UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER

THE SECURITIES EXCHANGE ACT OF 1934

For the month of April 2013

GRUPO AEROPORTUARIO DEL CENTRO NORTE, S.A.B. DE C.V.

(CENTRAL NORTH AIRPORT GROUP)

_________________________________________________________________

(Translation of Registrant’s Name Into English)

México

_________________________________________________________________

(Jurisdiction of incorporation or organization)

Torre Latitud, L501, Piso 5

Av. Lázaro Cárdenas 2225

Col. Valle Oriente, San Pedro Garza García

Nuevo León, México

_________________________________________________________________

(Address of principal executive offices)

(Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.)

| Form 20-F X Form 40-F |

(Indicate by check mark whether the registrant by furnishing the information contained in this form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.)

| Yes No X |

(If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82- .)

OMA Announces First Quarter 2013 Earnings

Monterrey, Mexico, April 26, 2013 – Mexican airport operator Grupo Aeroportuario del Centro Norte, S.A.B. de C.V., known as OMA (NASDAQ: OMAB; BMV: OMA), reported its unaudited results for the first quarter of 2013 today.1

Summary

OMA recorded solid results in the first quarter of 2013, with 10.7% growth of the sum of aeronautical and non-aeronautical revenues, 12.1% growth in Adjusted EBITDA2, and 14.3% growth in operating income. Consolidated net income increased 22.9% to Ps. 226 million.

The principal developments of the first quarter included:

|

§

|

Terminal passenger traffic increased 4.6% to 3.0 million in 1Q13; domestic traffic increased 5.1%, and international traffic increased 2.6%. Seven of the 15 airlines at our airports grew traffic in the quarter.

|

|

§

|

Three new domestic and one new international routes opened in the quarter.

|

|

§

|

Aeronautical revenues increased 7.5%, principally as a result of the growth in passenger traffic.

|

|

§

|

Non-aeronautical revenues increased 20.9%.

|

|

§

|

The sum of aeronautical and non-aeronautical revenues per passenger increased 5.8% to Ps. 231.4.

|

________________________________

1 Unless otherwise stated, all references are to the first quarter of 2013 (1Q13), and all percentage changes are with respect to the same period of the prior year. The exchange rates used to convert foreign currency amounts were Ps. 12.3480 per U.S. dollar as of March 31, 2013 and Ps. 12.7913 as of March 31, 2012.

2 Adjusted EBITDA excludes the non-cash maintenance provision, construction revenue, and construction expense. OMA provides a full reconciliation of Adjusted EBITDA in the corresponding section of this report; see also the Notes to the Financial Information.

|

§

|

Aeronautical revenues per passenger increased 2.7% to Ps. 170.7.

|

|

§

|

Non-aeronautical revenues per passenger increased 15.5% to Ps. 60.7; this marks the 20th consecutive quarter of growth in non-aeronautical revenues.

|

|

§

|

Adjusted EBITDA increased 12.1% to Ps. 393 million in 1Q13. The Adjusted EBITDA margin reached 56.0%, an increase of 70 basis points, reflecting OMA’s efforts to increase cash flow generation.

|

|

§

|

Consolidated net income rose 22.9% to Ps. 226 million. Earnings per share were Ps. 0.57, or US$ 0.37 per American Depositary Share (ADS).

|

|

§

|

Capital expenditures were Ps. 169 million.

|

Operating Results

Passenger Traffic, Flight Operations, and Cargo Volumes

See Notes to the Financial Information

The total number of flight operations (takeoffs and landings) decreased 4.3% to 79,393 operations. Domestic flight operations decreased 5.2% and international operations increased 0.9%.

Total passenger traffic increased 4.6% (+133,695 terminal passengers).

Traffic increased most in the Monterrey (+8.9%), Reynosa (+42.9%), Culiacán (+6.4%), and Acapulco (+6.4%) airports. Seven airlines had increases in passenger volumes. The Ciudad Juárez (-7.6%), Zacatecas (-13.5%), Zihuatanejo (-4.7%), and San Luis Potosí (-9.4%) airports had the largest decreases. (See Annex Table 1, Passenger Traffic for more detail.)

Of total passenger traffic, 82.5% was domestic, and 17.5% was international. Commercial aviation accounted for 97.5% of passenger traffic and general aviation 2.5%. Monterrey generated 46.3% of passenger traffic, Culiacán 9.2%, and Mazatlán 6.5%.

Domestic passenger traffic increased 5.1%.

Seven airports had increases in domestic traffic. Monterrey (+8.2%) had increases principally on the routes to Veracruz and Cancún. Reynosa (+43.0%) increased traffic on the Mexico City route; Culiacán (+5.7%) increased traffic on the Tijuana and San José del Cabo routes. Mazatlán (+7.8%) increased traffic on the Monterrey route, and Acapulco (+9.0%) increased traffic on the Mexico City route.

Ciudad Juárez (-7.7%), Zihuatanejo (-9.1%), and Zacatecas (-14.0%) all had decreased traffic on their Mexico City routes.

3

Three domestic routes opened and six closed during the quarter.

International passenger traffic increased 2.6%.

Six airports had increases in international traffic. The most significant increases were in Monterrey (+13.1%) with increases from the routes to Dallas and Chicago and Culiacán (+63.4%) with increases on the Los Angeles route.

Seven airports had reductions in international passenger traffic, with the most significant decreases in Mazatlán (-9.3%) and Zacatecas (-12.1%), as a result of lower traffic on the Seattle and Los Angeles routes, respectively.

Interjet opened one international route opened in the quarter, while VivaAerobus closed the same route.

Air Cargo volumes decreased 6.7%, principally as a result the end of operations by some freight consolidators.

Of total air cargo volume, 61.2% was domestic and 38.8% was international.

Non-Aeronautical and Commercial Operations

During 1Q13, we continued to expand and improve the commercial offering and passenger services available in our airport terminals, as part of our commercial strategy. Fifteen new retail, advertising, car rental, and communication services opened in our airports. The occupancy rate of our commercial space was 93%, as compared to 92% in 1Q12, as a result of our initiatives to achieve steady growth of commercial revenues.

NH Terminal 2 Hotel Operations

The NH T2 hotel in the Mexico City International Airport had an average occupancy rate of 81.4%, as compared to 81.0% in 1Q12. The NH T2 hotel had the highest occupancy rate in the Mexico City airport hotel market in 1Q13, and a 17.6% market share.

4

Consolidated Financial Results

Revenues

Total revenues increased 11.8% to Ps. 788 million. The sum of aeronautical and non-aeronautical revenues increased 10.7% to Ps. 701 million. Construction revenues increased to Ps. 87 million compared to Ps. 71 million in 1Q12; construction revenues represent the value of improvements to concessioned assets made during the quarter. (See Notes to the Financial Information.)

The 7.5% increase in aeronautical revenues was principally the result of the increase in passenger traffic. Non-aeronautical revenues rose 20.9%, principally because of increased revenues from checked baggage screening, OMA Carga, the NH T2 hotel, and advertising.

Non-aeronautical revenues were 26.2% of total aeronautical and non-aeronautical revenues. In 2006, when OMA carried out its IPO, non-aeronautical revenues were only 18.7% of the total.

The Monterrey airport contributed 47.7% of the sum of aeronautical and non-aeronautical revenues (Ps. 700 million), Culiacán 9.0%, and Mazatlán 7.4%.

Aeronautical revenues increased 7.5% to Ps. 517 million. Domestic passenger charges increased 9.7% principally as a result of increased domestic traffic. International passenger charges increased 0.4%, as a result of an increase in passenger traffic, which was partially offset by a less favorable exchange rate. Aeronautical revenue per passenger increased 2.7% to Ps. 170.7.

Non-aeronautical revenues increased 20.9%, principally because of growth in revenues from checked baggage screening, OMA Carga, the NH T2 hotel, and advertising.

Cargo revenues increased 40.5% to Ps. 9 million in 1Q13. The increase in revenues reflects principally the re-composition of the cargo business and the increased volumes of ground traffic in the in-bond zones of the Monterrey and Chihuahua airports.

5

NH T2 hotel revenues increased 5.3% to Ps. 40 million, principally as a result of increased restaurant revenues and a higher occupancy rate. Revenue per available room (RevPAR) was Ps. 1,230 in 1Q13, 4% higher than 1Q12. Room rentals were 78.7% of hotel revenues, food and beverages 18.4%, and other services 2.9%.

Monterrey contributed 38.2% of non-aeronautical revenues, the NH T2 hotel 21.9%, Mazatlán 4.8%, and Culiacán 4.4%.

Non-aeronautical revenues per passenger increased 15.5% to Ps. 60.7. Non-aeronautical revenues per passenger, excluding the NH T2 hotel, increased 20.5% to Ps. 47.4.

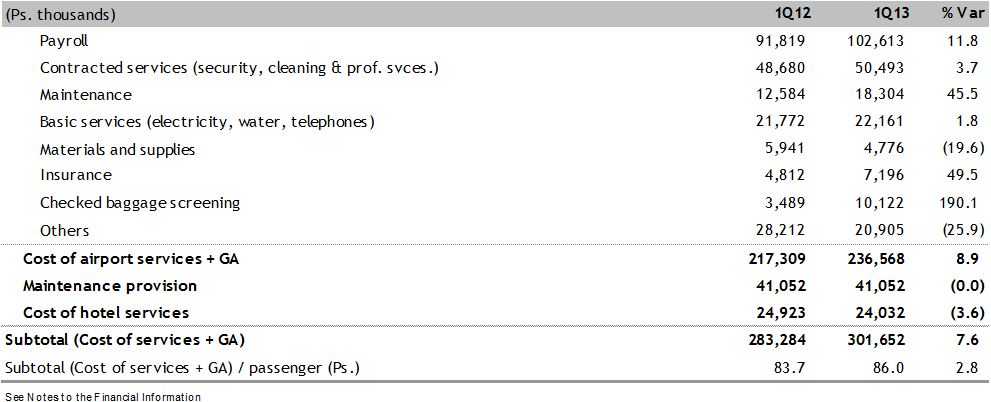

Costs and Operating Expenses

Total cost of services and general and administrative expenses, excluding the maintenance provision, construction costs, and hotel costs and expenses, increased 8.9%. The increase was principally the result of increases in costs for operating checked baggage screening, payroll, and insurance, all as a result of the start of operations for checked baggage screening, which became effective for all airlines in December 2012. In addition, minor maintenance increased as a result of work on several terminal buildings.

The increased costs related to checked baggage screening equipment are expected to be recovered through payment for this service by the airlines, as well as through each airport’s maximum rate.

6

The airport concession tax increased 9.0% because of the growth in revenues. The technical assistance fee increased 10.5%, as a result of the increase in EBITDA.

Depreciation and amortization increased 9.9%, principally as a result of increased investments, including the expansion of the Culiacán airport.

As a result of the foregoing and the increase in construction costs, total costs and expenses increased 10.3% to Ps. 485 million in 1Q13. Construction costs are equal to construction revenues and do not generate any gain or loss.

Adjusted EBITDA and Operating Income

Adjusted EBITDA increased 12.1% to Ps. 393 million in 1Q13. The Adjusted EBITDA margin was 56.0%, an increase of 70 basis points over the prior year period, and a reflection of OMA’s initiatives to increase cash flow.

OMA calculates Adjusted EBITDA as shown in the table below. The Adjusted EBITDA margin is calculated against the sum of aeronautical and non-aeronautical revenues. (See Notes to the Financial Information for additional discussion of Adjusted EBITDA.)

7

Operating income increased 14.3% to Ps. 302 million, and the operating margin was 38.4%.

Financing Expense and Taxes

Comprehensive financing expense was Ps. 11 million in 1Q13, as compared to a gain in the prior year period. The result reflects a reduction in the exchange gain and an increase in financial expense.

The tax provision was Ps. 65 million. There was an increase in current income tax and IETU single-rate corporate tax paid of Ps. 6 million as a result of a higher taxable base, which was offset by a reduction in deferred income tax and IETU of Ps. 29 million, principally from the application of expense provisions.

Net Income

8

Earnings per share were Ps. 0.57, and earnings per ADS were US$0.35 per ADS. Each ADS represents eight Series B shares. (See Annex Table 3.)

Capital Expenditures

During 1Q13, capital expenditures were Ps. 124 million, including Master Development Plan (MDP) projects and acquisitions as well as strategic investments. Major maintenance, which is part of MDP investments, was Ps. 40 million in 1Q13, and was a charge against the maintenance provision, reducing this long term liability. The most important investments during the first quarter were:

|

§

|

Remodeling of the Zihuatanejo airport terminal building.

|

|

§

|

Design, procurement and installation of two passenger jetways in Cuidad Juárez.

|

|

§

|

Rehabilitation of the Torreón airport runway.

|

|

§

|

Expansion of the commercial aviation platform, taxiway, and new commercial aviation zone at the San Luis Potosí airport.

|

|

§

|

Rehabilitation of the Reynosa airport runway.

|

|

§

|

Expansion and remodeling of the San Luis Potosí terminal building.

|

|

§

|

Rehabilitation of the Mazatlán airport runway.

|

|

§

|

Design, installation, and start of operations of closed circuit TV systems for the Monterrey airport.

|

|

§

|

Design engineering for the construction and reconfiguration of roadways in the Durango airport.

|

Debt

OMA’s debt obligations are summarized below:

|

Credit

|

Term

|

Amount

|

Final

Maturity

|

Rate

|

Use of proceeds

|

|

|

Short term bank lines

|

Revolving

|

Ps. 505 million

|

--

|

TIIE + 95 bp

|

Working capital

|

|

|

Notes (Certificados Bursátiles) OMA11

|

5 yr bullet

|

Ps. 1,300 million

|

2016

|

TIIE + 70 bp

|

Debt refinancing

|

|

|

Notes - OMA13

|

10 yr bullet

|

Ps. 1,500 million

|

2023

|

6.47%

|

Capex and debt refinancing

|

|

|

Commercial Paper

|

28 day

|

Ps. 100 million

|

Renewable

|

4.17%

|

Working capital

|

|

|

Term Loan

|

10 yr, equal quarterly amortization

|

US$ 16.3 million

|

2021

|

3m Libor +125 bp

|

Checked baggage screening equipment

|

|

|

Term Loan

|

5 yr, equal quarterly amortization

|

US$ 2.7 million

|

2017

|

3m Libor + 95 bp

|

Firefighting equipment

|

The ratio of net debt to LTM Adjusted EBITDA was 0.6 as of March 31, 2013.

9

For the full quarter of 2013, operating activities generated cash of Ps. 279 million compared to Ps. 250 million during 2012. The increase was principally because of higher operating income and improved working capital management in 1Q13.

During 1Q13, OMA made investments of Ps. 171 million, principally under the MDP, that are recorded in the following accounts: Ps. 46 million in the cash flow statement under investment in airport concessions, Ps. 18 million in acquisition of land, machinery, and equipment; and in the income statement, a Ps. 66 million maintenance provision, among others.

Investment activities, as presented in the cash flow statement, used cash of Ps. 50 million in 1Q13.

Financing activities generated an inflow of Ps. 1,510 million, principally from the issuance of Ps. 1,500 million in 10-year Notes and Ps. 100 million in Commercial Paper in March 2013.

OMA had a net increase in cash of Ps. 1,740 million in 1Q13. The balance of cash and cash equivalents was Ps. 2,893 million as of March 31, 2013. (See Annex Table 4).

OMA has no exposure to any financial derivative instruments as of the date of this report.

2013 Outlook

OMA expects that 2013 passenger traffic will increase approximately 3.5% to 4.5%, and expects that the sum of aeronautical and non-aeronautical revenues will increase approximately 8.0% to 10.0%. The Adjusted EBITDA margin for the full year is expected to be in the range 50.5% to 52.0%. Total MDP capex during 2013 is expected to be in the range of Ps. 700 million to Ps. 800 million. Investments for diversification activities are expected to be in the range of Ps. 100 million to Ps. 200 million.

OMA is providing this outlook based on internal estimates. A number of factors could have a significant effect on the estimates of traffic, revenue growth, Adjusted EBITDA, and Capex. These include changes in airline expansion plans, ticket prices and other factors affecting traffic volumes, the evolution of commercial and diversification projects, and economic conditions including oil prices, among others. OMA can provide no assurance that the Company will achieve these results.

Subsequent Events

Annual Shareholders’ Meeting: On April 16, 2013, the Annual Shareholders’ Meeting approved payment of a capital reimbursement to shareholders of Ps. 1,200 million, or Ps. 3.00 per share, without cancellation of shares, to be paid in five installments. A first extraordinary payment of Ps.400 million, or Ps.1.00 per share, will be paid no later than June 28, 2013. The remaining Ps. 800 million will be paid in four quarterly installments of Ps. 200 million (Ps. 0.50 per share) on or before the following dates: July 31, 2013, against delivery of coupon 25; October 31, 2013, against delivery of coupon 26; January 31, 2014, against delivery of coupon 27, and April 30, 2014, against delivery of coupon 28. In addition, the Shareholders’ Meeting approved the designation of Diego Quintana Kawage as Chairman of the Board, and the election of Elsa Beatriz García Bojorges, Ricardo Gutierrez Muñoz, and Carlos Guzmán Bofill as Independent Directors, replacing Aaron Dychter Poltolarek, Fernando Flores Pérez, and Cristina Gil White.

10

Prepayment of revolving credit: During April 2013, OMA repaid a Ps. 300 million revolving credit to Scotiabank, which carried an interest rate of TIIE + 90 bp, using the proceeds of the Note issuance.

| OMA (NASDAQ: OMAB; BMV: OMA) will hold its 1Q13 earnings conference call on April 29, 2013 at 11:00 am Eastern time, 10:00 am Mexico City time.

The conference call is accessible by calling 877-941-1428 toll-free from the U.S. or 1-480-629-9665 from outside the U.S. The conference ID is 4615867. A taped replay will be available through May 6, 2013 at 877-870-5176 toll free or + 1-858-384-5517, using the same ID.

The conference call will also be available by webcast at http://ir.oma.aero/events.cfm.

|

OMA (NASDAQ: OMAB; BMV: OMA) will hold its 1Q13 earnings conference call on April 29, 2013 at 11:00 am Eastern time, 10:00 am Mexico City time.

The conference call is accessible by calling 877-941-1428 toll-free from the U.S. or 1-480-629-9665 from outside the U.S. The conference ID is 4615867. A taped replay will be available through May 6, 2013 at 877-870-5176 toll free or + 1-858-384-5517, using the same ID.

The conference call will also be available by webcast at http://ir.oma.aero/events.cfm.

11

Annex Table 1

12

Annex Table 2

13

Annex Table 3

14

Annex Table 4

15

Annex Table 5

16

Annex Table 6

17

Notes to the Financial Information

Financial statements are prepared in accordance with International Financial Reporting Standards (“IFRS”), and presented in accordance with IAS 34 “Interim Financial Reporting.”

Adjusted EBITDA: OMA defines Adjusted EBITDA as net income minus net comprehensive financing income plus taxes and depreciation and amortization minus construction revenue plus construction expense and maintenance provision. Adjusted EBITDA should be not considered as an alternative to net income, as an indicator of our operating performance, or as an alternative to cash flow as an indicator of liquidity. Our management believes that Adjusted EBITDA provide a useful measure of our performance that is widely used by investors and analysts to evaluate our performance and compare it with other companies. Financial ratios calculated on the base of Adjusted EBITDA are also widely used by credit providers in order to gauge the debt servicing capacity of companies. Adjusted EBITDA is not defined under IFRS or U.S. GAAP, and may be calculated differently by different companies.

Aeronautical revenues: are revenues from rate-regulated services. These include revenue from airport services, regulated leases, and access fees from third parties to provide complementary and ground transportation services. Airport service revenues include principally departing domestic and international passenger charges (TUA), landing fees, aircraft parking charges, passenger and carry-on baggage screening, and use of passenger jetways, among others. Revenue from third party access fees to provide complementary services include revenue sharing for ramp services, aircraft towing, water loading and unloading, cabin cleaning, electricity supply, catering, security, and aircraft maintenance, among others. Revenues from regulated leases include principally rental to airlines of office space, hangars, and check-in and ticket sales counters. Revenues from access charges for providers of ground transportation services include charges for taxis and buses.

Airport Concession Tax (DUAC): This tax, the Derecho de Uso de Activos Concesionados, is equal to 5% of gross revenues, in accordance with the Federal Royalties Law.

American Depositary Shares (ADS): Securities issued by a U.S. depositary institution representing ownership interests in the deposited securities of non-U.S. companies. OMA’s depositary bank is Bank of New York Mellon. Each OMA ADS represents eight Series B shares.

Capital expenditures, Capex: includes investments in fixed assets (including investments in land, machinery, and equipment) and improvements to concessioned properties.

Cargo unit: equivalent to 100 kg of cargo. .

Checked Baggage Screening: During 2012, OMA began to operate checked baggage screening in its 13 airports in order to increase airport security and in compliance with the requirements of the Civil Aviation General Directorate (DGAC). This screening uses the latest technology and is designed to detect explosives in checked baggage. The cost of maintenance of the screening equipment is considered a regulated activity and will be recovered through the maximum rates, while the operational aspects are assessed as a non-regulated service charge. In accordance with the Civil Aviation Law and the regulations issued by the DGAC, the primary responsibility for damages and losses resulting from checked baggage lies with the airline. Notwithstanding the foregoing, OMA may be found jointly liable with the airline through a legal proceeding if and when all of the following elements are proven: a) occurrence of an illegal act, b) caused by the willful misconduct or bad faith of the airport, and c) related to or occurring during the baggage screening undertaken by the airport.

Construction revenue, construction cost: IFRIC 12 “Service Concession Arrangements” addresses how service concession operators should apply existing International Financial Reporting Standards (IFRSs) to account for the obligations they undertake and rights they receive in service concession arrangements. The concession contracts for each of OMA’s airport subsidiaries establishes that the concessionaire is obligated to carry out construction or improvements to the infrastructure transferred in exchange for the rights over the concession granted by the Federal Government. The latter will receive all the assets at the end of the concession period. As a result the concessionaire should recognize, using the percentage of completion method, the revenues and costs associated with the improvements to the concessioned assets. The amount of the revenues and costs so recognized should be the price that the concessionaire pays or would pay in an arm’s length transaction for the execution of the works or the purchase of machinery and equipment, with no profit recognized for the construction or improvement. The change does not affect operating income, net income, or EBITDA, but does affect calculations of margins based on total revenues.

18

Earnings per share and ADS: use the weighted average of shares or ADS outstanding for each period, excluding Treasury shares from the operation of the share purchase program.

Employee Benefits: IFRS 19 (modified) “Employee Benefits” requires that cumulative actuarial gains and losses from pension obligations be recognized immediately in comprehensive income. These gains and losses arise from the actuarial estimates used for calculating pension liabilities as of the date of the financial statements.

IAS 34 “Interim Financial Reporting”: This norm establishes the minimum content that interim financial statements should include, as well as the criteria for the formulation of the financial statements.

International Financial Reporting Standards (IFRS

In January 2009, the National Banking and Securities Commission (CNBV) published amendments to its Circular for Issuers to make mandatory the presentation of financial statements prepared in accordance with International Financial Reporting Standards (IFRS) starting with the year ending March 31, 2013, but allowing for early adoption. OMA’s Board of Directors approved early adoption of IFRS for the year ending March 31, 2012. The financial statements for the year ended March 31, 2010 were the last statements that were prepared in accordance with Mexican Financial Reporting Standards (MFRS). These financial statements have been reformulated for comparative effects under IFRS.

Financial statements and other information are presented in accordance with IFRS and their Interpretations. These standards differ in certain significant respects from U.S. GAAP.

Maintenance Provision: represents the obligation for future disbursements resulting from wear and tear or deterioration of the concessioned assets used in operations including: runways, platforms, taxiways, and terminal buildings. The provision is increased periodically for the wear and tear to the concessioned assets and the Company’s estimates of the disbursements it need to make. The use of the provision corresponds to the outflows made for the conservation of these operational assets.

Master Development Plan (MDP): The investment plan agreed to with the government every five years, under the terms of the concession agreement. These include capital investments and maintenance for aeronautical activities, and exclude commercial and other non-aeronautical investments. The investment horizon is 15 years, of which the first five years are committed investments.

Maximum Rate System: The Ministry of Communications and Transportation (SCT) regulates all our aeronautical revenues under a maximum rate system, which establishes the maximum amount of revenues per workload unit (one terminal passenger or 100kg of cargo) that may be earned by each airport each year from all regulated revenue sources. The concessionaire sets and registers the specific prices for services subject to regulation, which may be adjusted every six months as long as the combined revenue from regulated services per workload unit at an airport does not exceed the maximum rate. The SCT reviews compliance with maximum rates on an annual basis after the close of each year.

NH T2 hotel: The NH hotel in Terminal 2 of the Mexico City International Airport.

Non-aeronautical revenues: are revenues that are not subject to rate regulation. These include commercial services such as parking, advertising, car rentals, leasing of commercial space, freight management and handling, and other lease income, among others.

Passengers: all eferences to passenger traffic volumes are to terminal passengers.

Passenger charges (TUA, Tarifa de Uso de Aeropuerto): are paid by departing passengers (excluding connecting passengers, diplomats, and infants). Rates are established for each airport and are different for domestic and international travel.

19

Prior period comparisons: unless stated otherwise, all comparisons of operating or financial results are made with respect to the comparable prior year period. Percentage changes for passenger traffic or financial items are calculated based on actual numbers.

Strategic investments: refers only to those investments that are additional to those in the Master Development Plan.

Technical Assistance Fee: This fee is charged as the higher of US$3.0 million per year or 5% of EBITDA before technical assistance. The operating results of the NH T2 hotel are not included in calculating the airport concession tax or the technical assistance fee.

Terminal passengers: includes passengers on the three types of aviation (commercial, charter, and general aviation), and excludes passengers in transit.

Unaudited financials: financial statements are unaudited statements for the periods covered by the report

Workload Unit: one terminal passenger or one cargo unit.

Analyst Coverage: In accordance with the regulations of the Mexican Stock Exchange, the analysts who cover OMA are:

| Barclays – Benjamin Theurer

BBVA Bancomer – Pablo Abraham

Citigroup - Stephen Trent

Credit Suisse – Vanessa Quiroga

GBM – Luis Willard

HSBC – Francisco Suárez

Itaú – Vivian Salomón

|

JP Morgan – Fernando Abdalla

Merrill Lynch – Sara Delfim

Morgan Stanley – Nicolai Sebrell

Santander – Rogelio Urrutia

Scotia Capital – Rodrigo Echegaray

Vector – Marco Montañez

|

20

This report may contain forward-looking information and statements. Forward-looking statements are statements that are not historical facts. These statements are only predictions based on our current expectations and projections about future events. Forward-looking statements may be identified by the words “believe,” “expect,” “anticipate,” “target,” or similar expressions. While OMA's management believes that the expectations reflected in such forward-looking statements are reasonable, investors are cautioned that forward-looking information and statements are subject to various risks and uncertainties, many of which are difficult to predict and are generally beyond the control of OMA, that could cause actual results and developments to differ materially from those expressed in, or implied or projected by, the forward-looking information and statements. These risks and uncertainties include, but are not limited to, those discussed in our most recent annual report filed on Form 20-F under the caption “Risk Factors.” OMA undertakes no obligation to publicly update its forward-looking statements, whether as a result of new information, future events, or otherwise.

About OMA

Grupo Aeroportuario del Centro Norte, S.A.B. de C.V., known as OMA, operates 13 international airports in nine states of central and northern Mexico. OMA’s airports serve Monterrey, Mexico’s third largest metropolitan area, the tourist destinations of Acapulco, Mazatlán, and Zihuatanejo, and nine other regional centers and border cities. OMA also operates a hotel and commercial areas inside Terminal 2 of the Mexico City airport. OMA employs over 1,000 persons in order to offer passengers and clients, airport and commercial services in facilities that comply with all applicable international safety, security standards, and ISO 9001:2008. OMA’s strategic shareholder members are ICA, Mexico’s largest engineering, procurement, and construction company, and Aéroports de Paris Management, subsidiary of Aéroports de Paris, the second largest European airports operator. OMA is listed on the Mexican Stock Exchange (OMA) and on the NASDAQ Global Select Market (OMAB). For more information, please visit us at:

|

§

|

Website: |

http://www.oma.aero

|

|

§

|

Twitter: |

http://twitter.com/OMAeropuertos

|

|

§

|

Facebook: |

http://www.facebook.com/pages/OMA/137924482889484

|

21

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

Grupo Aeroportuario del Centro Norte, S.A.B. de C.V.

|

By:

|

/s/ José Luis Guerrero Cortés

|

|

|

José Luis Guerrero Cortés

|

||

|

Chief Financial Officer

|

||

Date: April 29, 2013