00013535382022FYFALSEP1YP3YP1Yhttp://fasb.org/us-gaap/2022#EmbeddedDerivativeGainLossOnEmbeddedDerivativeNethttp://fasb.org/us-gaap/2022#EmbeddedDerivativeGainLossOnEmbeddedDerivativeNet00013535382022-01-012022-12-3100013535382022-06-30iso4217:USD00013535382023-03-24xbrli:shares00013535382022-12-310001353538us-gaap:FairValueMeasurementsRecurringMember2022-12-3100013535382021-12-31iso4217:USDxbrli:shares00013535382021-01-012021-12-310001353538us-gaap:PreferredStockMember2020-12-310001353538us-gaap:CommonStockMember2020-12-310001353538us-gaap:AdditionalPaidInCapitalMember2020-12-310001353538us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001353538us-gaap:RetainedEarningsMember2020-12-3100013535382020-12-310001353538us-gaap:CommonStockMember2021-01-012021-12-310001353538us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001353538us-gaap:RetainedEarningsMember2021-01-012021-12-310001353538us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001353538us-gaap:PreferredStockMember2021-12-310001353538us-gaap:CommonStockMember2021-12-310001353538us-gaap:AdditionalPaidInCapitalMember2021-12-310001353538us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001353538us-gaap:RetainedEarningsMember2021-12-310001353538us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001353538us-gaap:RetainedEarningsMember2022-01-012022-12-310001353538us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310001353538us-gaap:PreferredStockMember2022-12-310001353538us-gaap:CommonStockMember2022-12-310001353538us-gaap:AdditionalPaidInCapitalMember2022-12-310001353538us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001353538us-gaap:RetainedEarningsMember2022-12-310001353538apgt:BrainspaceCorporationMember2022-01-012022-12-310001353538apgt:CyxteraTechnologiesIncMember2019-12-312019-12-31xbrli:pure0001353538apgt:CyxteraTechnologiesIncMember2019-12-310001353538apgt:BrainspaceCorporationMember2020-12-172020-12-170001353538apgt:BrainspaceCorporationMember2020-12-170001353538us-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2022-12-31apgt:segment0001353538srt:MinimumMember2022-01-012022-12-310001353538srt:MaximumMember2022-01-012022-12-3100013535382021-10-122021-10-120001353538apgt:AdvisorMember2021-10-122021-10-120001353538apgt:HoldersOfNewtownCommonStockAndAdvisorMember2021-10-120001353538apgt:SISHoldingsMember2021-10-1200013535382021-10-120001353538us-gaap:SegmentContinuingOperationsMember2021-01-012021-12-310001353538us-gaap:SegmentContinuingOperationsMember2022-01-012022-12-310001353538us-gaap:SegmentDiscontinuedOperationsMember2022-01-012022-12-310001353538us-gaap:SegmentDiscontinuedOperationsMember2021-01-012021-12-310001353538apgt:FormerParentMember2017-12-310001353538apgt:ManagementCompanyMember2021-01-012021-12-310001353538apgt:FormerParentAndManagementCompanyMemberapgt:PromissoryNotesMember2019-03-310001353538apgt:PromissoryNotesMember2021-01-012021-12-310001353538apgt:FormerParentMemberapgt:PromissoryNotesMember2021-02-082021-02-080001353538apgt:ManagementCompanyMemberapgt:PromissoryNotesMember2021-02-082021-02-080001353538apgt:ManagementCompanyMember2021-02-080001353538apgt:ManagementCompanyMember2021-02-082021-02-080001353538apgt:BrainspaceCorporationMember2021-01-202021-01-200001353538apgt:BrainspaceCorporationMember2021-01-200001353538apgt:MultiYearSubscriptionTermBasedLicensesMember2022-01-012022-12-310001353538apgt:MultiYearSubscriptionTermBasedLicensesMember2021-01-012021-12-310001353538apgt:SingleYearSubscriptionTermBasedLicensesMember2022-01-012022-12-310001353538apgt:SingleYearSubscriptionTermBasedLicensesMember2021-01-012021-12-310001353538apgt:SubscriptionTermBasedLicensesMember2022-01-012022-12-310001353538apgt:SubscriptionTermBasedLicensesMember2021-01-012021-12-310001353538apgt:SubscriptionSaaSMember2022-01-012022-12-310001353538apgt:SubscriptionSaaSMember2021-01-012021-12-310001353538apgt:SupportAndMaintenanceMember2022-01-012022-12-310001353538apgt:SupportAndMaintenanceMember2021-01-012021-12-310001353538apgt:SubscriptionRevenueMember2022-01-012022-12-310001353538apgt:SubscriptionRevenueMember2021-01-012021-12-310001353538apgt:PerpetualLicensesMember2022-01-012022-12-310001353538apgt:PerpetualLicensesMember2021-01-012021-12-310001353538apgt:ServicesAndOtherMember2022-01-012022-12-310001353538apgt:ServicesAndOtherMember2021-01-012021-12-310001353538country:US2022-01-012022-12-310001353538country:US2021-01-012021-12-310001353538country:CO2022-01-012022-12-310001353538country:CO2021-01-012021-12-310001353538apgt:OtherGeographicalLocationsMember2022-01-012022-12-310001353538apgt:OtherGeographicalLocationsMember2021-01-012021-12-310001353538apgt:UnitedStatesAndCanadaMember2022-01-012022-12-310001353538apgt:UnitedStatesAndCanadaMember2021-01-012021-12-310001353538srt:LatinAmericaMember2022-01-012022-12-310001353538srt:LatinAmericaMember2021-01-012021-12-310001353538us-gaap:EMEAMember2022-01-012022-12-310001353538us-gaap:EMEAMember2021-01-012021-12-310001353538srt:AsiaPacificMember2022-01-012022-12-310001353538srt:AsiaPacificMember2021-01-012021-12-310001353538us-gaap:SalesRevenueNetMembercountry:USus-gaap:GeographicConcentrationRiskMember2021-01-012021-12-310001353538country:COus-gaap:SalesRevenueNetMemberus-gaap:GeographicConcentrationRiskMember2021-01-012021-12-310001353538us-gaap:SalesRevenueNetMembercountry:USus-gaap:GeographicConcentrationRiskMember2022-01-012022-12-310001353538country:COus-gaap:SalesRevenueNetMemberus-gaap:GeographicConcentrationRiskMember2022-01-012022-12-3100013535382023-01-012022-12-310001353538us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001353538us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001353538us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001353538us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001353538us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001353538us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001353538us-gaap:FairValueMeasurementsRecurringMember2021-12-310001353538us-gaap:EmbeddedDerivativeFinancialInstrumentsMember2020-12-310001353538us-gaap:EmbeddedDerivativeFinancialInstrumentsMember2021-01-012021-12-310001353538us-gaap:EmbeddedDerivativeFinancialInstrumentsMember2021-12-310001353538us-gaap:EmbeddedDerivativeFinancialInstrumentsMember2022-01-012022-12-310001353538us-gaap:EmbeddedDerivativeFinancialInstrumentsMember2022-12-310001353538apgt:ConvertibleSeniorNotesMemberus-gaap:ConvertibleDebtMemberus-gaap:MeasurementInputPriceVolatilityMember2022-12-310001353538apgt:ConvertibleSeniorNotesMemberus-gaap:ConvertibleDebtMemberus-gaap:MeasurementInputPriceVolatilityMember2021-12-310001353538apgt:MeasurementInputBondRateMemberapgt:ConvertibleSeniorNotesMemberus-gaap:ConvertibleDebtMember2022-12-310001353538apgt:MeasurementInputBondRateMemberapgt:ConvertibleSeniorNotesMemberus-gaap:ConvertibleDebtMember2021-12-310001353538apgt:ConvertibleSeniorNotesMember2022-01-012022-12-310001353538apgt:ConvertibleSeniorNotesMember2021-01-012021-12-310001353538us-gaap:LeaseholdImprovementsMember2022-12-310001353538us-gaap:LeaseholdImprovementsMember2021-12-310001353538apgt:EquipmentAndFixturesMember2022-12-310001353538apgt:EquipmentAndFixturesMember2021-12-310001353538srt:MinimumMemberus-gaap:CustomerRelationshipsMember2022-01-012022-12-310001353538srt:MaximumMemberus-gaap:CustomerRelationshipsMember2022-01-012022-12-310001353538srt:MinimumMemberus-gaap:TrademarksAndTradeNamesMember2022-01-012022-12-310001353538srt:MaximumMemberus-gaap:TrademarksAndTradeNamesMember2022-01-012022-12-310001353538srt:MinimumMemberus-gaap:DevelopedTechnologyRightsMember2022-01-012022-12-310001353538srt:MaximumMemberus-gaap:DevelopedTechnologyRightsMember2022-01-012022-12-310001353538us-gaap:CustomerRelationshipsMember2022-12-310001353538us-gaap:CustomerRelationshipsMember2021-12-310001353538us-gaap:CustomerRelationshipsMember2022-01-012022-12-310001353538us-gaap:TrademarksAndTradeNamesMember2022-12-310001353538us-gaap:TrademarksAndTradeNamesMember2021-12-310001353538us-gaap:TrademarksAndTradeNamesMember2022-01-012022-12-310001353538us-gaap:DevelopedTechnologyRightsMember2022-12-310001353538us-gaap:DevelopedTechnologyRightsMember2021-12-310001353538us-gaap:DevelopedTechnologyRightsMember2022-01-012022-12-310001353538apgt:TrademarksAndTradenamesAndDevelopedTechnologyRightsMember2022-01-012022-12-310001353538us-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2021-12-310001353538apgt:ConvertibleSeniorNotesMemberus-gaap:ConvertibleDebtMember2022-12-310001353538apgt:ConvertibleSeniorNotesMemberus-gaap:ConvertibleDebtMember2021-12-310001353538us-gaap:RevolvingCreditFacilityMember2022-01-012022-12-310001353538us-gaap:RevolvingCreditFacilityMember2021-01-012021-12-310001353538apgt:ConvertibleSeniorNotesMemberus-gaap:ConvertibleDebtMember2022-01-012022-12-310001353538apgt:ConvertibleSeniorNotesMemberus-gaap:ConvertibleDebtMember2021-01-012021-12-310001353538us-gaap:NotesPayableOtherPayablesMemberapgt:PromissoryNotesMember2022-01-012022-12-310001353538us-gaap:NotesPayableOtherPayablesMemberapgt:PromissoryNotesMember2021-01-012021-12-310001353538us-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2022-04-260001353538apgt:ConvertibleSeniorNotesMemberus-gaap:ConvertibleDebtMember2021-02-090001353538apgt:ConvertibleSeniorNotesMemberus-gaap:ConvertibleDebtMember2021-10-120001353538apgt:ConvertibleSeniorNotesMemberus-gaap:ConvertibleDebtMemberapgt:CashInterestPaymentsMember2022-12-310001353538apgt:PaidInKindInterestPaymentsMemberapgt:ConvertibleSeniorNotesMemberus-gaap:ConvertibleDebtMember2022-12-310001353538us-gaap:DebtInstrumentRedemptionPeriodOneMemberapgt:ConvertibleSeniorNotesMemberus-gaap:ConvertibleDebtMember2022-01-012022-12-310001353538us-gaap:DebtInstrumentRedemptionPeriodTwoMemberapgt:ConvertibleSeniorNotesMemberus-gaap:ConvertibleDebtMember2022-01-012022-12-310001353538apgt:ConvertibleSeniorNotesMember2022-12-310001353538us-gaap:LetterOfCreditMember2022-12-310001353538apgt:ClassBProfitInterestUnitsMember2017-05-310001353538apgt:ClassBProfitInterestUnitsMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2022-01-012022-12-310001353538apgt:ClassBProfitInterestUnitsMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2022-01-012022-12-310001353538apgt:ClassBProfitInterestUnitsMember2022-01-012022-12-310001353538apgt:ClassBProfitInterestUnitsMember2020-12-310001353538apgt:ClassBProfitInterestUnitsMember2021-01-012021-12-310001353538apgt:ClassBProfitInterestUnitsMember2021-12-310001353538apgt:ClassBProfitInterestUnitsMember2022-12-310001353538us-gaap:CostOfSalesMember2022-01-012022-12-310001353538us-gaap:CostOfSalesMember2021-01-012021-12-310001353538us-gaap:SellingAndMarketingExpenseMember2022-01-012022-12-310001353538us-gaap:SellingAndMarketingExpenseMember2021-01-012021-12-310001353538us-gaap:ResearchAndDevelopmentExpenseMember2022-01-012022-12-310001353538us-gaap:ResearchAndDevelopmentExpenseMember2021-01-012021-12-310001353538us-gaap:GeneralAndAdministrativeExpenseMember2022-01-012022-12-310001353538us-gaap:GeneralAndAdministrativeExpenseMember2021-01-012021-12-310001353538apgt:A2021PlanMember2021-01-012021-12-310001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2021-12-310001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2021-12-310001353538us-gaap:PhantomShareUnitsPSUsMember2021-12-310001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2022-01-012022-03-310001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2022-01-012022-03-310001353538us-gaap:PhantomShareUnitsPSUsMember2022-01-012022-03-310001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2022-03-310001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2022-03-310001353538us-gaap:PhantomShareUnitsPSUsMember2022-03-310001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2022-04-012022-06-300001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2022-04-012022-06-300001353538us-gaap:PhantomShareUnitsPSUsMember2022-04-012022-06-300001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2022-06-300001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2022-06-300001353538us-gaap:PhantomShareUnitsPSUsMember2022-06-300001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2022-07-012022-09-300001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2022-07-012022-09-300001353538us-gaap:PhantomShareUnitsPSUsMember2022-07-012022-09-300001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2022-09-300001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2022-09-300001353538us-gaap:PhantomShareUnitsPSUsMember2022-09-300001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2022-01-012022-12-310001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2022-01-012022-12-310001353538us-gaap:PhantomShareUnitsPSUsMember2022-01-012022-12-310001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2022-12-310001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2022-12-310001353538us-gaap:PhantomShareUnitsPSUsMember2022-12-310001353538apgt:A2021PlanMember2022-01-012022-12-310001353538srt:MinimumMember2022-12-310001353538srt:MaximumMember2022-12-310001353538apgt:EmployerMatchTrancheOneMember2022-01-012022-12-310001353538apgt:EmployerMatchTrancheTwoMember2022-01-012022-12-310001353538srt:MinimumMemberapgt:EmployerMatchTrancheTwoMember2022-01-012022-12-310001353538srt:MaximumMemberapgt:EmployerMatchTrancheTwoMember2022-01-012022-12-310001353538apgt:OperatingLossCarryforwardExpirationPeriodYearOneMemberus-gaap:DomesticCountryMember2022-12-310001353538us-gaap:DomesticCountryMemberapgt:OperatingLossCarryforwardExpirationPeriodYearTwoMember2022-12-310001353538apgt:OperatingLossCarryforwardExpirationPeriodYearThreeMemberus-gaap:DomesticCountryMember2022-12-310001353538us-gaap:DomesticCountryMember2022-12-310001353538us-gaap:StateAndLocalJurisdictionMember2022-12-310001353538us-gaap:ForeignCountryMember2022-12-310001353538apgt:ReverseRecapitalizationAndPastAcquisitionsMember2022-12-310001353538country:US2022-12-310001353538country:SE2022-12-310001353538apgt:OtherGeographicalLocationsMember2022-12-310001353538country:US2021-12-310001353538country:SE2021-12-310001353538apgt:OtherGeographicalLocationsMember2021-12-310001353538us-gaap:AssetsMembercountry:USus-gaap:GeographicConcentrationRiskMember2022-01-012022-12-310001353538us-gaap:AssetsMembercountry:SEus-gaap:GeographicConcentrationRiskMember2021-01-012021-12-310001353538us-gaap:AssetsMembercountry:USus-gaap:GeographicConcentrationRiskMember2021-01-012021-12-310001353538us-gaap:AssetsMembercountry:SEus-gaap:GeographicConcentrationRiskMember2022-01-012022-12-310001353538apgt:CyxteraTechnologiesIncMember2022-12-31apgt:boardMember0001353538apgt:SISHoldingsMemberapgt:CyxteraTechnologiesIncMember2022-03-230001353538apgt:SaleOfCybersecurityProductsAndServicesMemberapgt:CyxteraTechnologiesIncMember2022-01-012022-12-310001353538apgt:SaleOfCybersecurityProductsAndServicesMemberapgt:CyxteraTechnologiesIncMember2022-12-310001353538apgt:SaleOfCybersecurityProductsAndServicesMemberapgt:CyxteraTechnologiesIncMember2021-12-310001353538apgt:PurchaseOfDataCenterCoLocationAndCXDServicesMemberapgt:CyxteraTechnologiesIncMember2022-01-012022-12-310001353538apgt:PurchaseOfDataCenterCoLocationAndCXDServicesMemberapgt:CyxteraTechnologiesIncMember2021-01-012021-12-310001353538apgt:PurchaseOfDataCenterCoLocationAndCXDServicesMemberapgt:CyxteraTechnologiesIncMember2022-12-310001353538apgt:PurchaseOfDataCenterCoLocationAndCXDServicesMemberapgt:CyxteraTechnologiesIncMember2021-12-310001353538apgt:ChewyIncMember2022-12-310001353538apgt:ChewyIncMemberapgt:SaleOfCybersecurityProductsAndServicesMember2022-01-012022-12-310001353538apgt:ChewyIncMemberapgt:SaleOfCybersecurityProductsAndServicesMember2021-01-012021-12-310001353538apgt:ChewyIncMemberapgt:SaleOfCybersecurityProductsAndServicesMember2021-12-310001353538apgt:ChewyIncMemberapgt:SaleOfCybersecurityProductsAndServicesMember2022-12-310001353538apgt:PetSmartMember2022-12-310001353538apgt:PetSmartMembersrt:DirectorMember2022-01-012022-12-310001353538apgt:CenturyLinkCommunicationsLLCMemberapgt:SISHoldingsMember2022-12-310001353538apgt:SaleOfCybersecurityProductsAndServicesMemberapgt:CenturyLinkCommunicationsLLCMember2022-01-012022-12-310001353538apgt:SaleOfCybersecurityProductsAndServicesMemberapgt:CenturyLinkCommunicationsLLCMember2021-01-012021-12-310001353538apgt:SaleOfCybersecurityProductsAndServicesMemberapgt:CenturyLinkCommunicationsLLCMember2022-12-310001353538apgt:SaleOfCybersecurityProductsAndServicesMemberapgt:CenturyLinkCommunicationsLLCMember2021-12-310001353538us-gaap:SubsequentEventMember2023-02-022023-02-020001353538us-gaap:SubsequentEventMember2023-01-012023-03-310001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMemberus-gaap:SubsequentEventMember2023-03-280001353538us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMemberus-gaap:SubsequentEventMember2023-03-280001353538us-gaap:SubsequentEventMemberus-gaap:PhantomShareUnitsPSUsMember2023-03-280001353538us-gaap:RevolvingCreditFacilityMemberus-gaap:SubsequentEventMemberus-gaap:LineOfCreditMember2023-01-312023-01-310001353538us-gaap:RevolvingCreditFacilityMemberus-gaap:SubsequentEventMemberus-gaap:LineOfCreditMember2023-03-310001353538apgt:PaidInKindNotesMemberus-gaap:NotesPayableOtherPayablesMemberus-gaap:SubsequentEventMember2023-02-012023-02-01

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| | | | | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2022

OR

| | | | | |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _____________ to _____________

Commission file number 000-52776

Appgate, Inc.

(Exact name of registrant as specified in its charter)

| | | | | |

| Delaware | 20-3547231 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| |

2 Alhambra Plaza, Suite PH-1-B | |

Coral Gables, FL | 33134 |

(Address of principal executive offices) | (Zip Code) |

(866) 524-4782

Registrant's telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| N/A | N/A | N/A |

Securities registered pursuant to section 12(g) of the Act:

Common Stock, $0.001 par value

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated filer | o | Accelerated filer | o |

Non-accelerated filer | x | Smaller reporting company | x |

| | Emerging growth company | o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. o

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No x

As of June 30, 2022, the last business day of the registrant’s most recently completed second quarter, the aggregate market value of the registrant’s common stock, par value $0.001 per share (“common stock”) held by non-affiliates of the registrant was approximately $40.1 million based on the closing price of $7.50 per share of the registrant’s common stock as quoted on the OTC Markets on that date. For purposes of determining this number, each executive officer, director, and holder (known to the registrant) of more than 10% of our common stock as of June 30, 2022 have been considered affiliates of the registrant. This number is provided solely for the purposes of this Annual Report on Form 10-K and does not represent an admission by either the registrant or any such person as to the affiliate status of such person.

As of March 24, 2023, the registrant had 131,793,660 shares of its common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

Table of Contents

| | | | | |

| Page |

| |

| Frequently Used Terms | |

| Cautionary Statement Regarding Forward-Looking Statements | |

| Summary of Principal Risk Factors | |

| |

| |

| |

Item 1A. Risk Factors | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

Item 9C. Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | |

| |

| |

Item 10. Directors, Executive Officers and Corporate Governance | |

Item 11. Executive Compensation | |

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

Item 13. Certain Relationships and Related Transactions, and Director Independence | |

| |

| |

| |

| |

| Item 16. Form 10-K Summary | |

| |

| |

Frequently Used Terms

Unless otherwise stated or unless the context otherwise requires, the terms “we,” “us,” “Appgate,” “our,” and the “Company” refer to Appgate, Inc., a Delaware corporation (f/k/a Newtown Lane Marketing, Incorporated), and its consolidated subsidiaries following the Closing (as defined below):

•“2021 Plan” means the Appgate, Inc. 2021 Incentive Compensation Plan.

•“A&R Bylaws” means our amended and restated bylaws, effective October 12, 2021.

•“A&R Charter” means our second amended and restated certificate of incorporation, dated October 12, 2021.

•“Additional Convertible Senior Notes” means the additional $25.0 million aggregate principal amount of Legacy Appgate’s 5.00% Convertible Senior Notes due 2024 issued on the Closing Date.

•“Board” or “Board of Directors” means the board of directors of the Company.

•“Closing” means the consummation of the Merger.

•“Closing Date” means the date of the Closing on October 12, 2021.

•“Code” means the Internal Revenue Code of 1986, as amended.

•“Convertible Senior Notes” means the Initial Convertible Senior Notes, Additional Convertible Senior Notes and PIK Notes, collectively, issued, or with respect to additional PIK Notes, if issued, by Legacy Appgate and guaranteed by the Company and certain of its subsidiaries, which Conversion Obligations and Change of Control Conversion Obligations (as such terms are defined in the Note Issuance Agreement) thereunder were assumed by the Company on the Closing Date.

•“Cyxtera” means Cyxtera Technologies, Inc., a Delaware corporation and Legacy Appgate’s former parent.

•“DGCL” means the General Corporation Law of the State of Delaware.

•“Exchange Act” means the Securities Exchange Act of 1934, as amended.

•“GAAP” means generally accepted accounting principles in the United States.

•“Initial Convertible Senior Notes” means the $50.0 million aggregate principal amount of Legacy Appgate’s 5.00% Convertible Senior Notes due 2024 issued on February 9, 2021.

•“Legacy Appgate” means Appgate Cybersecurity, Inc. (f/k/a Cyxtera Cybersecurity, Inc. d/b/a AppGate), a Delaware corporation.

•“Magnetar” means Magnetar Financial LLC.

•“Merger” means the merger of Merger Sub with and into Legacy Appgate, with Legacy Appgate surviving the Merger and becoming a wholly owned subsidiary of the Company pursuant to the terms of the Merger Agreement.

•“Merger Agreement” means that certain agreement and plan of reorganization, dated February 8, 2021 entered into by and among Newtown Lane, Merger Sub and Legacy Appgate.

•“Merger Sub” means Newtown Merger Sub. Corp., a Delaware corporation and wholly owned subsidiary of Newtown Lane.

•“Nasdaq” means the Nasdaq Stock Exchange.

•“Newtown Lane” means the Company, prior to the Merger, which then had the name Newtown Lane Marketing, Incorporated.

•“Noteholders” means the holders of the Company’s Convertible Senior Notes.

•“Note Issuance Agreement” means that certain note issuance agreement, dated as of February 8, 2021, as amended, governing the issuance and terms of the Convertible Senior Notes, among Legacy Appgate, Legacy Appgate’s wholly owned domestic subsidiaries and Magnetar Financial, LLC, as the representative of the Noteholders.

•“Note Purchase Agreement” means that certain note purchase agreement, dated as of February 8, 2021, as amended, by and among Legacy Appgate and the Noteholders, pursuant to which Legacy Appgate sold the Convertible Senior Notes to the Noteholders.

•“NYSE” means the New York Stock Exchange.

•“PIK Notes” means any of Legacy Appgate’s 5.00% Convertible Senior Notes due 2024 issued, or to be issued, as payment-in-kind with respect to interest payable under outstanding Convertible Senior Notes, including the additional approximately $2.1 million aggregate principal amount of Legacy Appgate’s 5.00% Convertible Senior Notes due 2024 issued on February 1, 2023.

•“Revolving Credit Facility” means that certain subordinated revolving credit facility, in an aggregate principal amount of $50.0 million, to be provided by SIS Holdings to Legacy Appgate pursuant to the Revolving Credit Agreement.

•“Revolving Credit Agreement” means that certain Revolving Credit Agreement entered into on April 26, 2022 by and among Legacy Appgate, the Company, certain subsidiaries of Legacy Appgate and SIS Holdings.

•“SIS Holdings” means SIS Holdings LP, a Delaware limited partnership.

•“SEC” means the U.S. Securities and Exchange Commission.

•“Securities Act” means the Securities Act of 1933, as amended.

Cautionary Statement Regarding Forward-Looking Statements

This Annual Report on Form 10-K (this “Annual Report”) contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and Section 27A of the Securities Act of 1933, as amended. Statements that do not relate strictly to historical or current facts are forward-looking and can be identified by the use of words such as “anticipate,” “estimate,” “could,” “would,” “should,” “will,” “may,” “forecast,” “approximate,” “expect,” “project,” “seek,” “predict,” “potential,” “intend,” “plan,” “believe,” and other words of similar meaning. Without limiting the generality of the foregoing, forward-looking statements contained in this Annual Report include statements regarding the Company and its industry relating to matters such as anticipated future financial and operational performance, business prospects, the percentage of the Company’s future revenue derived from subscription term-based licenses compared to revenue from services, expected future increases in revenue and sales, including increasing the Company’s customer base and customers with annual recurring revenue above $100,000, sales to existing customers, the U.S. federal government and governments around the world and through the Company’s channel partners and product partnerships, growth in international markets, revenue trends by geography, future gross profit, gross margin, operating losses and negative cash flows, expected increases in gross profit and gross margin, the Company’s expected future net loss position, planned investments in sales and marketing and related increases in operating and general and administrative expenses, expectations regarding our annual recurring revenue and other key business metrics, expected future decreases in sales and marketing and general and administrative expenses as a percentage of revenue over time, planned investments in research and development as a result of the Company’s expected growth, the expected future growth of the cybersecurity industry, including the growth in adoption of, and replacement of legacy perimeter-centric security solutions by, Zero Trust security solutions, the Company’s ability to innovate and add new functionality to existing products through research and development, the Company’s ability to compete with competitors who offer similar products or services, the Company’s ability to continue as a going concern absent access to sources of liquidity, the Company’s ability to remain in compliance with covenants under the Convertible Senior Notes and the Revolving Credit Facility, the impact of foreign currency

exchanges and inflation on the Company’s business, the Company’s ability to remain listed on a national stock exchange, strategy and plans and similar matters.

The forward-looking statements included in this Annual Report involve risks and uncertainties that could cause actual results to differ materially from projected results. Accordingly, investors should not place undue reliance on forward-looking statements as a prediction of actual results. The Company has based these forward-looking statements on current expectations and assumptions about future events, taking into account all information currently known by the Company. While the Company considers these expectations and assumptions to be reasonable, they are inherently subject to significant business, economic, competitive, regulatory and other risks and uncertainties, many of which are difficult to predict and beyond our control. These risks and uncertainties include, but are not limited to:

• our future financial performance, including our expectations regarding our annual recurring revenue and other key business metrics, total revenue, cost of revenue, gross profit or gross margin, operating expenses, including changes in operating expenses and our ability to achieve and maintain future profitability;

• our ability to continue as a going concern absent access to sources of liquidity;

• the effects of increased competition in our markets and our ability to compete effectively;

• growth in the total addressable market for our products and services;

• market acceptance of Zero Trust solutions and technology generally;

• market acceptance of our products and services and our ability to increase adoption of our products;

• our ability to maintain the security and availability of our products;

• our ability to develop new products, or enhancements to our existing products, and bring them to market in a timely manner;

• our ability to maintain and expand our customer base, including by attracting new customers;

• our ability to maintain, protect and enhance our intellectual property rights;

• our ability to comply with laws and regulations that currently apply or become applicable to our business both in the United States and internationally;

• our ability to maintain an effective system of disclosure controls and internal control over financial reporting;

• SIS Holdings’ significant influence over our business and affairs;

• the future trading prices and liquidity of our common stock;

• our indebtedness, which may increase risk to our business; and

• other risks and uncertainties, including those described in “Item 1A—Risk Factors” of this Annual Report.

All forward-looking statements made by us in this Annual Report are expressly qualified in their entirety by the foregoing cautionary statements. All such statements speak only as of the date made, and we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

Summary of Principal Risk Factors

Our business is subject to a number of risks, including risks that may prevent us from achieving our business objectives or may adversely affect our business, financial condition, results of operations, cash flows and prospects. These risks are discussed more in Item 1A of this Annual Report, and include, but are not limited to, the following:

•we have a history of losses, may not be able to achieve or sustain profitability in the future and expect to incur significant losses for the foreseeable future;

•we face significant competition and could lose market share to our competitors, which could adversely affect our business, financial condition and results of operations;

•our operating results may fluctuate significantly, which could make our future results difficult to predict and could cause our operating results to fall below expectations;

•false positive or false negative detection of risk, application tampering, viruses, spyware, vulnerability exploits, data patterns, or URL categories could adversely affect our business;

•if our software does not interoperate with our customers’ network and security infrastructure or with third-party products, websites or services, our products may become less competitive and our results of operations may be harmed;

•if we fail to develop or introduce new enhancements to our products on a timely basis, our ability to attract and retain customers, remain competitive and grow our business could be impaired. Our current research and development efforts may not produce successful products that result in significant revenue, cost savings or other benefits in the near future, if at all;

•if organizations do not adopt a Zero Trust model for cybersecurity, our ability to grow our business and operating results may be adversely affected;

•if we are unable to attract new customers or if our existing customers do not renew their subscriptions for our services or add additional users and services to their subscriptions the future results of our operations could be harmed;

•if the delivery of our services to our customers is interrupted or delayed for any reason, our business could suffer;

•a network or data security incident against us, whether actual, alleged, or perceived, could harm our reputation, create liability, and regulatory exposure, and adversely impact our business, operating results, and financial condition;

•the actual or perceived failure of our technology solutions to prevent a security breach or address targeted security threats could harm our reputation and adversely impact our business, financial condition and results of operations;

•claims by others that we infringe their proprietary technology or other rights, or other lawsuits asserted against us, could result in significant costs and substantially harm our business, financial condition, results of operations and prospects;

•if we fail to maintain effective disclosure controls and internal control over financial reporting, our ability to produce timely and accurate financial statements or comply with applicable regulations could be impaired;

•management has performed an analysis of our ability to continue as a going concern, and has determined that, based on our current financial position, there is a substantial doubt about our ability to continue as a going concern; in addition, our independent registered public accounting firm has raised substantial doubt as to our ability to continue as a going concern;

•SIS Holdings can control our business and affairs and may have conflicts of interest with us in the future;

•our common stock is currently thinly traded, liquidity is limited, and we may be unable to obtain listing of our common stock on a more liquid market; and

•we have indebtedness, which may increase risk to our business and your investment in us.

PART I

Item 1. Business

Mission Statement

Our mission is to empower and protect how people work and connect by enabling any user on any device to securely access any application, use any network or cloud and perform any transaction.

Overview

We believe we are defining a new category of Zero Trust access for enterprises and governments. Our Zero Trust platform is designed to protect against increasingly damaging breaches through innovative, identity-centric, context-aware solutions. Our pure-play focus on Zero Trust has enabled us to deliver the highest ranked current Zero Trust Network Access offering as determined by the Forrester New Wave™: Zero Trust Network Access, Q3 2021.

Legacy security platforms continue to fail. Secure access has always been essential to establishing trust between users and technologies. We believe that the Zero Trust framework secures all primary use cases including customer, employee, partner, cloud and Internet of Things (“IoT”). It is a framework for securing infrastructure and data for today’s modern digital environment. Legacy security models, such as virtual private network (“VPN”), give users unnecessarily wide, unrestricted and overprivileged network access. This enables attackers to move easily within organizations and cause tremendous damage. In contrast, Zero Trust is designed to transform security by granting users access to only those resources that are needed to do their job at a particular time and place. Zero Trust uniquely addresses the modern challenges of today’s business, including securing remote workers, controlling access to cloud environments, and defending against ransomware threats.

This new Zero Trust paradigm is needed today because enterprises are undergoing digital transformation as they seek to automate operations, generate new revenue streams, transition business models and deliver a seamless customer experience. Digital transformation, driven by growth in cloud computing, Software as a Service (“SaaS”), mobile devices, IoT, and similar technologies, as well as the increasing prevalence of remote work, has changed the nature of cybersecurity risks by proliferating the number of entry points to organizations’ networks. This is often referred to as “increasing the attack surface”. Simultaneously, the number and sophistication of cyberattacks have increased dramatically, as has their costs and frequency. This combination of more vulnerable networks and more malicious activity has created a cybersecurity crisis, changing the threat landscape organizations face. As a result, enterprises require security access solutions that proactively ensure the right user has authorized access to the right resources at the right time.

We have built a Zero Trust platform which, we believe, is a critical, central pillar of a modern cyber security architecture that will replace legacy perimeter-centric security solutions and is designed to address the current cybersecurity crisis. These legacy solutions are insufficient to secure organizations, their infrastructure and their data. By contrast, we believe that our Zero Trust solutions secure an enterprise’s exponentially increased attack surface, which occurs as a result of their digital transformation journey. We also offer digital threat protection and risk-based authentication tools to identify and eliminate attacks before they occur, across social media, phishing attacks, bogus websites, and malicious mobile apps.

Our solutions give our customers the ability to lower costs and increase efficiency, while improving compliance and providing security that is persistent, identity-centric and context-aware. Our platform enables enterprises to leverage existing investments in IT and security infrastructure. The subsequent cost savings and returns on investments include: leveraging existing network security controls to effectively apply policies, using a service desk business process to control network access and automating cloud security with a Zero Trust framework.

We are pioneering Zero Trust access across all environments, including public cloud, private cloud, multi-cloud, on-premises or permutations of all of the above and believe its rapid adoption signals the early stages of a long-term shift away from legacy perimeter-centric security solutions. We believe our purpose-built capabilities address the hybrid, cloud, and on-premises network security markets, which Gartner estimates was approximately a combined $39 billion market opportunity in 2021, expected to grow at a 14% compound annual growth rate (“CAGR”) to reach approximately $57 billion by 2024. Gartner has also stated that Zero Trust Network Access remains a dynamic space, with 2021 global market revenue exceeding 60% growth over 2020, and expected to almost triple from 2021 through 2025. We also believe a subset of our capabilities address the Fraud Detection and Prevention (“FDP”) market, which, according to Global Market Insights, was a $30 billion market in 2022 and is expected to grow at a 25% CAGR from 2023-2032.

Our leadership in Zero Trust has also been recognized by third party research firms. Forrester, the firm that originally coined the term “Zero Trust,” named us a leader in the Forrester New Wave™ for Zero Trust Network Access report (September 2021). The report highlighted our ability to address cloud, on-premises and hybrid IT models, noting that Appgate “Software Defined Perimeter”, or SDP, “is the best fit for companies that need high security and a self-hosted option. Appgate offers its Zero Trust Network Access (“ZTNA”) as a SaaS, but also as a self-hosted option for enterprises and agencies that need it.” Separately, Forrester also named us a leader in their initial Forrester Wave™ Zero Trust eXtended Ecosystem report (September 2020). The report noted that Appgate serves mega-enterprises and Department of Defense (“DoD”) customers, which we believe is a testament to our capabilities and positions us well to benefit from the rising demand for Zero Trust solutions.

We believe our solutions address the complex needs of global enterprises and governments. Our go-to-market strategy consists of both direct sales and indirect channel partners. As of December 31, 2022, we served approximately 650 organizations across approximately 70 countries, including domestic and international government agencies and Fortune 500 enterprises that include at least one of the largest companies by revenue in each of the defense contracting, telecommunications, systems integrator, and oil and gas sectors.

We sell our solutions primarily through a recurring revenue license model or subscription, and employ a ‘land and expand’ strategy to generate incremental revenue through the addition of new users and the sale of additional products. We believe the success of our strategy is validated by our strong dollar-based net retention rates. Our dollar based net retention rates were 96% and 114% at December 31, 2022 and 2021, respectively. Our annual recurring revenue (“ARR”) was $33.7 million and $31.1 million at December 31, 2022 and 2021, respectively. See “Item 7—Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Business Metrics” for additional information regarding ARR.

We achieved revenue of over $40.0 million in each of 2022 and 2021. We continue to invest in growing our business and, as a result, we incurred losses from continuing operations of $54.2 million for the year ended December 31, 2021 and $80.1 million for the year ended December 31, 2022.

Industry Background

Digital Transformation has Upended Traditional IT Architectures and Environments

Rapidly accelerating digitization has transformed traditional IT architectures, and organizations are confronting the need—indeed the requirement—to transform their business models and environments from legacy, standalone, static systems, and applications, to more dynamic, cloud-native, distributed solutions. For decades, IT environments were defined by company-owned devices operating on company-owned or controlled infrastructure and networks. However, the explosion of the internet, rise of cloud computing, and the proliferation of workloads and mobile devices has upended the legacy IT infrastructure model.

•Proliferation of the cloud and the rise of “as-a-service” solutions. Organizations have embraced cloud-based “as-a-service” delivery models to empower employees and customers and increase the speed of deployment. According to Gartner, more than 85% of organizations will embrace a cloud first principle by 2025 and will not be able to fully execute on their digital strategies without the use of cloud-native architectures and technologies. IDC forecasts the global public cloud services market to grow to approximately $809 billion in 2025 from $385 billion in 2021. These types of environments have massively increased the complexity of IT infrastructure and expanded the scope of the corporate network. This is especially true as enterprises increasingly adopt powerful but complex Infrastructure and Platform as a service (IaaS and PaaS) for the development and deployment of custom and mission-critical business applications.

•Work from anywhere and bring your own device (“BYOD”). Organizations now expect their workers to securely move from place-to-place and device-to-device without losing productivity. These same workers are also now encouraged, and often expected, to use their own devices for work-related activities. The work from anywhere, BYOD culture, with employees accessing corporate applications on their personal laptops, tablets, and smartphones, has accelerated over a number of years and now appears permanent. Businesses have been forced to adjust their IT environments in response to these trends and are faced with employee devices that lack the level of control and security of company-owned devices. As a result, the corporate network has been extended well beyond the secure boundaries of a corporate office, leaving it significantly more exposed to cyberthreats.

•Connected devices and the internet of things (“IoT”). From mobile devices to cameras and sensors, the number of devices on a corporate network has multiplied exponentially over the last few years and is expected to continue growing rapidly due to new technologies such as 5G and the business and technical benefits delivered by these new technologies and tools. According to IOT Analytics, the number of connected IoT devices is expected to reach 27 billion by 2025, up from 12.2 billion in 2021. This trend has served to significantly increase the attack surface.

Cybersecurity Threats and Impact Multiplying

The evolution of IT environments coupled with motivated and sophisticated hackers has increased the risk of cybersecurity attacks. Lateral network movement, ransomware, and insecure remote access are resulting in a higher number of attacks of worsening severity with a lengthened time to detection. According to Secureworks’ 2022 State of the Threat, ransomware remains the primary threat facing organizations.

•Expanded attack surfaces. As IT environments have evolved, the adoption of hybrid, multi-cloud, BYOD, and IoT, as well as the massive shift to remote work, has altered the nature of cybersecurity risks by growing exponentially the number of entry points to organizations’ networks. With each new user, connection, device, or online interaction, the attack surface, the scope of network vulnerabilities, and the likelihood of network infiltration all increase. The increased attack surface also serves as a source of increased complexity for enterprise defenders. To date, traditional security tools and strategies have not kept up with this increased complexity.

•Lateral movement. Once a hacker penetrates a network, their ability to move laterally allows them to travel extensively throughout the network, increasing the volume of data they are able to compromise, and increasing the risk that more sensitive data is exposed. The ability to move laterally and remain undetected for long periods of time in the network is one of the leading drivers behind the high costs of breaches. The 2020 “SolarWinds” attack, which affected as many as 425 of the Fortune 500 and all branches of the US military, highlights the ability of an attacker to leverage lateral movement after breaching an organization’s network. The original breach occurred sometime between March and June of 2020, when clients of SolarWinds downloaded a software update that was infected with malicious code. The perpetrators were then able to move laterally within the networks of these organizations, remaining undetected by traditional perimeter-based network security solutions until December of 2020, providing the hackers with ample time to gather sensitive data and install more malware. In addition to threats caused by external actors, insider threats, typically coming from employees or third-party contractors, also pose a growing security threat to organizations. According to the Ponemon Institute Cost of Insider Threats Global Report, insider incident average cost ranged from $485,000 to $805,000 per incident, with 56% of incidents due to negligence.

•Sophisticated adversaries. Today’s hackers are highly skilled, often backed by well-funded militaries, intelligence services, or criminal organizations and motivated by some combination of financial, criminal, and terrorist objectives. They can launch complex attacks, often executed over multiple steps, starting with an initial breach of the corporate network followed by lateral movement, slowly escalating their privileges to access increasingly critical and proprietary data.

The combination of more vulnerable networks and more malicious activity has created a cybersecurity crisis for organizations. Cybersecurity Ventures expects global cybercrime costs to grow by 15% per year, reaching $10.5 trillion annually by 2025. Cybersecurity breaches can also have a significant impact on society beyond the direct financial costs. This is illustrated by the Colonial Pipeline ransomware attack in 2021, which resulted in fuel shortages and spikes in gasoline prices across a number of U.S. states, and by the spike in cyberattacks on health care systems during the pandemic, impacting patient care.

Traditional Cybersecurity Tools are Limited in Protecting Against Today’s Threats

Traditional cybersecurity tools are failing to meet the challenge of modern IT environments due to inherent weaknesses in their structure and design philosophy.

•Implicit trust at the center of traditional perimeter-centric security model. Traditional cybersecurity tools are largely perimeter-centric, focused on securing the boundary between a private network and the public internet.

This model is built on the notion of implicit trust, which is the assumption that traffic originating from within a private network does not represent a risk. This critical characteristic allows for lateral movement, giving infiltrators the ability to remain undetected as they move across a network, causing widespread and costly damage. According to the IBM Cost of a Data Breach Report, in 2022 it took an average of 207 days to identify a breach, and another 70 days to contain, giving an attacker plenty of time to cause significant financial and reputational damage to an organization. While this perimeter-centric approach worked historically when enterprise networks had fewer points of entry, today’s IT environments and distributed workloads have softened the network perimeter, blunting the effectiveness of the perimeter-centric security model.

•Outdated tools are siloed and lack context awareness. Traditional security tools such as VPNs, firewall equipment, and network access control (“NAC”) equipment are outdated, siloed, have well-known and widely exploited vulnerabilities, and are unable to properly secure a modern IT environment. These tools employ an outdated model of a single network perimeter entry point and broad network access privileges. VPNs inherently have a “coarse-grained” access control model, granting or denying users access to broad sections of the network, and lack context-aware, fine-grained security permissions, resulting in increased severity of any breach.

•Cybersecurity defenses are overly complex. Organizations often deploy numerous cybersecurity tools from various vendors, reactively deploying new tools in response to emerging threats. This has left many organizations with a patchwork cybersecurity model consisting of a mix of tools from a range of vendors, typically with poor integration and communication among tools, lacking an integrated cybersecurity solution with a unified control point. The resulting complexity makes it challenging for IT professionals to manage the tools effectively and offers poor visibility into potential vulnerabilities and breaches. The need for a new paradigm and approach to cybersecurity is crucial to protect organizations from adversaries and to avoid costly network breaches.

Cybersecurity Defense is Shifting to a Context-Aware, Dynamic Security Model

Zero Trust represents a paradigm shift in cybersecurity. It moves from the legacy static, network-based, perimeter-centric security model to a dynamic, context-aware model based on users, identities, applications, and business processes. The foundation of the Zero Trust model is the idea that no person, device, or application should be implicitly trusted, and that the entire extended network represents an attack surface.

Why a Zero Trust Framework Works

•Eliminates the need for implicit trust. Zero Trust eliminates the need for the implicit trust that is often granted based on physical or network location, and instead requires that all access be identity-driven and earned via dynamic attributes and strong authentication.

•Context-aware and secure access privileges. The Zero Trust model grants users access only to specific and required resources unlike the traditional security model designed on the premise of implicit trust where users are given overprivileged access and can move laterally within a network. Users are continuously monitored, and if their context or device changes, network access can be revised accordingly or revoked entirely. This approach represents a paradigm shift in the cybersecurity posture, increasing organizational resiliency when facing attacks and better equipping them to isolate and limit the impact of any network breach.

Zero Trust framework has emerged as the clear answer to today’s cybersecurity threats. Following the “SolarWinds” attack, the National Institute of Standards and Technology (“NIST”), the National Security Agency (“NSA”) and the Cybersecurity and Infrastructure Security Agency (“CISA”) released guidance recommending a Zero Trust framework. Subsequently, in May 2021, President Joe Biden issued an Executive Order explicitly calling for the adoption of a Zero Trust Architecture by the federal government to improve the nation’s response to “persistent and increasingly sophisticated malicious cyber campaigns that threaten the public sector, the private sector, and ultimately the American people’s security and privacy.” The federal government continues to lead the industry in setting standards with ongoing work and publications by CISA, NIST, the U.S. Department of Defense, and others. These include a multi-vendor integration and architecture initiative led by NIST’s National Cybersecurity Center of Excellence, which Appgate was one of the participating vendors.

With an increasingly threatening landscape, to ensure security every organization and government in the world will need to update their traditional cybersecurity tools with a solution that is able to stand up to today’s threats. We believe that the Zero Trust framework has established itself as that solution and represents the next generation cybersecurity solution.

Our Solutions

We provide identity-centric and context-aware Zero Trust access solutions that ensure security and compliance across all environments, including on-premises, hybrid, and cloud-native. We also offer a digital threat protection and risk-based authentication and comprehensive risk management tool designed to identify and eliminate attacks before they occur, across social media, phishing attacks, bogus websites, and malicious mobile apps. The following combination of software and services are increasingly the central pillar of our customers’ cybersecurity architecture:

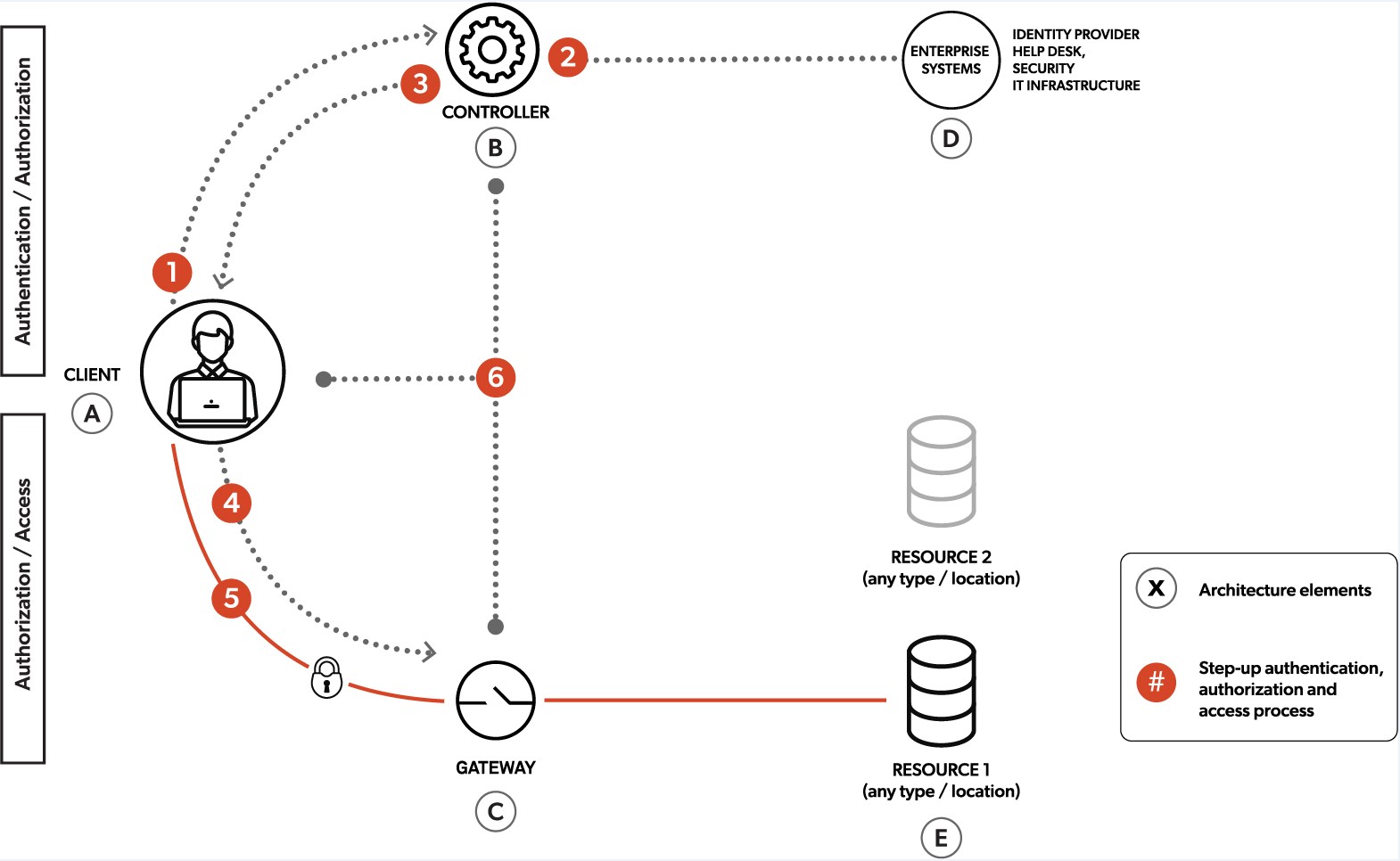

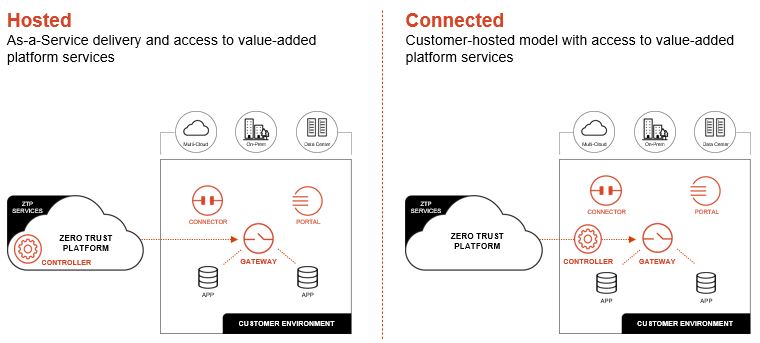

•Appgate Software-Defined Perimeter (“SDP”). Appgate SDP, leveraging unified access policies that are simple to understand and write, is designed to ensure trusted network access for users across all devices and IT environments, whether on-premises, hybrid or cloud-based. Unlike legacy solutions where users manually and constantly switch VPN tunnels to establish secure connections, SDP users connect once and gain access only to authorized applications across a heterogeneous and distributed IT landscape. SDP defends our customers’ networks from wrongful access and continuously monitors for changes in user behavior once a connection is made. In order to prevent lateral movement from unauthorized users, the network remains invisible, exposing no ports, until a user is authenticated and connected. Once authenticated and on the network, SDP employs the principles of “least-privileged access,” granting limited access, only to the extent required. Access is conditional and based on multiple factors, and if SDP detects changes during the online session, the user can be denied access in part or in full. The most common Appgate SDP use cases include VPN replacement for remote access, securing cloud access, supporting cloud migrations, securely providing third-party access, secure Development and Operations (“DevOps”), and integrating Merger & Acquisition (“M&A”) assets into a secure network environment. Appgate SDP supports customer choice of deployment models, including hosting it within Appgate’s cloud-native Zero Trust Platform, having customers deploy in a self-hosted model, or hybrid.

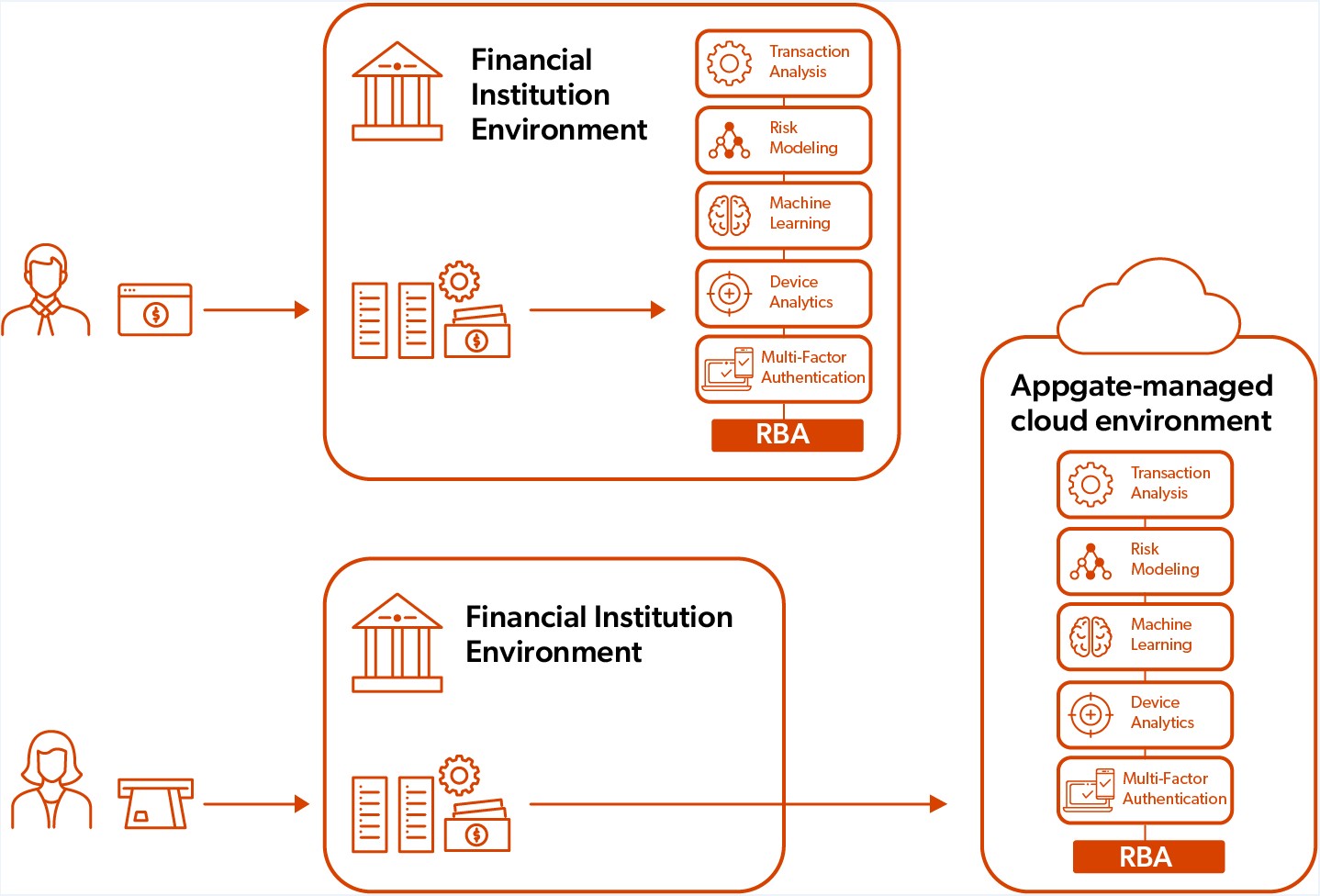

•Risk-Based Authentication (“RBA”). RBA offers an intelligent and contextually aware approach to authenticating users and approving transactions without friction. Legacy password-only solutions are a weak authentication measure that unintentionally creates friction for enterprise customers. By contrast, our RBA approach uses real-time behavioral risk assessments, context-based authentication and machine learning, all designed to protect individuals against targeted attacks. Transactions and user behavior are continuously monitored to qualify the risk on any channel. Should the RBA solution determine the person attempting to access their account is illegitimate, transactions can be blocked or challenged in real-time, preventing account takeover.

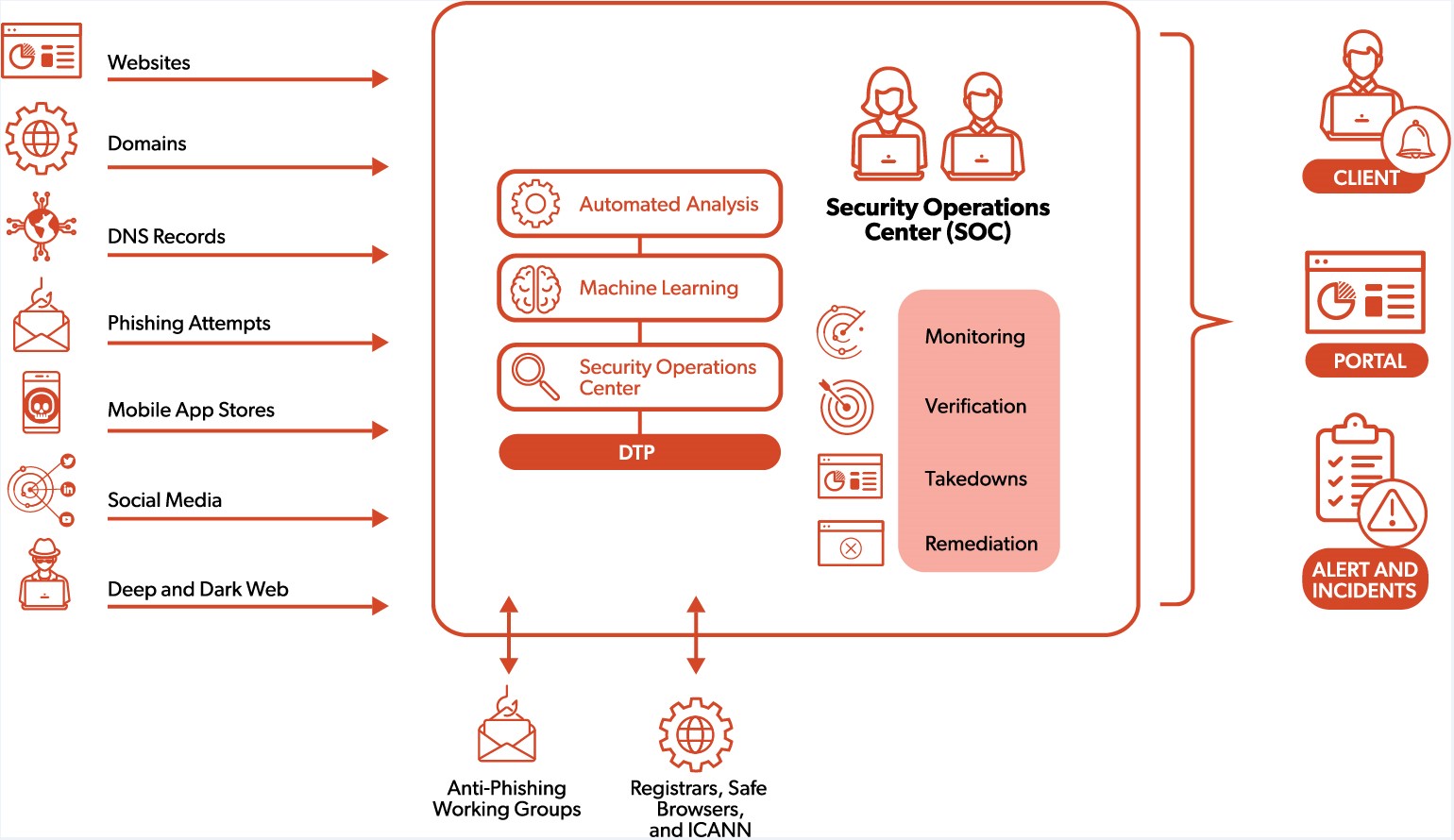

•Digital Threat Protection (“DTP”). Our DTP solution is designed to combat external threats targeting consumers across social, mobile and the dark web, including phishing links, malicious mobile apps, and fraudulent websites. DTP continuously monitors activity, provides early-stage warnings, orchestrates takedowns and can proactively stop attacks before damage is done, often before intended victims are aware.

•Threat Advisory Services. Our Threat Advisory Services are designed to proactively identify vulnerabilities and validate defenses using a combination of advanced penetration testing, adversary simulation and other customized services. We use highly sophisticated, bespoke processes based on the individual needs of our customers to simulate nation-state-level and other complex attacks. These engagements help organizations test and validate the security investments they’ve made and act as an opportunity to implement our software solutions based on remediation recommendations as we help our customers accelerate their Zero Trust journey. Threat Advisory Services are an important tool in our pursuit to future proof our customers’ defenses against malicious activity, as they allow us to gain real-time information from our services engagements to stay up to date on evolving cybersecurity threats. We leverage this data to inform our software technology roadmap, helping us effectively address our customers’ expanding security needs.

Key Benefits

Our platform based on Zero Trust principles is scalable, integrates with disparate security and non-security solutions and operates in any complex IT environment. Our platform empowers organizations to undertake their digital transformation

journey and enables development and operations teams to collaborate, quickly build and improve applications and drive business performance. Key benefits of our solutions include:

•Enhanced network security based on Zero Trust. As a pioneer, leader, and one of the earliest proponents of Zero Trust, we have built and honed a pure-play platform based on Zero Trust principles to facilitate secure interactions for organizations, users, and their devices. Our solutions use the principles of Zero Trust to strengthen network security, making it harder for adversaries to attack a network. Additionally, if a breach occurs, an attacker’s lateral movement is restricted so the attacker can be identified and swiftly contained, potentially limiting overall damage and exposure.

•Effective across all environments. Organizations require infrastructure to support on-premises, hybrid, cloud, IoT, BYOD, and other disparate platforms. Our identity-centric and context-aware solution dynamically adjusts to changes in user behavior across all interconnected environments. Many organizations have a patchwork of products that are often poorly integrated, creating additional complexity, security gaps, and administrative burden, creating an opportunity for our solutions. We believe we were among the first to identify the need for and deliver an enterprise class, software-based, unifying solution that dynamically works across all environments to become an organization’s executive team’s cyber-defense partner.

•Greater flexibility for customers and their users. Our solutions offer fast, secure, direct connections from any location, enabling increasingly popular remote workforce models. Unlike perimeter-based approaches, our SDP platform uses a dynamic identity-centric policy model to connect users from any device in any location. While remote workforce models typically expand security risk, our security architecture is designed to ensure that increased workforce mobility does not create incremental vulnerable access points. Appgate SDP can be deployed as-a-Service (hosted in the Appgate cloud environment) or deployed completely within customer environments.

•Strong integration capabilities. Our solutions can be deployed alongside existing security systems and across the entire IT environment. We utilize what we believe is the broadest set of APIs for Zero Trust in the industry to enable our products to coordinate and communicate with other IT systems and improve the interoperability with existing security infrastructure. Through integration with our Zero Trust security solution, customers have the potential to extend both the reach and value of their existing security and non-security tools. We believe this value proposition enables a faster purchasing decision and differs from “next generation” security solutions that require an overhaul of a customer’s existing security system architecture.

•Lower total cost of ownership. Adoption of our user-friendly software solutions frequently leads to improved operational efficiency for organizations. A survey of our customers by independent analyst firm Nemertes concluded that all respondents reported improvements in one or more key operational metrics, including average user provisioning time, average number of staff required for user provisioning, average login time, number of security incidents and trouble tickets and number of concurrent users, after adopting our solutions.

•Simplified and more effective security model. We allow system administrators to create a single set of access policies that can be used uniformly across multiple disparate environments, increasing ease of use, operational efficiency, and security. This is in sharp contrast to not only traditionally siloed products, such as VPNs and NACs, but also many other ZTNA providers, who utilize static versus dynamic security rules, or who cannot secure access for on-premises users.

•Seamless end user experience. We provide automatic, dynamic access without having to frequently engage with the end user or disrupt workflow processes. Users are authenticated the same way regardless of where they are located or what device they are using. This approach differs from, and can be a replacement for, inflexible tools like VPNs and static multi-factor authentication systems, which often require users to re-authenticate themselves routinely, frustrating users.

•Complex fraud prevention. We offer consumer-facing organizations a comprehensive set of solutions based on Zero Trust principles to prevent fraud. Powered by machine learning and behavioral analytics designed to identify and prevent fraudulent activities, we assess risk based on user behavior to authenticate connections. Our proprietary technology is focused on detecting and deactivating targeted external threats which utilize phishing links, malicious mobile apps, or fraudulent websites. We continuously analyze and monitor an array of digital channels to identify threats, and execute site take-downs, often before intended victims are aware. Finally, we

provide rich insights on potential victims, so organizations can be better prepared to stop future complex fraud campaigns.

Competitive Strengths

Our competitive strengths include:

•Pioneering Zero Trust solutions delivering next generation IT security. Our Zero Trust solutions are purpose-built to meet the needs of modern organizations, whose IT infrastructures are transforming with the adoption of containerized, cloud, SaaS, mobile, IoT, and remote work environments. Our solutions are designed from the ground up on Zero Trust principles to function and integrate across all IT environments, which has the potential to make them more effective at securing IT infrastructures as compared to repurposed legacy solutions. Our solutions allow system administrators to create a single set of policies that can be applied uniformly across multiple environments, reducing the risk of errors. We believe our primary focus on Zero Trust has enabled us to build an industry leading solution.

•Industry leading reputation. Our SDP product was named a “Leader” in the Forrester New Wave™ for Zero Trust Network Access (Q3 2021) and, as of March 10, 2023, received 4.6 out of 5 stars from customer reviews on Gartner Peer Insights. Appgate was also recognized by Forrester in their “New Tech: Zero Trust Network Access, 2021” report, as a mature or “Late-Stage” vendor, indicating significant company tenure, number of customers, employees, and funding level as compared to our peers. Our RBA solution was named a “Leader” in Quadrant Solutions’ SPARK Matrix™: Risk Based Authentication, 2022 report. We believe these high-profile recognitions received from trusted industry experts have elevated our reputation with existing and prospective customers.

•Highly scalable ‘land and expand’ go-to-market (“GTM”) strategy driving C-Suite engagement. We leverage a ‘land and expand’ GTM strategy that can scale rapidly as we demonstrate value to customers and achieve broader deployment across their infrastructure. We deploy an integrated technical sales approach complemented by channel partners, such as Lumen, Optiv, Presidio, Guidepoint Security, DXC, TechMatrix, SageNet, Q2, Alkami, Carahsoft, Ingram, GBM, CLM and Kite, which helps us meet the needs of our expanding customer base. This GTM approach is turbocharged by our battle-tested sales engineering team, which can help demonstrate the value of our solutions to stakeholders outside of the IT organization. We believe that cybersecurity has become a key business issue for executives, not just an area of concern for IT professionals; our ability to elevate conversations to a strategic level and secure buy-in from all stakeholders is a critical differentiator, unlocking broader deployment of our solutions.

•Strong customer focus. We are a trusted, long-term, strategic partner to our customers. In a Nemertes survey of our customers, 100% of respondents said Appgate accelerated their digital transformation, and of those implementing Appgate SDP, our importance to their strategy ranked 9.5 out of 10. These strong customer satisfaction metrics stem from our customer success team’s close collaboration with clients throughout their journey as a customer, communicating frequently with them through quarterly business reviews, supporting them as novel issues and use cases arise, and constantly seeking feedback to drive improvement in our solutions. We also continue to hold regular Customer Advisory Board meetings, which provide an open dialogue with customers to ensure that we prioritize, understand, and adapt to their changing needs. Our current customer base includes at least one of the largest companies by revenue in each of the defense contracting, telecommunications, systems integrator and oil and gas sectors, validating our customer-focused strategy.

•Seamless API-based integration. Our solutions offer feature-rich, easy-to-use APIs that allow for integration with existing solutions, which enables our customers to drive more value from their in-place solutions. Our APIs facilitate quick deployment alongside existing security solutions, from which threat data and context can be extracted, and are used to enrich our risk scoring and authentication decisions. We continue to partner with other cybersecurity vendors, such as Crowdstrike and others, to deepen the abilities of our API integrations. In addition, Appgate recently introduced new no-code integrations within our cloud-native security services, running in the Appgate Zero Trust Platform. This further improves our integration capabilities, and makes it easier for customers to benefit from it.

•Deep management strength with extensive cybersecurity experience. Our seasoned executives were among the earliest pioneers in Zero Trust security. Our senior management team has extensive expertise in the cybersecurity

industry with deep knowledge of the markets in which we operate. With an average of over 20 years of experience in the enterprise technology and cybersecurity space, our highly accomplished management team demonstrate a historical track record of success and are devoted to the continued growth and success of our business.

Our Opportunity

As organizations reshape their IT infrastructure around hybrid, multi-cloud, SaaS, mobility, IoT, BYOD, containerized workloads, and with remote working environments and cyber threats rising rapidly, the need for a new security model is increasingly mission-critical for many enterprises. Zero Trust security is emerging as the leading next generation security model and we believe we are a pioneer in this transforming industry and are well-positioned to capitalize on the market opportunity.

•Hybrid, multi-cloud, and on-premises network security. Gartner estimates this aggregate market was approximately $39 billion in 2021, expected to grow at a 14% CAGR to approximately $57 billion by 2024. According to Cisco’s May 2022 Global Hybrid Cloud Trends Report, 82% of IT leaders say that they have adopted the hybrid cloud. Our SDP platform is designed to ensure trusted access for all corporate users across all environments.

•VPN replacement. Gartner predicts that at least 70% of new remote access deployments will be served predominantly by ZTNA as opposed to VPN services by 2025, up from less than 10% at the end of 2021, and that 60% of enterprises will phase out their remote access VPN in favor of ZTNA by 2023. Our SDP platform offers secure VPN replacement across all environments including hybrid, multi-cloud, and on-premises.

•Secure Access Service Edge (“SASE”). SASE refers to integrated security and network solutions that secure IT environments. According to Gartner, the global SASE market is projected to grow at a CAGR of 36% reaching almost $15 billion by 2025. We believe that ZTNA is the most critical element of SASE given its role in regulating network access, and our SDP platform is a recognized leader in ZTNA.

•Fraud Detection and Prevention (“FDP”). Organizations and individuals face a growing set of active and targeted phishing campaigns, as well as increased use of malicious websites and mobile apps for criminal purposes. The growth in these threats is underpinned by continued expansion of online banking, e-commerce, and Peer-to-Peer (“P2P”) payment applications. According to Fortune Business Insights, the FDP market was estimated at approximately $25.7 billion in 2021 and is projected to reach approximately $129.2 billion by 2029, representing a 22.8% CAGR. Ensuring that their customers aren’t deceived by fraudulent websites, phishing campaigns, or mobile apps is critical to businesses’ reputations, and our RBA and DTP solutions are designed to address these threats and we believe are critical tools in the FDP ecosystem. Illustrating the imminent need for fraud prevention, the Federal Trade Commission reported that Americans lost over $5.8 billion to fraud in 2021, an increase of over 70% from 2020.

We believe we are well-positioned to capitalize on the market opportunity to displace legacy network security solutions, which are ill-equipped to effectively secure cloud or hybrid IT environments, and the use of which increases entry points for adversaries and the risk of network breaches.

Growth Strategies

Key elements of our growth strategy include:

•Continue to grow customer base. We believe our solutions are well positioned to serve not only large, security-conscious organizations with complex, hybrid IT environments, but also medium and small sized customers. We believe scaling our sales team and increasing our investment in channels and strategic partners will fuel our customer base growth.

•Increase adoption within our existing customers. We utilize a ‘land and expand’ strategy through which we expand existing customer accounts by adding new use cases or more users, including third-party users and contractors. We expect many of our existing SDP customers to use our network of other software and services, driving growth.

•Continue to innovate and enhance our offerings. We plan to continue to expand our Zero Trust platform and capabilities to develop new products and add new modules in existing offerings to address additional use cases. As a pioneer in Zero Trust access solutions and cybersecurity defense, we are continuing to invest in the platform, and have launched new services, such as our cloud-native Zero Trust platform, announced in November 2022. We invested approximately 31% of our revenue in research and development during the year ended December 31, 2022 and maintain a robust product and technology roadmap. Our roadmap incorporates customer feedback which gives us confidence that we will be able to monetize our development efforts as we seek to offer highly scalable, flexible, and user-friendly products to address a variety of high-impact use cases.

•Grow our global footprint. As of December 31, 2022, we had customers in approximately 70 countries, reflecting the importance of our global footprint and our success building an international presence. For the year ended December 31, 2022, international sales represented approximately 49% of our revenue. We believe global demand for our offerings will continue to increase as international organizations further embrace Zero Trust access solutions in response to evolving cybersecurity threats and sophisticated adversaries. While we expect our international markets to continue to grow, we anticipate the growth in North America to outpace that of international markets.