Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(MARK ONE)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2014

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

Commission File Number 001-36680

HubSpot, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 20-2632791 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

25 First Street, 2nd Floor

Cambridge, Massachusetts, 02141

(Address of principal executive offices)

(888) 482-7768

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, par value $0.001 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ¨ NO x

Indicate by check mark whether the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ¨ NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data file required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES x NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ¨ NO x

The aggregate market value of common stock held by non-affiliates of the registrant, based on the closing price of the registrant’s common stock on October 9, 2014, as reported by the New York Stock Exchange on such date was approximately $372,747,534. The registrant has elected to use October 9, 2014, which was the initial trading date on the New York Stock Exchange, as the calculation date because on June 30, 2014 (the last business day of the registrant’s mostly recently completed second fiscal quarter), the registrant was a privately-held company. Shares of the registrant’s common stock held by each executive officer, director and holder of 5% or more of the outstanding common stock have been excluded in that such persons may be deemed to be affiliates. This calculation does not reflect a determination that certain persons are affiliates of the registrant for any other purpose.

On February 27, 2015, the registrant had 31,498,756 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for its 2015 Annual Meeting of Stockholders are incorporated by reference in Part III of this Annual Report on Form 10-K. Such Proxy Statement will be filed with the U.S. Securities and Exchange Commission within 120 days after the end of the fiscal year to which this report relates. Except with respect to information specifically incorporated by reference in this Form 10-K, the Proxy Statement is not deemed to be filed as part of this Form 10-K.

Table of Contents

HUBSPOT, INC.

| Page No. | ||||||

| PART I | ||||||

| ITEM 1. |

3 | |||||

| ITEM 1A. |

19 | |||||

| ITEM 1B. |

42 | |||||

| ITEM 2. |

42 | |||||

| ITEM 3. |

42 | |||||

| ITEM 4. |

42 | |||||

| PART II | ||||||

| ITEM 5. |

43 | |||||

| ITEM 6. |

46 | |||||

| ITEM 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

48 | ||||

| ITEM 7A. |

69 | |||||

| ITEM 8. |

70 | |||||

| ITEM 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosures |

97 | ||||

| ITEM 9A. |

97 | |||||

| ITEM 9B. |

97 | |||||

| PART III | ||||||

| ITEM 10. |

98 | |||||

| ITEM 11. |

105 | |||||

| ITEM 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

112 | ||||

| ITEM 13. |

Certain Relationships and Related Transactions, and Director Independence |

118 | ||||

| ITEM 14. |

120 | |||||

| PART IV | ||||||

| ITEM 15. |

Exhibits, Financial Statement Schedules | 121 | ||||

| 122 | ||||||

i

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the federal securities laws, and these statements involve substantial risks and uncertainties. Forward-looking statements generally relate to future events or our future financial or operating performance. In some cases, you can identify forward-looking statements because they contain words such as “may,” “should,” “expects,” “plans,” “anticipates,” “could,” “intends,” “target,” “projects,” “contemplates,” “believes,” “estimates,” “predicts,” “potential” or “continue” or the negative of these words or other similar terms or expressions that concern our expectations, strategy, plans or intentions. Forward-looking statements contained in this Annual Report on Form 10-K include, but are not limited to, statements about:

| • | our future financial performance, including our expectations regarding our revenue, cost of revenue, gross margin and operating expenses; |

| • | maintaining and expanding our customer base and increasing our average subscription revenue per customer; |

| • | the impact of competition in our industry and innovation by our competitors; |

| • | our anticipated growth and expectations regarding our ability to manage our future growth; |

| • | our predictions about industry and market trends; |

| • | our ability to anticipate and address the evolution of technology and the technological needs of our customers, to roll-out upgrades to our existing software platform and to develop new and enhanced applications to meet the needs of our customers; |

| • | our ability to maintain our brand and inbound marketing thought leadership position; |

| • | the impact of our corporate culture and our ability to attract, hire and retain necessary qualified employees to expand our operations; |

| • | the anticipated effect on our business of litigation to which we are or may become a party; |

| • | our ability to successfully acquire and integrate companies and assets; and |

| • | our ability to stay abreast of new or modified laws and regulations that currently apply or become applicable to our business both in the United States and internationally. |

We caution you that the foregoing list may not contain all of the forward-looking statements made in this Annual Report on Form 10-K.

You should not rely upon forward-looking statements as predictions of future events. We have based the forward-looking statements contained in this Annual Report on Form 10-K primarily on our current expectations and projections about future events and trends that we believe may affect our business, financial condition, results of operations and prospects. The outcome of the events described in these forward-looking statements is subject to risks, uncertainties and other factors described in “Risk Factors” and elsewhere in this Annual Report on Form 10-K. Moreover, we operate in a very competitive and rapidly changing environment. New risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this Annual Report on Form 10-K. The results, events and circumstances reflected in the forward-looking statements may not be achieved or occur, and actual results, events or circumstances could differ materially from those described in the forward-looking statements.

The forward-looking statements made in this Annual Report on Form 10-K relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements made in this Annual Report on Form 10-K to reflect events or circumstances after the date of this Annual Report on Form 10-K or to reflect new information or the occurrence of unanticipated events, except as required by law.

1

Table of Contents

We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward-looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures or investments we may make.

2

Table of Contents

PART 1

Overview

We provide a cloud-based marketing and sales software platform that enables businesses to deliver an inbound experience. An inbound marketing and sales experience attracts, engages and delights customers by being more relevant, more helpful, more personalized and less interruptive than traditional marketing and sales tactics. Our software platform features integrated applications to help businesses attract visitors to their websites, convert visitors into leads, close leads into customers and delight customers so that they become promoters of those businesses. These integrated applications include social media, search engine optimization, blogging, website content management, marketing automation, email, CRM, analytics and reporting.

People have transformed how they consume information, research products and services, make purchasing decisions and share their views and experiences. Today, customers are blocking out the tactics from the traditional marketing and sales playbook, such as cold calls, unsolicited emails and disruptive advertisements. Customers are taking more control of the purchasing process by using technology, including search engines and social media, to research products and services. Despite this transformation, most businesses are using an outdated marketing and sales playbook that is essentially the same today as it was 10 years ago. To compete effectively, we believe businesses need to deliver an inbound experience by adopting new strategies and technologies to attract, engage and delight customers.

We designed our all-in-one platform from the ground up to enable businesses to provide an inbound experience to their prospects and customers. At the core of our platform is a single inbound database for each business that captures its customer activity throughout the customer lifecycle. Our platform uses our centralized inbound database to empower businesses to create more personalized interactions with customers, such as personalized emails, personalized social media alerts, personalized websites and targeted alerts for sales people. We provide a comprehensive set of integrated applications on our platform, which offers businesses ease of use, power and simplicity. We designed and built our platform to serve a large numbers of customers of any size with demanding use cases.

While our platform can scale to the enterprise, we focus on selling to mid-market businesses, which we define as businesses that have between 10 and 2,000 employees, because we believe we have significant competitive advantages attracting and serving them. We efficiently reach these businesses at scale through our proven inbound go-to-market approach and more than 2,200 marketing agency partners worldwide. Our platform is particularly suited to serving the needs of mid-market B2B companies. These mid-market businesses seek an integrated, easy to implement and easy to use solution to reach customers and compete with organizations that have larger marketing and sales budgets. As of December 31, 2014, we had 13,607 customers of varying sizes in more than 90 countries, representing almost every industry.

We have a leading brand in the cloud-based inbound marketing and sales software industry. Our brand recognition comes from our thought leadership, including our blog, which attracts more than 1.5 million visits each month, and our commitment to innovation. Our founders, Brian Halligan and Dharmesh Shah, wrote the best-selling marketing book Inbound Marketing: Get Found Using Google, Social Media and Blogs. We also have one of the largest social media followings in our industry and our INBOUND conference is one of the largest inbound industry events, with over 10,000 registered attendees in 2014.

We sell our platform on a subscription basis. Our total revenue increased from $51.6 million in 2012, to $77.6 million in 2013, and to $115.9 million in 2014, representing year-over-year increases of 50% in 2013 and 49% in 2014. We had net losses of $18.8 million in 2012, $34.3 million in 2013, and $48.2 million in 2014.

3

Table of Contents

Industry Background

People Have Changed How They Interact with Businesses

We believe an effective way to illustrate how people have transformed the way they consume information, research products and services, make purchasing decisions and share their views and experiences is by describing two hypothetical people—Traditional Ted and Modern Meghan.

Traditional Ted is an executive at a 300 person company in 2004. He keeps up to date on his industry by attending trade shows and reading the monthly industry print publication, often scanning the ads to see the vendors’ new products. He gets a fair amount of unsolicited emails from salespeople and marketers and sees an increasing number of ads on websites he visits. He also takes sales calls from vendors to stay current on industry developments. Ted opens his mail daily, and when his phone rings, he answers it because it is a critical communication tool. When Ted is looking for a new vendor, he will try to recall the ads he has seen recently or go through the brochures he has been mailed which he keeps in a file in his desk. If Ted is frustrated with a vendor, he calls the vendor and tells a couple of his colleagues about his bad experience. To relax, Ted watches TV and reads the newspaper, both of which contain advertisements.

Modern Meghan is an executive at a 300 person company in 2014. She keeps up to date on her industry by reading a number of industry blogs, following key companies and influencers on Twitter and LinkedIn and listening to podcasts in her car during her commute. She has an ad blocker running in her web browser and an email filter to block out unwanted messages. She rarely checks her mail because it is mostly “junk.” Meghan does not have a landline phone because “only salespeople call me there,” and she never answers her smartphone unless she recognizes the number. Meghan spends much more time on her phone using apps and the web than she does talking on it. If she is looking for a vendor for something her company needs, she starts by searching on Google and then asking her peers in her LinkedIn network about their experiences with different vendors. She does not even bother to talk to any of the vendor’s salespeople until she has narrowed the list and has already completed most of her decision-making process. When Meghan has trouble with one of her vendors, she contacts the vendor, but if she is not satisfied with the response, she sometimes writes a negative review online and posts a link to it on Twitter. In her free time, Meghan relaxes by watching TV shows she has previously recorded on her DVR so she can fast forward through the commercials.

We believe all of us are becoming more like Modern Meghan and less like Traditional Ted. Yet, most businesses are still doing marketing, sales and service as if everyone is like Ted. To be effective today, businesses need to transform to attract, engage and delight customers like Meghan.

The Traditional Business Playbook is Broken

Traditionally, most businesses have followed the same marketing and sales playbook to generate leads, close sales and provide support to their customers. Today, however, customers are increasingly selecting their own communication channels and expecting personalized experiences. They are blocking out traditional marketing and sales tactics, such as cold calls, unsolicited emails and disruptive advertisements, and instead, they are using search engines and social media to research products and services before they contact a vendor. Customers are increasingly taking more control of the purchasing process and influencing the purchasing behavior of others.

Customers are blocking out traditional marketing and sales tactics. Customers are ignoring traditional marketing and sales tactics, often by using technology to block them out. For example:

| • | There are over 223 million phone numbers that have been placed on the U.S. Do Not Call registry. |

| • | 91% of people have unsubscribed from email marketing lists. |

| • | Email services and spam filters are increasingly enabling customers to filter out and de-prioritize promotional messages. |

4

Table of Contents

| • | 68% of people who record TV content do so to skip advertisements, according to a recent Motorola Mobility study based on data collected in December 2012. |

| • | Online advertising has limited engagement. According to DoubleClick, as of March 26, 2014, overall 3-month average industry click-through rates on display ads is only 0.2%. |

Customers are taking control of the purchasing process. Customers can now get the information they need on their own terms. Using search engines, social media and websites, customers can research vendors and actively seek recommendations from members of their social networks. As a result, customers no longer need to talk to a salesperson until they have completed most of their purchasing decision. This limits the amount of influence businesses can have on purchase decisions when using the traditional business playbook. A 2012 Corporate Executive Board (CEB) study of more than 1,400 business-to-business customers across industries revealed that 57% of a typical purchase decision is already made before a customer even talks to a supplier.

Customers are influencing the purchasing behaviors of others. Customers are relying less on the promotional material from businesses and instead using online reviews and input from other purchasers to make their purchasing decision. Such social behavior is self-reinforcing: social buyers themselves are social sellers who influence others’ purchasing decisions. According to a survey conducted by Dimensional Research in 2013, 88% of respondents said that online reviews influenced their buying decisions. In addition, the Social Media Report published by Nielsen and NM Incite in 2011 revealed that 60% of consumers researching products through multiple online sources learned about a specific brand or retailer through social networking sites.

Businesses Need a New Playbook—The Inbound Experience

Businesses need a more effective way to attract, engage and delight customers who have access to an abundance of information and an ability to block traditional marketing and sales tactics. To do this, businesses need to deliver an inbound experience, which enables them to be more helpful, more relevant and less interruptive to their customers.

To deliver an inbound experience, businesses need to transform how they market, sell and serve customers.

| • | Marketing: Businesses need to attract potential customers by maximizing search engine rankings, having an engaging social media presence, and creating and distributing useful and relevant content. Businesses need to personalize their customer interactions on websites, in social media and in emails to engage customers. |

| • | Sales: Businesses need to build relationships with potential customers and become their trusted advisors. They must learn about and react to the signals being sent by customers through websites, social media and emails, to provide personalized and helpful responses. |

| • | Service: Businesses need to delight their customers and inspire them to become vocal promoters by exceeding their expectations. Every customer has a stronger, more public voice today through blogs and social media, underscoring the importance of positive reviews and referrals in building a quality brand. |

Existing Applications are Not Adequate for an Integrated Inbound Experience

Today, businesses often use a variety of point applications for their marketing and sales efforts, including advertising, marketing automation, content management, blogging, social media management, analytics, sales management and CRM. Most of these point applications were not designed to deliver an inbound experience. Typically, they do not provide a central view of all customer interactions across channels, are difficult and expensive to implement and use together, and make it hard to measure results. We believe that these existing point applications were not designed with the platform, architecture and functionality necessary to deliver a seamless integrated inbound experience.

5

Table of Contents

Not Designed for an Inbound Experience. Traditional marketing applications through rely on advertising and cold calling for lead generation instead of inbound methods. These applications are not designed to personalize and optimize every interaction with customers on websites, in social media and by email across devices, and do not typically allow sales and service teams to see the signals their prospects are sending in real time.

No Centralized Inbound Database of Customer Interactions. Businesses typically need to use one point application for website content management, a different point application for blogging, another point application for social media management, another point application for email and marketing automation, another point application for content personalization, another point application for analytics, another point application for sales management and CRM, and yet another point application to alert salespeople of key customer signals in real time. This disparate collection of point applications makes it difficult to get a 360-degree view of a customer’s interactions and use that data to provide a better customer experience and drive a more effective marketing and sales process. In addition, existing point applications are typically not designed to manage, process and analyze all of the customer data created by these various touchpoints because they use older technologies, not big data technologies such as HBase, Hadoop that are designed for massive scale.

Difficult and Expensive to Implement and Use. Using a collection of disparate point applications means a separate implementation process for each. Often businesses will need to use outside consultants or hire new employees with specific technical expertise to implement and use these different applications, resulting in significant additional costs. This collection of disparate point applications also requires that businesses manage a variety of different log-ins and user interfaces, as well as get support from different vendors, often just to do something the business sees as one process, such as running a marketing campaign. While ease of implementation and use are important for businesses of all sizes, they are critical for mid-market businesses.

Hard to Measure Results. Because all the customer touchpoints through the marketing, sales and service processes are typically stored in different disconnected point applications, it is very difficult to get a 360-degree view of a customer’s interactions and measure the effectiveness of marketing and sales programs. Businesses will often purchase yet another application to try to measure results across their multiple applications, adding even more expense and complexity to an already complex collection of different point applications.

Market Opportunity

We believe there is a large market opportunity created by the fundamental transformation in marketing and sales. Businesses of nearly all sizes and in nearly all industries can benefit from delivering an inbound experience to attract, engage and delight their customers. We focus on selling our platform to mid-market businesses. As of December 31, 2014, we had 13,607 customers, and our average subscription revenue per customer for the year ended December 31, 2014 was $8,926. According to AMI Partners, in 2014, there were 1.6 million of these mid-market businesses with a website presence in the United States and Canada and 1.4 million in Europe. According to a January 2014 study by Mintigo of 186,500 U.S.-based B2B companies of varying sizes, only 3% of those companies had implemented any of the most common marketing automation applications.

We believe our platform addresses several segments of existing marketing, sales and services software and that spending in each of these segments will increasingly shift to platforms that enable an inbound experience. According to a May 2014 report by IDC, worldwide spending on CRM applications, including marketing automation, sales automation, customer service and contact center, was forecast to be $24.4 billion in 2014 and is expected to grow to $31.7 billion in 2018.

Advantages of Our Solution

We provide a cloud-based, all-in-one inbound marketing and sales software platform that helps businesses attract, engage and delight customers throughout the customer lifecycle. Our platform features a central

6

Table of Contents

inbound database of customer interactions and integrated applications to help businesses attract visitors to their websites, convert visitors into leads, close leads into customers and delight customers so they become promoters of those businesses.

Designed for an Inbound Experience. Our platform was architected from the ground up to enable businesses to transform their marketing and sales playbook to meet the demands of today’s customers. Our platform includes integrated applications to help businesses efficiently attract more customers through search engine optimization, social media, blogging and other useful content. In addition, our platform is designed to help businesses personalize and optimize interactions with their customers through websites, landing pages, social media and emails, and across devices.

Ease of Use of All-In-One Platform. We provide a set of integrated applications on a common platform, which offers businesses ease of use and simplicity. Our platform has one login, one user interface, one inbound database and one number to call for support: 888-HUBSPOT. Our platform is designed to be used by people without technical training, does not require an expert or technical system administrator and was built to make it easy to get started. Because of its ease of use and integration, our platform enables businesses to focus on attracting, engaging and delighting customers, instead of spending time and money coordinating their marketing and sales efforts across multiple point applications.

Power of All-In-One Platform. At the core of our platform is a single inbound database for each business that captures its customer activity throughout the customer lifecycle. For example, our platform creates a unified timeline incorporating all the interactions with a particular person. If a business’s customer visits its website, comments on its blog, opens an email it sent, interacts with the business on Twitter, watches one of its videos, fills out a form, or is marked as a sales opportunity by its salesperson, all of that activity is centrally managed and presented on the timeline for that contact and is available for use across our applications. Our platform also makes it easy to use the customer data to empower more personalized interactions with the customer, such as personalized social media alerts, personalized content on a business’s website, personalized emails and targeted alerts to its sales people.

Clear ROI for Customers. Our platform delivers proven and measurable results for our customers. Our customers often experience significant increases in the volume of traffic to their websites, the volume of inbound leads and the rate of converting leads into customers. Based on our analysis of customer use in 2012 and 2013, our customers experienced, on average, a 5.7x increase in the number of leads that they generated after 12 months of active use of our platform.

Scalability. Our platform was designed and built to serve a large number of customers of any size and with demanding use cases. Our platform currently processes billions of data points each week, and we use leading global cloud infrastructure providers and our own automation technology to dynamically allocate capacity to handle processing workloads of all sizes. We have built our platform on modern technologies, including HBase and Hadoop, which we believe are more scalable than traditional database technologies. Our scalability gives us flexibility for future growth and enables us to service a large variety of businesses of different sizes across different industries.

Extendable and Open Architecture. Our platform features a variety of open APIs that allows easy integration of our platform with other applications. We enable our customers to connect our platform to their other applications, including CRM and ecommerce applications. By connecting third-party applications, our customers can leverage our centralized inbound database to perform additional functions and analysis.

Our Competitive Strengths

We believe that our market leadership position is based on the following key strengths:

Leading Platform. We have designed and built a world-class, inbound marketing and sales software platform. We believe our customers choose our platform over others because of its powerful, integrated and

7

Table of Contents

easy to use applications. Independent customer reviews and ratings of our platform compared to other applications show that we have high customer satisfaction. As of December 31, 2014 on G2Crowd (an independent business software and services review website), the features and functions of our platform were ranked #1 in customer satisfaction in the following categories: marketing automation, social media management, email marketing, and search marketing.

Market Leadership and Strong Brand. We are a recognized thought leader in the cloud-based inbound marketing and sales software industry with a leading brand. Our founders, Brian Halligan and Dharmesh Shah, wrote the best-selling marketing book Inbound Marketing: Get Found Using Google, Social Media and Blogs . More than 90,000 copies have been sold and is available in nine languages. There are more than 125 self-organized HubSpot user groups. We also have over 1.2 million followers and fans among Twitter, Facebook and LinkedIn as of December 31, 2014, including approximately 116,000 members of LinkedIn who belong to our inbound marketers group. Our INBOUND conference is one of the largest inbound industry conference events with attendance increasing from 1,100 in 2011 to over 10,000 registered attendees in 2014. We currently hold the world record for the largest online marketing seminar with 10,899 live participants. We believe that it is inherently hard to replicate the number of websites that link to us, the volume of useful content we have published, our large social media following, the breadth of our search engine rankings and our overall brand strength because these assets cannot be easily purchased or built.

Large and Growing Agency Partner Program. More than 2,200 agencies partner with us for the value of our platform to their business including being able to offer new inbound marketing and sales services to their clients which can grow their revenue per customer, attract new customers and increase the portion of their clients on a retainer relationship. We believe that the wide adoption of our platform in the marketing agency industry is evidence that we are becoming an industry standard. Marketing agency partners and customers referred to us by our marketing agency partners represented approximately 44% of our customers as of December 31, 2014 and 34% of our revenue for the year ended December 31, 2014. These marketing agency partners help us to promote the vision of the inbound experience, efficiently reach new mid-market businesses at scale and provide our mutual customers with more diverse and higher-touch services.

Mid-Market Focus. We believe we have significant competitive advantages reaching mid-market businesses and efficiently reach this market at scale as a result of our proven inbound go-to-market approach and our agency partner channel. In 2014, over 82% of the new leads we generated and over 93% of our new customers were from inbound marketing and did not have any advertising costs associated with them. We believe our large inbound marketing footprint and agency partner program provide competitive advantages in reaching mid-market businesses.

Powerful Network Effects. We have built a large and growing ecosystem around our platform and company. We have built what we believe is the largest engaged audience in our industry, which now comprises more than 2 million people between our blog subscribers, Twitter followers, Facebook fans, LinkedIn connections and our opt-in email list. We have attracted more than 2,200 marketing agency partners worldwide who promote our brand and extend our marketing and sales reach. Thousands of our customers integrate third-party applications with our platform using our built-in connectors and third-party developer partners. We have trained and certified more than 10,000 marketers on inbound marketing. Our annual INBOUND conference attracted more than 10,000 registered attendees in 2014. We believe this ecosystem drives more businesses and professionals to embrace the inbound playbook. As our engaged audience grows, more agencies partner with us, more third-party developers integrate their applications with our platform, and more professionals complete our certification programs, all of which drive more businesses to adopt our platform.

Our Growth Strategy

The key elements to our growth strategy are:

Grow Our U.S. Customer Base. The market for our platform is large and underserved. Mid-market businesses are particularly underserved by existing point application vendors and often lack sufficient resources

8

Table of Contents

to implement complex solutions. Our all-in-one platform allows mid-market businesses to efficiently adopt and execute an effective inbound marketing strategy to help them expand and grow. We will continue to leverage our inbound go-to-market approach and our network of marketing agency partners to keep growing our domestic business.

Increase Revenue from Existing Customers. With 13,607 customers in more than 90 countries spanning many industries, we believe we have a significant opportunity to increase revenue from our existing customers. We plan to increase revenue from our existing customers by expanding their use of our platform, selling to other parts of their organizations and upselling additional offerings and features. Our scalable pricing model allows us to capture more spend as our customers grow, increase the number of their customers and prospects managed on our platform, and require additional functionality available from our higher price tiers and add-ons, providing us with a substantial opportunity to increase the lifetime value of our customer relationships.

Keep Expanding Internationally. There is a significant opportunity for our inbound platform outside of the United States. As of December 31, 2014, approximately 22% of our customers were located outside of the United States and these customers generated approximately 21% of our total revenue for the year ended December 31, 2014, but we sell to those foreign customers from our U.S., Ireland, and Australia based operations. We intend to grow our presence in international markets through additional investments in local sales, marketing and professional service capabilities, as well as by leveraging our agency partner network. We opened our first international office focused on the European market in January 2013 and our second international office focused on the Asia Pacific market in Sydney, Australia in August 2014. We already have significant website traffic from regions outside the United States and we believe that markets outside the United States represent a significant growth opportunity.

Continue to Innovate and Expand Our Platform. Mid-market businesses are increasingly realizing the value of having an integrated marketing, sales and service platform. We believe we are well positioned to capitalize on this opportunity by introducing new products and applications to extend the functionality of our platform. For example, in 2013, we launched our Sidekick product designed to empower sales professionals to benefit from real-time interaction data to engage with their most relevant prospects.

Selectively Pursue Acquisitions. We plan to selectively pursue acquisitions of complementary businesses, technologies and teams that would allow us to add new features and functionalities to our platform and accelerate the pace of our innovation.

9

Table of Contents

Our Products

All-in-one Marketing and Sales Platform

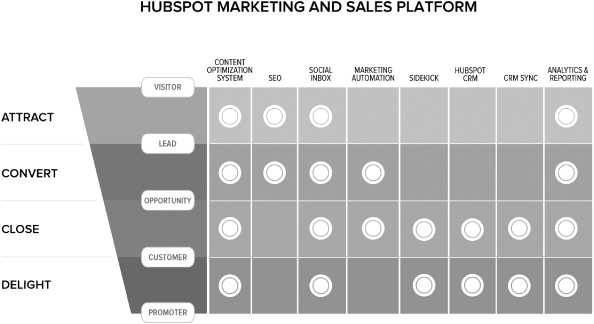

Designed from the ground up to deliver an inbound experience, our software platform enables businesses to attract, engage and delight customers. At the core of our platform is a single inbound database of customer information. This allows a complete view of customer interactions across all of our integrated applications, giving our platform substantial power. This integration makes it possible to personalize web content, social media engagement and email messages across devices, including mobile. The integrated applications on our platform have a common user interface, are accessed through a single login and are based on our inbound database. The following diagram sets forth the principal applications of our platform and how businesses use them in the various parts of the marketing and sales funnel.

Content Optimization System (COS). Our COS applications are part content management system and part personalization engine, enabling businesses to create new and edit existing web content while also personalizing their websites for different visitors and optimizing their websites to convert more visitors into leads and customers. Features include:

| • | Business Blogging —Designed for lead generation, our blog includes “get-as-you-type” SEO tips for how to improve articles, built-in social media integration to automatically post new articles in social media, mobile optimization that automatically optimizes posts for smartphones and tablets, and integrated analytics that allow marketers to see the performance of each post and their blogging overall. |

| • | Website Pages —A flexible system to build modern websites with responsive design, which means websites are dynamically optimized for desktops, laptops, tablets and smartphones without the need for maintaining different website versions for each device type. |

| • | Smart Content —Display customized text, images or other content to customers to provide a personalized experience based on any information stored in the inbound database. |

| • | Landing Pages and Forms —Easily build lead-capture forms and create landing pages with the ability to test and optimize different designs to improve conversion rates. |

| • | Calls-to-Action —Create buttons and callouts that direct visitors to landing pages, with the ability to optimize click-through rates by testing different designs and messages. |

10

Table of Contents

Search Engine Optimization (SEO). Our SEO applications are tightly integrated into all of the content applications on our platform, making it easy to select the right keywords and optimize content to attract more visitors from search engines. Features include:

| • | Keywords —Identify which search terms are used more frequently and are better opportunities, and track results on each keyword. |

| • | Page Performance —Generate automated diagnostic reports about which web pages are not properly optimized, including instructions on what to fix and how to fix it. |

Social Inbox. Our social media applications allow businesses to monitor, publish and track social media across Facebook, LinkedIn, Twitter and Google+, leveraging the personalized information about each contact stored in the inbound database. Features include:

| • | Monitoring —Monitor social media messages not just for keywords, but also using segmented lists created based on criteria in the inbound database such as active sales opportunities or customers who purchased in the last 30 days, and set alerts to be sent when new messages are posted meeting these criteria. |

| • | Publishing —Schedule messages to be posted at any time in multiple Twitter accounts, as well as personal pages, business pages and groups on LinkedIn, Google+ and Facebook. |

| • | Analysis —Measure which posts get the most engagement including the number of website visits, new contacts and new customers generated from each post. |

Marketing Automation and Email. Businesses can execute, manage and analyze sophisticated email marketing campaigns and segment and personalize emails using sophisticated triggers such as viewing a video, completing a form, or interacting via social media. Features include:

| • | Advanced Segmentation —Use all the information in the inbound database to create highly segmented groups for more personalized and engaging email marketing. |

| • | Personalization —Dynamically personalize the content of emails including the sender, images and text based on the information about the recipient in the inbound database. |

| • | Sophisticated Campaign Workflows —Create sophisticated marketing automation workflows that continue to automatically engage leads by using, for example, time delays of various lengths and multiple follow up emails that are customized based on different user actions or behavior. |

| • | Lead Scoring —Create a custom lead score based on the behavior and attributes of a potential customer, such as visiting a specific web page, watching certain videos, opening certain emails, having a certain job title, or other custom data in the inbound database. Define which leads are sent to the CRM system for sales engagement based on these criteria. |

| • | Analysis— Measure email open rates, click-through rates and other email marketing metrics. |

Sidekick. Our Sidekick product enhances the productivity of sales representatives. Businesses can track the signals being sent by potential customers including email engagement and website visits, and easily discover new contacts and connections with other businesses enabling sales representatives to focus on prospects who have demonstrated interest. Features include:

| • | Email Engagement Notifications —Get real-time alerts when email messages are opened or clicked by potential customers to know when they are engaged with messages. |

| • | New Lead and Website Visit Alerts — Receive real time notifications of new leads assigned to a salesperson as well as notifications about when and where an existing lead visits a business’s website to help salespeople more easily engage with potential customers. |

11

Table of Contents

| • | Email Templates and CRM Tracking —Use the email templates stored in salesforce.com directly in Outlook, Gmail or Mac Mail email, removing the need for copying and pasting email addresses and templates from window to window. Track the emails sent from Outlook, Gmail and Mac Mail in most CRM systems. |

| • | Contact Insights —Learn about more contacts at a potential customer when visiting its website or sending an email, identify other connections to a potential customer and add new contacts to a CRM with one click. |

CRM Sync. Businesses can synchronize information from our inbound database with their CRM application, enabling seamless transition from marketing to sales. Our native and third-party CRM integration features include:

| • | Bi-directional Syncing —Changes in HubSpot and the CRM are automatically updated in the other system regardless of where the information originated. |

| • | Inclusion Lists —Define which leads automatically sync to the CRM by setting conditions based on lead score or any other criteria in the inbound database. |

| • | Lead Intelligence —Information from the contact timeline such as recent website visit or social media engagement is displayed in the CRM making it easy for sales to leverage the data in the inbound database. |

| • | Closed Loop Reporting —Track which marketing activity was the original source of a new customer and measure in aggregate which campaigns are driving more or less sales. |

HubSpot CRM. Businesses can track their interactions with contacts and companies, manage their sales activities and report on their pipeline and sales.

| • | Contact Management — Manage contact information for people and companies. Track the history of every interaction with those contacts. |

| • | Salesforce Automation — Track active sales deals, store notes, track calls and meetings, and create tasks and reminders for follow-up with customers. |

| • | Pipeline Reporting — Report on what deals are in what stage of the sales process with visibility for sales representatives and aggregate reporting for sales managers. |

Reporting and Analytics. Businesses can use our reporting and analytics functionality built into our platform to measure which activities are attracting the most new leads and customers, develop a deeper understanding of their customers and measure the effectiveness of campaigns across the customer lifecycle.

| • | Sources —Track website visitors, new leads and new customers according to how they first found a business, helping to measure the effectiveness of different marketing channels. |

| • | Competitors —Track key inbound metrics against competition including the number of inbound links, social media followers and the relative website traffic. |

| • | Campaigns —Create collections of different marketing and sales assets like blog posts, emails, landing pages and keywords and track them all in one place to measure the impact of a specific marketing and sales campaign. |

| • | Attribution —Identify what marketing activity led to a key event in the marketing and sales process, such as conversion into a lead or a purchase, using various analytical models. |

| • | Events —Track and analyze a variety of custom events such as video views or custom webpage interactions to understand the effect those actions have on lead generation and sales. |

| • | Revenue —Report on the revenue generated by marketing and sales activity, including segmentation by deal stage, amount and close date. |

12

Table of Contents

Product Packaging

In 2012, we began pricing and packaging our products based on product plans, number of contacts and add-ons. We sell three product plans, each of which includes key functionality of our core platform but also includes different applications to meet the needs of the various businesses we serve.

HubSpot Basic is our entry level plan starting at $2,400 per year. This plan includes our platform with applications such as blogging, landing pages, Social Inbox, email marketing, and analytics and reporting.

HubSpot Pro is our plan for professional marketers starting at $9,600 per year. This plan includes the platform with all the applications included in HubSpot Basic plus more advanced applications such as CRM integration, marketing automation and smart content.

HubSpot Enterprise is an advanced plan for marketing teams starting at $28,800 per year. This plan includes our platform with all the applications included in HubSpot Pro, plus more sophisticated applications such as A/B testing and optimization, tracking custom events and advanced reporting capabilities.

Pricing for all plans is on a subscription basis and customers pay additional fees above the starting prices based on how many contacts will be stored and tracked in the inbound database. We generate additional revenue based on the purchase of additional subscriptions and applications and the number of account users, subdomains and website visits.

Add Ons. We also sell applications that are not included in any of our three plans on an add-on basis.

| • | CMS allows a business to build, edit and manage an entire website on our platform. CMS has a per-month fee in addition to the fee paid for our inbound platform, which is required to use CMS. |

| • | Sidekick notifies salespeople of the activity of their most highly engaged potential customers. The Starter version is free and includes a limited number of notifications and features, while the Power User version has a per-user fee and includes unlimited notifications and all available features. We had more than 300,000 monthly active users with a free or paid Sidekick account for our Sidekick product during December 31, 2014. |

Our Services

We complement our product offerings with professional services and support. The majority of our services and support is offered over the phone and via web meeting technology rather than in-person, which is a more efficient business model for us and more cost-effective for our customers.

Professional Services. We offer professional services to educate and train customers on how to leverage our software platform and inbound marketing methodology to transform how their business attracts, engages and delights customers. Depending on which product plan and professional services a customer buys, it either receives group training and education in online or in-person classes or one-on-one training and advice from one of our implementation specialists by phone and web meeting. Our professional services are also available to customers who need additional assistance on a one-time or ongoing basis for an additional fee.

Support. In addition to assistance provided by our online articles and customer discussion forums, we offer phone and email-based support staffed in the United States and Ireland, which is included in the cost of a subscription. We strive to maintain an exceptional quality of customer service. We continuously monitor key customer service metrics such as phone hold time, ticket response time and ticket resolution rates, and we monitor the customer satisfaction of our customer support interactions. We believe our customer support is an important reason why businesses choose our platform and recommend it to their colleagues.

13

Table of Contents

Our Customers

We have 13,607 customers in more than 90 countries, representing many industries. No single customer represented more than 1% of our revenue in 2012, 2013 or 2014. The following sets forth a list of representative customers:

By using our platform to deliver an inbound experience, many customers benefit from substantial increases in web traffic, leads and new customers, leading to a significant return on investment. The case studies below illustrate the results our customers have achieved by using our platform.

ShoreTel

Situation: ShoreTel is a leading provider of IP phone systems and unified communications solutions. ShoreTel was frustrated that “last generation” marketing tools impeded its ability to execute its marketing strategies. The main application ShoreTel used was an enterprise marketing automation application from one of the leading traditional vendors, which it found to be inflexible, slow and not user-friendly.

14

Table of Contents

Solution: The ShoreTel team evaluated a variety of leading marketing application vendors with a goal of finding a platform that was both easy to use and designed to help them offer an inbound experience. ShoreTel chose our platform over competitive marketing applications, because it found our platform to be the most comprehensive and complete, the easiest to use and the only platform designed to embrace an inbound experience.

Results: ShoreTel quickly saw the value of using our platform. Within the first two months, it was able to iterate and test new marketing automation workflows that led to a 100% increase in email nurturing response rates. After one year of using our platform, ShoreTel reported the following gains (year-over-year): 60% increase in traffic, 36% increase in leads and 110% increase in qualified leads.

AmeriFirst Home Mortgage

Situation: AmeriFirst Home Mortgage is a community mortgage banker specializing in lending to first-time home buyers. In business more than 25 years, AmeriFirst’s main challenge was taking the person to person business tactics it had always done and adapting them for the Internet era. AmeriFirst’s website served as an “online brochure” for more than a decade, but was not an effective channel to drive more business, and AmeriFirst struggled with using multiple point applications for its marketing and sales. AmeriFirst wanted to transform its web presence into a more efficient channel for growing its business and drive better ROI.

Solution: AmeriFirst moved from a variety of point applications to our platform and implemented an inbound experience throughout its marketing and sales functions. AmeriFirst uses our platform for blogging, SEO, social media, marketing automation and personalized content to attract more web visitors, engage its leads and provide more qualified sales opportunities to its sales team. AmeriFirst cut spending on traditional tactics like direct mail and phonebook advertising, and instead used our platform to focus on inbound marketing and sales that led to a better experience for AmeriFirst’s customers and better ROI for its business.

Results: After six months of using our platform, AmeriFirst reported that its monthly website traffic increased by 120% and monthly leads coming from its website grew more than 20-fold. After one year using our platform, AmeriFirst reported that its monthly web traffic grew 380% and leads grew by a factor of more than 51. After two years using our platform, AmeriFirst reported more than a 16-fold increase in monthly website traffic rates and 90 times as many leads coming from its website as compared to before. AmeriFirst attributed 147 new customers in the first year and 266 customers in the second year to its inbound marketing activities powered by our platform.

New Breed Marketing

Situation: New Breed Marketing was a traditional marketing agency specializing in branding and website design, though it would take on most marketing projects that came its way. New Breed lacked clear specialization, and the difficulty in proving long-term ROI to its clients left New Breed juggling numerous short-term projects rather than getting the long-term, retainer-based clients it desired. New Breed needed to transform its model to focus on longer-term client relationships. New Breed wanted a platform that would manage its own marketing as well as the marketing it did for clients all in one place, and a way to offer inbound marketing and sales services on a retainer basis to its clients.

Solution: New Breed used our platform to manage a client’s entire marketing strategy with all of the applications and reporting available in one place. By embracing an inbound experience and offering a new set of inbound marketing and sales services, New Breed was better positioned to be a long-term, strategic partner for its clients, increasing the amount of retainer business and attracting new clients as well, both of which improved cash flow and profitability. With our platform, New Breed could better prove the ROI of a client’s investment in its agency, shifting New Breed’s status from tactical vendor to strategic partner.

Results: Beyond having the tools to prove ROI and technology that enhances its value proposition, New Breed Marketing has seen its own gains with re-launching on the COS. Within four months of launching its new website built on our content management application and implementing the rest of our platform, New Breed reported a 99% increase in monthly traffic, 61% increase in visitor to lead conversion and 100% increase in lead to customer conversion.

15

Table of Contents

The data in the case studies set forth above as to increased visits, leads, qualified leads and conversions following implementation of our platform does not necessarily mean that our platform was the only factor causing such increases.

Our Technology

13,607 customers have chosen us as their marketing and sales platform, which we architected and built to be secure, highly distributed and highly scalable. Since our founding, we have embraced rapid, iterative product development lifecycles, cloud automation and open-source technologies, including big data platforms, to power marketing and sales programs and provide insights not previously possible or available.

Our platform is a multi-tenant, single code-based, globally available software-as-a-service delivered through web browsers or mobile applications. Our commitment to a highly available, reliable and scalable platform for businesses of all sizes is accomplished through the use of these technologies.

Modern Database Architecture. We process billions of data points weekly across various channels, including social media, email, SEO and website visits, and continue to drive nearly real-time analytics across these channels. This is possible because we built our database from the ground up using distributed big data technologies such as HBase and Hadoop to both process and analyze the large amounts of data we collect in our inbound database. Using modern database technologies, we can provide actionable insights across disparate data-sets in a manner not easily achievable or cost effectively, at scale or efficiently, with traditional databases or platform architectures.

Agility. Our infrastructure and development and software release processes allow us to update our platform for specific groups of customers or our entire customer base at any time. This means we can rapidly innovate and deliver new functionality frequently, without waiting for quarterly or annual release cycles. We typically deploy updates to our software platform hundreds of times a week, enabling us to gather immediate customer feedback and improve our product quickly and continuously.

Cost leverage. Because our platform was built on an almost exclusive footprint of open-source software and designed to operate in cloud-based data-centers, we have benefited from large-scale price reductions by these cloud computing service providers as they continue to innovate and compete for market share. As our processing volume continues to grow, we continue to receive larger volume discounts on a per-unit basis such as cost for storage, bandwidth and computing capacity. We also believe that our extensive use, and contribution to, open-source software will provide additional leverage as we scale our platform and infrastructure.

Scalability. By leveraging leading cloud infrastructure providers along with our automated technology stack, we are able to scale workloads of varying sizes at any time. This allows us to handle customers of all sizes and demands without traditional operational limitations such as network bandwidth, computing cycles, or storage capacity as we can scale our platform on-demand.

Reliability. Our platform’s uptime during 2014 exceeded 99.9% while we delivered hundreds of product improvements through thousands of software releases in a continuous software delivery cycle. Customer data is distributed and processed across multiple data centers within a region to provide redundancy. We built our platform on a distributed computing architecture with no single points of failure and we operate across data-center boundaries daily. In addition to data-center level redundancy, this architecture supports multiple live copies of each data set along with snapshot capabilities for faster, point-in-time data recovery instead of traditional backup and restore methodologies.

Security. We leverage industry standard network and perimeter defense technologies, DDoS protection systems (including web application firewalls) and enterprise grade DNS services across multiple vendors. Our data-center providers operate and certify to high industry compliance levels. Due to the broad footprint of our customer base, we regularly test and evaluate our platform with trusted third-party vendors to ensure the security and integrity of our services.

16

Table of Contents

As of December 31, 2014 we had 132 employees in our research and development organization. Our research and development expenses were $25.6 million in 2014, $15.0 million in 2013 and $10.6 million in 2012.

Marketing and Sales

We believe we are a global leader in implementing an inbound experience in marketing and sales. We believe that our marketing and sales model provides us with a competitive advantage, especially when targeting mid-market businesses, because we can attract and engage these businesses efficiently and at scale.

Inbound Marketing. Our marketing team focuses on inbound marketing and attracts over 40,000 new leads per month through our industry-leading blog and other content, free tools, large social media following, high search engine rankings and personalized website and email content. Inbound sources generated over 93% of our new customers and over 82% of new leads during 2014. We believe most companies of our size and scale typically have a far lower volume of lead generation with a much larger share of it coming from traditional advertising methods.

Inbound Direct Sales. Our sales representatives are based in our offices in Cambridge, Massachusetts and Dublin, Ireland and use phone, email and web meetings to interact with prospects and customers. The vast majority of revenue generated by our sales representatives originates with inbound leads produced by our marketing efforts.

Inbound Channel Sales. In addition to our direct sales team, we have sales representatives that manage relationships with our worldwide network of marketing agency partners who both use our platform for their own businesses and also, on a commissioned basis, refer customers to us. These marketing agencies partner with us not only to leverage our software platform and educational resources, but also to build their own business by offering new services and shifting their revenue mix to include more retainer-based business with a recurring revenue stream.

Employees and Culture

Transforming the business world to embrace the inbound experience requires a truly remarkable team. From the very beginning, our company was founded on a fundamental belief in radical transparency, individual autonomy and enlightened empathy.

To that end, we published our “Culture Code,” a document codifying how we went about building a business that employees, customers and partners alike truly love. Our Culture Code slide deck has been viewed more than 1.5 million times on LinkedIn’s SlideShare and become an important element of our recruiting efforts. The seven core principles of our Culture Code are:

| • | We are maniacal about our mission and our metrics. Our mission is to make the world inbound and transform how organizations attract, engage and delight their customers. |

| • | We empower every employee, at every level, to “Solve for the Customer”. We solve for the customer, company, team and self, in that order. |

| • | We are radically transparent. We believe that power is gained by sharing knowledge, not hoarding it and we share nearly all business information with all of our employees no matter their title or position. |

| • | We give ourselves the autonomy to be awesome. We trust and empower each employee to use good judgment, and believe that results should matter more than when or where they are produced and that influence should be independent of hierarchy. |

| • | We are unreasonably picky about our peers. We value people who are humble, effective and predisposed to action, adaptable to charge, remarkable standouts and transparent with others and with themselves. |

17

Table of Contents

| • | We invest in individual mastery and market value. We want to be as proud of the people we build as we are of the company we build. We believe in investing in our people with ongoing learning, broad exposure and big challenges. |

| • | We constantly question the status quo. We believe that remarkable outcomes rarely result from modest risk and we’d rather be failing frequently than never trying new things. |

We take great pride in recruiting and retaining people with HEART: Humble, Effective, Adaptable, Remarkable and Transparent employees at every level of our company who want to transform the business world with inbound. We’ve been recognized as one of Boston’s Best Places to Work, a Best Place to Work for Recent Grads and one of Glassdoor’s Most Difficult Companies to Interview, and our policies on employee autonomy and transparency have been widely profiled in the media. At the end of the day, however, we do not just talk about culture, we measure it, just as we do the rest of our business. Our founders review our quarterly employee feedback metrics and surveys, respond to them and use them in executive team evaluations.

As of December 31, 2014 we had 785 full-time employees. Of these employees, 680 are based in the United States, 97 are located in Ireland, and 8 are located in Australia.

Competition

Our market is evolving, highly competitive and fragmented, and we expect competition to increase in the future. We believe the principal competitive factors in our market are:

| • | vision for the market and product strategy and pace of innovation; |

| • | inbound marketing focus and domain expertise; |

| • | integrated all-in-one platform; |

| • | breadth and depth of product functionality; |

| • | ease of use; |

| • | scalable, open architecture; |

| • | time to value and total cost of ownership; |

| • | integration with third-party applications and data sources; and |

| • | name recognition and brand reputation. |

We believe we complete favorably with respect to all of these factors.

We face intense competition from other software companies that develop marketing software and from marketing services companies that provide interactive marketing services. Our competitors offer various point applications that provide certain functions and features that we provide, including:

| • | cloud-based marketing automation providers; |

| • | email marketing software vendors; |

| • | sales force automation and CRM software vendors; and |

| • | large-scale enterprise suites. |

In addition, instead of using our platform, some prospective customers may elect to combine disparate point applications, such as content management, marketing automation, analytics and social media management. We expect that new competitors, such as enterprise software vendors that have traditionally focused on enterprise resource planning or other applications supporting back office functions, will develop and introduce, or acquire, applications serving customer-facing and other front office functions.

18

Table of Contents

Intellectual Property

Our ability to protect our intellectual property, including our technology, will be an important factor in the success and continued growth of our business. We protect our intellectual property through trade secrets law, copyrights, trademarks and contracts. Some of our technology relies upon third-party licensed intellectual property.

In addition to the foregoing, we have established business procedures designed to maintain the confidentiality of our proprietary information, including the use of confidentiality agreements and assignment of inventions agreements with employees, independent contractors, consultants and companies with which we conduct business.

Financial Information About Segments

The Company operates as one operating segment. Operating segments are defined as components of an enterprise for which separate financial information is regularly evaluated by the chief operating decision makers (“CODMs”), which are the Company’s chief executive officer and chief operating officer, in deciding how to allocate resources and assess performance. The Company’s CODMs evaluate the Company’s financial information and resources and assess the performance of these resources on a consolidated basis. Since the Company operates in one operating segment, all required financial segment information can be found in the consolidated financial statements. See Footnote 7 within the consolidated financial statements for information by geographic area.

Available Information

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to reports filed pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended, are made available free of charge on or through our website at www.hubspot.com as soon as reasonably practicable after such reports are filed with, or furnished to, the SEC. The SEC also maintains a website, www.sec.gov, that contains reports and other information regarding issuers that file electronically with the SEC. The public may read and copy any files with the SEC Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling 1-800-SEC-0330. We are not, however, including the information contained on our website, or information that may be accessed through links on our website, as part of, or incorporating such information by reference into, this Annual Report on Form 10-K.

| ITEM 1A. | RISK FACTORS |

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below and the other information in this Annual Report on Form 10-K and in our other public filings before making an investment decision. Our business, prospects, financial condition, or operating results could be harmed by any of these risks, as well as other risks not currently known to us or that we currently consider immaterial. If any of such risks and uncertainties actually occurs, our business, financial condition or operating results could differ materially from the plans, projections and other forward-looking statements included in the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in this report and in our other public filings. The trading price of our common stock could decline due to any of these risks, and, as a result, you may lose all or part of your investment.

Risks Related to Our Business and Strategy

We have a history of losses and may not achieve profitability in the future.

We generated net losses of $48.2 million in 2014, of $34.3 million in 2013, and of $18.8 million in 2012. As of December 31, 2014, we had an accumulated deficit of $154.3 million. We will need to generate and sustain increased revenue levels in future periods to become profitable, and, even if we do, we may not be able to maintain or increase our level of profitability. We intend to continue to expend significant funds to grow our

19

Table of Contents

marketing and sales operations, develop and enhance our inbound platform, scale our data center infrastructure and services capabilities and expand into new markets. Our efforts to grow our business may be more costly than we expect, and we may not be able to increase our revenue enough to offset our higher operating expenses. We may incur significant losses in the future for a number of reasons, including the other risks described in this Annual Report on Form 10-K, and unforeseen expenses, difficulties, complications and delays and other unknown events. If we are unable to achieve and sustain profitability, the market price of our common stock may significantly decrease.

We are dependent upon customer renewals, the addition of new customers and the continued growth of the market for an inbound platform.

We derive, and expect to continue to derive, a substantial portion of our revenue from the sale of subscriptions to our inbound marketing platform. The market for inbound marketing and sales products is still evolving, and competitive dynamics may cause pricing levels to change as the market matures and as existing and new market participants introduce new types of point applications and different approaches to enable businesses to address their respective needs. As a result, we may be forced to reduce the prices we charge for our platform and may be unable to renew existing customer agreements or enter into new customer agreements at the same prices and upon the same terms that we have historically.

Our subscription renewal rates may decrease, and any decrease could harm our future revenue and operating results.

Our customers have no obligation to renew their subscriptions for our platform after the expiration of their subscription periods, substantially all of which are one year or less. In addition, our customers may seek to renew for lower subscription amounts or for shorter contract lengths. Also, customers may choose not to renew their subscriptions for a variety of reasons, including an inability or failure on the part of a customer to create blogging, social media and other content necessary to realize the benefits of our platform. Our renewal rates may decline or fluctuate as a result of a number of factors, including limited customer resources, pricing changes, adoption and utilization of our platform and add-on applications by our customers, adoption of our new products (such as our CRM and Sidekick products launched in September 2014), customer satisfaction with our platform, the acquisition of our customers by other companies and deteriorating general economic conditions. If our customers do not renew their subscriptions for our platform or decrease the amount they spend with us, our revenue will decline and our business will suffer.

We face significant competition from both established and new companies offering marketing and sales software and other related applications, as well as internally developed software, which may harm our ability to add new customers, retain existing customers and grow our business.

The marketing and sales software market is evolving, highly competitive and significantly fragmented. With the introduction of new technologies and the potential entry of new competitors into the market, we expect competition to persist and intensify in the future, which could harm our ability to increase sales, maintain or increase renewals and maintain our prices.

We face intense competition from other software companies that develop marketing and sales software and from marketing services companies that provide interactive marketing services. Competition could significantly impede our ability to sell subscriptions to our inbound marketing and sales platform on terms favorable to us. Our current and potential competitors may develop and market new technologies that render our existing or future products less competitive, or obsolete. In addition, if these competitors develop products with similar or superior functionality to our platform, we may need to decrease the prices or accept less favorable terms for our platform subscriptions in order to remain competitive. If we are unable to maintain our pricing due to competitive pressures, our margins will be reduced and our operating results will be negatively affected.

Our competitors include:

| • | cloud-based marketing automation providers; |

20

Table of Contents

| • | email marketing software vendors; |

| • | sales force automation and CRM software vendors; and |

| • | large-scale enterprise suites. |