Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

Form 10-Q

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2017

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-36281

DICERNA PHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 20-5993609 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

87 Cambridgepark Drive

Cambridge, MA 02140

(Address of principal executive offices and zip code)

(617) 621-8097

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days) Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Table of Contents

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer |

☐ |

Accelerated filer |

☐ | |||

| Non-accelerated filer |

☐ (Do not check if a smaller reporting company) |

Smaller reporting company |

☒ | |||

| Emerging growth company |

☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes ☐ No ☒

As of August 9, 2017, there were 20,844,429 shares of the registrant’s common stock, par value $0.0001 per share, outstanding.

Table of Contents

INDEX TO FORM 10-Q

3

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements other than statements of historical fact are “forward-looking statements” for purposes of this Quarterly Report on Form 10-Q. In some cases, you can identify forward-looking statements by terminology such as “may,” “could,” “will,” “would,” “should,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “intend,” “predict,” “seek,” “contemplate,” “project,” “continue,” “potential,” “ongoing,” “goal,” or the negative of these terms or other comparable terminology. These forward-looking statements include, but are not limited to, statements about:

| • | how long we expect to maintain liquidity to fund our planned level of operations and our ability to obtain additional funds for our operations; |

| • | the initiation, timing, progress and results of our research and development programs, preclinical studies, any clinical trials and Investigational New Drug (“IND”) application, New Drug Application (“NDA”) and other regulatory submissions; |

| • | our ability to identify and develop product candidates for treatment of additional disease indications; |

| • | our or a collaborator’s ability to obtain and maintain regulatory approval of any of our product candidates; |

| • | the rate and degree of market acceptance of any approved product candidates; |

| • | the commercialization of any approved product candidates; |

| • | our ability to establish and maintain additional collaborations and retain commercial rights for our product candidates in the collaborations; |

| • | the implementation of our business model and strategic plans for our business, technologies and product candidates; |

| • | our estimates of our expenses, ongoing losses, future revenue and capital requirements; |

| • | our ability to obtain and maintain intellectual property protection for our technologies and product candidates and our ability to operate our business without infringing the intellectual property rights of others; |

| • | our reliance on third parties to conduct our preclinical studies or any future clinical trials; |

| • | our reliance on third party supply and manufacturing partners to supply the materials and components for, and manufacture, our research and development, preclinical and clinical trial drug supplies; |

| • | our ability to attract and retain qualified key management and technical personnel; |

| • | our dependence on our existing collaborator, Kyowa Hakko Kirin Co., Ltd. (“KHK”), for developing, obtaining regulatory approval for and commercializing product candidates in the collaboration; |

| • | our receipt and timing of any milestone payments or royalties under our research collaboration and license agreement with KHK or arrangement with any future collaborator; |

| • | our expectations regarding the time during which we will be an emerging growth company under the Jumpstart Our Business Startups Act; |

| • | our financial performance; and |

| • | developments relating to our competitors or our industry. |

These statements relate to future events or to our future financial performance and involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by these forward-looking statements. Factors that may cause actual results to differ materially from current expectations include, among other things, those set forth in Part II, Item 1A—“Risk Factors” below and for the reasons described elsewhere in this Quarterly Report on Form 10-Q. Any forward-looking statement in this Quarterly Report on Form 10-Q reflects our current view with respect to future events and is subject to these and other risks, uncertainties and assumptions relating to our operations, results of operations, industry and future growth. Given these uncertainties, you should not place undue reliance on these forward-looking statements. Except as required by law, we assume no obligation to update or revise these forward-looking statements for any reason, even if new information becomes available in the future.

4

Table of Contents

This Quarterly Report on Form 10-Q also contains estimates, projections and other information concerning our industry, our business and the markets for certain drugs, including data regarding the estimated size of those markets, their projected growth rates and the incidence of certain medical conditions. Information that is based on estimates, forecasts, projections or similar methodologies is inherently subject to uncertainties and actual events or circumstances may differ materially from events and circumstances reflected in this information. Unless otherwise expressly stated, we obtained these industry, business, market and other data from reports, research surveys, studies and similar data prepared by third parties, industry, medical and general publications, government data and similar sources. In some cases, we do not expressly refer to the sources from which these data are derived.

Except where the context otherwise requires, in this Quarterly Report on Form 10-Q, “we,” “us,” “our,” “Dicerna” and the “Company” refer to Dicerna Pharmaceuticals, Inc. and, where appropriate, its consolidated subsidiaries.

Trademarks

This Quarterly Report on Form 10-Q includes trademarks, service marks and trade names owned by us or by other companies. All trademarks, service marks and trade names included in this Quarterly Report on Form 10-Q are the property of their respective owners.

5

Table of Contents

Condensed Consolidated Balance Sheets

(Unaudited)

(In thousands, except share data and par value)

| June 30, 2017 |

December 31, 2016 |

|||||||

| ASSETS |

||||||||

| CURRENT ASSETS: |

||||||||

| Cash and cash equivalents |

$ | 38,777 | $ | 20,865 | ||||

| Held-to-maturity investments (Note 3) |

49,953 | 25,009 | ||||||

| Prepaid expenses and other current assets |

2,966 | 1,952 | ||||||

|

|

|

|

|

|||||

| Total current assets |

91,696 | 47,826 | ||||||

|

|

|

|

|

|||||

| NONCURRENT ASSETS: |

||||||||

| Property and equipment—net |

1,837 | 2,234 | ||||||

| Restricted cash equivalents |

1,116 | 1,116 | ||||||

| Other noncurrent assets |

74 | 76 | ||||||

|

|

|

|

|

|||||

| Total noncurrent assets |

3,027 | 3,426 | ||||||

|

|

|

|

|

|||||

| TOTAL ASSETS |

$ | 94,723 | $ | 51,252 | ||||

|

|

|

|

|

|||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY |

||||||||

| CURRENT LIABILITIES: |

||||||||

| Accounts payable |

$ | 4,129 | $ | 4,318 | ||||

| Accrued expenses and other current liabilities |

5,454 | 5,726 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

9,583 | 10,044 | ||||||

|

|

|

|

|

|||||

| TOTAL LIABILITIES |

9,583 | 10,044 | ||||||

|

|

|

|

|

|||||

| Commitments and contingencies (Note 6) |

||||||||

| Redeemable convertible preferred stock, $0.0001 par value—5,000,000 shares authorized; 718,404 and no shares issued and outstanding at June 30, 2017 and December 31, 2016, respectively (aggregate liquidation preference of $71,841 and $0 at June 30, 2017 and December 31, 2016, respectively) (Note 4) |

71,872 | — | ||||||

|

|

|

|

|

|||||

| STOCKHOLDERS’ EQUITY: |

||||||||

| Common stock, $0.0001 par value—150,000,000 shares authorized at June 30, 2017 and December 31, 2016; 20,794,427 shares and 20,753,001 shares issued and outstanding at June 30, 2017 and December 31, 2016, respectively |

2 | 2 | ||||||

| Additional paid-in capital |

298,448 | 296,962 | ||||||

| Accumulated deficit |

(285,182 | ) | (255,756 | ) | ||||

|

|

|

|

|

|||||

| Total stockholders’ equity |

13,268 | 41,208 | ||||||

|

|

|

|

|

|||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY |

$ | 94,723 | $ | 51,252 | ||||

|

|

|

|

|

|||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

6

Table of Contents

Condensed Consolidated Statements of Operations

(Unaudited)

(In thousands, except share and per share data)

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||||||

| Revenue |

$ | 252 | $ | — | $ | 385 | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating expenses: |

||||||||||||||||

| Research and development |

9,320 | 11,032 | 18,196 | 22,296 | ||||||||||||

| General and administrative |

6,300 | 4,656 | 11,796 | 9,140 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total operating expenses |

15,620 | 15,688 | 29,992 | 31,436 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Loss from operations |

(15,368 | ) | (15,688 | ) | (29,607 | ) | (31,436 | ) | ||||||||

| Interest income |

143 | 66 | 181 | 121 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss |

(15,225 | ) | (15,622 | ) | (29,426 | ) | (31,315 | ) | ||||||||

| Dividends on redeemable convertible preferred stock |

(2,622 | ) | — | (2,622 | ) | — | ||||||||||

| Deemed dividend related to beneficial conversion feature of redeemable convertible preferred stock |

(6,144 | ) | — | (6,144 | ) | — | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss attributable to common stockholders |

$ | (23,991 | ) | $ | (15,622 | ) | $ | (38,192 | ) | $ | (31,315 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss per share attributable to common stockholders—basic and diluted |

$ | (1.15 | ) | $ | (0.75 | ) | $ | (1.84 | ) | $ | (1.51 | ) | ||||

| Weighted average common shares outstanding—basic and diluted |

20,794,193 | 20,726,108 | 20,792,925 | 20,706,388 | ||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

7

Table of Contents

Condensed Consolidated Statements of Cash Flows

(Unaudited)

(In thousands)

| Six Months Ended June 30, | ||||||||

| 2017 | 2016 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: |

||||||||

| Net loss |

$ | (29,426 | ) | $ | (31,315 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: |

||||||||

| Stock-based compensation |

4,033 | 4,795 | ||||||

| Depreciation and amortization |

363 | 414 | ||||||

| Net amortization of premium/discount on investments |

(35 | ) | 64 | |||||

| Loss on disposal of property and equipment |

51 | — | ||||||

| Changes in operating assets and liabilities: |

||||||||

| Prepaid expenses and other assets |

(1,013 | ) | 53 | |||||

| Accounts payable |

(599 | ) | 580 | |||||

| Accrued expenses and other liabilities |

(276 | ) | (181 | ) | ||||

| Deferred rent |

4 | 48 | ||||||

|

|

|

|

|

|||||

| Net cash used in operating activities |

(26,898 | ) | (25,542 | ) | ||||

|

|

|

|

|

|||||

| CASH FLOWS FROM INVESTING ACTIVITIES: |

||||||||

| Purchases of property and equipment |

(58 | ) | (279 | ) | ||||

| Maturities of held-to-maturity investments |

25,000 | 18,500 | ||||||

| Purchases of held-to-maturity investments |

(49,908 | ) | (20,016 | ) | ||||

|

|

|

|

|

|||||

| Net cash used in investing activities |

(24,966 | ) | (1,795 | ) | ||||

|

|

|

|

|

|||||

| CASH FLOWS FROM FINANCING ACTIVITIES: |

||||||||

| Proceeds from issuance of redeemable convertible preferred stock, net of issuance costs |

70,000 | — | ||||||

| Redeemable convertible preferred stock issuance costs |

(300 | ) | — | |||||

| Proceeds from stock option exercises and issuances under employee stock purchase plan |

87 | 493 | ||||||

| Settlement of restricted stock for tax withholding |

(11 | ) | (27 | ) | ||||

|

|

|

|

|

|||||

| Net cash provided by financing activities |

69,776 | 466 | ||||||

|

|

|

|

|

|||||

| INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS |

17,912 | (26,871 | ) | |||||

| CASH AND CASH EQUIVALENTS — Beginning of period |

20,865 | 56,058 | ||||||

|

|

|

|

|

|||||

| CASH AND CASH EQUIVALENTS — End of period |

$ | 38,777 | $ | 29,187 | ||||

|

|

|

|

|

|||||

| SUPPLEMENTAL CASH FLOW INFORMATION: |

||||||||

| NONCASH FINANCING ACTIVITIES: |

||||||||

| Dividends on redeemable convertible preferred stock |

$ | 2,622 | $ | — | ||||

|

|

|

|

|

|||||

| Deemed dividend related to beneficial conversion feature of redeemable convertible preferred stock |

$ | 6,144 | $ | — | ||||

|

|

|

|

|

|||||

| Redeemable convertible preferred stock issuance costs included in accounts payable |

$ | 450 | $ | — | ||||

|

|

|

|

|

|||||

| NONCASH INVESTING ACTIVITIES: |

||||||||

| Property and equipment purchases included in accounts payable |

$ | — | $ | 29 | ||||

|

|

|

|

|

|||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

8

Table of Contents

Notes to Condensed Consolidated Financial Statements

(Unaudited)

(tabular amounts in thousands, except share and per share data and where otherwise noted)

1. Description of Business and Basis of Presentation

Business

Dicerna Pharmaceuticals, Inc. (the “Company”) is a biopharmaceutical company focused on the discovery and development of innovative subcutaneously delivered ribonucleic acid interference (“RNAi”)-based pharmaceuticals using its GalXCTM RNAi platform for the treatment of diseases involving the liver, including rare diseases, chronic liver diseases, cardiovascular diseases and viral infectious diseases.

Basis of presentation

These condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) and in accordance with the rules and regulations of the Securities and Exchange Commission (“SEC”) for interim financial information. Accordingly, these condensed consolidated financial statements do not include all of the information and notes required by GAAP to constitute a complete set of financial statements. These condensed consolidated financial statements have been prepared on the same basis as the Company’s annual consolidated financial statements and, in the opinion of management, reflect all adjustments, which include only normal recurring adjustments, necessary to present fairly the Company’s financial position at June 30, 2017 and results of operations and cash flows for the interim periods ended June 30, 2017 and 2016. These unaudited condensed consolidated interim financial statements should be read in conjunction with the Company’s audited consolidated financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2016, as amended. The results of the three and six months ended June 30, 2017 are not necessarily indicative of the results to be expected for the year ending December 31, 2017 or for any other interim period or for any other future year.

Significant judgments and estimates

The preparation of consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, and the disclosure of contingent assets and liabilities at the date of the consolidated financial statements, as well as the revenue and expenses incurred during the reporting periods. On an ongoing basis, the Company evaluates judgments and estimates, including those related to accrued expenses, stock-based compensation and in relation to the accounting for, including cumulative dividends on, the Redeemable Convertible Preferred, as defined below. The Company bases its estimates on historical experience and on various other factors that the Company believes are reasonable under the circumstances, the results of which form the basis for making judgments about the carrying value of assets and liabilities that are not apparent from other sources. Changes in estimates are reflected in reported results for the period in which they become known. Actual results could differ materially from those estimates.

Liquidity risk

Based on the Company’s current operating plan and liquidity, including the receipt of gross proceeds of $70.0 million from the issuance of the Company’s Redeemable Convertible Preferred, as defined below, on April 11, 2017 (see Note 4), management believes that available cash, cash equivalents and held-to-maturity investments will be sufficient to fund the Company’s planned level of operations for at least the 12-month period following August 10, 2017, which is the date that these condensed consolidated financial statements have been issued. Notwithstanding the availability of current liquidity, the Company’s ability to fund its planned preclinical and clinical operations, including completion of its planned clinical trials, will depend on its ability to raise additional capital through a combination of public or private equity offerings, debt financings, and research collaborations and license agreements. If the Company is unable to generate funding from one or more of these sources within a reasonable timeframe, it may have to delay, reduce or terminate its research and development programs, preclinical or clinical trials, limit strategic opportunities or undergo reductions in its workforce or other corporate restructuring activities.

Summary of Significant Accounting Policies — There have been no changes to the significant accounting policies disclosed in the Company’s most recent Annual Report on Form 10-K, as amended, except as required by recently adopted accounting pronouncements, as discussed below, and as related to the Redeemable Convertible Preferred, as defined below.

9

Table of Contents

Recent Accounting Pronouncements

Adopted in 2017

Stock-based compensation

In March 2016, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2016-09, Compensation—Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting (“ASU 2016-09”), which involves several aspects of the accounting for share-based payment transactions, including the income tax consequences, classification of awards as either equity or liabilities and classification in the statement of cash flows. Also under the new guidance, excess tax benefits and deficiencies are to be recognized as income tax expense or benefit in the income statement as discrete items in the reporting period in which they occur instead of an increase or decrease to stockholders’ equity. With regard to forfeitures, an entity may make an accounting policy election either to estimate the number of awards that are expected to vest or account for forfeitures when they occur. The Company adopted ASU 2016-09 on January 1, 2017, and as a result, it will track stock option deductions in its net operating loss deferred tax asset on a modified retrospective basis. In addition, the Company’s policy has been to estimate forfeitures as of the grant date. The Company will continue to maintain its policy to estimate forfeiture as of the grant date in the future. Since the Company historically has maintained a full valuation allowance on its net deferred tax asset, there is no net impact to the Company’s accumulated deficit or on its net loss per share attributable to common stockholders from the adoption of ASU 2016-09. As such, adoption of this guidance did not have any impact on the Company’s consolidated financial statements.

Not yet adopted

Revenue recognition

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers (Topic 606), which amends the guidance for accounting for revenue from contracts with customers, superseding the revenue recognition requirements in Accounting Standards Codification Topic 605, Revenue Recognition, and creates a new Topic 606, Revenue from Contracts with Customers (“Topic 606”). Topic 606 is effective for annual reporting periods beginning after December 15, 2017, with early adoption permitted. Per Topic 606, two adoption methods are allowed: retrospectively to all prior reporting periods presented, with certain practical expedients permitted, or retrospectively with the cumulative effect of initially adopting Topic 606 recognized at the date of initial application. The Company has not yet determined which adoption method will be utilized or the effect that adoption of Topic 606 may have on the Company’s consolidated financial statements. However, management has determined that income associated with the Company’s National Institutes of Health (“NIH”) grant does not meet the definition of revenue under Topic 606 and that, while there will be no cumulative effect on initial adoption of Topic 606 related to the Company’s grants, grant income will no longer be presented as revenue in the Company’s consolidated statement of operations.

Income taxes

In October 2016, the FASB issued ASU No. 2016-16, Accounting for Income Taxes: Intra-Entity Asset Transfers of Assets Other than Inventory (“ASU 2016-16”), which is part of the FASB’s simplification initiative aimed at reducing complexity in accounting standards. ASU 2016-16 eliminates the current exception that the tax effects of intra-entity asset transfers (intercompany sales) be deferred until the transferred asset is sold to a third party or otherwise recovered through use. Instead, the new guidance will require a reporting entity to recognize any tax expense from the sale of the asset in the seller’s tax jurisdiction when the transfer occurs, even though the pre-tax effects of that transaction are eliminated in consolidation. Any deferred tax asset that arises in the buyer’s jurisdiction would also be recognized at the time of the transfer. ASU 2016-16 will be effective for public business entities in fiscal years beginning after December 15, 2017, including interim periods within those years. Management is currently evaluating the potential impact that this guidance may have on the Company’s consolidated financial statements.

Leases

In February 2016, the FASB issued ASU No. 2016-02, Leases (Topic 842) (“ASU 2016-02”), which amends the existing accounting standards for lease accounting, including requiring lessees to recognize most leases on their balance sheets and making targeted changes to lessor accounting. ASU 2016-02 will be effective beginning in the first quarter of 2019, with early adoption permitted. ASU 2016-02 requires a modified retrospective transition approach for all leases existing at, or entered into after, the date of initial application, with an option to use certain transition relief. Management is currently evaluating the impact of adopting ASU 2016-02 on the Company’s consolidated financial statements.

10

Table of Contents

Statement of cash flows

In August 2016, the FASB issued ASU No. 2016-15, Statement of Cash Flows (Topic 230) (“ASU 2016-15”), a consensus of the FASB’s Emerging Issues Task Force (“EITF”). ASU 2016-15 is intended to reduce diversity in practice in how certain transactions are classified in the statement of cash flows and requires companies, among other matters, to use reasonable judgment to separate cash flows. Specifically, in the absence of specific guidance, ASU 2016-15 prescribes that an entity should classify each separately identifiable cash source and use on the basis of the nature of the underlying cash flows. ASU 2016-15 is effective for fiscal years beginning after December 15, 2017, and interim periods within those fiscal years. Management is currently evaluating the potential impact that this guidance may have on the Company’s consolidated financial statements.

In November 2016, the FASB issued ASU No. 2016-18, Statement of Cash Flows (Topic 230): Restricted Cash (“ASU 2016-18”), a consensus of the FASB’s EITF. ASU 2016-18 requires that the statement of cash flows explain the change during the period in the total of cash, cash equivalents and amounts generally described as restricted cash or restricted cash equivalents. Entities will also be required to reconcile such total to amounts on the balance sheet and disclose the nature of the restrictions. ASU 2016-18 is effective for financial statements issued for fiscal years beginning after December 15, 2017, and interim periods within those fiscal years. Management is currently evaluating the potential impact that this guidance may have on the Company’s consolidated financial statements.

Stock-based compensation

In May 2017, the FASB issued ASU No. 2017-09, Compensation—Stock Compensation (Topic 718): Scope of Modification Accounting (“ASU 2017-09”), which clarifies when to account for a change to the terms or conditions of a share-based payment award as a modification. Per ASU 2017-09, modification accounting is required only if the fair value, the vesting conditions, or the classification of the award (as equity or liability) changes as a result of the change in terms or conditions, whereas under previous guidance, judgments about whether certain changes to an award are substantive may impact whether or not modification accounting is applied in certain situations. ASU 2017-19 is effective prospectively for annual periods beginning on or after December 15, 2017, with early adoption permitted. Management is currently evaluating the potential impact that this guidance may have on the Company’s consolidated financial statements.

2. Net Loss per Share Attributable to Common Stockholders

The outstanding securities presented below were excluded from the calculation of net loss per share attributable to common stockholders, because such securities would have been anti-dilutive due to the Company’s net loss per share attributable to common stockholders during the periods ending on the dates presented.

| June 30, 2017 |

June 30, 2016 |

|||||||

| Options to purchase common stock |

6,212,437 | 4,888,522 | ||||||

| Warrants to purchase common stock |

87,901 | 87,901 | ||||||

| Unvested restricted common stock |

10,000 | 25,859 | ||||||

| Redeemable convertible preferred stock |

718,404 | — | ||||||

3. Held-to-maturity investments

The following tables provide information relating to the Company’s held-to-maturity investments:

| As of June 30, 2017: | Amortized Cost |

Gross Unrealized Gains |

Gross Unrealized Losses |

Fair Value |

||||||||||||

|

Held-to-maturity investments |

||||||||||||||||

| U.S. treasury securities maturing in one year or less |

$ | 49,953 | $ | — | $ | (22 | ) | $ | 49,931 | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

| As of December 31, 2016: | Amortized Cost |

Gross Unrealized Gains |

Gross Unrealized Losses |

Fair Value |

||||||||||||

|

Held-to-maturity investments |

||||||||||||||||

| U.S. treasury securities maturing in one year or less |

$ | 25,009 | $ | — | $ | (5 | ) | $ | 25,004 | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

11

Table of Contents

4. Redeemable Convertible Preferred Stock

On April 11, 2017, pursuant to a redeemable convertible preferred stock purchase agreement (“SPA”) with seven institutional investors (“Investors”), led by funds advised by Bain Capital Life Sciences L.P. (“Lead Investor”), the Company issued and sold in a private placement 700,000 shares of its newly designated Redeemable Convertible Preferred Stock, par value $0.0001 per share (“Redeemable Convertible Preferred”), at a purchase price of $100.00 per share, for total gross proceeds of $70.0 million (“Private Placement”), less issuance costs of $0.8 million. The shares of Redeemable Convertible Preferred and the shares of common stock issuable upon conversion of the Redeemable Convertible Preferred were offered and sold by the Company pursuant to an exemption from the registration requirements of the Securities Act provided by Section 4(a)(2) thereunder.

In addition to the Lead Investor, other participants in the Private Placement included Cormorant Asset Management, Domain Associates, EcoR1 Capital, RA Capital and Skyline Ventures, among others. Domain Associates, RA Capital and Skyline Ventures are entities that are affiliated or were formerly affiliated with certain members of the Company’s board of directors.

The Redeemable Convertible Preferred has the rights and preferences set forth in a Certificate of Designation, which was filed with the Secretary of State of the State of Delaware. Those rights and preferences are summarized below.

Conversion

The Company has the right to require the Investors to convert the Redeemable Convertible Preferred into common stock at any time following the earlier of the second anniversary of the closing of the Private Placement or the occurrence of certain agreed-upon milestone events, provided, that, in each case, the trading price of the Company’s common stock exceeds 200% of $3.19 (the “Conversion Price”) for 45 out of 60 consecutive trading days. The Company’s ability to require conversion shall be subject to (i) a 19.99% blocker provision to comply with NASDAQ Listing Rules (“19.99% Conversion Blocker”), (ii) for certain Investors, a 9.99% blocker provision (“9.99% Conversion Blocker”) that will prohibit beneficial ownership of more than 9.99% of the outstanding shares of the Company’s common stock or voting power at any time, or (iii) applicable regulatory restrictions. The 19.99% Conversion Blocker and the 9.99% Conversion Blocker are hereinafter referred to as the “Conversion Blockers.” The Conversion Price is subject to proportionate adjustment for any stock split, stock dividend, combination or other similar recapitalization event.

At any time and from time to time at their election, the holders of Redeemable Convertible Preferred will have the option to convert the Redeemable Convertible Preferred into shares of the Company’s common stock by dividing (i) the sum of the Accrued Value plus an amount equal to all accrued or declared and unpaid dividends on the Redeemable Convertible Preferred that have not previously been added to the Accrued Value by (ii) the Conversion Price in effect at the time of such conversion. The conversion of shares of Redeemable Convertible Preferred into shares of common stock is subject to the Conversion Blockers. “Accrued Value” means, with respect to each share of Redeemable Convertible Preferred, the sum of (i) $100.00 plus (ii) on each quarterly dividend date, an additional amount equal to the dollar value of any dividends on a share of Redeemable Convertible Preferred which have accrued on any dividend payment date and have not previously been added to such Accrued Value.

Redemption

On or at any time following the seventh anniversary of the closing of the Private Placement, (i) the Company shall have the right to redeem the Redeemable Convertible Preferred for a cash consideration equal to the sum of the Accrued Value, as of the date of redemption, plus an amount equal to all accrued or declared and unpaid dividends on the Redeemable Convertible Preferred that have not previously been added to the Accrued Value, and (ii) the holders of a majority of the Redeemable Convertible Preferred shall also have the right to cause the Company to redeem the Redeemable Convertible Preferred at the same price.

Upon consummation of a specified change of control transaction, each holder of Redeemable Convertible Preferred will be entitled to receive in preference to the holders of common stock and any junior preferred stock, an amount equal to the greater of (i) 101% of the sum of the Accrued Value plus an amount equal to all accrued or declared and unpaid dividends on the Redeemable Convertible Preferred that have not previously been added to the Accrued Value, or (ii) the amount that such shares would have been entitled to receive if they had converted into common stock immediately prior to such event.

Liquidation preferences

In the event of the Company’s liquidation, dissolution or winding up, the holder of each share of Redeemable Convertible Preferred will be entitled to receive, in preference to the holders of the common stock and any junior preferred stock, an amount per share equal to the greater of (i) the sum of the Accrued Value plus an amount equal to all accrued or declared and unpaid dividends on the

12

Table of Contents

Redeemable Convertible Preferred that have not previously been added to the Accrued Value, or (ii) the amount that such shares would have been entitled to receive if they had converted into common stock immediately prior to such liquidation, dissolution or winding up.

Voting and other rights

Except as set forth above or as otherwise required by law, holders of shares of Redeemable Convertible Preferred are entitled to vote together with shares of common stock (based on one vote per share of common stock into which the shares of Redeemable Convertible Preferred are convertible on the applicable record date) on any matter on which the holders of common stock are entitled to vote.

Additionally, for so long as any shares of Redeemable Convertible Preferred remain outstanding, without the approval of holders of a majority of the Redeemable Convertible Preferred, the Company may not, among other things, (i) amend, modify or fail to give effect to any right of holders of the Redeemable Convertible Preferred, (ii) change the authorized number of Redeemable Convertible Preferred or issue additional Redeemable Convertible Preferred or create a new class or series of equity securities or securities convertible into equity securities with equal or superior rights, preferences or privileges to those of the Redeemable Convertible Preferred in terms of liquidation preference, dividend rights or certain governance rights, (iii) issue shares of common stock or securities convertible into common stock while the Company has insufficient shares to effect the conversion of the Redeemable Convertible Preferred into common stock, (iv) declare or pay dividends or redeem or repurchase any capital stock (other than certain repurchases from employees, directors, advisors or consultants upon termination of service) or (v) incur certain indebtedness in excess of $10 million.

On March 28, 2017, in accordance with the terms of the SPA, the Company increased the size of its board of directors from eight to nine directors and approved the appointment of Adam M. Koppel, M.D., Ph.D., a managing director of the Lead Investor, as a director of the Company, effective as of the closing of the Private Placement on April 11, 2017. To the extent that such director is not re-elected at any time and, so long as the Lead Investor owns at least 25% of the Redeemable Convertible Preferred (or underlying common stock) owned by it at the closing of the Private Placement, the Lead Investor shall have the right to designate a board observer.

The Company also entered into an amended and restated registration rights agreement, by and among the Company and the Investors (“Registration Rights Agreement”). Pursuant to the Registration Rights Agreement, the Investors will be entitled to certain demand, shelf and “piggyback” registration rights with respect to the shares of common stock issuable upon conversion of the Redeemable Convertible Preferred, subject to the limitations set forth in the Registration Rights Agreement.

Dividends

Each holder of Redeemable Convertible Preferred is entitled to receive cumulative dividends on the Accrued Value of each share of Redeemable Convertible Preferred at an initial rate of 12% per annum, compounded quarterly and subject to two rate reductions, of 4% each, upon the occurrence of certain agreed-upon milestone events. Dividends on the Redeemable Convertible Preferred are payable in kind and will accrue on the Accrued Value of each share of Redeemable Convertible Preferred until the earlier of conversion, redemption, consummation of a change of control, a liquidation event, or upon failure to mandatorily convert due to the Conversion Blockers or applicable regulatory restrictions.

For accounting purposes, in accordance with the FASB’s Accounting Standard Codification (“ASC”) Topic 480-10-S99, Distinguishing Liabilities from Equity—SEC Materials (“ASC 480-10-S99”), the Company records the additional shares issued as dividends at fair value at each declaration date. The fair value of the dividends is determined using a binary lattice model that captures the intrinsic value of the underlying common stock on the declaration date and the option value of the shares and future dividends. On June 30, 2017, the Company issued an aggregate of 18,404 additional shares of Redeemable Convertible Preferred as payment in kind of cumulative dividends. These dividends were charged against additional paid-in capital and increased the carrying value of the Redeemable Convertible Preferred as of June 30, 2017.

The lattice model used to determine fair value used an adjusted risk rate of 18.0%, a 6.75-year volatility of 70.0%, the underlying common stock price on the dividend date and other assumptions, including probability simulations of various outcomes largely associated with the conversion-related milestone events referred to below and with the progression of the Company’s per common share price. Use of the lattice model resulted in a fair value estimate of the dividends declared during the three months ended June 30, 2017 of approximately $1.87 million, or approximately $0.03 million above the increase in the liquidation preference amounts of the Redeemable Convertible Preferred.

13

Table of Contents

Classification and measurement

At the date of issuance, the Redeemable Convertible Preferred was classified as temporary equity in the mezzanine section of the Company’s consolidated balance sheet, since the underlying preferred shares are subject to redemption upon the occurrence of uncertain events not solely within the Company’s control, pursuant to ASC 480-10-S99. As of June 30, 2017, the Redeemable Convertible Preferred was not currently redeemable, and management concluded that it is not probable that the Redeemable Convertible Preferred will become redeemable, primarily due to the existence of the conversion right held by the Company, as discussed above.

In accordance with ASC Topic 470-20, Debt with Conversion and Other Options, the Company recorded a beneficial conversion feature (“BCF”) related to the issuance of the Redeemable Convertible Preferred. The BCF was recognized separately at issuance by allocating a portion of the proceeds equal to the intrinsic value of that feature to additional paid-in capital. The BCF was calculated at the commitment date, which management has determined to be the date of issuance. Intrinsic value is the difference between the conversion price and the fair value of the Company’s common stock into which the Redeemable Convertible Preferred is convertible, multiplied by the number of shares into which the issued shares of Redeemable Convertible Preferred are convertible. The Company recorded a deemed dividend charge of $6.1 million to reflect full and immediate accretion of the discount resulting from the BCF embedded within the Redeemable Convertible Preferred as a result of the shares being immediately convertible into shares of the Company’s common stock at the option of the Investors. Additionally, during the three months ended June 30, 2017, and as noted above, the Company recorded Redeemable Convertible Preferred dividends of $2.6 million. Accretion of the discount resulting from the BCF and cumulative dividends, including accretion of share issuance costs, were non-cash transactions and have been reflected below net loss to arrive at net loss attributable to common stockholders.

The following table reflects the changes in Redeemable Convertible Preferred.

| Balance at January 1, 2017 |

$ | — | ||

| Issuance of Redeemable Convertible Preferred |

70,000 | |||

| Share issuance costs |

(750 | ) | ||

|

|

|

|||

| Net proceeds |

69,250 | |||

| Discount resulting from the BCF at issuance |

(6,144 | ) | ||

| Accretion of the discount resulting from the BCF (deemed dividend) |

6,144 | |||

| Dividends accrued at the stated rate |

1,841 | |||

| Accretion of share issuance costs (additional dividends) |

750 | |||

|

|

|

|||

| Liquidation preference |

71,841 | |||

| Fair value in excess of dividends accrued at the stated rate |

31 | |||

|

|

|

|||

| Balance at June 30, 2017 |

$ | 71,872 | ||

|

|

|

No shares of Redeemable Convertible Preferred were converted since the original issuance thereof through June 30, 2017. As of June 30, 2017, 42,774,585 shares of common stock were issuable assuming full conversion of all outstanding shares of the Redeemable Convertible Preferred, representing approximately 71% ownership of the Company by the Investors on an as-converted basis and after application of the Conversion Blockers.

5. Stock Option Plan and Stock-Based Compensation

During the three and six month periods ended June 30, 2017, the Company granted stock options to purchase 352,500 and 1,330,997 shares of common stock to employees with aggregate grant date fair values of $0.7 million and $2.7 million, respectively, compared to stock options to purchase 517,500 and 1,445,275 shares of common stock granted to employees with aggregate grant date fair values of $1.6 million and $6.8 million, for the comparable three and six month periods in 2016.

The assumptions used to estimate the grant date fair value using the Black-Scholes option pricing model were as follows:

| Three Months Ended June 30, 2017 |

Six Months Ended June 30, 2017 | |||

| Stock price |

$2.91 – $3.47 | $2.49 – $3.47 | ||

| Expected option term (in years) |

5.50 – 6.25 | 5.50 – 6.25 | ||

| Expected volatility |

79.7% – 80.8% | 79.4% – 80.8% | ||

| Risk-free interest rate |

1.86% – 1.89% | 1.86% – 2.07% | ||

| Expected dividend yield |

0.00% | 0.00% |

14

Table of Contents

| Three Months Ended June 30, 2016 |

Six Months Ended June 30, 2016 | |||

| Stock price |

$3.26 – $5.55 | $3.26 – $9.09 | ||

| Expected option term (in years) |

5.50 – 6.25 | 5.50 – 6.25 | ||

| Expected volatility |

75.1% – 75.3% | 70.9% – 75.3% | ||

| Risk-free interest rate |

1.20% – 1.46% | 1.20% – 1.71% | ||

| Expected dividend yield |

0.00% | 0.00% |

The Company has classified stock-based compensation in its condensed consolidated statements of operations as follows:

| Three June 30, |

Six June 30, |

Three June 30, |

Six June 30, |

|||||||||||||

| 2017 | 2017 | 2016 | 2016 | |||||||||||||

| Research and development expenses |

$ | 972 | $ | 1,917 | $ | 1,126 | $ | 2,301 | ||||||||

| General and administrative expenses |

1,053 | 2,116 | 1,284 | 2,494 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 2,025 | $ | 4,033 | $ | 2,410 | $ | 4,795 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

5. Fair Value Measurements

A summary of the Company’s assets that are measured or disclosed at fair value as of June 30, 2017 and December 31, 2016 are presented below:

| Description |

At June 30, 2017 |

Level 1 | Level 2 | Level 3 | ||||||||||||

| Cash equivalents |

||||||||||||||||

| Money market fund |

$ | 26,040 | $ | 26,040 | $ | — | $ | — | ||||||||

| Held-to-maturity investments |

||||||||||||||||

| U.S. treasury securities |

49,931 | — | 49,931 | — | ||||||||||||

| Restricted cash equivalents |

||||||||||||||||

| Money market fund |

1,116 | — | 1,116 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 77,087 | $ | 26,040 | $ | 51,047 | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Description |

At December 31, 2016 |

Level 1 | Level 2 | Level 3 | ||||||||||||

| Cash equivalents |

||||||||||||||||

| Money market fund |

$ | 12,853 | $ | 12,853 | $ | — | $ | — | ||||||||

| Held-to-maturity investments |

||||||||||||||||

| U.S. treasury securities |

25,004 | — | 25,004 | — | ||||||||||||

| Restricted cash equivalents |

||||||||||||||||

| Money market fund |

1,116 | — | 1,116 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 38,973 | $ | 12,853 | $ | 26,120 | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The Company’s cash equivalents, which are in money market funds, are classified within Level 1 of the fair value hierarchy because they are valued using quoted prices as of June 30, 2017 and December 31, 2016.

The Company’s restricted cash equivalents bore interest at the prevailing market rates for instruments with similar characteristics and, accordingly, the carrying value of these instruments also approximated their fair value. These financial instruments were classified within Level 2 of the fair value hierarchy, because the inputs to the fair value measurement are valued using observable inputs as of June 30, 2017 and December 31, 2016.

The Company’s held-to-maturity investments bore interest at the prevailing market rates for instruments with similar characteristics. The financial instruments were classified within Level 2 of the fair value hierarchy, because the inputs to the fair value measurement are valued using observable inputs as of June 30, 2017 and December 31, 2016.

15

Table of Contents

As of June 30, 2017 and December 31, 2016, the carrying amounts of accounts payable and accrued expenses approximated their estimated fair values because of the short-term nature of these financial instruments.

For the three and six month periods ended June 30, 2017 and 2016 there were no transfers between Level 1 and Level 2.

6. Commitments and Contingencies

Facility lease

Future minimum lease payments on the Company’s non-cancelable operating lease for office and laboratory space are as follows:

| 12-Month Periods Ending June 30, |

Operating Lease |

|||

| 2018 |

$ | 1,606 | ||

| 2019 |

1,654 | |||

| 2020 |

1,703 | |||

| 2021* |

718 | |||

|

|

|

|||

| Total |

$ | 5,681 | ||

|

|

|

|||

| * | The end of the lease term is November 30, 2020. |

Litigation

On June 10, 2015, Alnylam Pharmaceuticals, Inc. (“Alnylam”) filed a complaint against the Company in the Superior Court of Middlesex County, Massachusetts (the “Court”). The complaint alleges misappropriation of confidential, proprietary, and trade secret information, as well as other related claims, in connection with the Company’s hiring of a number of former employees of Merck & Co., Inc. (“Merck”) and its discussions with Merck regarding the acquisition of its subsidiary, Sirna Therapeutics, Inc., which was subsequently acquired by Alnylam. The complaint seeks among other things, unspecified damages, attorneys’ fees, and an order permanently enjoining the Company from disclosing or using any of Alnylam’s confidential information or trade secrets. The Court has set a trial date of April 23, 2018.

The Company believes that these allegations lack merit, has filed an answer denying all liability and intends to continue to vigorously defend all claims asserted. At this time, the Company has not recorded a liability in connection with these matters because management believes that any potential loss is neither probable nor reasonably estimable.

From time to time, the Company may be subject to various claims and legal proceedings. If the potential loss from any claim, asserted or unasserted, or legal proceeding is considered probable and the amount is reasonably estimable, the Company will accrue a liability for the estimated loss. There were no litigation liabilities recorded as of June 30, 2017 or December 31, 2016.

******

16

Table of Contents

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following discussion contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those discussed here. Factors that could cause or contribute to such differences include, but are not limited to, those discussed in this section as well as factors described in Part II, Item 1A—“Risk Factors.”

Overview

Founded in 2006 as a Delaware corporation, we are a biopharmaceutical company focused on the discovery and development of innovative subcutaneously delivered ribonucleic acid RNAi-based pharmaceuticals using our GalXCTM RNAi platform for the treatment of diseases involving the liver, including rare diseases, chronic liver diseases, cardiovascular diseases and viral infectious diseases. Within these therapeutic areas, we believe our GalXC RNAi platform will allow us to build a broad pipeline with commercially attractive pharmaceutical properties, including a subcutaneous route of administration, infrequent dosing (e.g., dosing that is monthly or quarterly, and potentially even less frequent), high therapeutic index, and specificity to a single target gene.

All of our GalXC drug discovery and development efforts are based on the therapeutic modality of RNAi, a highly potent and specific mechanism for silencing the activity of a targeted gene. In this naturally occurring biological process, double-stranded RNA molecules induce the enzymatic destruction of the messenger RNA (“mRNA”) of a target gene that contains sequences that are complementary to one strand of the therapeutic double-stranded RNA molecule. The Company’s approach is to design proprietary double-stranded RNA molecules that have the potential to engage the enzyme Dicer and initiate an RNAi process to silence a specific target gene. These proprietary molecules are generally referred to as Dicer Substrate short-interfering RNAs (“DsiRNAs”). Our GalXC RNAi platform utilizes a particular Dicer Substrate structure configured for subcutaneous delivery to the liver. Due to the enzymatic nature of RNAi, a single GalXC molecule incorporated into the RNAi machinery can destroy hundreds or thousands of mRNAs from the targeted gene.

The GalXC RNAi platform supports Dicerna’s long-term strategy to retain, subject to the evaluation of potential licensing opportunities as they may arise, a full or substantial ownership stake and to invest internally in diseases with focused patient populations, such as certain rare diseases. We see such diseases as representing opportunities that carry high probabilities of success, with easily identifiable patient populations and a limited number of Centers of Excellence to facilitate reaching these patients, and the potential for more rapid clinical development programs. For more complex diseases with multiple gene dysfunctions and larger patient populations, we plan to pursue collaborations that can provide the enhanced scale, resources and commercial infrastructure required to maximize these prospects.

Development Programs

In choosing which development programs to advance, we apply scientific, clinical, and commercial criteria that we believe allow us to best leverage our GalXC RNAi platform and maximize value. The Company is focusing its efforts on four therapeutic programs: DCR-PHXC for the treatment of primary hyperoxaluria (“PH”); a program against an undisclosed rare disease; DCR-HBVS for the treatment of chronic hepatitis B virus (“HBV”) infection; and DCR-PCSK9 for the treatment of hypercholesterolemia. The Company’s goal is to advance five programs into the clinic by the end of 2019. We plan to file a Clinical Trial Application (“CTA”) for our lead GalXC product candidate, DCR-PHXC, at the end of 2017, followed by additional IND applications in 2018 and 2019.

17

Table of Contents

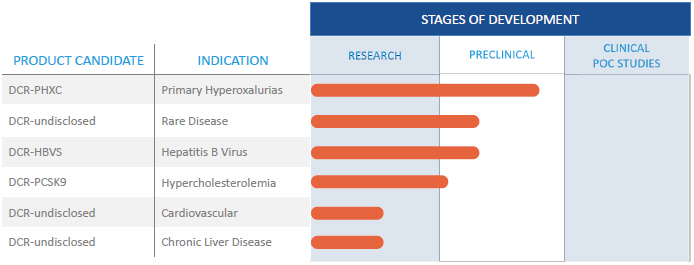

The table below sets forth the state of development of our various product candidates as of August 9, 2017.

Our current development programs are as follows:

| • | Primary Hyperoxaluria. We are developing DCR-PHXC for the treatment of all types of PH. PH is a family of rare inborn errors of metabolism in which the liver produces excessive levels of oxalate, which in turn causes damage to the kidneys and to other tissues in the body. In preclinical models of PH, DCR-PHXC reduces oxalate production to near-normal levels, ameliorating the disease condition. DCR-PHXC is in preclinical development and has advanced into IND application-enabling studies. We plan to file a CTA for DCR-PHXC in late 2017 and commence human clinical trials in the first quarter of 2018. |

On July 15, 2017, in a series of presentations at the 12th International Workshop on Primary Hyperoxaluria for Professionals, Patients and Families in Tenerife, Spain (“12th International Workshop”), we presented new preclinical data suggesting the potential utility of DCR-PHXC for treating all forms of PH. In particular, we presented research from animal models demonstrating how DCR-PHXC inhibits the lactate dehydrogenase A (“LDHA”) gene, which we have identified as potentially being an optimal therapeutic target in patients with PH. LDHA inhibition was shown in animal models to reduce oxalate to normal or near-normal levels in PH types 1, 2 and ethylene glycol-induced hyperoxaluria (a model for idiopathic PH).

LDHA reduction has a near-linear correlation with oxalate reduction and offers a minimal metabolic intervention. These benefits of LDHA inhibition may translate into consistent therapeutic activity even in the event of a missed dose. There are numerous case reports of LDHA deficiency naturally occurring in humans, with no reported adverse effects due to deficiency in the liver.

To facilitate DCR-PHXC development, we continue to advance our Primary HYperoxaluria Observational Study (“PHYOS”), an international, multicenter, observational study in patients with a genetically confirmed diagnosis of PH, type 1 (“PH1”). PHYOS is collecting data on key biochemical parameters implicated in the pathogenesis of PH1. We hope to use the data to better understand the baseline PH1 disease state, which will help guide long-term drug development plans. At the 12th International Workshop, we also reported data from 20 enrolled patients with a median age at screening of 21 years (range 12-61 years). The patients had been diagnosed at a median age of 7 years (range 1-59 years), and 14 patients (74%) had a medical history of renal stones. Over the six-month observation period, the variability (coefficient of variation) between 24-hour urine measurements of oxalate at different time points was 28%. These data will help our clinical team design future clinical studies using 24-hour urinary oxalate excretion as a surrogate marker for clinical benefit.

| • | An undisclosed rare disease involving the liver. We are developing a GalXC-based therapeutic, targeting a liver-expressed gene involved in a serious rare disease. For competitive reasons, we have not yet publicly disclosed the target gene or disease. We have selected this target gene and disease based on criteria that include having a strong therapeutic hypothesis, a readily-identifiable patient population, the availability of a potentially predictive biomarker, high unmet medical need, favorable competitive positioning, and what we believe is a rapid projected path to approval. We plan to file an IND application and/or CTA for this program in the second quarter of 2018. |

18

Table of Contents

| • | Chronic Hepatitis B Virus infection: We have recently initiated formal IND application-enabling work on DCR-HBVS, which targets HBV directly. We are using our GalXC RNAi platform to investigate potential pharmaceutical treatments for HBV. Current therapies for HBV rarely lead to a long-term immunological cure as measured by the clearance of HBV surface antigen (“HBsAg”) and sustained HBV deoxyribonucleic acid (“DNA”) suppression. Based on preclinical studies, we are evaluating whether our GalXC RNAi platform can produce an experimental HBV-targeted therapy that profoundly reduces HBsAg expression in HBV patients and that has the potential to be delivered in a commercially attractive subcutaneous dosing paradigm. We expect to file an IND application or a CTA at approximately the end of 2018. |

| • | Hypercholesterolemia (PCSK9 targeted therapy). We are using our GalXC RNAi platform to develop a therapeutic that targets the PCSK9 gene for the treatment of hypercholesterolemia. Based on the Company’s candidate development work during the fourth quarter of 2016, Dicerna is positioned to advance DCR-PCSK9, which targets the PCSK9 gene and will be evaluated for the treatment of statin-refractory patients with hypercholesterolemia, into formal preclinical development. PCSK9 is a validated target for hypercholesterolemia, and there are FDA-approved therapies targeting PCSK9 that are based on monoclonal antibody technology. Based on preclinical studies, we believe that our GalXC RNAi platform has the potential to produce a PCSK9-targeted therapy with attractive commercial properties, such as small subcutaneous injection volumes and less frequent dosing. |

In addition to our GalXC development programs, we have partnered an early generation of Dicer Substrate RNAi technology, non-GalXC technology, against two targets, the KRAS oncogene and an additional undisclosed gene, with the global pharmaceutical company, KHK, to use for development in oncology and formulated using KHK’s proprietary drug delivery system. KHK is responsible for global development of the KRAS program, including all development expenses. For the KRAS product candidate, we retain an option to co-promote in the U.S. for an equal share of the profits from U.S. net sales. We are also developing, with KHK, a therapeutic candidate targeting a second cancer-related gene, which we are not identifying at this time. For each product candidate in our collaboration with KHK, we have the potential to receive clinical, regulatory and commercialization milestone payments of up to $110.0 million and royalties on net sales of each such product candidate. KHK is responsible for all preclinical and clinical development activities, including the selection of patient population and disease indications for clinical trials. According to information received from KHK, both product candidates are in preclinical development.

We also have developed a wholly owned clinical candidate, DCR-BCAT, targeting the b-catenin oncogene. DCR-BCAT is based on an extended version of our earlier generation Dicer Substrate RNAi technology and is delivered by our LNP tumor delivery system, EnCoreTM. We plan to out-license or spin out the DCR-BCAT opportunity, given our focus on our GalXC platform-based programs.

Redeemable Convertible Preferred Stock

On April 11, 2017, we issued and sold 700,000 shares of our newly designated Redeemable Convertible Preferred to the Investors in a Private Placement for aggregate gross proceeds of $70.0 million, less issuance costs of $0.8 million. In addition to the Lead Investor, other participants in the Private Placement included Cormorant Asset Management, Domain Associates, EcoR1 Capital, RA Capital and Skyline Ventures, among others. Domain Associates, RA Capital and Skyline Ventures are entities that are affiliated or were formerly affiliated with certain members of our board of directors.

We have the right to require the Investors to convert the Redeemable Convertible Preferred into common stock (“Mandatory Conversion”) at any time following the earlier of (i) the second anniversary of the closing of the Private Placement or (ii) the occurrence of both of the following: (a) (1) the date that we first administer, after the issue date, a dose of a pharmaceutical product candidate (which such product candidate shall be one of the following candidates, or a variation thereof: DCR-PHXC, DCR-PCSK9 or the undisclosed rare disease program currently in pre-clinical development (each, a Product Candidate)) to a human being pursuant to an IND application filed by us with the FDA; or (2) after we have first administered, after the issue date, a dose of a Product Candidate to a human being pursuant to a clinical trial authorization with the Medicine and Healthcare Products Regulatory Agency in the EU and an IND application relating to such Product Candidate has become effective; and (b) the date we enter into a partnership or license agreement with a major company in the pharmaceutical or biotechnology industry relating to a non-Product Candidate, pursuant to which such company provides us with an up-front cash payment of a minimum amount agreed upon by us and the Lead Investor and agrees to customary future milestone and royalty payments, provided, that, in each case ((i) and (ii)), the trading price of our common stock exceeds 200% of the Conversion Price, as defined below, for 45 out of 60 consecutive trading days. Our ability to require conversion shall be subject to the Conversion Blockers and applicable regulatory restrictions. “Conversion Price” shall mean an initial price of $3.19 per share, subject to proportionate adjustment for any stock split, stock dividend, combination or other similar recapitalization event.

19

Table of Contents

Following the date of a Mandatory Conversion, any shares of Redeemable Convertible Preferred that are not converted as a result of the Conversion Blockers or applicable regulatory restrictions shall continue to be entitled to all of the rights of the holders of Redeemable Convertible Preferred except that they will no longer be entitled to further accrual of dividends, priority distribution of assets upon consummation of a change of control or a liquidation event and certain special voting provisions.

On or at any time following the seventh anniversary of the closing of the Private Placement, (i) we shall also have the right to redeem the Redeemable Convertible Preferred for a cash consideration equal to the sum of the Accrued Value, as of the date of redemption, plus an amount equal to all accrued or declared and unpaid dividends on the Redeemable Convertible Preferred that have not previously been added to the Accrued Value, and (ii) the holders of a majority of the Redeemable Convertible Preferred shall also have the right to cause us to redeem the Redeemable Convertible Preferred at the same price. “Accrued Value” means, with respect to each share of Redeemable Convertible Preferred, the sum of (i) $100.00 plus (ii) on each quarterly dividend date, an additional amount equal to the dollar value of any dividends on a share of Redeemable Convertible Preferred which have accrued on any dividend payment date and have not previously been added to such Accrued Value.

At any time and from time to time at their election, the holders of Redeemable Convertible Preferred will have the option to convert the Redeemable Convertible Preferred into shares of our common stock by dividing (i) the sum of the Accrued Value plus an amount equal to all accrued or declared and unpaid dividends on the Redeemable Convertible Preferred that have not previously been added to the Accrued Value by (ii) the Conversion Price in effect at the time of such conversion. The conversion of shares of Redeemable Convertible Preferred into shares of common stock is subject to the Conversion Blockers.

In the event of our liquidation, dissolution or winding up, the holder of each share of Redeemable Convertible Preferred will be entitled to receive, in preference to the holders of the common stock and any junior preferred stock, an amount per share equal to the greater of (i) the sum of the Accrued Value plus an amount equal to all accrued or declared and unpaid dividends on the Redeemable Convertible Preferred that have not previously been added to the Accrued Value, or (ii) the amount that such shares would have been entitled to receive if they had converted into common stock immediately prior to such liquidation, dissolution or winding up.

Upon consummation of a specified change of control transaction, each holder of Redeemable Convertible Preferred will be entitled to receive in preference to the holders of common stock and any junior preferred stock, an amount equal to the greater of (i) 101% of the sum of the Accrued Value plus an amount equal to all accrued or declared and unpaid dividends on the Redeemable Convertible Preferred that have not previously been added to the Accrued Value, or (ii) the amount that such shares would have been entitled to receive if they had converted into common stock immediately prior to such event.

In addition, for so long as any shares of Redeemable Convertible Preferred remain outstanding, without the approval of holders of a majority of the Redeemable Convertible Preferred, we may not, among other things, (i) amend, modify or fail to give effect to any right of holders of the Redeemable Convertible Preferred, (ii) change the authorized number of Redeemable Convertible Preferred or issue additional Redeemable Convertible Preferred or create a new class or series of equity securities or securities convertible into equity securities with equal or superior rights, preferences or privileges to those of the Redeemable Convertible Preferred in terms of liquidation preference, dividend rights or certain governance rights, (iii) issue shares of common stock or securities convertible into common stock while we have insufficient shares to effect the conversion of the Redeemable Convertible Preferred into common stock, (iv) declare or pay dividends or redeem or repurchase any capital stock (other than certain repurchases from employees, directors, advisors or consultants upon termination of service) or (v) incur certain indebtedness in excess of $10 million. Except as set forth above or as otherwise required by law, holders of shares of Redeemable Convertible Preferred are entitled to vote together with shares of common stock (based on one vote per share of common stock into which the shares of Redeemable Convertible Preferred are convertible on the applicable record date) on any matter on which the holders of common stock are entitled to vote.

Per the Certificate of Designation, each holder of Redeemable Convertible Preferred is entitled to receive cumulative dividends on the Accrued Value of each share of Redeemable Convertible Preferred at an initial rate of 12% per annum, compounded quarterly and subject to two rate reductions, of 4% each, upon the occurrence of certain agreed-upon milestone events. Dividends on the Redeemable Convertible Preferred are payable in kind and will accrue on the Accrued Value of each share of Redeemable Convertible Preferred until the earlier of conversion, redemption, consummation of a change of control, a liquidation event, or upon failure to mandatorily convert due to the Conversion Blockers or applicable regulatory restrictions.

In accordance with the terms of the SPA, on March 28, 2017, our board of directors voted to increase the size of the board from eight directors to nine directors and approved the appointment of Adam M. Koppel, M.D., Ph.D., a managing director of the Lead Investor, as a director of our Company, effective as of the closing of the Private Placement on April 11, 2017, to fill the resulting vacancy. To the extent such director is not re-elected at any time and, so long as the Lead Investor owns at least 25% of the Redeemable Convertible Preferred (or underlying common stock) owned by it at the closing of the Private Placement, it shall have the right to designate a board observer. On June 30, 2017, the Lead Investor, which appointed one of its managing directors to our board of directors, owned approximately 19% of the Company on an as-converted basis and after application of the Conversion Blockers.

20

Table of Contents

We also entered into a Registration Rights Agreement, by and among us and the Investors. Pursuant to the Registration Rights Agreement, the Investors will be entitled to certain demand, shelf and “piggyback” registration rights with respect to the shares of common stock issuable upon conversion of the Redeemable Convertible Preferred, subject to the limitations set forth in the Registration Rights Agreement.

The shares of Redeemable Convertible Preferred and the shares of common stock issuable upon conversion of the Redeemable Convertible Preferred were offered and sold by us pursuant to an exemption from the registration requirements of the Securities Act provided by Section 4(a)(2) thereunder.

Critical Accounting Policies and Significant Judgments and Estimates

Our management’s discussion and analysis of financial condition and results of operations is based on our consolidated financial statements, which have been prepared in accordance with GAAP. The preparation of our consolidated financial statements requires us to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the consolidated financial statements, as well as the revenue and expenses incurred during the reported periods. On an ongoing basis, we evaluate our estimates and judgments, including those related to accrued expenses and stock-based compensation and in relation to the accounting for the Redeemable Convertible Preferred, including cumulative dividends thereon. We base our estimates on historical experience and on various other factors that we believe are reasonable under the circumstances, the results of which form the basis for making judgments about the carrying value of assets and liabilities that are not apparent from other sources. Changes in estimates are reflected in reported results for the period in which they become known. Actual results may differ from these estimates under different assumptions or conditions.

The critical accounting policies that we believe impact significant judgments and estimates used in the preparation of our financial statements presented in this report are described in our Management’s Discussion and Analysis of Financial Condition and Results of Operations in our Annual Report on Form 10-K filed with the SEC on March 30, 2017, as amended. There have been no changes to our critical accounting policies during the three or six month periods ended June 30, 2017 from those discussed in “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies and Significant Judgments and Estimates” in our Annual Report on Form 10-K filed with the SEC on March 30, 2017, as amended, except as related to management’s judgment associated with the accounting for, including the valuation of dividends on, the Redeemable Convertible Preferred and as discussed below.

Recent Accounting Pronouncements

A summary of recent accounting pronouncements that have been adopted or are expected to be adopted by the Company is included in Note 1 to our condensed consolidated financial statements (see Part I, Item 1—“Financial Statements” of this Quarterly Report on Form 10-Q). Additional information regarding relevant accounting pronouncements is provided below.

Adopted in 2017

Stock-based compensation

In March 2016, the accounting guidance related to various aspects of share-based payment transactions was amended, including income tax consequences, classification of awards as either equity or liabilities and classification on the statement of cash flows. Under the new guidance, excess tax benefits and deficiencies are to be recognized as income tax expense or benefit in the income statement as discrete items in the reporting period in which they occur instead of an increase or decrease to stockholders’ equity. With regard to forfeitures, an entity may make an accounting policy election either to estimate the number of awards that are expected to vest or account for forfeitures when they occur. We adopted this new guidance on January 1, 2017, and as a result, we will track stock option deductions in our net operating loss deferred tax asset on a modified retrospective basis. In addition, our policy has been to estimate forfeitures as of the grant date. We will continue to maintain our policy to estimate forfeiture as of the grant date in the future. Since we historically have maintained a full valuation allowance on our net deferred tax asset, there is no net impact to our accumulated deficit or on our net loss per share attributable to common stockholders from the adoption of this new guidance. As such, adoption of this guidance did not have any impact on our consolidated financial statements.

Not yet adopted

Revenue recognition

In May 2014, the accounting guidance related to revenue recognition was amended to replace current guidance with a single, comprehensive standard for accounting for revenue from contracts with customers. The new guidance will become effective for us on January 1, 2018.

21

Table of Contents