UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

For the quarterly period ended March 31, 2024

Commission File Number 001-33289

ENSTAR GROUP LIMITED

(Exact name of Registrant as specified in its charter)

| BERMUDA | N/A | ||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

(Address of principal executive offices, including zip code)

Registrant’s telephone number, including area code: (441 ) 292-3645

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered | |||||||||

| LLC | |||||||||||

| LLC | |||||||||||

| Fixed-to-Floating Rate Perpetual Non-Cumulative Preferred Share, Series D, Par Value $1.00 Per Share | |||||||||||

| LLC | |||||||||||

| Perpetual Non-Cumulative Preferred Share, Series E, Par Value $1.00 Per Share | |||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | Emerging growth company | |||||||||||||||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As at May 1, 2024, the registrant had outstanding 15,229,358 voting ordinary shares, par value $1.00 per share.

1

Enstar Group Limited

Quarterly Report on Form 10-Q

For the Period Ended March 31, 2024

Table of Contents

| Page | ||||||||

| PART I | ||||||||

| Item 1. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

2

GLOSSARY OF KEY TERMS

| A&E | Asbestos and environmental | |||||||

| Acquisition costs | Costs that are directly related to the successful efforts of acquiring new insurance contracts or renewing existing insurance contracts, and which principally consist of incremental costs such as: commissions, brokerage expenses, premium taxes and other fees incurred at the time that a contract or policy is issued. | |||||||

| ADC | Adverse development cover – A retrospective reinsurance arrangement that will insure losses in excess of an established reserve and provide protection up to a contractually agreed amount. | |||||||

| Adjusted RLE | Adjusted run-off liability earnings - Non-GAAP financial measure calculated by dividing adjusted prior period development by average adjusted net loss reserves. See “Non-GAAP Financial Measures” for reconciliation. | |||||||

| Adjusted ROE | Adjusted return on equity - Non-GAAP financial measure calculated by dividing adjusted operating income (loss) attributable to Enstar ordinary shareholders by adjusted opening Enstar ordinary shareholders’ equity. See “Non-GAAP Financial Measures” for reconciliation. | |||||||

| Adjusted TIR | Adjusted total investment return - Non-GAAP financial measure calculated by dividing adjusted total investment return by average adjusted total investable assets. See “Non-GAAP Financial Measures” for reconciliation. | |||||||

| AFS | Available-for-sale | |||||||

| Allianz | Allianz SE | |||||||

| AmTrust | AmTrust Financial Services, Inc. | |||||||

Annualized | Calculation of the quarterly result or year-to-date result multiplied by four and then divided by the number of quarters elapsed within the applicable year-to-date period. | |||||||

| AOCI | Accumulated other comprehensive income | |||||||

APIC | Additional Paid-in Capital | |||||||

| ASC | Accounting Standards Codification | |||||||

| ASU | Accounting Standards Update | |||||||

| Arden | Arden Reinsurance Company Ltd. | |||||||

| Atrium | Atrium Underwriting Group Limited | |||||||

bps | Basis point(s) | |||||||

| BMA | Bermuda Monetary Authority | |||||||

| BSCR | Bermuda Solvency Capital Requirement | |||||||

| BVPS | Book value per ordinary share - GAAP financial measure calculated by dividing Enstar ordinary shareholders’ equity by the number of ordinary shares outstanding. | |||||||

| Cavello | Cavello Bay Reinsurance Limited, a wholly-owned subsidiary | |||||||

| Citco | Citco III Limited | |||||||

| CLO | Collateralized loan obligation | |||||||

| Core Specialty | Core Specialty Insurance Holdings, Inc. | |||||||

| DCo | DCo LLC | |||||||

| Defendant A&E liabilities | Defendant asbestos and environmental liabilities - Non-insurance liabilities relating to amounts for indemnity and defense costs for pending and future claims, as well as amounts for environmental liabilities associated with properties. | |||||||

| DCA | Deferred charge asset - The amount by which estimated ultimate losses payable exceed the consideration received at the inception of a retroactive reinsurance agreement and that are subsequently amortized over the estimated loss settlement period. | |||||||

DGL | Deferred gain liability - The amount by which consideration received exceeds estimated ultimate losses payable at the inception of a retroactive reinsurance agreement and that are subsequently amortized over the estimated loss settlement period. | |||||||

| EB Trust | Enstar Group Limited Employee Benefit Trust | |||||||

| Enhanzed Re | Enhanzed Reinsurance Ltd. | |||||||

| Enstar | Enstar Group Limited and its consolidated subsidiaries | |||||||

3

| Enstar Finance | Enstar Finance LLC | |||||||

| Exchange Transaction | The exchange of a portion of our indirect interest in Northshore for all of the Trident V Funds’ indirect interest in StarStone U.S. | |||||||

| FAL | Funds at Lloyd's - A deposit in the form of cash, securities, letters of credit or other approved capital instrument that satisfies the capital requirement to support the Lloyd's syndicate underwriting capacity. | |||||||

FDBVPS | Fully diluted book value per ordinary share - Non-GAAP financial measure calculated by dividing Enstar ordinary shareholders’ equity by the number of ordinary shares outstanding, adjusted for equity awards granted and not yet vested (similar to the calculation of diluted earnings per share). See “Non-GAAP Financial Measures” in Item 7 for reconciliation. | |||||||

| Funds held | The account created with premium due to the reinsurer pursuant to the reinsurance agreement, the balance of which is credited with investment income and losses paid are deducted. | |||||||

| Funds held by reinsured companies | Funds held, as described above, where we receive a fixed crediting rate of return or other contractually agreed return on the assets held. | |||||||

| Funds held - directly managed | Funds held, as described above, where we receive the actual investment portfolio return on the assets held. | |||||||

| Future policyholder benefits | The liability relating to life reinsurance contracts, which are based on the present value of anticipated future cash flows and mortality rates. | |||||||

| IBNR | Incurred but not reported - The estimated liability for unreported claims that have been incurred, as well as estimates for the possibility that reported claims may settle for amounts that differ from the established case reserves as well as the potential for closed claims to re-open. | |||||||

| Investable assets | The sum of total investments, cash and cash equivalents, restricted cash and cash equivalents and funds held | |||||||

| JSOP | Joint Share Ownership Plan | |||||||

| LAE | Loss adjustment expenses | |||||||

| Lloyd's | This term may refer to either the society of individual and corporate underwriting members that pool and spread risks as members of one or more syndicates, or the Corporation of Lloyd’s, which regulates and provides support services to the Lloyd’s market | |||||||

| LOC | Letters of credit | |||||||

| LPT | Loss Portfolio Transfer - Retroactive reinsurance transaction in which loss obligations that are already incurred are ceded to a reinsurer, subject to any stipulated limits | |||||||

Monument Midco | Monument Midco Limited, a wholly owned subsidiary of Monument Re | |||||||

| Monument Re | Monument Insurance Group Limited | |||||||

| Morse TEC | Morse TEC LLC | |||||||

| NAV | Net asset value | |||||||

| NCI | Noncontrolling interests | |||||||

| New business | Material transactions, which generally take the form of reinsurance or direct business transfers, or business acquisitions. | |||||||

| Northshore | Northshore Holdings Limited | |||||||

| OLR | Outstanding loss reserves - Provisions for claims that have been reported and accrued but are unpaid at the balance sheet date. | |||||||

| Parent Company | Enstar Group Limited, excluding its consolidated subsidiaries | |||||||

| pp | Percentage point(s) | |||||||

| PPD | Prior period development - Changes to loss estimates recognized in the current calendar year that relate to loss reserves established in previous calendar years. | |||||||

| Private equity funds | Investments in limited partnerships and limited liability companies | |||||||

QBE | QBE Insurance Group Limited | |||||||

RACQ | RACQ Insurance Limited | |||||||

| Reinsurance to close (RITC) | A business transaction to transfer estimated future liabilities attached to a given year of account of a Lloyd's syndicate into a later year of account of either the same or different Lloyd's syndicate in return for a premium. | |||||||

4

| Reserves for losses and LAE | Management's best estimate of the ultimate cost of settling losses as of the balance sheet date. This includes OLR and IBNR. | |||||||

| Retroactive reinsurance | Contracts that provide indemnification for losses and LAE with respect to past loss events. | |||||||

| RLE | Run-off liability earnings – GAAP-based financial measure calculated by dividing prior period development by average net loss reserves. | |||||||

| RNCI | Redeemable noncontrolling interests | |||||||

| ROE | Return on equity - GAAP-based financial measure calculated by dividing net income (loss) attributable to Enstar ordinary shareholders by opening Enstar ordinary shareholders’ equity | |||||||

| Run-off | A line of business that has been classified as discontinued by the insurer that initially underwrote the given risk | |||||||

| Run-off portfolio | A group of insurance policies classified as run-off. | |||||||

| SEC | U.S. Securities and Exchange Commission | |||||||

| SGL No. 1 | SGL No. 1 Limited | |||||||

| StarStone International | StarStone's non-U.S. operations | |||||||

| StarStone U.S. | StarStone U.S. Holdings, Inc. and its subsidiaries | |||||||

| Stone Point | Stone Point Capital LLC | |||||||

| TIR | Total investment return - GAAP financial measure calculated by dividing total investment return, including other comprehensive income, for the applicable period by average total investable assets | |||||||

| Trident V Funds | Trident V, L.P., Trident V Parallel Fund, L.P. and Trident V Professionals Fund, L.P. | |||||||

| U.S. GAAP | Accounting principles generally accepted in the United States of America | |||||||

| ULAE | Unallocated loss adjustment expenses - Loss adjustment expenses relating to run-off costs for the estimated payout of the run-off, such as internal claim management or associated operational support costs. | |||||||

Unearned premium | The unexpired portion of policy premiums that will be earned over the remaining term of the insurance contract. | |||||||

| VIE | Variable interest entities | |||||||

5

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This quarterly report and the documents incorporated by reference herein contain statements that constitute "forward-looking statements" within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, with respect to our financial condition, results of operations, business strategies, operating efficiencies, competitive positions, growth opportunities, plans and objectives of our management, as well as the markets for our securities and the insurance and reinsurance sectors in general.

Statements that include words such as "estimate," "project," "plan," "intend," "expect," "anticipate," "believe," "would," "should," "could," "seek," "may" and similar statements of a future or forward-looking nature identify forward-looking statements for purposes of the federal securities laws or otherwise.

All forward-looking statements are necessarily estimates or expectations, and not statements of historical fact, reflecting the best judgment of our management and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by the forward-looking statements.

These forward looking statements should, therefore, be considered in light of various important factors, including those set forth in this report and in our Annual Report on Form 10-K for the year ended December 31, 2023, which could cause actual results to differ materially from those suggested by the forward-looking statements. These risk factors include:

•the adequacy of our loss reserves and the need to adjust such reserves as claims develop over time, including due to the impact of emerging claim and coverage issues and disputes that could impact reserve adequacy;

•risks relating to our acquisitions, including our ability to evaluate opportunities, successfully price acquisitions, address operational challenges, support our planned growth and assimilate acquired portfolios and companies into our internal control system in order to maintain effective internal controls, provide reliable financial reports and prevent fraud;

•risks relating to climate change and its potential impact on the returns from our run-off business and our investments;

•changes in tax laws or regulations applicable to us or our subsidiaries, including the Bermuda Corporate Income Tax, or the risk that we or one of our non-U.S. subsidiaries become subject to significant, or significantly increased, income taxes in the U.S. or elsewhere;

•the risk that U.S. persons who own our ordinary shares might become subject to adverse U.S. tax consequences as a result of related person insurance income;

•risks relating to our ability to obtain regulatory approvals, including the timing, terms and conditions of any such approvals, and to satisfy other closing conditions in connection with our acquisition agreements, which could affect our ability to complete acquisitions;

•risks relating to the variability of statutory capital requirements and the risk that we may require additional capital in the future, which may not be available or may be available only on unfavorable terms;

•the risk that our reinsurance subsidiaries may not be able to provide the required collateral to ceding companies pursuant to their reinsurance contracts, including through the use of letters of credit;

•risks relating to the availability and collectability of our ceded reinsurance;

•the ability of our subsidiaries to distribute funds to us and the resulting impact on our liquidity;

•losses due to foreign currency exchange rate fluctuations;

•the risk that the value of our investment portfolios and the investment income that we receive from these portfolios may decline materially as a result of market fluctuations and economic conditions, including those related to interest rates, credit spreads and equity prices (including the risk that we may realize losses related to declines in the value of our investments portfolios if we elect to, or are required to, sell investments with unrealized losses);

•risks relating to our ability to structure our investments in a manner that recognizes our liquidity needs;

•risks relating to our strategic investments in alternative asset classes and joint ventures, which are illiquid and may be volatile;

6

•risks relating to our ability to accurately value our investments, which requires methodologies, estimates and assumptions that can be highly subjective, and the inaccuracy of which could adversely affect our financial condition;

•risks relating to our liquidity demands and the structure of our investment portfolios, which may adversely affect the performance of our investment portfolio and financial results;

•risks relating to the complex regulatory environment in which we operate, including that ongoing or future industry regulatory developments will disrupt our business, affect the ability of our subsidiaries to operate in the ordinary course or to make distributions to us, or mandate changes in industry practices in ways that increase our costs, decrease our revenues or require us to alter aspects of the way we do business;

•risks relating to laws and regulations regarding sanctions and foreign corrupt practices, the violation of which could adversely affect our financial condition and results of operations;

•loss of key personnel;

•the risk that some of our directors, large shareholders and their affiliates have interests that can create conflicts of interest through related party transactions;

•the risk that outsourced providers could breach their obligations to us which could adversely affect our business and results of operations;

•operational risks, including cybersecurity events, external hazards, human failures or other difficulties with our information technology systems that could disrupt our business or result in the loss of critical and confidential information, increased costs; and

•risks relating to the ownership of our shares resulting from certain provisions of our bye-laws and our status as a Bermuda company.

The factors listed above should not be construed as exhaustive and should be read in conjunction with the Risk Factors that are included in our Annual Report on Form 10-K for the year ended December 31, 2023. We undertake no obligation to publicly update or review any forward-looking statement, whether to reflect any change in our expectations with regard thereto, or as a result of new information, future developments or otherwise, except as required by law.

7

PART I — FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

| CONDENSED CONSOLIDATED FINANCIAL STATEMENTS | Page | ||||

Unaudited Condensed Consolidated Statements of Operations for the three months ended March 31, 2024 and 2023 | |||||

Unaudited Condensed Consolidated Statements of Cash Flows for the three months ended March 31, 2024 and 2023 | |||||

Enstar Group Limited | First Quarter 2024 | Form 10-Q 8

ENSTAR GROUP LIMITED

UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS

As of March 31, 2024 and December 31, 2023

| March 31, 2024 | December 31, 2023 | ||||||||||

| (expressed in millions of U.S. dollars, except share data) | |||||||||||

| ASSETS | |||||||||||

| Short-term investments, trading, at fair value | $ | $ | |||||||||

Short-term investments, available-for-sale, at fair value (amortized cost: 2024 — $ | |||||||||||

| Fixed maturities, trading, at fair value | |||||||||||

Fixed maturities, available-for-sale, at fair value (amortized cost: 2024 — $ | |||||||||||

| Funds held | |||||||||||

Equities, at fair value (cost: 2024 — $ | |||||||||||

Other investments, at fair value (includes consolidated variable interest entity: 2024 - $ | |||||||||||

| Equity method investments | |||||||||||

Cash and cash equivalents (includes consolidated variable interest entity: 2024 — $ | |||||||||||

| Restricted cash and cash equivalents | |||||||||||

| Accrued interest receivable | |||||||||||

Reinsurance balances recoverable on paid and unpaid losses (net of allowance: 2024 — $ | |||||||||||

| Other assets | |||||||||||

| TOTAL ASSETS | $ | $ | |||||||||

| LIABILITIES | |||||||||||

| $ | $ | ||||||||||

| Insurance and reinsurance balances payable | |||||||||||

| Debt obligations | |||||||||||

Other liabilities (includes consolidated variable interest entity: 2024 — $ | |||||||||||

| TOTAL LIABILITIES | |||||||||||

Voting ordinary shares (par value $ | |||||||||||

| Preferred Shares: | |||||||||||

Series C Preferred Shares (issued and held in treasury 2024 and 2023: | |||||||||||

Series D Preferred Shares (issued and outstanding 2024 and 2023: | |||||||||||

Series E Preferred Shares (issued and outstanding 2024 and 2023: | |||||||||||

| Treasury shares, at cost: | |||||||||||

Series C Preferred shares (2024 and 2023: | ( | ( | |||||||||

Joint Share Ownership Plan (voting ordinary shares, held in trust 2024 and 2023: | ( | ( | |||||||||

| Additional paid-in capital | |||||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

| Retained earnings | |||||||||||

| Total Enstar Shareholders’ Equity | |||||||||||

| TOTAL SHAREHOLDERS’ EQUITY | |||||||||||

| TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY | $ | $ | |||||||||

Enstar Group Limited | First Quarter 2024 | Form 10-Q 9

ENSTAR GROUP LIMITED

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

For the Three Months Ended March 31, 2024 and 2023

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (expressed in millions of U.S. dollars, except share and per share data) | |||||||||||

| REVENUES | |||||||||||

| Net premiums earned | $ | $ | |||||||||

| Net investment income | |||||||||||

| Net realized losses | ( | ( | |||||||||

| Fair value changes in trading securities, funds held and other investments | |||||||||||

| Other income | |||||||||||

| Total revenues | |||||||||||

| EXPENSES | |||||||||||

| Net incurred losses and loss adjustment expenses | |||||||||||

| Current period | |||||||||||

| Prior periods | ( | ( | |||||||||

| Total net incurred losses and loss adjustment expenses | ( | ||||||||||

| Amortization of net deferred charge assets | |||||||||||

| Acquisition costs | |||||||||||

| General and administrative expenses | |||||||||||

| Interest expense | |||||||||||

| Net foreign exchange gains | ( | ( | |||||||||

| Total expenses | |||||||||||

| INCOME BEFORE INCOME TAXES | |||||||||||

| Income tax (expense) benefit | ( | ||||||||||

| (Loss) income from equity method investments | ( | ||||||||||

| NET INCOME | |||||||||||

| Net income attributable to noncontrolling interests | ( | ||||||||||

| NET INCOME ATTRIBUTABLE TO ENSTAR | |||||||||||

| Dividends on preferred shares | ( | ( | |||||||||

| NET INCOME ATTRIBUTABLE TO ENSTAR ORDINARY SHAREHOLDERS | $ | $ | |||||||||

| Earnings per ordinary share attributable to Enstar Ordinary Shareholders: | |||||||||||

| Basic | $ | $ | |||||||||

| Diluted | $ | $ | |||||||||

| Weighted average ordinary shares outstanding: | |||||||||||

| Basic | |||||||||||

| Diluted | |||||||||||

See accompanying notes to the unaudited condensed consolidated financial statements.

Enstar Group Limited | First Quarter 2024 | Form 10-Q 10

ENSTAR GROUP LIMITED

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

For the Three Months Ended March 31, 2024 and 2023

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (expressed in millions of U.S. dollars) | |||||||||||

| NET INCOME | $ | $ | |||||||||

| Other comprehensive income (loss), net of income taxes: | |||||||||||

| Unrealized (losses) gains on fixed maturities, available-for-sale arising during the period | ( | ||||||||||

| Reclassification adjustment for change in allowance for credit losses recognized in net income | ( | ||||||||||

| Reclassification adjustment for net realized losses included in net income | |||||||||||

| Unrealized (losses) gains arising during the period, net of reclassification adjustments | ( | ||||||||||

| Reclassification adjustment for remeasurement of future policyholder benefits included in net income | ( | ||||||||||

| Change in currency translation adjustment | ( | ||||||||||

| Total other comprehensive loss | ( | ( | |||||||||

| Comprehensive income | |||||||||||

| Comprehensive loss attributable to noncontrolling interests | |||||||||||

| COMPREHENSIVE INCOME ATTRIBUTABLE TO ENSTAR | $ | $ | |||||||||

See accompanying notes to the unaudited condensed consolidated financial statements.

Enstar Group Limited | First Quarter 2024 | Form 10-Q 11

ENSTAR GROUP LIMITED

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY

For the Three Months Ended March 31, 2024 and 2023

| Share Capital | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Non-voting Convertible Ordinary Shares | Preferred Shares | Treasury Shares | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Voting Ordinary Shares | Series C | Series E | Series C Convertible Participating Non-Voting | Series D | Series E | Series C Preferred Shares | JSOP | APIC | AOCI | Retained Earnings | Total Enstar Shareholders' Equity | NCI | Total Shareholders' Equity | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (in millions of U.S. dollars) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Three Months Ended March 31, 2024 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance as at December 31, 2023 | $ | $ | $ | $ | $ | $ | $ | ( | $ | ( | $ | $ | ( | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income attributable to Enstar or noncontrolling interests | — | — | — | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Dividends on preferred shares | — | — | — | — | — | — | — | — | — | — | ( | ( | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Amortization of share-based compensation | — | — | — | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | — | — | — | — | — | — | — | — | — | ( | — | ( | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other | — | — | — | — | — | — | — | — | ( | — | — | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance as at March 31, 2024 | $ | $ | $ | $ | $ | $ | $ | ( | $ | ( | $ | $ | ( | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Three Months Ended March 31, 2023 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance as at December 31, 2022 | $ | $ | $ | $ | $ | $ | $ | ( | $ | ( | $ | $ | ( | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income attributable to Enstar or noncontrolling interests | — | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Dividends on preferred shares | — | — | — | — | — | — | — | — | — | — | ( | ( | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ordinary shares repurchased | — | ( | — | — | — | — | — | — | ( | — | — | ( | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Amortization of share-based compensation | — | — | — | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Acquisition of noncontrolling shareholders' interest in subsidiary | — | — | — | — | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | — | — | — | — | — | — | — | — | — | ( | — | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other | — | — | — | — | — | — | — | — | ( | — | — | ( | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance as at March 31, 2023 | $ | $ | $ | $ | $ | $ | $ | ( | $ | ( | $ | $ | ( | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

See accompanying notes to the unaudited condensed consolidated financial statements.

Enstar Group Limited | First Quarter 2024 | Form 10-Q 12

ENSTAR GROUP LIMITED

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

For the Three Months Ended March 31, 2024 and 2023

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (expressed in millions of U.S. dollars) | |||||||||||

| OPERATING ACTIVITIES: | |||||||||||

| Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to cash flows provided by operating activities: | |||||||||||

| Realized losses on investments | |||||||||||

| Fair value changes in trading securities, funds held and other investments | ( | ( | |||||||||

| Amortization of net deferred charge assets | |||||||||||

| Depreciation, accretion and other amortization | ( | ||||||||||

| Net gain on Enhanzed Re novation | ( | ||||||||||

| Loss (income) from equity method investments | ( | ||||||||||

| Other adjustments | ( | ( | |||||||||

| Changes in: | |||||||||||

| Reinsurance balances recoverable on paid and unpaid losses | ( | ||||||||||

| Losses and loss adjustment expenses | ( | ( | |||||||||

| Defendant asbestos and environmental liabilities | ( | ( | |||||||||

| Insurance and reinsurance balances payable | |||||||||||

| Other operating assets and liabilities | ( | ||||||||||

| Funds held | |||||||||||

| Cash from/to operating activities: | |||||||||||

| Cash consideration for the Enhanzed Re novation | |||||||||||

| Sales and maturities of trading securities | |||||||||||

| Purchases of trading securities | ( | ( | |||||||||

| Net cash flows (used in) provided by operating activities | ( | ||||||||||

| INVESTING ACTIVITIES: | |||||||||||

| Sales and maturities of available-for-sale securities | |||||||||||

| Purchase of available-for-sale securities | ( | ( | |||||||||

| Purchase of other investments | ( | ( | |||||||||

| Proceeds from other investments | |||||||||||

| Other investing activities | |||||||||||

| Net cash flows provided by investing activities | |||||||||||

| FINANCING ACTIVITIES: | |||||||||||

| Dividends on preferred shares | ( | ( | |||||||||

| Repurchase of shares | ( | ||||||||||

| Other | |||||||||||

| Net cash flows used in financing activities | ( | ( | |||||||||

| EFFECT OF EXCHANGE RATE CHANGES ON FOREIGN CURRENCY CASH AND CASH EQUIVALENTS | ( | ||||||||||

| NET DECREASE IN CASH AND CASH EQUIVALENTS | ( | ( | |||||||||

| CASH, CASH EQUIVALENTS AND RESTRICTED CASH, BEGINNING OF PERIOD | |||||||||||

| CASH, CASH EQUIVALENTS AND RESTRICTED CASH, END OF PERIOD | $ | $ | |||||||||

Enstar Group Limited | First Quarter 2024 | Form 10-Q 13

| Supplemental Cash Flow Information: | |||||||||||

| Income taxes (received) paid, net of refunds | $ | ( | $ | ||||||||

| Interest paid | $ | $ | |||||||||

| Reconciliation to Consolidated Balance Sheets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash and cash equivalents | |||||||||||

| Cash, cash equivalents and restricted cash | $ | $ | |||||||||

| Non-cash operating activities: | |||||||||||

| Novation of future policy holder benefits | |||||||||||

| Funds held directly managed transferred in exchange on novation of future policy holder benefits | ( | ||||||||||

| Other assets / liabilities transferred on novation of future policy holder benefits | ( | ||||||||||

| Losses and loss adjustment expenses transferred in connection with settlement of participation in Atrium's Syndicate 609 | |||||||||||

| Investments transferred in connection with settlement of participation in Atrium's Syndicate 609 | ( | ||||||||||

| Non-cash investing activities: | |||||||||||

| Unsettled purchases of available-for-sale securities and other investments | $ | $ | |||||||||

| Unsettled sales of available-for-sale securities and other investments | ( | ( | |||||||||

See accompanying notes to the unaudited condensed consolidated financial statements.

Enstar Group Limited | First Quarter 2024 | Form 10-Q 14

ENSTAR GROUP LIMITED

NOTES TO THE UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

1. BASIS OF PRESENTATION

Enstar Group Limited ("Enstar") is a leading global (re)insurance group that offers innovative capital release solutions through its network of group companies in Bermuda, the United States, the United Kingdom, Continental Europe and Australia. Our core focus is acquiring and managing (re)insurance companies and portfolios of (re)insurance business in run-off.

The results of operations for any interim period are not necessarily indicative of results for the full year. These unaudited condensed consolidated financial statements and related notes should be read in conjunction with the consolidated financial statements and related notes included in our Annual Report on Form 10-K for the year ended December 31, 2023.

Recently Issued Accounting Pronouncements Not Yet Adopted

ASU 2023-07 - Improvements to Reportable Segment Disclosures

In November 2023, the FASB issued ASU 2023-07, which includes the following amendments to Topic 280 Segment Reporting:

•Disclose, on an annual and interim basis, significant segment expenses that are regularly provided to the chief operating decision maker (“CODM”) and included within the segment measure of profit or loss;

•Disclose, on an annual and interim basis, an amount for other segment items by reportable segment and a description of its composition;

•Disclose, on an interim basis, all annual disclosures about a reportable segment’s profit or loss and assets currently required by Topic 280;

•Clarify that an entity is not precluded from reporting one or more additional measure(s) of segment profit or loss if the CODM uses more than one measure in assessing segment performance and deciding how to allocate resources;

•Disclose the title and position of the CODM and an explanation of how the CODM uses the reported measure(s) of segment profit or loss in assessing segment performance and deciding how to allocate resources; and

•Require an entity with a single reportable segment to provide all disclosures required by the amendments in ASU 2023-07 and all existing segment disclosures in Topic 280.

These amendments are effective for annual reporting periods beginning after December 15, 2023 and interim reporting periods beginning after December 15, 2024, and must be applied retrospectively to all prior periods presented. Early adoption is permitted.

Adopting ASU 2023-07 will require us to expand our segment disclosures. We are currently determining the period in which the new guidance will be adopted.

ASU 2023-09 - Improvements to Income Tax Disclosures

In December 2023, the FASB issued ASU 2023-09, which includes the following amendments to Topic 740 Income Taxes:

•Disclose, on an annual basis, specific categories in the rate reconciliation;

Enstar Group Limited | First Quarter 2024 | Form 10-Q 15

Item 1 | Notes to the Unaudited Condensed Consolidated Financial Statements | Note 1. Basis of Presentation

•Disclose, on an annual basis, additional information for reconciling items that meet a quantitative threshold (if the effect of those reconciling items is equal to or greater than 5% of the amount computed by multiplying pretax income (or loss) by the applicable statutory income tax rate);

•Disclose, on an annual basis, the amount of income taxes paid (net of refunds received) disaggregated by federal (national), state, and foreign taxes;

•Disclose, on an annual basis, the amount of income taxes paid (net of refunds received) disaggregated by individual jurisdictions in which income taxes paid (net of refunds received) is equal to or greater than 5% of total income taxes paid (net of refunds received);

•Disclose income (or loss) from continuing operations before income tax expense (or benefit) disaggregated between domestic and foreign;

•Disclose income tax expense (or benefit) from continuing operations disaggregated by federal (national), state, and foreign;

•Eliminates the requirement to disclose the nature and estimate of the range of the reasonably possible change in the unrecognized tax benefits balance in the next 12 months or make a statement that an estimate of the range cannot be made; and

•Eliminates the requirement to disclose the cumulative amount of each type of temporary difference when a deferred tax liability is not recognized because of the exceptions to comprehensive recognition of deferred taxes related to subsidiaries and corporate joint ventures.

These amendments are effective for annual reporting periods beginning after December 15, 2024, and should be applied prospectively, however retrospective application is permitted. Early adoption is permitted.

Adopting ASU 2023-09 will require us to expand our income tax disclosures. We are currently determining the period in which the new guidance will be adopted.

2. SEGMENT INFORMATION

Our segment structure is aligned with how our CODM, our Chief Executive Officer, views our business, assesses performance and allocates resources to our business components. Effective January 1, 2024, our business is organized into two reportable segments: (i) Run-off and (ii) Investments. In addition, our Corporate and other activities, which do not qualify as an operating segment, include income and expense items that are not directly attributable to our reportable segments and activities from the former Assumed Life and Legacy Underwriting reportable segments.

Effective January 1, 2024, each of our Assumed Life and Legacy Underwriting reportable segments were determined to no longer meet the definition of reportable segments as they no longer engage in any active business activities following the series of commutation and novation transactions in Enhanzed Re and the settlement of the arrangements between SGL No. 1, Arden, and Atrium. Given the cessation of business activities and that all remaining activities are not expected to be material, all residual income or expense of the former Assumed Life and Legacy Underwriting reportable segments will be prospectively included within our Corporate and other activities.

The Assumed Life segment previously included Enhanzed Re’s life and property aggregate excess of loss (catastrophe) business. In August 2022, Enhanzed Re entered into a Master Agreement with Cavello Bay Reinsurance Limited (“Cavello”), a wholly-owned subsidiary of Enstar, and Allianz, pursuant to which a series of commutation and novation agreements were completed which ceased any continuing reinsurance obligations for this segment. We recognized the impact of transactions that closed in the fourth quarter of 2022 in the first quarter of 2023 due to the quarter lag in reporting.

The Legacy Underwriting segment previously included participation in direct underwriting activities, including a 25 % participation within 2020 and prior underwriting years of Atrium's Syndicate 609 at Lloyd's, offset by the contractual transfer of the results of that business to the Atrium entities that were divested in an exchange transaction. All remaining contractual arrangements were settled in the second quarter of 2023. Other than the settlement of these amounts, no other transactions were recorded in the Legacy Underwriting segment in 2023.

Enstar Group Limited | First Quarter 2024 | Form 10-Q 16

Item 1 | Notes to the Unaudited Condensed Consolidated Financial Statements | Note 2. Segment Information

Our assets are reviewed on a consolidated basis by management for decision making purposes since they support business operations across both of our reportable segments as well as our Corporate and other activities. We do not allocate assets to our reportable segments with the exception of (re)insurance balances recoverable on paid and unpaid losses and goodwill (all goodwill is attributable to the Run-off segment) that are directly attributable to our reportable segments.

The following table sets forth select unaudited condensed consolidated statements of operations results by segment and our Corporate and other activities:

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (in millions of U.S. dollars) | |||||||||||

| Revenues | |||||||||||

| Run-off | $ | $ | |||||||||

| Investments | |||||||||||

Assumed Life (1) | |||||||||||

| Subtotal | |||||||||||

Corporate and other (1) | ( | ||||||||||

| Total revenues | $ | $ | |||||||||

| (Loss) income from equity method investments | |||||||||||

| Investments | $ | ( | $ | ||||||||

| Segment net income (loss) | |||||||||||

Run-off | $ | ( | $ | ( | |||||||

Investments | |||||||||||

Assumed Life (1) | |||||||||||

| Total segment net income | |||||||||||

Corporate and other (1): | |||||||||||

Other expense (2) | ( | ||||||||||

Net incurred losses and loss adjustment expenses (“LAE”) (3) | ( | ||||||||||

| Amortization of net deferred charge assets | ( | ( | |||||||||

| General and administrative expenses | ( | ( | |||||||||

| Interest expense | ( | ( | |||||||||

| Net foreign exchange gains | |||||||||||

| Income tax (expense) benefit | ( | ||||||||||

| Net income attributable to noncontrolling interests | ( | ||||||||||

| Dividends on preferred shares | ( | ( | |||||||||

Total - Corporate and other loss | ( | ( | |||||||||

| Net income attributable to Enstar Ordinary Shareholders | $ | $ | |||||||||

(1) Effective January 1, 2024, Assumed Life and Legacy Underwriting were determined to no longer meet the definition of reportable segments and their residual income and loss activities were prospectively included in Corporate and other activities. Activities prior to January 1, 2024 are recorded in their respective segments. In addition, Legacy Underwriting had no revenue or income activity for the three months ended March 31, 2024 and 2023 and therefore is excluded from the table above.

(2) Other expense for Corporate and other activities includes the amortization of fair value adjustments associated with the acquisition of DCo and Morse TEC.

(3) Net incurred losses and LAE for Corporate and other activities includes fair value adjustments associated with the acquisition of companies and the changes in the discount rate and risk margin components of the fair value of assets and liabilities related to our assumed retroactive reinsurance contracts for which we have elected the fair value option.

Enstar Group Limited | First Quarter 2024 | Form 10-Q 17

Item 1 | Notes to the Unaudited Condensed Consolidated Financial Statements | Note 3. Investments

3. INVESTMENTS

Short-term and Fixed Maturity Investments

Asset Types

The fair values of the following underlying asset categories are set out below:

| March 31, 2024 | |||||||||||||||||||||||||||||

| Short-term investments, trading | Short-term investments, AFS | Fixed maturities, trading | Fixed maturities, AFS | Total | |||||||||||||||||||||||||

| (in millions of U.S. dollars) | |||||||||||||||||||||||||||||

| U.S. government and agency | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| U.K. government | |||||||||||||||||||||||||||||

| Other government | |||||||||||||||||||||||||||||

| Corporate | |||||||||||||||||||||||||||||

| Municipal | |||||||||||||||||||||||||||||

| Residential mortgage-backed | |||||||||||||||||||||||||||||

| Commercial mortgage-backed | |||||||||||||||||||||||||||||

| Asset-backed | |||||||||||||||||||||||||||||

| Total fixed maturity and short-term investments | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| December 31, 2023 | |||||||||||||||||||||||||||||

| Short-term investments, trading | Short-term investments, AFS | Fixed maturities, trading | Fixed maturities, AFS | Total | |||||||||||||||||||||||||

| (in millions of U.S. dollars) | |||||||||||||||||||||||||||||

| U.S. government and agency | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| U.K. government | |||||||||||||||||||||||||||||

| Other government | |||||||||||||||||||||||||||||

| Corporate | |||||||||||||||||||||||||||||

| Municipal | |||||||||||||||||||||||||||||

| Residential mortgage-backed | |||||||||||||||||||||||||||||

| Commercial mortgage-backed | |||||||||||||||||||||||||||||

| Asset-backed | |||||||||||||||||||||||||||||

| Total fixed maturity and short-term investments | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

Included within residential mortgage-backed securities as of March 31, 2024 were securities issued by U.S. governmental agencies with a fair value of $278 million (December 31, 2023: $306 million).

Included within commercial mortgage-backed securities as of March 31, 2024 were securities issued by U.S. governmental agencies with a fair value of $66 million (December 31, 2023: $73 million).

Enstar Group Limited | First Quarter 2024 | Form 10-Q 18

Item 1 | Notes to the Unaudited Condensed Consolidated Financial Statements | Note 3. Investments

Contractual Maturities

The contractual maturities of our short-term and fixed maturity investments, classified as trading and AFS are shown below. Actual maturities may differ from contractual maturities because issuers may have the right to call or prepay obligations with or without call or prepayment penalties.

| As of March 31, 2024 | Amortized Cost | Fair Value | % of Total Fair Value | |||||||||||||||||

| (in millions of U.S. dollars) | ||||||||||||||||||||

| One year or less | $ | $ | % | |||||||||||||||||

| More than one year through five years | % | |||||||||||||||||||

| More than five years through ten years | % | |||||||||||||||||||

| More than ten years | % | |||||||||||||||||||

| Residential mortgage-backed | % | |||||||||||||||||||

| Commercial mortgage-backed | % | |||||||||||||||||||

| Asset-backed | % | |||||||||||||||||||

| $ | $ | % | ||||||||||||||||||

Unrealized Gains and Losses on AFS Short-term and Fixed Maturity Investments

The amortized cost, unrealized gains and losses, allowance for credit losses and fair values of our short-term and fixed maturity investments classified as AFS were as follows:

| Gross Unrealized Gains | Gross Unrealized Losses | |||||||||||||||||||||||||||||||

| As of March 31, 2024 | Amortized Cost | Non-Credit Related Losses | Allowance for Credit Losses | Fair Value | ||||||||||||||||||||||||||||

| (in millions of U.S. dollars) | ||||||||||||||||||||||||||||||||

| U.S. government and agency | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||

| U.K. government | ( | |||||||||||||||||||||||||||||||

| Other government | ( | |||||||||||||||||||||||||||||||

| Corporate | ( | ( | ||||||||||||||||||||||||||||||

| Municipal | ( | |||||||||||||||||||||||||||||||

| Residential mortgage-backed | ( | |||||||||||||||||||||||||||||||

| Commercial mortgage-backed | ( | ( | ||||||||||||||||||||||||||||||

| Asset-backed | ( | |||||||||||||||||||||||||||||||

| $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||

| Gross Unrealized Gains | Gross Unrealized Losses | |||||||||||||||||||||||||||||||

As of December 31, 2023 | Amortized Cost | Non-Credit Related Losses | Allowance for Credit Losses | Fair Value | ||||||||||||||||||||||||||||

| (in millions of U.S. dollars) | ||||||||||||||||||||||||||||||||

| U.S. government and agency | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||

| U.K. government | ( | |||||||||||||||||||||||||||||||

| Other government | ( | |||||||||||||||||||||||||||||||

| Corporate | ( | ( | ||||||||||||||||||||||||||||||

| Municipal | ( | |||||||||||||||||||||||||||||||

| Residential mortgage-backed | ( | |||||||||||||||||||||||||||||||

| Commercial mortgage-backed | ( | ( | ||||||||||||||||||||||||||||||

| Asset-backed | ( | |||||||||||||||||||||||||||||||

| $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||

Enstar Group Limited | First Quarter 2024 | Form 10-Q 19

Item 1 | Notes to the Unaudited Condensed Consolidated Financial Statements | Note 3. Investments

Gross Unrealized Losses on AFS Short-term and Fixed Maturity Investments

The following tables summarizes our short-term and fixed maturity investments classified as AFS that were in a gross unrealized loss position, for which an allowance for credit losses has not been recorded, as explained below:

| 12 Months or Greater | Less Than 12 Months | Total | ||||||||||||||||||||||||||||||||||||

| As of March 31, 2024 | Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | ||||||||||||||||||||||||||||||||

| (in millions of U.S. dollars) | ||||||||||||||||||||||||||||||||||||||

| U.S. government and agency | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||

| U.K. government | ( | ( | ||||||||||||||||||||||||||||||||||||

| Other government | ( | ( | ( | |||||||||||||||||||||||||||||||||||

| Corporate | ( | ( | ( | |||||||||||||||||||||||||||||||||||

| Municipal | ( | ( | ||||||||||||||||||||||||||||||||||||

| Residential mortgage-backed | ( | ( | ( | |||||||||||||||||||||||||||||||||||

| Commercial mortgage-backed | ( | ( | ( | |||||||||||||||||||||||||||||||||||

| Asset-backed | ( | ( | ( | |||||||||||||||||||||||||||||||||||

| Total short-term and fixed maturity investments | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||

| 12 Months or Greater | Less Than 12 Months | Total | ||||||||||||||||||||||||||||||||||||

| As of December 31, 2023 | Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | ||||||||||||||||||||||||||||||||

| (in millions of U.S. dollars) | ||||||||||||||||||||||||||||||||||||||

| U.S. government and agency | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||

| U.K. government | ( | ( | ||||||||||||||||||||||||||||||||||||

| Other government | ( | ( | ||||||||||||||||||||||||||||||||||||

| Corporate | ( | ( | ( | |||||||||||||||||||||||||||||||||||

| Municipal | ( | ( | ||||||||||||||||||||||||||||||||||||

| Residential mortgage-backed | ( | ( | ( | |||||||||||||||||||||||||||||||||||

| Commercial mortgage-backed | ( | ( | ( | |||||||||||||||||||||||||||||||||||

| Asset-backed | ( | ( | ( | |||||||||||||||||||||||||||||||||||

| Total short-term and fixed maturity investments | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||

As of March 31, 2024 and December 31, 2023, the number of securities classified as AFS in an unrealized loss position for which an allowance for credit loss is not recorded was 2,363 and 2,156 , respectively. Of these securities, the number of securities that had been in an unrealized loss position for twelve months or longer was 1,549 and 1,736 , respectively.

Enstar Group Limited | First Quarter 2024 | Form 10-Q 20

Item 1 | Notes to the Unaudited Condensed Consolidated Financial Statements | Note 3. Investments

Allowance for Credit Losses on AFS Fixed Maturity Investments

The following table provides a reconciliation of the beginning and ending allowance for credit losses on our AFS debt securities:

| Three Months Ended March 31, | |||||||||||||||||||||||||||||||||||

| 2024 | 2023 | ||||||||||||||||||||||||||||||||||

| Corporate | Commercial mortgage backed | Total | Other government | Corporate | Total | ||||||||||||||||||||||||||||||

| (in millions of U.S. dollars) | |||||||||||||||||||||||||||||||||||

| Allowance for credit losses, beginning of period | $ | ( | $ | ( | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||||||||||

| Allowances for credit losses on securities for which credit losses were not previously recorded | ( | ( | |||||||||||||||||||||||||||||||||

| Reductions for securities sold during the period | |||||||||||||||||||||||||||||||||||

| (Increase) decrease to the allowance for credit losses on securities that had an allowance recorded in the previous period | ( | ( | |||||||||||||||||||||||||||||||||

| Allowance for credit losses, end of period | $ | ( | $ | ( | $ | ( | $ | $ | ( | $ | ( | ||||||||||||||||||||||||

During the three months ended March 31, 2024 and 2023, we did not have any write-offs charged against the allowance for credit losses or any recoveries of amounts previously written off.

Equity Investments

The following table summarizes our equity investments:

| March 31, 2024 | December 31, 2023 | ||||||||||

| (in millions of U.S. dollars) | |||||||||||

| Equity Investments | |||||||||||

| Publicly traded equity investments in common and preferred stocks | $ | $ | |||||||||

| Exchange-traded funds | |||||||||||

| Privately held equity investments in common and preferred stocks | |||||||||||

| $ | $ | ||||||||||

Other Investments

The following table summarizes our other investments carried at fair value:

| March 31, 2024 | December 31, 2023 | ||||||||||

| (in millions of U.S. dollars) | |||||||||||

| Other Investments | |||||||||||

| Private equity funds | $ | $ | |||||||||

| Private credit funds | |||||||||||

| Hedge funds | |||||||||||

| Fixed income funds | |||||||||||

| Real estate funds | |||||||||||

| CLO equity funds | |||||||||||

| CLO equities | |||||||||||

| Equity funds | |||||||||||

| $ | $ | ||||||||||

Enstar Group Limited | First Quarter 2024 | Form 10-Q 21

Item 1 | Notes to the Unaudited Condensed Consolidated Financial Statements | Note 3. Investments

Other investments, including equities measured at fair value using NAV as a practical expedient

We use NAV as a practical expedient to fair value certain of our other investments, including equities.

The table below details the estimated period by which proceeds would be received if we had provided notice of our intent to redeem or initiated a sales process as of March 31, 2024 for our investments measured at fair value using NAV as a practical expedient:

| Less than 1 Year | 1-2 years | 2-3 years | More than 3 years | Not Eligible/ Restricted | Total | Redemption Frequency (1) | |||||||||||||||||||||||||||||||||||

| (in millions of U.S. dollars) | |||||||||||||||||||||||||||||||||||||||||

| Equities | |||||||||||||||||||||||||||||||||||||||||

| Privately held equity investments | $ | $ | $ | $ | $ | $ | not eligible/ restricted | ||||||||||||||||||||||||||||||||||

| Other investments | |||||||||||||||||||||||||||||||||||||||||

| Private equity funds | $ | $ | $ | $ | $ | $ | quarterly for unrestricted amount | ||||||||||||||||||||||||||||||||||

| Hedge funds | monthly to bi-annually | ||||||||||||||||||||||||||||||||||||||||

| Fixed income funds | monthly to quarterly | ||||||||||||||||||||||||||||||||||||||||

| Private credit funds | not eligible/ restricted | ||||||||||||||||||||||||||||||||||||||||

| Real estate funds | not eligible/ restricted | ||||||||||||||||||||||||||||||||||||||||

| CLO equity funds | quarterly to bi-annually | ||||||||||||||||||||||||||||||||||||||||

| $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||

(1) Redemption frequency relates to unrestricted amounts.

Equity Method Investments

The table below shows our equity method investments:

| March 31, 2024 | December 31, 2023 | |||||||||||||||||||||||||

| Ownership % | Carrying Value | Ownership % | Carrying Value | |||||||||||||||||||||||

| (in millions of U.S. dollars) | ||||||||||||||||||||||||||

Monument Re (1) | % | % | ||||||||||||||||||||||||

| Core Specialty | % | % | ||||||||||||||||||||||||

| Other | % | |||||||||||||||||||||||||

| $ | $ | |||||||||||||||||||||||||

(1) As of March 31, 2024, we own 24.6 % of the common shares in Monument Re. We converted all of our preferred shares in Monument Midco to common shares in Monument Re on January 2, 2024. As of December 31, 2023, we owned 20.0 % of the common shares in Monument Re as well as preferred shares in Monument Midco which had fixed dividend yields (where declared). Losses for the three months ended March 31, 2024 include an other-than-temporary impairment charge.

Funds Held

Under funds held arrangements, the reinsured company has retained funds that would otherwise have been remitted to us. The funds held balance is credited with investment income and losses paid are deducted.

| March 31, 2024 | December 31, 2023 | ||||||||||

| (in millions of U.S. dollars) | |||||||||||

| Funds held - directly managed | $ | $ | |||||||||

| Funds held by reinsured companies | |||||||||||

| Total funds held | $ | $ | |||||||||

Enstar Group Limited | First Quarter 2024 | Form 10-Q 22

Item 1 | Notes to the Unaudited Condensed Consolidated Financial Statements | Note 3. Investments

Funds Held - Directly Managed

The following table summarizes the components of the investments collateralizing the funds held - directly managed:

| March 31, 2024 | December 31, 2023 | ||||||||||

| (in millions of U.S. dollars) | |||||||||||

| Funds held - directly managed, at cost | $ | $ | |||||||||

| Fair value changes in: | |||||||||||

| Accumulated change in fair value - embedded derivative accounting | ( | ( | |||||||||

| Funds held - directly managed, at fair value | $ | $ | |||||||||

The majority of our funds held - directly managed is comprised of short-term and fixed maturities. The $166 million decrease in funds held - directly managed from December 31, 2023 to March 31, 2024 was primarily driven by net paid losses.

Funds Held by Reinsured Companies

The following table summarizes the components of our funds held by reinsured companies:

| March 31, 2024 | December 31, 2023 | ||||||||||

| (in millions of U.S. dollars) | |||||||||||

| Funds held by reinsurance companies, at amortized cost | $ | $ | |||||||||

Fair value of embedded derivative (1) | |||||||||||

| Funds held by reinsured companies | $ | $ | |||||||||

The $205 million decrease in funds held by reinsured companies from December 31, 2023 to March 31, 2024 was primarily driven by net paid losses specific to the Aspen LPT.

Net Investment Income

Major categories of net investment income are summarized as follows:

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (in millions of U.S. dollars) | |||||||||||

| Fixed maturity investments | $ | $ | |||||||||

| Short-term investments and cash and cash equivalents | |||||||||||

| Funds held | |||||||||||

| Investment income from fixed maturities and cash and cash equivalents | |||||||||||

| Equity investments | |||||||||||

| Other investments | |||||||||||

| Investment income from equities and other investments | |||||||||||

| Gross investment income | |||||||||||

| Investment expenses | ( | ( | |||||||||

| Net investment income | $ | $ | |||||||||

Enstar Group Limited | First Quarter 2024 | Form 10-Q 23

Item 1 | Notes to the Unaudited Condensed Consolidated Financial Statements | Note 3. Investments

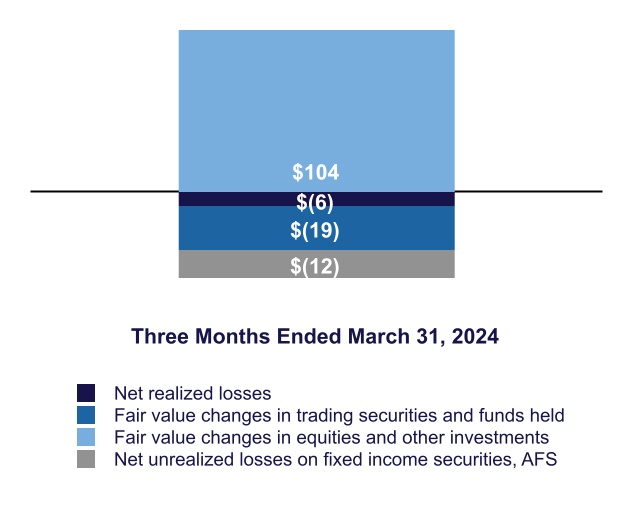

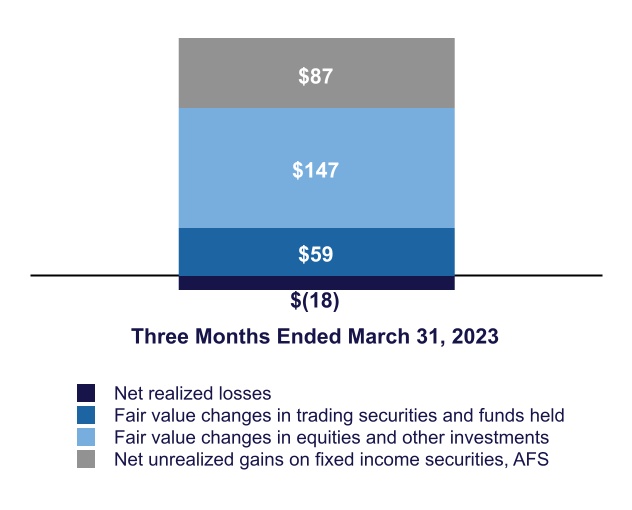

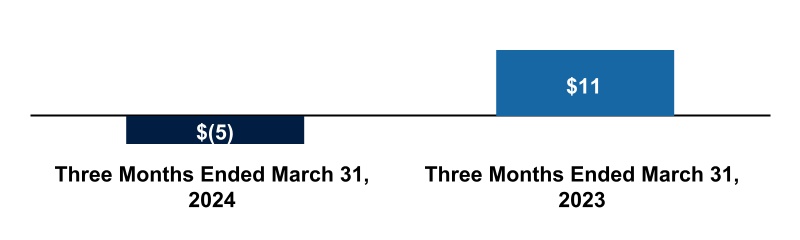

Net Realized Gains (Losses) and Fair Value Changes

Investment purchases and sales are recorded on a trade-date basis. Realized gains and losses on the sale of investments are based upon specific identification of the cost of investments. Components of net realized gains (losses) and fair value changes are recorded within our unaudited condensed consolidated statements of operations were as follows:

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (in millions of U.S. dollars) | |||||||||||

| Net realized losses on sales: | |||||||||||

| Gross realized gains on fixed maturity securities, AFS | $ | $ | |||||||||

| Gross realized losses on fixed maturity securities, AFS | ( | ( | |||||||||

| (Increase) decrease in allowance for expected credit losses on fixed maturity securities, AFS | ( | ||||||||||

| Total net realized losses on sales | $ | ( | $ | ( | |||||||

| Fair value changes in trading securities, funds held and other investments: | |||||||||||

| Fixed maturity securities, trading | $ | ( | $ | ||||||||

| Funds held - directly managed | ( | ||||||||||

| Equity securities | |||||||||||

| Other investments | |||||||||||

| Investment derivatives | |||||||||||

| Total fair value changes in trading securities, funds held and other investments | $ | $ | |||||||||

| Net realized gains and fair value changes in trading securities, funds held and other investments | $ | $ | |||||||||

The gross realized gains and losses on AFS investments for the three months ended March 31, 2024 and 2023 included in the table above resulted from sales of AFS investments of $436 million and $656 million, respectively.

For the three months ended March 31, 2024 and 2023, fair value changes in trading securities, funds held and other investments recorded within the statement of operations relating to equity securities still held on the balance sheet date were $37 million and $43 million, respectively.

Restricted Assets

The carrying value of our restricted assets, including restricted cash of $310 million and $266 million, as of March 31, 2024 and December 31, 2023, respectively, was as follows:

| March 31, 2024 | December 31, 2023 | ||||||||||

| (in millions of U.S. dollars) | |||||||||||

| Collateral in trust for third party agreements | $ | $ | |||||||||

| Assets on deposit with regulatory authorities | |||||||||||

| Collateral for secured letter of credit facilities | |||||||||||

Funds at Lloyd's (1) | |||||||||||

| $ | $ | ||||||||||

Enstar Group Limited | First Quarter 2024 | Form 10-Q 24

Item 1 | Notes to the Unaudited Condensed Consolidated Financial Statements | Note 4. Derivatives and Hedging Instruments

4. DERIVATIVES AND HEDGING INSTRUMENTS

Accounting for Derivatives

Freestanding Derivatives

Freestanding derivatives are recorded on trade-dates and carried on the consolidated balance sheet either as assets within other assets or as liabilities within other liabilities at estimated fair value. We do not offset the estimated fair value amounts recognized for derivatives executed with the same counterparty under the same master netting agreement.

If a derivative is not designated as an accounting hedge or its use in managing risk does not qualify for hedge accounting, changes in the estimated fair value of the derivative are reported in fair value changes in trading securities, funds held and other investments included in our consolidated statements of operations.

Hedge Accounting

To qualify for hedge accounting, at the inception of the hedging relationship, we formally document the risk management objective and strategy for undertaking the hedging transaction, as well as the designation of the hedge.

We have qualifying net investment in foreign operation (“NIFO”) hedges. We recognize changes in the estimated fair value of the hedging derivatives within OCI, consistent with the translation adjustment for the hedged net investment in the foreign operation.

Our documentation sets forth how the hedging instrument is expected to hedge the designated risks related to the hedged item and also sets forth the method that will be used to retrospectively and prospectively assess the hedging instrument’s effectiveness. A derivative designated as a hedging instrument must be assessed as being highly effective in offsetting the designated risk of the hedged item. Hedge effectiveness is formally assessed at inception and at least quarterly throughout the life of the designated hedging relationship. Assessments of hedge effectiveness are also subject to interpretation and estimation and different interpretations or estimates may have a material effect on the amount reported in net income.

When hedge accounting is discontinued pursuant to a NIFO hedge (due to a revaluation, payment of a dividend or the disposal of our investment in a foreign operation), the derivative continues to be carried on the balance sheet at its estimated fair value. Deferred gains and losses recorded in OCI pursuant to a discontinued NIFO hedge are recognized immediately in net foreign exchange losses (gains) in our consolidated statements of operations.

Embedded Derivatives

We are party to certain reinsurance agreements that have embedded derivatives. We also have embedded derivatives on our convertible bond portfolio, recorded within fixed maturities, trading on the consolidated balance sheets. We assess each identified embedded derivative to determine whether it is required to be bifurcated. The embedded derivative is bifurcated from the host contract and accounted for as a freestanding derivative if:

•the combined instrument is not accounted for in its entirety at estimated fair value with changes in estimated fair value recorded in net income;

•the terms of the embedded derivative are not clearly and closely related to the economic characteristics of the host contract; and

•a separate instrument with the same terms as the embedded derivative would qualify as a derivative instrument.

Such embedded derivatives are carried on the consolidated balance sheet at estimated fair value with the host contract and changes in their estimated fair value are generally reported within fair value changes in trading securities, funds held and other investments.

Derivative Strategies

We are exposed to various risks relating to our ongoing business operations, including interest rate, foreign currency exchange rate, credit and equity price risks. We use a variety of strategies to manage these risks, including the use of derivatives.

Derivatives are financial instruments with values derived from interest rates, foreign currency exchange rates, credit spreads and/or other financial indices. The types of derivatives we use include swaps and forwards.

Enstar Group Limited | First Quarter 2024 | Form 10-Q 25

Item 1 | Notes to the Unaudited Condensed Consolidated Financial Statements | Note 4. Derivatives and Hedging Instruments

Foreign Currency Derivatives

We use foreign currency exchange rate derivatives, including foreign currency forwards, to reduce the risk from fluctuations in foreign currency exchange rates associated with our assets and liabilities denominated in foreign currencies. We also use foreign currency derivatives to hedge the foreign currency exchange rate risk associated with certain of our net investments in foreign operations.

In a foreign currency forward transaction, we agree with another party to deliver a specified amount of an identified currency at a specified future date. The price is agreed upon at the time of the contract and payment for such a contract is made at the specified future date. We utilize foreign currency forwards in fair value, NIFO hedges and nonqualifying hedging relationships.

Interest Rate Derivatives

We use interest rate derivatives, specifically interest rate swaps, to reduce our exposure to changes in interest rates.

Interest rate swaps are used by us primarily to reduce market risks from changes in interest rates and to alter interest rate exposure arising from mismatches between assets and liabilities (duration mismatches). In an interest rate swap, we agree with another party to exchange, at specified intervals, the difference between fixed rate and floating rate interest amounts as calculated by reference to an agreed notional amount. We utilize interest rate swaps in nonqualifying hedging relationships.

In February 2023, we entered into a two-month forward interest rate swap, receiving a fixed rate and paying a floating rate with a notional value of $800 million to partially mitigate the risk that interest rates could decrease prior to our receipt of the cash consideration for the QBE LPT transaction. Following the expiration of the forward period in April 2023, we took delivery of a three-year receive fixed, pay floating interest rate swap. The notional value of the swap was subsequently partially unwound as the consideration received was invested. The swap was fully unwound in July 2023. As of March 31, 2024 and December 31, 2023, we had no interest rate swaps.

The following table presents the gross notional amounts and estimated fair values of our derivatives recorded within and on the consolidated balance sheets as of March 31, 2024 and December 31, 2023:

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||||||||||||||

| Gross Notional Amount | Fair Value | Gross Notional Amount | Fair Value | ||||||||||||||||||||||||||||||||

| Assets | Liabilities | Assets | Liabilities | ||||||||||||||||||||||||||||||||

| (in millions of U.S. dollars) | |||||||||||||||||||||||||||||||||||

| Derivatives designated as hedging instruments | |||||||||||||||||||||||||||||||||||

| Foreign currency forward contracts | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| Derivatives not designated as hedging instruments | |||||||||||||||||||||||||||||||||||

| Foreign currency forward contracts | |||||||||||||||||||||||||||||||||||

| Others | |||||||||||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

The following table presents the net gains and losses relating to our derivative instruments for the three months ended March 31, 2024 and 2023:

| Amount of Net Gains (Losses) | |||||||||||||||||

| Location of gain (loss) recognized on derivatives | Three Months Ended | ||||||||||||||||

| March 31, 2024 | March 31, 2023 | ||||||||||||||||

| (in millions of U.S. dollars) | |||||||||||||||||

| Derivatives designated as hedging instruments | |||||||||||||||||

| Foreign currency forward contracts | Accumulated other comprehensive income (loss) | $ | $ | ( | |||||||||||||

| Derivatives not designated as hedging instruments | |||||||||||||||||

| Foreign currency forward contracts | Net foreign exchange gains | ||||||||||||||||

| Interest rate swap | Fair value changes in trading securities, funds held and other investments | ||||||||||||||||

Enstar Group Limited | First Quarter 2024 | Form 10-Q 26

Item 1 | Notes to the Unaudited Condensed Consolidated Financial Statements | Note 5. Deferred Charge Assets and Deferred Gain Liabilities

5. DEFERRED CHARGE ASSETS AND DEFERRED GAIN LIABILITIES

If, at the inception of a retroactive reinsurance contract, the estimated liabilities for losses and LAE exceed the consideration received, a deferred charge asset (“DCA”) is recorded for this difference. In contrast, if the consideration received is in excess of the estimated undiscounted ultimate losses payable, a deferred gain liability (“DGL”) is recorded.

We amortize the net DCA balances over the estimated claim payment period of the related contracts with the amortization prospectively adjusted at each reporting period to reflect new estimates of the pattern and timing of remaining losses and LAE payments.

The following table presents a summary of the DCA balances and related activity for the three months ended March 31, 2024 and 2023 (there were no

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (in millions of U.S. dollars) | |||||||||||

| Beginning carrying value | $ | $ | |||||||||

| Amortization | ( | ( | |||||||||

| Ending carrying value | $ | $ | |||||||||

Enstar Group Limited | First Quarter 2024 | Form 10-Q 27

Item 1 | Notes to the Unaudited Condensed Consolidated Financial Statements | Note 6. Losses and Loss Adjustment Expenses

6. LOSSES AND LOSS ADJUSTMENT EXPENSES

The liability for losses and LAE, also referred to as loss reserves, represents our gross estimates before reinsurance for unpaid reported losses (Outstanding Loss Reserves, or "OLR") and includes losses that have been incurred but not yet reported ("IBNR") using a variety of actuarial methods. We recognize an asset for the portion of the liability that we expect to recover from reinsurers. LAE reserves include allocated LAE ("ALAE") and unallocated LAE ("ULAE"). ALAE are linked to the settlement of an individual claim or loss, whereas ULAE are based on our estimates of future costs to administer the claims. IBNR includes amounts for unreported claims, development on known claims and reopened claims.

Our loss reserves cover multiple lines of business, including asbestos, environmental, general casualty, workers' compensation, marine, aviation and transit, construction defect, professional indemnity/directors and officers, motor, property and other non-life lines of business. We complete most of our annual loss reserve studies in the fourth quarter of each year and, as a result, tend to record the largest movements, both favorable and adverse, to net incurred losses and LAE in this period.

Enstar Group Limited | First Quarter 2024 | Form 10-Q 28

Item 1 | Notes to the Unaudited Condensed Consolidated Financial Statements | Note 6. Losses and Loss Adjustment Expenses

The table below provides a consolidated reconciliation of the beginning and ending liability for losses and LAE:

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (in millions of U.S. dollars) | |||||||||||

| Balance as of beginning of period | $ | $ | |||||||||

| Reinsurance reserves recoverable on unpaid losses | ( | ( | |||||||||

| Net balance as of beginning of period | |||||||||||

| Net incurred losses and LAE: | |||||||||||

| Current period: | |||||||||||

| Increase in estimates of net ultimate losses | |||||||||||

| Total current period | |||||||||||

| Prior periods: | |||||||||||

| Reduction in estimates of net ultimate losses | ( | ( | |||||||||

| Reduction in provisions for ULAE | ( | ( | |||||||||

| Amortization of fair value adjustments | |||||||||||

Changes in fair value - fair value option (1) | ( | ||||||||||

| Total prior periods | ( | ( | |||||||||

| Total net incurred losses and LAE | ( | ||||||||||

| Net paid losses: | |||||||||||

| Current period | ( | ||||||||||

| Prior periods | ( | ( | |||||||||

| Total net paid losses | ( | ( | |||||||||

| Other changes: | |||||||||||

| Effect of exchange rate movement | ( | ||||||||||

Ceded business (2) | ( | ||||||||||

| Total other changes | ( | ( | |||||||||

Net balance as of March 31 | |||||||||||

| Reinsurance reserves recoverable on unpaid losses | |||||||||||

Balance as of March 31 | $ | $ | |||||||||

| As of | |||||||||||

| March 31, 2024 | December 31, 2023 | ||||||||||

| (in millions of U.S. dollars) | |||||||||||

| Reconciliation to Consolidated Balance Sheets: | |||||||||||

| Losses and loss adjustment expenses | $ | $ | |||||||||

| Losses and loss adjustment expenses, at fair value | |||||||||||

| Total losses and loss adjustment expenses | $ | $ | |||||||||

| Reinsurance balances recoverable on paid and unpaid losses | $ | $ | |||||||||

| Reinsurance balances recoverable on paid and unpaid losses - fair value option | |||||||||||

| Total reinsurance balances recoverable on paid and unpaid losses | |||||||||||

| Less: Paid losses recoverable | ( | ( | |||||||||

| Reinsurance reserves recoverable on unpaid losses | $ | $ | |||||||||

(1) Comprises discount rate and risk margin components.