UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Amendment No. 1)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For

the fiscal year ended | |

| OR | |

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to

Commission

file number:

(Exact name of registrant as specified in its charter)

(State of other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| (Address of principal executive offices) | (Zip Code) |

(Registrant’s Telephone Number, including area code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT: None

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: None

Indicate

by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes ☐

Indicate

by check mark whether the Registrant (1) has filed all reports required by Section 13 or 15(d) of the Securities Exchange Act of 1934

(“Exchange Act”) during the preceding 12 months (or for such shorter period that the Registrant was required to file such

reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data

File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding

12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | |||

Smaller

reporting company Emerging

Growth Company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the Registrant is a shell company, as defined in Rule 12b-2 of the Exchange Act. Yes ☐

As

of December 31, 2022, the aggregate market value of the voting and non-voting shares of common stock of the registrant issued and outstanding

on such date, excluding shares held by affiliates of the registrant as a group, was $

Number of shares of Common Stock outstanding as of April 17, 2023: .

EXPLANATORY NOTE

The certifications required under Sections 302 and 906 of the Sarbanes-Oxley Act of 2002 that were filed and furnished, respectively, as Exhibits 31.1 and 31.2 and Exhibits 32.1 and 32.2 to the Original Filing have been re-executed and re-filed as of the date of this Amendment and are included as Exhibits 31.3 and 31.4 and Exhibit 32.3 and 32.4. Item 15 of Part IV of the Original Filing has been amended to reflect the new certifications.

Except as described above, no changes have been made to the Original Form 10-K, and this Amendment does not amend, update or change any other items or disclosures in the Original Form 10-K. The Original Form 10-K continues to speak as of its original filing date. This Amendment does not reflect subsequent events occurring after the filing date of the Original Form 10-K or modify or update in any way disclosures in the Original Form 10-K.

TABLE OF CONTENTS

| 2 |

Cautionary Note to U.S. Residents Concerning Disclosure of Mineral Resources

Bunker Hill Mining Corp. (“Bunker Hill,” “we,” “us,” “our” or the “Company”) is a U.S. domestic issuer for U.S. Securities and Exchange Commission (“SEC”) purposes, it is required to report its financial results under U.S. Generally Accepted Accounting Principles (“U.S. GAAP”), and its shares of common stock trade on the Canadian Securities Exchange (the “CSE”) and the OTCQB Venture Market. However, certain prior regulatory filings made in Canada contain or incorporate by reference therein certain disclosure that satisfies the additional requirements of Canadian securities laws, which differ from the requirements of United States’ securities laws. Unless otherwise indicated, all resource estimates included in those Canadian filings, and in the documents incorporated by reference therein, had been prepared in accordance with Canadian National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”) classification system. NI 43-101 is a rule developed by the Canadian Securities Administrators which establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects.

Canadian standards, including NI 43-101, may differ from the requirements of subpart 1300 of Regulation S-K (“S-K 1300”). Thus, resource information contained, or incorporated by reference, in the Company’s Canadian filings, and in the documents incorporated by reference therein, may not be comparable to similar information disclosed by companies reporting mineral reserve and mineral resource information under S-K 1300.

The terms “mineral reserve,” “proven mineral reserve” and “probable mineral reserve” are Canadian mining terms as defined in accordance with NI 43-101 and CIM standards. Pursuant to S-K 1300, the SEC now recognizes estimates of “measured mineral resources,” “indicated mineral resources” and “inferred mineral resources.” In addition, the SEC has amended its definitions of “proven mineral reserves” and “probably mineral reserves” to be substantially similar to the corresponding standards of the CIM.

Investors are cautioned that while terms are substantially similar to CIM standards, there are differences in the definitions and standards under S-K 1300 and the CIM standards. Accordingly, there is no assurance any mineral reserves or mineral resources that the Company may report as “proven reserves,” “probable reserves,” “measured mineral resources,” “indicated mineral resources” and “inferred mineral resources” under NI 43-101 will be the same as the reserve or resource estimates prepared under the standards adopted under S-K 1300.

Investors are also cautioned that while the SEC now recognizes “measured mineral resources,” “indicated mineral resources” and “inferred mineral resources,” investors should not assume that any part or all of mineral deposits in these categories will ever be converted into mineral reserves.

Mineralization described using these terms has a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an “measured mineral resource,” “indicated mineral resource” or “inferred mineral resource” will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable. Disclosure of “contained ounces” in a resource is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that does not constitute “reserves” by SEC standards as in place tonnage and grade without reference to unit measures.

| 3 |

PART I

ITEM 1. BUSINESS

Our Business

Overview

The Company’s sole focus is the development and restart of its 100% owned flagship asset, the Bunker Hill mine (the “Mine”) in Idaho, USA. The Mine remains the largest single producing mine by tonnage in the Silver Valley region of northwest Idaho, producing over 165 million ounces of silver and 5 million tons of base metals between 1885 and 1981. The Bunker Hill Mine is located within Operable Unit 2 of the Bunker Hill Superfund site (EPA National Priorities Listing IDD048340921), where cleanup activities have been completed.

In early 2020, a new management team comprised of former executives from Barrick Gold Corp. assumed leadership of the Company. Since that time, the Company conducted multiple exploration campaigns, published multiple economic studies and Mineral Resource Estimates, and advanced the rehabilitation and development of the Mine. In December 2021, it announced a project finance package with Sprott Private Resource Streaming & Royalty Corp. (“Sprott”), an amended Settlement Agreement with the U.S. Environmental Protection Agency (“the EPA”), and the purchase of the Bunker Hill Mine, setting the stage for a rapid restart of the Mine.

In January 2022, with the closing of the purchase of the Bunker Hill Mine, the funding of the $8,000,000 Royalty Convertible Debenture and $6,000,000 Series Convertible Debenture, and the announcement of an Memorandum (“MOU”)for the purchase of the Pend Oreille process plant from a subsidiary of Teck Resources Limited, the Company embarked on a program of activities with the goal of achieving a restart of the Mine. Key milestones and achievements from January 2022 onwards have included the closing of the purchase of the Pend Oreille process plant, the demobilization of the process plant to the Bunker Hill site, the completion of demolition activities at the Pend Oreille site, a Prefeasibility Study envisaging the restart of the Mine, and the completion of the primary portion of the ramp decline connecting the 5 and 6 Levels of the Bunker Hill Mine.

The Company was incorporated for the initial purpose of engaging in mineral exploration activities at the Mine. The Company has moved into the development stage concurrent with (i) purchasing the Mine and a process plant, (ii) completing successive technical and economic studies, including a Prefeasibility Study, (iii) delineating mineral reserves, and (iv) conducting the program of activities outlined above.

Lease and Purchase of the Bunker Hill Mine

The Company purchased the Bunker Hill Mine in January 2022, as described below.

Prior to purchasing the Mine, the Company had entered into a series of agreements with Placer Mining Corporation (“Placer Mining”), the prior owner, for the lease and option to purchase the Mine. The first of these agreements was announced on August 28, 2017, with subsequent amendments and/or extensions announced on November 1, 2019, July 7, 2020, and November 20, 2020.

Under the terms of the November 20, 2020 amended agreement (the “Amended Agreement”), a purchase price of $7,700,000 was agreed, with $5,700,000 payable in cash (with an aggregate of $300,000 to be credited toward the purchase price of the Mine as having been previously paid by the Company) and $2,000,000 in shares of common stock of the Company (“Common Shares”). The Company agreed to make an advance payment of $2,000,000, credited toward the purchase price of the Mine, which had the effect of decreasing the remaining amount payable to purchase the Mine to an aggregate of $3,400,000 payable in cash and $2,000,000 in Common Shares of the Company.

The Amended Agreement also required payments pursuant to an agreement with the EPA whereby for so long as the Company leases, owns and/or occupies the Mine, the Company would make payments to the EPA on behalf of Placer Mining in satisfaction of the EPA’s claim for historical water treatment cost recovery in accordance with the Settlement Agreement reached with the EPA in 2018. Immediately prior to the purchase of the Mine, the Company’s liability to EPA in this regard totaled $11,000,000.

The Company completed the purchase of the Bunker Hill Mine on January 7, 2022. The terms of the purchase price were modified to $5,400,000 in cash, from $3,400,000 of cash and $2,000,000 of Common Shares. Concurrent with the purchase of the Mine, the Company assumed incremental liabilities of $8,000,000 to the EPA, consistent with the terms of the amended Settlement Agreement with the EPA that was executed in December 2021 (see “EPA 2018 Settlement Agreement & 2021 Amended Settlement Agreement” section below).

| 4 |

EPA 2018 Settlement Agreement & 2021 Amended Settlement Agreement

Bunker Hill entered into a Settlement Agreement and Order on Consent with the EPA on May 15, 2018. This agreement limits the Company’s exposure to the Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”) liability for past environmental damage to the mine site and surrounding area to obligations that include:

| ● | Payment of $20,000,000 for historical water treatment cost recovery for amounts paid by the EPA from 1995 to 2017 | |

| ● | Payment for water treatment services provided by the EPA at the Central Treatment Plant (“CTP”) in Kellogg, Idaho until such time that Bunker Hill either purchases or leases the CTP or builds a separate EPA-approved water treatment facility | |

| ● | Conducting a work program as described in the Ongoing Environmental Activities section of this study |

In December 2021, in conjunction with its intention to purchase the mine complex, the Company entered into an amended Settlement Agreement (the “Amendment”) between the Company, Idaho Department of Environmental Quality, US Department of Justice and the EPA modifying the payment schedule and payment terms for recovery of historical environmental response costs at Bunker Hill Mine incurred by the EPA. With the purchase of the mine in early 2022, the remaining payments of the EPA cost recovery liability were assumed by the Company, resulting in a total of $19,000,000 liability to the Company, an increase of $8,000,000. The new payment schedule included a $2,000,000 payment to the EPA within 30 days of execution of this amendment, which was made.

The remaining $17,000,000 will be paid on the following dates:

| Date | Amount | |||

| November 1, 2024 | $ | 3,000,000 | ||

| November 1, 2025 | $ | 3,000,000 | ||

| November 1, 2026 | $ | 3,000,000 | ||

| November 1, 2027 | $ | 3,000,000 | ||

| November 1, 2028 | $ | 3,000,000 | ||

| November 1, 2029 | $ | 2,000,000 plus accrued interest | ||

The resumption of payments in 2024 was agreed in order to allow the Company to generate sufficient revenue from mining activities at the Bunker Hill Mine to address remaining payment obligations from free cash flow.

The changes in payment terms and schedule were contingent upon the Company securing financial assurance in the form of performance bonds or letters of credit deemed acceptable to the EPA totaling $17,000,000, corresponding to the Company’s cost recovery obligations to be paid in 2024 through 2029 as outlined above. Should the Company fail to make its scheduled payment, the EPA can draw against this financial assurance. The amount of the bonds or letters of credit will decrease over time as individual payments are made. If the Company failed to post the final financial assurance within 180 days of the execution of the Amendment, the terms of the original agreement would be reinstated.

In June 2022, the Company was successful in obtaining financial assurance. Specifically, a $9,999,000 payment bond and a $7,001,000 letter of credit were secured and provided to the EPA. This milestone provides for the Company to recognize the effects of the change in terms of the EPA liability as outlined in the December 20, 2021, agreement. Once the financial assurance was put into place, the restructuring of the payment stream under the Amendment occurred with the entire $17,000,000 liability being recognized as long-term in nature. The aforementioned payment bond and letter of credit were secured by $2,475,000 and $7,001,000 of cash deposits, respectively as of September 30, 2022.

In October 2022, the Company reported that it had been successful in securing a new payment bond to replace the aforementioned $7,001,000 letter of credit, in two stages. Initially, the letter of credit was reduced to $2,000,001 as a result of a new $5,000,000 payment bond obtained through an insurance company. The collateral for the new payment bond is comprised of a $2,000,000 letter of credit and land pledged by third parties, with whom the Company has entered into a financing cooperation agreement that contemplates a monthly fee of $20,000 (payable in cash or common shares of the Company, at the Company’s election). The new payment bond is scheduled to increase to $7,001,000 (from $5,000,000) upon the advance of the multi-metals stream from Sprott Private Resource Streaming & Royalty Corp.

| 5 |

Project Finance Package with Sprott Private Resource Streaming & Royalty Corp.

On December 20, 2021, the Company executed a non-binding term sheet outlining a $50,000,000 project finance package with Sprott Private Resource Streaming and Royalty Corp. (“Royalty”). The non-binding term sheet with SRSR outlined a project financing package that the Company expects to fulfill the majority of its funding requirements to restart the Mine. The term sheet consisted of an $8,000,000 royalty convertible debenture (the “RCD”), a $5,000,000 convertible debenture (the “CD1”), and a multi-metals stream of up to $37,000,000 (the “Stream”). The CD1 was subsequently increased to $6,000,000, increasing the project financing package to $51,000,000.

On June 17, 2022, the Company consummated a new $15,000,000 convertible debenture (the “CD2”). As a result, total potential funding from SRSR was further increased to $66,000,000 including the RCD, CD1, CD2 and the Stream (together, the “Project Financing Package”).

The Company closed the $8,000,000 RCD on January 7, 2022. The RCD bears interest at an annual rate of 9.0%, payable in cash or Common Shares at the Company’s option, until such time that SRSR elects to convert a royalty, with such conversion option expiring at the earlier of advancement of the Stream or July 7, 2023 (subsequently amended as described below). In the event of conversion, the RCD will cease to exist and the Company will grant a royalty for 1.85% of life-of-mine gross revenue from mining claims considered to be historically worked, contiguous to current accessible underground development, and covered by the Company’s 2021 ground geophysical survey (the “SRSR Royalty”). A 1.35% rate will apply to claims outside of these areas. The RCD was initially secured by a share pledge of the Company’s operating subsidiary, Silver Valley, until a full security package was put in place concurrent with the consummation of the CD1. In the event of non-conversion, the principal of the RCD will be repayable in cash.

Concurrent with the funding of the CD2 in June 2022, the Company and SRSR agreed to a number of amendments to the terms of the RCD, including an amendment of the maturity date from July 7, 2023, to March 31, 2025. The parties also agreed to a Royalty Put Option such that in the event the RCD is converted into a royalty as described above, the holder of the royalty will be entitled to resell the royalty to the Company for $8,000,000 upon default under the CD1 or CD2 until such time that the CD1 and CD2 are paid in full.

The Company closed the $6,000,000 CD1 on January 28, 2022, which was increased from the previously announced $5,000,000. The CD1 bears interest at an annual rate of 7.5%, payable in cash or shares at the Company’s option, and matures on July 7, 2023 (subsequently amended, as described below). The CD1 is secured by a pledge of the Company’s properties and assets. Until the closing of the Stream, the CD1 was to be convertible into Common Shares at a price of C$0.30 per Common Share, subject to stock exchange approval (subsequently amended, as described below). Alternatively, SRSR may elect to retire the CD1 with the cash proceeds from the Stream. The Company may elect to repay the CD1 early; if SRSR elects not to exercise its conversion option at such time, a minimum of 12 months of interest would apply.

Concurrent with the funding of the CD2 in June 2022, the Company and SRSR agreed to a number of amendments to the terms of the CD1, including that the maturity date would be amended from July 7, 2023, to March 31, 2025, and that the CD1 would remain outstanding until the new maturity date regardless of whether the Stream is advanced, unless the Company elects to exercise its option of early repayment. The Company determined that amendments to the terms should not be treated as an extinguishment of CD1, but as a debt modification.

The Company closed the $15,000,000 CD2 on June 17, 2022. The CD2 bears interest at an annual rate of 10.5%, payable in cash or shares at the Company’s option, and matures on March 31, 2025. The CD2 is secured by a pledge of the Company’s properties and assets. The repayment terms include 3 quarterly payments of $2,000,000 each beginning June 30, 2024, and $9,000,000 on the maturity date. Concurrent with the funding of the CD2 in June 2022, the Company and SRSR agreed that the minimum quantity of metal delivered under the Stream, if advanced, will increase by 10% relative to the amounts noted above.

On December 6, 2022, the Company closed a new $5,000,000 loan facility with Sprott (the “Bridge Loan”). The Bridge Loan, which was primarily utilized to pay outstanding water treatment payables to the EPA, is secured by the same security package that is in place with respect to the RCD, CD1, and CD2. The Bridge Loan bears interest at a rate of 10.5% per annum and matures at the earlier of (i) the advance of the Stream, or (ii) June 30, 2024. In addition, the minimum quantity of metal delivered under the Stream, if advanced, would increase by 5% relative to amounts previously announced.

A minimum of $27,000,000 and a maximum of $37,000,000 (the “Stream Amount”) will be made available under the Stream, at the Company’s option, once the conditions of availability of the Stream have been satisfied including confirmation of full project funding by an independent engineer appointed by SRSR. If the Company draws the maximum funding of $37,000,000, the Stream will apply to 10% of payable metals sold until a minimum quantity of metal is delivered consisting of, individually, 63.5 million pounds of zinc, 40.4 million pounds of lead, and 1.2 million ounces of silver (including amendments agreed concurrent with closing of the CD2 and Bridge Loan, as described above). Thereafter, the Stream would apply to 2% of payable metals sold. If the Company elects to draw less than $37,000,000 under the Stream, the percentage and quantities of payable metals streamed will adjust pro-rata. The delivery price of streamed metals will be 20% of the applicable spot price. The Company may buy back 50% of the Stream Amount at a 1.40x multiple of the Stream Amount between the second and third anniversary of the date of funding, and at a 1.65x multiple of the Stream Amount between the third and fourth anniversary of the date of funding.

| 6 |

As of December 31, 2022, the Stream had not been advanced. The Company is finalizing discussions with Sprott regarding the advance of the Stream, which is conditional on satisfactory conclusion of the definitive documentation relating to the Stream, full project funding for the Bunker Hill Mine and certain other conditions precedent.

Concurrent with discussions with Sprott regarding the advance of the Stream, the Company is advancing efforts to secure offtake financing of up $20 million from third parties to complement the Stream in financing the restart of the Bunker Hill Mine.

Process Plant

On January 25, 2022, the Company announced that it had entered into a non-binding Memorandum of Understanding (“MOU”) with Teck Resources Limited (“Teck”) for the purchase of a comprehensive package of equipment and parts inventory from its Pend Oreille site (the “Process Plant”) in eastern Washington State, approximately 145 miles from the Bunker Hill Mine by road. The package comprises substantially all processing equipment of value located at the site, including complete crushing, grinding and flotation circuits suitable for a planned ~1,500 ton-per-day operation at Bunker Hill, and total inventory of nearly 10,000 components and parts for mill, assay lab, conveyer, field instruments, and electrical spares. The Company paid a $500,000 non-refundable deposit in January 2022.

On March 31, 2022, the Company announced that it had reached an agreement with a subsidiary of Teck to satisfy the remaining purchase price for the Process Plant by way of an equity issuance of the Company. Teck will receive 10,416,667 units of the Company (the “Teck Units”) at a deemed issue price of C$0.30 per unit. Each Teck Unit consists of one Common Share and one Common Share purchase warrant (the “Teck Warrants”). Each whole Teck Warrant entitles the holder to acquire one Common Share at a price of C$0.37 per Common Share for a period of three years. The equity issuance and purchase of the Process Plant occurred on May 13, 2022.

On August 30, 2022, the Company entered into an agreement to purchase a ball mill from D’Angelo International LLC for $675,000. The purchase of the mill is to be made in three cash payments. The first two payments were made as follows:

| ● | $100,000 on September 15, 2022, as a non-refundable deposit | |

| ● | $100,000 on October 13, 2022, as a refundable deposit |

The Company has not made the final payment of $475,000 as of the issuance of this report.

Business Operations

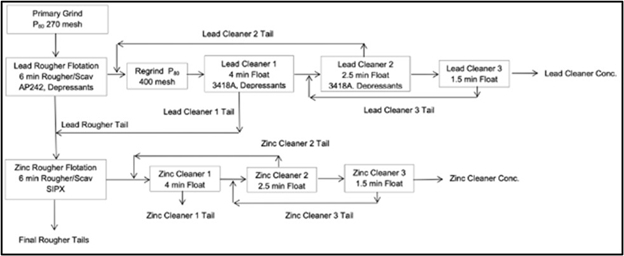

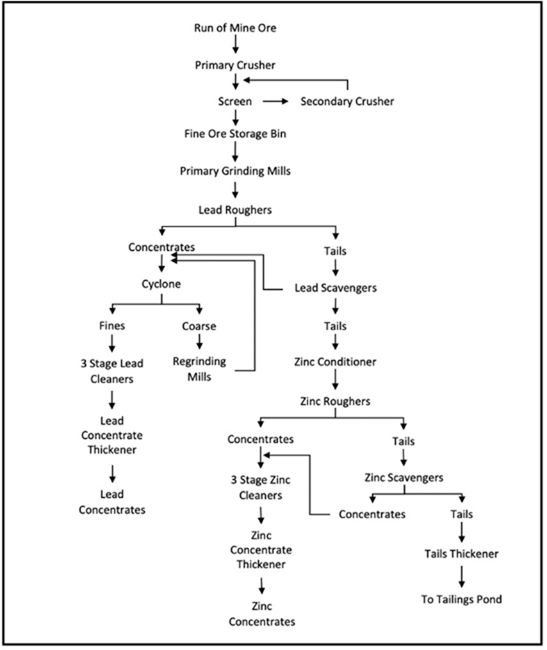

The Mine is a zinc-lead-silver Mine. When back in production, the Company intends to mill mineral resources on-site to produce both zinc and lead-silver concentrates which will then be shipped to a third-party smelter for processing.

Infrastructure

The Mine includes all mining rights and claims, surface rights, fee parcels, mineral interests, easements, existing infrastructure at Milo Gulch, and the majority of machinery and buildings at the Kellogg Tunnel portal level, as well as all equipment and infrastructure anywhere underground at the Bunker Hill Mine Complex. It also includes all current and historic data relating to the Bunker Hill Mine Complex, such as drill logs, reports, maps, and similar information located at the Mine site or any other location.

For further detail, please refer to the “Project Infrastructure” section in Item 2 below.

| 7 |

Government Regulation and Approval

Exploration and development activities, and any future mining operations, are subject to extensive laws and regulations governing the protection of the environment, waste disposal, worker safety, mine construction, and protection of endangered and protected species. The Company has made, and expects to make in the future, significant expenditures to comply with such laws and regulations. Future changes in applicable laws, regulations and permits or changes in their enforcement or regulatory interpretation could have an adverse impact on the Company’s financial condition or results of operations.

It may be necessary to obtain the following environmental permits or approved plans prior to commencement of mine operations:

| ● | Reclamation and Closure Plan | |

| ● | Water Discharge Permit | |

| ● | Air Quality Operating Permit | |

| ● | Industrial Artificial (tailings) pond permit | |

| ● | Obtaining Water Rights for Operations |

If these permits are required, there can be no assurance that the Company will be able to obtain them in a timely manner or at all. For further detail, please refer to the “Environmental Studies and Permitting” section of the “Technical Report Summary” in Item 2 below.

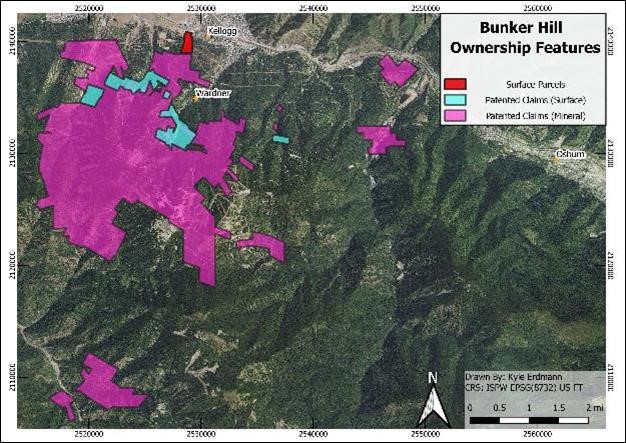

Property Description

The Company has mineral rights to approximately 440 patented mining claims covering over 5700 acres. Of these claims, 35 include surface ownership of approximately 259 acres. It also has certain parcels of fee property which include mineral and surface rights but not patented mining claims. Mining claims and fee properties are located in Townships 47, 48 North, Range 2 East, Townships 47, 48 North, Range 3 East, Boise Meridian, Shoshone County, Idaho.

Patented mining claims in the State of Idaho do not require permits for underground mining activities to commence on private lands. Other permits associated with underground mining may be required, such as water discharge and site disturbance permits. The water discharge is being handled by the EPA at the existing CTP. The Company expects to take on the water treatment responsibility in the future and obtain an appropriate discharge permit.

For further detail, please refer to the “Property Description and Ownership” section of the “Technical Report Summary” in Item 2 below.

Competition

The Company competes with other mining and exploration companies in connection with the acquisition of mining claims and leases on zinc and other base and precious metals prospects as well as in connection with the recruitment and retention of qualified employees. Many of these companies are much larger than the Company, have greater financial resources and have been in the mining business for much longer than it has. As such, these competitors may be in a better position through size, finances and experience to acquire suitable exploration and development properties. The Company may not be able to compete against these companies in acquiring new properties and/or qualified people to work on its current project, or any other properties that may be acquired in the future.

Given the size of the world market for base precious metals such as silver, lead and zinc, relative to the number of individual producers and consumers, it is believed that no single company has sufficient market influence to significantly affect the price or supply of these metals in the world market.

Employees

The Company has ten employees. The balance of the Company’s operations is contracted for as consultants.

Reports to Security Holders

The Company files reports with the SEC under section 15d of the Securities Exchange Act of 1934 (the “Exchange Act”). The reports will be filed electronically. All copies of any materials filed with the SEC may be read at the SEC’s Public Reference Room at 100 F Street, NE, Room 1580, Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC also maintains an Internet site that will contain copies of the reports that are filed electronically. The address for the SEC Internet site is http://www.sec.gov.

| 8 |

ITEM 1A. RISK FACTORS

As a Smaller Reporting Company, this item is not required under SEC rules. However, the Company believes that it is important to have an understanding of the risks associated with an investment in the Company. In addition, these risk factors are incorporated by reference in press releases and other Company publications for purposes of the Private Securities Reform Act of 1995.

General Risk Factors

The Company’s ability to operate as a going concern is in doubt.

The audit opinion and notes that accompany the Company’s Financial Statements disclose a going concern qualification to its ability to continue in business. The accompanying Financial Statements have been prepared under the assumption that the Company will continue as a going concern. The Company is an exploration and development stage company and has incurred losses since its inception. The Company has incurred losses resulting in an accumulated deficit of $71,592,559 as of December 31, 2022 and further losses are anticipated in the development of its business.

The Company currently has no historical recurring source of revenue and its ability to continue as a going concern is dependent on its ability to raise capital to fund its future exploration and working capital requirements or its ability to profitably execute its business plan. The Company’s plans for the long-term return to and continuation as a going concern include financing its future operations through sales of its Common Shares and/or debt and the eventual profitable exploitation of the Mine. Additionally, the volatility in capital markets and general economic conditions in the U.S. and elsewhere can pose significant challenges to raising the required funds. These factors raise substantial doubt about the Company’s ability to continue as a going concern.

The Company’s consolidated financial statements do not give effect to any adjustments required to realize its assets and discharge its liabilities in other than the normal course of business and at amounts different from those reflected in the accompanying Financial Statements.

The Company will require significant additional capital to fund its short-term obligations, continue its operations and remain in compliance with its debt agreements.

Neither the Company nor any of the directors of the Company nor any other party can provide any guarantee or assurance that the Company will be able to raise sufficient capital to satisfy the Company’s short-term obligations. The Company does not have sufficient funds to satisfy its short-term financial obligations, even after consideration of its recently completed equity financing. As at December 31, 2022, the Company had $708,105 in cash and total current liabilities of $10,155,582 and total liabilities of $59,106,835. The Company will likely require additional capital by the end of the second quarter of 2023 in order to continue its operations. Further, if the Company does not raise sufficient additional capital, the Company will be in breach of its debt agreements, including under the RCD, CD1, CD2 and Bridge Loan.

The Company may not be able to secure the Stream or alternative funding from Sprott or another capital provider.

Neither the Company nor any of the directors of the Company nor any other party can provide any guarantee or assurance that the Stream, the final contemplated tranche of the full $66,000,000 project financing package, will be finalized or close, or any other funding from Sprott. The Stream remains subject to Sprott internal approvals, full project funding, further technical and other due diligence and satisfactory documentation. If the Stream, or a portion thereof, does not close there is no guarantee that alternative capital can be raised on terms favorable to the Company, or at all.

Any additional equity funding, for which there can be no guarantee or assurance with regard to any amount or terms thereof, will dilute existing shareholders.

A concentrate offtake agreement with Teck Resources may not be reached, which could result in less favorable commercial terms for the sale of concentrates envisaged to be produced by the Bunker Hill Mine and could also impact the Company’s ability to secure offtake financing. Regardless of actions taken by Teck, there can be no assurance that the Company will be able to secure or close offtake financing, which could have an adverse effect on the Company’s financial position and negative impact the Company’s ability to secure additional funding from Sprott or an alternative capital provider.

The Company may not be able to execute a concentrate offtake agreement for the sale of concentrates to Teck Resources at its Trail smelter, as contemplated with Teck’s option to acquire 100% of zinc and lead concentrate produced in the first five years at the Bunker Hill Mine. If such an agreement cannot be reached, the Company may not be able to sell its zinc and lead concentrate to Teck, which could result in difficulties securing alternative commercial arrangements for the sale of concentrate, less favorable commercial terms in the event that alternative commercial arrangements can be secured, and/or higher transportation and other costs. In addition, the Company may not be able to secure or close offtake financing, regardless of whether an agreement is reached with Teck; the terms of any offtake financing might not be favorable to the Company; and/or the Company may incur substantial fees and costs related to such financing. The Company’s inability to secure or close offtake financing, or arrange a suitable alternative, may have an adverse effect on the Company’s operations and financial position, including its ability to secure the Stream from Sprott.

| 9 |

The Bunker Hill Mine restart is now expected to take place in 2024, with first concentrate production targeted for mid-2024. Changes to this timeline, or other factors impacting the restart project budget, could increase the Company’s required capital needs through the completion of the project, which would adversely affect the Company’s ability to secure additional funding, thereby adversely affecting its financial condition.

On February 28, 2023, the Company announced that primarily due to the inability to procure certain long-lead items that were planned to be ordered by February 2023, and longer estimated delivery times thereof, the Company now expects the Bunker Hill Mine restart to be achieved in 2024. On March 10, 2023, the Company announced that it has maintained the integrity of its total pre-production budget, under the assumption of first concentrate production in the second quarter of 2024.

In the event that the Company is unable to secure sufficient funding to materially advance the restart of the Mine in the second quarter of 2023, from Sprott or an alternative capital provider, it is likely that the restart timeline will be further delayed with a potentially materially adverse effect on the pre-production budget.

Notwithstanding financing-related risks, the Company’s pre-production budget estimates are subject to change based on factors beyond its control, including but not limited to cost inflation and supply chain dynamics. An increase in the Company’s pre-production budget estimates could have a materially adverse impact on its ability to secure project financing. This could have a material adverse effect on its financial condition, results of operations, or prospects. Sales of substantial amounts of securities may have a highly dilutive effect on the Company’s ownership or share structure. Sales of a large number of shares of the Company’s Common Shares in the public markets, or the potential for such sales, could decrease the trading price of the Common Shares and could impair the Company’s ability to raise capital through future sales of Common Shares. The Company has not yet commenced commercial production at any of its properties and, therefore, has not generated positive cash flows to date and has no reasonable prospects of doing so unless successful commercial production can be achieved at the Mine. The Company expects to continue to incur negative investing and operating cash flows until such time as it enters into successful commercial production. This will require the Company to deploy its working capital to fund such negative cash flow and to seek additional sources of financing. There is no assurance that any such financing sources will be available or sufficient to meet the Company’s requirements, or if available, available upon terms acceptable to the Company. There is no assurance that the Company will be able to continue to raise equity capital or to secure additional debt financing, or that the Company will not continue to incur losses.

Payment bonds securing $17,000,000 due by the Company to the EPA for cost recovery may not be renewable or may only be renewable on terms that are unfavorable to the Company, which would adversely affect its financial condition or cause a default under the revised settlement agreement with the EPA and Sprott.

In 2022, the Company secured financial assurance in the form of payment bonds in accordance with the revised settlement agreement with the EPA, in relation to $17,000,000 of payments due to the EPA for cost recovery between 2024-2029. These bonds are renewed annually, and currently require $6,476,000 of collateral in the form of letters of credit. To the extent that the parties providing the payment bonds demand additional collateral beyond the current requirements, or other unfavorable terms or conditions, the Company may not be able to renew the payment bonds on favorable conditions, or at all. This could have a materially adverse impact on the Company, including a potential default under the revised settlement agreement with the EPA.

The Company has a limited operating history on which to base an evaluation of its business and prospects.

Since its inception, the Company has had no revenue from operations. The Company has no history of producing products from the Bunker Hill property. The Mine is a historic, past producing mine with very little recent exploration work. Advancing the Mine through the development stage will require significant capital and time, and successful commercial production from the Mine will be subject to completing the requisite studies, permitting and re-commissioning of the Mine, constructing a processing plant, and other related works and infrastructure. As a result, the Company is subject to all of the risks associated with developing and establishing new mining operations and business enterprises, including:

| ● | completion of studies to verify reserves and commercial viability, including the ability to find sufficient ore reserves to support a commercial mining operation; | |

| ● | the timing and cost, which can be considerable, of further exploration, preparing feasibility studies, permitting and construction of infrastructure, mining and processing facilities; | |

| ● | the availability and costs of drill equipment, exploration personnel, skilled labor, and mining and processing equipment, if required; | |

| ● | the availability and cost of appropriate smelting and/or refining arrangements, if required; | |

| ● | compliance with stringent environmental and other governmental approval and permit requirements; | |

| ● | the availability of funds to finance exploration, development, and construction activities, as warranted; | |

| ● | potential opposition from non-governmental organizations, local groups or local inhabitants that may delay or prevent development activities; | |

| ● | potential increases in exploration, construction, and operating costs due to changes in the cost of fuel, power, materials, and supplies; and | |

| ● | potential shortages of mineral processing, construction, and other facilities related supplies. |

| 10 |

The costs, timing, and complexities of exploration, development, and construction activities may be increased by the location of its properties and demand by other mineral exploration and mining companies. It is common in exploration programs to experience unexpected problems and delays during drill programs and, if commenced, development, construction, and mine start-up. In addition, the Company’s management and workforce will need to be expanded, and sufficient housing and other support systems for its workforce will have to be established. This could result in delays in the commencement of mineral production and increased costs of production. Accordingly, the Company’s activities may not result in profitable mining operations, and it may not succeed in establishing mining operations or profitably producing metals at any of its current or future properties, including the Mine.

The Company has a history of losses and expects to continue to incur losses in the future.

The Company has incurred losses since inception, has had negative cash flow from operating activities, and expects to continue to incur losses in the future. The Company has incurred the following losses from operations during each of the following periods:

| ● | $16,487,161 for the year ended December 31, 2022; and | |

| ● | $18,752,504 for the year ended December 31, 2021 |

The Company expects to continue to incur losses unless and until such time as the Mine enters into commercial production and generates sufficient revenues to fund continuing operations. The Company recognizes that if it is unable to generate significant revenues from mining operations and dispositions of its properties, the Company will not be able to earn profits or continue operations. At this early stage of its operation, the Company also expects to face the risks, uncertainties, expenses, and difficulties frequently encountered by smaller reporting companies. The Company cannot be sure that it will be successful in addressing these risks and uncertainties and its failure to do so could have a materially adverse effect on its financial condition.

Epidemics, pandemics or other public health crises, including COVID-19, could adversely affect the Company’s business.

The Company’s operations could be significantly adversely affected by the effects of a widespread outbreak of epidemics, pandemics or other health crises, including the recent outbreak of respiratory illness caused by the novel coronavirus (“COVID-19”), which was declared a pandemic by the World Health Organization on March 12, 2020. The Company cannot accurately predict the impact COVID-19 or some future variant would have on its operations and the ability of others to meet their obligations with the Company, including uncertainties relating to the ultimate geographic spread of the virus, the severity of the disease, the duration of the outbreak, and the length of travel and quarantine restrictions imposed by governments of affected countries. In addition, a significant outbreak of contagious diseases in the human population could result in a widespread health crisis that could adversely affect the economies and financial markets of many countries, resulting in an economic downturn that could further affect the Company’s operations and ability to finance its operations.

The Russia/Ukraine crisis, including the impact of sanctions or retributions thereto, could adversely affect the Company’s business.

The Company’s operations could be adversely affected by the effects of the escalating Russia/Ukraine crisis and the effects of sanctions imposed against Russia or that country’s retributions against those sanctions, embargos or further-reaching impacts upon energy prices, food prices and market disruptions. The Company cannot accurately predict the impact the crisis will have on its operations and the ability of contractors to meet their obligations with the Company, including uncertainties relating the severity of its effects, the duration of the conflict, and the length and magnitude of energy bans, embargos and restrictions imposed by governments. In addition, the crisis could adversely affect the economies and financial markets of the United States in general, resulting in an economic downturn that could further affect the Company’s operations and ability to finance its operations. Additionally, the Company cannot predict changes in precious metals pricing or changes in commodities pricing which may alternately affect the Company either positively or negatively.

Risks Related to Mining and Exploration

The Company is in the development stage.

| 11 |

The nature of mineral exploration and production activities involves a high degree of risk and the possibility of uninsured losses.

Exploration for and the production of minerals is highly speculative and involves much greater risk than many other businesses. Most exploration programs do not result in the discovery of mineralization, and any mineralization discovered may not be of sufficient quantity or quality to be profitably mined. The Company’s operations are, and any future development or mining operations the Company may conduct will be, subject to all of the operating hazards and risks normally incidental to exploring for and development of mineral properties, including, but not limited to:

| ● | economically insufficient mineralized material; | |

| ● | fluctuation in production costs that make mining uneconomical; | |

| ● | labor disputes; | |

| ● | unanticipated variations in grade and other geologic problems; | |

| ● | environmental hazards; | |

| ● | water conditions; | |

| ● | difficult surface or underground conditions; | |

| ● | industrial accidents; | |

| ● | metallurgic and other processing problems; | |

| ● | mechanical and equipment performance problems; | |

| ● | failure of dams, stockpiles, wastewater transportation systems, or impoundments; | |

| ● | unusual or unexpected rock formations; and | |

| ● | personal injury, fire, flooding, cave-ins and landslides. |

Any of these risks can materially and adversely affect, among other things, the development of properties, production quantities and rates, costs and expenditures, potential revenues, and production dates. If the Company determines that capitalized costs associated with any of its mineral interests are not likely to be recovered, the Company would incur a write-down of its investment in these interests. All these factors may result in losses in relation to amounts spent that are not recoverable, or that result in additional expenses.

Commodity price volatility could have dramatic effects on the results of operations and the Company’s ability to execute its business plan.

The price of commodities varies on a daily basis. The Company’s future revenues, if any, will likely be derived from the extraction and sale of base and precious metals. The price of those commodities has fluctuated widely, particularly in recent years, and is affected by numerous factors beyond its control including economic and political trends, expectations of inflation, currency exchange fluctuations, interest rates, global and regional consumptive patterns, speculative activities and increased production due to new extraction developments and improved extraction and production methods. The effect of these factors on the price of base and precious metals, and therefore the economic viability of the Company’s business, could negatively affect its ability to secure financing or its results of operations.

The Company’s development and production plans, and cost estimates, in the Technical Report Summary may vary and/or not be achieved.

There is no certainty that the Technical Report Summary will be realized. The decision to implement the Mine restart scenario to be included in the Technical Report Summary will not be based on a feasibility study of mineral reserves demonstrating economic and technical viability, and therefore there is increased risk that the Technical Report Summary results will not be realized. If the Company is unable to achieve the results in the Technical Report Summary, it may have a material negative impact on the Company and its capital investment to implement the restart scenario may be lost.

Costs charged to the Company by the Idaho Department of Environmental Quality (“IDEQ”) for treatment of wastewater fluctuate a great deal and are not within the Company’s control.

The Company is billed annually for water treatment activities performed by the IDEQ for the EPA. The water treatment costs that Bunker Hill is billed for are partially related to the EPA’s direct cost of treating the water emanating from the Bunker Hill Mine, which are comprised of lime and flocculant usage, electricity consumption, maintenance and repair, labor and some overhead. Rate of discharge of effluent from the Bunker Hill Mine is largely dependent on the level of precipitation within a given year and how close in the calendar year the Company is to the spring run-off. Increases in water infiltrations and gravity flows within the mine generally increase after winter and result in a peak discharge rate in May. Increases in gravity flow and consequently the rate of water discharged by the mine have a highly robust correlation with metal concentrations and consequently metals loads of effluent.

Hydraulic loads (quantities of water per unit of time) and metal loads (quantities of metals per unit of volume of effluent per unit of time) are the two main determinants of cost of water treatment by the EPA in the relationship with the Bunker Hill Mine because greater metal loads consume more lime and more flocculent and more electricity to remove the increased levels of metals and make the water clean. The scale of the treatment plant is determined by how much total water can be processed (hydraulic load) at any one point in time. This determines how much labor is required to operate the plant and generally determines the amount of overhead required to run the EPA business.

| 12 |

The EPA has completed significant upgrades to the water treatment capabilities of the CTP and is now capable of producing treated water than can meet a much higher discharge standard (which Bunker Hill will be forced to meet beyond May 2023). While it was understood that improved performance capability would increase the cost of operating the plant, it was unclear to EPA, and consequently to Bunker Hill, how much the costs would increase by.

These elements described above, and others, impact the direct costs of water treatment. A significant portion of the total amount invoiced by EPA each year is indirect cost that is determined as a percentage of the direct cost. Each year the indirect costs percentage changes within each region of the EPA. Bunker Hill has no ability to impact the percentage of indirect cost that is set by the EPA regional office. Bunker Hill also has no advanced notice of what the percentage of indirect cost will be until it receives its invoice in June of the year following the billing period. The Company remains unable to estimate EPA billings to a high degree of accuracy.

Estimates of mineral reserves and resources are subject to evaluation uncertainties that could result in project failure.

Its exploration and future mining operations, if any, are and would be faced with risks associated with being able to accurately predict the quantity and quality of mineral resources/reserves within the earth using statistical sampling techniques. Estimates of any mineral resource/reserve on the Mine would be made using samples obtained from appropriately placed trenches, test pits, underground workings, and intelligently designed drilling. There is an inherent variability of assays between check and duplicate samples taken adjacent to each other and between sampling points that cannot be reasonably eliminated. Additionally, there also may be unknown geologic details that have not been identified or correctly appreciated at the current level of accumulated knowledge about the Mine. This could result in uncertainties that cannot be reasonably eliminated from the process of estimating mineral resources/reserves. If these estimates were to prove to be unreliable, the Company could implement an exploitation plan that may not lead to commercially viable operations in the future.

Any material changes in mineral resource/reserve estimates and grades of mineralization will affect the economic viability of placing a property into production and a property’s return on capital.

As the Company has not commenced actual production, mineral resource estimates may require adjustments or downward revisions. In addition, the grade of ore ultimately mined, if any, may differ from that indicated by future feasibility studies and drill results. Minerals recovered in small scale tests may not be duplicated in large scale tests under on-site conditions or in production scale.

The Company’s exploration activities may not be commercially successful, which could lead the Company to abandon its plans to develop the Mine and its investments in exploration.

The Company’s long-term success depends on its ability to identify mineral deposits on the Mine and other properties the Company may acquire, if any, that the Company can then develop into commercially viable mining operations. Mineral exploration is highly speculative in nature, involves many risks, and is frequently non-productive. These risks include unusual or unexpected geologic formations, and the inability to obtain suitable or adequate machinery, equipment, or labor. The success of commodity exploration is determined in part by the following factors:

| ● | the identification of potential mineralization based on surficial analysis; | |

| ● | availability of government-granted exploration permits; | |

| ● | the quality of its management and its geological and technical expertise; and | |

| ● | the capital available for exploration and development work. |

Substantial expenditures are required to establish proven and probable reserves through drilling and analysis, to develop metallurgical processes to extract metal, and to develop the mining and processing facilities and infrastructure at any site chosen for mining. Whether a mineral deposit will be commercially viable depends on a number of factors that include, without limitation, the particular attributes of the deposit, such as size, grade, and proximity to infrastructure; commodity prices, which can fluctuate widely; and government regulations, including, without limitation, regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals, and environmental protection. The Company may invest significant capital and resources in exploration activities and may abandon such investments if the Company is unable to identify commercially exploitable mineral reserves. The decision to abandon a project may have an adverse effect on the market value of the Company’s securities and the ability to raise future financing.

| 13 |

The Company is subject to significant governmental regulations that affect its operations and costs of conducting its business and may not be able to obtain all required permits and licenses to place its properties into production.

The Company’s current and future operations, including exploration and, development of the Mine, do and will require permits from governmental authorities and will be governed by laws and regulations, including:

| ● | laws and regulations governing mineral concession acquisition, prospecting, development, mining, and production; | |

| ● | laws and regulations related to exports, taxes, and fees; | |

| ● | labor standards and regulations related to occupational health and mine safety; and | |

| ● | environmental standards and regulations related to waste disposal, toxic substances, land use reclamation, and environmental protection. |

Specifically, it may be necessary to obtain the following environmental permits or approved plans prior to commencement of mine operations:

| ● | Reclamation and Closure Plan | |

| ● | Water Discharge Permit | |

| ● | Air Quality Operating Permit | |

| ● | Industrial Artificial (tailings) pond permit | |

| ● | Obtaining Water Rights for Operations |

If these permits are required, there can be no assurance that the Company will be able to obtain them in a timely manner or at all.

Companies engaged in exploration activities often experience increased costs and delays in production and other schedules as a result of the need to comply with applicable laws, regulations, and permits. Failure to comply with applicable laws, regulations, and permits may result in enforcement actions, including the forfeiture of mineral claims or other mineral tenures, orders issued by regulatory or judicial authorities requiring operations to cease or be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment, or costly remedial actions. The Company cannot predict if all permits that it may require for continued exploration, development, or construction of mining facilities and conduct of mining operations will be obtainable on reasonable terms, if at all. Costs related to applying for and obtaining permits and licenses may be prohibitive and could delay its planned exploration and development activities. The Company may be required to compensate those suffering loss or damage by reason of the mineral exploration or its mining activities, if any, and may have civil or criminal fines or penalties imposed for violations of, or its failure to comply with, such laws, regulations, and permits.

Existing and possible future laws, regulations, and permits governing operations and activities of exploration companies, or more stringent implementation of such laws, regulations and permits, could have a material adverse impact on the Company’s business and cause increases in capital expenditures or require abandonment or delays in exploration. The Mine is located in Northern Idaho and has numerous clearly defined regulations with respect to permitting mines, which could potentially impact the total time to market for the project.

The Company’s activities are subject to environmental laws and regulations that may increase its costs of doing business and restrict its operations.

Both mineral exploration and extraction require permits from various federal, state, and local governmental authorities and are governed by laws and regulations, including those with respect to prospecting, mine development, mineral production, transport, export, taxation, labor standards, occupational health, waste disposal, toxic substances, land use, environmental protection, mine safety and other matters. There can be no assurance that the Company will be able to obtain or maintain any of the permits required for the exploration of the mineral properties or for the construction and operation of the Mine at economically viable costs. If the Company cannot accomplish these objectives, its business could fail. The Company believes that it is in compliance with all material laws and regulations that currently apply to its activities but there can be no assurance that the Company can continue to remain in compliance. Current laws and regulations could be amended, and the Company might not be able to comply with them, as amended. Further, there can be no assurance that the Company will be able to obtain or maintain all permits necessary for its future operations, or that it will be able to obtain them on reasonable terms. To the extent such approvals are required and are not obtained, the Company may be delayed or prohibited from proceeding with planned exploration or development of the mineral properties.

The Company’s activities are subject to extensive laws and regulations governing environmental protection. The Company is also subject to various reclamation-related conditions. Although the Company closely follows and believes it is operating in compliance with all applicable environmental regulations, there can be no assurance that all future requirements will be obtainable on reasonable terms. Failure to comply may result in enforcement actions causing operations to cease or be curtailed and may include corrective measures requiring capital expenditures. Intense lobbying over environmental concerns by non-governmental organizations has caused some governments to cancel or restrict development of mining projects. Current publicized concern over climate change may lead to carbon taxes, requirements for carbon offset purchases or new regulation. The costs or likelihood of such potential issues to the Company cannot be estimated at this time.

The legal framework governing this area is constantly developing, therefore the Company is unable to fully ascertain any future liability that may arise from the implementation of any new laws or regulations, although such laws and regulations are typically strict and may impose severe penalties (financial or otherwise). The proposed activities of the Company, as with any exploration company, may have an environmental impact which may result in unbudgeted delays, damage, loss and other costs and obligations including, without limitation, rehabilitation and/or compensation. There is also a risk that the Company’s operations and financial position may be adversely affected by the actions of environmental groups or any other group or person opposed in general to the Company’s activities and, in particular, the proposed exploration and mining by the Company within the state of Idaho and the United States.

Environmental hazards unknown to the Company, which have been caused by previous or existing owners or operators of the Mine, may exist on the properties in which the Company holds an interest. Many of the properties in which the Company has ownership rights are located within the Coeur d’Alene Mining District, which is currently the site of a Federal Superfund cleanup project. It is possible that environmental cleanup or other environmental restoration procedures could remain to be completed or mandated by law, causing unpredictable and unexpected liabilities to arise.

| 14 |

Regulations and pending legislation governing issues involving climate change could result in increased operating costs, which could have a material adverse effect on the Company’s business.

A number of governments or governmental bodies have introduced or are contemplating legislative and/or regulatory changes in response to concerns about the potential impact of climate change. Legislation and increased regulation regarding climate change could impose significant costs on the Company, on its future venture partners, if any, and on its suppliers, including costs related to increased energy requirements, capital equipment, environmental monitoring and reporting, and other costs necessary to comply with such regulations. Any adopted future climate change regulations could also negatively impact the Company’s ability to compete with companies situated in areas not subject to such limitations. Given the emotional and political significance and uncertainty surrounding the impact of climate change and how it should be dealt with, the Company cannot predict how legislation and regulation will ultimately affect its financial condition, operating performance, and ability to compete. Furthermore, even without such regulation, increased awareness and any adverse publicity in the global marketplace about potential impacts on climate change by the Company or other companies in its industry could harm the Company’s reputation. The potential physical impacts of climate change on its operations are highly uncertain, could be particular to the geographic circumstances in areas in which the Company operates and may include changes in rainfall and storm patterns and intensities, water shortages, changing sea levels, and changing temperatures. These impacts may adversely impact the cost, production, and financial performance of the Company’s operations.

There are several governmental regulations that materially restrict mineral exploration. The Company will be subject to the federal regulations (environmental) and the laws of the State of Idaho as the Company carries out its exploration program. The Company may be required to obtain additional work permits, post bonds and perform remediation work for any physical disturbance to the land in order to comply with these laws. While the Company’s planned exploration program budgets for regulatory compliance, there is a risk that new regulations could increase its costs of doing business and prevent it from carrying out its exploration program.

Land reclamation requirements for the Company’s properties may be burdensome and expensive.

Although variable depending on location and the governing authority, land reclamation requirements are generally imposed on mineral exploration companies (as well as companies with mining operations) in order to minimize long-term effects of land disturbance.

Reclamation may include requirements to:

| ● | control dispersion of potentially deleterious effluents; | |

| ● | treat ground and surface water to drinking water standards; and | |

| ● | reasonably re-establish pre-disturbance landforms and vegetation. |

To date, the Company has not been subject to reclamation or bonding obligations in connection with its past or potential future development activities. If these obligations were to occur in the future, or if the Company is required to carry out reclamation work, the Company must allocate financial resources that might otherwise be spent on further exploration and development programs.

Social and environmental activism may have an adverse effect on the reputation and financial condition of the Company or its relationship with the communities in which it operates.

There is an increasing level of public concern relating to the effects of mining on the nature landscape, in communities and on the environment. Certain non-governmental organizations, public interest groups and reporting organizations (“NGOs”) who oppose resource development can be vocal critics of the mining industry. In addition, there have been many instances in which local community groups have opposed resource extraction activities, which have resulted in disruption and delays to the relevant operation. While the Company seeks to operate in a socially responsible manner and believes it has good relationships with local communities in the regions in which it operates, NGOs or local community organizations could direct adverse publicity against and/or disrupt the operations of the Company in respect to one or more of its properties, regardless of its successful compliance with social and environmental best practices, due to political factors, activities of unrelated third parties on lands in which the Company has an interest or the Company’s operations specifically. Any such actions and the resulting media coverage could have an adverse effect on the reputation and financial condition of the Company or its relationships with the communities in which it operates, which could have a material adverse effect on the Company’s business, financial condition, results of operations, cash flows or prospects.

| 15 |

The mineral exploration and mining industry is highly competitive.

The mining industry is intensely competitive in all of its phases. As a result of this competition, some of which is with large established mining companies with substantial capabilities and with greater financial and technical resources than the Company’s, the Company may be unable to acquire additional properties, if any, or financing on terms it considers acceptable. The Company also competes with other mining companies in the recruitment and retention of qualified managerial and technical employees. If the Company is unable to successfully compete for qualified employees, its exploration and development programs may be slowed down or suspended. The Company competes with other companies that produce its planned commercial products for capital. If the Company is unable to raise sufficient capital, its exploration and development programs may be jeopardized or it may not be able to acquire, develop, or operate additional mining projects.

The silver industry is highly competitive, and the Company is required to compete with other corporations and business entities, many of which have greater resources than it does. Such corporations and other business entities could outbid the Company for potential projects or produce minerals at lower costs, which would have a negative effect on the Company’s operations.

Metal prices are highly volatile. If a profitable market for its metals does not exist, the Company may have to cease operations.

Mineral prices have been highly volatile and are affected by numerous international economic and political factors over which the Company has no control. The Company’s long-term success is highly dependent upon the price of silver, as the economic feasibility of any ore body discovered on its current property, or on other properties the Company may acquire in the future, would, in large part, be determined by the prevailing market price of the minerals. If a profitable market does not exist, the Company may have to cease operations.

A shortage of equipment and supplies could adversely affect the Company’s ability to operate its business.

The Company is dependent on various supplies and equipment to carry out its mining exploration and, if warranted, development operations. Any shortage of such supplies, equipment, and parts could have a material adverse effect on the Company’s ability to carry out its operations and could therefore limit, or increase the cost of, production.

Joint ventures and other partnerships, including offtake arrangements, may expose the Company to risks.

The Company may enter into joint ventures, partnership arrangements, or offtake agreements, with other parties in relation to the exploration, development, and production of the properties in which the Company has an interest. Any failure of such other companies to meet their obligations to the Company or to third parties, or any disputes with respect to the parties’ respective rights and obligations, could have a material adverse effect on the Company, the development and production at its properties, including the Mine, and on future joint ventures, if any, or their properties, and therefore could have a material adverse effect on its results of operations, financial performance, cash flows and the price of its Common Shares.

The Company may experience difficulty attracting and retaining qualified management to meet the needs of its anticipated growth, and the failure to manage its growth effectively could have a material adverse effect on its business and financial condition.

The success of the Company is currently largely dependent on the performance of its directors and officers. The loss of the services of any of these people could have a materially adverse effect on the Company’s business and prospects. There is no assurance the Company can maintain the services of its directors, officers or other qualified personnel required to operate its business. As the Company’s business activity grows, the Company will require additional key financial, administrative and mining personnel as well as additional operations staff. There can be no assurance that these efforts will be successful in attracting, training and retaining qualified personnel as competition for people with these skill sets increase. If the Company is not successful in attracting, training and retaining qualified personnel, the efficiency of its operations could be impaired, which could have an adverse impact on the Company’s operations and financial condition. In addition, the COVID-19 pandemic may cause the Company to have inadequate access to an available skilled workforce and qualified personnel, which could have an adverse impact on the Company’s financial performance and financial condition.

The Company is dependent on a relatively small number of key employees, including its Chief Executive Officer (the “CEO”) and Chief Financial Officer (the “CFO”). The loss of any officer could have an adverse effect on the Company. The Company has no life insurance on any individual, and the Company may be unable to hire a suitable replacement for them on favorable terms, should that become necessary.

| 16 |

The Company may be subject to potential conflicts of interest with its directors and/or officers.

Certain directors and officers of the Company are or may become associated with other mining and/or mineral exploration and development companies which may give rise to conflicts of interest. Directors who have a material interest in any person who is a party to a material contract or a proposed material contract with the Company are required, subject to certain exceptions, to disclose that interest and generally abstain from voting on any resolution to approve such a contract. In addition, directors and officers are required to act honestly and in good faith with a view to the best interests of the Company. Some of the directors and officers of the Company have either other full-time employment or other business or time restrictions placed on them and accordingly, the Company will not be the only business enterprise of these directors and officers. Further, any failure of the directors or officers of the Company to address these conflicts in an appropriate manner or to allocate opportunities that they become aware of to the Company could have a material adverse effect on the Company’s business, financial condition, results of operations, cash flows or prospects.

The Company’s results of operations could be affected by currency fluctuations.

The Company’s properties are currently all located in the U.S. and while most costs associated with these properties are paid in U.S. dollars, a significant amount of its administrative expenses are payable in Canadian dollars. There can be significant swings in the exchange rate between the U.S. dollar and the Canadian dollar. There are no plans at this time to hedge against any exchange rate fluctuations in currencies.

Title to the Company’s properties may be subject to other claims that could affect its property rights and claims.

There are risks that title to the Company’s properties may be challenged or impugned. The Mine is located in Northern Idaho and may be subject to prior unrecorded agreements or transfers and title may be affected by undetected defects.

The Company may be unable to secure surface access or purchase required surface rights.