UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark one)

| ☒ | Quarterly Report Under Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the Quarterly Period Ended March 31, 2021

Or

| ☐ | Transition Report Under Section 13 or 15(d) of the Securities Exchange Act of 1934 |

Commission File Number 001-33672

PALISADE BIO, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 52-2007292 | |

| State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization | Identification No.) | |

| 5800 Armada Drive, Suite 210 | ||

| Carlsbad, California | 92008 | |

| (Address of principal executive offices) | (Zip Code) |

(858) 704-4900

(Registrant’s telephone number, including area code)

Seneca Biopharma, Inc. 20271 Goldenrod Lane Germantown, Maryland 20876 (Former Name and Address)

|

Securities registered pursuant to Section 12(b) of the Act:

| Title of Class | Trading Symbol | Name of Each Exchange on Which Registered |

| Common Stock, $0.01 par value | PALI | Nasdaq Capital Market |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☒ | Smaller reporting company ☒ |

Emerging Growth Company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) ☐ Yes ☒ No

As of May 5, 2021, there were 7,302,040shares of common

stock, $.01 par value, (not including 3,977,676 additional shares being held in escrow).

EXPLANATORY NOTE

On April 27, 2021, Seneca Biopharma, Inc. (“Seneca”) completed its previously announced merger transaction with Leading BioSciences, Inc. (“LBS”) in accordance with the terms of the Agreement and Plan of Merger, dated as of December 16, 2020 (the “Merger Agreement”), by and among Seneca, Townsgate Acquisition Sub 1, Inc., a wholly-owned subsidiary of Seneca (“Merger Sub”), and LBS, pursuant to which Merger Sub merged with and into LBS., with LBS. surviving as a wholly owned subsidiary of Seneca (the “Merger”). Immediately prior to the effective time of the Merger, LBS merged with and into Merger Sub. and LBS continued to exist as the surviving corporation. Concurrent with the closing of the Merger, on April 27, 2021 the Company effected a 1-for-6 reverse stock split of its common stock (“Reverse Stock Split”). Stockholders’ equity and all references to share and per share amounts in the accompanying consolidated financial statements have been retroactively adjusted to reflect the 1-for-6 reverse stock split for all periods presented. Immediately following the Merger, Seneca changed its name to “Palisade Bio, Inc.”

Unless the context otherwise requires, references to the “Company,” “Palisade,” the “combined organization,” “we,” “our” or “us” in this report refer to Palisade Bio, Inc. and its subsidiary after completion of the Merger. In addition, references to “Seneca” or refers to the registrant prior to the completion of the Merger.

| 1 |

Palisade Bio, Inc.

Table of Contents

| 2 |

FINANCIAL INFORMATION

| ITEM 1. | UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

See accompanying notes to unaudited condensed consolidated financial statements.

| 3 |

See accompanying notes to unaudited condensed consolidated financial statements.

| 4 |

| Preferred Stock Shares | Preferred Stock Amount | Common Stock Shares (see Note 1) | Common Stock Amount | Additional Paid-In Capital | Accumulated Other Comprehensive Income (Loss) | Accumulated Deficit | Total Stockholders' Equity | |||||||||||||||||||||||||

| Balance at January 1, 2021 | 200,000 | $ | 2,000 | 2,882,617 | $ | 28,826 | $ | 247,980,188 | $ | (734 | ) | $ | (238,242,364 | ) | $ | 9,767,916 | ||||||||||||||||

| Share-based payments | - | - | - | - | 247,993 | - | - | 247,993 | ||||||||||||||||||||||||

| Foreign currency translation adjustments | - | - | - | - | - | (2,042 | ) | - | (2,042 | ) | ||||||||||||||||||||||

| Net loss | - | - | - | - | - | - | (2,285,077 | ) | (2,285,077 | ) | ||||||||||||||||||||||

| Balance at March 31, 2021 | 200,000 | $ | 2,000 | 2,882,617 | $ | 28,826 | $ | 248,228,181 | $ | (2,776 | ) | $ | (240,527,441 | ) | $ | 7,728,790 | ||||||||||||||||

| 5 |

See accompanying notes to unaudited condensed consolidated financial statements.

| 6 |

PALISADE BIO, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2021 AND 2020

Note 1. Organization, Business and Financial Condition

Merger with Seneca Biopharma, Inc.

On April 27, 2021, Seneca Biopharma, Inc. (“Seneca”) completed its previously announced merger transaction with Leading BioSciences, Inc. (“LBS”) in accordance with the terms of the Agreement and Plan of Merger, dated as of December 16, 2020 (the “Merger Agreement”), by and among Seneca, Townsgate Acquisition Sub 1, Inc., a wholly-owned subsidiary of Seneca (“Merger Sub”), and LBS, pursuant to which Merger Sub merged with and into LBS., with LBS. surviving as a wholly owned subsidiary of Seneca (the “Merger”). Immediately prior to the effective time of the Merger, LBS merged with and into Merger Sub. and LBS continued to exist as the surviving corporation. Concurrent with the closing of the Merger, on April 27, 2021 the Company effected a 1-for-6 reverse stock split of its common stock (“Reverse Stock Split”). Stockholders’ equity and all references to share and per share amounts in the accompanying consolidated financial statements have been retroactively adjusted to reflect the 1-for-6 reverse stock split for all periods presented. Immediately following the Merger, Seneca changed its name to “Palisade Bio, Inc.”

Unless the context otherwise requires, references to the “Company,” “Palisade,” the “combined organization,” “we,” “our” or “us” in this report refer to Palisade Bio, Inc. and its subsidiary after completion of the Merger. In addition, references to “Seneca” or refers to the registrant prior to the completion of the Merger.

Prior to the Merger, LBS was incorporated as Leading Biosciences, Inc. under the laws of the State of Delaware on September 6, 2011, and is based in Carlsbad, California.

Nature of Business

Palisade Bio is a clinical-stage biopharmaceutical company focused on the discovery and development of innovative therapies to improve the lives of patients affected by a broad range of diseases and conditions triggered by gastrointestinal dysregulation. The Company is on the forefront of elucidating the role the gut plays in driving multiple disease states and conditions inside and outside the gastrointestinal tract. The Company is applying this knowledge and its industry experience to develop oral small-molecule drugs to maintain the integrity of the gut epithelial barrier, microbiome, and gut immune cells to improve acute and chronic Gastrobiome™-mediated outcomes. The Company’s initial focus is combatting the interruption of GI function (ileus) following major surgery to reduce recovery times and shorten patients’ length of stay in the hospital. The Company’s programs have the potential to prevent the formation of post-operative adhesions, as well as to address the myriad of health conditions and complications associated with chronic disruption of the intestinal mucosal barrier.

The following Unaudited Condensed Consolidated Financial Statements are representative of Seneca’s operations prior to the Closing and the adoption of LBS’s business plan and the commencement of conducting LBS’s business. The operations of our wholly-owned and controlled subsidiary located in the People’s Republic of China are consolidated in our condensed consolidated financial statements and all intercompany activity has been eliminated.

Liquidity and Going Concern

Financial Condition

Since our inception, we have financed our operations through the sales of our securities, issuance of long-term debt, the exercise of investor warrants, and to a lesser degree from grants and research contracts as well as the licensing of our intellectual property to third parties.

We had cash and cash equivalents of approximately $6.6 million at March 31, 2021.

Based on our expected operating cash requirements, we anticipate our current cash and investments on hand will be insufficient to fund our operations for more than 12 months after this filing. Accordingly, we will require additional capital to conduct our pre-clinical and clinical development programs and to fund our operations. Despite our ability to secure capital in the past, there can be no assurance that additional equity or debt financing will be available to us when needed or that we may be able to secure funding from any other sources. Consequently, management has determined that there is substantial doubt about our ability to continue as a going concern.

We will require additional capital to continue our pre-clinical and clinical development plans. To continue to fund our operations and the development of our product candidates we anticipate raising additional cash through the private and public sales of equity or debt securities, collaborative arrangements, licensing agreements, asset sales or a combination thereof. Although management believes that such funding sources will be available, there can be no assurance that any such collaborative arrangement will be entered into or that financing will be available to us when needed in order to allow us to continue our operations, or if available, on terms acceptable to us. If we do not raise sufficient funds in a timely manner, we may be forced to curtail operations, delay or stop our ongoing clinical trials, cease operations altogether, or file for bankruptcy. We currently do not have commitments for future funding from any source. We cannot assure you that we will be able to secure additional capital or that the expected income will materialize. Several factors will affect our ability to raise additional funding, including, but not limited to market conditions, interest rates and restrictions set forth in agreements between us and the investor in our pre-merger financing.

| 7 |

Impact of the COVID-19

The COVID-19 pandemic, which began in December 2019 and has spread worldwide, has caused many governments to implement measures to slow the spread of the outbreak. The outbreak and government measures taken in response have had a significant impact, both direct and indirect, on businesses and commerce, as worker shortages have occurred, supply chains have been disrupted, and facilities and production have been suspended. The future progression of the pandemic and its effects on the Company’s business and operations are uncertain. The COVID-19 pandemic may affect the Company’s ability to initiate and complete preclinical studies, delay its clinical trial or future clinical trials, disrupt regulatory activities, or have other adverse effects on its business and operations. The pandemic has already caused significant disruptions in the financial markets, and may continue to cause such disruptions, which could impact the Company’s ability to raise additional funds to support its operations. Moreover, the pandemic has significantly impacted economies worldwide and could result in adverse effects on the Company’s business and operations.

The Company continues to monitor the potential impact of the COVID-19 pandemic on its business and financial statements. To date, the Company has not experienced material business disruptions or incurred impairment losses in the carrying values of its assets as a result of the pandemic and it is not aware of any specific related event or circumstance that would require it to revise its estimates reflected in these consolidated financial statements. The extent to which the COVID-19 pandemic will directly or indirectly impact the Company’s business, results of operations and financial condition, including current and future clinical trials and research and development costs, will depend on future developments that are highly uncertain, including as a result of new information that may emerge concerning COVID-19, the actions taken to contain or treat it, and the duration and intensity of the related effects.

Note 2. Significant Accounting Policies and Basis of Presentation

Basis of Presentation

In management’s opinion, the accompanying interim unaudited condensed consolidated financial statements include all adjustments, consisting of normal recurring adjustments, which are necessary to present fairly Seneca’s financial position, results of operations and cash flows. The unaudited condensed consolidated balance sheet at December 31, 2020, has been derived from audited consolidated financial statements as of that date. The interim results of operations are not necessarily indicative of the results that may occur for the full fiscal year. Certain information and note disclosures normally included in the consolidated financial statements prepared in accordance with generally accepted accounting principles in the United States of America (“U.S. GAAP”) have been condensed or omitted pursuant to instructions, rules and regulations prescribed by the U.S. Securities and Exchange Commission (“SEC”). Seneca believes that the disclosures provided herein are adequate to make the information presented not misleading when these unaudited condensed consolidated financial statements are read in conjunction with the Financial Statements and Notes included in Seneca’s Annual Report on Form 10-K for the year ended December 31, 2020, filed with the SEC, and as may be amended.

Use of Estimates

The preparation of financial statements in accordance with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. The unaudited condensed consolidated financial statements include significant estimates for the expected economic life and value of Seneca’s licensed technology and related patents, Seneca’s net operating loss and related valuation allowance for tax purposes, the fair value of Seneca’s liability classified warrants and Seneca’s share-based compensation related to employees and directors, consultants and advisors, among other things. Because of the use of estimates inherent in the financial reporting process, actual results could differ significantly from those estimates.

Fair Value Measurements

The carrying amounts of our short-term financial instruments, which primarily include cash and cash equivalents, accounts payable and accrued expenses, approximate their fair values due to their short maturities. The fair values of Seneca’s liability classified warrants were estimated using Level 3 unobservable inputs. See Note 3 for further details.

Foreign Currency Translation

The functional currency of the combined organization’s wholly owned foreign subsidiary is its local currency. Assets and liabilities of the foreign subsidiary are translated into United States dollars based on exchange rates at the end of the reporting period; income and expense items are translated at the weighted average exchange rates prevailing during the reporting period. Translation adjustments for the foreign subsidiary are accumulated in other comprehensive income or loss, a component of stockholders' equity. Transaction gains or losses are included in the determination of net loss.

Cash, Cash Equivalents and Credit Risk

Cash equivalents consist of investments in low risk, highly liquid money market accounts and certificates of deposit with original maturities of 90 days or less. Cash deposited with banks and other financial institutions may exceed the amount of insurance provided on such deposits. If the amount of a deposit at any time exceeds the federally insured amount at a bank, the uninsured portion of the deposit could be lost, in whole or in part, if the bank were to fail.

Financial instruments that potentially subject Seneca to concentrations of credit risk consist primarily of cash equivalents. Seneca’s investment policy, approved by Seneca’s Board of Directors, limits the amount Seneca may invest in any one type of investment issuer, thereby reducing credit risk concentrations. Seneca attempts to limit its credit and liquidity risks through its investment policy and through regular reviews of Seneca’s portfolio against its policy. To date, Seneca has not experienced any loss or lack of access to its cash held in operating accounts or to Seneca’s cash equivalents.

| 8 |

Cash and cash equivalents at March 31, 2021 consist of approximately $6,560,900 of cash held and used and $51,300 of cash included in disposal group assets held for sale.

Revenue

Seneca analyzes contracts to determine the appropriate revenue recognition using the following steps: (i) identification of contracts with customers; (ii) identification of distinct performance obligations in the contract; (iii) determination of contract transaction price; (iv) allocation of contract transaction price to the performance obligations; and (v) determination of revenue recognition based on timing of satisfaction of the performance obligation. Seneca recognizes revenues upon the satisfaction of its performance obligation (upon transfer of control of promised goods or services to customers) in an amount that reflects the consideration to which it expects to be entitled to in exchange for those goods or services. Deferred revenue results from cash receipts from or amounts billed to customers in advance of the transfer of control of the promised services to the customer and is recognized as performance obligations are satisfied. When sales commissions or other costs to obtain contracts with customers are considered incremental and recoverable, those costs are deferred and then amortized as selling and marketing expenses on a straight-line basis over an estimated period of benefit.

Research and Development

Research and development costs are expensed as they are incurred. Research and development expenses consist primarily of costs associated with the pre-clinical development and clinical trials of Seneca’s product candidates. For the three months ended March 31, 2020, Seneca recorded approximately $52,200, of cost reimbursements from Seneca’s grants as an offset to research and development expenses. Seneca evaluated the grants and concluded that, based on the specific terms, they represent a cost reimbursement activity as opposed to a revenue generating activity, and are best reflected as an offset to the underlying research and development expense.

Income (Loss) per Common Share

Basic income (loss) per common share is computed by dividing total net income (loss) available to common stockholders by the weighted average number of common shares outstanding during the period.

For periods of net income when the effects are dilutive, diluted earnings per share is computed by dividing net income available to common stockholders by the weighted average number of shares outstanding and the dilutive impact of all dilutive potential common shares. Dilutive potential common shares consist primarily of convertible preferred stock, stock options, restricted stock units and common stock purchase warrants. The dilutive impact of potential common shares resulting from common stock equivalents is determined by applying the treasury stock method. Seneca’s unvested restricted shares contain non-forfeitable rights to dividends, and therefore are considered to be participating securities; the calculation of basic and diluted income per share excludes net income attributable to the unvested restricted shares from the numerator and excludes the impact of the shares from the denominator.

For all periods of net loss, diluted loss per share is calculated similarly to basic loss per share because the impact of all dilutive potential common shares is anti-dilutive due to the net losses; accordingly, diluted loss per share is the same as basic loss per share or the three-month periods ended March 31, 2021 and 2020. A total of approximately 1.1 and 1.3 million potential dilutive shares have been excluded in the calculation of diluted net income per share for the three-month periods ended March 31, 2021 and 2020, respectively as their inclusion would be anti-dilutive.

Share-Based Compensation

Seneca accounts for share-based compensation at fair value; accordingly, it expenses the estimated fair value of share-based awards over the requisite service period. Share-based compensation cost for stock options and warrants is generally determined at the grant date using an option pricing model. Option pricing models require Seneca to make assumptions, including expected volatility and expected term of the options. If any of the assumptions Seneca uses in the model were to significantly change, share-based compensation expense may be materially different. Share-based compensation cost for restricted stock and restricted stock units is generally determined at the grant date based on the closing price of our common stock on that date. The value of the award is generally recognized as expense on a straight-line basis over the requisite service period.

Intangible and Long-Lived Assets

Seneca assess impairment of our long-lived assets using a "primary asset" approach to determine the cash flow estimation period for a group of assets and liabilities that represents the unit of accounting for a long-lived asset to be held and used. Long-lived assets to be held and used are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. The carrying amount of a long-lived asset is not recoverable if it exceeds the sum of the undiscounted cash flows expected to result from the use and eventual disposition of the asset. No impairment losses were recognized during the three-month periods ended March 31, 2021 and 2020.

Income Taxes

Seneca account for income taxes using the asset and liability approach, which requires the recognition of future tax benefits or liabilities on the temporary differences between the financial reporting and tax bases of our assets and liabilities. A valuation allowance is established when necessary to reduce deferred tax assets to the amounts expected to be realized. Seneca also recognize a tax benefit from uncertain tax positions only if it is “more likely than not” that the position is sustainable based on its technical merits. Seneca’s policy is to recognize interest and penalties on uncertain tax positions as a component of income tax expense.

| 9 |

Leases

Seneca determines if an arrangement is or contains a lease at its inception. Seneca has made accounting policy elections whereby Seneca (i) does not recognize right-of-use (“ROU”) assets or lease liabilities for short-term leases (those with original terms of 12-months or less) and (ii) combine lease and non-lease elements of operating leases. Operating lease ROU assets are included in other noncurrent assets and operating lease liabilities are included in other current liabilities in Seneca’s condensed consolidated balance sheets. Seneca does not have any finance leases.

ROU assets represent Seneca’s right to use an underlying asset for the lease term and lease liabilities represent Seneca’s obligation to make lease payments arising from the lease. Operating lease ROU assets and liabilities are recognized at commencement date based on the present value of lease payments over the lease term. Rent expense is recognized on a straight-line basis over the lease term. See Note 5, Commitments and Contingencies, for additional disclosures.

Significant New Accounting Pronouncements

Recently Adopted Guidance

In August 2020, the FASB issued ASU No. 2020-06, Debt – Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging – Contracts in Entity’s Own Equity (Subtopic 815-40). This ASC addresses (i) accounting for convertible instruments, (ii) accounting for contracts in an entity’s own equity as derivatives and (iii) earnings per share calculations. The guidance attempts to simplify the accounting for convertible instruments by eliminating the requirement to separate embedded conversion options in certain circumstances. The guidance also provides for updated disclosure requirements for convertible instruments. The guidance further updates the criteria for determining whether a contract in an entity’s own equity can be classified as equity. Lastly, the guidance specifically addresses how to account for the effect of convertible instruments and potential cash settled instruments in calculating diluted earnings per share. The guidance is effective for smaller reporting companies as defined by the SEC for fiscal years beginning after December 15, 2023, including interim periods within those fiscal years and early adoption is permitted. The adoption of this guidance may be applied on a modified retrospective basis or a full retrospective basis. Seneca adopted this guidance effective January 1, 2021. The adoption did not have a material impact to our condensed consolidated financial statements.

Unadopted Guidance

In June 2016, the FASB issued ASU No. 2016-13, Financial Instruments – Credit Losses. This ASU relates to measuring credit losses on financial instruments, including trade receivables. The guidance eliminates the probable initial recognition threshold that was previously required prior to recognizing a credit loss on financial instruments. The credit loss estimate can now reflect an entity's current estimate of all future expected credit losses. Under the previous guidance, an entity only considered past events and current conditions. The guidance is effective for smaller reporting companies as defined by the SEC for fiscal years beginning after December 15, 2022, including interim periods within those fiscal years and early adoption is permitted. The adoption of certain amendments of this guidance must be applied on a modified retrospective basis and the adoption of the remaining amendments must be applied on a prospective basis. Seneca currently expects that the adoption of this guidance will likely change the way we assess the collectability of our receivables and recoverability of other financial instruments. Seneca has not yet begun to evaluate the specific impacts of this guidance nor have we determined the manner in which it will adopt this guidance.

Seneca has reviewed other recent accounting pronouncements and concluded that they are either not applicable to Seneca’s business, or that no material effect is expected on our condensed consolidated financial statements as a result of future adoption.

Note 3. Fair Value Measurements

Fair value is the price that would be received from the sale of an asset or paid to transfer a liability assuming an orderly transaction in the most advantageous market at the measurement date. U.S. GAAP establishes a hierarchical disclosure framework which prioritizes and ranks the level of observability of inputs used in measuring fair value. These levels are:

| · | Level 1 – inputs are based upon unadjusted quoted prices for identical instruments traded in active markets. |

| · | Level 2 – inputs are based upon quoted prices for similar instruments in active markets, quoted prices for identical or similar instruments in markets that are not active, and model-based valuation techniques for which all significant inputs are observable in the market or can be corroborated by observable market data for substantially the full term of the assets or liabilities. Where applicable, these models project future cash flows and discount the future amounts to a present value using market-based observable inputs including interest rate curves, foreign exchange rates, and forward and spot prices for currencies and commodities. |

| 10 |

| · | Level 3 – inputs are generally unobservable and typically reflect management's estimates of assumptions that market participants would use in pricing the asset or liability. The fair values are therefore determined using model-based techniques, including option pricing models and discounted cash flow models. |

Financial Assets and Liabilities Measured at Fair Value on a Recurring Basis

Seneca has segregated its financial assets and liabilities that are measured at fair value on a recurring basis into the most appropriate level within the fair value hierarchy based on the inputs used to determine the fair value at the measurement date.

At March 31, 2021 and December 31, 2020, Seneca had certain common stock purchase warrants that were originally issued in connection with our May 2016 and August 2017 offerings (See Note 4) that are accounted for as liabilities whose fair value was determined using Level 3 inputs. The following table identifies the carrying amounts of such liabilities:

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Liabilities | ||||||||||||||||

| Liability classified stock purchase warrants | $ | - | $ | - | $ | 75,298 | $ | 75,298 | ||||||||

| Balance at December 31, 2020 | $ | - | $ | - | $ | 75,298 | $ | 75,298 | ||||||||

| Liability classified stock purchase warrants | $ | - | $ | - | $ | 171,202 | $ | 171,202 | ||||||||

| Balance at March 31, 2021 | $ | - | $ | - | $ | 171,202 | $ | 171,202 | ||||||||

The following table presents the activity for those items measured at fair value on a recurring basis using Level 3 inputs:

| Mark-to-market liabilities - stock purchase warrants | ||||

| Balance at December 31, 2019 | $ | 84,596 | ||

| Change in fair value (gain) | (24,625 | ) | ||

| Balance at March 31, 2020 | $ | 59,971 | ||

| Balance at December 31, 2020 | $ | 75,298 | ||

| Change in fair value - loss | 95,904 | |||

| Balance at March 31, 2021 | $ | 171,202 | ||

The (gains) losses resulting from the changes in the fair value of the liability classified warrants are classified as other income or expense in the accompanying unaudited condensed consolidated statements of operations and comprehensive loss. The fair value of the common stock purchase warrants is determined based on the Black-Scholes option pricing model or other option pricing models as appropriate and includes the use of unobservable inputs such as the expected term, anticipated volatility and expected dividends. Changes in any of the assumptions related to the unobservable inputs identified above may change the embedded conversion options’ fair value; increases in expected term, anticipated volatility and expected dividends generally result in increases in fair value, while decreases in these unobservable inputs generally result in decreases in fair value.

For both the three-month periods ended March 31, 2021 and 2020, the changes in fair value of Seneca’s liability classified warrants are primarily due to changes in the underlying price of our common stock.

Note 4. Stockholders’ Equity

Seneca has granted share-based compensation awards to employees, board members and service providers. Awards may consist of common stock, restricted common stock, restricted common stock units, common stock purchase warrants, or common stock purchase options. Seneca common stock purchase options and stock purchase warrants have lives of up to ten years from the grant date. In addition, Seneca has issued warrants to purchase common stock in conjunction with debt and equity offerings. Awards vest either upon the grant date or over varying periods of time. The stock options provide for exercise prices equal to or greater than the fair value of the common stock at the date of the grant. Restricted stock units grant the holder the right to receive fully paid common shares with various restrictions on the holder’s ability to transfer the shares. As of March 31, 2021, Seneca had approximately 1.1 million shares of common stock reserved for issuance upon the granting of awards under Seneca’s equity incentive plans and the exercise of outstanding equity-linked instruments.

| 11 |

Seneca typically records share-based compensation expense on a straight-line basis over the requisite service period. Share-based compensation expenses included in our condensed consolidated statements of operations and comprehensive loss are as follows:

| Three Months Ended March 31, 2021 | ||||||||

| 2021 | 2020 | |||||||

| Research and development expenses | $ | 4,632 | $ | - | ||||

| General and administrative expenses | 243,361 | 75,892 | ||||||

| Total | $ | 247,993 | $ | 75,892 | ||||

Stock Options

A summary of stock option activity and related information for the three months ended March 31, 2021 follows:

| Number of Options | Weighted-Average Exercise Price | Weighted-Average Remaining Contractual Life (in years) | Aggregate Intrinsic Value | |||||||||||||

| Outstanding at January 1, 2021 | 299,563 | $ | 46.80 | 9.0 | $ | 438,650 | ||||||||||

| Granted | - | $ | - | |||||||||||||

| Exercised | - | $ | - | $ | - | |||||||||||

| Forfeited | - | $ | - | |||||||||||||

| Outstanding at March 31, 2021 | 299,563 | $ | 46.80 | 8.8 | $ | 1,821,552 | ||||||||||

| Exercisable at March 31, 2021 | 153,024 | $ | 87.60 | 8.6 | $ | 872,827 | ||||||||||

| Range of Exercise Prices | Number of Options Outstanding | Weighted-Average Exercise Price | Weighted-Average Remaining Contractual Life (in years) | Aggregate Intrinsic Value | ||||||||||||||

| $3.72 | 281,078 | $ | 3.72 | 9.0 | $ | 1,821,552 | ||||||||||||

| $35.40 | - | $52.80 | 8,626 | $ | 37.92 | 8.2 | - | |||||||||||

| $133.20 | - | $483.60 | 3,888 | $ | 175.26 | 4.2 | - | |||||||||||

| $1,435.20 | - | $5,928.00 | 5,971 | $ | 2,002.86 | 1.6 | - | |||||||||||

| 299,563 | $ | 46.80 | 8.8 | $ | 1,821,552 | |||||||||||||

| 12 |

Seneca uses the Black-Scholes option pricing model for “plain vanilla” options and other pricing models as appropriate to calculate the fair value of options. Seneca generally uses the “simplified method” to estimate expected life.

No options were granted in the three months ended March 31, 2021 or 2020.

All compensation expense related to outstanding awards had been recognized as of March 31, 2021.

In March 2021, certain executives were terminated. As part of their employment agreements, outstanding stock options continue vesting over their respective severance terms ranging from nine to twelve months. Expense for this subsequent vesting was recognized in total in the quarter end March 31, 2021 as there is no additional requisite service period.

In April 2021, in connection with the consummation of the Merger, all outstanding options were cancelled.

RSUs

Seneca has granted restricted stock units (RSU’s) to certain employees and board members that entitle the holders to receive shares of common stock upon vesting and subject to certain restrictions regarding the exercise of the RSUs. The grant date fair value of RSUs is based upon the market price of the underlying common stock on the date of grant.

No RSU’s were granted in the three months ended March 31, 2021 or 2020.

RSU’s vesting in the three months ended March 31, 2021 and 2020, had a total value of approximately $4,200 and $7,500, respectively.

At March 31, 2021, Seneca had 4,817 outstanding RSUs with a weighted average grant date fair value of $9.48 and a total intrinsic value of approximately $49,100. All RSU’s were fully vested and thus, there was no remaining unrecognized compensation expense at March 31, 2021.

No RSU’s were converted in either of the three months ended March 31, 2021 or 2020.

Restricted Stock

Seneca has granted restricted stock to certain board members that vest quarterly over the grant year. The grant date fair value of the restricted stock is based upon the market price of the common stock on the date of grant.

No restricted stock was granted in either of the three months ended March 31, 2021 or 2020.

Restricted stock vesting in the three months ending March 31, 2020, had a weighted average grant date fair value of $6.66 and a total intrinsic value of approximately $5,100. No restricted stock vested in the three months ended March 31, 2021.

No restricted stock was outstanding at March 31, 2021.

Stock Purchase Warrants.

Seneca has issued warrants to purchase common stock to certain officers, directors, stockholders and service providers as well as in conjunction with debt and equity offerings and at various times replacement warrants were issued as an inducement for warrant exercises.

In May 2016 and August 2017, Seneca issued a total of 14,552 and 18,750 common stock purchase warrants, respectively in conjunction with securities offerings. Such warrants are classified as liabilities due to the existence of certain net cash settlement provisions contained in the warrants. At March 31, 2021, after giving effect to exercises, 24,856 of these common stock purchase warrants remain outstanding and are recorded at fair value as mark-to-market liabilities (see Note 3).

| 13 |

A summary of outstanding warrants at March 31, 2021 follows:

| Range of Exercise Prices | Number of Warrants Outstanding | Range of Expiration Dates | ||||||

| $5.40 | - | $7.50 | 538,901 | May 2021 - May 2025 | ||||

| $10.20 | - | $20.28 | 180,056 | July 2024 - January 2025 | ||||

| $36.00 | - | $4,695.60 | 32,565 | July 2021 - April 2024 | ||||

| 751,522 | ||||||||

Preferred and Common Stock

Seneca has outstanding 200,000 shares of Series A 4.5% Convertible Preferred Stock issued in December 2016. Shares of the Series A 4.5% Convertible Preferred Stock are convertible into 6,479 shares of common stock.

Note 5. Commitments and Contingencies

Leases

As of March 31, 2021, Seneca operated one facility located in the United States and one facility located in China under leases which are both classified as operating leases.

Prior to the completion of the Merger, Seneca’s corporate offices and primary research facilities were located in Germantown, Maryland, where Seneca leased approximately 1,500 square feet. This lease provided for monthly payments of approximately $5,600 per month. This lease had an initial term of 12 months and expired on December 31, 2021. Seneca did not establish a right of use (“ROU”) asset or lease liability for this short-term lease. The lease was cancelled concurrently with the consummation of the Merger.

Prior to the completion of the Merger, Seneca leased approximately 11,300 square feet of research facility in the People’s Republic of China. This lease commenced in September 2019, provides for minimum lease payments of approximately $4,400 per month, expires in September 2024 and provides Seneca with a future first right of refusal for extending the lease beyond its expiration. This lease currently represents a long-term operating lease. The lease remains effective after the Merger.

Seneca recognized total rent expense of approximately $21,900 and $30,400 in the three months ended March 31, 2021 and 2020, respectively. Included in the expense is approximately $16,900 in each of the three months ended March 31, 2021 and 2020, relating to Seneca’s short-term leases. Lease costs, net of sublease income, for the three months ended March 31 consisted of the following:

| 2021 | 2020 | |||||

| Operating lease cost | $ | 21,900 | $30,417 | |||

| Variable lease cost | - | - | ||||

| Total net lease cost | $ | 21,900 | $30,417 | |||

At March 31, 2021, Seneca had approximately $188,700 of ROU assets included in Disposal Group Assets Held for Sale and approximately $147,300 of lease liability included in Disposal Group Liabilities Associated with Assets Held for Sale in the condensed consolidated balance sheets.

Future payments under the lone long-term operating lease as of March 31, 2021 are as follows:

| Future undiscounted cash flows: | |||||

| 2021 | * | $ | 42,500 | ||

| 2022 | 59,700 | ||||

| 2023 | 61,700 | ||||

| 2024 | 14,500 | ||||

| Total | 178,400 | ||||

| Discount factor | (31,100 | ) | |||

| Lease liability | 147,300 | ||||

| Less current liability | (42,000 | ) | |||

| Non-current lease liability | $ | 105,300 | |||

| * reflects the remaining 9 months of 2021 | |||||

| 14 |

Accrued Severance

In connection with the termination of certain employees pursuant to the Merger, the Company became obligated to pay an aggregate of approximately $4.35 million of severance payable to executives in accordance with their termination “without cause” pursuant to their employment agreements, and pursuant to Separation Agreements, change in control payments and the repurchase of options held by the executives upon completion of the Merger. Of this amount approximately $2.3 million was accrued at December 31, 2020. The executives were terminated in March 2021 and the corresponding severance amounts will be paid in accordance with the terms of their employment agreements and the Separation Agreements entered into between Seneca and the executives as follows:

Severance and Bonus Received upon termination “without cause”

| Name | Severance and Bonus | |||

| Kenneth Carter, PhD | $ | 816,995 | ||

| Dane Saglio | $ | 452,572 | ||

| Matthew Kalnik, PhD | $ | 599,868 | ||

| Senior VP of R&D | $ | 384,702 | ||

| Total: | $ | 2,254,137 |

Additional Severance in Connection with a Change in Control subsequent to the consummation of the Merger

| Name |

|

CIC Severance and Bonus1 |

| |

| Kenneth Carter, PhD | $ | 277,248 | ||

| Dane Saglio | $ | 100,857 | ||

| Matthew Kalnik, PhD | $ | 150,225 | ||

| Senior VP of R&D | $ | 85,567 | ||

| Total: | $ | 613,897 |

______________________________________

1. Represents additional severance benefits in connection with a termination without cause in connection with a change in control.

Repurchase of Employee Stock Options

Immediately prior to the closing of the Merger, each respective employee’s outstanding common stock options were purchased by Seneca for the following consideration:

| Name | Option Repurchase | |||

| Kenneth Carter, PhD | $ | 188,787 | ||

| Dane Saglio | $ | 362,391 | ||

| Matthew Kalnik, PhD | $ | 476,662 | ||

| Senior VP of R&D | $ | 395,166 | ||

| Total: | $ | 1,423,006 | ||

As of March 31, 2021, approximately $2.17 million in severance had been paid and subsequent to the closing of the Merger on April 27, 2021,an additional approximately $0.4 million has been paid with an additional $1.9 million expected to be paid out to the executives in installments until September 2022.

Other

From time to time, Seneca is party to legal proceedings that it believes to be ordinary, routine litigation incidental to the business. Seneca is currently not a party to any litigation or legal proceeding. As a result of the Merger, Seneca became involved in the following litigation related thereto as noted below. As of May 14, 2021, all of the following actions have been settled.

On January 8, 2021, Joseph Sheridan, a purported Seneca stockholder, filed a complaint in the United States District Court for the Southern District of New York against Seneca, the members of its board of directors, and LBS, captioned Sheridan v. Palisade Bio, Inc., et al., Case No. 1:21-cv-00166 (the “Sheridan Complaint”).

| 15 |

Also, on January 8, 2021, Hesam Pirjamaat, a purported Seneca stockholder, filed a complaint in the United States District Court for the Southern District of New York against Seneca, the members of its board of directors, Townsgate Acquisition Sub 1, Inc., and LBS, captioned Pirjamaat v. Palisade Bio, Inc., et al., Case No. 1:21-cv-00172 (the “Pirjamaat Complaint”).

On January 13, 2021, Brian Johnson, a purported Seneca stockholder, filed a complaint in the United States District Court for the Southern District of New York against Seneca and the members of its board of directors, captioned Johnson v. Palisade Bio, Inc., et al., Case No. 1:21-cv-00310 (the “Johnson Complaint”).

On January 15, 2021, Vipin Mathews, a purported Seneca stockholder, filed a complaint in the United States District Court for the Eastern District of New York against Seneca and the members of its board of directors, captioned Mathews v. Palisade Bio, Inc., et al., Case No. 1:21-cv-00242 (the “Mathews Complaint”).

On January 22, 2021, Emily Pechal, a purported Seneca stockholder, filed a complaint in the United States District Court for the Southern District of New York against Seneca and the members of its board of directors, captioned Pechal v. Palisade Bio, Inc., et al., Case No. 1:21-cv-00585 (the “Pechal Complaint”).

On February 25, 2021, Marcie Curtis, a purported Seneca stockholder, filed a complaint in the United States District Court for the District of Delaware against Seneca and the members of its board of directors, captioned Curtis v. Palisade Bio, Inc., et al., Case No. 1:21-cv-00292 (the “Curtis Complaint”).

On March 1, 2021, Juanesha Valdez, a purported Seneca stockholder, filed a complaint in the United States District Court for the Eastern District of Pennsylvania against Seneca, the members of its board of directors, Townsgate Acquisition Sub 1, Inc., and LBS, captioned Valdez v. Palisade Bio, Inc., et al., Case No. 1:21-cv-00980 (the “Valdez Complaint”).

On March 2, 2021, Bryan Anderson, a purported Seneca stockholder, filed a complaint in the United States District Court for the District of Delaware against Seneca and the members of its board of directors, captioned Anderson v. Palisade Bio, Inc., et al., Case No. 1:21-cv-00326 (the “Anderson Complaint”).

On March 3, 2021, Jack McIntire, a purported Seneca stockholder, filed a complaint in the United States District Court for the Southern District of New York against Seneca and the members of its board of directors, captioned McIntire v. Palisade Bio, Inc., et al., Case No. 1:21-cv-01869 (the “McIntire Complaint,” and, together with the Sheridan Complaint, the Pirjamaat Complaint, the Johnson Complaint, the Mathews Complaint, the Pechal Complaint, the Curtis Complaint, the Valdez Complaint, the Anderson Complaint, the “Stockholder Complaints”).

On February 26, 2021, the United States District Court for the Southern District of New York entered an order consolidating the Sheridan Complaint, the Pirjamaat Complaint, the Johnson Complaint, and the Pechal Complaint under Case No. 21-cv-0166.

Note 6. Related Party Receivable

On August 10, 2016, Seneca entered into a reimbursement agreement with a former executive officer. Pursuant to the reimbursement agreement, the former officer agreed to repay, over a six-year period, approximately $658,000 in expenses that Seneca determined to have been improperly paid under Seneca’s prior expense reimbursement policies.

In March 2019, in conjunction with the former executive officer’s termination, Seneca entered into a consulting agreement and release of claims agreement with the former executive officer. As partial consideration for the release, Seneca modified the reimbursement agreement to change the payment terms, extend the maturity and forgive approximately 50% or $229,000 of the outstanding receivable. Seneca has concluded that this outstanding balance is not recoverable and recorded an allowance against the entire remaining balance.

Note 7. Disposal Group Assets Held for Sale

In late 2020, Seneca engaged in negotiations with an interested third party for the sale of all of its assets and liabilities related to its neural stem cell program (NSI-566). Those negotiations have subsequently ended. Palisade is continuing the process to identify a purchaser for the assets and liabilities. Seneca previously concluded that it is probable that a sale will be completed within one year and that the assets and liabilities should be classified as a disposal group held for sale in its balance sheet at March 31, 2021. Assets and liabilities classified as held for sale will no longer be depreciated or amortized. Although Seneca believes a sale will be consummated, no binding agreements have been entered into and there can be no assurance that a sale will ultimately be consummated or on what terms and conditions.

Seneca concluded the net proceeds from the sale are expected to exceed the net carrying value of the assets and liabilities and accordingly, no impairment charge has been recognized as of March 31, 2021.

| 16 |

The assets and liabilities classified as a disposal group held for sale are comprised of the following:

| March 31, 2021 | ||||

| Cash | $ | 51,294 | ||

| Prepaid expenses | 146,659 | |||

| Property and equipment, net | 1,120 | |||

| Patents, net | 458,738 | |||

| ROU and other assets | 202,891 | |||

| Disposal group assets held for sale | $ | 860,702 | ||

| Accounts payable and accrued expenses | $ | 72,420 | ||

| Lease liabilities | 147,337 | |||

| Disposal group liabilities associated with assets held for sale | $ | 219,757 | ||

Note 8. Subsequent Events

On April 27, 2021, pursuant to the Merger Agreement, Seneca completed the previously announced merger transaction with LBS, pursuant to which Merger Sub merged with and into LBS, with LBS surviving such merger as a wholly owned subsidiary of the Company. In connection with the Merger, and immediately prior to the effective time of the Merger, Seneca effected a reverse stock split of Seneca’s common stock at a ratio of 1-for-6. In connection with the closing of the Merger, Seneca changed its name from “Seneca Biopharma, Inc.” to “Palisade Bio, Inc.” and the business conducted by the Company became primarily the business conducted by LBS, which is a clinical-stage biopharmaceutical company focused on advancing LBS’s clinical program and developing a therapeutic to combat the interruption of gastrointestinal function following major surgery for which there is currently a significant unmet need for safe and effective therapies. Seneca previously disclosed the closing of the Merger in its Current Report on Form 8-K filed on April 27, 2021.

| ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Statements in this Quarterly Report that are not strictly historical are forward-looking statements and include statements about products in development, our in-licensing/acquisition strategy, our out-licensing sales strategy, results and analyses of pre-clinical studies, clinical trials and studies, research and development expenses, cash expenditures, and alliances and partnerships, among other matters. You can identify these forward-looking statements because they involve our expectations, intentions, beliefs, plans, projections, anticipations, or other characterizations of future events or circumstances. These forward-looking statements are not guarantees of future performance and are subject to risks and uncertainties that may cause actual results to differ materially from those in the forward-looking statements as a result of any number of factors. Some of these factors are more fully discussed, as are other factors, in Seneca’s Annual Report on Form 10-K for the fiscal year ended December 31, 2020, as filed with the SEC, in our subsequent filings with the SEC as well as in the section of this Quarterly Report entitled “Risk Factors” and elsewhere herein. Seneca does not undertake to update any of these forward-looking statements or to announce the results of any revisions to these forward-looking statements except as required by law.

Seneca urges you to read this entire Quarterly Report on Form 10-Q, including the “Risk Factors” section, the condensed consolidated financial statements, and related notes. As used in this Quarterly Report, unless the context otherwise requires, the words “we,” “us,” “our,” “the Company” and “Palisade” refers to Palisade Bio, Inc. and its subsidiary, post Merger. Also, any reference to “common shares” or “common stock,” refers to our $0.01 par value common stock. Any reference to “Series A Preferred Stock” or “Preferred Stock” refers to our Series A 4.5% Convertible Preferred Stock. Any reference to “Seneca” refers to the company’s operations prior to the completion of the Merger. The information contained herein is current as of the date of this Quarterly Report (March 31, 2021), unless another date is specified.

On April 27, 2021, in connection with the consummation of the Merger, Seneca completed a 1-for-6 reverse stock split of its common stock. All shares and per share data in this report have been adjusted to reflect the reverse stock split. Seneca prepares its interim financial statements in accordance with U.S. GAAP. Seneca’s financials and results of operations for the three-month periods ended March 31, 2021 are not necessarily indicative of its prospective financial condition and results of operations for the pending full fiscal year ending December 31, 2021. The interim financial statements presented in this Quarterly Report as well as other information relating to Seneca contained in this Quarterly Report should be read in conjunction and together with the reports, statements and information filed by Seneca with the SEC.

Our Management’s Discussion and Analysis of Financial Condition and Results of Operations or MD&A is provided, in addition to the accompanying condensed consolidated financial statements and notes, to assist you in understanding our results of operations, financial condition and cash flows. The MD&A is organized as follows:

| · | Executive Overview — Discussion of our business and overall analysis of financial and other items affecting Seneca in order to provide context for the remainder of MD&A. |

| · | Critical Accounting Policies — Accounting policies that Seneca believes are important to understanding the assumptions and judgments incorporated in Seneca’s reported financial results and forecasts. |

| · | Results of Operations — Analysis of Seneca’s financial results comparing the three-month period ended March 31, 2021 to the comparable period of 2020. |

| · | Liquidity and Capital Resources — An analysis of cash flows and discussion of our financial condition and future liquidity needs. |

Executive Overview

Prior to Completion of the Merger

Historically, Seneca has been primarily focused on the research and development of nervous system therapies based on its proprietary human neural stem cells and its small molecule compounds with the ultimate goal of gaining approval from the “FDA”, and its international counterparts, to market and commercialize such therapies. In early 2019, Seneca commenced a strategic assessment of its clinical programs to determinate how to maximize shareholder value. As a result, Seneca subsequently initiated an:

| · | in-licensing and acquisition strategy in which it is evaluating novel therapeutics that could benefit from Seneca’s development experience with the goal of developing such technologies for commercialization; and |

| · | out-licensing strategy to find partners to acquire or license NSI-566 and NSI-189. |

On April 27, 2021, “Seneca completed its previously announced merger transaction with LBS in accordance with the terms of the Merger Agreement, by and among Seneca, Merger Sub, and LBS, pursuant to which Merger Sub merged with and into LBS., with LBS. surviving as a wholly owned subsidiary of Seneca. Immediately prior to the effective time of the Merger, LBS merged with and into Merger Sub. and LBS continued to exist as the surviving corporation. Concurrent with the closing of the Merger, on April 27, 2021 the Company effected a 1-for-6 Reverse Stock Split. Stockholders’ equity and all references to share and per share amounts in the accompanying consolidated financial statements have been retroactively adjusted to reflect the Reverse Stock Split for all periods presented. Immediately following the Merger, Seneca changed its name to “Palisade Bio, Inc.”

| 17 |

Operations Subsequent to Completion of the Merger

We are a clinical stage biopharmaceutical company focused on discovering, developing, and commercializing innovative oral therapies that

target serious diseases associated with the breakdown of the mucosal barrier protecting the gastrointestinal (“GI”) tract.

Our goal is to be an industry leader in developing therapies to treat these diseases and to improve the lives of patients suffering from

such diseases.

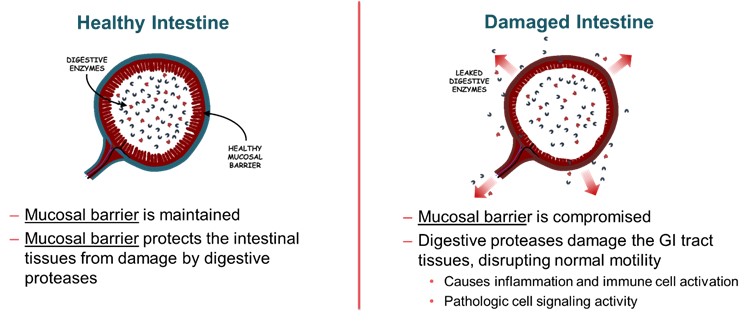

Our approach is founded on the discovery that damage to the intestinal epithelial barrier can result in leakage of digestive enzymes from the GI tract that can damage tissue and promote inflammation, causing a broad array of acute and chronic conditions.

Using our scientific and drug development expertise, we are developing a portfolio of oral product candidates to treat conditions driven by protease (intestinal enzymes) leakage through the intestinal epithelial barrier, including surgical complications and inflammatory conditions.

Our pipeline of product candidates is illustrated in this chart:

* Commercial right to LB1148 in Greater China (excluding Taiwan) have been out-licensed to Newsoara.

Our lead therapeutic candidate, LB1148, is a novel oral liquid formulation of the well-characterized digestive enzyme inhibitor, tranexamic acid, intended to inhibit digestive enzyme activity and preserve gut integrity during intestinal stress, such as results from reduced blood flow to the intestine, infections, and surgery. Peer reviewed publications of third-party research suggest that digestive enzyme leakage from the GI tract drives GI and organ dysfunction following these events.

We are initially developing LB1148 to be administered to patients prior to major surgeries that risk disrupting the intestinal mucosal barrier. As announced in March of 2020, a randomized, double-blind, parallel, placebo-controlled Phase 2 investigator-sponsored clinical trial of LB1148 in 120 patients undergoing coronary artery bypass grafting and/or heart valve replacement surgery requiring cardiopulmonary bypass was completed. Patients were randomized to receive LB1148 or placebo in conjunction with surgery. The trial’s primary endpoint was time to return of bowel function. Secondary endpoints include Intensive Care Unit (“ICU”) length of stay, hospital length of stay, organ function changes, inflammatory response and glucose control. LB1148 provided an approximately 30% improvement in the time to normal bowel function following cardiovascular (“CV”) surgery (p<0.001) compared to placebo. The treatment group also had an average 1.1-day shorter length of stay in the ICU and an average 1.1-day shorter hospital stay. Generally, treatment with LB1148 was well tolerated. Adverse events (“AEs”) were similar between the treatment groups and not considered unexpected for the subject population. None of the AEs or serious adverse events (“SAEs”) reported were considered drug-related by the sponsor-investigator. One of the primary factors in discharging patients from the hospital following surgery is the return of bowel function. LB1148 has been granted Fast Track designation from the “FDA” for the treatment of postoperative GI dysfunction (which may present as feeding intolerance, ileus, necrotizing enterocolitis (“NEC”), etc.) associated with gut hypoperfusion injury in pediatric patients who have undergone congenital heart disease repair surgery.

We are also currently conducting a randomized, double-blind, placebo-controlled, proof-of-concept Phase 2 clinical trial of LB1148 in patients undergoing elective bowel resection surgery in the Unites States. We expect to have initial data regarding the time to return of GI function from this clinical trial in the second half of 2021. The second part of this trial will evaluate whether patients treated with LB1148 also experience fewer postoperative intra-abdominal adhesions. In the second half of 2021, we are planning to initiate a Phase 2/3 clinical trial of LB1148 in neonatal patients undergoing CV surgery to correct congenital heart defects. We anticipate that this clinical trial will enroll 100 patients and that we will have data from the first 10 patients in late 2021 with final data from the full 100 patients in 2022.

Beyond our lead product candidate, we are continuing to develop additional therapeutic candidates. We believe that protease-based therapeutics hold promise in meeting a number of unmet needs resulting from chronic protease leak, beyond our initial therapeutic focus on GI-related pathology triggered by major surgeries.

| 18 |

Critical Accounting Policies

Seneca’s unaudited condensed consolidated financial statements have been prepared in accordance with U.S. GAAP. The preparation of these condensed consolidated financial statements requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues and expenses. Note 2 of the Notes to Unaudited Condensed Consolidated Financial Statements included elsewhere herein describes the significant accounting policies used in the preparation of the condensed consolidated financial statements. Certain of these significant accounting policies are considered to be critical accounting policies, as defined below.

A critical accounting policy is defined as one that is both material to the presentation of our condensed consolidated financial statements and requires management to make difficult, subjective or complex judgments that could have a material effect on Seneca’s financial condition and results of operations. Specifically, critical accounting estimates have the following attributes: (1) we are required to make assumptions about matters that are highly uncertain at the time of the estimate; and (2) different estimates we could reasonably have used, or changes in the estimate that are reasonably likely to occur, would have a material effect on our financial condition or results of operations.

Estimates and assumptions about future events and their effects cannot be determined with certainty. Seneca bases its estimates on historical experience and on various other assumptions believed to be applicable and reasonable under the circumstances. These estimates may change as new events occur, as additional information is obtained and as Seneca’s operating environment changes. These changes have historically been minor and have been included in the financial statements as soon as they became known. Based on a critical assessment of its accounting policies and the underlying judgments and uncertainties affecting the application of those policies, management believes that our condensed consolidated financial statements are fairly stated in accordance with U.S. GAAP and present a meaningful presentation of our financial condition and results of operations. Seneca believes the following critical accounting policies reflect Seneca’s more significant estimates and assumptions used in the preparation of Seneca’s condensed consolidated financial statements:

Use of Estimates - The preparation of financial statements in accordance with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. The condensed consolidated financial statements include significant estimates for the expected economic life and value of Seneca’s licensed technology and related patents, our net operating loss and related valuation allowance for tax purposes, the fair value of Seneca’s liability classified warrants and its share-based compensation related to employees and directors, consultants and advisors, among other things. Because of the use of estimates inherent in the financial reporting process, actual results could differ significantly from those estimates.

Long Lived Intangible Assets – Seneca’s long-lived intangible assets consist of its intellectual property patents including primarily legal fees associated with the filings and in defense of its patents. The assets are amortized on a straight-line basis over the expected useful life which Seneca defines as ending on the expiration of the patent group. These assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of the asset may not be recoverable. Seneca assesses this recoverability by comparing the carrying amount of the asset to the estimated undiscounted future cash flows to be generated by the asset. If an asset is deemed to be impaired, Seneca estimates the impairment loss by determining the excess of the asset’s carrying amount over the estimated fair value. These determinations use assumptions that are highly subjective and include a high degree of uncertainty. During the three-month periods ended March 31, 2021 and 2020, no impairment losses were recognized.

Fair Value Measurements - The fair value of our short-term financial instruments, which primarily include cash and cash equivalents, other short-term investments, accounts payable and accrued expenses, approximate their carrying values due to their short maturities. The fair value of our long-term indebtedness was estimated based on the quoted prices for the same or similar issues or on the current rates offered to the Company for debt of the same remaining maturities which approximates the carrying value. The fair values of our liability classified warrants are estimated using Level 3 unobservable inputs.

Share-Based Compensation - Seneca accounts for share-based compensation at fair value; accordingly, Seneca expenses the estimated fair value of share-based awards over the requisite service period. Share-based compensation cost for stock options and warrants issued to employees, board members and non-employee consultants is generally determined at the grant date using an option pricing model. Option pricing models require Seneca to make assumptions, including expected volatility and expected term of the options. If any of the assumptions Seneca uses in the model were to significantly change, share-based compensation expense may be materially different. Share-based compensation cost for restricted stock and restricted stock units issued to employees and board members is determined at the grant date based on the closing price of Seneca’s common stock on that date. The value of the award that is ultimately expected to vest is recognized as expense on a straight-line basis over the requisite service period.

RESULTS OF OPERATIONS

Revenue

Seneca generated no revenues from the sale of its proposed therapies for any of the periods presented.

Seneca has historically generated minimal revenue from the licensing of its intellectual property to third parties as well as payments under a settlement agreement.

Research and Development Expenses

Seneca’s research and development expenses have consisted primarily of clinical trial expenses, including payments to clinical trial sites that perform Seneca’s clinical trials and clinical research organizations (CROs) that help Seneca manage its clinical trials, manufacturing of small molecule drugs and stem cells for both human clinical trials and for pre-clinical studies and research, personnel costs for research and clinical personnel, and other costs including research supplies and facilities. Our 2020 research and development expenses reflect the costs identified above and additionally, the valuation and preparation of materials on the ALS development program

| 19 |

Seneca focused on the development of therapies with potential uses in multiple indications and use employee and infrastructure resources across several projects. Accordingly, many of Seneca’s costs are not attributable to a specifically identified product and Seneca does not account for internal research and development costs on a project-by-project basis.

In August 2017, Seneca was awarded a Small Business Innovation Research (“SBIR”) grant by the National Institutes of Health (“NIH”) to evaluate in preclinical studies the potential of NSI-189, a novel small molecule compound, for the prevention and treatment of diabetic neuropathy. The award of approximately $1 million was to be paid over a two-year period, if certain conditions are met at mid-term. In June 2018, Seneca was awarded a Department of Defense grant related to its efforts involving stem cell therapy for severe traumatic brain injury. The award of approximately $150,000 was received in 2019.

General and Administrative Expenses

General and administrative expenses are primarily comprised of salaries, benefits and other costs associated with Seneca’s operations including, finance, human resources, information technology, public relations and costs associated with maintaining a public company listing, legal, audit and compliance fees, facilities and other external general and administrative services, including the valuation of potential in-licensing initiatives.

Going Concern

Seneca’s auditors’ report issued in connection with our December 31, 2020 financial statements expressed an opinion that due to recurring losses from operations and an accumulated deficit, there is substantial doubt about Seneca’s ability to continue as a going concern.

The Company’s management has evaluated whether there is substantial doubt about the Company’s ability to continue as a going concern and has determined that substantial doubt existed as of the date of the end of the period covered by this Quarterly Report on Form 10-Q (the “Form 10-Q”). This determination was based on the following factors: (i) the Company’s available cash as of the date of this filing will not be sufficient to fund its anticipated level of operations for the next 12 months; (ii) the Company will require additional financing for the remainder of fiscal year 2021 to continue at its expected level of operations; and (iii) if the Company fails to obtain the needed capital, it will be forced to delay, scale back, or eliminate some or all of its development activities or perhaps cease operations. In the opinion of management, these factors, among others, raise substantial doubt about the ability of the Company to continue as a going concern as of the date of the end of the period covered by this Form 10-Q and for one year from the issuance of the unaudited condensed consolidated financial statements.

COVID-19

The COVID-19 pandemic has resulted in quarantines, restrictions on travel and other business and economic disruptions. Seneca has evaluated the impact of the pandemic on its business operations and plans, including but not limited to the impact on access to capital, planned and ongoing clinical trials, cash management and our investment policies regarding cash as well as the long term effects in the medical and drug development fields..

Comparison of the Three Months Ended March 31, 2021 and 2020

Revenue

During the three months ended March 31, 2020 Seneca recognized revenue of $2,500 related to ongoing fees pursuant to certain licenses of Seneca’s intellectual property to third parties. In addition, during the three months ended March 31, 2020, Seneca recognized $3,500 of royalty revenue related to a settlement of a prior patent infringement case. No revenue was recognized in the three months ended March 31, 2021.

Operating Expenses

Operating expenses for the three months ended March 31 were as follows:

| Three Months Ended March 31, | Increase (Decrease) | |||||||||||||||

| 2021 | 2020 | $ | % | |||||||||||||

| Operating Expenses | ||||||||||||||||

| Research and development expenses | $ | 471,107 | $ | 696,889 | $ | (225,782 | ) | (32 | %) | |||||||

| General and administrative expenses | 1,720,413 | 1,299,595 | 420,818 | 32 | % | |||||||||||

| Total operating expenses | $ | 2,191,520 | $ | 1,996,484 | $ | 195,036 | 10 | % | ||||||||

Research and Development Expenses

The decrease of approximately $226,000 or 32% in research and development expenses was primarily attributable to the continued wind down of clinical activities for Seneca’s stem cell and small molecule programs into 2021. The 2020 amount also reflected our evaluation of data and preparation of materials for the FDA meeting seeking FDA input on a potential Phase 3 clinical trial design for ALS.

| 20 |

General and Administrative Expenses

G&A expenses increased approximately $421,000 or 32%. The 2021 increase reflects the costs related to seeking shareholder approval for the LBS merger, associated legal expenses including the negotiation of settlement agreements with the shareholder legal actions described elsewhere in the filing.

Other income (expense)

Other expense, net totaled approximately $93,600 and $5,585,000 for the three months ended March 31, 2021 and 2020, respectively.

Other expense, net in 2021 consisted primarily of non-cash losses related to the fair value adjustment of Seneca’s liability classified stock purchase warrants partially offset by interest income.

Other income, net in 2020 consisted primarily of a non-cash warrant inducement charge of approximately $5,620,000 partially offset by $25,000 of noncash gains related to the fair value adjustment of Senaca’s liability classified warrants.

Liquidity and Capital Resources

Financial Condition

Since Seneca’s inception, it has financed its operations through the sales of its securities, issuance of long-term debt, the exercise of investor warrants, and to a lesser degree from grants and research contracts as well as the licensing of its intellectual property to third parties.

Seneca had cash and cash equivalents of approximately $6.6 million at March 31, 2021. Management expects the Company will incur substantial operating losses for the foreseeable future in order to complete clinical trials and launch and commercialize any product candidates for which it receives regulatory approval. The Company will need to raise additional capital through a combination of equity offerings, debt financings, collaborations, and other similar arrangements. The COVID-19 pandemic continues to rapidly evolve and has already resulted in a significant disruption of global financial markets. The Company’s ability to raise additional capital may be adversely impacted by potential worsening of global economic conditions and the recent disruptions to, and volatility in, the credit and financial markets in the United States and worldwide resulting from the pandemic. If the disruption persists and deepens, the Company could experience an inability to access additional capital. In addition, the Company is restricted, pursuant to agreements with the investor in the private financing conducted in connection with the Merger, from issuing equity securities in the near term without the consent of such investor.

Cash Flows – 2021 compared to 2020

| Three Months ended March 31, | Favorable (Unfavorable) | |||||||||||||||

| 2021 | 2020 | $ | % | |||||||||||||

| Net cash used in operating activities | $ | (3,941,235 | ) | $ | (1,677,629 | ) | $ | (2,263,606 | ) | (135 | %) | |||||

| Net cash provided by investing activities | $ | - | $ | - | $ | - | - | % | ||||||||

| Net cash provided by financing activities | $ | - | $ | 6,593,428 | $ | (6,593,428 | ) | 100 | % | |||||||

Net Cash Used in Operating Activities

Cash used in operating activities for the three months ended March 31, 2021, reflects Seneca’s $2,285,000 loss for the period adjusted for certain non-cash items including: (i) $2,009,000 of net cash outflows related to changes in operating assets and liabilities, (ii) $248,000 of share-based compensation and (iii) a $96,000 loss related to the change in fair value of Seneca’s liability classified warrants.

Net Cash (Used in) Provided by Investing Activities

There were no investing activities in either of the three months ended March 31, 2021 or 2020.

Net Cash Used in by Financing Activities

There were no investing financing activities in the three months ended March 31, 2021.

For the three months ended March 31, 2020, cash provided by financing activities consisted of $6.7 million of net proceeds generated from the exercise of warrants pursuant to an inducement offer partially offset by payments under Seneca’s short-term debt used to finance insurance premiums.

Future Liquidity and Needs

Seneca has incurred significant operating losses and negative cash flows since inception. Seneca has not been able to generate significant revenues nor achieved profitability.

As explained in the notes to Seneca’s condensed consolidated financial statements, prior to the consummation of the Merger, there was substantial doubt as to Seneca’s ability to continue as a going concern.

| 21 |

| ITEM 3. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |