Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended January 2, 2016

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 000-52059

PGT, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 20-0634715 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 1070 Technology Drive North Venice, Florida |

34275 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code:

(941) 480-1600

Former name, former address and former fiscal year, if changed since last report: Not applicable

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Exchange on Which Registered | |

| Common stock, par value $0.01 per share | NASDAQ Global Market |

Securities registered pursuant to Section 12 (g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “accelerated filer,” “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant as of July 2, 2015 was approximately $676,375,083 based on the closing price per share on that date of $14.33 as reported on the NASDAQ Global Market.

The number of shares of the registrant’s common stock, par value $0.01, outstanding as of February 29, 2016, was 48,899,102.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company’s Proxy Statement for the Company’s 2016 Annual Meeting of Stockholders are incorporated by reference into Part III of this Form 10-K.

Table of Contents

PGT, INC.

Table of Contents to Form 10-K

- 2 -

Table of Contents

| Item 1. | BUSINESS |

GENERAL DEVELOPMENT OF BUSINESS

Description of the Company

We are the leading U.S. manufacturer and supplier of residential impact-resistant windows and doors and pioneered the U.S. impact-resistant window and door industry. Our PGT impact-resistant products, which are marketed under the WinGuard®, PremierVue ™, PGT Architectural Systems and PGT Commercial Storefront System brand names, combine heavy-duty aluminum or vinyl frames with laminated glass to provide protection from hurricane-force winds and wind-borne debris by maintaining their structural integrity and preventing penetration by impacting objects. Impact-resistant windows and doors satisfy stringent building codes in hurricane-prone coastal states and provide an attractive alternative to shutters and other “active” forms of hurricane protection that require installation and removal before and after each storm. Combining the impact resistance of WinGuard, PremierVue ™ , PGT Architectural Systems, and PGT Commercial Storefront System with our insulating glass creates energy efficient windows that can significantly reduce cooling and heating costs. We also manufacture non-impact resistant products in both aluminum and vinyl frames including our SpectraGuard ™ line of products. Our current market share in Florida, which is the largest U.S. impact-resistant window and door market, is significantly greater than that of any of our competitors.

At our manufacturing facilities in North Venice, Florida, where we have nearly 2,000 employees, we produce fully-customized windows and doors. We are vertically integrated with glass insulating, tempering and laminating facilities, which provide us with a consistent source of impact-resistant laminated and insulating glass, shorter lead times, and lower costs relative to third-party sourcing.

On September 22, 2014, we completed the acquisition of CGI Windows and Doors Holdings, Inc. (CGI) which became a wholly-owned subsidiary of PGT Industries, Inc. CGI was established in 1992 and has consistently built a reputation based on designing and manufacturing quality impact resistant products that meet or exceed the stringent Miami-Dade County impact standards. CGI has over 300 employees at its manufacturing plant in Miami, Florida. Today, CGI continues to lead as an innovator in product craftsmanship, strength and style, and its brands are highly recognized and respected by the architectural community. CGI product lines include the Estate Collection, Sentinel by CGI, Estate Entrances, Commercial Series and Targa by CGI.

On February 16, 2016, we completed the acquisition of WinDoor, Incorporated (WinDoor), a provider of high-performance, impact-resistant windows and doors for five-star resorts, luxury high-rise condominiums, hotels and custom residential homes. WinDoor is now a wholly-owned subsidiary of PGT Industries, Inc. With approximately 200 employees at its manufacturing and administrative facilities in Orlando, Florida, WinDoor manufactures high-end-high quality aluminum and thermally-broken aluminum and vinyl products, featuring windows, sliding glass doors, and terrace doors.

The geographic regions in which we currently conduct business include the Southeastern U.S., Gulf Coast, Coastal mid-Atlantic, the Caribbean, Central America, and Canada. We distribute our products through multiple channels, including approximately 1,200 window distributors, building supply distributors, window replacement dealers and enclosure contractors. This broad distribution network provides us with the flexibility to meet demand as it shifts between the residential new construction and repair and remodeling end markets.

History

Our subsidiary, PGT Industries, Inc., a Florida Corporation, was founded in 1980 as Vinyl Tech, Inc. The PGT brand was established in 1987, and we introduced our WinGuard branded product line in the aftermath of Hurricane Andrew in 1992. CGI became a wholly-owned subsidiary of PGT Industries, Inc. on September 22, 2014. WinDoor became a wholly-owned subsidiary of PGT Industries, Inc. on February 16, 2016.

PGT, Inc. is a Delaware corporation formed on December 16, 2003, and on June 27, 2006, we became a publicly listed company on the NASDAQ Global Market under the symbol “PGTI”.

FINANCIAL INFORMATION ABOUT INDUSTRY SEGMENTS

We operate as one segment, the manufacture and sale of windows and doors. Additional required information is included in Item 8.

- 3 -

Table of Contents

NARRATIVE DESCRIPTION OF BUSINESS

Due to the recentness of our acquisition of WinDoor, the following narrative description of our business does not yet include complete information relating to WinDoor, which we expect to include in a future periodic filing with the SEC. For more information regarding WinDoor, its business and products, please go to http://www.windoorinc.com.

Our Products

We manufacture complete lines of premium, fully customizable aluminum and vinyl windows and doors and porch enclosure products targeting both the residential new construction and repair and remodeling end markets. All of our PGT products carry the PGT brand, and our consumer-oriented PGT products carry an additional, trademarked product name, including WinGuard, Eze-Breeze, SpectraGuard, PremierVue, WinGuard Vinyl and EnergyVue. CGI’s products carry the CGI brand and carry the trademarked product names of Estate Collection, Sentinel by CGI, Estate Entrances, Commercial Series and Targa by CGI.

Window and door products

Impact window and door products

WinGuard. WinGuard is an impact-resistant product line and combines heavy-duty aluminum or vinyl frames with laminated glass to provide protection from hurricane-force winds and wind-borne debris that satisfy increasingly stringent building codes and primarily target hurricane-prone coastal states in the U.S., as well as the Caribbean and Central America. Combining the impact resistance of WinGuard with our insulating glass creates energy efficient windows that can significantly reduce cooling and heating costs. In the first quarter of 2015, we announced the launch of our new WinGuard Vinyl line of windows and doors, our all-new impact-resistant vinyl window designed to offer some of the highest design pressures available on impact-resistant windows and doors and in an attractive modern profile, with larger sizes capable of handling the toughest hurricane codes in the country. It also protects against flying debris, intruders, outside noise and UV rays making it a top choice for customers seeking an impact-resistant window.

PremierVue. PremierVue is a complete line of impact-resistant vinyl window and door products that are tailored for the mid- to high-end of the replacement market, primarily targeting single and multi-family homes and low to mid-rise condominiums in Florida and other coastal regions of the Southeastern U.S. Combining structural strength and energy efficiency, these products are designed for flexibility in today’s market, offering both laminated and ENERGY STAR® rated laminated-insulated impact-resistant glass

Architectural Systems. Similar to WinGuard, Architectural Systems products are impact-resistant, offering protection from hurricane-force winds and wind-borne debris for mid- and high-rise buildings rather than single family homes.

Estate Collection. Our Estate Collection of windows and doors is CGI’s premium, high-end aluminum impact-resistant product line. These windows and doors can be found in elegant homes, prestigious resorts, hotels, schools and office buildings. Our Estate Collection combines best-in-class performance against hurricane force damage with architectural-grade quality, handcrafted details and superior engineering. Similar to WinGuard, Estate windows and doors protect and insulate against every imaginable external event, from hurricanes to UV protection, outside noise and forced entry. Estate’s aluminum frames are up to 100% thicker than many of our competitors making it an excellent choice for any coastal area prone to hurricanes.

Sentinel. Sentinel is a complete line of aluminum impact-resistant windows and doors from CGI that provide exceptional quality, craftsmanship, energy efficiency and durability at an affordable price. Sentinel windows and doors are manufactured to enhance the aesthetics of the home while delivering protection from the most extreme coastal conditions. Sentinel is custom manufactured to exact sizes within our wide range of design parameters, therefore, reducing on-site construction costs. In addition, Sentinel’s frame depth is designed for both new construction and replacement applications resulting in faster, less intrusive installations.

Targa. Targa is CGI’s line of vinyl energy-efficient, impact-resistant windows designed specifically to exceed the Florida impact codes, the most stringent impact standards in the U.S. Targa windows enhance the aesthetics of a home and are low maintenance windows with long-term durability, and environmental compatibility.

- 4 -

Table of Contents

Other window and door products

EnergyVue. EnergyVue is our all new non-impact vinyl window featuring energy-efficient insulating glass and multi-chambered frames that meet or exceed ENERGY STAR® standards in all climate zones to help save consumers on energy costs. The new design has a refined modern profile combined with robust construction to make larger sizes and higher design pressures an unparalleled offering. We rounded out the line with one of the industry’s most extensive selection of frame colors and a variety of hardware finishes, glass tints, grid styles and patterns for our customers. We announced the launch of EnergyVue in the first quarter of 2015.

Aluminum. We offer a complete line of fully customizable, non-impact-resistant aluminum frame windows and doors. These products primarily target regions with warmer climates, where aluminum is often preferred due to its ability to withstand higher structural loads. Adding our insulating glass creates energy-efficient windows that can significantly reduce cooling and heating costs.

Eze-Breeze. Eze-Breeze non-glass vertical and horizontal sliding panels for porch enclosures are vinyl-glazed, aluminum-framed products used for enclosing screened-in porches that provide protection from inclement weather. This line was completed with the addition of a cabana door.

PGT Commercial Storefront System. PGT’s Commercial Storefront window system and entry doors, launched in 2013, are engineered to provide a flexible yet economical solution for a variety of applications. Our system provides easy fabrication and assembly, while also reducing installation time and challenges.

Sales and Marketing

Our sales strategy primarily focuses on attracting and retaining distributors and dealers by consistently providing exceptional customer service, leading product designs and quality, and competitive pricing all using our advanced knowledge of building code requirements and technical expertise.

Our marketing strategy is designed to reinforce the high quality of our products and focuses on both coastal and inland markets. We support our markets through print and web-based advertising, consumer, dealer, and builder promotions, and selling and collateral materials. We also work with our dealers and distributors to educate architects, building officials, consumers and homebuilders on the advantages of using impact-resistant and energy-efficient products. We market our products based on quality, building code compliance, outstanding service, shorter lead times, and on-time delivery using our fleet of trucks and trailers.

Our Customers

We have a highly diversified customer base that is comprised of approximately 1,200 window distributors, building supply distributors, window replacement dealers and enclosure contractors. Our largest customer accounts for approximately 4% of net sales and our top ten customers account for approximately 18% of net sales. Our sales are comprised of residential new construction and home repair and remodeling end markets, which represented approximately 41% and 59% of our sales, respectively, during 2015. This compares to 38% and 62%, respectively, in 2014.

We do not supply our products directly to homebuilders, but believe demand for our products is also a function of our strong relationships with a number of national homebuilders.

- 5 -

Table of Contents

Materials and Supplier Relationships

Our primary manufacturing materials include aluminum and vinyl extrusions, glass, ionoplast, and polyvinyl butyral. Although in many instances we have agreements with our suppliers, these agreements are generally terminable by either party on limited notice. All of our materials are typically readily available from other sources. Aluminum and vinyl extrusions accounted for approximately 37% of our material purchases during fiscal year 2015. Sheet glass, which is sourced from two major national suppliers, accounted for approximately 14% of our material purchases during fiscal year 2015. Sheet glass that we purchase comes in various sizes, tints, and thermal properties. From the sheet glass purchased, we produce most of our own laminated glass needs. However, in 2015 due to some temporary capacity constraints, we did purchase some of our laminated glass needs from one major national supplier. This finished laminated glass made up approximately 13% of our material purchases in fiscal year 2015. Polyvinyl butyral and ionoplast, which are both used as inner layer in laminated glass, accounted for approximately 11% of our material purchases during fiscal year 2015.

Backlog

As of January 2, 2016, our backlog was $31.6 million. As of January 3, 2015, our backlog was $28.0 million. Our backlog consists of orders that we have received from customers that have not yet shipped, and we expect that substantially all of our current backlog will be recognized as sales in the first quarter of 2016, due in part to our lead times which range from one to five weeks.

Intellectual Property

We own and have registered trademarks in the United States. In addition, we own several patents and patent applications concerning various aspects of window assembly and related processes. We are not aware of any circumstances that would have a material adverse effect on our ability to use our trademarks and patents. As long as we continue to renew our trademarks when necessary, the trademark protection provided by them is perpetual.

Manufacturing

Our manufacturing facilities are located in Florida where we produce fully-customized products. The manufacturing process typically begins in our glass plant where we cut, temper, laminate, and insulate sheet glass to meet specific requirements of our customers’ orders.

Glass is transported to our window and door assembly lines in a make-to-order sequence where it is combined with an aluminum or vinyl frame. These frames are also fabricated to order. We start with a piece of extruded material which is cut and shaped into a frame that fits the customers’ specifications. Once complete, product is immediately staged for delivery and generally shipped on our trucking fleet within 48 hours of completion.

Competition

The window and door industry is highly fragmented, and the competitive landscape is based on geographic scope. The competition falls into the following categories.

Local and Regional Window and Door Manufacturers: This group of competitors consists of numerous local job shops and small manufacturing facilities that tend to focus on selling products to local or regional dealers and wholesalers. Competitors in this group typically lack marketing support and the service levels and quality controls demanded by larger distributors, as well as the ability to offer a full complement of products.

National Window and Door Manufacturers: This group of competitors tends to focus on selling branded products nationally to dealers and wholesalers and has multiple locations.

Active Protection: This group of competitors consists of manufactures that produce shutters and plywood, both of which are used to actively protect openings. Our impact windows and doors represent passive protection, meaning, once installed, no activity is required to protect a home from storm related hazards.

The principal methods of competition in the window and door industry are the development of long-term relationships with window and door dealers and distributors, and the retention of customers by delivering a full range of high-quality products on time while offering competitive pricing and flexibility in transaction processing. Trade professionals such as contractors, homebuilders, architects and engineers also engage in direct interaction and look to the manufacturer for training and education of product and code. Although some of our competitors may have greater geographic scope and access to greater resources and economies of scale than do we, our leading position in the U.S. impact-resistant window and door market, and the award winning designs and high quality of our products, position us well to meet the needs of our customers.

- 6 -

Table of Contents

Environmental Considerations

Although our business and facilities are subject to federal, state, and local environmental regulation, environmental regulation does not have a material impact on our operations, and we believe that our facilities are in material compliance with such laws and regulations.

Employees

As of the end of 2015, we employed approximately 2,300 people, including approximately 310 people at CGI, none of whom were represented by a collective bargaining unit. We believe we have good relations with our employees.

FINANCIAL INFORMATION ABOUT GEOGRAPHIC AREAS

Our domestic and international net sales for each of the three years ended January 2, 2016, January 3, 2015, and December 28, 2013, are as follows (in millions):

| Year Ended | ||||||||||||

| January 2, | January 3, | December 28, | ||||||||||

| 2016 | 2015 | 2013 | ||||||||||

| Domestic |

$ | 371.0 | $ | 295.8 | $ | 232.7 | ||||||

| International |

18.8 | 10.6 | 6.6 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total net sales |

$ | 389.8 | $ | 306.4 | $ | 239.3 | ||||||

|

|

|

|

|

|

|

|||||||

AVAILABLE INFORMATION

Our Internet address is www.pgtindustries.com. Through our Internet website under “Financial Information” in the Investors section, we make available free of charge, as soon as reasonably practical after such information has been filed with the SEC, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed pursuant to Section 13(a) or 15(d) of the Securities Exchange Act. Also available through our Internet website under “Corporate Governance” in the Investors section are our Code of Business Conduct and Ethics and our supplemental Code of Ethics for Senior Officers. We are not including this or any other information on our website as a part of, nor incorporating it by reference into this Form 10-K, or any of our other SEC filings. The SEC maintains an Internet site that contains our reports, proxy and information statements, and other information that we file electronically with the SEC at www.sec.gov.

| Item 1A. | RISK FACTORS |

We are subject to regional and national economic conditions. The economy in Florida and throughout the United States could negatively impact demand for our products as it has in the past, and macroeconomic forces such as employment rates and the availability of credit could have an adverse effect on our sales and results of operations.

New home construction while improving, remains below average. Also repair and remodeling markets are subject to many economic factors. Accordingly, either market could decline and lower the demand for, and the pricing of, our products, which could adversely affect our results. The window and door industry is subject to the cyclical market pressures of the larger new construction and repair and remodeling markets. In turn, these changes may be affected by adverse changes in economic conditions such as demographic trends, employment levels, interest rates, and consumer confidence. A decline in the economic environment or new home construction could negatively impact our sales and earnings.

Economic and credit market conditions impact our ability to collect receivables. Economic and credit conditions can negatively impact our bad debt expense, which can adversely impact our results of operations. If economic and credit conditions deteriorate, our results of operations may be adversely impacted by bad debts.

We are subject to fluctuations in the prices of our raw materials. We experience significant fluctuations in the cost of our raw materials, including aluminum extrusion, vinyl extrusion, polyvinyl butyral and glass. A variety of factors over which we have no control, including global demand for aluminum, fluctuations in oil prices, speculation in commodities futures and the creation of new

- 7 -

Table of Contents

laminates or other products based on new technologies impact the cost of raw materials which we purchase for the manufacture of our products. While we attempt to minimize our risk from severe price fluctuations by entering into aluminum forward contracts to hedge these fluctuations in the purchase price of aluminum extrusion we use in production, substantial, prolonged upward trends in aluminum prices could significantly increase the cost of the unhedged portions of our aluminum needs and have an adverse impact on our results of operations. We anticipate that these fluctuations will continue in the future. While we have entered into supply agreements with major producers of our primary raw materials that we believe provides us with reliable sources for certain of our raw materials with stable pricing on favorable terms, if one or both parties to the agreements do not satisfy the terms of the agreements, they may be terminated which could result in our inability to obtain certain raw materials on commercially reasonable terms having an adverse impact on our results of operations. While historically we have to some extent been able to pass on significant cost increases to our customers, our results between periods may be negatively impacted by a delay between the cost increases and price increases in our products.

We depend on third-party suppliers for our raw materials. Our ability to offer a wide variety of products to our customers depends on receipt of adequate material supplies from manufacturers and other suppliers. Generally, our raw materials and supplies are obtainable from various sources and in sufficient quantities. However, it is possible that our competitors or other suppliers may create laminates or products based on new technologies that are not available to us or are more effective than our products at surviving hurricane-force winds and wind-borne debris or that they may have access to products of a similar quality at lower prices. Although in many instances we have agreements with our suppliers, these agreements are generally terminable by either party on limited notice. Moreover, we do not have long-term contracts with the suppliers of all of our raw materials.

Transportation costs represent a significant part of our cost structure. A rapid and prolonged increase in fuel prices may significantly increase our costs and have an adverse impact on our results of operations.

The home building industry and the home repair and remodeling sector are regulated. The homebuilding industry and the home repair and remodeling sector are subject to various local, state, and federal statutes, ordinances, rules, and regulations concerning zoning, building design and safety, construction, and similar matters, including regulations that impose restrictive zoning and density requirements in order to limit the number of homes that can be built within the boundaries of a particular area. Increased regulatory restrictions could limit demand for new homes and home repair and remodeling products and could negatively affect our sales and results of operations.

Our operating results are substantially dependent on sales of our branded impact-resistant products. A majority of our net sales are, and are expected to continue to be, derived from the sales of our branded impact-resistant products. Accordingly, our future operating results will depend on the demand for our impact-resistant products by current and future customers, including additions to this product line that are subsequently introduced. If our competitors release new products that are superior to our impact-resistant products in performance or price, or if we fail to update our impact-resistant products with any technological advances that are developed by us or our competitors or introduce new products in a timely manner, demand for our products may decline. A decline in demand for our impact-resistant products as a result of competition, technological change or other factors could have a material adverse effect on our ability to generate sales, which would negatively affect results of operations.

In 2015, we launched a new line of vinyl impact-resistant and non-impact energy saving windows. In January 2015, we unveiled our new Vinyl WinGuard and EnergyVue line of vinyl windows. Our intent in launching this new line of vinyl products is that it will ultimately replace various existing lines of vinyl impact-resistant and energy saving windows. We designed these products to exceed the most stringent impact-resistance and energy-saving codes in the country, and they have been well received by the industry. However, if these products fail to continue to gain acceptance with our customers as replacements of our currently successful lines of vinyl windows, we could lose market share to our competitors that produce similar products, which could have a material impact on our sales and negatively affect results of operations.

Changes in building codes could lower the demand for our impact-resistant windows and doors. The market for our impact-resistant windows and doors depends in large part on our ability to satisfy state and local building codes that require protection from wind-borne debris. If the standards in such building codes are raised, we may not be able to meet their requirements, and demand for our products could decline. Conversely, if the standards in such building codes are lowered or are not enforced in certain areas, demand for our impact-resistant products may decrease. Further, if states and regions that are affected by hurricanes but do not currently have such building codes fail to adopt and enforce hurricane protection building codes; our ability to expand our business in such markets may be limited.

Our industry is competitive, and competition may increase as our markets grow or as more states adopt or enforce building codes that require impact-resistant products. The window and door industry is highly competitive. We face significant competition from numerous small, regional producers, as well as certain national producers. Any of these competitors may (i) foresee the course of market development more accurately than do we, (ii) develop products that are superior to our products, (iii) have the ability to

- 8 -

Table of Contents

produce similar products at a lower cost, or (iv) adapt more quickly to new technologies or evolving customer requirements than do we. Additionally, new competitors may enter our industry, and larger existing competitors may increase their efforts and devote substantially more resources to expand their presence in the impact-resistant market. If we are unable to compete effectively, demand for our products may decline. In addition, while we are skilled at creating finished impact-resistant and other window and door products, the materials we use can be purchased by any existing or potential competitor. New competitors can enter our industry, and existing competitors may increase their efforts in the impact-resistant market. Furthermore, if the market for impact-resistant windows and doors continues to expand, larger competitors could enter or expand their presence in the market and may be able to compete more effectively. Finally, we may not be able to maintain our costs at a level for us to compete effectively. If we are unable to compete effectively, demand for our products and our profitability may decline.

Our business is currently concentrated in one state. Our business is concentrated geographically in Florida. Focusing operations into manufacturing locations in Florida optimizes manufacturing efficiencies and logistics, and we believe that a focused approach to growing our share within our core wind-borne debris markets in Florida, from the Gulf Coast to the mid-Atlantic, and certain international markets, will maximize value and return. However, such a focus further concentrates our business, and another prolonged decline in the economy of the state of Florida or of certain coastal regions, a change in state and local building code requirements for hurricane protection, or any other adverse condition in the state or certain coastal regions, could cause a decline in the demand for our products, which could have an adverse impact on our sales and results of operations.

We have incurred additional indebtedness. We have incurred additional indebtedness under our credit facilities as a result of increasing our borrowing levels to fund acquisitions, and to provide for up to $40 million of revolving credit borrowings. We and our subsidiaries may incur additional indebtedness in the future to fund additional acquisitions and/or to borrow under our revolving credit facility to fund working capital needs. If new debt is added to our current debt levels, certain risks which we currently do not consider significant could intensify.

Our debt instruments contain various covenants that limit our ability to operate our business. Our credit facility contains various provisions that limit our ability to, among other things, transfer or sell assets, including the equity interests of our subsidiaries, or use asset sale proceeds; pay dividends or distributions on our capital stock, make certain restricted payments or investments; create liens to secure debt; enter into transactions with affiliates; merge or consolidate with another company; and engage in unrelated business activities.

In addition, under certain circumstances and depending on the degree of borrowing we may elect to incur under the revolving credit portion of our credit facility, our credit facility requires us to maintain a net leverage ratio, as defined in our credit facility, below certain maximums which decrease over time. Our ability to comply with the requirements of this maximum net leverage ratio, as well as other provisions of our credit facility, may be affected by changes in our operating and financial performance, changes in general business and economic conditions, adverse regulatory developments, or other events beyond our control. The breach of this maximum net leverage ratio requirement, could result in a default under our indebtedness, which could cause it and other obligations to become immediately due and payable. If any of our indebtedness is accelerated, we may not be able to repay it.

We may be adversely affected by any disruption in our information technology systems. Our operations are dependent upon our information technology systems, which encompass all of our major business functions. A disruption in our information technology systems for any prolonged period could result in delays in receiving inventory and supplies or filling customer orders and adversely affect our customer service and relationships.

In order to maintain our leadership position in the market and efficiently process increased business volume, we are making a significant upgrade to our computer hardware, software and our Enterprise Resource Planning (ERP) System. The ERP implementation was substantially completed by the end of 2015. Conversion to the new ERP system has caused significant inefficiencies that have adversely affected our results of operations and disrupted our manufacturing processes to varying degrees during the conversion. Additional disruptions due to the completion of the final stages of the conversion could affect our ability to maintain and grow the business, and our operations and financial results could be further adversely impacted.

We may be adversely affected by any disruptions to our manufacturing facilities or disruptions to our customer, supplier, or employee base. Any disruption to our facilities resulting from hurricanes and other weather-related events, fire, an act of terrorism, or any other cause could damage a significant portion of our inventory, affect our distribution of products, and materially impair our ability to distribute our products to customers. We could incur significantly higher costs and longer lead times associated with distributing our products to our customers during the time that it takes for us to reopen or replace a damaged facility. In addition, if there are disruptions to our customer and supplier base or to our employees caused by hurricanes, our business could be temporarily adversely affected by higher costs for materials, increased shipping and storage costs, increased labor costs, increased absentee rates, and scheduling issues. Furthermore, some of our direct and indirect suppliers have unionized work forces, and strikes, work stoppages, or slowdowns experienced by these suppliers could result in slowdowns or closures of their facilities. Any interruption in the production or delivery of our supplies could reduce sales of our products and increase our costs.

- 9 -

Table of Contents

The nature of our business exposes us to product liability and warranty claims. We are, from time to time, involved in product liability and product warranty claims relating to the products we manufacture and distribute that, if adversely determined, could adversely affect our financial condition, results of operations, and cash flows. In addition, we may be exposed to potential claims arising from the conduct of homebuilders and home remodelers and their sub-contractors. Although we currently maintain what we believe to be suitable and adequate insurance in excess of our self-insured amounts, we may not be able to maintain such insurance on acceptable terms or such insurance may not provide adequate protection against potential liabilities. Product liability claims can be expensive to defend and can divert the attention of management and other personnel for significant periods, regardless of the ultimate outcome. Claims of this nature could also have a negative impact on customer confidence in our products and our company.

We are subject to potential exposure to environmental liabilities and are subject to environmental regulation. We are subject to various federal, state, and local environmental laws, ordinances, and regulations. Although we believe that our facilities are in material compliance with such laws, ordinances, and regulations, as owners and lessees of real property, we can be held liable for the investigation or remediation of contamination on such properties, in some circumstances, without regard to whether we knew of or were responsible for such contamination. Remediation may be required in the future as a result of spills or releases of petroleum products or hazardous substances, the discovery of unknown environmental conditions, or more stringent standards regarding existing residual contamination. More burdensome environmental regulatory requirements may increase our general and administrative costs and may increase the risk that we may incur fines or penalties or be held liable for violations of such regulatory requirements.

We conduct all of our operations through our subsidiaries, and rely on payments from our subsidiaries to meet all of our obligations. We are a holding company and derive all of our operating income from our subsidiary, PGT Industries, Inc., and its subsidiaries, CGI Windows and Doors, Inc., and beginning on the acquisition date of February 16, 2016, WinDoor, Incorporated. All of our assets are held by our subsidiaries, and we rely on the earnings and cash flows of our subsidiaries to meet our obligations. The ability of our subsidiaries to make payments to us will depend on their respective operating results and may be restricted by, among other things, the laws of their jurisdictions of organization (which may limit the amount of funds available for distributions to us), the terms of existing and future indebtedness and other agreements of our subsidiaries, including our credit facilities, and the covenants of any future outstanding indebtedness we or our subsidiaries incur.

We are exposed to risks relating to evaluations of controls required by Section 404 of the Sarbanes-Oxley Act of 2002. We are required to comply with Section 404 of the Sarbanes-Oxley Act of 2002. While we have concluded that at January 2, 2016, we have no material weaknesses in our internal control over financial reporting, we cannot assure you that we will not have a material weakness in the future. A “material weakness” is a deficiency, or combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of the Company’s annual or interim financial statements will not be prevented or detected on a timely basis. If we fail to maintain our internal control over financial reporting that meets the requirements of Section 404, we might be subject to sanctions or investigation by regulatory authorities such as the SEC or by the NASDAQ Global Market LLC. Additionally, failure to comply with Section 404 or the report by us of a material weakness may cause investors to lose confidence in our financial statements and our stock price may be adversely affected. If we fail to remedy any material weakness, our financial statements may be inaccurate, we may not have access to the capital markets, and our stock price may be adversely affected.

We are exposed to risks relating to the continued expansion of our glass operations. We expanded our glass processing capacity with the completion of a new multi-million dollar facility, and are proceeding with the purchase of additional equipment. While the plant expansion continues to progress with no anticipated issues, there is always the potential risk of a delay in completion and of cost over-runs. Should a serious delay of this project take place, or if this project negatively impacted our operational efficiencies, this would impact the cost savings we expect to achieve during 2016 which could negatively affect our future results.

We may be adversely impacted by the loss of sales or market share from being unable to keep up with demand. We are currently experiencing growth through higher sales volume and growth in market share. To meet the increased demand, we have been hiring and training new employees for direct and indirect support, and adding to our glass capacity. However, should we be unable to find and retain quality employees to meet demand, or should there be disruptions to the increase in capacity, we may be unable to keep up with our higher sales demand. If our lag time on delivery falls behind, or we are unable to meet customer timing demands, we could lose market share to competitors.

We made significant acquisitions late in the third quarter of 2014, and again in February 2016 of companies that sell products similar to PGT’s own impact-resistant line of products in PGT’s primary market of Florida. Late in the third quarter of 2014, we acquired CGI Windows and Doors, Inc. CGI produces the Estate, Sentinel and Targa lines of impact-resistant branded products which are very similar to our WinGuard line of impact-resistant branded products. In February 2016, we acquired WinDoor. WinDoor

- 10 -

Table of Contents

produces impact-resistant windows and sliding glass and terrace doors, very similar to PGT and CGI. Nearly all of CGI’s and WinDoor’s sales are in Florida, PGT’s primary market. We believe that adding CGI’s and WinDoor’s branded products and presence in Florida to PGT’s already successful, established line of branded products in Florida will benefit PGT through higher sales and market share. However, no assurances can be given that the combination of these three lines of branded products within a single company will not result in dilution of these brands, resulting in loss of market share and demand for these products.

| Item 1B. | UNRESOLVED STAFF COMMENTS |

None.

| Item 2. | PROPERTIES |

We have the following properties as of January 2, 2016:

| Manufacturing | Support | Storage | ||||||||||

| (in square feet) | ||||||||||||

| Owned: |

||||||||||||

| Main Plant and Corporate Office, North Venice, FL |

348,000 | 15,000 | — | |||||||||

| Glass tempering and laminating, North Venice, FL |

80,000 | — | — | |||||||||

| New glass facility, North Venice, FL |

96,000 | — | — | |||||||||

| Insulated Glass, North Venice, FL |

42,000 | — | — | |||||||||

| PGT Wellness Center, North Venice, FL |

— | 3,600 | — | |||||||||

| Leased: |

||||||||||||

| James Street Storage, Venice, FL |

15,000 | — | — | |||||||||

| Center Court, Venice, FL |

19,600 | 15,400 | — | |||||||||

| Endeavor Court, Nokomis, FL |

— | 2,300 | — | |||||||||

| Endeavor Court, Nokomis, FL |

— | 6,100 | — | |||||||||

| Technology Park, Nokomis, FL |

— | 1,800 | — | |||||||||

| Sarasota Warehouse, Bradenton, FL |

— | — | 48,000 | |||||||||

| Plant and Administrative Offices, Miami, FL |

90,000 | 17,000 | — | |||||||||

| Light manufacturing and Storage, Doral, FL |

5,000 | — | 30,000 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total square feet |

695,600 | 61,200 | 78,000 | |||||||||

|

|

|

|

|

|

|

|||||||

On February 16, 2016, we acquired WinDoor. WinDoor manufactures impact-resistant windows and doors from its approximately 320,000 square foot manufacturing and administrative facility in Orlando, Florida. This facility is leased by WinDoor, and we believe it has adequate space for Windoor’s current level of operating activity, as well as additional room for growth and expansion, if needed. This lease expires in February 2021.

On August 16, 2013, we purchased land to build our new glass operations plant. We officially broke ground on January 9, 2014, and completed construction during 2014. The glass plant became operational late in the third quarter of 2014. This facility added 96,000 square foot to our glass cutting, tempering and laminating process. We also own three additional parcels of land available for future growth.

Our leases listed above expire between March 2016 and December 2018. Each of the leases provides for a fixed annual rent. The leases require us to pay taxes, insurance and common area maintenance expenses associated with the properties.

All of our owned properties secure borrowings under our credit agreement. We believe all of these operating facilities are adequate in capacity and condition to service existing customer needs.

| Item 3. | LEGAL PROCEEDINGS |

We are involved in various claims and lawsuits incidental to the conduct of our business in the ordinary course. We carry insurance coverage in such amounts in excess of our self-insured retention as we believe to be reasonable under the circumstances and that may or may not cover any or all of our liabilities in respect of claims and lawsuits. We do not believe that the ultimate resolution of these matters will have a material adverse impact on our financial position, cash flows or results of operations.

| Item 4. | MINE SAFETY DISCLOSURES |

Not Applicable

- 11 -

Table of Contents

| Item 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our Common Stock is traded on the NASDAQ Global Market ® under the symbol “PGTI”. On March 4, 2016, the closing price of our Common Stock was $9.32 as reported on the NASDAQ Global Market. The approximate number of stockholders of record of our Common Stock on that date was 50, although we believe that the number of beneficial owners of our Common Stock is substantially greater.

The table below sets forth the price range of our Common Stock during the periods indicated:

| High | Low | |||||||

| 2015 |

||||||||

| 1st Quarter |

$ | 11.38 | $ | 8.28 | ||||

| 2nd Quarter |

$ | 15.35 | $ | 10.63 | ||||

| 3rd Quarter |

$ | 16.28 | $ | 11.56 | ||||

| 4th Quarter |

$ | 14.05 | $ | 9.77 | ||||

| High | Low | |||||||

| 2014 |

||||||||

| 1st Quarter |

$ | 12.61 | $ | 9.75 | ||||

| 2nd Quarter |

$ | 11.93 | $ | 7.87 | ||||

| 3rd Quarter |

$ | 10.97 | $ | 7.34 | ||||

| 4th Quarter |

$ | 10.26 | $ | 8.25 | ||||

Dividends

We do not pay a regular dividend. Any determination relating to dividend policy will be made at the discretion of our Board of Directors. The terms of our credit facility currently restrict our ability to pay dividends.

Securities Authorized for Issuance under Equity Compensation Plans

The information required by this item appears in our definitive proxy statement for our annual meeting of stockholders under the caption “Security Ownership of Certain Beneficial Owners and Management” and “Equity Compensation Plan Information,” which information is incorporated herein by reference.

Unregistered Sales of Equity Securities

None.

Issuer Purchases of Equity Securities

None.

- 12 -

Table of Contents

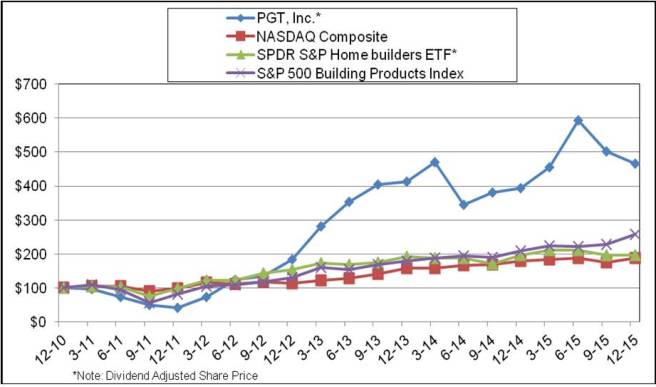

Performance Graph

The following graphs compare the percentage change in PGT, Inc.’s cumulative total stockholder return on its Common Stock with the cumulative total stockholder return of the Standard & Poor’s Building Products Index and the NASDAQ Composite Index over the period from January 1, 2011, to December 31, 2015.

COMPARISON OF 60 MONTH CUMULATIVE TOTAL RETURN*

AMONG PGT, INC., THE NASDAQ COMPOSITE INDEX,

AND THE S&P BUILDING PRODUCTS INDEX

| * | $100 invested on January 1, 2011 in stock or in index-including reinvestment of dividends for 60 months ending December 31, 2015. |

- 13 -

Table of Contents

| Item 6. | SELECTED FINANCIAL DATA |

The following table sets forth selected historical consolidated financial information and other data as of and for the periods indicated and have been derived from our audited consolidated financial statements.

All information included in the following tables should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” contained in Item 7, and with the consolidated financial statements and related notes in Item 8. All years presented consisted of 52 weeks, except for the year ended January 3, 2015, which consisted of 53 weeks.

| Year Ended | Year Ended | Year Ended | Year Ended | Year Ended | ||||||||||||||||

| Selected Consolidated Financial Data | January 2, | January 3, | December 28, | December 29, | December 31, | |||||||||||||||

| (in thousands except per share data) |

2016 | 2015 | 2013 | 2012 | 2011 | |||||||||||||||

| Net sales |

$ | 389,810 | $ | 306,388 | $ | 239,303 | $ | 174,540 | $ | 167,276 | ||||||||||

| Cost of sales |

270,678 | 213,596 | 159,169 | 114,872 | 128,171 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross profit |

119,132 | 92,792 | 80,134 | 59,668 | 39,105 | |||||||||||||||

| Impairment charges (1) |

— | — | — | — | 5,959 | |||||||||||||||

| Gain on sale of assets held (2) |

— | — | (2,195 | ) | — | — | ||||||||||||||

| Selling, general and administrative expenses |

68,190 | 56,377 | 54,594 | 47,094 | 48,619 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) from operations |

50,942 | 36,415 | 27,735 | 12,574 | (15,473 | ) | ||||||||||||||

| Interest expense |

11,705 | 5,960 | 3,520 | 3,437 | 4,168 | |||||||||||||||

| Debt extinguishment costs |

— | 2,625 | 333 | — | — | |||||||||||||||

| Other expense (income), net (3) |

388 | 1,750 | 437 | 72 | (419 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) before income taxes |

38,849 | 26,080 | 23,445 | 9,065 | (19,222 | ) | ||||||||||||||

| Income tax expense (benefit) |

15,297 | 9,675 | (3,374 | ) | 110 | (2,324 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

$ | 23,552 | $ | 16,405 | $ | 26,819 | $ | 8,955 | $ | (16,898 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) per common share: |

||||||||||||||||||||

| Basic |

$ | 0.49 | $ | 0.35 | $ | 0.55 | $ | 0.17 | $ | (0.31 | ) | |||||||||

| Diluted |

$ | 0.47 | $ | 0.33 | $ | 0.51 | $ | 0.16 | $ | (0.31 | ) | |||||||||

| Weighted average shares outstanding: |

||||||||||||||||||||

| Basic |

48,272 | 47,376 | 48,881 | 53,620 | 53,659 | |||||||||||||||

| Diluted |

50,368 | 49,777 | 52,211 | 55,262 | 53,659 | |||||||||||||||

| Other financial data: |

||||||||||||||||||||

| Depreciation |

$ | 7,008 | $ | 4,534 | $ | 4,622 | $ | 5,731 | $ | 7,590 | ||||||||||

| Amortization |

3,413 | 1,446 | 6,458 | 6,502 | 6,502 | |||||||||||||||

| As Of | As Of | As Of | As Of | As Of | ||||||||||||||||

| January 2, | January 3, | December 28, | December 29, | December 31, | ||||||||||||||||

| 2016 | 2015 (4)(5) | 2013 (4) | 2012 | 2011 (4) | ||||||||||||||||

| Balance Sheet data: |

||||||||||||||||||||

| Cash and cash equivalents |

$ | 61,493 | $ | 42,469 | $ | 30,204 | $ | 18,743 | $ | 10,940 | ||||||||||

| Total assets |

345,729 | 306,589 | 153,869 | 141,317 | 142,785 | |||||||||||||||

| Total debt, including current portion |

192,468 | 193,754 | 77,255 | 37,500 | 45,550 | |||||||||||||||

| Shareholders’ equity |

106,961 | 73,976 | 49,075 | 74,210 | 67,362 | |||||||||||||||

| (1) | In 2011, amounts relate to intangible asset impairment charges. See Notes 2 and 8 in Item 8. |

| (2) | Relates to the sale of the Salisbury, NC facility. The net selling price of the facility was approximately $7.5 million and the carrying value of the asset at the time of sale was $5.3 million. |

| (3) | Other expense (income), net, includes fair value adjustments on derivative financial instruments. |

| (4) | Total assets changed from amount previously reported due to the reclassification of current deferred tax assets pursuant to |

| ASU 2015-17. |

| (5) | Late in the third quarter of 2014, we acquired CGI. See Note 4 in Item 8. |

- 14 -

Table of Contents

| Item 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINACIAL CONDITION AND RESULTS OF OPERATIONS |

Our Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) should be read in conjunction with our Consolidated Financial Statements and related Notes included in Item 8. We also advise you read the risk factors in Item 1A. Our MD&A is presented in seven sections:

| • | Executive Overview; |

| • | Results of Operations; |

| • | Liquidity and Capital Resources; |

| • | Disclosures of Contractual Obligations and Commercial Commitments; |

| • | Critical Accounting Estimates; |

| • | Recently Issued Accounting Standards; and |

| • | Forward Outlook |

EXECUTIVE OVERVIEW

Sales and Operations

On February 25, 2016, we issued a press release and held a conference call, to review the results of operations for our fourth quarter and fiscal year ended January 2, 2016. During the call, we also discussed current market conditions and progress made regarding certain of our initiatives. The overview and estimates contained in this report are consistent with those given in our press release and discussed on the call. We are neither updating nor confirming that information.

Our sales grew 27.2%, to $389.8 million, a company record and a level we have not seen since 2006. This increase resulted from execution on our long-term strategies, including acquisitions which meet our requirements for growth potential, profitability and culture, coupled with the continued improvement in the housing market. Gross profit increased 28.4% and we continued to leverage selling, general and administrative expenses which, as a percent of sales, decreased to 17.5%, compared to 18.4% in 2014. Our net income was $23.6 million, an increase of $7.2 million when compared to 2014’s net income of $16.4 million. The increase in net income was primarily the result of higher profitability on the leverage from higher sales.

In terms of sales strategies, we continued to leverage our dominant presence in our core market, Florida, which included the acquisition of CGI in 2014, which added to our market share. We also continued to establish programs and partnerships with national accounts to increase our sales presence. As a result of our efforts and the improving macro-economic conditions, specifically in Florida, sales during 2015 increased $83.4 million, or 27.2%, compared to 2014. This increase includes CGI’s sales for the full year of 2015, compared to sales from just the late third quarter acquisition date in 2014. New construction sales increased $44.2 million, or 38.3%, while repair and remodel sales increased by $39.2 million, or 20.5%. By region, our sales in Florida increased $73.6 million, or 27.2%, and sales in the out of state markets increased $1.6 million, or 6.4%. Sales in the international markets increased $8.2 million, or 77.4%.

By product category, sales in our impact-resistant window and door products increased $78.9 million, or 32.8%, driven by an increase in our WinGuard and Storefront products, but also the inclusion of CGI’s sales for the entire year, versus only the post-acquisition period in 2014. All of CGI’s products are impact-resistant. Our Storefront products, introduced in 2013, have enjoyed steady sales increases since their introduction, and increased 59.4% from last year. Sales of our non-impact window and door products increased by $4.5 million, or 6.9%.

Liquidity and Cash Flow

During 2015, we generated $32.5 million in cash flow from operations, which was used to fund working capital needs, service our long-term debt, and for capital expenditures of $17.4 million, including the addition of new glass processing equipment for our state of the art glass processing facility on which we completed construction in 2014. Late in the third quarter of 2014, we entered into a senior secured credit facility which included a $200 million term loan and $35 million revolving line of credit. This facility

- 15 -

Table of Contents

increased our outstanding debt to $200 million, the proceeds from which we used to acquire CGI, including the payment of financing costs, and to repay existing long-term debt which at that time was $79 million which was the result of a debt refinancing we consummated in May 2013. The proceeds from the 2013 refinancing was used to fund our stock repurchase from JLL Partners.

In February 2016, we entered into a new senior secured credit facility which increased the term loan component of our borrowings to $270 million and has a $40 million revolving line of credit. We used proceeds under this new facility, combined with approximately $43 million of cash on hand to acquire WinDoor, including the payment of financing costs, and repay then existing borrowings of $197.5 million under our 2014 credit facility.

On October 28, 2015, the Board of Directors authorized and approved a share repurchase program of up to $20 million. Repurchases will be made in open market or privately negotiated transactions, subject to market conditions, applicable legal requirements, our 2016 Credit Agreement, and other relevant factors. We do not intend to repurchase any shares from directors, officers, or other affiliates. The program does not obligate us to acquire any specific number of shares. The timing, manner, price and amount of repurchases will be determined at the Company’s discretion, and the program may be suspended, terminated or modified at any time for any reason. No share repurchases had been consummated under this buyback program as of January 2, 2016. However, during 2016, through the date of this filing, we made repurchases of 278,883 shares of our common stock at a total cost of $2.6 million. During the remainder of 2016, we may continue to make opportunistic repurchases of our common stock as we see fit.

Other Expected Impacts of the WinDoor Acquisition and Refinancing

As the result of the February 2016 refinancing, we expect interest expense will increase approximately $9 million on an annualized basis. This is due to the higher debt balance, coupled with a higher interest rate under the new credit facility, as well as our expectation that non-cash amortization of deferred financing costs and debt discount will increase.

In addition to the estimated impacts on sales and EBITDA discussed above we expect that amortizable intangible assets, as well as property and equipment, related to the WinDoor acquisition will result in an estimated increase in depreciation and amortization of approximately $4 million on an annualized basis.

Incremental interest expense and depreciation and amortization are expected to be spread ratably during the year, starting from the acquisition date.

- 16 -

Table of Contents

RESULTS OF OPERATIONS

Analysis of Selected Items from our Consolidated Statements of Operations

| Year Ended | Percent Change | |||||||||||||||||||

| January 2, 2016 |

January 3, 2015 |

December 28, 2013 |

Increase / (Decrease) | |||||||||||||||||

| (in thousands, except per share amounts) | 2015-2014 | 2014-2013 | ||||||||||||||||||

| Net sales |

$ | 389,810 | $ | 306,388 | $ | 239,303 | 27.2 | % | 28.0 | % | ||||||||||

| Cost of sales |

270,678 | 213,596 | 159,169 | 26.7 | % | 34.2 | % | |||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Gross profit |

119,132 | 92,792 | 80,134 | 28.4 | % | 15.8 | % | |||||||||||||

| Gross margin |

30.6 | % | 30.3 | % | 33.5 | % | ||||||||||||||

| Gain on sale of assets held |

— | — | (2,195 | ) | ||||||||||||||||

| SG&A expenses |

68,190 | 56,377 | 54,594 | 21.0 | % | 3.3 | % | |||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| SG&A expenses as a percentage of sales |

17.5 | % | 18.4 | % | 22.8 | % | ||||||||||||||

| Income from operations |

50,942 | 36,415 | 27,735 | |||||||||||||||||

| Interest expense, net |

11,705 | 5,960 | 3,520 | |||||||||||||||||

| Debt extinguishment costs |

— | 2,625 | 333 | |||||||||||||||||

| Other expenses, net |

388 | 1,750 | 437 | |||||||||||||||||

| Income tax expense (benefit) |

15,297 | 9,675 | (3,374 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Net income |

$ | 23,552 | $ | 16,405 | $ | 26,819 | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Net income per common share: |

||||||||||||||||||||

| Basic |

$ | 0.49 | $ | 0.35 | $ | 0.55 | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Diluted |

$ | 0.47 | $ | 0.33 | $ | 0.51 | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

- 17 -

Table of Contents

2015 Compared with 2014

Net sales

Net sales for 2015 were $389.8 million, a $83.4 million, or 27.2%, increase in sales from $306.4 million in the prior year.

The following table shows net sales classified by major product category (in millions, except percentages):

| Year Ended | ||||||||||||||||||||

| January 2, 2016 | January 3, 2015 | |||||||||||||||||||

| Sales | % of sales | Sales | % of sales | % change | ||||||||||||||||

| Product category: |

||||||||||||||||||||

| Impact-resistant window and door products |

$ | 319.2 | 81.9 | % | $ | 240.3 | 78.4 | % | 32.8 | % | ||||||||||

| Non-impact window and door products |

70.6 | 18.1 | % | 66.1 | 21.6 | % | 6.9 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total net sales |

$ | 389.8 | 100.0 | % | $ | 306.4 | 100.0 | % | 27.2 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

Net sales of our impact window and door products, which include our PGT WinGuard, Architectural Systems, Storefront and PremierVue products, as well as the Estate Collection, Sentinel and Targa products of CGI, were $319.2 million in 2015, an increase of $78.9 million, or 32.8%, driven by an increase in sales of our WinGuard and Storefront products, but also the inclusion of CGI’s sales for the entire year, versus only the post-acquisition period in 2014, from $240.3 million in the prior year. All of CGI’s products are impact-resistant. Our Storefront products, introduced in 2013, have enjoyed steady sales increases since their introduction, and increased 59.4% from last year. Included in sales of our impact-resistant window and door products were $247.4 million of aluminum impact sales, an increase of $65.1 million, or 35.7%, and $71.8 million of vinyl impact sales, an increase of $13.8 million, or 23.8%.

Sales of our non-impact window and door products increased by $4.5 million, or 6.9%. Included in sales of our non-impact window and door products were $27.0 million of aluminum non-impact sales, a decrease of $0.2 million, or 0.7%, and $43.6 million of vinyl non-impact sales, an increase of $4.7 million, or 12.0%.

Gross profit and gross margin

Gross profit was $119.1 million in 2015, an increase of $26.3 million, or 28.4%, from $92.8 million in the prior year. The gross margin percentage was 30.6% in 2015 compared to 30.3% in the prior year, an increase of 0.3%. Gross margin was positively impacted by several factors, including our first quarter 2015 price increase, which benefitted gross margin by 1.0%, by the leverage provided by higher sales volume, which benefitted gross margin by 0.6%, lower glass cost due to the increase in our capacity to process our own glass, which has reduced our dependence on outsourced, higher-cost glass, which benefitted gross margin by 0.2%, and by lower aluminum prices, which benefitted gross margin by 0.2%. Also, the addition of CGI benefitted gross margin by 1.2%. These improvements were partially offset by decreases as the result of higher overhead costs, resulting in a decrease in gross margin of 2.2%, and product mix, which decreased gross margin by 0.7%. Gross margins in both periods were negatively impacted by certain costs related to labor inefficiencies and material costs relating to issues encountered during our ERP systems conversion, new product launch costs, and glass line installation costs in 2015, and glass processing facility and new product launch costs in 2014. These costs negatively impacted gross margin by 1.3% in 2015 and by 0.5% in 2014. Excluding these negative impacts, our gross margins would have been 31.9% and 30.8% in 2015 and 2014, respectively.

Selling, general and administrative expenses

Selling, general and administrative expenses were $68.2 million, an increase of $11.8 million, or 21.0%, from $56.4 million in the prior year. As a percentage, we leveraged these costs to 17.5%, a decrease of 0.9% from 18.4% from fiscal year 2014. Selling, general, and administrative expenses includes $12.5 million related to CGI, compared to $3.0 million last year. Excluding CGI, selling, general and administrative costs increased $2.3 million. Contributing to the increase was a $1.6 million increase in selling and distribution costs as the result of an increase in volume, but which includes a $0.5 million decrease in fuel costs due to a decrease in the price of gasoline. There were also increases in depreciation expense of $0.7 million due to higher levels of capital investment, stock-based compensation expenses of $0.6 million, and bank credit card fees of $0.5 million due to higher credit card sales. These increases were partially offset by a decrease of $1.1 million related to acquisition-related costs incurred in 2014, which did not recur in 2015.

- 18 -

Table of Contents

Interest expense

Interest expense was $11.7 million in 2015, an increase of $5.7 million from $6.0 million in the prior year. During 2014, concurrent with the acquisition of CGI late in the third quarter of 2014, we refinanced our then existing credit agreement into a new $200 million senior secured credit facility (“2014 Credit Agreement”) which increased our outstanding debt balance to $200 million, up from $79.0 million at the end of 2013. The increase in interest expense was due primarily to the increase in outstanding debt under the 2014 Credit Agreement and resulting increase in average outstanding debt balance during 2015 compared to 2014.

Debt extinguishment costs

In 2014, there were write-offs of deferred financing costs of $2.6 million relating to the debt refinancing resulting from entering into the 2014 Credit Agreement.

Other expenses, net

Other expenses, net were $0.4 million and $1.8 million in 2015 and 2014, respectively. In 2015, other expenses relates entirely to the ineffective portion of our aluminum hedging activities. In 2014, other expenses includes expenses related to termination of our interest rate swap agreement of $1.5 million and the ineffective portion of our aluminum hedging activity of 0.2 million.

Income tax expense (benefit)

Our income tax expense was $15.3 million for 2015, representing an effective tax rate of 39.4%. Income tax expense in 2015 includes a $1.6 million discrete item of income tax expense representing income tax expense previously classified within accumulated other comprehensive losses, relating to the intraperiod income taxes on our effective aluminum hedges, which we reversed in the second quarter of 2015 as the result of the culmination of our remaining cash flow hedges. Income tax expense in 2015 also includes the beneficial effect of $0.8 million, net of federal effect, from a Florida jobs credit we received as the result of our increased employment levels. Excluding the effects of these discrete items in income tax expense, our effective tax rate in 2015 would have been 37.3%, compared to 37.1% in 2014, slightly lower than our combined statutory federal and state tax rate of 38.8%, primarily as the result of the section 199 domestic manufacturing deduction in both years.

2014 Compared with 2013

Net sales

Net sales for 2014 were $306.4 million, a $67.1 million, or 28.0%, increase in sales from $239.3 million in the prior year.

The following table shows net sales classified by major product category (in millions, except percentages):

| Year Ended | ||||||||||||||||||||

| January 3, 2015 | December 28, 2013 | |||||||||||||||||||

| Sales | % of sales | Sales | % of sales | % change | ||||||||||||||||

| Product category: |

||||||||||||||||||||

| Impact-resistant window and door products |

$ | 240.3 | 78.4 | % | $ | 183.4 | 76.6 | % | 31.0 | % | ||||||||||

| Non-impact window and door products |

66.1 | 21.6 | % | 55.9 | 23.4 | % | 18.2 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total net sales |

$ | 306.4 | 100.0 | % | $ | 239.3 | 100.0 | % | 28.0 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

Net sales of our impact window and door products, which include our PGT WinGuard, Architectural Systems, Storefront and PremierVue products, as well as the Estate Collection, Sentinel and Targa products of CGI, were $240.3 million in 2014, an increase of $56.9 million, or 31.0%, driven by an increase in sales of our WinGuard and Storefront products, but also from the late third quarter 2014 addition of CGI, from $183.4 million in the prior year. All of CGI’s products are impact-resistant. Our Storefront products, introduced in 2013, have enjoyed steady sales increases since their introduction. Included in sales of our impact-resistant window and door products were $182.3 million of aluminum impact sales, an increase of $42.5 million, or 30.4%, and $58.0 million of vinyl impact sales, an increase of $14.4 million, or 32.9%.

Sales of our non-impact window and door products increased by $10.2 million, or 18.2%. Included in sales of our non-impact window and door products were $27.2 million of aluminum non-impact sales, an increase of $3.1 million, or 12.9%, and $38.9 million of vinyl non-impact sales, an increase of $7.1 million, or 22.3%.

- 19 -

Table of Contents

Gross profit and gross margin

Gross profit was $92.8 million in 2014, an increase of $12.7 million, or 15.8%, from $80.1 million in the prior year. The gross margin percentage was 30.3% in 2014 compared to 33.5% in the prior year, a decrease of 3.2%. Gross margin was negatively impacted by 1.5% due to excess labor and overhead costs resulting from the hiring and training of new manufacturing employees to meet the increased demand for our products. In addition, gross margin was negatively impacted by 1.3% due to increased material costs due to an increase in aluminum prices during 2014, as well as our need to purchase finished glass from outside suppliers due to certain internal capacity constraints. In response to these constraints, during 2014 we completed the construction of a new glass processing facility which became operational late in the third quarter of 2014 but for which gross margin was negatively impacted by 0.5% due to start-up costs of the new glass facility. Our gross margin was also negatively impacted by 0.5% due to pricing and product mix, including pricing and mix on certain large projects done during 2014. Lastly, 2014 was a 53-week year which included an extra week of fixed costs in the fourth quarter during which we had no sales activity. The fixed costs from this extra week resulted in a negative impact to gross margin of 0.3%. These items were offset by leverage on higher sales volume of 0.6% and the addition of CGI, which benefited gross margin by 0.3%.

Selling, general and administrative expenses

Selling, general and administrative expenses were $56.4 million, an increase of $1.8 million, or 3.3%, from $54.6 million in the prior year. As a percentage, we leveraged these costs to 18.4%, a decrease of 4.4% from 22.8% from fiscal year 2013. Selling, general, and administrative expenses includes $3.0 million related to CGI. Excluding CGI, selling, general and administrative costs decreased $1.2 million. Contributing to the decrease was a decrease of $6.0 million in intangible assets amortization expense due to our amortizable intangible assets, not including those acquired with the acquisition of CGI, becoming fully amortized early in 2014. There was also a $0.3 million decrease in depreciation expense and a $0.2 million decrease in professional, consulting and public company fees and costs. Offsetting these decreases, was a $5.3 million increase in selling and distribution costs as the result of an increase in volume.

Interest expense

Interest expense was $6.0 million in 2014, an increase of nearly $2.5 million from $3.5 million in the prior year. During 2014, concurrent with the acquisition of CGI late in the third quarter of 2014, we refinanced our then existing credit agreement into a new $200 million senior secured credit facility which increased our outstanding debt balance to $200 million, up from $79.0 million at the end of 2013. The increase in interest expense was due primarily to the increase in outstanding debt under the new credit facility and resulting increase in average outstanding debt balance during 2014 compared to 2013.

Debt extinguishment costs

In 2014, there were write-offs of deferred financing costs of $2.6 million relating to the debt refinancing resulting from entering into the 2014 Credit Agreement. In 2013, the write-off of deferred financing costs relating to the debt refinancing resulting from entering into the 2013 Credit Agreement totaled $0.3 million.

Other expenses, net

Other expenses, net were $1.8 million and $0.4 million in 2014 and 2013, respectively. In 2014, other expenses includes expenses related to termination of our interest rate swap agreement of $1.5 million and the ineffective portion of our aluminum hedging activity of $0.2 million. There was other expense of less than $0.1 million in 2014 relating to the interest rate cap. In 2013, the expense relates to the ineffective portion of our aluminum hedging activity.

Income tax expense (benefit)

Our income tax expense was $9.7 million for 2014, representing an effective tax rate of 37.1%, slightly lower than our combined statutory federal and state tax rate of 38.8% as the result of the section 199 domestic manufacturing deduction. In 2013, we had a tax benefit of $3.4 million as we released our valuation allowances on deferred tax assets as we were no longer in a cumulative loss position and we concluded that it was more likely than not that our deferred tax assets will be realized. Excluding the impact of the 2013 reversal of the valuation allowance, our effective tax rate would have been 40.7% in 2013.

- 20 -

Table of Contents

LIQUIDITY AND CAPITAL RESOURCES