UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

For the fiscal year ended December 31 , 2022

or

For the transition period from ___ to ___

Commission file number 001-38160

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||

| (Address of Principal Executive Offices) | (Zip Code) | |||||||||||||

| Registrant's telephone number, including area code | |||||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | ||||||||||||||

| ☒ | ☐ | No | ||||||||||||

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. | ||||||||||||||

| ☐ | Yes | ☒ | ||||||||||||

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | ||||||||||||||

| ☒ | ☐ | No | ||||||||||||

| Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | ||||||||||||||

| ☒ | ☐ | No | ||||||||||||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ||||||||||||||

| ☐ | ||||||||||||||

| Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. | ||||||||||||||

| If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statement of the registrant included in the filing reflect the correction of an error to previously issued financial statements. | ||||||||||||||

| ☐ | ||||||||||||||

| Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). | ||||||||||||||

| ☐ | ||||||||||||||

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | ||||||||||||||

| Yes | ☒ | No | ||||||||||||

As of the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the registrant's common stock held by its non-affiliates, computed by reference to the price at which the common stock was last sold, was $864,727,436 .

The registrant had 109,735,021 shares of common stock outstanding as of February 10, 2023.

DOCUMENTS INCORPORATED BY REFERENCE

Redfin Corporation

Annual Report on Form 10-K

For the Year Ended December 31, 2022

Table of Contents

| PART I | Page | |||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II | ||||||||

Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 9C. | ||||||||

| PART III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| PART IV | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

As used in this annual report, the terms "Redfin," "we," "us," and "our" refer to Redfin Corporation and its subsidiaries taken as a whole, unless otherwise noted or unless the context indicates otherwise. However, when referencing (i) the 2023 notes, the 2025 notes, and the 2027 notes, the terms “we,” “us,” and “our” refer only to Redfin Corporation and not to Redfin Corporation and its subsidiaries taken as a whole, (ii) the secured revolving credit facility with Goldman Sachs, the terms "we," "us," and "our" refer only to RedfinNow Borrower LLC, and (iii) each warehouse credit facility, the terms "we," "us"," and "our" refer only to Redfin Mortgage, LLC or Bay Equity LLC, as the context dictates.

Note Regarding Forward-Looking Statements

This annual report contains forward-looking statements. All statements contained in this report other than statements of historical fact, including statements regarding our future operating results and financial position, our business strategy and plans, our market growth and trends, and our objectives for future operations, are forward-looking statements. The words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “could,” “would,” “project,” “plan,” "hope," “potentially,” “preliminary,” “likely,” and similar expressions are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and trends that we believe may affect our financial condition, results of operations, business strategy, short-term and long-term business operations and objectives, and financial needs. These forward-looking statements are subject to a number of risks, uncertainties, and assumptions, including those described under Item 1A. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the effect of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties, and assumptions, the future events and trends discussed in this report may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements. Accordingly, you should not rely on forward-looking statements as predictions of future events. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee that the future results, performance, or events and circumstances reflected in the forward-looking statements will be achieved or occur. We undertake no obligation to update any of these forward-looking statements for any reason after the date of this report or to conform these statements to actual results or revised expectations.

Note Regarding Industry and Market Data

This annual report contains information using industry publications that generally state that the information contained therein has been obtained from sources believed to be reliable, but such information may not be accurate or complete. While we are not aware of any misstatements regarding the information from these industry publications, we have not independently verified any of the data from third-party sources nor have we ascertained the underlying economic assumptions relied on therein.

i

PART I

Item 1. Business

Overview

We help people buy and sell homes. Representing customers in over 100 markets in the United States, we are a residential real estate brokerage. We pair our own agents with our own technology to create a service that is faster, better, and costs less. We meet customers through our listings-search website and mobile application.

We use the same combination of technology and local service to originate mortgage loans and offer title and settlement services. Beginning in April 2021, we also offer digital platforms to connect consumers with available apartments and houses for rent.

Our mission is to redefine real estate in the consumer’s favor.

Representing Customers

Our brokerage efficiency results in savings that we share with our customers. We charge most home sellers a commission of 1% to 1.5%, compared to the 2.5% to 3% typically charged by traditional brokerages.

The results of our customer-first approach are clear. We:

•helped customers buy or sell more than 497,000 homes worth more than $249 billion through 2022;

•saved customers more than $1.5 billion, when compared to a 2.5% commission, since our launch in 2006;

•drew more than 49 million monthly average visitors to our website and mobile application in 2022, 5% more compared to 2021;

•had customers buy and sell the same home with us at a 32% higher rate than competing brokerages;

•sold Redfin-listed homes for nearly $1,800 more on average than competing brokerages’ similar listings in 2022, according to a study we commissioned; and

•had listings on the market for an average of less than 23 days in 2021 compared to the industry average of more than 26 days, according to a study we commissioned; and, according to the same study, approximately 97% of Redfin listings sold within 90 days versus the industry average of approximately 95%.

To serve customers when our own agents can’t due to high demand or geographic limitations, we’ve developed partnerships with over 8,700 agents at other brokerages. Once we refer a customer to a partner agent, that agent, not us, represents the customer from the initial meeting through closing, at which point the agent pays us a portion of her commission as a referral fee.

Complete Customer Solution

Our long-term goal is to combine brokerage, rentals, mortgage, and title services into one solution, sharing information, coordinating deadlines, and streamlining processes so that a consumer's move is easier and often less costly. As we integrate these services more closely over time, we believe we can help consumers move much more efficiently than a combination of stand-alone companies ever could.

Bay Equity underwrites mortgage loans and, after originating each loan, Bay Equity sells most of the loans to third-party mortgage investors, retains a small amount of mortgage servicing rights, and services a small portfolio of loans. Bay Equity is licensed in 49 states and the District of Columbia. These markets accounted for 84% of our brokerage's buy-side transactions in 2022.

Title Forward offers title and settlement services. Title Forward has officially launched in 27 markets across eight states and the District of Columbia. These markets accounted for 45% of our brokerage's transactions in 2022.

1

RedfinNow bought homes directly from homeowners and resells them to homebuyers. In November 2022, we decided to wind-down RedfinNow and expect to complete the liquidation of our RedfinNow inventory in the second quarter of 2023.

Rent. offers an end-to-end digital marketing platform that connects consumers with available apartments and houses for rent across all 50 states and the District of Columbia.

Competition

The residential brokerage industry is highly fragmented, with numerous active licensed agents and brokerages, and is evolving rapidly in response to technological advancements, changing customer preferences, and new offerings. We compete primarily against other residential real estate brokerages, which include franchise operations affiliated with national or local brands, and small independent brokerages. We also compete with hybrid residential brokerages, which combine Internet technology and brokerage services, and a growing number of others that operate with non-traditional real estate business models. Competition is particularly intense in some of the densely populated metropolitan markets we serve, as they are dominated by entrenched real estate brokerages and are the primary markets for innovative and well-capitalized new entrants.

We believe we compete primarily based on:

•access to timely, accurate data about homes for sale;

•traffic to our website and mobile application, which themselves are subject to competition against real estate data websites that aggregate listings and sell advertising to traditional brokers;

•the speed and quality of our service, including agent responsiveness and local knowledge;

•our ability to hire and retain agents who deliver the best customer service;

•the costs of delivering our service and the price of our service to consumers;

•consumer awareness of our service and the effectiveness of our marketing efforts;

•technological innovation; and

•depth and breadth of local referral networks.

Bay Equity competes with numerous national and local multi-product banks as well as focused mortgage originators. We compete primarily on service, product selection, interest rates, and origination fees.

Title Forward competes with numerous national and local companies that typically focus solely on these services. We compete primarily on timeliness of service and fees.

Rent. competes with companies that provide an online marketplace for residential rental listings and related digital marketing solutions. We compete primarily on the scope and quality of listings we offer on our digital platforms, our value-added digital marketing solutions, traffic generated through our websites and mobile applications, and the breadth of our broader marketing services.

Seasonality

For the impact of seasonality on our business, see "Quarterly Results of Operations and Key Business Metrics" under Item 7.

2

Our Lead Agents

Our goal is to be the best employer in real estate. At the heart of this goal is an investment in the real estate agents who directly help our customers buy and sell homes. We refer to these agents as our lead agents. Unlike traditional real estate brokerages, where agents work as independent contractors, we employ our lead agents and pay them a salary, offer them an opportunity to earn additional cash and equity compensation, and provide them with health insurance and other benefits. As a result, our lead agents in 2022 earned a median income that was more than two times as much as agents at competing brokerages. Also in 2022, our lead agents were, on average, more than twice as productive as agents at competing brokerages. Our investment in our lead agents has resulted in a significant competitive advantage in agent retention. From 2020 to 2021, our lead agent retention was 77% compared with 66% for the industry, and from 2021 to 2022 (which was impacted by our layoffs) our retention was 66% compared with 61% for the industry. Our ability to attract, develop, and retain lead agents is critical to our success.

As of December 31, 2022, we had 5,572 employees. For 2022, our average number of lead agents was 2,426. See "Key Business Metrics - Average Number of Lead Agents" under Item 7.

Our Executive Officers

Below is information regarding our executive officers. Each executive officer holds office until his or her successor is duly elected and qualified or until the officer’s earlier resignation, disqualification, or removal.

•Glenn Kelman, age 52, has served as our chief executive officer since September 2005 and one of our directors since March 2006.

•Bridget Frey, age 45, has been employed by us since June 2011 and has served as our chief technology officer since February 2015.

•Anthony Kappus, age 42, has been employed by us since March 2014 and has served as our chief legal officer since May 2021. Mr. Kappus previously served as our senior vice president - legal affairs from August 2018 to May 2021 and vice president - legal from September 2014 to August 2018.

•Chris Nielsen, age 56, has served as our chief financial officer since June 2013.

•Anna Stevens, age 49, has served as our chief human resources officer since August 2022. Prior to joining Redfin, Ms. Stevens served as the Chief People Officer of HD Supply, Inc., a North American industrial distributor.

•Christian Taubman, age 44, has served as our chief growth officer since April 2021. Mr. Taubman previously served as our chief product officer from October 2019 to April 2021. Prior to joining Redfin, Mr. Taubman served in several different roles with Amazon (a technology company) from April 2011 to October 2019. As Director - Smart Home Verticals from December 2017 to October 2019, Mr. Taubman led employees in product management, software engineering, and program management, with the mission of helping customers to connect more smart devices to Amazon's Alexa virtual assistant.

•Adam Wiener, age 44, has been employed by us since October 2007 and has served as our president of real estate operations since April 2021. Mr. Wiener previously served as our chief growth officer from July 2015 to April 2021.

Our Regulatory Environment

The residential real estate industry is heavily regulated by federal, state, and local governments in the United States. Because of our complete customer solution approach of combining brokerage, rentals, mortgage, title services, a customer may be able to receive more than one real estate-related service from us. Accordingly, some government regulations affect more than one of our operating segments and may impact our ability to offer multiple services to the same customer.

3

For example, the Real Estate Settlement Procedures Act of 1974 restricts, with some exceptions, kickbacks or referral fees that real estate settlement service providers, such as brokerages, mortgage originators, and title and closing service providers, may pay or receive in connection with the referral of settlement services. Furthermore, the Fair Housing Act of 1968 (the “FHA”) prohibits discrimination in the purchase or sale of homes. The FHA applies to real estate agents, mortgage lenders, title companies, and home sellers, such as RedfinNow, as well as many forms of advertising and communications, including MLS listings and insights about home listings.

Additionally, our brokerage, mortgage, and title business each requires a license specific to its business from each state in which it operates, and the licensing requirements vary by state. Furthermore, some of our employees who provide services for these businesses must also hold individual licenses. These entity and individual licenses may be costly to obtain and maintain, which may adversely affect our company’s earnings.

Our Website and Public Filings

Our website is www.redfin.com. Through this website, we make available, free of charge, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as soon as reasonably practicable after we file such material with, or furnish it to, the U.S. Securities and Exchange Commission (the "SEC").

4

Item 1A. Risk Factors

You should carefully consider the risks described below, together with all other information in this annual report, before investing in any of our securities. The occurrence of any single risk or any combination of risks could materially and adversely affect our business, operating results, financial condition, liquidity, or competitive position, and consequently, the value of our securities. The material adverse effects include, but are not limited to, not growing our revenue or market share at the pace that they have grown historically or at all, our revenue and market share fluctuating on a quarterly and annual basis, an extension of our history of losses and a failure to become profitable, not achieving the revenue and net income (loss) guidance that we provide, and harm to our reputation and brand.

Risks Related to Our Business and Industry

Our business depends significantly on the health of the U.S. residential real estate industry and macroeconomic factors.

Our success depends largely on the health of the U.S. residential real estate industry. This industry, in turn, is affected by changes in general economic conditions, which are beyond our control. Any of the following factors could reduce the volume of residential real estate transactions, cause a decline in the prices at which homes are bought and sold, or otherwise adversely affect the industry and harm our business:

•seasonal or cyclical downturns in the U.S. residential real estate industry, which may be due to any single factor, or a combination of factors, listed below, or factors which are currently not known to us or that have not historically affected the industry;

•slow economic growth or recessionary conditions;

•increased unemployment rates or stagnant or declining wages;

•inflationary conditions;

•low consumer confidence in the economy or the U.S. residential real estate industry;

•adverse changes in local or regional economic conditions in the markets that we serve, particularly our top-10 markets and markets into which we are attempting to expand;

•increased mortgage rates; reduced availability of mortgage financing; or increased down payment requirements;

•low home inventory levels, which may result from zoning regulations, higher construction costs, and housing market uncertainty that discourages some home sellers, among other factors;

•lack of affordably priced homes, which may result from home prices growing faster than wages, among other factors;

•volatility and general declines in the stock market or lower yields on individuals' investment portfolios;

•increased expenses associated with home ownership, including rising insurance costs that may result from more frequent and severe natural disasters and inclement weather;

•newly enacted and potential federal, state, and local legislative actions, as well as new judicial decisions, that would affect the residential real estate industry generally or in our top-10 markets, including (i) actions or decisions that would increase the tax liability arising from buying, selling, or owning real estate, (ii) actions or decisions that would change the way real estate brokerage commissions are negotiated, calculated, or paid, and (iii) actions or decisions that would discourage individuals from owning, or obtaining a mortgage on, more than one home, and (iv) potential reform relating to Fannie Mae, Freddie Mac, and other government sponsored entities that provide liquidity to the mortgage market;

•changes that cause U.S. real estate to be more expensive for foreign purchases, such as (i) increases in the exchange rate for the U.S. dollar compared to foreign currencies and (ii) foreign regulatory changes or capital controls that make it more difficult for foreign purchasers to withdraw capital from their home countries or purchase and hold U.S. real estate;

•changed generational views on homeownership and generally decreased financial resources available for purchasing homes; and

5

•war, terrorism, political uncertainty, natural disasters, inclement weather, health epidemics or pandemics, and acts of God, including the affect of COVID-19 on the residential real estate market in the United States.

Our real estate services segment, which is our largest segment by gross profit, is concentrated in certain geographic markets. Our failure to adapt to any substantial shift in the relative percentage of residential housing transactions from these markets to other markets in the United States could adversely affect our financial performance.

For the year ended December 31, 2022, our top-10 markets by real estate services revenue consisted of the metropolitan areas of Boston, Chicago, Denver (including Boulder and Colorado Springs), Los Angeles (including Santa Barbara), Maryland, Northern Virginia, Portland (including Bend), San Diego, San Francisco, and Seattle.

Local and regional conditions in these markets may differ significantly from prevailing conditions in the United States or other parts of the country. Accordingly, events may adversely and disproportionately affect demand for and sales prices of homes in these markets. Any overall or disproportionate downturn in demand or home prices in any of our largest markets, particularly if we are unable to increase revenue from our other markets, could adversely affect growth of our revenue and market share or otherwise harm our business.

Our top markets are primarily major metropolitan areas, where home prices and transaction volumes are generally higher than other markets. As a result, our real estate services revenue and gross margin are generally higher in these markets than in our smaller markets. To the extent there is a long-term net migration to cities outside of these markets, the relative percentage of residential housing transactions may shift away from the top markets where we have historically generated most of our revenue. Our inability to adapt to any shift, including failing to increase revenue from other markets, could adversely affect our financial performance and market share.

Competition in each of our lines of business is intense.

Many of our competitors across each of our businesses have substantial competitive advantages, such as longer operating histories, stronger brand recognition, greater financial resources, more management, sales, marketing and other resources, superior local referral networks, perceived local knowledge and expertise, and extensive relationships with participants in the residential real estate industry, including third-party data providers such as multiple listing services ("MLSs"). Consequently, these competitors may have an advantage in recruiting and retaining agents, attracting consumers, and growing their businesses. They may also be able to provide consumers with offerings that are different from or superior to those we provide. The success of our competitors could result in our loss of market share and harm our business.

We may be unable to maintain or improve our current technology offerings at a competitive level or develop new technology offerings that meet customer or agent expectations. Our technology offerings may also contain undetected errors or vulnerabilities.

Our technology offerings, including tools, features, and products, are key to our competitive plan for attracting potential customers and hiring and retaining lead agents. Maintaining or improving our current technology to meet evolving industry standards and customer and agent expectations, as well as developing commercially successful and innovative new technology, is challenging and expensive. For example, the nature of development cycles may result in delays between the time we incur expenses and the time we introduce new technology and generate revenue, if any, from those investments. Anticipated customer demand for a technology offering could also decrease after the development cycle has commenced, and we would not be able to recoup costs, which may be substantial, we incurred.

As standards and expectations evolve and new technology becomes available, we may be unable to identify, design, develop, and implement, in a timely and cost-effective manner, new technology offerings to meet those standards and expectations. As a result, we may be unable to compete effectively, and to the extent our competitors develop new technology offerings faster than us, they may render our offerings noncompetitive or obsolete. Additionally, even if we implemented new technology offerings in a timely manner, our customers and agents may not accept or be satisfied by the offerings.

6

Furthermore, our development and testing processes may not detect errors and vulnerabilities in our technology offerings prior to their implementation. Any inefficiencies, errors, technical problems, or vulnerabilities arising in our technology offerings after their release could reduce the quality of our services or interfere with our customers' and agents' access to and use of our technology and offerings.

We may be unable to obtain and provide comprehensive and accurate real estate listings quickly, or at all.

We believe that users of our website and mobile application come to us primarily because of the real estate listing data that we provide. Accordingly, if we were unable to obtain and provide comprehensive and accurate real estate listings data, our primary channels for meeting customers will be diminished. We get listings data primarily from MLSs in the markets we serve. We also source listings data from public records, other third-party listing providers, and individual homeowners and brokers. Many of our competitors and other real estate websites also have access to MLSs and other listings data, including proprietary data, and may be able to source listings data or other real estate information faster or more efficiently than we can. Since MLS participation is voluntary, brokers and homeowners may decline to post their listings data to their local MLS or may seek to change or limit the way that data is distributed. A competitor or another industry participant could also create an alternative listings data service, which may reduce the relevancy and comprehensive nature of the MLSs. If MLSs cease to be the predominant source of listings data in the markets that we serve, we may be unable to get access to comprehensive listings data on commercially reasonable terms, or at all, which may result in fewer people using our website and mobile application.

We rely on business data to make decisions and drive our machine-learning technology, and errors or inaccuracies in such data may adversely affect our business decisions and the customer experience.

We regularly analyze business data to evaluate growth trends, measure our performance, establish budgets, and make strategic decisions. While our business decisions are based on what we believe to be reasonable calculations for the applicable period of measurement, there are inherent challenges in measuring and interpreting the data, and we cannot be certain that the data are accurate. Errors or inaccuracies in the data could result in poor business decisions, resource allocation, or strategic initiatives. For example, if we overestimate traffic to our website and mobile application, we may not invest an adequate amount of resources in attracting new customers or we may hire more lead agents in a given market than necessary to meet customer demand.

We also use our business data and proprietary algorithms to inform our machine learning, such as in the calculation of our Redfin Estimate, which provides an estimate on the market value of individual homes. If customers disagree with us or if our Redfin Estimate fails to accurately reflect market pricing such that we are unable to attract homebuyers or help our customers sell their homes at satisfactory prices, or at all, customers may lose confidence in us.

We may be unable to attract homebuyers and home sellers to our website and mobile application in a cost-effective manner.

Our website and mobile application are our primary channels for meeting new customers. Accordingly, our success depends on our ability to attract homebuyers and home sellers to our website and mobile application in a cost-effective manner. To meet customers, we rely heavily on traffic generated from search engines and downloads of our mobile application from mobile application stores. We also rely on marketing methods such as targeted email campaigns, paid search advertising, social media marketing, and traditional media, including TV, radio, and billboards.

7

The number of visitors to our website and downloads of our mobile application depend in large part on how and where our website and mobile application rank in Internet search results and mobile application stores, respectively. While we use search engine optimization to help our website rank highly in search results, maintaining or improving our search result rankings is not within our control. Internet search engines frequently update and change their ranking algorithms, referral methodologies, or design layouts, which determine the placement and display of a user’s search results. In some instances, Internet search engines may change these rankings, which may have the effect of promoting their own competing services or the services of one or more of our competitors. Similarly, mobile application stores can change how they display searches and how mobile applications are featured. For instance, editors at the Apple App Store can feature prominently editor-curated mobile applications and cause the mobile application to appear larger than other applications or more visibly on a featured list.

Additionally, our marketing efforts may fail to attract the desired number of customers for a variety of reasons, including the possibility that the creative treatment for our advertisements may be ineffective or new third-party email delivery policies may make it more difficult for us to execute targeted email campaigns.

If we are unable to deliver a rewarding experience on mobile devices, whether through our mobile website or mobile application, we may be unable to attract and retain customers.

Developing and supporting a mobile website and mobile application across multiple operating systems and devices requires substantial time and resources. We may not be able to consistently provide a rewarding customer experience on mobile devices and, as a result, customers we meet through our mobile website or mobile application may not choose to use our services at the same rate as customers we meet through our website.

As new mobile devices and mobile operating systems are released, we may encounter problems in developing or supporting our mobile website or mobile application for them. Developing or supporting our mobile website or mobile application for new devices and their operating systems may require substantial time and resources. The success of our mobile website and mobile application could also be harmed by factors outside of our control, such as:

•increased costs to develop, distribute, or maintain our mobile website or mobile application;

•changes to the terms of service or requirements of a mobile application store that requires us to change our mobile application development or features in an adverse manner; and

•changes in mobile operating systems, such as Apple’s iOS and Google’s Android, that disproportionately affect us, degrade the functionality of our mobile website or mobile application, require that we make costly upgrades to our technology offerings, or give preferential treatment to competitors' websites or mobile applications.

Our business model of employing lead agents subjects us to challenges not faced by our competitors. Our ability to hire and retain a sufficient number of lead agents is critical to our ability to maintain and grow our market share and to provide an adequate level of service to customers who want to work with our lead agents.

As a result of our business model of employing our lead agents, our lead agents generally earn less on a per transaction basis than traditional agents who work as independent contractors at traditional brokerages. Because our model is uncommon in our industry, agents considering working for us may not understand our compensation model or may not perceive it to be more attractive than the independent contractor, commission-driven compensation model used by most traditional brokerages. Additionally, due to the costs of employing our lead agents, lead agent turnover may be more costly to us than to traditional brokerages. If we are unable to attract, retain, effectively train, motivate, and utilize lead agents, we will be unable to offset the costs of employing them and grow our business. We may also be required to change our compensation model, which could significantly increase our lead agent compensation or other costs.

Also as a result of employing our lead agents, we incur costs that our brokerage competitors do not, such as base pay, employee benefits, expense reimbursement, training, and employee transactional support staff. Because of this, we have significant costs that, in the event of downturns in demand in the markets we serve, may result in us being unable to adjust as rapidly as some of our competitors. In turn, such downturns may impact us more than our competitors.

8

Conversely, in times of rapidly rising demand we may face a shortfall of lead agents. To the extent our customer demand increases from current levels, our ability to adequately serve the additional customers, and in turn grow our revenue and U.S. market share by value, depends, in part, on our ability to timely hire and retain additional lead agents. To the extent we are unable to hire, either timely or at all, or retain the required number of lead agents to serve our customer demand, we will be unable to maximize our revenue and market share growth. Although we are able to refer excess demand to our partner agents, historically our partner agents have closed transactions with customers they meet at a lower rate than our lead agents and have generated lower revenue per transaction.

Referring customers to our partner agents may harm our business.

We refer customers to third-party partner agents when we do not have a lead agent available due to high demand or geographic limitations. Our dependence on partner agents can be particularly heavy in certain new markets as we build our operations to scale in those markets or during times of rapidly rising demand for our services. Our partner agents are independent licensed agents affiliated with other brokerages, and we do not have any control over their actions. If our partner agents were to provide poor customer service, engage in malfeasance, or otherwise violate the laws and rules to which we are subject, we may be subject to legal claims and our reputation and business may be harmed.

Our arrangements with third parties may limit our growth and brand awareness. For example, referring customers to partner agents potentially redirects repeat and referral opportunities to the partner agents.

If we do not comply with the rules, terms of service, and policies of REALTOR® associations and MLSs, our access to and use of listings data may be restricted or terminated.

We must comply with the rules, terms of service, and policies of REALTOR® associations and MLSs to access and use MLSs' listings data. We belong to numerous REALTOR® associations and MLSs, and each has adopted its own rules, terms of service, and policies governing, among other things, how MLS data may be used and how listings data must be displayed on our website and mobile application. These rules typically do not contemplate multi-jurisdictional online brokerages like ours and vary widely among markets. They also are in some cases inconsistent with the rules of other REALTOR® associations and MLSs such that we are required to customize our website, mobile application, or service to accommodate differences between rules of REALTOR® associations and MLSs. Complying with the rules of each REALTOR® association and MLS requires significant investment, including personnel, technology and development resources, and the exercise of considerable judgment. If we are deemed to be noncompliant with a REALTOR® association or MLS’s rules, we may face disciplinary sanctions in that association or MLS, which could include monetary fines, restricting or terminating our access to that MLS’s data, or other disciplinary measures. The loss or degradation of this listings data could materially and adversely affect traffic to our website and mobile application, making us less relevant to consumers and restricting our ability to attract customers. It also could reduce agent and customer confidence in our services and harm our business.

If we fail to comply with the requirements governing the licensing of our brokerage, mortgage, and title businesses in the jurisdictions in which we operate, then our ability to operate those businesses in those jurisdictions may be revoked.

Redfin, as a brokerage, and our agents must comply with the requirements governing the licensing and conduct of real estate brokerage and brokerage-related businesses in the markets where we operate. Furthermore, we are also required to comply with the requirements governing the licensing and conduct of mortgage and title and settlement businesses in the markets where we operate. Due to the geographic scope of our operations, we and our agents may not be in compliance with all of the required licenses at all times. Additionally, if we enter into new markets, we may become subject to additional licensing requirements. If we or our agents fail to obtain or maintain the required licenses for conducting our brokerage, mortgage, and title businesses or fail to strictly adhere to associated regulations, the relevant government authorities may order us to suspend relevant operations or impose fines or other penalties.

9

Our wind-down plan for our RedfinNow operations may adversely impact our business, results of operations, financial performance, and reputation.

There are risks and uncertainties inherent to the wind-down of RedfinNow operations that could adversely impact our overall business, results of operations, financial performance, and reputation, including, but not limited to:

•Our ability to operate RedfinNow during the wind-down period, including our ability to successfully complete ongoing renovations of homes we’ve purchased, and to market and close on the sale of homes in inventory, may be adversely impacted by market conditions or other factors which could lead to longer hold times for homes in inventory, increased holding, renovation, and transactions costs, lower sales prices, and an overall decrease in profitability.

•Our financial projections and financial performance may be adversely impacted by, among other things, the accuracy of the estimates and assumptions related to the wind-down of RedfinNow operations on which our projections are based; other facts we discover that could require us to incur additional expense and record additional charges that may be materially different from our initial expectations about the financial performance of the business and the costs of the wind-down; and unanticipated changes to management’s estimates (including, but not limited to, the accounting for the estimated net realizable value of inventory), reserves, or allowances and future costs we incur, such as those related to warranty or consumer claims.

•Our decision to wind-down our RedfinNow operations may have unintended impacts on our other business lines by, among other things, limiting our ability to meet new potential homebuyers and home sellers through marketing cash offers fulfilled by RedfinNow, limiting, and ultimately eliminating, the sale of RedfinNow-owned homes through our real estate services segment, and similarly impacting our title and settlement operations.

•RedfinNow may have overestimated the amount it should pay to purchase a home, and homes owned by it may significantly decline in value prior to being sold. As a result, we may be required to significantly write down the inventory value of homes and, to the extent we are able to resell homes at all, resell them at a price that is substantially less than our costs of acquiring and renovating the homes.

The extent to which the wind-down will impact our operations will depend on future developments, which are highly uncertain and cannot be predicted. Any of these risks could delay our wind-down of RedfinNow operations, increase costs and charges associated with the wind-down and disrupt the operations of our other businesses, any of which may adversely impact our business, results of operations, financial performance, and reputation.

It’s possible that the net proceeds Bay Equity receives from the sale of mortgage loans it originates may not exceed the loan amount. Additionally, Bay Equity may also be unable to sell its originated loans at all. In that situation, Bay Equity will need to service the loans and potentially foreclose on the home by itself or through a third party, and either option could impose significant costs, time, and resources on Bay Equity. Bay Equity’s inability to sell its originated loans could also expose us to adverse market conditions affecting mortgage loans.

Bay Equity intends to sell most of the mortgage loans that it originates to investors in the secondary mortgage market. Bay Equity's ability to sell its originated loans in the secondary market, and receive net proceeds from the sale that exceed the loan amount, depends largely on there being sufficient liquidity in the secondary market and its compliance with contracts with investors who have purchased the loans.

10

Demand in the secondary market for mortgage loans, and Bay Equity’s ability to sell the mortgage loans that it originates on favorable terms and in a timely manner, can be hindered by many factors, including changes in regulatory requirements, the willingness of the agencies, aggregators, or other investors to provide funding for and purchase mortgage loans, and general economic conditions. If Bay Equity were unable to sell its originated loans, either initially or following a repurchase, then it may need to service the loans and we would be exposed to adverse market conditions affecting mortgage loans. For example, we may be required to write down the value of the loan, which reduces the amount of our current assets. Additionally, if Bay Equity borrowed under a warehouse credit facility for the loan, then it will be required to repay the borrowed amount, which reduces our cash on hand that is available for other corporate uses. Finally, if a homeowner were unable to make his or her mortgage payments, then we may be required to foreclose on the home securing the loan. Bay Equity may be unable to retain its subservicer on economically feasible terms to foreclose a home. Furthermore, any proceeds from selling a foreclosed home may be significantly less than the remaining amount of the loan due to Bay Equity.

The growth of Rent.'s business depends on its ability to attract property managers' advertising spending.

Rent.'s growth depends on advertising revenue generated primarily through property managers. Rent.'s ability to attract and retain advertisers may be adversely affected by any of the following factors:

•a prolonged period of high occupancy within rental properties;

•declining quantity and quality of renter leads it provides to property managers;

•its inability to keep pace with changes in technology and features expected by renters when visiting an online rental portal;

•its failure to offer an attractive return on investment to advertisers; and

•the inability of property managers to evict tenants for delinquent rent payments.

Rent. does not have long-term contracts with many of its advertisers, and these advertisers may choose to end their relationships with Rent. with little or no advance notice. As Rent.'s existing subscriptions for advertising terminate, it may not be successful in securing new subscriptions.

We may not realize the anticipated benefits from, and may incur substantial costs related to, our acquisitions of Rent. and Bay Equity.

We acquired Rent. on April 2, 2021 and Bay Equity on April 1, 2022. The anticipated benefits of each acquisition may not come to fruition. Integrating Rent. and Bay Equity will be challenging and time consuming, and may subject us to additional costs that we have not anticipated in evaluating the transaction. Furthermore, GAAP requires us to test the goodwill associated with these acquisitions at least annually and we review our goodwill and intangible assets for impairment when events change indicate that an impairment may be appropriate. Depending on the results of these reviews, we may be required to record a non-cash charge to our earnings in the period we determined impairment was appropriate, which may negatively impact our results of operations in that period.

11

Cybersecurity incidents could disrupt our business or result in the loss of critical and confidential information.

Cybersecurity incidents directed at us or our third-party service providers can range from uncoordinated individual attempts to gain unauthorized access to information technology systems to sophisticated and targeted measures known as advanced persistent threats. Cybersecurity incidents are also constantly evolving, increasing the difficulty of detecting and successfully defending against them. In the ordinary course of our business, we and our third-party service providers collect and store sensitive data, including our proprietary business information and intellectual property and that of our customers and employees, including personally identifiable information. Additionally, we rely on third-parties and their security procedures for the secure storage, processing, maintenance, and transmission of information that are critical to our operations. Despite measures designed to prevent, detect, address, and mitigate cybersecurity incidents, such incidents may occur to us or our third-party providers and, depending on their nature and scope, could potentially result in the misappropriation, destruction, corruption, or unavailability of critical data and confidential or proprietary information (our own or that of third parties, including personally identifiable information of our customers and employees) and the disruption of business operations. Any real or perceived compromises to our security, or that of our third-party providers, could cause customers to lose trust and confidence in us and stop using our website and mobile applications. In addition, we may incur significant costs for remediation that may include liability for stolen assets or information, repair of system damage, and compensation to customers, employees, and business partners. We may also be subject to government enforcement proceedings and legal claims by private parties.

We process, transmit, and store personal information, and unauthorized access to, or the unintended release of, this information could result in a claim for damages, regulatory action, loss of business, or unfavorable publicity.

We process, transmit, and store personal information to provide services to our customers and as an employer. As a result, we are subject to certain contractual terms, as well as federal, state, and foreign laws and regulations designed to protect personal information. While we take measures to protect the security and privacy of this information, it is possible that our security controls over personal data and other practices we follow may not prevent the unauthorized access to, or the unintended release of, personal information. If such unauthorized access or unintended release occurred, we could suffer significant damage to our brand and reputation, customers could lose confidence in the security and reliability of our services, and we could incur significant costs to address and fix these security incidents. These incidents could also lead to lawsuits and regulatory investigations and enforcement actions.

We rely on third-party licensed technology, and the inability to maintain these licenses or errors in the software we license could result in increased costs or reduced service levels.

We employ certain third-party software obtained under licenses from other companies in our technology. Our reliance on this third-party software may become costly if the licensor increases the price for the license or changes the terms of use and we cannot find commercially reasonable alternatives. Even if we were to find an alternative, integration of our technology with new third-party software may require substantial investment of our time and resources.

Any undetected errors or defects in the third-party software we license could prevent the deployment or impair the functionality of our technology, delay new service offerings, or result in a failure of our website or mobile application.

We use open source software in some aspects of our technology and may fail to comply with the terms of one or more of these open source licenses.

Our technology incorporates software covered by open source licenses. The terms of various open source licenses have not been interpreted by U.S. courts, and if they were interpreted, such licenses could be construed in a manner that imposes unanticipated restrictions on our technology. If portions of our proprietary software are determined to be subject to an open source license, we could be required to publicly release the affected portions of our source code, re-engineer all or a portion of our technologies, or otherwise be limited in our use of such software, each of which could reduce or eliminate the value of our technologies.

12

Moreover, our processes for controlling our use of open source software may not be effective. If we do not comply with the terms of an open source software license, we could be required to seek licenses from third parties to continue offering our services on terms that are not economically feasible, to re-engineer our technology to remove or replace the open source software, to discontinue the use of certain technology if re-engineering could not be accomplished on a timely basis, to pay monetary damages, to make generally available the source code for our proprietary technology, or to waive certain intellectual property rights.

We may be unable to secure intellectual property protection for all of our technology and methodologies, enforce our intellectual property rights, or protect our other proprietary business information.

Our success and ability to compete depends in part on our intellectual property and our other proprietary business information. To protect our proprietary rights, we rely on trademark, copyright, and patent law, trade-secret protection, and contractual provisions and restrictions. However, we may be unable to secure intellectual property protection for all of our technology and methodologies or the steps we take to enforce our intellectual property rights may be inadequate. Furthermore, we may also be unable to protect our proprietary business information from misappropriation.

If we are unable to secure intellectual property rights, our competitors could use our intellectual property to market offerings similar to ours and we would have no recourse to enjoin or stop their actions. Additionally, any of our intellectual property rights may be challenged by others and invalidated through administrative processes or litigation. Moreover, even if we secured our intellectual property rights, others may infringe on our intellectual property and we may be unable to successfully enforce our rights against the infringers because we may be unaware of the infringement or our legal actions may not be successful. Finally, others may misappropriate our proprietary business information, and we may be unaware of the misappropriation or unable to enforce our legal rights in a cost-effective manner. If any of these events were to occur, our ability to compete effectively would be impaired.

We may be unable to maintain and scale the technology underlying our offerings.

As the number of homebuyers and home sellers, renters, agents, and listings shared on our website and mobile application and the extent and types of data grow, our need for additional network capacity and computing power will also grow. Operating our underlying technology systems is expensive and complex, and we could experience operational failures. If we experience interruptions or failures in these systems for any reason, the security and availability of our services and technologies could be affected.

We are subject to a variety of federal, state and local laws, and our compliance with these laws, or the enforcement of our rights under these laws, may increase our expenses, require management's resources, or force us to change our business practices.

We are currently subject to a variety of, and may in the future become subject to additional, federal, state, and local laws. The laws include, but are not limited to, those relating to real estate, brokerage, title, mortgage, advertising, privacy and consumer protection, labor and employment, and intellectual property. These laws and their related regulations may evolve frequently and may be inconsistent from one jurisdiction to another. Additionally, certain of these laws and regulations were created for traditional real estate brokerages, and it is unclear how they may affect us given our business model that is unlike traditional brokerages or certain of our services that historically have not been offered by traditional brokerages.

These laws can be costly for us to comply with or enforce. Additionally, if we are unable to comply with and become liable for violations of these laws, or if courts or regulatory bodies provide unfavorable interpretations of existing regulations, our operations in affected markets may become prohibitively expensive, consume significant amounts of management's time, or need to be discontinued.

13

We are subject to costs associated with defending and resolving proceedings brought by government entities and claims brought by private parties.

We are from time to time involved in, and may in the future be subject to, government investigations or enforcement actions and private third-party claims arising from the laws to which we are subject or the contracts to which we are a party. Such investigations, actions, and claims include, but are not limited to, matters relating to employment law (including misclassification), intellectual property, privacy and consumer protection, website accessibility, the Real Estate Settlement Procedures Act of 1974, the Fair Housing Act of 1968 or other fair housing statutes, cybersecurity incidents, data breaches, commercial or contractual disputes, and exposure to COVID-19. They may also relate to ordinary-course brokerage disputes, including, but not limited to, failure to disclose property defects, failure to meet client legal obligations, commission disputes, personal injury or property damage claims, and vicarious liability based upon conduct of individuals or entities outside of our control, including partner agents and third-party contractor agents. See Note 8 to our consolidated financial statements for a discussion of pending third-party claims that we believe may be material to us.

Any such investigations, actions, or claims can be costly to defend or resolve, require significant time from management, or result in negative publicity. Furthermore, to the extent we are unsuccessful in defending an action or claim, we may be subject to civil or criminal penalties, including significant fines or damages, the loss of ability to operate in a jurisdiction, or the need to change certain business practices (including redesigning, or obtaining a license for, our technology or modifying or ceasing to offer certain services).

In August 2019, Devin Cook, a former associate agent, filed a complaint against us in a California state court alleging misclassification as an independent contractor. On May 23, 2022, we settled Ms. Cook’s and a related case through global mediation for an aggregate of $3.0 million. This amount is subject to adjustment if the actual number of our agents or their workweeks differ from the number we provided to the plaintiffs. The settlement is subject to court approval. If it does not get approved or a court finds against us on classification of our associate agents, we may have to pay significant additional damages and change our business practices, which may be costly and time-consuming. Changes could require us to reclassify associate agents as employees, thereby subjecting them to wage and hour laws, and resulting in related tax and employment liabilities. Agents may also opt out of our platform given the loss of flexibility under an employment model.

The real estate market may be negatively impacted by industry changes as the result of certain class action lawsuits.

The real estate industry faces significant antitrust pressure, both from several private lawsuits and from the Department of Justice (the “DOJ”)’s related investigation. The National Association of Realtors (“NAR”) and certain companies (Realogy, HomeServices of America, RE/MAX, and Keller Williams) are defendants in class action complaints referred to as the “Moehrl-related suits” which allege violations of federal antitrust law. The DOJ also agreed to settle a suit with NAR in which NAR agreed to adopt certain rule changes, such as increased disclosure of commission offers from sellers’ agents to buyers’ agents, but the direct and indirect effects, if any, of the settlement upon the real estate industry are not yet entirely clear and the DOJ recently walked away from this settlement and reopened its investigation. Moreover, the Moehrl-related suits seek additional changes in real estate industry practices beyond the changes NAR agreed to in the DOJ settlement. Further, these lawsuits have prompted discussion of regulatory changes to rules established by local or state real estate boards or multiple listing services. Although the settlement between NAR and the DOJ does not require changes to agent and broker compensation, the resolution of the Moehrl-related suits and/or other regulatory changes may require changes to our or our brokers’ business models, including changes in agent and broker compensation. Even if commission sharing remains the norm, it may no longer be mandated in places where it is currently mandated, leading to hourly or a la carte services. If buyers end up having to compensate buyer brokers, they may be more likely to contact listing agents directly, driving dual agent broker commissions down. These potential changes in agent and broker compensation in particular could reduce the fees we receive from our agents, which, in turn, could adversely affect our financial condition and results of operations.

14

Risks Related to Our Indebtedness

We may not have sufficient cash flow to make the payments required by our convertible senior notes, and a failure to make payments when due may result in the entire principal amount of the convertible senior notes becoming due prior to the notes' maturity, which may result in our bankruptcy.

We are required to pay interest on our 2023 notes and 2027 notes on a semi-annual basis. In addition, holders of our convertible senior notes have the right to require us to repurchase their notes upon the occurrence of a fundamental change at a repurchase price equal to 100% of the principal amount of the notes to be repurchased, plus any accrued and unpaid interest. Furthermore, holders of our notes have the right to convert their notes upon any of the conditions described below:

•during any calendar quarter, if the last reported sale price of our common stock for at least 20 trading days (whether or not consecutive) during a period of 30 consecutive trading days ending on, and including, the last trading day of the immediately preceding calendar quarter is greater than or equal to 130% of the conversion price of the notes on each applicable trading day;

•during the five business day period after any five consecutive trading day period in which the trading price per $1,000 principal amount of the notes for each trading day of the measurement period was less than 98% of the product of the last reported sale price of our common stock and the conversion rate of the notes on each such trading day;

•if we call any or all of the notes for redemption, at any time prior to the close of business on the scheduled trading day prior to the redemption date; or

•upon the occurrence of specified corporate events.

If any of these conversion features under a tranche of our notes are triggered, then holders of such notes will be entitled to convert the notes at any time during specified periods at their option. Upon conversion, we will be required to make cash payments in respect of the notes being converted, unless we elect to deliver solely shares of our common stock to settle such conversion (other than paying cash in lieu of delivering any fractional share).

Our ability to make these payments depends on having sufficient cash on hand when the payments are due. Our cash availability, in turn, depends on our future performance, which is subject to the other risks described in this Item 1A. If we are unable to generate sufficient cash flow to make the payments when due, then we may be required to adopt one or more alternatives, such as selling assets, refinancing the notes, or raising additional capital. However, we may not be able to engage in any of these activities or engage in these activities on desirable terms.

Our failure to make payments when due may result in an event of default under the indentures governing our convertible senior notes and cause (i) with respect to our 2023 notes, the remaining $23.5 million aggregate principal amount, which will mature on July 15, 2023; (ii) with respect to our 2025 notes, the remaining $518.7 million aggregate principal amount, and (iii) with respect to our 2027 notes, the entire $575.0 million aggregate principal amount, plus, in each case, any accrued and unpaid interest, to become due immediately and prior to the maturity date. Any such acceleration of the principal amount could result in our bankruptcy. In a bankruptcy, the holders of our convertible senior notes would have a claim to our assets that is senior to the claims of holders of our common stock.

A substantial portion of our mortgage business’s assets are measured at fair value. If our estimates of fair value are inaccurate, we may be required to record a significant write down of our assets.

Bay Equity’s mortgage servicing rights (“MSRs”), interest rate lock commitments (“IRLCs”), and mortgage loans held for sale are recorded at fair value on our balance sheet. Fair value determinations require many assumptions and complex analyses, and we cannot control many of the underlying factors. If our estimates are incorrect, we could be required to write down the value of these assets, which could adversely affect our financial condition and results of operations.

15

In particular, our estimates of the fair value of Bay Equity’s MSRs are based on the cash flows projected to result from the servicing of the related mortgage loans and continually fluctuate due to a number of factors, including estimated discount rate, the cost of servicing, objective portfolio characteristics, contractual service fees, default rates, prepayment rates and other market conditions that affect the number of loans that ultimately become delinquent or are repaid or refinanced. These estimates are calculated by a third party using financial models that account for a high number of variables that drive cash flows associated with MSRs and anticipate changes in those variables over the life of the MSR. The accuracy of our estimates of the fair value of our MSRs are dependent on the reasonableness of the results of such models and the variables and assumptions that are built into them. If prepayment speeds or loan delinquencies are higher than anticipated, or other factors perform worse than modeled, the recorded value of certain of our MSRs may decrease, which could adversely affect our financial condition and results of operations.

Bay Equity relies on its warehouse credit facilities to fund the mortgage loans that it originates. If one or more of those facilities were to become unavailable, Bay Equity may be unable to find replacement financing on commercially reasonable terms, or at all, and this could adversely affect its ability to originate additional mortgage loans.

Bay Equity relies on borrowings from warehouse credit facilities to fund substantially all of the mortgage loans that it originates. To grow its business, Bay Equity depends, in part, on having sufficient borrowing capacity under its current facilities or obtaining additional borrowing capacity under new facilities. A current facility may become unavailable if Bay Equity fails to comply with its ongoing obligations under the facility, including failing to satisfy applicable financial covenants, or if it cannot agree with the lender on terms to renew the facility. New facilities may not be available on terms acceptable to us. If Bay Equity were unable to secure sufficient borrowing capacity through its warehouse credit facilities, then it may need to rely on our cash on hand to originate mortgage loans. If this cash were unavailable, then Bay Equity may be unable to maintain or increase the amount of mortgage loans that it originates, which will adversely affect its growth.

The cross-acceleration and cross-default provisions in the agreements governing our current indebtedness may result in an immediate obligation to repay all of either our 2025 and 2027 convertible senior notes or our warehouse credit facilities.

The indentures governing our 2025 and 2027 convertible senior notes contain cross-acceleration and cross-default provisions. These provisions could have the effect of creating an event of default under the indenture for either our 2025 or 2027 convertible senior notes, despite our compliance with that agreement, due solely to an event of default or failure to pay amounts owed under the indenture for the other tranche of convertible senior notes. Accordingly, all or a significant portion of our outstanding convertible senior notes could become immediately payable due solely to our failure to comply with the terms of a single agreement governing either our 2025 or 2027 convertible senior notes. Our warehouse credit facilities contain cross-acceleration and cross-default provisions. These provisions could have the effect of creating an event of default under the agreement for any such warehouse credit facility, despite our compliance with that agreement, due solely to an event of default or failure to pay amounts owed under the agreement for another warehouse credit facility. Accordingly, all or a significant portion of our outstanding warehouse indebtedness could become immediately payable due solely to our failure to comply with the terms of a single agreement governing one of our warehouse credit facilities. The cross-default provisions in our existing warehouse credit facilities do not pick up defaults under our convertible senior notes. Our existing warehouse credit facilities are also carved out of the cross-payment default provisions in our 2025 and 2027 senior notes given that they constitute non-recourse debt.

16

Risks Related to Our Convertible Preferred Stock

We may be required to make cash payments to our preferred stockholders before our preferred stock's final redemption date of November 30, 2024, and any cash payments may materially reduce our net working capital.

On November 30, 2024, we will be required to redeem all shares of our convertible preferred stock then outstanding and pay accrued dividends on those shares. A preferred stockholder has the option of receiving cash, shares of our common stock, or a combination of cash and shares for this redemption. However, before this redemption, we may be required to make cash payments to our preferred stockholders in the two situations described below, and any such cash payments will reduce our cash available for other corporate uses and may materially reduce our net working capital.

Dividends accrue on each $1,000 of our outstanding convertible preferred stock at a rate of 5.5% per year and are payable quarterly. Assuming we satisfy the "equity conditions" (as defined in the certificate of designation governing our preferred stock), we will pay dividends in shares of our common stock. These conditions principally include (i) we have ensured the liquidity and transferability of our common stock held by the preferred stockholders, (ii) we have issued common stock and paid cash to the preferred stockholders, as required by the certificate of designation, (iii) we are not in bankruptcy or have had a bankruptcy proceeding instituted against us, and (iv) we have not breached an agreement that governs the preferred stockholders' rights with respect to the preferred stock and such breach materially and adversely impacts our business or a preferred stockholder's economic benefits under the agreement. However, if we fail to satisfy these "equity conditions," then we must pay cash dividends in amount equal to (i) the number of shares of our common stock that we would have issued as dividends, assuming we satisfied the conditions, multiplied by (ii) the volume-weighted-average closing price of our common stock for the ten trading days preceding the date the dividends are payable.

A preferred stockholder has the right to require us to redeem its preferred stock for cash following the occurrence of a "triggering event" (as defined in the certificate of designation governing our preferred stock). These events are similar in nature to the "equity conditions" described above. The cash payment, for each share of preferred stock, would equal the sum of (i) $1,000, (ii) any accrued dividends on the preferred stock, and (iii) an amount equal to all scheduled dividend payments (excluding any accrued dividends) on the preferred stock for all remaining dividend periods from the date the preferred stockholder requests redemption through November 29, 2024.

Risks Relating to Ownership of Our Common Stock

Our restated certificate of incorporation designates the Court of Chancery of the State of Delaware and the U.S. federal district courts as the exclusive forums for certain types of actions that may be initiated by our stockholders. These provisions may limit a stockholder's ability to bring a claim in a judicial forum that it finds favorable for disputes with us or our directors, officers, or employees, which may discourage lawsuits with respect to such claims.

Our restated certificate of incorporation provides that, unless we consent in writing to an alternative forum, the Court of Chancery of the State of Delaware will be the sole and exclusive forum for (i) any derivative action or proceeding brought on our behalf, (ii) any action asserting a claim of breach of a fiduciary duty owed by any of our directors, officers, or employees to us or our stockholders, (iii) any action asserting a claim arising pursuant to any provision of the Delaware General Corporation Law, our restated certificate of incorporation, or our restated bylaws, (iv) any action to interpret, apply, enforce or determine the validity of our restated certificate of incorporation or our restated bylaws, or (iv) any action asserting a claim that is governed by the internal affairs doctrine. This exclusive forum provision does not apply to actions arising under the Securities Exchange Act of 1934, or, as described below, the Securities Act of 1933.

Our restated certificate of incorporation further provides that, unless we consent in writing to an alternative forum, the U.S. federal district courts will be the exclusive forum for any complaint asserting a cause of action arising under the Securities Act of 1933. Notwithstanding this provision, stockholders will not be deemed to have waived our compliance with the federal securities laws and the rules and regulations thereunder.

17

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

None.

Item 3. Legal Proceedings

See "Legal Proceedings" under Note 8 to our consolidated financial statements for a discussion of our material, pending legal proceedings.

Item 4. Mine Safety Disclosures

Not applicable.

18

PART II

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information, Holders of Record, and Dividends

Our common stock is listed on The Nasdaq Global Select Market under the symbol “RDFN.”

As of February 10, 2023, we had 60 holders of record of our common stock. Because many of our shares of common stock are held by brokers and other institutions on behalf of stockholders, we are unable to estimate the total number of beneficial owners of our common stock represented by these record holders.

The holders of our convertible preferred stock are entitled to dividends, which accrue daily based on a 360-day fiscal year at a rate of 5.5% per annum based on the issue price and are payable quarterly in arrears on the first business day following the end of each calendar quarter. Assuming we satisfy certain conditions, we will pay dividends in shares of common stock at a rate of the dividend payable divided by $17.95. If we do not satisfy such conditions, we will pay dividends in a cash amount equal to (1) the dividend shares otherwise issuable on the dividends multiplied by (2) the volume-weighted average closing price of our common stock for the ten trading days preceding the date the dividends are payable. Except for the foregoing, we have no intention of paying cash dividends in the foreseeable future.

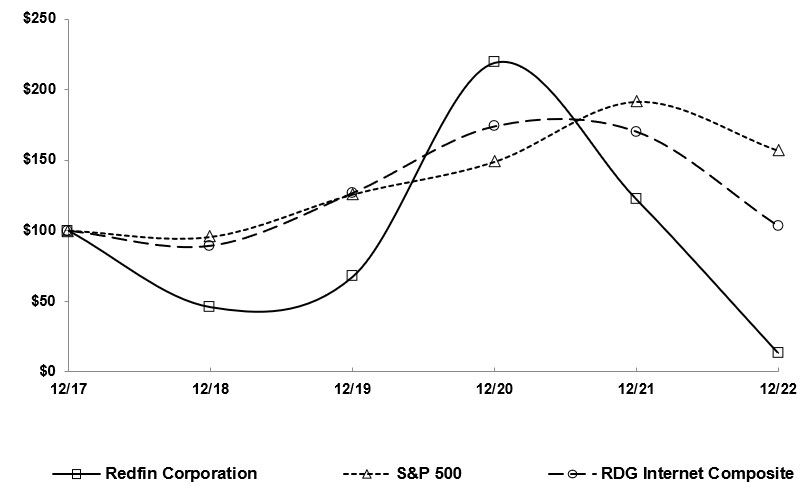

Stock Performance Graph