0001360604falsefalse2020FY12/310001495491falsefalse2020FY12/31Includes amounts attributable to redeemable noncontrolling interests. P1YP3YP3MP1YP1YP3YP1Y203930351738303938392539363935393539353900013606042020-01-012020-12-310001360604hta:HealthcareTrustofAmericaHoldingsLPMember2020-01-012020-12-31iso4217:USD00013606042020-06-30xbrli:shares00013606042021-02-1800013606042020-12-3100013606042019-12-31iso4217:USDxbrli:shares00013606042019-01-012019-12-3100013606042018-01-012018-12-310001360604us-gaap:CommonStockMember2017-12-310001360604us-gaap:AdditionalPaidInCapitalMember2017-12-310001360604us-gaap:AccumulatedOtherComprehensiveIncomeMember2017-12-310001360604us-gaap:RetainedEarningsMember2017-12-310001360604us-gaap:ParentMember2017-12-310001360604us-gaap:NoncontrollingInterestMember2017-12-3100013606042017-12-310001360604us-gaap:CommonStockMember2018-01-012018-12-310001360604us-gaap:AdditionalPaidInCapitalMember2018-01-012018-12-310001360604us-gaap:ParentMember2018-01-012018-12-310001360604us-gaap:NoncontrollingInterestMember2018-01-012018-12-310001360604us-gaap:RetainedEarningsMember2018-01-012018-12-310001360604us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-01-012018-12-310001360604us-gaap:CommonStockMember2018-12-310001360604us-gaap:AdditionalPaidInCapitalMember2018-12-310001360604us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-12-310001360604us-gaap:RetainedEarningsMember2018-12-310001360604us-gaap:ParentMember2018-12-310001360604us-gaap:NoncontrollingInterestMember2018-12-3100013606042018-12-310001360604us-gaap:CommonStockMember2019-01-012019-12-310001360604us-gaap:AdditionalPaidInCapitalMember2019-01-012019-12-310001360604us-gaap:ParentMember2019-01-012019-12-310001360604us-gaap:NoncontrollingInterestMember2019-01-012019-12-310001360604us-gaap:RetainedEarningsMember2019-01-012019-12-310001360604us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-01-012019-12-310001360604us-gaap:CommonStockMember2019-12-310001360604us-gaap:AdditionalPaidInCapitalMember2019-12-310001360604us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-310001360604us-gaap:RetainedEarningsMember2019-12-310001360604us-gaap:ParentMember2019-12-310001360604us-gaap:NoncontrollingInterestMember2019-12-310001360604us-gaap:CommonStockMember2020-01-012020-12-310001360604us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310001360604us-gaap:ParentMember2020-01-012020-12-310001360604us-gaap:NoncontrollingInterestMember2020-01-012020-12-310001360604us-gaap:RetainedEarningsMember2020-01-012020-12-310001360604us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-12-310001360604us-gaap:CommonStockMember2020-12-310001360604us-gaap:AdditionalPaidInCapitalMember2020-12-310001360604us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001360604us-gaap:RetainedEarningsMember2020-12-310001360604us-gaap:ParentMember2020-12-310001360604us-gaap:NoncontrollingInterestMember2020-12-310001360604hta:HealthcareTrustofAmericaHoldingsLPMember2020-12-310001360604hta:HealthcareTrustofAmericaHoldingsLPMember2019-12-310001360604hta:HealthcareTrustofAmericaHoldingsLPMember2019-01-012019-12-310001360604hta:HealthcareTrustofAmericaHoldingsLPMember2018-01-012018-12-310001360604us-gaap:GeneralPartnerMemberhta:HealthcareTrustofAmericaHoldingsLPMember2017-12-310001360604us-gaap:LimitedPartnerMemberhta:HealthcareTrustofAmericaHoldingsLPMember2017-12-310001360604hta:HealthcareTrustofAmericaHoldingsLPMember2017-12-310001360604us-gaap:GeneralPartnerMemberhta:HealthcareTrustofAmericaHoldingsLPMember2018-01-012018-12-310001360604us-gaap:LimitedPartnerMemberhta:HealthcareTrustofAmericaHoldingsLPMember2018-01-012018-12-310001360604us-gaap:GeneralPartnerMemberhta:HealthcareTrustofAmericaHoldingsLPMember2018-12-310001360604us-gaap:LimitedPartnerMemberhta:HealthcareTrustofAmericaHoldingsLPMember2018-12-310001360604hta:HealthcareTrustofAmericaHoldingsLPMember2018-12-310001360604us-gaap:GeneralPartnerMemberhta:HealthcareTrustofAmericaHoldingsLPMember2019-01-012019-12-310001360604us-gaap:LimitedPartnerMemberhta:HealthcareTrustofAmericaHoldingsLPMember2019-01-012019-12-310001360604us-gaap:GeneralPartnerMemberhta:HealthcareTrustofAmericaHoldingsLPMember2019-12-310001360604us-gaap:LimitedPartnerMemberhta:HealthcareTrustofAmericaHoldingsLPMember2019-12-310001360604us-gaap:GeneralPartnerMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-01-012020-12-310001360604us-gaap:LimitedPartnerMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-01-012020-12-310001360604us-gaap:GeneralPartnerMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-12-310001360604us-gaap:LimitedPartnerMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-12-31hta:state0001360604us-gaap:BuildingMembersrt:MaximumMember2020-01-012020-12-310001360604hta:TenantImprovementsMembersrt:MinimumMember2020-01-012020-12-310001360604hta:TenantImprovementsMembersrt:MaximumMember2020-01-012020-12-310001360604hta:FurnitureFixturesandEquipmentMember2020-01-012020-12-310001360604us-gaap:BuildingAndBuildingImprovementsMember2020-01-012020-12-310001360604us-gaap:BuildingAndBuildingImprovementsMember2019-01-012019-12-310001360604us-gaap:BuildingAndBuildingImprovementsMember2018-01-012018-12-310001360604srt:MinimumMember2020-12-310001360604srt:MaximumMember2020-12-310001360604srt:MaximumMember2020-01-012020-12-310001360604srt:MinimumMember2020-01-012020-12-310001360604us-gaap:SecuredDebtMember2020-01-012020-12-310001360604us-gaap:SecuredDebtMember2020-12-31xbrli:purehta:segmenthta:building0001360604hta:MedicalOfficeBuildingInKansasCityMember2020-01-012020-12-31utr:sqft0001360604hta:LandinMiamiFloridaMember2020-01-012020-12-310001360604hta:PropertyInGreenvilleSouthCarolinaMember2018-08-012018-08-31hta:transaction0001360604hta:MedicalOfficeBuildingInMassachusettsMember2019-01-012019-12-310001360604hta:MedicalOfficeBuildingsInTennesseeTexasAndSouthCarolinaMember2018-01-012018-12-310001360604us-gaap:LeasesAcquiredInPlaceMember2020-12-310001360604us-gaap:LeasesAcquiredInPlaceMember2020-01-012020-12-310001360604us-gaap:LeasesAcquiredInPlaceMember2019-12-310001360604us-gaap:LeasesAcquiredInPlaceMember2019-01-012019-12-310001360604us-gaap:CustomerRelationshipsMember2020-12-310001360604us-gaap:CustomerRelationshipsMember2020-01-012020-12-310001360604us-gaap:CustomerRelationshipsMember2019-12-310001360604us-gaap:CustomerRelationshipsMember2019-01-012019-12-310001360604us-gaap:AboveMarketLeasesMember2020-12-310001360604us-gaap:AboveMarketLeasesMember2020-01-012020-12-310001360604us-gaap:AboveMarketLeasesMember2019-12-310001360604us-gaap:AboveMarketLeasesMember2019-01-012019-12-310001360604hta:BelowMarketLeaseMember2020-12-310001360604hta:BelowMarketLeaseMember2020-01-012020-12-310001360604hta:BelowMarketLeaseMember2019-12-310001360604hta:BelowMarketLeaseMember2019-01-012019-12-310001360604hta:RentalIncomeMember2020-01-012020-12-310001360604hta:RentalIncomeMember2019-01-012019-12-310001360604hta:RentalIncomeMember2018-01-012018-12-310001360604hta:RentalExpensesMember2020-01-012020-12-310001360604hta:RentalExpensesMember2019-01-012019-12-310001360604hta:RentalExpensesMember2018-01-012018-12-310001360604hta:LeasesAcquiredInPlaceAndCustomerRelationshipsMember2020-01-012020-12-310001360604hta:LeasesAcquiredInPlaceAndCustomerRelationshipsMember2019-01-012019-12-310001360604hta:LeasesAcquiredInPlaceAndCustomerRelationshipsMember2018-01-012018-12-31hta:lease0001360604us-gaap:RevolvingCreditFacilityMember2020-12-310001360604us-gaap:RevolvingCreditFacilityMember2019-12-310001360604us-gaap:UnsecuredDebtMember2020-12-310001360604us-gaap:UnsecuredDebtMember2019-12-310001360604us-gaap:SeniorNotesMember2020-12-310001360604us-gaap:SeniorNotesMember2019-12-310001360604us-gaap:MortgagesMember2020-12-310001360604us-gaap:MortgagesMember2019-12-310001360604us-gaap:RevolvingCreditFacilityMember2017-12-310001360604us-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2017-12-310001360604us-gaap:UnsecuredDebtMemberhta:ThreeHundredMillionUnsecuredTermLoanMember2017-12-310001360604srt:MinimumMemberus-gaap:LondonInterbankOfferedRateLIBORMemberus-gaap:RevolvingCreditFacilityMember2020-01-012020-12-310001360604us-gaap:LondonInterbankOfferedRateLIBORMembersrt:MaximumMemberus-gaap:RevolvingCreditFacilityMember2020-01-012020-12-310001360604srt:MinimumMemberus-gaap:RevolvingCreditFacilityMember2020-01-012020-12-310001360604srt:MaximumMemberus-gaap:RevolvingCreditFacilityMember2020-01-012020-12-310001360604us-gaap:RevolvingCreditFacilityMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-01-012020-12-310001360604srt:MinimumMemberus-gaap:LondonInterbankOfferedRateLIBORMemberus-gaap:UnsecuredDebtMemberhta:ThreeHundredMillionUnsecuredTermLoanMember2020-01-012020-12-310001360604us-gaap:LondonInterbankOfferedRateLIBORMemberus-gaap:UnsecuredDebtMemberhta:ThreeHundredMillionUnsecuredTermLoanMembersrt:MaximumMember2020-01-012020-12-310001360604us-gaap:UnsecuredDebtMemberhta:ThreeHundredMillionUnsecuredTermLoanMember2020-01-012020-12-310001360604us-gaap:UnsecuredDebtMemberhta:ThreeHundredMillionUnsecuredTermLoanMember2020-12-310001360604hta:TwoHundredMillionUnsecuredTermLoanMemberus-gaap:UnsecuredDebtMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-12-310001360604hta:TwoHundredMillionUnsecuredTermLoanMemberus-gaap:UnsecuredDebtMemberhta:HealthcareTrustofAmericaHoldingsLPMember2018-12-310001360604hta:TwoHundredMillionUnsecuredTermLoanMemberus-gaap:UnsecuredDebtMemberhta:HealthcareTrustofAmericaHoldingsLPMember2018-01-012018-12-310001360604hta:TwoHundredMillionUnsecuredTermLoanMembersrt:MinimumMemberus-gaap:LondonInterbankOfferedRateLIBORMemberus-gaap:UnsecuredDebtMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-01-012020-12-310001360604hta:TwoHundredMillionUnsecuredTermLoanMemberus-gaap:LondonInterbankOfferedRateLIBORMemberus-gaap:UnsecuredDebtMembersrt:MaximumMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-01-012020-12-310001360604hta:TwoHundredMillionUnsecuredTermLoanMemberus-gaap:UnsecuredDebtMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-01-012020-12-310001360604us-gaap:SeniorNotesMemberhta:UnsecuredSeniorNotesDue2023Memberhta:HealthcareTrustofAmericaHoldingsLPMember2020-09-300001360604us-gaap:SeniorNotesMemberhta:UnsecuredSeniorNotes8000MillionMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-09-012020-09-300001360604us-gaap:SeniorNotesMemberhta:UnsecuredSeniorNotesDue2023Memberhta:HealthcareTrustofAmericaHoldingsLPMember2020-09-012020-09-300001360604us-gaap:SeniorNotesMemberhta:UnsecuredSeniorNotesDue2026Memberhta:HealthcareTrustofAmericaHoldingsLPMember2020-09-300001360604us-gaap:SeniorNotesMemberhta:UnsecuredSeniorNotes650.0MillionMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-12-310001360604hta:UnsecuredSeniorNotes250.0MillionMemberus-gaap:SeniorNotesMemberhta:HealthcareTrustofAmericaHoldingsLPMember2019-09-012019-09-300001360604hta:UnsecuredSeniorNotes350.0MillionMemberus-gaap:SeniorNotesMemberhta:HealthcareTrustofAmericaHoldingsLPMember2016-07-120001360604hta:UnsecuredSeniorNotes250.0MillionMemberus-gaap:SeniorNotesMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-09-300001360604us-gaap:SeniorNotesMemberhta:UnsecuredSeniorNotesDue2026Memberhta:HealthcareTrustofAmericaHoldingsLPMember2020-12-310001360604hta:UnsecuredSeniorNotesDueJuly2027Memberus-gaap:SeniorNotesMemberhta:HealthcareTrustofAmericaHoldingsLPMember2018-12-310001360604hta:UnsecuredSeniorNotesDueJuly2027Memberus-gaap:SeniorNotesMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-12-310001360604us-gaap:SeniorNotesMemberhta:UnsecuredSeniorNotes650.0MillionMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-09-300001360604us-gaap:SeniorNotesMemberhta:UnsecuredSeniorNotes8000MillionMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-12-310001360604us-gaap:MortgagesMemberhta:HealthcareTrustofAmericaHoldingsLPMember2020-01-012020-12-31hta:derivative0001360604us-gaap:InterestRateSwapMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:CashFlowHedgingMember2020-12-310001360604us-gaap:InterestRateSwapMemberhta:ReceivablesandOtherAssetsMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:CashFlowHedgingMember2020-12-310001360604us-gaap:InterestRateSwapMemberhta:ReceivablesandOtherAssetsMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:CashFlowHedgingMember2019-12-310001360604us-gaap:InterestRateSwapMemberus-gaap:DerivativeFinancialInstrumentsLiabilitiesMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:CashFlowHedgingMember2020-12-310001360604us-gaap:InterestRateSwapMemberus-gaap:DerivativeFinancialInstrumentsLiabilitiesMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:CashFlowHedgingMember2019-12-310001360604us-gaap:InterestRateSwapMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:CashFlowHedgingMember2020-01-012020-12-310001360604us-gaap:InterestRateSwapMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:CashFlowHedgingMember2019-01-012019-12-310001360604us-gaap:InterestRateSwapMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:CashFlowHedgingMember2018-01-012018-12-310001360604hta:ATMOfferingProgramMember2018-12-310001360604hta:ATMOfferingProgramMember2019-11-300001360604hta:ATMOfferingProgramMember2020-01-012020-12-310001360604hta:ATMOfferingProgramMember2020-12-31hta:Arrangement0001360604hta:ForwardSaleArrangementsMember2020-01-012020-12-3100013606042020-09-300001360604hta:A2006IncentivePlanMember2020-12-310001360604us-gaap:RestrictedStockMember2020-01-012020-12-310001360604us-gaap:RestrictedStockMember2019-01-012019-12-310001360604us-gaap:RestrictedStockMember2018-01-012018-12-310001360604us-gaap:RestrictedStockMembersrt:MinimumMember2020-01-012020-12-310001360604us-gaap:RestrictedStockMembersrt:MaximumMember2020-01-012020-12-310001360604us-gaap:RestrictedStockMemberus-gaap:GeneralAndAdministrativeExpenseMember2020-01-012020-12-310001360604us-gaap:RestrictedStockMemberus-gaap:GeneralAndAdministrativeExpenseMember2019-01-012019-12-310001360604us-gaap:RestrictedStockMemberus-gaap:GeneralAndAdministrativeExpenseMember2018-01-012018-12-310001360604us-gaap:RestrictedStockMember2020-12-310001360604us-gaap:RestrictedStockMember2019-12-310001360604us-gaap:RestrictedStockMember2018-12-310001360604us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Memberus-gaap:CarryingReportedAmountFairValueDisclosureMember2020-12-310001360604us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Memberus-gaap:EstimateOfFairValueFairValueDisclosureMember2020-12-310001360604us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Memberus-gaap:CarryingReportedAmountFairValueDisclosureMember2019-12-310001360604us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Memberus-gaap:EstimateOfFairValueFairValueDisclosureMember2019-12-310001360604hta:ForwardSaleArrangementsMember2020-12-310001360604srt:ParentCompanyMember2020-01-012020-03-310001360604srt:ParentCompanyMember2020-04-012020-06-300001360604srt:ParentCompanyMember2020-07-012020-09-300001360604srt:ParentCompanyMember2020-10-012020-12-310001360604srt:ParentCompanyMember2019-01-012019-03-310001360604srt:ParentCompanyMember2019-04-012019-06-300001360604srt:ParentCompanyMember2019-07-012019-09-300001360604srt:ParentCompanyMember2019-10-012019-12-310001360604hta:HealthcareTrustofAmericaHoldingsLPMember2020-01-012020-03-310001360604hta:HealthcareTrustofAmericaHoldingsLPMember2020-04-012020-06-300001360604hta:HealthcareTrustofAmericaHoldingsLPMember2020-07-012020-09-300001360604hta:HealthcareTrustofAmericaHoldingsLPMember2020-10-012020-12-310001360604hta:HealthcareTrustofAmericaHoldingsLPMember2019-01-012019-03-310001360604hta:HealthcareTrustofAmericaHoldingsLPMember2019-04-012019-06-300001360604hta:HealthcareTrustofAmericaHoldingsLPMember2019-07-012019-09-300001360604hta:HealthcareTrustofAmericaHoldingsLPMember2019-10-012019-12-310001360604hta:ShelbyMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ShelbyMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:SimonWilliamsonClinicMember2020-12-310001360604hta:OperatingPropertiesMemberhta:SimonWilliamsonClinicMember2020-01-012020-12-310001360604hta:JasperMemberhta:OperatingPropertiesMember2020-12-310001360604hta:JasperMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:PhoenixMedCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:PhoenixMedCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ThunderbirdMedicalPlazaMedicalOfficeMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ThunderbirdMedicalPlazaMedicalOfficeMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:PeoriaMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:PeoriaMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:BaptistMCMemberhta:OperatingPropertiesMember2020-12-310001360604hta:BaptistMCMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DesertRidgeMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DesertRidgeMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DignityPhoenixMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:EstrellaMedCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:EstrellaMedCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:SunCityBoswellMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SunCityBoswellMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:SunCityBoswellWestMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SunCityBoswellWestMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:SunCityWebbMPMember2020-12-310001360604hta:OperatingPropertiesMemberhta:SunCityWebbMPMember2020-01-012020-12-310001360604hta:SunCityWestMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SunCityWestMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:GatewayMedPlazaMemberhta:OperatingPropertiesMember2020-12-310001360604hta:GatewayMedPlazaMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:TucsonAcademyMOPMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TucsonAcademyMOPMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:TucsonDesertLifeMOPMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TucsonDesertLifeMOPMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DignityMercyMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DignityMercyMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:FiveNineNineFivePlazaDriveMemberhta:OperatingPropertiesMember2020-12-310001360604hta:FiveNineNineFivePlazaDriveMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DignityGlendaleMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DignityGlendaleMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ThirdStreetMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ThirdStreetMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:MissionMedicalCenterBuilding1Member2020-12-310001360604hta:OperatingPropertiesMemberhta:MissionMedicalCenterBuilding1Member2020-01-012020-12-310001360604hta:DignityNorthridgeMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SanLuisObispoMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SanLuisObispoMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:FaceyMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:FaceyMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DignityMarianMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SCLHealthMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SCLHealthMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:RampartMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:RampartMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:HampdenPlaceMedicalOfficeBuildingMemberhta:OperatingPropertiesMember2020-12-310001360604hta:HampdenPlaceMedicalOfficeBuildingMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:HighlandsRanchParkPlazaMedicalOfficeMemberhta:OperatingPropertiesMember2020-12-310001360604hta:HighlandsRanchParkPlazaMedicalOfficeMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:LoneTreeMedicalOfficeBuildingsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:LoneTreeMedicalOfficeBuildingsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:LincolnMedicalCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:LincolnMedicalCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:EightyFisherMemberhta:OperatingPropertiesMember2020-12-310001360604hta:EightyFisherMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:FiveHundredThirtyThreeCottageNorthwesternMemberhta:OperatingPropertiesMember2020-12-310001360604hta:FiveHundredThirtyThreeCottageNorthwesternMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:NorthwesternMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:NorthwesternMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:FourHundredSixFarmingtonMemberhta:OperatingPropertiesMember2020-12-310001360604hta:FourHundredSixFarmingtonMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:SevenHundredFourHebronMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SevenHundredFourHebronMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:GatewaysMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:GatewaysMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:HamdenMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:HamdenMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:HaynesMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:HaynesMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:PomeroyMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:PomeroyMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:SaybrookMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SaybrookMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:YaleLongWharfMember2020-12-310001360604hta:OperatingPropertiesMemberhta:YaleLongWharfMember2020-01-012020-12-310001360604hta:DevineMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DevineMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:EvergreenMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:EvergreenMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:WestportCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:WestportCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:DayHillMOBsMember2020-12-310001360604hta:OperatingPropertiesMemberhta:DayHillMOBsMember2020-01-012020-12-310001360604hta:RiversideMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:RiversideMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:BrandonMOPMemberhta:OperatingPropertiesMember2020-12-310001360604hta:BrandonMOPMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:McMullenMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:McMullenMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OrlandoRehabHospitalMemberhta:OperatingPropertiesMember2020-12-310001360604hta:OrlandoRehabHospitalMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:PalmettoMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:PalmettoMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:PalmettoIIMemberhta:OperatingPropertiesMember2020-12-310001360604hta:PalmettoIIMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:EastFLSeniorJacksonvilleMemberhta:OperatingPropertiesMember2020-12-310001360604hta:EastFLSeniorJacksonvilleMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:KingStreetMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:KingStreetMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:JupiterMPMemberhta:OperatingPropertiesMember2020-12-310001360604hta:JupiterMPMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CentralFLSCMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CentralFLSCMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:VistaProCenterMOPMemberhta:OperatingPropertiesMember2020-12-310001360604hta:VistaProCenterMOPMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:LargoMedicalCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:LargoMedicalCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:LargoMOPMemberhta:OperatingPropertiesMember2020-12-310001360604hta:LargoMOPMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:FLFamilyMedicalCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:FLFamilyMedicalCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:NorthwestMedicalParkMemberhta:OperatingPropertiesMember2020-12-310001360604hta:NorthwestMedicalParkMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:NorthShoreMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:NorthShoreMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:SunsetProfessionalandKendallMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SunsetProfessionalandKendallMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CommonVMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CommonVMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OrlandoLakeUnderhillMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:OrlandoLakeUnderhillMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:FloridaHospitalMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:FloridaHospitalMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OrlandoOviedoMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:OrlandoOviedoMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:HeartFamilyHealthMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:HeartFamilyHealthMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:St.LucieMCMemberhta:OperatingPropertiesMember2020-12-310001360604hta:St.LucieMCMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:EastFLSeniorSunriseMemberhta:OperatingPropertiesMember2020-12-310001360604hta:EastFLSeniorSunriseMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:TallahasseeRehabHospitalMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TallahasseeRehabHospitalMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OptimalMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:OptimalMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:TampaMedicalVillageMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TampaMedicalVillageMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:VAMOBsMember2020-12-310001360604hta:OperatingPropertiesMemberhta:VAMOBsMember2020-01-012020-12-310001360604hta:FLOrthoInstituteMemberhta:OperatingPropertiesMember2020-12-310001360604hta:FLOrthoInstituteMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:WellingtonMAPIIIMember2020-12-310001360604hta:OperatingPropertiesMemberhta:WellingtonMAPIIIMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:VictorFarrisMOBMember2020-12-310001360604hta:OperatingPropertiesMemberhta:VictorFarrisMOBMember2020-01-012020-12-310001360604hta:EastFLSeniorWinterParkMemberhta:OperatingPropertiesMember2020-12-310001360604hta:EastFLSeniorWinterParkMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CampCreekMedCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CampCreekMedCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CampCreekMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CampCreekMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:NorthAtlantaMOBsMember2020-12-310001360604hta:OperatingPropertiesMemberhta:NorthAtlantaMOBsMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:AugustaRehabHospitalMember2020-12-310001360604hta:OperatingPropertiesMemberhta:AugustaRehabHospitalMember2020-01-012020-12-310001360604hta:AustellMedicalParkMemberhta:OperatingPropertiesMember2020-12-310001360604hta:AustellMedicalParkMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:HarbinClinicMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DecaturMPMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DecaturMPMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:YorktownMCMemberhta:OperatingPropertiesMember2020-12-310001360604hta:YorktownMCMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:GwinettMOPMemberhta:OperatingPropertiesMember2020-12-310001360604hta:GwinettMOPMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:MariettaHealthParkMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MariettaHealthParkMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:WellStarTowerMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:WellStarTowerMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ShakeragMCMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ShakeragMCMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OverlookAtEaglesLandingMemberhta:OperatingPropertiesMember2020-12-310001360604hta:OverlookAtEaglesLandingMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:SouthcrestMedicalPlazaMedicalOfficeMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SouthcrestMedicalPlazaMedicalOfficeMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CherokeeMedicalCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CherokeeMedicalCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:HonoluluMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:HonoluluMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:KapoleiMedicalParkMemberhta:OperatingPropertiesMember2020-12-310001360604hta:KapoleiMedicalParkMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:NorthCurtisRoadMemberhta:OperatingPropertiesMember2020-12-310001360604hta:NorthCurtisRoadMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:EagleRoadMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:EagleRoadMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ChicagoMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:OperatingPropertiesMemberhta:StreetervilleCenterMOBMember2020-12-310001360604hta:OperatingPropertiesMemberhta:StreetervilleCenterMOBMember2020-01-012020-12-310001360604hta:RushOakParkMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:RushOakParkMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:BrownsburgMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:BrownsburgMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:AthensSCMemberhta:OperatingPropertiesMember2020-12-310001360604hta:AthensSCMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CrawfordsvilleMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CrawfordsvilleMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DeaconessClinicDowntownMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DeaconessClinicDowntownMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DeaconessClinicWestsideMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DeaconessClinicWestsideMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DupontMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DupontMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:Ft.WayneMOBMember2020-12-310001360604hta:OperatingPropertiesMemberhta:Ft.WayneMOBMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:CommunityMPMember2020-12-310001360604hta:OperatingPropertiesMemberhta:CommunityMPMember2020-01-012020-12-310001360604hta:EagleHighlandsMOPMemberhta:OperatingPropertiesMember2020-12-310001360604hta:EagleHighlandsMOPMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:EplerParkeMOPDomainhta:OperatingPropertiesMember2020-12-310001360604hta:EplerParkeMOPDomainhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:GlendaleProfPlazaMember2020-12-310001360604hta:OperatingPropertiesMemberhta:GlendaleProfPlazaMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:MMPEagleHighlandsMember2020-12-310001360604hta:OperatingPropertiesMemberhta:MMPEagleHighlandsMember2020-01-012020-12-310001360604hta:MMPEastMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MMPEastMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:MMPNorthMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MMPNorthMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:MMPSouthMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MMPSouthMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:SouthpointeMOPMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SouthpointeMOPMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:St.VincentMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:St.VincentMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:KokomoMedicalOfficeParkMedicalOfficeMemberhta:OperatingPropertiesMember2020-12-310001360604hta:KokomoMedicalOfficeParkMedicalOfficeMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DeaconessClinicGatewayMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DeaconessClinicGatewayMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CommunityHealthPavilionMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CommunityHealthPavilionMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ZionsvilleMCMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ZionsvilleMCMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:NashobaValleyMedCenterMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:NashobaValleyMedCenterMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:A670AlbanyMemberhta:OperatingPropertiesMember2020-12-310001360604hta:A670AlbanyMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:TuftsMedicalCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TuftsMedicalCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:St.ElizabethsMedCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:St.ElizabethsMedCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:PearlStreetMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:PearlStreetMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:GoodSamaritanCancerCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:GoodSamaritanCancerCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CarneyHospitalMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CarneyHospitalMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:St.AnnesHospitalMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:St.AnnesHospitalMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:NorwoodHospitalMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:NorwoodHospitalMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:HolyFamilyHospitalMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:HolyFamilyHospitalMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:MortonHospitalMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MortonHospitalMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:StetsonMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:StetsonMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:JohnstonProfessionalBuildingMemberhta:OperatingPropertiesMember2020-12-310001360604hta:JohnstonProfessionalBuildingMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:TriadTechCenterMember2020-12-310001360604hta:OperatingPropertiesMemberhta:TriadTechCenterMember2020-01-012020-12-310001360604hta:StJohnProvidenceMobMemberhta:OperatingPropertiesMember2020-12-310001360604hta:StJohnProvidenceMobMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:FortRoadMedicalBuildingMemberhta:OperatingPropertiesMember2020-12-310001360604hta:FortRoadMedicalBuildingMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:GalleryProfessionalBuildingMemberhta:OperatingPropertiesMember2020-12-310001360604hta:GalleryProfessionalBuildingMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ChesterfieldRehabHospitalMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ChesterfieldRehabHospitalMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:BJCWestCountyMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:BJCWestCountyMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:WinghavenMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:WinghavenMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:BJCMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:BJCMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DesPeresMAPIIMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DesPeresMAPIIMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:BaptistMemorialMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:BaptistMemorialMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:MedicalParkOfCaryMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MedicalParkOfCaryMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:RexCaryMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:RexCaryMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:TyronOfficeCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TyronOfficeCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CarolinasHealthMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CarolinasHealthMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:DavidsonMOBMember2020-12-310001360604hta:OperatingPropertiesMemberhta:DavidsonMOBMember2020-01-012020-12-310001360604hta:DukeFertilityCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DukeFertilityCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:HockPlazaIIMemberhta:OperatingPropertiesMember2020-12-310001360604hta:HockPlazaIIMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:UNCRexHollySpringsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:UNCRexHollySpringsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:HuntersvilleOfficeParkMemberhta:OperatingPropertiesMember2020-12-310001360604hta:HuntersvilleOfficeParkMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:RosedaleMOBMember2020-12-310001360604hta:OperatingPropertiesMemberhta:RosedaleMOBMember2020-01-012020-12-310001360604hta:MedicalParkMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MedicalParkMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ThreeOneZeroZeroBlueRidgeMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ThreeOneZeroZeroBlueRidgeMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:RaleighMedicalCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:RaleighMedicalCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:SandyForksMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SandyForksMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:SunsetRidgeMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SunsetRidgeMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:PiedmondMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:PiedmondMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:HackensackMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:HackensackMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:MountainViewMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MountainViewMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:SantaFe440MOBMember2020-12-310001360604hta:OperatingPropertiesMemberhta:SantaFe440MOBMember2020-01-012020-12-310001360604hta:SanMartinMAPMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SanMartinMAPMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:MadisonAveMOBMember2020-12-310001360604hta:OperatingPropertiesMemberhta:MadisonAveMOBMember2020-01-012020-12-310001360604hta:PatroonCreekHQMemberhta:OperatingPropertiesMember2020-12-310001360604hta:PatroonCreekHQMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:PatroonCreekMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:PatroonCreekMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:WashingtonAveMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:WashingtonAveMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:PutnamMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:PutnamMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CapitalRegionHealthParkMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CapitalRegionHealthParkMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ACPMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ACPMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:A210WestchesterMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:A210WestchesterMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:WestchesterMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:WestchesterMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DileyRidgeMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DileyRidgeMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:GoodSamMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:GoodSamMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:JewishMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:JewishMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:TrihealthMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TrihealthMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OlentangyMemberhta:OperatingPropertiesMember2020-12-310001360604hta:OlentangyMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:MarketExchangeMOPMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MarketExchangeMOPMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:PolarisMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:PolarisMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:GahannaMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:GahannaMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:KindredMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:KindredMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:HillardIIMemberhta:OperatingPropertiesMember2020-12-310001360604hta:HillardIIMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:HilliardMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:HilliardMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:ParkPlaceMOPMember2020-12-310001360604hta:OperatingPropertiesMemberhta:ParkPlaceMOPMember2020-01-012020-12-310001360604hta:LibertyFallsMedicalPlazaMedicalOfficeMemberhta:OperatingPropertiesMember2020-12-310001360604hta:LibertyFallsMedicalPlazaMedicalOfficeMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ParmaRidgeMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ParmaRidgeMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:StAnnsMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:StAnnsMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DeaconessMOPMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DeaconessMOPMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:SilvertonHealthMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SilvertonHealthMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:MonroevilleMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MonroevilleMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:A2750MonroeMOBMember2020-12-310001360604hta:OperatingPropertiesMemberhta:A2750MonroeMOBMember2020-01-012020-12-310001360604hta:OneSevenFourZeroSouthMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:OneSevenFourZeroSouthMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:MainLineBrynMawrMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MainLineBrynMawrMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:FederalNorthMedicalOfficeBuildingMember2020-12-310001360604hta:OperatingPropertiesMemberhta:FederalNorthMedicalOfficeBuildingMember2020-01-012020-12-310001360604hta:HighmarkPennAveMemberhta:OperatingPropertiesMember2020-12-310001360604hta:HighmarkPennAveMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:WPAlleghenyHQMOBMember2020-12-310001360604hta:OperatingPropertiesMemberhta:WPAlleghenyHQMOBMember2020-01-012020-12-310001360604hta:ThirtyNineBroadStreetMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ThirtyNineBroadStreetMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CannonParkPlaceMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CannonParkPlaceMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:MUSCElmMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MUSCElmMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:TidesMedicalArtsCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TidesMedicalArtsCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:EastCooperMedicalArtsCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:EastCooperMedicalArtsCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:EastCooperMedicalCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:EastCooperMedicalCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:MUSCUniversityMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MUSCUniversityMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:St.ThomasDePaulMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:St.ThomasDePaulMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:MountainEmpireMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MountainEmpireMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:AmarilloHospitalMemberhta:OperatingPropertiesMember2020-12-310001360604hta:AmarilloHospitalMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:AustinHeartMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:AustinHeartMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:BSWMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:BSWMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:PostOakNorthMCMemberhta:OperatingPropertiesMember2020-12-310001360604hta:PostOakNorthMCMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:MatureWellMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MatureWellMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:TexasAMHealthScienceCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TexasAMHealthScienceCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DalasRehabHospitalMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DalasRehabHospitalMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CedarHillMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CedarHillMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CedarParkMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CedarParkMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CorsicanaMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CorsicanaMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DallasLtacHospitalMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DallasLtacHospitalMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ForestParkPavilionMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ForestParkPavilionMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ForestParkTowerMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ForestParkTowerMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:NorthpointMedicalMemberhta:OperatingPropertiesMember2020-12-310001360604hta:NorthpointMedicalMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:BaylorMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:BaylorMOBsMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DentonMedicalRehabilitationHospitalMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DentonMedicalRehabilitationHospitalMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:DentonMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:DentonMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ElPasoMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ElPasoMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CliffMedicalPlazaMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CliffMedicalPlazaMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ProvidenceMedicalPlazaMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ProvidenceMedicalPlazaMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:SierraMedicalMember2020-12-310001360604hta:OperatingPropertiesMemberhta:SierraMedicalMember2020-01-012020-12-310001360604hta:TexasTechMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TexasTechMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:TexasHealthMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TexasHealthMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ConiferMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ConiferMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ForestParkFriscoMCMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ForestParkFriscoMCMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:GreenvilleMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:GreenvilleMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:GeminiMOBMember2020-12-310001360604hta:OperatingPropertiesMemberhta:GeminiMOBMember2020-01-012020-12-310001360604hta:A7900FanninMemberhta:OperatingPropertiesMember2020-12-310001360604hta:A7900FanninMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CypressMedicalBuildingMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CypressMedicalBuildingMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:CypressStationMedicalOfficeBuildingMedicalOfficeMemberhta:OperatingPropertiesMember2020-12-310001360604hta:CypressStationMedicalOfficeBuildingMedicalOfficeMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:ParkPlazaMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:ParkPlazaMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:TriumphHospitalNWMember2020-12-310001360604hta:OperatingPropertiesMemberhta:TriumphHospitalNWMember2020-01-012020-12-310001360604hta:MemorialHermannMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:JordantonMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:JordantonMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:HoustonMethodistMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:LoneStarEndoscopyMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:LoneStarEndoscopyMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:SetonMedicalMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SetonMedicalMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:LewisvilleMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:LewisvilleMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:LongviewRegionalMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TerraceMedicalBuildingMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TerraceMedicalBuildingMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:TowersMedicalPlazaMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TowersMedicalPlazaMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:NorthCypressMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:PearlandMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:PearlandMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:IndependenceMedicalVillageMemberhta:OperatingPropertiesMember2020-12-310001360604hta:IndependenceMedicalVillageMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:SanAngeloMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SanAngeloMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:MtnPlainsPecanValleyMember2020-12-310001360604hta:OperatingPropertiesMemberhta:MtnPlainsPecanValleyMember2020-01-012020-12-310001360604hta:SugarLand2MedicalOfficeBuildingMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SugarLand2MedicalOfficeBuildingMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:TriumphHospitalSWMemberhta:OperatingPropertiesMember2020-12-310001360604hta:TriumphHospitalSWMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:MtnPlainsClearLakeMemberhta:OperatingPropertiesMember2020-12-310001360604hta:MtnPlainsClearLakeMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:N.TexasNeurologyMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:N.TexasNeurologyMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:WylieMedicalPlazaMemberhta:OperatingPropertiesMember2020-12-310001360604hta:WylieMedicalPlazaMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:RenaissanceMedicalCenterMemberhta:OperatingPropertiesMember2020-12-310001360604hta:RenaissanceMedicalCenterMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:SaltLakeRegionalMedicalBuildingMemberhta:OperatingPropertiesMember2020-12-310001360604hta:SaltLakeRegionalMedicalBuildingMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:FairfaxMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:FairfaxMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:FairOaksMOBMemberhta:OperatingPropertiesMember2020-12-310001360604hta:FairOaksMOBMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:AuroraMenomeneeMemberhta:OperatingPropertiesMember2020-12-310001360604hta:AuroraMenomeneeMemberhta:OperatingPropertiesMember2020-01-012020-12-310001360604hta:OperatingPropertiesMemberhta:AuroraMilwaukeeMember2020-12-310001360604hta:OperatingPropertiesMemberhta:AuroraMilwaukeeMember2020-01-012020-12-310001360604hta:ColumbiaSt.MarysMOBsMemberhta:OperatingPropertiesMember2020-12-310001360604hta:OperatingPropertiesMember2020-12-310001360604us-gaap:LandMemberhta:CoralReefMember2020-12-310001360604us-gaap:LandMemberhta:ForestParkPavilionIIIMember2020-12-310001360604us-gaap:LandMemberhta:A1737NLoopMember2020-12-310001360604us-gaap:LandMember2020-12-310001360604hta:DignityPhoenixMOBsMembersrt:MinimumMember2020-01-012020-12-310001360604hta:DignityPhoenixMOBsMembersrt:MaximumMember2020-01-012020-12-310001360604hta:DignityNorthridgeMOBsMembersrt:MinimumMember2020-01-012020-12-310001360604hta:DignityNorthridgeMOBsMembersrt:MaximumMember2020-01-012020-12-310001360604srt:MinimumMemberhta:DignityMarianMOBsMember2020-01-012020-12-310001360604srt:MaximumMemberhta:DignityMarianMOBsMember2020-01-012020-12-310001360604srt:MinimumMemberhta:HarbinClinicMOBsMember2020-01-012020-12-310001360604hta:HarbinClinicMOBsMembersrt:MaximumMember2020-01-012020-12-310001360604hta:ChicagoMOBsMembersrt:MinimumMember2020-01-012020-12-310001360604hta:ChicagoMOBsMembersrt:MaximumMember2020-01-012020-12-310001360604hta:MemorialHermannMOBsMembersrt:MinimumMember2020-01-012020-12-310001360604hta:MemorialHermannMOBsMembersrt:MaximumMember2020-01-012020-12-310001360604srt:MinimumMemberhta:LongviewRegionalMOBsMember2020-01-012020-12-310001360604srt:MaximumMemberhta:LongviewRegionalMOBsMember2020-01-012020-12-310001360604hta:NorthCypressMOBsMembersrt:MinimumMember2020-01-012020-12-310001360604hta:NorthCypressMOBsMembersrt:MaximumMember2020-01-012020-12-310001360604srt:MinimumMemberhta:HoustonMethodistMOBsMember2020-01-012020-12-310001360604hta:HoustonMethodistMOBsMembersrt:MaximumMember2020-01-012020-12-310001360604srt:MinimumMemberhta:ColumbiaSt.MarysMOBsMember2020-01-012020-12-310001360604srt:MaximumMemberhta:ColumbiaSt.MarysMOBsMember2020-01-012020-12-310001360604hta:MedicalRealEstateInTexasMaturingInJune2021Memberstpr:TX2020-01-012020-12-310001360604hta:MedicalRealEstateInTexasMaturingInJune2021Memberstpr:TX2020-12-310001360604hta:MedicalRealEstateInTexasMaturingInMarch2021Memberstpr:TX2020-01-012020-12-310001360604hta:MedicalRealEstateInTexasMaturingInMarch2021Memberstpr:TX2020-12-31hta:payment

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the year ended December 31, 2020

or

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-35568 (Healthcare Trust of America, Inc.)

Commission File Number: 333-190916 (Healthcare Trust of America Holdings, LP)

HEALTHCARE TRUST OF AMERICA, INC.

HEALTHCARE TRUST OF AMERICA HOLDINGS, LP

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | | | | | | | | | | |

| Maryland | (Healthcare Trust of America, Inc.) | | | 20-4738467 | |

| Delaware | (Healthcare Trust of America Holdings, LP) | | | 20-4738347 | |

| (State or other jurisdiction of incorporation or organization) | | | (I.R.S. Employer Identification No.) | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 16435 N. Scottsdale Road, Suite 320, | Scottsdale, | Arizona | 85254 | | | (480) | 998-3478 | | | http://www.htareit.com | |

| (Address of principal executive office and zip code) | | | (Registrant's telephone number, including area code) | | | (Internet address) | |

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading symbol(s) | | Name of each exchange on which registered |

| Common stock, $0.01 par value | | HTA | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Healthcare Trust of America, Inc. | ☒ | Yes | ☐ | No | | Healthcare Trust of America Holdings, LP | ☒ | Yes | ☐ | No |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Healthcare Trust of America, Inc. | ☐ | Yes | ☒ | No | | Healthcare Trust of America Holdings, LP | ☐ | Yes | ☒ | No |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Healthcare Trust of America, Inc. | ☒ | Yes | ☐ | No | | Healthcare Trust of America Holdings, LP | ☒ | Yes | ☐ | No |

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Healthcare Trust of America, Inc. | ☒ | Yes | ☐ | No | | Healthcare Trust of America Holdings, LP | ☒ | Yes | ☐ | No |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | |

| Healthcare Trust of America, Inc. | ☒ | Large accelerated filer | ☐ | Accelerated filer | ☐ | Non-accelerated filer |

| Healthcare Trust of America Holdings, LP | ☐ | Large accelerated filer | ☐ | Accelerated filer | ☒ | Non-accelerated filer |

| | | | | | | | | | | | | | |

| Healthcare Trust of America, Inc. | ☐ | Smaller reporting company | ☐ | Emerging growth company |

| Healthcare Trust of America Holdings, LP | ☐ | Smaller reporting company | ☐ | Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13 (a) of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Healthcare Trust of America, Inc. | ☐ | | | | | Healthcare Trust of America Holdings, LP | ☐ | | | |

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Healthcare Trust of America, Inc. | ☒ | Yes | ☐ | No | | Healthcare Trust of America Holdings, LP | ☒ | Yes | ☐ | No |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Healthcare Trust of America, Inc. | ☐ | Yes | ☒ | No | | Healthcare Trust of America Holdings, LP | ☐ | Yes | ☒ | No |

The aggregate market value of Healthcare Trust of America, Inc.’s Class A common stock held by non-affiliates as of June 30, 2020, the last business day of the most recently completed second fiscal quarter, was approximately $5,769,387,334, computed by reference to the closing price as reported on the New York Stock Exchange.

As of February 18, 2021, there were 218,745,900 shares of Class A common stock of Healthcare Trust of America, Inc. outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive Proxy statement for the Annual Meeting of Stockholders are incorporated by reference into Part III, Items 10-14 of this Annual Report on Form 10-K.

Explanatory Note

This annual report combines the Annual Reports on Form 10-K (“Annual Report”) for the year ended December 31, 2020, of Healthcare Trust of America, Inc. (“HTA”), a Maryland corporation, and Healthcare Trust of America Holdings, LP (“HTALP”), a Delaware limited partnership. Unless otherwise indicated or unless the context requires otherwise, all references in this Annual Report to “we,” “us,” “our,” “the Company” or “our Company” refer to HTA and HTALP, collectively, and all references to “common stock” shall refer to the Class A common stock of HTA.

HTA operates as a real estate investment trust (“REIT”) and is the general partner of HTALP. As of December 31, 2020, HTA owned a 98.4% partnership interest in HTALP, and other limited partners, including some of HTA’s directors, executive officers and their affiliates, owned the remaining partnership interest (including the long-term incentive plan (“LTIP” Units)) in HTALP. As the sole general partner of HTALP, HTA has the full, exclusive and complete responsibility for HTALP’s day-to-day management and control, including its compliance with the Securities and Exchange Commission (“SEC”) filing requirements.

We believe it is important to understand the few differences between HTA and HTALP in the context of how we operate as an integrated consolidated company. HTA operates as an umbrella partnership REIT structure in which HTALP and its subsidiaries hold substantially all of the assets. HTA’s only material asset is its ownership of partnership interests of HTALP. As a result, HTA does not conduct business itself, other than acting as the sole general partner of HTALP, issuing public equity from time to time and guaranteeing certain debts of HTALP. HTALP conducts the operations of the business and issues publicly-traded debt, but has no publicly-traded equity. Except for net proceeds from public equity issuances by HTA, which are generally contributed to HTALP in exchange for partnership units of HTALP, HTALP generates the capital required for the business through its operations and by direct or indirect incurrence of indebtedness or through the issuance of its partnership units (“OP Units”).

Noncontrolling interests, stockholders’ equity and partners’ capital are the primary areas of difference between the consolidated financial statements of HTA and HTALP. Limited partnership units in HTALP are accounted for as partners’ capital in HTALP’s consolidated balance sheets and as a noncontrolling interest reflected within equity in HTA’s consolidated balance sheets. The differences between HTA’s stockholders’ equity and HTALP’s partners’ capital are due to the differences in the equity issued by HTA and HTALP, respectively.

We believe combining the Annual Reports of HTA and HTALP, including the notes to the consolidated financial statements, into this single Annual Report results in the following benefits:

•enhances stockholders’ understanding of HTA and HTALP by enabling stockholders to view the business as a whole in the same manner that management views and operates the business;

•eliminates duplicative disclosure and provides a more streamlined and readable presentation since a substantial portion of the disclosure in this Annual Report applies to both HTA and HTALP; and

•creates time and cost efficiencies through the preparation of a single combined Annual Report instead of two separate Annual Reports.

In order to highlight the material differences between HTA and HTALP, this Annual Report includes sections that separately present and discuss areas that are materially different between HTA and HTALP, including:

•the Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities in Item 5 of this Annual Report;

•the Selected Financial Data in Item 6 of this Annual Report;

•as defined by the National Association of Real Estate Investment Trusts (“NAREIT”), the Funds From Operations (“FFO”) and Normalized FFO in Item 7 of this Annual Report;

•the Controls and Procedures in Item 9A of this Annual Report;

•the consolidated financial statements in Item 15 of this Annual Report;

•certain accompanying notes to the consolidated financial statements in Item 15 of this Annual Report, including Note 8 - Debt, Note 12 - Stockholders’ Equity and Partners’ Capital, Note 14 - Per Share Data of HTA, and Note 15 - Per Unit Data of HTALP, Note 17 - Tax Treatment of Dividends of HTA, Note 18 - Selected Quarterly Financial Data of HTA and Note 19 - Selected Quarterly Financial Data of HTALP; and

•the Certifications of the Chief Executive Officer and the Chief Financial Officer included as Exhibits 31 and 32 to this Annual Report.

In the sections of this Annual Report that combine disclosure for HTA and HTALP, this Annual Report refers to actions or holdings as being actions or holdings of the Company. Although HTALP (directly or indirectly through one of its subsidiaries) is generally the entity that enters into contracts, holds assets and issues or incurs debt, management believes this presentation is appropriate for the reasons set forth above and because the business of the Company is a single integrated enterprise operated through HTALP.

HEALTHCARE TRUST OF AMERICA, INC. AND

HEALTHCARE TRUST OF AMERICA HOLDINGS, LP

TABLE OF CONTENTS

PART I

Item 1. Business

BUSINESS OVERVIEW

HTA, a Maryland corporation, and HTALP, a Delaware limited partnership, were incorporated or formed, as applicable, on April 20, 2006.

HTA is a publicly-traded REIT and is the largest dedicated owner and operator of medical office buildings (“MOBs”) in the United States (“U.S.”). We focus on owning and operating MOBs that serve the future of healthcare delivery and are located on health system campuses, near university medical centers, or in community core outpatient locations. We also focus on key markets that have attractive demographics and macro-economic trends and where we can utilize our institutional full-service operating platform to generate strong tenant and health system relationships and operating cost efficiencies. Our primary objective is to enhance the value of our real estate assets through our dedicated asset management and leasing platform, which generates consistent revenue streams and manageable expenses. As a result of our core business strategy, we seek to generate stockholder value through consistent and growing dividends, which are attainable through sustainable cash flows.

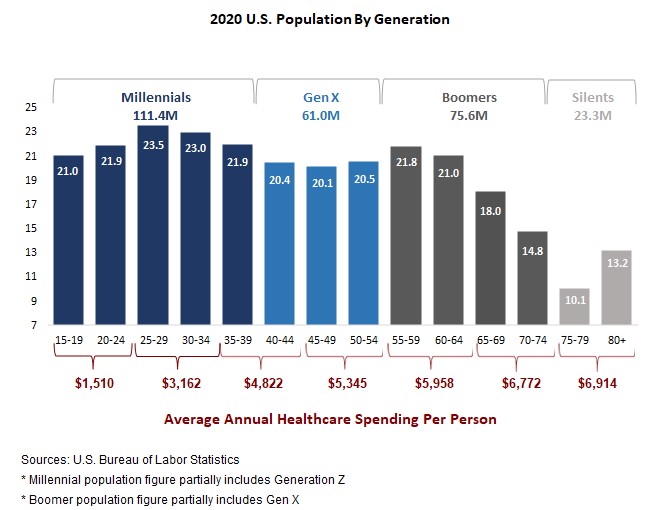

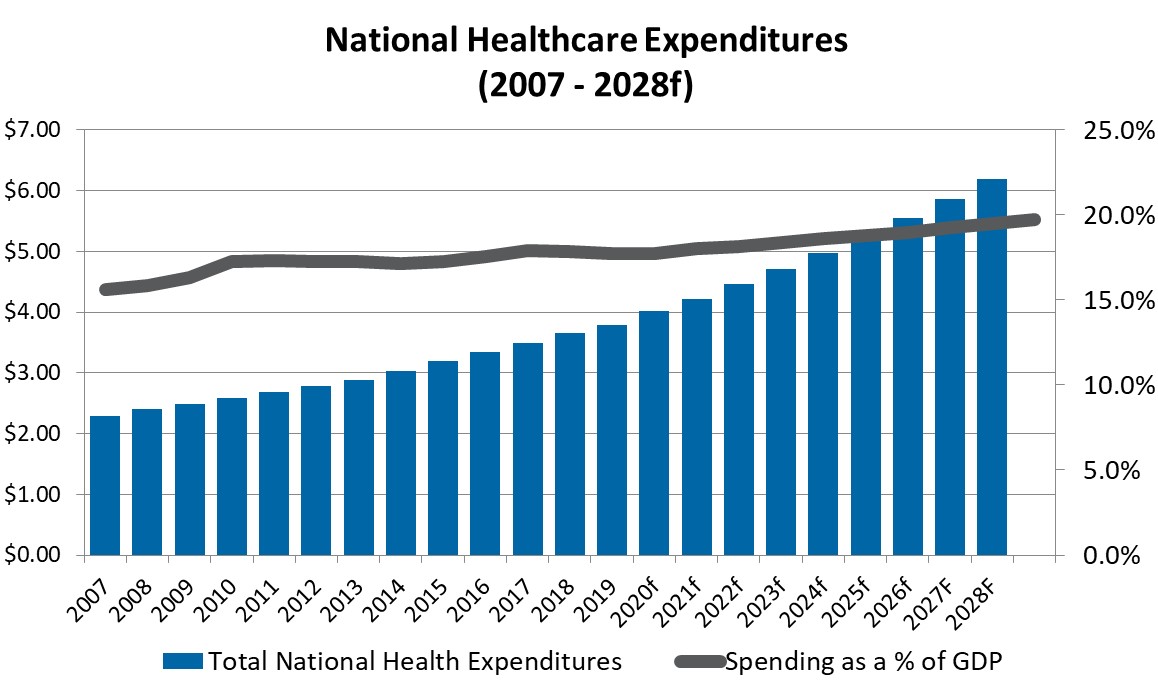

We invest in MOBs that we believe are critical to the delivery of healthcare in a changing environment. Healthcare is one of the fastest growing segments of the U.S. economy, with an expected average growth rate of approximately 6% annually through 2028. Overall U.S. spending is expected to increase by approximately 20% of gross domestic product (“GDP”) by 2028 according to the U.S. Centers for Medicare & Medicaid Services. In addition, healthcare is experiencing the fastest employment growth in the U.S., a trend that is expected to continue over the next decade. These high levels of demand are primarily driven by an aging U.S. population and the long-term impact of an increasing number of insured individuals nationwide. This increase in demand, combined with advances in less invasive medical procedures, is driving many healthcare services to lower costs and to more convenient outpatient settings that are less reliant on hospital campuses. As a result, HTA believes that well-located MOBs should provide stable cash flows with relatively low vacancy risk, resulting in consistent long-term growth.

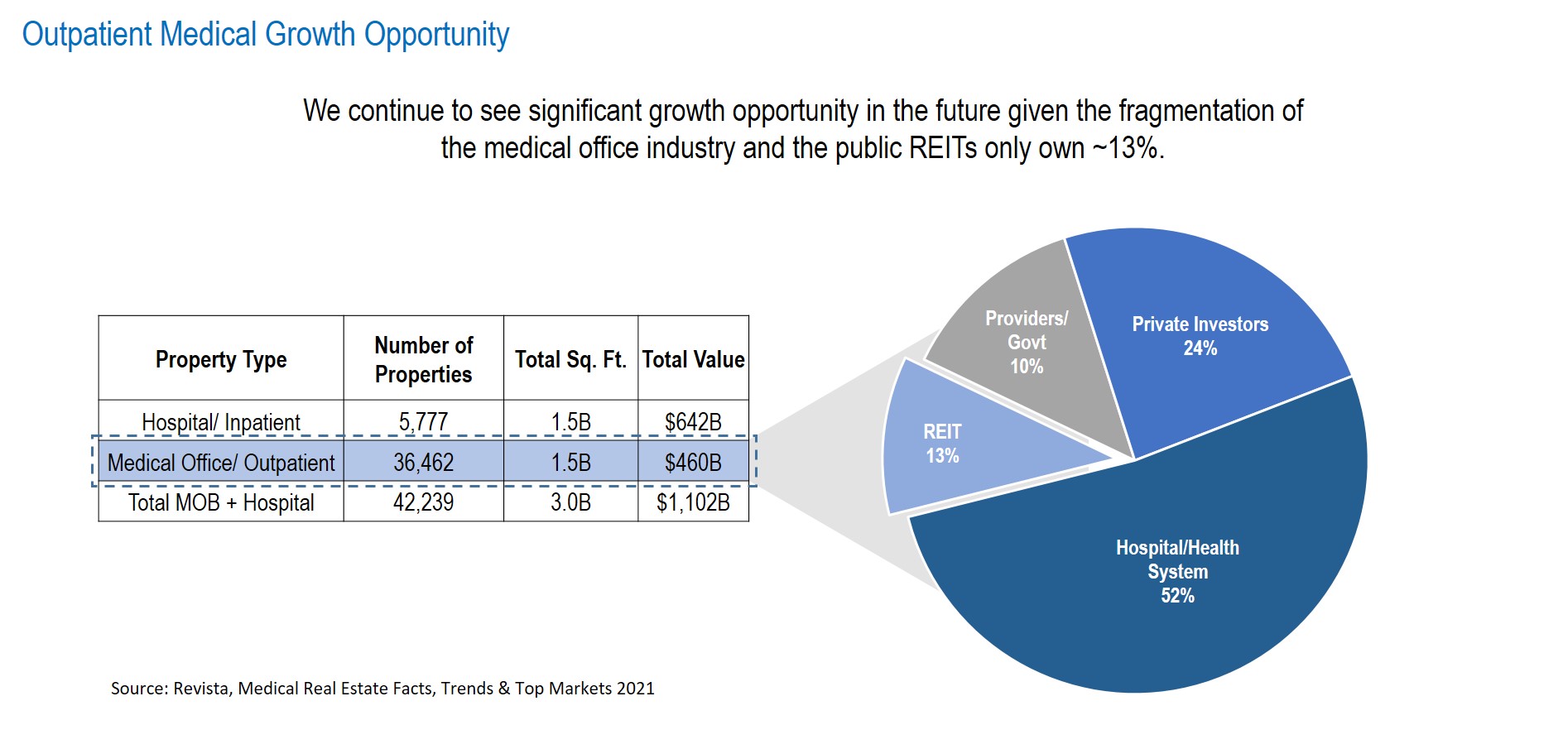

Since inception, the Company has invested $7.5 billion primarily in MOBs, development projects, land and other healthcare real estate assets that are primarily located in 20 to 25 high quality markets that possess above average economic and socioeconomic drivers. Our portfolio consists of approximately 25.4 million square feet of gross leasable area (“GLA”) throughout the U.S. As of December 31, 2020, approximately 67% of our portfolio was located on the campuses of, or adjacent to, nationally and regionally recognized healthcare systems. We believe these key locations and affiliations create significant demand from healthcare related tenants for our properties. Further, our portfolio is primarily concentrated within major U.S. metropolitan statistical areas (“MSAs”) that we believe will provide above-average economic growth and socioeconomic benefits over the coming years. As of December 31, 2020, we had approximately 1 million square feet of GLA in ten of our top 20 key markets and approximately 94% of our portfolio, based on GLA, is located in the top 75 MSAs, with Dallas, Houston, Boston, Tampa and Hartford/New Haven being our largest markets by investment.

Our principal executive office is located at 16435 North Scottsdale Road, Suite 320, Scottsdale, AZ 85254, and our telephone number is (480) 998-3478. We maintain a website at www.htareit.com where additional information about us can be accessed. The contents of our website are not incorporated by reference in, or otherwise a part of this filing. We make our periodic and current reports, as well as any amendments to such reports, available free of charge at www.htareit.com as soon as reasonably practicable after such materials are electronically filed with the SEC. These reports are also available in hard copy to any stockholder upon request by contacting our investor relations staff at the number above or via email at info@htareit.com.

HIGHLIGHTS

Earnings

•For the year ended December 31, 2020, total revenue increased 6.8%, or $46.9 million, to $739.0 million, compared to $692.0 million for the year ended December 31, 2019.

•For the year ended December 31, 2020, net income increased 73.8%, or $22.7 million, to $53.5 million, compared to $30.8 million for the year ended December 31, 2019.

•For the year ended December 31, 2020, net income attributable to common stockholders was $0.24 per diluted share, or $52.6 million, compared to $0.14 per diluted share, or $30.2 million, for the year ended December 31, 2019.

•For the year ended December 31, 2020, HTA’s FFO, as defined by NAREIT, was $344.7 million, or $1.56 per diluted share, compared to $1.53 per diluted share, or $319.7 million, for the year ended December 31, 2019.

•For the year ended December 31, 2020, HTALP’s FFO, as defined by NAREIT, was $345.6 million, or $1.56 per diluted OP Unit, compared to $1.53 per diluted OP Unit, or $320.3 million, for the year ended December 31, 2019.

•For the year ended December 31, 2020, HTA’s and HTALP’s Normalized FFO was a record $1.71 per diluted share and OP Unit, or $379.3 million, compared to $1.64 per diluted share and OP Unit, or $344.3 million, for the year ended December 31, 2019, an increase of 4.3%.

•For additional information on FFO and Normalized FFO, see “FFO and Normalized FFO” below, which includes a reconciliation to net income attributable to common stockholders/unitholders and an explanation of why we present this financial measure which is not a financial measure based on generally accepted accounting principles (“GAAP”).

•For the year ended December 31, 2020, Net Operating Income (“NOI”) increased 6.6%, or $31.5 million, to $512.1 million, compared to $480.6 million for the year ended December 31, 2019.

•For the year ended December 31, 2020, Same-Property Cash NOI increased 1.6%, or $7.2 million, to $457.1 million, compared to $449.9 million for the year ended December 31, 2019.

•For additional information on NOI and Same-Property Cash NOI, see “NOI, Cash NOI and Same-Property Cash NOI” below, which includes a reconciliation from net income and an explanation of why we present these non-GAAP financial measures.

Portfolio Performance

•For the year ended December 31, 2020, our leased rate (which includes leases which have been executed, but which have not yet commenced) was 89.8% by GLA, and our occupancy rate was 89.1% by GLA. The leased rate for our Same-Property portfolio was 90.5%.

•During the year ended December 31, 2020, we executed 3.9 million square feet of GLA of new and renewal leases, or 15.2%, of the total GLA of our portfolio. Re-leasing spreads increased to 4.7% and tenant retention continued to be strong at 87% for the Same-Property portfolio as of December 31, 2020. Tenant retention is defined as the sum of the total leased GLA of tenants that renewed a lease during the period over the total GLA of leases that renewed or expired during the period.

•For the year ended December 31, 2020, HTA closed on approximately $191.7 million of MOB investments totaling approximately 600,000 square feet of GLA, with expected year-one contractual yields of approximately 6.0%. These properties were approximately 94% leased as of closing, and are located within HTA's key markets.

•During 2020, HTA had the following development and redevelopment projects in place:

◦Completed: During 2020, HTA completed its initial ground-up development in Raleigh, North Carolina. Total construction costs on this development were approximately $44 million and totaled approximately 127,000 square feet of GLA and is currently 77% leased.

◦Developments: During 2020, HTA continued to develop three new on-campus MOBs located in the key markets of Miami, Florida; Bakersfield, California; and Dallas, Texas. In total, HTA has development projects in process of approximately $110 million and totaling approximately 244,000 square feet of GLA. They are expected to be more than 79% pre-leased upon completion.