Table of Contents

Index to Financial Statements

As filed with the Securities and Exchange Commission on February 17, 2017.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

Under

The Securities Act of 1933

MULESOFT, INC.

(Exact name of Registrant as specified in its charter)

| Delaware | 7372 | 20-5158650 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

77 Geary Street, Suite 400

San Francisco, California 94108

(415) 229-2009

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Greg Schott

Chairman and Chief Executive Officer

MuleSoft, Inc.

77 Geary Street, Suite 400

San Francisco, California 94108

(415) 229-2009

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Jon Avina, Esq. Wilson Sonsini Goodrich & Rosati, P.C. 650 Page Mill Road Palo Alto, California 94304 (650) 493-9300 |

Rob Horton, Esq. MuleSoft, Inc. 77 Geary Street, Suite 400 San Francisco, California 94108 (415) 229-2009 |

Richard A. Kline, Esq. Anthony J. McCusker, Esq. Andrew T. Hill, Esq. Goodwin Procter LLP 135 Commonwealth Drive Menlo Park, California 94025 (650) 752-3100 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||||

| Non-accelerated filer | ☒ | (Do not check if a smaller reporting company) | Smaller reporting company | ☐ |

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee | ||

| Class A Common Stock, $0.000025 par value per share |

$100,000,000 | $11,590 | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes the aggregate offering price of additional shares that the underwriters have the option to purchase from the Registrant. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

Index to Financial Statements

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted. Subject To Completion. Dated , 2017. Shares MuleSoft, Inc. Class A Common Stock This is an initial public offering of shares of Class A common stock of MuleSoft, Inc. Prior to this offering, there has been no public market for the Class A common stock. It is currently estimated that the initial public offering price per share will be between $ and $ . We intend to apply to list the Class A common stock on the New York Stock Exchange under the symbol “MULE”. Following this offering, we will have two classes of common stock, Class A common stock and Class B common stock. The rights of the holders of Class A common stock and Class B common stock are identical, except voting and conversion rights. Each share of Class A common stock is entitled to one vote. Each share of Class B common stock is entitled to 10 votes and is convertible at any time into one share of Class A common stock. All shares of our capital stock outstanding immediately prior to this offering, including all shares held by our executive officers, employees and directors, and their respective affiliates, will be reclassified into shares of our Class B common stock immediately prior to this offering. The holders of our outstanding Class B common stock will hold approximately % of the voting power of our outstanding capital stock following this offering. We are an “emerging growth company” as defined under the federal securities laws, and as such, we have elected to comply with certain reduced reporting requirements for this prospectus and may elect to do so in future filings. See “Risk Factors” on page 12 to read about factors you should consider before buying shares of the Class A common stock. Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense. Per Share Total Initial public offering price $ $ Underwriting discount(1) $ $ Proceeds, before expenses, to MuleSoft $ $ (1) See “Underwriting” for additional information regarding underwriting compensation. The underwriters have the option to purchase up to an additional shares of Class A common stock from MuleSoft at the initial public offering price less the underwriting discount. The underwriters expect to deliver the shares against payment in New York, New York on , 2017. Goldman, Sachs & Co. J.P. Morgan BofA Merrill Lynch Allen & Company LLC Barclays Jefferies Canaccord Genuity Piper Jaffray William Blair Prospectus dated , 2017

Table of Contents

Index to Financial Statements

MuleSoft®

Connect anything. Change everything.

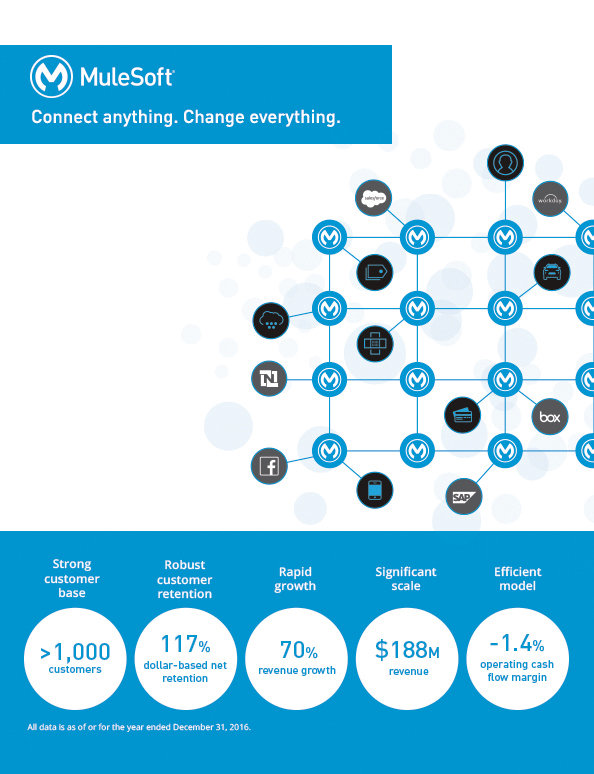

Strong customer base > 1,000 customers

Robust customer retention 117% dollar-based net retention

Rapid growth 70% revenue growth

Significant scale $188M revenue

Efficient model -1.4% operating cash flow margin

All data is as of or for the year ended December 31, 2016.

Table of Contents

Index to Financial Statements

Prospectus

| 1 | ||||

| 12 | ||||

| 43 | ||||

| 45 | ||||

| 46 | ||||

| 47 | ||||

| 48 | ||||

| 51 | ||||

| 54 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

57 | |||

| 83 | ||||

| 102 | ||||

| 112 | ||||

| 127 | ||||

| 133 | ||||

| 136 | ||||

| 142 | ||||

| MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES TO NON-U.S. HOLDERS OF OUR CLASS A COMMON STOCK |

145 | |||

| 149 | ||||

| 156 | ||||

| 156 | ||||

| 156 | ||||

| F-1 |

Through and including , 2017 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

We have not authorized anyone to provide any information or make any representations other than those contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are offering to sell, and seeking offers to buy, shares of our Class A common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our Class A common stock.

For investors outside of the United States: Neither we nor the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus outside of the United States.

i

Table of Contents

Index to Financial Statements

This summary highlights selected information that is presented in greater detail elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our Class A common stock. You should read this entire prospectus carefully, including the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes included elsewhere in this prospectus, before making an investment decision. Our fiscal year ends on December 31. Unless the context otherwise requires, the terms “MuleSoft,” “the company,” “we,” “us” and “our” in this prospectus refer to MuleSoft, Inc. and its consolidated subsidiaries.

MULESOFT, INC.

Our mission is to help organizations change and innovate faster by making it easy to connect the world’s applications, data, and devices.

We are entering a new era of business where competitive advantage is no longer primarily determined by the physical assets organizations own and control, but rather by how they connect and orchestrate a multitude of physical and technology assets. Winning organizations are “composable enterprises” that can quickly and effectively adopt new technologies and rapidly connect these assets to drive competitive advantage.

The convergence of major technology forces such as mobile, cloud, big data, and Internet of Things, or IoT, is driving the shift to composability and placing unrelenting demands on IT as it attempts to connect these increasingly distributed new technologies. This strains legacy IT infrastructures that are built on heavy and hardwired architectures and creates a bottleneck to transformation.

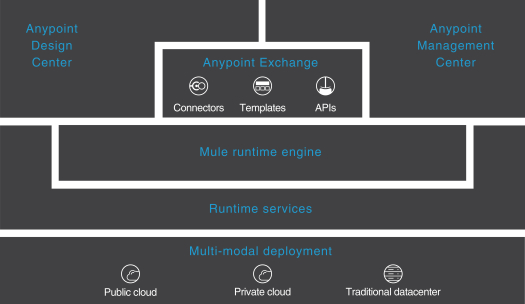

We are enabling a fundamental shift in organizations’ technology operating models and self-serve innovation by developers across the organization. Our customers use our Anypoint Platform to connect their applications, data, and devices into an “application network” in which these IT assets are pluggable using application programming interfaces, or APIs, instead of glued together with custom integration code. The application network becomes an infrastructure of discoverable building blocks that can be used and reused to rapidly compose applications. Anypoint Platform is a single, unified platform that allows organizations to easily build and rapidly scale application networks.

Anypoint Platform enables our customers to change and innovate faster by resolving the IT bottleneck. It speeds innovation by empowering developers to experiment and prototype new solutions, and freeing IT from writing manual integrations. Our platform connects and exposes existing IT investments as nodes on the application network for continued reuse, which can dramatically increase the longevity of, and return on, these assets. Application networks built on Anypoint Platform increase in value as new nodes are added, resulting in network effects that drive increasing speed and agility and lower costs.

A Customer Journey with Anypoint Platform

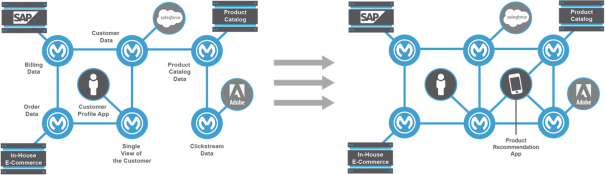

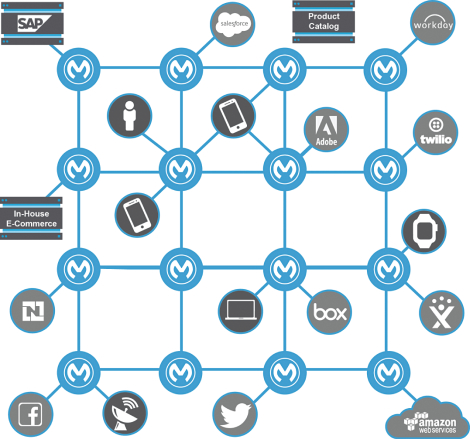

Each of our customers takes a different journey in building an application network with Anypoint Platform. For example, a large organization may begin with a single integration project, such as composing a customer profile web app for its sales team to better engage with its customers. This app

1

Table of Contents

Index to Financial Statements

would require real-time data feeds from various back-end applications, including order data from an on-premises eCommerce system, billing data from SAP, and customer data from Salesforce. With Anypoint Platform, our customer exposes this data as discoverable and consumable APIs and then combines those APIs to compose a “single view of the customer.” This single view itself can then become a consumable API. All four of these APIs are building blocks that are accessible as nodes on a nascent application network.

Next, the same organization may want to build a new product recommendation mobile app that requires the same order, billing, and customer data. In this case, the mobile app developer can use Anypoint Platform to discover and reuse the previously built single view of the customer API. She now has access to all of that information without depending on the IT organization or writing a single line of code. The developer can focus her energy on adding value to the app by using an API for product catalog data and an API for web clickstream data that tracks customer interest and intent. She can then combine these new APIs with the previously-created single view of a customer API to compose the new product recommendation mobile app. By having the existing APIs available on the application network, the barriers to creating a new app and the time to realizing value are dramatically reduced.

As more applications are built and added, the application network organically expands, increasing an organization’s delivery speed. Every incremental project builds on what has been built before. Applications that are plugged into the network are now accessible and reusable by any developer with

2

Table of Contents

Index to Financial Statements

access to the network. The organization can more easily change any app or system without breaking or impacting other applications running on the application network.

Our Opportunity

We estimate our current market opportunity to be $29 billion. We calculate our market opportunity by identifying the number of companies worldwide across all industries based on certain independent industry data from the S&P CapIQ database, segmented by cohorts based on annual revenue. We then multiply the number of companies worldwide in each cohort by our average annual contract value of subscription and support contracts per cohort. See the section titled “Business—Our Opportunity.”

We are disrupting large, existing markets. Forrester estimates that $32 billion will be spent in 2017 on the integration software market. Separately, Forrester estimates an additional $394 billion will be spent in 2017 on systems integration project work, which does not include the spending on custom-coded integrations by internal development teams. As the market for application networks continues to develop, we believe there is an opportunity to convert a meaningful portion of this spend to a software-based approach.

See the sections titled “Risk Factors—Risks Related to Our Business and Industry—The market for application networks and our platform is new and unproven” and “Risk Factors—Risks Related to Our Business and Industry—The estimates of market opportunity and forecasts of market growth included in this prospectus may prove to be inaccurate, and even if the market in which we compete achieves the forecasted growth, our business could fail to grow at similar rates, if at all” for certain risks related to our market opportunity.

Our Customers

We currently have over 1,000 customers located in over 60 countries across every major industry, including 30 customers with over $1.0 million in annual contract value of subscription and support contracts. Although our platform can be adopted by organizations of nearly any size, we focus our sales efforts on the largest global organizations. Our direct sales force targets CIOs, IT architects, and other business leaders, who are driving digital transformation in their organizations. We also partner with systems integrators and independent software vendors, which enhances our sales leverage by sourcing new prospects and providing systems integration services on implementations of our platform.

Financial Overview

We have grown rapidly in recent periods. Our revenue for 2014, 2015, and 2016 was $57.6 million, $110.3 million, and $187.7 million, respectively, representing a growth rate of 91% and 70%, respectively. We incurred net losses of $47.8 million, $65.4 million, and $49.6 million in 2014, 2015, and 2016, respectively.

Risk Factors Summary

Our business is subject to numerous risks and uncertainties, including those highlighted in the section titled “Risk Factors” immediately following this prospectus summary. Some of these risks are:

| • | We have a history of losses, and as our costs increase, we may not be able to generate sufficient revenue to achieve and sustain profitability; |

3

Table of Contents

Index to Financial Statements

| • | We have experienced rapid growth in recent periods. If we fail to continue to grow and to manage our growth effectively, we may be unable to execute our business plan, increase our revenue, improve our results of operations, maintain high levels of service, or adequately address competitive challenges; |

| • | We currently derive substantially all of our revenue and cash flows from Anypoint Platform, and any failure of this platform to satisfy customer demands or to achieve increased market acceptance would adversely affect our business, results of operations, financial condition, and growth prospects; |

| • | Our business and results of operations depend substantially on our customers renewing their subscriptions with us and expanding their use of our platform. Any decline in our customer renewals or failure to convince our customers to broaden their use of our platform would harm our business, results of operations, and financial condition; |

| • | If we were unable to attract new customers in a manner that is cost-effective and assures customer success, we would not be able to grow our business, which would adversely affect our results of operations, and financial condition; |

| • | We face a number of risks in our strategy to target larger organizations for sales of our platform, and if we do not manage these efforts effectively, our business and results of operations could be adversely affected; |

| • | Interruptions or performance problems associated with our technology and infrastructure may adversely affect our business, results of operations, and financial condition; |

| • | Incorrect or improper implementation or use of our platform could result in customer dissatisfaction and negatively affect our business, results of operations, financial condition, and growth prospects; and |

| • | The dual class structure of our common stock has the effect of concentrating voting control with those stockholders who held our capital stock prior to the completion of this offering, including our executive officers, employees and directors and their affiliates, which will limit your ability to influence the outcome of important transactions, including a change in control. Upon the completion of this offering, outstanding shares of Class B common stock will represent approximately % of the voting power of our outstanding capital stock, and outstanding shares of Class B common stock held by our directors, executive officers, and each of our stockholders who owns greater than five percent of our outstanding capital stock, will represent approximately % of the voting power of our outstanding capital stock. |

Corporate Information

Our principal executive offices are located at 77 Geary Street, Suite 400, San Francisco, California 94108, and our telephone number is (415) 229-2009. Our website address is www.mulesoft.com. Information contained on, or that can be accessed through, our website does not constitute part of this prospectus, and inclusions of our website address in this prospectus are inactive textual references only. We were incorporated in the state of Delaware in April 2006 as Azechi, Inc., and in July 2006, we changed our name to MuleSource, Inc. In August 2009, we changed our name to MuleSoft, Inc.

The MuleSoft design logo, “MuleSoft” and our other registered or common law trademarks, service marks, or trade names appearing in this prospectus are the property of MuleSoft, Inc. Other trademarks and trade names referred to in this prospectus are the property of their respective owners.

4

Table of Contents

Index to Financial Statements

Emerging Growth Company

The Jumpstart Our Business Startups Act, or the JOBS Act, was enacted in April 2012 with the intention of encouraging capital formation in the United States and reducing the regulatory burden on newly public companies that qualify as “emerging growth companies.” We are an emerging growth company within the meaning of the JOBS Act. As an emerging growth company, we may take advantage of certain exemptions from various public reporting requirements, including the requirement that our internal control over financial reporting be audited by our independent registered public accounting firm pursuant to Section 404 of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act, certain requirements related to the disclosure of executive compensation in this prospectus and in our periodic reports and proxy statements, and the requirement that we hold a nonbinding advisory vote on executive compensation and any golden parachute payments. We may take advantage of these exemptions until we are no longer an emerging growth company.

We have elected to take advantage of certain of the reduced disclosure obligations in this prospectus and may elect to take advantage of other reduced reporting requirements in our future filings with the SEC. As a result, the information that we provide to our stockholders may be different than what you might receive from other public reporting companies in which you hold equity interests.

The JOBS Act also provides that an emerging growth company can take advantage of an extended transition period for complying with new or revised accounting standards. We have irrevocably elected not to avail ourselves of this exemption, and therefore, we will be subject to the same new or revised accounting standards as other public companies that are not emerging growth companies.

We will remain an emerging growth company until the earliest to occur of (i) the last day of the fiscal year in which we have more than $1.0 billion in annual revenue; (ii) the date we qualify as a “large accelerated filer,” with at least $700 million of equity securities held by non-affiliates as of the last day of our then most recently completed second fiscal quarter; (iii) the date on which we have issued, in any three-year period, more than $1.0 billion in non-convertible debt securities; and (iv) the last day of the fiscal year ending after the fifth anniversary of the completion of this offering.

See the section titled “Risk Factors—Risks Related to this Offering and Ownership of Our Class A Common Stock—We are an ‘emerging growth company,’ and our election to comply with the reduced disclosure requirements as a public company may make our Class A common stock less attractive to investors” for certain risks related to our status as an emerging growth company.

5

Table of Contents

Index to Financial Statements

THE OFFERING

| Class A common stock offered by us |

shares |

| Class A common stock to be outstanding after this offering |

shares |

| Class B common stock to be outstanding after this offering |

shares |

| Total Class A common stock and Class B common stock to be outstanding after this offering |

shares |

| Option to purchase additional shares of Class A common stock from us |

shares |

| Use of proceeds |

We estimate that the net proceeds from the sale of shares of our Class A common stock in this offering will be approximately $ million (or approximately $ million if the underwriters’ option to purchase additional shares of our Class A common stock from us is exercised in full), based upon the assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

| The principal purposes of this offering are to increase our capitalization and financial flexibility, create a public market for our Class A common stock, and enable access to the public equity markets for us and our stockholders. We intend to use the net proceeds from this offering for general corporate purposes, including working capital, operating expenses, and capital expenditures. We may also use a portion of the net proceeds to acquire complementary businesses, products, services, or technologies. However, we do not have agreements or commitments for any material acquisitions at this time. See the section titled “Use of Proceeds” for additional information. |

| Voting rights |

Following this offering, we will have two classes of authorized common stock, Class A common stock and Class B common stock. The holders of our Class A common stock are entitled to one vote per share, and the holders of our Class B common stock are entitled to 10 votes per share, on all matters that are subject to a stockholder vote. |

6

Table of Contents

Index to Financial Statements

| All shares of our capital stock outstanding immediately prior to this offering, including all shares held by our executive officers, employees and directors, and their respective affiliates, will be reclassified into shares of our Class B common stock immediately prior to this offering. Holders of our Class A common stock and Class B common stock will generally vote together as a single class, unless otherwise required by law or our amended and restated certificate of incorporation. The holders of our outstanding Class B common stock will hold approximately % of the voting power of our outstanding capital stock following this offering and will have the ability to control the outcome of matters submitted to our stockholders for approval, including the election of our directors and the approval of any change in control transaction. See the sections titled “Principal Stockholders” and “Description of Capital Stock” for additional information. |

| Proposed New York Stock Exchange trading symbol |

“MULE” |

The number of shares of our Class A common stock and Class B common stock that will be outstanding after this offering is based on no shares of our Class A common stock and 112,991,577 shares of our Class B common stock (including shares of our convertible preferred stock on an as-converted basis) outstanding as of December 31, 2016, and excludes:

| • | 21,915,624 shares of our Class B common stock issuable upon the exercise of options to purchase shares of our Class B common stock outstanding as of December 31, 2016, with a weighted-average exercise price of $4.54 per share; |

| • | 532,746 shares of our Class B common stock issuable upon the exercise of options to purchase shares of our Class B common stock granted after December 31, 2016, with an exercise price of $12.53 per share; |

| • | 42,312 shares of our Class B common stock issuable upon the vesting of restricted stock units, or RSUs, granted after December 31, 2016; |

| • | 19,640 shares of our Class B common stock, on an as-converted basis, issuable upon the exercise of a warrant to purchase shares of our convertible preferred stock outstanding as of December 31, 2016, with an exercise price of $0.76375 per share; and |

| • | shares of our Class A common stock reserved for future issuance under our equity compensation plans, consisting of: |

| • | shares of our Class A common stock reserved for future issuance under our 2017 Equity Incentive Plan, or our 2017 Plan, which will become effective prior to the completion of this offering; |

| • | 3,183,229 shares of our Class A common stock that will be added to the shares of our Class A common stock reserved under our 2017 Plan upon its effectiveness, which shares are currently |

7

Table of Contents

Index to Financial Statements

| reserved for future issuance under our 2016 Equity Incentive Plan, or our 2016 Plan (after giving effect to the grant of 575,058 shares of our common stock issuable upon the exercise of options to purchase shares of our common stock and the vesting of RSUs granted after December 31, 2016), at which time we will cease granting awards under our 2016 Plan; and |

| • | shares of our Class A common stock reserved for future issuance under our 2017 Employee Stock Purchase Plan, or our ESPP, which will become effective prior to the completion of this offering. |

Our 2017 Plan and our ESPP each provide for annual automatic increases in the number of shares of Class A common stock reserved thereunder, and our 2017 Plan also provides for increases in the number of shares of Class A common stock reserved thereunder based on awards under our 2016 Plan that expire, are forfeited, or otherwise repurchased by us. See the section titled “Executive Compensation—Employee Benefit and Stock Plans” for additional information.

Except as otherwise indicated, all information in this prospectus assumes:

| • | the filing and effectiveness of our amended and restated certificate of incorporation and the effectiveness of our amended and restated bylaws, each of which will occur immediately prior to the completion of this offering; |

| • | the authorization of our Class A common stock and the reclassification of all outstanding shares of our common stock into an equivalent number of shares of our Class B common stock, each of which will occur immediately prior to the completion of this offering; |

| • | the automatic conversion and reclassification of all outstanding shares of our convertible preferred stock into an aggregate of 86,030,961 shares of our Class B common stock, which will occur immediately prior to the completion of this offering; |

| • | the automatic conversion and reclassification of an outstanding warrant to purchase 19,640 shares of our convertible preferred stock into a warrant to purchase 19,640 shares of our Class B common stock, which will occur immediately prior to the completion of this offering; |

| • | no exercise of outstanding stock options or warrants or settlement of outstanding RSUs subsequent to December 31, 2016; and |

| • | no exercise by the underwriters of their option to purchase up to an additional shares of our Class A common stock from us. |

8

Table of Contents

Index to Financial Statements

SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA

The following tables summarize our consolidated financial and other data. We have derived the summary consolidated statements of operations data for the years ended December 31, 2014, 2015, and 2016 and the consolidated balance sheet data as of December 31, 2016 from our audited consolidated financial statements included elsewhere in this prospectus. Our historical results are not necessarily indicative of the results that may be expected in the future. The following summary consolidated financial and other data should be read in conjunction with the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes included elsewhere in this prospectus.

| Year Ended December 31, | ||||||||||||

| 2014 | 2015 | 2016 | ||||||||||

| (In thousands, except share and per share data) | ||||||||||||

| Consolidated Statements of Operations Data: |

||||||||||||

| Revenue: |

||||||||||||

| Subscription and support |

$ | 48,436 | $ | 88,096 | $ | 152,843 | ||||||

| Professional services and other |

9,181 | 22,156 | 34,904 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total revenue |

57,617 | 110,252 | 187,747 | |||||||||

| Cost of revenue: |

||||||||||||

| Subscription and support(1) |

5,304 | 7,525 | 13,722 | |||||||||

| Professional services and other(1) |

11,509 | 24,645 | 35,341 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total cost of revenue |

16,813 | 32,170 | 49,063 | |||||||||

|

|

|

|

|

|

|

|||||||

| Gross profit |

40,804 | 78,082 | 138,684 | |||||||||

| Operating expenses: |

||||||||||||

| Research and development(1) |

17,046 | 24,725 | 32,862 | |||||||||

| Sales and marketing(1) |

58,676 | 93,057 | 122,630 | |||||||||

| General and administrative(1) |

11,911 | 24,368 | 31,577 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total operating expenses |

87,633 | 142,150 | 187,069 | |||||||||

|

|

|

|

|

|

|

|||||||

| Loss from operations |

(46,829 | ) | (64,068 | ) | (48,385 | ) | ||||||

| Interest income |

49 | 220 | 465 | |||||||||

| Other expense, net |

(248 | ) | (729 | ) | (340 | ) | ||||||

|

|

|

|

|

|

|

|||||||

| Net loss before provision for income taxes |

(47,028 | ) | (64,577 | ) | (48,260 | ) | ||||||

| Provision for income taxes |

728 | 862 | 1,339 | |||||||||

|

|

|

|

|

|

|

|||||||

| Net loss |

$ | (47,756 | ) | $ | (65,439 | ) | $ | (49,599 | ) | |||

|

|

|

|

|

|

|

|||||||

| Net loss attributable to common stockholders |

$ | (47,756 | ) | $ | (65,439 | ) | $ | (59,035 | ) | |||

|

|

|

|

|

|

|

|||||||

| Net loss per share attributable to common stockholders, basic and diluted(2) |

$ | (3.07 | ) | $ | (3.57 | ) | $ | (2.73 | ) | |||

|

|

|

|

|

|

|

|||||||

| Shares used to compute net loss per share attributable to common stockholders, basic and diluted(2) |

15,531,314 | 18,324,048 | 21,623,610 | |||||||||

|

|

|

|

|

|

|

|||||||

| Pro forma net loss per share, basic and diluted (unaudited)(2) |

$ | (0.45 | ) | |||||||||

|

|

|

|||||||||||

| Shares used to compute pro forma net loss per share, basic and diluted (unaudited)(2) |

110,919,770 | |||||||||||

|

|

|

|||||||||||

| (1) | Includes stock-based compensation expense and other compensation expense related to our 2015 Common Stock Repurchase and 2016 Tender Offer as follows (in thousands): |

| Year Ended December 31, |

||||||||||||

| 2014 | 2015 | 2016 | ||||||||||

| Cost of revenue—subscription and support |

$ | 26 | $ | 146 | $ | 255 | ||||||

| Cost of revenue—professional services and other |

76 | 324 | 675 | |||||||||

| Research and development |

238 | 2,506 | 2,831 | |||||||||

| Sales and marketing |

569 | 4,891 | 8,619 | |||||||||

| General and administrative |

520 | 4,542 | 4,120 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total stock-based and other compensation expense |

$ | 1,429 | $ | 12,409 | $ | 16,500 | ||||||

|

|

|

|

|

|

|

|||||||

9

Table of Contents

Index to Financial Statements

| See the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for further information about the 2015 Common Stock Repurchase and 2016 Tender Offer. |

| (2) | See Notes 2, 11, and 12 to our consolidated financial statements included elsewhere in this prospectus for an explanation of the calculations of our basic and diluted net loss per share attributable to common stockholders, pro forma net loss per share, and the weighted-average number of shares used in the computation of the per share amounts. |

| As of December 31, 2016 | ||||||||||||

| Actual | Pro Forma(1) | Pro Forma As Adjusted(2)(3) |

||||||||||

| (In thousands) | ||||||||||||

| Consolidated Balance Sheet Data: |

||||||||||||

| Cash, cash equivalents, and investments |

$ | 102,613 | $ | $ | ||||||||

| Working capital |

33,550 | |||||||||||

| Total assets |

202,938 | |||||||||||

| Deferred revenue, current and non-current |

135,614 | |||||||||||

| Convertible preferred stock |

255,946 | |||||||||||

| Total stockholders’ equity |

40,103 | |||||||||||

| (1) | Reflects the automatic conversion and reclassification of all outstanding shares of our convertible preferred stock as of December 31, 2016 into an aggregate of 86,030,961 shares of our Class B common stock immediately prior to completion of this offering. |

| (2) | Reflects the pro forma adjustment described in footnote (1) above and the sale and issuance of shares of our Class A common stock by us in this offering, at the assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

| (3) | Each $1.00 increase (decrease) in the assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, would increase (decrease) our cash, cash equivalents, and investments, working capital, total assets, and total stockholders’ equity by approximately $ million, assuming that the number of shares of our Class A common stock offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions. Each increase (decrease) of 1,000,000 shares in the number of shares offered by us would increase (decrease) the amount of our cash, cash equivalents, and investments, working capital, total assets and total stockholders’ equity by approximately $ million, assuming an initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, after deducting estimated underwriting discounts and commissions. |

Key Metrics

We monitor the following key metrics to help us evaluate our business, identify trends affecting our business, formulate business plans, and make strategic decisions.

| December 31, | ||||||||||||

| 2014 | 2015 | 2016 | ||||||||||

| Customers (as of end of period) |

590 | 839 | 1,071 | |||||||||

| Average subscription and support revenue per customer (in thousands) |

$ | 82 | $ | 105 | $ | 143 | ||||||

| Dollar-based net retention rate |

110 | % | 121 | % | 117 | % | ||||||

For a discussion of our key metrics, see the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Metrics.”

Non-GAAP Financial Measures

Free Cash Flow and Free Cash Flow Margin

Free cash flow is a non-GAAP financial measure that we calculate as net cash (used in) provided by operating activities less purchases of property and equipment. Free cash flow margin is calculated as free cash flow divided by total revenue. We believe that free cash flow and free cash flow margin are useful indicators of liquidity that provide information to management and investors about the amount of cash generated from our core operations that, after the purchases of property and

10

Table of Contents

Index to Financial Statements

equipment, can be used for strategic initiatives, including investing in our business and making strategic acquisitions. See the section titled “Selected Consolidated Financial and Other Data—Non-GAAP Financial Measures—Reconciliation of Non-GAAP Financial Measures” for information regarding the limitations of using free cash flow and free cash flow margin as financial measures.

Our free cash flows and free cash flow margins were as follows:

| Year Ended December 31, | ||||||||||||

| 2014 | 2015 | 2016 | ||||||||||

| Free cash flow (in thousands) |

$ | (41,753 | ) | $ | (48,640 | ) | $ | (7,203 | ) | |||

| Free cash flow margin |

(72.5 | )% | (44.1 | )% | (3.8 | )% | ||||||

The following table presents a reconciliation of free cash flow and free cash flow margin to net cash (used in) provided by operating activities, the most directly comparable financial measure calculated in accordance with generally accepted accounting principles, or GAAP:

| Year Ended December 31, | ||||||||||||

| 2014 | 2015 | 2016 | ||||||||||

| (In thousands, except percentages) | ||||||||||||

| Net cash used in operating activities |

$ | (39,647 | ) | $ | (47,134 | ) | $ | (2,702 | ) | |||

| Less: Purchases of property and equipment |

(2,106 | ) | (1,506 | ) | (4,501 | ) | ||||||

|

|

|

|

|

|

|

|||||||

| Free cash flow |

$ | (41,753 | ) | $ | (48,640 | ) | $ | (7,203 | ) | |||

|

|

|

|

|

|

|

|||||||

| Net cash used in operating activities (as a percentage of revenue) |

(68.8 | )% | (42.7 | )% | (1.4 | )% | ||||||

| Less: Purchases of property and equipment (as a percentage of revenue) |

(3.7 | )% | (1.4 | )% | (2.4 | )% | ||||||

|

|

|

|

|

|

|

|||||||

| Free cash flow margin |

(72.5 | )% | (44.1 | )% | (3.8 | )% | ||||||

|

|

|

|

|

|

|

|||||||

11

Table of Contents

Index to Financial Statements

Investing in our Class A common stock involves a high degree of risk. You should carefully consider the following risks, together with all of the other information contained in this prospectus, including our consolidated financial statements and related notes, before making a decision to invest in our Class A common stock. Any of the following risks could have an adverse effect on our business, results of operations, financial condition and prospects, and could cause the trading price of our Class A common stock to decline, which would cause you to lose all or part of your investment. Our business, results of operations, financial condition, or prospects could also be harmed by risks and uncertainties not currently known to us or that we currently do not believe are material.

Risks Related to Our Business and Industry

We have a history of losses, and as our costs increase, we may not be able to generate sufficient revenue to achieve and sustain profitability.

We have incurred net losses in each period since our inception, including net losses of $47.8 million, $65.4 million, and $49.6 million for 2014, 2015, and 2016, respectively. As a result, we had an accumulated deficit of $236.2 million as of December 31, 2016. We expect our operating expenses to increase significantly as we increase our sales and marketing efforts, continue to invest heavily in research and development, and expand our operations and infrastructure, both domestically and internationally. In addition, we expect to incur significant additional legal, accounting, and other expenses related to being a public company. While our revenue has grown in recent years, if our revenue declines or fails to grow at a rate faster than these increases in our operating expenses, we will not be able to achieve and maintain profitability in future periods. As a result, we may continue to generate losses. We cannot assure you that we will achieve profitability in the future or that, if we do become profitable, we will be able to sustain profitability.

We have experienced rapid growth in recent periods. If we fail to continue to grow and to manage our growth effectively, we may be unable to execute our business plan, increase our revenue, improve our results of operations, maintain high levels of service, or adequately address competitive challenges.

We have recently experienced a period of rapid growth in our business, operations, and employee headcount. For 2014, 2015, and 2016, our revenue was $57.6 million, $110.3 million, and $187.7 million, respectively, representing a 91% and 70% growth rate, respectively. We have also significantly increased the size of our customer base from 590 customers as of December 31, 2014 to over 1,000 customers today, and we grew from 444 employees as of December 31, 2014 to 841 employees as of December 31, 2016. We expect to continue to expand our operations and employee headcount in the near term. Our success will depend in part on our ability to continue to grow and to manage this growth effectively.

Our recent growth has placed, and future growth will continue to place, a significant strain on our management, administrative, operational, and financial infrastructure. We will need to continue to improve our operational, financial, and management controls, and our reporting systems and procedures to manage the expected growth of our operations and personnel, which will require significant capital expenditures and allocation of valuable management and employee resources. If we fail to implement these infrastructure improvements effectively, our ability to ensure uninterrupted operation of key business systems and comply with the rules and regulations that are applicable to public reporting companies will be impaired. Further, if we do not effectively manage the growth of our business and operations, the quality of our platform and services could suffer, and we may not be able to adequately address competitive challenges. This could impair our ability to attract new customers,

12

Table of Contents

Index to Financial Statements

retain existing customers and expand their use of our platform, all of which would adversely affect our brand, overall business, results of operations and financial condition.

We currently derive substantially all of our revenue and cash flows from Anypoint Platform, and any failure of this platform to satisfy customer demands or to achieve increased market acceptance would adversely affect our business, results of operations, financial condition, and growth prospects.

We derive substantially all of our revenue and cash flows from subscriptions for, and services related to, Anypoint Platform. Demand for Anypoint Platform is affected by a number of factors beyond our control, including increased market acceptance of our platform by existing customers and potential new customers, the extension of our platform for new use cases, the timing of development and release of new products by our competitors and additional capabilities and functionality by us, technological change, and growth or contraction of the market in which we compete. In addition, we cannot assure you that our platform and future enhancements to our platform will be able to address future advances in technology or requirements of existing customers or potential new customers. For example, our platform may not be able to be used to build application networks that can scale with the massive proliferation of applications, data, and devices that reside on-premises and in the cloud. If we are unable to continue to meet customer demands or to achieve more widespread market acceptance of our platform, our business, results of operations, financial condition and growth prospects will be adversely affected.

We began selling Anypoint Platform in 2014. Due to our limited experience selling the platform, it may be difficult to forecast our future results of operations and subjects us to a number of uncertainties, including the pace and degree of customer adoption of our platform. We have encountered and will continue to encounter risks and uncertainties frequently experienced by growing companies operating in new or developing markets. If our assumptions regarding these uncertainties, which we use to plan our business, are incorrect or change in reaction to changes in our markets, or if we do not address these risks successfully, our results of operations and financial condition could differ materially from our expectations and our business could suffer.

The market for application networks and our platform is new and unproven.

We introduced Anypoint Platform in 2014 to address the developing need to connect applications, data and devices within and between the organization and its external ecosystems. While we believe that, over time, the concept of an application network will become fundamental to an organization’s core operations, the market for application networks is largely unproven and is subject to a number of risks and uncertainties, including:

| • | organizations may determine that they only need point-to-point products to address their software integration needs; |

| • | organizations may decide that the investments needed to construct an application network are too significant or that such investments are better spent on other strategic initiatives within the organization; and |

| • | organizations may not understand the benefits that can be achieved with an application network. |

Moreover, even if the market for application networks develops, we may not be able to differentiate the benefits of Anypoint Platform from other products that may be developed to address the demand for application networks. Our ability to successfully market and sell Anypoint Platform will depend on a number of factors, including:

| • | our ability to support our customers as they build application networks that increase the speed at which they operate and innovate; |

13

Table of Contents

Index to Financial Statements

| • | our ability to include technologies for the broadening diversity of use cases and respond to the rapid evolution of new technologies; |

| • | our ability to design and engineer our platform for ease-of-use across an organization; and |

| • | our ability to enable customers to successfully adopt and deploy our platform in their organizations. |

The market for application networks and our platform is still new, and therefore, it is difficult to predict the size and growth rate of this market, whether and how rapidly customers will adopt our platform, whether we will be able to retain such customers and expand their usage of our platform, and the impact of competitive products and services. If the market for application networks and Anypoint Platform does not achieve significant growth or there is a reduction in demand for solutions in our market for any reason, it could result in reduced customer adoption of our platform, decreased customer retention, or weaker customer expansion with respect to the use of our platform, any of which would adversely affect our business, results of operations, and financial condition.

Our business and results of operations depend substantially on our customers renewing their subscriptions with us and expanding their use of our platform. Any decline in our customer renewals or failure to convince our customers to broaden their use of our platform would harm our business, results of operations, and financial condition.

Subscriptions to our platform are term-based and are typically one year in duration. In order for us to maintain or improve our results of operations, it is important that our customers renew their subscriptions with us when the existing subscription term expires. While our customers are not entitled to maintain the applications developed using Anypoint Platform after the termination of a subscription, they have no obligation to renew their subscriptions upon expiration. Based on our relatively limited experience selling and marketing Anypoint Platform, we may not be able to accurately predict customer renewal rates. In addition, the growth of our business depends in part on our customers expanding their use of our platform. We utilize our dollar-based net retention rate to measure our ability to retain customers and expand their use of our platform. Although our dollar-based net retention rate has historically been strong, some of our customers have elected not to renew their subscriptions with us in the past for a variety of reasons, including as a result of changes in their strategic IT priorities. Our dollar-based net retention rate may also decline or fluctuate as a result of a number of other factors, including our customers’ satisfaction or dissatisfaction with our platform, the increase in the contract value of subscription and support contracts from new customers, the effectiveness of our customer support services, our pricing, the prices of competing products or services, mergers and acquisitions affecting our customer base, global economic conditions, and the other risk factors included herein. As a result, we cannot assure you that customers will renew subscriptions or increase their usage of our platform. If our customers do not renew their subscriptions or renew on less favorable terms, or if we are unable to expand our customers’ use of our platform, our business, results of operations, and financial condition may be adversely affected.

If we were unable to attract new customers in a manner that is cost-effective and assures customer success, we would not be able to grow our business, which would adversely affect our results of operations, and financial condition.

In order to grow our business, we must continue to attract new customers in a cost-effective manner and enable such customers to realize the benefits associated with an application network. We may not be able to attract new customers to our platform for a variety of reasons, including as a result of their use of traditional approaches to technology integration, such as manual project-by-project integrations and the use of legacy point-to-point software integration products, their internal timing,

14

Table of Contents

Index to Financial Statements

budget or structural constraints that hinder their ability to build application networks, or the pricing of our platform compared to products and services offered by our competitors. After a customer makes a purchasing decision, we often must also help them successfully deploying our platform in their organization, a process that can last several months.

Even if we do attract customers, the cost of new customer acquisition or ongoing customer support may prove so high as to prevent us from achieving or sustaining profitability. For example, in 2014, 2015, and 2016, total sales and marketing expense represented 102%, 84%, and 65% of revenue, respectively. We intend to continue to hire additional sales personnel, increase our marketing activities to help educate the market about the benefits of application networks and our platform, grow our domestic and international operations, and build brand awareness. We also intend to continue to cultivate the MuleSoft developer community and our partner ecosystem of systems integrators, or SIs, and independent software vendors, or ISVs. If the costs of these sales and marketing efforts increase dramatically, if we do not experience a substantial increase in leverage from our partner ecosystem, or if our sales and marketing efforts do not result in substantial increases in revenue, our business, results of operations, and financial condition may be adversely affected. In addition, we expect to continue to invest in our professional services organization to accelerate our customers’ ability to adopt our platform and ultimately create and expand the size of their application network over time. We cannot assure you that any of these investments will lead to the cost-effective acquisition of additional customers.

We face a number of risks in our strategy to target larger organizations for sales of our platform, and if we do not manage these efforts effectively, our business and results of operations could be adversely affected.

We are increasingly focusing our sales and marketing efforts on larger organizations. As a result, we face a number of risks with respect to this strategy. For example, we expect to incur higher costs and longer sales cycles for larger organizations, and we may be less effective at predicting when we will complete these sales. In this market segment, the decision to invest in our platform may require a greater number of product evaluations and multiple approvals within a potential customer’s organization, which may require us to invest more time educating these potential customers. In addition, larger organizations may demand more features and professional services. As a result, these sales opportunities would likely lengthen our typical sales cycle and may require us to devote greater research and development, sales, support, and professional services resources to individual customers. This could strain our resources and result in increased costs. Moreover, larger customers may demand discounts in pricing, which could lower the amount of revenue we generate from any particular subscription. If an expected transaction is delayed until a subsequent period, or if we are unable to close one or more expected significant transactions with larger customers or potential new customers in a particular period, our results of operations for that period, and for any future periods in which revenue from such transaction would otherwise have been recognized, may be adversely affected. Our investments in marketing and selling to large organizations may not be successful, which could harm our results of operations and our overall ability to grow our customer base.

Interruptions or performance problems associated with our technology and infrastructure may adversely affect our business, results of operations, and financial condition.

Our continued growth depends in part on the ability of our existing customers and new customers to access our platform, particularly our cloud-based deployments, at any time and within an acceptable amount of time. We have experienced, and may in the future experience, service disruptions, outages and other performance problems due to a variety of factors, including infrastructure changes, human or software errors or capacity constraints. In some instances, we may not be able to identify the cause or causes of these performance problems within an acceptable period of time. It may become

15

Table of Contents

Index to Financial Statements

increasingly difficult to maintain and improve our performance as our platform becomes more complex. If our platform is unavailable or if our customers are unable to access features of our platform within a reasonable amount of time or at all, our business would be negatively affected. In addition, our infrastructure does not currently include the real-time mirroring of data. Therefore, in the event of any of the factors described above or other failures, customer data and other important information may be permanently lost.

We outsource our cloud infrastructure to Amazon Web Services, or AWS, which hosts our platform. Our customers need to be able to access our platform at any time, without interruption or degradation of performance. AWS runs its own platform that we access, and we are, therefore, vulnerable to service interruptions at AWS. We have experienced, and expect that in the future we may experience interruptions, delays and outages in service and availability from time to time due to a variety of factors, including infrastructure changes, human or software errors, website hosting disruptions and capacity constraints. Capacity constraints could be due to a number of potential causes including technical failures, natural disasters, fraud or security attacks. In addition, if our security, or that of AWS, is compromised, our platform is unavailable or our customers are unable to use our platform within a reasonable amount of time or at all, then our business, results of operations and financial condition could be adversely affected. In some instances, we may not be able to identify the cause or causes of these performance problems within a period of time acceptable to our customers. It may become increasingly difficult to maintain and improve our platform performance, especially during peak usage times, as the features of our platform become more complex and the usage of our platform increases. Any of the above circumstances or events may harm our reputation, cause customers to stop using our platform, impair our ability to increase revenue from existing customers, impair our ability to grow our customer base, subject us to financial penalties and liabilities under our service level agreements and otherwise harm our business, results of operations, and financial condition.

To the extent that we do not effectively anticipate capacity demands, upgrade our systems as needed, and continually develop our technology and network architecture to accommodate actual and anticipated changes in technology, our business and results of operations may be adversely affected. Moreover, our customer agreements include warranties and service level agreements that obligate us to provide future credits for customers of our cloud offerings in the event of a significant disruption in our platform. Any unscheduled downtime that exceeds such service level commitments could adversely affect our results of operations, financial condition, business, and reputation, which in turn could harm our ability to acquire new customers and expand relationships with existing customers.

Incorrect or improper implementation or use of our platform could result in customer dissatisfaction and negatively affect our business, results of operations, financial condition, and growth prospects.

Our platform is deployed in a wide variety of technology environments, both on-premises and in the cloud. Increasingly, our platform has been deployed in large scale, complex technology environments, and we believe our future success will depend on our ability to increase sales of our platform for use in such deployments. We must often assist our customers in achieving successful implementations of our platform, which we do through our professional services organization. The time required to implement our platform can range from three months for smaller deployments to six months or more for larger deployments. If our customers are unable to implement our platform successfully, or unable to do so in a timely manner, customer perceptions of our platform may be harmed, our reputation and brand may suffer, and customers may choose to cease usage of our platform or not to expand their use of our platform. Our customers and third-party partners may need training in the proper use of and the variety of benefits that can be derived from our platform to maximize its benefits. If our platform is not effectively implemented or used correctly or as intended, or if we fail to adequately

16

Table of Contents

Index to Financial Statements

train customers on how to efficiently and effectively use our platform, our customers may not be able to build application networks or otherwise achieve satisfactory outcomes. This could result in negative publicity and legal claims against us, which may cause us to generate fewer sales to new customers and reductions in renewals or expansions of the use of our platform with existing customers, any of which would harm our business and results of operations.

If our security measures are breached or unauthorized access to private or proprietary data is otherwise obtained, our platform may be perceived as not being secure, customers may reduce the use of or stop using our platform, and we may incur significant liabilities.

Because our platform allows customers to store and transmit data, there exists an inherent risk that an unauthorized third party could conduct a security breach, resulting in the loss of this data, which could lead to litigation, indemnity obligations, and other liability. While we have taken steps to protect the confidential information to which we have access, we do not have the ability to monitor or review the content that our customers store or transmit through our platform. Therefore, if customers use our software for the transmission or storage of personally identifiable information and our security measures are breached as a result of third-party action, employee error, malfeasance or otherwise, our reputation could be damaged, our business may suffer, and we could incur significant liability. Because techniques used to obtain unauthorized access or sabotage systems change frequently and generally are not identified until they are launched against a target, we may be unable to anticipate these techniques or to implement adequate preventative measures. Any or all of these issues could negatively impact our ability to attract new customers and increase engagement by existing customers, cause existing customers to elect not to renew their subscriptions, or subject us to third-party lawsuits, regulatory fines or other action or liability, thereby adversely affecting our financial results.

If we fail to adapt and respond effectively to rapidly changing technology, evolving industry standards, changing regulations and changing customer needs, requirements or preferences, our products may become less competitive.

The market in which we compete is relatively new and subject to rapid technological change, evolving industry standards and changing regulations, as well as changing customer needs, requirements and preferences. The success of our business will depend, in part, on our ability to adapt and respond effectively to these changes on a timely basis. If we were unable to enhance our platform or develop new solutions that keep pace with rapid technological and industry change, our business, results of operations, and financial condition could be adversely affected. If new technologies emerge that are able to deliver competitive products and services at lower prices, more efficiently, more conveniently or more securely, such technologies could adversely impact our ability to compete effectively. For example, Anypoint Platform was architected to connect and orchestrate applications, data and devices through the use of APIs. If new technologies emerge that displace the use of APIs, we may not be able to adapt our platform to such new technologies on a timely basis.

Our success also depends on the interoperability of our platform with third-party applications, data and devices that we have not developed and do not control. Any changes in such applications, data or devices that degrade the functionality of our platform or give preferential treatment to competitive software could adversely affect the adoption and usage of our platform. We may not be successful in adapting our platform to operate effectively with these applications, data, or devices. If it is difficult for our customers to access and use our platform, or if our platform cannot connect a broadening range of applications, data and devices, then our customer growth and retention may be harmed, and our business and results of operations could be adversely affected.

17

Table of Contents

Index to Financial Statements

Our future quarterly results may fluctuate significantly, and if we fail to meet the expectations of analysts or investors, our stock price and the value of your investment could decline substantially.

Our results of operations, including our revenue, operating expenses and cash flows have fluctuated from quarter to quarter in the past and may continue to fluctuate as a result of a variety of factors, many of which are outside of our control, may be difficult to predict and may or may not fully reflect the underlying performance of our business. Some of the factors that may cause our results of operations to fluctuate from quarter to quarter include:

| • | the mix of revenue and associated costs attributable to subscriptions and support and professional services, which may impact our gross margins and operating income; |

| • | our ability to attract new customers; |

| • | our ability to retain customers and expand their usage of our platform, particularly for our largest customers; |

| • | delays in closing sales, including the timing of renewals, which may result in revenue being pushed into the next quarter, particularly because a large portion of our sales occur toward the end of each quarter; |

| • | the timing of revenue recognition; |

| • | the mix of revenue attributable to larger transactions as opposed to smaller transactions; |

| • | changes in customers’ budgets and in the timing of their purchasing decisions; |

| • | potential customers opting for alternative products, including developing their own in-house solutions; |

| • | our ability to control costs, including our operating expenses; |

| • | the timing and success of new products, features and services by us and our competitors or any other change in the competitive dynamics of our industry, including consolidation among competitors, customers or strategic partners; |

| • | significant security breaches of, technical difficulties with, or interruptions to, the delivery and use of our platform; |

| • | the collectability of receivables from customers and resellers, which may be hindered or delayed if these customers or resellers experience financial distress; |

| • | general economic conditions, both domestically and internationally, as well as economic conditions specifically affecting industries in which our customers participate; |

| • | sales tax and other tax determinations by authorities in the jurisdictions in which we conduct business; |

| • | the impact of new accounting pronouncements; and |

| • | fluctuations in stock-based compensation expense. |

The occurrence of one or more of the foregoing and other factors may cause our results of operations to vary significantly. We also intend to continue to invest significantly to grow our business in the near future rather than optimizing for profitability or cash flows. Accordingly, our results of operations in any one quarter may not be meaningful and should not be relied upon as indicative of future performance. Additionally, if our quarterly results of operations fall below the expectations of investors or securities analysts who follow our stock, the price of our Class A common stock could decline substantially, and we could face costly lawsuits, including securities class action suits.

18

Table of Contents

Index to Financial Statements

We may not be able to compete successfully against current and future competitors.

We believe that we are the pioneer in the market for application networks because we provide the only complete offering for building application networks. However, there are many other companies addressing various aspects of this market. As a result, the competitive landscape is fragmented, intense and characterized by rapid changes in technology, customer requirements, and industry standards and by frequent new product introductions and improvements. We are likely to face continued challenges from current competitors, which include:

| • | manual integration efforts, which are either conducted in-house or through custom integration services providers; |

| • | legacy integration software vendors such as IBM, Oracle, and TIBCO; and |

| • | smaller specialized companies such as Apigee (recently acquired by Google), which are focused on various niches in integration and API management. |

Many of our principal competitors have substantially longer operating histories, greater financial, technical, marketing or other resources, stronger brand and customer recognition, larger intellectual property portfolios and broader global distribution and presence. Our competitors may be able to offer products or functionality similar to ours at a more attractive price than we can by integrating or bundling such products with their other product offerings. Acquisitions and consolidation in our industry may provide our competitors even more resources or may increase the likelihood of our competitors offering bundled or integrated products with which we cannot effectively compete. In addition, we face potential competition from participants in adjacent markets that may enter our markets by leveraging related technologies and partnering with or acquiring other companies, or providing alternative approaches to provide similar results, particularly as organizations are increasingly choosing to deploy applications on cloud platforms such as those offered by AWS, Microsoft Azure, and Google Cloud Platform. New innovative start-ups and existing large companies that are making significant investments in research and development could also launch new products and services, delivered either on-premises or in the cloud, that we do not offer and that could gain market acceptance quickly. If we were unable to anticipate or react to these competitive challenges, our competitive position would weaken, which would adversely affect our business and results of operations.

Real or perceived errors, failures or bugs in our software could adversely affect our business, results of operations, financial condition, and growth prospects.

Our platform is complex, and therefore, undetected errors, failures or bugs may occur. Our platform may be used in IT environments with different operating systems, system management software, applications, devices, databases and equipment and networking configurations, which may cause errors or failures of our platform or other aspects of the IT environment into which it is deployed. Despite testing by us, errors, failures or bugs may not be found until our platform is used by our customers. Real or perceived errors, failures or bugs in our products could result in negative publicity, loss of or delay in market acceptance of our platform, weakening of our competitive position, claims by customers for losses sustained by them or failure to meet the stated service level commitments in our customer agreements. In such an event, we may be required, or may choose, for customer relations or other reasons, to expend significant additional resources in order to help correct the problem. We have experienced from time to time errors, failures and bugs in our platform that have resulted in customer downtime. While we were able to remedy these situations, we cannot assure you that we will be able to mitigate future errors, failures or bugs in a quick or cost-effective manner. Any errors, failures or bugs in our platform could impair our ability to attract new customers, retain existing customers or expand their use of our platform, which would adversely affect our business, results of operations, and financial condition.

19

Table of Contents

Index to Financial Statements

The estimates of market opportunity and forecasts of market growth included in this prospectus may prove to be inaccurate, and even if the market in which we compete achieves the forecasted growth, our business could fail to grow at similar rates, if at all.

Market opportunity estimates and growth forecasts included in this prospectus, including those we have generated ourselves, are subject to significant uncertainty and are based on assumptions and estimates that may not prove to be accurate. Even if the market in which we compete meets the size estimates and growth forecasted in this prospectus, our business could fail to grow for a variety of reasons, which would adversely affect our results of operations. For more information regarding the estimates of market opportunity and the forecasts of market growth included in this prospectus, see the section titled “Market and Industry Data.”

Our sales cycle is long and unpredictable, and our sales efforts require considerable time and expense.

The timing of our sales and related revenue recognition is difficult to predict because of the length and unpredictability of the sales cycle for our platform before a sale. We are often required to spend significant time and resources to better educate and familiarize potential customers with the value proposition of our platform. Customers often view the subscription to our platform as a strategic decision and significant investment and, as a result, frequently require considerable time to evaluate, test and qualify our platform prior to entering into or expanding a subscription. During the sales cycle, we expend significant time and money on sales and marketing and contract negotiation activities, which may not result in a sale. Additional factors that may influence the length and variability of our sales cycle include: