As filed with the Securities and Exchange Commission on January 18, 2012

Registration No. 333-173700

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON D.C. 20549

____________________________

AMENDMENT NO. 3

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

_____________________________

ANHUI TAIYANG POULTRY CO., INC.

(Name of registrant in its charter)

|

|

Delaware

|

|

2015

|

|

65-0918608

|

|

|

|

(State or other Jurisdiction

of Incorporation or Organization)

|

|

(Primary Standard Industrial

Classification Code Number)

|

|

(I.R.S. Employer

Identification No.)

|

|

No. 88, Eastern Outer Ring Road

Ningguo City, Anhui Province, 242300

People’s Republic of China

(+86) 0563-430-9999

(Address and telephone number of principal executive offices and principal place of business)

Wu Qiyou, Chief Executive Officer

Anhui Taiyang Poultry Co., Inc.

No. 88, Eastern Outer Ring Road

Ningguo City, Anhui Province, 242300

People’s Republic of China

(+86) 0563-430-9999

(Name, address and telephone number of agent for service)

Copies to:

Marc A. Ross, Esq.

James M. Turner, Esq.

Sichenzia Ross Friedman Ference LLP

61 Broadway, 32nd Flr.

New York, New York 10006

(212) 930-9700

(212) 930-9725 (fax)

APPROXIMATE DATE OF PROPOSED SALE TO THE PUBLIC:

From time to time after this Registration Statement becomes effective.

If any securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, other than securities offered only in connection with dividend or interest reinvestment plans, check the following box: x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ________

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. _________

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. _________

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. _________

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a small reporting company. See definitions of “large accelerated filer,” “accelerated filed,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer o

|

Accelerated filer o

|

|

Non-accelerated filer o

|

Smaller reporting company x

|

|

(Do not check if a smaller reporting company)

|

|

CALCULATION OF REGISTRATION FEE

|

Title of Each Class Of

Securities To Be Registered

|

|

Amount To Be

Registered (1)

|

|

Proposed Maximum

Offering Price

Per Security (2)

|

|

Proposed Maximum

Aggregate

Offering Price

|

|

Amount Of

Registration Fee

|

|

||||

|

Common Stock, $.001 par value

|

|

|

5,485,300

|

$

|

1.50

|

|

$

|

8,227,950

|

$

|

955.26

|

|

||

|

Common Stock, $.001 par value issuable upon exercise of warrants

|

|

|

1,142,396

|

|

$

|

4.00

|

|

$

|

4,569,584

|

|

$

|

530.53

|

|

|

Total

|

|

|

6,627,696

|

|

|

$

|

12,797,534

|

|

$

|

1,485.79

|

(3)

|

||

|

(1)

|

Includes shares of our common stock, par value $0.001 per share, which may be offered pursuant to this registration statement, which shares are issuable upon exercise of warrants held by the selling stockholders. In addition to the shares set forth in the table, the amount to be registered includes an indeterminate number of shares issuable upon exercise of the warrants, as such number may be adjusted as a result of stock splits, stock dividends and similar transactions in accordance with Rule 416. The number of shares of common stock registered hereunder represents a good faith estimate by us of the number of shares of common stock issuable upon exercise of the warrants. For purposes of estimating the number of shares of common stock to be included in this registration statement, we calculated a good faith estimate of the number of shares of our common stock that we believe will be issuable upon exercise of the warrants to account for market fluctuations, and antidilution and price protection adjustments, respectively. Should the conversion ratio result in our having insufficient shares, we will not rely upon Rule 416, but will file a new registration statement to cover the resale of such additional shares should that become necessary. In addition, should a decrease in the exercise price as a result of an issuance or sale of shares below the then current market price, result in our having insufficient shares, we will not rely upon Rule 416, but will file a new registration statement to cover the resale of such additional shares should that become necessary.

|

|

|

(2)

|

Estimated solely for purposes of calculating the registration fee in accordance with Rule 457(c) and Rule 457(g) under the Securities Act of 1933, using the average of the high and low price as reported on the Over-the-Counter Bulletin Board on April 20, 2011, which was $1.50 per share.

|

|

|

(3)

|

Previously paid.

|

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

i

PRELIMINARY PROSPECTUS SUBJECT TO COMPLETION, DATED January 18, 2012

ANHUI TAIYANG POULTRY CO., INC.

6,627,696 SHARES OF

COMMON STOCK

This prospectus relates to the resale by the selling stockholders of up to 6,627,696 shares of our common stock, including up to 1,142,396 shares of common stock underlying warrants exercisable at $4.00 per share. The selling stockholders may sell common stock from time to time in the principal market on which the stock is traded at the prevailing market price or in negotiated transactions. The selling stockholders may be deemed underwriters of the shares of common stock which they are offering. We will pay the expenses of registering these shares.

Our common stock is registered under Section 12(g) of the Securities Exchange Act of 1934 and is available for quotation on the Over-the-Counter Bulletin Board under the symbol “DUKS”. The last reported sales price per share of our common stock as reported by the Over-the-Counter Bulletin Board on January 9, 2012 , was $ 1.25 .

Investing in these securities involves significant risks. See “Risk Factors” beginning on page 7.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is _____, 2012 .

The information in this prospectus is not complete and may be changed. This prospectus is included in the Registration Statement that was filed by Anhui Taiyang Poultry Co., Inc. with the Securities and Exchange Commission. The selling stockholders may not sell these securities until the registration statement becomes effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the sale is not permitted.

ii

TABLE OF CONTENTS

|

|

|

Page

|

|

|

1

|

|

|

|

1

|

|

|

|

2

|

|

|

|

6

|

|

|

|

19

|

|

|

|

20

|

|

|

|

21

|

|

|

|

41

|

|

|

|

52

|

|

|

|

52

|

|

|

|

53

|

|

|

|

56

|

|

|

|

57

|

|

|

|

61

|

|

|

|

62

|

|

|

|

63

|

|

|

|

64

|

|

|

|

66

|

|

|

|

71

|

|

|

|

72

|

|

|

|

72

|

|

|

|

73

|

You should rely only on the information contained in this prospectus. We have not, and the underwriter has not, authorized anyone to provide you with information that is different. If anyone provides you with different or inconsistent information, you should not rely on it. We are offering to sell, and are seeking offers to buy, shares of common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of the common stock. Our business, financial conditions, results of operations and prospects may have changed since that date.

iii

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with information different from that contained in this prospectus. The selling stockholders are offering to sell and seeking offers to buy shares of our common stock, including shares they acquire upon exercise of their warrants, only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common stock. The prospectus will be updated and updated prospectuses made available for delivery to the extent required by the federal securities laws.

No person is authorized in connection with this prospectus to give any information or to make any representations about us, the selling stockholders, the securities or any matter discussed in this prospectus, other than the information and representations contained in this prospectus. If any other information or representation is given or made, such information or representation may not be relied upon as having been authorized by us or any selling stockholder. This prospectus does not constitute an offer to sell, or a solicitation of an offer to buy the securities in any circumstances under which the offer or solicitation is unlawful. Neither the delivery of this prospectus nor any distribution of securities in accordance with this prospectus shall, under any circumstances, imply that there has been no change in our affairs since the date of this prospectus. The prospectus will be updated and updated prospectuses made available for delivery to the extent required by the federal securities laws.

This prospectus contains some forward-looking statements. Forward-looking statements give our current expectations or forecasts of future events. You can identify these statements by the fact that they do not relate strictly to historical or current facts. Forward-looking statements involve risks and uncertainties. Forward-looking statements include statements regarding, among other things, (a) our projected sales, profitability, and cash flows, (b) our growth strategies, (c) anticipated trends in our industries, (d) our future financing plans and (e) our anticipated needs for working capital. They are generally identifiable by use of the words “may,” “will,” “should,” “anticipate,” “estimate,” “plans,” “potential,” “projects,” “continuing,” “ongoing,” “expects,” “management believes,” “we believe,” “we intend” or the negative of these words or other variations on these words or comparable terminology. These statements may be found under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business,” as well as in this prospectus generally. In particular, these include statements relating to future actions, prospective products or product approvals, future performance or results of current and anticipated products, sales efforts, expenses, the outcome of contingencies such as legal proceedings, and financial results.

Any or all of our forward-looking statements in this report may turn out to be inaccurate. They can be affected by inaccurate assumptions we might make or by known or unknown risks or uncertainties. Consequently, no forward-looking statement can be guaranteed. Actual future results may vary materially as a result of various factors, including, without limitation, the risks outlined under “Risk Factors” and matters described in this prospectus generally. In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this filing will in fact occur. You should not place undue reliance on these forward-looking statements.

The forward-looking statements speak only as of the date on which they are made, and, except to the extent required by federal securities laws, we undertake no obligation to publicly update any forward-looking statements, whether as the result of new information, future events, or otherwise.

1

The following summary highlights selected information contained in this prospectus. This summary does not contain all the information you should consider before investing in the securities. Before making an investment decision, you should read the entire prospectus carefully, including the “risk factors” section, the financial statements and the notes to the financial statements.

ANHUI TAIYANG POULTRY CO., INC.

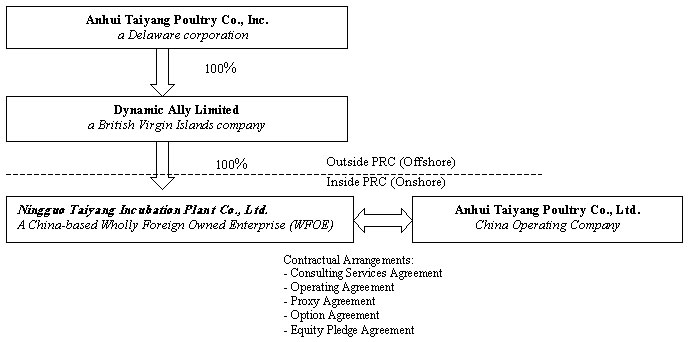

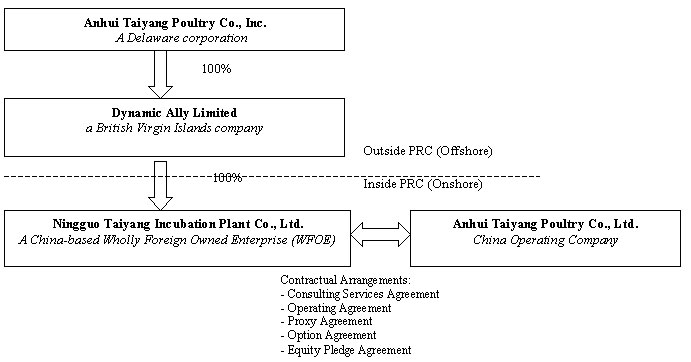

We are private breeder and seller of ducks and duck parts in the People’s Republic of China (“China” or “PRC”). Our wholly-owned subsidiary, Dynamic Ally Limited (“Dynamic”) was incorporated in the British Virgin Islands on March 2, 2010. Dynamic owns 100% of the issued and outstanding capital stock of Ningguo Taiyang Incubation Plant C., Ltd. (“Ningguo”), a wholly foreign owned enterprise (“WFOE”) established under the laws of the PRC. On May 26, 2010, Ningguo entered into a series of contractual agreements with Anhui Taiyang Poultry Co., Ltd. (“Taiyang”), a company incorporated under the laws of the PRC, and its three owners, in which Ningguo effectively assumed management of the business activities of Taiyang and has the right to appoint all executives and senior management and the members of the board of directors of Taiyang. The contractual arrangements are comprised of a series of agreements, including a Consulting Services Agreement and Operating Agreement, through which Ningguo has the right to advise, consult and manage Taiyang and its business operations for a quarterly consulting fee equal to all of Taiyang’s quarterly net profit. We will receive distributions from our consolidated affiliates only to the extent service fees are paid to Ningguo under these series of agreements and further distributed as dividends or other shareholder distributions by Ningguo. To secure payment of the service fees, Taiyang’s shareholders have pledged their rights, titles and equity interest in Taiyang as security for Ningguo to collect the consulting fee from Taiyang through an Equity Pledge Agreement. In order to further reinforce Ningguo’s rights to control and manage Taiyang, Taiyang’s shareholders have granted Ningguo the exclusive right to exercise their voting rights pursuant to a Voting Rights Proxy Agreement, as well as the exclusive right and option to acquire all of their equity interests in Taiyang through an Option Agreement.

All of the business operations are carried out by Taiyang, which we control through contractual arrangements between Ningguo and Taiyang. Through Taiyang, we raise, process and market ducks and duck related food products through three business lines:

|

o

|

Breeding Unit – breeds, hatches, and cultivates ducklings for resale and processing by Food Processing Unit

|

|

|

o

|

Feed Unit – produces duck feed for internal use and external sale

|

|

|

o

|

Food Processing Unit – processes ducklings into frozen raw food product for commercial resale.

|

All of the business operations are in Ninnguo City, located in the province of Anhui, in southern-central China.

2

Corporate Structure

Our organizational structure was carefully developed to abide by the laws of the PRC and maintain tax benefits as well as internal organizational efficiencies. Our organizational structure is summarized in the figure below:

We had revenues of $41,684,988 and $28,859,699 and generated net income of $3,395,524and $2,489,323 for the years ended December 31, 2010 and 2009, respectively. For the three and nine months ended September 30, 2011, we had revenues of $ 7,159,083 and $ 23,221,725 , respectively, and generated net (loss)/ income of ($321,764) and $1,745,481 , respectively . We had a working capital deficit of $3,867,880at September 30, 2011, primarily as a result of approximately $13.5 million in current loans payable and $2.8 million in accounts payable.

Our principal offices are located at No. 88, Eastern Outer Ring Road, Ningguo City, Anhui Province, 242300, People’s Republic of China, and our telephone number is (+86) 0563-430-9999. We are a Delaware corporation.

The Offering

|

Common stock offered by the selling stockholders

|

|

Up to 6,627,696 shares of common stock, including the following: | |

|

- 5,485,300 shares of common stock, and

- up to 1,142,396 shares of common stock issuable upon the exercise of common stock purchase warrants at an exercise price of $4.00 per share (includes a good faith estimate of the shares underlying warrants to account for antidilution protection adjustments).

|

|||

|

|

|

|

|

|

Common stock to be outstanding after the offering

|

|

Up to 11,582,429 shares. | |

|

|

|

|

|

|

Use of proceeds

|

|

We will not receive any proceeds from the sale of the common stock. However, we will receive the sale price of any common stock we sell to the selling stockholders upon exercise of the warrants. We expect to use the proceeds received from the exercise of the warrants, if any, for general working capital purposes. | |

|

|

|

|

|

|

OTCBB symbol

|

|

DUKS | |

3

The above information regarding common stock to be outstanding after the offering is based on 10,440,033 shares of common stock outstanding as of January 9, 2012 and includes the 1,142,396 shares of common stock issuable upon the exercise of all warrants outstanding as of January 9, 2012 registered pursuant to the registration statement that this prospectus is part of.

Unless otherwise indicated, all share amounts and prices give effect to the 1-for-3 reverse stock split of our common stock, which was effective on June 1, 2010.

The following is a summary of the transactions relating to the securities being registered hereunder.

Reverse Merger Transaction

On November 10, 2010, we executed and consummated a share exchange agreement by and among Dynamic and the stockholders of 100% of Dynamic common stock, on the one hand, and us and certain holders of our issued and outstanding common stock on the other hand. In connection with the share exchange agreement, we granted piggyback registration rights to our existing stockholders, of which an aggregate of 314,347 shares are included in this prospectus.

November 2010 Private Placement

In November 2010, we sold to certain investors (the “Old Purchasers”) units (the “Old Units”) for aggregate cash gross proceeds of $5,107,472, at a price of $8.00 per Unit and the exchange of $549,984 in previously issued debentures that were converted into Units at a price of $6.00 per Unit (the “Old Financing”). Each Old Unit consists of four (4) shares of Common Stock and a warrant to purchase one (1) share (the “Old Warrants”).

Pursuant to a placement agent agreement with Laidlaw & Company (UK) Ltd. (“Laidlaw”), dated as of February 8, 2010, Laidlaw received (i) a cash payment equal to 8% of the gross proceeds delivered by investors in the Old Financing and (ii) five-year placement agent warrants to acquire 226,298 shares of Common Stock, at an exercise price of $4.00 per share. The placement agent warrants may be exercised on a cashless exercise basis.

Pursuant to the Old Warrants, no holder may exercise such holder’s Old Warrant if such exercise would result in the holder beneficially owning in excess of 4.9% of our then issued and outstanding common stock. A holder may, however, increase or decrease this limitation (but in no event exceed 9.99% of the number of shares of Common Stock issued and outstanding) by providing us with 61 days’ notice that such holder wishes to increase or decrease this limitation.

On November 10, 2010 we entered into a registration rights agreement with the Old Purchasers, under which we agreed to prepare and file with the SEC and maintain the effectiveness of a “resale” registration statement providing for the resale of (i) all of the shares of Common Stock (ii) all of the shares of Common Stock issuable upon exercise of the Old Warrants, (iii) all of the shares of Common Stock issuable upon exercise of the warrants issued to Laidlaw; (iv) any additional shares issuable in connection with any anti-dilution provisions associated with such Old Warrants, and (v) any securities issued or issuable upon any stock split, dividend or other distribution, recapitalization or similar event with respect to the foregoing (collectively, the “Old Registrable Securities”).

Under the terms of the registration rights agreement, we were required to have a registration statement filed with the SEC by January 9, 2011, and declared effective by the SEC not later than March 10, 2011. We are required to pay liquidated damages to each Old Purchaser in an amount equal to 1% of the Old Purchaser’s purchase price paid for any Old Registrable Securities then held by the Old Purchaser for the first thirty (30) calendar days past the relevant deadline that the registration statement is not filed or not declared effective, for any period that we fail to keep the registration statement effective. The liquidated damages increases to 2% of the Old Purchaser’s purchase price for any Old Registrable Securities held after the first thirty (30) calendar day period thereafter, subject to a maximum payment of 10% of the Old Purchaser’s purchase price paid. We have accrued the maximum amount of liquidated damages of 10% to the Old Purchasers.

4

On November 10, 2010 and in connection with the Old Financing , we entered into a Performance Milestone Shares Escrow Agreement (the “Escrow Agreement”) with Laidlaw, on behalf of the Old Purchasers, and Firm Success International, Ltd., our largest shareholder (“Firm Success”), pursuant to which Firm Success agreed to deposit and pledge 1,466,097 shares of our common stock into an escrow account (the “Pledged Shares”), which Pledged Shares represented 30% of Firm Success’ shares, as security for our achieving Adjusted Net Income (as hereinafter defined) of not less than $6,936,889 for the fiscal year ending December 31, 2010 (the “Target Income”). “Adjusted Net Income” means net income for the year ending December 31, 2010, as reported in our audited financial statements, as filed with the SEC, plus (a) stock based compensation charges associated with closing the Share Exchange and the private placement offering, and (b) cash charges related to the Share Exchange and the private placement offering, which (b) shall not exceed $705,000 in the aggregate.

As the Old Financing was being done in connection with the reverse merger transaction, there was no established market to value our Common Stock. As a result, in support of our valuation, we determined the Target Income we anticipated to achieve for the fiscal year ended December 31, 2010. As a result of negotiations between us and Laidlaw, it was agreed that Firm Success would pledge 30% of its shares, as a guarantee to the Old Purchasers that we would achieve the Target Income, which supported our valuation in the Old Financing. It was agreed to by the parties that a pledge of Firm Success’ shares was preferable than a make-good provision of additional shares from our company, as we wanted to reduce the potential dilution if the Target Income was not met.

In April 2011, the Pledged Shares were released from the pledge and returned to Firm Success subsequent to filing of our Annual Report on Form 10-K for year ended December, 31, 2010, as the Target Income was achieved. On November 11, 2011, we filed an amended Annual Report on Form 10-K/A for the year ended December, 31, 2010 , pursuant to which the Adjusted Net Income fell below the Target Income. Accordingly, the Pledged Shares are due to be distributed from Firm Success pro rata to the holders of the Old Units.

March 2011 Private Placement

In March 2011, we sold to certain investors (the “New Purchasers”) units (the “New Units”) for aggregate cash gross proceeds of $1,150,000, at a price of $8.00 per Unit (the “New Financing”). Each New Unit consists of four (4) shares of Common Stock and a warrant to purchase one (1) share (the “New Warrants”).

Pursuant to a placement agent agreement with Corinthian Partners, L.L.C. (“Corinthian”), Corinthian received (i) a cash payment equal to 8% of the gross proceeds delivered by investors in the New Financing and (ii) five-year placement agent warrants to acquire 46,000 shares of Common Stock, at an exercise price of $4.00 per share. The placement agent warrants may be exercised on a cashless exercise basis.

Pursuant to the New Warrants, no holder may exercise such holder’s New Warrant if such exercise would result in the holder beneficially owning in excess of 4.9% of our then issued and outstanding common stock. A holder may, however, increase or decrease this limitation (but in no event exceed 9.99% of the number of shares of Common Stock issued and outstanding) by providing us with 61 days’ notice that such holder wishes to increase or decrease this limitation.

On March 7, 2011 we entered into a registration rights agreement with the New Purchasers, under which we agreed to prepare and file with the SEC and maintain the effectiveness of a “resale” registration statement providing for the resale of (i) all of the shares of Common Stock (ii) all of the shares of Common Stock issuable upon exercise of the New Warrants, (iii) all of the shares of Common Stock issuable upon exercise of the warrants issued to Corinthian; (iv) any additional shares issuable in connection with any anti-dilution provisions associated with such New Warrants, and (v) any securities issued or issuable upon any stock split, dividend or other distribution, recapitalization or similar event with respect to the foregoing (collectively, the “New Registrable Securities”). Under the terms of the registration rights agreement, we were required to have a registration statement filed with the SEC by May 6, 2011, and declared effective by the SEC not later than September 3 , 2011. We are required to pay liquidated damages to each New Purchaser in an amount equal to 1% of the New Purchaser’s purchase price paid for any New Registrable Securities then held by the New Purchaser for the first thirty (30) calendar days past the relevant deadline that the registration statement is not filed or not declared effective, for any period that we fail to keep the registration statement effective. The liquidated damages increases to 2% of the New Purchaser’s purchase price for any New Registrable Securities held after the first thirty (30) calendar day period thereafter, subject to a maximum payment of 10% of the New Purchaser’s purchase price paid. As of December 19, 2011, we have accrued liquidated damages in the amount of approximately $55,000 related to this financing, which is the maximum amount of liquidated damages to be paid. As of September 30, 2011, we had not accrued any liability related to these liquidated damages because the ultimate amount of the liquidated damages was not reasonably determinable at the time those financial statements were issued. The maximum amount of such liquidated damages pursuant to the registration rights agreement is $115,000. If the registration statement was declared effective as of January 9, 2012, we would owe liquidated damages to the investors in the amount of $85,867 .

5

This investment has a high degree of risk. Before you invest you should carefully consider the risks and uncertainties described below and the other information in this prospectus. If any of the following risks actually occur, our business, operating results and financial condition could be harmed and the value of our stock could go down. This means you could lose all or a part of your investment.

RISKS RELATED TO OUR BUSINESS

We may be unable to sustain our past growth or manage our future growth, which may have a material adverse effect on our future operating results.

We have generally experienced growth since our inception, and realized revenues of approximately $41.7 million and $28.9 million in the years ended December 31, 2010 and 2009, respectively, and $23.2 million for the nine months ended September 30, 2011. If we are unable to manage our growth effectively, we may not be able to take advantage of market opportunities, develop new products, enhance our technological capabilities, satisfy customer requirements, execute our business plan or respond to competitive pressures. To effectively manage growth, we need to:

|

·

|

Hire, train, integrate and manage additional qualified technicians and breeding farm directors and sales and marketing personnel;

|

|

|

·

|

Implement additional, and improve existing, administrative, financial and operations systems, procedures and controls;

|

|

|

·

|

Continue to enhance manufacturing and customer resource management systems;

|

|

|

·

|

Continue to expand and upgrade our feed ingredient composition, poultry immunization system and breeding technology;

|

|

|

·

|

Manage multiple relationships with distributors, suppliers and certain other third parties; and

|

|

|

·

|

Manage our financial condition.

|

Our success also depends largely on our ability to anticipate and respond to expected changes in future demand for our products, and our ducks’ performance and disease resistance ability. If the timing of our expansion does not match market demand, our business strategy may need to be revised. If we over-expand and demand for our products does not increase as we may have projected, our financial results will be materially and adversely affected. However, if we do not expand, and demand for our products increases sharply, our business could be seriously harmed because we may not be as cost-effective as our competitors due to our inability to take advantage of increased economies of scale. In addition, we may not be able to satisfy the needs of current customers or attract new customers, and we may lose credibility and our relationships with our customers may be negatively affected. Moreover, if we do not properly allocate our resources in line with future demand for our products, we may miss changing market opportunities and our business and financial results could be materially and adversely affected. We cannot assure you that we will be able to successfully manage our growth in the future.

Outbreaks of poultry disease, such as avian influenza, or the perception that outbreaks may occur, can significantly restrict our ability to conduct our operations.

Taiyang takes precautions to ensure that its flocks are healthy and that its production facilities operate in a sanitary and environmentally sound manner. While Taiyang has ability and experience in product quality improvement as well as poultry disease resistance, events beyond its control, such as the outbreak of avian influenza in 2006, may restrict its ability to conduct its operations and sales. An outbreak of disease could result in governmental restrictions on the import and export of products from Taiyang’s customers, or require it to destroy one or more of its flocks. This could result in the cancellation of orders by its customers and create adverse publicity that may have a material adverse effect on our business, reputation and prospects.

6

Worldwide fears about avian diseases, such as avian influenza, have depressed, and may continue to adversely impact, Taiyang’s sales. Avian influenza is a respiratory disease of birds. The milder forms occur occasionally around the world. Recently, there has been substantial publicity regarding a highly pathogenic strain of avian influenza, known as H5N1, which has affected Asia since 2002. It is widely believed that H5N1 is spread by migratory birds, such as ducks and geese. There have also been some cases where H5N1 is believed to have passed from birds to humans as humans came into contact with live birds that were infected with the disease. Although there are vaccines available for H5N1 and other forms of avian influenza, and the PRC government mandates, and Taiyang vaccinates its breeding stock against avian influenza, there is no guarantee that the disease can be completely prevented as the virus continues to mutate. Taiyang’s livestock have never been infected with avian influenza. Taiyang is required to maintain an immunization permit on an annual basis issued by the provincial Animal Husbandry Bureau.

Taiyang does not typically have long-term purchase contracts with its customers and its customers have in the past and could at any time in the future, reduce or cease purchasing products from them, harming our operating results and business.

Taiyang typically does not have long-term volume purchase contracts with their customers, and they are not obligated to purchase products from Taiyang. Accordingly, their customers could at any time reduce their purchases from Taiyang or cease purchasing their products altogether. In addition, any decline in demand for Taiyang’s products and any other negative development affecting its major customers or the poultry industry in general, would likely harm our results of operations. For example, if any of Taiyang’s customers experience serious financial difficulties, it may lead to a decline in sales of Taiyang’s products to such customer and our operating results could be harmed through, among other things, decreased sales volumes and write-offs of accounts receivable related to sales to such customer.

Competition in the poultry industry with other poultry companies, especially companies with greater resources, may make us unable to compete successfully, which could adversely affect our business.

The Chinese poultry industry is highly competitive. In general, competitive factors in the Chinese duck industry include price, product quality, brand identification, breadth of product line and customer service. Taiyang’s success depends in part on its ability to manage costs and be efficient in the highly competitive poultry industry. Many of Taiyang’s competitors have greater financial and marketing resources. Because of this, we may not be able to successfully increase Taiyang’s market penetration or Taiyang’s overall share of the poultry market.

Increased competition may result in price reductions, increased sales incentive offerings, lower gross margins, sales expenses, marketing programs and expenditures to expand channels to market. Taiyang’s competitors may offer products with better market acceptance, better price or better quality. We may be adversely affected if Taiyang is unable to maintain current product cost reductions, or achieve future product cost reductions.

Taiyang competes against a number of other suppliers of ducks. Although it attempts to develop and support high-quality products that its customers demand, products developed by competing suppliers could render its products noncompetitive. If Taiyang fails to address these competitive challenges, there could be a material adverse effect upon our business, consolidated results of operations and financial condition.

Taiyang derives a significant portion of its revenues from a single distributor, the loss of which would significantly reduce Taiyang’s revenues and may impair its ability to operate profitably.

Taiyang has derived, and believes that it will continue to derive, a significant portion of its revenues from a single distributor, Yu Qigui. Revenue from Taiyang’s Feed Unit, which was $13.9 million in the year ended December 31, 2010, was almost exclusively a result of sales to this distributor. As a result, to the extent that such distributor continues to accounts for a large percentage of Taiyang’s revenue, the loss of this distributor could materially affect Taiyang’s ability to operate profitably. Since Yu Qigui accounted for approximately 33% of our revenue for the year ended December 31, 2010, the loss of this distributor would have a material adverse effect upon Taiyang’s business and may impair its ability to operate profitably.

7

Taiyang anticipates that this primary dependence on a single distributor will continue for the foreseeable future. There is a risk that the existing distributor will elect not to do business with us in the future or will experience financial difficulties. Furthermore, this distributor could experience financial difficulties, business reverses or the loss of orders or anticipated orders which reduces or eliminates the need for the products that it orders from Taiyang. If Taiyang does not develop relationships with new distributors, it may not be able to increase, or even maintain, its revenue, and its financial condition, results of operations, business and/or prospects may be materially adversely affected.

If demand for Taiyang’s products declines in the markets that it serves, its selling prices and overall sales will decrease. Even if the demand for its products increases, when such increase cannot outgrow the decrease in its selling price, our overall sales revenues may decrease.

Demand for Taiyang’s products is affected by a number of factors, including the general demand for the products in the end markets that it serves and the price attractiveness. A vast majority of its sales are derived directly or indirectly from end users who are duck raisers and large integrated duck companies whose duck seedling production is not sufficient for their own use. Any significant decrease in the demand for ducks may result in a decrease in Taiyang’s revenues and earnings. A variety of factors, including economic, health, regulatory, political and social instability, could contribute to a slowdown in the demand for ducks because demand for duck is highly correlated with general economic activities. As a result, even if the demand for Taiyang’s products increases, when the increase of demand cannot outgrow the decrease of selling price, our overall sales revenues may decrease.

Industry cyclicality can affect our earnings, especially due to fluctuations in commodity prices of feed ingredients and breeding stock.

Currently, all Taiyang’s raw materials are domestically procured. Profitability in the poultry industry is materially affected by the supply of parent breeding stocks and the commodity prices of feed ingredients, including corn, soybean cake, and other nutrition ingredients from numerous sources, mainly from wholesalers who collect the feed ingredients directly from farmers. As a result, the poultry industry is subject to wide fluctuations and cycles. These prices are determined by supply and demand factors. Prices for raw materials have been volatile in recent years. For instance, our average unit price for corn, one of our principal raw materials, increased from approximately $0.18 (RMB 1.44) per kilogram in 2006 to approximately $0.30 (RMB 1.97) per kilogram in 2011, showing an increase of 67%. Historically, Taiyang’s financial results have improved when duck prices are high and feed prices are low and feed ingredients are in adequate supply. However, it is very difficult to predict when feed price spiral cycles will occur.

Various factors can affect the supply of corn and soybean meal, which are the primary ingredients of the feed Taiyang uses for parent breeding stocks. In particular, weather patterns, the level of supply inventories and demand for feed ingredients, and the agricultural policies of the Chinese government affect the supply of feed ingredients. Weather patterns often change agricultural conditions in an unpredictable manner. A sudden and significant change in weather patterns could affect supplies of feed ingredients, as well as both the industry’s and Taiyang’s ability to obtain feed ingredients, grow ducks or deliver products. Increases in the prices of feed ingredients will result in increases in raw material costs and operating costs.

Increased water, energy and gas costs would increase Taiyang’s expenses and reduce its profitability.

Taiyang requires a substantial amount, and as it expands its business it will require additional amounts, of water, electricity and natural gas to produce and process its duck products. The prices of water, electricity and natural gas fluctuate significantly over time. One of the primary competitive factors in the Chinese duck market is price, and it may not be able to pass on increased costs of production to its customers. As a result, increases in the cost of water, electricity or natural gas could substantially harm our business and results of operations.

8

Taiyang’s products might contain undetected defects that are not discovered until after shipping.

Although Taiyang has strict quality control over its products and it produces high-quality ducks supported by its know-how in feed ingredient composition, immunization system and breeding techniques gained through many years of business and continuous research and development, its products may contain undetected problems. Problems could result in a loss or delay in market acceptance of its products and thus harm our reputation and revenues.

The loss of key personnel or the failure to attract or retain specialized technical and management personnel could impair our ability to grow our business.

We rely heavily on the services of our key employees, including Wu Qiyou, our founder, Chief Executive Officer, and chairman of our board of directors. In addition, our engineers and other key technical personnel are a significant asset and are the source of Taiyang’s technological and product innovations. Taiyang depends substantially on the leadership of a small number of farm directors and technicians who are devoted to research and development. Additionally, all of Taiyang’s packaged food products, accounting for approximately 36% and 73% of our revenue in 2009 and 2010, respectively, are sold through third party distributors. The loss of these distributors could have a material adverse effect on our business, results of operations and financial condition. We believe Taiyang’s future success will depend upon its ability to retain these key employees and sales distributors. We may not be successful in attracting and retaining sufficient numbers of technical personnel to support Taiyang’s anticipated growth. Despite the incentives we provide, our current employees may not continue to work for Taiyang, and if additional personnel are required for Taiyang’s operations, we may not be able to obtain the services of additional personnel necessary for Taiyang’s growth. In addition, we do not maintain “key person” life insurance for any of Taiyang’s senior management or other key employees. The loss of the key employees or the inability to attract or retain qualified personnel, including technicians, could delay the development and introduction of, and have an adverse effect on Taiyang’s ability to sell, its products, as well as its overall growth.

In addition, if any other members of Taiyang’s senior management or any of its other key personnel join a competitor or form a competing company, we may not be able to replace them easily and we may lose customers, business partners, key professionals and staff members.

We have made inter-enterprise loans that may be in violation of PRC lending regulations.

As of September 30, 2011 and December 31, 2010 and 2009, the Company had outstanding $3,404,577, $4,268,057 and $2,816,943, respectively, of unsecured loans receivable from unrelated parties. These loans, and other loans made by the Company during the years ended December 31, 2009 and 2010 that were repaid prior to the end of the respective reporting period, constitute inter-enterprise lending that violate the PRC General Lending Rules. A fine in the amount of one to three times the income generated by the Company from such inter-enterprise loans may be imposed by the People’s Bank of China, at their discretion, if the Company were found to be in violation of the PRC General Lending Rules. We estimate the range of potential fines to be between approximately $560,000, and $1,670,000 based on the guidelines established by PRC General Lending Rules, but such fines are levied discretion of the People’s Bank of China. In the opinion of management after discussion with its Chinese legal counsel, the probability of the fine being imposed is low.

We do not have any registered patents or other registered intellectual property on our production processes and we may not be able to maintain the confidentiality of our processes.

While we have four design patents relating to package bags for our products, we have no patents or registered intellectual property covering our production processes and we rely on the confidentiality of our production processes in producing a competitive product. The confidentiality of our know-how may not be maintained and we may lose any meaningful competitive advantage which might arise through our proprietary processes. Due to the lack of such protection, unauthorized parties may attempt to copy or otherwise obtain and use our proprietary production technology. Monitoring unauthorized use of our production process is difficult, particularly in China. This may have a material adverse effect on our competitive advantage.

9

We do not presently maintain product liability insurance, and our property and equipment insurance does not cover the full value of our property and equipment, which leaves us with exposure in the event of loss or damage to our properties or claims filed against us.

We currently do not carry any product liability or other similar insurance. Unlike the U.S. and other countries, product liability claims and lawsuits are extremely rare in the PRC. However, we cannot guarantee that we would not face liability in the event of any problems with our products, including disease or contamination. We cannot assure you that, especially as China’s domestic consumer economy and industrial economy continues to expand, product liability exposures and litigation will not become more commonplace in the PRC, or that we will not face product liability exposure or actual liability if we expand our sales into international markets, like the United States, where product liability claims are more prevalent, although we currently do not have any plans to expand our operations into the United States or international markets.

Except for property and automobile insurance, we do not have other insurance such as business liability or disruption insurance coverage for our operations in the PRC.

RISKS RELATED TO OUR CORPORATE STRUCTURE

We conduct our business through Taiyang by means of contractual arrangements. If the Chinese government determines that these contractual arrangements do not comply with applicable regulations, our business could be adversely affected. If the PRC regulatory bodies determine that the agreements that establish the structure for operating our business in China do not comply with PRC regulatory restrictions on foreign investment, we could be subject to severe penalties. In addition, changes in such Chinese laws and regulations may materially and adversely affect our business.

There are uncertainties regarding the interpretation and application of PRC laws, rules and regulations, including but not limited to the laws, rules and regulations governing the validity and enforcement of the contractual arrangements between Ningguo and Taiyang. Although we have been advised by our PRC counsel, that based on their understanding of the current PRC laws, rules and regulations, the structure for operating our business in China (including our corporate structure and contractual arrangements with Taiyang and its owners) comply with all applicable PRC laws, rules and regulations, and do not violate, breach, contravene or otherwise conflict with any applicable PRC laws, rules or regulations, we cannot assure you that the PRC regulatory authorities will not determine that our corporate structure and contractual arrangements violate PRC laws, rules or regulations. If the PRC regulatory authorities determine that our contractual arrangements are in violation of applicable PRC laws, rules or regulations, our contractual arrangements will become invalid or unenforceable. In addition, new PRC laws, rules and regulations may be introduced from time to time to impose additional requirements that may be applicable to our contractual arrangements. For example, the PRC Property Rights Law that became effective on October 1, 2007 may require us to register with the relevant government authority the security interests on the equity interests in Taiyang granted to us under the equity pledge agreements that are part of the contractual arrangements. If we are required to register such security interests, failure to complete such registration in a timely manner may result in such equity pledge agreements to be unenforceable against third party claims.

The Chinese government has broad discretion in dealing with violations of laws and regulations, including levying fines, revoking business and other licenses and requiring actions necessary for compliance. In particular, licenses and permits issued or granted to us by relevant governmental bodies may be revoked at a later time by higher regulatory bodies. We cannot predict the effect of the interpretation of existing or new Chinese laws or regulations on our businesses. We cannot assure you that our current ownership and operating structure would not be found in violation of any current or future Chinese laws or regulations. As a result, we may be subject to sanctions, including fines, and could be required to restructure our operations or cease to provide certain services. Any of these or similar actions could significantly disrupt our business operations or restrict us from conducting a substantial portion of our business operations, which could materially and adversely affect our business, financial condition and results of operations.

10

If Ningguo or Taiyang are determined to be in violation of any existing or future PRC laws, rules or regulations or fail to obtain or maintain any of the required governmental permits or approvals, the relevant PRC regulatory authorities would have broad discretion in dealing with such violations, including:

|

·

|

revoking the business and operating licenses of our PRC consolidated entities;

|

|

|

·

|

discontinuing or restricting the operations of our PRC consolidated entities;

|

|

|

·

|

imposing conditions or requirements with which we or our PRC consolidated entities may not be able to comply;

|

|

|

·

|

requiring us or our PRC consolidated entities to restructure the relevant ownership structure or operations;

|

|

|

·

|

restricting or prohibiting our use of the proceeds from our initial public offering to finance our business and operations in China; or

|

|

|

·

|

imposing fines.

|

The imposition of any of these penalties would severely disrupt our ability to conduct business and have a material adverse effect on our financial condition, results of operations and prospects.

Our contractual arrangements with Taiyang and its owners may not be as effective in providing control over these entities as direct ownership.

We have no equity ownership interest in Taiyang, and rely on contractual arrangements to control and operate Taiyang and its businesses. These contractual arrangements may not be as effective in providing control over the company as direct ownership. For example, Taiyang could fail to take actions required for our business despite its contractual obligation to do so. If Taiyang fails to perform under its agreements with us, we may have to rely on legal remedies under Chinese law, which may not be effective. In addition, we cannot assure you that the owners of Taiyang will act in our best interests.

Because we rely on the consulting services agreement with Taiyang for our revenue, the termination of this agreement will severely and detrimentally affect our continuing business viability under our current corporate structure.

We are a holding company and do not have any assets or conduct any business operations other than the contractual arrangements between Ningguo, our wholly owned subsidiary, and Taiyang. As a result, we currently rely entirely for our revenues on dividends payments from Ningguo after it receives payments from Taiyang pursuant to the consulting services agreement which forms a part of the contractual arrangements. The consulting services agreement has an unlimited term and continues in full force and effect until terminated. The consulting services agreement may be terminated by written notice of Ningguo or Taiyang in the event that: (a) Taiyang causes a material breach of the agreement, provided that if the breach does not relate to a financial obligation of the breaching party, that party may attempt to remedy the breach following the receipt of the written notice; (b) one party becomes bankrupt, insolvent, is the subject of proceedings or arrangements for liquidation or dissolution, ceases to carry on business, or becomes unable to pay its debts as they become due; (c) Ningguo terminates its operations; or (d) circumstances arise which would materially and adversely affect the performance or the objectives of the agreement. Additionally, Ningguo may terminate the consulting services agreement without cause. Because neither we nor our direct and indirect subsidiaries own equity interests of Taiyang, the termination of the consulting services agreement would sever our ability to continue receiving payments from Taiyang under our current holding company structure. While we are currently not aware of any event or reason that may cause the consulting services agreement to terminate, we cannot assure you that such an event or reason will not occur in the future. In the event that the consulting services agreement is terminated, this may have a severe and detrimental effect on our continuing business viability under our current corporate structure, which in turn may affect the value of your investment.

11

We rely principally on dividends paid by our consolidated operating entity to fund any cash and financing requirements we may have, and any limitation on the ability of our consolidated PRC entities to pay dividends to us could have a material adverse effect on our ability to conduct our business.

We are a holding company, and rely principally on dividends paid by our consolidated PRC operating entity for cash requirements, including the funds necessary to service any debt we may incur. In particular, we rely on earnings generated by Taiyang, which are passed on to us through Ningguo. If any of our consolidated operating subsidiaries incurs debt in its own name in the future, the instruments governing the debt may restrict dividends or other distributions on its equity interest to us. In addition, the PRC tax authorities may require us to adjust our taxable income under the contractual arrangements Ningguo currently have in place with Taiyang, in a manner that would materially and adversely affect our ability to pay dividends and other distributions on our equity interest.

Furthermore, applicable PRC laws, rules and regulations permit payment of dividends by our consolidated PRC entity only out of its retained earnings, if any, determined in accordance with PRC accounting standards. Under PRC laws, rules and regulations, our consolidated PRC entities are required to set aside at least 10.0% of their after-tax profit based on PRC accounting standards each year to their statutory surplus reserve fund until the accumulative amount of such reserves reach 50.0% of their respective registered capital. As a result, our consolidated PRC entity is restricted in its ability to transfer a portion of its net income to us whether in the form of dividends, loans or advances. As of December 31, 2010, we had retained earnings of approximately $11.5 million, of which approximately $1.4 million were appropriated as statutory reserves. Our retained earnings are not distributable as cash dividends. Any limitation on the ability of our consolidated operating subsidiaries to pay dividends to us could materially and adversely limit our ability to grow, make investments or acquisitions that could be beneficial to our businesses, pay dividends or otherwise fund and conduct our business.

Our Chief Executive Officer has potential conflicts of interest with us, which may adversely affect our business and your ability for recourse.

Mr. Wu Qiyou, our Chief Executive Officer, is also the Chairman of Taiyang and executive director of Ningguo. Conflicts of interests between their respective duties to us and Taiyang may arise. As our director and executive officer, Mr. Wu Qiyou has a duty of loyalty and care to us under U.S. and BVI law when there are any potential conflicts of interests between our company and Taiyang. We cannot assure you, however, that when conflicts of interest arise, Mr. Wu will act completely in our interests or that conflicts of interests will be resolved in our favor. For example, Mr. Wu may determine that it is in Taiyang’s interests to sever the contractual arrangements with Ningguo, irrespective of the effect such action may have on us. In addition, Mr. Wu could violate his legal duties by diverting business opportunities from us to others, thereby affecting the amount of payment that Taiyang is obligated to remit to us under the consulting services agreement.

In the event that you believe that your rights have been infringed under the securities laws or otherwise as a result of any one of the circumstances described above, it may be difficult or impossible for you to bring an action against Taiyang or our officers or directors who are members of Taiyang’s management, all of whom reside within China. Even if you are successful in bringing an action, the laws of China may render you unable to enforce a judgment against the assets of Taiyang and its management, all of which are located in China.

RISKS RELATED TO DOING BUSINESS IN CHINA

Taiyang is subject to restrictions on making payments to us.

We are a holding company incorporated in Delaware and do not have any assets or conduct any business operations other than our indirect investments in Taiyang. As a result of the holding company structure, we rely entirely on payments from Taiyang under the contractual arrangements with Ningguo. The Chinese government also imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of China. We may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency. See “Government control of currency conversion may affect the value of your investment.” Furthermore, if our affiliated entity in China incurs debt on their own in the future, the instruments governing the debt may restrict their ability to make payments. If we are unable to receive all of the revenues from our operations through these contractual arrangements, we may be unable to pay dividends on our common stock.

12

Labor laws in the PRC may adversely affect our results of operations.

On January 1, 2008, the PRC government promulgated the Labor Contract Law of the PRC, or the New Labor Contract Law. The New Labor Contract Law imposes greater liabilities on employers and significantly impacts the cost of an employer’s decision to reduce its workforce. Further, it requires certain terminations to be based upon seniority and not merit. In the event we decide to significantly change or decrease our workforce, the New Labor Contract Law could adversely affect our ability to enact such changes in a manner that is most advantageous to our business or in a timely and cost effective manner, thus materially and adversely affecting our financial condition and results of operations.

We are subject to government regulations and any change in these regulations, or the possible retroactive application of these regulations could result in additional tax liability.

Pursuant to PRC law, full-time employees are entitled to staff welfare benefits including medical care, welfare subsidies, unemployment insurance, and pension benefits through a PRC government-mandated multiemployer pension plan. We are required to contribute a portion of the employees’ salaries to the retirement benefit scheme to fund the benefits, of which, the government reserves right to change rates retroactively. In the event that the government decides to increase the amount we are required to contribute or applies such a change retroactively, we would have to reduce our capital for working capital purposes and incur charges to our earnings that could be material.

Various tax laws may result in additional tax liabilities.

Tax declarations, together with other legal compliance areas, such as customs and currency controls, are subject to review and investigation by various agencies and authorities, who are enabled by law to impose very severe fines, penalties and interest charges. These facts create tax risks in PRC substantially more significant than typically found in countries with more developed tax systems and structures. Various tax authorities could take differing positions on interpretive issues and the effect could be significant. The fact that a year has been reviewed does not close that year, or any tax declaration applicable to that year, from future review and assessment by tax authorities. If taxing authorities determine that there is an underpayment of taxes, they could impose a penalty between zero and five times the amount of taxes payable, at their discretion. If that should occur, we could incur significant penalties, which in turn could adversely affect our results of operations and financial condition.

Because our assets are located overseas, shareholders may not receive distributions that they would otherwise be entitled to if we were declared bankrupt or insolvent.

Because substantially all of our assets are located in the PRC, they may be outside of the jurisdiction of U.S. courts to administer if we are the subject of an insolvency or bankruptcy proceeding. As a result, if we declared bankruptcy or insolvency, our shareholders may not receive the distributions on liquidation that they would otherwise be entitled to if our assets were to be located within the U.S., under U.S. Bankruptcy law.

Adverse changes in economic and political policies of the PRC government could have a material adverse effect on the overall economic growth of China, which could adversely affect our business.

All of our business operations are currently conducted in the PRC, under the jurisdiction of the PRC government. Accordingly, our results of operations, financial condition and prospects are subject to a significant degree to economic, political and legal developments in China. China’s economy differs from the economies of most developed countries in many respects, including with respect to the amount of government involvement, level of development, growth rate, and control of foreign exchange and allocation of resources. While the PRC economy has experienced significant growth in the past 20 years, growth has been uneven across different regions and among various economic sectors of China. The PRC government has implemented various measures to encourage economic development and guide the allocation of resources. Some of these measures benefit the overall PRC economy, but may also have a negative effect on us. For example, our financial condition and results of operations may be adversely affected by government control over capital investments or changes in tax regulations that are applicable to us. Since early 2004, the PRC government has implemented certain measures to control the pace of economic growth. Such measures may cause a decrease in the level of economic activity in China, which in turn could adversely affect our results of operations and financial condition.

13

Unprecedented rapid economic growth in China may increase our costs of doing business, and may negatively impact our profit margins and/or profitability.

Our business depends in part upon the availability of relatively low-cost labor and materials. Rising wages in China may increase our overall costs of production. In addition, rising raw material costs, due to strong demand and greater scarcity, may increase our overall costs of production. If we are not able to pass these costs on to our customers in the form of higher prices, our profit margins and/or profitability could decline.

You may face difficulties in protecting your interests, and your ability to protect your rights through the U.S. federal courts may be limited, because our subsidiaries are incorporated in non-U.S. jurisdictions, we conduct substantially all of our operations in China, and most of our officers reside outside the United States.

Although we are incorporated in Delaware, all of our business operations are conducted in China by Taiyang. Most of our officers and directors reside in China and some or all of the assets of those persons are located outside of the United States. As a result, it may be difficult or impossible for you to bring an action against us or against these individuals in China in the event that you believe that your rights have been infringed under the securities laws or otherwise. Even if you are successful in bringing an action of this kind, the laws of the PRC may render you unable to enforce a judgment against our assets or the assets of our directors and officers.

As a result of all of the above, our shareholders may have more difficulty in protecting their interests through actions against our management, directors or major shareholders than would shareholders of a corporation doing business entirely within the United States.

Governmental control of currency conversion may affect the value of your investment.

The Chinese government imposes controls on the convertibility of RMB into foreign currencies and, in certain cases, the remittance of currency out of China. We receive substantially all of our revenues in RMB. Under our current structure, our income is primarily derived from payments from Taiyang. Shortages in the availability of foreign currency may restrict the ability of our Chinese subsidiaries and our affiliated entity to remit sufficient foreign currency to pay dividends or other payments to us, or otherwise satisfy their foreign currency denominated obligations. Under existing Chinese foreign exchange regulations, payments of current account items, including profit distributions, interest payments and expenditures from trade-related transactions, can be made in foreign currencies without prior approval from China State Administration of Foreign Exchange by complying with certain procedural requirements. However, approval from appropriate government authorities is required where RMB is to be converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of bank loans denominated in foreign currencies. The Chinese government may also at its discretion restrict access in the future to foreign currencies for current account transactions. If the foreign exchange control system prevents us from obtaining sufficient foreign currency to satisfy our currency demands, we may not be able to pay dividends in foreign currencies to our stockholders.

Fluctuation in the value of RMB may have a material adverse effect on your investment.

The value of RMB against the U.S. dollar and other currencies may fluctuate and is affected by, among other things, changes in political and economic conditions. Our revenues and costs are mostly denominated in RMB, while a significant portion of our financial assets are denominated in U.S. dollars. We rely entirely on fees paid to us by our affiliated entity in China. Any significant fluctuation in the value of RMB may materially and adversely affect our cash flows, revenues, earnings and financial position, and the value of, and any dividends payable on, our stock in U.S. dollars. For example, an appreciation of RMB against the U.S. dollar would make any new RMB denominated investments or expenditures more costly to us, to the extent that we need to convert U.S. dollars into RMB for such purposes. An appreciation of RMB against the U.S. dollar would also result in foreign currency translation losses for financial reporting purposes when we translate our U.S. dollar denominated financial assets into RMB, as RMB is our reporting currency.

14

Dividends we receive from our subsidiary located in the PRC may be subject to PRC withholding tax.

The recently enacted PRC Enterprise Income Tax Law, or the EIT Law, and the implementation regulations for the EIT Law issued by the PRC State Council, became effective as of January 1, 2008. The EIT Law provides that a maximum income tax rate of 20% is applicable to dividends payable to non-PRC investors that are “non-resident enterprises,” to the extent such dividends are derived from sources within the PRC, and the State Council has reduced such rate to 10% through the implementation regulations. We are a Delaware holding company and substantially all of our income is derived from the operations of Taiyang located in the PRC, which is contractually obligated to pay its quarterly profits to our WFOE. Therefore, dividends paid to us by our WFOE in China may be subject to the 10% income tax if we are considered as a “non-resident enterprise” under the EIT Law. We believe that we will be considered a non-resident enterprise. If we are required under the EIT Law and its implementation regulations to pay income tax for any dividends we receive from our WFOE, it may have a material and adverse effect on our net income and materially reduce the amount of dividends, if any, we may pay to our shareholders.

Governmental control of currency conversion may affect the value of your investment.

The PRC government imposes controls on the convertibility of the RMB into foreign currencies and, in certain cases, the remittance of currency out of China. We receive all our revenues in RMB. Under our current corporate structure, our income is primarily derived from dividend payments from our WFOE. Shortages in the availability of foreign currency may restrict the ability of our WFOE to remit sufficient foreign currency to pay dividends or other payments to us, or otherwise satisfy their foreign currency-denominated obligations. Under existing PRC foreign exchange regulations, payments of current account items, including profit distributions, interest payments and expenditures from trade related transactions, can be made in foreign currencies without prior approval from the State Administration of Foreign Exchange (“SAFE”) by complying with certain procedural requirements. However, approval from the SAFE or its local branch is required where RMB is to be converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of loans denominated in foreign currencies. The PRC government may also at its discretion restrict access in the future to foreign currencies for current account transactions. If the foreign exchange control system prevents us from obtaining sufficient foreign currency to satisfy our currency demands, we may not be able to pay dividends in foreign currencies to our shareholders.

The land on which our facilities are located could be subject to appropriation by the PRC government.

There is no private ownership of land in China. All land ownership is held by the government of the PRC, its agencies and collectives. Land use rights can be transferred upon approval by the land administrative authorities of the PRC (State Land Administration Bureau) upon payment of the required land transfer fee. We have acquired the land use rights for our facilities through 2055, however, under PRC law, land use rights can be revoked and the tenants forced to vacate at any time when re-development of the land is in the public interest. There is no assurance that the land use rights for this location will not be revoked.

We may have difficulty establishing adequate management, legal and financial controls in the PRC.

The PRC historically has not adopted a Western style of management and financial reporting concepts and practices, as in modern banking, computer and other control systems. Although we currently have over 500 employees in China, have not experienced difficulty to date in hiring qualified employees, and do not have any plans to hire a significant amount of employees or any significant employees in the near future, we may have difficulty in the future hiring and retaining a sufficient number of qualified employees to work in the PRC. As a result of these factors, we may experience difficulty in establishing management, legal and financial controls, collecting financial data and preparing financial statements, books of account and corporate records and instituting business practices that meet Western standards. Therefore, we may, in turn, experience difficulties in implementing and maintaining adequate internal controls as will be required under Section 404 of the Sarbanes Oxley Act of 2002.

15

RISKS RELATED TO OUR COMMON STOCK

There has been a limited trading market for our Common Stock and no market.

It is anticipated that there will be a limited trading market for the Common Stock on the Over-the-Counter Bulletin Board. The lack of an active market may impair your ability to sell your shares at the time you wish to sell them or at a price that you consider reasonable. The lack of an active market may also reduce the fair market value of your shares. An inactive market may also impair our ability to raise capital by selling shares of capital stock and may impair our ability to acquire other companies or technologies by using Common Stock as consideration.

You may have difficulty trading and obtaining quotations for our Common Stock.

The Common Stock may not be actively traded, and the bid and asked prices for our Common Stock on the Over-the-Counter Bulletin Board may fluctuate widely. As a result, investors may find it difficult to dispose of, or to obtain accurate quotations of the price of, our securities. This severely limits the liquidity of the Common Stock, and would likely reduce the market price of our Common Stock and hamper our ability to raise additional capital.

The market price of our Common Stock may, and is likely to continue to be, highly volatile and subject to wide fluctuations.

The market price of our Common Stock is likely to be highly volatile and could be subject to wide fluctuations in response to a number of factors that are beyond our control, including:

|

·

|

dilution caused by our issuance of additional shares of Common Stock and other forms of equity securities, which we expect to make in the Offering and in connection with future capital financings to fund our operations and growth, to attract and retain valuable personnel and in connection with future strategic partnerships with other companies;

|

|

|

·

|

quarterly variations in our revenues and operating expenses;

|

|

|

·

|

changes in the valuation of similarly situated companies, both in our industry and in other industries;

|

|

|

·

|

changes in analysts’ estimates affecting our company, our competitors and/or our industry;

|

|

|

·

|

changes in the accounting methods used in or otherwise affecting our industry;

|

|

|

·

|

additions and departures of key personnel;

|

|

|

·

|