UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________________

FORM

(Mark one)

For the quarterly period ended

or

For the transition period from ________________ to __________________

Commission File Number:

____________________

(Exact name of registrant as specified in its charter)

|

(State or other jurisdiction of incorporation or organization) |

Not Applicable (I.R.S. Employer Identification No.) |

|

(Address of principal executive offices) (Zip Code) |

|

(

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Trading Symbol |

Name of each exchange on which registered |

|

|

|

The |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐ |

Accelerated filer ☐ |

|

|

Smaller reporting company Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES

As of November 6, 2023, there were

DiaMedica Therapeutics Inc.

FORM 10-Q

September 30, 2023

TABLE OF CONTENTS

|

Description |

Page |

|

|

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS |

1 | |

|

PART I. |

FINANCIAL INFORMATION |

|

|

Item 1. |

Financial Statements |

2 |

|

Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

14 |

|

Item 3. |

Quantitative and Qualitative Disclosures about Market Risk |

20 |

|

Item 4. |

Controls and Procedures |

20 |

|

PART II. |

OTHER INFORMATION |

|

|

Item 1. |

Legal Proceedings |

21 |

|

Item 1A. |

Risk Factors |

21 |

|

Item 2. |

Unregistered Sales of Equity Securities and Use of Proceeds |

22 |

|

Item 3. |

Defaults Upon Senior Securities |

22 |

|

Item 4. |

Mine Safety Disclosures |

22 |

|

Item 5. |

Other Information |

22 |

|

Item 6. |

Exhibits |

22 |

|

SIGNATURE PAGE |

24 |

|

_________________

This quarterly report on Form 10-Q contains certain forward-looking statements within the meaning of Section 27A of the United States Securities Act of 1933, as amended, and Section 21E of the United States Securities Exchange Act of 1934, as amended, that are subject to the safe harbor created by those sections. For more information, see “Cautionary Note Regarding Forward-Looking Statements.”

As used in this report, references to “DiaMedica,” the “Company,” “we,” “our” or “us,” unless the context otherwise requires, refer to DiaMedica Therapeutics Inc. and its subsidiaries, all of which are consolidated in DiaMedica’s condensed consolidated financial statements. References in this report to “common shares” mean our voting common shares, no par value per share.

We own various unregistered trademarks and service marks, including our corporate logo. Solely for convenience, the trademarks and trade names in this report are referred to without the ® and ™ symbols, but such references should not be construed as any indicator that the owner of such trademarks and trade names will not assert, to the fullest extent under applicable law, their rights thereto. We do not intend the use or display of other companies’ trademarks and trade names to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Statements in this report that are not descriptions of historical facts are forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995 that are based on management’s current expectations and are subject to risks and uncertainties that could negatively affect our business, operating results, financial condition and share price. We have attempted to identify forward-looking statements by terminology including “anticipates,” “believes,” “can,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “should,” “will,” “would,” the negative of these terms or other comparable terminology and the use of future dates.

The forward-looking statements in this report are subject to risks and uncertainties and include, among other things:

|

● |

our plans to develop, obtain regulatory approval for and commercialize our DM199 product candidate for the treatment of acute ischemic stroke (AIS) and cardio-renal disease (CRD) and our expectations regarding the benefits of our DM199 product candidate; |

|

● |

our ability to conduct successful clinical testing of our DM199 product candidate for AIS or CRD and meet certain anticipated or target dates with respect to our clinical studies, including in particular our ReMEDy2 trial and anticipated site activations, enrollment and interim analysis timing, especially in the light of COVID-19, hospital and medical facility staffing shortages, concerns managing logistics and protocol compliance for participants discharged from the hospital to an intermediate care facility and competition for research staff and trial subjects due to other stroke trials; |

|

● |

uncertainties relating to regulatory applications and related filing and approval timelines and the possibility of additional future adverse events associated with or unfavorable results from the ReMEDy2 trial; |

|

● |

the adaptive design of our ReMEDy2 trial, which is intended to enroll approximately 350 participants at up to 100 sites in the United States and internationally, and the possibility that these numbers and other aspects of the study could increase depending upon certain factors, including additional input from the United States Food and Drug Administration (FDA) and results of the interim analysis as determined by the independent data safety monitoring board; |

|

● |

the perceived benefits of our DM199 product candidate over existing treatment options for AIS and CRD; |

|

● |

the potential size of the markets for our DM199 product candidate for AIS and CRD and our ability to serve those markets and the rate and degree of market acceptance of, and our ability to obtain coverage and adequate reimbursement for, our DM199 product candidate for AIS and CRD both in the United States and internationally; |

|

● |

our ability to partner with and generate revenue from biopharmaceutical or pharmaceutical partners to develop, obtain regulatory approval for and commercialize our DM199 product candidate for AIS and CRD; |

|

● |

the success, cost and timing of our ReMEDy2 clinical trial, as well as our reliance on third parties to conduct our clinical trials; |

|

● |

our commercialization, marketing and manufacturing capabilities and strategy; |

|

● |

expectations regarding federal, state and foreign regulatory requirements and developments, such as potential FDA regulation of our DM199 product candidate for AIS and CRD; |

|

● |

our estimates regarding expenses, future revenue, capital requirements, how long our current cash resources will last and need for additional financing; |

|

● |

our expectations regarding our ability to obtain and maintain intellectual property protection for our DM199 product candidate; |

|

● |

expectations regarding competition and our ability to obtain data exclusivity for our DM199 product candidate for AIS and CRD; and |

|

● |

our anticipated use of the net proceeds from our recent private placements and our ability to obtain additional funding for our operations, including funding necessary to complete planned clinical trials and obtain regulatory approvals for our DM199 product candidate for AIS and CRD. |

These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including those described under “Part I. Item 1A. Risk Factors” in our annual report on Form 10-K for the fiscal year ended December 31, 2022, in our subsequent quarterly reports on Form 10-Q and those described above and elsewhere in this report. Moreover, we operate in a very competitive and rapidly-changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties and assumptions, the forward-looking events and circumstances discussed in this report may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements. Forward-looking statements should not be relied upon as predictions of future events. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee that the future results, levels of activity, performance or events and circumstances reflected in the forward-looking statements will be achieved or occur. Except as required by law, including the securities laws of the United States, we do not intend to update any forward-looking statements to conform these statements to actual results or to changes in our expectations.

PART I - FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

DiaMedica Therapeutics Inc.

Condensed Consolidated Balance Sheets

(In thousands, except share amounts)

|

September 30, 2023 |

December 31, 2022 |

|||||||

|

(unaudited) |

||||||||

|

ASSETS |

||||||||

|

Current assets: |

||||||||

|

Cash and cash equivalents |

$ | $ | ||||||

|

Short term marketable securities |

||||||||

|

Prepaid expenses and other assets |

||||||||

|

Amounts receivable |

||||||||

|

Total current assets |

||||||||

|

Non-current assets: |

||||||||

|

Long term marketable securities |

||||||||

|

Operating lease right-of-use asset, net |

||||||||

|

Property and equipment, net |

||||||||

|

Total non-current assets |

||||||||

|

Total assets |

$ | $ | ||||||

|

LIABILITIES AND EQUITY |

||||||||

|

Current liabilities: |

||||||||

|

Accounts payable |

$ | $ | ||||||

|

Accrued liabilities |

||||||||

|

Operating lease obligation |

||||||||

|

Financing lease obligation |

||||||||

|

Total current liabilities |

||||||||

|

Non-current liabilities: |

||||||||

|

Operating lease obligation, non-current |

||||||||

|

Finance lease obligation, non-current |

||||||||

|

Total non-current liabilities |

||||||||

|

Shareholders’ equity: |

||||||||

|

Common shares, par value; authorized; |

||||||||

|

Paid-in capital |

||||||||

|

Accumulated other comprehensive loss |

( |

) | ( |

) | ||||

|

Accumulated deficit |

( |

) | ( |

) | ||||

|

Total shareholders’ equity |

||||||||

|

Total liabilities and shareholders’ equity |

$ | $ | ||||||

See accompanying notes to the condensed consolidated financial statements.

DiaMedica Therapeutics Inc.

Condensed Consolidated Statements of Operations and Comprehensive Loss

(In thousands, except share and per share amounts)

(Unaudited)

|

Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

|

2023 |

2022 |

2023 |

2022 |

|||||||||||||

|

Operating expenses: |

||||||||||||||||

|

Research and development |

$ | $ | $ | $ | ||||||||||||

|

General and administrative |

||||||||||||||||

|

Operating loss |

( |

) |

( |

) |

( |

) |

( |

) |

||||||||

|

Other income: |

||||||||||||||||

|

Other income, net |

||||||||||||||||

|

Total other income, net |

||||||||||||||||

|

Loss before income tax expense |

( |

) |

( |

) |

( |

) |

( |

) |

||||||||

|

Income tax expense |

( |

) |

( |

) |

( |

) |

( |

) |

||||||||

|

Net loss |

( |

) |

( |

) |

( |

) |

( |

) |

||||||||

|

Other comprehensive (loss) gain |

||||||||||||||||

|

Unrealized (loss) gain on marketable securities |

( |

) |

( |

) |

( |

) |

||||||||||

|

Net loss and comprehensive loss |

$ | ( |

) |

$ | ( |

) |

$ | ( |

) |

$ | ( |

) |

||||

|

Basic and diluted net loss per share |

$ | ( |

) |

$ | ( |

) |

$ | ( |

) |

$ | ( |

) |

||||

|

Weighted average shares outstanding – basic and diluted |

||||||||||||||||

See accompanying notes to the condensed consolidated financial statements.

DiaMedica Therapeutics Inc.

Condensed Consolidated Statements of Shareholders’ Equity

For the Nine Months Ended September 30, 2023 and 2022

(In thousands, except share amounts)

(Unaudited)

|

Common Shares |

Paid-In Capital |

Accumulated Other Comprehensive Loss |

Accumulated Deficit |

Total Shareholders’ Equity |

||||||||||||||||

|

Balances at December 31, 2022 |

$ | $ | ( |

) | $ | ( |

) | $ | ||||||||||||

|

Issuance of common shares in settlement of deferred stock units |

— | — | — | — | ||||||||||||||||

|

Issuance of common shares upon the vesting of restricted stock units |

||||||||||||||||||||

|

Share-based compensation expense |

— | — | — | |||||||||||||||||

|

Unrealized gain on marketable securities |

— | — | — | |||||||||||||||||

|

Net loss |

— | — | — | ( |

) | ( |

) | |||||||||||||

|

Balances at March 31, 2023 |

$ | $ | ( |

) | $ | ( |

) | $ | ||||||||||||

|

Issuance of common shares net of offering costs of $ |

||||||||||||||||||||

|

Issuance of common shares upon the vesting of restricted stock units |

||||||||||||||||||||

|

Share-based compensation expense |

— | |||||||||||||||||||

|

Unrealized loss on marketable securities |

— | ( |

) | ( |

) | |||||||||||||||

|

Net loss |

— | ( |

) | ( |

) | |||||||||||||||

|

Balances at June 30, 2023 |

$ | $ | ( |

) | $ | ( |

) | $ | ||||||||||||

|

Offering costs on previously issued common shares |

— | ( |

) |

( |

) | |||||||||||||||

|

Issuance of common shares upon the vesting of restricted stock units |

||||||||||||||||||||

|

Share-based compensation expense |

||||||||||||||||||||

|

Unrealized loss on marketable securities |

— | — | ( |

) | ( |

) | ||||||||||||||

|

Net loss |

— | ( |

) | ( |

) | |||||||||||||||

|

Balances at September 30, 2023 |

$ | $ | ( |

) | $ | ( |

) | $ | ||||||||||||

|

Common Shares |

Paid-In Capital |

Accumulated Other Comprehensive Loss |

Accumulated Deficit |

Total Shareholders’ Equity |

||||||||||||||||

|

Balances at December 31, 2021 |

$ | $ | ( |

) | $ | ( |

) | $ | ||||||||||||

|

Share-based compensation expense |

— | |||||||||||||||||||

|

Unrealized loss on marketable securities |

— | ( |

) | ( |

) | |||||||||||||||

|

Net loss |

— | ( |

) | ( |

) | |||||||||||||||

|

Balances at March 31, 2022 |

$ | $ | ( |

) | $ | ( |

) | $ | ||||||||||||

|

Share-based compensation expense |

— | |||||||||||||||||||

|

Unrealized loss on marketable securities |

— | ( |

) | ( |

) | |||||||||||||||

|

Net loss |

— | ( |

) | ( |

) | |||||||||||||||

|

Balances at June 30, 2022 |

$ | $ | ( |

) | $ | ( |

) | $ | ||||||||||||

|

Share-based compensation expense |

— | |||||||||||||||||||

|

Unrealized gain on marketable securities |

— | |||||||||||||||||||

|

Net loss |

— | ( |

) | ( |

) | |||||||||||||||

|

Balances at September 30, 2022 |

$ | $ | ( |

) | $ | ( |

) | $ | ||||||||||||

See accompanying notes to the condensed consolidated financial statements.

DiaMedica Therapeutics Inc.

Condensed Consolidated Statements of Cash Flows

(In thousands)

(Unaudited)

|

Nine Months Ended September 30, |

||||||||

|

2023 |

2022 |

|||||||

|

Cash flows from operating activities: |

||||||||

|

Net loss |

$ | ( |

) |

$ | ( |

) |

||

|

Adjustments to reconcile net loss to net cash used in operating activities: |

||||||||

|

Share-based compensation |

||||||||

|

Amortization of (discount) premium on marketable securities |

( |

) |

||||||

|

Non-cash lease expense |

||||||||

|

Depreciation |

||||||||

|

Changes in operating assets and liabilities: |

||||||||

|

Amounts receivable |

( |

) |

||||||

|

Prepaid expenses and other assets |

( |

) |

( |

) |

||||

|

Accounts payable |

||||||||

|

Accrued liabilities |

( |

) |

( |

) |

||||

|

Net cash used in operating activities |

( |

) |

( |

) |

||||

|

Cash flows from investing activities: |

||||||||

|

Purchase of marketable securities |

( |

) |

( |

) |

||||

|

Maturities of marketable securities |

||||||||

|

Purchases of property and equipment |

( |

) |

( |

) |

||||

|

Net cash (used in) provided by investing activities |

( |

) |

||||||

|

Cash flows from financing activities: |

||||||||

|

Proceeds from issuance of common shares, net of offering costs |

||||||||

|

Principal payments on finance lease obligations |

( |

) |

( |

) |

||||

|

Net cash provided by (used in) financing activities |

( |

) |

||||||

|

Net decrease in cash and cash equivalents |

( |

) |

( |

) |

||||

|

Cash and cash equivalents at beginning of period |

||||||||

|

Cash and cash equivalents at end of period |

$ | $ | ||||||

|

Supplemental disclosure of non-cash transactions: |

||||||||

|

Cash paid for income taxes |

$ | $ | ||||||

| Assets acquired under operating lease | $ | $ | ||||||

See accompanying notes to the condensed consolidated financial statements.

DiaMedica Therapeutics Inc.

Notes to the Condensed Consolidated Financial Statements

(Unaudited)

|

1. |

Business |

DiaMedica Therapeutics Inc. and its wholly owned subsidiaries, DiaMedica USA Inc. and DiaMedica Australia Pty Ltd. (collectively, we, us, our, DiaMedica and the Company), exist for the primary purpose of advancing the clinical and commercial development of our proprietary recombinant KLK1 protein called DM199, for the treatment of neurological and cardio-renal diseases. Currently, our primary focus is on developing DM199, a recombinant form of the human tissue kallikrein-1 (KLK1) protein, for the treatment of acute ischemic stroke (AIS) and cardio-renal disease (CRD). Our parent company is governed under British Columbia’s Business Corporations Act, and our common shares are publicly traded on The Nasdaq Capital Market under the symbol “DMAC.”

|

2. |

Risks and Uncertainties |

DiaMedica operates in a highly regulated and competitive environment. The development, manufacturing and marketing of pharmaceutical products require approval from, and are subject to ongoing oversight by, the United States Food and Drug Administration (FDA) in the United States, the European Medicines Agency (EMA) in the European Union and comparable agencies in other countries. We are in the clinical stage of development of our initial product candidate, DM199, for the treatment of AIS and CRD. The Company has not completed the development of any product candidate and does not generate any revenues from the commercial sale of any product candidate. DM199 requires significant additional clinical testing and investment prior to seeking marketing approval and is not expected to be commercially available for at least three years, if at all.

On July 6, 2022, we announced that the FDA placed a clinical hold on the investigational new drug application (IND) for our Phase 2/3 ReMEDy2 trial. The clinical hold was issued following us voluntarily pausing participant enrollment in the trial to investigate three unexpected instances of clinically significant hypotension (low blood pressure) occurring shortly after initiation of the intravenous (IV) dose of DM199. In September 2022, we submitted our analysis of the events leading to and causing the hypotensive events, and proposed protocol modifications to address the mitigation of these events for future trial participants. Following review of this analysis, the FDA informed us that they were continuing the clinical hold and requesting, among other items, an additional in-use in vitro stability study of the IV administration of DM199, which includes testing the combination of the IV bag, IV tubing and mechanical infusion pump, to further rule out any other cause of the hypotension events. The requested in-use study was completed at an independent laboratory and the results were substantially consistent with our earlier testing of the IV bags. In May 2023, these additional supporting data were submitted to the FDA in our clinical hold response. In June 2023, the FDA completed review of our clinical hold response and informed us that the clinical hold was removed allowing us to begin preparations to resume our Phase 2/3 ReMEDy2 trial.

Prior to voluntarily halting enrollment in our ReMEDy2 trial, we had experienced slower than expected site activations and enrollment and may continue to experience these conditions as we resume site engagement and subject enrollment. We believe this was due to a number of factors, including the reduction or suspension of research activities at our previously targeted clinical study sites, as well as site staffing shortages, due to COVID-19 and concerns managing logistics and protocol compliance for participants discharged from the hospital into an intermediate care facility. We intend to continue to take certain actions, including engaging a clinical services consulting firm to provide staff support to study sites as needed, to assist study sites in overcoming these issues when we resume enrollment in the ReMEDy2 trial, however no assurances can be provided as to whether these issues will resolve or new issues will arise. For example, it is possible we may compete with other stroke clinical trials for research staff and trial subjects for our ReMEDy2 trial.

Our future success is dependent upon the success of our development efforts, our ability to demonstrate clinical progress for our DM199 product candidate in the United States or other markets, our ability, or the ability of any future partner, to obtain required governmental approvals of our product candidate, our ability to license or market and sell our DM199 product candidate and our ability to obtain additional financing to fund these efforts.

As of September 30, 2023, we have incurred losses of $

We expect that we will need substantial additional capital to further our research and development activities, complete the required clinical studies, regulatory activities and manufacturing development for our product candidate, DM199, or any future product candidates, to a point where they may be licensed or commercially sold. We expect our current cash, cash equivalents and marketable securities to fund our planned operations for at least the next 12 months from the date of issuance of these condensed consolidated financial statements. However, the amount and timing of our future funding requirements will depend on many factors, including the timing and results of our ongoing development efforts, and specifically the resumption of our ReMEDy2 trial, the rate of site activation and enrollment in our trial, the effects on our trial of COVID-19, site staffing shortages, competition for research staff and trial subjects due to other stroke trials and other factors, as well as the potential expansion of our current and potential new development programs and operating expenses incurred in connection with such activities. We may require significant additional funds earlier than we currently expect and there is no assurance that we will not need or seek additional funding prior to such time, especially if market conditions for raising additional capital are favorable.

|

3. |

Summary of Significant Accounting Policies |

Interim financial statements

We have prepared the accompanying condensed consolidated financial statements in accordance with accounting principles generally accepted in the United States (US GAAP) for interim financial information and with the instructions to Form 10-Q and Regulation S-X of the Securities and Exchange Commission (SEC). Accordingly, they do not include all of the information and footnotes required by US GAAP for complete financial statements. These condensed consolidated financial statements reflect all adjustments consisting of normal recurring accruals which, in the opinion of management, are necessary to present fairly our condensed consolidated financial position, condensed consolidated results of operations, condensed consolidated statement of shareholders’ equity and condensed consolidated cash flows for the periods and as of the dates presented. Our fiscal year ends on December 31. The condensed consolidated balance sheet as of December 31, 2022 was derived from our audited consolidated financial statements. Certain prior year amounts have been reclassified to conform to the current year presentation. These condensed consolidated financial statements should be read in conjunction with our annual consolidated financial statements and the notes thereto. The nature of our business is such that the results of any interim period may not be indicative of the results to be expected for the entire year.

Cash and cash equivalents

The Company considers all bank deposits, including money market funds and other investments, purchased with an original maturity to the Company of three months or less, to be cash and cash equivalents. The carrying amount of our cash equivalents approximates fair value due to the short maturity of the investments.

Marketable securities

The Company’s marketable securities typically consist of obligations of the United States government and its agencies, bank certificates of deposit and/or investment grade corporate obligations, which are classified as available-for-sale. Marketable securities which mature within 12 months from their date of purchase are included in current assets. Securities are valued based on market prices for similar assets using third party certified pricing sources. Available-for-sale securities are carried at fair value. The amortized cost of debt securities is adjusted for amortization of premiums and accretion of discounts to maturity. Such amortization or accretion is included in interest income. Realized gains and losses, if any, are calculated on the specific identification method and are included in other income in the condensed consolidated statements of operations.

We conduct periodic reviews to identify and evaluate each available-for-sale debt security that is in an unrealized loss position in order to determine whether an other-than-temporary impairment exists. An unrealized loss exists when the current fair value of an individual security is less than its amortized cost basis. Declines in fair value considered to be temporary and caused by noncredit-related factors, are recorded in accumulated other comprehensive loss, which is a separate component of shareholders’ equity. Declines in fair value that are other than temporary or caused by credit-related factors, are recorded within earnings as an impairment loss. There were no other-than-temporary unrealized losses as of September 30, 2023.

Concentration of credit risk

Financial instruments that potentially expose the Company to concentration of credit risk consist primarily of cash, cash equivalents and marketable securities. The Company maintains its cash balances primarily with two financial institutions. These balances generally exceed federally insured limits. The Company has not experienced any losses in such accounts and believes it is not exposed to any significant credit risk in cash and cash equivalents. The Company believes that the credit risk related to marketable securities is limited due to the adherence to an investment policy focused on the preservation of principal.

Fair value measurements

Under the authoritative guidance for fair value measurements, fair value is defined as the exit price, or the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants as of the measurement date. The authoritative guidance also establishes a hierarchy for inputs used in measuring fair value that maximizes the use of observable inputs and minimizes the use of unobservable inputs by requiring that the most observable inputs be used when available. Observable inputs are inputs market participants would use in valuing the asset or liability developed based on market data obtained from sources independent of the Company. Unobservable inputs are inputs that reflect the Company’s assumptions about the factors market participants would use in valuing the asset or liability developed based upon the best information available in the circumstances. The categorization of financial assets and financial liabilities within the valuation hierarchy is based upon the lowest level of input that is significant to the fair value measurement.

The hierarchy is broken down into three levels defined as follows:

Level 1 Inputs — quoted prices in active markets for identical assets and liabilities

Level 2 Inputs — observable inputs other than quoted prices in active markets for identical assets and liabilities

Level 3 Inputs — unobservable inputs

As of September 30, 2023, the Company believes that the carrying amounts of its other financial instruments, including amounts receivable, accounts payable and accrued liabilities, approximate their fair value due to the short-term maturities of these instruments. See Note 4, titled “Marketable Securities” for additional information.

Patent costs

Costs associated with applying for, prosecuting and maintaining patents are expensed as incurred given the uncertainty of patent approval and, if approved, the resulting probable future economic benefit to the Company. Patent-related costs, consisting primarily of legal expenses and filing/maintenance fees, are included in general and administrative costs and were $

Recently Adopted Accounting Pronouncements

In June 2016, the FASB issued ASU No. 2016-13, Financial Instruments – Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments, which requires the measurement and recognition of expected credit losses for financial assets held at amortized cost. This ASU replaces the existing incurred loss impairment model with an expected loss model. It also eliminates the concept of other-than-temporary impairment and requires credit losses related to available-for-sale debt securities to be recorded through an allowance for credit losses rather than as a reduction in the amortized cost basis of the securities. These changes will result in earlier recognition of credit losses. The standard was effective for smaller reporting companies in fiscal years beginning after December 15, 2022 with early adoption permitted for all periods beginning after December 15, 2018. We adopted ASU No. 2016-13 on January 1, 2023, which did not have an impact on our condensed consolidated financial statements.

|

4. |

Marketable Securities |

The available-for-sale marketable securities are primarily comprised of investments in commercial paper, corporate bonds and government securities and consist of the following, measured at fair value on a recurring basis (in thousands):

|

Fair Value Measurements Using Inputs Considered as of: |

||||||||||||||||||||||||||||||||

| September 30, 2023 |

December 31, 2022 |

|||||||||||||||||||||||||||||||

|

Total |

Level 1 |

Level 2 |

Level 3 |

Total |

Level 1 |

Level 2 |

Level 3 |

|||||||||||||||||||||||||

|

Commercial paper and corporate bonds |

$ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

|

Government securities |

||||||||||||||||||||||||||||||||

|

Total |

$ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

Accrued interest receivable on marketable securities is included in amounts receivable and was $

There were no transfers of assets between Level 1 and Level 2 of the fair value measurement hierarchy during the nine months ended September 30, 2023.

Under the terms of the Company’s investment policy, purchases of marketable securities are limited to investment grade governmental and corporate obligations and bank certificates of deposit with a primary objective of principal preservation. Maturities of individual securities are less than 18 months and the amortized cost of all securities approximated fair value as of September 30, 2023 and December 31, 2022.

|

5. |

Amounts Receivable |

Amounts receivable consisted primarily of accrued interest receivable on marketable securities of $

|

6. |

Prepaid Expenses and Other Assets |

Prepaid expenses and other assets consisted of the following (in thousands):

|

September 30, 2023 |

December 31, 2022 |

|||||||

|

Prepaid expenses |

$ | $ | ||||||

|

Advances to vendors |

||||||||

|

Total prepaid expenses and other assets |

$ | $ | ||||||

We periodically advance funds to vendors engaged to support the performance of our clinical trials and related supporting activities. The funds advanced are held, interest free, for varying periods of time and may be recovered by DiaMedica through partial reductions of ongoing invoices, application against final study/project invoices or refunded upon completion of services to be provided. Deposits are classified as current or non-current based upon their expected recovery time.

|

7. |

Property and Equipment |

Property and equipment consisted of the following (in thousands):

|

September 30, 2023 |

December 31, 2022 |

|||||||

|

Furniture and equipment |

$ | $ | ||||||

|

Computer equipment |

||||||||

|

Leasehold improvements |

||||||||

|

Less accumulated depreciation |

( |

) | ( |

) | ||||

|

Property and equipment, net |

$ | $ | ||||||

|

8. |

Accrued Liabilities |

Accrued liabilities consisted of the following (in thousands):

|

September 30, 2023 |

December 31, 2022 |

|||||||

|

Accrued compensation |

$ | $ | ||||||

|

Accrued research and other professional fees |

||||||||

|

Accrued clinical trial costs |

||||||||

|

Accrued other liabilities |

||||||||

|

Total accrued liabilities |

$ | $ | ||||||

|

9. |

Operating Lease |

Office lease

Our operating lease costs were $

Maturities of our operating lease obligation are as follows as of September 30, 2023 (in thousands):

|

2023 |

||||

|

2024 |

||||

|

2025 |

||||

|

2026 |

||||

|

2027 |

||||

|

2028 |

||||

|

Total lease payments |

$ | |||

|

Less interest portion |

( |

) | ||

|

Present value of lease obligation |

$ |

|

10. |

Shareholders’ Equity |

Authorized capital stock

The Company has authorized share capital of an unlimited number of voting common shares, and the shares do not have a stated par value. Common shareholders are entitled to receive dividends as declared by the Company, if any, and are entitled to one vote per share at the Company's annual general meeting and any special meeting.

Equity issued during the nine months ended September 30, 2023

On April 10, 2023, in conjunction with his appointment as Chief Business Officer of DiaMedica, Mr. David Wambeke purchased

On June 21, 2023, we issued and sold an aggregate

In connection with the June 2023 private placement, we entered into a registration rights agreement (Registration Rights Agreement) with the investors pursuant to which we agreed to file with the United States Securities and Exchange Commission (SEC) a registration statement registering the resale of the shares sold in the June 2023 private placement (Resale Registration Statement). The Resale Registration Statement was filed with the SEC on June 30, 2023 and declared effective by the SEC on July 7, 2023. Under the terms of the Registration Rights Agreement, we agreed to keep the Resale Registration Statement effective at all times until the shares are no longer considered “Registrable Securities” under the Registration Rights Agreement and if we fail to keep the Resale Registration Statement effective, subject to certain permitted exceptions, we will be required to pay liquidated damages to the investors in an amount of up to

During the nine months ended September 30, 2023,

Equity issued during the nine months ended September 30, 2022

During the nine months ended September 30, 2022, we did issue any common shares.

Shares reserved

Common shares reserved for future issuance are as follows:

|

September 30, 2023 |

||||

|

Common shares issuable upon exercise of employee and non-employee stock options |

||||

|

Common shares issuable upon settlement of deferred stock units |

||||

|

Common shares issuable upon vesting of restricted stock units |

||||

|

Common shares issuable upon exercise of common share purchase warrants |

||||

|

Shares available for grant under the 2019 Omnibus Incentive Plan |

||||

|

Shares available for grant under the 2021 Employment Inducement Incentive Plan |

||||

|

Total |

||||

|

11. |

Net Loss Per Share |

We compute net loss per share by dividing our net loss (the numerator) by the weighted-average number of common shares outstanding (the denominator) during the period. Shares issued during the period and shares reacquired during the period, if any, are weighted for the portion of the period that they were outstanding. The computation of diluted earnings per share, or EPS, is similar to the computation of basic EPS except that the denominator is increased to include the number of additional common shares that would have been outstanding if the dilutive potential common shares had been issued. Our diluted EPS is the same as basic EPS due to common equivalent shares being excluded from the calculation, as their effect is anti-dilutive.

The following table summarizes our calculation of net loss per common share for the periods presented (in thousands, except share and per share data):

|

Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

|

2023 |

2022 |

2023 |

2022 |

|||||||||||||

|

Net loss |

$ | ( |

) |

$ | ( |

) |

$ | ( |

) |

$ | ( |

) |

||||

|

Weighted average shares outstanding—basic and diluted |

||||||||||||||||

|

Basic and diluted net loss per share |

$ | ( |

) |

$ | ( |

) |

$ | ( |

) |

$ | ( |

) |

||||

The following outstanding potential common shares were not included in the diluted net loss per share calculations as their effects were not dilutive:

|

Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

|

2023 |

2022 |

2023 |

2022 |

|||||||||||||

|

Employee and non-employee stock options |

||||||||||||||||

|

Common shares issuable under common share purchase warrants |

||||||||||||||||

|

Common shares issuable under deferred stock units |

||||||||||||||||

|

Common shares issuable upon vesting of restricted stock units |

||||||||||||||||

|

12. |

Share-Based Compensation |

Amended and Restated 2019 Omnibus Incentive Plan

The DiaMedica Therapeutics Inc. Amended and Restated 2019 Omnibus Incentive Plan (the 2019 Plan) was adopted by the Board of Directors (Board) on March 10, 2022 and approved by our shareholders at our 2022 Annual General Meeting of Shareholders held on May 18, 2022.

The 2019 Plan permits the Board, or a committee or subcommittee thereof, to grant to the Company’s eligible employees, non-employee directors and certain consultants non-statutory and incentive stock options, stock appreciation rights, restricted stock awards, restricted stock units, deferred stock units (DSUs), performance awards, non-employee director awards and other stock-based awards. We grant options to purchase common shares under the 2019 Plan at no less than the fair market value of the underlying common shares as of the date of grant. Options granted to employees and non-employee directors have a maximum term of years and generally vest over to years. Options granted to non-employees have a maximum term of years and generally vest over year. Subject to adjustment as provided in the 2019 Plan, the maximum number of the Company’s common shares authorized for issuance under the 2019 Plan is

2021 Employment Inducement Incentive Plan

On December 3, 2021, the Board adopted the DiaMedica Therapeutics Inc. 2021 Employment Inducement Incentive Plan (Inducement Plan) to facilitate the granting of equity awards as an inducement material to new employees joining the Company. The Inducement Plan is administered by the Compensation Committee of the Board of Directors. The Board reserved

Prior Stock Option Plan

The DiaMedica Therapeutics Inc. Stock Option Plan, Amended and Restated November 6, 2018 (Prior Plan), was terminated by the Board of Directors in conjunction with the shareholder approval of the 2019 Plan. Awards outstanding under the Prior Plan remain outstanding in accordance with and pursuant to the terms thereof. Options granted under the Prior Plan have terms similar to those used under the 2019 Plan. As of September 30, 2023, options to purchase an aggregate of

Prior Deferred Stock Unit Plan

The DiaMedica Therapeutics Inc. Amended and Restated Deferred Stock Unit Plan (Prior DSU Plan) was terminated by the Board of Directors in conjunction with the shareholder approval of the 2019 Plan. Awards outstanding under the Prior DSU Plan remain outstanding in accordance with and pursuant to the terms thereof. As of September 30, 2023, there were

Share-based compensation expense for each of the periods presented is as follows (in thousands):

|

Three Months Ended September 30 |

Nine Months Ended September 30 |

|||||||||||||||

|

2023 |

2022 |

2023 |

2022 |

|||||||||||||

|

Research and development |

$ | $ | $ | $ | ||||||||||||

|

General and administrative |

||||||||||||||||

|

Total share-based compensation |

$ | $ | $ | $ | ||||||||||||

We recognize share-based compensation based on the fair value of each award as estimated using the Black-Scholes option valuation model. Ultimately, the total expense recognized over the vesting period will only be for those shares that actually vest.

A summary of option activity is as follows (in thousands, except share and per share amounts):

|

Shares Underlying Options Outstanding |

Weighted Average Exercise Price Per Share |

Aggregate Intrinsic Value |

||||||||||

|

Balances at December 31, 2022 |

$ | $ | ||||||||||

|

Granted |

||||||||||||

|

Expired/cancelled |

( |

) | ||||||||||

|

Forfeited |

( |

) | ||||||||||

|

Balances at September 30, 2023 |

$ | $ | ||||||||||

Information about stock options outstanding, vested and expected to vest as of September 30, 2023, is as follows:

|

Outstanding, Vested and Expected to Vest |

Options Vested and Exercisable |

|||||||||||||||||||||

|

Per Share Exercise Price |

Shares |

Weighted Average Remaining Contractual Life (Years) |

Weighted Average Exercise Price |

Options Exercisable |

Weighted Average Remaining Contractual Life (Years) |

|||||||||||||||||

| $ |

- |

$ |

$ | |||||||||||||||||||

| $ |

- |

$ |

||||||||||||||||||||

| $ |

- |

$ |

||||||||||||||||||||

| $ |

- |

$ |

||||||||||||||||||||

| $ |

- |

$ |

||||||||||||||||||||

| $ | ||||||||||||||||||||||

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations is based upon accounting principles generally accepted in the United States of America and discusses the financial condition and results of operations for DiaMedica Therapeutics Inc. and our subsidiaries for the three and nine months ended September 30, 2023 and 2022.

This discussion should be read in conjunction with our condensed consolidated financial statements and related notes included elsewhere in this report and our annual report on Form 10-K for the year ended December 31, 2022. The following discussion contains forward-looking statements that involve numerous risks and uncertainties. Our actual results could differ materially from the forward-looking statements as a result of these risks and uncertainties. See “Cautionary Note Regarding Forward-Looking Statements” for additional cautionary information.

Business Overview

We are a clinical stage biopharmaceutical company committed to improving the lives of people suffering from serious diseases. Our lead candidate DM199 is the first pharmaceutically active recombinant (synthetic) form of the human tissue kallikrein-1 (KLK1) protein to be clinically studied in patients. KLK1 is an established therapeutic modality in Asia for the treatment of acute ischemic stroke (AIS) and cardio-renal disease (CRD). Our long-term goal is to use our patented and in-licensed technologies to establish our Company as a leader in the development and commercialization of therapeutic treatments from novel recombinant proteins. Our current focus is on the treatment of AIS and CRD. We plan to advance DM199, our lead drug candidate, through required clinical trials to create shareholder value by establishing its clinical and commercial potential as a therapy for AIS and CRD.

KLK1 is a serine protease (protein), produced primarily in the kidneys, pancreas and salivary glands, which plays a critical role in the regulation of local blood flow and vasodilation (the widening of blood vessels which decreases vascular resistance) in the body, as well as an important role in reducing inflammation and oxidative stress (an imbalance between potentially damaging reactive oxygen species, or free radicals and antioxidants in the body). We believe DM199 has the potential to treat a variety of diseases where healthy functioning requires sufficient activity of KLK1 and its system, the kallikrein-kinin system (KKS).

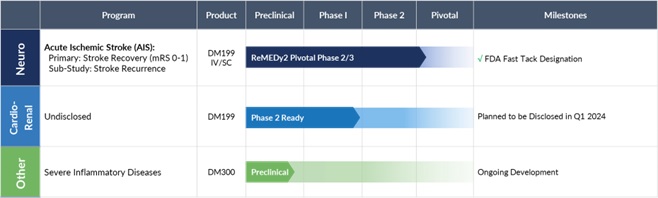

Our product development pipeline is as follows:

Neuro: AIS Phase 2/3 ReMEDy2 Study of DM199

Our ReMEDy2 trial is an adaptive design, randomized, double-blind, placebo-controlled trial intended to enroll approximately 350 patients at up to 100 sites in the United States and internationally. Patients enrolled in the trial will be treated with either DM199 or placebo within 24 hours of the onset of AIS symptoms. The trial excludes patients treated with tissue plasminogen activator (tPA) and those with large vessel occlusions. The study population is representative of the approximately 80% of AIS patients who do not have treatment options today, primarily due to the limitations on treatment with tPA or mechanical thrombectomy. We believe that the proposed trial has the potential to serve as a pivotal registration study of DM199 in this patient population.

On July 6, 2022, we announced that the FDA placed a clinical hold on the investigational new drug application (IND) for our Phase 2/3 ReMEDy2 trial. The clinical hold was issued following us voluntarily pausing participant enrollment in the trial to investigate three unexpected instances of clinically significant hypotension (low blood pressure) occurring shortly after initiation of the intravenous (IV) dose of DM199. In September 2022, we submitted our analysis of the events leading to and causing the hypotensive events, and proposed protocol modifications to address the mitigation of these events for future trial participants. Following review of this analysis, the FDA informed us that they were continuing the clinical hold and requested, among other items, an additional in-use in vitro stability study of the IV administration of DM199, which includes testing the combination of the IV bag, IV tubing and mechanical infusion pump, to further rule out any other cause of the hypotension events. The requested in-use study was completed at an independent laboratory and the results were substantially consistent with our earlier testing of the IV bags. In May 2023, these additional supporting data were submitted to the FDA in our clinical hold response. In June 2023, the FDA completed review of our clinical hold response and informed us that the clinical hold was removed allowing us to begin preparations to resume our Phase 2/3 ReMEDy2 trial.

We also conducted a Phase 1C open label, single ascending dose (SAD) study of DM199 administered with the PVC IV bags used in the ReMEDy2 trial. The purpose of the study was to confirm, with human data, the DM199 blood concentration level achieved with the IV dose and further evaluate safety and tolerability. This study was conducted in Australia and enrollment commenced in March 2023. The third cohort, which received the 0.50 µg/kg dose level proposed for the ReMEDy2 trial, was dosed in April 2023 with no significant adverse events related to DM199. The pharmacokinetic data, including the DM199 blood concentration levels, for all three cohorts was included as supplemental information in our clinical hold response. We also completed an additional cohort of hypertensive patients (Part B) being treated with angiotensin-converting enzyme inhibitors (ACEi). In this Part B, all ACEi patients received the full IV dose at the 0.5 µg/kg level with no instances of hypotension. We believe that these results provide further assurance to potential investigators that ACEi patients may be safely included in the ReMEDy2 trial. This Phase 1C study is complete.

Prior to voluntarily halting enrollment in the ReMEDy2 trial, we had experienced slower than expected site activations and enrollment and may continue to experience these conditions as we resume site engagement and subject enrollment. We believe this was due to a number of factors, including the reduction or suspension of research activities at our previously targeted clinical study sites, as well as site staffing shortages, due to COVID-19 and concerns managing logistics and protocol compliance for participants discharged from the hospital into an intermediate care facility. We intend to continue to take certain actions, including engaging a clinical services consulting firm to provide staff support to study sites as needed, to assist study sites in overcoming these issues when we resume enrollment in the ReMEDy2 trial, however no assurances can be provided as to whether these issues will resolve or new issues will arise. For example, it is possible we may compete with other stroke clinical trials for research staff and trial subjects for our ReMEDy2 trial.

Cardio-Renal: Phase 2 REDUX Clinical Trial of DM199

We continue to work towards finalizing the data analyses and clinical study report from our Phase 2 REDUX clinical trial of DM199 for the treatment of chronic kidney disease as we evaluate next steps for our CRD program.

Financial Overview

We have not generated any revenues from product sales. We have financed our operations from public and private sales of equity, including our April and June 2023 private placements, the exercise of warrants and stock options, interest income on funds available for investment and government grants and tax credits. Our April and June 2023 private placements together generated $36.8 million in net proceeds after deducting offering expenses. We have incurred losses in each year since our inception. Our net losses were $14.2 million and $9.9 million for the nine months ended September 30, 2023 and 2022, respectively. As of September 30, 2023, we had an accumulated deficit of $110.4 million. Substantially all of our operating losses resulted from expenses incurred in connection with our product candidate development programs, our primary research and development (R&D) activities, and general and administrative (G&A) support costs associated with our operations and status as a publicly listed company.

While we expect our rate of future negative cash flow per month will generally increase as we resume our ReMEDy2 trial, we expect our current cash resources will be sufficient to allow us to resume our ReMEDy2 trial, complete the data analysis from our REDUX Phase 2 trial and evaluate next steps for our CRD program and otherwise fund our planned operations for at least the next 12 months from the date of issuance of the condensed consolidated financial statements included in this report. However, the amount and timing of our future funding requirements will depend on many factors, including the timing and results of our ongoing development efforts, and specifically the resumption of our ReMEDy2 trial, the rate of site activation and enrollment in our trial, the effects on our trial of COVID-19, site staffing shortages, competition for research staff and trial subjects due to other stroke trials, and other factors, as well as the potential expansion of our current and potential new development programs, and operating expenses incurred in connection with such activities. We may require significant additional funds earlier than we currently expect and there is no assurance that we will not need or seek additional funding prior to such time. We may elect to raise additional funds even before we need them if market conditions for raising additional capital are favorable.

Overview of Expense Components

Research and Development (R&D) Expenses

R&D expenses consist primarily of fees paid to external service providers such as contract research organizations; clinical support services; clinical development including clinical sites; outside nursing services and laboratory testing and preclinical trials; development of manufacturing processes; costs for production runs of DM199; salaries, benefits, share-based compensation; and other personnel costs.

At this time, due to the risks inherent in the clinical development process and the clinical stage of our product development programs, we are unable to estimate with any certainty the costs we will incur in developing DM199 through marketing approval or any of our preclinical development programs. The process of conducting clinical studies necessary to obtain regulatory approval and manufacturing scale-up to support expanded development and potential future commercialization is costly and time consuming. Any failure by us or delay in completing clinical studies, manufacturing scale-up or in obtaining regulatory approvals could lead to increased R&D expenses and, in turn, have a material adverse effect on our results of operations.

We expect that our R&D expenses will increase in the future if we are successful in advancing DM199, or any of our preclinical programs, through the required stages of clinical development. The process of conducting clinical trials necessary to obtain regulatory approval and manufacturing scale-up to support expanded development and potential future commercialization is costly and time consuming. Any failure by us or delay in completing clinical trials, manufacturing scale-up or in obtaining regulatory approvals, could lead to increased R&D expenses and, in turn, have a material adverse effect on our results of operations.

General and Administrative (G&A) Expenses

G&A expenses consist primarily of salaries, employee benefits, share-based compensation and other personnel costs related to our executive, finance, business development and support functions. G&A expenses also include insurance, including directors and officers liability coverage, rent and utilities, travel expenses, patent costs, and professional fees, including for auditing, tax and legal services.

Other Income, Net

Other income, net consists primarily of interest income earned on marketable securities.

Results of Operations

Comparison of the Three and Nine Months ended September 30, 2023 and 2022

The following table summarizes our unaudited results of operations for the three and nine months ended September 30, 2023 and 2022 (in thousands):

|

Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

|

2023 |

2022 |

2023 |

2022 |

|||||||||||||

|

Operating expenses: |

||||||||||||||||

|

Research and development |

$ | 3,272 | $ | 1,640 | $ | 9,433 | $ | 5,569 | ||||||||

|

General and administrative |

1,885 | 1,488 | 5,986 | 4,459 | ||||||||||||

|

Other income, net |

693 | 76 | 1,220 | 124 | ||||||||||||

Research and Development Expenses

R&D expenses increased to $3.3 million for the three months ended September 30, 2023, up $1.7 million from $1.6 million for the three months ended September 30, 2022. R&D expenses increased to $9.4 million for the nine months ended September 30, 2023, up from $5.6 million for the nine months ended September 30, 2022. The increase for the nine-month comparison was driven principally by costs incurred for the in-use studies performed to address the recently lifted clinical hold on our ReMEDy2 AIS trial, costs incurred for the Phase 1C study determining the DM199 blood concentration levels achieved with the IV dose of DM199 and increased manufacturing and process development costs. Also contributing to the increase were higher personnel costs associated with expanding the clinical team. These increases were partially offset by decreased costs incurred for the Phase 2/3 ReMEDy2 AIS trial as activity was limited prior to the June 2023 lift of the clinical hold.

General and Administrative Expenses

G&A expenses were $1.9 million for the three months ended September 30, 2023, up from $1.5 million for the three months ended September 30, 2022. G&A expenses were $6.0 million for the nine months ended September 30, 2023, up from $4.5 million for the nine months ended September 30, 2022. The increase for the nine-month comparison was driven principally by increased legal fees incurred in connection with our lawsuit against PRA Netherlands and increased personnel costs incurred in conjunction with expanding our team. Increased cost for patent prosecution and non-cash share-based compensation also contributed to the increase.

Other Income, Net

Other income, net was $693 thousand and $1.2 million for the three and nine months ended September 30, 2023, respectively, compared to $76 thousand and $124 thousand for the three and nine months ended September 30, 2022, respectively. These increases were due to increased interest income earned on marketable securities during the current year periods due to higher weighted average invested cash balances.

Liquidity and Capital Resources

The following tables summarize our liquidity and capital resources as of September 30, 2023 and December 31, 2022, and our sources and uses of cash for each of the nine month periods ended September 30, 2023 and 2022, and is intended to supplement the more detailed discussion that follows (in thousands):

|

September 30, 2023 |

December 31, 2022 |

|||||||

|

Cash, cash equivalents and marketable securities |

$ | 56,212 | $ | 33,502 | ||||

|

Total assets |

58,139 | 34,395 | ||||||

|

Total current liabilities |

2,170 | 2,168 | ||||||

|

Total shareholders’ equity |

55,629 | 31,827 | ||||||

|

Working capital |

45,716 | 31,667 | ||||||

|

Nine Months Ended September 30, |

||||||||

|

Cash Flow Data |

2023 |

2022 |

||||||

|

Cash flow provided by (used in): |

||||||||

|

Operating activities |

$ | (14,916 | ) | $ | (8,745 | ) | ||

|

Investing activities |

(24,423 | ) | 6,814 | |||||

|

Financing activities |

36,843 | (5 | ) | |||||

|

Net decrease in cash |

$ | (2,496 | ) | $ | (1,936 | ) | ||

Working Capital

We had aggregate cash, cash equivalents and marketable securities of $56.2 million, current liabilities of $2.2 million and working capital of $45.7 million as of September 30, 2023, compared to aggregate cash, cash equivalents and marketable securities of $33.5 million, $2.2 million in current liabilities and $31.7 million in working capital as of December 31, 2022. The increases in our combined cash, cash equivalents and marketable securities and in our working capital are due primarily to the net proceeds received from our April and June 2023 private placements, partially offset by cash used to fund our current operations.

Cash Flows

Operating Activities

Net cash used in operating activities for the nine months ended September 30, 2023 was $14.9 million compared to $8.7 million for the nine months ended September 30, 2022. The increase in cash used in operating activities is driven primarily by our net loss and increased amortization of discounts on marketable securities, partially offset by non-cash share-based compensation and the effects of the changes in operating assets and liabilities.

Investing Activities

Investing activities consist primarily of purchases and maturities of marketable securities. Net cash used in investing activities was $24.4 million for the nine months ended September 30, 2023 compared to net cash provided by investing activities of $6.8 million for the nine months ended September 30, 2022. This change resulted primarily from the timing of maturities and investments of the net proceeds from our June 2023 private placement.

Financing Activities

Net cash provided by financing activities was $36.8 million for the nine months ended September 30, 2023 consisting primarily of net proceeds from the sale of common shares in our April and June 2023 private placements, compared to net cash used in financing activities of $5 thousand consisting of principal payments on finance lease obligations for the nine months ended September 30, 2022.

Capital Requirements

Since our inception, we have incurred losses while advancing the R&D of our DM199 product candidate. We have not generated any revenues from product sales and do not know when or if we will generate any revenues from product sales of our DM199 product candidate or any future product candidate. We expect to continue to incur substantial operating losses until such time as any future product sales, royalty payments, licensing fees and/or milestone payments are sufficient to generate revenues to fund our continuing operations. We expect our operating losses to increase in the near term as compared to prior periods as we continue the research, development and clinical studies of our DM199 product candidate, including in particular the resumption of our ReMEDy2 trial. In the long-term, subject to obtaining regulatory approval of our DM199 product candidate, or any future product candidate, and in the absence of the assistance of a strategic partner, we would expect to incur significant commercialization expenses for product sales, marketing, manufacturing and distribution.

Accordingly, and notwithstanding the completion of our April and June 2023 private placements from which we received aggregate net proceeds of $36.8 million, we expect we will need substantial additional capital to further our R&D activities, current and anticipated future clinical studies, regulatory activities and otherwise develop our product candidate, DM199, or any future product candidate, to a point where the product candidate may be licensed or commercially sold. Although we are striving to achieve these plans, there is no assurance that these and other strategies will be achieved or that additional funding will be obtained on favorable terms or at all. We expect our rate of future negative cash flow per month will vary depending on our clinical activities and the timing of expenses incurred and will increase as we resume our ReMEDy2 trial. We expect our current cash resources will be sufficient to resume our ReMEDy2 trial in patients with AIS, complete the data analysis from our REDUX Phase 2 trial in patients with CRD, evaluate our next steps for our CRD program, and otherwise fund our planned operations for at least the next twelve months from the date of issuance of the condensed consolidated financial statements included in this report. However, the amount and timing of our future funding requirements will depend on many factors, including the timing and results of our ongoing development efforts, and specifically the resumption of our ReMEDy2 trial, the rate of site activation and enrollment in such trial, the effects on such trial of COVID-19, site staffing shortages, competition for research staff and trial subjects due to other stroke trials, and other factors, as well as the potential expansion of our current and potential new development programs, and operating expenses incurred in connection with such activities. We may require significant additional funds earlier than we currently expect and there is no assurance that we will not need or seek additional funding prior to such time, especially if market conditions for raising additional capital are favorable.

Historically, we have financed our operations primarily from sales of equity securities and the exercise of warrants and stock options, and we expect to continue this practice for the foreseeable future. We do not have any existing credit facilities under which we could borrow funds. We may seek to raise additional funds through various sources, such as equity or debt financings, or through strategic collaborations and license agreements. We can give no assurances that we will be able to secure additional sources of funds to support our operations, or if such funds are available to us, that such additional financing will be sufficient to meet our needs or on terms acceptable to us. This is particularly true if our clinical data is not positive or economic and market conditions deteriorate.

To the extent we raise additional capital through the sale of equity or convertible debt securities, the ownership interests of our shareholders will be diluted. Debt financing, if available, may involve agreements that include conversion discounts, pledging our intellectual property as collateral or covenants limiting or restricting our ability to take specific actions, such as incurring additional debt or making capital expenditures. If we raise additional funds through government or other third-party funding, marketing and distribution arrangements or other collaborations, or strategic alliances or licensing arrangements with third parties, we may have to relinquish valuable rights to our technologies, future revenue streams, research programs or product candidates or grant licenses on terms that may not be favorable to us. The availability of financing will be affected by our clinical data and other results of scientific and clinical research; the ability to attain regulatory approvals and other regulatory actions; market acceptance of our product candidates; the state of the capital markets generally with particular reference to pharmaceutical, biotechnology and medical companies; the status of strategic alliance agreements; and other relevant commercial considerations.

If adequate funding is not available when needed, we may be required to scale back our operations by taking actions that may include, among other things, implementing cost reduction strategies, such as reducing use of outside professional service providers, reducing the number of our employees or employee compensation, modifying or delaying the development of our DM199 product candidate; licensing to third parties the rights to commercialize our DM199 product candidate for AIS, CRD or other indications that we would otherwise seek to pursue, or otherwise relinquishing significant rights to our technologies, future revenue streams, research programs or product candidates or granting licenses on terms that may not be favorable to us; and/or divesting assets or ceasing operations through a merger, sale, or liquidation of our company.

Critical Accounting Policies and Estimates

There have been no material changes to our critical accounting policies and estimates from the information provided in “Part II. Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies,” included in our annual report on Form 10-K for the fiscal year ended December 31, 2022.

|

ITEM 3. |

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

As a smaller reporting company, we are not required to provide disclosure pursuant to this item.

|

ITEM 4. |

CONTROLS AND PROCEDURES |

Evaluation of Disclosure Controls and Procedures

We maintain disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the United States Securities Exchange Act of 1934, as amended (Exchange Act)) that are designed to provide reasonable assurance that information required to be disclosed by us in the reports we file or submit under the Exchange Act, is recorded, processed, summarized and reported, within the time periods specified in the SEC’s rules and forms and that such information is accumulated and communicated to our management, including our principal executive officer and principal financial officer, or persons performing similar functions, as appropriate to allow timely decisions regarding required disclosure. Our management evaluated, with the participation of our Chief Executive Officer and Chief Financial Officer, the effectiveness of the design and operation of our disclosure controls and procedures as of the end of the period covered in this report. Based on that evaluation, our Chief Executive Officer and Chief Financial Officer concluded that our disclosure controls and procedures were effective as of the end of such period to provide reasonable assurance that information required to be disclosed in the reports that we file or submit under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms, and that such information is accumulated and communicated to our management, including our Chief Executive Officer and Chief Financial Officer, as appropriate, to allow timely decisions regarding required disclosure.

Changes in Internal Control over Financial Reporting

There was no change in our internal control over financial reporting that occurred during the three months ended September 30, 2023 that has materially affected or is reasonably likely to materially affect our internal control over financial reporting.

|

PART II - |

OTHER INFORMATION |

|

ITEM 1. |

LEGAL PROCEEDINGS |

Litigation with Pharmaceutical Research Associates Group B.V., acquired by ICON plc as of July 1, 2021, (ICON/PRA Netherlands)

On November 23, 2022, we filed a petition requesting leave for a prejudgment attachment of all relevant documents in possession of Pharmaceutical Research Associates Group B.V., acquired by ICON plc as of July 1, 2021, (ICON/PRA Netherlands), which was granted on November 28, 2022, by the District Court of Northern Netherlands. A representative of the District Court served ICON/PRA Netherlands with the prejudgment attachment on or about December 7 and 8, 2022. The case was formally introduced to the Netherlands Commercial Court (NCC) on December 28, 2022 and a hearing by the NCC to determine whether we are entitled to take possession of the records seized was scheduled and held on March 16, 2023.

On April 21, 2023, the NCC issued a judgement affirming our ownership of the physical documents, including 51 hardcopy folders and certain digital files, related to the clinical studies performed by ICON/PRA Netherlands and seized by the Dutch courts in December 2022. The NCC further ordered ICON/PRA Netherlands to allow and tolerate the surrender of the documents, including digital and source data. Additionally, the NCC found that we are not in breach of any obligation under the clinical study agreement and PRA Netherlands had no basis to suspend the fulfillment of its obligations under the clinical study agreement to provide us all clinical data and access to perform an audit of the study. On June 15, 2023, ICON/PRA Netherlands filed an appeal of this decision and requested a scheduling hearing with the NCC on September 5, 2023. Notwithstanding this appeal, we are moving forward with our primary case against ICON/PRA Netherlands. Our initial pleading document was filed July 26, 2023, and PRA filed their response on October 18, 2023. The hearing of this case is scheduled for December 7, 2023.

In addition to the foregoing, from time to time, we may be subject to various ongoing or threatened legal actions and proceedings, including those that arise in the ordinary course of business, which may include employment matters and breach of contract disputes. Such matters are subject to many uncertainties and to outcomes that are not predictable with assurance and that may not be known for extended periods of time. We are not currently engaged in or aware of any threatened legal actions which we believe could have a material adverse effect on our condensed consolidated result of operations or financial position.

|

ITEM 1A. |

RISK FACTORS |

Although Item 1A. is inapplicable to us as a smaller reporting company, we hereby disclose the following new risk factor in addition to those disclosed in our annual report on Form 10-K for the fiscal year ended December 31, 2022: