UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________

Form 8-K

______________________

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (Date of earliest event Reported): December 31, 2019

Proteon Therapeutics, Inc.

(Exact Name of Registrant as Specified in Charter)

| Delaware | 001-36694 | 20-4580525 |

| (State or Other Jurisdiction of Incorporation) |

(Commission File Number) | (I.R.S. Employer Identification Number) |

| 200 West Street, Waltham, MA 02451 |

| (Address of Principal Executive Offices) (Zip Code) |

(781) 890-0102

(Registrant's telephone number, including area code)

N/A

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ||

| x | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) | |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) | |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) | |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) | |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, $0.001 par value per share | PRTO | Nasdaq Capital Market |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (17 CFR §230.405) or Rule 12b-2 of the Securities Exchange Act of 1934 (17 CFR §240.12b-2).

Emerging growth company x

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Introductory Comment

Throughout this Current Report on Form 8-K, the terms “we,” “us,” “our”, “Company” and “Proteon” refer to Proteon Therapeutics, Inc., a Delaware corporation.

Item 8.01. Other Events.

On December 19, 2019, Proteon filed a registration statement on Form S-4, File No. 333-234549 (the “Registration Statement”), containing a definitive proxy statement/prospectus/information statement (the “Definitive Proxy Statement”) with the Securities and Exchange Commission (the “SEC”) with respect to the special meeting of Proteon’s stockholders scheduled to be held on January 9, 2020 in order to, among other things, obtain the stockholder approvals necessary to complete the planned merger of REM 1 Acquisition, Inc., a wholly owned subsidiary of Proteon (“Merger Sub”) with and into ArTara Therapeutics, Inc. (“ArTara”), under that certain Agreement and Plan of Merger and Reorganization dated as of September 23, 2019, as amended (the “Merger Agreement”), pursuant to which, among other matters, and subject to the satisfaction or waiver of the conditions set forth in the Merger Agreement, Merger Sub will merge with and into ArTara, with ArTara surviving the Merger as a wholly owned subsidiary of Proteon (the “Merger”).

With this filing, Proteon is hereby supplementing its disclosure in the Definitive Proxy Statement in connection with litigation brought by its stockholders, which is described below. Nothing in this Current Report on Form 8-K shall be deemed an admission of the legal necessity or materiality under applicable laws of any of the disclosures set forth herein. Proteon and the other named defendants believe the claims asserted in the litigation to be without merit, intend to defend against them vigorously and deny any wrongdoing alleged in the litigation.

Stockholder Litigation

As previously disclosed in the Definitive Proxy Statement, between November 15 and December 2, 2019, three putative lawsuits (captioned Patrick Plumley v. Proteon Therapeutics, Inc., et al., Case No. 1:19-cv-02143-UNA (D. Del. filed November 15, 2019), Jeffrey Teow v. Proteon Therapeutics, Inc., et al., Case No. 1:19-cv-06745 (E.D.N.Y. filed November 30, 2019), and Neil Lanteigne v. Proteon Therapeutics, et al., Case No. 1:19-cv-12436 (D. Mass. filed on December 2, 2019)) were filed in federal court against Proteon and the individual members of the Proteon board of directors (the “Proteon Board”), and in the case of the Plumley complaint and the Lanteigne complaint, also against ArTara.

On December 23, 2019, one additional lawsuit entitled Stephen Wagner v. Proteon Therapeutics, Inc., et al., Case No. 1:19-cv-02343-UNA, was filed in the United States District Court for the District of Delaware against Proteon, ArTara, Merger Sub and the individual members of the Proteon Board. The Wagner complaint also alleges that the preliminary registration statement filed by Proteon on November 7, 2019 with the SEC, as amended, in connection with the proposed Merger omits material information with respect to the transactions contemplated by the Merger Agreement, rending it false and misleading in violation of Sections 14(a) (and Rule 14a-9 promulgated thereunder) and 20(a) of the Exchange Act. The plaintiff seeks, among other things, injunctive relief, rescission, declaratory relief and unspecified monetary damages.

While Proteon believes that the disclosures set forth in the Definitive Proxy Statement comply fully with all applicable law and denies the allegations in the pending actions described above, in order to moot plaintiffs’ disclosure claims, avoid nuisance and possible expense and business delays, and provide additional information to its stockholders, Proteon has determined voluntarily to supplement certain disclosures in the Definitive Proxy Statement related to plaintiffs’ claims with the supplemental disclosures set forth below (the “Supplemental Disclosures”). These Supplemental Disclosures should be read in conjunction with the rest of the Definitive Proxy Statement, which is available on the Internet site maintained by the SEC at http://www.sec.gov, and which we urge you to read in its entirety. Nothing in the Supplemental Disclosures shall be deemed an admission of the legal merit, necessity or materiality under applicable laws of any of the disclosures set forth herein. To the contrary, the Company and the other named defendants specifically deny all allegations in the various litigation matters that any additional disclosure was or is required or material. To the extent that the information set forth herein differs from or updates information contained in the Definitive Proxy Statement, the information set forth herein shall supersede or supplement the information in the Definitive Proxy Statement. References to sections and subsections herein are references to the corresponding sections or subsections in the Definitive Proxy Statement, all page references are to pages in the Definitive Proxy Statement, and terms used herein, unless otherwise defined, have the meanings set forth in the Definitive Proxy Statement.

Supplemental Disclosures to Proxy Statement

1. The following language is added at the end of the third full paragraph on page 98:

In Proteon’s meetings with Company G’s financial advisors in early June, Company G’s financial advisors indicated that Company G was interested in a potential strategic transaction with Proteon as Company G was currently a wholly-owned subsidiary of another public company and was considering spinning out. Company G’s financial advisors indicated that Proteon’s shareholders would be expected to receive approximately 10 – 20% in the combined company, that Company G would need Proteon to provide the full management team for the combined company and would need Proteon to raise additional funding prior to or in connection with the closing of such a potential transaction.

2. The second to last sentence of the last full paragraph on page 98 is hereby amended and restated as follows (changes shown in underline/strikethrough):

At the end of the meeting, it was decided that the financial

advisors to Company G would send additional materials to Proteon’s management and that both sides would think about

ways to address some of the issues identified during the discussion and get back in touch in the coming weeks consider

how to address personnel retention issues for the combined company’s management team and Company G’s need for funding

prior to or in connection with closing a potential transaction.

3. The following language is added at the end of the third full paragraph on page 99:

Proteon also met with members of the Company E management team in July to discuss Company E’s preliminary oral proposal for a potential strategic transaction with Proteon. In this meeting Company E’s management team explained that Proteon’s shareholders would receive well under 50% of the ownership in the combined company and that Company E would require a capital raise and additional management team members prior to the completion of any proposed strategic transaction. Further, in July, Proteon also met with Company F’s chief executive officer. In this meeting, Company F’s chief executive officer stated that Company F was considering an initial public offering or a potential reverse merger with a company like Proteon. With respect to a potential reverse merger with Proteon, Company F’s chief executive officer explained that Proteon’s shareholders would own approximately 10% of the combined company and that Company F would need to raise approximately $60 million prior to or in connection with any such reverse merger transaction.

4. The following language is added immediately following the first full sentence on page 101:

Furthermore, the revised proposal clarified that the $20 million investment was based on a $200 million valuation for the combined company, but that the investment would include a full ratchet provision whereby the new investors would review the value of the combined company, based on trading prices, at closing and 45 days after closing and would invest at the lower of the $200 million valuation or the combined company trading value at closing and 45 days after closing.

5. The last sentence of the second full paragraph on page 101 is hereby amended and restated as follows (changes shown in underline/strikethrough):

Company H was also believed to have a strong, recognizable management team but had an inferior financing term sheet to support Company H’s merger proposal, including, without limitation, the full ratchet provision included in Company H’s proposed financing term sheet.

6. The second paragraph under the heading “Discounted Cash Flow Analysis” beginning on page 123 is hereby amended and restated as follows (changes shown in underline/strikethrough and all tables are added):

Wainwright applied a 23% tax rate to the projected cash flows contained in the ArTara financial projections (described above in the section titled "Certain Unaudited ArTara Financial Projections") to calculate ArTara's estimated net operating profit after taxes, or NOPAT, for each period covered by the projections to estimate the Present Value of Artara's Free Cash Flows used in both the Perpetuity and Terminal Value Discounted Cash Flow calculations. The table below shows the EBIT projection for each period from the projected cash flows contained in the ArTara financial projections (described above in the section titled “Certain Unaudited ArTara Financial Projections”) and Wainwright’s calculation of NOPAT and Free Cash Flows for each period (dollars in millions):

| Year | FY2020 | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 | FY2026 | FY2027 | FY2028 | FY2029 | FY2030 | FY2031 | FY2032 | FY2033 | FY2034 | FY2035 | ||||||||||||||||||||||||||||||||||||||||||||||||

| EBIT(1) | $ | (20.6 | ) | $ | (11.5 | ) | $ | (34.0 | ) | $ | (19.7 | ) | $ | (35.3 | ) | $ | (25.3 | ) | $ | 27.4 | $ | 95.5 | $ | 178.5 | $ | 250.6 | $ | 309.5 | $ | 374.6 | $ | 465.4 | $ | 550.0 | $ | 611.5 | $ | 693.2 | ||||||||||||||||||||||||||

| Less Tax 23.0% | -- | -- | -- | -- | -- | -- | $ | 6.3 | $ | 22.0 | $ | 41.0 | $ | 57.6 | $ | 71.2 | $ | 86.2 | $ | 107.0 | $ | 126.5 | $ | 140.6 | $ | 159.4 | ||||||||||||||||||||||||||||||||||||||

| NOPAT | $ | (20.6 | ) | $ | (11.5 | ) | $ | (34.0 | ) | $ | (19.7 | ) | $ | (35.3 | ) | $ | (25.3 | ) | $ | 21.1 | $ | 73.5 | $ | 137.4 | $ | 193.0 | $ | 238.3 | $ | 288.5 | $ | 358.3 | $ | 423.5 | $ | 470.9 | $ | 533.8 | ||||||||||||||||||||||||||

| Plus D&A | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | ||||||||||||||||||||||||||||||||||||||||||||||||

| Less CAPEX | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | ||||||||||||||||||||||||||||||||||||||||||||||||

| +/- Change in NWC | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | -- | ||||||||||||||||||||||||||||||||||||||||||||||||

| FCF | $ | (20.6 | ) | $ | (11.5 | ) | $ | (34.0 | ) | $ | (19.7 | ) | $ | (35.3 | ) | $ | (25.3 | ) | $ | 21.1 | $ | 73.5 | $ | 137.4 | $ | 193.0 | $ | 238.3 | $ | 288.5 | $ | 358.3 | $ | 423.5 | $ | 470.9 | $ | 533.8 | ||||||||||||||||||||||||||

| PV of Unlevered FCF(2) | $ | (17.4 | ) | $ | (7.8 | ) | $ | (18.4 | ) | $ | (8.5 | ) | $ | (12.2 | ) | $ | (7.0 | ) | $ | 4.7 | $ | 13.0 | $ | 19.5 | $ | 21.9 | $ | 21.6 | $ | 23.4 | $ | 26.0 | $ | 24.6 | $ | 21.8 | $ | 19.8 | ||||||||||||||||||||||||||

| (1) | From ArTara projections. |

| (2) | 25% discount rate base case. |

Present Value of Unlevered Free Cash Flow $125.0

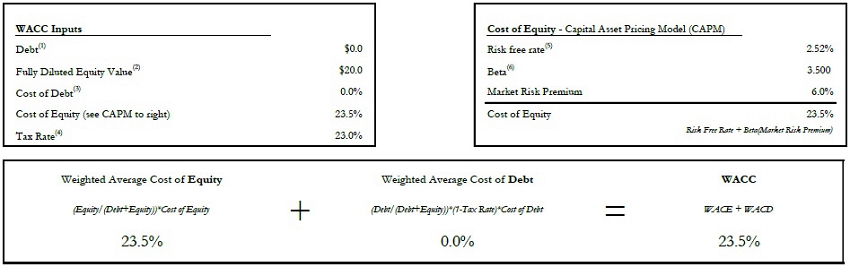

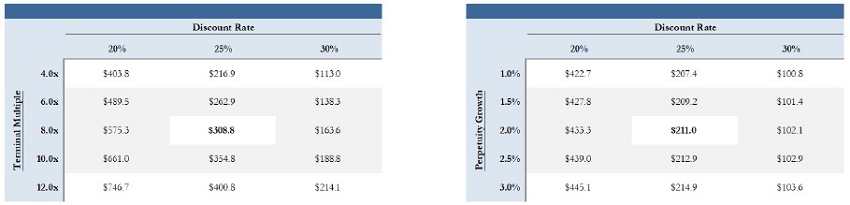

Wainwright estimated the present value of ArTara’s Terminal Value using an assumed terminal valuation range of 4x and 12x EBIT which was added to the estimated Present Value of ArTara’s Free Cash Flows to calculate the Terminal Value Discounted Cash Flow. Wainwright determined the range of 4x to 12x based on its analysis of EBIT multiples implied from acquisition transactions in the specialty pharmaceutical industry that Wainwright believe were comparable to the Merger. Wainwright used an assumed perpetuity growth rate of between 1% and 3% to estimate the Perpetuity Growth Free cash flow, the Present Value of which was added to the Present Value of ArTara’s Free Cash Flows to calculate the Perpetuity Growth Discounted Cash Flow. Wainwright chose 1% as the bottom of the growth range which equated to nominal growth and 3% as the top of the growth range which was intended to reflect generally accepted estimates of future population growth. In each case, Wainwright applied a 20.0% to 30.0% discount rate based on a WACC analysis. Wainwright’s WACC calculation is set forth in the table below:

| (1) | ArTara does not currently have any debt outstanding |

| (2) | Based on ArTara’s pre-money valuation of $20.0M |

| (3) | ArTara does not currently have any debt outstanding |

| (4) | Illustrative corporate tax rate |

| (5) | Average yield on a 10-year U.S. Treasury bill over the last 10 years |

| (6) | Hypothetical beta based on ArTara being a private biotechnology company with a lead asset currently in phase 2 studies (TARA-002) |

Based on these inputs, Wainwright calculated an enterprise value range between $214.1 million and $403.8 million using the terminal multiple methodology and between $103.6 million and $422.7 million using the perpetuity growth methodology. The table below shows the calculations performed by Wainwright (dollars in millions):

$308.8 million and $211.0 million reflect the midpoint of the estimated discounted cash flow ranges using the terminal multiple and perpetuity growth rate methodologies, respectively, compared to the $141.7 million minimum valuation for the combined company that would result in the 10.8% of the combined company to be owned by existing Proteon stockholders having an implied valuation of at least $12.1 million.

Additional Information about the Merger and Where to Find It

In connection with the proposed Merger, Proteon filed the Registration Statement, including the Definitive Proxy Statement. The Registration Statement was declared effective on December 19, 2019. The Definitive Proxy Statement was first mailed on December 19, 2019 to the Company’s stockholders of record as of the close of business on December 3, 2019. STOCKHOLDERS OF PROTEON ARE URGED TO READ THE REGISTRATION STATEMENT, THE DEFINITIVE PROXY STATEMENT (INCLUDING ANY AMENDMENTS OR SUPPLEMENTS THERETO) AND OTHER DOCUMENTS FILED WITH THE SEC CAREFULLY IN THEIR ENTIRETY, AS THEY CONTAIN IMPORTANT INFORMATION THAT STOCKHOLDERS OF PROTEON SHOULD CONSIDER BEFORE MAKING A DECISION ABOUT THE PROPOSED MERGER AND RELATED MATTERS. The Registration Statement, including the Definitive Proxy Statement, and any amendments or supplements thereto (when such amendments or supplements become available) and other documents filed by Proteon with the SEC may be obtained, without charge, from the SEC’s website at www.sec.gov or, without charge, by directing a written request to: Proteon Therapeutics, Inc., 200 West St. Waltham, MA 02451, Attention: Investor Relations.

This communication does not constitute an offer to sell, or the solicitation of an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No public offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended.

Participants in the Solicitation

Proteon, ArTara and their respective executive officers, directors, certain members of management and certain employees may be deemed, under the SEC rules, to be participants in the solicitation of proxies from Proteon stockholders with respect to the matters relating to the proposed Merger. Information regarding the special interests of Proteon’s directors and executive officers in the proposed Merger is included in the Definitive Proxy Statement. Additional information regarding Proteon’s executive officers and directors is available in Proteon’s proxy statement on Schedule 14A for its 2018 annual meeting of stockholders, filed with the SEC on April 26, 2018 and Proteon’s Annual Report on Form 10-K and the amendment thereto for the year ended December 31, 2018. These documents are available free of charge at the SEC’s website at www.sec.gov or by going to Proteon’s investor and media page on its corporate website at www.proteontherapeutics.com.

Forward-Looking Statements

This report contains certain statements regarding matters that are not historical facts and that are forward-looking statements within the meaning of Section 21E of the Securities and Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, known as the PSLRA. These include statements regarding management’s intentions, plans, beliefs, expectations or forecasts for the future, and, therefore, stockholders are cautioned not to place undue reliance on them. No forward-looking statement can be guaranteed, and actual results may differ materially from those projected. We use words such as “anticipates,” “believes,” “plans,” “expects,” “projects,” “future,” “intends,” “may,” “will,” “should,” “could,” “estimates,” “predicts,” “potential,” “continue,” “guidance,” and similar expressions to identify these forward-looking statements that are intended to be covered by the safe-harbor provisions of the PSLRA. Such forward-looking statements are based on management expectations and involve risks and uncertainties; consequently, actual results may differ materially from those expressed or implied in the forward-looking statements due to a number of factors, including, but not limited to, risks relating to the completion of the proposed Merger, including the need for Proteon’s and ArTara’s stockholder approval and the satisfaction of certain closing conditions; the anticipated financing to be completed concurrently with the closing of the proposed Merger; the cash balance of the combined company following the closing of the proposed Merger and the financing, and expectations with respect thereto; the potential benefits of the proposed Merger; the business and prospects of the combined company following the proposed Merger; and the ability of Proteon to remain listed on the Nasdaq Global Market. Risks and uncertainties that may cause actual results to differ materially from those expressed or implied in any forward-looking statement include, but are not limited to: the closing of the proposed Merger; ArTara’s plans to develop and commercialize its product candidates, including TARA-002, and Choline Chloride; the timing, costs and outcomes of ArTara’s planned clinical trials; expectations regarding potential market size; the timing of the availability of data from ArTara’s clinical trials; the timing of any planned investigational new drug application or new drug application; ArTara’s plans to research, develop and commercialize its current and future product candidates; ArTara’s ability to successfully collaborate with existing collaborators or enter into new collaborations, and to fulfill its obligations under any such collaboration agreements; the clinical utility, potential benefits and market acceptance of ArTara’s product candidates; ArTara’s commercialization, marketing and manufacturing capabilities and strategy; ArTara’s ability to identify additional products or product candidates with significant commercial potential; developments and projections relating to ArTara’s competitors and industry; the impact of government laws and regulations; ArTara’s ability to protect its intellectual property position; and ArTara’s estimates regarding future revenue, expenses, capital requirements, and the need for and timing of additional financing following the proposed Merger. These risks, as well as other risks associated with the proposed Merger, are more fully discussed in the Definitive Proxy Statement. Additional risks and uncertainties are identified and discussed in the “Risk Factors” section of Proteon’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and other documents filed from time to time with the SEC. Forward-looking statements included in this report are based on information available to Proteon and ArTara as of the date of this report. Neither Proteon nor ArTara undertakes any obligation to update such forward-looking statements to reflect events or circumstances after the date of this report.

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| Proteon Therapeutics, Inc. | |||

| Date: December 31, 2019 | By: | /s/ Timothy P. Noyes | |

| Timothy P. Noyes | |||

| President & Chief Executive Officer | |||