UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For the fiscal year ended

or

For the transition period from _____________to ______________

Commission file number

(Exact name of registrant as specified in its charter)

| State or other jurisdiction of | (I.R.S. Employer | |

| Incorporation or organization | Identification No.) |

Hebei Province, The People’s Republic

of

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including

area code:

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Securities registered pursuant to section 12(g) of the Act:

Common Stock

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer,

as defined in Rule 405 of the Securities Act. ☐ Yes ☒

Indicate by check mark if the registrant is not required to file reports

pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days. ☒

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant

has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial

reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or

issued its audit report.

If securities are registered pursuant to Section

12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction

of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as

defined in Rule 12b-2 of the Act). ☐ Yes

The aggregate market value of the voting and non-voting common stock

of the registrant held by non-affiliates as of June 30, 2023 was approximately $

As of March 27, 2024, there were

DOCUMENTS INCORPORATED BY REFERENCE:

TABLE OF CONTENTS

i

INTRODUCTION

All references to “we,” “us,” “our,” or similar terms used in this annual report refer to IT Tech Packaging, Inc., a Nevada corporation, including its wholly-owned subsidiaries, and, in the context of describing our operations and consolidated financial information, our variable interest entity in China, Hebei Baoding Dongfang Paper Milling Company Limited, or Dongfang Paper. “IT Tech Packaging” refers to IT Tech Packaging, Inc. “VIE” or “Dongfang Paper” refers to our variable interest entity in China. “Baoding Shengde” refers to our wholly-owned subsidiary, Baoding Shengde Paper Co., Ltd, a PRC company. “Qianrong”, refers to our indirect wholly-owned subsidiary, QianrongQianhui Hebei Technology Co., Ltd, a PRC company. “Tengsheng Paper” refers to the subsidiary of Dongfang Paper, Hebei Tengsheng Paper Co., Ltd., a PRC company.

All references to “PRC” or “China” refers to the People’s Republic of China, including, for the purpose of this annual report, Taiwan, Hong Kong and Macau; all references to “RMB” or “Renminbi” refer to the legal currency of China; all references to “US$,” “dollars,” “U.S. dollars” and “$” refer to the legal currency of the United States.

This annual report on Form 10-K includes our audited consolidated statements of income and comprehensive income and our audited consolidated balance sheets as of December 31, 2023 and 2022.

FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K contains “forward-looking statements.” These statements are made under the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. You can identify these forward-looking statements by terms such as “may,” “will,” “expects,” “anticipates,” “future,” “intend,” “plan,” “believe,” “estimate,” “is/are likely to” and similar expressions. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements. Factors that could cause or contribute to such differences in results and outcomes include, without limitation, our anticipated revenues from the corrugating medium paper business segment and offset printing paper business, our ability to implement the planned capacity expansion of tissue paper, our ability to introduce new products, market acceptance of new products, general economic and business conditions, the ability to attract or retain qualified senior management personnel and research and development staff, and those specifically addressed under the headings “Risks Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” The forward-looking statements made in this annual report relate only to events as of the date on which the statements are made. We undertake no obligation, beyond any than as required by law, to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made, even though our situation changes in the future.

We operate in an emerging and evolving environment. New risk factors emerge from time to time and it is impossible for our management to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statement.

ii

PART I

Item 1. Business

IT Tech Packaging, Inc. (the “Company,” “IT Tech Packaging,” or “ITP”) is not an operating company but a Nevada holding company with operations primarily conducted by its subsidiaries and through contractual arrangements with Hebei Baoding Dongfang Paper Milling Company Limited, a People’s Republic of China company (“Dongfang Paper”), the variable interest entity, or VIE, based in China. IT Tech Packaging operated its business in China through its wholly-owned PRC subsidiaries, namely Baoding Shengde Paper Co., Ltd., a People’s Republic of China company (“Baoding Shengde”) and QianrongQianhui Hebei Technology Co., Ltd., a People’s Republic of China company (“Qianrong”) (together with Baoding Shengde, the “PRC Subsidiaries”), and Dongfang Paper, which we refer to as our VIE in this annual report, and rely on contractual arrangements that establish the VIE structure among Baoding Shengde, the VIE and VIE’s shareholders to operate our business in China.

IT Tech Packaging is a Nevada holding company with no operations of its own. Operations in China are primarily conducted through Dongfang Paper, the consolidated VIE. Dongfang Paper is consolidated for accounting purposes but is not an entity in which you own equity.

Investors in our common stock should be aware that they may never directly hold equity interests in the Chinese operating entities, but rather purchasing equity solely in IT Tech Packaging Inc., our Nevada holding company, which does not directly own substantially all of our business in China conducted by our PRC Subsidiaries and VIE. As a holding company with no material operations of our own, we conduct our operations through the VIE established in the PRC. We do not have any equity ownership of the VIE; instead, we control and receive the economic benefits of the VIE’s business operations through the VIE Agreements, and we consolidate the VIE for accounting purposes only because we met the conditions under the U.S. GAAP to consolidate the VIE. The VIE Agreements are used to provide contractual exposure to foreign investment in China-based companies where Chinese law prohibits direct foreign investment in the Chinese operating companies. Pursuant to the VIE Agreements, the VIE pays service fees equal to 80% of its total annual net profits to Baoding Shengde, while Baoding Shengde has the power to direct the activities of the VIE that can significantly impact the VIE’s economic performance and has the right to receive substantially all of the economic benefits of the VIE. Such contractual arrangements are designed so that the operations of the VIE are solely for the benefit of Baoding Shengde and ultimately, ITP. As such, under the U.S. GAAP, ITP is deemed to have a controlling financial interest in, and be the primary beneficiary of, the VIE for accounting purposes and must consolidate the VIE.

As a result of the prohibitions on direct investments by foreign enterprises, we conduct our production and distribution of paper products and medical face masks in China primarily through a series of VIE Agreements among Baoding Shende, the VIE and the VIE’s shareholders. Substantially all of the VIE’s operations are conducted in China in the paper making industry, over which the Chinese government exercises significant oversight and discretion. Due to PRC legal restrictions on foreign ownership in the paper making industry, ITP is unable to own any equity interest in the consolidated VIE. The VIE structure is used to provide investors with exposure to foreign investment in China-based companies where PRC laws restrict direct foreign investment in certain aspects of the paper making industry in which the VIE operates. As a result, you are not directly investing in and may never hold equity interests in the VIE in China. The VIE structure involves unique risks to investors. The VIE Agreements have not been tested in a court of law and may not be effective in providing control over the VIE as would direct equity ownership. We are subject to risks due to the uncertainty of the interpretation and application of the laws and regulations of the PRC regarding the consolidated VIE and the VIE structure, including, but not limited to, regulatory review of overseas listing of PRC companies through a special purpose vehicle and the validity and enforcement of the contractual arrangements with the consolidated VIE. We are also subject to the risk that the Chinese regulatory authorities could disallow the VIE structure, which could result in a material change in the operations of us, the consolidated VIE and the value of ITP’s securities could decline or become worthless.

We have evaluated the guidance in FASB ASC 810 and determined that the Baoding Shengde is the primary beneficiary of the VIE that is party to the relevant VIE Agreements for accounting purposes, because, pursuant to the VIE Agreements, shareholders of the VIE lack the right to receive any expected residual returns from the VIE, shareholders of the VIE lack the ability to make decisions about the activities of the VIE that have a significant effect on their operation and substantially all of the VIE’s businesses are conducted on behalf of ITP or its subsidiaries. Such contractual arrangements are designed so that the operations of the VIE are solely for the benefit of Baoding Shengde and, ultimately, ITP. ITP has indirect ownership in 100% of the equity in Baoding Shengde. Accordingly, under U.S. GAAP, we treat the VIE as a consolidated affiliated entity and have consolidated its financial results in our financial statements. As used in this annual report, “we,” “ITP,” “us,” “our company” and “our” refers to ITP and its subsidiaries, and, in the context of describing the operations and consolidated financial information, “we, the consolidated VIE and its subsidiary”.

1

We are also subject to legal and operational risks associated with being based in and having the majority of the Company’s operations in China. These risks may result in a material change in our operations, or a complete hindrance of our ability to offer or continue to offer our securities to investors, and could cause the value of such securities to significantly decline or become worthless. Recently, the PRC government initiated a series of regulatory actions and made a number of public statements on the regulation of business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using a VIE structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding efforts in anti-monopoly enforcement. We do not believe that these regulatory actions or statements impact our ability to conduct our business, accept foreign investments, or list on a U.S. or other foreign exchange. But because these statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies in China will respond to them, or what existing or new laws or regulations will be modified or promulgated, if any, or the potential impact such modified or new laws and regulations will have on the consolidated VIE’s daily business operations or ITP’s ability to accept foreign investments and remain listed on the NYSE American. For a description of relevant risks related to our corporate structure, see “Risk Factors – Risks Relating to Doing Business in China” and “Risk Factors – Risks Relating to Our Corporate Structure.”

Corporate History

IT Tech Packaging was incorporated in the State of Nevada on December 9, 2005, under the name “Carlateral, Inc.” Through the steps described below, we became the holding company with operations primarily conducted by our subsidiaries and our VIE, Dongfang Paper, a producer and distributor of paper products in China, on October 29, 2007. Effective on August 1, 2018, we changed our corporate name to “IT Tech Packaging, Inc.” The name change was effected through a parent/subsidiary short-form merger of IT Tech Packaging, Inc., our wholly-owned Nevada subsidiary formed solely for the purpose of the name change, with and into us. We were the surviving entity. In connection with the name change, our common stock began being traded under a new NYSE symbol, “ITP,” at such time.

On October 29, 2007, pursuant to an agreement and plan of merger (the “Merger Agreement”), the Company acquired Dongfang Zhiye Holding Limited (“Dongfang Holding”), a corporation formed on November 13, 2006 under the laws of the British Virgin Islands, and issued the shareholders of Dongfang Holding an aggregate of 7,450,497 (as adjusted for a four-for-one reverse stock split effected in November 2009) shares of our common stock, which shares were distributed pro-rata to the shareholders of Dongfang Holding in accordance with their respective ownership interests in Dongfang Holding. At the time of the Merger Agreement, Dongfang Holding owned all of the issued and outstanding stock and ownership of Dongfang Paper and such shares of Dongfang Paper were held in trust with Zhenyong Liu, Xiaodong Liu and Shuangxi Zhao, for Mr. Liu, Mr. Liu and Mr. Zhao (the original shareholders of Dongfang Paper) to exercise control over the disposition of Dongfang Holding’s shares in Dongfang Paper on Dongfang Holding’s behalf until Dongfang Holding successfully completed the change in registration of Dongfang Paper’s capital with the relevant PRC Administration of Industry and Commerce as the 100% owner of Dongfang Paper’s shares. As a result of the merger transaction, Dongfang Holding became a wholly owned subsidiary of the Company, and Dongfang Holding’s wholly owned subsidiary, Dongfang Paper, became an indirectly owned subsidiary of the Company.

Dongfang Holding, as the 100% owner of Dongfang Paper, was unable to complete the registration of Dongfang Paper’s capital under its name within the proper time limits set forth under PRC law. In connection with the consummation of the restructuring transactions described below, Dongfang Holding directed the trustees to return the shares of Dongfang Paper to their original shareholders, and the original Dongfang Paper shareholders entered into certain agreements with Baoding Shengde Paper Co., Ltd. (“Baoding Shengde”) to transfer the control of Dongfang Paper over to Baoding Shengde.

On June 24, 2009, the Company consummated a number of restructuring transactions pursuant to which it acquired all of the issued and outstanding shares of Shengde Holdings Inc., a Nevada corporation. Shengde Holdings Inc. was incorporated in the State of Nevada on February 25, 2009, and holds a wholly-owned subsidiary, Baoding Shengde, a limited liability company organized under the laws of the PRC on June 1, 2009. Because Baoding Shengde is a wholly-owned subsidiary of Shengde Holdings Inc., it is regarded as a wholly foreign-owned entity under PRC law.

2

Effective June 24, 2009, Baoding Shengde, Dongfang Paper and the original shareholders of Dongfang Paper entered into a number of contractual arrangements, as subsequently amended on February 10, 2010, pursuant to which Baoding Shengde acts as the management company for Dongfang Paper, and Dongfang Paper conducts the principal operations of the business. The contractual arrangements, as amended, effectively transferred the preponderance of the economic benefits of Dongfang Paper to Baoding Shengde, and as a result, Baoding Shengde assumed effective control and management over, is considered the primary beneficiary of Dongfang Paper for accounting purposes and we consolidate Dongfang Paper’s operating results in IT Tech Packaging’s financial statements under U.S. GAAP. The contractual arrangements, as amended, include the following:

| (i) | Exclusive Technical Service and Business Consulting Agreement |

The exclusive technical service and business consulting agreement, entered into by and between Baoding Shengde and Dongfang Paper, provides that Baoding Shengde shall provide exclusive technical, business and management consulting services to Dongfang Paper, in exchange for service fees including a fee equivalent to 80% of Dongfang Paper’s total annual net profits. The agreement is terminable upon mutual written agreement.

| (ii) | Call Option Agreement |

The call option agreement, entered into by and between Baoding Shengde, Dongfang Paper and the shareholders of Dongfang Paper, provides that the shareholders of Dongfang Paper irrevocably grant to Baoding Shengde an option to purchase all or part of each shareholder’s equity interest in Dongfang Paper. The exercise price for the options shall be RMB yuan for each of the shareholders’ equity interests, or if at any time there are PRC laws regulating the minimum exercise price of such options, then to the extent permitted under PRC Law. The call option agreement contains covenants from Dongfang Paper and its shareholders that they will refrain from taking certain actions without Baoding Shengde’s consent that would materially affect Dongfang Paper’s operations and asset value, including (i) supplementing or amending its articles of association or bylaws, (ii) changing Dongfang Paper’s registered capital or shareholding structure, (iii) selling, transferring, mortgaging or disposing of any interests in Dongfang Paper’s assets or income, or encumbering Dongfang Paper’s assets or income in a way that would approve a security interest on such assets, (iv) incurring or guaranteeing any debts not incurred in its normal business operations, (v) entering into any material contract or urging Dongfang Paper management to dispose of any Dongfang Paper assets, unless it is within the company’s normal business operations; (vi) providing any loan or guarantee to any third party; (vii) appointing or removing any management personnel or directors that can be changed upon Dongfang Paper shareholder approval; (viii) declaring or distributing any dividends to the stockholders. The agreement remains effective until Baoding Shengde or its designees have acquired 100% of the equity interests of Dongfang Paper underlying the options.

| (iii) | Share Pledge Agreement |

The share pledge agreement entered into by and between Baoding Shengde, Dongfang Paper and the shareholders of Dongfang Paper, provides that the Dongfang Paper shareholders will pledge all of their equity interests in Dongfang Paper to Baoding Shengde as security for their obligations under the other management agreements described in this section. Specifically, Baoding Shengde is entitled to dispose of the pledged equity interests in the event that the Dongfang Paper shareholders or Dongfang Paper fails to pay the service fees to Baoding Shengde pursuant to the exclusive technical service and business consulting agreement or fails to perform their other obligations under the other management agreement. The agreement contains covenants from Dongfang Paper’s shareholders that they will refrain from taking certain actions without Baoding Shengde’s prior written consent, such as transferring or assigning their equity interests, or creating or permitting the creation of any pledges which may have an adverse effect on the rights or benefits of Baoding Shengde under the agreement. The Dongfang Paper shareholders also promise to comply with the laws and regulations relevant to the pledges under the agreement and to facilitate in good faith the protection of the ability of Baoding Shengde to exercise its rights under the agreement. The terms of the share pledge agreement remains in effect until all the obligations under the other management agreements have been fulfilled, whether or not the terms of the other management agreements have expired.

| (iv) | Proxy Agreement |

The proxy agreement, entered into by and between Baoding Shengde, Dongfang Paper and the shareholders of Dongfang Paper, provides that the Dongfang Paper shareholders shall irrevocably entrust a designee of Baoding Shengde with such shareholder’s voting rights and the right to represent such shareholder to exercise his or her rights at any shareholder’s meeting of Dongfang Paper or with respect to any shareholder action to be taken in accordance with the laws and Dongfang Paper’s Articles of Association. The terms of the agreement are binding on the parties for as long as the Dongfang Paper shareholders continue to hold any equity interest in Dongfang Paper. Dongfang Paper shareholder will cease to be a party to the agreement once it transfers its equity interests with the prior approval of Baoding Shengde.

3

On June 24, 2009, Zhao Tianqing, the sole shareholder of Shengde Holdings Inc., assigned to the Company, for good and valuable consideration, 100 shares representing 100% of the issued and outstanding shares of Shengde Holdings Inc. As a result of this assignment and the restructuring transactions described above, Shengde Holdings Inc., Baoding Shengde, and Dongfang Paper became directly and indirectly controlled by the Company, and Dongfang Paper continued to function as the Company’s operating entity.

In addition to controlling the operations and beneficial ownership of Dongfang Paper, Baoding Shengde also acquired a digital photo paper production line (including two photo paper coating lines and ancillary equipment) in an asset acquisition transaction on November 25, 2009 and began directly conducting business in the PRC. We suspended production of photo paper in June 2016 and now are upgrading the production line to produce more competitive photo paper products.

An agreement was entered into among Baoding Shengde, Dongfang Paper and the shareholders of Dongfang Paper on December 31, 2010, reiterating that Baoding Shengde is entitled to the distributable profit of Dongfang Paper, pursuant to the above mentioned Exclusive Technical Service and Business Consulting Agreement. In addition, Dongfang Paper and the shareholders of Dongfang Paper agreed that they would not declare any of Dongfang Paper’s unappropriated earnings, including any earnings of Dongfang Paper from its establishment to 2010 and thereafter, as dividend.

The contractual agreements described above have not been tested in a court of law.

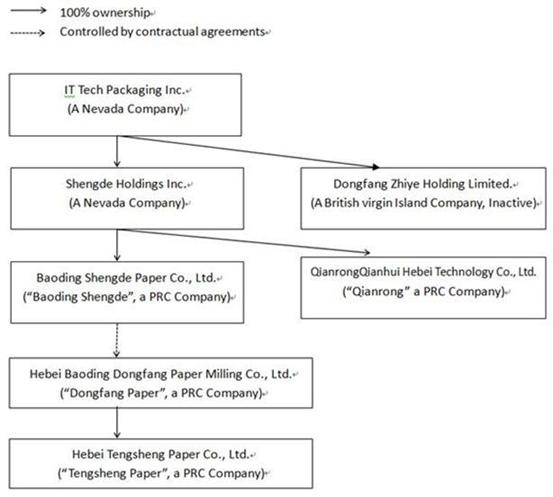

The diagram below illustrates our corporate structure and contractual arrangements with respect to each of our subsidiaries and consolidated VIE and the place of incorporation of each named entity as of the date of this annual report:

4

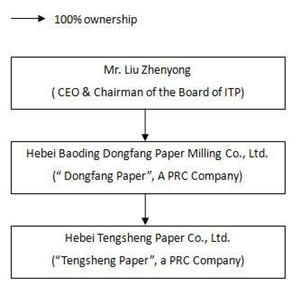

The following diagram sets forth the current ownership of Dongfang Paper:

Our subsidiaries and the VIE in which our operations are conducted include:

| ● | Baoding Shengde Paper Co., Ltd. (“Baoding Shengde”) is a PRC entity that is 100% indirectly owned by the Company. Baoding Shengde has entered into VIE agreements with the VIE identified below. |

| ● | Each of the following, which are PRC companies that are consolidated with the Company: |

1. Hebei Baoding Dongfang Paper Milling Co., Ltd. (“Dongfang Paper”) is a PRC entity that entered into VIE Agreements with Baoding Shengde; Dongfang Paper is the VIE.

| 2. | Hebei Tengsheng Paper Co., Ltd. (“Tengsheng”) is a PRC entity that is 100% owned by Dongfang Paper. |

| ● | QianrongQianHui Hebei Technology Co., Ltd. (“Qianrong”) is a PRC entity, incorporated on July 15, 2021, that is 100% indirectly owned by the Company. |

| ● | Shengde Holdings Inc., a Nevada company and our wholly-owned U.S. subsidiary, and Dongfang Zhiye Holding Limited, a British Virgin Islands company, are subsidiaries outside of China. Dongfang Zhiye Holding Limited has been inactive since 2010. |

5

Recent Regulatory Developments

On January 4, 2022, the Cyberspace Administration of China, or CAC, issued the revised Measures on Cyberspace Security Review (the “Revised Measures”), which came into effect on February 15, 2022. Under the Revised Measures, any “network platform operator” controlling personal information of no less than one million users which seeks to list in a foreign stock exchange should also be subject to cybersecurity review.

We do not believe we are “network platform operator” who control over one million personal information as mentioned above; as such, we believe we are currently not be subject to the cybersecurity review by the CAC. However, the definition of “network platform operator” is unclear and it is also unclear on how it will be interpreted and implemented by the relevant PRC governmental authorities. See “Risk factors — Risk Factors Relating to Doing Business in China — Our business may be subject to a variety of PRC laws and other obligations regarding cybersecurity and data protection.”

On July 6, 2021, the relevant PRC governmental authorities made public the Opinions on Strictly Cracking Down Illegal Securities Activities in Accordance with the Law. These opinions emphasized the need to strengthen the administration over illegal securities activities and the supervision on overseas listings by China-based companies and proposed to take effective measures, such as promoting the construction of relevant regulatory systems to deal with the risks and incidents faced by China-based overseas-listed companies. As these opinions are recently issued, official guidance and related implementation rules have not been issued yet and the interpretation of these opinions remains unclear at this stage. See “Risk Factors — Risk Factors Relating to Doing Business in China — While the approval and/or other requirements of the CSRC or other PRC governmental authorities are currently not required, they may be required, in connection with our oversea listing under PRC rules, regulations or policies, and, if required, we cannot predict whether or how soon we will be able to obtain such approval.” As of the date of this annual report, we have not received any inquiry, notice, warning, or sanctions regarding listing abroad or offshore offering from the CSRC or any other PRC governmental authorities.

We believe that we are currently not required to obtain any permission or approval from the China Securities Regulatory Commission (“CSRC”) and Cyberspace Administration of China (“CAC”) in the PRC to issue securities to foreign investors. However, there is no guarantee that this will continue to be the case in the future in relation to any future offerings of our company or the continued listing of our company’s securities on the NYSE American, or even in the event such permission or approval is required and obtained, it will not be subsequently revoked or rescinded. If we do not receive or maintain the approvals, or we inadvertently conclude that such approvals are not required, or applicable laws, regulations, or interpretations change such that we are required to obtain approval in the future, we may be subject to an investigation by competent regulators, fines or penalties, or an order prohibiting us from conducting an offering, and these risks could result in a material adverse change in our operations and the value of our securities, significantly limit or completely hinder our ability to offer or continue to offer securities to investors, or cause such securities to significantly decline in value or become worthless.

On February 17, 2023, the CSRC released the Trial Administrative Measures for Administration of Overseas Securities Offerings and Listings by Domestic Companies (the “Trial Measures”) and five supporting guidelines, which came into effect on March 31, 2023. Pursuant to the Trial Measures, domestic companies that seek to offer or list securities overseas, both directly and indirectly, should fulfill the filing procedures and report relevant information to the CSRC. If a domestic company fails to complete the filing procedures or conceals any material fact or falsifies any major content in its filing documents, such domestic company may be subject to administrative penalties by the CSRC, such as order to rectify, warnings, fines, and its controlling shareholders, actual controllers, the person directly in charge and other directly liable persons may also be subject to administrative penalties, such as warnings and fines. As a listed company, we believe that we, all of our PRC Subsidiaries, the consolidated VIE and its subsidiary are not required to fulfill filing procedures and obtain approvals from the CSRC to continue to offer our securities or operate business of the consolidated VIE and its subsidiary as of the date of this annual report. In addition, to date, none of us, our PRC Subsidiaries, the consolidated VIE and its subsidiary has received any filing or compliance requirements from CSRC for the listing of the Company at NYSE American and all of its overseas offerings. Furthermore, based on our understanding of the current PRC laws, we believe that the CSRC’s approval is not required to be obtained for the Company’s listing on NYSE American; however, there are substantial uncertainties regarding the interpretation and application of the Regulation on Mergers and Acquisitions of Domestic Companies by Foreign Investors (“M&A Rules”), other PRC Laws and future PRC laws and regulations, and there can be no assurance that any governmental agency will not take a view that is contrary to or otherwise different from our belief stated herein. See “Risk Factors — Risk Factors Relating to Doing Business in China — The CSRC has released the Trial Measures for Administration of Overseas Securities Offerings and Listings by Domestic Companies (the “Trial Measures”). While such rules have become into effect, the Chinese government may exert more oversight and control over offerings that are conducted overseas and foreign investment in China-based issuers, which could significantly limit or completely hinder our ability to continue to offer our securities to investors and could cause the value of our securities to significantly decline or become worthless”

6

On December 24, 2021, the Standing Committee of the National People’s Congress issued Law of the People’s Republic of China on the Prevention and Control of Noise Pollution (the “Prevention and Control of Noise Pollution Law”), which became effective on June 5, 2022. According to the Prevention and Control of Noise Pollution Law, entities subject to the pollutant discharge licensing management requirements shall not emit industrial noise without a pollutant discharge permit and shall prevent and control noise pollution according to the requirements of the pollutant discharge permit. The noise pollution has been included in the Pollution Discharge Permit, and we conduct quarterly test on the noise through qualified testing institutions to comply with the laws, which is required by laws.

Consolidation

We conduct substantially all of our business in China through contractual arrangements with Dongfang Paper, the VIE, due to PRC legal restrictions of foreign ownership in certain sectors. Substantially most of IT Tech Packaging’s revenues, costs and net income in China are directly or indirectly generated through the VIE. IT Tech Packaging, through Baoding Shengde, has signed various agreements with the VIE and shareholders of the VIE to allow the transfer of economic benefits from the VIE to Baoding Shengde and to direct the activities of the VIE.

Total assets and liabilities presented on IT Tech Packaging’s consolidated balance sheets and revenue, expense, net income presented on consolidated statement of operations and comprehensive income as well as the cash flow from operating, investing and financing activities presented on the consolidated statement of cash flows are substantially the financial position, operation and cash flow of the VIE. As of December 31, 2023, our variable interest entity accounted for an aggregate of 94.81% and 75.92% of our total assets and total liabilities. As of December 31, 2022, our variable interest entity accounted for an aggregate of 88.54% and 72.59% of our total assets and total liabilities. As of December 31, 2023 and 2022, $3,705,111 and $7,612,294 of cash and cash equivalents were denominated in RMB, respectively.

IT Tech Packaging and its directly owned subsidiary, Shengde Holding, do not have any substantial assets or liabilities or result of operations. The following table sets forth the assets, liabilities, results of operations and changes in cash, cash equivalents of the VIE, which were included in the Company’s consolidated balance sheets and statements of comprehensive income and statements of cash flows with intercompany transactions eliminated:

| As of | ||||||||

| December 31, | December 31, | |||||||

| 2023 | 2022 | |||||||

| Current assets | $ | 26,317,876 | $ | 33,832,930 | ||||

| Total non-current assets | $ | 158,555,747 | $ | 147,178,884 | ||||

| Total Assets | $ | 184,873,623 | $ | 181,011,814 | ||||

| Total liabilities | $ | 20,084,995 | $ | 16,784,877 | ||||

| For the Fiscal Year Ended | ||||||||

| December 31, | ||||||||

| 2023 | 2022 | |||||||

| Net cash provided by operating activities | $ | 17,444,376 | $ | 13,064,529 | ||||

| Net cash used in investing activities | $ | (22,239,297 | ) | $ | (7,494,805 | ) | ||

| Net cash provided by (used in) financing activities | $ | 3,965,631 | $ | (7,074,857 | ) | |||

7

Distributions and Other Transfers of Cash through our Organization

We are a holding company, although other means are available for us to obtain financing at the holding company level, we may receive dividends and other distributions on equity paid by our subsidiary established in China for our cash needs, including the funds necessary to pay dividends and other cash distributions to our shareholders to the extent we choose to do so, to service any debt we may incur and to pay our operating expenses. Our PRC Subsidiaries, consolidated VIE and its subsidiary in China are subject to restrictions on making dividends and other payments to us. Baoding Shengde’s income in turn depends on the service and other fees paid by the consolidated VIE and its subsidiary. ITP, its subsidiaries, the consolidated VIE and its subsidiary may also transfer cash to each other as part of the group cash management. If any of our subsidiaries, the consolidated VIE and its subsidiary incurs debt on its own behalf in the future, the instruments governing such debt may restrict their ability to pay dividends or make other payments to us. Current PRC regulations permit our PRC Subsidiaries in China to pay dividends to us only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. In addition, under the applicable requirements of PRC law, our PRC Subsidiaries, consolidated VIE and its subsidiary incorporated as companies may only distribute dividends after they have made allowances to fund certain statutory reserves. These reserves are not distributable as cash dividends.

IT Tech Packaging conducts its business operations in China through its PRC Subsidiaries and Dongfang Paper, the VIE. If needed, IT Tech Packaging can transfer cash to the PRC Subsidiaries through loans and/or capital contributions, and the PRC Subsidiaries can transfer cash to IT Tech Packaging through issuing dividends or other distributions. The PRC Subsidiaries can transfer cash to the VIE through intercompany loans and capital contributions, and the VIE can transfer cash to the PRC Subsidiaries as services fees under the VIE contractual arrangements. For the year ended December 31, 2023, the major cash flows occurred between IT Tech Packaging, its subsidiaries and the VIE included (i) loans in the total amount of $4,251,821 provided by Baoding Shengde to Tengsheng Paper; (ii) loans in the total amount of $2,834,547 from Baoding Shengde loans to Dongfang Paper; (iii) the payment in the amount of $5,491,139 made from Dongfang Paper to Baoding Shengde for purchase of raw materials; and (iv) funding through Shengde Holdings Inc. to Qianrong, with an amount of $500,000 as capital contributions. We do not have an established cash management policy that dictates how funds are transferred between us, our subsidiaries, consolidated VIE and its subsidiary. We do not, at this time, intend to distribute earnings or settle amounts owed under the VIE Agreements.

Current PRC regulations permit the PRC Subsidiaries to pay dividends to its shareholders only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. The PRC Subsidiaries are required to set aside 10% of its after-tax profits to fund a statutory reserve until such reserve reaches 50% of its registered capital if it distributes its after-tax profits for the current financial year. For details, see “Risk Factors — Risk Factors Relating to Doing Business in China — We may rely on dividends and other distributions on equity paid by our PRC subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our PRC Subsidiaries to make payments to us could have a material and adverse effect on our ability to conduct our business.” In addition, cash transfers from IT Tech Packaging are subject to applicable PRC laws and regulations on loans and direct investment. For details, see “Risk Factors — Risk Factors Relating to Doing Business in China — PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay us from making loans or additional capital contributions to our PRC Subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand our business.”

8

In addition, the PRC government imposes controls on the convertibility of the Renminbi into foreign currencies and, in certain cases, the remittance of currency out of China. IT Tech Packaging receives a significant portion of its revenues in Renminbi. Under IT Tech Packaging’s current corporate structure, IT Tech Packaging’s Nevada holding company may rely on dividend payments from the PRC Subsidiaries to fund any cash and financing requirements it may have. Under existing PRC foreign exchange regulations, payments of current account items, including profit distributions, interest payments and trade and service-related foreign exchange transactions, can be made in foreign currencies without prior approval of State Administration of Foreign Exchange, or SAFE, by complying with certain procedural requirements. However, approval from or registration with appropriate government authorities is required where Renminbi is to be converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of loans denominated in foreign currencies. As a result, we need to obtain SAFE approval to use cash generated from the operations of the PRC Subsidiaries and VIE to pay off their respective debt in a currency other than Renminbi owed to entities outside China, or to make other capital expenditure payments outside China in a currency other than Renminbi. If the foreign exchange control system prevents us from obtaining sufficient foreign currencies to satisfy our foreign currency demands, we may not be able to pay dividends in foreign currencies to its shareholders. See “Risk Factors — Risk Factors Relating to Doing Business in China — Governmental control of currency conversion may limit our ability to utilize our revenues effectively and affect the value of your investment”. In order to secure the amounts owed under the VIE agreements, the VIE and its shareholders entered into a share pledge agreement with Baoding Shengde, pursuant to which if the VIE fails to pay the service fees to the Baoding Shengde pursuant to the exclusive technical service and business consulting agreement or fails to perform their other obligations under the other management agreement, Baoding Shengde is entitled to dispose of the pledged equity interests in the VIE.

IT Tech Packaging declared and paid four quarterly cash dividends to its U.S. investors in April 2012 and November 2013. As of the date of this annual report, other than those cash dividends, none of IT Tech Packaging’s subsidiaries have ever issued any dividends or made other distributions to IT Tech Packaging or their respective holding companies nor has IT Tech Packaging or any of IT Tech Packaging’s subsidiaries ever paid dividends or made other distributions to U.S. investors. IT Tech Packaging currently intend to retain all future earnings to finance its operations and to expand its business. As a result, IT Tech Packaging does not expect to pay any cash dividends in the foreseeable future.

Holding Foreign Company Accountable Act (“HFCAA”)

Our common stock may be delisted from the NYSE American under the Holding Foreign Companies Accountable Act (“HFCAA”), if the PCAOB is unable to adequately inspect audit documentation located in China, or investigate our auditor. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which was signed into law on December 29, 2022, amends the HFCAA and requires the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years instead of three. Our auditor, GGF CPA Limited, is a China-based accounting firm registered with the PCAOB, and is subject to laws in the United States pursuant to which the PCAOB conducts regular inspections to assess its compliance with the applicable professional standards. On August 26, 2022, the PCAOB signed the Protocol with the CSRC and the MOF of the People’s Republic of China, governing inspections and investigations of audit firms based in mainland China and Hong Kong. The Protocol remains unpublished and is subject to further explanation and implementation. Pursuant to the fact sheet with respect to the Protocol disclosed by the SEC, the PCAOB shall have independent discretion to select any issuer audits for inspection or investigation and the unfettered ability to transfer information to the SEC. On December 15, 2022, the PCAOB announced that it was able to secure complete access to inspect and investigate PCAOB-registered public accounting firms headquartered in China mainland and Hong Kong completely in 2022. The PCAOB Board vacated its previous 2021 determinations that the PCAOB was unable to inspect or investigate completely registered public accounting firms headquartered in China mainland and Hong Kong. However, whether the PCAOB will continue to be able to satisfactorily conduct inspections of PCAOB-registered public accounting firms headquartered in China mainland and Hong Kong is subject to uncertainty and depends on a number of factors out of our, and our auditor’s control. The PCAOB is continuing to demand complete access in China mainland and Hong Kong moving forward and is already making plans to resume regular inspections in early 2023 and beyond, as well as to continue pursuing ongoing investigations and initiate new investigations as needed. The PCAOB has indicated that it will act immediately to consider the need to issue new determinations with the HFCAA if needed. Therefore, the PCAOB in the future may determine that it is unable to inspect or investigate completely registered public accounting firms in mainland China and Hong Kong. Our auditor’s working papers related to us and the consolidated VIE and its subsidiary are located in China. If our auditor is not permitted to provide requested audit work papers located in China to the PCAOB, investors would be deprived of the benefits of PCAOB’s oversight of our auditor through such inspections which could result in limitation or restriction to our access to the U.S. capital markets and trading of our securities may be prohibited under the HFCAA, which would result in the delisting of our securities from the NYSE American.

9

See “Risk Factors—Risks Associated with Our Company— Our common stock may be delisted from the NYSE American under the Holding Foreign Companies Accountable Act if the PCAOB is unable to adequately inspect audit documentation located in China. The delisting of our common stock, or the threat of their being delisted, may materially and adversely affect the value of your investment.”

Summary of Risk Factors

Investing in our securities involves significant risks and uncertainties. You should carefully consider all of the information in this annual report before making an investment in our securities. Below please find a summary of the principal risks we face, organized under relevant headings. These risks are discussed more fully in the section titled “Risk Factors.”

Risks Relating to our Business

| ● | Our operating history may not serve as an adequate basis to judge our future prospects and results of operations. |

| ● | Dongfang Paper and Baoding Shengde’s failure to compete effectively may adversely affect our ability to generate revenue. |

| ● | We may not be able to effectively control and manage our growth. |

| ● | We, through our subsidiaries, may engage in future acquisitions that could dilute the ownership interests of our stockholders and cause us to incur debt and assume contingent liabilities. |

| ● | We are responsible for the indemnification of our officers and directors. |

| ● | We are dependent on certain key personnel and loss of these key personnel could have a material adverse effect on our business, financial condition and results of operations. |

| ● | We may not be able to hire and retain qualified personnel to support our growth and if we are unable to retain or hire these personnel in the future, our ability to improve our products and implement our business objectives could be adversely affected. |

| ● | Our operating results may fluctuate as a result of factors beyond our control. |

| ● | We face risks related to product liability claims. |

| ● | Our operating results also depend on the availability and pricing of energy and raw materials. |

| ● | A material disruption at one of our manufacturing facilities could prevent us from meeting customer demand, reduce our sales, and/or negatively affect our net income. |

| ● | Our certificates, permits, and licenses related to our papermaking operations are subject to governmental control and renewal and failure to obtain renewal will cause all or part of our operations to be terminated. |

| ● | Compliance with environmental regulations is expensive, and noncompliance may result in adverse publicity and potentially significant monetary damages and fines or suspension of our business operations. |

10

| ● | If we are unable to respond to pricing pressures, our business may be harmed. |

| ● | If we fail to introduce enhancements to our existing products or to develop new products, our business and results of operations could be adversely affected. |

| ● | We have limited insurance coverage and may incur losses resulting from product liability claims or business interruptions. |

| ● | Our failure to protect our intellectual property rights may undermine our competitive position, and external infringements of our intellectual property rights may adversely affect our business. |

| ● | We may be subject to intellectual property infringement claims or other allegations, which may materially and adversely affect our business, financial condition and prospects. |

Risks Related To Doing Business in the PRC

| ● | The PRC government has significant oversight and discretion over the conduct of a PRC company’s business operations or to exert control over any offering of securities conducted overseas and/or foreign investment in China-based issuers, and may intervene with or influence our operations, may limit or completely hinder our ability to offer or continue to offer securities to investors, and may cause the value of such securities to significantly decline or be worthless, as the government deems appropriate to further regulatory, political and societal goals. |

| ● | The CSRC has released the Trial Measures for Administration of Overseas Securities Offerings and Listings by Domestic Companies (the “Trial Measures”). While such rules have become into effect, the Chinese government may exert more oversight and control over offerings that are conducted overseas and foreign investment in China-based issuers, which could significantly limit or completely hinder our ability to continue to offer our securities to investors and could cause the value of our securities to significantly decline or become worthless. |

| ● | Recent greater oversight by the Cyberspace Administration of China, or the “CAC,” over data security, particularly for companies seeking to list on a foreign exchange, could adversely impact the business of us, the consolidated VIE and its subsidiary and investing in our securities. |

| ● | The occurrence of security breaches and cyber-attacks could negatively impact our business. |

| ● | Our business may be subject to a variety of PRC laws and other obligations regarding cybersecurity and data protection. |

| ● | Changes in the policies of the PRC government could have a significant impact upon the business we may be able to conduct in the PRC and the profitability of such business. |

| ● | The PRC laws and regulations governing our current business operations are sometimes vague and uncertain. Any changes in such PRC laws and regulations may harm our business. |

| ● | A slowdown, inflation or other adverse developments in the PRC economy may harm our customers and the demand for our services and products. |

| ● | Our PRC Subsidiaries, consolidated VIE and its subsidiary in China are subject to restrictions on making dividends and other payments to us or any other affiliated company. |

| ● | We may rely on dividends and other distributions on equity paid by our PRC subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our PRC Subsidiaries to make payments to us could have a material and adverse effect on our ability to conduct our business. |

| ● | Governmental control of currency conversion may limit our ability to utilize our revenues effectively and affect the value of investors’ investment. |

11

| ● | PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay us from making loans or additional capital contributions to our PRC Subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand our business. |

| ● | The fluctuation of the Renminbi may harm your investment. |

| ● | Failure to comply with PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may materially adversely affect us. |

| ● | While the approval and/or other requirements of the CSRC or other PRC governmental authorities are currently not required, they may be required, in connection with our oversea listing under PRC rules, regulations or policies, and, if required, we cannot predict whether or how soon we will be able to obtain such approval. |

| ● | The M&A Rules and certain other PRC regulations establish complex procedures for some acquisitions of Chinese companies by foreign investors, which could make it more difficult for us to pursue growth through acquisitions in China. |

| ● | The PRC’s legal and judicial system may not adequately protect our business and operations and the rights of foreign investors. |

| ● | Because our principal assets are located outside of the United States and most of our directors and officers reside outside of the United States, it may be difficult for you to effect service of legal process, enforce your rights based on U.S. federal securities laws against us and our officers or to enforce U.S. court judgment against us or them in the PRC. |

| ● | It may be difficult for overseas regulators to conduct investigation or collect evidence within China. |

| ● | We may be required to broaden the coverage of the mandatory social security insurance programs under the Labor Law of the PRC. |

| ● | The current tensions in international trade and rising political tensions, particularly between U.S. and China, may adversely impact our business, financial condition, and results of operations. |

Risks Related to Our Corporate Structure

| ● | Our current corporate structure and business operations may be affected by the newly enacted Foreign Investment Law. |

| ● | Any failure by our consolidated VIE or their shareholders to perform their obligations under our contractual arrangements with them would have a material adverse effect on our business. |

| ● | In order to comply with PRC regulatory requirements, we operate our businesses through companies with which we have contractual relationships but in which we do not have controlling ownership. |

| ● | Because we rely on the consulting services agreement with Dongfang Paper for essentially all of our revenue and cash flows, any difficulty for Dongfang Paper to pay consulting fees to Baoding Shengde under the consulting agreement may have a material adverse effect on our operations. |

| ● | If the PRC government determines that the contractual agreements constituting part of our VIE structure do not comply with applicable PRC regulations, or if these regulations change or are interpreted differently in the future, we may be unable to assert our contractual rights over the assets of the VIE, and our common stock may decline in value. |

| ● | The contractual arrangements under a VIE Structure may not be as effective as direct ownership in respect of our relationship with the VIE, and thus, we may incur substantial costs to enforce the terms of the arrangements, which we may not be able to enforce at all. |

| ● | The shareholders of Dongfang Paper may have actual or potential conflicts of interests with us, which may adversely affect our business. |

12

| ● | We may lose the ability to use and enjoy assets held by the VIE that are material to the operation of our business if the entity goes bankrupt or becomes subject to a dissolution or liquidation proceeding. |

| ● | Our arrangements with Dongfang Paper and its shareholders may be subject to a transfer pricing adjustment by the PRC tax authorities which could have an adverse effect on our income and expenses. |

| ● | We may lose the ability to use, or otherwise benefit from, the licenses, approvals and assets held by the VIE, which could severely disrupt our business, render us unable to conduct some of our business operations and constrain our growth. |

| ● | The exercise of our option to purchase part or all of the equity interests in Dongfang Paper under the Call Option Agreement might be subject to approval by the PRC government. Our failure to obtain this approval may impair our ability to substantially control Dongfang Paper and could result in actions by Dongfang Paper that conflict with our interests. |

Risks Related to Our Common Stock

| ● | Our common stock may be delisted from the NYSE American under the Holding Foreign Companies Accountable Act if the PCAOB is unable to adequately inspect audit documentation located in China. The delisting of our common stock, or the threat of their being delisted, may materially and adversely affect the value of your investment.. |

| ● | If we fail to comply with Section 404 of the Sarbanes-Oxley Act of 2002 in a timely manner, our business could be harmed and our stock price could decline. |

| ● | If we become directly subject to the scrutiny involving U.S. listed Chinese companies, we may have to expend significant resources to investigate and/or defend the matter, which could harm our business operations, stock price and reputation. |

| ● | Our officers and directors control us through their positions and stock ownership and their interests may differ from other stockholders. |

| ● | We may not continue to pay cash dividends and any return on investment may be limited to the value of our common stock. |

| ● | Our common stock may be affected by limited trading volume and may fluctuate significantly. |

| ● | Future financings may dilute stockholders or impair our financial condition. |

13

Our Business

We, through our PRC Subsidiaries and VIE, engage in production and distribution of three categories of paper products: corrugating medium paper, offset printing paper, tissue paper products and medical face masks in China.

Our principal executive offices are located at Science Park, Juli Road, Xushui District, Baoding City, Hebei Province, People’s Republic of China.

Our telephone number is (86) 312-869-8215. Our website is located at https://www.itpackaging.cn.

Manufacturing Process

Corrugating Medium Paper and Offset Printing Paper

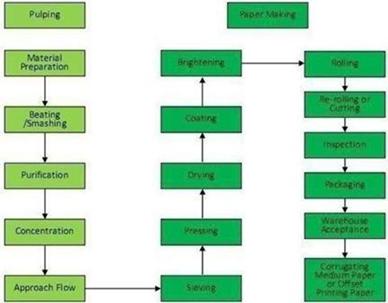

Our current products (excluding tissue paper products) generally undergo two stages of manufacturing: (1) creating pulp from recycled paper products, and (2) treating the pulp and molding it into the desired types of paper products. A brief overview of the pulp and papermaking process is provided below.

Pulping

The recycled waste paper is first sorted by machine, and then broken down and beaten or smashed into small pieces using water and mechanical energy. It is then put through a course screening drum, followed by a fine screening drum to separate different grades of pulp, a process that we refer as “concentration”. In order to purify the pulp further, an approach flow system is used to filter out any impurities or inconsistencies, such as sand, in the pulp.

Paper Making

The pulp is sieved to remove the excess water and molded into a specific size. The moisture content is further reduced by applying hydraulic pressure to the pulp. The pulp then enters the drying section where it is rolled over by heated cylinders. The dried paper is then coated with a mixture of clay, white pigment and binder to produce a surface on which ink can sit without being fully absorbed, enabling crisper, and more consistent print quality.

The paper goes through a process called calendaring, which flattens and smoothens the paper into long sheets. The paper is then wound onto a reel that is mounted in a roll-slitting machine for rewinding, during which cutters are used to cut the paper into the desired widths. Upon completion, the rolls are fitted with sleeves and labeled, and then sent to quality control before shipment or storage.

14

Base Tissue Paper

While we make tissue paper products, we currently purchase paper pulp from suppliers and use it to manufacture base tissue paper directly.

Products

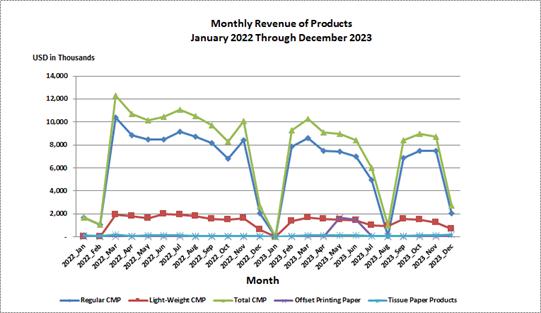

Corrugating medium paper

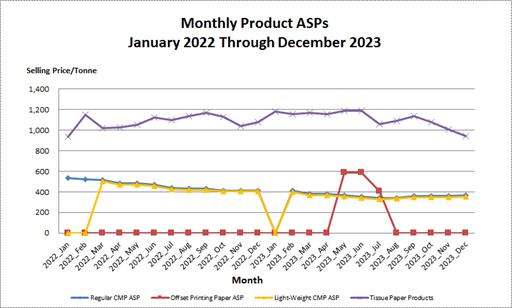

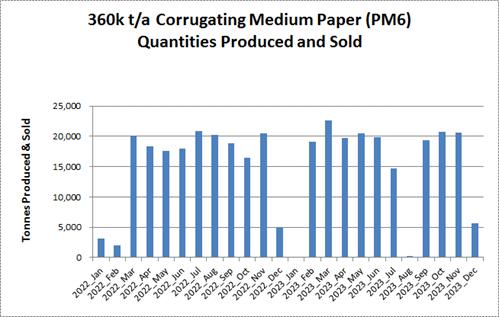

Corrugating medium paper, or CMP is used in the manufacturing of cardboard. Since the launch of our new Paper Machine (“PM6”) production line in December 2011, corrugating medium paper has become a major product of the Company. For the year ended December 31, 2023, corrugating medium paper comprised approximately 97.06% of our total paper production quantities and roughly 94.47% of our total revenue. Raw materials used in the production of corrugating medium paper include recycled paper board (or Old Corrugating Cardboard or “OCC,” as it is commonly referred to in the United States) and certain supplementary agents. In January 2013, we suspended the operation of our PM1 production line for renovation, which was then used to produce corrugating medium paper. In May 2014, we launched the commercial production of a renovated PM1 production line. The renovated PM1 production line produces light-weight corrugating medium paper with a specification of 40 to 80 grams per square meter (“g/s/m”). PM1’s light-weight corrugating medium paper products have a wide range of commercial applications. For example, they can be used as a construction material for wall and floor insulation or to manufacture moisture-proof packaging materials for the transportation of books and magazines by the publishing industry. It can also be used as corrugating medium to make corrugating cardboard for packaging that requires light-weight boxes. The manufacturing process of light-weight corrugating medium paper is similar to that of the regular corrugating medium paper and also uses recycled paper boards as a major source of raw material. We now have two corrugating medium paper production lines, PM6 and PM1. We refer to products produced from the PM6 production line as Regular CMP and products produced from the PM1 production line as Light-Weight CMP.

Offset printing paper

Offset printing paper is used for offset printing in the publishing industry. Revenue from offset printing paper was $3,215,190 with 5,573 tonnes sold for the year ended December 31, 2023. Raw materials used in making offset printing paper include recycled white scrap paper, fluorescent whitening agent and sizing agent. We currently have two production lines, PM2 and PM3, for the production of offset printing paper.

Tissue Paper Products

We began the commercial production of tissue paper products in Wei County Industry Park in June 2015. We process base tissue paper purchased from long-term cooperative third party and produce finished tissue paper products, including toilet paper, boxed and soft-packed tissues, handkerchief tissues and paper napkins, as well as bathroom and kitchen paper towels that are marketed and sold under the Dongfang Paper brand. In December 2018 and November 2019, we completed the construction, installation and test of operation of PM8 and PM9, respectively, and commercially launched tissue paper production of PM8 and PM9 at such time. On May 5, 2020, the Company announced it planned the commercial launch of a new tissue paper production line PM10 and the Company entered into an agreement to purchase paper machine with paper machine supplier. The Company expected the new tissue paper production line to be launched after the completion of trial run. The machine supplier was delayed because of pandemic. We are closely following up the provider for further actions. Tissue paper products comprised approximately 0.52% of our total paper production quantities and approximately 1.51% of our total sales revenue for the year ended December 31, 2023.

Face Masks

On April 29, 2020, we launched a production line of non-medical single-use face masks, following the completion of raw materials preparation, trial run of the equipment and the sample products inspection. In May 2021, the Company obtained the license for its new single-use surgical masks from local food and drug administration in Hebei province, and began commercial production in November 2021.

15

Market for our Products

The PRC Paper Making Industry

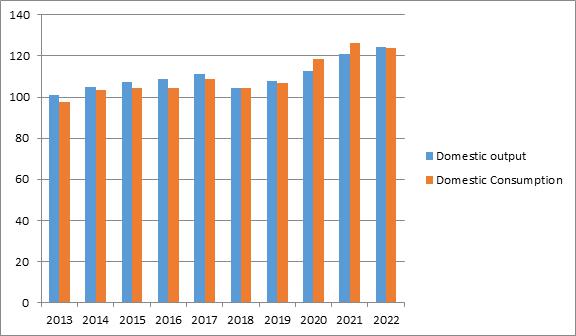

According to the 2022 China Paper Industry Annual Report, issued by the China Paper Association, there were approximately 2,500 paper and paper board manufacturers in China, with a total output of 124.25 million tonnes, up by 2.64% from 121.05 million tonnes in 2021. Total domestic consumption was 124.03 million tonnes in 2022, down by 1.94% from 126.48 million tonnes in 2021.

The output of paper and paper board maintained an average growth rate of approximately 2.32% during the ten-year period from 2013 to 2022, while consumption increased at an average annual rate of 2.67%. The growth is expected to continue. It is estimated that China currently has the largest paper and paper board products output and consumption in the world. (Data source: 2022 Annual Report of China Paper Manufacturing, May 2023,China Paper Association)

Unit: Million tons

Data source: 2022Annual Report of China’s Paper Industry, May 2023, China Paper Association

Corrugating medium paper production in China totaled 27.70 million tonnes in 2022, a 3.17% increase from 2021. Consumption of corrugating medium paper in China amounted to 30.10 million tonnes in 2022, an increase of 1.11% as compared to 2021.

Uncoated offset printing paper production in China totaled 17.35 million tonnes in 2022, a 0.87% increase from 2021. Consumption of uncoated offset printing paper in China amounted to 16.78 million tonnes in 2022, a decrease of 6.41% as compared to 2021.

The paper making industry in China is concentrated in the east coast provinces. The largest paper production capacities by province for 2022 and 2021 (the most recent year for which relevant information is available) are summarized in the table below. The three provinces with largest capacities showed moderate decreases in paper production capacities.

| 2022 Capacity | 2021 Capacity | % | ||||||||||

| Province | (10k tonnes) | (10k tonnes) | Change | |||||||||

| Shandong | 2,015 | 2,035 | (0.98 | ) | ||||||||

| Guangdong | 1,969 | 1,970 | (0.05 | ) | ||||||||

| Jiangsu | 1,373 | 1,415 | (2.97 | ) | ||||||||

| Zhejiang | 1,193 | 1,050 | 13.62 | |||||||||

| Fujian | 821 | 845 | (2.84 | ) | ||||||||

| Henan | 715 | 672 | 6.40 | |||||||||

| Hubei | 592 | 570 | 3.86 | |||||||||

| Guangxi | 559 | 423 | 65.88 | |||||||||

| Chongqing | 408 | 423 | (3.55 | ) | ||||||||

| Hebei | 378 | 408 | (7.35 | ) | ||||||||

Data Sources: 2022 Annual Report of China’s Paper Industry, May 2023, China Paper Association

16

Customers

We generally sell our corrugating medium paper to companies making corrugating cardboards and offset printing paper to printing companies. Our largest customer is a packaging company in Hebei Province. Our total corrugating medium and offset printing paper revenue in 2023 was primarily derived from customers in Hebei Province and Shandong Province.

For the year ended December 31, 2023, five major customers who individually accounted for more than 5% of our total sales revenue are as follows:

| 2023 | ||||||||

| Sales | ||||||||

| Amount | ||||||||

| (USD$, net of | % of | |||||||

| applicable | Total | |||||||

| VAT) | Revenue | |||||||

| Company A (Hebei) | 6,387,786 | 7.38 | % | |||||

| Company B (Shandong) | 6,167,272 | 7.13 | % | |||||

| Company C (Hebei) | 6,097,717 | 7.05 | % | |||||

| Company D (Shandong) | 6,085,824 | 7.03 | % | |||||

| Company E (Tianjin) | 6,006,103 | 6.94 | % | |||||

| Total Major Customers | 30,744,703 | 35.53 | % | |||||

Eight of our top-ten customers of 2023 are also in the top-ten customer list in 2022, representing 85.66% of the 2022 top-ten customer sales.

Target Market

We target corporate customers in the middle range of the marketplace, where, with solid quality and competitive pricing, we see potential for high volume growth for corrugating medium paper and offset printing paper. Our primary market has been the region of North China, especially in the province of Hebei.

Our Production Lines

During the year ended December 31, 2023, we had six PM production lines in operation and are in the process of launching one more that is designated as PM7. These production lines include the followings:

| Paper Product | Designed Capacity | |||||||||

| PM# | Produced | (tonnes/year) | Owned by | Operated by | Status as of December 31, 2023 | |||||

| PM1 | Corrugating Medium Paper | 60,000 | Dongfang Paper | Dongfang Paper | In production | |||||

| PM2 | Offset Printing Paper | 50,000 | Dongfang Paper | Dongfang Paper | In production | |||||

| PM3 | Offset Printing Paper | 40,000 | Dongfang Paper | Dongfang Paper | In production | |||||

| PM4 | Digital Photo Paper | ** | Baoding Shengde | Baoding Shengde | Suspended in June 2016 due to low market demand | |||||

| PM5 | Digital Photo Paper | ** | Baoding Shengde | Baoding Shengde | Suspended in June 2016 due to low market demand | |||||

| PM6 | Corrugating Medium Paper | 360,000 | Baoding Shengde | Dongfang Paper*** | In production | |||||

| PM7* | Specialty paper | 10,000 | Dongfang Paper | Dongfang Paper | In renovation | |||||

| PM8 | Tissue paper | 15,000 | Dongfang Paper | Dongfang Paper | In production | |||||

| PM9 | Tissue paper | 15,000 | Dongfang Paper | Dongfang Paper | In production. | |||||

| PM10 | Tissue paper | 20,000 | Dongfang Paper | Dongfang Paper | In construction |

| *: | Paper machines under renovation, under construction, or in the planning stage. |

| ***: | PM6 is funded and owned by Baoding Shengde; ancillary facilities that support the PM6 operation are built and owned by Dongfang Paper. |

17

On December 31, 2009, we acquired a digital photo paper production line, including two coating lines that are designated as PM4 and PM5 and ancillary equipment, for a total purchase price of approximately $13.6 million. We suspended production of photo paper in June 2016.

In order to meet the growing domestic demand for paper, which we believe currently exceeds domestic supply in the case of corrugating medium paper, especially in the region of North China, we installed a corrugating medium paper production line (PM6) with a designed capacity of 360,000 tonnes per year. We completed the installation of the PM6 production line in November 2011 and began commercial production in December 2011.

We have implemented a plan to renovate one of the old production lines that has been idle since the end of 2007. We previously made paper with anti-counterfeit features from that production line. When the renovation is completed, we intend to use the renovated production line to produce high-profit margin specialty papers.

On November 27, 2012, we signed a 15-year lease relating to approximately 49.4 acres of land in the Economic Development Zone in Wei County, Hebei Province, China for the purpose of developing a new tissue paper production plant. We planned to build two tissue paper production lines, each with 15,000 tonnes/year capacity, and other packaging facilities and infrastructures on the leased land. In December 2012, we signed a contract with an equipment contractor in Shanghai to build PM8, the first of our two tissue paper production lines in Wei County. In December 2018 and November 2019, we completed the construction, installation and test of operation of PM8 and PM9, respectively and commercially launched tissue paper productions of PM8 and PM9 at such time. On May 5, 2020, the Company announced it planned the commercial launch of a new tissue paper production line PM10 and the Company signed an agreement to purchase paper machine with paper machine supplier. The Company expected the new tissue paper production line to be launched after the completion of trial run.

We voluntarily renovated our 150,000 tonnes/year corrugating medium paper PM1 in anticipation of increased regulatory concerns on energy efficiencies as well as to improve the quality of our corrugating medium products. Rather than converting PM1 to a regular corrugating medium paper machine, we decided in 2013 that, based on the market conditions and our waste water treatment capability, the better option was to convert PM1 to produce Light-Weight CMP with a specification of 40 to 80 grams per square meter (“g/s/m”) with a designed capacity of 60,000 tonnes/year. We started the renovation in January 2013 and launched commercial production of the renovated PM1 production line in May 2014.

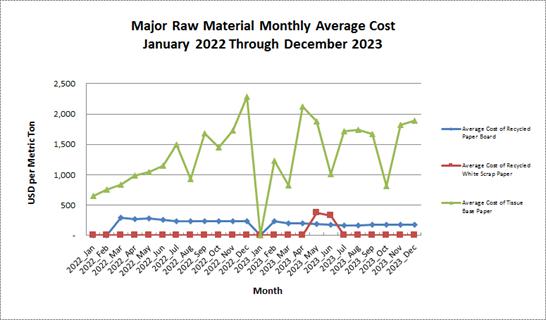

Raw Materials and Principal Suppliers

The supplies used in our production processes are comprised mainly of recycled paper board and unprinted recycled white scrap paper, both of which are ready-to-use items and available from multiple domestic and foreign sources. We currently purchase all of our recycled paper supplies from some domestic recycling stations and do not rely on imported recycled paper. We also purchase gas and chemical agents from nearby suppliers. Ongoing inflationary pressures and higher demand for recycled paper could lead to an increase in our costs of raw materials and production, which we may or may not be able to pass to our customers.

We sign annual raw materials supplier contracts with our suppliers. Although we have contracts with our suppliers, these contracts do not lock-in the purchase price of our raw materials or provide hedge against the fluctuation in the market price of these raw materials. For the year ended December 31, 2023, we had two large suppliers which accounted for approximately 72% and 17% of our total purchases, respectively.

For the year ended December 31, 2023, three major suppliers who individually accounted for more than 5% of our total purchase are as follows:

| 2023 | ||||||||

| Purchase | % of | |||||||

| Amount | Total | |||||||

| (USD$) | Purchase | |||||||

| Company A (Hebei) | 56,159,754 | 72 | % | |||||

| Company B (Hebei) | 13,631,622 | 17 | % | |||||

| Company C (Hebei) | 5,034,368 | 6 | % | |||||

| Total Major Suppliers | 64,825,744 | 95 | % | |||||

18

Competition

Dongfang Paper’s main competitors are: Chenming Paper Group Limited, Huatai Group Limited, Nine Dragons Paper (Holdings) Limited and Sun Paper Group Limited. A number of our competitors are public entities with larger capacities, broader customer bases and greater financial resources than those available to us. The businesses of our primary competitors are briefly described below:

Chenming Paper Group, Ltd. (“Chenming”), based in Shandong Province (located in northeast China), produces primarily news print paper and art paper (high quality, heavy and two-side coated printing paper). Chenming is believed to be the first company to have listed on all three stock exchanges in China: Renminbi A-shares and foreign currency B-shares in Shenzhen, the smaller of the mainland’s two stock exchanges, and H-shares in Hong Kong. Chenming has annual production capacity of 8.5 million tonnes for its coated wood-free paper product and is believed to rank among the top 500 enterprises in China.

Huatai Group, Ltd. (“Huatai”), based in Shandong Province (located in the northern part of the eastern coastal region of China), primarily produces newsprint, fine paper, special printing paper, coated board and tissue paper. Huatai is the first Shandong papermaker to publicly list its stock and has become a famous brand in China. Its annual paper production is estimated to have reached 4 million tonnes.

Nine Dragons Paper (Holdings) Limited (“ND Paper”), based in Guangdong Province (located in southern China), is the largest paper manufacturer in China and primarily produces craft paper and high-strength corrugating medium paper with annual capacity of 13 million tonnes. ND Paper has reported that it has five production lines in the city of Tianjin with a total designed capacity of 2.15 million tonnes, producing products such as craft paper, high strength corrugating medium paper and grey-back duplex board.

Sun Paper Group, Ltd., based in Shandong Province, primarily produces card paper, whiteboard paper and art paper. It also produces alkaline peroxide mechanical pulp, sourced in part from wood chips harvested by the company’s poplar plantations. This company has reported that it has an aggregate annual production capacity of paper and pulp of approximately 5.7 million tonnes and has been listed on the Shenzhen Stock Exchange since 2006.