UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31 , 2020

Commission File Number 001-33720

| State of Incorporation | IRS Employer Identification Number | |||||||||||||

Address, including zip code, of principal executive offices

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☑

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||||||||||

| ☑ | Smaller reporting company | |||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

As of June 30, 2020, the aggregate market value of our voting and non-voting common equity held by non-affiliates was $220.9 million.

As of March 29, 2021, a total of 99,916,941 shares of our common stock were outstanding.

TABLE OF CONTENTS

| PART I | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| PART III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| PART IV | ||||||||

| Item 15. | ||||||||

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

The matters discussed in this Annual Report on Form 10-K (this “2020 Form 10-K”) include “forward-looking statements” about the plans, strategies, objectives, goals or expectations of Remark Holdings, Inc. and subsidiaries (“Remark”, “we”, “us”, “our”). You will find forward-looking statements principally in the sections entitled Risk Factors and Management’s Discussion and Analysis of Financial Condition and Results of Operations. These forward-looking statements are identifiable by words or phrases indicating that Remark or management “expects,” “anticipates,” “plans,” “believes,” or “estimates,” or that a particular occurrence or event “will,” “may,” “could,” “should,” or “will likely” result, occur or be pursued or “continue” in the future, that the “outlook” or “trend” is toward a particular result or occurrence, that a development is an “opportunity,” “priority,” “strategy,” “focus,” that we are “positioned” for a particular result, or similarly stated expectations. Undue reliance should not be placed on these forward-looking statements, which speak only as of the date of this 2020 Form 10-K, other report, release, presentation, or statement.

In addition to other risks and uncertainties described in connection with the forward-looking statements contained in this 2020 Form 10-K and other periodic reports filed with the Securities and Exchange Commission (“SEC”), there are many important factors that could cause actual results to differ materially. Such risks and uncertainties include general business conditions, changes in overall economic conditions, our ability to integrate acquired assets, the impact of competition and other factors which are often beyond our control.

This should not be construed as a complete list of all of the economic, competitive, governmental, technological and other factors that could adversely affect our expected consolidated financial position, results of operations or liquidity. Additional risks and uncertainties not currently known to us or that we currently believe are immaterial also may impair our business, operations, liquidity, financial condition and prospects. We undertake no obligation to update or revise our forward-looking statements to reflect developments that occur or information that we obtain after the date of this 2020 Form 10-K.

PART I

ITEM 1. BUSINESS.

OVERVIEW

Remark Holdings, Inc. and subsidiaries (“Remark”, “we”, “us”, or “our”), which include its consolidated variable-interest entities (“VIEs”), are a diversified global technology company with leading artificial intelligence (“AI”) and data-analytics, as well as a portfolio of digital media properties.

Our innovative artificial intelligence (“AI”) and data analytics solutions continue to gain worldwide awareness and recognition through comparative testing, product demonstrations, media exposure, and word of mouth. We continue to see positive responses and increased acceptance of our software and applications in a growing number of industries. We intend to expand our business in three major regions, Asia-Pacific, North America, and Europe. The Asia-Pacific region has a fast-growth AI market with significant opportunities for our solutions. In North America, primarily in the United States, and Europe, we see robust demand for AI products and solutions in a growing number of industries, including potential growth opportunities particularly in the workplace and public safety markets, especially in response to the COVID-19 pandemic. The COVID-19 pandemic, as well as economic and geopolitical conditions, particularly in international markets, could adversely affect our business. We continue to pursue large business opportunities where we can quickly deploy our software solutions in the market segments we have identified, in which we may face a number of large, well-known competitors.

Our U.S. operations are headquartered in Las Vegas, Nevada, and our China operations are headquartered in Chengdu, China with additional operations in Beijing, Shanghai, and Hangzhou. Our common stock, par value $0.001 per share, is listed on the NASDAQ Capital Market under the ticker symbol MARK.

OUR BUSINESS

Development

In 2009, we co-founded a U.S.-based venture, Sharecare, Inc. (“Sharecare”), to build a web-based platform that simplifies the search for health and wellness information. The other co-founders of Sharecare were Dr. Mehmet Oz, HARPO Productions, Discovery Communications, Jeff Arnold and Sony Pictures Television. As a part of the transactions, we received an equity stake in Sharecare, which constitutes approximately 4.4 percent of Sharecare’s issued capital stock at December 31, 2020. We also maintain representation on Sharecare’s board of directors.

In September 2015, we acquired Vegas.com LLC (“Vegas.com” or “VDC”) to give us a deeper reach into the travel and entertainment market in Las Vegas and the surrounding area. After operating Vegas.com for several years, we determined that we would further focus on our AI business and reduce our debt by disposing of Vegas.com. On May 15, 2019, we completed the sale of all of the issued and outstanding membership interests of Vegas.com pursuant to a Membership Interest Purchase Agreement, dated as of March 15, 2019, with VDC-MGG Holdings LLC, an affiliate of our lenders, for an aggregate purchase price of $30 million (the “VDC Transaction”). The cash proceeds of the VDC Transaction were used to pay amounts due to our lenders.

After spending most of the first quarter of 2020 on product development and relationship building, we were able to launch our biosafety business in the second quarter of 2020 and begin recognizing revenue from sales of the new products. Our expectation is that the U.S. will be the primary market for this new product line, though we will continue to work to develop other markets as well.

Business Model

We currently earn the majority of our revenue from sales of AI-based products and services. Excluding general and administrative expense, the primary costs we incur to earn the revenue described above include:

•software development costs, including licensing costs for third-party software

•cost of equipment related to customized AI products

•costs associated with marketing our brands

AI Business

Through our proprietary data and AI platform, our Remark AI business (currently known in the Asia-Pacific region as KanKan) generates revenue by delivering AI-based software products, AI computing devices and software-as-a-service solutions for businesses in many industries. In addition to the other work that we have ramped up, we continue partnering with top universities on research projects targeting algorithm, artificial neural network and computing architectures which we believe keeps us among the leaders in technology development. Our research team continues to participate in various computer vision competitions at which it wins or ranks near or at the top.

We continue to market Remark AI’s innovative AI-based solutions to customers in the retail, urban life cycle and workplace and food safety markets.

Retail Solutions. Utilizing a client’s existing cameras and IoT devices placed throughout the store, Remark AI’s retail solutions swiftly analyze real-time customer shopping behavior, such as time of store entry and shelf-browsing habits, and provide managers with a customer heatmap that reflects traffic patterns. Purchase history is also analyzed, leading to relevant offers for future purchase conversions, and customers for their continued loyalty through a special VIP status that brings customized promotions and coupons along with attentive customer service. Remark AI’s retail solutions allow retailers and store managers to make better data-driven decisions regarding store layout, item placement, and pricing strategy, all while anonymizing customers’ identities to protect their privacy.

Urban Life Cycle Solutions. We offer and have installed several solutions in what we call the urban life cycle category. Our urban life cycle solutions include our AI community system which assists in building “smart” communities by enhancing community security and safety. We also have AI solutions that help to make schools “smart” by (i) providing an accurate and convenient method for student check-in and check-out, (ii) providing an autonomous method of campus monitoring that enhances students’ safety by, for example, monitoring students for elevated body temperatures that could indicate viral infections such as influenza or COVID-19, detecting trespassers, detecting dangerous behaviors or physical accidents that could result in injury, and (iii) monitoring the school kitchen for safety violations.

In traffic management, our solutions assist in monitoring traffic for various violations by automatically detecting, capturing, and obtaining evidence regarding violations such as speeding, running red lights, driving against the flow of traffic and even using counterfeit registration plates. Additionally, our solutions provide constant road-condition monitoring, providing control centers with real-time information on traffic conditions such as areas of congestion or other traffic anomalies.

Workplace and Food Safety Solutions. The monitoring and detection capabilities of our solutions ensure that workers are practicing established food safety protocols, wearing the proper personal protective equipment, and complying with local health codes. From commercial kitchens to factories to construction work zones, our safety-compliance algorithms manage regulatory functions, review hygienic and equipment status while checking and alerting management regarding violations.

Biosafety Business

The first half of 2020 was one of renewed focus for us as we repurposed and improved our existing urban life cycle solution that we were selling to make schools in China “smart” schools to build a new product line of high-quality, highly-effective thermal imaging solutions that leverage our innovative software. We currently focus our efforts predominantly in the U.S. market.

Remark AI Thermal Kits. We sell our Remark AI Thermal Kits to customers needing the ability to scan crowds and areas of high foot traffic for indications that certain persons with elevated temperatures may require secondary screening. Though the kits are semi-customizable, they generally consist primarily of a thermal imaging camera, a calibrating device, a computer to monitor the video feed, supporting equipment and our AI software. Once set up and calibrated, the kits scan a large number of

people each minute, providing both thermally enhanced and standard video feeds that allow our customers to evaluate high volumes of people at large gatherings.

Remark AI Thermal Pads. Our Remark AI rPad thermal imaging devices, usually mounted on a wall or a single-post stand, are designed for customers needing the ability to scan individuals on a one-by-one basis in situations where rapid, high-volume scanning is not necessary, such as at a customer’s office entrances where employees can be scanned as they enter for indications of an elevated temperature that may require secondary screening. In addition to thermal scanning, we can customize our AI software embedded in the rPad to perform additional safety and security functions including identifying persons for authorized entry.

Other Businesses

In addition to our AI and data analytics solutions, we maintain a digital media portfolio which, in addition to operating businesses, includes an approximately 4.4 percent ownership in the issued stock of Sharecare, an established health and wellness platform with more than 100 million users. We continue to evaluate opportunities to monetize and maximize the value of this asset for our shareholders. In addition to Data Platform Services revenue from our AI business, activities such as online merchandise sales generated from Bikini.com, our e-commerce website selling swimwear and accessories in the latest styles, also contributed to our consolidated revenue in the current-year and prior-year periods, while advertising also contributed to revenue in prior-year periods.

Competition

We compete for business primarily on the basis of the quality and reliability of our products and services, and primarily in the AI marketplace, which is intensely competitive and rapidly evolving.

Our AI-based products and services represent a significant opportunity for us in the future. We offer AI products and we also build and deploy custom AI solutions. Our AI products compete with companies such as SenseTime, Face++, Google, GoGoVan, WeLab and others, while we compete with companies such as PricewaterhouseCoopers, Hewlett Packard, Baidu and others for business in the AI solutions market space.

Some of the companies we compete against, or may compete against in the future, may have greater brand recognition and may have significantly greater financial, marketing and other resources than we have. As a result of the potentially greater brand recognition and resources, some of our competitors may bring new products and services to market more quickly, and they may be able to adopt more aggressive pricing policies than we could adopt.

Intellectual Property

We rely upon trademark, copyright and trade secret laws in various jurisdictions, as well as confidentiality procedures and contractual provisions to protect our proprietary assets and brands. We own 12 copyright registrations, we have 62 AI-related patents pending in China and we have several additional patent applications we are preparing to file in China. We also hold various trademarks for our brands, and we have additional applications pending.

Technology

Our technologies include software applications built to run on third-party cloud hosting providers including Amazon Web Services and Alibaba located in North America and Asia. We make substantial use of off-the-shelf available open-source technologies such as Linux, PHP, MySQL, Drupal, mongoDB, Memcache, Apache, Nginx, CouchBase, Hadoop, HBase, ElasticSearch, Lua, Java, Redis, Akka and Wordpress, in addition to commercial platforms such as Microsoft, including Windows Operating Systems, SQL Server, and .NET. Such systems are connected to the Internet via load balancers, firewalls, and routers installed in multiple redundant pairs. We also utilize third-party services to geographically deliver data using major content distribution network providers. We rely heavily on virtualization throughout our technology architecture, which enables the scaling of dozens of digital media properties in an efficient and cost-effective manner.

We use third-party cloud hosting providers to host most of our public-facing websites and applications, as well as many of our back-end business intelligence and financial systems. Each of our significant websites is designed to be fault-tolerant, with collections of application servers, typically configured in a load-balanced state, to provide additional resiliency. The infrastructure is equipped with enterprise-class security solutions to combat events such as large-scale distributed denial of service attacks. Our environment is staffed and equipped with a full-scale monitoring solution.

Governmental Regulation

The services we provide are subject to various laws and regulations. We are subject to a number of U.S. federal and state and foreign laws and regulations that affect companies conducting business on the Internet. These laws and regulations may involve privacy, rights of publicity, data protection, content regulation, intellectual property, competition, protection of minors, consumer protection, taxation or other subjects. Many of these laws and regulations are still evolving and being tested in courts and could be interpreted in ways that could harm our business. In addition, the application and interpretation of these laws and regulations often are uncertain, particularly in the new and rapidly evolving industry in which we operate. There are a number of legislative proposals pending before federal, state, and foreign legislative and regulatory bodies concerning data protection that may affect us. We incorporated the principles of the European Union (“EU”) General Data Protection Regulation (“GDPR”) into our internal data protection policy for our product development and solution implementation. In addition, we voluntarily hired an independent, authorized third party in Germany to conduct a GDPR audit of our privacy practices. The audit found that we are compliant with the GDPR principles.

We post our privacy policy and practices concerning the use and disclosure of any user data on our web properties and our distribution applications. Any failure by us to comply with posted privacy policies, federal and state regulatory requirements or foreign privacy-related laws and regulations could result in proceedings by governmental or regulatory bodies that could potentially harm our businesses, results of operations and financial condition.

Foreign data protection, privacy, and other laws and regulations can be more restrictive than those in the United States. The Chinese government has at times taken measures to restrict digital platforms, publishers or specific content themes from consumption by its citizens. We invest significant efforts into ensuring that our published content in China is consistent with our most current understanding of prevailing Chinese laws, regulations, and policies; and to date our published content in China has been met with successful distribution and no action or inquiry from the Chinese government. However, unforeseen regulatory restrictions or policy changes in China regarding digital content could have a material adverse effect on our business.

The Chinese government has not yet adopted a clear regulatory framework governing the new and rapidly-evolving artificial intelligence industry in which we operate. The Chinese government’s adoption of more stringent laws or enforcement protocols affecting participants in such industries (including, without limitation, restrictions on foreign investment, capital requirements and licensing requirements) could have a material adverse effect on our business.

Corporate Structure

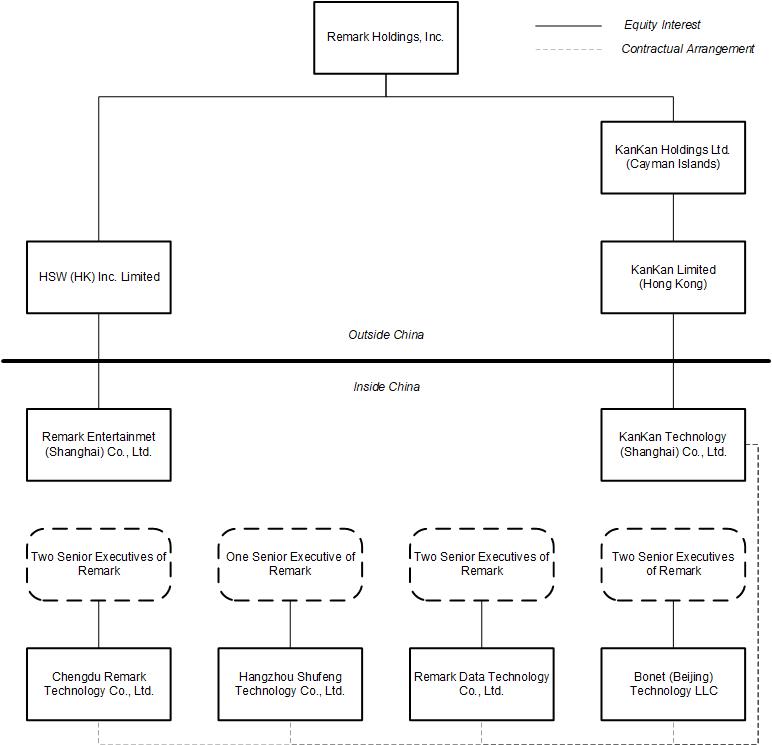

To comply with China’s laws which restrict foreign ownership of entities that operate within industries deemed sensitive by the Chinese government, we employ what we believe is a commonly-used organizational structure consisting of a wholly-foreign owned enterprise (“WFOE”) and VIEs to operate our KanKan business. We own 100% of the equity of the WFOE, while the VIEs are companies formed in China under local laws which are owned by members of our management team. We funded the registered capital and operating expenses of the VIEs by extending loans to the VIEs’ owners. We believe that we are the primary beneficiary of the VIEs because the equity holders of such entities do not have significant equity at risk and because we have been able to direct the operations of the VIEs.

The following diagram illustrates our China holding structure as of the date of this 2020 Form 10-K. The diagram omits certain entities which are immaterial to our results of operations and financial condition. Equity interests depicted in this diagram are 100% owned. The relationships between each of Chengdu Remark Technology Co., Ltd.; Hangzhou Shufeng Technology Co., Ltd.; Remark Data Technology Co., Ltd. and BoNet (Beijing) Technology LLC, on the one hand, and KanKan Technology (Shanghai) Co., Ltd., on the other hand, as illustrated in the following diagram are governed by contractual arrangements, including in each case an Exclusive Call Option Agreement, an Exclusive Business Cooperation Agreement, a Proxy Agreement and an Equity Pledge Agreement, and do not constitute equity ownership.

Employees

We employed 77 people as of March 29, 2021, all of which are full-time employees.

ADDITIONAL INFORMATION

We were originally incorporated in Delaware in March 2006 as HSW International, Inc., we changed our name to Remark Media, Inc. in December 2011, and as our business continued to evolve, we changed our name to Remark Holdings, Inc. in April 2017.

As soon as reasonably practicable after we electronically file such materials with, or furnish them to, the SEC, we provide free access through our website (www.remarkholdings.com) to our Annual Reports on Form 10-K, Quarterly Reports on Form

10-Q, Current Reports on Form 8-K and all amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). We do not incorporate any information found on our website into the materials we file with, or furnish to, the SEC; therefore, you should not consider any such information a part of any filing we make with the SEC. You may also obtain the reports noted above at the SEC’s website (www.sec.gov), which contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC.

ITEM 1A. RISK FACTORS

Investing in our common stock involves a high degree of risk. You should carefully consider the following risk factors, as well as the other information contained in this 2020 Form 10-K, including our consolidated financial statements and notes thereto, before deciding whether to invest in our common stock. Additional risks and uncertainties that we are unaware of may become important factors that affect us. If any of these risks actually occur, our business, financial condition or operating results may suffer, the trading price of our common stock could decline, and you may lose all or part of your investment.

Risks Relating to Our Business and Industry

We have insufficient authorized capital stock to issue common stock to all of the holders of our outstanding stock options and warrants and will need to seek stockholder approval to authorize additional shares of common stock in connection with the exercise of such outstanding securities or any future equity financing transactions.

Our Amended and Restated Certificate of Incorporation authorizes us to issue up to 100,000,000 shares of our common stock, of which 99,916,941 shares were outstanding as of March 29, 2021. In addition, as of March 29, 2021, we had outstanding stock options allowing for the purchase of as many as approximately 15.3 million shares of common stock and we had outstanding warrants to purchase 40,000 shares of common stock. If all of our outstanding stock options and warrants were exercised, the total number of shares of our common stock that we would be required to issue would greatly exceed the number of our remaining authorized but unissued shares of common stock.

As a result of such potential shortfall in the number of our authorized shares of common stock, we will have insufficient shares of common stock available to issue in connection with the exercise of our outstanding stock options and warrants or any future equity financing transaction we may seek to undertake. Accordingly, we are currently seeking approval of an increase in the number of our authorized shares of common stock at a special meeting of stockholders to be held on April 6, 2021. However, we cannot assure you that our stockholders will authorize an increase in the number of shares of our common stock. Our failure to have a sufficient number of authorized shares of common stock for issuance upon future conversion of our outstanding stock options and warrants could result in a breach under such securities, which could adversely affect our business, financial condition, results of operations and prospects.

The continuing impacts of COVID-19 are highly unpredictable and could be significant, and may have an adverse effect on our business and financial results.

The global outbreak of COVID-19 has impacted our business and could continue to have a significant impact on our business. The impact of COVID-19 on our business and future financial results could include, but may not be limited to:

•lack of revenue growth or decreases in revenue due to a lack of, or at least a decline in, customer demand and (or) deterioration in the credit quality of our customers;

•a significant increase in our need for external financing to maintain operations as a result of decreased revenue;

•significant decline in the debt and equity markets, thus impacting our ability to conduct financings on terms acceptable to us; and

•the rapid and broad-based shift to a remote working environment creates inherent productivity, connectivity, and oversight challenges. Preventative measures implemented by governmental authorities, such as travel restrictions, shelter-in-place orders and business closures, could significantly impact the ability of our employees and vendors to work productively. Governmental restrictions have been globally inconsistent and it is not clear when a return to worksite locations or travel will be permitted or what restrictions will be in place in those environments. In addition, the changed environment under which we are operating could have an impact on our internal controls over financial reporting as well as our ability to meet a number of our compliance requirements in a timely or quality manner.

The extent of the impact of the pandemic on our business and financial results will depend largely on future developments, including the duration and severity of the outbreak, the length of the travel restrictions and business closures imposed by

domestic and foreign governments, the impact on capital and financial markets and the related impact on the financial circumstances of our customers, all of which are highly uncertain and cannot be predicted. The situation is changing rapidly, and additional impacts may arise that we are not aware of currently.

The artificial intelligence market is new and unproven, and it may decline or experience limited growth, which would adversely affect our ability to fully realize the potential of our AI platform.

The artificial intelligence market is relatively new and unproven and is subject to a number of risks and uncertainties. We believe that our future success will depend in large part on the growth and acceptance of this market. The utilization of our platform by customers is still relatively new, and customers may not recognize the need for, or benefits of, our platform, which may prompt them to decide to adopt alternative products and services to satisfy their cognitive computing search and analytics requirements. Our ability to expand the market that our platform addresses depends upon a number of factors, including the cost, performance and perceived value of our platform. Market opportunity estimates are subject to significant uncertainty and are based on assumptions and estimates, including our internal analysis and industry experience. Assessing the market for our AI-based products in each of the vertical markets we compete in, or plan to compete in, is particularly difficult due to a number of factors, including limited available information and rapid evolution of the market. As a result, we may experience significant reduction in demand for our products and services due to lack of customer acceptance, technological challenges, competing products and services, decreases in spending by current and prospective customers, weakening economic conditions and other causes. If our market does not experience significant growth, or if demand for our AI-based products decreases, then our business, results of operations and financial condition will be adversely affected.

Laws and regulations concerning data privacy are continually evolving. Failure to comply with these laws and regulations could harm our business.

Portions of our business, primarily our AI solutions, are subject to certain privacy and data protection laws in the U.S and internationally. Our failure to comply with existing privacy or data protection laws and regulations could increase our costs, force us to change or limit the features of our AI software or result in proceedings or litigation against us by governmental authorities or others, any or all of which could result in significant fines or judgments against us, result in damage to our reputation, and result in negative effects on our financial condition and results of operations. Even if concerns raised by regulators, the media, or consumers about our privacy and data protection or consumer protection practices are unfounded, we could suffer damage to our reputation that causes significant negative effects on our financial condition and results of operations.

Privacy and data protection laws are rapidly changing and likely will continue to do so for the foreseeable future, which could have an impact on how we develop and customize our AI products and software. In the U.S., the California Consumer Privacy Act ("CCPA") became effective on January 1, 2020 and applies to processing of personal information of California residents. Other states, including Nevada, have enacted or are considering similar privacy or data protection laws that may apply to us. The U.S. government, including the Federal Trade Commission and the Department of Commerce, also continue to review the need for greater or different regulation over the collection of personal information and information about consumer behavior on the Internet and on mobile devices, and the U.S. Congress is considering a number of legislative proposals to regulate in this area. Various government and consumer agencies worldwide have also called for new regulation and changes in industry practices. For example, the GDPR became effective on May 25, 2018. GDPR would apply to us should we expand our AI business into member countries of the EU. Violations of the GDPR may result in significant penalties, and countries in the EU are still enacting national laws that correspond to certain portions of the GDPR.

The growth and development of AI may prompt calls for more stringent consumer privacy protection laws that may impose additional burdens on companies such as ours. Any such changes would require us to devote legal and other resources to address such regulation.

Our continuous access to publicly-available data and to data from partners may be restricted, disrupted or terminated, which would restrict our ability to develop new products and services, or to improve existing products and services, which are based upon our AI platform.

The success of our AI-based solutions depends substantially on our ability to continuously ingest and process large amounts of data available in the public domain and provided by our partners, and any interruption to our free access to such publicly-available data or to the data we obtain from our partners will restrict our ability to develop new products and services, or to improve existing products and services. While we have not encountered any significant disruption of such access to date, there is no guarantee that this trend will continue without costs. Public data sources may change their policies to restrict access or implement procedures to make it more difficult or costly for us to maintain access, and partners could decide to terminate our existing agreements with them. If we no longer have free access to public data, or access to data from our partners, our ability to maintain or improve existing products, or to develop new AI-based solutions may be severely limited. Furthermore, we may be forced to pay significant fees to public data sources or to partners to maintain access, which would adversely affect our financial condition and results of operations.

Our AI software and our application software are highly technical and run on very sophisticated third-party hardware platforms. If such software or hardware contains undetected errors, our AI solutions may not perform properly and our business could be adversely affected.

Our AI-based solutions and internal systems rely on software, including software developed or maintained internally and(or) by third parties, that is highly technical and complex. In addition, our AI-based solutions and internal systems depend on the ability of such software to store, retrieve, process, and manage immense amounts of data. The software on which we rely has contained, and may now or in the future contain, undetected errors, bugs, or vulnerabilities. Some errors may only be discovered after the AI-based solution or application software has been released for external or internal use. Errors or other design defects within the software on which we rely may result in a negative experience for our customers, delay product introductions or enhancements, result in measurement or billing errors, or compromise our ability to protect our customers’ data and(or) our intellectual property. Any errors, bugs, or defects discovered in the software on which we rely could result in damage to our reputation, loss of users, loss of revenue, or liability for damages, any of which could adversely affect our business and financial results.

The successful operation of our AI platform will depend upon the performance and reliability of the Internet infrastructure in China.

The successful operation of KanKan will depend on the performance and reliability of the Internet infrastructure in China. Almost all access to the Internet is maintained through state-owned telecommunication operators under the administrative control and regulatory supervision of the Ministry of Industry and Information Technology of China. In addition, the national networks in China are connected to the Internet through state-owned international gateways, which are the only channels through which a domestic user can connect to the Internet outside of China. We may not have access to alternative networks in the event of disruptions, failures or other problems with China’s Internet infrastructure. In addition, the Internet infrastructure in China may not support the demands associated with continued growth in Internet usage.

The failure of telecommunications network operators to provide us with the requisite bandwidth could also interfere with the speed and availability of KanKan. We have no control over the costs of the services provided by the national telecommunications operators. If the prices that we pay for telecommunications and Internet services rise significantly, our gross margins could be adversely affected. In addition, if Internet access fees or other charges to Internet users increase, our user traffic may decrease, which in turn may cause a decrease in our revenues.

Delays in collecting amounts receivable arising from our KanKan business in China could negatively impact our results of operations and cash flows.

Generally, Chinese entities tend to pay their vendors on longer timelines than the timelines typically observed in U.S. commerce, while contracts in China can lack the specificity regarding timing of collection that current accounting rules in the U.S. require to record revenue from contracts with customers. The combination of longer collection times and lack of contract specificity regarding timing of collection could result in higher amounts of bad debt expense, less revenue recorded in any particular period and mismatches between the timing of our cash needs and the timing of our cash inflows that could negatively affect our reported results of operations and harm relationships with our vendors, which in turn could harm our business.

If the Chinese government deems that the contractual arrangements in relation to our variable interest entities (“VIEs”) do not comply with its restrictions on foreign investment, or if Chinese regulations or the interpretation of existing regulations changes in the future, we could be subject to penalties or be forced to relinquish our interests in our China operations.

Various regulations in China restrict or prohibit wholly foreign-owned enterprises from operating in specified industries such as Internet information, financial services, Internet access and certain other industries. To comply with Chinese regulatory requirements, we conduct certain of our operations in China through contractual arrangements with our VIEs, which are incorporated in China and owned by members of our management team. These contractual arrangements are intended to give us effective control over each of the VIEs and enable us to receive substantially all of the economic benefits arising from the VIEs as well as consolidate the financial results of the VIEs in our results of operations. We expect that an increased amount of our revenue will be generated through our VIEs. Although the VIE structure we have adopted is consistent with longstanding industry practice, and has been adopted by comparable companies in China, there are substantial uncertainties regarding the interpretation and application of Chinese laws and regulations, and there can be no assurance that the Chinese government would agree that these contractual arrangements comply with China’s licensing, registration or other regulatory requirements, with existing policies or with requirements or policies that may be adopted in the future. Chinese laws and regulations governing the validity of these contractual arrangements are uncertain and the relevant government authorities have broad discretion in interpreting these laws and regulations.

If the VIE structure is deemed by Chinese regulators having competent authority to be illegal, either in whole or in part, we may lose control of our VIEs and have to modify such structure to comply with regulatory requirements. However, there can be no assurance that we could achieve this without material disruption to our business. Further, if the VIE structure is found to be in violation of any existing or future Chinese laws or regulations, the relevant regulatory authorities would have broad discretion in dealing with such violations. Furthermore, new Chinese laws, rules and regulations may be introduced to impose additional requirements that may be applicable to our contractual arrangements with our VIEs. Occurrence of any of these events could materially and adversely affect our business, financial condition and results of operations.

Our contractual arrangements may not be as effective in providing control over the VIEs as direct ownership.

Because we are restricted or prohibited by the Chinese government from owning certain Internet operations in China, we are dependent on our VIEs, in which we have no direct ownership interest, to provide our AI-based products and services through contractual arrangements among the parties and to hold some of our assets. These contractual arrangements may not be as effective in providing control over our operations as direct ownership of these businesses. For example, if we had direct ownership of our VIEs, we would be able to exercise our rights as a shareholder to effect changes in their boards of directors, which in turn could effect changes at the management level. Due to our VIE structure, we have to rely on contractual rights to effect control and management of our VIEs, which exposes us to the risk of potential breach of contract by the VIEs or their shareholders. In addition, as each of our VIEs is jointly owned by its shareholders, it may be difficult for us to change our corporate structure if such shareholders refuse to cooperate with us. In addition, some of our subsidiaries and VIEs could fail to take actions required for our business. Furthermore, if the shareholders of any of our VIEs were involved in proceedings that had an adverse impact on their shareholder interests in such VIE or on our ability to enforce relevant contracts related to the VIE structure, our business would be adversely affected.

Any failure by our VIEs or their shareholders to perform their obligations under the contractual arrangements would have a material adverse effect on our business, financial condition and results of operations.

If our VIEs or their shareholders fail to perform their respective obligations under the contractual arrangements, we may have to incur substantial costs and expend additional resources to enforce the arrangements. We have also entered into equity pledge agreements with respect to each VIE to secure certain obligations of such variable interest entity or its shareholders to us under the contractual arrangements. However, the enforcement of these agreements through arbitration or judicial agencies may be costly and time-consuming and will be subject to uncertainties in China’s legal system. Moreover, our remedies under the equity pledge agreements are primarily intended to help us collect debts owed to us by the VIEs or the VIEs’ shareholders under the contractual arrangements and may not help us in acquiring the assets or equity of the VIEs.

The contractual arrangements with our VIEs may be subject to scrutiny by China’s tax authorities. Any adjustment of related party transaction pricing could lead to additional taxes, and therefore substantially reduce our consolidated net income and the value of your investment.

The tax regime in China is rapidly evolving and there is significant uncertainty for Chinese taxpayers as Chinese tax laws may be interpreted in significantly different ways. China’s tax authorities may assert that we or the VIEs or their shareholders are required to pay additional taxes on previous or future revenue or income. In particular, under applicable Chinese laws, rules and regulations, arrangements and transactions among related parties, such as the contractual arrangements with our VIEs, may be subject to audit or challenge by China’s tax authorities. If China’s tax authorities determine that any contractual arrangements were not entered into on an arm's length basis and therefore constitute a favorable transfer pricing, the China tax liabilities of the relevant subsidiaries, VIEs or VIE shareholders could be increased, which could increase our overall tax liabilities. In addition, China’s tax authorities may impose interest on late payments. Our net income may be materially reduced if our tax liabilities increase. It is uncertain whether any new China laws, rules or regulations relating to VIE structures will be adopted or, if adopted, what they would provide.

If we or any of our VIEs are found to be in violation of any existing or future China laws, rules or regulations, or if we fail to obtain or maintain any of the required permits or approvals, the relevant China regulatory authorities would have broad discretion to take action in dealing with these violations or failures, including revoking the business and operating licenses of our China subsidiaries or the VIEs, requiring us to discontinue or restrict our operations, restricting our right to collect revenue, blocking one or more of our websites, requiring us to restructure our operations or taking other regulatory or enforcement actions against us. The imposition of any of these measures could result in a material adverse effect on our ability to conduct all or any portion of our business operations. In addition, it is unclear what impact Chinese government actions would have on us and on our ability to consolidate the financial results of any of our VIEs in our consolidated financial statements, if China’s governmental authorities were to find our legal structure and contractual arrangements to be in violation of China laws, rules and regulations. If the imposition of any governmental actions causes us to lose our right to direct the activities of any of our material VIEs or otherwise separate from any of these entities, and if we are not able to restructure our ownership structure and operations in a satisfactory manner, we would no longer be able to consolidate the financial results of our VIEs in our consolidated financial statements. Any of these events would have a material adverse effect on our business, financial condition and results of operations.

The shareholders, directors and executive officers of the VIEs may have potential conflicts of interest with us.

Our VIEs are owned by members of our management team. In addition, these individuals are also directors and officers of the VIEs. Chinese laws provide that a director and an executive officer owe a fiduciary duty to the company he or she directs or manages. The directors and executive officers of the VIEs must therefore act in good faith and in the best interests of the VIEs, and must not use their respective positions for personal gain. These laws, however, do not require them to consider the best interests of Remark when making decisions as a director or member of the management of the VIEs. Conflicts may arise between these individuals’ fiduciary duties as directors and officers of the VIEs and Remark.

Conflicts of interest may also arise due to the individuals’ roles as shareholders of the VIEs and their duties as our employees. The shareholders of the VIEs may breach, or cause the VIEs to breach, the VIE contracts. As a result, we might have to rely on legal or arbitral proceedings to enforce our contractual rights. Any failure by our VIEs or their shareholders to perform their obligations under the contractual arrangements would have a material adverse effect on our business, financial condition and results of operations.

The Note (as defined below) contains certain covenants that restrict our ability to engage in certain transactions and may impair our ability to respond to changing business and economic conditions.

On February 10, 2021, we entered into a senior secured promissory note (the “Note”) with certain of our subsidiaries as guarantors (the “Guarantors”) and Jefferson Remark Funding LLC (the “Lender”), pursuant to which the Lender extended credit to us consisting of a one-year term loan in the principal amount of $5.0 million. The Note requires us to satisfy various covenants, including using the proceeds from borrowings under the Note for general corporate purposes in a manner consistent with the identified use of proceeds previously disclosed by us to the Lender. The Note also contains restrictions on our abilities to engage in certain transactions without the consent of the Lenders, and may limit our ability to respond to changing business and economic conditions. The restrictions include, among other things, limitations on our ability and the ability of our subsidiaries to:

•change its name or corporate form or jurisdiction of organization;

•merge with another entity (other than an affiliate of Lender);

•consolidate, or sell or dispose of any material portion of our assets;

•sell, lease, license, convey, assign (by operation of law or otherwise), exchange or otherwise voluntarily or involuntarily transfer or dispose of any interest in any of its assets (other than upon receipt of fair consideration for obsolete assets, trade-ins and disposition, sales or licenses in the ordinary course of business) or any portion thereof or encumber, or hypothecate, or create, incur or permit to exist any pledge, mortgage, lien, security interest, charge, encumbrance or adverse claim upon or other interest in or with respect to any of its assets (other than permitted liens); and

•directly or indirectly enter into or permit to exist any transaction with any affiliate (other than a wholly-owned subsidiary) of us.

Our products and internal systems rely on software that is highly technical, and if it contains undetected errors, our business could be adversely affected.

Our products and internal systems rely on software, including software developed or maintained internally and/or by third parties, that is highly technical and complex. In addition, our products and internal systems depend on the ability of such software to store, retrieve, process, and manage immense amounts of data. The software on which we rely has contained, and may now or in the future contain, undetected errors, bugs, or vulnerabilities. Some errors may only be discovered after the code has been released for external or internal use. Errors or other design defects within the software on which we rely may result in a negative experience for users and marketers who use our products, delay product introductions or enhancements, result in measurement or billing errors, or compromise our ability to protect the data of our users and/or our intellectual property. Any errors, bugs, or defects discovered in the software on which we rely could result in damage to our reputation, loss of users, loss of revenue, or liability for damages, any of which could adversely affect our business and financial results.

We may be subject to liability in China with respect to Remark Entertainment for content that is alleged to be socially destabilizing, obscene, defamatory, libelous or otherwise unlawful.

Under the laws of the People’s Republic of China, we will be required to monitor our websites and the websites hosted on our servers and mobile interfaces for items or content deemed to be socially destabilizing, obscene, superstitious or defamatory, as well as items, content or services that are illegal to sell online or otherwise in other jurisdictions in which we operate, and promptly take appropriate action with respect to such items, content or services. We may also be subject to potential liability in China for any unlawful actions of our customers or users of our websites or mobile interfaces or for content we distribute that is deemed inappropriate. It may be difficult to determine the type of content that may result in liability to us, and if we are found to be liable, we may be subject to fines, have our relevant business operation licenses revoked, or be prevented from operating our websites or mobile interfaces in China.

Unauthorized use of our intellectual property by third parties, and the expenses incurred in protecting our intellectual property rights, may adversely affect our business.

We regard our copyrights, service marks, trademarks, trade secrets and other intellectual property as critical to our success. Unauthorized use of our intellectual property by third parties may adversely affect our business and reputation. We rely on trademark and copyright law, trade secret protection and confidentiality agreements with our employees, customers, business partners and others to protect our intellectual property rights. Despite our precautions, it is possible for third parties to obtain and use our intellectual property without authorization. Furthermore, the validity, enforceability and scope of protection of intellectual property in Internet related industries are uncertain and still evolving. In particular, the laws of the People’s Republic of China are uncertain or do not protect intellectual property rights to the same extent as do the laws of the United States. Moreover, litigation may be necessary in the future to enforce our intellectual property rights, to protect our trade secrets or to determine the validity and scope of the proprietary rights of others. Future litigation could result in substantial costs and diversion of resources.

We may be subject to intellectual property infringement claims, which may force us to incur substantial legal expenses and, if determined adversely against us, materially disrupt our business.

We cannot be certain that our brands and services will not infringe valid patents, copyrights or other intellectual property rights held by third parties. We cannot provide assurance that we will avoid the need to defend against allegations of infringement of third-party intellectual property rights, regardless of their merit. Intellectual property litigation is very expensive, and becoming involved in such litigation could consume a substantial portion of our managerial and financial resources, regardless of whether we win. Substantially greater resources may allow some of our competitors to sustain the cost of complex intellectual property litigation more effectively than us; we may not be able to afford the cost of such litigation.

Should we suffer an adverse outcome from intellectual property litigation, we may incur significant liabilities, we may be required to license disputed rights from third parties, or we may have to cease using the subject technology. If we are found to infringe upon third-party intellectual property rights, we cannot provide assurance that we would be able to obtain licenses to such intellectual property on commercially reasonable terms, if at all, or that we could develop or obtain alternative technology. If we fail to obtain such licenses at a reasonable cost, such failure may materially disrupt the conduct of our business, and could consume substantial resources and create significant uncertainties. Any legal action against us or our collaborators could lead to:

•payment of actual damages, royalties, lost profits, potentially treble damages and attorneys’ fees if we are found to have willfully infringed a third party’s patent rights;

•injunctive or other equitable relief that may effectively block our ability to further develop, commercialize and sell our products;

•us or our collaborators having to enter into license arrangements that may not be available on commercially acceptable terms, if at all; or

•significant cost and expense, as well as distraction of our management from our business.

The negative outcomes discussed above could adversely affect our ability to conduct business, financial condition, results of operations and cash flows.

We face intense competition from larger, more established companies, and we may not be able to compete effectively, which could reduce demand for our services.

The market for the services we offer is increasingly and intensely competitive. Nearly all our competitors have longer operating histories, larger customer bases, greater brand recognition and significantly greater financial, marketing and other resources than we do. Our competitors may secure more favorable revenue arrangements with advertisers, devote greater resources to marketing and promotional campaigns, adopt more aggressive growth strategies and devote substantially more resources to website and systems development than we do. In addition, the Internet media and advertising industries continue to experience consolidation, including the acquisitions of companies offering travel and finance-related content and services and paid search services. Industry consolidation has resulted in larger, more established and well-financed competitors with a

greater focus. If these industry trends continue, or if we are unable to compete in the Internet media and paid search markets, our financial results may suffer.

Additionally, larger companies may implement policies and/or technologies into their search engines or software that make it less likely that consumers can reach our websites and less likely that consumers will click-through on sponsored listings from our advertisers. The implementation of such technologies could result in a decrease in our revenues. If we are unable to successfully compete against current and future competitors, our operating results will be adversely affected.

If we do not effectively manage our growth, our operating performance will suffer and our financial condition could be adversely affected.

Substantial future growth will be required for us to realize our business objectives. To the extent we are capable of achieving this growth, it will place significant demands on our managerial, operational and financial resources. Additionally, this growth will require us to make significant capital expenditures, hire, train and manage a larger work force, and allocate valuable management resources. We must manage any such growth through appropriate systems and controls in each of these areas. If we do not manage the growth of our business effectively, our business, financial condition, results of operations and cash flows could be materially and adversely affected.

In addition, as our business grows, our technological and network infrastructure must keep in-line with our needs. Future demand is difficult to forecast and we may not be able to adequately handle large increases unless we spend substantial amounts to augment our ability to handle increased traffic. Additionally, the implementation of increased network capacity contains some execution risks and may lead to ineffectiveness or inefficiency. This could lead to a diminished experience for our consumers and advertisers and damage our reputation and relationship with them, leading to lower marketability and negative effects on our operating results. Moreover, the pace of innovative change in network technology is fast and if we do not keep up, we may lag behind competitors. The costs of upgrading and improving technology could be substantial and negatively affect our business, financial condition, results of operations and cash flows.

Risks Relating to our Company

We have a history of operating losses and we may not generate sufficient revenue to support our operations.

During the year ended December 31, 2020, and in each fiscal year since our inception, we have incurred net losses and generated negative cash flow from operations, resulting in an accumulated deficit of $360.5 million.

We cannot provide assurance that revenue generated from our businesses will be sufficient to sustain our operations in the long term. We have implemented measures to reduce operating costs, and we continuously evaluate other opportunities to reduce costs further. Additionally, we are working with our advisors to evaluate strategic alternatives, including the potential sale of certain non-core assets, investment assets and operating businesses. We may also need to obtain additional capital through equity financing or debt financing. Should we fail to successfully implement our plans described herein, such failure would have a material adverse effect on our business, including the possible cessation of operations.

Conditions in the debt and equity markets, as well as the volatility of investor sentiment regarding macroeconomic and microeconomic conditions (including developments and volatility arising from COVID-19) will play primary roles in determining whether we can successfully obtain additional capital. We cannot be certain that we will be successful at raising capital, whether in an equity financing, debt financing, or by divesting of certain assets or businesses, on commercially reasonable terms, if at all. In addition, if we obtain capital by issuing equity, such transaction(s) may dilute existing stockholders.

Our independent registered public accounting firm’s reports for the fiscal years ended December 31, 2020 and 2019 have raised substantial doubt regarding our ability to continue as a “going concern.”

Our independent registered public accounting firm indicated in its report on our audited consolidated financial statements as of and for the years ended December 31, 2020 and 2019 that there is substantial doubt about our ability to continue as a going concern. A “going concern” opinion indicates that the financial statements have been prepared assuming we will continue as a going concern and do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets, or the amounts and classification of liabilities that may result if we do not continue as a going concern.

Therefore, you should not rely on our consolidated balance sheet as an indication of the amount of proceeds that would be available to satisfy claims of creditors, and potentially be available for distribution to stockholders, in the event of liquidation. The presence of the going concern note to our financial statements may have an adverse impact on the relationships we are developing and plan to develop with third parties as we continue the commercialization of our products and could make it difficult for us to raise additional financing, all of which could have a material adverse impact on our business and prospects and result in a significant or complete loss of your investment.

Expanding our international operations involves additional risks, and our exposure to such risks increases as our business continues to expand outside of the United States.

We operate outside of the United States in China. China has different economic conditions, languages, currency, consumer expectations, levels of consumer acceptance and use of the Internet for commerce, legislation, regulatory environments (including labor laws and customs), tax laws and levels of political stability. We are subject to associated risks typical of international businesses, including, but not limited to, the following:

•Local economic or political instability;

•Threatened or actual acts of terrorism;

•Compliance with additional laws applicable to companies operating internationally as well as local laws and regulations, including the Foreign Corrupt Practices Act, data privacy requirements, labor and employment law, laws regarding advertisements and promotions and anti-competition regulations;

•Diminished ability to legally enforce contractual rights;

•Increased risk and limits on enforceability of intellectual property rights;

•Restrictions on, or adverse consequences related to, the withdrawal of non-U.S. investment and earnings;

•Restrictions on repatriation of cash as well as restrictions on investments in operations;

•Financial risk arising from transactions in multiple currencies as well as foreign currency exchange restrictions;

•Difficulties in managing staff and operations due to distance, time zones, language and cultural differences; and

•Uncertainty regarding liability for services, content and intellectual property rights, including uncertainty as a result of local laws and lack of precedent.

Operating our business in China exposes us to particular risks and uncertainties relating China’s laws and regulations, some of which restrict foreign investment in businesses including Internet content providers, mobile communication and related businesses. In addition, compliance with legal, regulatory or tax requirements in multiple jurisdictions places demands on our time and resources, and we may nonetheless experience unforeseen and potentially adverse legal, regulatory or tax consequences. In China, legal and other regulatory requirements may prohibit or limit participation by foreign businesses, such as by making foreign ownership or management of Internet businesses illegal or difficult, or may make direct participation in those markets uneconomic, which could make our entry into and expansion in those markets difficult or impossible, require that we work with a local partner or result in higher operating costs. Although we have established effective control of our Chinese business through a series of contractual arrangements, future developments in the interpretation or enforcement of Chinese laws and regulations or a dispute relating to these contractual arrangements could restrict our ability to operate or restructure our business or to engage in strategic transactions. The success of our business in China, and of any future investments in China, is subject to risks and uncertainties regarding the application, development and interpretation of China’s laws and regulations. If we cannot effectively manage our China operations, our business, results of operations and financial condition could be adversely affected.

Furthermore, when we accumulate large amounts of cash in China, which we will consider indefinitely reinvested in our China operations, the repatriation of such funds for use in the United States, including for corporate purposes such as acquisitions, stock repurchases, dividends or debt refinancing, may result in additional U.S. income tax expense and higher cost for such capital.

We continue to evolve our business strategy and develop new brands, products and services, and our future prospects are difficult to evaluate.

We are in varying stages of development with regard to our business, including our artificial intelligence business driven by our AI platform, so our prospects must be considered in light of the many risks, uncertainties, expenses, delays, and difficulties frequently encountered by companies in the early stages of development of business models and products. Some of such risks and difficulties include our ability to, among other things:

•manage and implement new business strategies;

•successfully commercialize and monetize our assets;

•continue to raise additional working capital;

•manage operating expenses;

•establish and take advantage of strategic relationships;

•successfully avoid diversion of management’s attention or of other resources from our existing business

•successfully avoid impairment of goodwill or other intangible assets such as trademarks or other intellectual property arising from acquisitions;

•prevent, or successfully temper, adverse market reaction to acquisitions;

•manage and adapt to rapidly changing and expanding operations;

•respond effectively to competitive developments; and

•attract, retain and motivate qualified personnel.

Because of the early stage of development of certain of our business operations, we cannot be certain that our business strategy will be successful or that it will successfully address the risks described or alluded to above. Any failure by us to successfully implement our new business plans could have a material adverse effect on our business, financial condition, results of operations and cash flows. Furthermore, growth into new areas may require changes to our cost structure, modifications to our infrastructure and exposure to new regulatory, legal and competitive risks.

If we fail to manage our growth, we may need to improve our operational, financial and management systems and processes which may require significant capital expenditures and allocation of valuable management and employee resources. As we continue to grow, we must effectively integrate, develop and motivate new employees, including employees in international markets, while maintaining the beneficial aspects of our company culture. If we do not manage the growth of our business and operations effectively, the quality of our platform and efficiency of our operations could suffer, which could harm our brand, results of operations and business.

We cannot assure you that these investments will be successful or that such endeavors will result in the realization of the full benefits of synergies, cost savings, innovation and operational efficiencies that may be possible or that we will achieve these benefits within a reasonable period of time.

Our investment in Sharecare’s equity securities is currently illiquid.

Our investment in Sharecare’s equity securities is illiquid. Sharecare is unlikely to pay current dividends on its equity securities, and our ability to realize a return on our investment, and recover our investment, will be dependent on Sharecare’s continued success. There is currently no public market for Sharecare’s securities, which are subject to restrictions on resale that might prevent us from selling such securities during periods in which it would be advantageous to do so. Additionally, our equity position in Sharecare may be diluted if Sharecare issues additional equity, options, or warrants.

Risks Relating to Our Common Stock

Our stock price has fluctuated considerably and is likely to remain volatile, and various factors could negatively affect the market price or market for our common stock.

The trading price of our common stock has been and may continue to be volatile. From January 1, 2019, through March 29, 2021, the high and low sales prices for our common stock were $4.72 and $0.25, respectively. The trading price of our common stock may fluctuate significantly in response to numerous factors, many of which are beyond our control, including:

•general market and economic conditions;

•the low trading volume and limited public market for our common stock;

•minimal third-party research regarding our company; and

•the current and anticipated future operating performance and equity valuation of Sharecare, in which we have a significant equity investment.

In addition, the stock market in general, and the market prices for Internet-related companies in particular, have experienced volatility that often has been unrelated to the operating performance of such companies. Such broad market and industry fluctuations may adversely affect the price of our stock, regardless of our operating performance.

The concentration of our stock ownership may limit individual stockholder ability to influence corporate matters.

As of March 29, 2021, our Chairman and Chief Executive Officer, Kai-Shing Tao, may be deemed to beneficially own 10,200,634 shares, or 9.8% of our common stock, and Lawrence Rosen may be deemed to beneficially own 5,418,616 shares, or 5.4% of our common stock. The interests of these stockholders may not always coincide with the interests of other stockholders, and they may act in a manner that advances their best interests and not necessarily those of other stockholders, and might affect the prevailing market price for our securities.

If these stockholders act together, they may be able to exert significant control over our management and affairs requiring stockholder approval, including approval of significant corporate actions. Such concentration of ownership may have the effect of delaying or preventing a change in control and might adversely affect the market price of our common stock.

A significant number of additional shares of our common stock may be issued under the terms of existing securities, which issuances would substantially dilute existing stockholders and may depress the market price of our common stock.

As of March 29, 2021, we had outstanding stock options allowing for the purchase of as many as approximately 15.3 million shares of common stock. Also outstanding were warrants we issued as part of the consideration for our acquisition of assets of China Branding Group Limited (the “CBG Acquisition” and such warrants, the “CBG Acquisition Warrants”), providing for the right to purchase 40,000 shares of common stock at per-share exercise prices of $10.00. We are also obligated to issue additional CBG Acquisition Warrants allowing for the purchase of 5,710,000 shares of common stock at a per-share exercise price of $10.00 (we have already accounted for the liability associated with such unissued CBG Acquisition Warrants in our consolidated balance sheet as part of the line item Warrant liability). On February 21, 2018, we initiated a legal proceeding seeking, among other things, a declaration that we are not required to deliver the unissued CBG Acquisition Warrants. The parties to the proceeding entered into a Stipulation for Settlement which sets forth terms with respect to the issuance of such unissued CBG Acquisition Warrants. We describe the Stipulation for Settlement in more detail in Item 3 of this 2020 Form 10-K.

The CBG Acquisition Warrants are exercisable on a cashless basis only, such that they cannot be exercised for the entire amount of shares purchasable under the warrants, and they effectively cannot be exercised to purchase shares of common stock unless the applicable market value of the common stock exceeds the applicable exercise price under the terms thereof.

The issuance of common stock pursuant to the warrants described above would substantially dilute the proportionate ownership and voting power of existing stockholders, and their issuance, or the possibility of their issuance, may depress the market price of our common stock.

Provisions in our corporate charter documents and under Delaware law could make an acquisition of Remark more difficult, which acquisition may be beneficial to stockholders.

Provisions in our Amended and Restated Certificate of Incorporation and Amended and Restated Bylaws, as well as provisions of the General Corporation Law of the State of Delaware (“DGCL”), which may discourage, delay or prevent a merger with, acquisition of or other change in control of Remark, even if such a change in control would be beneficial to our stockholders, include the following:

•only our Board of Directors may call special meetings of our stockholders;

•our stockholders may take action only at a meeting of our stockholders and not by written consent;

•we have authorized, undesignated preferred stock, the terms of which may be established and shares of which may be issued without stockholder approval.

Additionally, Section 203 of the DGCL prohibits a person who owns in excess of 15% of our outstanding voting stock from merging or combining with us for a period of three years after the date of the transaction in which the person acquired in excess of 15% of our outstanding voting stock, unless the merger or combination is approved in a prescribed manner. We have not opted out of the restriction under Section 203, as permitted under DGCL.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None

ITEM 2. PROPERTIES

We conduct our operations primarily from office space located in Las Vegas, Nevada, and Chengdu, China. The locations are leased pursuant to agreements expiring in March 2023 and September 2022, respectively. We also lease support offices in Shanghai and Hangzhou, China.

ITEM 3. LEGAL PROCEEDINGS

CBG Litigation