UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Form 10-Q

ý QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934.

For the quarterly period ended March 31, 2018

Or

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934.

For the Transition period from to .

Commission File Number 001-34820

KKR & CO. L.P.

(Exact name of Registrant as specified in its charter)

Delaware | 26-0426107 | |

(State or other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification Number) | |

9 West 57th Street, Suite 4200

New York, New York 10019

Telephone: (212) 750-8300

(Address, zip code, and telephone number, including

area code, of registrant’s principal executive office.)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o | Emerging growth company o | ||||

(Do not check if a smaller reporting company) | ||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

As of May 7, 2018, there were 496,891,815 Common Units of the registrant outstanding.

KKR & CO. L.P.

FORM 10-Q

For the Quarter Ended March 31, 2018

INDEX

Page No. | ||

PART I - FINANCIAL INFORMATION | ||

Item 1. | Condensed Consolidated Financial Statements (Unaudited) | |

Item 2. | Management's Discussion and Analysis of Financial Condition and Results of Operations | |

Item 3. | Quantitative and Qualitative Disclosures About Market Risk | |

Item 4. | Controls and Procedures | |

PART II - OTHER INFORMATION | ||

Item 1. | Legal Proceedings | |

Item 1A. | Risk Factors | |

Item 2. | Unregistered Sales of Equity Securities | |

Item 3. | Defaults Upon Senior Securities | |

Item 4. | Mine Safety Disclosures | |

Item 5. | Other Information | |

Item 6. | Exhibits | |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the "Securities Act"), and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), which reflect our current views with respect to, among other things, our operations and financial performance. You can identify these forward-looking statements by the use of words such as "outlook," "believe," "expect," "potential," "continue," "may," "should," "seek," "approximately," "predict," "intend," "will," "plan," "estimate," "anticipate," the negative version of these words, other comparable words or other statements that do not relate strictly to historical or factual matters. Without limiting the foregoing, statements regarding the declaration and payment of distributions on common or preferred units of KKR or, after converting from a limited partnership to a corporation, dividends on common or preferred stock of KKR, the timing, manner and volume of repurchases of common units or common stock pursuant to a repurchase program, and the expected synergies and benefits from acquisitions, reorganizations or strategic partnerships, may constitute forward-looking statements. Forward-looking statements are subject to various risks and uncertainties. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated in these statements or cause the anticipated benefits and synergies from transactions to not be realized. We believe these factors include those described under the section entitled "Risk Factors" in this report and in our Annual Report on Form 10-K for the year ended December 31, 2017. These factors should be read in conjunction with the other cautionary statements that are included in this report and in our other filings with the U.S. Securities and Exchange Commission (the "SEC"). We do not undertake any obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law.

In this report, references to "KKR," "we," "us," "our" and "our partnership" refer to KKR & Co. L.P. and its consolidated subsidiaries, except where the context requires otherwise. Prior to KKR & Co. L.P. becoming listed on the New York Stock Exchange ("NYSE") on July 15, 2010, KKR Group Holdings L.P. ("Group Holdings") consolidated the financial results of KKR Management Holdings L.P. and KKR Fund Holdings L.P. (together, the "KKR Group Partnerships") and their consolidated subsidiaries. On August 5, 2014, KKR International Holdings L.P. became a KKR Group Partnership. Each KKR Group Partnership has an identical number of partner interests and, when held together, one Class A partner interest in each of the KKR Group Partnerships together represents one "KKR Group Partnership Unit." In connection with KKR's issuance of 6.75% Series A Preferred Units ("Series A Preferred Units") and 6.50% Series B Preferred Units ("Series B Preferred Units"), the KKR Group Partnerships issued preferred units with economic terms designed to mirror those of the Series A Preferred Units and Series B Preferred Units, respectively.

References to our "Managing Partner" are to KKR Management LLC, which acts as our general partner and unless otherwise indicated, references to equity interests in KKR's business, or to percentage interests in KKR's business, reflect the aggregate equity interests in the KKR Group Partnerships and are net of amounts that have been allocated to our principals and other employees and non-employee operating consultants in respect of the carried interest from KKR's business as part of our "carry pool" and certain minority interests. References to "principals" are to our senior employees and non-employee operating consultants who hold interests in KKR's business through KKR Holdings L.P. ("KKR Holdings") and references to our "senior principals" are to our senior employees who hold interests in our Managing Partner entitling them to vote for the election of its directors.

References to "non-employee operating consultants" include employees of KKR Capstone, who are not employees of KKR. KKR Capstone refers to a group of entities that are owned and controlled by their senior management. KKR Capstone is not a subsidiary or affiliate of KKR. KKR Capstone operates under several consulting agreements with KKR and uses the "KKR" name under license from KKR.

Prior to October 1, 2009, KKR's business was conducted through multiple entities for which there was no single holding entity, but were under common control of senior KKR principals, and in which senior principals and KKR's other principals and individuals held ownership interests (collectively, the "Predecessor Owners"). On October 1, 2009, we completed the acquisition of all of the assets and liabilities of KKR & Co. (Guernsey) L.P. (f/k/a KKR Private Equity Investors, L.P) ("KPE") and, in connection with such acquisition, completed a series of transactions pursuant to which the business of KKR was reorganized into a holding company structure. The reorganization involved a contribution of certain equity interests in KKR's business that were held by the Predecessor Owners to the KKR Group Partnerships in exchange for equity interests in the KKR Group Partnerships held through KKR Holdings. We refer to the acquisition of the assets and liabilities of KPE and to our subsequent reorganization into a holding company structure as the "KPE Transaction."

3

In this report, the term "GAAP" refers to accounting principles generally accepted in the United States of America.

We disclose certain financial measures in this report that are calculated and presented using methodologies other than in accordance with GAAP. We believe that providing these performance measures on a supplemental basis to our GAAP results is helpful to unitholders in assessing the overall performance of KKR's businesses. These financial measures should not be considered as a substitute for similar financial measures calculated in accordance with GAAP, if available. We caution readers that these non-GAAP financial measures may differ from the calculations of other investment managers, and as a result, may not be comparable to similar measures presented by other investment managers. Reconciliations of these non-GAAP financial measures to the most directly comparable financial measures calculated and presented in accordance with GAAP, where applicable, are included within Note 14 "Segment Reporting" to our condensed consolidated financial statements and under "Management's Discussion and Analysis of Financial Condition and Results of Operations—Segment Operating and Performance Measures" and "—Segment Balance Sheet."

This report uses the terms assets under management ("AUM"), fee paying assets under management ("FPAUM"), economic net income ("ENI"), fee related earnings ("FRE"), distributable earnings, capital invested, syndicated capital and book value. You should note that our calculations of these financial measures and other financial measures may differ from the calculations of other investment managers and, as a result, our financial measures may not be comparable to similar measures presented by other investment managers. These and other financial measures are defined in the section "Management's Discussion and Analysis of Financial Condition and Results of Operations—Segment Operating and Performance Measures" and "—Segment Balance Sheet."

References to our "funds" or our "vehicles" refer to investment funds, vehicles and accounts advised, sponsored or managed by one or more subsidiaries of KKR, including collateralized loan obligations ("CLOs") and commercial real estate mortgage-backed securities ("CMBS") vehicles, unless the context requires otherwise. They do not include investment funds, vehicles or accounts of any hedge fund manager with which we have formed a strategic partnership where we have acquired a non-controlling interest.

Unless otherwise indicated, references in this report to our fully exchanged and diluted common units outstanding, or to our common units outstanding on a fully exchanged and diluted basis, reflect (i) actual common units outstanding, (ii) common units into which KKR Group Partnership Units not held by us are exchangeable pursuant to the terms of the exchange agreement described in this report, (iii) common units issuable in respect of exchangeable equity securities issued in connection with the acquisition of Avoca Capital ("Avoca"), and (iv) common units issuable pursuant to any equity awards actually granted from the KKR & Co. L.P. 2010 Equity Incentive Plan (our "Equity Incentive Plan"). Our fully exchanged and diluted common units outstanding do not include (i) common units available for issuance pursuant to our Equity Incentive Plan for which equity awards have not yet been granted and (ii) common units that we have the option to issue in connection with our acquisition of additional interests in Marshall Wace LLP (together with its affiliates, "Marshall Wace").

4

KKR & CO. L.P.

CONDENSED CONSOLIDATED STATEMENTS OF FINANCIAL CONDITION (UNAUDITED)

(Amounts in Thousands, Except Unit Data)

March 31, 2018 | December 31, 2017 | ||||||

Assets | |||||||

Cash and Cash Equivalents | $ | 1,880,834 | $ | 1,876,687 | |||

Cash and Cash Equivalents Held at Consolidated Entities | 868,114 | 1,802,372 | |||||

Restricted Cash and Cash Equivalents | 59,316 | 56,302 | |||||

Investments | 42,101,905 | 39,013,934 | |||||

Due from Affiliates | 565,681 | 554,349 | |||||

Other Assets | 2,103,303 | 2,531,075 | |||||

Total Assets | $ | 47,579,153 | $ | 45,834,719 | |||

Liabilities and Equity | |||||||

Debt Obligations | $ | 22,041,271 | $ | 21,193,859 | |||

Due to Affiliates | 265,190 | 323,810 | |||||

Accounts Payable, Accrued Expenses and Other Liabilities | 3,503,754 | 3,654,250 | |||||

Total Liabilities | 25,810,215 | 25,171,919 | |||||

Commitments and Contingencies | |||||||

Redeemable Noncontrolling Interests | 690,630 | 610,540 | |||||

Equity | |||||||

Series A Preferred Units (13,800,000 units issued and outstanding as of March 31, 2018 and December 31, 2017) | 332,988 | 332,988 | |||||

Series B Preferred Units (6,200,000 units issued and outstanding as of March 31, 2018 and December 31, 2017) | 149,566 | 149,566 | |||||

KKR & Co. L.P. Capital - Common Unitholders (489,242,042 and 486,174,736 common units issued and outstanding as of March 31, 2018 and December 31, 2017, respectively) | 6,918,185 | 6,703,382 | |||||

Total KKR & Co. L.P. Partners' Capital | 7,400,739 | 7,185,936 | |||||

Noncontrolling Interests | 13,677,569 | 12,866,324 | |||||

Total Equity | 21,078,308 | 20,052,260 | |||||

Total Liabilities and Equity | $ | 47,579,153 | $ | 45,834,719 | |||

See notes to condensed consolidated financial statements.

5

KKR & CO. L.P.

CONDENSED CONSOLIDATED STATEMENTS OF FINANCIAL CONDITION (Continued) (UNAUDITED)

(Amounts in Thousands)

The following presents the portion of the consolidated balances presented in the condensed consolidated statements of financial condition attributable to consolidated variable interest entities ("VIEs") as of March 31, 2018 and December 31, 2017. KKR's consolidated VIEs consist primarily of certain collateralized financing entities ("CFEs") holding collateralized loan obligations ("CLOs") and commercial real estate mortgage-backed securities ("CMBS") and certain investment funds. With respect to consolidated VIEs, the following assets may only be used to settle obligations of these consolidated VIEs and the following liabilities are only the obligations of these consolidated VIEs. The noteholders, limited partners and other creditors of these VIEs have no recourse to KKR's general assets. Additionally, KKR has no right to the benefits from, nor does KKR bear the risks associated with, the assets held by these VIEs beyond KKR's beneficial interest therein and any income generated from the VIEs. There are neither explicit arrangements nor does KKR hold implicit variable interests that would require KKR to provide any material ongoing financial support to the consolidated VIEs, beyond amounts previously committed, if any.

March 31, 2018 | |||||||||||

Consolidated CFEs | Consolidated KKR Funds and Other Entities | Total | |||||||||

Assets | |||||||||||

Cash and Cash Equivalents Held at Consolidated Entities | $ | 594,873 | $ | 250,516 | $ | 845,389 | |||||

Restricted Cash and Cash Equivalents | — | 27,309 | 27,309 | ||||||||

Investments | 16,063,337 | 11,550,688 | 27,614,025 | ||||||||

Due from Affiliates | — | 5,919 | 5,919 | ||||||||

Other Assets | 185,800 | 223,436 | 409,236 | ||||||||

Total Assets | $ | 16,844,010 | $ | 12,057,868 | $ | 28,901,878 | |||||

Liabilities | |||||||||||

Debt Obligations | $ | 15,251,646 | $ | 984,199 | $ | 16,235,845 | |||||

Accounts Payable, Accrued Expenses and Other Liabilities | 875,365 | 388,732 | 1,264,097 | ||||||||

Total Liabilities | $ | 16,127,011 | $ | 1,372,931 | $ | 17,499,942 | |||||

December 31, 2017 | |||||||||||

Consolidated CFEs | Consolidated KKR Funds and Other Entities | Total | |||||||||

Assets | |||||||||||

Cash and Cash Equivalents Held at Consolidated Entities | $ | 1,467,829 | $ | 231,423 | $ | 1,699,252 | |||||

Restricted Cash and Cash Equivalents | — | 21,255 | 21,255 | ||||||||

Investments | 15,573,203 | 9,408,967 | 24,982,170 | ||||||||

Due from Affiliates | — | 23,562 | 23,562 | ||||||||

Other Assets | 176,572 | 168,003 | 344,575 | ||||||||

Total Assets | $ | 17,217,604 | $ | 9,853,210 | $ | 27,070,814 | |||||

Liabilities | |||||||||||

Debt Obligations | $ | 15,586,216 | $ | 770,350 | $ | 16,356,566 | |||||

Accounts Payable, Accrued Expenses and Other Liabilities | 923,494 | 243,660 | 1,167,154 | ||||||||

Total Liabilities | $ | 16,509,710 | $ | 1,014,010 | $ | 17,523,720 | |||||

See notes to condensed consolidated financial statements.

6

KKR & CO. L.P.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

(Amounts in Thousands, Except Unit Data)

Three Months Ended March 31, | |||||||

2018 | 2017 | ||||||

Revenues | |||||||

Fees and Other | $ | 394,394 | $ | 380,179 | |||

Capital Allocation-Based Income | 78,212 | 387,576 | |||||

Total Revenues | 472,606 | 767,755 | |||||

Expenses | |||||||

Compensation and Benefits | 298,136 | 402,963 | |||||

Occupancy and Related Charges | 14,215 | 14,851 | |||||

General, Administrative and Other | 124,250 | 122,200 | |||||

Total Expenses | 436,601 | 540,014 | |||||

Investment Income (Loss) | |||||||

Net Gains (Losses) from Investment Activities | 472,800 | 506,645 | |||||

Dividend Income | 33,064 | 9,924 | |||||

Interest Income | 298,256 | 280,980 | |||||

Interest Expense | (219,590 | ) | (186,854 | ) | |||

Total Investment Income (Loss) | 584,530 | 610,695 | |||||

Income (Loss) Before Taxes | 620,535 | 838,436 | |||||

Income Taxes | 17,641 | 40,542 | |||||

Net Income (Loss) | 602,894 | 797,894 | |||||

Net Income (Loss) Attributable to Redeemable Noncontrolling Interests | 25,674 | 20,933 | |||||

Net Income (Loss) Attributable to Noncontrolling Interests | 398,777 | 509,277 | |||||

Net Income (Loss) Attributable to KKR & Co. L.P. | 178,443 | 267,684 | |||||

Net Income Attributable to Series A Preferred Unitholders | 5,822 | 5,822 | |||||

Net Income Attributable to Series B Preferred Unitholders | 2,519 | 2,519 | |||||

Net Income (Loss) Attributable to KKR & Co. L.P. Common Unitholders | $ | 170,102 | $ | 259,343 | |||

Net Income (Loss) Attributable to KKR & Co. L.P. Per Common Unit | |||||||

Basic | $ | 0.36 | $ | 0.57 | |||

Diluted | $ | 0.32 | $ | 0.52 | |||

Weighted Average Common Units Outstanding | |||||||

Basic | 487,704,838 | 453,695,846 | |||||

Diluted | 535,918,274 | 496,684,340 | |||||

See notes to condensed consolidated financial statements.

7

KKR & CO. L.P.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) (UNAUDITED)

(Amounts in Thousands)

Three Months Ended March 31, | |||||||

2018 | 2017 | ||||||

Net Income (Loss) | $ | 602,894 | $ | 797,894 | |||

Other Comprehensive Income (Loss), Net of Tax: | |||||||

Foreign Currency Translation Adjustments | 3,624 | 16,576 | |||||

Comprehensive Income (Loss) | 606,518 | 814,470 | |||||

Less: Comprehensive Income (Loss) Attributable to Redeemable Noncontrolling Interests | 25,674 | 20,933 | |||||

Less: Comprehensive Income (Loss) Attributable to Noncontrolling Interests | 398,050 | 520,109 | |||||

Comprehensive Income (Loss) Attributable to KKR & Co. L.P. | $ | 182,794 | $ | 273,428 | |||

See notes to condensed consolidated financial statements.

8

KKR & CO. L.P.

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY (UNAUDITED)

(Amounts in Thousands, Except Unit Data)

KKR & Co. L.P. | |||||||||||||||||||||||||||||

Common Units | Capital - Common Unitholders | Accumulated Other Comprehensive Income (Loss) | Total Capital - Common Units | Capital - Series A Preferred Units | Capital - Series B Preferred Units | Noncontrolling Interests | Total Equity | Redeemable Noncontrolling Interests | |||||||||||||||||||||

Balance at January 1, 2017 | 452,380,335 | $ | 5,506,375 | $ | (49,096 | ) | $ | 5,457,279 | $ | 332,988 | $ | 149,566 | $ | 10,545,902 | $ | 16,485,735 | $ | 632,348 | |||||||||||

Net Income (Loss) | 259,343 | 259,343 | 5,822 | 2,519 | 509,277 | 776,961 | 20,933 | ||||||||||||||||||||||

Other Comprehensive Income (Loss)- Foreign Currency Translation (Net of Tax) | 5,744 | 5,744 | 10,832 | 16,576 | |||||||||||||||||||||||||

Changes in Consolidation | — | (71,657 | ) | (71,657 | ) | ||||||||||||||||||||||||

Transfer of interests under common control (See Note 15 "Equity") | 12,269 | (1,988 | ) | 10,281 | (10,281 | ) | — | ||||||||||||||||||||||

Exchange of KKR Holdings L.P. Units and Other Securities to KKR & Co. L.P. Common Units | 3,190,630 | 43,564 | (388 | ) | 43,176 | (43,176 | ) | — | |||||||||||||||||||||

Tax Effects Resulting from Exchange of KKR Holdings L.P. Units | 1,802 | 167 | 1,969 | 1,969 | |||||||||||||||||||||||||

Equity-Based and Other Non-Cash Compensation | 49,943 | 49,943 | 61,093 | 111,036 | |||||||||||||||||||||||||

Capital Contributions | — | 528,833 | 528,833 | 128,499 | |||||||||||||||||||||||||

Capital Distributions | (72,381 | ) | (72,381 | ) | (5,822 | ) | (2,519 | ) | (262,361 | ) | (343,083 | ) | (352 | ) | |||||||||||||||

Balance at March 31, 2017 | 455,570,965 | $ | 5,800,915 | $ | (45,561 | ) | $ | 5,755,354 | $ | 332,988 | $ | 149,566 | $ | 11,268,462 | $ | 17,506,370 | $ | 781,428 | |||||||||||

KKR & Co. L.P. | |||||||||||||||||||||||||||||

Common Units | Capital - Common Unitholders | Accumulated Other Comprehensive Income (Loss) | Total Capital - Common Units | Capital - Series A Preferred Units | Capital - Series B Preferred Units | Noncontrolling Interests | Total Equity | Redeemable Noncontrolling Interests | |||||||||||||||||||||

Balance at January 1, 2018 | 486,174,736 | $ | 6,722,863 | $ | (19,481 | ) | $ | 6,703,382 | $ | 332,988 | $ | 149,566 | $ | 12,866,324 | $ | 20,052,260 | $ | 610,540 | |||||||||||

Net Income (Loss) | 170,102 | 170,102 | 5,822 | 2,519 | 398,777 | 577,220 | 25,674 | ||||||||||||||||||||||

Other Comprehensive Income (Loss)- Foreign Currency Translation (Net of Tax) | 4,351 | 4,351 | (727 | ) | 3,624 | ||||||||||||||||||||||||

Exchange of KKR Holdings L.P. Units and Other Securities to KKR & Co. L.P. Common Units | 3,067,306 | 51,221 | (132 | ) | 51,089 | (51,089 | ) | — | |||||||||||||||||||||

Tax Effects Resulting from Exchange of KKR Holdings L.P. Units and Other | 4,205 | 17 | 4,222 | 4,222 | |||||||||||||||||||||||||

Equity-Based and Other Non-Cash Compensation | 67,796 | 67,796 | 32,695 | 100,491 | |||||||||||||||||||||||||

Capital Contributions | — | 1,270,723 | 1,270,723 | 56,950 | |||||||||||||||||||||||||

Capital Distributions | (82,757 | ) | (82,757 | ) | (5,822 | ) | (2,519 | ) | (839,134 | ) | (930,232 | ) | (2,534 | ) | |||||||||||||||

Balance at March 31, 2018 | 489,242,042 | $ | 6,933,430 | $ | (15,245 | ) | $ | 6,918,185 | $ | 332,988 | $ | 149,566 | $ | 13,677,569 | $ | 21,078,308 | $ | 690,630 | |||||||||||

See notes to condensed consolidated financial statements.

9

KKR & CO. L.P.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

(Amounts in Thousands)

Three Months Ended March 31, | |||||||

2018 | 2017 | ||||||

Operating Activities | |||||||

Net Income (Loss) | $ | 602,894 | $ | 797,894 | |||

Adjustments to Reconcile Net Income (Loss) to Net Cash Provided (Used) by Operating Activities: | |||||||

Equity-Based and Other Non-Cash Compensation | 96,227 | 111,036 | |||||

Net Realized (Gains) Losses on Investments | (30,380 | ) | (146,164 | ) | |||

Change in Unrealized (Gains) Losses on Investments | (442,420 | ) | (360,481 | ) | |||

Capital Allocation-Based Income | (78,212 | ) | (387,576 | ) | |||

Other Non-Cash Amounts | 74,156 | 37,860 | |||||

Cash Flows Due to Changes in Operating Assets and Liabilities: | |||||||

Change in Consolidation and Other | — | (1,254 | ) | ||||

Change in Due from / to Affiliates | (71,686 | ) | (48,964 | ) | |||

Change in Other Assets | 420,004 | 539,623 | |||||

Change in Accounts Payable, Accrued Expenses and Other Liabilities | (41,480 | ) | 310,776 | ||||

Investments Purchased | (9,515,686 | ) | (8,345,252 | ) | |||

Proceeds from Investments | 6,829,083 | 6,341,592 | |||||

Net Cash Provided (Used) by Operating Activities | (2,157,500 | ) | (1,150,910 | ) | |||

Investing Activities | |||||||

Purchase of Fixed Assets | (8,670 | ) | (21,384 | ) | |||

Development of Oil and Natural Gas Properties | — | (177 | ) | ||||

Net Cash Provided (Used) by Investing Activities | (8,670 | ) | (21,561 | ) | |||

Financing Activities | |||||||

Distributions to Partners | (82,757 | ) | (72,381 | ) | |||

Distributions to Redeemable Noncontrolling Interests | (2,534 | ) | (352 | ) | |||

Contributions from Redeemable Noncontrolling Interests | 56,950 | 128,499 | |||||

Distributions to Noncontrolling Interests | (839,134 | ) | (262,361 | ) | |||

Contributions from Noncontrolling Interests | 1,263,774 | 520,269 | |||||

Preferred Unit Distributions | (8,341 | ) | (8,341 | ) | |||

Proceeds from Debt Obligations | 3,588,463 | 2,160,958 | |||||

Repayment of Debt Obligations | (2,750,750 | ) | (1,154,415 | ) | |||

Financing Costs Paid | (7,500 | ) | (5,790 | ) | |||

Net Cash Provided (Used) by Financing Activities | 1,218,171 | 1,306,086 | |||||

Effect of exchange rate changes on cash, cash equivalents and restricted cash | 20,902 | 7,680 | |||||

Net Increase/(Decrease) in Cash, Cash Equivalents and Restricted Cash | (927,097 | ) | 141,295 | ||||

Cash, Cash Equivalents and Restricted Cash, Beginning of Period | 3,735,361 | 4,345,815 | |||||

Cash, Cash Equivalents and Restricted Cash, End of Period | $ | 2,808,264 | $ | 4,487,110 | |||

See notes to condensed consolidated financial statements.

10

KKR & CO. L.P.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED) (Continued)

(Amounts in Thousands)

Three Months Ended March 31, | |||||||

2018 | 2017 | ||||||

Supplemental Disclosures of Cash Flow Information | |||||||

Payments for Interest | $ | 207,703 | $ | 197,242 | |||

Payments for Income Taxes | $ | 19,295 | $ | 9,687 | |||

Supplemental Disclosures of Non-Cash Investing and Financing Activities | |||||||

Equity-Based and Other Non-Cash Contributions | $ | 100,491 | $ | 111,036 | |||

Non-Cash Contributions from Noncontrolling Interests | $ | 6,949 | $ | 8,564 | |||

Debt Obligations - Net Gains (Losses), Translation and Other | $ | (11,724 | ) | $ | (78,860 | ) | |

Tax Effects Resulting from Exchange of KKR Holdings L.P. Units and delivery of KKR & Co. L.P. Common Units | $ | 4,222 | $ | 1,969 | |||

Change in Consolidation and Other | |||||||

Investments | $ | — | $ | (70,403 | ) | ||

Noncontrolling Interests | $ | — | $ | (71,657 | ) | ||

March 31, 2018 | December 31, 2017 | ||||||

Reconciliation to the Condensed Consolidated Statements of Financial Condition | |||||||

Cash and Cash Equivalents | $ | 1,880,834 | $ | 1,876,687 | |||

Cash and Cash Equivalents Held at Consolidated Entities | 868,114 | 1,802,372 | |||||

Restricted Cash and Cash Equivalents | 59,316 | 56,302 | |||||

Cash, Cash Equivalents and Restricted Cash, End of Period | $ | 2,808,264 | $ | 3,735,361 | |||

See notes to condensed consolidated financial statements.

11

KKR & CO. L.P.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

(All Amounts in Thousands, Except Unit, Per Unit Data, and Except Where Noted)

1. ORGANIZATION

KKR & Co. L.P. (NYSE: KKR), together with its consolidated subsidiaries ("KKR"), is a leading global investment firm that manages multiple alternative asset classes including private equity, energy, infrastructure, real estate and credit, with strategic manager partnerships that manage hedge funds. KKR aims to generate attractive investment returns for its fund investors by following a patient and disciplined investment approach, employing world-class people, and driving growth and value creation with KKR's portfolio companies. KKR invests its own capital alongside the capital it manages for fund investors and provides financing solutions and investment opportunities through its capital markets business.

KKR & Co. L.P. was formed as a Delaware limited partnership on June 25, 2007 and its general partner is KKR Management LLC (the "Managing Partner"). KKR & Co. L.P. is the parent company of KKR Group Limited, which is the non-economic general partner of KKR Group Holdings L.P. ("Group Holdings"), and KKR & Co. L.P. is the sole limited partner of Group Holdings. Group Holdings holds a controlling economic interest in each of (i) KKR Management Holdings L.P. ("Management Holdings") through KKR Management Holdings Corp., a Delaware corporation which is a domestic corporation for U.S. federal income tax purposes, (ii) KKR Fund Holdings L.P. ("Fund Holdings") directly and through KKR Fund Holdings GP Limited, a Cayman Island limited company which is a disregarded entity for U.S. federal income tax purposes, and (iii) KKR International Holdings L.P. ("International Holdings", and together with Management Holdings and Fund Holdings, the "KKR Group Partnerships") directly and through KKR Fund Holdings GP Limited. Group Holdings also owns certain economic interests in Management Holdings through a wholly owned Delaware corporate subsidiary of KKR Management Holdings Corp. and certain economic interests in Fund Holdings through a Delaware partnership of which Group Holdings is the general partner with a 99% economic interest and KKR Management Holdings Corp. is a limited partner with a 1% economic interest. KKR & Co. L.P., through its indirect controlling economic interests in the KKR Group Partnerships, is the holding partnership for the KKR business.

KKR & Co. L.P. both indirectly controls the KKR Group Partnerships and indirectly holds Class A partner units in each KKR Group Partnership (collectively, "KKR Group Partnership Units") representing economic interests in KKR's business. The remaining KKR Group Partnership Units are held by KKR Holdings L.P. ("KKR Holdings"), which is not a subsidiary of KKR. As of March 31, 2018, KKR & Co. L.P. held approximately 59.5% of the KKR Group Partnership Units and principals through KKR Holdings held approximately 40.5% of the KKR Group Partnership Units. The percentage ownership in the KKR Group Partnerships will continue to change as KKR Holdings and/or principals exchange units in the KKR Group Partnerships for KKR & Co. L.P. common units or when KKR & Co. L.P. otherwise issues or repurchases KKR & Co. L.P. common units. The KKR Group Partnerships also have outstanding equity interests that provide for the carry pool and preferred units with economic terms that mirror the preferred units issued by KKR & Co. L.P.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The accompanying unaudited condensed consolidated financial statements of KKR & Co. L.P. have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) for interim financial information and the instructions to Form 10-Q. The condensed consolidated financial statements (referred to hereafter as the “financial statements”), including these notes, are unaudited and exclude some of the disclosures required in annual financial statements. Management believes it has made all necessary adjustments (consisting of only normal recurring items) such that the financial statements are presented fairly and that estimates made in preparing the financial statements are reasonable and prudent. The operating results presented for interim periods are not necessarily indicative of the results that may be expected for any other interim period or for the entire year. The December 31, 2017 condensed consolidated balance sheet data was derived from audited consolidated financial statements included in KKR & Co. L.P.’s Annual Report on Form 10-K for the year ended December 31, 2017, which include all disclosures required by GAAP. These financial statements should be read in conjunction with the audited consolidated financial statements included in KKR & Co. L.P.’s Annual Report on Form 10-K for the year ended December 31, 2017 filed with the Securities and Exchange Commission (“SEC”).

KKR & Co. L.P. consolidates the financial results of the KKR Group Partnerships and their consolidated subsidiaries, which include the accounts of KKR's investment management and capital markets companies, the general partners of certain unconsolidated investment funds, general partners of consolidated investment funds and their respective consolidated

12

Notes to Condensed Consolidated Financial Statements (Continued)

investment funds and certain other entities including CFEs. References in the accompanying financial statements to "principals" are to KKR's senior employees and non‑employee operating consultants who hold interests in KKR's business through KKR Holdings.

All intercompany transactions and balances have been eliminated.

Use of Estimates

The preparation of the financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues, expenses and investment income (loss) during the reporting periods. Such estimates include but are not limited to the valuation of investments and financial instruments. Actual results could differ from those estimates, and such differences could be material to the financial statements.

Principles of Consolidation

The types of entities KKR assesses for consolidation include (i) subsidiaries, including management companies, broker-dealers and general partners of investment funds that KKR manages, (ii) entities that have all the attributes of an investment company, like investment funds, (iii) CFEs and (iv) other entities, including entities that employ non-employee operating consultants. Each of these entities is assessed for consolidation on a case by case basis depending on the specific facts and circumstances surrounding that entity.

Pursuant to its consolidation policy, KKR first considers whether an entity is considered a VIE and therefore whether to apply the consolidation guidance under the VIE model. Entities that do not qualify as VIEs are assessed for consolidation as voting interest entities ("VOEs") under the voting interest model.

KKR's funds are, for GAAP purposes, investment companies and therefore are not required to consolidate their investments in portfolio companies even if majority-owned and controlled. Rather, the consolidated funds and vehicles reflect their investments at fair value as described below in "Fair Value Measurements."

An entity in which KKR holds a variable interest is a VIE if any one of the following conditions exist: (a) the total equity investment at risk is not sufficient to permit the legal entity to finance its activities without additional subordinated financial support, (b) the holders of the equity investment at risk (as a group) lack either the direct or indirect ability through voting rights or similar rights to make decisions about a legal entity's activities that have a significant effect on the success of the legal entity or the obligation to absorb the expected losses or right to receive the expected residual returns, or (c) the voting rights of some investors are disproportionate to their obligation to absorb the expected losses of the legal entity, their rights to receive the expected residual returns of the legal entity, or both and substantially all of the legal entity's activities either involve or are conducted on behalf of an investor with disproportionately few voting rights. Limited partnerships and other similar entities where unaffiliated limited partners have not been granted (i) substantive participatory rights or (ii) substantive rights to either dissolve the partnership or remove the general partner ("kick-out rights") are VIEs under condition (b) above. KKR's investment funds that are not CFEs (i) are generally limited partnerships, (ii) generally provide KKR with operational discretion and control, and (iii) generally have fund investors with no substantive rights to impact ongoing governance and operating activities of the fund, including the ability to remove the general partner, and as such the limited partners do not hold kick-out rights. Accordingly, most of KKR's investment funds are categorized as VIEs.

KKR consolidates all VIEs in which it is the primary beneficiary. A reporting entity is determined to be the primary beneficiary if it holds a controlling financial interest in a VIE. A controlling financial interest is defined as (a) the power to direct the activities of a VIE that most significantly impact the VIE's economic performance and (b) the obligation to absorb losses of the VIE that could potentially be significant to the VIE or the right to receive benefits from the VIE that could potentially be significant to the VIE. The consolidation guidance requires an analysis to determine (i) whether an entity in which KKR holds a variable interest is a VIE and (ii) whether KKR's involvement, through holding interests directly or indirectly in the entity or contractually through other variable interests (for example, management and performance related fees), would give it a controlling financial interest. Performance of that analysis requires the exercise of judgment. Fees earned by KKR that are customary and commensurate with the level of effort required to provide those services, and where KKR does not hold other economic interests in the entity that would absorb more than an insignificant amount of the expected losses or returns of the entity, would not be considered variable interests. KKR factors in all economic interests including interests held through related parties, to determine if it holds a variable interest. KKR determines whether it is the primary beneficiary of a VIE at the time it becomes involved with a VIE and reconsiders that conclusion periodically.

13

Notes to Condensed Consolidated Financial Statements (Continued)

For entities that are determined not to be VIEs, these entities are generally considered VOEs and are evaluated under the voting interest model. KKR consolidates VOEs it controls through a majority voting interest or through other means.

The consolidation assessment, including the determination as to whether an entity qualifies as a VIE or VOE depends on the facts and circumstances surrounding each entity and therefore certain of KKR's investment funds may qualify as VIEs whereas others may qualify as VOEs.

With respect to CLOs (which are generally VIEs), in its role as collateral manager, KKR generally has the power to direct the activities of the CLO that most significantly impact the economic performance of the entity. In some, but not all cases, KKR, through its residual interest in the CLO may have variable interests that represent an obligation to absorb losses of, or a right to receive benefits from, the CLO that could potentially be significant to the CLO. In cases where KKR has both the power to direct the activities of the CLO that most significantly impact the CLO's economic performance and the obligation to absorb losses of the CLO or the right to receive benefits from the CLO that could potentially be significant to the CLO, KKR is deemed to be the primary beneficiary and consolidates the CLO.

With respect to CMBS vehicles (which are generally VIEs), KKR holds unrated and non-investment grade rated securities issued by the CMBS, which are the most subordinate tranche of the CMBS vehicle. The economic performance of the CMBS is most significantly impacted by the performance of the underlying assets. Thus, the activities that most significantly impact the CMBS economic performance are the activities that most significantly impact the performance of the underlying assets. The special servicer has the ability to manage the CMBS assets that are delinquent or in default to improve the economic performance of the CMBS. KKR generally has the right to unilaterally appoint and remove the special servicer for the CMBS and as such is considered the controlling class of the CMBS vehicle. These rights give KKR the ability to direct the activities that most significantly impact the economic performance of the CMBS. Additionally, as the holder of the most subordinate tranche, KKR is in a first loss position and has the right to receive benefits, including the actual residual returns of the CMBS, if any. In these cases, KKR is deemed to be the primary beneficiary and consolidates the CMBS vehicle.

Redeemable Noncontrolling Interests

Redeemable Noncontrolling Interests represent noncontrolling interests of certain investment funds and vehicles that are subject to periodic redemption by fund investors following the expiration of a specified period of time (typically one year), or may be withdrawn subject to a redemption fee during the period when capital may not be otherwise withdrawn. Fund investors interests subject to redemption as described above are presented as Redeemable Noncontrolling Interests in the accompanying condensed consolidated statements of financial condition and presented as Net Income (Loss) Attributable to Redeemable Noncontrolling Interests in the accompanying condensed consolidated statements of operations.

When redeemable amounts become legally payable to fund investors, they are classified as a liability and included in Accounts Payable, Accrued Expenses and Other Liabilities in the accompanying condensed consolidated statements of financial condition. For all consolidated investment vehicles and funds in which redemption rights have not been granted, noncontrolling interests are presented within Equity in the accompanying condensed consolidated statements of financial condition as noncontrolling interests.

Noncontrolling Interests

Noncontrolling interests represent (i) noncontrolling interests in consolidated entities and (ii) noncontrolling interests held by KKR Holdings.

Noncontrolling Interests in Consolidated Entities

Noncontrolling interests in consolidated entities represent the non-redeemable ownership interests in KKR that are held primarily by:

(i) | third party fund investors in KKR's funds; |

(ii) | third parties entitled to up to 1% of the carried interest received by certain general partners of KKR's funds that have made investments on or prior to December 31, 2015; |

(iii) | certain former principals and their designees representing a portion of the carried interest received by the general partners of KKR's private equity funds that was allocated to them with respect to private equity investments made during such former principals' tenure with KKR prior to October 1, 2009; |

14

Notes to Condensed Consolidated Financial Statements (Continued)

(iv) | certain principals and former principals representing all of the capital invested by or on behalf of the general partners of KKR's private equity funds prior to October 1, 2009 and any returns thereon; |

(v) | third parties in KKR's capital markets business; and |

(vi) | holders of exchangeable equity securities representing ownership interests in a subsidiary of a KKR Group Partnership issued in connection with the acquisition of Avoca Capital ("Avoca"). |

On January 16, 2018, KKR Financial Holdings LLC ("KFN") completed the redemption of all of its outstanding 7.375% Series A LLC Preferred Shares.

Noncontrolling Interests held by KKR Holdings

Noncontrolling interests held by KKR Holdings include economic interests held by principals in the KKR Group Partnerships. Such principals receive financial benefits from KKR's business in the form of distributions received from KKR Holdings and through their direct and indirect participation in the value of KKR Group Partnership Units held by KKR Holdings. These financial benefits are not paid by KKR & Co. L.P. and are borne by KKR Holdings.

The following table presents the calculation of noncontrolling interests held by KKR Holdings:

Three Months Ended March 31, | |||||||

2018 | 2017 | ||||||

Balance at the beginning of the period | $ | 4,793,475 | $ | 4,293,337 | |||

Net income (loss) attributable to noncontrolling interests held by KKR Holdings (1) | 121,002 | 216,432 | |||||

Other comprehensive income (loss), net of tax (2) | 3,143 | 4,920 | |||||

Impact of the exchange of KKR Holdings units to KKR & Co. L.P. common units (3) | (33,775 | ) | (35,904 | ) | |||

Equity-based and other non-cash compensation | 32,695 | 61,093 | |||||

Capital contributions | 39 | 37 | |||||

Capital distributions | (57,167 | ) | (56,637 | ) | |||

Transfer of interests under common control and Other (See Note 15 "Equity") | — | 7,919 | |||||

Balance at the end of the period | $ | 4,859,412 | $ | 4,491,197 | |||

(1) | Refer to the table below for calculation of net income (loss) attributable to noncontrolling interests held by KKR Holdings. |

(2) | Calculated on a pro rata basis based on the weighted average KKR Group Partnership Units held by KKR Holdings during the reporting period. |

(3) | Calculated based on the proportion of KKR Holdings units exchanged for KKR & Co. L.P. common units pursuant to the exchange agreement during the reporting period. The exchange agreement provides for the exchange of KKR Group Partnership Units held by KKR Holdings for KKR & Co. L.P. common units. |

Net income (loss) attributable to KKR & Co. L.P. Common Unitholders and KKR Holdings, with the exception of certain tax assets and liabilities that are directly allocable to KKR Management Holdings Corp., is attributed based on the percentage of the weighted average KKR Group Partnership Units held by KKR and KKR Holdings, each of which holds equity of the KKR Group Partnerships. However, primarily because of the (i) contribution of certain expenses borne entirely by KKR Holdings, (ii) the periodic exchange of KKR Holdings units for KKR & Co. L.P. common units pursuant to the exchange agreement and (iii) the contribution of certain expenses borne entirely by KKR associated with the KKR & Co. L.P. 2010 Equity Incentive Plan ("Equity Incentive Plan"), equity allocations shown in the condensed consolidated statement of changes in equity differ from their respective pro rata ownership interests in KKR's net assets.

15

Notes to Condensed Consolidated Financial Statements (Continued)

The following table presents net income (loss) attributable to noncontrolling interests held by KKR Holdings:

Three Months Ended March 31, | |||||||

2018 | 2017 | ||||||

Net income (loss) | $ | 602,894 | $ | 797,894 | |||

Less: Net income (loss) attributable to Redeemable Noncontrolling Interests | 25,674 | 20,933 | |||||

Less: Net income (loss) attributable to Noncontrolling Interests in consolidated entities | 277,775 | 292,845 | |||||

Less: Net income (loss) attributable to Series A and Series B Preferred Unitholders | 8,341 | 8,341 | |||||

Plus: Income tax / (benefit) attributable to KKR Management Holdings Corp. | 6,068 | 19,160 | |||||

Net income (loss) attributable to KKR & Co. L.P. Common Unitholders and KKR Holdings | $ | 297,172 | $ | 494,935 | |||

Net income (loss) attributable to Noncontrolling Interests held by KKR Holdings | $ | 121,002 | $ | 216,432 | |||

Investments

Investments consist primarily of private equity, real assets, credit, investments of consolidated CFEs, equity method, carried interest and other investments. Investments denominated in currencies other than the entity's functional currency are valued based on the spot rate of the respective currency at the end of the reporting period with changes related to exchange rate movements reflected as a component of Net Gains (Losses) from Investment Activities in the condensed consolidated statements of operations. Security and loan transactions are recorded on a trade date basis. Further disclosure on investments is presented in Note 4 "Investments."

The following describes the types of securities held within each investment class.

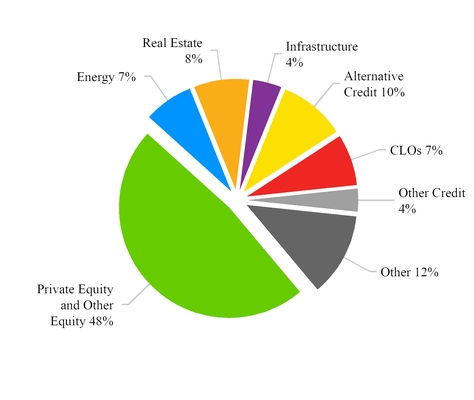

Private Equity - Consists primarily of equity investments in operating businesses, including growth equity investments.

Credit - Consists primarily of investments in below investment grade corporate debt securities (primarily high yield bonds and syndicated bank loans), distressed and opportunistic debt and interests in unconsolidated CLOs.

Investments of Consolidated CFEs - Consists primarily of (i) investments in below investment grade corporate debt securities (primarily high yield bonds and syndicated bank loans) held directly by the consolidated CLOs and (ii) investments in originated, fixed-rate mortgage loans held directly by the consolidated CMBS vehicles.

Real Assets - Consists primarily of investments in (i) energy related assets, principally oil and natural gas producing properties, (ii) infrastructure assets, and (iii) real estate, principally residential and commercial real estate assets and businesses.

Equity Method - Other - Consists primarily of (i) certain direct interests in operating companies in which KKR is deemed to exert significant influence under GAAP and (ii) certain interests in partnerships and joint ventures that hold private equity and real estate investments.

Equity Method - Capital Allocation - Based Income - Consists primarily of (i) the capital interest KKR holds as the general partner in certain investment funds, which are not consolidated and (ii) the carried interest component of the general partner interest, which are accounted for as a single unit of account.

Other - Consists primarily of investments in common stock, preferred stock, warrants and options of companies that are not private equity, real assets, credit or investments of consolidated CFEs.

16

Notes to Condensed Consolidated Financial Statements (Continued)

Investments held by Consolidated Investment Funds

The consolidated investment funds are, for GAAP purposes, investment companies and reflect their investments and other financial instruments, including portfolio companies that are majority-owned and controlled by KKR's investment funds, at fair value. KKR has retained this specialized accounting for the consolidated funds in consolidation. Accordingly, the unrealized gains and losses resulting from changes in fair value of the investments and other financial instruments held by the consolidated investment funds are reflected as a component of Net Gains (Losses) from Investment Activities in the condensed consolidated statements of operations.

Certain energy investments are made through consolidated investment funds, including investments in working and royalty interests in oil and natural gas producing properties as well as investments in operating companies that operate in the energy industry. Since these investments are held through consolidated investment funds, such investments are reflected at fair value as of the end of the reporting period.

Investments in operating companies that are held through KKR's consolidated investment funds are generally classified within private equity investments and investments in working and royalty interests in oil and natural gas producing properties are generally classified as real asset investments.

Energy Investments held directly by KKR

Certain energy investments are made by KKR directly in working and royalty interests in oil and natural gas producing properties and not through investment funds. Oil and natural gas producing activities are accounted for under the successful efforts method of accounting and such working interests are consolidated based on the proportion of the working interests held by KKR. Accordingly, KKR reflects its proportionate share of the underlying statements of financial condition and statements of operations of the consolidated working interests on a gross basis and changes in the value of these working interests are not reflected as unrealized gains and losses in the condensed consolidated statements of operations. Under the successful efforts method, exploration costs, other than the costs of drilling exploratory wells, are charged to expense as incurred. Costs that are associated with the drilling of successful exploration wells are capitalized if proved reserves are found. Lease acquisition costs are capitalized when incurred. Costs associated with the drilling of exploratory wells that do not find proved reserves, geological and geophysical costs and costs of certain nonproducing leasehold costs are charged to expense as incurred.

Expenditures for repairs and maintenance, including workovers, are charged to expense as incurred.

The capitalized costs of producing oil and natural gas properties are depleted on a field-by-field basis using the units-of production method based on the ratio of current production to estimated total net proved oil, natural gas and natural gas liquid reserves. Proved developed reserves are used in computing depletion rates for drilling and development costs and total proved reserves are used for depletion rates of leasehold costs.

Estimated dismantlement and abandonment costs for oil and natural gas properties, net of salvage value, are capitalized at their estimated net present value and amortized on a unit-of-production basis over the remaining life of the related proved developed reserves.

Whenever events or changes in circumstances indicate that the carrying amounts of oil and natural gas properties may not be recoverable, KKR evaluates oil and natural gas properties and related equipment and facilities for impairment on a field-by-field basis. The determination of recoverability is made based upon estimated undiscounted future net cash flows. The amount of impairment loss, if any, is determined by comparing the fair value, as determined by a discounted cash flow analysis, with the carrying value of the related asset. Any impairment in value is recognized when incurred and is recorded in General, Administrative, and Other expense in the condensed consolidated statements of operations.

17

Notes to Condensed Consolidated Financial Statements (Continued)

Fair Value Option

For certain investments and other financial instruments, KKR has elected the fair value option. Such election is irrevocable and is applied on a financial instrument by financial instrument basis at initial recognition. KKR has elected the fair value option for certain private equity, real assets, credit, investments of consolidated CFEs, equity method - other and other financial instruments not held through a consolidated investment fund. Accounting for these investments at fair value is consistent with how KKR accounts for its investments held through consolidated investment funds. Changes in the fair value of such instruments are recognized in Net Gains (Losses) from Investment Activities in the condensed consolidated statements of operations. Interest income on interest bearing credit securities on which the fair value option has been elected is based on stated coupon rates adjusted for the accretion of purchase discounts and the amortization of purchase premiums. This interest income is recorded within Interest Income in the condensed consolidated statements of operations.

Equity Method

For certain investments in entities over which KKR exercises significant influence but which do not meet the requirements for consolidation and for which KKR has not elected the fair value option, KKR uses the equity method of accounting. The carrying value of equity method investments for which KKR has not elected the fair value option, is determined based on the amounts invested by KKR, adjusted for the equity in earnings or losses of the investee allocated based on KKR's respective ownership percentage, less distributions.

For equity method investments for which KKR has not elected the fair value option, KKR records its proportionate share of the investee's earnings or losses based on the most recently available financial information of the investee, which in certain cases may lag the date of KKR's financial statements by no more than three calendar months. As of March 31, 2018, equity method investees for which KKR reports financial results on a lag include Marshall Wace LLP ("Marshall Wace"). KKR evaluates its equity method investments for which KKR has not elected the fair value option for impairment whenever events or changes in circumstances indicate that the carrying amounts of such investments may not be recoverable.

The carrying value of Equity Method - Capital Allocation - Based Income investments approximate fair value, because the underlying investments of the unconsolidated investment funds are reported at fair value.

Financial Instruments held by Consolidated CFEs

KKR measures both the financial assets and financial liabilities of the consolidated CFEs in its financial statements using the more observable of the fair value of the financial assets and the fair value of the financial liabilities which results in KKR's consolidated net income (loss) reflecting KKR's own economic interests in the consolidated CFEs including (i) changes in the fair value of the beneficial interests retained by KKR and (ii) beneficial interests that represent compensation for services rendered.

For the consolidated CLOs, KKR has determined that the fair value of the financial assets of the consolidated CLOs is more observable than the fair value of the financial liabilities of the consolidated CLOs. As a result, the financial assets of the consolidated CLOs are being measured at fair value and the financial liabilities are being measured in consolidation as: (1) the sum of the fair value of the financial assets and the carrying value of any nonfinancial assets that are incidental to the operations of the CLOs less (2) the sum of the fair value of any beneficial interests retained by KKR (other than those that represent compensation for services) and KKR's carrying value of any beneficial interests that represent compensation for services. The resulting amount is allocated to the individual financial liabilities (other than the beneficial interests retained by KKR).

For the consolidated CMBS vehicles, KKR has determined that the fair value of the financial liabilities of the consolidated CMBS vehicles is more observable than the fair value of the financial assets of the consolidated CMBS vehicles. As a result, the financial liabilities of the consolidated CMBS vehicles are being measured at fair value and the financial assets are being measured in consolidation as: (1) the sum of the fair value of the financial liabilities (other than the beneficial interests retained by KKR), the fair value of the beneficial interests retained by KKR and the carrying value of any nonfinancial liabilities that are incidental to the operations of the CMBS vehicles less (2) the carrying value of any nonfinancial assets that are incidental to the operations of the CMBS vehicles. The resulting amount is allocated to the individual financial assets.

18

Notes to Condensed Consolidated Financial Statements (Continued)

Fair Value Measurements

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Except for certain of KKR's equity method investments (see "Equity Method" above in this Note 2 "Summary of Significant Accounting Policies") and debt obligations (as described in Note 10 "Debt Obligations"), KKR's investments and other financial instruments are recorded at fair value or at amounts whose carrying values approximate fair value. Where available, fair value is based on observable market prices or parameters or derived from such prices or parameters. Where observable prices or inputs are not available, valuation techniques are applied. These valuation techniques involve varying levels of management estimation and judgment, the degree of which is dependent on a variety of factors.

GAAP establishes a hierarchical disclosure framework which prioritizes and ranks the level of market price observability used in measuring financial instruments at fair value. Market price observability is affected by a number of factors, including the type of financial instrument, the characteristics specific to the financial instrument and the state of the marketplace, including the existence and transparency of transactions between market participants. Financial instruments with readily available quoted prices in active markets generally will have a higher degree of market price observability and a lesser degree of judgment used in measuring fair value.

Investments and financial instruments measured and reported at fair value are classified and disclosed based on the observability of inputs used in the determination of fair values, as follows:

Level I - Pricing inputs are unadjusted, quoted prices in active markets for identical assets or liabilities as of the measurement date. The types of financial instruments included in this category are publicly-listed equities and securities sold short.

Level II - Pricing inputs are other than quoted prices in active markets, which are either directly or indirectly observable as of the measurement date, and fair value is determined through the use of models or other valuation methodologies. The types of financial instruments included in this category are credit investments, investments and debt obligations of consolidated CLO entities, convertible debt securities indexed to publicly-listed securities, less liquid and restricted equity securities and certain over-the-counter derivatives such as foreign currency option and forward contracts.

Level III - Pricing inputs are unobservable for the financial instruments and include situations where there is little, if any, market activity for the financial instrument. The inputs into the determination of fair value require significant management judgment or estimation. The types of financial instruments generally included in this category are private portfolio companies, real assets investments, credit investments, equity method investments for which the fair value option was elected and investments and debt obligations of consolidated CMBS entities.

In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, the level in the fair value hierarchy within which the fair value measurement in its entirety falls has been determined based on the lowest level input that is significant to the fair value measurement in its entirety. KKR's assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment and consideration of factors specific to the asset.

A significant decrease in the volume and level of activity for the asset or liability is an indication that transactions or quoted prices may not be representative of fair value because in such market conditions there may be increased instances of transactions that are not orderly. In those circumstances, further analysis of transactions or quoted prices is needed, and a significant adjustment to the transactions or quoted prices may be necessary to estimate fair value.

The availability of observable inputs can vary depending on the financial asset or liability and is affected by a wide variety of factors, including, for example, the type of instrument, whether the instrument has recently been issued, whether the instrument is traded on an active exchange or in the secondary market, and current market conditions. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised by KKR in determining fair value is greatest for instruments categorized in Level III. The variability and availability of the observable inputs affected by the factors described above may cause transfers between Levels I, II, and III, which KKR recognizes at the beginning of the reporting period.

Investments and other financial instruments that have readily observable market prices (such as those traded on a securities exchange) are stated at the last quoted sales price as of the reporting date. KKR does not adjust the quoted price for these investments, even in situations where KKR holds a large position and a sale could reasonably affect the quoted price.

19

Notes to Condensed Consolidated Financial Statements (Continued)

Management's determination of fair value is based upon the methodologies and processes described below and may incorporate assumptions that are management's best estimates after consideration of a variety of internal and external factors.

Level II Valuation Methodologies

Credit Investments: These instruments generally have bid and ask prices that can be observed in the marketplace. Bid prices reflect the highest price that KKR and others are willing to pay for an instrument. Ask prices represent the lowest price that KKR and others are willing to accept for an instrument. For financial assets and liabilities whose inputs are based on bid-ask prices obtained from third party pricing services, fair value may not always be a predetermined point in the bid-ask range. KKR's policy is generally to allow for mid-market pricing and adjusting to the point within the bid-ask range that meets KKR's best estimate of fair value.

Investments and Debt Obligations of Consolidated CLO Vehicles: Investments of consolidated CLO vehicles are reported within Investments of Consolidated CFEs and are valued using the same valuation methodology as described above for credit investments. Under ASU 2014-13, KKR measures CLO debt obligations on the basis of the fair value of the financial assets of the CLO.

Securities indexed to publicly-listed securities: The securities are typically valued using standard convertible security pricing models. The key inputs into these models that require some amount of judgment are the credit spreads utilized and the volatility assumed. To the extent the company being valued has other outstanding debt securities that are publicly-traded, the implied credit spread on the company's other outstanding debt securities would be utilized in the valuation. To the extent the company being valued does not have other outstanding debt securities that are publicly-traded, the credit spread will be estimated based on the implied credit spreads observed in comparable publicly-traded debt securities. In certain cases, an additional spread will be added to reflect an illiquidity discount due to the fact that the security being valued is not publicly-traded. The volatility assumption is based upon the historically observed volatility of the underlying equity security into which the convertible debt security is convertible and/or the volatility implied by the prices of options on the underlying equity security.

Restricted Equity Securities: The valuation of certain equity securities is based on an observable price for an identical security adjusted for the effect of a restriction.

Derivatives: The valuation incorporates observable inputs comprising yield curves, foreign currency rates and credit spreads.

Level III Valuation Methodologies

Investments and financial instruments categorized as Level III consist primarily of the following:

Private Equity Investments: KKR generally employs two valuation methodologies when determining the fair value of a private equity investment. The first methodology is typically a market comparables analysis that considers key financial inputs and recent public and private transactions and other available measures. The second methodology utilized is typically a discounted cash flow analysis, which incorporates significant assumptions and judgments. Estimates of key inputs used in this methodology include the weighted average cost of capital for the investment and assumed inputs used to calculate terminal values, such as exit EBITDA multiples. Other inputs are also used in both methodologies. In addition, when a definitive agreement has been executed to sell an investment, KKR generally considers a significant determinant of fair value to be the consideration to be received by KKR pursuant to the executed definitive agreement.

Upon completion of the valuations conducted using these methodologies, a weighting is ascribed to each method, and an illiquidity discount is typically applied where appropriate. The ultimate fair value recorded for a particular investment will generally be within a range suggested by the two methodologies, except that the value may be higher or lower than such range in the case of investments being sold pursuant to an executed definitive agreement.

When determining the weighting ascribed to each valuation methodology, KKR considers, among other factors, the availability of direct market comparables, the applicability of a discounted cash flow analysis, the expected hold period and manner of realization for the investment, and in the case of investments being sold pursuant to an executed definitive agreement, an estimated probability of such sale being completed. These factors can result in different weightings among investments in the portfolio and in certain instances may result in up to a 100% weighting to a single methodology.

20

Notes to Condensed Consolidated Financial Statements (Continued)

When an illiquidity discount is to be applied, KKR seeks to take a uniform approach across its portfolio and generally applies a minimum 5% discount to all private equity investments. KKR then evaluates such private equity investments to determine if factors exist that could make it more challenging to monetize the investment and, therefore, justify applying a higher illiquidity discount. These factors generally include (i) whether KKR is unable to sell the portfolio company or conduct an initial public offering of the portfolio company due to the consent rights of a third party or similar factors, (ii) whether the portfolio company is undergoing significant restructuring activity or similar factors and (iii) characteristics about the portfolio company regarding its size and/or whether the portfolio company is experiencing, or expected to experience, a significant decline in earnings. These factors generally make it less likely that a portfolio company would be sold or publicly offered in the near term at a price indicated by using just a market multiples and/or discounted cash flow analysis, and these factors tend to reduce the number of opportunities to sell an investment and/or increase the time horizon over which an investment may be monetized. Depending on the applicability of these factors, KKR determines the amount of any incremental illiquidity discount to be applied above the 5% minimum, and during the time KKR holds the investment, the illiquidity discount may be increased or decreased, from time to time, based on changes to these factors. The amount of illiquidity discount applied at any time requires considerable judgment about what a market participant would consider and is based on the facts and circumstances of each individual investment. Accordingly, the illiquidity discount ultimately considered by a market participant upon the realization of any investment may be higher or lower than that estimated by KKR in its valuations.

In the case of growth equity investments, enterprise values may be determined using the market comparables analysis and discounted cash flow analysis described above. A scenario analysis may also be conducted to subject the estimated enterprise values to a downside, base and upside case, which involves significant assumptions and judgments. A milestone analysis may also be conducted to assess the current level of progress towards value drivers that we have determined to be important, which involves significant assumptions and judgments. The enterprise value in each case may then be allocated across the investment's capital structure to reflect the terms of the security and subjected to probability weightings. In certain cases, the values of growth equity investments may be based on recent or expected financings.

Real Asset Investments: Real asset investments in infrastructure, energy and real estate are valued using one or more of the discounted cash flow analysis, market comparables analysis and direct income capitalization, which in each case incorporates significant assumptions and judgments. Infrastructure investments are generally valued using the discounted cash flow analysis. Key inputs used in this methodology can include the weighted average cost of capital and assumed inputs used to calculate terminal values, such as exit EBITDA multiples. Energy investments are generally valued using a discounted cash flow analysis. Key inputs used in this methodology that require estimates include the weighted average cost of capital. In addition, the valuations of energy investments generally incorporate both commodity prices as quoted on indices and long-term commodity price forecasts, which may be substantially different from commodity prices on certain indices for equivalent future dates. Certain energy investments do not include an illiquidity discount. Long-term commodity price forecasts are utilized to capture the value of the investments across a range of commodity prices within the energy investment portfolio associated with future development and to reflect a range of price expectations. Real estate investments are generally valued using a combination of direct income capitalization and discounted cash flow analysis. Key inputs used in such methodologies that require estimates include an unlevered discount rate and current capitalization rate. The valuations of real assets investments also use other inputs.

Credit Investments: Credit investments are valued using values obtained from dealers or market makers, and where these values are not available, credit investments are generally valued by KKR based on ranges of valuations determined by an independent valuation firm. Valuation models are based on discounted cash flow analyses, for which the key inputs are determined based on market comparables, which incorporate similar instruments from similar issuers.

Other Investments: With respect to other investments including equity method investments for which the fair value election has been made, KKR generally employs the same valuation methodologies as described above for private equity investments when valuing these other investments.

Investments and Debt Obligations of Consolidated CMBS Vehicles: Under ASU 2014-13, KKR measures CMBS investments, which are reported within Investments of Consolidated CFEs on the basis of the fair value of the financial liabilities of the CMBS. Debt obligations of consolidated CMBS vehicles are valued based on discounted cash flow analyses. The key input is the expected yield of each CMBS security using both observable and unobservable factors, which may include recently offered or completed trades and published yields of similar securities, security-specific characteristics (e.g. securities ratings issued by nationally recognized statistical rating organizations, credit support by other subordinate securities issued by the CMBS and coupon type) and other characteristics.

Key unobservable inputs that have a significant impact on KKR's Level III investment valuations as described above are included in Note 5 "Fair Value Measurements." KKR utilizes several unobservable pricing inputs and assumptions in

21

Notes to Condensed Consolidated Financial Statements (Continued)

determining the fair value of its Level III investments. These unobservable pricing inputs and assumptions may differ by investment and in the application of KKR's valuation methodologies. KKR's reported fair value estimates could vary materially if KKR had chosen to incorporate different unobservable pricing inputs and other assumptions or, for applicable investments, if KKR only used either the discounted cash flow methodology or the market comparables methodology instead of assigning a weighting to both methodologies.

Level III Valuation Process

The valuation process involved for Level III measurements is completed on a quarterly basis and is designed to subject the valuation of Level III investments to an appropriate level of consistency, oversight, and review.