UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21897

Manager Directed Portfolios

(Exact name of registrant as specified in charter)

(Exact name of registrant as specified in charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

(Address of principal executive offices) (Zip code)

Douglas J. Neilson, President

Manager Directed Portfolios

c/o U.S. Bancorp Fund Services, LLC

777 East Wisconsin Avenue, 5th Floor

Milwaukee, WI 53202

(Name and address of agent for service)

(Name and address of agent for service)

(414) 287-3101

Registrant's telephone number, including area code

Date of fiscal year end: March 31, 2019

Date of reporting period: March 31, 2019

Item 1. Reports to Stockholders.

Pemberwick Fund

Annual Report

March 31, 2019

Pemberwick Fund

Table of Contents

|

Letter to Shareholders/Commentary

|

3

|

|

|

Sector Allocation of Portfolio Assets

|

6

|

|

|

Schedule of Investments

|

7

|

|

|

Statement of Assets and Liabilities

|

23

|

|

|

Statement of Operations

|

24

|

|

|

Statements of Changes in Net Assets

|

25

|

|

|

Financial Highlights

|

26

|

|

|

Notes to the Financial Statements

|

27

|

|

|

Report of Independent Registered Public Accounting Firm

|

36

|

|

|

Expense Example

|

37

|

|

|

Notice to Shareholders

|

39

|

|

|

Trustees and Officers

|

40

|

|

|

Approval of the Investment Advisory Agreement and Sub-Advisory Agreement

|

43

|

|

|

Privacy Notice

|

47

|

Pemberwick Fund (Unaudited)

We are pleased to present the Pemberwick Fund annual report covering the year from April 1, 2018 through March 31, 2019.

Portfolio performance information, market commentary and our outlook for the period ended March 31, 2019 follows. We encourage you to carefully review the enclosed information to stay informed.

PORTFOLIO PERFORMANCE AND MARKET REVIEW:

For the year ended March 31, 2019 Pemberwick Fund (“Pemberwick”) generated a periodic total investment return of 2.53% net of

expenses. The Portfolio’s primary benchmark, the Bloomberg Barclays 1-3 Year US Government/Credit Index returned 3.03% during the same period (the benchmark index does not include expenses). Pemberwick outperformed the benchmark by 0.67% during the

period from April 1, 2018 to September 30, 2018. Pemberwick underperformed the benchmark by 1.81% during the period from October 1, 2018 to December 31, 2018. Pemberwick then outperformed the benchmark by 0.64% during the period from January 1,

2019 to March 31, 2019. During the period of underperformance vs. the benchmark (from October 1, 2018 to December 31, 2018), 3-month-Libor (“3ML”) increased from 2.40% on September 30, 2018 to 2.81% on December 31, 2018. This increase in 3ML caused

spreads on investment grade floating rate bonds to widen significantly thus resulting in price declines for a majority of Pemberwick’s holdings during that period. The benchmark index holds approximately 72% Treasuries and Agencies and as such was

not as adversely impacted by the increase in 3ML during that period. Since its inception on February 1, 2010 Pemberwick has generated an annual return net of expenses of 1.30% vs. Pemberwick’s benchmark return of 1.30% for the same period (the

benchmark index does not include expenses). Pemberwick generated an annual return net of expenses of 2.53% for the year ended March 31, 2019. Pemberwick’s annual return for the 5-year period from April 1, 2014 to March 31, 2019 was 1.20% net of

expenses, vs. Pemberwick’s benchmark annual return of 1.22% (the benchmark index does not include expenses).

Performance data quoted represents past performance; past performance does not guarantee future results.

The investment return and principal value of an investment will change so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance

quoted. Performance data current to the most recent month end may be obtained by calling 1-888-893-4491. The gross expense ratio of the fund was 0.43% as of the 7/31/18 prospectus. Pemberwick Fund’s advisor currently voluntarily waives 0.10% of its

0.25% fee resulting in an expense cap of 0.33% as of 7/31/18. The voluntary waiver does not have an end date and will continue until Pemberwick notifies the Fund of a change in its voluntary waiver or its discontinuation. Please see page 26 for

the gross and net expense ratios as of March 31, 2019.

During the year ended March 31, 2019 Pemberwick primarily continued its strategy of building a portfolio of investment grade

floating rate bonds with laddered maturities during the period from March 31, 2018 through September 30, 2018. However, since then Pemberwick has remained on the sidelines with regards to adding investment grade floating rate bonds as 3ML rose

substantially during the last three months of 2018. 3ML has since retreated towards September 30, 2018 levels, causing spreads of investment grade floating rate bonds to tighten since the end of 2018. As such, for the three months ended March 31,

2019, Pemberwick generated a return of 1.85% net of expenses vs. Pemberwick’s benchmark return of 1.21% for the same period (the benchmark index does not include expenses). We are pleased with Pemberwick’s performance for the year ended March 31,

2019 given the substantial increase in 3ML and associated price volatility during the fourth quarter of 2018 and will continue to seek opportunities to increase the fund’s positions in floating rate notes as we generally expect short term rates to

gradually increase over time.

3

Pemberwick Fund

PORTFOLIO POSITIONING:

As of March 31, 2019, Pemberwick Fund continues to be invested primarily in investment grade floating rate bonds issued by

financial institutions with assets greater than $200 billion (82% of Pemberwick’s net assets, with a weighted average duration of 2.83 years) and a small percentage of fixed rate bonds (3% of Pemberwick’s net assets, with a weighted average

duration of 1.90 years) and securities issued by the US Treasury and Agencies (12% of Pemberwick’s net assets, with a weighted average duration of 1.61 years). In addition, as of March 31, 2019 Pemberwick had approximately 3% of its assets invested

in short-term securities with maturities of less than 7 days. Pemberwick’s net assets have increased by approximately 30% during the year ended March 31, 2019: net assets have increased from approximately $280.3 million as of March 31, 2018 to

approximately $365.3 million as of March 31, 2019. Current net assets are $371.5 million as of April 30, 2019.

This letter is intended to assist shareholders in understanding how Pemberwick performed during the year ended March 31, 2019

and includes the views of the investment advisor at the time of this writing. Of course, these views may change and do not guarantee the future performance of Pemberwick or the markets. Portfolio composition is subject to change. The current and

future portfolio holdings of Pemberwick are subject to investment risk.

Pemberwick Investment Advisors, LLC

Must be preceded or accompanied by a prospectus.

Mutual fund investing involves risk. Principal loss is possible. Fixed-income securities are or may be

subject to interest rate, credit, liquidity, prepayment and extension risks. By concentrating its assets in the banking industry, the Fund is subject to the risk that economic, business, political or other conditions that have a negative effect on

the banking industry will negatively impact the Fund to a greater extent than if the Fund’s assets were diversified across different industries or sectors. The municipal market is volatile and can be significantly affected by adverse tax,

legislative or political changes and the financial condition of the issuers of municipal securities.

Bloomberg Barclays 1-3

Year US Government/Credit Total Return Index Value Unhedged – The Bloomberg Barclays 1-3 Year US Government/Credit Bond Index is a broad-based benchmark that measures the non-securitized component of the US Aggregate Index. It

includes investment grade, US dollar-denominated, fixed-rate Treasuries, government-related and corporate securities. It is not possible to invest in an index.

ICE LIBOR USD 3 Month –

London – Interbank Offered Rate – ICE Benchmark Administration Fixing for US Dollar. The fixing is conducted each day at 11am & released at 11.45am (London time). The rate is an average derived from the quotations provided by the banks

determined by the ICE Benchmark Administration.

Duration (Workout Date in

Years) – The number of years from today to the workout of the instrument. The workout of the instrument is the call date (if applicable) or the maturity date. For mortgage backed instruments the weighted average life is used instead

of the maturity.

Investment grade –

issuer credit ratings are those that are above BBB- or Baa for S&P or Moody’s respectively.

The Pemberwick Fund is distributed by Quasar Distributors, LLC

4

Pemberwick Fund

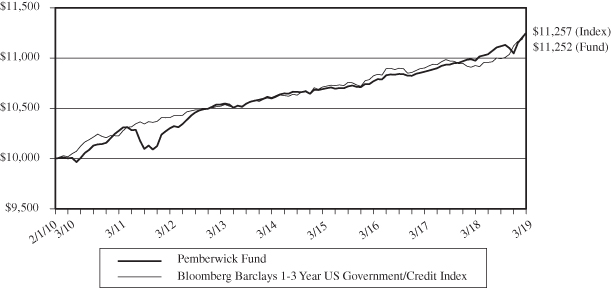

Comparison of the Change in Value of a Hypothetical $10,000 Investment

in the Pemberwick Fund and

Bloomberg Barclays 1-3 Year US Government/Credit Index

(Unaudited)

|

Average Annual Return

|

Since Inception

|

|||

|

Periods Ended March 31, 2019:

|

1 Year

|

3 Year

|

5 Year

|

(2/1/2010)

|

|

Pemberwick Fund (No Load)

|

2.53%

|

1.47%

|

1.20%

|

1.30%

|

|

Bloomberg Barclays 1-3 Year

|

||||

|

US Government/Credit Index

|

3.03%

|

1.32%

|

1.22%

|

1.30%

|

Total Annual Fund Operating Expenses as of 7/31/2018 Prospectus: 0.43%

Performance data quoted represents past performance; past performance does not guarantee future results.

The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance

quoted. Performance data current to the most recent month end may be obtained by calling 1-888-893-4491.

This chart illustrates the performance of a hypothetical $10,000 investment made in the Fund on February 1, 2010, the Fund’s

inception date. Returns reflect the reinvestment of income and capital gain distributions. The performance data shown reflects a voluntary waiver made by the Adviser. In the absence of fee waivers, returns would be reduced. The performance data

and graph do not reflect the deduction of taxes that a shareholder may pay on dividends, capital gain distributions, or redemption of Fund shares. This chart does not imply any future performance.

The Bloomberg Barclays 1-3 Year US Government/Credit Index is an unmanaged market index and should not be considered

indicative of any Pemberwick investment. One cannot invest directly in an index.

5

Pemberwick Fund

|

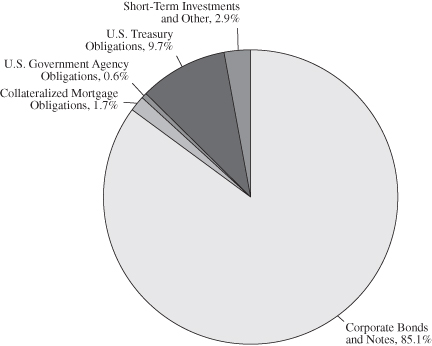

SECTOR ALLOCATION OF PORTFOLIO ASSETS

|

|

at March 31, 2019 (Unaudited)

|

Percentages represent market value as a percentage of net assets.

6

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS

|

|

at March 31, 2019

|

|

Par

|

||||||||

|

CORPORATE BONDS AND NOTES – 85.1%

|

Value

|

Value

|

||||||

|

Basic Materials – 0.0%

|

||||||||

|

Praxair, Inc.

|

||||||||

|

2.250%, 09/24/2020

|

$

|

30,000

|

$

|

29,866

|

||||

|

Communications – 1.5%

|

||||||||

|

AT&T, Inc

|

||||||||

|

3.737% (3 Month LIBOR USD + 0.950%), 07/15/2021 (a)

|

5,000,000

|

5,060,648

|

||||||

|

Cisco Systems, Inc.

|

||||||||

|

2.200%, 02/28/2021

|

100,000

|

99,345

|

||||||

|

3.000%, 06/15/2022

|

105,000

|

106,603

|

||||||

|

Comcast Corp.

|

||||||||

|

1.625%, 01/15/2022

|

60,000

|

58,365

|

||||||

|

2.850%, 01/15/2023

|

100,000

|

100,384

|

||||||

|

NBCUniversal Media LLC

|

||||||||

|

5.150%, 04/30/2020

|

100,000

|

102,538

|

||||||

|

The Walt Disney Co.

|

||||||||

|

1.800%, 06/05/2020

|

30,000

|

29,728

|

||||||

|

2.150%, 09/17/2020

|

70,000

|

69,644

|

||||||

|

5,627,255

|

||||||||

|

Consumer, Cyclical – 0.8%

|

||||||||

|

American Honda Finance Corp.

|

||||||||

|

2.600%, 11/16/2022

|

50,000

|

49,900

|

||||||

|

3.625%, 10/10/2023

|

200,000

|

207,312

|

||||||

|

3.550%, 01/12/2024

|

50,000

|

51,547

|

||||||

|

General Motors Financial Co., Inc.

|

||||||||

|

3.911% (3 Month LIBOR USD + 1.310%), 06/30/2022 (a)

|

2,000,000

|

1,985,846

|

||||||

|

PACCAR Financial Corp.

|

||||||||

|

1.300%, 05/10/2019

|

12,000

|

11,983

|

||||||

|

3.100%, 05/10/2021

|

62,000

|

62,515

|

||||||

|

3.400%, 08/09/2023

|

60,000

|

60,824

|

||||||

|

The Home Depot, Inc.

|

||||||||

|

2.000%, 06/15/2019

|

30,000

|

29,966

|

||||||

|

2.000%, 04/01/2021

|

100,000

|

98,964

|

||||||

|

Toyota Motor Credit Corp.

|

||||||||

|

2.125%, 07/18/2019

|

40,000

|

39,945

|

||||||

|

2.200%, 01/10/2020

|

40,000

|

39,884

|

||||||

|

4.250%, 01/11/2021

|

100,000

|

102,923

|

||||||

|

2.150%, 09/08/2022

|

30,000

|

29,607

|

||||||

The accompanying notes are an integral part of these financial statements.

7

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

Par

|

||||||||

|

Value

|

Value

|

|||||||

|

Consumer, Cyclical – 0.8% (Continued)

|

||||||||

|

Walmart, Inc.

|

||||||||

|

1.900%, 12/15/2020

|

$

|

30,000

|

$

|

29,756

|

||||

|

4.250%, 04/15/2021

|

60,000

|

62,339

|

||||||

|

2,863,311

|

||||||||

|

Consumer, Non-cyclical – 2.5%

|

||||||||

|

AstraZeneca PLC

|

||||||||

|

3.221% (3 Month LIBOR USD + 0.620%), 06/10/2022 (a)(e)

|

2,000,000

|

1,986,014

|

||||||

|

Colgate-Palmolive Co.

|

||||||||

|

2.250%, 11/15/2022

|

75,000

|

74,630

|

||||||

|

Danaher Corp.

|

||||||||

|

2.400%, 09/15/2020

|

25,000

|

24,893

|

||||||

|

Eli Lilly & Co.

|

||||||||

|

2.350%, 05/15/2022

|

70,000

|

69,657

|

||||||

|

Johnson & Johnson

|

||||||||

|

2.250%, 03/03/2022

|

60,000

|

59,759

|

||||||

|

Merck & Co., Inc.

|

||||||||

|

1.850%, 02/10/2020

|

14,000

|

13,911

|

||||||

|

3.875%, 01/15/2021

|

50,000

|

51,082

|

||||||

|

Novartis Capital Corp.

|

||||||||

|

1.800%, 02/14/2020

|

70,000

|

69,521

|

||||||

|

PepsiCo, Inc.

|

||||||||

|

2.150%, 10/14/2020

|

60,000

|

59,807

|

||||||

|

3.600%, 03/01/2024

|

100,000

|

104,579

|

||||||

|

Pfizer, Inc.

|

||||||||

|

1.700%, 12/15/2019

|

50,000

|

49,590

|

||||||

|

Reckitt Benckiser Treasury Services PLC

|

||||||||

|

3.162% (3 Month LIBOR USD + 0.560%), 06/24/2022

|

||||||||

|

(Acquired 02/15/2018, Cost $5,772,443) (a)(d)(e)

|

5,775,000

|

5,729,648

|

||||||

|

The Coca-Cola Co.

|

||||||||

|

1.375%, 05/30/2019

|

20,000

|

19,950

|

||||||

|

2.200%, 05/25/2022

|

50,000

|

49,758

|

||||||

|

3.200%, 11/01/2023

|

60,000

|

61,721

|

||||||

|

The Hershey Co.

|

||||||||

|

3.100%, 05/15/2021

|

150,000

|

151,578

|

||||||

|

The Procter & Gamble Co.

|

||||||||

|

2.300%, 02/06/2022

|

60,000

|

59,955

|

||||||

The accompanying notes are an integral part of these financial statements.

8

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

Par

|

||||||||

|

Value

|

Value

|

|||||||

|

Consumer, Non-cyclical – 2.5% (Continued)

|

||||||||

|

Unilever Capital Corp.

|

||||||||

|

2.750%, 03/22/2021

|

$

|

100,000

|

$

|

100,406

|

||||

|

UnitedHealth Group, Inc.

|

||||||||

|

2.700%, 07/15/2020

|

155,000

|

155,367

|

||||||

|

3.500%, 02/15/2024

|

160,000

|

164,920

|

||||||

|

9,056,746

|

||||||||

|

Energy – 0.1%

|

||||||||

|

BP Capital Markets America, Inc.

|

||||||||

|

3.790%, 02/06/2024

|

200,000

|

207,774

|

||||||

|

Chevron Corp.

|

||||||||

|

2.419%, 11/17/2020

|

50,000

|

49,927

|

||||||

|

3.191%, 06/24/2023

|

50,000

|

51,182

|

||||||

|

EOG Resources, Inc.

|

||||||||

|

5.625%, 06/01/2019

|

15,000

|

15,071

|

||||||

|

2.625%, 03/15/2023

|

100,000

|

99,373

|

||||||

|

423,327

|

||||||||

|

Financial – 79.1%

|

||||||||

|

American Express Co.

|

||||||||

|

3.346% (3 Month LIBOR USD + 0.610%), 08/01/2022 (a)

|

3,391,000

|

3,391,348

|

||||||

|

3.289% (3 Month LIBOR USD + 0.650%), 02/27/2023 (a)

|

2,700,000

|

2,696,554

|

||||||

|

American Express Credit Corp.

|

||||||||

|

2.250%, 08/15/2019

|

95,000

|

94,855

|

||||||

|

3.321% (3 Month LIBOR USD + 0.570%), 10/30/2019 (a)

|

1,000,000

|

1,002,675

|

||||||

|

3.045% (3 Month LIBOR USD + 0.430%), 03/03/2020 (a)

|

1,799,000

|

1,802,018

|

||||||

|

3.315% (3 Month LIBOR USD + 0.700%), 03/03/2022 (a)

|

6,990,000

|

7,015,924

|

||||||

|

Athene Global Funding

|

||||||||

|

4.038% (3 Month LIBOR USD + 1.230%), 07/01/2022

|

||||||||

|

(Acquired 02/22/2018, Cost $3,046,805) (a)(d)

|

3,000,000

|

3,015,079

|

||||||

|

AvalonBay Communities, Inc.

|

||||||||

|

3.625%, 10/01/2020

|

50,000

|

50,602

|

||||||

|

Banco Santander SA

|

||||||||

|

4.359% (3 Month LIBOR USD + 1.560%), 04/11/2022 (a)(e)

|

4,800,000

|

4,841,904

|

||||||

|

3.741% (3 Month LIBOR USD + 1.090%), 02/23/2023 (a)(e)

|

13,250,000

|

13,082,300

|

||||||

|

3.917% (3 Month LIBOR USD + 1.120%), 04/12/2023 (a)(e)

|

500,000

|

494,155

|

||||||

The accompanying notes are an integral part of these financial statements.

9

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

Par

|

||||||||

|

Value

|

Value

|

|||||||

|

Financial – 79.1% (Continued)

|

||||||||

|

Bank of America Corp.

|

||||||||

|

2.650%, 04/01/2019

|

$

|

60,000

|

$

|

60,000

|

||||

|

4.181% (3 Month LIBOR USD + 1.420%), 04/19/2021 (a)

|

3,500,000

|

3,574,979

|

||||||

|

3.421% (3 Month LIBOR USD + 0.660%), 07/21/2021 (a)

|

1,000,000

|

1,002,599

|

||||||

|

3.242% (3 Month LIBOR USD + 0.650%), 10/01/2021 (a)

|

2,000,000

|

2,006,643

|

||||||

|

3.252% (3 Month LIBOR USD + 0.650%), 06/25/2022 (a)

|

2,500,000

|

2,501,326

|

||||||

|

3.941% (3 Month LIBOR USD + 1.180%), 10/21/2022 (a)

|

5,400,000

|

5,465,182

|

||||||

|

3.921% (3 Month LIBOR USD + 1.160%), 01/20/2023 (a)

|

850,000

|

860,811

|

||||||

|

3.389% (3 Month LIBOR USD + 0.790%), 03/05/2024 (a)

|

950,000

|

947,249

|

||||||

|

Bank of Montreal

|

||||||||

|

3.231% (3 Month LIBOR USD + 0.630%), 09/11/2022 (a)(e)

|

4,300,000

|

4,309,619

|

||||||

|

BB&T Corp.

|

||||||||

|

3.242% (3 Month LIBOR USD + 0.650%), 04/01/2022 (a)

|

3,600,000

|

3,611,566

|

||||||

|

Berkshire Hathaway Finance Corp.

|

||||||||

|

4.250%, 01/15/2021

|

210,000

|

216,835

|

||||||

|

BlackRock, Inc.

|

||||||||

|

5.000%, 12/10/2019

|

75,000

|

76,196

|

||||||

|

Canadian Imperial Bank of Commerce

|

||||||||

|

3.105% (3 Month LIBOR USD + 0.310%), 10/05/2020 (a)(e)

|

4,000,000

|

4,009,142

|

||||||

|

3.335% (3 Month LIBOR USD + 0.720%), 06/16/2022 (a)(e)

|

4,496,000

|

4,518,680

|

||||||

|

Capital One Financial Corp.

|

||||||||

|

3.458% (3 Month LIBOR USD + 0.760%), 05/12/2020 (a)

|

5,848,000

|

5,874,211

|

||||||

|

3.551% (3 Month LIBOR USD + 0.950%), 03/09/2022 (a)

|

3,000,000

|

3,013,536

|

||||||

|

3.471% (3 Month LIBOR USD + 0.720%), 01/30/2023 (a)

|

4,583,000

|

4,526,476

|

||||||

|

Capital One, N.A.

|

||||||||

|

3.558% (3 Month LIBOR USD + 0.820%), 08/08/2022 (a)

|

3,385,000

|

3,384,033

|

||||||

|

3.901% (3 Month LIBOR USD + 1.150%), 01/30/2023 (a)

|

5,291,000

|

5,303,063

|

||||||

|

Chubb INA Holdings, Inc.

|

||||||||

|

2.300%, 11/03/2020

|

80,000

|

79,643

|

||||||

|

Citigroup, Inc.

|

||||||||

|

4.075% (3 Month LIBOR USD + 1.310%), 10/26/2020 (a)

|

2,000,000

|

2,027,704

|

||||||

|

3.981% (3 Month LIBOR USD + 1.380%), 03/30/2021 (a)

|

550,000

|

559,485

|

||||||

|

3.928% (3 Month LIBOR USD + 1.190%), 08/02/2021 (a)

|

1,570,000

|

1,592,832

|

||||||

|

3.665% (3 Month LIBOR USD + 1.070%), 12/08/2021 (a)

|

5,000,000

|

5,058,216

|

||||||

|

3.731% (3 Month LIBOR USD + 0.960%), 04/25/2022 (a)

|

1,890,000

|

1,905,541

|

||||||

|

3.455% (3 Month LIBOR USD + 0.690%), 10/27/2022 (a)

|

2,700,000

|

2,691,043

|

||||||

|

3.729% (3 Month LIBOR USD + 0.950%), 07/24/2023 (a)

|

4,350,000

|

4,359,103

|

||||||

The accompanying notes are an integral part of these financial statements.

10

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

Par

|

||||||||

|

Value

|

Value

|

|||||||

|

Financial – 79.1% (Continued)

|

||||||||

|

Credit Suisse Group AG

|

||||||||

|

3.793% (3 Month LIBOR USD + 1.200%), 12/14/2023

|

||||||||

|

(Acquired 09/11/2017, Cost $10,445,011) (a)(d)(e)

|

$

|

10,300,000

|

$

|

10,261,506

|

||||

|

Deutsche Bank AG

|

||||||||

|

3.767% (3 Month LIBOR USD + 0.970%), 07/13/2020 (a)(e)

|

8,000,000

|

7,974,096

|

||||||

|

ERP Operating LP

|

||||||||

|

4.625%, 12/15/2021

|

75,000

|

78,464

|

||||||

|

HSBC Holdings PLC

|

||||||||

|

4.835% (3 Month LIBOR USD + 2.240%), 03/08/2021 (a)(e)

|

1,000,000

|

1,031,520

|

||||||

|

3.283% (3 Month LIBOR USD + 0.600%), 05/18/2021 (a)(e)

|

6,300,000

|

6,298,875

|

||||||

|

4.295% (3 Month LIBOR USD + 1.500%), 01/05/2022 (a)(e)

|

9,400,000

|

9,609,321

|

||||||

|

Manufacturers & Traders Trust Co.

|

||||||||

|

3.266% (3 Month LIBOR USD + 0.640%), 12/01/2021 (a)

|

5,000,000

|

4,977,645

|

||||||

|

Mitsubishi UFJ Financial Group, Inc.

|

||||||||

|

3.561% (3 Month LIBOR USD + 0.790%), 07/25/2022 (a)(e)

|

1,975,000

|

1,976,507

|

||||||

|

3.355% (3 Month LIBOR USD + 0.740%), 03/02/2023 (a)(e)

|

2,000,000

|

2,000,143

|

||||||

|

Mizuho Financial Group, Inc.

|

||||||||

|

3.748% (3 Month LIBOR USD + 1.140%), 09/13/2021 (a)(e)

|

4,000,000

|

4,046,993

|

||||||

|

3.569% (3 Month LIBOR USD + 0.940%), 02/28/2022 (a)(e)

|

7,300,000

|

7,341,377

|

||||||

|

3.481% (3 Month LIBOR USD + 0.880%), 09/11/2022 (a)(e)

|

1,100,000

|

1,105,360

|

||||||

|

3.389% (3 Month LIBOR USD + 0.790%), 03/05/2023 (a)(e)

|

3,900,000

|

3,905,692

|

||||||

|

Morgan Stanley

|

||||||||

|

3.905% (3 Month LIBOR USD + 1.140%), 01/27/2020 (a)

|

1,334,000

|

1,342,799

|

||||||

|

4.161% (3 Month LIBOR USD + 1.400%), 04/21/2021 (a)

|

1,000,000

|

1,018,094

|

||||||

|

3.941% (3 Month LIBOR USD + 1.180%), 01/20/2022 (a)

|

1,900,000

|

1,919,571

|

||||||

|

3.691% (3 Month LIBOR USD + 0.930%), 07/22/2022 (a)

|

7,920,000

|

7,964,063

|

||||||

|

4.179% (3 Month LIBOR USD + 1.400%), 10/24/2023 (a)

|

4,900,000

|

4,978,251

|

||||||

|

3.958% (3 Month LIBOR USD + 1.220%), 05/08/2024 (a)

|

1,029,000

|

1,037,127

|

||||||

|

National Rural Utilities Cooperative Finance Corp.

|

||||||||

|

2.300%, 11/15/2019

|

25,000

|

24,936

|

||||||

|

2.000%, 01/27/2020

|

75,000

|

74,753

|

||||||

|

Northern Trust Corp.

|

||||||||

|

3.450%, 11/04/2020

|

25,000

|

25,366

|

||||||

|

3.375%, 08/23/2021

|

25,000

|

25,482

|

||||||

|

PNC Bank, N.A.

|

||||||||

|

2.400%, 10/18/2019

|

3,000,000

|

2,995,875

|

||||||

The accompanying notes are an integral part of these financial statements.

11

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

Par

|

||||||||

|

Value

|

Value

|

|||||||

|

Financial – 79.1% (Continued)

|

||||||||

|

Public Storage

|

||||||||

|

2.370%, 09/15/2022

|

$

|

180,000

|

$

|

178,275

|

||||

|

Royal Bank of Canada

|

||||||||

|

3.466% (3 Month LIBOR USD + 0.730%), 02/01/2022 (a)(e)

|

5,355,000

|

5,410,930

|

||||||

|

Simon Property Group LP

|

||||||||

|

4.375%, 03/01/2021

|

50,000

|

51,405

|

||||||

|

2.500%, 07/15/2021

|

120,000

|

119,738

|

||||||

|

2.350%, 01/30/2022

|

50,000

|

49,667

|

||||||

|

State Street Corp.

|

||||||||

|

1.950%, 05/19/2021

|

25,000

|

24,683

|

||||||

|

Sumitomo Mitsui Banking Corp.

|

||||||||

|

3.090% (3 Month LIBOR USD + 0.310%), 10/18/2019 (a)(e)

|

2,000,000

|

2,002,310

|

||||||

|

3.123% (3 Month LIBOR USD + 0.350%), 01/17/2020 (a)(e)

|

2,525,000

|

2,529,644

|

||||||

|

Sumitomo Mitsui Financial Group, Inc.

|

||||||||

|

3.897% (3 Month LIBOR USD + 1.110%), 07/14/2021 (a)(e)

|

6,013,000

|

6,085,293

|

||||||

|

3.901% (3 Month LIBOR USD + 1.140%), 10/19/2021 (a)(e)

|

2,000,000

|

2,024,820

|

||||||

|

3.567% (3 Month LIBOR USD + 0.780%), 07/12/2022 (a)(e)

|

5,400,000

|

5,416,813

|

||||||

|

SunTrust Bank

|

||||||||

|

3.274% (3 Month LIBOR USD + 0.530%), 01/31/2020 (a)

|

2,000,000

|

2,006,106

|

||||||

|

3.265% (3 Month LIBOR USD + 0.500%), 10/26/2021 (a)

|

3,000,000

|

3,003,452

|

||||||

|

3.328% (3 Month LIBOR USD + 0.590%), 08/02/2022 (a)

|

8,500,000

|

8,447,504

|

||||||

|

The Bank of New York Mellon Corp.

|

||||||||

|

4.600%, 01/15/2020

|

30,000

|

30,445

|

||||||

|

2.450%, 11/27/2020

|

35,000

|

34,859

|

||||||

|

3.801% (3 Month LIBOR USD + 1.050%), 10/30/2023 (a)

|

11,036,000

|

11,170,666

|

||||||

|

The Bank of Nova Scotia

|

||||||||

|

3.187% (3 Month LIBOR USD + 0.390%), 07/14/2020 (a)(e)

|

3,000,000

|

3,008,248

|

||||||

|

3.247% (3 Month LIBOR USD + 0.640%), 03/07/2022 (a)(e)

|

5,900,000

|

5,927,907

|

||||||

|

The Goldman Sachs Group, Inc.

|

||||||||

|

4.131% (3 Month LIBOR USD + 1.360%), 04/23/2021 (a)

|

1,000,000

|

1,015,031

|

||||||

|

3.854% (3 Month LIBOR USD + 1.170%), 11/15/2021 (a)

|

2,000,000

|

2,019,138

|

||||||

|

3.875% (3 Month LIBOR USD + 1.110%), 04/26/2022 (a)

|

1,941,000

|

1,951,957

|

||||||

|

3.524% (3 Month LIBOR USD + 0.780%), 10/31/2022 (a)

|

7,020,000

|

6,993,429

|

||||||

|

3.779% (3 Month LIBOR USD + 1.000%), 07/24/2023 (a)

|

550,000

|

550,008

|

||||||

|

4.229% (3 Month LIBOR USD + 1.600%), 11/29/2023 (a)

|

5,600,000

|

5,729,540

|

||||||

|

The Toronto-Dominion Bank

|

||||||||

|

3.031% (3 Month LIBOR USD + 0.430%), 06/11/2021 (a)(e)

|

2,350,000

|

2,358,867

|

||||||

The accompanying notes are an integral part of these financial statements.

12

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

Par

|

||||||||

|

Value

|

Value

|

|||||||

|

Financial – 79.1% (Continued)

|

||||||||

|

The Travelers Cos, Inc.

|

||||||||

|

3.900%, 11/01/2020

|

$

|

110,000

|

$

|

112,294

|

||||

|

Visa, Inc.

|

||||||||

|

2.200%, 12/14/2020

|

70,000

|

69,712

|

||||||

|

2.150%, 09/15/2022

|

50,000

|

49,518

|

||||||

|

Wells Fargo & Co.

|

||||||||

|

2.150%, 01/30/2020

|

200,000

|

199,095

|

||||||

|

3.431% (3 Month LIBOR USD + 0.680%), 01/30/2020 (a)

|

2,000,000

|

2,009,749

|

||||||

|

2.500%, 03/04/2021

|

30,000

|

29,870

|

||||||

|

3.955% (3 Month LIBOR USD + 1.340%), 03/04/2021 (a)

|

2,500,000

|

2,544,401

|

||||||

|

4.600%, 04/01/2021

|

60,000

|

62,006

|

||||||

|

2.100%, 07/26/2021

|

110,000

|

108,324

|

||||||

|

3.627% (3 Month LIBOR USD + 0.930%), 02/11/2022 (a)

|

4,500,000

|

4,532,151

|

||||||

|

3.889% (3 Month LIBOR USD + 1.110%), 01/24/2023 (a)

|

6,890,000

|

6,961,167

|

||||||

|

3.974% (3 Month LIBOR USD + 1.230%), 10/31/2023 (a)

|

925,000

|

940,208

|

||||||

|

288,796,173

|

||||||||

|

Industrial – 0.6%

|

||||||||

|

Caterpillar Financial Services Corp.

|

||||||||

|

2.250%, 12/01/2019

|

20,000

|

19,953

|

||||||

|

2.950%, 05/15/2020

|

50,000

|

50,173

|

||||||

|

1.850%, 09/04/2020

|

25,000

|

24,731

|

||||||

|

2.900%, 03/15/2021

|

15,000

|

15,082

|

||||||

|

Caterpillar, Inc.

|

||||||||

|

3.400%, 05/15/2024

|

60,000

|

62,216

|

||||||

|

Emerson Electric Co.

|

||||||||

|

4.875%, 10/15/2019

|

45,000

|

45,522

|

||||||

|

General Dynamics Corp.

|

||||||||

|

3.000%, 05/11/2021

|

105,000

|

105,924

|

||||||

|

2.250%, 11/15/2022

|

60,000

|

59,441

|

||||||

|

General Electric Co.

|

||||||||

|

6.000%, 08/07/2019

|

50,000

|

50,480

|

||||||

|

5.500%, 01/08/2020

|

100,000

|

102,189

|

||||||

|

4.625%, 01/07/2021

|

250,000

|

256,796

|

||||||

|

4.000% (3 Month LIBOR USD + 2.280%), 12/29/2049 (a)(b)

|

1,234,000

|

902,640

|

||||||

|

Honeywell International, Inc.

|

||||||||

|

1.800%, 10/30/2019

|

60,000

|

59,710

|

||||||

|

1.850%, 11/01/2021

|

60,000

|

58,965

|

||||||

The accompanying notes are an integral part of these financial statements.

13

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

Par

|

||||||||

|

Value

|

Value

|

|||||||

|

Industrial – 0.6% (Continued)

|

||||||||

|

John Deere Capital Corp.

|

||||||||

|

1.950%, 06/22/2020

|

$

|

75,000

|

$

|

74,430

|

||||

|

2.375%, 07/14/2020

|

50,000

|

49,858

|

||||||

|

2.650%, 01/06/2022

|

50,000

|

50,001

|

||||||

|

2.800%, 01/27/2023

|

60,000

|

60,292

|

||||||

|

Pall Corp.

|

||||||||

|

5.000%, 06/15/2020

|

50,000

|

51,280

|

||||||

|

United Parcel Service, Inc.

|

||||||||

|

3.125%, 01/15/2021

|

30,000

|

30,366

|

||||||

|

2.350%, 05/16/2022

|

50,000

|

49,722

|

||||||

|

2,179,771

|

||||||||

|

Technology – 0.3%

|

||||||||

|

Apple, Inc.

|

||||||||

|

1.550%, 02/07/2020

|

10,000

|

9,924

|

||||||

|

1.900%, 02/07/2020

|

45,000

|

44,796

|

||||||

|

1.800%, 05/11/2020

|

50,000

|

49,625

|

||||||

|

2.250%, 02/23/2021

|

63,000

|

62,773

|

||||||

|

2.150%, 02/09/2022

|

155,000

|

153,526

|

||||||

|

2.400%, 05/03/2023

|

60,000

|

59,482

|

||||||

|

IBM Credit LLC

|

||||||||

|

1.800%, 01/20/2021

|

100,000

|

98,526

|

||||||

|

Intel Corp.

|

||||||||

|

1.700%, 05/19/2021

|

110,000

|

108,171

|

||||||

|

3.300%, 10/01/2021

|

33,000

|

33,650

|

||||||

|

3.100%, 07/29/2022

|

50,000

|

50,924

|

||||||

|

International Business Machines Corp.

|

||||||||

|

1.900%, 01/27/2020

|

100,000

|

99,384

|

||||||

|

Microsoft Corp.

|

||||||||

|

4.200%, 06/01/2019

|

30,000

|

30,072

|

||||||

|

1.550%, 08/08/2021

|

225,000

|

219,753

|

||||||

|

Oracle Corp.

|

||||||||

|

5.000%, 07/08/2019

|

30,000

|

30,185

|

||||||

|

2.500%, 05/15/2022

|

130,000

|

129,406

|

||||||

|

1,180,197

|

||||||||

The accompanying notes are an integral part of these financial statements.

14

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

Par

|

||||||||

|

Value

|

Value

|

|||||||

|

Utilities – 0.2%

|

||||||||

|

DTE Electric Co.

|

||||||||

|

3.900%, 06/01/2021

|

$

|

55,000

|

$

|

56,323

|

||||

|

Duke Energy Carolinas LLC

|

||||||||

|

4.300%, 06/15/2020

|

25,000

|

25,500

|

||||||

|

3.900%, 06/15/2021

|

25,000

|

25,692

|

||||||

|

Duke Energy Progress LLC

|

||||||||

|

2.800%, 05/15/2022

|

70,000

|

70,445

|

||||||

|

Entergy Gulf States Louisiana LLC

|

||||||||

|

3.950%, 10/01/2020

|

50,000

|

50,781

|

||||||

|

Kansas City Power & Light Co.

|

||||||||

|

7.150%, 04/01/2019

|

20,000

|

20,000

|

||||||

|

Kentucky Utilities Co.

|

||||||||

|

3.250%, 11/01/2020

|

30,000

|

30,252

|

||||||

|

Northern States Power Co.

|

||||||||

|

2.200%, 08/15/2020

|

30,000

|

29,865

|

||||||

|

Public Service Co. of Colorado

|

||||||||

|

3.200%, 11/15/2020

|

30,000

|

30,206

|

||||||

|

Public Service Electric & Gas Co.

|

||||||||

|

1.800%, 06/01/2019

|

25,000

|

24,964

|

||||||

|

2.000%, 08/15/2019

|

75,000

|

74,822

|

||||||

|

San Diego Gas & Electric Co.

|

||||||||

|

3.000%, 08/15/2021

|

30,000

|

30,171

|

||||||

|

Southern California Edison Co.

|

||||||||

|

3.875%, 06/01/2021

|

40,000

|

40,330

|

||||||

|

3.400%, 06/01/2023

|

50,000

|

49,660

|

||||||

|

Westar Energy, Inc.

|

||||||||

|

5.100%, 07/15/2020

|

75,000

|

77,024

|

||||||

|

Wisconsin Power & Light Co

|

||||||||

|

5.000%, 07/15/2019

|

25,000

|

25,162

|

||||||

|

661,197

|

||||||||

|

TOTAL CORPORATE BONDS AND NOTES

|

||||||||

|

(Cost $312,098,333)

|

310,817,843

|

|||||||

The accompanying notes are an integral part of these financial statements.

15

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

COLLATERALIZED

|

Par

|

|||||||

|

MORTGAGE OBLIGATIONS – 1.7%

|

Value

|

Value

|

||||||

|

Federal Home Loan Mortgage

|

||||||||

|

Corporation REMICS – 0.7%

|

||||||||

|

Series 3799, Class GK

|

||||||||

|

2.750%, 01/15/2021

|

$

|

66,958

|

$

|

66,849

|

||||

|

Series 3784, Class BH

|

||||||||

|

3.500%, 01/15/2021

|

132,691

|

133,302

|

||||||

|

Series 2989, Class TG

|

||||||||

|

5.000%, 06/15/2025

|

20,551

|

21,186

|

||||||

|

Series 3002, Class YD

|

||||||||

|

4.500%, 07/15/2025

|

8,428

|

8,778

|

||||||

|

Series 3990, Class UB

|

||||||||

|

2.500%, 01/15/2026

|

123,922

|

123,396

|

||||||

|

Series 3917, Class AB

|

||||||||

|

1.750%, 07/15/2026

|

87,326

|

86,021

|

||||||

|

Series 2097, Class PZ

|

||||||||

|

6.000%, 11/15/2028

|

257,997

|

280,304

|

||||||

|

Series 2091, Class PG

|

||||||||

|

6.000%, 11/15/2028

|

407,512

|

444,102

|

||||||

|

Series 2526, Class FI

|

||||||||

|

3.484% (1 Month LIBOR USD + 1.000%), 02/15/2032 (a)

|

47,224

|

47,133

|

||||||

|

Series 4203, Class DM

|

||||||||

|

3.000%, 04/15/2033

|

181,109

|

183,076

|

||||||

|

Series 4363, Class EJ

|

||||||||

|

4.000%, 05/15/2033

|

130,130

|

135,676

|

||||||

|

Series 4453, Class DA

|

||||||||

|

3.500%, 11/15/2033

|

251,348

|

256,574

|

||||||

|

Series 2759, Class TC

|

||||||||

|

4.500%, 03/15/2034

|

243,448

|

257,775

|

||||||

|

Series 2881, Class AE

|

||||||||

|

5.000%, 08/15/2034

|

5,777

|

5,918

|

||||||

|

Series 2933, Class HD

|

||||||||

|

5.500%, 02/15/2035

|

11,090

|

11,918

|

||||||

|

Series 4305, Class KA

|

||||||||

|

3.000%, 03/15/2038

|

26,819

|

26,844

|

||||||

|

Series 3843, Class GH

|

||||||||

|

3.750%, 10/15/2039

|

28,328

|

28,946

|

||||||

|

Series 3824, Class PA

|

||||||||

|

4.500%, 11/15/2039

|

210,057

|

213,459

|

||||||

The accompanying notes are an integral part of these financial statements.

16

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

Par

|

||||||||

|

Value

|

Value

|

|||||||

|

Federal Home Loan Mortgage

|

||||||||

|

Corporation REMICS – 0.7% (Continued)

|

||||||||

|

Series 3786, Class NA

|

||||||||

|

4.500%, 07/15/2040

|

$

|

51,763

|

$

|

53,948

|

||||

|

Series 4305, Class A

|

||||||||

|

3.500%, 06/15/2048

|

73,933

|

75,292

|

||||||

|

2,460,497

|

||||||||

|

Federal National Mortgage Association REMICS – 0.8%

|

||||||||

|

Series 2005-40, Class YG

|

||||||||

|

5.000%, 05/25/2025

|

17,772

|

18,277

|

||||||

|

Series 2011-122, Class A

|

||||||||

|

3.000%, 12/25/2025

|

14,713

|

14,682

|

||||||

|

Series 2011-110, Class CA

|

||||||||

|

3.500%, 06/25/2026

|

412,061

|

413,190

|

||||||

|

Series 2011-110, Class CY

|

||||||||

|

3.500%, 11/25/2026

|

375,000

|

385,861

|

||||||

|

Series 2007-27, Class MQ

|

||||||||

|

5.500%, 04/25/2027

|

5,434

|

5,813

|

||||||

|

Series 2013-124, Class BD

|

||||||||

|

2.500%, 12/25/2028

|

192,504

|

190,919

|

||||||

|

Series 2014-8, Class DA

|

||||||||

|

4.000%, 03/25/2029

|

142,020

|

146,680

|

||||||

|

Series 2002-56, Class PE

|

||||||||

|

6.000%, 09/25/2032

|

117,511

|

130,504

|

||||||

|

Series 2013-72, Class HG

|

||||||||

|

3.000%, 04/25/2033

|

288,755

|

291,583

|

||||||

|

Series 2003-127, Class EG

|

||||||||

|

6.000%, 12/25/2033

|

142,380

|

158,107

|

||||||

|

Series 2004-60, Class AB

|

||||||||

|

5.500%, 04/25/2034

|

369,815

|

391,981

|

||||||

|

Series 2005-48, Class AR

|

||||||||

|

5.500%, 02/25/2035

|

2,976

|

2,990

|

||||||

|

Series 2005-62, Class CQ

|

||||||||

|

4.750%, 07/25/2035

|

2,435

|

2,468

|

||||||

|

Series 2005-64, Class PL

|

||||||||

|

5.500%, 07/25/2035

|

27,665

|

29,923

|

||||||

The accompanying notes are an integral part of these financial statements.

17

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

Par

|

||||||||

|

Value

|

Value

|

|||||||

|

Federal National Mortgage

|

||||||||

|

Association REMICS – 0.8% (Continued)

|

||||||||

|

Series 2005-68, Class PG

|

||||||||

|

5.500%, 08/25/2035

|

$

|

22,047

|

$

|

23,956

|

||||

|

Series 2005-83A, Class LA

|

||||||||

|

5.500%, 10/25/2035

|

11,832

|

12,834

|

||||||

|

Series 2006-57, Class AD

|

||||||||

|

5.750%, 06/25/2036

|

41,935

|

43,616

|

||||||

|

Series 2014-23, Class PA

|

||||||||

|

3.500%, 08/25/2036

|

66,694

|

67,584

|

||||||

|

Series 2007-39, Class NA

|

||||||||

|

4.250%, 01/25/2037

|

45

|

45

|

||||||

|

Series 2013-83, Class CA

|

||||||||

|

3.500%, 10/25/2037

|

41,626

|

42,040

|

||||||

|

Series 2011-9, Class LH

|

||||||||

|

3.500%, 01/25/2039

|

424,294

|

433,432

|

||||||

|

Series 2009-47, Class PA

|

||||||||

|

4.500%, 07/25/2039

|

2,787

|

2,854

|

||||||

|

Series 2011-113, Class NE

|

||||||||

|

4.000%, 03/25/2040

|

5,574

|

5,577

|

||||||

|

Series 2012-134, Class VP

|

||||||||

|

3.000%, 10/25/2042

|

169,257

|

170,751

|

||||||

|

2,985,667

|

||||||||

|

Government National Mortgage

|

||||||||

|

Association REMICS – 0.2%

|

||||||||

|

Series 2013-88, Class WA

|

||||||||

|

5.029%, 06/20/2030 (a)

|

68,871

|

71,705

|

||||||

|

Series 2002-22, Class GF

|

||||||||

|

6.500%, 03/20/2032

|

27,238

|

27,194

|

||||||

|

Series 2002-51, Class D

|

||||||||

|

6.000%, 07/20/2032

|

30,874

|

30,835

|

||||||

|

Series 2008-50, Class NA

|

||||||||

|

5.500%, 03/16/2037

|

963

|

966

|

||||||

|

Series 2007-11, Class PE

|

||||||||

|

5.500%, 03/20/2037

|

16,029

|

17,641

|

||||||

|

Series 2009-127, Class PK

|

||||||||

|

4.000%, 10/20/2038

|

138,751

|

139,684

|

||||||

The accompanying notes are an integral part of these financial statements.

18

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

Par

|

||||||||

|

Value

|

Value

|

|||||||

|

Government National Mortgage

|

||||||||

|

Association REMICS – 0.2% (Continued)

|

||||||||

|

Series 2013-113, Class UB

|

||||||||

|

3.000%, 11/20/2038

|

$

|

34,488

|

$

|

34,611

|

||||

|

Series 2010-58, Class YJ

|

||||||||

|

3.000%, 05/16/2039

|

124,451

|

124,982

|

||||||

|

Series 2011-18, Class NH

|

||||||||

|

3.500%, 05/20/2039

|

132,085

|

131,844

|

||||||

|

Series 2012-39, Class MP

|

||||||||

|

2.000%, 08/20/2039

|

108,878

|

108,250

|

||||||

|

Series 2010-112, Class NG

|

||||||||

|

2.250%, 09/16/2040

|

190,446

|

186,227

|

||||||

|

873,939

|

||||||||

|

TOTAL COLLATERALIZED

|

||||||||

|

MORTGAGE

OBLIGATIONS (Cost $6,236,641)

|

6,320,103

|

|||||||

|

U.S. GOVERNMENT AGENCY OBLIGATIONS – 0.6%

|

||||||||

|

Federal Home Loan Bank – 0.1%

|

||||||||

|

Federal Home Loan Banks

|

||||||||

|

0.875%, 08/05/2019

|

200,000

|

198,916

|

||||||

|

1.000%, 09/26/2019

|

300,000

|

297,927

|

||||||

|

496,843

|

||||||||

|

Federal Home Loan Mortgage Corp. – 0.2%

|

||||||||

|

1.750%, 05/30/2019

|

200,000

|

199,771

|

||||||

|

1.500%, 01/17/2020

|

355,000

|

352,357

|

||||||

|

5.500%, 04/01/2021, Gold Pool #G11941

|

6,887

|

7,001

|

||||||

|

5.500%, 11/01/2021, Gold Pool #G12454

|

4,011

|

4,101

|

||||||

|

5.500%, 04/01/2023, Gold Pool #G13145

|

10,003

|

10,351

|

||||||

|

4.000%, 02/01/2026, Gold Pool #J14494

|

30,289

|

31,283

|

||||||

|

4.000%, 06/01/2026, Gold Pool #J15974

|

11,144

|

11,514

|

||||||

|

3.000%, 12/01/2026, Gold Pool #J17508

|

99,773

|

101,124

|

||||||

|

4.500%, 06/01/2029, Gold Pool #C91251

|

10,757

|

11,261

|

||||||

|

4.500%, 12/01/2029, Gold Pool #C91281

|

20,840

|

21,819

|

||||||

|

4.500%, 04/01/2030, Gold Pool #C91295

|

11,429

|

11,965

|

||||||

|

762,547

|

||||||||

The accompanying notes are an integral part of these financial statements.

19

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

Par

|

||||||||

|

Value

|

Value

|

|||||||

|

Federal National Mortgage Association – 0.3%

|

||||||||

|

1.000%, 08/28/2019

|

$

|

125,000

|

$

|

124,261

|

||||

|

2.000%, 01/05/2022

|

610,000

|

605,688

|

||||||

|

6.000%, 09/01/2019, Pool #735439

|

30

|

30

|

||||||

|

5.500%, 06/01/2020, Pool #888601

|

161

|

161

|

||||||

|

5.000%, 05/01/2023, Pool #254762

|

6,817

|

7,206

|

||||||

|

5.500%, 01/01/2024, Pool #AD0471

|

4,323

|

4,424

|

||||||

|

5.000%, 12/01/2025, Pool #256045

|

16,268

|

17,195

|

||||||

|

5.500%, 05/01/2028, Pool #257204

|

16,083

|

17,174

|

||||||

|

4.000%, 08/01/2029, Pool #MA0142

|

18,772

|

19,318

|

||||||

|

5.500%, 04/01/2037, Pool #AD0249

|

21,790

|

23,767

|

||||||

|

5.000%, 10/01/2039, Pool #AC3237

|

48,243

|

52,172

|

||||||

|

871,396

|

||||||||

|

TOTAL U.S. GOVERNMENT AGENCY OBLIGATIONS

|

||||||||

|

(Cost $2,131,354)

|

2,130,786

|

|||||||

|

U.S. TREASURY OBLIGATIONS – 9.7%

|

||||||||

|

U.S. Treasury Notes – 9.7%

|

||||||||

|

1.000%, 08/31/2019

|

690,000

|

685,876

|

||||||

|

1.750%, 09/30/2019

|

515,000

|

513,230

|

||||||

|

1.500%, 11/30/2019

|

410,000

|

407,486

|

||||||

|

1.125%, 12/31/2019

|

640,000

|

633,925

|

||||||

|

1.625%, 12/31/2019

|

220,000

|

218,681

|

||||||

|

1.250%, 01/31/2020

|

850,000

|

841,832

|

||||||

|

1.375%, 01/31/2020

|

250,000

|

247,900

|

||||||

|

1.375%, 02/29/2020

|

680,000

|

673,652

|

||||||

|

1.125%, 03/31/2020

|

300,000

|

296,338

|

||||||

|

1.375%, 04/30/2020

|

2,080,000

|

2,057,697

|

||||||

|

1.500%, 05/15/2020

|

1,300,000

|

1,287,406

|

||||||

|

1.500%, 05/31/2020

|

1,460,000

|

1,445,257

|

||||||

|

1.875%, 06/30/2020

|

200,000

|

198,770

|

||||||

|

2.500%, 06/30/2020

|

3,500,000

|

3,505,332

|

||||||

|

1.625%, 07/31/2020

|

2,130,000

|

2,109,158

|

||||||

|

2.000%, 07/31/2020

|

910,000

|

905,752

|

||||||

|

1.375%, 08/31/2020

|

1,230,000

|

1,213,063

|

||||||

The accompanying notes are an integral part of these financial statements.

20

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

Par

|

||||||||

|

Value

|

Value

|

|||||||

|

U.S. Treasury Notes – 9.7% (Continued)

|

||||||||

|

1.375%, 09/30/2020

|

$

|

1,975,000

|

$

|

1,946,802

|

||||

|

1.375%, 10/31/2020

|

1,435,000

|

1,413,727

|

||||||

|

1.750%, 10/31/2020

|

6,950,000

|

6,887,016

|

||||||

|

1.625%, 11/30/2020

|

490,000

|

484,468

|

||||||

|

2.000%, 11/30/2020

|

390,000

|

387,943

|

||||||

|

1.375%, 01/31/2021

|

2,300,000

|

2,261,951

|

||||||

|

2.125%, 01/31/2021

|

345,000

|

343,956

|

||||||

|

1.125%, 02/28/2021

|

1,165,000

|

1,139,789

|

||||||

|

1.250%, 03/31/2021

|

2,135,000

|

2,093,384

|

||||||

|

1.375%, 04/30/2021

|

1,025,000

|

1,006,582

|

||||||

|

3.125%, 05/15/2021

|

100,000

|

101,746

|

||||||

|

TOTAL U.S. TREASURY OBLIGATIONS

|

||||||||

|

(Cost $35,442,459)

|

35,308,719

|

|||||||

|

SHORT-TERM INVESTMENTS – 2.5%

|

||||||||

|

Commercial Paper – 1.1%

|

||||||||

|

MUFG Bank Ltd., 2.381%, 04/01/2019

|

2,000,000

|

1,999,598

|

||||||

|

MUFG Bank Ltd., 2.381%, 04/02/2019

|

2,000,000

|

1,999,464

|

||||||

|

TOTAL COMMERCIAL PAPER

|

||||||||

|

(Cost $3,999,868)

|

3,999,062

|

|||||||

The accompanying notes are an integral part of these financial statements.

21

Pemberwick Fund

|

SCHEDULE OF INVESTMENTS (Continued)

|

|

at March 31, 2019

|

|

Shares

|

Value

|

|||||||

|

Money Market Funds – 1.4%

|

||||||||

|

First American Government Obligations Fund –

|

||||||||

|

Class X, 2.36% (c) (Cost $5,221,124)

|

5,221,124

|

$

|

5,221,124

|

|||||

|

TOTAL SHORT-TERM INVESTMENTS

|

||||||||

|

(Cost $9,220,992)

|

9,220,186

|

|||||||

|

TOTAL INVESTMENTS

|

||||||||

|

(Cost $365,129,779) – 99.6%

|

363,797,637

|

|||||||

|

Other Assets in Excess of Liabilities – 0.4%

|

1,483,822

|

|||||||

|

TOTAL NET ASSETS – 100.0%

|

$

|

365,281,459

|

||||||

Percentages are stated as a percent of net assets.

PLC – Public Limited Company

REMICS – Real Estate Mortgage Investment Conduits

|

(a)

|

Variable or Floating Rate Security. The rate shown represents the rate at March 31, 2019.

|

|

(b)

|

Security is a perpetual bond and has no definite maturity date.

|

|

(c)

|

The rate shown represents the fund’s 7-day yield as of March 31, 2019.

|

|

(d)

|

Security exempt from registration pursuant to Rule 144A under the Securities Act of 1933, as amended. These

securities may be resold in transactions exempt from registration to qualified institutional investors. At March 31, 2019, the market value of these securities total $19,006,233 which represents 5.2% of total net assets.

|

|

(e)

|

U.S. traded security of a foreign issuer or corporation.

|

Investment in a previous affiliated security was called before the end of the reporting period. Quasar Distributors, LLC,

which serves as the Fund’s distributor, is a subsidiary of U.S. Bancorp. Details of the transaction with this affiliated company for the fiscal year ended March 31, 2019 was as follows:

|

Issuer

|

U.S. Bancorp1

|

|||

|

Market Value at 3/31/18

|

$

|

74,602

|

||

|

Purchases

|

$

|

0

|

||

|

Sales

|

$

|

(75,000

|

)

|

|

|

Amortization

|

$

|

(547

|

)

|

|

|

Change in Unrealized Appreciation (Depreciation)

|

$

|

945

|

||

|

Net Realized Gains (Losses)

|

$

|

0

|

||

|

Market Value at 3/31/19

|

$

|

0

|

||

| Interest Income | $ |

1,075 | ^ | |

|

1

|

Par values were $75,000 and $0 at 3/31/18 and 3/31/19, respectively.

|

|

^

|

Includes amortization of $(547).

|

The accompanying notes are an integral part of these financial statements.

22

Pemberwick Fund

|

STATEMENT OF ASSETS AND LIABILITIES

|

|

at March 31, 2019

|

|

Assets:

|

||||

|

Investments in securities, at value (cost of $365,129,779)

|

$

|

363,797,637

|

||

|

Receivables:

|

||||

|

Dividends and interest

|

1,899,265

|

|||

|

Prepaid expenses and other assets

|

1,135

|

|||

|

Total assets

|

365,698,037

|

|||

|

Liabilities:

|

||||

|

Payables:

|

||||

|

Due to custodian

|

457

|

|||

|

Distribution payable

|

144,887

|

|||

|

Fund shares redeemed

|

130,000

|

|||

|

Advisory fee

|

46,254

|

|||

|

Administration and fund accounting fees

|

52,346

|

|||

|

Reports to shareholders

|

3,771

|

|||

|

Custody fees

|

5,679

|

|||

|

Transfer agent fees and expenses

|

9,825

|

|||

|

Other accrued expenses

|

23,359

|

|||

|

Total liabilities

|

416,578

|

|||

|

Net assets

|

$

|

365,281,459

|

||

|

Net assets consist of:

|

||||

|

Capital stock

|

$

|

367,414,693

|

||

|

Total accumulated deficit

|

(2,133,234

|

)

|

||

|

Net assets

|

$

|

365,281,459

|

||

|

Shares issued (Unlimited number of beneficial interest

|

||||

|

authorized, $0.01 par value)

|

36,635,347

|

|||

|

Net asset value, offering price and redemption price per share

|

$

|

9.97

|

||

The accompanying notes are an integral part of these financial statements.

23

Pemberwick Fund

|

STATEMENT OF OPERATIONS

|

|

Year Ended March 31, 2019

|

|

Investment income:

|

||||

|

Interest income from unaffiliated securities

|

$

|

10,136,061

|

||

|

Interest income from affiliated securities

|

1,075

|

|||

|

Total investment income

|

10,137,136

|

|||

|

Expenses:

|

||||

|

Investment advisory fees (Note 4)

|

872,988

|

|||

|

Administration and fund accounting fees (Note 4)

|

310,167

|

|||

|

Transfer agent fees and expenses

|

62,384

|

|||

|

Federal and state registration fees

|

17,540

|

|||

|

Audit fees

|

17,000

|

|||

|

Compliance expense

|

16,737

|

|||

|

Legal fees

|

14,465

|

|||

|

Reports to shareholders

|

3,500

|

|||

|

Trustees’ fees and expenses

|

10,047

|

|||

|

Custody fees

|

33,766

|

|||

|

Other

|

9,499

|

|||

|

Total expenses before reimbursement from advisor

|

1,368,093

|

|||

|

Expense reimbursement from advisor (Note 4)

|

(349,195

|

)

|

||

|

Net expenses

|

1,018,898

|

|||

|

Net investment income

|

9,118,238

|

|||

|

Realized and unrealized gain (loss) on investments:

|

||||

|

Net realized loss on unaffiliated investments

|

(118,386

|

)

|

||

|

Net realized gain (loss) on affiliated investments

|

—

|

|||

|

Net change in unrealized appreciation (depreciation)

|

||||

|

on unaffiliated investments

|

(435,164

|

)

|

||

|

Net change in unrealized appreciation (depreciation)

|

||||

|

on affiliated investments

|

945

|

|||

|

Net realized and unrealized loss on investments

|

(552,605

|

)

|

||

|

Net increase in net assets resulting from operations

|

$

|

8,565,633

|

||

The accompanying notes are an integral part of these financial statements.

24

Pemberwick Fund

|

STATEMENTS OF CHANGES IN NET ASSETS

|

|

Year Ended

|

Year Ended

|

|||||||

|

March 31, 2019

|

March 31, 2018

|

|||||||

|

Operations:

|

||||||||

|

Net investment income

|

$

|

9,118,238

|

$

|

3,148,112

|

||||

|

Net realized loss on investments

|

(118,386

|

)

|

(8,467

|

)

|

||||

|

Net change in unrealized

|

||||||||

|

appreciation (depreciation) on investments

|

(434,219

|

)

|

(1,113,784

|

)

|

||||

|

Net increase in net assets

|

||||||||

|

resulting from operations

|

8,565,633

|

2,025,861

|

||||||

|

Distributions to Shareholders From:

|

||||||||

|

Distributable earnings

|

(9,138,771

|

)

|

(3,195,328

|

)

|

||||

|

Total distributions

|

(9,138,771

|

)

|

(3,195,328

|

)(1)

|

||||

|

Capital Share Transactions:

|

||||||||

|

Proceeds from shares sold

|

191,436,335

|

133,860,651

|

||||||

|

Proceeds from shares issued to holders

|

||||||||

|

in reinvestment of dividends

|

8,989,855

|

3,190,364

|

||||||

|

Cost of shares redeemed

|

(114,891,314

|

)

|

(39,660,295

|

)

|

||||

|

Net increase in net assets from

|

||||||||

|

capital share transactions

|

85,534,876

|

97,390,720

|

||||||

|

Total increase in net assets

|

84,961,738

|

96,221,253

|

||||||

|

Net Assets:

|

||||||||

|

Beginning of year

|

280,319,721

|

184,098,468

|

||||||

|

End of year

|

$

|

365,281,459

|

$

|

280,319,721

|

(2)

|

|||

|

Changes in Shares Outstanding:

|

||||||||

|

Shares sold

|

19,188,022

|

13,360,376

|

||||||

|

Proceeds from shares issued to

|

||||||||

|

holders in reinvestment of dividends

|

902,596

|

318,422

|

||||||

|

Shares redeemed

|

(11,539,728

|

)

|

(3,955,495

|

)

|

||||

|

Net increase in shares outstanding

|

8,550,890

|

9,723,303

|

||||||

|

(1)

|

Includes net investment income distributions of $3,195,328.

|

|

(2)

|

Includes accumulated net investment income of $0.

|

The accompanying notes are an integral part of these financial statements.

25

Pemberwick Fund

|

FINANCIAL HIGHLIGHTS

|

|

For a capital share outstanding throughout each period

|

|

Eleven

|

||||||||||||||||||||||||

|

Months

|

||||||||||||||||||||||||

|

Year Ended

|

Ended

|

|||||||||||||||||||||||

|