1

BB&T Capital Markets

Investor Conference

August 10, 2011

Exhibit 99.1 |

2

Non-GAAP Financial Measures

Non-GAAP Financial Measures

The Company presents adjusted income (loss) from operations, adjusted operating margin,

adjusted EBITDA, adjusted EBITDA margin, adjusted net income (loss), adjusted

net income (loss) per share, free cash flow and net

debt as non-GAAP measures. Adjusted income (loss) from operations represents

income (loss) from operations excluding restructuring. This amount divided

by net sales is adjusted operating margin. Adjusted EBITDA represents

income (loss) from operations excluding restructuring, depreciation and amortization. This amount

divided by net sales is adjusted EBITDA margin. The Company presents adjusted

income (loss) from operations, adjusted operating margin, adjusted EBITDA and

adjusted EBITDA margin because these are measures management believes are

frequently used by securities analysts, investors and interested parties in the

evaluation of financial performance. Adjusted net income (loss)

and adjusted net income (loss) per share

exclude restructuring, certain costs from settled interest rate swap contracts, the

income tax effects of these excluded items and a tax adjustment for the

repatriation of earnings. These items are excluded because they are not

considered indicative of recurring operations. Free cash flow represents cash flow from operating activities

less capital expenditures. It is presented as a measurement of cash flow because

it is commonly used by the investment community. Net debt represents total

debt less cash and cash equivalents. Net debt is commonly used by the

investment community as a measure of indebtedness. These non-GAAP measures have limitations as

analytical tools, and securities analysts, investors and interested parties should not

consider any of these non- GAAP measures in isolation or as a substitute for

analysis of the Company's results as reported under accounting principles

generally accepted in the United States ("GAAP"). A

reconciliation of non-GAAP to GAAP results is included as an attachment to this presentation and has been

posted online at www.muellerwaterproducts.com.

|

3

Safe Harbor Statement

Safe Harbor Statement

This presentation contains certain statements that may be deemed

“forward-looking statements”

within the

meaning of the Private Securities Litigation Reform Act of 1995.

All statements that address activities, events or

developments that we intend, expect, plan, project, believe or anticipate will or may

occur in the future are forward-looking statements. Examples of

forward-looking statements include, but are not limited to, statements we

make regarding spending trends by municipalities on water infrastructure and the market reception of Mueller

Systems’

and Echologics’

products and services, and the impact of these factors on our businesses.

Forward- looking statements are based on certain assumptions and assessments

made by us in light of our experience and perception of historical trends,

current conditions and expected future developments. Actual results and

the timing of events may differ materially from those contemplated by the

forward-looking statements due to a number of factors, including regional,

national or global political, economic, business, competitive, market and

regulatory conditions and the following:

•

the spending level for water and wastewater infrastructure;

•

the demand level of manufacturing and construction activity;

•

our ability to service our debt obligations; and

•

the other factors that are described in the section entitled

“RISK FACTORS”

in Item 1A of our most recently

filed Annual Report on Form 10-K and in Part I, Item 1A of our quarterly report on

Form 10-Q for the quarter ended March

31, 2011. Undue reliance should not be placed on any forward-looking

statements. We do not have any intention or obligation to update

forward-looking statements, except as required by law. |

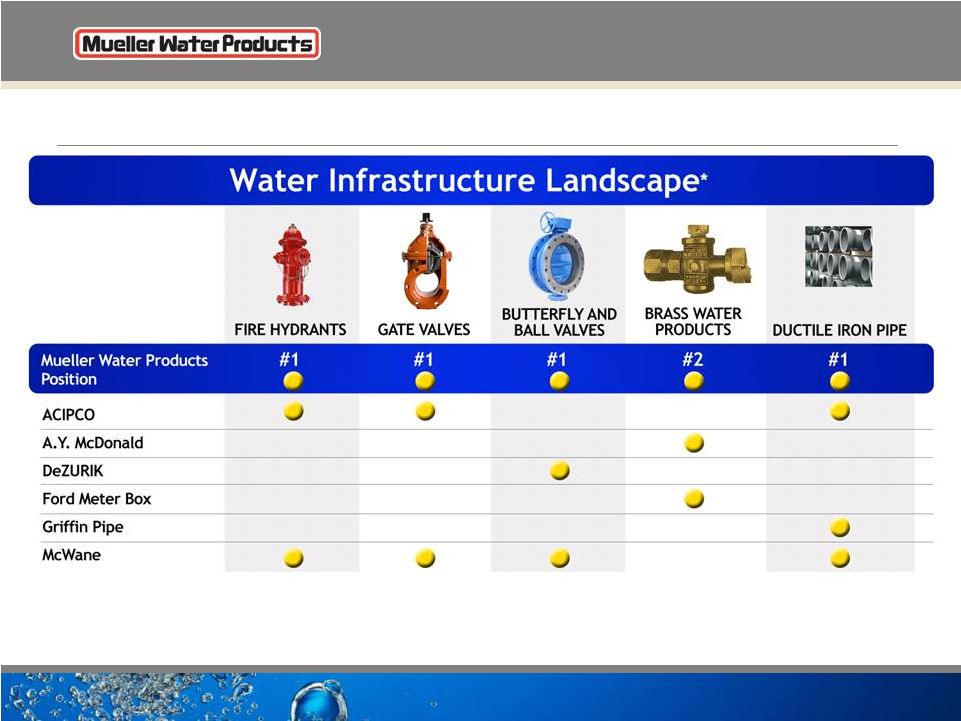

4

Leading North American provider of water

infrastructure and flow control products

and services

Investment Highlights

Leading brands in water infrastructure

Leveraging brands to expand intelligent water

technology offering for diagnostic and data

management

Low-cost manufacturing processes

Increasing investment needed in water

infrastructure industry

One of the largest installed bases in the U.S. |

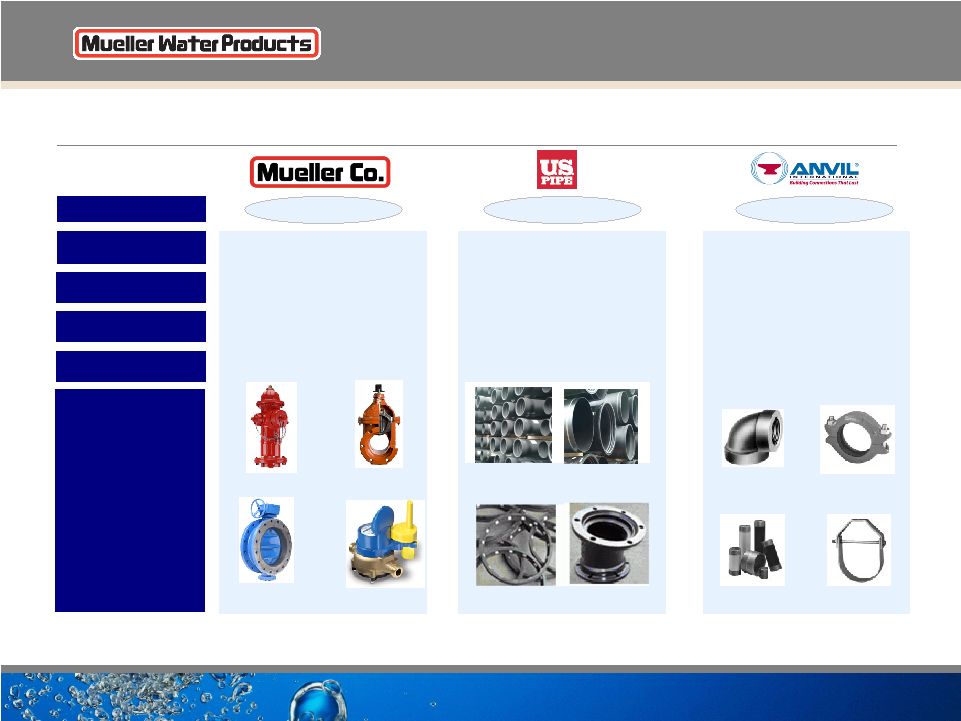

5

Our Business

•

$1.3B LTM net sales (as of June 30, 2011)

•

Portfolio includes:

•

Fire hydrants

•

Valves

•

Pipe fittings

•

Ductile iron pipe

•

Metering systems

•

Leak detection

•

Specified in 100 largest U.S. metropolitan markets

(1)

•

More than 75% of FY2010 net sales from products with

#1 or #2 position

(1)

Valves or hydrants

(2)

Based on management estimates

* Residential construction systems driven primarily by new community development

FY2010 Primary End Markets

(2)

Net Sales $1.3B

The largest publicly traded water infrastructure company in the United States

|

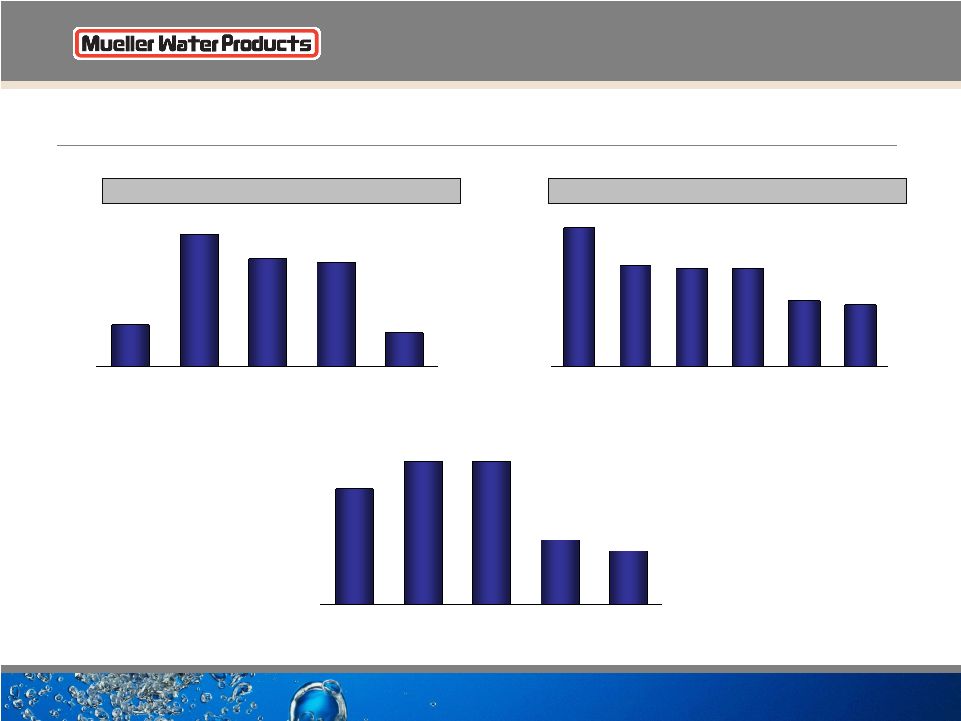

6

Broad Product Portfolio

$608

$69

$48

$117

SEGMENT NET SALES

PRODUCT

PORTFOLIO

ADJUSTED OPERATING

INCOME (LOSS)

(1)

$352

($46)

$19

($27)

$352

$31

$15

$45

Iron Gate

Valves

Butterfly, Ball

and Plug Valves

Fittings &

Couplings

Cast Iron

Fittings

Hangers &

Supports

Metering

Systems

Pipe Nipples

Hydrants

DEPRECIATION AND

AMORTIZATION

(2)

Est. 1857

Est. 1899

Est. 1999 (1850)

HISTORICAL ROOTS

ADJUSTED EBITDA

(1) (2)

Note: All statistics are actuals for LTM ended June 30, 2011

(1)

Segment operating income (loss) excludes corporate expenses of $30mm. Mueller Co.

excludes $1.2 mm of restructuring. U.S. Pipe excludes $4.2 mm of restructuring. Anvil excludes $1.6 mm of restructuring.

(2)

Segment depreciation and amortization excludes corporate depreciation of $0.6mm.

($ in millions)

Ductile Iron

Pipe

Joint Restraints

Restrained Pipe

Joint

Joint Fittings |

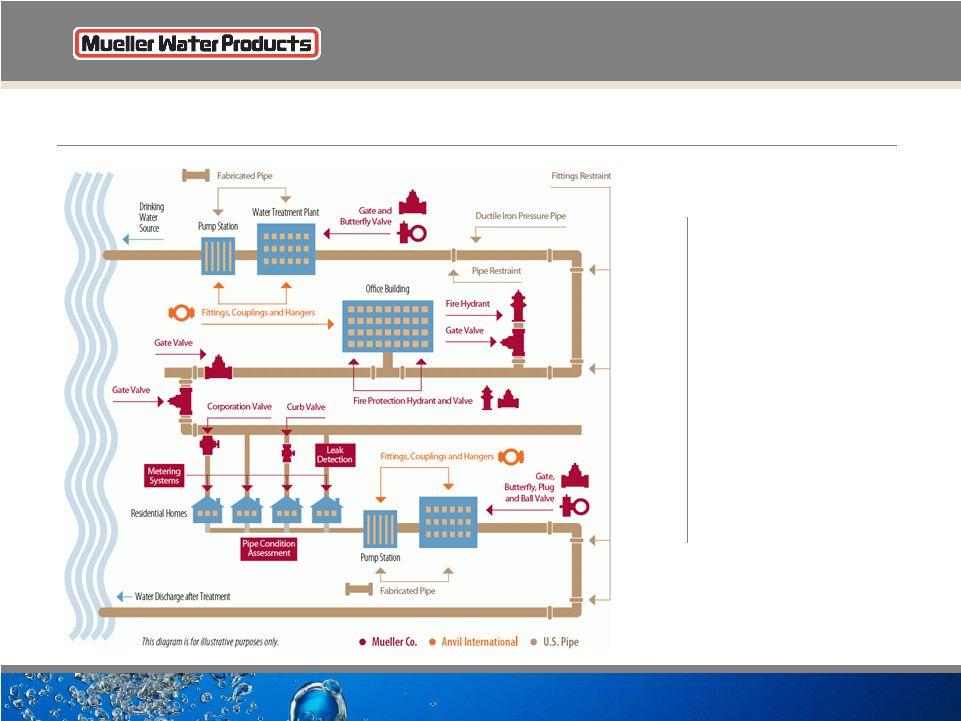

7

Complete Water Transmission Solutions

Mueller Water Products

manufactures and

markets products and

services that are used in

the transmission,

distribution and

monitoring of safe, clean

drinking water and in

water treatment

facilities. |

*

Company estimates based on internal analysis and information from trade associations and our distributor networks, where available.

8 |

Strategy

And Objectives Maintain leadership positions with

customers and end users

Broaden breadth and depth of

products and services

Continue to enhance operational

and organizational excellence

Expand internationally

9

Capitalize on the large,

attractive and growing

water infrastructure

markets worldwide |

Strategic Initiatives

Maintain leadership positions with customers and end users

Continue to enhance operational and organizational excellence

Broaden breadth and depth of products and services

Expand internationally

•

Leveraging the Mueller brand

•

Developing value-added products

and services

•

Strengthened balance sheet

•

Implemented Lean Six Sigma

•

Introduced first wireless mesh

agreement for water industry

•

Enhanced AMI system with

remote disconnect meter and customer portal

•

Export orders

•

Evaluating opportunities

•

Leveraging distribution network

•

Improving customer service levels

•

Consolidated plants

•

Automated DIP facility

•

Acquired leak detection and pipe

condition assessment services company

10 |

11

Our End Markets |

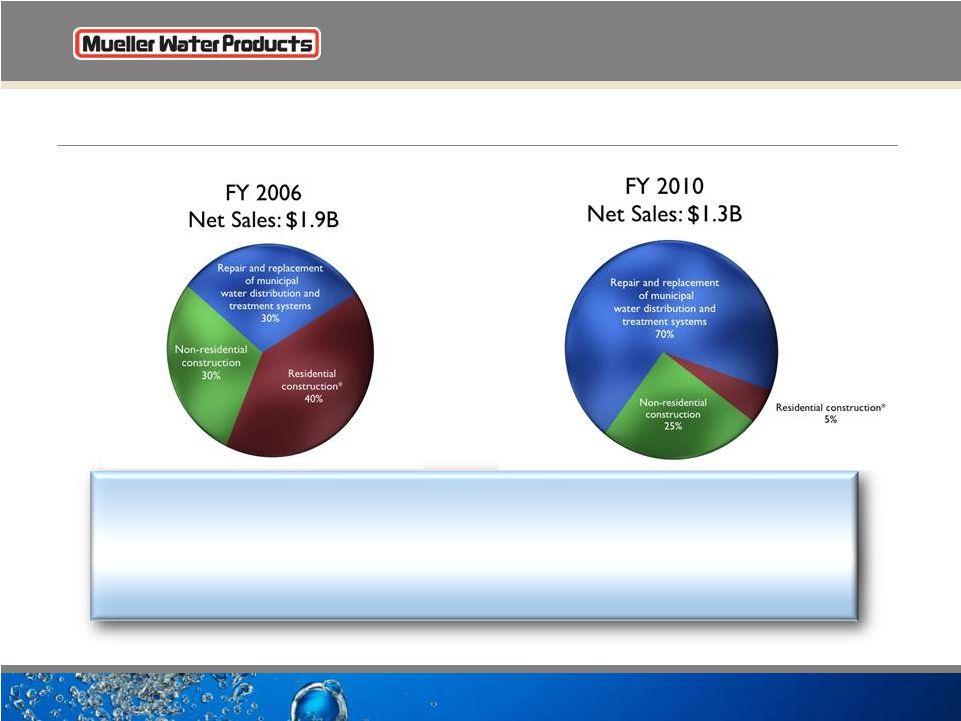

Primary

End Markets: 2006-2010 Source: Management estimates

*

Residential construction is driven primarily by new community development

Since 2006, our exposure to the residential construction

market has declined from roughly 40% to 5%.

12 |

Historical Housing Starts

13 |

Non-Residential Construction

Architecture Billings Index Trends

Source: IHS Global Insight

Data as of July 20, 2011

Non-Residential Construction Actual / Forecast

Data as of July 21, 2011

We continue to see signs that the non-residential market has stabilized

14 |

15

Significant Market

Opportunities |

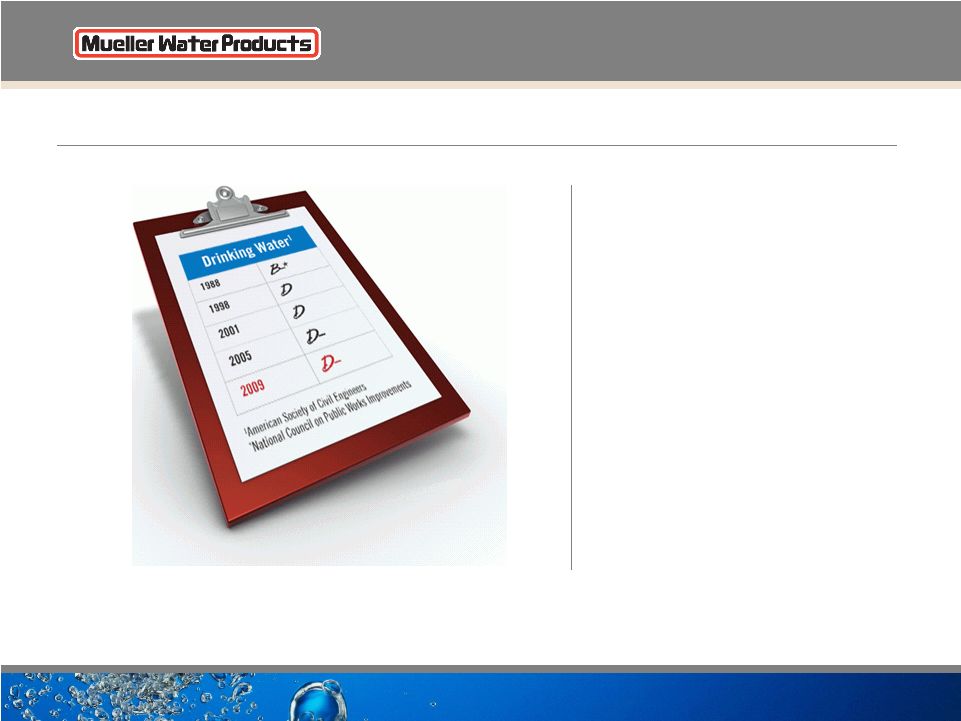

16

Opportunity: Aging Water Infrastructure

“America’s drinking water systems

face an annual shortfall of at

least $11 billion

to replace aging

facilities that are near the end of

their useful lives and to comply

with existing and future federal

water regulations. This does not

account for growth in the demand

for drinking water over the next

20 years.”

2009 Report Card for America’s Infrastructure

American Society of Civil Engineers (ASCE) |

17

The Market Opportunity Is Significant And Growing

Repair and Replacement Market

•

Aging water pipes need to be repaired/ replaced

•

Valves and hydrants typically replaced at same time as pipes

•

More than 36 states project water shortages between now and

2013

(1)

•

Up

to

15%

-

30%

of

treated

potable

water

lost

in

leaky

pipes

(2)

•

Emphasis on improving operational efficiencies

Funding and Spending

•

90% funded at local level

(3)

•

29% of water systems charge less than cost

(4)

•

63% of American voters willing to pay more to upgrade water

system

(5)

Source:

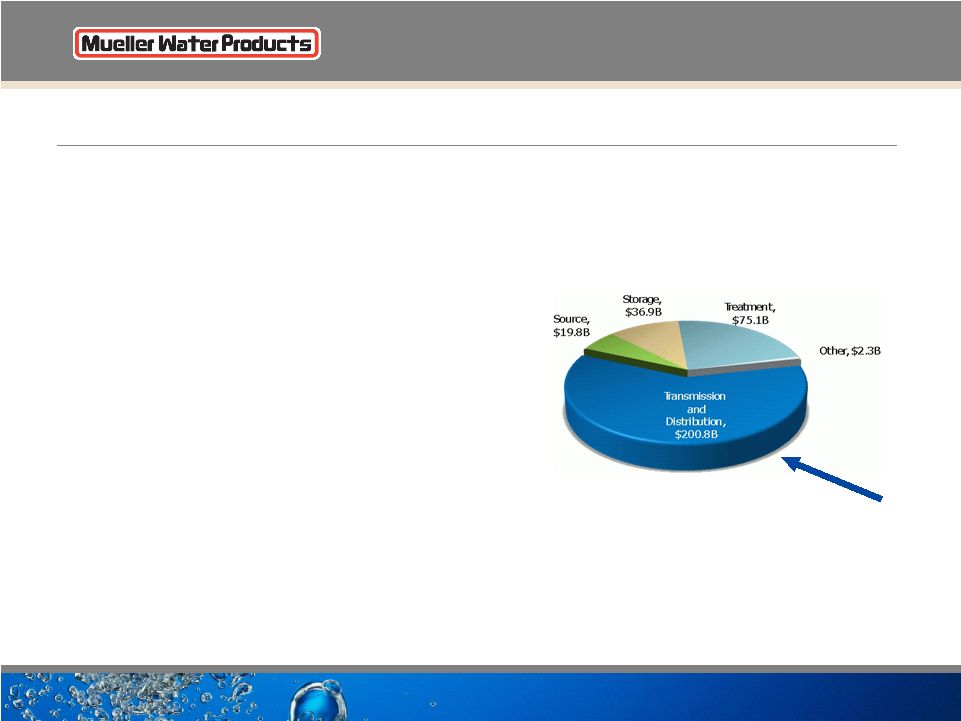

(1) EPA: WaterSense Statistics and Facts

(2) Global Water Intelligence Water Technology Markets 2010

(3) EPA Clean Water and Drinking Water Infrastructure Gap Analysis

(4) Government Accountability Office 2004 report on water infrastructure

(5) Americans on the U.S. Water Crisis, ITT

(6) EPA 2007 Drinking Water Needs Survey and Assessment

Future Drinking Water

Infrastructure Expenditure Needs

(6)

Area in which

Mueller Water

Products operates

20-YR Need for

Water Infrastructure = $335B |

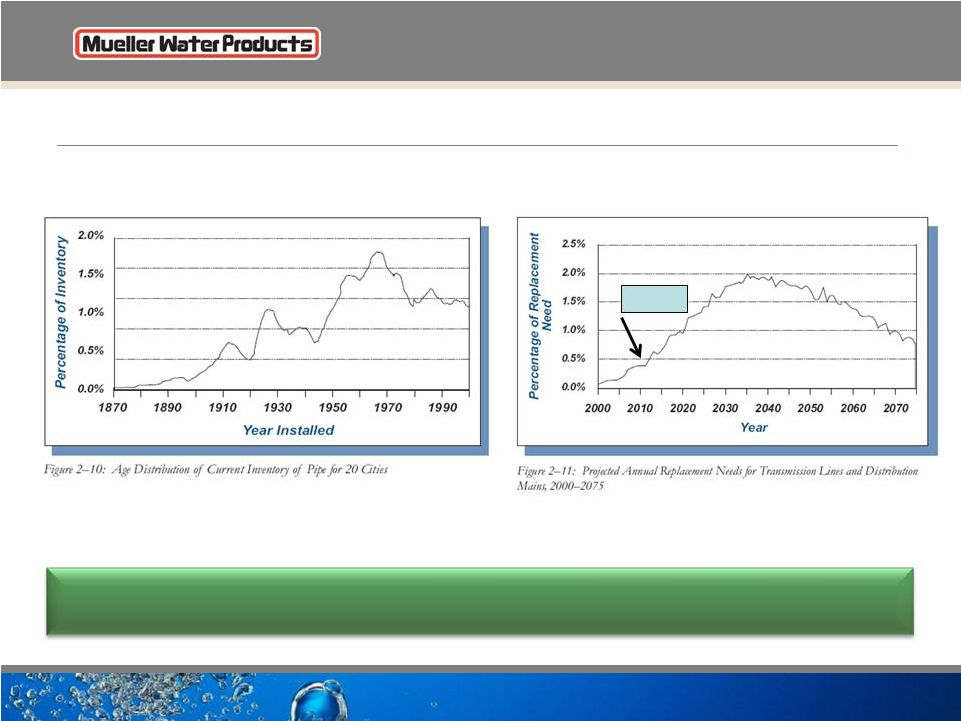

Aging

Water Infrastructure

Average life of 100 year and 75 year old pipe is converging, contributing

to accelerating need for pipe replacement.

(1) The EPA Clean Water and Drinking Water Infrastructure Gap Analysis 2002

Accelerating

Need

18 |

19

Increasing Federal Awareness of Funding Needs

•

At least 40 cities under consent decrees

—

Atlanta $4.0B

—

Washington, D.C. $2.6B

—

Baltimore City and county $1.7B

—

Kansas City $2.5B

—

Cincinnati $1.5B

•

1974/1996 Safe Drinking Water Act

•

2011 federal budget

—

$965 million for Drinking Water

State Revolving Funding (SRF)

—

Decline of $422 million from FY2010

Stronger EPA regulations should lead to increased investment

“New Jersey can maintain

a viable economy with a

sound environment only if

it ensures that its water

supply, wastewater and

stormwater infrastructure

is effectively maintained in

a manner that produces

the lowest life-cycle cost.”

The Clean Water Council of

New

Jersey

-

October

2010 |

20

Funding Water Infrastructure Repair

Sources:

(1) Bureau of Labor Statistics

(2) AWWA State of the Industry Report 2010

(3) Black & Veatch 2009/2010 50 Largest Cities Water/Wastewater Rate Survey for

residential 7,500 gallons Sources of Funding

Water Infrastructure

Repair

(2)

Historical Water

Rates Compared to

Other Utilities

(1)

Long-term trends in consumer prices (CPI) for utilities (1913-2010)

Other

15%

Bonds

9%

Loans

16%

Operational

Savings

47%

Rate

Increases

10%

Grants

3%

From 2007-2009, average annual

residential water rates increased

about 10%

(3) |

21

Opportunities: Smart Metering and Pipe Condition Assessment

Smart Metering

•

Advanced

Metering

Infrastructure

20%

of

market

-

$200 million today*

•

Forecasted to grow an average of 20% per year

through 2015*

•

Transition from one-way to two-way AMI Systems

Pipe Condition Assessment

•

Constrained municipal budgets

•

Greater attention on condition assessment

•

Help prioritize capital spending

•

Two-way mesh network

•

Enhanced AMI System

•

Mi.Hydrant

•

Mi.Data

•

420 Remote Disconnect Meter

•

Pioneered acoustic, non-invasive

leak detection and pipe condition

assessment

•

Proven technology

* Proprietary publishing for AWWA; Canada/Mex. Scott Report for AMI/AMR Dec.2010;

Management estimates |

22

Actions & Business

Results |

23

Management Actions/Initiatives

Objectives

Actions

Reduce costs and improve

operating leverage

•

Closed six plants since FY2006

•

Sold two non-core assets of Anvil

•

Reduced headcount by about 23% from September 30, 2008 to June 30,

2011 from approximately 6,300 to approximately 4,800

•

Took actions to lower labor costs

•

Implemented Lean Six Sigma and other manufacturing improvements (continuous

improvement)

•

Invested in new automated ductile iron pipe operation to lower costs

•

Consolidated distribution centers and smaller manufacturing facilities at Anvil

Manage working capital and

capital expenditures to generate

free cash flow

•

Capital spending decreased from FY2007/FY2008 levels

•

FY2009 capital spending of $39.7 million; FY2010 capital spending of $32.8

million •

Reduced inventory by $116.6 million in FY2009; $74.4 million reduction in FY2010

•

Reduced debt by $403 million from September 30, 2008 through June 30, 2011

•

Inventory

turns

have

improved

close

to

half

a

turn

at

the

end

of

June

2011

from

June 2010

Leverage Mueller brands to

pursue strategic growth

opportunities

•

Acquired and invested in AMI technology

•

Acquired leak detection and pipe condition assessment business

•

Established first AMI wireless mesh agreement for water industry

•

Entered into advanced metering agreement with Landis+Gyr for electric meters

|

24

$509

$536

$618

$664

$804

$756

$718

$547

$613

$492

$465

$551

$598

$595

$537

$546

$411

$378

$393

$387

$431

$485

$535

$556

$595

$470

$347

2002

2003

2004

2005

2006

2007

2008

2009

2010

2002

2003

2004

2005

2006

2007

2008

2009

2010

2002

2003

2004

2005

2006

2007

2008

2009

2010

NET SALES

ADJUSTED EBITDA

&

ADJ. EBITDA

MARGIN

($ in millions)

History of Strong Financial Performance

(see appendices for GAAP reconciliation)

(a)

(c)

(b)

$131

$139

$167

$190

$248

$207

$179

$101

$131

$44

$26

$42

$56

$57

$24

($34)

$48

$38

$47

$62

$73

$81

$94

$61

$38

25.7%

25.9%

27.1%

28.6%

30.8%

27.3%

24.9%

18.5%

21.3%

8.8%

3.3%

4.4%

7.0%

9.3%

10.7%

4.3%

(4.9%)

(9.0%)

12.3%

9.7%

10.8%

12.8%

13.6%

14.6%

15.8%

13.0%

11.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2002

2003

2004

2005

2006

2007

2008

2009

2010

2002

2003

2004

2005

2006

2007

2008

2009

2010

($20)

$16

c)

Excludes inventory step-up costs of $17.3 million in 2006; restructuring costs of

$4.0 million in 2009; goodwill impairment charges of $92.7 million in 2009; restructuring charges of $0.5 million in 2010

a)

Fiscal year end as of September 30th. Reflects inventory step-up costs of $53.1

million in 2006; restructuring charges of $2.0million in 2009; goodwill impairment charges of $818.7 million in 2009; restructuring charges of $0.1 million in 2010

b)

Financial results for 2002, 2003 and 2004 are calendar year while subsequent years are

fiscal years ending September 30th. Excludes $6.5 million of litigation settlement expenses in 2003; environmental-related insurance settlement benefits

of $1.9 million and $5.1 million in 2004 and 2005, respectively. U.S. Pipe

Chattanooga closing costs of $49.9 million in 2006; restructuring charges of $18.3 million in 2008 and goodwill impairment charges of $59.5 million and restructuring

charges of $41.6 million in 2009; restructuring charges of $12.5 million in

2010 |

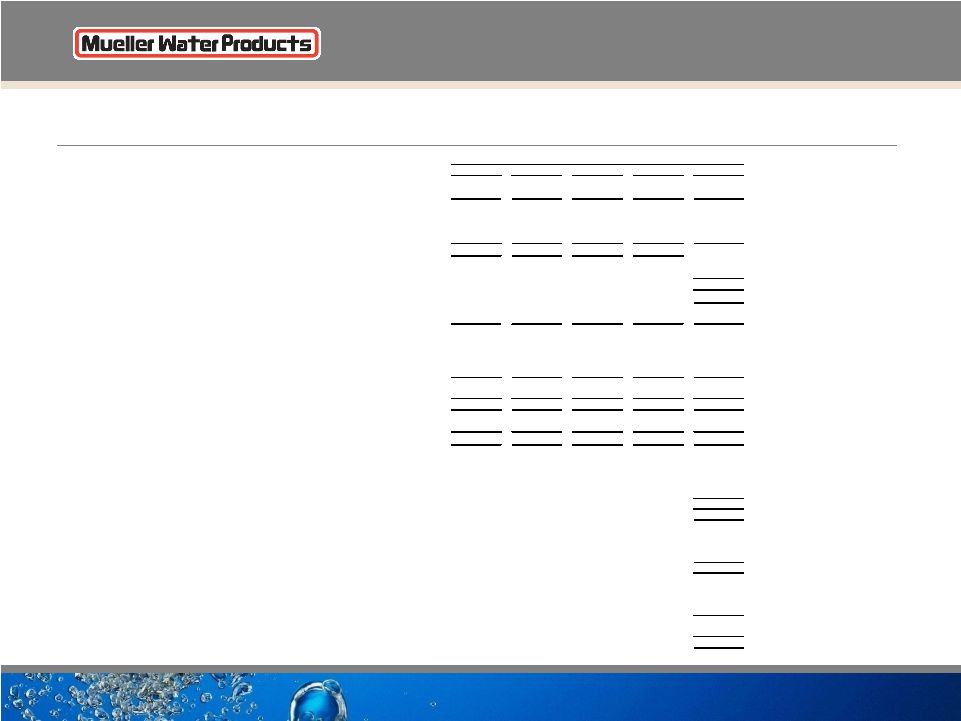

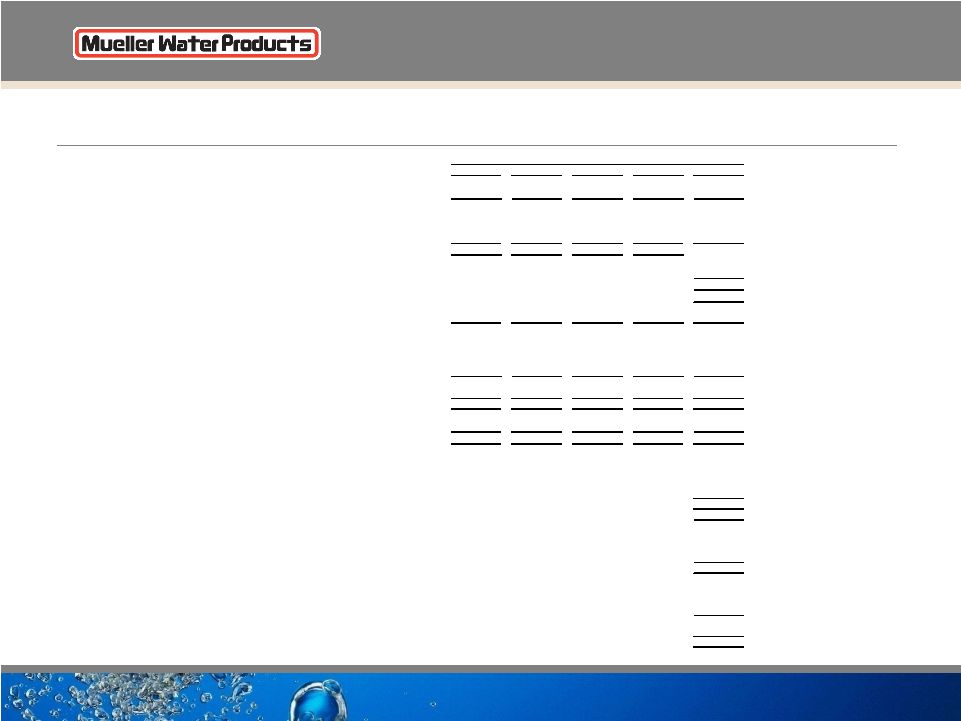

25

Consolidated Non-GAAP Results

•

Adj. operating income improved year-over-year, although not as much as

expected •

Higher sales pricing covered increased raw material costs in all

three businesses

•

U.S. Pipe operating performance improved both year-over-year and

sequentially •

Anvil’s performance was particularly strong with 15.7% increase in net

sales and more than doubling of

operating income

•

Market reception of newer water-technology businesses is encouraging. Mueller

Systems experienced double digit sales growth year-over-year. Bookings

were up in both Mueller Systems and Echologics. $ in millions (except per share

amounts) 2011

2010

Net sales

$366.7

$375.9

Adj. income from operations

$15.6

$13.4

Adj. operating margin

4.3%

3.6%

Adj. net income (loss) per share

$0.00

($0.01)

Adj. EBITDA

$35.9

$34.5

Adj. EBITDA margin

9.8%

9.2%

Third Quarter Fiscal

FY 3Q11 results exclude restructuring costs of $1.7 million, $1.0 million net of

tax; and interest rate swap costs of $2.1 million, $1.3 million net of tax. FY

3Q10 results exclude restructuring costs of $0.9 million, $0.5 million net of tax; and $2.2 million tax expense on the repatriation of Canadian earnings. |

26

Debt Structure

•

FY 2010 recapitalization provided a long-term

capital structure

•

Extended maturities with no significant required

principal payments before 2015

•

Locked in long-term capital at attractive rates

•

Preserved deleveraging capability

•

Expect greater operational flexibility

•

Eliminated financial maintenance covenants with

excess availability at the greater of $34 million or

12.5% of facility amount

•

More than $174 million of excess availability at

June 30, 2011

•

Reduced limitations on business operations

including acquisitions, investments, restricted

payments and divestitures

New

structure:

•$420 million 7.375% Senior Subordinated Notes due 2017

•$225 million 8.75

% Senior Unsecured Notes due 2020

•$275 million ABL Revolver Credit Facility due 2015

|

27

Key Financial Metrics

$37

$115

$94

$91

$30

$0

$20

$40

$60

$80

$100

$120

$140

FY2006

FY2007*

FY2008

FY2009**

FY2010***

Free Cash Flow

($ in millions)

$1,549

$1,127

$1,101

$1,096

$740

$692

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

Mar-2006

FY2006

FY2007*

FY2008

FY2009

FY2010

Total Debt

($ in millions)

$71

$88

$88

$40

$33

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

FY2006

FY2007

FY2008

FY2009

FY2010

Capital Expenditures

($ in millions)

* FY2007 results exclude $48.1 million of debt restructuring activities

** FY2009 results include $6.3 million of cash used to settle certain interest rate

swap contracts. *** FY2010 results include $18.3 million of cash used to

settle certain interest rate swap contracts. $73 million free cash flow average

over last five years Debt has declined $857 million from 2006

|

Why

Invest in MWA? Water industry

has fundamentally strong long-term dynamics

•

Driven by new and upgraded infrastructure

•

Limited number of suppliers to end markets

Strong

competitive

position

•

Leading brand positions with large installed base

•

Leading municipal specification positions

•

Comprehensive distribution network

•

Low-cost manufacturing operations

Operating leverage

when volumes improve

•

Recovery of residential market

•

Increased municipal spending

•

Operating excellence initiatives

Leveraging

strengths

in

the

evolving

market

•

Expand smart metering

•

Expand diagnostic offerings (leak detection and pipe condition assessment)

•

Develop intelligent water technology solutions

•

Strategic acquisitions/partnerships

28 |

29

Supplemental Data |

30

Segment Results and Reconciliation of Non-GAAP to GAAP

Performance Measures

(in millions, except per share amounts)

Three months ended June 30, 2011

Mueller Co.

U.S. Pipe

Anvil

Corporate

Total

GAAP results:

Net sales

165.8

$

107.1

$

93.8

$

-

$

366.7

$

Gross profit (loss)

46.7

$

(2.8)

$

26.6

$

(0.2)

$

70.3

$

Selling, general and administrative expenses

23.9

6.6

17.0

7.2

54.7

Restructuring

0.2

1.4

0.1

-

1.7

Income (loss) from operations

22.6

$

(10.8)

$

9.5

$

(7.4)

$

13.9

Interest expense, net

16.8

Income tax benefit

(0.2)

Net loss

(2.7)

$

Net loss per diluted share

(0.02)

$

Capital expenditures

4.1

$

1.8

$

1.8

$

-

$

7.7

$

Non-GAAP results:

Adjusted income (loss) from operations and EBITDA:

Income (loss) from operations

22.6

$

(10.8)

$

9.5

$

(7.4)

$

13.9

$

Restructuring

0.2

1.4

0.1

-

1.7

Adjusted income (loss) from operations

22.8

(9.4)

9.6

(7.4)

15.6

Depreciation and amortization

11.8

4.6

3.7

0.2

20.3

Adjusted EBITDA

34.6

$

(4.8)

$

13.3

$

(7.2)

$

35.9

$

Adjusted operating margin

13.8%

-8.8%

10.2%

-

4.3%

Adjusted EBITDA margin

20.9%

-4.5%

14.2%

-

9.8%

Adjusted net loss:

Net loss

(2.7)

$

Restructuring, net of tax

1.0

Interest rate swap settlement costs, net of tax

1.3

Adjusted net loss

(0.4)

$

Adjusted net loss per diluted share

-

$

Free cash flow:

Net cash provided by operating activities

12.1

$

Capital expenditures

(7.7)

Free cash flow

4.4

$

Net debt (end of period):

Current portion of long-term debt

0.9

$

Long-term debt

692.1

Total debt

693.0

Less cash and cash equivalents

(45.8)

Net debt

647.2

$

30 |

31

Segment Results and Reconciliation of Non-GAAP to GAAP

Performance Measures

(in millions, except per share amounts)

Three months ended June 30, 2010

Mueller Co.

U.S. Pipe

Anvil

Corporate

Total

GAAP results:

Net sales

174.6

$

120.2

$

81.1

$

-

$

375.9

$

Gross profit (loss)

52.1

$

(2.7)

$

21.1

$

0.1

$

70.6

$

Selling, general and administrative expenses

23.3

7.7

16.6

9.6

57.2

Restructuring

-

0.9

-

-

0.9

Income (loss) from operations

28.8

$

(11.3)

$

4.5

$

(9.5)

$

12.5

Interest expense, net

15.8

Income tax expense

0.5

Net loss

(3.8)

$

Net loss per diluted share

(0.02)

$

Capital expenditures

2.7

$

2.1

$

2.0

$

-

$

6.8

$

Non-GAAP results:

Adjusted income (loss) from operations and EBITDA:

Income (loss) from operations

28.8

$

(11.3)

$

4.5

$

(9.5)

$

12.5

$

Restructuring

-

0.9

-

-

0.9

Adjusted income (loss) from operations

28.8

(10.4)

4.5

(9.5)

13.4

Depreciation and amortization

12.3

4.6

3.9

0.3

21.1

Adjusted EBITDA

41.1

$

(5.8)

$

8.4

$

(9.2)

$

34.5

$

Adjusted operating margin

16.5%

-8.7%

5.5%

-

3.6%

Adjusted EBITDA margin

23.5%

-4.8%

10.4%

-

9.2%

Adjusted net loss:

Net loss

(3.8)

$

Tax on repatriation on Canadian earnings

2.2

Restructuring, net of tax

0.5

Adjusted net loss

(1.1)

$

Adjusted net loss per diluted share

(0.01)

$

Free cash flow:

Net cash used in operating activities

(8.6)

$

Capital expenditures

(6.8)

Free cash flow

(15.4)

$

Net debt (end of period):

Current portion of long-term debt

10.5

$

Long-term debt

682.2

Total debt

692.7

Less cash and cash equivalents

(77.1)

Net debt

615.6

$

31 |

32

Segment Results and Reconciliation of Non-GAAP to GAAP

Performance Measures

(in millions, except per share amounts)

Nine months ended June 30, 2011

Mueller Co.

U.S. Pipe

Anvil

Corporate

Total

GAAP results:

Net sales

444.5

$

257.3

$

263.8

$

-

$

965.6

$

Gross profit (loss)

109.7

$

(13.3)

$

73.4

$

0.1

$

169.9

$

Selling, general and administrative expenses

67.6

21.2

50.4

22.3

161.5

Restructuring

1.2

3.3

1.2

-

5.7

Income (loss) from operations

40.9

$

(37.8)

$

21.8

$

(22.2)

$

2.7

Interest expense, net

49.0

Income tax benefit

(17.8)

Net loss

(28.5)

$

Net loss per diluted share

(0.18)

$

Capital expenditures

11.0

$

6.0

$

4.4

$

0.5

$

21.9

$

Non-GAAP results:

Adjusted income (loss) from operations and EBITDA:

Income (loss) from operations

40.9

$

(37.8)

$

21.8

$

(22.2)

$

2.7

$

Restructuring

1.2

3.3

1.2

-

5.7

Adjusted income (loss) from operations

42.1

(34.5)

23.0

(22.2)

8.4

Depreciation and amortization

35.7

13.8

10.9

0.6

61.0

Adjusted EBITDA

77.8

$

(20.7)

$

33.9

$

(21.6)

$

69.4

$

Adjusted operating margin

9.5%

-13.4%

8.7%

-

0.9%

Adjusted EBITDA margin

17.5%

-8.0%

12.9%

-

7.2%

Adjusted net loss:

Net loss

(28.5)

$

Interest rate swap settlement costs, net of tax

3.7

Restructuring, net of tax

3.5

Adjusted net loss

(21.3)

$

Adjusted net loss per diluted share

(0.14)

$

Free cash flow:

Net cash used in operating activities

(2.7)

$

Capital expenditures

(21.9)

Free cash flow

(24.6)

$

Net debt (end of period):

Current portion of long-term debt

0.9

$

Long-term debt

692.1

Total debt

693.0

Less cash and cash equivalents

(45.8)

Net debt

647.2

$

32 |

33

Segment Results and Reconciliation of Non-GAAP to GAAP

Performance Measures

(in millions, except per share amounts)

Nine months ended June 30, 2010

Mueller Co.

U.S. Pipe

Anvil

Corporate

Total

GAAP results:

Net sales

449.1

$

282.9

$

258.8

$

-

$

990.8

$

Gross profit (loss)

121.2

$

(19.6)

$

63.0

$

0.1

$

164.7

$

Selling, general and administrative expenses

66.7

22.3

48.0

26.0

163.0

Restructuring

0.1

11.6

0.1

-

11.8

Income (loss) from operations

54.4

$

(53.5)

$

14.9

$

(25.9)

$

(10.1)

Interest expense, net

47.4

Loss on early extinguishment of debt

0.5

Income tax benefit

(19.8)

Net loss

(38.2)

$

Net loss per diluted share

(0.25)

$

Capital expenditures

9.8

$

7.4

$

4.1

$

0.1

$

21.4

$

Non-GAAP results:

Adjusted income (loss) from operations and EBITDA:

Income (loss) from operations

54.4

$

(53.5)

$

14.9

$

(25.9)

$

(10.1)

$

Restructuring

0.1

11.6

0.1

-

11.8

Adjusted income (loss) from operations

54.5

(41.9)

15.0

(25.9)

1.7

Depreciation and amortization

37.2

14.0

11.5

0.6

63.3

Adjusted EBITDA

91.7

$

(27.9)

$

26.5

$

(25.3)

$

65.0

$

Adjusted operating margin

12.1%

-14.8%

5.8%

-

0.2%

Adjusted EBITDA margin

20.4%

-9.9%

10.2%

-

6.6%

Adjusted net loss

Net loss

(38.2)

$

Restructuring, net of tax

7.1

Tax on repatriation on Canadian earnings

2.2

Interest rate swap settlement costs, net of

tax (0.7)

Loss on early extinguishment of debt, net of tax

0.3

Adjusted net loss

(29.3)

$

Adjusted net loss per diluted share

(0.19)

$

Free cash flow:

Net cash provided by operating activities

35.7

$

Capital expenditures

(21.4)

Free cash flow

14.3

$

Net debt (end of period):

Current portion of long-term debt

10.5

$

Long-term debt

682.2

Total debt

692.7

Less cash and cash equivalents

(77.1)

Net debt

615.6

$

33 |

34

Segment Results and Reconciliation of Non-GAAP to GAAP

Performance Measures

(in millions, except per share amounts)

Year ended September 30, 2010

Mueller Co.

U.S. Pipe

Anvil

Corporate

Total

GAAP results:

Net sales

612.8

$

377.8

$

346.9

$

-

$

1,337.5

$

Gross profit (loss)

170.3

$

(22.7)

$

88.8

$

-

$

236.4

$

Selling, general and administrative expenses

89.2

30.5

66.2

33.4

219.3

Restructuring

0.1

12.5

0.5

-

13.1

Income (loss) from operations

81.0

$

(65.7)

$

22.1

$

(33.4)

$

4.0

Interest expense, net

68.0

Loss on early extinguishment of debt

4.6

Income tax benefit

(23.4)

Net loss

(45.2)

$

Net loss per diluted share

(0.29)

$

Capital expenditures

15.6

$

11.0

$

6.0

$

0.2

$

32.8

$

Non-GAAP results:

Adjusted income (loss) from operations and EBITDA:

Income (loss) from operations

81.0

$

(65.7)

$

22.1

$

(33.4)

$

4.0

$

Restructuring

0.1

12.5

0.5

-

13.1

Adjusted income (loss) from operations

81.1

(53.2)

22.6

(33.4)

17.1

Depreciation and amortization

49.7

18.9

15.4

0.6

84.6

Adjusted EBITDA

130.8

$

(34.3)

$

38.0

$

(32.8)

$

101.7

$

Adjusted net loss:

Net loss

(45.2)

$

Restructuring, net of tax

7.9

Interest rate swap settlement costs, net of tax

4.8

Loss on early extinguishment of debt, net of tax

2.8

Tax on repatriation on Canadian earnings

2.2

Adjusted net loss

(27.5)

$

Adjusted net loss per diluted share

(0.18)

$

Free cash flow:

Net cash provided by operating activities

63.0

$

Capital expenditures

(32.8)

Free cash flow

30.2

$

Net debt (end of period):

Current portion of long-term debt

0.7

$

Long-term debt

691.5

Total debt

692.2

Less cash and cash equivalents

(83.7)

Net debt

608.5

$

|

35

Segment Results and Reconciliation of Non-GAAP to GAAP

Performance Measures

(in millions, except per share amounts)

Year ended September 30, 2009

Mueller Co.

U.S. Pipe

Anvil

Corporate

Total

GAAP results:

Net sales

547.1

$

410.9

$

469.9

$

-

$

1,427.9

$

Gross profit (loss)

134.3

$

(5.7)

$

128.2

$

0.1

$

256.9

$

Selling, general and administrative expenses

84.2

35.6

84.9

34.4

239.1

Impairment and restructuring

820.7

101.1

96.7

0.2

1,018.7

Loss from operations

(770.6)

$

(142.4)

$

(53.4)

$

(34.5)

$

(1,000.9)

Interest expense, net

78.3

Loss on early extinguishment of debt

3.8

Income tax benefit

(86.3)

Net loss

(996.7)

$

Net loss per diluted share

(8.55)

$

Capital expenditures

16.2

$

11.2

$

11.9

$

0.4

$

39.7

$

Non-GAAP results:

Adjusted income (loss) from operations and EBITDA:

Loss from operations

(770.6)

$

(142.4)

$

(53.4)

$

(34.5)

$

(1,000.9)

$

Impairment and restructuring

820.7

101.1

96.7

0.2

1,018.7

Adjusted income (loss) from operations

50.1

(41.3)

43.3

(34.3)

17.8

Depreciation and amortization

50.9

21.1

17.6

0.6

90.2

Adjusted EBITDA

101.0

$

(20.2)

$

60.9

$

(33.7)

$

108.0

$

Adjusted net loss

Net loss

(996.7)

$

Impairment and restructuring, net of tax

954.9

Interest rate swap settlement costs, net of tax

3.8

Loss on early extinguishment of debt, net of tax

2.3

Adjusted net loss

(35.7)

$

Adjusted net loss per diluted share

(0.31)

$

Free cash flow:

Net cash provided by operating activities

130.5

$

Capital expenditures

(39.7)

Free cash flow

90.8

$

Net debt (end of period):

Current portion of long-term debt

11.7

$

Long-term debt

728.5

Total debt

740.2

Less cash and cash equivalents

(61.5)

Net debt

678.7

$

|

36

Questions |