As filed with the Securities and Exchange Commission on September 21, 2018

Registration No. 333-225876

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 2 to

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

CREATIVE REALITIES, INC.

(Exact name of registrant as specified in its charter)

| Minnesota | 41-1967918 | |

| (State or other

jurisdiction of incorporation or organization) |

(I.R.S. Employer

Identification Number) |

13100 Magisterial Drive, Suite 100 Louisville, KY 40223 Telephone: (502) 791-8800 (Address, including Zip Code, and Telephone Number, including Area Code, of Registrant’s Principal Executive Offices) |

Mr. Richard Mills Chief Executive Officer 13100 Magisterial Drive, Suite 100 Louisville, KY 40223 Telephone: (502) 791-8800 (Name, Address, Including Zip Code,

and Telephone Number, |

Copy to: |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of the registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act (check one):

| Large accelerated filer ☐ | Accelerated filer ☐ | |

| Non-accelerated filer ☐ (Do not check if a smaller reporting company) | Smaller reporting company ☑ | |

| Emerging growth company ☐ |

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | Amount to be Registered | Proposed Maximum Offering Price Per Unit | Proposed Maximum Aggregate Offering Price (1) | Amount of Registration Fee (2) | ||||||||||||

| Common stock, $0.01 par value per share | $ | 13,000,000 | $ | 1,618.50 | ||||||||||||

| (1) | Estimated solely for the purpose of calculating the amount of the registration fee in accordance with Rule 457(o) of the Securities Act of 1933. |

| (2) | Of the registration fee amount, $996 was earlier paid in connection with the June 25, 2018 filing of this registration statement. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is declared effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is prohibited.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION | DATED SEPTEMBER 21, 2018 |

[●]

Shares

Common Stock

We are offering [●] shares of our common stock at a public offering price of $[●] per share. The underwriters have the option to purchase up to [●] additional shares from us at the price to the public less the underwriting discounts and commissions.

Our common stock is currently traded on the OTCQX Marketplace under the symbol “CREX.” On September 20, 2018, the closing price of our common stock was $0.26 per share. We have reserved the symbol “CREX” for purposes of listing our common stock on The NASDAQ Capital Market and have applied to list our common stock on that exchange. If the application is approved, trading of our common stock on The NASDAQ Capital Market is expected to begin within five days after the date on which we sell and issue the common stock under this prospectus. We will not consummate and close this offering without a listing approval letter from The NASDAQ Capital Market. In this prospectus, we assume that the price per share in this offering will be in the range of $[●] to $[●], and we have used the midpoint of such range ($[●]) for the assumptions set forth herein.

You should read this prospectus carefully before you invest. You should not assume that the information in this prospectus is accurate as of any date other than the date on the front of this prospectus.

Investing in our common stock involves a high degree of risk. Before making any investment in these securities, you should read and carefully consider the risks described in this prospectus under “Risk Factors” beginning on page 5 of this prospectus. We are a “smaller reporting company” under applicable law and will be subject to reduced public company reporting requirements.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

A.G.P./Alliance Global Partners is acting as the representative of the underwriters for the offering. There is no arrangement for funds to be received in any escrow, trust or similar arrangement. Delivery of the shares of our common stock will be made on or about [●], 2018.

The date of this prospectus is , 2018

| i |

ABOUT THIS PROSPECTUS

Unless otherwise stated or the context otherwise requires, the terms “we,” “us,” “our,” “Creative Realities” and the “Company” refer to Creative Realities, Inc. and its subsidiaries.

Neither we nor the underwriters have authorized anyone to provide you with information different from that contained in this prospectus and any free writing prospectus we have prepared. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We and the underwriters are offering to sell shares of common stock and seeking offers to buy shares of common stock only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of any sale of the common stock. Our business, liquidity position, financial condition, prospects or results of operations may have changed since the date of this prospectus.

This prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. See “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements.”

Until , 2018 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

Presentation of Financial and Operating Data

Unless otherwise indicated, the historical financial and operating information presented in this prospectus for the years ended and as of December 31, 2017 and December 31, 2016 and as of and for the six months ended June 30, 2018 and June 30, 2017 is that of Creative Realities, Inc.

Industry and Market Data

The industry, market and data used throughout this prospectus have been obtained from our own research, surveys or studies conducted by third parties and industry or general publications. Industry publications and surveys generally state that they have obtained information from sources believed to be reliable, but do not guarantee the accuracy and completeness of such information. We believe that each of these studies and publications is reliable.

| i |

This summary contains basic information about us and the offering contained elsewhere in this prospectus. Because it is a summary, it does not contain all the information that you should consider before investing in our common stock. You should read and carefully consider the entire prospectus before making an investment decision, especially the information presented under the headings “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and all other information included in this prospectus in its entirety before you decide whether to purchase any shares offered by this prospectus.

Company Overview

Creative Realities, Inc. is a Minnesota corporation that provides innovative digital marketing technology solutions to a broad range of companies, individual brands, enterprises, and organizations throughout the United States and in certain international markets. We have expertise in a broad range of existing and emerging digital marketing technologies across 18 vertical markets, as well as the related media management and distribution software platforms and networks, device and content management, product management, customized software service layers, systems, experiences, workflows, and integrated solutions. Our technology and solutions include: digital merchandising systems and omni-channel customer engagement systems; content creation, production and scheduling programs and systems; a comprehensive series of recurring maintenance, support, and field service offerings; interactive digital shopping assistants, advisors and kiosks; and, other interactive marketing technologies such as mobile, social media, point-of-sale transactions, beaconing and web-based media that enable our customers to transform how they engage with consumers.

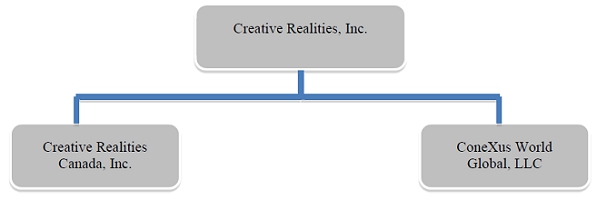

Our main operations are conducted directly through Creative Realities, Inc. and our wholly owned subsidiaries Creative Realities Canada, Inc. a Canadian corporation, and ConeXus World Global, LLC, a Kentucky limited liability company. Our other wholly owned subsidiary Creative Realities, LLC, a Delaware limited liability company, has been effectively dormant since October 2015, the date of the merger with ConeXus World Global, LLC.

We generate revenue in this business by:

| ● | consulting with our customers to determine the technologies and solutions required to achieve their specific goals, strategies and objectives; |

| ● | designing our customers’ digital marketing experiences, content and interfaces; |

| ● | engineering the systems architecture delivering the digital marketing experiences we design – both software and hardware – and integrating those systems into a customized, reliable and effective digital marketing experience; |

| ● | managing the efficient, timely and cost-effective deployment of our digital marketing technology solutions for our customers; |

| ● | delivering and updating the content of our digital marketing technology solutions using a suite of advanced media, content and network management software products; and |

| ● | maintaining our customers’ digital marketing technology solutions by: providing content production and related services; creating additional software-based features and functionality; hosting the solutions; monitoring solution service levels; and responding to and/or managing remote or onsite field service maintenance, troubleshooting and support calls. |

These activities generate revenue through: bundled-solution sales; consulting services, experience design, content development and production, software development, engineering, implementation, and field services; software license fees; and maintenance and support services related to our software, managed systems and solutions.

We currently market and sell our technology and solutions primarily through our sales and business development personnel, but we also utilize agents, strategic partners, and lead generators who provide us with access to additional sales, business development and licensing opportunities.

Our digital marketing technology solutions have application in a wide variety of industries. The industries in which we sell our solutions are established and include automotive, apparel & accessories, banking, baby/children, beauty, CPG, department stores, digital out-of-home (“DOOH”), electronics, fashion, fitness, foodservice/quick service restaurant (“QSR”), financial services, gaming, luxury, mass merchants, mobile operators, and pharmacy retail; however, the planning, development, implementation and maintenance of technology-enabled experiences involving combinations of digital marketing technologies is relatively new and evolving. Moreover, a number of participants in these industries have only recently started considering or expanding the adoption of these types of technologies, solutions and experiences as part of their overall marketing strategies. As a result, we remain an early stage company without an established history of profitability.

On September 20, 2018, we entered into a Stock Purchase Agreement with Christie Digital Systems, Inc. (the “Purchase Agreement”) to acquire Allure Global Solutions, Inc., a wholly owned subsidiary of Christie Digital Systems (“Allure”). Allure, headquartered in Atlanta, Georgia, is an enterprise software development company providing software solutions, a suite of complementary services, and ongoing support for an array of digital media and POS solutions. The company provides a wide range of products for the theatre, restaurant, convenience store, theme park, and retail spaces and works to create, develop, deploy, and maintain enterprise software solutions including those designed specifically to integrate, manage, and power ambient client-owned networks. Those networks manage data and marketing content that has been designed and proven to influence consumer purchase behavior.

| 1 |

Subject to the terms and conditions of the Purchase Agreement, upon the closing of the acquisition, we will acquire ownership of all of Allure’s issued and outstanding capital shares in consideration for a total purchase price of approximately $8,450,000, subject to a post-closing working capital adjustment. Of this purchase price amount, we expect to pay approximately $6,300,000 in cash from the proceeds of this offering. Of the remaining purchase price amount, approximately $1,250,000 will be paid in the form of our assumption of certain retention bonus obligations of Allure, and approximately $900,000 (subject to increase in the event the acquisition is not consummated prior to the close of business on October 31, 2018) will be paid through our assumption of debt owed by Allure to its current shareholder, Christie Digital Systems. That debt will be represented by our issuance to the seller of a promissory note accruing interest at 3.5% per annum. The promissory note will require us to make quarterly payments of interest only through calendar 2019, and monthly payments of interest and principal from January 2020 through December 31, 2020, on which date the promissory note will mature and all remaining amounts owing thereunder will be due. We will be able to prepay in whole or in part amounts owing under the promissory note, without penalty, at our option, at any time and from time to time.

The promissory note will be convertible into shares of Creative Realities common stock, at the seller’s option on or after the 180th day after issuance, at an initial conversion price of $0.28 per share (i.e., every $1,000 owing under the promissory note may convert into 3,572 shares of our common stock), subject to customary equitable adjustments. Conversion of all amounts owing under the promissory note will be mandatory if the 30-day volume-weighted average price of our common stock exceeds 200% of the common stock trading price at the closing of the acquisition. We will grant the seller customary registration rights for the shares of our common stock issuable upon conversion of the promissory note.

The stock purchase agreement contemplates additional consideration or $2,000 to be paid by us to seller in the event that acquiree revenue exceeds $13,000, wherein revenues from one specifically-named customer add only 70% of their gross value to the total, for any of (i) the 12-month period ending December 31, 2019, or (ii) any of the next following trailing 12-month periods ending on each of March 31, June 30, September 30 and December 31, 2020.

We presently expect the transaction to be completed on or prior to the close of business on October 31, 2018, subject, however, to the completion of this offering and the satisfaction of other customary closing conditions contained in the Purchase Agreement. The Purchase Agreement contains certain termination rights for both us and Christie Digital Systems, including rights to terminate the Purchase Agreement in the event of a breach by the other party (which right includes the right to recover out-of-pocket costs incurred by the non-breaching party) and our limited rights to terminate the Purchase Agreement upon certain adverse developments in the Allure’s business. Please see our Current Report on Form 8-K filed with the SEC on September 20, 2018 for further information on the Purchase Agreement.

Audited historical financial information for the operations comprising the business of Allure, together with pro forma financial information, each as required by applicable SEC rules, is contained elsewhere in this prospectus.

We intend to fund the entire cash purchase price for our acquisition of Allure with net proceeds from this offering. Nevertheless, we may be unable to consummate the Allure acquisition, and this offering is not conditioned on the consummation of the Allure acquisition or any other transaction. See “Risk Factors” for certain risks relating to the Allure acquisition.

Market Opportunity

We believe that the adoption and evolution of digital marketing technology solutions will increase substantially in years to come both in the industries in which we currently focus and in others. We also believe that adoption of our solutions depends not only upon the services and solutions that we provide but also depends heavily upon the cost of hardware used to process and display content on them. While the costs of hardware configurations and software media players have historically decreased and we believe they will continue to do so at an accelerating rate, flat panel displays and players typically constitute a large portion of the expenditure customers make relative to the entire cost of implementing a digital marketing system implementation and can be a barrier to customer deployment. As a result, we believe that the broader adoption of digital marketing technology solutions is likely to increase, although we cannot predict the rate at which such adoption will occur.

Another key component of our business strategy, given the evolving dynamics of the industry in which we operate, is to acquire and integrate other operating companies in the industry in conjunction with pursuing our organic growth objectives. We believe that the selective acquisition and successful integration of certain companies will: accelerate our growth in targeted vertical and operating markets; enable us to cost-effectively aggregate multiple customer bases onto a single business and technology platform; provide us with greater operating scale on a consolidated basis; enable us to leverage a common set of processes and tools, and cost efficiencies company-wide; and ultimately result in higher operating profitability and cash flow from operations. Our management team is actively pursuing and evaluating alternative acquisition opportunities on an ongoing basis. Our management team and Board of Directors have broad experience with the execution, integration and financing of acquisitions. We believe that, based on the foregoing and other factors, we can successfully serve as a consolidator of multiple business and technology platforms serving similar markets.

Our company sells products and services primarily throughout North America.

Corporate Organization

Our principal offices are located at 13100 Magisterial Drive, Suite 100, Louisville, KY 40223, and our telephone number at that office is (502) 791-8800. Our fiscal year ends December 31.

Our corporate structure, including our principal operating subsidiaries after giving effect to our acquisition of Allure, is as follows:

| 2 |

The Offering

The summary below describes some of the terms of the offering. For a more complete description of the common stock, see “Description of Securities.”

|

Issuer |

Creative Realities, Inc. |

Securities offered by us |

[●] shares of our common stock. |

|

Public offering price |

$[●] per share. |

| Over-allotment option |

We have granted the underwriters an option to purchase up to [●] additional shares of common stock. This option is exercisable, in whole or in part, for a period of 45 days from the date of this prospectus. |

| Representative’s warrants | We will issue to Alliance Global Partners (“A.G.P.”), the representative of the underwriters, upon closing of this offering, compensation warrants entitling A.G.P. or its designees to purchase 3.5% of the aggregate number of shares of common stock that we issue in this offering (excluding any shares issued upon exercise of the underwriters’ over-allotment option).

The representative’s warrants will be exercisable at a price per share equal to 120% of the public offering price per share of common stock issued in this offering for no more than 48 months commencing six months after the date of effectiveness of the registration statement of which this prospectus forms a part. |

| Common stock outstanding prior to this offering | 88,870,344 shares (1) |

| Common stock outstanding after this offering |

[●] shares (1)(2) |

| Use of proceeds |

We estimate that the net proceeds from our issuance and sale of [●] shares of our common stock in this offering will be approximately $[●], assuming an initial public offering price of $[●] per share, after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. In this regard, we estimate that our own offering related expenses will be approximately $[●].

We intend to use the net proceeds from this offering to (1) fund the acquisition of Allure Global Solutions, Inc., an enterprise software development company providing software solutions, a suite of complementary services and ongoing support for its array of digital media and POS solutions, (2) achieve the capital requirements necessary to obtain a listing for our common stock on a national securities exchange and (3) fund general corporate activities and working capital requirements.

For more information, see “Use of Proceeds” below. |

| Market and trading symbol |

Our common stock is currently traded on the OTCQX Marketplace under the symbol “CREX.” |

| Proposed NASDAQ Capital Market symbol | CREX (3) |

| (1) | The number of shares of our common stock outstanding both before and after this offering is based on the number of shares outstanding as of September 20, 2018, and excludes: |

| ● | 8,665,500 common shares issuable upon exercise of stock options granted under both our 2006 Amended and Restated Equity Incentive Plan and 2014 Stock Incentive Plan and outstanding as of September 20, 2018, with a weighted-average exercise price of $0.29 per share; |

| ● | 44,790,585 common shares issuable upon exercise of warrants outstanding as of September 20, 2018, with a weighted-average exercise price of $0.30 per share; |

| ● | 21,706,636 shares of our common stock issuable upon conversion of Series A Convertible Preferred Stock outstanding as of September 20, 2018; |

| ● | 297,574 shares of our common stock potentially issuable, as of September 20, 2018, on account of dividends that have accrued (but are not presently payable) on currently outstanding shares of Series A Convertible Preferred Stock; and | |

| ● | 15,866,639 shares of our common stock issuable upon conversion of convertible promissory notes outstanding as of September 20, 2018. |

| (2) | Except as otherwise indicated, the number of shares of common stock presented in this prospectus excludes shares of our common stock issuable if the underwriters exercise their over-allotment option and shares of our common stock underlying warrants to be issued to the representative of the underwriters in connection with this offering. |

| (3) | We have reserved the symbol “CREX” for purposes of listing our common stock on The NASDAQ Capital Market and expect to apply to list our common stock on that exchange. |

| 3 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

The Information in this prospectus includes “forward-looking statements” under Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements, other than statements of historical fact included in this prospectus, regarding our strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects, plans and objectives of management are forward-looking statements. When used in this prospectus, the words “could,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. When considering forward-looking statements, you should keep in mind the risk factors and other cautionary statements described under the heading “Risk Factors” included in this prospectus. These forward-looking statements are based on our current expectations and assumptions about future events and are based on currently available information as to the outcome and timing of future events. Nevertheless, and despite the fact that management’s expectations and estimates are based on assumptions management believes to be reasonable and data management believes to be reliable, our actual results, performance or achievements are subject to future risks and uncertainties, any of which could materially affect our actual performance. Risks and uncertainties that could affect such performance include, but are not limited to:

| ● | the adequacy of funds for future operations; |

| ● | future expenses, revenue and profitability; |

| ● | trends affecting financial condition and results of operations; |

| ● | ability to convert proposals into customer orders under mutually agreed upon terms and conditions; |

| ● | general economic conditions and outlook; |

| ● | the ability of customers to pay for products and services received; |

| ● | the impact of changing customer requirements upon revenue recognition; |

| ● | customer cancellations; |

| ● | the availability and terms of additional capital; |

| ● | industry trends and the competitive environment; |

| ● | the impact of the company’s financial condition upon customer and prospective customer relationships; |

| ● | potential litigation and regulatory actions directed toward our industry in general; |

| ● | the ultimate control of our management and our Board of Directors by our controlling shareholder, Slipstream Funding, LLC; |

| ● | our reliance on certain key personnel in the management of our businesses; |

| ● | employee and management turnover; |

| ● | the existence of material weaknesses in internal controls over financial reporting; |

| ● | the inability to successfully integrate the operations of acquired companies; and |

| ● | the fact that our common stock is presently thinly traded in an illiquid market. |

These and other risk factors are discussed in reports we file with the SEC.

We caution you that these forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond our control. These risks include, but are not limited to, the risks described under “Risk Factors” in this prospectus. Should one or more of the risks or uncertainties described in this prospectus occur, or should underlying assumptions prove incorrect, our actual results and plans could differ materially from those expressed in any forward-looking statements.

All forward-looking statements, expressed or implied, included in this prospectus are expressly qualified in their entirety by this cautionary statement. This cautionary statement should also be considered in connection with any subsequent written or oral forward-looking statements that we or persons acting on our behalf may issue. Except as otherwise required by applicable law, we disclaim any duty to update any forward-looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this prospectus.

Although federal securities laws provide a safe harbor for forward-looking statements made by a public company that files reports under the federal securities laws, this safe harbor is not available to certain issuers, including issuers that do not have their equity traded on a recognized national exchange or The Nasdaq Capital Market. Our common stock does not trade on any recognized national exchange or The Nasdaq Capital Market. As a result, we will not have the benefit of this safe harbor protection in the event of any legal action based upon a claim that the material provided by us contained a material misstatement of fact or was misleading in any material respect because of our failure to include any statements necessary to make the statements not misleading.

| 4 |

Investing in our securities involves a high degree of risk. You should carefully consider the specific risks described below, the risks described in our Annual Report on Form 10-K for the fiscal year ended December 31, 2017, and our Quarterly Report on Form 10-Q for the quarter ended June 30, 2018, and any risks described in our other filings with the Securities and Exchange Commission, pursuant to Sections 13(a), 13(c), 14, or 15(d) of the Securities Exchange Act of 1934, before making an investment decision. See the section of this prospectus entitled “Where You Can Find More Information.” Any of the risks we describe below could cause our business, financial condition, results of operations or future prospects to be materially adversely affected.

The market price of our common stock could decline if one or more of these risks and uncertainties develop into actual events and you could lose all or part of your investment. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially and adversely affect our business, financial condition, results of operations or future prospects. In addition, some of the statements in this section of the prospectus are forward-looking statements. For more information about forward-looking statements, please see the section of this prospectus entitled “Risks Relating to Forward-Looking Statements” above. Amounts within the “Risk Factors” section are stated in thousands with the exception of share information.

RISKS RELATED TO OUR BUSINESS AND OUR INDUSTRY

We have generally incurred losses, and may never become or remain profitable.

Except for the second and fourth quarters of 2016 and the first quarter of 2017, we have incurred net losses, have negative cash flows from operations and have a working capital deficit. We incurred net losses in each of the years ended December 31, 2017 and 2016, respectively. We do not know with any degree of certainty whether or when we will become profitable. Even if we are able to achieve profitability in future periods, we may not be able to sustain or increase our profitability in successive periods.

We have formulated our business plans and strategies based on certain assumptions regarding the acceptance of our business model and the marketing of our products and services. Nevertheless, our assessments regarding market size, market share, market acceptance of our products and services and a variety of other factors may prove incorrect. Our future success will depend upon many factors, including factors which may be beyond our control or which cannot be predicted at this time.

Our digital marketing business is evolving in a rapidly changing market, and we cannot ensure the long-term successful operation of our business or the execution of our business plan.

Our digital marketing technology and solutions are an evolving business offering and the markets in which we compete are rapidly changing. As a result, our prospects must be considered in light of the risks, expenses and difficulties frequently encountered by growing companies in new and rapidly evolving markets. We may be unable to accomplish any of the following, which would materially impact our ability to implement our business plan:

| ● | establishing and maintaining broad market acceptance of our technology, solutions, services, and platforms, and converting that acceptance into direct and indirect sources of revenue; |

| ● | establishing and maintaining adoption of our technology, solutions, services, and platforms in and on a variety of environments, experiences, and device types; |

| ● | timely and successfully developing new technology, solution, service, and platform features, and increasing the functionality and features of our existing technology, solution, service, and platform offerings; |

| ● | developing technology, solutions, services, and platforms that result in a high degree of customer satisfaction and a high level of end-customer usage; |

| ● | successfully responding to competition, including competition from emerging technologies and solutions; |

| ● | developing and maintaining strategic relationships to enhance the distribution, features, content and utility of our technology, solutions, services, and platforms; |

| ● | identifying, attracting and retaining talented engineering, network operations, program management, technical services, creative services, and other personnel at reasonable market compensation rates in the markets in which we employ such personnel; and |

| ● | integration of acquisitions. |

Our business strategy may be unsuccessful and we may be unable to address the risks we face in a cost-effective manner, if at all. If we are unable to successfully accomplish these tasks, our business will be harmed.

| 5 |

Adequate funds for our operations may not be available, requiring us to raise additional financing or else curtail our activities significantly.

We may be required to raise additional funding through public or private financings, including equity financings, through 2019. Any additional equity financings may be dilutive to shareholders and may be completed at a discount to the then-current market price of our common stock. Debt financing, if available, would likely involve restrictive covenants on our operations or pertaining to future financing arrangements. Nevertheless, we may not successfully complete any future equity or debt financing. Adequate funds for our operations, whether from financial markets, collaborative or other arrangements, may not be available when needed or on terms attractive to us. If adequate funds are not available, our plans to operate our business may be adversely affected and we could be required to curtail our activities significantly and/or cease operating.

We are reliant on the continued support of a related party for adequate financing of our operations.

We may be required to raise additional funding through public or private financings, including equity financings, through 2019. As of the date of this filing, our majority shareholder and investor, Slipstream Communications LLC is the holder of 100% of our outstanding debt instruments including the term loan, secured revolving promissory note and convertible promissory notes. If we are unable to extend the maturity or replace our existing financing agreements in the future, our plans to operate our business may be adversely affected and we could be required to curtail our activities significantly and/or cease operating.

We may be unable to implement our business plan if we cannot raise sufficient capital and may be required to pay a high price for capital.

We will need to obtain additional capital to implement our business plan and meet our financial obligations as they become due. We may not be able to raise the additional capital needed or may be required to pay a high price for capital. Factors affecting the availability and price of capital may include the following:

| ● | the availability and cost of capital generally; |

| ● | our financial results; |

| ● | the experience and reputation of our management team; |

| ● | market interest, or lack of interest, in our industry and business plan; |

| ● | the trading volume of, and volatility in, the market for our common stock; |

| ● | our ongoing success, or failure, in executing our business plan; |

| ● | the amount of our capital needs; and |

| ● | the amount of debt, options, warrants, and convertible securities we have outstanding. |

We may be unable to meet our current or future obligations or to adequately exploit existing or future opportunities if we cannot raise sufficient capital. If we are unable to obtain capital for an extended period of time, we may be forced to discontinue operations.

| 6 |

We expect that there will be significant consolidation in our industry. Our failure or inability to lead that consolidation would have a severe adverse impact on our access to financing, customers, technology, and human resources.

Our industry is currently composed of a large number of relatively small businesses, no single one of which is dominant or which provides integrated solutions and product offerings incorporating much of the available technology. Accordingly, we believe that substantial consolidation may occur in our industry in the near future. If we do not play a positive role in that consolidation, either as a leader or as a participant whose capability is merged in a larger entity, we may be left out of this process, with product offerings of limited value compared with those of our competitors. Moreover, even if we lead the consolidation process, the market may not validate the decisions we make in that process.

Our success depends on our interactive marketing technologies achieving and maintaining widespread acceptance in our targeted markets.

Our success will depend to a large extent on broad market acceptance of our interactive marketing technologies among our current and prospective customers. Our prospective customers may still not use our solutions for a number of other reasons, including preference for static advertising, lack of familiarity with our technology, preference for competing technologies or perceived lack of reliability. We believe that the acceptance of our interactive marketing technologies by prospective customers will depend primarily on the following factors:

| ● | our ability to demonstrate the economic and other benefits attendant our marketing technologies; |

| ● | our customers becoming comfortable with using our interactive marketing technologies; and |

| ● | the reliability of our interactive marketing technologies. |

Our interactive technologies are complex and must meet stringent user requirements. Some undetected errors or defects may only become apparent as new functions are added to our technologies and products. The need to repair or replace products with design or manufacturing defects could temporarily delay the sale of new products and adversely affect our reputation. Delays, costs and damage to our reputation due to product defects could harm our business.

Our financial condition and potential for continued net losses may negatively impact our relationships with customers, prospective customers and third-party suppliers.

Our financial condition and potential for continued net losses may cause current and prospective customers to defer placing orders with us, to require terms that are less favorable to us, or to place their orders with competing marketing technology suppliers, which could adversely affect our business, financial condition and results of operations. On the same basis, third-party suppliers may refuse to do business with us, or may do so only on terms that are unfavorable to us, which also could cause our revenue to decline.

Because we do not have long-term purchase commitments from our customers, the failure to obtain anticipated orders or the deferral or cancellation of commitments could have adverse effects on our business.

Our business is characterized by short-term purchase orders and contracts that do not require that purchases be made. This makes forecasting our sales difficult. The failure to obtain anticipated orders and deferrals or cancellations of purchase commitments because of changes in customer requirements, or otherwise, could have a material adverse effect on our business, financial condition and results of operations. We have experienced such challenges in the past and may experience such challenges in the future.

| 7 |

Our continued growth could be adversely affected by the loss of several key customers, including a significant related party customer.

Our largest customers account for a majority of our total revenue on a consolidated basis. We had three customers that accounted for 56% of our revenue for each of the years ended December 31, 2017 and 2016. We had two customers that accounted for 67% and 49% of our revenue for the three months ended June 30, 2018 and 2017, respectively. We had two customers that accounted for 59% and 60% of revenue for the six months ended June 30, 2018 and 2017, respectively. One of these customers for all periods was a related party. We had two customers that accounted for 66% and 63% of accounts receivable as of June 30, 2018 and December 31, 2017, respectively. One of these customers for both periods was a related party.

Decisions by one or more of these key customers to not renew, terminate or substantially reduce their use of our products, technology, services, and platform could substantially slow our revenue growth and lead to a decline in revenue. Our business plan assumes continued growth in revenue, and it is unlikely that we will become profitable without a continued increase in revenue.

Our financial performance, condition and continued growth could be adversely affected by a key related party.

For the years ended December 31, 2017 and 2016, we had sales of $3,390 and $1,344, respectively, with a related party entity that was 22.5% owned by a member of senior management. Accounts receivable due from the related party was $3,017 and $543 at December 31, 2017 and 2016, respectively. For the quarter ended June 30, 2018, we had sales with this same related party entity which is now approximately 17.5% owned by a member of senior management. For the three and six months ended June 30, 2018, we had sales with a related party entity that is approximately 17.5% owned by a member of senior management. Sales to this related party were $618 and $1,035 for the three and six months ended June 30, 2018.

Most of our contracts are terminable by our customers with limited notice and without penalty payments, and early terminations could have a material effect on our business, operating results and financial condition.

Most of our contracts are terminable by our customers following limited notice and without early termination payments or liquidated damages due from them. In addition, each stage of a project often represents a separate contractual commitment, at the end of which the customers may elect to delay or not to proceed to the next stage of the project. We cannot assure you that one or more of our customers will not terminate a material contract or materially reduce the scope of a large project. The delay, cancellation or significant reduction in the scope of a large project or a number of projects could have a material adverse effect on our business, operating results and financial condition.

It is common for our current and prospective customers to take a long time to evaluate our products, most especially during economic downturns that affect our customers’ businesses. The lengthy and variable sales cycle makes it difficult to predict our operating results.

It is difficult for us to forecast the timing and recognition of revenue from sales of our products and services because our actual and prospective customers often take significant time to evaluate our products before committing to a purchase. Even after making their first purchases of our products and services, existing customers may not make significant purchases of those products and services for a long period of time following their initial purchases, if at all. The period between initial customer contact and a purchase by a customer may be years with potentially an even longer period separating initial purchases and any significant purchases thereafter. During the evaluation period, prospective customers may decide not to purchase or may scale down proposed orders of our products for various reasons, including:

| ● | reduced need to upgrade existing visual marketing systems; |

| ● | introduction of products by our competitors; |

| ● | lower prices offered by our competitors; and |

| ● | changes in budgets and purchasing priorities. |

Our prospective customers routinely require education regarding the use and benefit of our products. This may also lead to delays in receiving customers’ orders.

| 8 |

Our industry is characterized by frequent technological change. If we are unable to adapt our products and services and develop new products and services to keep up with these rapid changes, we will not be able to obtain or maintain market share.

The market for our products and services is characterized by rapidly changing technology, evolving industry standards, changes in customer needs, heavy competition and frequent new product and service introductions. If we fail to develop new products and services or modify or improve existing products and services in response to these changes in technology, customer demands or industry standards, our products and services could become less competitive or obsolete.

We must respond to changing technology and industry standards in a timely and cost-effective manner. We may not be successful in using new technologies, developing new products and services or enhancing existing products and services in a timely and cost-effective manner. Furthermore, even if we successfully adapt our products and services, these new technologies or enhancements may not achieve market acceptance.

A portion of our business involves the use of software technology that we have developed or licensed. Industries involving the ownership and licensing of software-based intellectual property are characterized by frequent intellectual-property litigation, and we could face claims of infringement by others in the industry. Such claims are costly and add uncertainty to our operational results.

A portion of our business involves our ownership and licensing of software. This market space is characterized by frequent intellectual-property claims and litigation. We could be subject to claims of infringement of third-party intellectual-property rights resulting in significant expense and the potential loss of our own intellectual-property rights. From time to time, third parties may assert copyright, trademark, patent or other intellectual-property rights to technologies that are important to our business. Any litigation to determine the validity of these claims, including claims arising through our contractual indemnification of our business partners, regardless of their merit or resolution, would likely be costly and time consuming and divert the efforts and attention of our management and technical personnel. If any such litigation resulted in an adverse ruling, we could be required to:

| ● | pay substantial damages; |

| ● | cease the development, use, licensing or sale of infringing products; |

| ● | discontinue the use of certain technology; or |

| ● | obtain a license under the intellectual property rights of the third party claiming infringement, which license may not be available on reasonable terms or at all. |

Our proprietary platform architectures and data tracking technology underlying certain of our services are complex and may contain unknown errors in design or implementation that could result in system performance failures or inability to scale.

The platform architecture, data tracking technology and integration layers underlying our proprietary platforms, our contract administration, procurement, timekeeping, content and network management, network services, device management, virtualized services, software automation and other tools, and back-end services are complex and include software and code used to generate customer invoices. This software and code is developed internally, licensed from third parties, or integrated by in-house personnel and third parties. Any of the system architecture, system administration, integration layers, software or code may contain errors, or may be implemented or interpreted incorrectly, particularly when they are first introduced or when new versions or enhancements to our tools and services are released. Consequently, our systems could experience performance failure or we may be unable to scale our systems, which may:

| ● | adversely impact our relationship with customers and others who experience system failure, possibly leading to a loss of affected and unaffected customers; |

| ● | increase our costs related to product development or service delivery; or |

| ● | adversely affect our revenues and expenses. |

| 9 |

Our business may be adversely affected by malicious applications that interfere with, or exploit security flaws in, our products and services.

Our business may be adversely affected by malicious applications that make changes to our customers’ computer systems and interfere with the operation and use of our products or products that impact our business. These applications may attempt to interfere with our ability to communicate with our customers’ devices. The interference may occur without disclosure to or consent from our customers, resulting in a negative experience that our customers may associate with our products and services. These applications may be difficult or impossible to uninstall or disable, may reinstall themselves and may circumvent other applications’ efforts to block or remove them. The ability to provide customers with a superior interactive marketing technology experience is critical to our success. If our efforts to combat these malicious applications fail, or if our products and services have actual or perceived vulnerabilities, there may be claims based on such failure or our reputation may be harmed, which would damage our business and financial condition.

We compete with other companies that have more resources, which puts us at a competitive disadvantage.

The market for interactive marketing technologies is generally highly competitive and we expect competition to increase in the future. Some of our competitors or potential competitors may have significantly greater financial, technical and marketing resources than us. These competitors may be able to respond more rapidly than we can to new or emerging technologies or changes in customer requirements. They may also devote greater resources to the development, promotion and sale of their products than us.

We expect competitors to continue to improve the performance of their current products and to introduce new products, services and technologies. Successful new product and service introductions or enhancements by our competitors could reduce sales and the market acceptance of our products and services, cause intense price competition or make our products and services obsolete. To be competitive, we must continue to invest significant resources in research and development, sales and marketing and customer support. If we do not have sufficient resources to make these investments or are unable to make the technological advances necessary to be competitive, our competitive position will suffer. Increased competition could result in price reductions, fewer customer orders, reduced margins and loss of market share. Our failure to compete successfully against current or future competitors could adversely affect our business and financial condition.

Our future success depends on key personnel and our ability to attract and retain additional personnel.

Our key personnel include:

| ● | Richard Mills, our Chief Executive Officer; |

| ● | John Walpuck, our Chief Operating Officer; and |

| ● | Will Logan, our Chief Financial Officer |

If we fail to retain our key personnel or to attract, retain and motivate other qualified employees, our ability to maintain and develop our business may be adversely affected. Our future success depends significantly on the continued service of our key technical, sales and senior management personnel and their ability to execute our growth strategy. The loss of the services of our key employees could harm our business. We may be unable to retain our employees or to attract, assimilate and retain other highly qualified employees who could migrate to other employers who offer competitive or superior compensation packages.

Unpredictability in financing markets could impair our ability to grow our business through acquisitions.

We anticipate that opportunities to acquire similar businesses will materially depend on the availability of financing alternatives with acceptable terms. As a result, poor credit and other market conditions or uncertainty in financial markets could materially limit our ability to grow through acquisitions since such conditions and uncertainty make obtaining financing more difficult.

| 10 |

We are subject to cyber security risks and interruptions or failures in our information technology systems. A cyber incident could occur and result in information theft, data corruption, operational disruption and/or financial loss.

We depend on digital technologies to process and record financial and operating data and rely on sophisticated information technology systems and infrastructure to support our business, including process control technology. At the same time, cyber incidents, including deliberate attacks, have increased. The U.S. government has issued public warnings that indicate that energy assets might be specific targets of cyber security threats. Our technologies, systems and networks and those of our vendors, suppliers and other business partners may become the target of cyberattacks or information security breaches that could result in the unauthorized release, gathering, monitoring, misuse, loss or destruction of proprietary and other information, or other disruption of business operations. In addition, certain cyber incidents, such as surveillance, may remain undetected for an extended period. Our systems for protecting against cyber security risks may not be sufficient. As the sophistication of cyber incidents continues to evolve, we will likely be required to expend additional resources to continue to modify or enhance our protective measures or to investigate and remediate any vulnerability to cyber incidents. Additionally, any of these systems may be susceptible to outages due to fire, floods, power loss, telecommunications failures, usage errors by employees, computer viruses, cyber-attacks or other security breaches or similar events. The failure of any of our information technology systems may cause disruptions in our operations, which could adversely affect our revenues and profitability.

Our reliance on information management and transaction systems to operate our business exposes us to cyber incidents and hacking of our sensitive information if our outsourced service provider experiences a security breach.

Effective information security internal controls are necessary for us to protect our sensitive information from illegal activities and unauthorized disclosure in addition to denial of service attacks and corruption of our data. In addition, we rely on the information security internal controls maintained by our outsourced service provider. Breaches of our information management system could also adversely affect our business reputation. Finally, significant information system disruptions could adversely affect our ability to effectively manage operations or reliably report results.

Because our technology, products, platform, and services are complex and are deployed in and across complex environments, they may have errors or defects that could seriously harm our business.

Our technology, proprietary platforms, products and services are highly complex and are designed to operate in and across data centers, large and complex networks, and other elements of the digital media workflow that we do not own or control. On an ongoing basis, we need to perform proactive maintenance services on our platform and related software services to correct errors and defects. In the future, there may be additional errors and defects in our software that may adversely affect our services. We may not have in place adequate reporting, tracking, monitoring, and quality assurance procedures to ensure that we detect errors in our software in a timely manner. If we are unable to efficiently and cost-effectively fix errors or other problems that may be identified, or if there are unidentified errors that allow persons to improperly access our services, we could experience loss of revenues and market share, damage to our reputation, increased expenses and legal actions by our customers.

We may have insufficient network or server capacity, which could result in interruptions in our services and loss of revenues.

Our operations are dependent in part upon: network capacity provided by third-party telecommunications networks; data center services provider owned and leased infrastructure and capacity; our dedicated and virtualized server capacity located at its data center services provider partner and a geo-redundant micro-data center location; and our own infrastructure and equipment. Collectively, this infrastructure, equipment, and capacity must be sufficiently robust to handle all of our customers’ web-traffic, particularly in the event of unexpected surges in high-definition video traffic and network services incidents. We may not be adequately prepared for unexpected increases in bandwidth and related infrastructure demands from our customers. In addition, the bandwidth we have contracted to purchase may become unavailable for a variety of reasons, including payment disputes, outages, or such service providers going out of business. Any failure of these service providers or our own infrastructure to provide the capacity we require, due to financial or other reasons, may result in a reduction in, or interruption of, service to our customers, leading to an immediate decline in revenue and possible additional decline in revenue as a result of subsequent customer losses.

We do not have sufficient capital to engage in material research and development, which may harm our long-term growth.

In light of our limited resources in general, we have made no material investments in research and development over the past several years. This conserves capital in the short term. In the long term, as a result of our failure to invest in research and development, our technology and product offerings may not keep pace with the market and we may lose any existing competitive advantage. Over the long term, this may harm our revenues growth and our ability to become profitable.

Our business operations are susceptible to interruptions caused by events beyond our control.

Our business operations are susceptible to interruptions caused by events beyond our control. We are vulnerable to the following potential problems, among others:

| ● | our platform, technology, products, and services and underlying infrastructure, or that of our key suppliers, may be damaged or destroyed by events beyond our control, such as fires, earthquakes, floods, power outages or telecommunications failures; |

| ● | we and our customers and/or partners may experience interruptions in service as a result of the accidental or malicious actions of Internet users, hackers or current or former employees; |

| 11 |

| ● | we may face liability for transmitting viruses to third parties that damage or impair their access to computer networks, programs, data or information. Eliminating computer viruses and alleviating other security problems may require interruptions, delays or cessation of service to our customers; and |

| ● | failure of our systems or those of our suppliers may disrupt service to our customers (and from our customers to their customers), which could materially impact our operations (and the operations of our customers), adversely affect our relationships with our customers and lead to lawsuits and contingent liability. |

The occurrence of any of the foregoing could result in claims for consequential and other damages, significant repair and recovery expenses and extensive customer losses and otherwise have a material adverse effect on our business, financial condition and results of operations.

General global market and economic conditions may have an adverse impact on our operating performance and results of operations.

Our business has been and could continue to be affected by general global economic and market conditions. Weakness in the United States and worldwide economy has had and could continue to have a negative effect on our operating results, including a decrease in revenue and operating cash flow. To the extent our customers are unable to profitably leverage various forms of digital marketing technology and solutions, and/or the content we create, deliver and publish on their behalf, they may reduce or eliminate their purchase of our products and services. Such reductions in traffic would lead to a reduction in our revenues. Additionally, in a down-cycle economic environment, we may experience the negative effects of increased competitive pricing pressure, customer loss, slowdown in commerce over the Internet and corresponding decrease in traffic delivered over our network and failures by our customers to pay amounts owed to us on a timely basis or at all. Suppliers on which we rely for equipment, field services, servers, bandwidth, co-location and other services could also be negatively impacted by economic conditions that, in turn, could have a negative impact on our operations or revenues. Flat or worsening economic conditions may harm our operating results and financial condition.

The markets in which we operate are rapidly emerging, and we may be unable to compete successfully against existing or future competitors to our business.

The market in which we operate is becoming increasingly competitive. Our current competitors generally include general digital signage companies, specialized digital signage operators targeting certain vertical markets (e.g., financial services), content management software companies, or integrators and vertical solution providers who develop single implementations of content distribution, digital marketing technology, and related services. These competitors, including future new competitors who may emerge, may be able to develop a comparable or superior solution capabilities, software platform, technology stack, and/or series of services that provide a similar or more robust set of features and functionality than the technology, products and services we offer. If this occurs, we may be unable to grow as necessary to make our business profitable.

Whether or not we have superior products, many of these current and potential future competitors have a longer operating history in their current respective business areas and greater market presence, brand recognition, engineering and marketing capabilities, and financial, technological and personnel resources than we do. Existing and potential competitors with an extended operating history, even if not directly related to our business, have an inherent marketing advantage because of the reluctance of many potential customers to entrust key operations to a company that may be perceived as unproven. In addition, our existing and potential future competitors may be able to use their extensive resources to:

| ● | develop and deploy new products and services more quickly and effectively than we can; |

| ● | develop, improve and expand their platforms and related infrastructures more quickly than we can; |

| ● | reduce costs, particularly hardware costs, because of discounts associated with large volume purchases and longer term relationships and commitments; |

| ● | offer less expensive products, technology, platform, and services as a result of a lower cost structure, greater capital reserves or otherwise; |

| ● | adapt more swiftly and completely to new or emerging technologies and changes in customer requirements; |

| ● | take advantage of acquisition and other opportunities more readily; and |

| ● | devote greater resources to the marketing and sales of their products, technology, platform, and services. |

If we are unable to compete effectively in our various markets, or if competitive pressures place downward pressure on the prices at which we offer our products and services, our business, financial condition and results of operations may suffer.

| 12 |

RISKS RELATED TO THIS OFFERING AND OUR COMPANY

Because of our limited resources, we may not have in place various processes and protections common to more mature companies and may be more susceptible to adverse events.

We have limited resources subsequent to the restructuring and integration costs incurred in connection with prior acquisition activities. As a result, we may not have in place systems, processes and protections that many of our competitors have or that may be essential to protect against various risks. For example, we have in place only limited resources and processes addressing human resources, timekeeping, data protection, business continuity, personnel redundancy, and knowledge institutionalization concerns. As a result, we are at risk that one or more adverse events in these and other areas may materially harm our business, balance sheet, revenues, expenses or prospects.

Failure to achieve and maintain effective internal controls could limit our ability to detect and prevent fraud and thereby adversely affect our business and stock price.

Effective internal controls are necessary for us to provide reliable financial reports. Nevertheless, all internal control systems, no matter how well designed, have inherent limitations. Even those systems determined to be effective can provide only reasonable assurance with respect to financial statement preparation and presentation. Our inability to maintain an effective control environment may cause investors to lose confidence in our reported financial information, which could in turn have a material adverse effect on our stock price. We have identified several material weaknesses in internal controls and have concluded in our 2017 and 2018 filings that our disclosure controls and procedures and internal controls over financial reporting were not effective at the reasonable assurance level.

Our controlling shareholder possesses controlling voting power with respect to our common stock and voting preferred stock, which will limit your influence on corporate matters.

Our controlling shareholder, Slipstream Communications, LLC, has beneficial ownership of 80,756,141 shares of common stock, including common shares that are beneficially owned by an affiliate of Slipstream Communications named Slipstream Funding, LLC. These shares represent beneficial ownership of approximately 57.80% of our common stock (on an as-converted basis, and assuming no other convertible securities, options and warrants are converted or exercised) as of the date of September 20, 2018. In addition, in the last quarter of 2016 and the first quarter of 2017, Slipstream Communications, LLC purchased all of our outstanding debt from the original debtholders. The terms of the debt have remained the same. As a result, Slipstream Funding has the ability to control our management and affairs through the election and removal of our entire Board of Directors and all other matters requiring shareholder approval, including the future merger, consolidation or sale of all or substantially all of our assets. This concentrated control could discourage others from initiating any potential merger, takeover or other change-of-control transaction that may otherwise be beneficial to our shareholders. Furthermore, this concentrated control will limit the practical effect of your participation in Company matters, through shareholder votes and otherwise.

Our Articles of Incorporation grant our Board of Directors the power to issue additional shares of common and preferred stock and to designate other classes of preferred stock, all without shareholder approval.

Our authorized capital consists of 250 million shares of capital stock. Pursuant to authority granted by our Articles of Incorporation, our Board of Directors, without any action by our shareholders, may designate and issue shares in such classes or series (including other classes or series of preferred stock) as it deems appropriate and establish the rights, preferences and privileges of such shares, including dividends, liquidation and voting rights, provided it is consistent with Minnesota law. The rights of holders of other classes or series of stock that may be issued could be superior to the rights of holders of our common shares. The designation and issuance of shares of capital stock having preferential rights could adversely affect other rights appurtenant to shares of our common stock. Furthermore, any issuances of additional stock (common or preferred) will dilute the percentage of ownership interest of then-current holders of our capital stock and may dilute our book value per share.

| 13 |

Significant issuances of our common stock, or the perception that significant issuances may occur in the future, could adversely affect the market price for our common stock.

Significant actual or perceived potential future issuance of our common stock could adversely affect the market price of our common stock. Generally, issuances of substantial amounts of common stock in the public market, and the availability of shares for future sale, could adversely affect the prevailing market price of our common stock and could cause the market price of our common stock to remain low for a substantial amount of time.

We cannot foresee the impact of potential securities issuances of common shares on the market for our common stock, but it is possible that the market for our shares may be adversely affected, perhaps significantly. It is also unclear whether or not the market for our common stock could absorb a large number of attempted sales in a short period of time, regardless of the price at which they might be offered.

Our common stock trades only in an illiquid trading market.

Trading of our common stock is conducted on the OTC Markets (OTCQX). This has an adverse effect on the liquidity of our common stock, not only in terms of the number of shares that can be bought and sold at a given price, but also through delays in the timing of transactions and reduction in security analysts’ and the media’s coverage of us and our common stock. This may result in lower prices for our common stock than might otherwise be obtained and could also result in a larger spread between the bid and asked prices for our common stock.

There is not now and there may not ever be an active market for shares of our common stock.

In general, there has been minimal trading volume in our common stock. The small trading volume will likely make it difficult for our shareholders to sell their shares as and when they choose. Furthermore, small trading volumes are generally understood to depress market prices. As a result, you may not always be able to resell shares of our common stock publicly at the time and prices that you feel are fair or appropriate.

We do not intend to pay dividends on our common stock for the foreseeable future. We will, however, pay dividends on our Series A Convertible Preferred Stock.

When permitted by Minnesota law, we are required to pay dividends to the holders of our Series A Convertible Preferred Stock, each share of which carries a $1.00 stated value. There are presently 5,535,192 shares of Series A Convertible Preferred Stock outstanding. Our Series A Convertible Preferred Stock entitles its holders to:

| ● | a cumulative 6% dividend, payable on a semi-annual basis in cash unless (i) we are unable to pay the dividend in cash under applicable law, or (ii) we have not demonstrated positive cash flow during the prior quarter reported on our Form 10-Q, in which case we may at our election pay the dividend through either the issuance of additional shares of preferred stock or, from and after the three-year anniversary of the issuance of the preferred stock in duly authorized, validly issued, fully paid and non-assessable shares of common stock; |

| ● | in the event of a liquidation or dissolution of the Company, a preference in the amount of all accrued but unpaid dividends plus the stated value of such shares before any payment shall be made or any assets distributed to the holders of any junior securities, including our common stock; |

| ● | convert their preferred shares into our common shares at a conversion rate that is presently $0.255 per share (the equivalent of approximately 3.92 shares of common for each full share of preferred stock converted), subject, however, to full-ratchet price protection in the event that we issue common stock below the then-current conversion price (subject to certain customary exceptions); and |

| ● | vote their preferred shares on an as-if-converted basis. |

| 14 |

We have the right to call and redeem some or all of such preferred shares, subject to a 30-day notice period and certain other conditions, at a price equal to $1.00 per share plus accrued but unpaid dividends thereon. Holders of Series A Convertible Preferred Stock have no preemptive or cumulative-voting rights.

We do not anticipate that we will pay any dividends for the foreseeable future on our common stock. Accordingly, any return on an investment in us will be realized only when you sell shares of our common stock. When legally permitted, we must expect to pay dividends to our preferred shareholders.

We do not have significant tangible assets that could be sold upon liquidation.

We have nominal tangible assets. As a result, if we become insolvent or otherwise must dissolve, there will be no tangible assets to liquidate and no corresponding proceeds to disburse to our shareholders. If we become insolvent or otherwise must dissolve, shareholders will likely not receive any cash proceeds on account of their shares.

Because of our early stage of operations and limited resources, we may not have in place various systems capabilities, processes and protections common to more mature companies and may be more susceptible to adverse events.

We are in an early stage of operations and have limited resources. As a result, we may not have in place systems, processes and protections that many of our competitors have or that may be essential to protect against various risks. For example, we have in place only limited resources and processes addressing human resources, timekeeping, data protection, business continuity, personnel redundancy, and knowledge institutionalization concerns. As a result, we are at risk that one or more adverse events in these and other areas may materially harm our business, balance sheet, revenues, expenses or prospects.

| 15 |

RISKS RELATING TO OUR PROPOSED ACQUISTION OF ALLURE GLOBAL SOLUTIONS, INC.

The loss of the services of certain key management personnel at Allure could impair our ability to execute our business strategy and as a result, reduce our sales and profitability.

We depend on the continued services of our senior management team. As we integrate and combine Allure with our business, the loss of key personnel at Allure could have a material adverse effect on our ability to execute our business strategy and on our financial condition and results of operations. Allure does not maintain key-person insurance for members of its senior management team and we do not anticipate obtaining any such insurance after our acquisition of Allure.

We may be unable to successfully integrate Allure with our business, which could cause our business to suffer.