Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | ||

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended September 30, 2011 |

||

or |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

Commission File No. 001-35235

WESCO AIRCRAFT HOLDINGS, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware (State of Incorporation) |

20-5441563 (I.R.S. Employer Identification Number) |

27727 Avenue Scott

Valencia, California 91355

(Address of Principal Executive Offices and Zip Code)

(661) 775-7200

(Registrant's Telephone Number, Including Area Code)

Securities Registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |

|---|---|---|

| Common Stock, par value $0.001 per share | New York Stock Exchange |

Securities Registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 of Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Securities Exchange Act of 1934.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

As of March 31, 2011, there was no public trading market for the registrant's common stock.

The number of shares of common stock (par value $0.001 per share) of the registrant outstanding as of December 1, 2011 was 85,752,087.

Documents Incorporated by Reference

Part III of this annual report on Form 10-K incorporates by reference certain information from the registrants' definitive proxy statement for the 2012 annual meeting of stockholders, which the registrant intends to file pursuant to Regulation 14A with the Securities and Exchange Commission not later than 120 days after the registrant's fiscal year end of September 30, 2011. With the exception of the sections of the definitive proxy statement specifically incorporated herein by reference, the definitive proxy statement is not deemed to be filed as part of this annual report on Form 10-K.

Unless otherwise noted in this Annual Report, the term "Wesco Aircraft" means Wesco Aircraft Holdings, Inc., our top-level holding company, and the terms "Wesco," "the Company," "we," "us," "our" and "our company" mean Wesco Aircraft and its subsidiaries, including Wesco Aircraft Hardware Corp., our primary domestic operating company, and Wesco Aircraft Europe, Ltd., our primary foreign operating company. References to "fiscal year" mean the year ending or ended September 30. For example, "fiscal year 2011" or "fiscal 2011" means the period from October 1, 2010 to September 30, 2011.

1

PART I

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements. The words "believe," "expect," "anticipate," "intend," "estimate" and other expressions that are predictions of or indicate future events and trends and that do not relate to historical matters identify forward-looking statements. You should not place undue reliance on these forward-looking statements. Although forward-looking statements reflect management's good faith beliefs, reliance should not be placed on forward-looking statements because they involve known and unknown risks, uncertainties and other factors, which may cause the actual results, performance or achievements to differ materially from anticipated future results, performance or achievements expressed or implied by such forward-looking statements. Forward-looking statements speak only as of the date the statements are made. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events, changed circumstances or otherwise. These forward-looking statements are subject to numerous risks and uncertainties, including, but not limited to:

- •

- general economic and industry conditions;

- •

- changes in military spending;

- •

- risks unique to suppliers of equipment and services to the U.S. government;

- •

- risks associated with our long-term, fixed-price agreements that have no guarantee of future sales volumes;

- •

- risks associated with the loss of significant customers, a material reduction in purchase orders by significant customers

or the delay, scaling back or elimination of significant programs on which we rely;

- •

- our ability to effectively manage our inventory;

- •

- our suppliers' ability to provide us with the products we sell in a timely manner, in adequate quantities and/or at a

reasonable cost;

- •

- our ability to maintain an effective IT system;

- •

- our ability to retain key personnel;

- •

- risks associated with our international operations;

- •

- fluctuations in our financial results from period-to-period;

- •

- affiliates of The Carlyle Group's ("Carlyle") ability to control the majority of the voting power of our outstanding

common stock;

- •

- our ability to effectively compete in our industry;

- •

- risks related to our indebtedness; and

- •

- and other risks and uncertainties.

Important factors that could cause actual results to differ materially from our expectations are disclosed under Part I, Item 1A. "Risk Factors." All written and oral forward-looking statements attributable to us, or persons acting on our behalf, are expressly qualified in their entirety by the cautionary statements as well as other cautionary statements that are made from time to time in our public communications. You should evaluate all forward-looking statements made in this Annual Report on Form 10-K in the context of these risks and uncertainties.

2

Company Overview

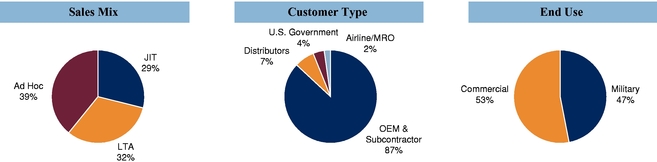

We are one of the world's largest distributors and providers of comprehensive supply chain management services to the global aerospace industry on an annual sales basis. Our services range from traditional distribution to the management of supplier relationships, quality assurance, kitting, just-in-time, or JIT, delivery and point-of-use inventory management. We supply approximately 475,000 different stock keeping units, or SKUs, including hardware, bearings, tools and more recently, electronic components and machined parts. In fiscal 2011, sales of hardware represented 82% of our net sales, with highly engineered fasteners constituting 82% of that amount. We serve our customers under three types of arrangements: JIT contracts, which govern comprehensive outsourced supply chain management services; long term agreements, or LTAs, which set prices for specific parts; and ad hoc sales. JIT contracts and LTAs, which together comprised approximately 61% of our fiscal 2011 net sales, are multi-year arrangements that provide us with significant visibility into our future sales.

Founded in 1953 by the father of our current Chief Executive Officer, or CEO, Wesco has grown to serve over 7,200 customers in the commercial, military and general aviation sectors, including the leading OEMs and their subcontractors, through which we support nearly all major Western aircraft programs. We have grown our net sales at a 13.5% compound annual growth rate, or CAGR, over the past 20 years to $710.9 million in fiscal 2011. We serve a large and growing global market, and believe that with more than 1,000 employees across 30 locations in 10 countries, we are well positioned to continue our track record of strong long-term growth and profitability. The following charts illustrate the composition of our 2011 net sales based on our sales data or management estimates.

We have invested in building an integrated, highly customized IT system that enables our purchasing and sales organization to make more informed decisions and our inventory management system to operate at maximum efficiency. Specifically, our customized IT system provides us visibility into inventory quantities, stocking locations and purchases across our customer base by individual SKU, enabling us to accurately fill approximately 8,000 orders per day and provide an exceptional level of customer service. The scalable nature of our IT system helps us improve productivity and financial performance as sales volume increases. We believe our customized IT system is a key competitive advantage and critical element in our unique business model that creates significant value for our customers and our suppliers.

We believe that our success has been driven by our focus on customer service and our ability to offer tailored solutions to our customers. We believe customers that utilize our comprehensive JIT supply chain management services are frequently able to realize significant benefits, including:

- •

- reduced inventory levels and inventory excess and obsolescence expense, in part because such customers only purchase what

they need, and make more efficient use of floor space;

- •

- increased accuracy in forecasting and planning, resulting in substantially improved on-time delivery, reduced expediting costs and fewer disruptions of production schedules;

3

- •

- improved quality assurance resulting in a substantial reduction in customer parts rejection rates; and

- •

- reduced administrative and overhead costs relating to procurement, quality assurance, supplier management, expediting and stocking functions.

Our customers also benefit from the strong relationships we maintain with a diverse group of over 1,200 suppliers. We believe these suppliers in turn derive several benefits from our scale, global reach and unique business model, including:

- •

- access to over 7,200 customer accounts;

- •

- larger production runs that facilitate more efficient manufacturing processes;

- •

- a reduction of inventory levels and related obsolescence costs;

- •

- improved performance in meeting on-time-delivery targets to end customers; and

- •

- consolidation of customer accounts, resulting in a reduction in administrative and overhead costs relating to sales and marketing, customer service and other functions.

We believe we are well positioned to continue our track record of strong growth by partnering with our suppliers to provide a compelling combination of value-added services to our customers.

Competitive Strengths

We believe that our key competitive strengths include the following:

Leader in Attractive Global Market. We are one of the world's largest distributors and providers of comprehensive supply chain management services to the global aerospace industry on an annual sales basis. We believe we offer the world's broadest inventory of aerospace parts comprised of approximately 475,000 SKUs. In addition, we fill over 8,000 orders per work day and manage approximately 400,000 stocking bins throughout our customers' facilities. We believe that the scale of our global distribution network, our value-added services and the depth, breadth and dollar investment in our inventory provide us with a significant competitive advantage in an attractive market.

Compelling Value Proposition. We offer a compelling value proposition to our customers by combining access to what we believe to be the world's broadest inventory of aerospace parts with our unique capabilities in comprehensive supply chain management. Our services can significantly improve on-time-delivery performance, enabling our customers to reduce their inventory while at the same time decreasing the frequency of production interruptions caused by part shortages. Due to the high levels of precision and engineering standards in the aerospace industry, our customers must ensure the highest levels of quality assurance. Many of our customers have chosen to outsource these critical quality assurance functions to us, relying on our rigorous inspection processes. Aerospace companies that do not outsource to a supply chain manager like Wesco can incur significant additional overhead and administrative costs relating to internal procurement, quality assurance, inventory stocking and other related personnel.

Diverse Customer and Program Base. We maintain strong relationships with over 7,200 active customers including major OEMs such as Airbus, Boeing, Bombardier, Embraer, Cessna, Gulfstream, BAE Systems, Bell Helicopter, Lockheed Martin, Northrop Grumman and Raytheon. We supply products to nearly every major Western aircraft in production, including the B-787, B-737, B-747, A-320, A330, A340, F-35 Joint Strike Fighter, or JSF, V-22, F18 and all Gulfstream production aircraft inclusive of the new G650 as well as all Bombardier aircraft, inclusive of the new C Series. During fiscal 2011, no single customer or aircraft program represented more than 16% of our net sales. We have actively worked to transition our largest customers from ad hoc purchases to multi-year LTAs or

4

comprehensive JIT supply chain management agreements, the latter two of which together represented approximately 61% of our fiscal 2011 net sales. By developing strong, long-term relationships with a diverse set of customers, we have significant visibility into our future sales.

Superior Purchasing Capabilities and Supplier Relationships. Our management is highly skilled in analyzing supply, demand, cost and pricing factors in order to make optimal inventory investment decisions, and we maintain close relationships with the leading suppliers in the industry. In particular, Alcoa Fastening Systems and Precision Castparts supplied approximately 22% and 20%, respectively, of the products we purchased during fiscal 2011. Our top 10 suppliers have been doing business with us for an average of more than 10 years. We believe that our business model allows our suppliers to smooth out production, improve their cash flow and reduce administrative costs. As a result of our scale and the strength of our relationships, many of our suppliers offer us attractive volume-based price discounts. Our success in making optimal inventory purchasing decisions is driven by our management's deep understanding of our industry and their skill in analyzing fundamental supply, demand, cost and pricing data. These decisions are facilitated by our highly customized IT system. Our superior inventory purchasing capabilities and the strength of our supplier relationships have contributed substantially to what we believe are our industry-leading operating margins.

Experienced Management Team with Significant Equity Ownership. Our management team has extensive industry experience and company tenure. Our Chief Executive Officer and other executive officers have an average of more than 20 years of experience with us and more than 30 years in our industry. In addition, our executive officers owned approximately 12.3% of the common stock of the Company as of September 30, 2011. We believe that this significant equity ownership aligns the interests of our executive officers with our stockholders.

Our Strategy for Continued Growth

We intend to pursue the following strategies in order to continue to grow our business:

Continued Focus on Operational Excellence. We have built strong relationships with our existing customers and suppliers through a relentless focus on operational excellence and improvement. We intend to continue providing our customers with best-in-class on-time delivery performance and quality assurance. We also intend to continue investing in our integrated, highly customized IT system and process automation technology. We believe that by focusing on operational excellence, we will be able to maintain high customer satisfaction and industry-leading operating margins.

Win New Business from Existing Customers. We will continue our strategy of expanding our relationships with existing customers by transitioning them to our comprehensive JIT supply chain management services as well as expanding our programs to include additional customer sites and SKUs. We are a key partner supplying fasteners and other C class parts to support the launch of new aircraft programs, such as the Boeing 787 and Lockheed Martin JSF. We will continue to support our customers in the launch of new aircraft programs by introducing new supply chain solutions that minimize costs, improve productivity, lower inventory investment and ensure a seamless supply of parts for new production and aftermarket support.

Expand Customer Base. We believe that our services and capabilities are attractive to potential new customers and plan to expand our customer base. We have had significant success in winning business when competing distributors have been unable to meet customer service level requirements and in situations where customers have outsourced work that was previously performed internally. Historically, we have focused our activities on the major OEMs and their subcontractors and less on airlines and airline maintenance organizations due to their tendency to order parts in smaller quantities with greater frequency, which makes them more costly to serve.

5

Further Expand into International Markets. We have recently established a presence in international locations such as China, India and Saudi Arabia, and we intend to expand into other high growth regions such as Mexico to support new and existing customers. Our international expansion efforts will enable us to better reach new customers and more effectively serve our existing customer base as the manufacture of aircraft and aircraft structures continues to become more global. We believe that we mitigate many of the risks associated with international expansion by entering into customer contracts before we establish a new stocking facility. Our international expansion will enable us to better reach new customers and more effectively serve our existing customer base as the manufacture of aircraft and aircraft structures becomes increasingly international and interconnected.

Selectively Pursue Strategic Acquisitions. Our industry is highly fragmented and we believe that there are opportunities for continued consolidation. In 2008, we acquired Airtechnics, Inc., or Airtechnics, which enabled us to expand our product offering to include electronic components, as well as gain additional customers. We believe that we are well positioned to expand our product offering and geographical footprint through strategic acquisitions. Consistent with this strategy, we continue to evaluate potential acquisition opportunities.

Our Products and Services

Our Products

We offer more than 475,000 different SKUs, consisting of C class aerospace hardware, bearings, electronic components and machined parts, which are generally priced below $350 per part. Many of the products we sell are highly engineered, precision parts that are specified for use in particular aircraft programs.

Our product categories include the following:

| |

Hardware | Electronic Components |

Bearings | Machined Parts and Other |

||||

|---|---|---|---|---|---|---|---|---|

Wesco Fiscal 2011 Net Product Sales (in millions) |

$585 | $82 | $22 | $22 | ||||

% of Wesco Fiscal 2011 Net Product Sales |

82% | 12% | 3% | 3% | ||||

Types of Products Offered |

• Blind fasteners |

• Connectors |

• Airframe control bearings |

• Brackets |

||||

|

• Panel fasteners |

• Relays |

• Rod ends |

• Milled parts |

||||

|

• Bolts and screws |

• Switches |

• Spherical bearings |

• Shims |

||||

|

• Clamps |

• Circuit breakers |

• Ball bearing rod ends |

• Stampings |

||||

|

• Hi lok pins and collars |

• Lighted products |

• Roller bearings |

• Turned parts |

||||

|

• Hose assemblies |

• Bushings |

• Welded assemblies |

|||||

|

• Hydraulic fittings |

• Installation tooling |

||||||

|

• Inserts |

|||||||

|

• Lockbolts and collars |

|||||||

|

• Nuts |

|||||||

|

• Rivets |

|||||||

|

• Springs |

|||||||

|

• Valves |

|||||||

|

• Washers |

Hardware

Sales of C class aerospace hardware represented approximately 82% of our fiscal 2011 product sales. Fasteners are our largest product category, comprising approximately 82% of our hardware sales in fiscal 2011. Fasteners include a wide range of highly engineered aerospace parts that are designed to hold together two or more components, such as rivets (both blind and solid), bolts (including blind

6

bolts), screws, nuts and washers. Many of these fasteners are designed for use in specific aircraft platforms and others can be used across multiple platforms. Materials used in the manufacture of these fasteners range from standard alloys, such as aluminum, steel or stainless steel, to more advanced materials, such as titanium, Inconel and Waspalloy.

Electronic Components

In 2008, we acquired Wichita, Kansas-based Airtechnics, one of the largest distributors of aerospace electronic components in North America, which helped expand our product offering to our customer base. We offer highly reliable interconnect and electro-mechanical products, including connectors, relays, switches, circuit breakers and lighted products. We also offer value-added assembled products including mil-circular and rack and panel connectors and illuminated push button switches. We maintain large quantities of connector components in inventory, which allows us to respond quickly to customer orders. In addition, our lighted switch assembly operation affords customers same day service, including engraving capabilities in multiple languages.

Bearings

We began to offer aerospace bearings after acquiring the bearing distribution business of Kaman Industrial Technologies in 1999, which enabled us to support new customers and expand our product offering. Our product offering includes a variety of standard anti-friction products designed to both commercial and military aircraft specifications, such as airframe control bearings, rod ends, spherical bearings, ball bearing rod ends, roller bearings and bushings.

Machined Parts and Other

Machined parts are designed for a specific customer and are assigned unique OEM-specific SKUs. The machined parts we distribute include laser cut or stamped brackets, milled parts, shims, stampings, turned parts and welded assemblies made of materials ranging from high-grade steel or titanium to nickel based alloys.

We stock a full range of tools needed for the installation of our products, including air and hydraulic tools as well as drill motors, and we also offer factory authorized maintenance and repair services for these tools. In addition to selling these tools, we also rent or lease these tools to our customers.

Our Services

In addition to our traditional distribution services, we have developed innovative value-added services, such as quality assurance, kitting and JIT supply chain management for our customers.

Quality Assurance

Our quality assurance, or QA, function is a key component of our service offering, with approximately 10% of our employees dedicated to this area. We believe we offer an industry-leading QA function as a result of our rigorous processes, sophisticated testing equipment and dedicated QA staff, and as evidenced by a comparison of our customers' aggregate rejection rate of the products we deliver, which was approximately 0.3% during fiscal 2011, to our rejection rate of the products we receive from our suppliers, which was approximately 2.1% during fiscal 2011.

7

Our QA department inspects the inventory we purchase to ensure the accuracy and completeness of documentation. We also maintain an electronic copy of the relevant certifications for the inventory, which can include a manufacturer certificate of conformance, test reports, process certifications, material distributor certifications and raw material mill certifications. In addition, dimensional inspections are performed on all lots from suppliers that are not certified by our QA department, and all lots for our JIT customers undergo dimensional, and in some cases, structural inspections. For many of our customers, these inspections are conducted at our in-house laboratory, where we operate sophisticated testing equipment. Our industry-leading QA capabilities also allow our JIT customers to reduce the number of personnel dedicated to the QA function and reduce the delays caused by the rejection of improperly inspected parts.

Kitting

Kitting involves the packaging of an entire bill of materials or a complete "ship-set" of parts, which reduces the amount of time workers spend retrieving parts from storage locations. Kits can be customized in varying configurations and sizes and can contain up to several hundred different parts. All of our kits and components contain fully certified and traceable parts and are assembled by our full-service kitting department at our central stocking locations, or CSLs, or at our customer sites.

JIT Supply Chain Management

JIT supply chain management involves the delivery of parts on an as-needed basis to the point-of-use at a customer's manufacturing line. JIT programs are designed to prevent excess inventory build-up and shortages and improve manufacturing efficiency. Each JIT contract requires us to maintain an efficient inventory tracking, analysis and replenishment program and is designed to provide high levels of stock availability and on-time delivery. We began offering JIT supply chain management services in 1993 as some OEMs began outsourcing certain support functions in an effort to cut costs at a time when defense spending was declining and the commercial aerospace industry was entering a cyclical downturn. Since that time, the popularity of our JIT programs has grown and we now support over 150 customer locations, including approximately 400,000 bins serviced worldwide. During fiscal 2011, our on-time delivery rate for JIT customers was approximately 98.5%. We believe customers that utilize our comprehensive JIT supply chain management services are frequently able to realize significant benefits including:

- •

- reduced inventory levels and lower inventory excess and obsolescence expense, in part because such customers only purchase

what they need, and make more efficient use of their floor space;

- •

- increased accuracy in forecasting and planning, resulting in substantially improved on-time delivery, reduced

expediting costs and fewer disruptions of production schedules;

- •

- improved quality assurance resulting in a substantial reduction in customer parts rejection rates; and

- •

- reduced administrative and overhead costs relating to procurement, QA, supplier management and stocking functions.

Before signing a JIT contract, our customers typically experience outages of many SKUs and, in some cases, have up to a year's worth of inventory on hand. As part of our JIT programs, we generally assume the customer's existing inventory at the onset of the contract, immediately reducing their inventory on-hand and the associated management costs. Customer inventory is generally assumed on a consignment basis and is entered in our database in a distinct customer-specific "virtual warehouse." Software protocol in our IT system requires the system to first "look" to a customer's consigned inventory when parts replenishment is required. In many cases, we can sell this consigned inventory to our base of 7,200 active customers around the world, gradually drawing down the customer's inventory.

8

As the consigned inventory for each SKU is exhausted, our stock of Wesco-sourced product is then used for replenishment. Due to the reliable nature of our services, our customers typically carry approximately 45 days worth of inventory in point-of-use bins instead of months or years worth of such products which is typical for many aerospace manufacturers.

Another key strength of our JIT program is our ability to utilize highly scalable and customizable point-of-use systems to develop an efficient supply chain management system and automated replenishment solution for any number of SKUs. In order to minimize inventory on hand, certain indicators are used to trigger the replenishment of product from a supplying location to the location of consumption. Our "Twin-Bin" system is an example of such an indicator. A JIT program designed around a Twin-Bin system utilizes a specially manufactured unit composed of two bins stacked on top of one another. In this system, a clear plastic bag, typically containing a 30-day supply of parts, is loaded in each bin. Production workers use all of the parts within the bottom bin before drawing a pullout slide between the two bins that drops the full plastic bag of parts from the top bin into the bottom bin. An empty top bin indicates the need to initiate replenishment of the parts and provides a clear visual management process on the manufacturing floor. All replenishment activity is done via hand-held scanners that transmit orders to our stocking locations.

Customer Contracts

We sell parts to our customers under three types of arrangements: JIT supply chain management contracts, LTAs and ad hoc sales.

JIT Contracts

JIT contracts are typically three to five years in length and are structured to supply the parts requirement for specific SKUs, production lines or facilities. Given our direct involvement with JIT customers, volume requirements and purchasing frequency under these contracts is highly predictable. Under JIT contracts, customers commit to purchase specified parts from us at a fixed price, on an if-and-when needed basis, and we are responsible for maintaining high levels of stock availability of those parts. JIT contracts typically contain termination for convenience provisions, which generally allow our customers to terminate their contracts on short notice without meaningful penalties, provided that we are reimbursed for the cost of any inventory specifically procured for the customer. JIT customers also often purchase parts from us that are not covered under their contracts on an ad hoc basis. Approximately 29% of our net sales during fiscal 2011 were generated from JIT contracts.

Long-Term Agreements

Like JIT contracts, LTAs also typically run for three to five years. LTAs are essentially negotiated price lists for customers or individual customer sites that cover a range of pre-determined parts, purchased on an as-needed basis. The negotiated prices are typically tiered based on order size. LTAs generally obligate the customer to buy contracted SKUs from us and may obligate us to maintain stock availability for those parts. Once an LTA is in place, the customer is then able to place individual purchase orders with us for any of the contractually specified parts. LTAs typically contain termination for convenience provisions, which generally allow for our customers to terminate their contracts on short notice without meaningful penalties, provided that we are reimbursed for the cost of any inventory specifically procured for the customer. LTA customers also frequently purchase parts from us that are not captured under the pricing arrangement on an ad hoc basis. Approximately 32% of our net sales during fiscal 2011 were derived from our LTAs.

9

Ad Hoc Sales

Ad hoc customers purchase parts from us on an as-needed basis and are generally supplied out of our existing inventory. Typically, ad hoc orders are for smaller quantities of parts than those ordered under either JIT contracts or LTAs, and are often urgent in nature. Given our breadth and volume of inventory, it is not uncommon for even our competitors to purchase parts from us on an ad hoc basis when their own stocks prove to be inadequate. In an environment of increasing aircraft production, parts shortages can become increasingly common for OEMs, subcontractors, MROs and distributors with less sophisticated forecasting abilities and procurement organizations. Approximately 39% of our net sales during fiscal 2011 were generated from ad hoc sales.

Under each of the sales arrangements described above we typically warrant that the products we sell conform to the drawings and specifications that are in effect at the time of delivery in the applicable contract, and that we will replace defective or non-conforming products for a period of time that varies from contract to contract. The product manufacturer, in turn, typically indemnifies us for liabilities resulting from defective or non-conforming products. We do not accrue for warranty expenses as our claims related to defective and non-conforming products have been nominal.

We believe that backlog is not a relevant measure of our business, given the long-term nature of our JIT contracts and LTAs with our customers.

Customers

We sell to over 7,200 active customers worldwide. Boeing was our largest customer during fiscal 2011 and accounted for approximately 16% of our net sales. No other customer accounted for more than 10% of our net sales during fiscal 2011, and only two customers accounted for over 5% of our net sales during the same period, with each consisting of multiple independent programs. Our top 10 customers collectively accounted for 49% of our net sales during fiscal 2011.

Approximately 87% of our fiscal 2011 net sales were derived from major OEMs, such as Airbus, Boeing, Bombardier, Embraer, Cessna, Gulfstream, BAE Systems, Bell Helicopter, Lockheed Martin, Northrop Grumman and Raytheon, and certain of their subcontractors. Government sales comprised roughly 4% of our net sales during fiscal 2011 and were derived from various military parts procurement agencies such as the U.S. Defense Logistics Agency, or from defense contractors buying on their behalf. Aftermarket sales to airline-affiliated or independent MROs made up roughly 2% of our fiscal 2011 net sales. Airlines and airline maintenance organizations traditionally order parts in smaller quantities with greater frequency, making them more costly to serve. We are currently targeting international airlines and aircraft maintenance centers that are assuming an expanded role within the MRO market. The balance of our net sales are to other distributors.

We estimate that during fiscal 2011, approximately 53% of our net sales were derived from customers supporting commercial programs and approximately 47% of our net sales were derived from customers supporting military programs. Our customers are principally located in the United States, comprising approximately 70% of our net sales during fiscal 2011. We also service international customers in markets that include Canada, the United Kingdom, Italy, France, Germany, China, South Korea, India and Australia.

Suppliers

We source our inventory from over 1,200 suppliers, including Alcoa Fastening Systems, Precision Castparts, Amphenol Corporation, Lisi Aerospace and Monogram Aerospace Fasteners. During fiscal 2011, we purchased approximately 42% of our inventory from Alcoa Fastening Systems and Precision Castparts. Suppliers typically prefer to deal with a relatively small number of large and sophisticated distributors in order to improve machine utilization, reduce finished goods inventory and maintain

10

pricing discipline. As a result of the scale of our operations and our long-standing relationships with many of our suppliers, we are often able to take advantage of significant volume-based discounts when purchasing inventory. Given our industry position, financial strength and philosophy of cooperation with suppliers, we believe we are in an excellent position to become a distributor for new product lines as they become available.

Procurement

We consider our procurement expertise to be one of our principal competitive advantages. Our management is highly skilled in analyzing supply, demand, cost and pricing factors to make optimal inventory investment decisions and we maintain close relationships with the leading suppliers in the industry. In particular, Alcoa Fastening Systems and Precision Castparts supplied approximately 22% and 20%, respectively, of the products we purchased during fiscal 2011. Our strong understanding of the global aerospace industry is derived from our long-term relationships with major OEMs, subcontractors and suppliers. In addition, our direct insight into our customers' production rates often allows us to detect industry trends. Furthermore, our ability to forecast demand and place purchase orders with our suppliers well in advance of our customer requirements provides us with a distinct advantage in an industry where inventory availability is critical for customers that need specific parts within a stipulated timeframe to meet their own production and delivery commitments.

We have created a structured procurement process that focuses on return on invested capital, or ROIC, and minimizes excess inventory, which helps us maintain what we believe are our industry-leading operating margins and parts availability. Prior to placing a purchase order, members of our supply chain organization analyze a "buy requisition," which is generated by our IT system. Buy requisitions provide several key pieces of information, including the amount of that SKU currently on-hand, a listing of all active customers that use the specific SKU, the quantities and rates at which the part has been consumed by these customers in the past, tiered pricing for various quantities at which the supplier offers price breaks and recent selling prices of various order sizes. Using the information obtained from the buy requisition, a Wesco employee then conducts an ROIC analysis to determine the expected payback period and margin on the specified inventory investment before making the final procurement decision. This calculated approach to inventory investment, combined with our unique market insight, has enabled us to generate and sustain industry-leading operating margins.

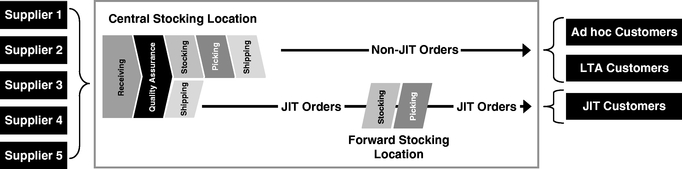

Operations

We have developed a highly structured system in order to manage the receipt, processing and shipment of inventory. This system is based on an efficient warehouse layout, automated machinery, our customized IT system and hand-held scanners. The typical process that each lot of inventory undergoes is outlined below.

11

CSLs and FSLs

Our warehouse operations are divided between Central Stocking Locations, or CSLs, and Forward Stocking Locations, or FSLs. Our primary CSL is located at our global headquarters in Valencia, California. We also operate a CSL in Wichita, Kansas, which primarily serves our global Electronics Products Group or EPG business, and a CSL in Clayton West, U.K., which primarily serves Europe, India and the Middle East. Our CSLs serve as the primary supply warehouses for most of our net sales and also house our procurement, customer service, document control, IT, material support and quality assurance functions. Our CSLs are supported by sales offices throughout the U.S., Canada, United Kingdom, Germany, France, Italy and China.

Complementing our CSLs and sales offices are FSLs. An FSL is a specialized stocking point for one or more JIT contracts located within a geographic region. FSLs are typically located either near or within a customer facility and are established to support large contracts. In certain instances, FSLs initially established to service a single customer are expanded to service other regional customers.

Receiving

All inventory enters our warehouses through a common receiving area. When shipments are received, each package is opened and the documentation is examined. If the documentation is missing or deficient, the shipment is either returned to the supplier or set aside in a designated holding area until accurate documentation is received. If the documentation is acceptable, a Wesco employee inputs the relevant information into our inventory management system, including the SKU, lot number, receipt date, quantity and unit cost.

Quality Assurance

After a shipment has gone through receiving, it is then processed by our QA department. This department inspects the inventory we purchase to ensure the accuracy and completeness of documentation. We also maintain an electronic copy of the relevant certifications for the inventory, which can include a manufacturer certificate of conformance, test reports, process certifications, material distributor certifications and raw material mill certifications. In addition, dimensional inspections are performed on all lots from suppliers that are not certified by our QA department, and all lots for our JIT customers undergo dimensional, and in some cases, structural inspections. For many of our customers, these inspections are conducted at our in-house laboratory, where we operate sophisticated testing equipment.

Stocking

Inventory that passes the quality assurance inspection is placed on a conveyor to a staging area, where warehouse employees assign stocking locations to the parts. Upon arrival at the designated stocking location, an employee scans the bar code affixed to the lot of inventory and the bar code corresponding to the specific shelf location where the lot is to be placed. This stocking information is then transmitted wirelessly to our inventory management system.

Picking

When we receive a purchase order from a customer, notification is sent to the warehouse, where an employee uses a picker truck to retrieve the required part from its stocking location. Each picker truck is equipped with scales used to count the requested number of parts. Each different part type is then placed in a clear plastic bag and sealed. Labels are then generated using hand-held equipment and placed on the bags, and any required documentation is printed and placed along with the bags into color coded crates (crates are color coded based on order urgency so warehouse staff can effectively prioritize shipping requirements). The crates then travel on a conveyer system to the shipping area.

12

Shipping

Upon arriving in the shipping area, parts bags and related documentation are placed into boxes and sealed. The shipping clerk enters the order into a third-party shipping system, generating a label based on the shipping requirements for that customer (e.g., FedEx, UPS, DHL, etc.). Once processed, the system uploads tracking numbers and freight costs, if applicable, and can send an automatic notification to a customer that their order has shipped, or automatically send documentation via e-mail to a freight forwarder to prepare shipments for export. A variety of shipping options are available (same day, overnight, etc.) depending on customer requirements. The picking and shipping processes are organized such that, if necessary, we are able to ship product on the same day a purchase order is received in order to satisfy urgent customer requirements.

Information Technology System

Our scalable IT infrastructure is based on IBM servers and the Oracle JD Edwards EnterpriseOne, or JDE, ERP system. Our IT system provides a powerful, highly distributed computing environment that enables us to quickly scale on demand as business dictates. We also employ virtualization technology to increase system availability, reduce hardware and maintenance costs and respond efficiently to market dynamics. Our entire data services infrastructure runs 24/7 and is protected by network security technologies, an uninterrupted power supply and a backup diesel generator. Remote access to our systems is provided via separate, high speed connections. Our IT infrastructure supports our business critical applications, such as JDE, TRA/X Shipping, AIMS Warehouse Management, or AIMS, and Electronic Data Interchange, or EDI.

At the core of our IT system is our JDE ERP system. JDE covers the full lifecycle of our distribution process, including procurement, planning, supply chain management, sales and accounting. JDE is fully capable of interfacing with external business systems and we have developed additional functionality within JDE for JIT delivery and direct line feed of the products we sell. This functionality includes recognition of signals and actions to fill customer bins from hand-held scanners, min/max data or proprietary signals from a customer's ERP system. JDE also supports our EDI functionality, which allows our system to interface with customers and suppliers, regardless of technology, data format or connectivity.

For our shipping logistics and export compliance support, we employ Precision Software's TRA/X. TRA/X enables us to ship globally while maintaining tracking numbers and rating information for each customer shipment. In addition, at several of our distribution facilities, we use Minerva's AIMS inventory management system in order to provide the best possible warehouse flow and cycle times. AIMS is tailored to fit our global warehouse operational needs and allows us to provide an expandable warehouse management system that can also incorporate transaction processing, work-in-progress and other manufacturing operations. AIMS interfaces with a broad range of material handling equipment, including horizontal and vertical carousels, conveyors, sorting equipment, pick systems and cranes.

Competition

The industry in which we operate is highly competitive and fragmented. We believe the principal competitive factors in our industry include the ability to provide superior customer service and support, on-time delivery, sufficient inventory availability, competitive pricing and an effective quality assurance program. Our competitors include both U.S. and foreign companies, including divisions of larger companies, some of which have significantly greater financial resources than we do, and therefore may be able to adapt more quickly to changes in customer requirements than we can. In addition to facing competition for JIT customers from our primary competitors, JIT customers or potential JIT customers may also determine that it is more cost effective to establish or re-establish an in-house supply chain

13

management system. Under these circumstances, we may be unable to sufficiently reduce our costs in order to provide competitive pricing while also maintaining acceptable operating margins.

Sales and Marketing

As of September 30, 2011, we employed 242 sales personnel with an average of over 8 years of experience at Wesco. Our sales professionals as of that date were located in the following regions: 180 in the U.S., 46 in Europe, 13 in Canada and 3 in Asia. Our marketing efforts are continuing to expand into emerging markets, including a recent office opening in India. We believe that maintaining both inside and outside sales representatives who are extremely facile in the technical details of the products we sell provides a substantial competitive advantage over our smaller competitors. As of September 30, 2011, we had 221 inside sales representatives who provide access to our entire inventory, as well as technical expertise on the products we sell. In addition, as of September 30, 2011, we also had 21 outside sales representatives, or OSRs, worldwide who provide support at certain of our customer sites. The support provided by these OSRs includes making recommendations for the products best suited for specific applications, providing technical assistance with drilling and the installation of fasteners and troubleshooting issues relating to installation tooling. Our OSRs' hands-on expertise and access to the customer site allows them a unique opportunity to market additional products to our customers.

Employees

As of September 30, 2011, we employed 1,014 personnel worldwide, 122 of which were located at customer sites. We have 245 employees located outside of North America. We are not a party to any collective bargaining agreements with our employees.

Regulatory Matters

Governmental agencies throughout the world, including the U.S. Federal Aviation Administration, or the FAA, prescribe standards for aircraft components, including virtually all commercial airline and general aviation products, as well as regulations regarding the repair and overhaul of airframes and engines. Specific regulations vary from country to country, although compliance with FAA requirements generally satisfies regulatory requirements in other countries. In addition, the products we distribute must also be certified by aircraft and engine OEMs. If any of the material authorizations or approvals that allow us to supply products is revoked or suspended, then the sale of the related products would be prohibited by law, which would have an adverse effect on our business, financial condition and results of operations.

From time to time, the FAA or equivalent regulatory agencies in other countries propose new regulations or changes to existing regulations, which are usually more stringent than existing regulations. If these proposed regulations are adopted and enacted, we could incur significant additional costs to achieve compliance, which could have a material adverse effect on our business, financial condition and results of operations.

We are also subject to government rules and regulations that include the FCPA, ITAR and the False Claims Act. See "Risk Factors—We are subject to unique business risks as a result of supplying equipment and services to the U.S. Government" and "—Our international operations require us to comply with anti-corruption laws and regulations of the U.S. government and various international jurisdictions."

Environmental Matters

Although we are subject to various environmental regulations, we are not aware of any environmental issues that would be likely to have a materially adverse impact upon our business or financial condition.

14

Available Information

We file annual, quarterly and current reports and other information with the SEC. You may read and copy any documents that we file at the SEC's public reference room at 100 F Street, N.E., Washington, D.C. 20549. You may call the SEC at 1-800-SEC-0330 to obtain further information about the public reference room. In addition, the SEC maintains an Internet website (www.sec.gov) that contains reports, proxy and information statements and other information regarding registrants that file electronically with the SEC, including us. You may also access, free of charge, our reports filed with the SEC (for example, our Annual Report on Form 10-K, our Quarterly Reports on Form 10-Q and our Current Reports on Form 8-K and any amendments to those forms) through the "Investor Relations" portion of our Internet website (www.wescoair.com). Reports filed with or furnished to the SEC will be available as soon as reasonably practicable after they are filed with or furnished to the SEC. Our website is included in this Annual Report as an inactive textual reference only. The information found on our website is not part of this or any other report filed with or furnished to the SEC.

15

You should consider and read carefully all of the risks and uncertainties described below, as well as other information included in this Annual Report, including our consolidated financial statements and related notes. The risks described below are not the only ones facing us. The occurrence of any of the following risks or additional risks and uncertainties not presently known to us or that we currently believe to be immaterial could materially and adversely affect our business, financial condition, or results of operations. This Annual Report also contains forward-looking statements and estimates that involve risks and uncertainties. Our actual results could differ materially from those anticipated in the forward-looking statements as a result of specific factors, including the risks and uncertainties described below.

Risks Related to Our Business and Industry

We are directly dependent upon the condition of the aerospace industry, which is closely tied to global economic conditions, and if the volatility in the global financial markets were to result in a slowdown in the current economic recovery or a return to a recession, our business, financial condition and results of operations could be negatively impacted.

Demand for the products and services we offer is directly tied to the delivery of new aircraft and aircraft utilization, which, in turn, is impacted by global economic conditions. Although the economy has exhibited signs of recovery, global financial markets have experienced extreme volatility and disruption for nearly three years, which, at times, reached unprecedented levels as a result of the financial crisis affecting the banking system and participants in the global financial markets. Concerns over the tightening of the corporate credit markets, sovereign debt, inflation, energy costs and the dislocation of the real estate and mortgage markets have contributed to the volatility in the global financial markets and, together with the global financial crisis, have created uncertainties for global economic conditions in the future. The aerospace industry is particularly sensitive to changes in economic conditions. In 2009, revenue passenger miles, or RPMs, on commercial aircraft declined due to the global recession. During the same period, the industry experienced declines in large commercial, regional jet and business jet deliveries. While demand for commercial jets has recovered somewhat, both regional and business jet orders and deliveries have recovered more slowly. A slowdown in the current economic recovery or a return to a recession would negatively impact the aerospace industry, and could negatively impact our business, financial condition and results of operations.

Military spending, including spending on the products we sell, is dependent upon national defense budgets, and a reduction in military spending could have a material adverse effect on our business, financial condition and results of operations.

During the year ended September 30, 2011, approximately 47% of our net sales were related to military aircraft. The military market is significantly dependent upon government budget trends, particularly the U.S. Department of Defense, or DoD, budget. Future DoD budgets could be negatively impacted by several factors, including, but not limited to, a change in defense spending policy by the current and future presidential administrations and Congress, the U.S. Government's budget deficits, spending priorities, the cost of sustaining the U.S. military presence in overseas operations and possible political pressure to reduce U.S. Government military spending, each of which could cause the DoD budget to decline. A decline in U.S. military expenditures could result in a reduction in military aircraft production, which could have a material adverse effect on our business, financial condition and results of operations.

In particular, military spending may be negatively impacted by the Budget Control Act of 2011 (the "Budget Act"), which was passed in August 2011. The Budget Act calls for a $917.0 billion reduction in discretionary spending over the next decade, and also created a joint committee of Congress (the "Super Committee") that was responsible for identifying up to an additional $1.5 trillion

16

in deficit reductions by November 23, 2011. The Super Committee failed to reach an agreement by the November 23, 2011 deadline, and accordingly, $1.2 trillion in automatic spending cuts split between defense and non-defense programs are currently scheduled to be triggered beginning in 2013. We are unable to predict the impact such cuts, if enacted, would have on funding for the military programs which we support. However, such cuts could result in reductions, delays or cancellations of these programs, which could have a material adverse effect on our business, financial condition and results of operations.

We are subject to unique business risks as a result of supplying equipment and services to the U.S. Government directly and as a subcontractor, which could lead to a reduction in our net sales from, or the profitability of our supply arrangements with, the U.S. Government.

Companies engaged in supplying defense-related equipment and services to U.S. Government agencies are subject to business risks specific to the defense industry. We contract directly with the U.S. Government and as a subcontractor to customers contracting with the U.S. Government. These risks include the ability of the U.S. Government to unilaterally suspend us from receiving new contracts pending resolution of alleged violations of procurement laws or regulations, reduce the value of existing contracts and audit our contract-related costs and fees. In addition, most of our U.S. Government contracts and subcontracts can be terminated by the U.S. Government or the contracting party, as applicable, at its convenience. Termination for convenience provisions provide only for our recovery of costs incurred or committed, settlement expenses and profit on the work completed prior to termination.

In addition, the U.S. Government may seek to review our costs to determine whether our pricing is "fair and reasonable." Such a review could be costly and time consuming for our management and could distract from our ability to effectively manage the business. As a result of such a review, we could be required to provide a refund to the U.S. Government or we could be asked to enter into an arrangement whereby our prices would be based on cost or the DoD could seek to pursue alternative sources of supply for our parts. Any of those occurrences could lead to a reduction in our net sales from, or the profitability of certain of our supply arrangements with, certain agencies and buying organizations of the U.S. Government.

We are also subject to the federal False Claims Act, which provides for substantial civil penalties and treble damages where a contractor presents a false or fraudulent claim to the government for payment. Actions under the False Claims Act may be brought by the government or by other persons on behalf of the government (who may then share in any recovery).

We do not have guaranteed future sales of the products we sell and when we enter into JIT contracts and LTAs with our customers we generally take the risk of cost overruns, and our business, financial condition, results of operations and operating margins may be negatively affected if we purchase more products than our customers require, product costs increase unexpectedly, we experience high start up costs on new contracts or our contracts are terminated.

Our JIT contracts and LTAs are long-term, fixed-price agreements with no guarantee of future sales volumes, and they may be terminated for convenience on short notice by our customers, often without meaningful penalties, provided that we are reimbursed for the cost of any inventory specifically procured for the customer. In addition, we purchase inventory based on our forecasts of anticipated future customer demand. As a result, we may take the risk of having excess inventory in the event that our customers do not place orders consistent with our forecasts. We also run the risk of not being able to pass along or otherwise recover unexpected increases in our product costs, including as a result of commodity price increases, which may increase above our established prices at the time we entered into the customer contract and established prices for parts we provide. We were recently awarded a major new JIT contract. When we are awarded new contracts, particularly JIT contracts, we may incur high

17

costs, including salary and overtime costs to hire and train on-site personnel, in the start up phase of our performance. In the event that we purchase more products than our customers require, product costs increase unexpectedly, we experience high start up costs on new contracts or our contracts are terminated, our business, financial condition, results of operations and operating margins could be negatively affected.

If we lose significant customers, significant customers materially reduce their purchase orders or significant programs on which we rely are delayed, scaled back or eliminated, our business, financial condition and results of operations may be adversely affected.

Our top ten customers for the year ended September 30, 2011 accounted for approximately 49% of our net sales. Boeing was our largest customer during fiscal 2011, accounting for approximately 16% of our net sales through purchases by its various divisions and subsidiaries. A reduction in purchasing by or loss of one of our larger customers for any reason, such as changes in manufacturing practices, loss of a customer as a result of the acquisition of such customer by a purchaser who does not fully utilize a distribution model or uses a competitor, in-sourcing by customers, a transfer of business to a competitor, an economic downturn, failure to adequately service our clients, decreased production or a strike, could have a material adverse effect on our business, financial condition and results of operations.

As an example of changes in manufacturing practices that could impact us, OEMs such as Boeing and Airbus are currently incorporating an increasing amount of composite materials in the aircraft they manufacture. Aircraft utilizing composite materials generally require the use of significantly fewer C class aerospace parts than new aircraft made of more traditional non-composite materials, although the parts used are generally higher priced than C class aerospace parts used in non-composite aircraft structures. As Boeing, Airbus and other customers increase their reliance on composite materials, they may materially reduce their purchase orders from us.

During fiscal 2011, we were notified by Boeing of its intent to perform certain supply chain management functions in-house that we were providing at two facilities under JIT contracts that were awarded to us prior to these particular facilities being acquired by Boeing. In fiscal 2011, JIT sales at these facilities accounted for approximately 3.1% of net sales.

As an example of the potential loss of business due to customer in-sourcing, it is our understanding that Boeing is undertaking an initiative to cause its first and second tier suppliers to source certain Boeing-specific materials, including fasteners, directly from manufacturers, rather than through distributors such as us. If Boeing's initiative is broadly implemented, a portion of our sales to these Boeing suppliers, and consequently our business, financial condition and results of operations, could be adversely affected.

While we believe that we have a diversified customer and aircraft program base, we expect to derive a significant portion of our net sales from certain aerospace programs in their early production stages. In particular, our future growth will be dependent, in part, upon our sales to various OEMs and subcontractors related to the Boeing 787 and the Lockheed Martin JSF. If production of any of the programs we support is terminated or delayed, or if our sales to customers affiliated with these programs are reduced or eliminated, our business, financial condition and results of operations could be adversely affected.

We operate in a highly competitive market and our failure to compete effectively may negatively impact our results of operations.

We operate in a highly competitive global industry and compete against a number of companies, including divisions of larger companies, some of which may have significantly greater financial resources than we do, and therefore may be able to adapt more quickly to changes in customer requirements

18

than we can. Our competitors consist of both U.S. and foreign companies and range in size from divisions of large public corporations to small privately held entities. We believe that our ability to compete depends on superior customer service and support, on-time delivery, sufficient inventory availability, competitive pricing and effective quality assurance programs. In order to remain competitive, we may have to adjust the prices of some of the products and services we sell and continue investing in our procurement, supply-chain management and sales and marketing functions, the costs of which could negatively impact our results of operations.

In addition, we face competition for our JIT and LTA customers from both competitors in our industry and the in-sourcing of supply-chain management by our customers themselves. If any of our JIT or LTA customers decides to in-source the services we provide or switch to one of our competitors, we would be adversely affected.

We may be unable to effectively manage our inventory as we grow, which could have a material adverse effect on our business, financial condition and results of operations.

We have experienced rapid growth in recent periods and intend to continue to grow our business by increasing our product offerings and expanding our customer base. Due to the lead times required by our suppliers, we order products in advance of expected sales, and the volume of such orders may be significant as a result of our growth strategy. Lead times generally range from several weeks up to two years, depending on industry conditions, which make it difficult to successfully manage our inventory as we plan for expected growth. For example, in 2009, our cash flows were negatively impacted as our suppliers continued filling orders that we had placed in anticipation of future sales, while orders from our customers slowed because the aerospace industry had entered a significant downturn. In the future, if we are unable to effectively manage our inventory as we attempt to grow our business, our cash flows may be negatively affected, which could have a material adverse effect on our business, financial condition and results of operations.

If suppliers are unable to supply us with the products we sell in a timely manner, in adequate quantities and/or at a reasonable cost, we may be unable to meet the demands of our customers, which could have a material adverse effect on our business, financial condition and results of operations.

Our inventory is primarily sourced directly from manufacturing firms, and we depend on the availability of large supplies of the products we sell. Our largest supplier for the year ended September 30, 2011 was Alcoa Fastening Systems. During fiscal 2011, approximately 22% of the products we purchased were from Alcoa Fastening Systems and 20% were purchased from Precision Castparts. In addition, our ten largest suppliers during fiscal 2011 accounted for approximately 56% of our purchases. These manufacturers may experience capacity constraints that result in their being unable to supply us with products in a timely manner, in adequate quantities and/or at a reasonable cost. Contributing factors to manufacturer capacity constraints include, among other things, industry or customer demands in excess of machine capacity, labor shortages and changes in raw material flows. Any significant interruption in the supply of these products or termination of our relationship with any of our suppliers could result in us being unable to meet the demands of our customers, which would have a material adverse effect on our business, financial condition and results of operations.

Our business is highly dependent on complex information technology.

The provision and application of IT is an increasingly critical aspect of our business. Among other things, our IT system must frequently interact with those of our customers, suppliers and logistics providers. Our future success will depend on our continued ability to employ an IT system that meets our customers' demands. The failure of the hardware or software that supports our IT system, including redundancy systems, could significantly disrupt our ability to service our customers and cause economic losses for which we could be held liable and which could damage our reputation.

19

Our competitors may have or may develop IT systems that permit them to be more cost effective and otherwise better situated to meet customer demands than we are able to acquire or develop. Larger competitors may be able to develop or license IT systems more cost effectively than we can by spreading the cost across a larger revenue base, and competitors with greater financial resources may be able to acquire or develop IT systems that we cannot afford. If we fail to meet the demands of our customers or protect against disruptions of our IT system, we may lose customers, which could seriously harm our business and adversely affect our operating results and operating cash flow.

We may be unable to retain personnel who are key to our operations.

Our success, among other things, is dependent on our ability to attract, develop and retain highly qualified senior management and other key personnel. Competition for key personnel is intense, and our ability to attract and retain key personnel is dependent on a number of factors, including prevailing market conditions and compensation packages offered by companies competing for the same talent. The inability to hire, develop and retain these key employees may adversely affect our operations.

There are risks inherent in international operations that could have a material adverse effect on our business, financial condition and results of operations.

While the majority of our operations are based in the United States, we have significant international operations, with facilities in Canada, China, France, Germany, Israel, Italy, Saudi Arabia, South Korea and the United Kingdom, and customers throughout North America, Latin America, Europe, Asia and the Middle East. For the years ended September 30, 2011 and 2010, 30% and 26%, respectively, of our net sales were derived from customers located outside the United States.

Our international operations are subject to, without limitation, the following risks:

- •

- the burden of complying with multiple and possibly conflicting laws and any unexpected changes in regulatory requirements;

- •

- political risks, including risks of loss due to civil disturbances, acts of terrorism, acts of war, guerilla activities

and insurrection;

- •

- unstable economic, financial and market conditions and increased expenses as a result of inflation, or higher interest

rates;

- •

- difficulties in enforcement of third-party contractual obligations and collecting receivables through foreign legal

systems;

- •

- difficulties in staffing and managing international operations and the application of foreign labor regulations;

- •

- differing local product preferences and product requirements; and

- •

- potentially adverse tax consequences from changes in tax laws, requirements relating to withholding taxes on remittances and other payments by subsidiaries and restrictions on our ability to repatriate dividends from our subsidiaries.

In addition, fluctuations in the value of foreign currencies affect the dollar value of our net investment in foreign subsidiaries, with these fluctuations being included in a separate component of stockholders' equity. At September 30, 2011, we reported a cumulative foreign currency translation adjustment of approximately $0.7 million in stockholders' equity as a result of foreign currency adjustments, and we may incur additional adjustments in future periods. In addition, operating results of foreign subsidiaries are translated into U.S. dollars for purposes of our statement of operations at average monthly exchange rates. Moreover, to the extent that our net sales are not denominated in the same currency as our expenses, our net earnings could be materially adversely affected. For example, a

20

portion of labor, material and overhead costs for our facilities in the United Kingdom, Germany, France and Italy are incurred in British Pounds or Euros, but the related net sales are generally denominated in U.S. dollars. Changes in the value of the U.S. dollar or other currencies could result in material fluctuations in foreign currency translation amounts or the U.S. dollar value of transactions and, as a result, our net earnings could be materially adversely affected. Although we at times engage in hedging transactions to manage or reduce our foreign exchange risk, our attempts to manage our foreign currency exchange risk may not be successful and, as a result, our business, financial condition and results of operations could be materially adversely affected. For example, in fiscal 2009, the strengthening of the U.S. dollar relative to the British pound resulted in a negative impact on net sales of approximately $22.1 million while in fiscal 2011 and 2010, the weakening of the U.S. dollar relative to the British pound resulted in a positive impact of approximately $2.7 million and $0.1 million respectively. Although we at times engage in hedging transactions to manage or reduce our foreign exchange risk, our attempts to manage our foreign currency exchange risk may not be successful and, as a result, our business, financial condition and results of operations could be materially adversely affected.

Our international operations also cause our business to be subject to the U.S. Export Control regime and similar regulations in other countries, in particular in the United Kingdom. In the United States, items of a commercial nature are generally subject to regulatory control by the U.S. Department of Commerce's Bureau of Industry and Security and to Export Administration Regulations, and other international trade regulations may apply as well. Additionally, we are not permitted to export some of the products we sell. In the future, regulatory authorities may require us to obtain export licenses or other export authorizations to export the products we sell abroad, depending upon the nature of items being exported, as well as the country to which the export is to be made. We cannot assure you that any of our applications for export licenses or other authorizations will be granted or approved. Furthermore, the export license and export authorization process is often time-consuming. Violation of export control regulations could subject us to fines and other penalties, such as losing the ability to export for a period of years, which would limit our sales and significantly hinder our attempts to expand our business internationally.

Our international operations require us to comply with anti-corruption laws and regulations of the U.S. government and various international jurisdictions, and our failure to comply with these laws and regulations could adversely affect our reputation, business, financial condition and results of operations.

Doing business on a worldwide basis requires us and our subsidiaries to comply with the laws and regulations of the U.S. government and various international jurisdictions, and our failure to successfully comply with these rules and regulations may expose us to liabilities. These laws and regulations apply to companies, individual directors, officers, employees and agents, and may restrict our operations, trade practices, investment decisions and partnering activities. In particular, our international operations are subject to U.S. and foreign anti-corruption laws and regulations, such as the U.S. Foreign Corrupt Practices Act, or FCPA. The FCPA prohibits us from providing anything of value to foreign officials for the purposes of influencing official decisions or obtaining or retaining business or otherwise obtaining favorable treatment, and requires companies to maintain adequate record-keeping and internal accounting practices to accurately reflect the transactions of the company. As part of our business, we deal with state-owned business enterprises, the employees and representatives of which may be considered foreign officials for purposes of the FCPA. In addition, some of the international locations in which we operate lack a developed legal system and have elevated levels of corruption. As a result of the above activities, we are exposed to the risk of violating anti-corruption laws.

We are also subject to International Traffic in Arms Regulation, or ITAR. ITAR requires export licenses from the U.S. Department of State for products shipped outside the U.S. that have military or

21