UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD OF _________ TO _________. |

Commission File Number:

(Exact name of registrant as specified in its charter)

| Not-Applicable | |

State or other jurisdiction of incorporation or organization |

| (I.R.S. Employer Identification No.) |

(Address of principal executive offices, including zip code)

Registrant’s telephone number, including area code:

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol | Name of each exchange on which registered |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act

Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act.

Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ | Accelerated filer ☐ | Smaller reporting company | |

|

| Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes

As of February 24, 2021, there were

DOCUMENTS INCORPORATED BY REFERENCE

Certain information required for Items 10, 11, 12, 13 and 14 of Part III of this Annual Report on Form 10-K is incorporated by reference to the registrant’s definitive proxy statement for the 2021 Annual Meeting of Shareholders.

UR-ENERGY INC.

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

| 2 |

| Table of Contents |

When we use the terms “Ur-Energy,” “we,” “us,” “our,” or the “Company,” we are referring to Ur-Energy Inc. and its subsidiaries, unless the context otherwise requires. We have included technical terms important to an understanding of our business under “Glossary of Common Terms” at the end of this section. Throughout this document we make statements that are classified as “forward-looking.” Please refer to the “Cautionary Statement Regarding Forward-Looking Statements” section of this document for an explanation of these types of assertions.

Cautionary Statement Regarding Forward-Looking Information

This annual report on Form 10-K contains "forward-looking statements" within the meaning of applicable United States and Canadian securities laws, and these forward-looking statements can be identified by the use of words such as "expect," "anticipate," "estimate," "believe," "may," "potential," "intends," "plans" and other similar expressions or statements that an action, event or result "may," "could" or "should" be taken, occur or be achieved, or the negative thereof or other similar statements. These statements are only predictions and involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements, or industry results, to be materially different from any future results, performance, or achievements expressed or implied by these forward-looking statements. Such statements include, but are not limited to: (i) the ability to maintain controlled and reduced level operations at Lost Creek in safe and compliant fashion; (ii) the timing to determine future development and construction priorities, and the ability to readily and cost-effectively ramp-up production operations when market and other conditions warrant; (iii) the continuing technical and economic viability of Lost Creek; (iv) the timing and outcome of remaining permitting and regulatory approvals of the amendments to the Lost Creek permits and licenses; (v) the ability and timing to complete additional favorable uranium sales agreements including spot sales when warranted; (vi) the production rates and life of the Lost Creek Project and subsequent development of and production from adjoining projects within the Lost Creek Property, including plans at LC East; (vii) the potential of exploration targets throughout the Lost Creek Property (including the ability to expand resources); (viii) the potential of our other exploration and development projects, including Shirley Basin, the projects in the Great Divide Basin and the Excel project (ix) the technical and economic viability of Shirley Basin; (x) the timing and outcome for remaining regulatory approvals to build and operate an in situ recovery mine at Shirley Basin; (xi) current and near-term market conditions including without limitation supply and demand projections; (xii) further action on the recommendations from the U.S. Nuclear Fuel Working Group, including the timeline and scope of proposed remedies; (xiii) outcome of the process to establish the national uranium reserve program, including the procurement process and our role in it, as well as further budget appropriations processes related to the reserve. These other factors include, among others, the following: future estimates for production, development and production operations, capital expenditures, operating costs, mineral resources, recovery rates, grades and market prices; business strategies and measures to implement such strategies; competitive strengths; estimates of goals for expansion and growth of the business and operations; plans and references to our future successes; our history of operating losses and uncertainty of future profitability; status as an exploration stage company; the lack of mineral reserves; risks associated with obtaining permits and other authorizations in the U.S.; risks associated with current variable economic conditions; our ability to service our debt and maintain compliance with all restrictive covenants related to the debt facility and security documents; the possible impact of future financings; the hazards associated with mining production; compliance with environmental laws and regulations; uncertainty regarding the pricing and collection of accounts; the possibility for adverse results in potential litigation; uncertainties associated with changes in government policy and regulation; uncertainties associated with a Canada Revenue Agency or U.S. Internal Revenue Service audit of any of our cross border transactions; adverse changes in general business conditions in any of the countries in which we do business; changes in size and structure; the effectiveness of management and our strategic relationships; ability to attract and retain key personnel; uncertainties regarding the need for additional capital; uncertainty regarding the fluctuations of quarterly results; foreign currency exchange risks; ability to enforce civil liabilities under U.S. securities laws outside the United States; ability to maintain our listing on the NYSE American LLC (“NYSE American”) and Toronto Stock Exchange (“TSX”); risks associated with the expected classification as a "passive foreign investment company" under the applicable provisions of the U.S. Internal Revenue Code of 1986, as amended; risks associated with our investments and other risks and uncertainties described under the heading “Risk Factors” of this annual report.

| 3 |

| Table of Contents |

Cautionary Note to U.S. Investors Concerning Disclosure of Mineral Resources

Unless otherwise indicated, all resource estimates included in this annual report on Form 10-K have been prepared in accordance with Canadian National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum Definition Standards for Mineral Resources and Mineral Reserves (“CIM Definition Standards”). NI 43-101 is a rule developed by the Canadian Securities Administrators which establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. NI 43-101 permits the disclosure of an historical estimate made prior to the adoption of NI 43-101 that does not comply with NI 43-101 to be disclosed using the historical terminology if the disclosure: (a) identifies the source and date of the historical estimate; (b) comments on the relevance and reliability of the historical estimate; (c) to the extent known, provides the key assumptions, parameters and methods used to prepare the historical estimate; (d) states whether the historical estimate uses categories other than those prescribed by NI 43-101; and (e) includes any more recent estimates or data available.

Canadian standards, including NI 43-101, differ significantly from the requirements of the U.S. Securities and Exchange Commission (“SEC”), and resource information contained in this Form 10-K may not be comparable to similar information disclosed by U.S. companies. In particular, the term “resource” does not equate to the term “‘reserves.” Under SEC Industry Guide 7, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. SEC Industry Guide 7 does not define and the SEC’s disclosure standards normally do not permit the inclusion of information concerning “measured mineral resources,” “indicated mineral resources” or “inferred mineral resources” or other descriptions of the amount of mineralization in mineral deposits that do not constitute “reserves” by U.S. standards in documents filed with the SEC. U.S. investors should also understand that “inferred mineral resources” have a great amount of uncertainty as to their existence and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an “inferred mineral resource” will ever be upgraded to a higher category. Under Canadian rules, estimated “inferred mineral resources” may not form the basis of feasibility or pre-feasibility studies except in rare cases. Investors are cautioned not to assume that all or any part of an “inferred mineral resource” exists or is economically or legally mineable. Disclosure of “contained ounces” in a resource is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that does not constitute “reserves” by SEC standards as in-place tonnage and grade without reference to unit measures. Accordingly, information concerning mineral deposits set forth herein may not be comparable to information made public by companies that report in accordance with U.S. standards.

NI 43-101 Review of Technical Information: Michael Mellin, Ur-Energy / Lost Creek Mine Geologist, P.Geo. and Qualified Person as defined by NI 43-101, reviewed and approved the technical information contained in this Form 10-K.

| 4 |

| Table of Contents |

Glossary of Common Terms and Abbreviations

Mineral Resource |

| is a concentration or occurrence of solid material of economic interest in or on the Earth’s crust in such form, grade or quality and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade or quality, continuity and other geological characteristics of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge, including sampling. CIM Definition Standards; NI 43-101, Section 1.1. |

|

|

|

Inferred Mineral Resource |

| is that part of a Mineral Resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. Geologic evidence is sufficient to imply but not verify geological and grade or quality continuity. An Inferred Mineral Resource has a lower level of confidence than that applying to an Indicated Mineral Resource and must not be converted to a Mineral Reserve. It is reasonably expected that the majority of Inferred Mineral Resources could be upgraded to Indicated Mineral Resources with continued exploration. CIM Definition Standards; NI 43-101, Section 1.1. |

|

|

|

Indicated Mineral Resource |

| is that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics are estimated with sufficient confidence to allow the application of Modifying Factors in sufficient detail to support mine planning and evaluation of the economic viability of the deposit. Geological evidence is derived from adequately detailed and reliable exploration, sampling and testing and is sufficient to assume geological and grade or quality continuity between points of observation. An Indicated Mineral Resource has a lower level of confidence than that applying to a Measured Mineral Resource and may only be converted to a Probable Mineral Reserve. CIM Definition Standards; NI 43-101, Section 1.1. |

|

|

|

Measured Mineral Resource |

| is that part of a Mineral Resource for which quantity, grade or quality, densities, shape, and physical characteristics are estimated with confidence sufficient to allow the application of Modifying Factors to support detailed mine planning and final evaluation of the economic viability of the deposit. Geological evidence is derived from detailed and reliable exploration, sampling and testing and is sufficient to confirm geological and grade or quality continuity between points of observation. A Measured Mineral Resource has a higher level of confidence than that applying to either an Indicated Mineral Resource or an Inferred Mineral Resource. It may be converted to a Proven Mineral Reserve or to a Probable Mineral Reserve. CIM Definition Standards; NI 43‑101, Section 1.1. |

|

|

|

Cut-off or cut-off grade |

| when determining economically viable mineral resources, the lowest grade of mineralized material that can be mined |

|

|

|

Formation |

| a distinct layer of sedimentary or volcanic rock of similar composition |

|

|

|

Grade |

| quantity or percentage of metal per unit weight of host rock |

|

|

|

Host Rock |

| the rock containing a mineral or an ore body |

|

|

|

Modifying Factors |

| are considerations used to convert Mineral Resources to Mineral Reserves. These include, but are not restricted to, mining, processing, metallurgical, infrastructure, economic, marketing, legal, environmental, social and governmental factors. CIM Definition Standards |

| 5 |

| Table of Contents |

Lithology |

| is a description of a rock; generally, its physical nature. The description would address such things as grain size, texture, rounding, and even chemical composition. An example of a lithologic description would be ‘coarse grained well-rounded quartz sandstone with 10% pink feldspar and 1% muscovite.’ |

|

|

|

Mineral |

| a naturally formed chemical element or compound having a definite chemical composition and, usually, a characteristic crystal form. |

|

|

|

Mineralization |

| a natural occurrence, in rocks or soil, of one or more metal yielding minerals |

|

|

|

Outcrop |

| is that part of a geologic formation or structure that appears at the surface of the Earth. |

|

|

|

PFN |

| is a modern geologic logging method known as Prompt Fission Neutron. PFN is considered a direct measurement of true uranium concentration (% U) and is used to verify the grades of mineral intercepts previously reported by gamma logging. PFN logging is accomplished by a down-hole probe in much the same manner as gamma logs, however, only the mineralized interval plus a buffer interval above and below are logged. |

|

|

|

PPP |

| is the Paycheck Protection Program of the Small Business Administration, implemented as a part of the CARES Act (March 2020). |

|

|

|

Preliminary Economic Assessment (or PEA) |

| is a Preliminary Economic Assessment performed under NI 43-101. A Preliminary Economic Assessment is a study, other than a prefeasibility study or feasibility study, which includes an economic analysis of the potential viability of mineral resources. |

|

|

|

Reclamation |

| is the process by which lands disturbed as a result of mineral extraction activities are modified to support beneficial land use. Reclamation activity may include the removal of buildings, equipment, machinery, and other physical remnants of mining activities, closure of tailings storage facilities, leach pads, and other features, and contouring, covering and re-vegetation of waste rock, and other disturbed areas. |

|

|

|

Restoration |

| is the process by which aquifers affected by mineral extraction activities are treated in an effort to return the concentration of pre-determined chemicals in the aquifer to pre-mining levels or, if approved by applicable government agencies, a pre-mining class of use such as industrial or livestock. |

|

|

|

Uranium |

| a heavy, naturally radioactive, metallic element of atomic number 92. Uranium in its pure form is a heavy metal. Its two principal isotopes are U-238 and U-235, of which U-235 is the necessary component for the nuclear fuel cycle. However, “uranium” used in this Annual Report refers to triuranium octoxide, also called “U3O8” and is produced from uranium deposits. It is the most actively traded uranium-related commodity. Our operations produce and ship “yellowcake” which typically contains 70% to 90% U3O8 by weight. |

|

|

|

Uranium concentrate |

| a yellowish to yellow-brownish powder obtained from the chemical processing of uranium-bearing material. Uranium concentrate typically contains 70% to 90% U3O8 by weight. Uranium concentrate is also referred to as “yellowcake.” |

|

|

|

U3O8 |

| a standard chemical formula commonly used to express the natural form of uranium mineralization. U represents uranium and O represents oxygen. U3O8 is contained in “yellowcake” or “uranium concentrate” accounting for 70% to 90% by weight. |

| 6 |

| Table of Contents |

Abbreviations:

AAFS | American Assured Fuel Supply |

ANIA | American Nuclear Infrastructure Act of 2020 |

BLM | U.S. Bureau of Land Management |

CERCLA | Comprehensive Environmental Response and Liability Act |

CIM | Canadian Institute of Mining, Metallurgy and Petroleum |

DDW | Deep Disposal Well |

DEIS | Draft Environmental Impact Statement |

DOC | U.S. Department of Commerce |

DOE | U.S. Department of Energy |

eU3O8 | Equivalent U3O8 as measured by a calibrated gamma instrument |

EIA | U.S. Energy Information Administration |

EMT | East Mineral Trend, located within our LC East Project (Great Divide Basin, Wyoming) |

EPA | U.S. Environmental Protection Agency |

FEIS | Final Environmental Impact Statement |

GDB | Great Divide Basin, Wyoming |

GPM | Gallons per minute |

GT | Grade x Thickness product (% ft.) of a mineral intercept (expressed without units) |

HH | Header house |

IX | Ion Exchange |

ISR | In Situ Recovery (literally, ‘in place’ recovery) (also known as in situ leach or ISL) |

LT | Long-term (as relates to long-term pricing in the uranium market) |

MMT | Main Mineral Trend, located within our Lost Creek Project (Great Divide Basin, Wyoming) |

MU | Mine Unit (also referred to as wellfield) |

NEPA | U.S. National Environmental Policy Act |

NI 43-101 | Canadian National Instrument 43-101 (Standards of Disclosure for Mineral Properties) |

NRC | U.S. Nuclear Regulatory Commission |

PEA | Preliminary Economic Assessment |

PPM | Parts per million |

PPP | Paycheck Protection Program created by the CARES Act (and modified by the Flexibility Act), 2020, administered by the Small Business Administration |

RCRA | Resource Conservation and Recovery Act |

RO | Reverse Osmosis |

RSA | Russian Suspension Agreement (as amended and extended, October 2020, through 2040) |

SBA | U.S. Small Business Administration |

SEC | U.S. Securities Exchange Commission |

U3O8 | A standard chemical formula commonly used to express the natural form of uranium mineralization. U represents uranium and O represents oxygen. |

UIC | Underground Injection Control (pursuant to U.S. Environmental Protection Agency regulations) |

URP | Wyoming Uranium Recovery Program - WDEQ program name for Agreement State Program approved and effective September 30, 2018 |

USFWS | U.S. Fish and Wildlife Service |

WDEQ | Wyoming Department of Environmental Quality (and its various divisions, LQD/Land Quality Division, URP/Uranium Recovery Program; WQD/Water Quality Division; AQD/Air Quality Division; and SHWD/Solid and Hazardous Waste Division) |

WGFD | Wyoming Game and Fish Department |

| 7 |

| Table of Contents |

Metric/Imperial Conversion Table

The imperial equivalents of the metric units of measurement used in this annual report are as follows:

Imperial Measure | Metric Unit | Metric Unit | Imperial Measure |

2.4711 acres | 1 hectare | 0.4047 hectares | 1 acre |

2.2046 pounds | 1 kilogram | 0.4536 kilograms | 1 pound |

0.6214 miles | 1 kilometer | 1.6093 kilometers | 1 mile |

3.2808 feet | 1 meter | 0.3048 meters | 1 foot |

1.1023 short tons | 1 tonne | 0.9072 tonnes | 1 short ton |

0.2642 gallons | 1 litre | 3.785 litres | 1 gallon |

Reporting Currency

All amounts in this report are expressed in United States (U.S.) dollars, unless otherwise indicated. The Financial Statements are presented in accordance with accounting principles generally accepted in the U.S.

| 8 |

| Table of Contents |

PART I

Items 1 and 2. BUSINESS AND PROPERTIES

Overview and Corporate Structure

Incorporated on March 22, 2004, Ur-Energy is an exploration stage mining company, as that term is defined in Securities and Exchange Commission (“SEC”) Industry Guide 7. We are engaged in uranium mining, recovery and processing activities, including the acquisition, exploration, development and operation of uranium mineral properties in the U.S. Through our Wyoming operating subsidiary, Lost Creek ISR, LLC, we began operation of our first in situ recovery uranium mine at our Lost Creek Project in 2013. Ur-Energy is a corporation continued under the Canada Business Corporations Act on August 8, 2006. Our Common Shares are listed on the NYSE American under the symbol “URG” and on the TSX under the symbol “URE.”

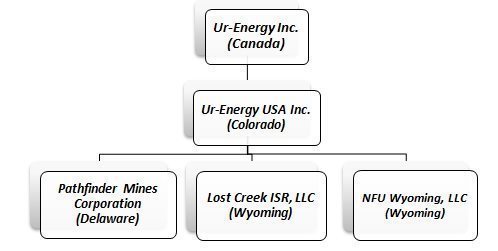

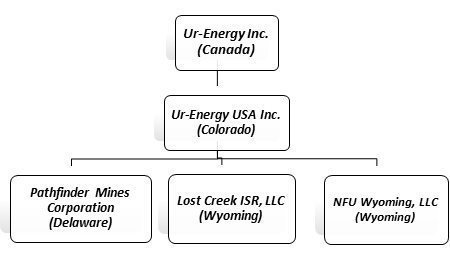

Ur-Energy has one direct wholly-owned subsidiary: Ur-Energy USA Inc. (“Ur-Energy USA”), a company incorporated under the laws of the State of Colorado. It has offices in Colorado and Wyoming and has employees in both states, in addition to having one employee based in Arizona.

Ur-Energy USA has three wholly-owned subsidiaries: NFU Wyoming, LLC (“NFU Wyoming”), a limited liability company formed under the laws of the State of Wyoming which acts as our land holding and exploration entity; Lost Creek ISR, LLC, a limited liability company formed under the laws of the State of Wyoming to hold and operate our Lost Creek Project and certain other of our Lost Creek properties and assets; and Pathfinder Mines Corporation (“Pathfinder”), a company incorporated under the laws of the State of Delaware, which holds, among other assets, the Shirley Basin and Lucky Mc properties in Wyoming. Lost Creek ISR, LLC employs personnel at the Lost Creek Project.

Currently, and at December 31, 2020, our principal direct and indirect subsidiaries, and affiliated entities, and the jurisdictions in which they were incorporated or organized, are as follows:

We are engaged in uranium mining, recovery and processing operations, in addition to the exploration for and development of uranium mineral properties. Uranium fuels carbon-free, emission-free nuclear power which is a clean, cost-effective, and reliable form of electrical power. Nuclear power is estimated to provide more than 50 percent of the carbon-free electricity in the U.S. and approximately one-third of carbon-free electricity worldwide. As a uranium producer, we are allowed to advance the interests of clean energy, thereby addressing global climate change.

Our wholly owned Lost Creek Project in Sweetwater County, Wyoming is our flagship property. The project has been fully permitted and licensed since October 2012. We received operational approval from the U.S. Nuclear Regulatory Commission (“NRC”) and started production operation activities in August 2013. Our first sales of Lost Creek production were made in December 2013.

| 9 |

| Table of Contents |

From commencement of operations until 2020, we had multiple term uranium sales agreements in place with U.S. utilities for the sale of Lost Creek production or other yellowcake product at contracted pricing. We sold 200,000 pounds of Uranium Oxide (“U3O8”) during 2020, at an average price of approximately $42 per pound. In more recent years, we took advantage of the low prices to enter into purchase agreements for delivery into our contractual commitments and, again for 2020, secured such purchase agreements for the 200,000 pounds of U3O8. The average cost of the 2020 purchases was $26 per pound. We completed all commitments into existing term agreements in 2020 Q2.

Our other material asset, Shirley Basin, is one of the assets we acquired as a part of the Pathfinder transaction in 2013. We also acquired all the historic geologic and engineering data for the project. During 2014, we completed a drill program of a limited number of confirmatory holes to complete an NI 43‑101 mineral resource estimate which was released in August 2014; subsequently, an NI 43‑101 Preliminary Economic Assessment for Shirley Basin was completed in January 2015. Baseline studies necessary for the permitting and licensing of the project commenced in 2014 and were completed in 2015.

In December 2015, our application for a permit to mine at Shirley Basin was submitted to the State of Wyoming Department of Environmental Quality (“WDEQ”). WDEQ has completed its technical review of our application for a permit to mine, and the State of Wyoming Uranium Recovery Program (“URP”) review of our application for source material license is also complete. We anticipate the state processes to be complete, with necessary permits and authorizations received, in 2021 H1. The BLM initiated its review of the Plan of Operations in 2019 and we received approval from the BLM in 2020. Work is well underway on initial engineering evaluations, designs and studies.

We utilize in situ recovery (“ISR”) of the uranium at Lost Creek and will do so at other projects where this is possible. The ISR technique is employed in uranium extraction because it allows for a lower cost and effective recovery of roll front mineralization. The in situ technique does not require the installation of tailings facilities or significant surface disturbance. This mining method utilizes injection wells to introduce a mining solution, called lixiviant, into the mineralized zone. The lixiviant is made of natural groundwater fortified with oxygen as an oxidizer, sodium bicarbonate as a complexing agent, and carbon dioxide for pH control. The complexing agent bonds with the uranium to form uranyl carbonate, which is highly soluble. The dissolved uranyl carbonate is then recovered through a series of production wells and piped to a processing plant where the uranyl carbonate is removed from the solution using Ion Exchange (“IX”) and captured on resin contained within the IX columns. The groundwater is re-fortified with the oxidizer and complexing agent and sent back to the wellfield to recover additional uranium. A low-volume bleed is permanently removed from the lixiviant flow. A reverse osmosis (“RO”) process is available to minimize the wastewater stream generated. Brine from the RO process, if used, and bleed are disposed of by means of injection into deep disposal wells. Each wellfield is made up of dozens of injection and production wells installed in patterns to optimize the areal sweep of fluid through the uranium deposit.

Our Lost Creek processing facility includes all circuits for the capture, concentration, drying and packaging of uranium yellowcake for delivery into sales. Our processing facility, in addition to the IX circuit, includes dual processing trains with separate elution, precipitation, filter press and drying circuits (this contrasts with certain other uranium in situ recovery facilities which operate as a capture plant only, and rely on agreements with other producers for the finishing, drying and packaging of their yellowcake end-product). Additionally, a restoration circuit including an RO unit was installed during initial construction to complete groundwater restoration once mining is complete. A pre-IX filtration and wastewater treatment facility is being contemplated and lab tested to further enhance the ion exchange effectiveness as well as reduce final wastewater volumes. The system, as currently planned, will allow for more effective use of current and future deep disposal wells working in conjunction with the Class V water recycling system.

| 10 |

| Table of Contents |

The elution circuit (the first step after ion exchange) is utilized to transfer the uranium from the IX resin and concentrate it to the point where it is ready for the next phase of processing. The resulting rich eluate is an aqueous solution containing uranyl carbonate, salt and sodium carbonate and/or sodium bicarbonate. The precipitation circuit follows the elution circuit and removes the carbonate from the concentrated uranium solution and combines the uranium with peroxide to create a yellowcake crystal slurry. Filtration and washing is the next step, in which the slurry is loaded into a filter press where excess contaminants such as chloride are removed and a large portion of the water is removed. The final stage occurs when the dewatered slurry is moved to a yellowcake dryer, which will further reduce the moisture content, yielding the final dried, free-flowing, product. Refined, salable yellowcake is packaged in 55-gallon steel drums.

The restoration circuit may be utilized in the production as well as the post-mining phases of the operation. The RO is being utilized as a part of our Class V recycling circuit to minimize the wastewater stream generated during production. Once production is complete, the groundwater must be restored to its pre-mining class of use or better. The first step of restoration involves removing a small portion of the groundwater and disposing of it (commonly known as sweep). Following sweep, the groundwater is treated utilizing RO and re-injecting the clean water. Finally, the groundwater is homogenized and sampled to ensure the cleanup is complete, concluding the mining process.

Our Lost Creek processing facility was constructed in 2012 – 2013, with production operations commencing in August 2013. Our first sales were made in December 2013. Nameplate design and NRC-licensed capacity of our Lost Creek processing plant is two million pounds per year, of which approximately one million pounds per year may be produced from our wellfields. The Lost Creek plant and the allocation of resources to mine units and resource areas were designed to generate approximately one million pounds of production per year at certain flow rates and uranium concentrations subject to regulatory and license conditions. The excess capacity in the design of the processing circuits of the plant is intended, first, to facilitate routine (and, non-routine) maintenance on any particular circuit without hindering production operational schedules. The capacity was also designed to permit us to process uranium from other mineral projects in proximity to Lost Creek if circumstances warrant in the future (e.g., Shirley Basin Project) or, alternatively, to be able to contract to toll mill/process product from other in situ uranium mine sites in the region. The design permits us to conduct either of these activities while Lost Creek is producing and processing uranium and/or in years following Lost Creek production from wellfields during final restoration activities.

Our Lost Creek processing facility includes all circuits for the production, drying and packaging of uranium yellowcake for delivery into sales. As contemplated in the Preliminary Economic Assessment of Shirley Basin, we expect that the Lost Creek processing facility may be utilized for the drying and packaging of uranium from Shirley Basin, for which we currently anticipate the need only for a satellite plant. However, the Shirley Basin permit application contemplates the construction of a full processing facility, providing greater construction and operating flexibility as may be dictated by market conditions.

| 11 |

| Table of Contents |

Our Mineral Properties

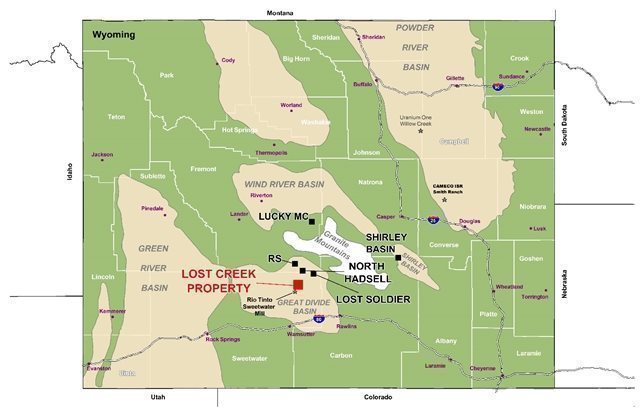

Our current land portfolio in Wyoming includes 12 projects. Ten of these projects are in the Great Divide Basin, Wyoming, including our flagship project, Lost Creek Project, which began production operations in August 2013. Currently we control nearly 1,800 unpatented mining claims and three State of Wyoming mineral leases for a total of approximately 36,000 acres (~15,500 hectares) at our Lost Creek Property, including the Lost Creek permit area (the “Lost Creek Project” or “Lost Creek”) and certain adjoining properties which we refer to as LC East, LC West, LC North, LC South and EN project areas (collectively, with the Lost Creek Project, the “Lost Creek Property”). Five of the projects at the Lost Creek Property contain NI 43‑101 compliant mineral resources: Lost Creek, LC East, LC West, LC South and LC North. See Resource Summary below in Updated Preliminary Economic Assessment for Lost Creek Property. Below is a map showing our Wyoming projects and the geologic basins in which they are located.

Our Wyoming properties together total approximately 48,000 acres (approximately 19,425 hectares) and include two properties, Shirley Basin and Lucky Mc, obtained through our 2013 acquisition of Pathfinder Mines Corporation. Our Pathfinder acquisition also included a significant exploration and development database compiled by Pathfinder over several decades.

Our first gold exploration project (Excel Project) is located in west-central Nevada, and currently comprises 114 federal lode mining claims (approximately 2,600 acres). The project is located within the Excelsior Mountains, in proximity to the Camp Douglas and Candelaria Mining Districts. We identified the mineral potential of this project area from exploration data acquired through our purchase of Pathfinder. Historic exploration programs conducted by Pathfinder in the area of the Excel Project encountered high-grade gold and silver assays. Our initial land acquisition activities were complete in 2018, after which rock sampling and geochemical soil sampling programs were conducted. Since securing the land position, we have conducted additional work at the project on a time-to-time basis. Plans for the project for 2021 are not yet established.

| 12 |

| Table of Contents |

Operating Properties

Lost Creek Project – Great Divide Basin, Wyoming

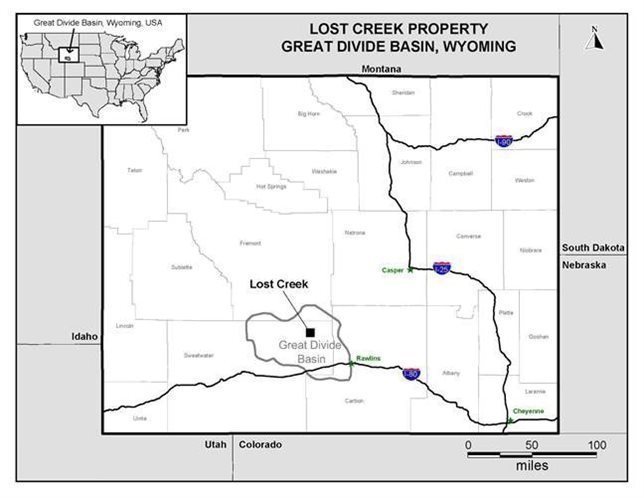

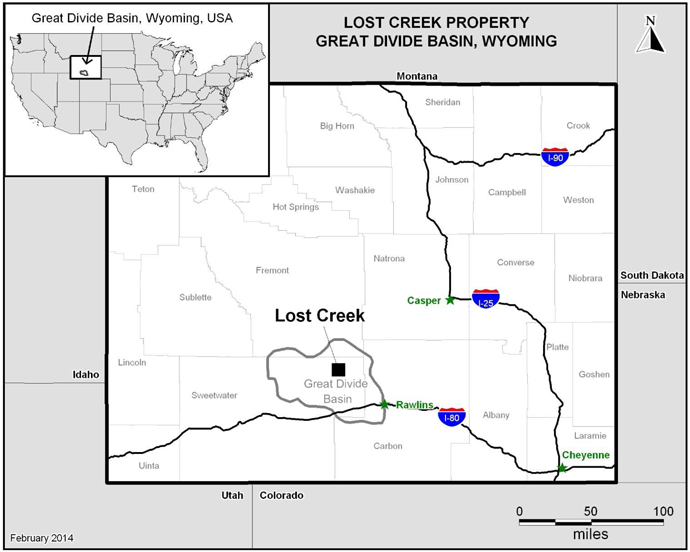

We acquired the Lost Creek Project area in 2005. Lost Creek is located in the Great Divide Basin (“GDB”), Wyoming. The Main Mineral Trend of the Lost Creek uranium deposit (the “MMT”) is located within the Lost Creek Project. The permit area of the Lost Creek Project covers 4,254 acres (1,722 hectares), comprising 201 lode mining claims and one State of Wyoming mineral lease section. Regional access relies almost exclusively on existing public roads and highways. The local and regional transportation network consists of primary, secondary, local and unimproved roads. Direct access to Lost Creek is mainly on two crown-and-ditched gravel paved access roads to the processing plant. One road enters from the west from Sweetwater County Road 23N (Wamsutter-Crooks Gap Road); the other enters from the east off of U.S. Bureau of Land Management (“BLM”) Sooner Road. On a wider basis, from population centers, the Lost Creek property area is served by an Interstate Highway (Interstate 80), a US Highway (US 287), Wyoming state routes (SR 220 and 73 to Bairoil), local county roads, and BLM roads. The Lost Creek Property is located as shown here:

The basic infrastructure (power, water, and transportation) necessary to support our ISR operation is located within reasonable proximity. Generally, the proximity of Lost Creek to paved roads is beneficial with respect to transportation of equipment, supplies, personnel and product to and from the property. Existing regional overhead electrical service is aligned in a north-to-south direction along the western boundary of the Lost Creek Project. An overhead power line, approximately two miles in length, was constructed to bring power from the existing Pacific Power line to the Lost Creek plant. Power drops have been made to the property and distributed to the plant, offices, wellfields, and other facilities. Additional power drops will be installed as we expand the wellfield operations.

| 13 |

| Table of Contents |

There are no royalties at the Lost Creek Project, except the royalty on the State of Wyoming section mineral lease as provided by law. Currently, there is only limited production planned from the State lease section. There is a production royalty of one percent on certain claims of the LC East Project, and other royalties on other claims within the other adjoining projects (LC South and EN projects) as well as the other State sections on which we maintain mineral leases (LC West and EN projects).

Production Operations

Following receipt of the final regulatory authorization in October 2012, we commenced construction at Lost Creek. Construction included the plant facility and office building, installation of all process equipment, installation of two access roads, additional power lines and drop lines, deep disposal wells, construction of two holding ponds, warehouse building, and drill shed building. In August 2013 we were given operational approval by the NRC and commenced production operation activities. See also discussion of the operational methods used at Lost Creek, above, under heading “Business and Properties.”

For the Lost Creek PEA, in order to accurately reflect existing resources, all resources produced through September 30, 2015 (1,358,407 pounds) were subtracted from total Measured Resources from the HJ Horizon in Mine Unit 1 (“MU1”). All the wells to support the originally planned 13 header houses (“HHs”) have been completed. HHs 1-1 through 1-11 were operational as of the effective date of the Lost Creek PEA, October 15, 2015. Subsequently, the last two of the originally planned header houses in MU1 were brought online.

All monitor ring wells in Mine Unit 2 (“MU2”) have been installed, pump-tested and approved for operational use. As of October 15, 2015, the effective date for the Lost Creek PEA, 138 pattern wells were piloted within HHs 2-1, 2-2 and 2-3. In a limited development program in 2018, the wells previously piloted were completed for use and HHs 2-2 and 2-3 were constructed. HH 2-2 was brought into operation in August 2017, HH 2‑3 started in January 2018 and HH 2-1 was brought online in May 2018. No further development work has been conducted at Lost Creek, since HH 2-1 came online.

We began 2020 with continued, controlled production at market appropriate reduced levels. In Q3, we further reduced production operations at Lost Creek. For the year, 10,789 pounds of U3O8 were captured within the Lost Creek plant and 15,873 pounds U3O8 were packaged in drums.

2016 Preliminary Economic Assessment for Lost Creek Property

In 2016, we issued a Preliminary Economic Assessment for the Lost Creek Property Sweetwater County Wyoming, as amended (February 8, 2016 (TREC, Inc.)) (the “Lost Creek PEA”). The Lost Creek PEA was prepared for the Company and its subsidiary, Lost Creek ISR, LLC, by Douglass H. Graves, P.E., TREC, Inc. (“TREC”) and James A. Bonner, P.Geo., in accordance with NI 43-101.

According to the Lost Creek PEA, the mineral resources at the Lost Creek Property at the date of the report were as follows:

| 14 |

| Table of Contents |

Lost Creek Property - Resource Summary

|

| MEASURED |

|

| INDICATED |

|

| INFERRED |

| |||||||||||||||||||||||||||

PROJECT |

| AVG GRADE |

|

| SHORT TONS |

|

| POUNDS |

|

| AVG GRADE |

|

| SHORT TONS |

|

| POUNDS |

|

| AVG GRADE |

|

| SHORT TONS |

|

| POUNDS |

| |||||||||

|

| % eU3O8 |

|

| (X 1000) |

|

| (X 1000) |

|

| % eU3O8 |

|

| (X 1000) |

|

| (X 1000) |

|

| % eU3O8 |

|

| (X 1000) |

|

| (X 1000) |

| |||||||||

LOST CREEK |

|

| 0.048 |

|

|

| 8,339 |

|

|

| 7,937 |

|

|

| 0.046 |

|

|

| 3,831 |

|

|

| 3,491 |

|

|

| 0.046 |

|

|

| 3,116 |

|

|

| 2,844 |

|

MU1 production through 9/30/15 |

|

| (0.048 | ) |

|

| (1,415 | ) |

|

| (1,358 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LC EAST |

|

| 0.052 |

|

|

| 1,392 |

|

|

| 1,449 |

|

|

| 0.041 |

|

|

| 1,891 |

|

|

| 1,567 |

|

|

| 0.042 |

|

|

| 2,954 |

|

|

| 2,484 |

|

LC NORTH |

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

|

| 0.045 |

|

|

| 645 |

|

|

| 581 |

| ||||||

LC SOUTH |

| — |

|

| — |

|

| — |

|

|

| 0.037 |

|

|

| 220 |

|

|

| 165 |

|

|

| 0.039 |

|

|

| 637 |

|

|

| 496 |

| |||

LC WEST |

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

|

| 0.109 |

|

|

| 16 |

|

|

| 34 |

| ||||||

EN |

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

| |||||||||

GRAND TOTAL |

|

| 0.048 |

|

|

| 8,316 |

|

|

| 8,028 |

|

|

| 0.044 |

|

|

| 5,942 |

|

|

| 5,223 |

|

|

| 0.044 |

|

|

| 7,368 |

|

|

| 6,439 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| MEASURED + INDICATED = |

|

| 14,258 |

|

|

| 13,251 |

|

|

|

|

|

|

|

|

|

| |||||||||||||

Notes:

1. | Sum of Measured and Indicated tons and pounds may not add to the reported total due to rounding. |

|

|

2. | % eU3O8 is a measure of gamma intensity from a decay product of uranium and is not a direct measurement of uranium. Numerous comparisons of eU3O8 and chemical assays of Lost Creek rock samples, as well as PFN logging, indicate that eU3O8 is a reasonable indicator of the chemical concentration of uranium. |

|

|

3. | Table shows resources based on grade cutoff of 0.02 % eU3O8 and a grade x thickness cutoff of 0.20 GT. |

|

|

4. | Measured, Indicated, and Inferred Mineral Resources as defined in Section 1.2 of NI 43-101 (the CIM Definition Standards (CIM Council, 2015)). |

|

|

5. | Resources are reported through October 15, 2015. |

|

|

6. | All reported resources occur below the static water table. |

|

|

7. | 1,358,407 lbs. of uranium have been produced from the HJ Horizon in MU1 (Lost Creek Project) as of September 30, 2015. |

|

|

8. | Mineral resources that are not mineral reserves do not have demonstrated economic viability. |

Information shown in the table above differs from the disclosure requirements of the SEC. See Cautionary Note to U.S. Investors Concerning Disclosure of Mineral Resources, above.

The Lost Creek PEA discloses changes for the Lost Creek Property which come in the form of an updated mineral resource estimate prompted by drilling within Lost Creek’s MU2, exploratory drilling at the Lost Creek and LC East Projects, and the re-estimation of all previously-identified resources for the Property at a revised 0.20 grade-thickness (GT) cut-off. The economic analyses within the Lost Creek PEA were revised to evaluate the impact of additional identified resources with information and data acquired through two years of ISR operations at Lost Creek. The Lost Creek PEA therefore replaced the last economic analyses for the Lost Creek Property (December 2013) and the NI 43-101 Technical Report on the Lost Creek Property, dated June 17, 2015 (the “2015 Technical Report”). The Lost Creek PEA covers production through September 30, 2015 and drilling and other exploration and operational activities conducted through October 15, 2015.

| 15 |

| Table of Contents |

We published the 2015 Technical Report for the Lost Creek Property to report increased resources for its operating MU1 and from exploration drilling conducted early in 2015. In order to reconcile higher-than-expected uranium recoveries from production operations in this mine unit, various analyses were conducted. These analyses, including detailed remapping of mineralized trends within ten sand horizons and interpretation of data from an additional 85 closely-spaced wells and core-holes, resulted in the re-estimation of the mineral resources and the conclusion that it was most appropriate to lower the grade-thickness (“GT”) cut-offs from 0.30 to 0.20 within our GT contouring resource estimation technique. Employing these revised guidelines, resources for MU1 were re-mapped and re-evaluated, increasing the MU1 Measured Resources by 55% (after subtraction of MU1 production). Through the monitoring of continued production from MU1, the authors believe the 0.20 GT cutoff better represents the uranium resources for the Lost Creek Property and is supported by the economic analysis included in the PEA as well as the actual production achieved at the property to the cut-off date of the PEA. Accordingly, for the Lost Creek PEA, all resource estimations for Lost Creek Property have used the new 0.20 GT cutoff, again, following re-mapping and re-evaluation. Between the 2015 Technical Report and the Lost Creek PEA’s publication, our activities resulted in a cumulative increase of mineral resources at the Lost Creek Property of 31% in the Measured and Indicated categories and 28% in the Inferred category as was then reported in the Lost Creek PEA.

The Lost Creek Property includes six individual contiguous Projects: Lost Creek Project, LC East Project, LC West Project, LC North Project, LC South Project and EN Project. The fully-licensed and operating Lost Creek Project is considered the core project while the others are collectively referred to as the Adjoining Projects in the Lost Creek PEA. The Adjoining Projects were acquired by the Company as exploration targets to provide resources supplemental to those recognized at the Lost Creek Project. Most were initially viewed as stand-alone projects but expanded over time such that, collectively, they represent a contiguous block of land along with the Lost Creek Project.

The Lost Creek PEA mineral resource estimate includes drill data and analyses of approximately 3,200 historic and current holes and over 1.8 million feet of drilling at the Lost Creek Project alone. With the acquisition of the Lost Creek Project, we acquired logs and analyses from 569 historic holes representing 366,268 feet of data. Since our acquisition of the project, and until the October 15, 2015 drill data cut-off for the PEA, 2,629 holes and wells were drilled, including the construction and development drilling during 2013-2015 for MU1 and initial work in MU2 at Lost Creek. Additionally, drilling from the other five projects at the Lost Creek Property, both historic and our drill programs, is included in the mineral resource estimate. Collectively, this represents an additional 2,387 drill holes (1,306,331 feet).

The Lost Creek PEA is the first technical report prepared since production began at Lost Creek which includes an updated preliminary economic assessment. It reflects production from August 3, 2013 to September 30, 2015 and subtracts that amount (1,358,407 pounds) when summing the Measured Resources.

Based upon the Lost Creek PEA, since September 30, 2015 up through December 31, 2020, another 1,376,022 pounds U3O8 have been produced. Total production from MU1 and MU2, through December 31, 2020, equaled 2,734,393 pounds U3O8 and the remaining Lost Creek PEA resources following that production are as follows:

12/31/20 Reconciliation of Lost Creek Property Resource Estimate |

| MEASURED |

|

| INDICATED |

|

| INFERRED |

| |||||||||||||||||||||||||||

PROJECT |

| AVG GRADE |

|

| SHORT TONS |

|

| POUNDS |

|

| AVG GRADE |

|

| SHORT TONS |

|

| POUNDS |

|

| AVG GRADE |

|

| SHORT TONS |

|

| POUNDS |

| |||||||||

|

| % eU3O8 |

|

| (X 1000) |

|

| (X 1000) |

|

| % eU3O8 |

|

| (X 1000) |

|

| (X 1000) |

|

| % eU3O8 |

|

| (X 1000) |

|

| (X 1000) |

| |||||||||

LOST CREEK |

|

| 0.048 |

|

|

| 8,339 |

|

|

| 7,937 |

|

|

| 0.046 |

|

|

| 3,831 |

|

|

| 3,491 |

|

|

| 0.046 |

|

|

| 3,116 |

|

|

| 2,844 |

|

LC production through 12/31/20 |

|

| -0.048 |

|

|

| -2,834 |

|

|

| -2,734 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lost Creek Subtotal at 12/31/20 |

|

| 0.048 |

|

|

| 5,505 |

|

|

| 5,203 |

|

|

| 0.046 |

|

|

| 3,831 |

|

|

| 3,491 |

|

|

| 0.046 |

|

|

| 3,116 |

|

|

| 2,844 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LC EAST |

|

| 0.052 |

|

|

| 1,392 |

|

|

| 1,449 |

|

|

| 0.041 |

|

|

| 1,891 |

|

|

| 1,567 |

|

|

| 0.042 |

|

|

| 2,954 |

|

|

| 2,484 |

|

LC NORTH |

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

|

| 0.045 |

|

|

| 645 |

|

|

| 581 |

| ||||||

LC SOUTH |

| — |

|

| — |

|

| — |

|

|

| 0.037 |

|

|

| 220 |

|

|

| 165 |

|

|

| 0.039 |

|

|

| 637 |

|

|

| 496 |

| |||

LC WEST |

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

|

| 0.109 |

|

|

| 16 |

|

|

| 34 |

| ||||||

EN |

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

| |||||||||

Grand Total at 12/31/20 |

|

| 0.048 |

|

|

| 6,897 |

|

|

| 6,652 |

|

|

| 0.044 |

|

|

| 5,943 |

|

|

| 5,223 |

|

|

| 0.044 |

|

|

| 7,368 |

|

|

| 6,440 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| MEASURED + INDICATED = |

|

|

| 0.046 |

|

|

| 12,840 |

|

|

| 11,875 |

|

|

|

|

|

|

| |||||||||||||||

| 16 |

| Table of Contents |

Since the date of the Lost Creek PEA, no additional exploration drilling has been conducted on the Lost Creek Property. As expected, development drilling for the initial MU2 construction at Lost Creek in 2017 did not result in the identification of significant additional mineral resources and no additional drilling has been conducted since that time. Absent a significant change in the uranium markets to warrant further development, no additional exploration or development drilling is now planned at the Lost Creek Property for 2021. If a ramp-up in production operations is warranted, development and construction will be a priority, with exploration activities to follow when appropriate.

Regulatory Authorizations and Land Title of Lost Creek

Beginning in 2007, we completed all necessary applications and related processes to obtain the required permitting and licenses for the Lost Creek Project, of which the three most significant are: a Source and Byproduct Materials License from the NRC (received August 2011); a Plan of Operations with the BLM (Record of Decision (“ROD”)) received October 2012; and a Permit and License to Mine from the WDEQ (October 2011). The WDEQ Permit includes the approval of the first mine unit, as well as the Wildlife Management Plan, including a positive determination of the protective measures at the project for the greater sage-grouse species.

Potential risks to the accessibility of the estimated mineral resource may include changes in the designation of the sage grouse as an endangered species by the USFWS because the Lost Creek Property lies within a sage grouse core area as defined by the state of Wyoming. In 2015, the USFWS issued its finding that the greater sage grouse does not warrant protection under the Endangered Species Act (ESA). The USFWS reached this determination after evaluating the species’ population status, along with the collective efforts by the BLM and U.S. Forest Service, state agencies, private landowners and other partners to conserve its habitat.

After a thorough analysis of the best available scientific information and considering ongoing key conservation efforts and their projected benefits, the USFWS determined the species does not face the risk of extinction now or in the foreseeable future and therefore does not need protection under the ESA. Should future decisions vary, or state or federal agencies alter their management of the species, there could potentially be an impact on future expansion operations. However, the Company continues to work closely with the Wyoming Game and Fish Department (“WGFD”) and the BLM to mitigate impacts to the sage grouse.

The State of Wyoming has developed a “core-area strategy” to help protect the greater sage-grouse species within certain core areas of the state. The Lost Creek property is within a designated core area and is thus subject to work activity restrictions from March 1 to July 15 of each year. The timing restriction precludes exploration drilling and other non-operational based activities which may disturb the sage-grouse. The sage-grouse timing restrictions relevant to ISR production and operational activities at the Lost Creek Project are somewhat different because the State has recognized that mining projects within core areas must be allowed to operate year-round. As a result, there are no timing restrictions on operational activities in pre-approved disturbed areas within our permit to mine.

Meanwhile, in related regulatory processes, the BLM prepared and issued environmental impact statements for and issued amendments to eleven Resource Management Plans (“RMPs”), related to the greater sage-grouse, which have subsequently been amended from time to time. In 2017, the BLM cancelled the land withdrawal program. Aspects of the RMPs have been or are being litigated, including the land withdrawal decision which has recently been remanded by the courts to the BLM for further consideration and NEPA review.

| 17 |

| Table of Contents |

Additional authorizations from federal, state and local agencies for the Lost Creek project include: WDEQ-Air Quality Division Air Quality Permit and WDEQ-Water Quality Division Class I Underground Injection Control (“UIC”) Permit. Following the plugging of one of our deep disposal wells in 2019, the UIC permit allows Lost Creek to operate up to four Class I injection wells to meet the anticipated disposal requirements for the life of the Lost Creek Project. The Environmental Protection Agency (“EPA”) issued an aquifer exemption for the Lost Creek project. The WDEQ’s separate approval of the aquifer reclassification is a part of the WDEQ Permit. We also received approval from the EPA and the Wyoming State Engineer’s Office for the construction and operation of two holding ponds at Lost Creek.

In 2014, applications for amendments to the primary authorizations to mine at Lost Creek were submitted to federal regulatory agencies, NRC and BLM, for the development and mining of the LC East Project. In 2015, the BLM issued a notice of intent to complete an environmental impact statement for the application. The NRC participated in this review as a cooperating agency. The BLM published a Final Environmental Impact Statement (“FEIS”) on the amendment application in January 2019 and, in February 2019, a related ROD authorizing the plan. A permit amendment requesting approval to mine at the LC East Project was also submitted to the WDEQ. Approval will include an aquifer exemption. The air quality permit for Lost Creek will be revised to account for additional surface disturbance. Certain of our earlier Sweetwater County approvals will be amended. Numerous well permits from the State Engineer’s Office will be required. It is anticipated that all remaining permits and authorizations will be completed in 2021. See also Lost Creek Regulatory Proceedings, in Management Discussion and Analysis, below.

During 2016, we received all authorizations for the operation of Underground Injection Control (UIC) Class V wells at Lost Creek, and operation of the circuit began in early 2017. This allows for the onsite reinjection of fresh permeate (i.e., clean water) into relatively shallow Class V wells. Site operators use the RO circuits, which were installed during initial construction of the plant, to treat process wastewater into brine and permeate streams. The brine stream continues to be disposed of in the UIC Class I deep wells while the clean, permeate stream is injected into the UIC Class V wells after treatment for radium. These operational procedures continue to significantly enhance wastewater capacity at the site, ultimately reducing the injection requirements of our Class I deep disposal wells and extending the life of those valuable assets.

In September 2018, Wyoming assumed responsibility from the NRC for the regulation of radiation safety at uranium recovery facilities like Lost Creek. The Wyoming State Uranium Recovery Program (“URP”), a part of the WDEQ, oversees the licensing process for source material licenses as well as the operations of licensees in Wyoming. The URP has demonstrated that its integration into the overall WDEQ oversight of uranium recovery streamlines the process of licensing, offer greater consistency in authorizations and oversight, and results in reduced costs in the licensing phase. We anticipate that the URP will issue our Source Material License for LC East in 2021.

Through certain of our subsidiaries, we control the federal unpatented lode mining claims and State of Wyoming mineral leases which make up the Lost Creek Property. Title to the mining claims is subject to rights of pedis possessio against all third-party claimants as long as the claims are maintained. The mining claims do not have an expiration date. Affidavits have been timely filed with the BLM and recorded with the Sweetwater County Recorder attesting to the payment for the Lost Creek Property mining claims of annual maintenance fees to the BLM as established by law from time to time. The state leases have a ten-year term, subject to renewal for successive ten-year terms.

The surface of all the mining claims is controlled by the BLM, and we have the right to use as much of the surface as is necessary for exploration and mining of the claims, subject to compliance with all federal, state and local laws and regulations. Surface use on BLM lands is administered under federal regulations. Similarly, access to state-controlled land is largely inherent within a State of Wyoming mineral lease. The state lease at the Lost Creek Project requires a nominal surface impact fee to be paid. The other state mineral leases currently do not have surface impact payment obligations.

| 18 |

| Table of Contents |

Exploration and Development Properties

Together with the Lost Creek Project, Five Adjoining Projects Form the Lost Creek Property

The LC East and LC West Projects (currently, approximately 5,710 acres (2,310 hectares) and 3,840 acres (1,554 hectares), respectively) were added to the Lost Creek Property in 2012. In 2012, all baseline studies at LC East were initiated. As discussed above, in 2014, we submitted applications for amendments of the Lost Creek licenses and permits to include development of LC East. We also located additional lode mining claims to secure the lands in what will be the LC East permit area. The East Mineral Trend (the “EMT”) is a second mineral trend of significance, in addition to the MMT at Lost Creek, identified by historic drilling on the lands forming LC East. Although geologically similar, it appears to be a separate and independent trend from the MMT. The Lost Creek PEA contains a recommendation that delineation drilling of identified resources in the EMT continue, together with progressing all necessary permit and license amendments to permit future production.

The LC North Project (approximately 6,200 acres (2,500 hectares)) is located to the north and to the west of the Lost Creek Project. Historical wide-spaced exploration drilling on this project consisted of 175 drill holes. We have conducted two drilling programs at the project. We may conduct exploration drilling at LC North in the future to pursue the potential of an extension of the MMT in the HJ and KM horizons.

The LC South Project (approximately 10,125 acres (4,100 hectares)) is located to the south and southeast of the Lost Creek Project. Historical drilling on the LC South Project consisted of 488 drill holes. In 2010, we drilled 159 exploration holes (total, 101,270 feet (30,867 meters)) which confirmed numerous individual roll front systems occurring within several stratigraphic horizons correlative to mineralized horizons in the Lost Creek Project. Also, a series of wide-spaced drill holes were part of this exploration program which identified deep oxidation (alteration) that represents the potential for several additional roll front horizons. In the future, we may conduct additional drilling to further evaluate the potential of deeper mineralization.

The EN Project (approximately 5,475 acres (2,200 hectares)) is adjacent to and east of LC South. We have over 50 historical drill logs from the EN project. Some minimal, deep, exploration drilling has been conducted at the project. Although no mineral resource is yet reported due to the limited nature of the data, we may in the future explore this area further with wide-spaced framework drilling to assess regional alteration and stratigraphic relationships. In an effort to contain costs, in recent years we have reduced the number of federal mining claims and state mineral leases held at the EN project.

History and Geology of the Lost Creek Property

Uranium was discovered in the Great Divide Basin, where Lost Creek is located, in 1936. Exploration activity increased in Wyoming in the early 1950s after the Gas Hills District discoveries, and continued to increase in the 1960s, with the discovery of numerous additional occurrences of uranium. Wolf Land and Exploration (which later became Inexco), Climax (Amax) and Conoco Minerals were the earliest operators in the Lost Creek area and made the initial discoveries of low-grade uranium mineralization in 1968. Kerr-McGee, Humble Oil, and Valley Development, Inc. were also active in the area. Drilling within the current Lost Creek Project area from 1966 to 1976 consisted of approximately 115 wide-spaced exploration holes by several companies including Conoco, Climax (Amax), and Inexco.

Texasgulf acquired the western half of what is now the Lost Creek Project in 1976 through a joint venture with Climax and identified what is now referred to as the Main Mineral Trend (MMT). In 1978, Texasgulf optioned into a 50% interest in the adjoining Conoco ground to the east and continued drilling, fully identifying the MMT eastward to the current Project boundary; Texasgulf drilled approximately 412 exploration holes within what is now the Lost Creek Project. During this period Minerals Exploration Company (a subsidiary of Union Oil Company of California) drilled approximately eight exploration holes in what is currently the western portion of the Lost Creek Project. Texasgulf dropped the project in 1983 due to declining market conditions. The ground was subsequently picked up by Cherokee Exploration, Inc. which conducted no field activities.

| 19 |

| Table of Contents |

In 1987, Power Nuclear Corporation (also known as PNC Exploration) acquired 100% interest in the project from Cherokee Exploration, Inc. PNC Exploration conducted a limited exploration program and geologic investigation, as well as an evaluation of previous in situ leach testing by Texasgulf. PNC Exploration drilled a total of 36 holes within the current Project area.

In 2000, New Frontiers Uranium, LLC acquired the property and database from PNC Exploration, but conducted no drilling or geologic studies. New Frontiers Uranium, LLC later transferred the Lost Creek Project-area property along with its other Wyoming properties to its successor NFU Wyoming, LLC. In June 2005, Ur‑Energy USA purchased 100% ownership of NFU Wyoming, LLC.

The Lost Creek Property is situated in the northeastern part of the GDB which is underlain by up to 25,000 ft. of Paleozoic to Quaternary sediments. The GDB lies within a unique divergence of the Continental Divide and is bounded by structural uplifts or fault displaced Precambrian rocks, resulting in internal drainage and an independent hydrogeologic system. The surficial geology in the GDB is dominated by the Battle Spring Formation of Eocene age. The dominant lithology in the Battle Spring Formation is coarse arkosic sandstone, interbedded with intermittent mudstone, claystone and siltstone. Deposition occurred as alluvial-fluvial fan deposits within a south-southwest flowing paleodrainage. The sedimentary source is considered to be the Granite Mountains, approximately 30 miles to the north. Maximum thickness of the Battle Spring Formation sediments within the GDB is 6,000 ft.

Uranium deposits in the GDB are found principally in the Battle Spring Formation, which hosts the Lost Creek Project deposit. Lithology within the Lost Creek deposit consists of approximately 60% to 80% poorly consolidated, medium to coarse arkosic sands up to 50 ft. thick, and 20% to 40% interbedded mudstone, siltstone, claystone and fine sandstone, each generally less than 25 ft. thick. This lithological assemblage remains consistent throughout the entire vertical section of interest in the Battle Spring Formation.

Outcrop at Lost Creek is exclusively that of the Battle Spring Formation. Due to the soft nature of the formation, the Battle Spring Formation occurs largely as sub-crop beneath the soil. The alluvial fan origin of the formation yields a complex stratigraphic regime which has been subdivided throughout Lost Creek into several thick horizons dominated by sands, with intervening named mudstones. Lost Creek is currently licensed and permitted to produce from the HJ horizon. The LC East permit and license amendments will include authorizations to recover uranium from the HJ and KM horizons.

We occasionally perform leach testing on various samples from the Lost Creek Project. Most recently, in 2010, we performed leach testing on samples from the KM Horizon of the Lost Creek Project. Seven samples obtained from one-foot sections of core were tested for mineral recovery using the same test methods as in prior tests from the HJ Horizon (currently licensed for production at Lost Creek, and being recovered in MU1). Twenty-five pore volumes of various bicarbonate leach solutions were passed through the samples. Uranium recovery ranged from 54.1 to 93.0% with an average uranium recovery of 80.6%. These results are similar to earlier leaching and recovery tests conducted on behalf of the Company on samples from the HJ Horizon, which returned results consistently averaging 82 – 83%. We believe these results are consistent with industry experience.

| 20 |

| Table of Contents |

Pathfinder Mines Corporation: Shirley Basin Mine Site (Shirley Basin, Wyoming) and Lucky Mc Mine Site (Gas Hills Mine District, Wyoming)

As a result of the Pathfinder acquisition, we now own the Shirley Basin and Lucky Mc mine sites in the Shirley Basin and Gas Hills mining districts of Wyoming, respectively, from which Pathfinder and its predecessors historically produced more than seventy-one million pounds of uranium, primarily from the 1960s through the 1990s. Pathfinder’s predecessors included COGEMA, Lucky Mc Uranium Corporation, and Utah Construction/Utah International.

Both Lucky Mc and Shirley Basin conventional mine operations were suspended in the 1990s due to low uranium pricing, and facility reclamation was substantially completed. We assumed the remaining reclamation responsibilities, including financial surety for reclamation, at Shirley Basin and at the Lucky Mc mine site. The Lucky Mc tailings site was fully reclaimed and, at the time of our acquisition, was in the process of being transferred to the U.S. Department of Energy. Therefore, we assumed no obligations with respect to the Lucky Mc tailings site, which were retained by the seller upon closing, or the NRC license at the site.

Together with property holdings of patented lands, unpatented mining claims, and State of Wyoming and private leases totalling more than 5,500 acres (nearly 3,700 acres at Shirley Basin (~1,500 hectares); approximately 1,800 at Lucky Mc (~750 hectares)), we also acquired all historic geologic, engineering and operational data related to the two mine areas.

As with the Lost Creek mining claims, title to the mining claims at Shirley Basin and Luck Mc is subject to rights of pedis possessio against all third-party claimants as long as the claims are maintained. The mining claims do not have an expiration date. Affidavits have been timely filed with the BLM and recorded with the Carbon and Fremont County Recorders attesting to the payment for the mining claims of annual maintenance fees to the BLM as established by law from time to time. The surface of all the unpatented mining claims is controlled by the BLM, and we have the right to use as much of the surface as is necessary for exploration and mining of the claims, subject to compliance with all federal, state and local laws and regulations. Surface use on BLM lands is administered under federal regulations.

Our project in the Shirley Basin (the “Shirley Basin Project”) is in Carbon County, Wyoming, approximately 40 miles south of Casper, Wyoming. The project is accessed by travelling west from Casper, on Highway 220. After travelling 18 miles, turn south on Highway 487 and travel an additional 35 miles; the entrance to Shirley Basin Mine is to the east.

In addition to the two projects and related data, we acquired an extensive U.S. exploration and development database estimated to comprise hundreds of project descriptions in more than 20 states, including thousands of drill logs and geologic reports. Our geology staff continues with its evaluation of this database, assessing opportunities to monetize this additional asset.

The tailings facility at the Shirley Basin site is one of the few remaining facilities in the U.S. that is licensed by the NRC to receive and dispose of byproduct waste material from other in situ uranium mines. We assumed the operation of the byproduct disposal site in 2013 and have accepted deliveries since then under several existing contracts.

| 21 |

| Table of Contents |

Preliminary Economic Assessment for Shirley Basin Uranium Project

In 2015, we issued a Preliminary Economic Assessment for the Shirley Basin Uranium Project Carbon County Wyoming, January 27, 2015 (the “Shirley Basin PEA”). The Shirley Basin PEA was prepared under the supervision of WWC Engineering. The current mineral resources at the Shirley Basin Project are estimated as follows:

Shirley Basin Uranium Project - Resource Summary

|

| MEASURED |

|

| INDICATED |

| ||||||||||||||||||

RESOURCE |

| AVG GRADE |

|

| SHORT TONS |

|

| POUNDS |

|

| AVG GRADE |

|

| SHORT TONS |

|

| POUNDS |

| ||||||

AREA |

| % eU3O8 |

|

| (X 1000) |

|

| (X 1000) |

|

| (X 1000) |

|

| (X 1000) |

|

| (X 1000) |

| ||||||

FAB TREND |

|

| 0.280 |

|

|

| 1,172 |

|

|

| 6,574 |

|

|

| 0.119 |

|

|

| 456 |

|

|

| 1,081 |

|

AREA 5 |

|

| 0.243 |

|

|

| 195 |

|

|

| 947 |

|

|

| 0.115 |

|

|

| 93 |

|

|

| 214 |

|

TOTAL |

|

| 0.275 |

|

|

| 1,367 |

|

|

| 7,521 |

|

|

| 0.118 |

|

|

| 549 |

|

|

| 1,295 |

|

|

| MEASURED + INDICATED = |

|

|

| 0.230 |

|

|

| 1,915 |

|

|

| 8,816 |

| |||||||||

Notes:

1. | Sum of Measured and Indicated tons and pounds may not add to the reported total due to rounding. |

2. | Mineral resources that are not mineral reserves do not have demonstrated economic viability. |

3. | Based on grade cutoff of 0.02 percent eU3O8 and a grade x thickness cutoff of 0.25 GT. |

4. | Measured and Indicated Mineral Resources as defined in Section 1.2 of NI 43-101 (the CIM Definition Standards (CIM Council, 2015)). |

5. | Resources are reported through July 2014. |

6. | All reported resources occur below the historical, pre-mining static water table. |

7. | Sandstone density is 16.0 cu. ft./ton. |