UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| (Mark One) | |||||

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the Quarterly Period Ended June 30, 2024

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission File Number: 001-35060

(Exact Name of Registrant as Specified in its Charter)

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |||||||

(Address and Zip Code of Principal Executive Offices)

(813 ) 553-6680

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol | Name of each exchange on which registered | ||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files.) ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | ||||||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

As of July 26, 2024, 46,126,946 shares of the registrant’s common stock, $0.001 par value per share, were outstanding.

PACIRA BIOSCIENCES, INC.

QUARTERLY REPORT ON FORM 10-Q

FOR THE QUARTER ENDED JUNE 30, 2024

TABLE OF CONTENTS

| Page # | ||||||||

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 3

PART I — FINANCIAL INFORMATION

Item 1. FINANCIAL STATEMENTS (Unaudited)

PACIRA BIOSCIENCES, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(In thousands, except share and per share amounts)

(Unaudited)

| June 30, 2024 | December 31, 2023 | ||||||||||

| ASSETS | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Short-term available-for-sale investments | |||||||||||

| Accounts receivable, net | |||||||||||

| Inventories, net | |||||||||||

| Prepaid expenses and other current assets | |||||||||||

| Total current assets | |||||||||||

| Noncurrent available-for-sale investments | |||||||||||

| Fixed assets, net | |||||||||||

| Right-of-use assets, net | |||||||||||

| Goodwill | |||||||||||

| Intangible assets, net | |||||||||||

| Deferred tax assets | |||||||||||

| Investments and other assets | |||||||||||

| Total assets | $ | $ | |||||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Accrued expenses | |||||||||||

| Lease liabilities | |||||||||||

| Current portion of convertible senior notes, net | |||||||||||

| Total current liabilities | |||||||||||

| Convertible senior notes, net | |||||||||||

| Long-term debt, net | |||||||||||

| Lease liabilities | |||||||||||

| Contingent consideration | |||||||||||

| Other liabilities | |||||||||||

| Total liabilities | |||||||||||

Commitments and contingencies (Note 15) | |||||||||||

| Stockholders’ equity: | |||||||||||

Preferred stock, par value $ | |||||||||||

Common stock, par value $ | |||||||||||

Treasury stock, at cost, | ( | ||||||||||

| Additional paid-in capital | |||||||||||

| Accumulated deficit | ( | ( | |||||||||

| Accumulated other comprehensive income | |||||||||||

| Total stockholders’ equity | |||||||||||

| Total liabilities and stockholders’ equity | $ | $ | |||||||||

See accompanying notes to condensed consolidated financial statements.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 4

PACIRA BIOSCIENCES, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(In thousands, except per share amounts)

(Unaudited)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

| Revenues: | |||||||||||||||||||||||

| Net product sales | $ | $ | $ | $ | |||||||||||||||||||

| Royalty revenue | |||||||||||||||||||||||

| Total revenues | |||||||||||||||||||||||

| Operating expenses: | |||||||||||||||||||||||

| Cost of goods sold | |||||||||||||||||||||||

| Research and development | |||||||||||||||||||||||

| Selling, general and administrative | |||||||||||||||||||||||

| Amortization of acquired intangible assets | |||||||||||||||||||||||

| Contingent consideration charges (gains), restructuring charges and other | ( | ( | |||||||||||||||||||||

| Total operating expenses | |||||||||||||||||||||||

| Income from operations | |||||||||||||||||||||||

| Other income (expense): | |||||||||||||||||||||||

| Interest income | |||||||||||||||||||||||

| Interest expense | ( | ( | ( | ( | |||||||||||||||||||

| Gain (loss) on early extinguishment of debt | ( | ||||||||||||||||||||||

| Other, net | ( | ( | ( | ( | |||||||||||||||||||

| Total other income (expense), net | ( | ( | |||||||||||||||||||||

| Income before income taxes | |||||||||||||||||||||||

| Income tax expense | ( | ( | ( | ( | |||||||||||||||||||

| Net income | $ | $ | $ | $ | |||||||||||||||||||

| Net income per share: | |||||||||||||||||||||||

| Basic net income per common share | $ | $ | $ | $ | |||||||||||||||||||

| Diluted net income per common share | $ | $ | $ | $ | |||||||||||||||||||

| Weighted average common shares outstanding: | |||||||||||||||||||||||

| Basic | |||||||||||||||||||||||

| Diluted | |||||||||||||||||||||||

See accompanying notes to condensed consolidated financial statements.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 5

PACIRA BIOSCIENCES, INC.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(In thousands)

(Unaudited)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

| Net income | $ | $ | $ | $ | |||||||||||||||||||

| Other comprehensive (loss) income: | |||||||||||||||||||||||

| Net unrealized (loss) gain on investments, net of tax | ( | ( | ( | ||||||||||||||||||||

| Foreign currency translation adjustments | ( | ( | |||||||||||||||||||||

| Total other comprehensive (loss) income | ( | ( | ( | ||||||||||||||||||||

| Comprehensive income | $ | $ | $ | $ | |||||||||||||||||||

See accompanying notes to condensed consolidated financial statements.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 6

PACIRA BIOSCIENCES, INC.

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

FOR THE THREE MONTHS ENDED JUNE 30, 2024 AND 2023

(In thousands)

(Unaudited)

| Number of Shares Outstanding | Additional Paid-In Capital | Accumulated Deficit | Accumulated Other Comprehensive Income | ||||||||||||||||||||||||||||||||||||||||||||

| Common Shares | Treasury Shares | Common Stock | Treasury Stock | Total | |||||||||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2024 | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||||||||||||||

| Vested restricted stock units | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||

| Common stock withheld for employee withholding tax liabilities on vested restricted stock units | — | — | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||||||||

| Common stock issued under employee stock purchase plan | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||

| Purchase of treasury stock, inclusive of excise tax | — | ( | — | ( | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||

| Purchase of capped call transaction, net of tax | — | — | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss (Note 10) | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||

| Balance at June 30, 2024 | ( | $ | $ | ( | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||||||||||||

| Common Stock | Additional Paid-In Capital | Accumulated Deficit | Accumulated Other Comprehensive Loss | ||||||||||||||||||||||||||||||||

| Shares | Amount | Total | |||||||||||||||||||||||||||||||||

| Balance at March 31, 2023 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

| Exercise of stock options | — | — | — | ||||||||||||||||||||||||||||||||

| Vested restricted stock units | — | — | — | — | — | ||||||||||||||||||||||||||||||

| Common stock issued under employee stock purchase plan | — | — | — | ||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Other comprehensive loss (Note 10) | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||

| Net income | — | — | — | — | |||||||||||||||||||||||||||||||

| Balance at June 30, 2023 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

See accompanying notes to condensed consolidated financial statements.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 7

PACIRA BIOSCIENCES, INC.

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

FOR THE SIX MONTHS ENDED JUNE 30, 2024 AND 2023

(In thousands)

(Unaudited)

| Number of Shares Outstanding | Additional Paid-In Capital | Accumulated Deficit | Accumulated Other Comprehensive Income | ||||||||||||||||||||||||||||||||||||||||||||

| Common Shares | Treasury Shares | Common Stock | Treasury Stock | Total | |||||||||||||||||||||||||||||||||||||||||||

| Balance at December 31, 2023 | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||||||||||||||

| Vested restricted stock units | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Common stock withheld for employee withholding tax liabilities on vested restricted stock units | — | — | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||||||||

| Common stock issued under employee stock purchase plan | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||

| Purchase of treasury stock, inclusive of excise tax | — | ( | — | ( | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||

| Purchase of capped call transaction, net of tax | — | — | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss (Note 10) | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||

| Balance at June 30, 2024 | ( | $ | $ | ( | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||||||||||||

| Common Stock | Additional Paid-In Capital | Accumulated Deficit | Accumulated Other Comprehensive Loss | ||||||||||||||||||||||||||||||||

| Shares | Amount | Total | |||||||||||||||||||||||||||||||||

| Balance at December 31, 2022 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

| Exercise of stock options | — | — | — | ||||||||||||||||||||||||||||||||

| Vested restricted stock units | — | — | — | — | — | ||||||||||||||||||||||||||||||

| Common stock issued under employee stock purchase plan | — | — | — | ||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Other comprehensive income (Note 10) | — | — | — | — | |||||||||||||||||||||||||||||||

| Net income | — | — | — | — | |||||||||||||||||||||||||||||||

| Balance at June 30, 2023 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

See accompanying notes to condensed consolidated financial statements.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 8

PACIRA BIOSCIENCES, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In thousands)

(Unaudited)

| Six Months Ended June 30, | |||||||||||

| 2024 | 2023 | ||||||||||

| Operating activities: | |||||||||||

| Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||

| Deferred taxes | |||||||||||

| Depreciation of fixed assets and amortization of intangible assets | |||||||||||

| Amortization of debt issuance costs | |||||||||||

| Amortization of debt discount | |||||||||||

| (Gain) loss on early extinguishment of debt | ( | ||||||||||

| Stock-based compensation | |||||||||||

| Changes in contingent consideration | ( | ( | |||||||||

| Other net losses | |||||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Accounts receivable, net | ( | ||||||||||

| Inventories, net | |||||||||||

| Prepaid expenses and other assets | ( | ( | |||||||||

| Accounts payable | |||||||||||

| Accrued expenses and income taxes payable | ( | ||||||||||

| Other liabilities | ( | ||||||||||

| Net cash provided by operating activities | |||||||||||

| Investing activities: | |||||||||||

| Purchases of fixed assets | ( | ( | |||||||||

| Purchases of available-for-sale investments | ( | ( | |||||||||

| Sales of available-for-sale investments | |||||||||||

| Purchases of debt investments | ( | ||||||||||

| Net cash (used in) provided by investing activities | ( | ||||||||||

| Financing activities: | |||||||||||

| Proceeds from exercises of stock options | |||||||||||

| Proceeds from shares issued under employee stock purchase plan | |||||||||||

| Payment of employee withholding taxes on restricted stock unit vests | ( | ||||||||||

| Purchase of treasury stock | ( | ||||||||||

| Proceeds from 2029 convertible senior notes | |||||||||||

| Proceeds from Term loan A facility | |||||||||||

| Repayment of 2024 convertible senior notes | ( | ||||||||||

| Repayment of 2025 convertible senior notes | ( | ||||||||||

| Repayment of Term loan B facility | ( | ||||||||||

| Repayment of Term loan A facility | ( | ( | |||||||||

| Purchase of capped call transactions | ( | ||||||||||

| Debt extinguishment costs | ( | ||||||||||

| Payment of debt issuance and financing costs | ( | ( | |||||||||

| Net cash provided by (used in) financing activities | ( | ||||||||||

| Net increase (decrease) in cash and cash equivalents | ( | ||||||||||

| Cash and cash equivalents, beginning of period | |||||||||||

| Cash and cash equivalents, end of period | $ | $ | |||||||||

See accompanying condensed notes to consolidated financial statements. | |||||||||||

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 9

PACIRA BIOSCIENCES, INC. CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (CONTINUED) (In thousands) (Unaudited) | |||||||||||

| Six Months Ended June 30, | |||||||||||

| 2024 | 2023 | ||||||||||

| Supplemental cash flow information: | |||||||||||

| Cash paid for interest | $ | $ | |||||||||

| Net cash paid for income taxes | $ | $ | |||||||||

| Non-cash investing and financing activities: | |||||||||||

| Fixed assets included in accounts payable and accrued liabilities | $ | $ | |||||||||

See accompanying notes to condensed consolidated financial statements.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 10

PACIRA BIOSCIENCES, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

NOTE 1—DESCRIPTION OF BUSINESS

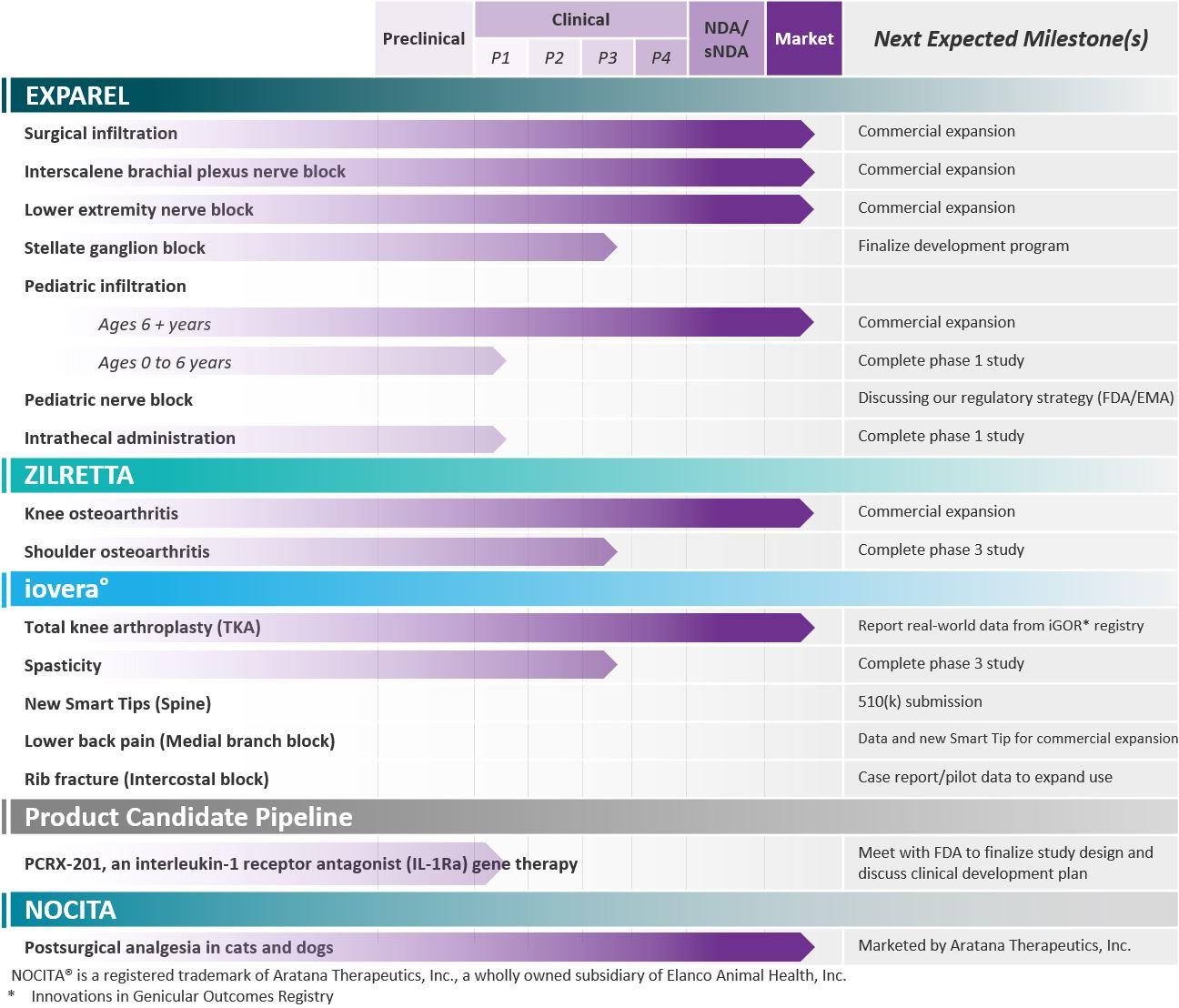

Pacira BioSciences, Inc. and its subsidiaries (collectively, the “Company” or “Pacira”) is the therapeutic area leader in non-opioid pain management with a stated corporate mission of providing non-opioid pain management options to as many patients as possible and redefining the role of opioids for rescue therapy only. The Company’s long-acting, local analgesic, EXPAREL® (bupivacaine liposome injectable suspension), was commercially launched in the United States, or U.S., in April 2012 and approved in select European countries and the United Kingdom, or U.K., in November 2021. EXPAREL utilizes the Company’s proprietary multivesicular liposome, or pMVL, drug delivery technology that encapsulates drugs without altering their molecular structure and releases them over a desired period of time. In November 2021, the Company acquired Flexion Therapeutics, Inc., or Flexion (the “Flexion Acquisition”), and added ZILRETTA® (triamcinolone acetonide extended-release injectable suspension) to its product portfolio. ZILRETTA is the first and only extended-release, intra-articular (meaning in the joint) injection indicated for the management of osteoarthritis, or OA, knee pain. In April 2019, the Company added iovera°® to its commercial offering with the acquisition of MyoScience, Inc., or MyoScience (the “MyoScience Acquisition”). The iovera° system is a handheld cryoanalgesia device used to deliver a precise, controlled application of cold temperature to targeted nerves.

Pacira is subject to risks common to companies in similar industries and stages, including, but not limited to, competition from larger companies, reliance on revenue from three products, reliance on a limited number of wholesalers, reliance on a limited number of manufacturing sites, new technological innovations, dependence on key personnel, reliance on third-party service providers and sole source suppliers, protection of proprietary technology, compliance with government regulations and risks related to cybersecurity.

The Company is managed and operated as a single business focused on the development, manufacture, marketing, distribution and sale of non-opioid pain management and regenerative health solutions. The Company is managed by a single management team, and consistent with its organizational structure, the Chief Executive Officer—who is the Company’s chief operating decision maker—manages and allocates resources at a consolidated level. Effective January 2, 2024, the Company appointed a new Chief Executive Officer. Consistent with the Company’s predecessor chief operating decision maker, the Company views its business as one reportable operating segment to evaluate its performance, allocate resources, set operational targets and forecast its future financial results.

NOTE 2—SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation and Principles of Consolidation

These interim condensed consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America, or GAAP, and in accordance with the rules and regulations of the United States Securities and Exchange Commission (the “SEC”), for interim reporting. Pursuant to these rules and regulations, certain information and footnote disclosures normally included in complete annual financial statements have been condensed or omitted. Therefore, these interim condensed consolidated financial statements should be read in conjunction with the audited annual consolidated financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2023 (the “2023 Annual Report”).

The condensed consolidated financial statements at June 30, 2024, and for the three and six-month periods ended June 30, 2024 and 2023, are unaudited, but include all adjustments (consisting of only normal recurring adjustments) which, in the opinion of management, are necessary to present fairly the financial information set forth herein in accordance with GAAP. The condensed consolidated balance sheet at December 31, 2023 is derived from the audited consolidated financial statements included in the Company’s 2023 Annual Report. The condensed consolidated financial statements as presented reflect certain reclassifications from previously issued financial statements to conform to the current year presentation. The accounts of wholly-owned subsidiaries are included in the condensed consolidated financial statements. Intercompany accounts and transactions have been eliminated in consolidation.

The results of operations for these interim periods are not necessarily indicative of results that may be expected for any other interim periods or for the full year.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 11

Concentration of Major Customers

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

| Largest wholesaler | |||||||||||||||||||||||

| Second largest wholesaler | |||||||||||||||||||||||

| Third largest wholesaler | |||||||||||||||||||||||

| Total | |||||||||||||||||||||||

Recent Accounting Pronouncements Not Adopted as of June 30, 2024

In November 2023, the Financial Accounting Standards Board, or FASB, issued Accounting Standards Update, or ASU, 2023-07, Segment Reporting (Topic 280), Improvements to Reportable Segment Disclosures. The ASU amendment improves reportable segment disclosure requirements, primarily through enhanced disclosures about significant segment expenses on an interim and annual basis. The new segment disclosure requirements apply for entities with a single reportable segment. The ASU’s amendments are effective for fiscal years beginning after December 15, 2023 and interim periods thereafter, with early adoption permitted. The ASU amendment will require adoption on a retrospective basis. The Company is currently evaluating the impact of adopting ASU 2023-07 on its consolidated financial statements.

In December 2023, the FASB issued ASU 2023-09, Income Taxes (Topic 740), Improvements to Income Tax Disclosures. The ASU amendment addresses investor requests for more transparency about income tax information through improvements to income tax disclosures primarily related to the rate reconciliation and income taxes paid information. The ASU’s amendments are effective for fiscal years beginning after December 15, 2024 and may be adopted on a prospective or retrospective basis. The Company is currently evaluating the impact of adopting ASU 2023-09 on its consolidated financial statements.

NOTE 3—REVENUE

Revenue from Contracts with Customers

The Company’s net product sales consist of (i) EXPAREL in the U.S., the European Union, or E.U., and the U.K.; (ii) ZILRETTA in the U.S.; (iii) iovera° in the U.S., Canada and Europe and (iv) sales of its bupivacaine liposome injectable suspension for veterinary use. Royalty revenues are related to a collaborative licensing agreement from the sale of its bupivacaine liposome injectable suspension for veterinary use. The Company does not consider revenue from sources other than sales of EXPAREL and ZILRETTA to be material sources of its consolidated revenue. As such, the following disclosure is limited to revenue associated with net product sales of EXPAREL and ZILRETTA.

Net Product Sales

The Company sells EXPAREL through a drop-ship program under which orders are processed through wholesalers based on orders of the product placed by end-users, namely hospitals, ambulatory surgery centers and healthcare provider offices. EXPAREL is delivered directly to the end-user without the wholesaler ever taking physical possession of the product. The Company primarily sells ZILRETTA to specialty distributors and specialty pharmacies, who then subsequently resell ZILRETTA to physicians, clinics and certain medical centers or hospitals. The Company also contracts directly with healthcare providers and intermediaries such as group purchasing organizations, or GPOs. Product revenue is recognized when control of the promised goods are transferred to the customer, in an amount that reflects the consideration the Company expects to be entitled to in exchange for transferring those goods. EXPAREL and ZILRETTA revenue is recorded at the time the products are transferred to the customer.

Revenues from sales of products are recorded net of returns allowances, prompt payment discounts, service fees, government rebates, volume rebates and chargebacks. These reserves are based on estimates of the amounts earned or to be claimed on the related sales. These amounts are treated as variable consideration, estimated and recognized as a reduction of the transaction price at the time of the sale, using the most likely amount method, except for returns, which is based on the expected

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 12

value method. The Company includes these estimated amounts in the transaction price to the extent it is probable that a significant reversal of cumulative revenue recognized for such transaction will not occur, or when the uncertainty associated with the variable consideration is resolved.

Chargebacks for fees and discounts represent the estimated obligations resulting from contractual commitments to sell products to Department of Veteran Affairs hospitals, participating GPO members, 340B qualified entities and other contracted customers at prices lower than the list price. The 340B Drug Discount Program is a U.S. federal government program that requires participating drug manufacturers to provide outpatient drugs to eligible health care organizations and covered entities at reduced prices. Customers claim the difference between the amount invoiced and the discounted selling price through a chargeback issued by a wholesaler. Reserves are established in the same period that the related revenue is recognized, resulting in a reduction of product revenue and trade receivables, net. Chargeback amounts are determined at the time of sale and the Company generally issues credits for such amounts within weeks of receiving notification from a wholesaler. Reserves for chargebacks consist of anticipated credits the Company expects to issue based on expected units sold and chargebacks that customers have claimed for which credits have not yet been issued.

The calculation for some of these items requires management to make estimates based on sales data, historical return data, contracts, statutory requirements and other related information that may become known in the future. The adequacy of these provisions is reviewed on a quarterly basis.

Accounts Receivable

The majority of accounts receivable arise from product sales and represent amounts due from wholesalers, hospitals, ambulatory surgery centers, specialty distributors, specialty pharmacies and individual physicians. Payment terms generally range from to four months from the date of the transaction, and accordingly, there is no significant financing component.

Performance Obligations

A performance obligation is a promise in a contract to transfer a distinct good or service to the customer and is the unit of account in Accounting Standards Codification, or ASC, 606. A contract’s transaction price is allocated to each distinct performance obligation and recognized as revenue when, or as, the performance obligation is satisfied.

At contract inception, the Company assesses the goods promised in its contracts with customers and identifies a performance obligation for each promise to transfer to the customer a good that is distinct. When identifying individual performance obligations, the Company considers all goods promised in the contract regardless of whether explicitly stated in the customer contract or implied by customary business practices. The Company’s contracts with customers require it to transfer an individual distinct product, which represents a single performance obligation. The Company’s performance obligation with respect to its product sales is satisfied at a point in time, which transfers control upon delivery of EXPAREL and ZILRETTA to its customers. The Company considers control to have transferred upon delivery because the customer has legal title to the asset, physical possession of the asset has been transferred, the customer has significant risks and rewards of ownership of the asset and the Company has a present right to payment at that time.

Disaggregated Revenue

The following table represents disaggregated net product sales in the periods presented as follows (in thousands):

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

| Net product sales: | |||||||||||||||||||||||

| EXPAREL | $ | $ | $ | $ | |||||||||||||||||||

| ZILRETTA | |||||||||||||||||||||||

| iovera° | |||||||||||||||||||||||

| Bupivacaine liposome injectable suspension | |||||||||||||||||||||||

| Total net product sales | $ | $ | $ | $ | |||||||||||||||||||

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 13

NOTE 4—INVENTORIES

The components of inventories, net are as follows (in thousands):

| June 30, | December 31, | ||||||||||

| 2024 | 2023 | ||||||||||

| Raw materials | $ | $ | |||||||||

| Work-in-process | |||||||||||

| Finished goods | |||||||||||

| Total | $ | $ | |||||||||

NOTE 5—FIXED ASSETS

Fixed assets, net, summarized by major category, consist of the following (in thousands):

| June 30, | December 31, | ||||||||||

| 2024 | 2023 | ||||||||||

Machinery and equipment (1) | $ | $ | |||||||||

| Leasehold improvements | |||||||||||

| Computer equipment and software | |||||||||||

| Office furniture and equipment | |||||||||||

Construction in progress (2) | |||||||||||

| Total | |||||||||||

Less: accumulated depreciation (1) | ( | ( | |||||||||

| Fixed assets, net | $ | $ | |||||||||

(1) During the six months ended June 30, 2024, the Company disposed of $19.0 million of fully depreciated machinery and equipment associated with its 45-liter EXPAREL manufacturing process at its contract manufacturing facility located in Swindon, England. The Company continues to operate its 200-liter EXPAREL manufacturing process at the same facility.

(2) In July 2024, a new 200-liter EXPAREL manufacturing suite at the Company’s Science Center Campus in San Diego, California was placed into service, for which approximately $76.1

For the three months ended June 30, 2024 and 2023, depreciation expense was $4.5 million and $4.7 million, respectively. For the three months ended June 30, 2024 and 2023, there was $0.7 million and $0.7 million of capitalized interest on the construction of manufacturing sites, respectively.

For the six months ended June 30, 2024 and 2023, depreciation expense was $8.6 million and $10.0 million, respectively. For the six months ended June 30, 2024 and 2023, there was $1.4 million and $2.1 million of capitalized interest on the construction of manufacturing sites, respectively.

At June 30, 2024 and December 31, 2023, total fixed assets, net, includes manufacturing process equipment and leasehold improvements located in Europe in the amount of $32.5 million and $36.8 million, respectively.

As of June 30, 2024 and December 31, 2023, the Company had asset retirement obligations of $4.0 million and $4.3 million, respectively, included in accrued expenses and other liabilities on its condensed consolidated balance sheets, for costs associated with returning leased spaces to their original condition upon the termination of certain of its lease agreements.

NOTE 6—LEASES

The Company leases all of its facilities, including its EXPAREL and iovera° handpiece manufacturing facility at its Science Center Campus in San Diego, California. The Company also has two embedded leases with Thermo Fisher Scientific Pharma Services for the use of their manufacturing facility in Swindon, England for the production of EXPAREL and ZILRETTA. A portion of the associated monthly base fees has been allocated to the lease components based on a relative fair value basis.

Since July 2022 and February 2023, the Company has been recognizing sublease income for laboratory space leased in Woburn, Massachusetts and a portion of office space leased in Burlington, Massachusetts, respectively, from leases that were

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 14

assumed as part of the Flexion Acquisition. In February 2024, the lease and sublease term concluded for the laboratory space in Woburn, Massachusetts.

The operating lease costs for the facilities include lease and non-lease components, such as common area maintenance and other common operating expenses, along with executory costs such as insurance and real estate taxes. Total operating lease expense, net is as follows (in thousands):

| Three Months Ended | Six Months Ended | |||||||||||||||||||||||||

| June 30, | June 30, | |||||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||||||

| Fixed lease costs | $ | $ | $ | $ | ||||||||||||||||||||||

| Variable lease costs | ||||||||||||||||||||||||||

| Sublease income | ( | ( | ( | ( | ||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

Supplemental cash flow information related to operating leases is as follows (in thousands):

| Six Months Ended | ||||||||||||||

| June 30, | ||||||||||||||

| 2024 | 2023 | |||||||||||||

| Cash paid for operating lease liabilities, net of lease incentives | $ | $ | ||||||||||||

The Company has elected to net the amortization of the right-of-use asset and the reduction of the lease liability principal in other liabilities in the condensed consolidated statements of cash flows.

The Company has measured its operating lease liabilities at an estimated discount rate at which it could borrow on a collateralized basis over the remaining term for each operating lease. The weighted average remaining lease terms and the weighted average discount rates are summarized as follows:

| June 30, | ||||||||||||||

| 2024 | 2023 | |||||||||||||

| Weighted average remaining lease term | ||||||||||||||

| Weighted average discount rate | % | % | ||||||||||||

Maturities of the Company’s operating lease liabilities are as follows (in thousands):

| Year | Aggregate Minimum Payments Due | |||||||

| 2024 (remaining six months) | $ | |||||||

| 2025 | ||||||||

| 2026 | ||||||||

| 2027 | ||||||||

| 2028 | ||||||||

| Thereafter | ||||||||

| Total future lease payments | ||||||||

| Less: imputed interest | ( | |||||||

| Total operating lease liabilities | $ | |||||||

NOTE 7—GOODWILL AND INTANGIBLE ASSETS

Goodwill

The Company’s goodwill results from the acquisition of Pacira Pharmaceuticals, Inc. (the Company’s California operating subsidiary) from SkyePharma Holding, Inc. (now Vectura Group Limited, a subsidiary of Philip Morris International, Inc.) in 2007, the MyoScience Acquisition in 2019 and the Flexion Acquisition in 2021. The goodwill balance at each of June 30, 2024 and December 31, 2023 was $163.2

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 15

Intangible Assets

Intangible assets, net, consists of the in-process research and development, or IPR&D, and developed technology from the Flexion Acquisition and developed technology and customer relationships from the MyoScience Acquisition and are summarized as follows (dollar amounts in thousands):

| June 30, 2024 | Gross Carrying Value | Accumulated Amortization | Intangible Assets, Net | Weighted-Average Useful Lives | ||||||||||||||||||||||

| Developed technologies | $ | $ | ( | $ | ||||||||||||||||||||||

| Customer relationships | ( | |||||||||||||||||||||||||

| Total finite-lived intangible assets, net | ( | |||||||||||||||||||||||||

| Acquired IPR&D | — | |||||||||||||||||||||||||

| Total intangible assets, net | $ | $ | ( | $ | ||||||||||||||||||||||

| December 31, 2023 | Gross Carrying Value | Accumulated Amortization | Intangible Assets, Net | Weighted-Average Useful Lives | ||||||||||||||||||||||

| Developed technologies | $ | $ | ( | $ | ||||||||||||||||||||||

| Customer relationships | ( | |||||||||||||||||||||||||

| Total finite-lived intangible assets, net | ( | |||||||||||||||||||||||||

| Acquired IPR&D | — | |||||||||||||||||||||||||

| Total intangible assets, net | $ | $ | ( | $ | ||||||||||||||||||||||

Amortization expense on intangible assets was $14.3 28.6

Assuming no changes in the gross carrying amount of these intangible assets, the future estimated amortization expense on the finite-lived intangible assets will be $28.6 million for the remaining six months of 2024, $57.3 37.4 million in 2031, $7.9 million in 2032 and $2.2 million in 2033.

NOTE 8—DEBT

The carrying value of the Company’s outstanding debt is summarized as follows (in thousands):

| June 30, | December 31, | ||||||||||

| 2024 | 2023 | ||||||||||

| Term loan A facility maturing March 2028 | $ | $ | |||||||||

| Total | $ | $ | |||||||||

(1) The 3.375 % convertible senior notes due May 2024 matured and were repaid on May 1, 2024.

2028 Term Loan A Facility

On March 31, 2023, the Company entered into a credit agreement (as amended to date, the “TLA Credit Agreement”) with JPMorgan Chase Bank, N.A., as administrative agent, and certain lenders, to refinance the indebtedness outstanding under the Company’s then-existing TLB Credit Agreement (as defined and discussed below). The term loan issued under the TLA Credit Agreement (the “TLA Term Loan”) was issued at a 0.30 % discount and provides for a single-advance term loan A facility in the principal amount of $150.0 million, which is secured by substantially all of the Company’s and any subsidiary guarantor’s assets. Subject to certain conditions, the Company may, at any time, on one or more occasion, add one or more new classes of term facilities and/or increase the principal amount of the loans of any existing class by requesting one or more incremental term facilities. The net proceeds of the TLA Term Loan were approximately $149.6 million after deducting an original issue discount of $0.4 million.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 16

On May 8, 2024, the Company, JPMorgan Chase Bank, N.A., as administrative agent, and certain lenders entered into a first amendment (the “First TLA Amendment”) to the TLA Credit Agreement. The First TLA Amendment, among other things, (i) permits the Company’s $150.0 million share repurchase program and (ii) this offering, including the Capped Call Transactions as described below.

The total debt composition of the TLA Term Loan is as follows (in thousands):

| June 30, | December 31, | ||||||||||

| 2024 | 2023 | ||||||||||

| Term loan A facility maturing March 2028 | $ | $ | |||||||||

| Deferred financing costs | ( | ( | |||||||||

| Discount on debt | ( | ( | |||||||||

| Total debt, net of debt discount and deferred financing costs | $ | $ | |||||||||

The TLA Term Loan matures on March 31, 2028 and the TLA Credit Agreement requires quarterly repayments of principal in the amount of $2.8 million which commenced on June 30, 2023, increasing to $3.8 million commencing March 31, 2025, with a remaining balloon payment of approximately $85.3 million due at maturity. Due to voluntary principal prepayments made, the Company is not required to make further principal payments until June 2026, although the Company retains the option to do so.

The TLA Credit Agreement requires the Company to, among other things, maintain (i) a Senior Secured Net Leverage Ratio (as defined in the TLA Credit Agreement), determined as of the last day of each fiscal quarter, of no greater than 3.00 to 1.00 and (ii) a Fixed Charge Coverage Ratio (as defined in the Credit Agreement), determined as of the last day of each fiscal quarter, of no less than 1.50 to 1.00. The TLA Credit Agreement requires the Company to maintain an unrestricted cash and cash equivalents balance of at least $300.0 million ($500.0 million less a $200.0 million prepayment in the six months ended June 30, 2024) less any additional prepayments of the 2025 Notes (as defined below) at any time from 91 days prior to the maturity date through the earlier of (i) the latest maturity date of the 2025 Notes and (ii) the date on which there is no outstanding principal amount of the 2025 Notes. The TLA Credit Agreement also contains customary affirmative and negative covenants, financial covenants, representations and warranties, events of default and other provisions. As of June 30, 2024, the Company was in compliance with all financial covenants under the TLA Credit Agreement.

The Company may elect to borrow either (i) alternate base rate borrowings or (ii) term benchmark borrowings or daily simple SOFR (as defined in the TLA Credit Agreement) borrowings. Each term loan borrowing that is an alternate base rate borrowing bears interest at a rate per annum equal to (i) the Alternate Base Rate (as defined in the TLA Credit Agreement), plus (ii) a spread based on the Company’s Senior Secured Net Leverage Ratio ranging from 2.00 % to 2.75 %. Each term loan borrowing that is a term benchmark borrowing or daily simple SOFR borrowing bears interest at a rate per annum equal to (i) the Adjusted Term SOFR Rate or Adjusted Daily Simple SOFR (as each is defined in the Credit Agreement), plus (ii) a spread based on the Company’s Senior Secured Net Leverage Ratio ranging from 3.00 % to 3.75 %. During the six months ended June 30, 2024, the Company made $5.6 million voluntary principal prepayments. During the year ended December 31, 2023, the Company made a scheduled principal payment of $2.8 million as well as $30.6 million of voluntary principal prepayments. As of June 30, 2024, borrowings under the TLA Term Loan consisted entirely of term benchmark borrowings at a rate of 8.43 %.

2026 Term Loan B Facility

In December 2021, the Company entered into a term loan credit agreement (the “TLB Credit Agreement”) with JPMorgan Chase Bank, N.A., as administrative agent and the initial lender. The term loan issued under the TLB Credit Agreement (the “TLB Term Loan”) was issued at a 3.00 % discount and allowed for a single-advance term loan B facility in the principal amount of $375.0 million, which was secured by substantially all of the Company’s and each subsidiary guarantor’s assets. The net proceeds of the TLB Term Loan were approximately $363.8 million after deducting an original issue discount of $11.2 million.

On March 31, 2023, the Company used the $149.6 million of net borrowings under the TLA Credit Agreement and cash on hand to repay the $296.9 million then-outstanding principal under the TLB Credit Agreement and concurrently terminated the TLB Credit Agreement, which resulted in a $16.9 million loss on early extinguishment of debt. The Company incurred a prepayment fee of 2.00 % of the outstanding principal balance of the TLB Term Loan in connection with the termination.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 17

Convertible Senior Notes Due 2029

In May 2024, the Company completed a private placement of $287.5 million in aggregate principal amount of its 2.125 % convertible senior notes due 2029, or 2029 Notes, and entered into an indenture with Computershare Corporate Trust, N.A., or 2029 Indenture, with respect to the 2029 Notes. The 2029 Notes accrue interest at a fixed rate of 2.125 % per year, payable semiannually in arrears on May 15th and November 15th of each year. The 2029 Notes mature on May 15, 2029.

The total debt composition of the 2029 Notes is as follows (in thousands):

| June 30, | |||||

| 2024 | |||||

| $ | |||||

| Deferred financing costs | ( | ||||

| Total debt, net of deferred financing costs | $ | ||||

Holders may convert the 2029 Notes prior to the close of business on the business day immediately preceding November 15, 2028, only if certain circumstances are met, including, but not limited to, if during the previous calendar quarter, the last reported sales price of the Company’s common stock was greater than 130 % of the conversion price then applicable for at least 20 out of the last 30 consecutive trading days of the quarter. During the quarter ended June 30, 2024, the conditions for conversion were not met.

On or after November 15, 2028, until the close of business on the second scheduled trading day immediately preceding May 15, 2029, holders may convert their 2029 Notes at any time.

Upon conversion, holders will receive the principal amount of their 2029 Notes and any excess conversion value, calculated based on the per share volume-weighted average price for each of the 50 consecutive trading days during the observation period (as more fully described in the 2029 Indenture). For the principal, the Company will settle in cash per the terms of the 2029 Notes. For any excess conversion value, holders may receive cash, shares of the Company’s common stock or a combination of cash and shares of the Company’s common stock, at the Company’s option. The initial conversion rate for the 2029 Notes is 25.2752 shares of common stock per $1,000 principal amount, which is equivalent to an initial conversion price of $39.56 per share of the Company’s common stock. The conversion rate will be subject to adjustment in some events but will not be adjusted for any accrued and unpaid interest. The initial conversion price of the 2029 Notes represents a premium of approximately 32.5 % to the closing sale price of $29.86 per share of the Company’s common stock on the Nasdaq Global Select Market on May 9, 2024, the date that the Company priced the private offering of the 2029 Notes.

As of June 30, 2024, the 2029 Notes had a market price of $996 per $1,000 principal amount. In the event of conversion, holders would forgo all future interest payments, any unpaid accrued interest and the possibility of further stock price appreciation. Upon the receipt of conversion requests, the settlement of the 2029 Notes will be paid pursuant to the terms of the 2029 Indenture. In the event that all of the 2029 Notes are converted, the Company would be required to repay the $287.5 million in principal value in cash, whereas any conversion premium would be required to be repaid in any combination of cash and shares of its common stock (at the Company’s option).

Prior to the close of business on the business day immediately preceding November 15, 2028, the 2029 Notes are convertible only under the following circumstances: (1) during any calendar quarter commencing after the calendar quarter ending on June 30, 2024 (and only during such calendar quarter), if the last reported sale price of the Common Stock for at least 20 trading days (whether or not consecutive) during a period of 30 consecutive trading days ending on the last trading day of the immediately preceding calendar quarter is equal to or greater than 130 % of the conversion price on each applicable trading day; (2) during the five business-day period after any five consecutive trading-day period (the “measurement period”) in which the trading price per $1,000 principal amount of the 2029 Notes for each trading day of the measurement period was less than 98 % of the product of the last reported sale price of the Company’s common stock and the conversion rate on each such trading day; (3) upon the occurrence of specified corporate events; or (4) upon a Company redemption. On or after November 15, 2028, until the close of business on the second scheduled trading day immediately preceding May 15, 2029, holders of the 2029 Notes may convert all or a portion of their 2029 Notes, at any time. Upon conversion, the 2029 Notes will be settled by paying or delivering, as applicable, cash or a combination of cash and shares of the Company’s common stock, based on the applicable conversion rate. No sinking fund is provided for the 2029 Notes.

On or after May 17, 2027 and on or before the 50 th scheduled trading day immediately before the maturity date, the Company may redeem for cash all or part of the 2029 Notes if (i) the 2029 Notes are “freely tradable” (as defined in the 2029 Indenture) and any accrued and unpaid additional interest has been paid as of the date the Company sends the related notice of the redemption and (ii) the last reported sales price of the Company’s common stock exceeds 130 % of the conversion price then

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 18

in effect for (1) each of at least 20 trading days (whether or not consecutive) during any 30 consecutive trading days ending on, and including, the trading day immediately before the date the Company sends the related notice of the redemption; and (2) the trading day immediately before the date the Company sends such notice. The redemption price of each 2029 Note to be redeemed will be the principal amount of such 2029 Note, plus accrued and unpaid interest, if any. In addition, calling any 2029 Notes for redemption will constitute a make-whole fundamental change, in which case the conversion rate applicable to those 2029 Notes, if converted in connection with the redemption, will be increased in certain circumstances. Upon the occurrence of a “make-whole fundamental change” (as defined in the 2029 Indenture), subject to a limited exception for certain cash mergers, holders may require the Company to repurchase all or a portion of their 2029 Notes for cash at a price equal to 100 % of the principal amount of the 2029 Notes to be repurchased plus any accrued and unpaid interest.

While the 2029 Notes are currently classified on the Company’s condensed consolidated balance sheet at June 30, 2024 as long-term debt, the future convertibility and resulting balance sheet classification of this liability is monitored at each quarterly reporting date and is analyzed dependent upon market prices of the Company’s common stock during the prescribed measurement periods. In the event that the holders of the 2029 Notes have the election to convert the 2029 Notes at any time during the prescribed measurement period, the 2029 Notes would then be considered a current obligation and classified as such.

On May 9, 2024, in connection with the pricing of the 2029 Notes, and on May 10, 2024, in connection with the exercise in full by the initial purchasers of the 2029 Notes (the “Initial Purchasers”) of their option to purchase additional 2029 Notes, the Company entered into privately negotiated capped call transactions (the “Capped Call Transactions”) with certain of the Initial Purchasers of the 2029 Notes and/or their respective affiliates and/or other financial institutions (the “Option Counterparties”). The Capped Call Transactions are expected to cover, subject to anti-dilution adjustments substantially similar to those applicable to the 2029 Notes, the number of shares of the Company’s common stock underlying the 2029 Notes.

The Capped Call Transactions are expected to reduce the potential dilution to the Company’s common stock upon any conversion of the 2029 Notes and/or offset any potential cash payments the Company is required to make in excess of the principal amount of converted 2029 Notes, as the case may be, upon any conversion of the 2029 Notes, with such reduction and/or offset subject to a cap. The cap price of the Capped Call Transactions will initially be approximately $53.75 per share, representing a premium of approximately 80 % over the closing price of $29.86 per share of the Company’s common stock on May 9, 2024, and is subject to certain adjustments under the terms of the Capped Call Transactions. The capped call was recorded as a reduction to additional paid-in capital at its cost of $26.7 million.

The Capped Call Transactions are separate transactions entered into by the Company with the Option Counterparties, are not part of the terms of the 2029 Notes and will not affect any holder’s rights under the 2029 Notes. Holders of the 2029 Notes will not have any rights with respect to the Capped Call Transactions.

Convertible Senior Notes Due 2025

In July 2020, the Company completed a private placement of $402.5 million in aggregate principal amount of its 0.750 % convertible senior notes due 2025, or 2025 Notes, and entered into an indenture with Computershare Corporate Trust, N.A. (formerly Wells Fargo Bank, N.A.), or 2025 Indenture, with respect to the 2025 Notes. The 2025 Notes accrue interest at a fixed rate of 0.750 % per year, payable semiannually in arrears on February 1st and August 1st of each year. The 2025 Notes mature on August 1, 2025.

In May 2024, the Company used part of the net proceeds from the issuance of the 2029 Notes to repurchase $200.0 million aggregate principal amount of the 2025 Notes in privately negotiated transactions at a discount for $191.4 million in cash (including accrued interest). The partial repurchase of the 2025 Notes resulted in a $7.5 million gain on early extinguishment of debt.

The total debt composition of the 2025 Notes is as follows (in thousands):

| June 30, | December 31, | ||||||||||

| 2024 | 2023 | ||||||||||

| $ | $ | ||||||||||

| Deferred financing costs | ( | ( | |||||||||

| Total debt, net of deferred financing costs | $ | $ | |||||||||

Holders may convert the 2025 Notes at any time prior to the close of business on the business day immediately preceding February 3, 2025, only if certain circumstances are met, including, but not limited to, if during the previous calendar quarter, the last reported sales price of the Company’s common stock was greater than 130 % of the conversion price then applicable for at least 20 out of the last 30 consecutive trading days of the quarter. During the quarter ended June 30, 2024, the conditions for conversion were not met.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 19

On or after February 3, 2025, until the close of business on the second scheduled trading day immediately preceding August 1, 2025, holders may convert their 2025 Notes at any time.

Upon conversion, holders will receive the principal amount of their 2025 Notes and any excess conversion value, calculated based on the per share volume-weighted average price for each of the 40 consecutive trading days during the observation period (as more fully described in the 2025 Indenture). For both the principal and excess conversion value, holders may receive cash, shares of the Company’s common stock or a combination of cash and shares of the Company’s common stock, at the Company’s option. The initial conversion rate for the 2025 Notes is 13.9324 shares of common stock per $1,000 principal amount, which is equivalent to an initial conversion price of $71.78 per share of the Company’s common stock. The conversion rate will be subject to adjustment in some events but will not be adjusted for any accrued and unpaid interest. The initial conversion price of the 2025 Notes represents a premium of approximately 32.5 % to the closing sale price of $54.17 per share of the Company’s common stock on the Nasdaq Global Select Market on July 7, 2020, the date that the Company priced the private offering of the 2025 Notes.

As of June 30, 2024, the 2025 Notes had a market price of $938 per $1,000 principal amount. In the event of conversion, holders would forgo all future interest payments, any unpaid accrued interest and the possibility of further stock price appreciation. Upon the receipt of conversion requests, the settlement of the 2025 Notes will be paid pursuant to the terms of the 2025 Indenture. In the event that all of the 2025 Notes are converted, the Company would be required to repay the remaining $202.5 million in principal value and any conversion premium in any combination of cash and shares of its common stock (at the Company’s option).

Since August 1, 2023 (but, in the case of a redemption of less than all of the outstanding 2025 Notes, no later than the 40 th scheduled trading day immediately before the maturity date), the Company may redeem for cash all or part of the 2025 Notes if the last reported sale price (as defined in the 2025 Indenture) of the Company’s common stock has been at least 130 % of the conversion price then in effect for (i) each of at least 20 trading days (whether or not consecutive) during any 30 consecutive trading days ending on, and including, the trading day immediately before the date the Company sends the related notice of redemption and (ii) the trading day immediately before the date the Company sends such notice. The redemption price will equal the sum of (i) 100 % of the principal amount of the 2025 Notes being redeemed, plus (ii) accrued and unpaid interest, including additional interest, if any, to, but excluding, the redemption date. In addition, calling the 2025 Notes for redemption will constitute a “make-whole fundamental change” (as defined in the 2025 Indenture) and will, in certain circumstances, increase the conversion rate applicable to the conversion of such notes if it is converted in connection with the redemption. No sinking fund is provided for the 2025 Notes.

While the 2025 Notes are currently classified on the Company’s condensed consolidated balance sheet at June 30, 2024 as long-term debt, the future convertibility and resulting balance sheet classification of this liability is monitored at each quarterly reporting date and is analyzed dependent upon market prices of the Company’s common stock during the prescribed measurement periods. In the event that the holders of the 2025 Notes have the election to convert the 2025 Notes at any time during the prescribed measurement period, the 2025 Notes would then be considered a current obligation and classified as such.

Convertible Senior Notes Due 2024 Assumed from the Flexion Acquisition

Prior to the Flexion Acquisition, in May 2017, Flexion issued an aggregate of $201.3 million principal amount of 3.375 % convertible senior notes due 2024 (the “Flexion 2024 Notes”), pursuant to the indenture, dated as of May 2, 2017 (the “Original Flexion Indenture”), between Flexion and Computershare Corporate Trust, N.A. (formerly Wells Fargo Bank, N.A.), as trustee (the “Flexion Trustee”), as supplemented by the First Supplemental Indenture, dated as of November 19, 2021, between Flexion and the Flexion Trustee (the “First Supplemental Flexion Indenture” and, together with the Original Flexion Indenture, the “Flexion Indenture”). The Flexion 2024 Notes had a maturity date of May 1, 2024, were unsecured, and accrued interest at a rate of 3.375 % per annum, payable semi-annually on May 1st and November 1st of each year. Upon the Flexion Acquisition, the principal was assumed and recorded at fair value by the Company.

On January 7, 2022, following the expiration of the offer to purchase, the Company accepted the $192.6 million aggregate principal amount of Flexion 2024 Notes that were validly tendered (and not validly withdrawn). No Flexion 2024 Notes were converted in connection with the Notice. The remaining principal of $8.6 million was repaid at maturity on May 1, 2024.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 20

Interest Expense

The following table sets forth the total interest expense recognized in the periods presented (dollar amounts in thousands):

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

| Contractual interest expense | $ | $ | $ | $ | |||||||||||||||||||

| Amortization of debt issuance costs | |||||||||||||||||||||||

| Amortization of debt discount | |||||||||||||||||||||||

Capitalized interest (Note 5) | ( | ( | ( | ( | |||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

| Effective interest rate on total debt | % | % | % | % | |||||||||||||||||||

NOTE 9—FINANCIAL INSTRUMENTS

Fair Value Measurements

Fair value is defined as the price that would be received to sell an asset or be paid to transfer a liability in the principal or most advantageous market in an orderly transaction. To increase consistency and comparability in fair value measurements, the FASB established a three-level hierarchy which requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring fair value. The three levels of fair value measurements are:

•Level 1: Quoted prices (unadjusted) in active markets that are accessible at the measurement date for assets or liabilities. The fair value hierarchy gives the highest priority to Level 1 inputs.

•Level 2: Observable prices that are based on inputs not quoted on active markets, but corroborated by market data.

•Level 3: Unobservable inputs that are used when little or no market data is available. The fair value hierarchy gives the lowest priority to Level 3 inputs.

The carrying value of financial instruments including cash and cash equivalents, accounts receivable and accounts payable approximate their respective fair values due to the short-term nature of these items. The fair value of the Company’s convertible senior notes and its TLA Term Loan are calculated utilizing market quotations from an over-the-counter trading market for these notes (Level 2). The fair value of the Company’s acquisition-related contingent consideration is reported at fair value on a recurring basis (Level 3). The carrying amounts of equity investments and convertible notes receivable without readily determinable fair values have not been adjusted for either an impairment or upward or downward adjustments based on observable transactions.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 21

At June 30, 2024, the carrying values and fair values of the following financial assets and liabilities were as follows (in thousands):

| Carrying Value | Fair Value Measurements Using | |||||||||||||||||||||||||

| Level 1 | Level 2 | Level 3 | ||||||||||||||||||||||||

| Financial Assets and Financial Liabilities Measured at Fair Value on a Recurring Basis: | ||||||||||||||||||||||||||

| Financial Assets: | ||||||||||||||||||||||||||

| Equity investments | $ | $ | $ | $ | ||||||||||||||||||||||

| Convertible notes receivable | $ | $ | $ | $ | ||||||||||||||||||||||

| Financial Liabilities: | ||||||||||||||||||||||||||

| Acquisition-related contingent consideration | $ | $ | $ | $ | ||||||||||||||||||||||

| Financial Liabilities Measured at Amortized Cost: | ||||||||||||||||||||||||||

| Term loan A facility due March 2028 | $ | $ | $ | $ | ||||||||||||||||||||||

| $ | $ | $ | $ | |||||||||||||||||||||||

| $ | $ | $ | $ | |||||||||||||||||||||||

(1) The closing price of the Company’s common stock as reported on the Nasdaq Global Select Market was $28.61 per share on June 28, 2024, the last trading day of the quarter ended June 30, 2024, compared to a conversion price of $39.56 per share. At June 30, 2024, as the conversion price was above the stock price, the requirements for conversion have not been met.

(2) The closing price of the Company’s common stock as reported on the Nasdaq Global Select Market was $28.61 per share on June 28, 2024, the last trading day of the quarter ended June 30, 2024, compared to a conversion price of $71.78 per share. At June 30, 2024, as the conversion price was above the stock price, the requirements for conversion have not been met. The maximum conversion on the principal that could have been due on the 2025 Notes is 2.8 million shares of the Company’s common stock, which assumes no increase in the conversion rate for certain corporate events.

Financial Assets and Liabilities Measured at Fair Value on a Recurring Basis

Equity and Convertible Note Investments

The Company holds strategic investments in clinical and preclinical stage privately-held biotechnology companies in the form of equity and convertible note investments. The following investments have no readily determinable fair value and are recorded at cost minus impairment, if any, plus or minus observable price changes of identical or similar investments (in thousands):

| Equity Investments | Convertible Notes Receivable | Total | ||||||||||||||||||

Balance at December 31, 2022 | $ | $ | $ | |||||||||||||||||

| Purchases | ||||||||||||||||||||

| Foreign currency adjustments | ||||||||||||||||||||

Balance at December 31, 2023 | ||||||||||||||||||||

| Foreign currency adjustments | ( | ( | ||||||||||||||||||

Balance at June 30, 2024 | $ | $ | $ | |||||||||||||||||

Acquisition-Related Contingent Consideration

The Company has recognized contingent consideration related to the Flexion Acquisition in the amount of $22.4 million and $24.7 million as of June 30, 2024 and December 31, 2023, respectively. The Company’s contingent consideration obligations are recorded at their estimated fair values and are revalued each reporting period if and until the related contingencies are resolved. The Company has measured the fair value of its contingent consideration using a probability-weighted discounted cash flow approach that is based on unobservable inputs and a Monte Carlo simulation. These inputs include, as applicable, estimated probabilities and the timing of achieving specified commercial and regulatory milestones, estimated forecasts of revenue and costs and the discount rates used to calculate the present value of estimated future payments. Significant changes may increase or decrease the probabilities of achieving the related commercial and regulatory events, shorten or lengthen the time required to achieve such events, or increase or decrease estimated forecasts.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 22

In November 2021, the Company completed the Flexion Acquisition, which provided for contingent consideration related to contingent value rights that were issued to Flexion shareholders and certain equity award holders which could aggregate up to a total of $372.3 million if certain regulatory and commercial milestones are met. The aggregate amount was initially $425.5 million prior to the Company’s September 2022 decision to formally discontinue further development of Flexion’s product candidate, PCRX-301. The Company’s obligation to make milestone payments is limited to those milestones achieved through December 31, 2030, and are to be paid within 60 days of the end of the fiscal quarter of achievement. During the three months ended June 30, 2024, the Company recognized a contingent consideration charge of $1.5 million primarily due to revisions to the latest discount rates. During the six months ended June 30, 2024, the Company recognized a contingent consideration gain of $2.3 million primarily due to an adjustment reflecting the probability of achieving the remaining Flexion regulatory milestone by the milestone expiration date. During the three and six months ended June 30, 2023, the Company recognized gains of $18.3 million and $6.6 million, respectively, due to adjustments to long-term forecasts which reduced the probability of meeting the sales-based contingent consideration milestones by December 31, 2030, the expiration date for achieving the milestones. The gains recognized during the six months ended June 30, 2023 were partially offset by a decrease in the assumed discount rate that is utilized in calculating the liability’s present value, based on a significant improvement in the Company’s incremental borrowing rate resulting from the TLA Credit Agreement entered into in March 2023. These adjustments were recorded within contingent consideration charges (gains), restructuring charges and other in the condensed consolidated statements of operations. At June 30, 2024, the weighted average discount rate was 8.5 %.

The following table includes the key assumptions used in the valuation of the Company’s contingent consideration:

| Assumption | Ranges Utilized as of June 30, 2024 | |||||||

| Discount rates | ||||||||

| Probability of payment for remaining regulatory milestone | ||||||||

The change in the Company’s contingent consideration recorded at fair value using Level 3 measurements is as follows (in thousands):

| Contingent Consideration Fair Value | ||||||||

Balance at December 31, 2022 | $ | |||||||

| Fair value adjustments and accretion | ( | |||||||

Balance at December 31, 2023 | ||||||||

| Fair value adjustments and accretion | ( | |||||||

Balance at June 30, 2024 | $ | |||||||

Available-for-Sale Investments

Short-term investments consist of asset-backed securities collateralized by credit card receivables, investment grade commercial paper and corporate, federal agency and government bonds with maturities greater than three months, but less than one year. Noncurrent investments consist of asset-backed securities collateralized by credit card receivables and contain maturities greater than one year but less than three years . Net unrealized gains and losses (excluding credit losses, if any) from the Company’s short-term investments are reported in other comprehensive income. At June 30, 2024 and December 31, 2023, all of the Company’s short-term and noncurrent investments are classified as available-for-sale investments and are determined to be Level 2 instruments, with the exception of U.S. government bonds, which are measured at fair value using standard industry models with observable inputs. The fair value of the commercial paper is measured based on a standard industry model that uses the three-month U.S. Treasury bill rate as an observable input. The fair value of the asset-backed securities and corporate bonds is principally measured or corroborated by trade data for identical issues in which related trading activity is not sufficiently frequent to be considered a Level 1 input or that of comparable securities. The fair value of U.S. government bonds is based on level 1 trading activity. At the time of purchase, all available-for-sale investments had an “A” or better rating by Standard & Poor’s.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 23

The following summarizes the Company’s short-term and noncurrent available-for-sale investments at June 30, 2024 and December 31, 2023 (in thousands):

June 30, 2024 Investments | Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value (Level 2) | ||||||||||||||||||||||

| Current: | ||||||||||||||||||||||||||

| Asset-backed securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

| Commercial paper | ( | |||||||||||||||||||||||||

| Corporate bonds | ( | |||||||||||||||||||||||||

| U.S. federal agency bonds | ( | |||||||||||||||||||||||||

| Total | $ | $ | $ | ( | $ | |||||||||||||||||||||

December 31, 2023 Investments | Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value (Level 1) | Fair Value (Level 2) | |||||||||||||||||||||||||||

| Current: | ||||||||||||||||||||||||||||||||

| Asset-backed securities | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

| Commercial paper | ||||||||||||||||||||||||||||||||

| U.S. federal agency bonds | ( | |||||||||||||||||||||||||||||||

| U.S. government bonds | ( | |||||||||||||||||||||||||||||||

| Subtotal | ( | |||||||||||||||||||||||||||||||

| Noncurrent: | ||||||||||||||||||||||||||||||||

| Asset-backed securities | ||||||||||||||||||||||||||||||||

| Subtotal | ||||||||||||||||||||||||||||||||

| Total | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||

At June 30, 2024, there were no investments available for sale that were materially less than their amortized cost.

The Company elects to recognize its interest receivable separate from its available-for-sale investments. At June 30, 2024 and December 31, 2023, the interest receivable from its available-for-sale investments recognized in prepaid expenses and other current assets was $0.2 million and $0.4 million, respectively.

Credit Risk

Financial instruments that potentially subject the Company to concentrations of credit risk consist primarily of cash and cash equivalents, short-term and long-term available-for-sale investments and accounts receivable. The Company maintains its cash and cash equivalents with high-credit quality financial institutions. Such amounts may exceed federally-insured limits.

As of June 30, 2024, three wholesalers each accounted for over 10% of the Company’s accounts receivable, at 36 %, 18 % and 15 %. At December 31, 2023, three wholesalers each accounted for over 10% of the Company’s accounts receivable, at 37 %, 19 % and 16 %. For additional information regarding the Company’s wholesalers, see Note 2, Summary of Significant Accounting Policies. EXPAREL and ZILRETTA revenues are primarily derived from major wholesalers and specialty distributors that generally have significant cash resources. The Company performs ongoing credit evaluations of its customers as warranted and generally does not require collateral. Allowances for credit losses on the Company’s accounts receivable are maintained based on historical payment patterns, current and estimated future economic conditions, aging of accounts receivable and its write-off history. As of June 30, 2024, there were $0.2 million of allowances for credit losses on its accounts receivable associated with iovera°. As of December 31, 2023, the Company did no t deem any allowances for credit losses on its accounts receivable necessary.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 24

NOTE 10—STOCKHOLDERS’ EQUITY

Accumulated Other Comprehensive Income (Loss)

The following tables illustrate the changes in the balances of the Company’s accumulated other comprehensive income (loss) for the periods presented (in thousands):

| Net Unrealized Gain (Loss) From Available-For-Sale Investments | Unrealized Foreign Currency Translation | Accumulated Other Comprehensive Income | ||||||||||||||||||

Balance at December 31, 2023 | $ | $ | $ | |||||||||||||||||

Net unrealized loss on investments, net of tax(1) | ( | — | ( | |||||||||||||||||

| Foreign currency translation adjustments | — | |||||||||||||||||||

Balance at June 30, 2024 | $ | ( | $ | $ | ||||||||||||||||

| Net Unrealized Loss From Available-For-Sale Investments | Unrealized Foreign Currency Translation | Accumulated Other Comprehensive Loss | ||||||||||||||||||

Balance at December 31, 2022 | $ | ( | $ | $ | ( | |||||||||||||||

Net unrealized gain on investments, net of tax (1) | — | |||||||||||||||||||

| Foreign currency translation adjustments | — | ( | ( | |||||||||||||||||

Balance at June 30, 2023 | $ | ( | $ | $ | ( | |||||||||||||||

Share Repurchase Program

On May 7, 2024, the Company announced that its Board of Directors has approved a new share repurchase program, effective immediately, which authorizes the Company to repurchase up to an aggregate of $150.0 million of its outstanding common stock. Repurchases under this program may be made at management’s discretion on the open market or through privately negotiated transactions. The share repurchase program may be suspended or discontinued at any time by the Company and has an expiration date of December 31, 2026.

On May 9, 2024, concurrently with the pricing of the offering of the 2029 Notes, the Company entered into separate privately negotiated agreements with certain of the initial purchasers of the 2029 Notes or their respective affiliates and/or certain other financial institutions to repurchase 837,240 shares of the Company’s common stock for a total cost of $25.1 million, inclusive of $0.1 million of accrued excise tax. The repurchase occurred on May 10, 2024.

Repurchases of the Company’s common stock are accounted for at cost and recorded as treasury stock. The excise tax on repurchases of the Company’s common stock is recorded as a cost of acquiring treasury stock. Reissued treasury stock will be accounted for at average cost. Gains or losses on reissued treasury stock arising from the difference between the average cost and the fair value of the award will be recorded in additional paid-in capital.

Pacira BioSciences, Inc. | Q2 2024 Form 10-Q | Page 25

NOTE 11—STOCK PLANS

Stock-Based Compensation

The Company recognized stock-based compensation expense in the periods presented as follows (in thousands):

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||||||

| Cost of goods sold | $ | $ | $ | $ | ||||||||||||||||||||||

| Research and development | ||||||||||||||||||||||||||

| Selling, general and administrative | ||||||||||||||||||||||||||

| Contingent consideration charges (gains), restructuring charges and other | ||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

| Stock-based compensation from: | ||||||||||||||||||||||||||

| Stock options | $ | $ | $ | $ | ||||||||||||||||||||||

| Restricted stock units | ||||||||||||||||||||||||||