OTHER INFORMATION | |||||||

| ITEM 1. | ||||||||

| ITEM 1A. | ||||||||

| ITEM 2. | ||||||||

| ITEM 3. | ||||||||

| ITEM 4. | ||||||||

| ITEM 5. | ||||||||

| ITEM 6. | ||||||||

-2-

Forward-Looking Statements

This quarterly report may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These statements include, but are not limited to, discussions related to Apollo’s expectations regarding the performance of its business, its liquidity and capital resources and the other non-historical statements in the discussion and analysis. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. When used in this quarterly report, the words “believe,” “anticipate,” “estimate,” “expect,” “intend,” “target” and similar expressions are intended to identify forward-looking statements. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to have been correct. These statements are subject to certain risks, uncertainties and assumptions, including risks relating to the impact of COVID-19, the impact of energy market dislocation, market conditions, and interest rate fluctuations, generally, our ability to manage our growth, our ability to operate in highly competitive environments, the performance of the funds we manage, our ability to raise new funds, the variability of our revenues, earnings and cash flow, our dependence on certain key personnel, the accuracy of management’s assumptions and estimates, our use of leverage to finance our businesses and investments by the funds we manage, changes in our regulatory environment and tax status, litigation risks and our ability to recognize the benefits expected to be derived from the merger with Athene Holding Ltd. (“Athene”), among others. We believe these factors include but are not limited to those described under the section entitled “Risk Factors” in the Company’s Annual Report on Form 10-K filed with the United States Securities and Exchange Commission (“SEC”) on February 25, 2022 (the “2021 Annual Report”), as such factors may be updated from time to time in our periodic filings with the SEC, which are accessible on the SEC’s website at www.sec.gov. These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this report and in our other filings with the SEC. We undertake no obligation to publicly update or review any forward-looking statements, whether as a result of new information, future developments or otherwise, except as required by applicable law.

Terms Used in This Report

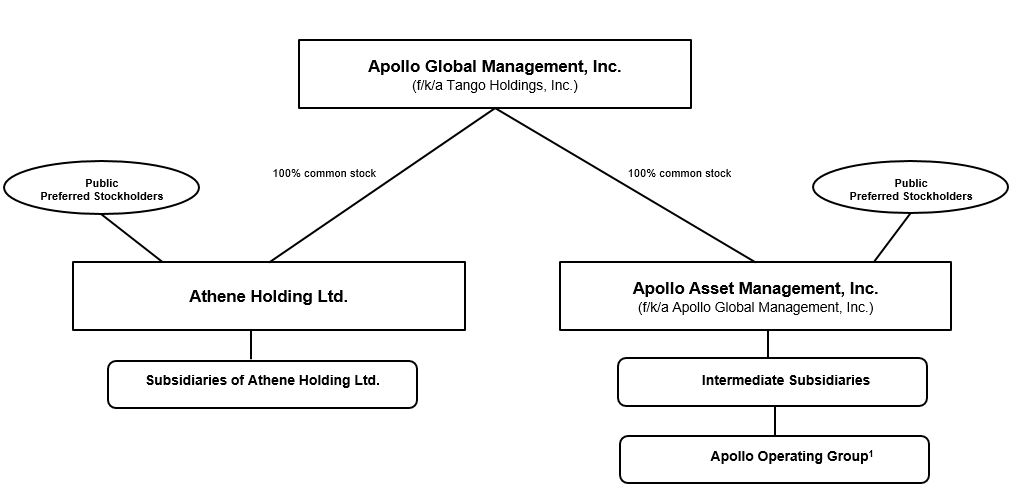

On January 1, 2022, Apollo Global Management, Inc. completed the previously announced merger transactions with Athene (the “Mergers”). Upon the closing of the Mergers, Apollo Global Management, Inc. was renamed Apollo Asset Management, Inc. (“AAM”) and became a subsidiary of Tango Holdings, Inc., and Tango Holdings, Inc. was renamed Apollo Global Management, Inc. (“AGM ”).

In this quarterly report, references to “Apollo,” “we,” “us,” “our,” and the “Company” refer collectively to AAM and its subsidiaries. References to “Class A shares” refer to the Class A common stock, $0.00001 par value per share, of AAM prior to the Mergers; “Class B share” refers to the Class B common stock, $0.00001 par value per share, of AAM prior to the Mergers; “Class C share” refers to the Class C common stock, $0.00001 par value per share, of AAM prior to the Mergers; “Series A Preferred shares” refers to the 6.375% Series A preferred stock of AAM; “Series B Preferred shares” refers to the 6.375% Series B preferred stock of AAM; and “Preferred shares” refers to the Series A Preferred shares and the Series B Preferred shares, collectively. In addition, references to “common stock” of the Company refer to the authorized shares of common stock, par value $0.00001 per share, of AAM following the Mergers.

The use of any defined term in this report to mean more than one entity, person, security or other item collectively is solely for convenience of reference and in no way implies that such entities, persons, securities or other items are one indistinguishable group. For example, notwithstanding the use of the defined terms "Apollo," "we", “us”, "our" and the “Company” in this report to refer to AAM and its subsidiaries, each subsidiary of AAM is a standalone legal entity that is separate and distinct from AAM and any of its other subsidiaries. Any AAM entity referenced herein is responsible for its own financial, contractual and legal obligations.

“AMH” refers to Apollo Management Holdings, L.P., a Delaware limited partnership, that is an indirect subsidiary of AAM;

“Apollo funds”, “our funds” and references to the “funds” we manage, refer to the funds (including the parallel funds and alternative investment vehicles of such funds), partnerships, accounts, including strategic investment accounts or “SIAs,” alternative asset companies and other entities for which subsidiaries of the Apollo Operating Group provide investment management or advisory services;

“Apollo Operating Group” refers to (i) the entities through which we currently operate our businesses and (ii) one or more entities formed for the purpose of, among other activities, holding certain of our gains or losses on our principal investments in the funds, which we refer to as our “principal investments”;

“Assets Under Management”, or “AUM”, refers to the assets of the funds, partnerships and accounts to which we provide investment management, advisory, or certain other investment-related services, including, without limitation, capital that such funds, partnerships and accounts have the right to call from investors pursuant to capital commitments. Our AUM equals the sum of:

-3-

(i)the net asset value, or “NAV,” plus used or available leverage and/or capital commitments, or gross assets plus capital commitments, of the yield and certain hybrid funds, partnerships and accounts for which we provide investment management or advisory services, other than certain collateralized loan obligations (“CLOs”), collateralized debt obligations (“CDOs”), and certain perpetual capital vehicles, which have a fee-generating basis other than the mark-to-market value of the underlying assets; for certain perpetual capital vehicles in yield, gross asset value plus available financing capacity;

(ii)the fair value of the investments of the equity and certain hybrid funds, partnerships and accounts we manage or advise, plus the capital that such funds, partnerships and accounts are entitled to call from investors pursuant to capital commitments, plus portfolio level financings;

(iii)the gross asset value associated with the reinsurance investments of the portfolio company assets we manage or advise; and

(iv)the fair value of any other assets that we manage or advise for the funds, partnerships and accounts to which we provide investment management, advisory, or certain other investment-related services, plus unused credit facilities, including capital commitments to such funds, partnerships and accounts for investments that may require pre-qualification or other conditions before investment plus any other capital commitments to such funds, partnerships and accounts available for investment that are not otherwise included in the clauses above.

Our AUM measure includes Assets Under Management for which we charge either nominal or zero fees. Our AUM measure also includes assets for which we do not have investment discretion, including certain assets for which we earn only investment-related service fees, rather than management or advisory fees. Our definition of AUM is not based on any definition of Assets Under Management contained in our governing documents or in any management agreements of the funds we manage. We consider multiple factors for determining what should be included in our definition of AUM. Such factors include but are not limited to (1) our ability to influence the investment decisions for existing and available assets; (2) our ability to generate income from the underlying assets in the funds we manage; and (3) the AUM measures that we use internally or believe are used by other investment managers. Given the differences in the investment strategies and structures among other alternative investment managers, our calculation of AUM may differ from the calculations employed by other investment managers and, as a result, this measure may not be directly comparable to similar measures presented by other investment managers. Our calculation also differs from the manner in which our affiliates registered with the SEC report “Regulatory Assets Under Management” on Form ADV and Form PF in various ways.

We use AUM, Gross capital deployed and Dry powder as performance measurements of our investment activities, as well as to monitor fund size in relation to professional resource and infrastructure needs;

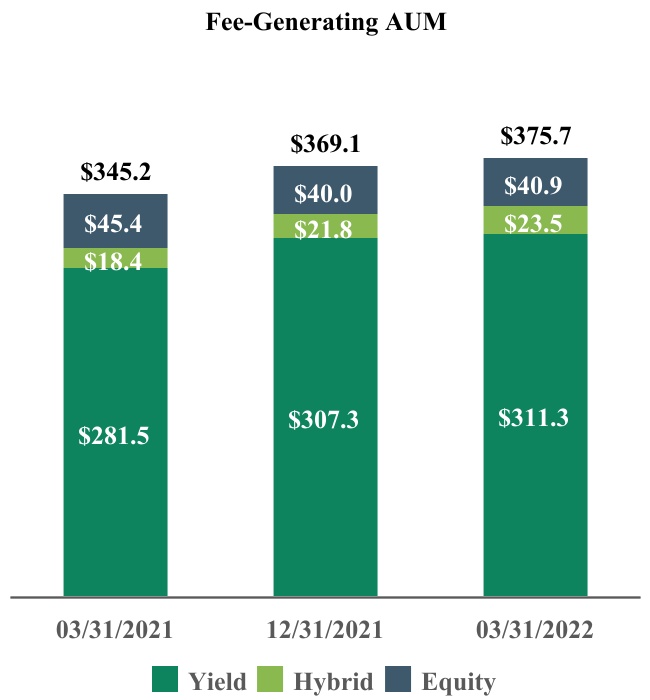

“Fee-Generating AUM” consists of assets of the funds, partnerships and accounts to which we provide investment management, advisory, or certain other investment-related services and on which we earn management fees, monitoring fees or other investment-related fees pursuant to management or other fee agreements on a basis that varies among the Apollo funds, partnerships and accounts. Management fees are normally based on “net asset value,” “gross assets,” “adjusted par asset value,” “adjusted cost of all unrealized portfolio investments,” “capital commitments,” “adjusted assets,” “stockholders’ equity,” “invested capital” or “capital contributions,” each as defined in the applicable management agreement. Monitoring fees, also referred to as advisory fees, with respect to the structured portfolio company investments of the funds, partnerships and accounts we manage or advise, are generally based on the total value of such structured portfolio company investments, which normally includes leverage, less any portion of such total value that is already considered in Fee-Generating AUM;

“Non-Fee-Generating AUM” refers to AUM that does not produce management fees or monitoring fees. This measure generally includes the following:

(i)fair value above invested capital for those funds that earn management fees based on invested capital;

(ii)net asset values related to general partner and co-investment interests;

(iii)unused credit facilities;

(iv)available commitments on those funds that generate management fees on invested capital;

-4-

(v)structured portfolio company investments that do not generate monitoring fees; and

(vi)the difference between gross asset and net asset value for those funds that earn management fees based on net asset value.

“Performance Fee-Eligible AUM” refers to the AUM that may eventually produce performance fees. All funds for which we are entitled to receive a performance fee allocation or incentive fee are included in Performance Fee-Eligible AUM, which consists of the following:

(i) “Performance Fee-Generating AUM”, which refers to invested capital of the funds, partnerships and accounts we manage, advise, or to which we provide certain other investment-related services, that is currently above its hurdle rate or preferred return, and profit of such funds, partnerships and accounts is being allocated to, or earned by, the general partner in accordance with the applicable limited partnership agreements or other governing agreements;

(ii) “AUM Not Currently Generating Performance Fees”, which refers to invested capital of the funds, partnerships and accounts we manage, advise, or to which we provide certain other investment-related services, that is currently below its hurdle rate or preferred return; and

(iii) “Uninvested Performance Fee-Eligible AUM”, which refers to capital of the funds, partnerships and accounts we manage, advise, or to which we provide certain other investment-related services, that is available for investment or reinvestment subject to the provisions of applicable limited partnership agreements or other governing agreements, which capital is not currently part of the NAV or fair value of investments that may eventually produce performance fees allocable to, or earned by, the general partner.

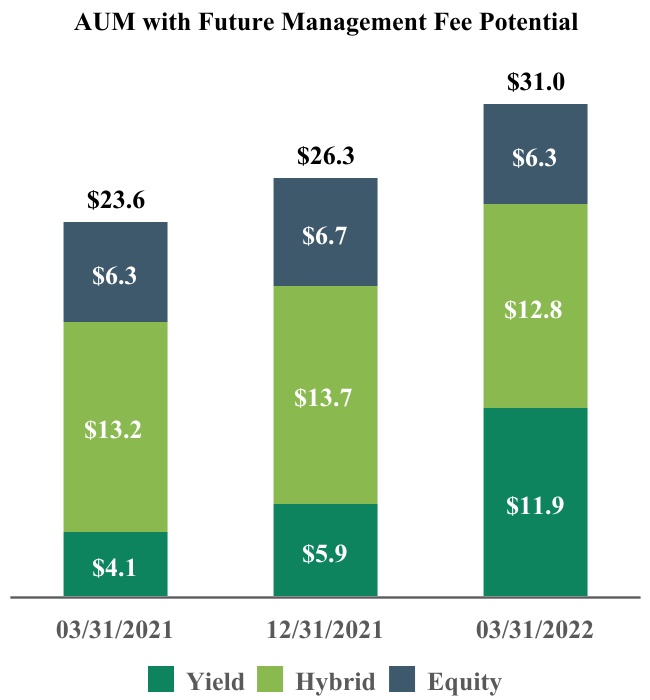

“AUM with Future Management Fee Potential” refers to the committed uninvested capital portion of total AUM not currently earning management fees. The amount depends on the specific terms and conditions of each fund;

We use AUM as a performance measure of investment activities of the funds we manage, as well as to monitor fund size in relation to professional resource and infrastructure needs. Non-Fee-Generating AUM includes assets on which we could earn performance fees;

“Athene Holding” or “AHL” refers to Athene Holding Ltd. (together with its subsidiaries, “Athene”), a leading retirement services company that issues, reinsures and acquires retirement savings products designed for the increasing number of individuals and institutions seeking to fund retirement needs, and to which Apollo, through its consolidated subsidiary Apollo Insurance Solutions Group LP (formerly known as Athene Asset Management LLC) (“ISG”), provides asset management and advisory services. Athene Holding is a subsidiary of our parent company, Apollo Global Management, Inc.;

“Athora Holding” refers to Athora Holding, Ltd. (“Athora Holding” and together with its subsidiaries, “Athora”), a strategic platform that acquires or reinsures blocks of insurance business in the German and broader European life insurance market (collectively, the “Athora Accounts”). The Company, through ISGI, provides investment advisory services to Athora. Athora Non-Sub-Advised Assets includes the Athora assets which are managed by Apollo but not sub-advised by Apollo nor invested in Apollo funds or investment vehicles. Athora Sub-Advised includes assets which the Company explicitly sub-advises as well as those assets in the Athora Accounts which are invested directly in funds and investment vehicles Apollo manages;

“Contributing Partners” refer to those of our current and former partners and their related parties (other than Messrs. Leon Black, Joshua Harris and Marc Rowan, our co-founders) who indirectly beneficially owned (through Holdings) Apollo Operating Group units;

“Dry Powder” represents the amount of capital available for investment or reinvestment subject to the provisions of the applicable limited partnership agreements or other governing agreements of the funds, partnerships and accounts we manage. Dry powder excludes uncalled commitments which can only be called for fund fees and expenses and commitments from Perpetual Capital Vehicles;

“Equity Plan” refers to AGM’s 2007 Omnibus Equity Incentive Plan, which effective as of July 22, 2019, was amended, restated and renamed the 2019 Omnibus Equity Incentive Plan;

“Former Managing Partners” refer to Messrs. Leon Black, Joshua Harris and Marc Rowan collectively and, when used in reference to holdings of interests in Apollo or Holdings, includes certain related parties of such individuals;

-5-

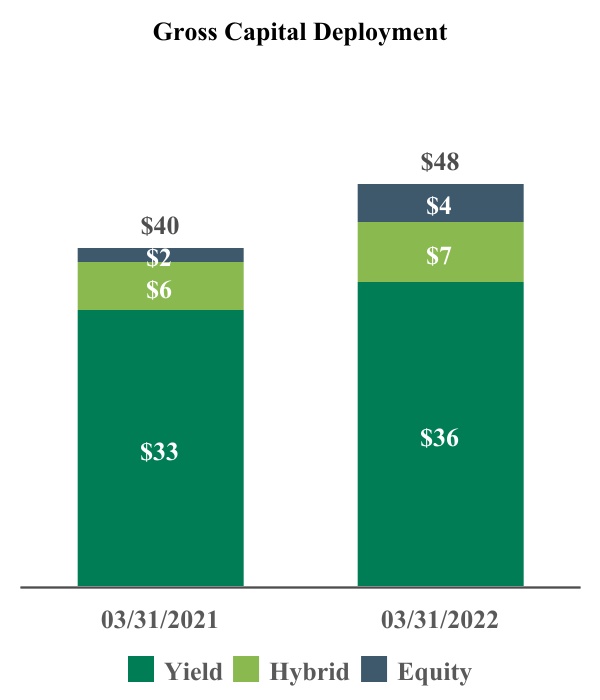

“Gross capital deployment” represents the gross capital that has been invested in investments by the funds and accounts we manage during the relevant period, but excludes certain investment activities primarily related to hedging and cash management functions at the firm. Gross capital deployment is not reduced or netted down by sales or refinancings, and takes into account leverage used by the funds and accounts we manage in gaining exposure to the various investments that they have made;

“gross IRR” of a traditional private equity or hybrid value fund represents the cumulative investment-related cash flows (i) for a given investment for the fund or funds which made such investment, and (ii) for a given fund, in the relevant fund itself (and not any one investor in the fund), in each case, on the basis of the actual timing of investment inflows and outflows (for unrealized investments assuming disposition on March 31, 2022 or other date specified) aggregated on a gross basis quarterly, and the return is annualized and compounded before management fees, performance fees and certain other expenses (including interest incurred by the fund itself) and measures the returns on the fund’s investments as a whole without regard to whether all of the returns would, if distributed, be payable to the fund’s investors. In addition, gross IRRs at the fund level will differ from those at the individual investor level as a result of, among other factors, timing of investor-level inflows and outflows. Gross IRR does not represent the return to any fund investor;

“gross return” or “gross ROE” of a total return yield fund or the hybrid credit hedge fund is the monthly or quarterly time-weighted return that is equal to the percentage change in the value of a fund’s portfolio, adjusted for all contributions and withdrawals (cash flows) before the effects of management fees, incentive fees allocated to the general partner, or other fees and expenses. Returns for these categories are calculated for all funds and accounts in the respective strategies. Returns over multiple periods are calculated by geometrically linking each period’s return over time. Gross return and gross ROE do not represent the return to any fund investor;

“HoldCo” refers to Tango Holdings, Inc., which was subsequently renamed Apollo Global Management, Inc. in connection with the Mergers;

“Holdings” means AP Professional Holdings, L.P., a Cayman Islands exempted limited partnership through which our Former Managing Partners and Contributing Partners indirectly beneficially owned their interests in the Apollo Operating Group units;

“inflows” represents (i) at the individual segment level, subscriptions, commitments, and other increases in available capital, such as acquisitions or leverage, net of inter-segment transfers, and (ii) on an aggregate basis, the sum of inflows across the yield, hybrid and equity strategies;

“net IRR” of a traditional private equity or hybrid value fund means the gross IRR applicable to a fund, including returns for related parties which may not pay fees or performance fees, net of management fees, certain expenses (including interest incurred or earned by the fund itself) and realized performance fees all offset to the extent of interest income, and measures returns at the fund level on amounts that, if distributed, would be paid to investors of the fund. The timing of cash flows applicable to investments, management fees and certain expenses, may be adjusted for the usage of a fund’s subscription facility. To the extent that a fund exceeds all requirements detailed within the applicable fund agreement, the estimated unrealized value is adjusted such that a percentage of up to 20.0% of the unrealized gain is allocated to the general partner of such fund, thereby reducing the balance attributable to fund investors. In addition, net IRR at the fund level will differ from that at the individual investor level as a result of, among other factors, timing of investor-level inflows and outflows. Net IRR does not represent the return to any fund investor;

“net return” or “net ROE” of a total return yield fund or the hybrid credit hedge fund represents the gross return after management fees, performance fees allocated to the general partner, or other fees and expenses. Returns over multiple periods are calculated by geometrically linking each period’s return over time. Net return and net ROE do not represent the return to any fund investor;

“other operating expenses” within the Principal Investing segment represents expenses incurred in the normal course of business and includes allocations of non-compensation expenses related to managing the business;

“performance allocations”, “performance fees”, “performance revenues”, “incentive fees” and “incentive income” refer to interests granted to Apollo by an Apollo fund that entitle Apollo to receive allocations, distributions or fees which are based on the performance of such fund or its underlying investments;

“perpetual capital vehicles” refers to (a) assets that are owned by or related to Athene or Athora but only to the extent that origination or acquisitions of new liabilities exceed the run off driven by maturity or termination of existing liabilities, (b) assets that are owned by or related to MidCap FinCo Designated Activity Company (“MidCap”) and managed by Apollo, (c) assets of publicly traded vehicles managed by Apollo such as Apollo Investment Corporation (“AINV”), Apollo Commercial Real Estate Finance, Inc. (“ARI”), Apollo Tactical Income Fund Inc. (“AIF”), and Apollo Senior Floating Rate Fund Inc. (“AFT”), in each case that do not have redemption provisions or a requirement to return capital to investors upon exiting the investments made with such capital, except as required by applicable law, (d) assets of Apollo Debt Solutions BDC ("ADS"), a non-traded business development company managed by Apollo, and (e) a publicly traded business development company from which

-6-

Apollo earns certain investment-related service fees. The investment management agreements of AINV, AIF and AFT have one year terms and the investment management agreement of ADS has an initial term of two years and then is subject to annual renewal. These investment management agreements are reviewed annually and remain in effect only if approved by the boards of directors of such companies or by the affirmative vote of the holders of a majority of the outstanding voting shares of such companies, including in either case, approval by a majority of the directors who are not “interested persons” as defined in the Investment Company Act of 1940, as amended (the “Investment Company Act”). In addition, the investment management agreements of AINV, AIF, AFT and ADS may be terminated in certain circumstances upon 60 days’ written notice. The investment management agreement of ARI has a one year term and is reviewed annually by ARI’s board of directors and may be terminated under certain circumstances by an affirmative vote of at least two-thirds of ARI’s independent directors. The investment management or advisory arrangements between each of MidCap and Apollo, Athene and Apollo and Athora and Apollo, may also be terminated under certain circumstances. The agreement pursuant to which Apollo earns certain investment-related service fees from a non-traded business development company may be terminated under certain limited circumstances;

“Principal investing compensation” within the Principal Investing segment represents realized performance compensation, distributions related to investment income and dividends, and includes allocations of certain compensation expenses related to managing the business;

“private equity investments” refer to (i) direct or indirect investments in existing and future private equity funds managed or sponsored by Apollo, (ii) direct or indirect co-investments with existing and future private equity funds managed or sponsored by Apollo, (iii) direct or indirect investments in securities which are not immediately capable of resale in a public market that Apollo identifies but does not pursue through its private equity funds, and (iv) investments of the type described in (i) through (iii) above made by Apollo funds;

“Redding Ridge” refers to Redding Ridge Asset Management, LLC and its subsidiaries, which is a standalone, self-managed asset management business established in connection with risk retention rules that manages CLOs and retains the required risk retention interests; and

“traditional private equity funds” refers to Apollo Investment Fund I, L.P. (“Fund I”), AIF II, L.P. (“Fund II”), a mirrored investment account established to mirror Fund I and Fund II for investments in debt securities (“MIA”), Apollo Investment Fund III, L.P. (together with its parallel funds, “Fund III”), Apollo Investment Fund IV, L.P. (together with its parallel fund, “Fund IV”), Apollo Investment Fund V, L.P. (together with its parallel funds and alternative investment vehicles, “Fund V”), Apollo Investment Fund VI, L.P. (together with its parallel funds and alternative investment vehicles, “Fund VI”), Apollo Investment Fund VII, L.P. (together with its parallel funds and alternative investment vehicles, “Fund VII”), Apollo Investment Fund VIII, L.P. (together with its parallel funds and alternative investment vehicles, “Fund VIII”) and Apollo Investment Fund IX, L.P. (together with its parallel funds and alternative investment vehicles, “Fund IX”).

-7-

PART I - FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

APOLLO ASSET MANAGEMENT, INC.

CONDENSED CONSOLIDATED STATEMENTS OF FINANCIAL CONDITION (UNAUDITED)

AS OF MARCH 31, 2022 AND DECEMBER 31, 2021

(dollars in thousands, except share data)

| As of March 31, 2022 | As of December 31, 2021 | ||||||||||

| Assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash and cash equivalents | |||||||||||

| Investments (includes performance allocations of $3,062,672 and $2,731,733 as of March 31, 2022 and December 31, 2021, respectively) | |||||||||||

| Assets of consolidated variable interest entities: | |||||||||||

| Cash and cash equivalents | |||||||||||

| Investments, at fair value | |||||||||||

| Other assets | |||||||||||

| Due from related parties | |||||||||||

| Deferred tax assets, net | |||||||||||

| Other assets | |||||||||||

| Lease assets | |||||||||||

| Goodwill | |||||||||||

| Total Assets | $ | $ | |||||||||

| Liabilities, Redeemable non-controlling interests and Stockholders’ Equity | |||||||||||

| Liabilities: | |||||||||||

| Accounts payable and accrued expenses | $ | $ | |||||||||

| Accrued compensation and benefits | |||||||||||

| Deferred revenue | |||||||||||

| Due to related parties | |||||||||||

| Profit sharing payable | |||||||||||

| Debt | |||||||||||

| Liabilities of consolidated variable interest entities: | |||||||||||

| Debt, at fair value | |||||||||||

| Notes payable | |||||||||||

| Other liabilities | |||||||||||

| Other liabilities | |||||||||||

| Lease liabilities | |||||||||||

| Total Liabilities | |||||||||||

| Commitments and Contingencies (see note 15) | |||||||||||

| Redeemable non-controlling interests: | |||||||||||

| Redeemable non-controlling interests | |||||||||||

| Stockholders’ Equity: | |||||||||||

| Apollo Asset Management, Inc. Stockholders’ Equity: | |||||||||||

| Series A Preferred Stock, 11,000,000 shares issued and outstanding as of March 31, 2022 and December 31, 2021 | |||||||||||

| Series B Preferred Stock, 12,000,000 shares issued and outstanding as of March 31, 2022 and December 31, 2021 | |||||||||||

-8-

| Common Stock, $0.00001 par value, 40,000,000 and 0 shares authorized as of March 31, 2022 and December 31, 2021, respectively, 1,000 and 0 shares issued and outstanding as of March 31, 2022 and December 31, 2021, respectively | |||||||||||

| Class A Common Stock, $0.00001 par value, 0 and 90,000,000,000 shares authorized as of March 31, 2022 and December 31, 2021, respectively, 0 and 248,896,649 shares issued and outstanding as of March 31, 2022 and December 31, 2021, respectively | |||||||||||

| Class B Common Stock, $0.00001 par value, 0 and 999,999,999 shares authorized as of March 31, 2022 and December 31, 2021, respectively, 0 shares issued and outstanding as of March 31, 2022 and December 31, 2021 | |||||||||||

| Class C Common Stock, $0.00001 par value, 0 and 1 share authorized as of March 31, 2022 and December 31, 2021, respectively, 0 shares issued and outstanding as of March 31, 2022 and December 31, 2021 | |||||||||||

| Additional paid in capital | |||||||||||

| Retained earnings | |||||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

| Total Apollo Asset Management, Inc. Stockholders’ Equity | |||||||||||

| Non-Controlling Interests in consolidated entities | |||||||||||

| Non-Controlling Interests in Apollo Operating Group | |||||||||||

| Total Stockholders’ Equity | |||||||||||

| Total Liabilities, Redeemable non-controlling interests and Stockholders’ Equity | $ | $ | |||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

-9-

APOLLO ASSET MANAGEMENT, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

FOR THE THREE MONTHS ENDED MARCH 31, 2022 AND 2021

(dollars in thousands, except share data)

| For the Three Months Ended March 31, | |||||||||||

| 2022 | 2021 | ||||||||||

| Revenues: | |||||||||||

| Management fees | $ | $ | |||||||||

| Advisory and transaction fees, net | |||||||||||

| Investment income | |||||||||||

| Incentive fees | |||||||||||

| Total Revenues | $ | $ | |||||||||

| Expenses: | |||||||||||

| Compensation and benefits | |||||||||||

| Interest expense | |||||||||||

| General, administrative and other | |||||||||||

| Total Expenses | $ | $ | |||||||||

| Other Income: | |||||||||||

| Net gains from investment activities | |||||||||||

| Net gains from investment activities of consolidated variable interest entities | |||||||||||

| Interest income | |||||||||||

| Other income (loss), net | ( | ( | |||||||||

| Total Other Income | |||||||||||

| Income before income tax provision | |||||||||||

| Income tax provision | ( | ( | |||||||||

| Net Income | |||||||||||

| Net income attributable to Non-Controlling Interests | ( | ( | |||||||||

| Net Income Attributable to Apollo Asset Management, Inc. | |||||||||||

| Series A Preferred share dividends | ( | ( | |||||||||

| Series B Preferred share dividends | ( | ( | |||||||||

| Net Income Attributable to Apollo Asset Management, Inc. Common Stockholders | $ | $ | |||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

-10-

APOLLO ASSET MANAGEMENT, INC.

CONDENSED CONSOLIDATED STATEMENTS OF

COMPREHENSIVE INCOME (UNAUDITED)

FOR THE THREE MONTHS ENDED MARCH 31, 2022 AND 2021

(dollars in thousands, except share data)

| For the Three Months Ended March 31, | |||||||||||

| 2022 | 2021 | ||||||||||

| Net Income | $ | $ | |||||||||

| Other Comprehensive Income (Loss), net of tax: | |||||||||||

| Currency translation adjustments, net of tax | ( | ( | |||||||||

| Net gain from change in fair value of cash flow hedge instruments | |||||||||||

| Net gain (loss) on available-for-sale securities | ( | ||||||||||

| Total Other Comprehensive Loss, net of tax | ( | ( | |||||||||

| Comprehensive Income | |||||||||||

| Comprehensive Income attributable to Non-Controlling Interests | ( | ( | |||||||||

| Comprehensive Income Attributable to Apollo Asset Management, Inc. | $ | $ | |||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

-11-

APOLLO ASSET MANAGEMENT, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES

IN STOCKHOLDERS’ EQUITY (UNAUDITED)

FOR THE THREE MONTHS ENDED MARCH 31, 2022 AND 2021

(dollars in thousands, except share data)

| Apollo Asset Management, Inc. Stockholders | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Class A Common Stock | Class B Common Stock | Class C Common Stock | Series A Preferred Stock | Series B Preferred Stock | Additional Paid in Capital | Retained Earnings | Accumulated Other Comprehensive Loss | Total Apollo Asset Management, Inc. Stockholders’ Equity | Non- Controlling Interests in Consolidated Entities | Non- Controlling Interests in Apollo Operating Group | Total Stockholders’ Equity | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at January 1, 2021 | $ | $ | $ | $ | $ | ( | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accretion of redeemable non-controlling interests | — | — | — | — | — | ( | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Dilution impact of issuance of Class A Common Stock | — | — | — | — | — | ( | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Capital increase related to equity-based compensation | — | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Capital contributions | — | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Dividends/ Distributions | — | — | — | ( | ( | — | ( | — | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Payments related to issuances of Class A Common Stock for equity-based awards | — | — | — | — | — | ( | — | ( | — | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Exchange of AOG Units for Class A Common Stock | — | — | — | — | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Currency translation adjustments, net of tax | — | — | — | — | — | — | — | ( | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net gain from change in fair value of cash flow hedge instruments | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income on available-for-sale securities | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2021 | $ | $ | $ | $ | $ | ( | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Apollo Asset Management, Inc. Stockholders | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Common Stock | Series A Preferred Stock | Series B Preferred Stock | Additional Paid in Capital | Retained Earnings | Accumulated Other Comprehensive Loss | Total Apollo Asset Management, Inc. Stockholders’ Equity | Non- Controlling Interests in Consolidated Entities | Non- Controlling Interests in Apollo Operating Group | Total Stockholders’ Equity | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at January 1, 2022 | $ | $ | $ | $ | $ | ( | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||

| Reverse stock split | ( | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||

| Deconsolidation of VIEs | — | — | — | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Accretion of redeemable non-controlling interests | — | — | — | ( | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||

| Contributions | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Dividends/ Distributions | — | ( | ( | ( | ( | — | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Currency translation adjustments, net of tax | — | — | — | — | — | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Net gain from change in fair value of cash flow hedge instruments | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net loss on available-for-sale securities | — | — | — | — | — | ( | ( | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2022 | $ | $ | $ | $ | $ | ( | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

-12-

APOLLO ASSET MANAGEMENT, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

FOR THE THREE MONTHS ENDED MARCH 31, 2022 AND 2021

(dollars in thousands, except share data)

| For the Three Months Ended March 31, | |||||||||||

| 2022 | 2021 | ||||||||||

| Cash Flows from Operating Activities: | |||||||||||

| Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to net cash provided by (used in) operating activities: | |||||||||||

| Equity-based compensation | |||||||||||

| Depreciation and amortization | |||||||||||

| Unrealized (gains) losses from investment activities | ( | ||||||||||

| Principal investment income | ( | ( | |||||||||

| Performance allocations | ( | ( | |||||||||

| Change in fair value of contingent obligations | ( | ||||||||||

| (Gain) loss from change in tax receivable agreement liability | ( | ||||||||||

| Deferred taxes, net | ( | ||||||||||

| Non-cash lease expense | |||||||||||

| Other non-cash amounts included in net income (loss), net | ( | ( | |||||||||

| Cash flows due to changes in operating assets and liabilities: | |||||||||||

| Due from related parties | |||||||||||

| Accounts payable and accrued expenses | ( | ||||||||||

| Accrued compensation and benefits | ( | ||||||||||

| Deferred revenue | |||||||||||

| Due to related parties | ( | ||||||||||

| Profit sharing payable | |||||||||||

| Lease liability | ( | ||||||||||

| Other assets and other liabilities, net | ( | ( | |||||||||

| Earnings from principal investments | |||||||||||

| Earnings from performance allocations | |||||||||||

| Satisfaction of contingent obligations | ( | ( | |||||||||

| Apollo Funds and VIE related: | |||||||||||

| Net realized and unrealized gains from investing activities and debt | ( | ( | |||||||||

| Deconsolidation of VIEs | ( | ||||||||||

| Purchases of investments | ( | ( | |||||||||

| Proceeds from sale of investments | |||||||||||

| Changes in other assets and other liabilities, net | ( | ||||||||||

| Net Cash Provided by (Used in) Operating Activities | $ | ( | $ | ( | |||||||

| Cash Flows from Investing Activities: | |||||||||||

| Purchases of fixed assets | $ | ( | $ | ( | |||||||

| Proceeds from sale of investments | |||||||||||

| Purchase of investments | ( | ||||||||||

| Purchase of U.S. Treasury securities | ( | ||||||||||

| Proceeds from maturities of U.S. Treasury securities | |||||||||||

| Cash contributions to principal investments | ( | ( | |||||||||

| Cash distributions from principal investments | |||||||||||

| Issuance of related party loans | ( | ||||||||||

| Repayment of related party loans | |||||||||||

| Other investing activities | ( | ( | |||||||||

| Apollo Funds and VIE related: | |||||||||||

| Purchase of U.S. Treasury securities | ( | ( | |||||||||

| Proceeds from maturities of U.S. Treasury | |||||||||||

| Net Cash Provided by (Used in) Investing Activities | $ | ( | $ | ||||||||

-13-

| Cash Flows from Financing Activities: | |||||||||||

| Dividends to Preferred Stockholders | ( | ( | |||||||||

| Distributions related to AGM’s repurchase of Common Stock | ( | ||||||||||

| Distributions related to deliveries of AGM’s Common Stock for RSUs | ( | ( | |||||||||

| Dividends paid | ( | ( | |||||||||

| Distributions paid to Non-Controlling Interests in Apollo Operating Group | ( | ||||||||||

| Other financing activities, net | ( | ( | |||||||||

| Apollo Funds and VIE related: | |||||||||||

| Issuance of debt | |||||||||||

| Principal repayment of debt | ( | ( | |||||||||

| Distributions paid to Non-Controlling Interests in consolidated entities | ( | ( | |||||||||

| Contributions from Non-Controlling Interests in consolidated entities | |||||||||||

| Proceeds from issuance of Class A Units of a SPAC | |||||||||||

| Payment of underwriting discounts | ( | ||||||||||

| Net Cash Provided by (Used in) Financing Activities | $ | $ | |||||||||

| Net Increase in Cash and Cash Equivalents, Restricted Cash and Cash Equivalents, and Cash and Cash Equivalents Held at Consolidated Funds and VIEs | |||||||||||

| Cash and Cash Equivalents, Restricted Cash and Cash Equivalents, and Cash and Cash Equivalents Held at Consolidated Funds and VIEs, Beginning of Period | |||||||||||

| Cash and Cash Equivalents, Restricted Cash and Cash Equivalents, and Cash and Cash Equivalents Held at Consolidated Funds and VIEs, End of Period | $ | $ | |||||||||

| Supplemental Disclosure of Cash Flow Information: | |||||||||||

| Interest paid | $ | $ | |||||||||

| Interest paid by consolidated variable interest entities | |||||||||||

| Income taxes paid | |||||||||||

| Supplemental Disclosure of Non-Cash Investing Activities: | |||||||||||

| Non-cash distributions from principal investments | $ | $ | ( | ||||||||

| Change in accrual for purchase of fixed assets | ( | ||||||||||

| Non-cash strategic transactions | |||||||||||

| Supplemental Disclosure of Non-Cash Financing Activities: | |||||||||||

| Capital increases related to equity-based compensation | $ | $ | |||||||||

| Issuance of restricted shares | |||||||||||

| Other non-cash financing activities | ( | ( | |||||||||

| Net Assets Deconsolidated from Consolidated Variable Interest Entities and Funds: | |||||||||||

| Investments, at fair value | ( | ||||||||||

| Other assets | ( | ||||||||||

| Debt at Fair Value | |||||||||||

| Notes payable | |||||||||||

| Other liabilities | |||||||||||

| Non-Controlling interest in consolidated entities | |||||||||||

| Adjustments related to exchange of Apollo Operating Group units: | |||||||||||

| Deferred tax assets | $ | $ | |||||||||

| Due to related parties | ( | ||||||||||

| Additional paid in capital | ( | ||||||||||

| Non-Controlling Interest in Apollo Operating Group | |||||||||||

| Reconciliation of Cash and Cash Equivalents, Restricted Cash and Cash Equivalents, and Cash and Cash Equivalents Held at Consolidated Variable Interest Entities to the Consolidated Statements of Financial Condition: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash and cash equivalents | |||||||||||

| Cash and cash equivalents held at consolidated variable interest entities | |||||||||||

| Total Cash and Cash Equivalents, Restricted Cash and Cash Equivalents, and Cash and Cash Equivalents Held at Consolidated Variable Interest Entities | $ | $ | |||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

-14-

APOLLO ASSET MANAGEMENT, INC.

NOTES TO CONDENSED CONSOLIDATED

FINANCIAL STATEMENTS (UNAUDITED)

(dollars in thousands, except share data, except where noted)

1. ORGANIZATION

Apollo Asset Management, Inc. (“AAM”, together with its consolidated subsidiaries, the “Company” or “Apollo”) is a high-growth, global alternative asset manager whose predecessor was founded in 1990. Its primary business is to raise, invest and manage funds on behalf of pension, endowment and sovereign wealth funds, as well as other institutional and individual investors. For these investment management services, Apollo receives management fees generally related to the amount of assets managed, transaction and advisory fees, incentive fees and performance allocations related to the performance of the respective funds that it manages. As of March 31, 2022, Apollo had two primary business segments:

•Asset Management — focuses on three investing strategies: yield, hybrid and equity; yield focuses on generating excess returns through high quality credit underwriting and origination of safe-yielding assets; hybrid focuses across debt and equity to offer a differentiated risk-adjusted return with an emphasis on structured downside protected opportunities across asset classes; and within equity, controlled transactions are principally buyouts, corporate carveouts and distressed investments, while our real estate funds generally focus on single asset, portfolio and platform acquisitions;

•Principal Investing — primarily includes our general partner investments in the funds we manage, where we earn realized performance fee income based on the investment performance of these funds. Principal investing also includes our growth capital and liquidity resources, and seeks to deploy capital into strategic investments over time to help accelerate the growth of the asset management segment.

Organization of the Company

As of March 31, 2022, the Company owned 57.4 % of the economic interests of, and operated and controlled all of the businesses and affairs of, the Apollo Operating Group. The remaining 42.6 % of the economic interests of the Apollo Operating Group are owned by Apollo Global Management, Inc. (“AGM”).

Apollo and Athene Merger

On January 1, 2022, Apollo and Athene Holding Ltd. (“Athene”) completed the previously announced merger transactions pursuant to the Agreement and Plan of Merger (the “Merger Agreement”) by and among AAM, Tango Holdings, Inc., a Delaware corporation and a then wholly-owned subsidiary of AAM (“HoldCo”), Blue Merger Sub, Ltd., a Bermuda exempted company and a direct wholly-owned subsidiary of HoldCo (“AHL Merger Sub”), and Green Merger Sub, Inc., a Delaware corporation and a direct wholly-owned subsidiary of HoldCo (“AAM Merger Sub”). At the closing of the transactions, AHL Merger Sub merged with and into AHL (the “AHL Merger”), with AHL as the surviving entity in the AHL Merger and a subsidiary of HoldCo, and AAM Merger Sub merged with and into AAM (the “AAM Merger” and, together with the AHL Merger, the “Mergers”) with AAM as the surviving entity in the AAM Merger and a subsidiary of HoldCo.

In connection with the closing of the Mergers, HoldCo was renamed “Apollo Global Management, Inc.” Following the closing of the Mergers, all of the common shares of AHL and AAM are owned by AGM.

In connection with the closing of the Mergers, the Company completed a corporate recapitalization (the “Corporate Recapitalization”) which resulted in the recapitalization of AGM from an umbrella partnership C corporation (“up-C”) structure to a corporation with a single class of common stock with one vote per share.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The accompanying unaudited condensed consolidated financial statements are prepared in accordance with generally accepted accounting principles in the United States of America (“U.S. GAAP”). These condensed consolidated financial statements should be read in conjunction with the annual financial statements included in the 2021 Annual Report. Certain disclosures included in the annual financial statements have been condensed or omitted as they are not required for interim financial statements under U.S. GAAP and the rules of the SEC. The operating results presented for interim periods are not necessarily indicative of the results that may be expected for any other interim period or for the entire year.

-15-

APOLLO ASSET MANAGEMENT, INC.

NOTES TO CONDENSED CONSOLIDATED

FINANCIAL STATEMENTS (UNAUDITED)

(dollars in thousands, except share data, except where noted)

Consolidation

When an entity is consolidated, the accounts of the consolidated entity, including its assets, liabilities, revenues, expenses and cash flows, are presented on a gross basis. Consolidation does not have an effect on the amounts of net income reported. The Company consolidates entities where it has a controlling financial interest unless there is a specific scope exception that prevents consolidation. The types of entities with which the Company is involved generally include, but are not limited to:

•Subsidiaries, including management companies and general partners of funds that the Company manages

•Entities that have attributes of an investment company (e.g., funds)

•Special purpose acquisition companies (“SPACs”)

•Securitization vehicles (e.g., collateralized loan obligations (“CLOs”))

Each of these entities is assessed for consolidation depending on the specific facts and circumstances surrounding that entity. In determining whether to consolidate an entity, the Company first evaluates whether the entity is a variable interest entity (“VIE”) or a voting interest entity (“VOE”) and applies the appropriate consolidation model as discussed below. If an entity is not consolidated, then the Company’s investment is generally accounted for under the equity method of accounting or as a financial instrument as discussed in the related policy discussions below.

Investment Companies

Funds managed by the Company are generally accounted for as investment companies and are not required to consolidate their investments in operating companies. Judgment is required to evaluate whether entities have the characteristics of an investment company and are thus eligible to be accounted for as an investment company. Funds that meet the investment company criteria reflect their investments at fair value as required by specialized accounting guidance. The Company has retained this specialized accounting for investment companies in consolidation.

Variable Interest Entities

All entities are first considered under the VIE model. VIEs are entities that i) do not have sufficient equity at risk to finance its activities without additional subordinated financial support or ii) have equity investors that do not have the ability to make significant decisions related to the entity’s operations, absorb expected losses, or receive expected residual returns.

The Company consolidates a VIE if it is the primary beneficiary of the entity. The Company is deemed the primary beneficiary when it has a controlling financial interest in the VIE, which is defined as possessing both (i) the power to direct the activities of the VIE that most significantly impact the VIE’s economic performance and (ii) the obligation to absorb losses or the right to receive benefits from the VIE that could potentially be significant. The Company performs the VIE and primary beneficiary assessment at inception of its involvement with a VIE and on an ongoing basis as facts and circumstances change.

To assess whether the Company has the power to direct the activities that most significantly impact the VIE’s economic performance, it considers the design of the entity as well as ongoing rights and responsibilities. In general, the parties that can make the most significant decisions regarding asset management, servicing, liquidation rights or have the right to unilaterally remove those decision-makers are deemed to have the power to direct the activities of the VIE. To assess whether the Company has the obligation to absorb losses or right to receive benefits that could potentially be significant, the Company considers all its economic interests that are considered variable interests in the entity including interests held through related parties. This assessment requires judgment in considering whether those interests are significant.

Assets and liabilities of the consolidated VIEs, other than SPACs, are primarily shown in separate sections within the condensed consolidated statements of financial condition. Changes in the fair value of the consolidated VIEs’ assets and liabilities and related interest, dividend and other income and expenses are primarily presented within net gains from investment activities of consolidated variable interest entities in the condensed consolidated statements of operations. The portion attributable to Non-Controlling Interests is reported within net income attributable to Non-Controlling Interests in the condensed consolidated statements of operations. For additional disclosures regarding VIEs, see notes 6 and 14.

-16-

APOLLO ASSET MANAGEMENT, INC.

NOTES TO CONDENSED CONSOLIDATED

FINANCIAL STATEMENTS (UNAUDITED)

(dollars in thousands, except share data, except where noted)

Voting Interest Entities

For entities that are not determined to be VIEs, the entities are generally considered VOEs. Under the voting interest model, Apollo consolidates those entities it controls through a majority voting interest. Apollo does not consolidate those VOEs in which substantive kick-out rights have been granted to the unrelated investors to either dissolve the fund or remove the general partner.

Use of Estimates

The preparation of the condensed consolidated financial statements requires management to make estimates and assumptions that affect the reported amounts in the financial statements and the related footnotes. Apollo’s most significant estimates include goodwill, intangible assets, income taxes, performance allocations, incentive fees, contingent consideration obligation related to an acquisition, non-cash compensation, and fair value of investments and debt. While such impact may change considerably over time, the estimates and assumptions affecting the Company’s condensed consolidated financial statements are based on the best available information as of March 31, 2022. Actual results could differ materially from those estimates.

Cash and Cash Equivalents

Apollo considers all highly liquid short-term investments with original maturities of three months or less when purchased to be cash equivalents. Cash and cash equivalents include money market funds and U.S. Treasury securities. Interest income from cash and cash equivalents is recorded in interest income in the condensed consolidated statements of operations. The carrying values of the money market funds and U.S. Treasury securities represent their fair values due to their short-term nature. Substantially all of the Company’s cash on deposit is in interest bearing accounts with major financial institutions and exceed insured limits.

Restricted Cash and Cash Equivalents

Restricted cash and cash equivalents includes cash deposited at a bank, which is pledged as collateral in connection with leased premises.

U.S. Treasury securities, at fair value

U.S. Treasury securities, at fair value includes U.S. Treasury bills with original maturities greater than three months when purchased. These securities are recorded at fair value within investments on the condensed consolidated statements of financial condition. Interest income on such securities is separately presented from the overall change in fair value and is recognized in interest income in the condensed consolidated statements of operations. Any remaining change in fair value of such securities, that is not recognized as interest income, is recognized in net gains (losses) from investment activities in the condensed consolidated statements of operations. Securities are generally recognized on a trade date basis.

Fair Value of Financial Instruments

The fair value of a financial instrument is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date in an orderly transaction. Changes in the fair value of financial instruments are recorded and presented in net gains (losses) from investment activities except for certain investments for which the Company is entitled to receive performance allocations. For those investments, changes in fair value are presented in principal investment income.

-17-

APOLLO ASSET MANAGEMENT, INC.

NOTES TO CONDENSED CONSOLIDATED

FINANCIAL STATEMENTS (UNAUDITED)

(dollars in thousands, except share data, except where noted)

Financial instruments are generally recorded at fair value or at amounts whose carrying values approximate fair value. The actual realized gains or losses will depend on, among other factors, future operating results, the value of the assets and market conditions at the time of disposition, any related transaction costs and the timing and manner of sale, all of which may ultimately differ significantly from the assumptions on which the valuations were based.

Fair Value Option

Entities are permitted to elect the fair value option (“FVO”) to carry at fair value certain financial assets and financial liabilities, including investments otherwise accounted for under the equity method of accounting. The Company has elected the FVO for financial instruments held by its consolidated CLOs, which includes investments in loans and corporate bonds, as well as debt obligations and contingent obligations. Certain consolidated VIEs have applied the fair value option for certain investments in private debt securities that otherwise would not have been carried at fair value with gains and losses in net income. The FVO election is irrevocable and is applied to financial instruments on an individual basis at initial recognition or at eligible remeasurement events. Please refer to note 4 for additional information and other instances of when the Company has elected the FVO.

Fair Value Hierarchy

U.S. GAAP establishes a hierarchical disclosure framework which prioritizes and ranks the level of market price observability used in measuring financial instruments at fair value. Market price observability is affected by a number of factors, including the type of financial instrument, the characteristics specific to the financial instrument and the state of the marketplace, including the existence and transparency of transactions between market participants. Financial instruments with readily available quoted prices in active markets generally will have a higher degree of market price observability and a lesser degree of judgment used in measuring fair value.

Financial instruments measured and reported at fair value are classified and disclosed based on the observability of inputs used in the determination of fair values, as follows:

Level I - Quoted prices are available in active markets for identical financial instruments as of the reporting date. The types of financial instruments included in Level I include listed equities and debt. The Company does not adjust the quoted price for these financial instruments, even in situations where the Company holds a large position and the sale of such position would likely deviate from the quoted price.

Level II - Pricing inputs are other than quoted prices in active markets, which are either directly or indirectly observable as of the reporting date, and fair value is determined through the use of models or other valuation methodologies. Financial instruments that are generally included in this category include corporate bonds and loans, less liquid and restricted equity securities and certain over-the-counter derivatives where the fair value is based on observable inputs. These financial instruments exhibit higher levels of liquid market observability as compared to Level III financial instruments.

Level III - Pricing inputs are unobservable for the financial instrument and includes situations where there is little observable market activity for the financial instrument. The inputs into the determination of fair value may require significant management judgment or estimation. Financial instruments that are included in this category generally include general and limited partner interests in equity and hybrid funds, distressed debt and non-investment grade residual interests in securitizations, and CDOs and CLOs where the fair value is based on observable inputs as well as unobservable inputs.

When a security is valued based on broker quotes, the Company subjects those quotes to various criteria in making the determination as to whether a particular financial instrument would qualify for classification as Level II or Level III. These criteria include, but are not limited to, the number and quality of the broker quotes, the standard deviations of the observed broker quotes, and the percentage deviation from external pricing services.

Investments in securities that are traded on a securities exchange or comparable over-the-counter quotation systems are valued based on the last reported sale price at that date. If no sales of such investments are reported on such date, and in the case of over-the-counter securities or other investments for which the last sale date is not available, valuations are based on independent market quotations obtained from market participants, recognized pricing services or other sources deemed relevant, and the prices are based on the average of the “bid” and “ask” prices, or at ascertainable prices at the close of business on such day. Market quotations are generally based on valuation pricing models or market transactions of similar securities adjusted for

-18-

APOLLO ASSET MANAGEMENT, INC.

NOTES TO CONDENSED CONSOLIDATED

FINANCIAL STATEMENTS (UNAUDITED)

(dollars in thousands, except share data, except where noted)

security-specific factors such as relative capital structure priority and interest and yield risks, among other factors. When market quotations are not available, a model based approach is used to determine fair value.

In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, a financial instrument’s level within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement. The Company’s assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment and considers factors specific to the financial instrument when the fair value is based on unobservable inputs.

Equity Method Investments

For investments in entities where the Company exercises significant influence but does not meet the requirements for consolidation and has not elected the fair value option, the Company uses the equity method of accounting. Under the equity method of accounting, the Company records its share of the underlying income or loss of such entities adjusted for distributions. The Company’s share of the underlying net income or loss of such entities is recorded in principal investment income (loss) in the condensed consolidated statements of operations.

The carrying amounts of equity method investments are recorded in investments in the condensed consolidated statements of financial condition. Generally, the underlying entities that the Company manages and invests in are investment companies and the carrying value of the Company’s equity method investments approximates fair value.

Financial Instruments held by Consolidated VIEs

Under a measurement alternative permissible for consolidated collateralized financing entities, the Company measures both the financial assets and financial liabilities of consolidated CLOs in its condensed consolidated financial statements using the fair value of the financial assets or financial liabilities, whichever are more observable.

Where financial assets are more observable, the financial assets of the consolidated CLOs are measured at fair value and the financial liabilities are measured in consolidation as: (i) the sum of the fair value of the financial assets and the carrying value of any nonfinancial assets that are incidental to the operations of the CLOs less (ii) the sum of the fair value of any beneficial interests retained by the Company (other than those that represent compensation for services) and the Company’s carrying value of any beneficial interests that represent compensation for services. The resulting amount is allocated to the individual financial liabilities (other than the beneficial interest retained by the Company) using a reasonable and consistent methodology.

Where financial liabilities are more observable, the financial liabilities of the consolidated CLOs are measured at fair value and the financial assets are measured in consolidation as: (i) the sum of the fair value of the financial liabilities, and the carrying value of any nonfinancial liabilities that are incidental to the operations of the CLOs less (ii) the carrying value of any nonfinancial assets that are incidental to the operations of the CLOs. The resulting amount is allocated to the individual financial assets using a reasonable and consistent methodology.

Net income attributable to Apollo Asset Management, Inc. reflects the Company’s own economic interests in the consolidated CLOs including (i) changes in the fair value of the beneficial interests retained by the Company and (ii) beneficial interests that represent compensation for collateral management services.

Deferred Revenue

Apollo records deferred revenue, which is a type of contract liability, when consideration is received in advance of management services provided.

Apollo also earns management fees subject to the Management Fee Offset (described below). When advisory and transaction fees are earned by the management company, the Management Fee Offset reduces the management fee obligation of the fund. When the Company receives cash for advisory and transaction fees, a certain percentage of such advisory and/or transaction fees, as applicable, is allocated as a credit to reduce future management fees, otherwise payable by such fund. Such credit is recorded as deferred revenue in the condensed consolidated statements of financial condition. A portion of any excess advisory and transaction fees may be required to be returned to the limited partners of certain funds upon such fund’s liquidation. As the management fees earned by the Company are presented on a gross basis, any Management Fee Offsets calculated are presented as a reduction to advisory and transaction fees in the condensed consolidated statements of operations.

-19-

APOLLO ASSET MANAGEMENT, INC.

NOTES TO CONDENSED CONSOLIDATED

FINANCIAL STATEMENTS (UNAUDITED)

(dollars in thousands, except share data, except where noted)

Additionally, Apollo earns advisory fees pursuant to the terms of the advisory agreements with certain of the portfolio companies that are owned by the funds Apollo manages. When Apollo receives a payment from a portfolio company that exceeds the advisory fees earned at that point in time, the excess payment is recorded as deferred revenue in the condensed consolidated statements of financial condition. The advisory agreements with the portfolio companies vary in duration and the associated fees are received monthly, quarterly or annually.

Deferred revenue is reversed and recognized as revenue over the period that the agreed upon services are performed. There was $107.4 million of revenue recognized during the three months ended March 31, 2022 that was previously deferred as of January 1, 2022.

Under the terms of the funds’ partnership agreements, Apollo is normally required to bear organizational expenses over a set dollar amount and placement fees or costs in connection with the offering and sale of interests in the funds it manages to investors. The placement fees are payable to placement agents, who are independent third parties that assist in identifying potential investors, securing commitments to invest from such potential investors, preparing or revising offering and marketing materials, developing strategies for attempting to secure investments by potential investors and/or providing feedback and insight regarding issues and concerns of potential investors, when a limited partner either commits or funds a commitment to a fund. In cases where the limited partners of the funds are determined to be the customer in an arrangement, placement fees may be capitalized as a cost to acquire a customer contract, and amortized over the life of the customer contract. Capitalized placement fees are recorded within other assets in the condensed consolidated statements of financial condition, while amortization is recorded within placement fees in the condensed consolidated statements of operations. In certain instances, the placement fees are paid over a period of time. Based on the management agreements with the funds, Apollo considers placement fees and organizational costs paid in determining if cash has been received in excess of the management fees earned. Placement fees and organizational costs are normally the obligation of Apollo but can be paid for by the funds. When these costs are paid by the fund, the resulting obligations are included within deferred revenue. The deferred revenue balance will also be reduced during future periods when management fees are earned but not paid.

Revenues

The Company’s revenues include (i) management fees; (ii) advisory and transaction fees, net; (iii) investment income, which is comprised of performance allocations and principal investment income; and (iv) incentive fees.

The Company is required to recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services (i.e., the transaction price). When determining the transaction price, the Company may recognize variable consideration only to the extent that it is probable to not be significantly reversed. The Company is also required to disclose the nature, amount, timing, and uncertainty of revenue that is recognized.

Performance allocations are accounted for as equity method investments. The Company recognizes performance allocations within investment income along with the related principal investment income (as further described below) in the condensed consolidated statements of operations and within the investments line in the condensed consolidated statements of financial condition.

Refer to disclosures below for additional information on each of the Company’s revenue streams.

Management Fees

Management fees are recognized over time during the periods in which the related services are performed in accordance with the contractual terms of the related agreement. Management fees are generally based on (1) a percentage of the capital

-20-

APOLLO ASSET MANAGEMENT, INC.

NOTES TO CONDENSED CONSOLIDATED

FINANCIAL STATEMENTS (UNAUDITED)

(dollars in thousands, except share data, except where noted)

Advisory and Transaction Fees, Net

Advisory fees, including management consulting fees and directors’ fees, are generally recognized over time as the underlying services are provided in accordance with the contractual terms of the related agreement. The Company receives such fees in exchange for ongoing management consulting services provided to portfolio companies of funds it manages. Transaction fees, including structuring fees and arranging fees related to the Company’s funds, portfolio companies of funds and third parties are generally recognized at a point in time when the underlying services rendered are complete.

The amounts due from fund portfolio companies are recorded in due from related parties on the condensed consolidated statements of financial condition, which is discussed further in note 14. Under the terms of the limited partnership agreements for certain funds, the management fee payable by the funds may be subject to a reduction based on a certain percentage of such advisory and transaction fees, net of applicable broken deal costs (“Management Fee Offset”). Advisory and transaction fees are presented net of the Management Fee Offset in the condensed consolidated statements of operations.

Underwriting fees, which are also included within advisory and transaction fees, net, include gains, losses and fees, arising from securities offerings in which one of the Company’s subsidiaries participates in the underwriter syndicate. Underwriting fees are recognized at a point in time when the underwriting is completed. Underwriting fees recognized but not received are recorded in other assets on the condensed consolidated statements of financial condition.

Investment Income

Investment income is comprised of performance allocations and principal investment income.

Performance Allocations

Performance allocations are a type of performance revenue (i.e., income earned based on the extent to which an entity’s performance exceeds predetermined thresholds). Performance allocations are generally structured from a legal standpoint as an allocation of capital in which the Company’s capital account receives allocations of the returns of an entity when those returns exceed predetermined thresholds. The determination of which performance revenues are considered performance allocations is primarily based on the terms of an agreement with the entity.

The Company recognizes performance allocations within investment income along with the related principal investment income (as described further below) in the condensed consolidated statements of operations and within the investments line in the condensed consolidated statements of financial condition.

When applicable, the Company may record a general partner obligation to return previously distributed performance allocations. The general partner obligation is based upon an assumed liquidation of a fund’s net assets as of the reporting date and is reported within due to related parties on the condensed consolidated statements of financial condition. The actual determination and any required payment of any such general partner obligation would not take place until the final disposition of a fund’s investments based on the contractual termination of the fund or as otherwise set forth in the respective limited partnership agreement or other governing document of the fund.

-21-

APOLLO ASSET MANAGEMENT, INC.

NOTES TO CONDENSED CONSOLIDATED

FINANCIAL STATEMENTS (UNAUDITED)

(dollars in thousands, except share data, except where noted)

Incentive Fees

Incentive fees are a type of performance revenue. Incentive fees differ from performance allocations in that incentive fees do not represent an allocation of capital but rather a contractual fee arrangement with the entity.

Compensation and Benefits

Salaries, Bonus and Benefits

Salaries, bonus and benefits include base salaries, discretionary and non-discretionary bonuses, severance and employee benefits. Bonuses are generally accrued over the related service period.

Equity-Based Compensation