UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One)

[ ] REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 25, 2010

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

[ ] SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report _________________________

For the transition period from ___________to ___________.

Commission file number: 000-52132

CHINA OUMEI REAL ESTATE INC.

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of

Registrant’s name into English)

Cayman Islands

(Jurisdiction of

incorporation or organization)

Floor 28, Block C

Longhai Mingzhu Building

No.182

Haier Road, Qingdao 266000

People’s Republic of China

(Address

of principal executive offices)

Mr. Zhaohui John Liang

634 Donna Ct.

River

Vale, NJ 07675

Phone: (201) 497-5400

Email: john.liang@chinaoumeirealestate.com

(Name,

Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

None

(Title of Class)

Securities registered or to be registered pursuant to Section 12(g) of the Act.

Ordinary shares, par value $0.002112 per share

(Title

of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report (December 25, 2010): 31,020,062 ordinary shares.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [X]

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files)

Yes [ ] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer.

| Large Accelerated Filer [ ] | Accelerated Filer [ ] | Non-Accelerated Filer [X] |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP [X] | International Financial Reporting [ ] | Other [ ] |

| Standards as issued by the International | ||

| Accounting Standards Board |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

[ ] Item 17 [ ] Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [X]

Annual Report on Form 20-F

For the

Fiscal Year Ended December 25, 2010

TABLE OF CONTENTS

|

|

Page | ||

| PART I | |||

|

|

|||

|

Item 1. |

Identity of Directors, Senior Management and Advisers | 2 | |

|

Item 2. |

Offer Statistics and Expected Timetable | 2 | |

|

Item 3. |

Key Information | 2 | |

|

Item 4. |

Information on the Company | 15 | |

|

Item 4A. |

Unresolved Staff Comments | 43 | |

|

Item 5. |

Operating and Financial Review and Prospects | 43 | |

|

Item 6. |

Directors, Senior Management and Employees | 57 | |

|

Item 7. |

Major Shareholders and Related Party Transactions | 66 | |

|

Item 8. |

Financial Information | 66 | |

|

Item 9. |

The Offer and Listing | 67 | |

|

Item 10. |

Additional Information | 67 | |

|

Item 11. |

Quantitative and Qualitative Disclosures About Market Risk | 79 | |

|

Item 12. |

Description of Securities Other Than Equity Securities | 80 | |

|

|

|||

|

|

|||

| PART II | |||

|

|

|||

|

Item 13. |

Defaults, Dividend Arrearages and Delinquencies | 80 | |

|

Item 14. |

Material Modifications to the Rights of Securities Holders and Use of Proceeds | 80 | |

|

Item 15. |

Controls and Procedures | 80 | |

|

Item 16A. |

Audit Committee Financial Expert | 82 | |

|

Item 16B. |

Code of Ethics | 82 | |

|

Item 16C. |

Principal Accountant Fees and Services | 82 | |

|

Item 16D. |

Exemptions from the Listing Standards for Audit Committees | 82 | |

|

Item 16E. |

Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 82 | |

|

Item 16F. |

Change in Registrant’s Certifying Accountant | 83 | |

|

Item 16G. |

Corporate Governance | 83 | |

|

|

|||

|

|

|||

| PART III | |||

|

|

|||

|

Item 17. |

Financial Statements | 83 | |

|

Item 18. |

Financial Statements | 83 | |

|

Item 19. |

Exhibits | 83 | |

i

USE OF CERTAIN DEFINED TERMS

Except as otherwise indicated by the context, references in this annual report to:

-

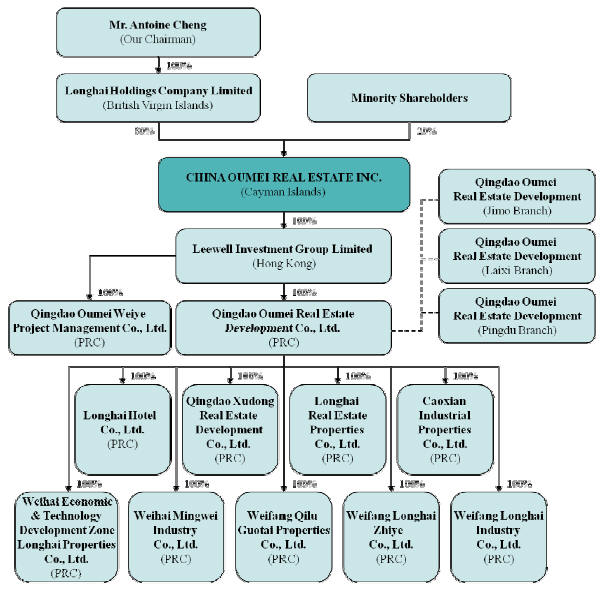

“we,” “us,” “our,” “our Company,” or “the Company” are to the combined business of China Oumei Real Estate Inc., a Cayman Islands company, and its consolidated subsidiaries, Leewell, Oumei, Oumei Weiye, Caoxian Industrial, Longhai Hotel, Longhai Real Estate, Qingdao Xudong, Weifang Longhai Industry, Weifang Longhai Zhiye, Weifang Qilu, Weihai Economic and Weihai Mingwei;

-

“Leewell” are to Leewell Investment Group Limited, a Hong Kong company;

-

“Oumei” are to Qingdao Oumei Real Estate Development Co., Ltd., a PRC limited company;

-

“Oumei Weiye” are to Qingdao Oumei Weiye Project Management Co., Ltd., a PRC limited company;

-

“Caoxian Industrial” are to Caoxian Industrial Properties Co., Ltd., a PRC limited company;

-

“Longhai Hotel” are to Longhai Hotel Co., Ltd., a PRC limited company;

-

“Longhai Real Estate” are to Longhai Real Estate Properties Co., Ltd., a PRC limited company;

-

“Qingdao Xudong” are to Qingdao Xudong Real Estate Development Co., Ltd., a PRC limited company;

-

“Weifang Longhai Industry” are to Weifang Longhai Industry Co., Ltd., a PRC limited company;

-

“Weifang Longhai Zhiye” are to Weifang Longhai Zhiye Co., Ltd., a PRC limited company;

-

“Weifang Qilu” are to Weifang Qilu Guotai Properties Co., Ltd., a PRC limited company;

-

“Weihai Economic” are to Weihai Economic & Technology Development Zone Longhai Properties Co., Ltd., a PRC limited company;

-

“Weihai Mingwei” are to Weihai Mingwei Industry Co., Ltd., a PRC limited company;

-

“Hong Kong” are to the Hong Kong Special Administrative Region of the People’s Republic of China;

-

“PRC” and “China” are to the People’s Republic of China;

-

“Renminbi” and “RMB” are to the legal currency of China;

- “U.S. dollars,” “dollars” and “$” are to the legal currency of the United States;

In addition, at present, there is no uniform standard to categorize the different types and sizes of cities in China. In this annual report, we refer to Beijing, Shanghai, Guangzhou and Shenzhen as tier one cities, which are the most populous, affluent and competitive cities in the country. Tier two cities are cities that generally meet the following criteria, excluding the four aforementioned tier one cities: (1) Gross Domestic Product, or GDP, over RMB 200 billion (US$29 billion); (2) GDP per capita over RMB 14,000 (US$2,050); (3) population with permanent residency in urban area over 1 million; (4) urban area over 100 km2; (5) annual sales in residential real estate over 1.5 million square meters; and (6) average unit selling price of residential real estate over RMB 3,000 (US$439) per square meter. Tier three cities are the cities that do not meet one or more criteria listed above.

FORWARD-LOOKING INFORMATION

In addition to historical information, this annual report contains forward-looking statements. These statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements. These risks and uncertainties include, but are not limited to, the factors described in Item 3, “Key information—Risk Factors” below. In some cases, you can identify forward-looking statements by terms such as “anticipates,” “believes,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “projects,” “should,” “would” and similar expressions intended to identify forward-looking statements. Forward-looking statements reflect our current views with respect to future events and are based on assumptions and subject to risks and uncertainties. Given these uncertainties, you should not place undue reliance on these forward-looking statements.

Also, forward-looking statements represent our estimates and assumptions only as of the date of this annual report. You should read this annual report and the documents that we reference and filed as exhibits to this report completely and with the understanding that our actual future results may be materially different from what we expect. Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statements, even if new information becomes available in the future.

1

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

Selected Financial Data

Selected Consolidated Financial Data

The following table presents selected financial data regarding our business. It should be read in conjunction with our consolidated financial statements and related notes contained elsewhere in this annual report and the information under Item 5, “Operating and Financial Review and Prospects.” The financial statements contained elsewhere fully represent our financial condition and operations; however, they are not indicative of our future performance.

The selected consolidated statement of operations data for the years ended December 25, 2008, 2009 and 2010 and the consolidated balance sheet data as of December 31, 2008, 2009 and 2010 have been derived from our audited consolidated financial statements included in this annual report. The selected consolidated statement of operations data for the years ended December 25, 2006 and 2007 and the selected consolidated balance sheet data as of December 25, 2006 and 2007 have been derived from our unaudited financial statements not included in this annual report. Our consolidated financial statements are prepared and presented in accordance with generally accepted accounting principles in the United States, or U.S. GAAP.

| Fiscal Year Ended December 25, | |||||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | |||||||||||

| Statements of Operations Data | (unaudited) | (unaudited) | |||||||||||||

| Total sales | $ | 54,291,244 | $ | 51,850,312 | $ | 77,032,561 | $ | 94,315,500 | $ | 110,518,421 | |||||

| Total cost of sales | (33,703,168 | ) | (36,243,778 | ) | (46,321,251 | ) | (58,296,408 | ) | (77,209,814 | ) | |||||

| Gross profit | 20,588,076 | 15,606,534 | 30,711,310 | 36,019,092 | 33,308,607 | ||||||||||

| Advertising expenses | (47,051 | ) | (46,492 | ) | (112,263 | ) | (268,222 | ) | (217,596 | ) | |||||

| Commission expenses | (789,497 | ) | (134,989 | ) | (574,262 | ) | (84,982 | ) | (214,566 | ) | |||||

| Selling expenses | (6,192 | ) | (2,187 | ) | (81,415 | ) | (49,800 | ) | (61,967 | ) | |||||

| Bad debt recovery (expense) | (154,710 | ) | (245,243 | ) | (1,198,942 | ) | (207,523 | ) | 987,374 | ||||||

| General and administrative expenses | (4,092,355 | ) | (807,589 | ) | (2,283,744 | ) | (4,655,596 | ) | (7,390,963 | ) | |||||

| Income from operations | 15,498,271 | 14,370,034 | 26,460,684 | 30,752,969 | 26,410,889 | ||||||||||

| Miscellaneous income (expense) | 16,022 | 10,280 | 91,945 | 327,294 | 23,899,865 | ||||||||||

| Interest expense | (121,597 | ) | (70,963 | ) | (968,710 | ) | (866,751 | ) | (325,969 | ) | |||||

| Income before income taxes and extraordinary item | 15,392,696 | 14,309,351 | 25,583,919 | 30,213,512 | 49,984,785 | ||||||||||

| Income taxes | (5,130,644 | ) | (5,090,161 | ) | (6,602,194 | ) | (9,058,226 | ) | (15,042,327 | ) | |||||

| Income before extraordinary item | 10,262,052 | 9,219,190 | 18,981,725 | 21,155,286 | 34,942,458 | ||||||||||

| Extraordinary item, net | — | — | 12,499,576 | — | — | ||||||||||

| Net income | 10,262,052 | 9,219,190 | 31,481,301 | 21,155,286 | 34,942,458 | ||||||||||

| Foreign currency translation adjustment | 687,566 | 2,107,856 | 3,486,204 | 474,414 | 3,470,209 | ||||||||||

| Comprehensive income | $ | 10,949,618 | $ | 11,327,046 | $ | 34,967,505 | $ | 21,629,700 | $ | 38,412,667 | |||||

| Earnings per common share basic | $ | 0.34 | $ | 0.30 | $ | 1.04 | $ | 0.70 | $ | 1.14 | |||||

| Earnings per common share diluted | $ | 0.34 | $ | 0.30 | $ | 1.04 | $ | 0.70 | $ | 1.07 | |||||

| Weighted average common shares outstanding basic | 30,235,062 | 30,235,062 | 30,235,062 | 30,235,062 | 30,770,172 | ||||||||||

| Weighted average common shares outstanding diluted | 30,235,062 | 30,235,062 | 30,235,062 | 30,235,062 | 32,708,661 | ||||||||||

| Cash Flow Data | |||||||||||||||

| Net cash provided by (used in) | |||||||||||||||

| Operating Activities | $ | (5,953,059 | ) | $ | 1,212,951 | $ | 61,015,081 | $ | 11,250,820 | $ | 27,325,191 | ||||

| Investing Activities | (59,164 | ) | (13,689,661 | ) | (58,521,630 | ) | 234,814 | (136,156 | ) | ||||||

| Financing Activities | 5,759,286 | 14,167,583 | (3,805,052 | ) | (9,866,408 | ) | 3,435,399 | ||||||||

| Effect of exchange rate changes on cash | (57,807 | ) | 9,891 | 16,518 | 6,573 | 701,545 | |||||||||

| Net increase (decrease) in cash | $ | (310,744 | ) | $ | 1,700,764 | $ | (1,295,083 | ) | $ | 1,625,799 | $ | 31,325,979 | |||

2

| As of December 25, | |||||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | |||||||||||

| Balance Sheet Data | (unaudited) | (unaudited) | |||||||||||||

| Current assets | $ | 92,211,870 | $ | 69,443,412 | $ | 105,072,009 | $ | 133,002,971 | $ | 194,356,501 | |||||

| Total assets | 94,711,799 | 87,822,788 | 178,648,355 | 196,332,843 | 260,120,259 | ||||||||||

| Current liabilities | 57,741,400 | 59,977,634 | 86,240,752 | 88,795,899 | 91,775,418 | ||||||||||

| Long-term liabilities | 7,686,000 | — | 29,160,895 | 13,185,998 | 23,703,855 | ||||||||||

| Total liabilities | 65,427,400 | 59,977,634 | 115,401,647 | 101,981,897 | 115,479,273 | ||||||||||

| Stockholders’ equity | 29,284,399 | 27,845,154 | 63,246,708 | 94,350,946 | 144,640,986 | ||||||||||

Exchange Rate Information

Our reporting and financial statements are expressed in the U.S. dollar, which is our reporting and functional currency. However, substantially all of the revenues and expenses of our consolidated operating subsidiaries are denominated in RMB. This annual report contains translations of RMB amounts into U.S. dollars at specific rates solely for the convenience of the reader. The conversion of RMB into U.S. dollars in this annual report is based on daily RMB to U.S. Dollar Interbank Exchange Rates published on OANDA.com. Unless otherwise noted, all translations from RMB to U.S. dollars and from U.S. dollars to RMB in this annual report were made at a rate of RMB1 to US$0.1507, the rate in effect as of December 25, 2010. We make no representation that any RMB or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or RMB, as the case may be, at any particular rate, the rates stated below, or at all. The Chinese government imposes control over its foreign currency reserves in part through direct regulation of the conversion of RMB into foreign exchange. On June 19, 2011, the exchange rate was RMB1 to US$0.1546.

The following table sets forth information concerning exchange rates between the RMB and the U.S. dollar for the periods indicated. These rates are provided solely for your convenience and are not necessarily the exchange rates that we used in this annual report or will use in the preparation of our periodic reports or any other information to be provided to you. The source of these rates is daily RMB to U.S. Dollar Interbank Exchange Rates published on OANDA.com.

| InterBank Buying Rate | ||||||||||||

| Period End | Average(2) | High | Low | |||||||||

| (U.S. Dollar per RMB) | ||||||||||||

| Fiscal Year Ended: | ||||||||||||

| December 25, 2006 | 0.1281 | 0.1255 | 0.1278 | 0.1234 | ||||||||

| December 25, 2007 | 0.1360 | 0.1315 | 0.1356 | 0.1276 | ||||||||

| December 25, 2008 | 0.1462 | 0.1440 | 0.1466 | 0.1356 | ||||||||

| December 25, 2009 | 0.1468 | 0.1466 | 0.1466 | 0.1455 | ||||||||

| December 25, 2010 | 0.1507 | 0.1479 | 0.1508 | 0.1461 | ||||||||

| December 25, 2011 (through June 19, 2011) | 0.1546 | 0.1529 | 0.1546 | 0.1502 | ||||||||

| Most Recent Six Months Ended: | ||||||||||||

| December 25, 2010 | 0.1507 | 0.1491 | 0.1508 | 0.1465 | ||||||||

| January 25, 2011 | 0.1522 | 0.1497 | 0.1520 | 0.1465 | ||||||||

| February 25, 2011 | 0.1523 | 0.1505 | 0.1524 | 0.1465 | ||||||||

| March 25, 2011 | 0.1527 | 0.1512 | 0.1530 | 0.1489 | ||||||||

| April 25, 2011 | 0.1542 | 0.1517 | 0.1538 | 0.1491 | ||||||||

| May 25, 2011 | 0.1539 | 0.1523 | 0.1540 | 0.1495 | ||||||||

| June 25, 2011 (through June 19, 2011) | 0.1546 | 0.1529 | 0.1546 | 0.1502 | ||||||||

___________

(1) Annual averages are calculated using the average of the

rates on each calendar day of each month during the relevant year. Monthly

averages are calculated using the average of the daily rates during the relevant

month.

3

Capitalization and Indebtedness

Not applicable.

Reasons for the Offer and Use of Proceeds

Not applicable.

Risk Factors

An investment in our ordinary shares involves a high degree of risk. You should carefully consider the risks described below, together with all of the other information included in this annual report, before making an investment decision. If any of the following risks actually occurs, our business, financial condition or results of operations could suffer. In that case, the trading price of our ordinary shares could decline, and you may lose all or part of your investment.

RISKS RELATED TO OUR BUSINESS

The recent financial crisis could negatively affect our business, results of operations, and financial condition.

The recent credit crisis and turmoil in the global financial system may have an impact on our business and our financial condition, and we may face challenges if conditions in the financial markets do not improve. Our ability to access the capital markets may be restricted at a time when we would like, or need, to raise capital, which could have an impact on our flexibility to react to changing economic and business conditions. Our business requires access to substantial financing. If we are not able to obtain adequate financing in a timely manner, our ability to complete existing projects and expand our business could be materially adversely affected. In addition, these economic conditions also impact levels of consumer spending, which have recently deteriorated significantly and may remain depressed for the foreseeable future. Real estate market generally declines during recessionary periods and other periods where disposable income is adversely affected. If demand for our products fluctuates as a result of economic conditions or otherwise, our revenue and gross margin could be harmed.

Our business is susceptible to fluctuations in the real estate market of China, especially in certain areas of eastern China where our operations are concentrated, which may adversely affect our sales and results of operations.

Our business depends substantially on the conditions of the PRC real estate market. Demand for real estate in China has grown rapidly in the recent decade but such growth is often coupled with volatility in market conditions and fluctuations in real estate prices. For example, the rapid expansion of the real estate market in major provinces and cities in China in the early 1990s, such as Shanghai, Beijing and Guangdong province, led to an oversupply in the mid-1990s and a corresponding fall in real estate values and rentals in the second half of the decade. Following a period of rising real estate prices and transaction volume in most major cities, the industry experienced a severe downturn in 2008, with transaction volume in many major cities declining by more than 40% compared to 2007.

Average selling prices also declined in many cities during 2008. Fluctuations of supply and demand in China’s real estate market are caused by economic, social, political and other factors. To the extent fluctuations in the real estate market adversely affect real estate transaction volumes or prices, our financial condition and results of operations may be materially and adversely affected.

We are heavily dependent on the performance of the residential property market in China, which is at a relatively early development stage.

The residential property industry in the PRC is still in a relatively early stage of development. Although demand for residential property in the PRC has been growing rapidly in recent years, such growth is often coupled with volatility in market conditions and fluctuation in property prices. It is extremely difficult to predict how much and when demand will develop, as many social, political, economic, legal, and other factors, most of which are beyond our control, may affect the development of the market. The level of uncertainty is increased by the limited availability of accurate financial and market information and the overall low level of transparency in the PRC, especially in tier-two cities that have lagged in progress in these aspects when compared to tier-one cities.

4

The lack of a liquid secondary market for residential property may discourage investors from acquiring new properties. The limited amount of property mortgage financing available to PRC individuals may further inhibit demand for residential developments.

The PRC government has recently introduced certain policy and regulatory measures to control the rapid increase in housing prices and cool down the real estate market and our business may be materially and adversely affected by these government measures.

Since the second half of 2009, the PRC real estate market has experienced strong recovery from the financial crisis and housing prices rose rapidly in certain cities. In response to concerns over the scale of the increase in property investments, the PRC government has implemented measures and introduced policies to curtail property speculation and promote the healthy development of the real estate industry in China. On January 7, 2010, the PRC State Council issued a circular to control the rapid increase in housing prices and cool down the real estate market in China. It reiterated that the purchasers of a second residential property for their households must make down payments of no less than 40% of the purchase price and real estate developers must commence the sale within the mandated period as set forth in the pre-sale approvals and at the publicly announced prices. The circular also requested the local government to increase the effective supply of low-income housing and ordinary commodity housing and instructed the People’s Bank of China, or PBOC, and the China Bank Regulatory Commission to tighten the supervision of the bank lending to the real estate sector and mortgage financing. On February 25, 2010, the PBOC increased the reserve requirement ratio for commercial banks by 0.5% to 16.5% and has further increased it from 16.5% to 17.0% effective May 10, 2010. Further, in order to implement the requirements set out in the State Council’s circular, the Ministry of Land and Resources, or the MLR, issued a notice on March 8, 2010 in relation to increasing the supply of, and strengthening the supervision over, land for real estate development purposes. MLR’s notice stipulated that the floor price of a parcel of land must not be lower than 70% of the benchmark land price set for the area in which the parcel is located, and that real estate developers participating in land auctions must pay a deposit equivalent to 20% of the land parcel’s floor price.

In April 2010, the PRC State Council issued a further circular, which provided as follows: purchasers of a first residential property for their households with a gross floor area of greater than 90 square meters must make down payments of no less than 30% of the purchase price; purchasers of a second residential property for their households must make down payments of no less than 50% of the purchase price and the interest rate of any mortgage for such property must equal at least the benchmark interest rate plus 10%; and for purchasers of a third residential property, both the minimum down payment amount and applied interest rate must be significantly higher than the relevant minimum down payment and interest rate which would have been applicable prior to the issuance of the circular (the specific figures shall be decided by the relevant bank on a case-by-case based on the principle of proper risk management). Moreover, the circular provided that banks can decline to provide mortgage financing to either a purchaser of a third residential property or a non-resident purchaser.

It is possible that the government agencies may adopt further measures to implement the policies outlined in the January and April circulars. The full effect of the circulars on the real estate industry and our business will depend in large part on the implementation and interpretation of the circulars by governmental agencies, local governments and banks involved in the real estate industry. The PRC government’s policies and regulatory measures on the PRC real estate sector could limit our access to required financing and other capital resources, adversely affect the property purchasers’ ability to obtain mortgage financing or significantly increase the cost of mortgage financing, reduce market demand for our properties and increase our operating costs. We cannot be certain that the PRC government will not issue additional and more stringent regulations or measures or that agencies and banks will not adopt restrictive measures or practices in response to PRC governmental policies and regulations, which could substantially reduce pre-sales of our properties and cash flow from operations and substantially increase our financing needs, which would in turn materially and adversely affect our business, financial condition, results of operations and prospects.

Our sales will be affected if mortgage financing becomes more costly or otherwise becomes less attractive.

Substantially all purchasers of our residential properties rely on mortgages to fund their purchases. An increase in interest rates may significantly increase the cost of mortgage financing, thus affecting the affordability of residential properties. Since October 20, 2010, PBOC has raised the lending rates four times. As a result, the benchmark lending rate for loans with a term of over five years, which affects mortgage rates, was increased to 6.80% on April 6, 2011. The PRC government and commercial banks may also increase the down payment requirement, impose other conditions or otherwise change the regulatory framework in a manner that would make mortgage financing unavailable or unattractive to potential property purchasers. If the availability or attractiveness of mortgage financing is reduced or limited, many of our prospective customers may not be able to purchase our properties and, as a result, our business, liquidity and results of operations could be adversely affected.

5

If we are prevented from guaranteeing loans to prospective home purchasers, our sales and pre-sales may decline.

In line with industry practice, we provide guarantees to PRC banks with respect to loans procured by the purchasers of our properties, in the form of a transfer of 5% of the home purchasers’ loan amount from our bank account to a bank designated account, as collateral for the home purchasers’ timely debt service payments. The bank will release these deposits after construction is completed, final deliveries are made, and home purchasers have obtained the ownership documents necessary to secure a mortgage loan. If there are changes in laws, regulations, policies, and practices that would prohibit property developers from providing guarantees to banks in respect of mortgages offered to property purchasers and as a result, banks would not accept any alternative guarantees by third parties, or if no third party is available or willing in the market to provide such guarantees, it may become more difficult for property purchasers to obtain mortgages from banks and other financial institutions during sales and pre-sales of our properties. Such difficulties in financing could result in a substantially lower rate of sale and pre-sale of our properties, which would adversely affect our cash flow, financial condition, and results of operations. We are not aware of any impending changes in laws, regulations, policies, or practices that will prohibit such practice in China. However, there can be no assurance that such changes in laws, regulations, policies, or practices will not occur in China in the future.

We may be unable to acquire land use rights from the government through Longhai Group as we currently do which could increase our cost of sales.

Our revenue depends on the completion and sale of our projects, which in turn depends on our ability to acquire land use rights for such projects. Our land use rights costs are a major component of our cost of real estate sales and increases in such costs could diminish our gross margin. From time to time, we acquire our land use rights through companies owned by Longhai Group, a company wholly-owned by Mr. Antoine Cheng, our Chairman. Longhai Group’s primary business is infrastructure and building construction. Through its infrastructure construction business, Longhai Group works with local governments and often finances (by agreeing to be paid sometime following the completion of construction instead of being paid as construction progresses) the government’s public infrastructure projects that can include old city relocation projects. In exchange for such financing, the local governments invite Longhai Group to bid for premium parcels of land for residential use at public auction as a preferred candidate or grant Longhai Group the right of first refusal to bid for industrial parcels for which the Longhai Group already has land use rights, but whose use has been changed to real estate development. Since Longhai Group does not have the necessary license to engage in residential development in China, it typically sold companies owning these land use rights to us so that we could develop these parcels using our real estate development license.

Although we believe that the aforementioned way in which Longhai Group obtains land use rights is consistent with the PRC government’s long-term policy to develop healthy real estate market, we cannot assure you that the local government will continue to provide Longhai Group land use rights in this way in the future. If this happens, we will have to acquire our land use rights primarily through a public tender, auction or listing-for-sale. Competition in these bidding processes can result in higher land use rights costs for us. In addition, we may not successfully obtain desired land use rights at commercially reasonable costs due to the increasingly intense competition in the bidding processes. We may also need to acquire land use rights through acquisition, which could increase our costs.

We have significant short-term debt obligations, which mature in less than one year. Failure to extend those maturities of, or to refinance, that debt could result in defaults, and in certain instances, foreclosures on our assets. Moreover, we may be unable to obtain financing to fund ongoing operations and future growth.

The real estate development industry is capital intensive, and development requires significant up-front expenditures to acquire land and begin development. Accordingly, we incur substantial indebtedness to finance our development activities.

At December 25, 2010, we had short-term bank loans outstanding of $1,417,264, long-term bank loans of $35,414,500 maturing within one year, long-term bank loans of $0 maturing in more than one year, and notes payable of $0, which were secured by our land use rights and projects under construction. Failure to obtain extensions of the maturity dates of, or to refinance, these obligations or to obtain additional equity financing to meet these debt obligations would result in an event of default with respect to such obligations and could result in the foreclosure on the collateral. The sale of such collateral at foreclosure would significantly disrupt our business, which could significantly lower our sales and profitability. We may be able to refinance or obtain extensions of the maturities of all or some of such debt only on terms that significantly restrict our ability to operate, including terms that place additional limitations on our ability to incur other indebtedness, to pay dividends, to use our assets as collateral for other financing, to sell assets or to make acquisitions or enter into other transactions. Such restrictions may adversely affect our ability to finance our future operations or to engage in other business activities. If we finance the repayment of our outstanding indebtedness by issuing additional equity or convertible debt securities, such issuances could result in substantial dilution to our stockholders.

6

While we believe that our revenue growth projections and our ongoing cost controls will allow us to generate cash and achieve profitability in the foreseeable future, there is no assurance as to when or if we will be able to achieve our projections. Our future cash flows from operations, combined with our accessibility to cash and credit, may not be sufficient to allow us to finance ongoing operations or to make required investments for future growth. We may need to seek additional credit or access capital markets for additional funds. There is no assurance that we would be successful in this regard.

Our practice of pre-selling projects may expose us to substantial liabilities.

It is common practice by property developers in China, including us, to pre-sell properties (while still under construction), which involves certain risks. For example, we may fail to complete a property development that may have been fully or partially pre-sold, which would leave us liable to purchasers of pre-sold units for losses suffered by them without adequate resources to pay the liability if funds have been used on the project. In addition, if a pre-sold property development is not completed on time, the purchasers of pre-sold units may be entitled to compensation for late delivery. If the delay extends beyond a certain period, the purchasers may be entitled to terminate the pre-sale agreement and pursue a claim for damages that exceeds the amount paid and our ability to recoup the resulting liability from future sales.

We may not be able to successfully execute our strategy of expanding into new geographical markets in China, which could have a material adverse effect on our business and results of operations.

We plan to continue to expand our business into new geographical areas in China. Since China is a large and diverse market, consumer trends and demands may vary significantly by region and our experience in the markets in which we currently operate may not be applicable in other parts of China. As a result, we may not be able to leverage our experience to expand into other parts of China. When we enter new markets, we may face intense competition from companies with greater experience or an established presence in the targeted geographical areas or from other companies with similar expansion targets. Therefore, we may not be able to grow our sales in the new cities we enter due intense competitive pressures and or the substantial costs involved.

We are dependent on third-party subcontractors, manufacturers, and distributors for all architecture, engineering and construction services, and construction materials. A discontinued supply of such services and materials will adversely affect our projects.

We are dependent on third-party subcontractors, manufacturers, and distributors for all architecture, engineering and construction services, and construction materials. Services and materials purchased from our five largest subcontractors or suppliers accounted for 86.9% for the year ended December 25, 2010. A discontinued supply of such services and materials will adversely affect our construction projects and the success of the Company.

We are subject to extensive government regulation that could cause us to incur significant liabilities or restrict our business activities.

Regulatory requirements could cause us to incur significant liabilities and operating expenses and could restrict our business activities. We are subject to statutes and rules regulating, among other things, certain developmental matters, building and site design, and matters concerning the protection of health and the environment. Our operating expenses may be increased by governmental regulations, such as building permit allocation ordinances and impact and other fees and taxes, that may be imposed to defray the cost of providing certain governmental services and improvements. Any delay or refusal from government agencies to grant us necessary licenses, permits, and approvals could have an adverse effect on our operations.

7

We depend on the availability of additional human resources for future growth.

We are currently experiencing a period of significant growth in our sales volume. We believe that continued expansion is essential for us to remain competitive and to capitalize on the growth potential of our business. Such expansion may place a significant strain on our management and operations and financial resources. As our operations continue to grow, we will have to continually improve our management, operational, and financial systems, procedures and controls, and other resources infrastructure, and expand our workforce. There can be no assurance that our existing or future management, operating and financial systems, procedures, and controls will be adequate to support our operations, or that we will be able to recruit, retain, and motivate our employees. Further, there can be no assurance that we will be able to establish, develop, or maintain the business relationships beneficial to our operations, or to do so or to implement any of the above activities in a timely manner. Failure to manage our growth effectively could have a material adverse effect on our business and the results of our operations and financial condition.

We may be adversely affected by the fluctuation in raw material prices and selling prices of our products.

The land and raw materials used in our projects have experienced significant price fluctuations in the past. There is no assurance that they will not be subject to future price fluctuations or pricing control. The land and raw materials used in our projects may experience price volatility caused by events such as market fluctuations or changes in governmental programs. The market price of land and raw materials may also experience significant upward adjustment, if, for instance, there is a material under-supply or over-demand in the market. These price changes may ultimately result in increases in the selling prices of our products, and may, in turn, adversely affect our sales volume, sales, operating income, and net income.

We face intense competition from other real estate developers.

The property industry in the PRC is highly competitive. In the tier-two cities we focus on, local and regional property developers are our major competitors, and an increasing number of large state-owned and private national property developers have started entering these markets. Many of our competitors, especially the state-owned and private national property developers, are well capitalized and have greater financial, marketing, and other resources than we have. Some also have larger land banks, greater economies of scale, broader name recognition, a longer track record, and more established relationships in certain markets. In addition, the PRC government’s recent measures designed to reduce land supply further increased competition for land among property developers.

Competition among property developers may result in increased costs for the acquisition of land for development, increased costs for raw materials, shortages of skilled contractors, oversupply of properties, decrease in property prices in certain parts of the PRC, a slowdown in the rate at which new property developments will be approved and/or reviewed by the relevant government authorities and an increase in administrative costs for hiring or retaining qualified personnel, any of which may adversely affect our business and financial condition. Furthermore, property developers that are better capitalized than we are may be more competitive in acquiring land through the auction process. If we cannot respond to changes in market conditions as promptly and effectively as our competitors, or effectively compete for land acquisition through the auction systems and acquire other factors of production, our business and financial condition will be adversely affected.

In addition, risk of property over-supply is increasing in parts of China, where property investment, trading and speculation have become overly active. We are exposed to the risk that in the event of actual or perceived over-supply, property prices may fall drastically, and our revenue and profitability will be adversely affected.

We may have to suffer monetary losses by reducing up to $0.80 of the excise price of the warrants that we issued to our investors in the April 2010 private placement since the registration statement has not been declared effective within the time periods specified.

In connection with the April 2010 private placement described elsewhere in this report, we entered into a subscription agreement with the investors, or the Subscription Agreement. Under the terms of the Subscription Agreement, if a registration statement is not declared effective by the SEC within 180 days following the closing of the April 2010 private placement, then we are required to pay the investors, as liquidated damages, 1.0% of the amount invested for each 30-day period during which such failure continues, for up to a maximum of 10% of each investor’s investment pursuant to the Subscription Agreement. On October 11, 2010, we entered into Amendment No. 1 to the Subscription Agreement with certain investors, pursuant to which we amended Section 8.1 of the Subscription Agreement with respect to the liquidated damages that we may be liable for. Pursuant to Amendment No. 1, in lieu of the cash liquidated damages amount that would otherwise have been payable by us for our failure to cause the registration statement to be declared effective within the prescribed period, we are required to reduce the initial exercise price of the warrants issued to each investor by $0.08 per calendar month, or portion thereof, until such time that this registration statement is declared effective by the SEC; provided that, in no event will we be obligated to reduce the initial exercise price of the warrants by more than $0.80 in aggregate. We have failed to cause the registration statement to be declared effective by the SEC with the prescribed period. There can be no assurance that the registration statement will be declared effective by the SEC in the coming future. Therefore, we may have to suffer monetary losses by reducing up to $0.80 of the exercise price of the warrants.

8

We could be adversely affected by the occurrence of natural disasters.

From time to time, our developed sites may experience strong winds, storms, flooding and earth quakes. Natural disasters could impede operations, damage infrastructure necessary to our constructions and operations. The occurrence of natural disasters could adversely affect our business, the results of our operations, prospects and financial condition.

We have limited insurance coverage against damages or loss we might suffer.

The insurance industry in China is still in an early stage of development and business interruption insurance available in China offers limited coverage compared to that offered in many developed countries. We carry insurance for potential liabilities related to our vehicles, but we do not carry business interruption insurance and therefore any business disruption or natural disaster could result in substantial damages or losses to us. In addition, there are certain types of losses (such as losses from forces of nature) that are generally not insured because either they are uninsurable or insurance cannot be obtained on commercially reasonable terms. Should an uninsured loss or a loss in excess of insured limits occur, our business could be materially adversely affected. If we were to suffer any losses or damages to our properties, our business, financial condition and results of operations would be materially and adversely affected.

Our operating subsidiaries must comply with environmental protection laws that could adversely affect our profitability.

We are required to comply with the environmental protection laws and regulations promulgated by the national and local governments of the PRC. Some of these regulations govern the level of fees payable to government entities providing environmental protection services and the prescribed standards relating to construction. Although our construction technologies allow us to efficiently control the level of pollution resulting from our construction process, due to the nature of our business, wastes are unavoidably generated in the processes. If we fail to comply with any of these environmental laws and regulations in the PRC, depending on the types and seriousness of the violation, we may be subject to, among other things, warning from relevant authorities, imposition of fines, specific performance and/or criminal liability, forfeiture of profits made, or an order to close down our business operations and suspension of relevant permits.

Our business depends substantially on the continuing efforts of our senior executives and other key personnel, and our business may be severely disrupted if we lost their services.

Our future success heavily depends on the continued service of our senior executives and other key employees. In particular, we rely on the expertise and experience of Mr. Antoine Cheng, our Chairman, Mr. Weiqing Zhang, our Chief Executive Officer, Mr. Zhaohui John Liang, our Chief Financial Officer, and Mr. Yang Chen, our President. If one or more of our senior executives are unable or unwilling to continue to work for us in their present positions, we may have to spend a considerable amount of time and resources searching, recruiting, and integrating the replacements into our operations, which would substantially divert management’s attention from our business and severely disrupt our business. This may also adversely affect our ability to execute our business strategy. Moreover, if any of our senior executives joins a competitor or forms a competing company, we may lose customers, suppliers, know-how, and key employees.

Failure to achieve and maintain an effective system of internal control over financial reporting could have a material and adverse effect on the trading price of our ordinary shares.

We are subject to reporting obligations under the U.S. securities law. The Securities and Exchange Commission, or SEC, as required by Section 404 of the Sarbanes-Oxley Act of 2002, or SOX 404, adopted rules requiring every public company to include a management report on such company’s internal control over financial reporting in its annual report, which must also contain management’s assessment of the effectiveness of the company’s internal control over financial reporting. In addition, the independent registered public accounting firm auditing the financial statements of a company that is not a non-accelerated filer under Rule 12b-2 of the Securities Exchange Act of 1934, as amended, or the Exchange Act, must also attest to the operating effectiveness of the company’s internal controls.

9

Our management has concluded that our internal control over financial reporting was effective as of December 25, 2010. Our independent registered public accounting firm was not required to attest to the operating effectiveness of our internal controls since we are a non-accelerated filer. However, if we fail to maintain effective internal control over financial reporting in the future, our management and our independent registered public accounting firm (when required) may not be able to conclude that we have effective internal control over financial reporting at a reasonable assurance level. This could negatively affect the reliability of our financial information and reduce investors’ confidence in our reported financial information, which in turn could result in lawsuits being filed against us by our shareholders, otherwise harm our reputation or negatively impact the trading price of our ordinary shares. Furthermore, we have incurred and anticipate that we will continue to incur considerable costs and use significant management time and other resources in an effort to comply with SOX 404 and other requirements of the Sarbanes-Oxley Act.

RISKS RELATED TO DOING BUSINESS IN CHINA

Uncertainties with respect to the PRC legal system could limit the legal protections available to you and us.

We conduct substantially all of our business through our operating subsidiaries in the PRC. Our operating subsidiaries are generally subject to laws and regulations applicable to foreign investments in China and, in particular, laws applicable to foreign-invested enterprises. The PRC legal system is based on written statutes, and prior court decisions may be cited for reference but have limited precedential value. Since 1979, a series of new PRC laws and regulations have significantly enhanced the protections afforded to various forms of foreign investments in China. However, since the PRC legal system continues to evolve rapidly, the interpretations of many laws, regulations, and rules are not always uniform, and enforcement of these laws, regulations, and rules involve uncertainties, which may limit legal protections available to you and us. In addition, any litigation in China may be protracted and result in substantial costs and diversion of resources and management attention. In addition, most of our executive officers and directors are residents of China and not of the United States, and substantially all the assets of these persons are located outside the United States. As a result, it could be difficult for investors to affect service of process in the United States or to enforce a judgment obtained in the United States against our Chinese operations and subsidiaries.

You may have difficulty enforcing judgments against us.

Most of our assets are located outside of the United States and most of our current operations are conducted in the PRC. In addition, most of our directors and officers are nationals and residents of countries other than the United States. A substantial portion of the assets of these persons is located outside the United States. As a result, it may be difficult for you to effect service of process within the United States upon these persons. It may also be difficult for you to enforce in U.S. courts judgments on the civil liability provisions of the U.S. federal securities laws against us and our officers and directors, most of whom are not residents in the United States and the substantial majority of whose assets are located outside of the United States. In addition, there is uncertainty as to whether the courts of the PRC would recognize or enforce judgments of U.S. courts. Our counsel as to PRC law has advised us that the recognition and enforcement of foreign judgments are provided for under the PRC Civil Procedures Law. Courts in China may recognize and enforce foreign judgments in accordance with the requirements of the PRC Civil Procedures Law based on treaties between China and the country where the judgment is made or on reciprocity between jurisdictions. China does not have any treaties or other arrangements that provide for the reciprocal recognition and enforcement of foreign judgments with the United States. In addition, according to the PRC Civil Procedures Law, courts in the PRC will not enforce a foreign judgment against us or our directors and officers if they decide that the judgment violates basic principles of PRC law or national sovereignty, security, or the public interest. So it is uncertain whether a PRC court would enforce a judgment rendered by a court in the United States.

The PRC government exerts substantial influence over the manner in which we must conduct our business activities.

The PRC government has exercised and continues to exercise substantial control over virtually every sector of the Chinese economy through regulation and state ownership. Our ability to operate in China may be harmed by changes in its laws and regulations, including those relating to taxation, import and export tariffs, environmental regulations, land use rights, property, and other matters. We believe that our operations in China are in material compliance with all applicable legal and regulatory requirements. However, the central or local governments of the jurisdictions in which we operate may impose new, stricter regulations or interpretations of existing regulations that would require additional expenditures and efforts on our part to ensure our compliance with such regulations or interpretations.

10

Accordingly, government actions in the future, including any decision not to continue to support recent economic reforms and to return to a more centrally planned economy or regional or local variations in the implementation of economic policies, could have a significant effect on economic conditions in China or particular regions thereof and could require us to divest ourselves of any interest we then hold in Chinese properties or joint ventures.

Future inflation in China may inhibit our ability to conduct business in China.

In recent years, the Chinese economy has experienced periods of rapid expansion and highly fluctuating rates of inflation. During the past ten years, the rate of inflation in China has been as high as 5.9% and as low as -0.8%. These factors have led to the adoption by the Chinese government, from time to time, of various corrective measures designed to restrict the availability of credit or regulate growth and contain inflation. High inflation may in the future cause the Chinese government to impose controls on credit and/or prices, or to take other action, which could inhibit economic activity in China, and thereby harm the market for our products and our company.

Restrictions on currency exchange may limit our ability to receive and use our sales effectively.

The majority of our sales will be settled in RMB and U.S. dollars, and any future restrictions on currency exchanges may limit our ability to use revenue generated in RMB to fund any future business activities outside China or to make dividend or other payments in U.S. dollars. Although the Chinese government introduced regulations in 1996 to allow greater convertibility of the RMB for current account transactions, significant restrictions still remain, including primarily the restriction that foreign-invested enterprises may only buy, sell or remit foreign currencies after providing valid commercial documents, at those banks in China authorized to conduct foreign exchange business. In addition, conversion of RMB for capital account items, including direct investment and loans, is subject to governmental approval in China, and companies are required to open and maintain separate foreign exchange accounts for capital account items. We cannot be certain that the Chinese regulatory authorities will not impose more stringent restrictions on the convertibility of the RMB.

Fluctuations in exchange rates could adversely affect our business and the value of our securities.

Because our business transactions are denominated in RMB and our funding and results of operations will be denominated in USD, fluctuations in exchange rates between USD and RMB will affect our balance sheet and financial results. Since July 2005, RMB is no longer solely pegged to the USD but instead is pegged against a basket of currencies as a whole in order to keep a more stable exchange rate for international trading. With the very strong economic growth in China in the last few years, RMB is facing very high pressure to appreciate against USD. Such pressure could result more fluctuations in exchange rates and in turn our business would be suffered from higher exchange rate risk. There are very limited hedging tools available in China to hedge our exposure in exchange rate fluctuations. The hedging tools that are available are also ineffective in the sense that these hedges cannot be freely preformed in the PRC financial market, and more important, the frequent changes in PRC exchange control regulations would limit our hedging ability for RMB.

Restrictions under PRC law on our PRC subsidiaries’ ability to make dividends and other distributions could materially and adversely affect our ability to grow, make investments or acquisitions that could benefit our business, pay dividends to you, and otherwise fund and conduct our business.

Substantially all of our sales are earned by our PRC subsidiaries. However, as discussed more fully under Item 4, “Information on the Company—Business Overview—PRC Government Regulations—Dividend Distributions,” PRC regulations restrict the ability of our PRC subsidiaries to make dividends and other payments to their offshore parent company. Any limitations on the ability of our PRC subsidiaries to transfer funds to us could materially and adversely limit our ability to grow, make investments or acquisitions that could be beneficial to our business, pay dividends and otherwise fund and conduct our business.

Failure to comply with PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident shareholders to personal liability, limit our ability to acquire PRC companies or to inject capital into our PRC subsidiaries, limit our PRC subsidiaries’ ability to distribute profits to us or otherwise materially adversely affect us.

In October 2005, the PRC State Administration of Foreign Exchange, or SAFE, issued the Notice on Relevant Issues in the Foreign Exchange Control over Financing and Return Investment Through Special Purpose Companies by Residents Inside China, generally referred to as Circular 75. Circular 75 and its implementing guidelines, issued in June 2007 (known as Notice 106), require PRC residents to register with the competent local SAFE branch before establishing or acquiring control over an offshore special purpose company, or SPV, for the purpose of engaging in an equity financing outside of China. See Item 4, “Information on the Company—Business Overview—PRC Government Regulations—Circular 75” for a detailed discussion of Circular 75 and its implementation.

11

We have asked our shareholders, who are PRC residents as defined in Circular 75, to register with the relevant branch of SAFE, as currently required, in connection with their equity interests in us and our acquisitions of equity interests in our PRC subsidiaries. However, we cannot provide any assurances that they can obtain the above SAFE registrations required by Circular 75 and Notice 106. Moreover, because of uncertainty over how Circular 75 will be interpreted and implemented, and how or whether SAFE will apply it to us, we cannot predict how it will affect our business operations or future strategies. For example, our present and prospective PRC subsidiaries’ ability to conduct foreign exchange activities, such as the remittance of dividends and foreign currency-denominated borrowings, may be subject to compliance with Circular 75 and Notice 106 by our PRC resident beneficial holders.

In addition, such PRC residents may not always be able to complete the necessary registration procedures required by Circular 75 and Notice 106. We also have little control over either our present or prospective direct or indirect shareholders or the outcome of such registration procedures. A failure by our PRC resident beneficial holders or future PRC resident shareholders to comply with Circular 75 and Notice 106, if SAFE requires it, could subject these PRC resident beneficial holders to fines or legal sanctions, restrict our overseas or cross-border investment activities, limit our subsidiaries’ ability to make distributions or pay dividends or affect our ownership structure, which could adversely affect our business and prospects.

Our business and financial performance may be materially adversely affected if the PRC regulatory authorities determine that our acquisition of Oumei constitutes a Round-trip Investment without MOFCOM approval.

On August 8, 2006, six PRC regulatory agencies promulgated the Regulation on Mergers and Acquisitions of Domestic Companies by Foreign Investors which were further amended by PRC Ministry of Commerce, or MOFCOM, on June 22, 2009, or the 2006 M&A Rule. Among other things, the 2006 M&A Rule regulates “Round-trip Investments,” defined as having taken place when a PRC business that is owned by PRC individual(s) is sold to a non-PRC entity that is established or controlled, directly or indirectly, by those same PRC individual(s). See Item 4, “Information on the Company—Business Overview—PRC Government Regulations—Mergers and Acquisitions” for a detailed discussion of the 2006 M&A Rule.

Leewell acquired Oumei in 2007 from Mr. Weiqing Zhang and Ms. Xiaoyan Cheng. At the time of the acquisition, Leewell was owned and controlled by Mr. Li Zhou, a citizen of the Commonwealth of Australia, who was acting as a nominee for Mr. Zhang and Ms. Cheng. The PRC authorities could take the position that this transaction therefore constituted a “Round-Trip Investment” requiring the prior approval of the central office of MOFCOM in Beijing, which we did not obtain. If the PRC authorities take this position, they could invalidate our acquisition and ownership of our Chinese subsidiaries. If this were to happen, we would replace our ownership structure of Oumei with a series of contractual arrangements which would give us control over, and the economic benefit of, the operations of our Chinese subsidiaries. These arrangements are described more fully under Item 4, “Information on the Company—Business Overview—PRC Government Regulations—Mergers and Acquisitions.”

Additionally, the PRC regulatory authorities may take the view that these transactions require the prior approval of the China Securities Regulatory Commission, or CSRC, before MOFCOM approval is obtained. If we cannot obtain MOFCOM or CSRC approval if required by the PRC regulatory authorities to do so, the PRC regulatory authorities may impose fines and penalties on our operations in the PRC, limit our operating privileges in the PRC, delay or restrict the repatriation of the proceeds from our financing activities in other countries into the PRC, restrict or prohibit payment or remittance of dividends to us or take other actions that could have a material adverse effect on our business, financial condition, results of operations, reputation and prospects, as well as the trading price of our shares.

Under the New Enterprise Income Tax Law, we may be classified as a “resident enterprise” of China. Such classification will likely result in unfavorable tax consequences to us and our non-PRC shareholders.

China passed a New Enterprise Income Tax Law, or the EIT Law, and its implementing rules, both of which became effective on January 1, 2008. Under the EIT Law, an enterprise established outside of China with “de facto management bodies” within China is considered a “resident enterprise,” meaning that it can be treated in a manner similar to a Chinese enterprise for enterprise income tax purposes. See Item 4, “Information on the Company—Business Overview—PRC Government Regulations—Dividend Distributions” for a detailed discussion of the EIT Law.

12

It remains unclear whether the PRC tax authorities would require or permit our overseas registered entities to be treated as PRC resident enterprises. We do not currently consider our company to be a PRC resident enterprise. However, if the PRC tax authorities determine that we are a “resident enterprise” for PRC enterprise income tax purposes, a number of unfavorable PRC tax consequences could follow. First, we may be subject to the enterprise income tax at a rate of 25% on our worldwide taxable income as well as PRC enterprise income tax reporting obligations. In our case, this would mean that our non-China source income would be subject to PRC enterprise income tax at a rate of 25%. Second, although under the EIT Law and its implementing rules dividends paid to us from our PRC subsidiaries would qualify as “tax-exempt income,” we cannot guarantee that such dividends will not be subject to a 10% withholding tax, as the PRC foreign exchange control authorities, which enforce the withholding tax, have not yet issued guidance with respect to the processing of outbound remittances to entities that are treated as resident enterprises for PRC enterprise income tax purposes. Finally, it is possible that future guidance issued with respect to the new “resident enterprise” classification could result in a situation in which a 10% withholding tax is imposed on dividends we pay to our non-PRC shareholders and with respect to gains derived by our non-PRC shareholders from transferring our shares.

We may be exposed to liabilities under the Foreign Corrupt Practices Act and Chinese anti-corruption laws, and any determination that we violated these laws could have a material adverse effect on our business.

We are subject to the Foreign Corrupt Practices Act, or FCPA, and other laws that prohibit improper payments or offers of payments to foreign governments and their officials and political parties by U.S. persons and issuers as defined by the statute, for the purpose of obtaining or retaining business. We have operations, agreements with third parties, and make most of our sales in China. The PRC also strictly prohibits bribery of government officials. Our activities in China create the risk of unauthorized payments or offers of payments by the employees, consultants, sales agents, or distributors of our Company, even though they may not always be subject to our control. It is our policy to implement safeguards to discourage these practices by our employees. However, our existing safeguards and any future improvements may prove to be less than effective, and the employees, consultants, sales agents, or distributors of our Company may engage in conduct for which we might be held responsible. Violations of the FCPA or Chinese anti-corruption laws may result in severe criminal or civil sanctions, and we may be subject to other liabilities, which could negatively affect our business, operating results and financial condition. In addition, the U.S. government may seek to hold our Company liable for successor liability FCPA violations committed by companies in which we invest or that we acquire.

RISKS RELATED TO THE MARKET FOR OUR ORDINARY SHARES

There is no current trading market for our ordinary shares, and there is no assurance of an established public trading market, which would adversely affect the ability of our investors to sell their securities in the public market.

Our ordinary shares are not currently listed or quoted for trading on any national securities exchange or national quotation system. We have applied for the listing of our ordinary shares on the NASDAQ Global Market under the symbol “OMEI”. There is no guarantee that the NASDAQ Global Market, or any other exchange or quotation system, will permit our shares to be listed and traded. If we fail to obtain a listing on the NASDAQ Global Market, we may seek quotation on the OTC Bulletin Board. FINRA has enacted changes that limit quotations on the OTC Bulletin Board to securities of issuers that are current in their reports filed with the SEC. The effect on the OTC Bulletin Board of these rule changes and other proposed changes cannot be determined at this time. The OTC Bulletin Board is an inter-dealer, over-the-counter market that provides significantly less liquidity than the NASDAQ Global Market. The quotation of our shares on the OTC Bulletin Board may result in a less liquid market available for existing and potential stockholders to trade our shares, could depress the trading price of our ordinary shares and could have a long-term adverse impact on our ability to raise capital in the future.

The price of our ordinary shares could be volatile and could decline at a time when you want to sell your holdings.

We have applied to have our ordinary shares listed on the NASDAQ Global Market under the symbol “OMEI”. Although we believe that the NASDAQ listing will improve the liquidity for our ordinary shares, there is no assurance that the listing will improve volume, reduce volatility and stabilize our share price. Numerous factors, many of which are beyond our control, may cause the market price of our ordinary shares to fluctuate significantly. These factors include:

-

our earnings releases, actual or anticipated changes in our earnings, fluctuations in our operating results or our failure to meet the expectations of financial market analysts and investors;

-

changes in financial estimates by us or by any securities analysts who might cover our stock;

- speculation about our business in the press or the investment community;

13

-

significant developments relating to our relationships with our customers or suppliers;

-

stock market price and volume fluctuations of other publicly traded companies and, in particular, those that are in the real estate industry;

-

customer demand for our projects;

-

investor perceptions of the real estate industry in general and our company in particular;

-

the operating and stock performance of comparable companies;

-

general economic conditions and trends;

-

major catastrophic events;

-

announcements by us or our competitors of new products, significant acquisitions, strategic partnerships or divestitures;

-

changes in accounting standards, policies, guidance, interpretation or principles;

-

loss of external funding sources;

-

failure to maintain compliance with NASDAQ rules;

-

sales of our ordinary shares, including sales by our directors, officers or significant shareholders; and

- additions or departures of key personnel.

Securities class action litigation is often instituted against companies following periods of volatility in their stock price. This type of litigation could result in substantial costs to us and divert our management’s attention and resources.

Moreover, securities markets may from time to time experience significant price and volume fluctuations for reasons unrelated to operating performance of particular companies. For example, from September 2008 until June 2009, securities markets in the United States, China and throughout the world experienced a historically large decline in share price. These market fluctuations may adversely affect the price of our ordinary shares and other interests in our company at a time when you want to sell your interest in us.

We may be subject to penny stock regulations and restrictions and you may have difficulty selling our ordinary shares.

The SEC has adopted regulations which generally define so-called “penny stocks” as an equity security that has a market price of less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exemptions. If our ordinary shares become a “penny stock”, we may become subject to Rule 15g-9 under the Exchange Act, or the Penny Stock Rule. This rule imposes additional sales practice requirements on broker-dealers that sell such securities to persons other than established customers and “accredited investors” (generally, individuals with a net worth in excess of $1,000,000 or annual income exceeding $200,000, or $300,000 together with their spouses). For transactions covered by Rule 15g-9, a broker-dealer must make a special suitability determination for the purchaser and receive the purchaser’s written consent to the transaction prior to sale. As a result, this rule may affect the ability of broker-dealers to sell our securities and may affect the ability of purchasers to sell any of our securities in the secondary market.

For any transaction involving a penny stock, unless exempt, the rules require delivery, prior to any transaction in a penny stock, of a disclosure schedule prepared by the SEC relating to the penny stock market. Disclosure is also required to be made about sales commissions payable to both the broker-dealer and the registered representative and current quotations for the securities. Finally, monthly statements are required to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stock.

There can be no assurance that our ordinary shares will qualify for exemption from the Penny Stock Rule. In any event, even if our ordinary shares were exempt from the Penny Stock Rule, we would remain subject to Section 15(b)(6) of the Exchange Act, which gives the SEC the authority to restrict any person from participating in a distribution of penny stock if the SEC finds that such a restriction would be in the public interest.

We do not intend to pay dividends for the foreseeable future.

For the foreseeable future, we intend to retain any earnings to finance the development and expansion of our business, and we do not anticipate paying any cash dividends on our ordinary shares. Accordingly, investors must be prepared to rely on sales of their ordinary shares after price appreciation to earn an investment return, which may never occur. Investors seeking cash dividends should not purchase our ordinary shares. Any determination to pay dividends in the future will be made at the discretion of our board of directors and will depend on our results of operations, financial condition, contractual restrictions, restrictions imposed by applicable law and other factors our board of directors deems relevant.

14

Holders of our ordinary shares may face difficulties in protecting their interests because we are incorporated under Cayman Islands law.

Our corporate affairs are governed by our amended and restated memorandum and articles of association, and by the Companies Law (2010 Revision) and the common law of the Cayman Islands. The rights of our shareholders and the fiduciary responsibilities of our directors under Cayman Islands law are not as clearly established as under statutes or judicial precedent in existence in jurisdictions in the United States. Therefore, shareholders may have more difficulty in protecting their interests in the face of actions by our management or board of directors than would shareholders of a corporation incorporated in a jurisdiction in the United States, due to the comparatively less developed nature of Cayman Islands law in this area.