0001396502falseN-2/AfalsefalsefalsefalsefalsefalsefalsefalsefalsefalseNofalsefalseIf Common Shares are sold to or through underwriters, the Prospectus Supplement will set forth any applicable sales load and the estimated offering expenses.The Advisor contractually agrees to waive a portion of its management fee and/or reimburse expenses for the fund and certain other John Hancock funds according to an asset level breakpoint schedule that is based on the aggregate net assets of all the funds participating in the waiver or reimbursement, including the fund (the participating portfolios). This waiver equals, on an annualized basis, 0.0100% of that portion of the aggregate net assets of all the participating portfolios that exceeds $75 billion but is less than or equal to $125 billion; 0.0125% of that portion of the aggregate net assets of all the participating portfolios that exceeds $125 billion but is less than or equal to $150 billion; 0.0150% of that portion of the aggregate net assets of all the participating portfolios that exceeds $150 billion but is less than or equal to $175 billion; 0.0175% of that portion of the aggregate net assets of all the participating portfolios that exceeds $175 billion but is less than or equal to $200 billion; 0.0200% of that portion of the aggregate net assets of all the participating portfolios that exceeds $200 billion but is less than or equal to $225 billion; and 0.0225% of that portion of the aggregate net assets of all the participating portfolios that exceeds $225 billion. The amount of the reimbursement is calculated daily and allocated among all the participating portfolios in proportion to the daily net assets of each participating portfolio. During its most recent fiscal year, the fund’s reimbursement amounted to 0.01% of the fund’s average daily net assets. This agreement expires on July 31, 2025, unless renewed by mutual agreement of the fund and the Advisor based upon a determination that this is appropriate under the circumstances at that time. Participants in the fund’s dividend reinvestment plan do not pay brokerage charges with respect to Common Shares issued directly by the fund. However, whenever Common Shares are purchased or sold on the NYSE or otherwise on the open market, each participant will pay a pro rata portion of brokerage trading fees, currently $0.05 per share purchased or sold. Brokerage trading fees will be deducted from amounts to be invested. Shareholders participating in the Plan may buy additional Common Shares of the fund through the Plan at any time and will be charged a $5 transaction fee plus $0.05 per share brokerage trading fee for each order. See “Distribution Policy” and “Dividend Reinvestment Plan” in the accompanying Prospectus. 0001396502 2024-02-23 2024-02-23 0001396502 2023-10-31 2023-10-31 0001396502 cik0001396502:CommonSharesMember 2024-02-23 2024-02-23 0001396502 cik0001396502:PreferredSharesMember 2024-02-23 2024-02-23 0001396502 cik0001396502:LIBORdiscontinuationriskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:LeverageRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:FixedIncomeSecuritiesRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:EsgIntegrationRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:EconomicAndMarketEventsRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:DistributionRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:DefensivePositionsRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:DividendStrategyRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:CurrencyRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:AntitakeoverProvisionsMember 2024-02-23 2024-02-23 0001396502 cik0001396502:TaxRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:SecondaryMarketForTheCommonSharesMember 2024-02-23 2024-02-23 0001396502 cik0001396502:PortfolioTurnoverRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:IlliquidAndRestrictedSecuritiesRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:CommonStockAndOtherEquitySecuritiesRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:HongKongStockConnectProgramStockConnectRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:RepurchaseAgreementRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:NonUSInvestmentRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:LargeCompanyRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:IndustryOrSectorRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:OperationalAndCybersecurityRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:MarketDiscountRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:SmallAndMidSizedCompanyRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:GreaterChinaRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:EuropeanMarketsRiskMember 2024-02-23 2024-02-23 0001396502 cik0001396502:EmergingMarketsRiskMember 2024-02-23 2024-02-23 0001396502 dei:BusinessContactMember 2024-02-23 2024-02-23 0001396502 cik0001396502:CommonSharesMember 2024-02-14 0001396502 cik0001396502:CommonSharesMember 2021-11-01 2022-01-31 0001396502 cik0001396502:CommonSharesMember 2022-02-01 2022-04-30 0001396502 cik0001396502:CommonSharesMember 2022-05-01 2022-07-31 0001396502 cik0001396502:CommonSharesMember 2022-08-01 2022-10-31 0001396502 cik0001396502:CommonSharesMember 2022-11-01 2023-01-31 0001396502 cik0001396502:CommonSharesMember 2023-02-01 2023-04-30 0001396502 cik0001396502:CommonSharesMember 2023-05-01 2023-07-31 0001396502 cik0001396502:CommonSharesMember 2023-08-01 2023-10-31 0001396502 cik0001396502:CommonSharesMember 2023-11-01 2024-01-31 0001396502 cik0001396502:CommonSharesMember 2024-02-14 2024-02-14 xbrli:pure xbrli:shares iso4217:USD iso4217:USD xbrli:shares

As filed with the Securities and Exchange

Commission on February 23, 2024

1933 Act File No. 333-276048

1940 Act File No. 811-22056

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933[x]

Pre-Effective Amendment No. 2 [x]

Post-Effective Amendment No. [

]

REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 [x]

Amendment No. 27 [x]

JOHN HANCOCK TAX-ADVANTAGED GLOBAL SHAREHOLDER YIELD FUND

(Exact Name of Registrant as Specified in Charter)

200 Berkeley Street,

Boston, Massachusetts 02116-2805

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code:

1-800-225-6020

Christopher Sechler

, Esq.200 Berkeley Street,

Boston, Massachusetts 02116-2805

Name and Address (of Agent for Service)

Copies of Communications to:

Mark P. Goshko, Esq.

K&L Gates LLP

One Congress Street

Suite 2900

Boston, MA 02114

Approximate Date of Proposed Public Offering: From time to time after the effective date of this Registration Statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis in reliance on Rule 415 under the Securities Act

of 1933, as amended, other than securities offered in connection with a dividend reinvestment plan, check the following box. [x]

If this Form is a registration statement pursuant to General Instruction A.2 or a post-effective amendment thereto, check the following box [x].

If this Form is a registration statement pursuant to General Instruction B or a post-effective amendment thereto that will become effective upon filing

with the Commission pursuant to Rule 462(e) under the Securities Act, check the following box [

].

If this Form is a post-effective amendment to a registration statement filed pursuant to General Instruction B to register additional securities or

additional classes of securities pursuant to Rule 413(b) under the Securities Act, check the following box [

].

It is proposed that this filing will become effective (check appropriate box): |

|

|

|

when declared effective pursuant to section 8(c) |

|

|

If appropriate, check the following box: |

|

This post-effective amendment designates a new effective date for a previously filed registration statement. |

|

This form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act and the Securities Act registration statement number of the earlier effective registration statement for the same offering is ________. |

|

This Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, and the Securities Act registration statement number of the earlier effective registration statement for the same offering is ________. |

|

This Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, and the Securities Act registration statement number of the earlier effective registration statement for the same offering is ________. |

|

|

Check each box that appropriately characterizes the Registrant: |

|

|

|

Registered closed-end fund. |

|

Business development company. |

|

|

|

|

|

Well-Known Seasoned Issuer (as defined by Rule 405 under the Securities Act). |

|

Emerging Growth Company (as defined by Rule 12b-2 under the Securities Exchange Act of 1934 (“Exchange Act”). |

|

|

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant

shall file a further amendment which specifically states this Registration Statement shall thereafter become effective in accordance with Section 8(a) of

the Securities Act of 1933 or until the Registration Statement shall become effective on such dates as the Commission, acting pursuant to said

Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the

Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these

securities in any state where the offer or sale is not permitted.

Base Prospectus Dated March 1, 2024

John Hancock Tax-Advantaged Global Shareholder Yield Fund

John Hancock Tax-Advantaged Global Shareholder Yield Fund (the “Fund” or “fund”) is a diversified, closed-end management investment company. The

fund commenced operations in September 2007 following an initial public offering.

The fund’s investment objective is to provide total return consisting of a high level of current income and gains and long term

capital appreciation. In pursuing its investment objective of total return, the fund will seek to emphasize high current income. In pursuing its

investment objective, the fund seeks to achieve favorable after-tax returns for its shareholders by seeking to minimize the U.S. federal income tax

consequences on income and gains generated by the fund. There can be no assurance that the fund will achieve its investment objective.

The fund may offer, from time to time, in one or more offerings, the fund’s common shares of beneficial interest, par value

$

0.01 per

share (“Common Shares”). Common Shares may be offered at prices and on terms to be set forth in one or more supplements to this Prospectus

(each, a “Prospectus Supplement”). You should read this Prospectus and the applicable Prospectus Supplement carefully before you invest in

Common Shares.

Common Shares may be offered directly to one or more purchasers, through agents designated from time to time by the fund, or to or through

underwriters or dealers. The Prospectus Supplement relating to the offering will identify any agents, underwriters or dealers involved in the offer or

sale of Common Shares, and will set forth any applicable offering price, sales load, fee, commission or discount arrangement between the fund and its

agents or underwriters, or among its underwriters, or the basis upon which such amount may be calculated, net proceeds and use of proceeds, and

the terms of any sale. The fund may not sell any Common Shares through agents, underwriters or dealers without delivery of a Prospectus Supplement

describing the method and terms of the particular offering of the Common Shares.

Under normal market conditions, the fund invests at least 80% of its total assets in a diversified portfolio of dividend-paying

securities of issuers located throughout the world. This policy is subject to the requirement that the manager believes at the time of investment that

such securities are eligible to pay tax-advantaged dividends. The fund seeks to produce superior, risk-adjusted returns by using a disciplined,

proprietary investment approach that is focused on identifying companies with strong free cash flow and that use their free cash flow to seek to

maximize “shareholder yield” through dividend payments, stock repurchases and debt reduction. By assembling a diversified portfolio of securities

which, in the aggregate, possess positive growth of free cash flow, high cash dividend yields, share buyback programs and net debt reductions, the

fund seeks to provide shareholders an attractive total return with less volatility than the global equity market as a whole. “Free cash flow” is the cash

available for distribution to investors after all planned capital investment and taxes. The Advisor (as defined below) believes that free cash flow is

important because it allows a company to pursue opportunities that enhance shareholder value.

Investment Advisor and Subadvisor.

The fund’s investment advisor is John Hancock Investment Management LLC (the “Advisor” or “JHIM”) and its

subadvisor is Epoch Investment Partners, Inc. (“Epoch”), the “subadvisor”).

The fund’s currently outstanding Common Shares are listed on the New York Stock Exchange (“NYSE”) under the symbol “HTY.”

Any new Common Shares offered and sold hereby are expected to be listed on the NYSE and trade under this symbol. As of February

14

last reported sale price for the Common Shares was $

5.05

.

Manulife, Manulife Investment Management, Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life

Insurance Company and are used by its affiliates under license.

The Common Shares have traded both at a premium and a discount to net asset value (“NAV”). The fund cannot predict whether

Common Shares will trade in the future at a premium or discount to NAV. The provisions of the Investment Company Act of 1940, as

amended, generally require that the public offering price of common shares (less any underwriting commissions and discounts) must

equal or exceed the NAV per share of a company’s common stock (calculated within 48 hours of pricing). The fund’s issuance of

Common Shares may have an adverse effect on prices in the secondary market for the Common Shares by increasing the number of

Common Shares available, which may put downward pressure on the market price for the Common Shares. Shares of common stock of

closed-end investment companies frequently trade at a discount from NAV, which may increase investors’ risk of loss.

Investing in the Common Shares involves certain risks. You could lose all or some of your investment. You should consider carefully

these risks together with all of the other information contained in this Prospectus before making a decision to purchase the fund’s

securities. See “Risk Factors” beginning on page

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of

these securities or determined whether this Prospectus is truthful or complete. Any representation to the contrary is a criminal

This Prospectus, together with any applicable Prospectus Supplement, sets forth concisely the information about the fund that a prospective investor

should know before investing. You should read this Prospectus and the applicable Prospectus Supplement, which contain important information,

before deciding whether to invest in the Common Shares. You should retain the Prospectus and Prospectus Supplement for future reference. A

Statement of Additional Information (“SAI”), dated March 1, 2024, containing additional information about the fund, has been filed with the SEC and is

incorporated by reference in its entirety into this Prospectus. The Table of Contents for the SAI is on page

44

of the Prospectus. A paper copy of the

Registration Statement or SAI may be obtained without charge by calling 800-225-6020 (toll-free) or electronically from the SEC’s website at sec.gov.

Copies of the fund’s annual report and semi-annual report and other information about the fund may be obtained upon request by writing to the fund,

by calling 800-225-6020, or by visiting the fund’s website at https://www.jhinvestments.com/investments/closed-end-fund/international-equity-funds/tax-advantaged-global-shareholder-yield-fund-ce-hty.

You also may obtain a copy of any information regarding the fund filed with the SEC from

the SEC’s website (sec.gov).

The fund’s Common Shares do not represent a deposit or obligation of, and are not guaranteed or endorsed by, any bank or other insured depositary

institution, and are not federally insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board or any other government agency.

Prospectus dated March 1, 2024

You should rely only on the information contained in, or incorporated by reference into, this Prospectus, any related Prospectus

Supplement and the SAI in making your investment decisions. The Fund has not authorized any person to provide you with different

information. If anyone provides you with different or inconsistent information, you should not rely on it. The fund is not making an offer

to sell the Common Shares in any jurisdiction where the offer or sale is not permitted. You should assume that the information in this

Prospectus and any Prospectus Supplement is accurate only as of the dates on their covers. The fund’s business, financial condition

and prospects may have changed since the date of its description in this Prospectus or the date of its description in any Prospectus

This is only a summary. You should review the more detailed information elsewhere in this prospectus (“Prospectus”), in any related

supplement to this Prospectus (each, a “Prospectus Supplement”), and in the Statement of Additional Information (the “SAI”) prior to

making an investment in the fund. See “Risk Factors”

John Hancock Tax-Advantaged Global Shareholder Yield Fund (the “fund”) is a diversified, closed-end management investment company. The fund

commenced operations in September 2007 following an initial public offering.

The fund’s investment advisor is John Hancock Investment Management LLC (the “Advisor” or “JHIM”) and its subadvisor is Epoch Investment Partners,

Inc. (“Epoch”).

The fund’s investment objective is to provide total return consisting of a high level of current income and gains and long term capital appreciation. In

pursuing its investment objective of total return, the fund will seek to emphasize high current income. In pursuing its investment objective, the fund

seeks to achieve favorable after-tax returns for its shareholders by seeking to minimize the U.S. federal income tax consequences on income and gains

generated by the fund. There can be no assurance that the fund will achieve its investment objective. The fund’s investment objective is fundamental and

may not be changed without shareholder approval.

The fund may offer, from time to time, in one or more offerings, up to 1,000,000 of the fund’s common shares of beneficial interest, par value $0.01 per

share (“Common Shares”), on terms to be determined at the time of the offering. The Common Shares may be offered at prices and on terms to be set

forth in one or more Prospectus Supplements. You should read this Prospectus and the applicable Prospectus Supplement carefully before you invest in

Common Shares. Common Shares may be offered directly to one or more purchasers, through agents designated from time to time by the fund, or to or

through underwriters or dealers. The Prospectus Supplement relating to the offering will identify any agents, underwriters or dealers involved in the

offer or sale of Common Shares, and will set forth any applicable offering price, sales load, fee, commission or discount arrangement between the fund

and its agents or underwriters, or among its underwriters, or the basis upon which such amount may be calculated, net proceeds and use of proceeds,

and the terms of any sale. See “Plan of Distribution.” The fund may not sell any Common Shares through agents, underwriters or dealers without delivery

of a Prospectus Supplement describing the method and terms of the particular offering of Common Shares.

The fund’s currently outstanding Common Shares are listed on the New York Stock Exchange (“NYSE”) under the symbol “JHI.” Any new Common Shares

offered and sold hereby will be listed on the NYSE and trade under this symbol. As of February

14

, 2024, the last reported sale price for the Common

Shares was $

5.05

.

Under normal market conditions, the fund invests at least 80% of its total assets in a diversified portfolio of dividend-paying securities of issuers located

throughout the world. This policy is subject to the requirement that the manager believes at the time of investment that such securities are eligible to

pay tax-advantaged dividends. The fund seeks to produce superior, risk-adjusted returns by using a disciplined, proprietary investment approach that is

focused on identifying companies with strong free cash flow and that use their free cash flow to seek to maximize “shareholder yield” through dividend

payments, stock repurchases and debt reduction. By assembling a diversified portfolio of securities which, in the aggregate, possess positive growth of

free cash flow, high cash dividend yields, share buyback programs and net debt reductions, the fund seeks to provide shareholders an attractive total

return with less volatility than the global equity market as a whole. “Free cash flow” is the cash available for distribution to investors after all planned

capital investment and taxes. The Advisor believes that free cash flow is important because it allows a company to pursue opportunities that enhance

shareholder value.

The fund’s investments in securities of U.S. and non-U.S. issuers are expected to vary over time. Under normal market conditions, the fund invests at

least 40% of its total assets in securities of non-U.S. issuers, unless the manager deems market conditions and/or company valuations to be less

favorable to non-U.S. issuers, in which case, the fund will invest at least 30% of its total assets in non-U.S. issuers. The fund may invest up to 20% of its

total assets in securities issued by companies located in emerging markets when Epoch, the fund’s subadvisor, believes such companies offer attractive

opportunities. Securities held by the fund may be denominated in both U.S. dollars and non-U.S. currencies. Under normal conditions, the fund invests

in the securities of issuers located in at least three different countries, including the United States, and the actual number of countries represented in

the fund’s portfolio will vary over time. As of the end of the last fiscal year, 10 countries were represented in the fund’s portfolio. The fund may not invest

more than 25% of its total assets in the securities of issuers in any single industry or group of related industries. The fund may trade securities actively

and may engage in short-term trading strategies.

On an overall basis, the fund seeks to implement an investment strategy designed to minimize the U.S. federal income tax consequences on income and

gains generated by the fund. The fund seeks to accomplish this primarily by (i) investing in dividend-paying securities that are eligible to pay dividends

that qualify for U.S. federal income taxation at rates applicable to long-term capital gain (“tax-advantaged dividends”), and complying with the holding

period and other requirements for such favorable tax treatment; and (ii) offsetting any ordinary income and realized short-term capital gain against fund

expenses and realized short-term loss. In this regard, as discussed above, the fund’s policy described above of investing at least 80% of its total assets

in dividend-paying securities of issuers located throughout the world is subject to the requirement that Epoch believes at the time of investment that

such securities are eligible to pay tax-advantaged dividends.

The fund invests in global equity securities across a broad range of market capitalizations. The fund generally invests in companies with a market

capitalization (i.e., total market value of a company’s shares) of $500 million or greater at the time of purchase. The Advisor has engaged Epoch to

serve as subadvisor to the fund. Epoch is responsible for the day-to-day management of the fund’s portfolio investments. Although the fund may invest in

securities of companies with any capitalization, it may at any given time invest a significant portion of its total assets in companies of one particular

market capitalization category when Epoch believes such companies offer attractive opportunities. Epoch seeks to produce superior, risk-adjusted

returns by investing in businesses with outstanding risk/reward profiles and a focus on high “shareholder yield.” Shareholder yield refers to the

collective financial impact on shareholders from the return of free cash flow through cash dividends, stock repurchases and debt reduction. By

assembling a diversified portfolio of securities with these qualities, Epoch believes fund investors will have the opportunity to realize an attractive total

return with less volatility than the global equity market as a whole.

Epoch seeks to produce an efficient portfolio on a risk/return basis with a dividend yield that exceeds the dividend yield of the MSCI World Index. The

MSCI World Index captures large- and mid- cap representation across 23 developed market countries. With approximately 1,511 constituents, the

index covers approximately 85% of the free float-adjusted market capitalization in each country as of October 31, 2023. In selecting securities for the

fund, Epoch utilizes an investment strategy that combines bottom-up stock research and selection with top-down analysis. Epoch looks for companies it

believes have solid long-term prospects, attractive valuation comparisons and adequate market liquidity. The equity securities Epoch finds attractive

generally have valuations lower than Epoch’s estimate of their fundamental value, as reflected in price-to-cash flow, price-to-book ratios or other stock

valuation measures.

In selecting securities for the fund’s portfolio, Epoch focuses on dividend-paying common stocks and to a lesser extent preferred securities that produce

an attractive level of tax-advantaged income. Epoch also considers an equity security’s potential for capital appreciation. Epoch generally uses a value

approach in selecting the fund’s equity investments. Epoch evaluates an equity security’s potential value, including the attractiveness of its market

valuation, based on the company’s assets and prospects for earnings growth. Investment decisions are made primarily on the basis of fundamental

research. Epoch relies upon information provided by, and the expertise of, Epoch’s research staff in making investment decisions. In selecting equity

securities, Epoch considers (among other factors) a company’s cash flow capabilities, dividend prospects and the anticipated U.S. federal income tax

treatment of a company’s dividends, the strength of the company’s business franchises and estimates of the company’s net value.

Epoch sells or reduces a position in a security when it sees the goals of its investment thesis failing to materialize, or when it believes those goals have

been met and the valuation of the company’s shares fully reflect the opportunities once thought unrecognized in share price. The reasons for a

determination by Epoch that such goals are not being met include: the economic or competitive environment might be changing; company

management’s execution could be disappointing; or in certain cases, management proves to be less than forthright or have an inappropriate

assessment of the company’s state and the task at hand.

The fund may seek to enhance the level of dividend income it receives by engaging in dividend capture trading. In a dividend capture trade, the fund sells

a security after having held the security long enough to satisfy the holding period requirements for tax-advantaged dividends, but shortly after the

security’s ex-dividend date. The fund then uses the sale proceeds to purchase one or more other securities that are expected to pay dividends before the

next dividend payment date on the security being sold. Through this practice, the fund may receive more dividend payments over a given period of time

than if it held a single security. Receipt of a greater number of dividend payments during a given time period could augment the total amount of dividend

income received by the fund. See “Investment Strategies—Equity Strategy.”

. Under normal market conditions, the fund invests primarily in a diversified portfolio of dividend-paying securities of issuers

located throughout the world that Epoch believes at the time of investment are eligible to pay tax-advantaged dividends.

Tax-advantaged dividends generally include dividends from U.S. and non-U.S. corporations that meet certain specified criteria. The fund generally can

pass the tax treatment of tax-advantaged dividends it receives through to its holders of Common Shares (the “Common Shareholders”). For the fund to

receive tax-advantaged dividends, the fund must, in addition to other requirements, hold the otherwise qualified security for more than 60 days during

the 121-day period beginning 60 days before the ex-dividend date (or, in the case of a preferred security, more than 90 days during the 181-day period

beginning 90 days before the ex-dividend date). The “ex-dividend date” is the date that is established by a stock exchange (usually two business days

before the record date) whereby the owner of a security at the commencement of such date is entitled to receive the next issued dividend payment for

such security, even if the security is sold by such owner on the ex-dividend date or thereafter. In addition, the fund cannot be obligated to make

payments (pursuant to a short sale or otherwise) with respect to substantially similar or related property. For a Common Shareholder to be taxed at the

long-term capital gain rates, the Common Shareholder must hold his or her Common Shares for more than 60 days during the 121-day period

beginning 60 days before the ex-dividend date. Consequently, short-term investors in the fund will not realize the benefits of tax-advantaged dividends.

There can be no assurance as to the portion of the fund’s dividends that will be tax-advantaged. Although the fund invests at least 80% of its assets in

equity securities that pay tax-advantaged dividends and to satisfy the holding period and other requirements, a portion of the fund’s income

distributions may be taxable as ordinary income (i.e., income other than tax-advantaged dividends).

The foregoing policies relating to investments in equity securities are the fund’s primary investment policies. In addition to its primary investment

policies, the fund may invest to a limited extent in other types of securities and engage in certain other investment practices. The fund may use a variety

of derivative instruments (including long and short positions) for hedging purposes, to adjust portfolio characteristics or more generally for purposes of

attempting to increase the fund’s investment return, including put and call options, options on futures contracts, futures and forward contracts and

swap agreements (including total return swaps) with respect to securities, indices and currencies. The fund may invest in securities of other open- and

closed-end investment companies, including exchange-traded funds, to the extent that such investments are consistent with the fund’s investment

objective and policies and permissible under the Investment Company Act of 1940, as amended (the “1940 Act”). The fund may lend its portfolio

securities. The fund may invest in debt securities, including below investment-grade debt securities (also known as “junk bonds”). See “Investment

Strategies.” Normally, the fund invests substantially all of its total assets to meet its investment objective. The fund may invest the remainder of its

assets in other equity securities and fixed-income securities with remaining maturities of less than one year or cash equivalents, or it may hold cash. For

temporary defensive purposes, the fund may depart from its principal investment strategies and invest part or all of its total assets in fixed-income

securities with remaining maturities of less than one year, or cash or cash equivalents. During such periods, the fund may not be able to achieve its

investment objective.

Investment Advisor and Subadvisor

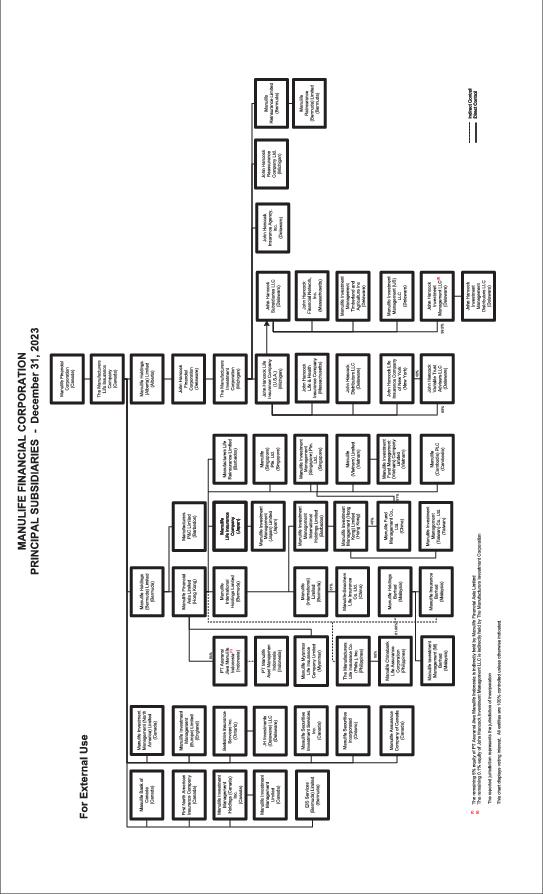

JHIM, the fund’s investment advisor, is an indirect principally owned subsidiary of and subadvisor Manulife Financial Corporation. The Advisor is

responsible for overseeing the management of the fund, including its day-to-day business operations and monitoring Epoch. As of December 31, 2023,

the Advisor had total assets under management of approximately $

153.7

billion.

Epoch, the subadvisor to the fund, handles the fund’s portfolio management activities, subject to oversight by the Advisor. Epoch, founded in 2004, is a

wholly-owned subsidiary of The Toronto-Dominion Bank. As of December 31, 2023, Epoch managed on a worldwide basis approximately $

34.3

billion.

The Advisor also engaged its affiliate Manulife Investment Management (North America) Limited (formerly, John Hancock Asset Management a division

of Manulife Asset Management (North America) Limited) to consult from time to time with the Advisor on matters relating to the general application of

U.S. federal income tax laws and regulations, compliance and legal issues.

See “Management of the Fund—The Advisor” and “—The Subadvisor.”

The fund makes regular quarterly distributions to Common Shareholders which may consist of the fund’s cash available for distribution and return of

capital. “Cash available for distribution” consists of the fund’s (i) investment company taxable income, which includes among other things, dividend and

ordinary income after payment of fund expenses, the excess of net short-term capital gain over net long-term capital loss, and income from certain

hedging and interest rate transactions, (ii) qualified dividend income and (iii) long-term capital gain (gain from the sale of capital assets held longer than

one year). The Board of Trustees of the fund (the “Board”) may modify this distribution policy at any time without obtaining the approval of Common

Shareholders.

Pursuant to the requirements of the 1940 Act, in the event the fund makes distributions from sources other than income, a notice will accompany each

quarterly distribution with respect to the estimated sources of the distribution made. Such notices will describe the portion, if any, of the quarterly

dividend which, in the fund’s good faith judgment, constitutes long-term capital gain, short-term capital gain, investment company taxable income or a

return of capital. The actual character of such dividend distributions for U.S. federal income tax purposes, however, will only be determined finally by the

fund at the close of its fiscal year, based on the fund’s full year performance and its actual net investment company taxable income and net capital gain

for the year, which may result in a recharacterization of amounts distributed during such fiscal year from the characterization in the quarterly estimates.

If, for any calendar year, as discussed above, the total distributions made exceed the fund’s current and accumulated earnings and profits, the excess

generally will be treated as a return of capital to each Common Shareholder (up to the amount of the Common Shareholder’s basis in his or her Common

Shares) and thereafter as gain from the sale of Common Shares. In each fiscal year the fund has paid distributions, the fund’s total distributions

exceeded the fund’s current and accumulated earnings and profits, and such excess was treated as a return of capital to each Common Shareholder.

The amount treated as a return of capital reduces the Common Shareholder’s adjusted basis in his or her Common Shares, thereby increasing his or her

potential gain or reducing his or her potential loss on the subsequent sale of his or her Common Shares. Distributions in any year may include a

substantial return of capital component. To permit the fund to maintain more stable distributions, distribution rates are based on projected annual cash

available for distribution and return of capital. As a result, the distributions paid by the fund for any particular quarter may be more or less than the

amount of cash available for distribution from that quarterly period. In certain circumstances, the fund may be required to sell a portion of its

investment portfolio to fund distributions. Distributions will reduce the Common Shares’ net asset value (“NAV”).

The 1940 Act currently limits the number of times the fund may distribute long-term capital gain in any tax year, which may increase the variability of

the fund’s distributions and result in certain distributions being comprised more heavily of long-term capital gain eligible for favorable income tax rates.

In the future, the Advisor may seek Board approval to implement a managed distribution plan for the fund. The managed distribution plan would be

implemented pursuant to an exemptive order previously granted by the Securities and Exchange Commission (the “SEC”), which provides an exemption

from Section 19(b) of the 1940 Act and Rule 19b-1 thereunder to permit the fund to include long-term capital gain as a part of its regular distributions

to Common Shareholders more frequently than would otherwise be permitted by the 1940 Act (generally once or twice per year). If the fund implements

a managed distribution plan, it would do so without a vote of the Common Shareholders.

Dividend Reinvestment Plan

The fund has established an automatic dividend reinvestment plan (the “Plan”). Under the Plan, distributions of dividends and capital gains are

automatically reinvested in Common Shares of the fund by Computershare Trust Company, N.A. Every shareholder holding at least one full share of the

fund will be automatically enrolled in the Plan. Shareholders who do not participate in the Plan will receive all distributions in cash. Common

Shareholders who intend to hold their Common Shares through a broker or nominee should contact such broker or nominee regarding the Plan. See

“Dividend Reinvestment Plan.”

Closed-End Fund Structure

Closed-end funds differ from open-end management investment companies (which generally are referred to as “mutual funds”) in that closed-end funds

generally list their shares for trading on a securities exchange and do not redeem their shares at the option of the shareholder. Mutual funds do not

trade on securities exchanges and issue securities redeemable at the option of the shareholder. The continuous outflows of assets in a mutual fund can

make it difficult to manage the fund’s investments. Closed-end funds generally are able to stay more fully invested in securities that are consistent with

their investment objectives and also have greater flexibility to make certain types of investments and to use certain investment strategies, such as

financial leverage and investments in illiquid securities. Although the fund has no current intention to do so, the fund is authorized and reserves the

flexibility to utilize leverage through borrowings and/or the issuance of preferred shares, including the issuance of debt securities. The Common Shares

are designed primarily for long-term investors; you should not purchase Common Shares if you intend to sell them shortly after purchase.

Common shares of closed-end funds frequently trade at prices lower than their NAV. Since inception, the market price of the Common Shares has

fluctuated and at times has traded below the fund’s NAV and at times has traded above the fund’s NAV. The fund cannot predict whether in the future the

Common Shares will trade at, above or below NAV. In addition to NAV, the market price of the Common Shares may be affected by such factors as the

fund’s dividend stability, dividend levels, which are in turn affected by expenses, and market supply and demand.

In recognition of the possibility that the Common Shares may trade at a discount from their NAV, and that any such discount may not be in the best

interest of Common Shareholders, the Board, in consultation with the Advisor, from time to time may review possible actions to reduce any such

discount. There can be no assurance that the Board will decide to undertake any of these actions or that, if undertaken, such actions would result in the

Common Shares trading at a price equal to or close to NAV per Common Share. In the event that the fund conducts an offering of new Common Shares

and such offering constitutes a “distribution” under Regulation M, the fund and certain of its affiliates may be subject to an applicable restricted period

that could limit the timing of any repurchases by the fund.

The fund’s principal risk factors are listed below by general risks, and equity strategy risks. The fund’s main risks are listed below in alphabetical order,

not in order of importance. Before investing, be sure to read the additional descriptions of these risks beginning on page

of this Prospectus.

Anti-takeover Provisions.

The fund’s Declaration of Trust includes provisions that could limit the ability of other persons or entities to acquire control

of the fund or to change the composition of its Board. These provisions may deprive shareholders of opportunities to sell their Common Shares at a

premium over the then current market price of the Common Shares. See “Certain Provisions in the Declaration of Trust and By-Laws—Anti-takeover

provisions.”

Defensive Positions Risk.

During periods of adverse market or economic conditions, the fund may temporarily invest all or a substantial portion of its

total assets in short-term money market instruments, securities with remaining maturities of less than one year, cash or cash equivalents. The fund will

not be pursuing its investment objective in these circumstances and could miss favorable market developments.

There can be no assurance that quarterly distributions paid by the fund to shareholders will be maintained at current levels or

increase over time. The quarterly distributions shareholders receive from the fund are derived from the fund’s dividends and interest income after

payment of fund expenses. The fund’s cash available for distribution may vary widely over the short- and long-term. If, for any calendar year, the total

distributions made exceed the fund’s net investment taxable income and net capital gain, the excess generally will be treated as a return of capital to

each Common Shareholder (up to the amount of the Common Shareholder’s basis in his or her Common Shares) and thereafter as gain from the sale of

Common Shares. The amount treated as a return of capital reduces the Common Shareholder’s adjusted basis in his or her Common Shares, thereby

increasing his or her potential gain or reducing his or her potential loss on the subsequent sale of his or her Common Shares. Distributions in any year

may include a substantial return of capital component.

Economic and market events risk.

Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreign

central banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impact

performance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Banks and financial services companies

could suffer losses if interest rates rise or economic conditions deteriorate.

Although the fund has no current intention to do so, the fund is authorized and reserves the flexibility to utilize leverage through

borrowings and/or the issuance of preferred shares, including the issuance of debt securities. In the event that the fund determines in the future to use

investment leverage, there can be no assurance that such a leveraging strategy will be successful during any period in which it is employed. Leverage

creates risks for Common Shareholders, including the likelihood of greater volatility of the NAV and market price of the Common Shares and the risk

that fluctuations in distribution rates on any preferred shares or fluctuations in borrowing costs may affect the return to Common Shareholders. To the

extent the returns derived from securities purchased with proceeds received from leverage exceeds the cost of leverage, the fund’s distributions may be

greater than if leverage had not been used. Conversely, if the returns from the securities purchased with such proceeds are not sufficient to cover the

cost of leverage, the amount available for distribution to Common Shareholders will be less than if leverage had not been used. In the latter case, the

Advisor, in its best judgment, may nevertheless determine to maintain the fund’s leveraged position if it deems such action to be appropriate. The costs

of an offering of preferred shares and/or a borrowing program would be borne by Common Shareholders and consequently would result in a reduction

of the NAV of Common Shares. In addition, the fee paid to the Advisor is calculated on the basis of the fund’s average daily gross assets, including

proceeds from borrowings and/or the issuance of preferred shares, so the fee will be higher when leverage is utilized, which may create an incentive for

the Advisor to employ financial leverage.

LIBOR discontinuation risk.

The official publication of the London Interbank Offered Rate (LIBOR), which many debt securities, derivatives and other

financial instruments traditionally utilized as the reference or benchmark rate for interest rate calculations, was discontinued as of June 30, 2023.

However, a subset of British pound sterling and U.S. dollar LIBOR settings will continue to be published on a “synthetic” basis. The synthetic publication

of the three-month sterling LIBOR will continue until March 31, 2024, and the publication of the one-, three- and six-month U.S. dollar LIBOR will

continue until September 30, 2024. The discontinuation of LIBOR and a transition to replacement rates may lead to volatility and illiquidity in markets

and may adversely affect the fun

d’

s performance.

The fund’s Common Shares will be offered only when Common Shares of the fund are trading at a price equal to or above the

fund’s NAV per Common Share plus the per Common Share amount of commissions. As with any security, the market value of the Common Shares may

increase or decrease from the amount initially paid for the Common Shares. The fund’s Common Shares have traded at both a premium and at a

discount to NAV. The shares of closed-end management investment companies frequently trade at a discount from their NAV. This characteristic is a risk

separate and distinct from the risk that the fund’s NAV could decrease as a result of investment activities. Investors bear a risk of loss to the extent that

the price at which they sell their shares is lower in relation to the fund’s NAV than at the time of purchase, assuming a stable NAV.

Operational and cybersecurity risk.

Cybersecurity breaches may allow an unauthorized party to gain access to fund assets, customer data, or

proprietary information, or cause a fund or its service providers to suffer data corruption or lose operational functionality. Similar incidents affecting

issuers of a fund’s securities may negatively impact performance. Operational risk may arise from human error, error by third parties, communication

errors, or technology failures, among other causes.

The fund may engage in short-term trading strategies, and securities may be sold without regard to the length of time held

when, in the opinion of Epoch, investment considerations warrant such action. In addition, the fund’s dividend capture program also may increase the

level of portfolio turnover the fund experiences. These policies may have the effect of increasing the annual rate of portfolio turnover of the fund. Higher

rates of portfolio turnover likely would result in higher brokerage commissions and may generate short-term capital gain taxable as ordinary income,

which may have a negative impact on the fund’s performance over time. The portfolio turnover rate of the fund may vary from year to year, as well as

within a year.

Secondary Market for the Common Shares.

The issuance of new Common Shares may have an adverse effect on the secondary market for the

Common Shares. When Common Shares are trading at a premium, the fund may issue new Common Shares of the fund. The increase in the amount of

the fund’s outstanding Common Shares resulting from the offering of new Common Shares may put downward pressure on the market price for the

Common Shares of the fund. Common Shares will not be issued at any time when Common Shares are trading at a price lower than a price equal to the

fund’s NAV per Common Share plus the per Common Share amount of commissions.

The fund also issues Common Shares through its dividend reinvestment plan. Common Shares may be issued under the plan at a discount to the market

price for such Common Shares, which may put downward pressure on the market price for Common Shares of the fund.

The voting power of current Common Shareholders will be diluted to the extent that such shareholders do not purchase shares in any future Common

Share offerings or do not purchase sufficient shares to maintain their percentage interest. In addition, if the proceeds of such offering are unable to be

invested as intended, the fund’s per Common Share distribution may decrease (or may consist of return of capital) and the fund may not participate in

market advances to the same extent as if such proceeds were fully invested as planned.

To qualify for the special tax treatment available to regulated investment companies, the fund must: (i) derive at least 90% of its annual gross

income from certain kinds of investment income; (ii) meet certain asset diversification requirements at the end of each quarter; and (iii) distribute in

each taxable year at least 90% of its net investment income (including net interest income and net short-term capital gain). If the fund failed to meet any

of these requirements, subject to the opportunity to cure such failures under applicable provisions of the Internal Revenue Code of 1986, as amended

(the “Code”), the fund would be subject to U.S. federal income tax at regular corporate rates on its taxable income, including its net capital gain, even if

such income were distributed to its shareholders. All distributions by the fund from earnings and profits, including distributions of net capital gain (if

any), would be taxable to the shareholders as ordinary income. To the extent designated by the fund, such distributions generally would be eligible (i) to

be treated as qualified dividend income in the case of individual and other non-corporate shareholders and (ii) for the dividends received deduction in

the case of corporate shareholders, provided that in each case the shareholder meets applicable holding period requirements. In addition, in order to

requalify for taxation as a regulated investment company, the fund might be required to recognize unrealized gain, pay substantial taxes and interest,

and make certain distributions. See “U.S. Federal Income Tax Matters.”

The tax treatment and characterization of the fund’s distributions may vary significantly from time to time due to the nature of the fund’s investments.

The ultimate tax characterization of the fund’s distributions in a calendar year may not finally be determined until after the end of that calendar year. The

fund may make distributions during a calendar year that exceed the fund’s net investment income and net realized capital gain for that year. In such a

situation, the amount by which the fund’s total distributions exceed net investment income and net realized capital gain generally would be treated as a

return of capital up to the amount of the Common Shareholder’s tax basis in his or her Common Shares, with any amounts exceeding such basis treated

as gain from the sale of his or her Common Shares. The fund’s income distributions that qualify for favorable tax treatment may be affected by Internal

Revenue Service (“IRS”) interpretations of the Code and future changes in tax laws and regulations all of which may apply with retroactive effect. See

“U.S. Federal Income Tax Matters.”

No assurance can be given as to what percentage of the distributions paid on the Common Shares, if any, will consist of long-term capital gain or what

the tax rates on various types of income will be in future years.

Common Stock and Other Equity Securities Risk.

The fund invests primarily in common stocks, and to a lesser extent in preferred securities.

Common stock, preferred securities and other equity securities represent equity ownership in a company. Common stocks and similar equity securities

are more volatile and more risky than some other forms of investment. The price of equity securities will fluctuate, and can decline and reduce the value

of the fund. Therefore, the value of your investment in the fund may fluctuate and may be worth less than your initial investment. The price of equity

securities fluctuates based on changes in a company’s financial condition, and overall market and economic conditions. The value of equity securities

purchased by the fund could decline if the financial condition of the companies in which the fund invests declines, or if overall market and economic

conditions deteriorate. Even if the fund invests in high-quality or “blue chip” equity securities, or securities of established companies with large market

capitalizations (which generally have strong financial characteristics), the fund can be negatively impacted by poor overall market and economic

conditions.

The fund also may invest in securities that can be exercised for or converted into common stocks (such as convertible preferred securities). Because

convertible securities can be converted into equity securities, their values normally will increase or decrease as the values of the underlying equity

securities increase or decrease.

The fund maintains substantial exposure to equities and generally does not attempt to time the market. Because of this exposure, the possibility that

stock market prices in general will decline over short or extended periods subjects the fund to unpredictable declines in the value of its investments, as

well as periods of poor performance. In addition, common stock prices may be sensitive to rising interest rates, as the costs of capital rise for issuers.

Epoch may not be able to anticipate the level of dividends that companies will pay in any given timeframe. In accordance with

the fund’s strategies, Epoch attempts to identify and take advantage of opportunities such as the announcement of major corporate actions that may

lead to high current dividend income. These situations typically are non-recurring or infrequent, may be difficult to predict and may not result in an

opportunity that allows Epoch to fulfill the fund’s investment objective. In addition, the dividend policies of the fund’s target companies are heavily

influenced by the current economic climate and the favorable U.S. federal tax treatment afforded to dividends.

When a fund invests a substantial portion of its assets in a particular industry or sector of the economy, the fund’s investments are not as

varied as the investments of most funds and are far less varied than the broad securities markets. As a result, the fund’s performance tends to be more

volatile than other funds, and the values of the fund’s investments tend to go up and down more rapidly. In addition, to the extent that a fund invests

significantly in a particular industry or sector, it is particularly susceptible to the impact of market, economic, regulatory and other factors affecting that

industry or sector. The principal risks of investing in certain sectors are described below.

Illiquid and Restricted Securities Risk.

Restricted securities are securities with restrictions on public resale, such as securities offered in

accordance with an exemption under Rule 144A under the Securities Act of 1933 (the “1933 Act”), or commercial paper issued under Section 4(a)(2)

of the 1933 Act. Restricted securities are often required to be sold in private sales to institutional buyers, markets for restricted securities may or may

not be well developed, and restricted securities can be illiquid. Illiquid and restricted securities may be difficult to value and may involve greater risks

than liquid securities. Illiquidity may have an adverse impact on a particular security’s market price and the fund’s ability to sell the security. The fund

may invest up to 15% of its net assets in securities for which there is no readily available trading market or which are otherwise illiquid. The extent (if at

all) to which a security may be sold or a derivative position closed without negatively impacting its market value may be impaired by reduced market

activity or participation, legal restrictions, or other economic and market impediments. Liquidity risk may be magnified in rising interest rate

environments due to higher than normal redemption rates. Widespread selling of fixed-income securities to satisfy redemptions during periods of

reduced demand may adversely impact the price or salability of such securities. Periods of heavy redemption could cause the fund to sell assets at a

loss or depressed value, which could negatively affect performance. Redemption risk is heightened during periods of declining or illiquid markets. Any

depositary receipts are subject to most of the risks associated with investing in foreign securities directly because the value of a depositary receipt is

dependent upon the market price of the underlying foreign equity security. Depositary receipts are also subject to liquidity risk.

Larger companies may grow more slowly than smaller companies or be slower to respond to business developments.

Large-capitalization securities may underperform the market as a whole.

Non-U.S. Investment Risk.

As compared to U.S. companies, less information may be publicly available regarding foreign issuers. Non-U.S. securities

may be subject to foreign taxes and may be more volatile than U.S. securities. Currency fluctuations and political and economic developments may

adversely impact the value of foreign securities. If applicable, depository receipts are subject to most of the risks associated with investing in foreign

securities directly because the value of a depository receipt is dependent upon the market price of the underlying foreign equity security. Depository

receipts are also subject to liquidity risk. Investments in emerging-market countries are subject to greater levels of non-U.S. investment risk.

Repurchase agreement risk.

Repurchase agreements are arrangements involving the purchase of an obligation and the simultaneous agreement to

resell the same obligation on demand or at a specified future date and at an agreed-upon price. A repurchase agreement can be viewed as a loan made

by the fund to the seller of the obligation with such obligation serving as collateral for the seller’s agreement to repay the amount borrowed with interest.

Repurchase agreements provide the opportunity to earn a return on cash that is only temporarily available. Repurchase agreements may be entered

with banks, brokers, or dealers. However, a repurchase agreement will only be entered with a broker or dealer if the broker or dealer agrees to deposit

additional collateral should the value of the obligation purchased decrease below the resale price.

Generally, repurchase agreements are of a short duration, often less than one week but on occasion for longer periods. Securities subject to repurchase

agreements will be valued every business day and additional collateral will be requested if necessary so that the value of the collateral is at least equal

to the value of the repurchase obligation, including the interest accrued thereon.

The subadvisor shall engage in a repurchase agreement transaction only with those banks or broker dealers who meet the subadvisor’s quantitative and

qualitative criteria regarding creditworthiness, asset size and collateralization requirements. The Advisor also may engage in repurchase agreement

transactions on behalf of the fund. The counterparties to a repurchase agreement transaction are limited to a:

Federal Reserve System member bank;

primary government securities dealer reporting to the Federal Reserve Bank of New York’s Market Reports Division; or

broker dealer that reports U.S. government securities positions to the Federal Reserve Board.

The fund also may participate in repurchase agreement transactions utilizing the settlement services of clearing firms that meet the subadvisors'

creditworthiness requirements.

The Advisor and the subadvisor will continuously monitor repurchase agreement transactions to ensure that the collateral held with respect to a

repurchase agreement equals or exceeds the amount of the obligation.

The risk of a repurchase agreement transaction is limited to the ability of the seller to pay the agreed-upon sum on the delivery date. In the event of

bankruptcy or other default by the seller, the instrument purchased may decline in value, interest payable on the instrument may be lost and there may

be possible difficulties and delays in obtaining collateral and delays and expense in liquidating the instrument. If an issuer of a repurchase agreement

fails to repurchase the underlying obligation, the loss, if any, would be the difference between the repurchase price and the underlying obligation’s

market value. A fund also might incur certain costs in liquidating the underlying obligation. Moreover, if bankruptcy or other insolvency proceedings are

commenced with respect to the seller, realization upon the underlying obligation might be delayed or limited.

Small and mid-sized company risk.

Small and mid-sized companies are generally less established and may be more volatile than larger companies.

Small and/or mid-capitalization securities may underperform the market as a whole.

Given the risks described above, an investment in Common Shares may not be appropriate for all investors. You should carefully

consider your ability to assume these risks before making an investment in the fund.

The purpose of the table below is to help you understand all fees and expenses that you, as a Common Shareholder, would bear directly or indirectly. In

accordance with SEC requirements, the table below shows the fund’s expenses as a percentage of its average net assets as of October 31, 2023, and

not as a percentage of total assets. By showing expenses as a percentage of average net assets, expenses are not expressed as a percentage of all of

the assets in which the fund invests. The offering costs to be paid or reimbursed by the fund are not included in the Annual Expenses table below.

However, these expenses will be borne by Common Shareholders and may result in a reduction in the NAV of the Common Shares. See “Management of

the Fund” and “Dividend Reinvestment Plan.” The table and example are based on the fund’s capital structure as of October 31, 2023.

Shareholder Transaction Expenses (%) |

|

Sales load ( as a percentage of offering price | |

Offering expenses ( as a percentage of offering price | |

Dividend Reinvestment Plan fees 2 |

|

Percentage of Net Assets Attributable to Common Shares | |

| |

|

| |

|

Total Annual Operating Expenses |

|

Contractual expense reimbursement 3 |

|

Total annual fund operating expenses after expense reimbursements |

|

If Common Shares are sold to or through underwriters, the Prospectus Supplement will set forth any applicable sales load and the estimated offering expenses.

Participants in the fund’s dividend reinvestment plan do not pay brokerage charges with respect to Common

Sha

res issued directly by the fund. However, whenever

Common Shares are purchased or sold on the NYSE or otherwise on the open market, each participant will pay a pro rata portion of brokerage trading fees, currently

$0.05 per share purchased or sold. Brokerage trading fees will be deducted from amounts to be invested. Shareh

old

ers participating in the Plan may buy additional

Common Sh

a

res of the fund through the Plan at any time and will be charged a $5 transaction fee plus $0.05 per share brokerage trading fee for each

order. Se

e

“Distribution Policy” and “Dividend Reinvestmen

t Pla

n” in the accompanying Prospectus.

The Advisor contractually agrees to waive a portion of its management fee and/or reimburse expenses for the fund and certain other John Hancock funds according to

an asset level breakpoint schedule that is based on the aggregate net assets of all the funds participating in the waiver or reimbursement, including the fund (the

participating portfolios). This waiver equals, on an annualized basis, 0.0100% of that portion of the aggregate net assets of all the participating portfolios that

exceeds $75 billion but is less than or equal to $125 billion; 0.0125% of that portion of the aggregate net assets of all the participating portfolios that exceeds

$125 billion but is less than or equal to $150 billion; 0.0150% of that portion of the aggregate net assets of all the participating portfolios that exceeds $150 billion

but is less than or equal to $175 billion; 0.0175% of that portion of the aggregate net assets of all the participating portfolios that exceeds $175 billion but is less

than or equal to $200 billion; 0.0200% of that portion of the aggregate net assets of all the participating portfolios that exceeds $200 billion but is less than or equal

to $225 billion; and 0.0225% of that portion of the aggregate net assets of all the participating portfolios that exceeds $225 billion. The amount of the

reimbursement is calculated daily and allocated among all the participating portfolios in proportion to the daily net assets of each participating portfolio. During its

most recent fiscal year, the fund’s reimbursement amounted to 0.01% of the fund’s average daily net assets. This agreement expires on July 31, 2025, unless renewed

by mutual agreement of the fund and the Advisor based upon a determination that this is appropriate under the circumstances at that time.

The following example illustrates the expenses that Common Shareholders would pay on a $1,000 inv

e

stment in Common Shares, assuming (i) total

annual expenses set forth above, including any reimbursements through their current expiration date; (ii) a 5% annual return; and (iii) all distributions

are reinvested at NAV:

The above table and example and the assumption in the example of a 5% annual return are required by regulations of the SEC that are applicable to all

investment companies; the assumed 5% annual return is not a prediction of, and does not represent, the projected or actual performance of the

Common Shares. For more complete descriptions of certain of the fund’s costs and expenses, see “Management of the fund”. In addition, while the

example assumes reinvestment of all dividends and distributions at NAV, participants in the fund’s dividend reinvestment plan may receive Common

Shares purchased or issued at a price or value different from NAV. See “Distribution Policy” and “Dividend Reinvestment Plan.” The example does not

include sales load or estimated offering costs, which would cause the expenses shown in the example to increase.

The example should not be considered a representation of past or future expenses, and the fund’s actual expenses may be greater or less

than those shown. Moreover, the fund’s actual rate of return may be greater or less than the hypothetical 5% return shown in the

This table details the financial performance of the Common Shares, including total return information showing how much an investment in the fund has

increased or decreased each period (assuming reinvestment of all dividends and distributions).

The financial statements of the fund as of October 31, 2023, 2022, 2021, 2020, and 2019 have been audited by

PricewaterhouseCoopers LLP

(“

PwC

”)

, the fund’s independent registered public accounting firm. The report of

PwC

, along with the fund’s financial statements in the fund’s annual

report for the fiscal period ended October 31, 2023, has been incorporated by reference into the SAI. Copies of the fund’s most recent annual and

semi-annual reports are available upon request.

| |

|

|

|

|

|

Per share operating performance |

|

|

|

|

|

Net asset value, beginning of period |

|

|

|

|

|

| |

|

|

|

|

|

Net realized and unrealized gain (loss) on investments |

|

|

|

|

|

Total from investment operations |

|

|

|

|

|

| |

|

|

|

|

|

From net investment income |

|

|

|

|

|

From tax return of capital |

|

|

|

|

|

| |

|

|

|

|

|

Anti-dilutive impact of repurchase plan |

|

|

|

|

|

Net asset value, end of period |

|

|

|

|

|

Per share market value, end of period |

|

|

|

|

|

Total return at net asset value (%) |

|

|

|

|

|

Total return at market value (%) |

|

|

|

|

|

Ratios and supplemental data |

|

|

|

|

|

Net assets, end of period (in millions) |

|

|

|

|

|

Ratios (as a percentage of average net assets): |

|

|

|

|

|

Expenses before reductions |

|

|

|

|

|

Expenses including reductions |

|

|

|

|

|

| |

|

|

|

|

|

| |

|

|

|

|

|

Based on average daily shares outstanding.

Less than $0.005 per share.

The repurchase plan was completed at an average repurchase price of $6.97 for 24,933 shares and $6.80 for 106,001 shares for the periods ended 10-31-20 and

10-31-19, respectively.

Total return based on net asset value reflects changes in the fund’s net asset value during each period. Total return based on market value reflects changes in market

value. Each figure assumes that distributions from income, capital gains and tax return of capital, if any, were reinvested.

Total returns would have been lower had certain expenses not been reduced during the applicable periods.

|

|

|

|

|

|

Per share operating performance |

|

|

|

|

|

Net asset value, beginning of period |

|

|

|

|

|

|

|

|

|

|

|

Net realized and unrealized gain (loss) on investments |

| |

| | |

Total from investment operations |

| |

| | |

|

|

|

|

|

|

From net investment income |

|

|

|

|

|

From tax return of capital |

| | | | |

|

| | | | |

Anti-dilutive impact of shelf offering |

|

|

|

|

|

Net asset value, end of period |

|

|

|

|

|

Per share market value, end of period |

|

|

|

|

|

Total return at net asset value (%) | | |

| | |

Total return at market value (%) | | | |

| |

Ratios and supplemental data |

|

|

|

|

|

Net assets, end of period (in millions) |

|

|

|

|

|

Ratios (as a percentage of average net assets): |

|

|

|

|

|

Expenses before reductions |

|

|

|

|

|

Expenses including reductions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Based on average daily shares outstanding.

Total return based on net asset value reflects changes in the fund’s net asset value during each period. Total return based on market value reflects changes in market

value. Each figure assumes that distributions from income, capital gains and tax return of capital, if any, were reinvested.

Total returns would have been lower had certain expenses not been reduced during the applicable periods.

Market and Net Asset Value Information

The fund’s currently outstanding Common Shares are listed on the New York Stock Exchange (“NYSE”) under the symbol “HTY” and commenced trading

on the NYSE o

n

September 26, 2007.

The Common Shares have traded both at a premium and a discount to their net asset value (“NAV”). The fund cannot predict whether its shares will trade

in the future at

a

premium or discount to NAV. The provisions of the 1940 Act generally require that the public offering price of common shares (less any

underwriting commissions and discounts) must equal or exceed the NAV per share of a company’s common stock (calculated within 48 hours of

pricing). The fund’s issuance of Common Shares may have an adverse effect on prices in the secondary market for Common Shares by increasing the

number of Common Shares available, which may put downward pressure on the market price for Common Shares. Shares of common stock of

closed-end investment companies frequently trade at a discount from NAV. See “Risk Factors—General Risks—Market Discount Risk” and “—Secondary

Market for the Common Shares.”

The following table sets forth for each of the periods indicated the high and low closing market prices for Common Shares on the NYSE, and the

corresponding NAV per share and the premium or discount to NAV per share at which the Common Shares were trading as of such date. NAV is

determined once daily as of the close of regular trading of the NYSE (typically 4:00

p.m.

, Eastern Time). See “Determination of Net Asset Value” for

information as to the determination of the fund’s NAV.

The last reported sale price, NAV per share and percentage premium to NAV per share of the Common Shares as of February 14, 2024 were $5.05, $5.23 and -3.44 %, respectively. As of February 14, 2024, the fund had 10,921,751 Common Shares outstanding and net assets of the fund were $57,149,121.

The fund is a diversified, closed-end management investment company registered under the 1940 Act. The fund was organized on April 23, 2007 as a

Massachusetts business trust pursuant to an Agreement and Declaration of Trust (as amended and/or restated from time to time, the “Declaration of

Trust”). The fund commenced operations in September 2007 following an initial public offering. On September 25, 2007, the fund issued an aggregate

of 8,750,000 Common Shares of beneficial interest, par value $0.01 per share, pursuant to the initial public offering thereof. On November 14, 2007,

the fund issued an additional 600,000 Common Shares in connection with the exercise by the initial underwriters of an over-allotment option. The

fund’s principal office is located at 200 Berkeley Street, Boston, Massachusetts 02116 and its phone number is 800-225-6020.