EXHIBIT 1

TPG-AXON SENDS SECOND LETTER TO SANDRIDGE BOARD OF DIRECTORS

- Calls for Board to be Destaggered -

-- Announces Intent to Replace Current Directors –

--Lays Out Path to Restore Shareholder Value --

NEW YORK, November 30, 2012 – TPG-Axon, beneficial owners of 6.5% of the outstanding shares of SandRidge Energy, Inc. (NYSE: SD), sent a second letter today to SandRidge’s Board of Directors.

In the letter, TPG-Axon reiterated its desire to run a process to restructure or sell the Company, responds to SandRidge’s third quarter earnings announcement and provides greater detail on the market’s loss of confidence in management based on their poor strategy and structural challenges including staggering overhead costs.

TPG-Axon also notified SandRidge of its intent to conduct a consent solicitation of shareholders to amend the bylaws of SandRidge to:

| ● | de-stagger the board of directors; |

| ● | provide that directors be removed with or without cause; and, |

| ● | remove and replace the current board of directors. |

“We would emphasize and re-iterate that the time has come for change, and for a focus on delivering shareholder value,” said Dinakar Singh, founder and CEO of TPG-Axon. “We continue to believe that SandRidge stock is dramatically undervalued, and that a sensible restructuring or sale of the Company could provide dramatic upside for shareholders.”

TPG-Axon is separately sending a formal request that SandRidge set a record date for this consent solicitation, and a demand to exercise TPG-Axon’s rights as shareholders to inspect the shareholder list.

TPG-Axon has retained Mackenzie Partners Inc. to act on its behalf in the solicitation process.

The full text of the letter is attached.

About TPG-Axon Capital

TPG-Axon Capital is a leading global investment firm. Through offices in New York, London, Hong Kong and Tokyo, TPG-Axon invests across global markets and asset classes.

Contacts:

Anton Nicholas, Phil Denning, Jason Chudoba

203-682-8200

Anton.Nicholas@icrinc.com

Phil.Denning@icrinc.com

Jason.Chudoba@icrinc.com

TPG-AXON MANAGEMENT LP, TPG-AXON PARTNERS GP, L.P., TPG-AXON GP, LLC, TPG-AXON PARTNERS, LP, TPG-AXON INTERNATIONAL, L.P., TPG-AXON INTERNATIONAL GP, LLC, DINAKAR SINGH LLC AND DINAKAR SINGH (COLLECTIVELY, “TPG-AXON”) INTEND TO FILE WITH THE SECURITIES AND EXCHANGE COMMISSION (THE “SEC”) A DEFINITIVE CONSENT STATEMENT AND ACCOMPANYING CONSENT CARD TO BE USED TO SOLICIT WRITTEN CONSENTS FROM THE STOCKHOLDERS OF SANDRIDGE ENERGY, INC. IN CONNECTION WITH TPG-AXON'S INTENT TO TAKE CORPORATE ACTION BY WRITTEN CONSENT. ALL STOCKHOLDERS OF SANDRIDGE ENERGY, INC. ARE ADVISED TO READ THE DEFINITIVE CONSENT STATEMENT AND OTHER DOCUMENTS RELATED TO THE SOLICITATION OF WRITTEN CONSENTS BY TPG-AXON AND ANY OTHER PARTICIPANTS AT SUCH TIME (COLLECTIVELY, THE "PARTICIPANTS") FROM THE STOCKHOLDERS OF SANDRIDGE ENERGY, INC., WHEN THEY BECOME AVAILABLE, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION, INCLUDING ADDITIONAL INFORMATION RELATED TO THE PARTICIPANTS. WHEN COMPLETED, THE DEFINITIVE CONSENT STATEMENT AND FORM OF WRITTEN CONSENT WILL BE FURNISHED TO SOME OR ALL OF THE STOCKHOLDERS OF SANDRIDGE ENERGY, INC. AND WILL, ALONG WITH OTHER RELEVANT DOCUMENTS, BE AVAILABLE AT NO CHARGE ON THE SEC'S WEB SITE AT HTTP://WWW.SEC.GOV. IN ADDITION, TPG-AXON WILL PROVIDE COPIES OF THE DEFINITIVE CONSENT STATEMENT AND ACCOMPANYING CONSENT CARD (WHEN AVAILABLE) WITHOUT CHARGE UPON REQUEST.

|

|

November 30, 2012

Board of Directors

SandRidge Energy Inc.

123 Robert S. Kerr Avenue

Oklahoma City OK 73102

Dear Sirs,

As you know, we are among the largest shareholders of SandRidge Energy, with beneficial ownership of 6.5% of the common stock of the company. We write to provide you with updated thoughts, both regarding our concerns, and on the path ahead for shareholders. We will outline the reasons why we believe there are only two possible options:

|

1)

|

Dramatic simplification and restructuring of the company, or

|

|

2)

|

Sale of the company.

|

Of these two options, a lack of confidence in management, as well as the complexity involved in a potential restructuring, lead us to believe that an outright sale of the company is the most realistic path to restoring the shareholder value that has been destroyed. We continue to believe that the company has significant asset value, and that SandRidge shares are dramatically undervalued. However, the continued leakage of value from massive overhead costs (triple that of most Exploration & Production companies), high cost of capital (more than double that of most Exploration &Production companies), and strategic incoherence, have resulted in enormous destruction of value. Most of these problems are a function of management, not of the assets themselves, and therefore, we believe change is imperative to create value for shareholders.

SandRidge stock has declined almost 80% from its IPO level in 2007, and is the single worst performing energy stock over that period in the Russell 1000 Index. The stock today trades at the greatest discount to its estimated Net Asset Value of any energy company, and therefore would have 50 to 100% near-term upside IF markets had greater confidence in management. Management actions have caused tremendous damage to shareholders, and steps must be taken to repair this damage. As we noted in our previous letter, we are a firm that makes focused, long-term investments in companies, on the basis of exhaustive fundamental analysis. Most often, we are ‘involved’ shareholders, not ‘activist’ shareholders. However, in instances where we come to believe that management is acting in a manner that is destructive of value, we believe it is important to actively engage. In that context, we advise you of the following:

As is our right under the charter and bylaws of the company, we hereby notify you that we will commence a consent solicitation of shareholders to (i) amend the bylaws of the company to de-stagger the board of directors, and provide that directors be removed with or without cause; and (ii) to remove and replace the current board of directors.

We are separately sending a formal request that the company set a record date for this consent solicitation; and a demand to exercise our rights as shareholders to inspect the shareholder list. Please note that we have retained Mackenzie Partners Inc. to act on our behalf in the solicitation process.

|

|

RECENT DEVELOPMENTS:

Since our last communication with you, there have been several significant developments. The company reported 3rd quarter earnings, and in addition to disclosing financial results, it also offered updated data on well results in the Mississippian formation, as well as guidance regarding 2013 operating and cashflow expectations. The company also announced an intention to sell various Permian Basin assets. In aggregate, the company announcements were poorly received by the market, as reflected in the significant decline in the stock subsequent to earnings.

From our perspective, several aspects of the earnings and strategy announcements were of great concern:

Capital Expenditures:

Capital expenditures, yet again, significantly exceeded management projections and guidance. As we highlighted in our previous letter, this management team seems incapable of realistically forecasting its needs, and/or completely lacks budget discipline. In general, the persistent inaccuracy in forecasts, and overspending in capital expenditures has severely damaged management credibility. The company also announced a significant future reduction in projected capital expenditures for 2013. However, at this point, few investors believe management projections; most assume that the company is simply saying what they think investors want to hear, rather than having any realistic understanding of their capital expenditure needs, or any real intention of sticking to their budget.

The core problem for the company is the mismatch between its (balance sheet and operational) capabilities, and the scale of the needed investment. A small company like SandRidge simply cannot prudently and efficiently drill over 11,000 wells over 1.8 million acres, as the company claims it will do. Particularly since rights to acreage are generally lost if drilling does not commence in five years, the company needs to build out wells and infrastructure over a massive amount of acreage. As a result, either it must drill inefficiently (too little density of wells, and therefore high infrastructure costs per well) or massively stretch its balance sheet and face soaring cost of capital….or both, as has actually happened at SandRidge.

Overall, the company argues that costs will decrease over time, as acreage is developed and well density improves. However, unfortunately time is money, in an industry with high fixed costs. Because SandRidge has bitten off far more than it can chew, and because extended timeframes now result in significant declines in IRR on investments, the company constantly faces undesirable trade-offs of speed vs. efficiency and quantity vs. quality.

Well Results:

Even more importantly, the company provided updated well results for the Mississippian formation. We believe these well results, particularly in light of previous management commentary, were primarily responsible for the severe decline in the stock. As had been rumoured in weeks preceding the earnings announcement, well results showed that Mississippian wells drilled by the company have had a higher content of natural gas, and lower content of oil, than the company had previously projected. In general, the ‘type curve’ now implied by company data is less attractive than management had previously projected – higher costs, lower revenues, and more extended period of payback. Once again, the problem is management credibility. Some other E&P companies involved with the Mississippian have been providing much more regular and detailed information to investors regarding well cost and quality, and have been much more conservative in their assumptions and forecasts. By contrast, SandRidge has been projecting dramatically higher returns for the Mississippian, and has done a poor job of disclosing accurate information to investors. Management has generally been trumpeting 80%+ IRR potential of Mississippian wells, which is dramatically greater than that projected by competitors. In hindsight, it is clear that others were right to be conservative, and SandRidge was wrong. The good news is that even with more sensible and conservative assumptions, the Mississippian formation appears to be a solid investment – after all, for an efficient company, with low cost of capital, 20 – 40% IRR is highly attractive, and that is what realistic forecasts suggest. However, for SandRidge, there are two significant problems. First, management continues to cement a reputation as one that always ‘over-promises and under-delivers’. In every regard, management forecasts seem increasingly more ‘hope’ (or even hype) rather than realistic expectation. Even more importantly, however is the issue of cost - higher capital costs, higher overhead costs, and high infrastructure costs mean that a more moderate IRR is devastating to value. For competitors, a very high return is icing on the cake; by contrast, SandRidge’s funding and cost situation essentially require extraordinary IRR to create value.

Asset Sales:

The company also announced plans to sell various Permian Basin assets, in order to raise funds for development of the Mississippian assets. The market reaction to the announcement was generally negative, largely because it revealed that the ‘funding gap’ faced by the company was much greater than previously revealed by management, and because it demonstrated further incoherence of strategy…it is astonishing that just months after completing the $1.3 billion acquisition of Dynamic Offshore, the company is now reversing course and selling assets. Overall, the increasing scepticism regarding management projections is causing investors to fear the sale of good assets to fund ‘hope’ by management. The following quotes provide a representative sample of investor perception and reaction:

Ryan Todd, Deutsche Bank, 11/13/2012. “At the end of the day, the biggest casualty of a Permian sale may be investors’ confidence in management, with its second significant strategic change in less than a year”

Joseph Allman, JPMorgan, 11/16/2012. “Since the market seems to lack confidence in the company’s financial position and strategy, we think the company will trade at a discount to the group median until that confidence grows”. “Several investors have questioned SD’s decision to sell the Permian”.

Stephen Shepherd, Simmons, 11/9/2012. “SD’s decision to sell the Permian comes as a bit of a surprise… At this point, with the switch in strategy and significant moving parts we are unsure if it is prudent to give SD the benefit of the doubt.”

From our perspective (as outlined in more detail later), asset sales to unlock value are not a bad thing, if done at a good price. However, the company is not selling assets to deliver shareholder value; it is selling assets because of greater than expected funding requirements. The need for these sales highlights almost all of the concerns we have raised about the sustainability of the company under current management and in current form. At current rates of well cost and spending, SandRidge would need as much as $40 billion to develop its wells in the Mississippian. Even IF it could instantly reduce costs to more efficient levels, this figure would still be over $30 billion…these figures are staggering in any context, but remarkably so for a company with a market capitalization of less than $3 billion, whose cost of capital is more than double that of its peers, and whose corporate overhead is more than triple most of its peers! Overall the combination of soaring funding needs, extremely high cost of capital, and massive overhead are creating a toxic combination – a need to shrink to provide for funding, which then creates even more pressure on remaining assets from the company’s high costs.

Overall, we believe the developments in the past quarter crystallize the key challenges the company faces. As we noted in our previous letter, management has pursued a reckless strategy that has left no margin for error. The Mississippian assets are good, and have tremendous value and potential. However, recent results make clear that the returns are not as high, and payback as quick, as management had trumpeted. Hence, the sudden shift towards selling the Permian assets. If these sales represented a newfound commitment to realizing and delivering value for shareholders, we would not be having this dialogue. Instead, they are yet another symptom of a management team that has had reckless disregard for transparency, for prudence, and for shareholders.

MANAGEMENT & STRATEGY

In recent days, management has attempted to defend its record. In particular, management has cited the collapse of natural gas as an unforeseeable accident that befell the company; that management was visionary in foreseeing the collapse of gas; and that the actions management took to ‘pivot’ towards oil ‘saved’ the company. Therefore, prior to examining the current challenges and the path ahead, we must analyze management claims and action. After all, they are central to an assessment of whether this management team can add value in the future.

Most E&P companies understand that oil and gas exploration is a risky business, and that nothing is certain in this industry. Most companies realize that the underlying commodities are volatile, and that business plans must incorporate the possibility of significant swings in the prices of underlying commodities. Therefore, even the boldest companies attempt to diversify exposures to some degree, and ensure that their balance sheet and funding are suitable to the business risk of the company. In the case of SandRidge, Mr Ward was not a visionary. Rather, essentially at the peak of the natural gas market, he chose to bet the entire company on high cost natural gas production. Essentially all funds raised from shareholders in 2007 were used to expand as aggressively as possible into the West Texas Overthrust. There was no diversification to mitigate risks for shareholders – rather, Mr Ward was so certain that natural gas would rise, that he ‘bet the ranch’ (or at least the shareholder’s ranch – his ranch was never at risk). Not only did he bet almost exclusively on natural gas, but he did so with massive leverage and on high-cost production, thus leaving shareholders dramatically levered to the fortunes of natural gas. As natural gas spiked in mid-2008, Mr Ward did not foresee the coming collapse. Instead, at the absolute peak of the market, he entered into a Carbon Dioxide processing joint agreement with Occidental Petroleum, in which he essentially guaranteed minimum volumes of Carbon Dioxide (a by-product of SandRidge’s natural gas production) to Occidental. Now, because of this deal, the company is incurring tens of millions of annual payments to Occidental. Other companies can at least limit or halt development of natural gas, if low prices render production uneconomic. In the case of SandRidge, because Mr Ward was so confident that natural gas would remain at high levels, he committed to high levels of production (of CO2, and thereby natural gas) for 30 years! Therefore, despite the fact that it no longer makes sense for SandRidge to produce high volumes of gas from the West Texas Overthrust, SandRidge is obligated to either produce high levels of gas and CO2 or make compensatory payments of as much as $40+ million per year…for decades.

As natural gas began to collapse in mid-2008, did Mr Ward ‘pivot’ from natural gas to oil, as he claims? In short, no - In fact, the company never sold its gas assets – they were simply written down over time, at the expense of shareholders. It is true that future purchases of assets (in late 2009) were of oil assets, but it did not take a visionary to realize that natural gas was troubled, by late 2009. In fact, there was only one sale of natural gas assets made – and we agree that it was extraordinary…it was the sale by Mr Ward of his entire interest in the West Texas Overthrust wells back to SandRidge for just under $70 million in October 2008. As we noted in our previous letter, at this point, natural gas was plunging, markets had collapsed, credit markets were frozen, SandRidge stock had collapsed, and SandRidge debt was trading at 60 cents on the dollar. It was not ‘vision’ that led Mr Ward to sell his natural gas interests to the company, it was greed and brazen contempt for shareholder interests. For his personal interest, Mr Ward ‘pivoted’ from natural gas to cash while the market was collapsing; shareholders, unfortunately, ended up being forced to increase their exposure. Regarding this issue, we demand that Directors of the company disclose details of their deliberation and rationale for approving this sale. Shareholders are owed an explanation for why the Board of Directors approved this transfer of wealth from the company to Mr Ward at the peak of the financial crisis.

In fairness, the subsequent purchase of the Permian oil assets in late 2009 has been a good investment. Here too, there are two important qualifications. First, the purchase was paid for with additional borrowing (at high cost of debt) and massive equity issuance. Second, over time, the company could not leave well enough alone – Mr Ward proceeded to sell off the eastern and western Permian assets (Midland and Delaware basins) in order to fund expansion in the Mississippian. That was a mistake, as the Midland and Delaware assets have continued to appreciate in value relative to the remaining Central Basin assets that Mr Ward kept.

Since then, Mr Ward has been on an aggressive acquisition spree of land in the Mississippian formation. An important, but lesser, issue is that there have been significant conflicts of interest – land leased at significant prices from Mr Ward and other SandRidge-related parties. Most importantly, Mr Ward simply did not learn the lesson that prudence was a virtue. We give Mr Ward credit for being early to identify the potential of the Mississippian formation. However, once again, the company ‘bet the ranch’, by acquiring far more acreage than it has the realistic capability to develop in an economic and efficient manner. As a result, funding has become a constant drama in recent quarters. To put figures in context, the company has estimated that its acreage could support over 11,000 wells in the future. At past costs per well – $4 to $6 million – the total capital expenditures required would be over $40 billion, and even with reduced costs, capital expenditures will exceed $30 billion. Because of the vast amount of acreage the company is trying to drill, it simply does not have economy of scale. As noted previously, infrastructure costs (water disposal, electricity, etc.) are higher than they should be, on a per well basis, because of the low density of drilling (the company must drill in every section of acreage within 5 years in order to maintain mineral rights; therefore, the vast amount of acreage acquired has forced the company to drill across vast amounts of acreage, rather than concentrating efforts). In theory, costs per well should decline from current levels – to approximately $3 million per well (as it is for some competitors). However, the vast scope of acreage that needs drilling means that this decline in cost, and economy of scale, might not happen for many years. Even at lower costs per well, the company would need to spend over $30 billion in years ahead. In the context of the current assets, it is obvious that the future capital expenditure investment will dwarf existing asset value in importance over time.

The company’s aggressive capital expenditure program, and accompanying funding needs, ‘required’ massive returns on wells drilled (and early payback), in order to provide the funding for future wells. By assuming high rates of return and optimistic ‘type curves’, the company was able to argue that funding needs were manageable, and that capital expenditures could be funded from operating cashflow by next year. It has become clear that management estimates were simply unrealistic, and that more realistic assumptions result in a substantially greater ‘funding gap’ than the company had previously disclosed. It has become increasingly apparent that it is simply nonsensical to think the company could efficiently and economically develop the amount of acreage it has acquired.

Concerns about overspending and inadequate funding led to a collapse in the stock in mid-2011. After the company assured the market that it had adequate funding and that it would be disciplined in the future, the stock recovered somewhat. However, the company then shocked investors by announcing the Dynamic Offshore acquisition in early 2012. As we noted in our previous letter, this acquisition was strategically incoherent, and damaging to shareholder value. The company had been trumpeting its vision in switching to oil, and its focus on Permian and Mississippian formation assets – therefore the purchase of mature, rapidly-declining offshore oil assets was a radical departure from the company’s stated focus and strategy. Management touted the low multiple of EBITDA at which the assets were acquired as a measure of the wisdom of the deal. However, careful examination renders this argument invalid and foolish. The acquired assets were short-life, rapidly declining, offshore oil wells, which is why they were sold at a low multiple of EBITDA. In fact, SandRidge is now projecting to spend over $200 million next year in capital expenditures on the Dynamic Offshore assets in order to prop up production levels. If one subtracts this required capital expenditure from EBITDA (as any sensible person would), it reveals that the multiple paid of true cashflow was over 10x – this is hardly a bargain! Why did Mr Ward make the acquisition? In short, it was an accounting gimmick. The company had greater funding needs than it had disclosed to the market, and yet had limitations on its ability to borrow more money because of a debt covenant restricting total debt as a multiple of EBITDA. By ‘acquiring EBITDA’ (even if it was of very low quality, and expensive relative to true value), the company was able to gain additional flexibility in its calculation of ‘Debt to EBITDA’, and therefore gained some breathing room under its debt covenants. For shareholders, however, it was a high price to pay for an accounting gimmick – massive dilution, with the stock at an enormous discount to NAV. Overall, SandRidge paid a full valuation, for assets that were strategically incoherent, and while using massively discounted SandRidge stock as currency.

Overall, we do not believe management’s track record merits giving them the benefit of the doubt regarding vision and strategy.

| ● | Management chose to make a massive and levered bet on high-cost natural gas near the peak of the market. |

| ● | Management has consistently over-reached in its spending and leverage, putting shareholders at risk. |

| ● | Management has shown either an inability or a disinterest in realistically assessing its funding needs, and communicating accurately and |

| candidly with shareholders. | |

| ● | Management has shown a constant propensity for ‘trading’ assets, in a manner that often creates confusion and complexity, rather than |

| value. |

Therefore, we do not believe that management’s track record suggests great vision and wisdom; rather it has been marked by reckless and chaotic behaviour. Management has made some spectacularly poor decisions. Even more troubling is that even good decisions have been squandered by subsequent over-reaching or zigzagging. Overall, we struggle to understand why Mr Ward and this management team would claim to be the saviours of shareholders and the company. In many ways, it is tantamount to an arsonist claiming credit for calling the fire department after his own fire has burned a building down.

The ultimate reflection of management missteps has been the stock price. As we noted in our previous letter, SandRidge stock has declined almost 80% since its 2007 IPO, and has been the single worst performing energy stock in the Russell 1000 over the past five years. However, just as extraordinary is the fact that this underperformance is not just a function of 2008, and the financial crisis. SandRidge stock has continued to underperform peers every year since then (including many companies who focused on natural gas, rather than oil). The collapse in SandRidge stock in 2008 was not just a function of the financial crisis – it was a result of choices made by management. However, even if one absolved management of all responsibility for the initial collapse in the stock in 2008, it is shocking that underperformance has continued year after year.

The company has made repeated, and unexpected, shifts in strategy in recent years, and after almost every such action the stock has declined precipitously. Rather than focus on operational issues, and efficient and effective execution of strategy, the company consistently acts as if it can ‘wheel and deal’ its way to prosperity. Unfortunately, shareholders have suffered at every turn, even as management continues to reward itself to an astonishing degree.

STRUCTURAL CHALLENGES

In addition to strategic missteps, the continued underperformance of the stock has been driven by two significant persistent and structural problems – high cost of capital, and extraordinarily high levels of overhead costs.

High cost of capital: SandRidge’s cost of capital is substantially higher than all relevant comparable companies or competitors. For example, the six other companies with meaningful development programs in the Mississippian formation have cost of debt ranging from 2% to 4% (with the exception of Chesapeake, and even their cost of debt capital is lower at 5.7%). By contrast, SandRidge debt yields 7%. This comparison might actually be too generous, since the other companies have substantial ability to borrow money at those rates, while SandRidge has limited ability to borrow any additional money, given high leverage and existing debt covenants. Given the capital intensive nature of the business, and the fact that enormous amounts of capital are required to develop the assets, a high cost of capital is a significant drain on shareholder value. For example, the differential in incremental cost of debt between Devon Energy and SandRidge, as applied to SandRidge debt, represents over $100 million per year in damage to shareholders! This represents a drain of value, from stockholders, of almost 4% of the market value of the company, each and every year!

As we noted in our previous letter, the high cost of capital is a direct function of management, and management decisions. Poor corporate governance, aggressive capital spending, erratic strategy, and a highly stretched balance sheet have all contributed to the reluctance of capital markets to fund SandRidge. The high cost of debt is an enormous ‘tax’ on shareholders, and has drained significant value. The reluctance of debt investors to fund SandRidge has forced the company to issue equity repeatedly (at enormous discounts to NAV) to fund strategic shifts – the company has been forced to issue equity 5 times in its 5 year history! We do not know of a single other major energy company that has been forced to issue equity as much!

|

Interest Rate1

|

G&A

(% mkt cap)2

|

||||

|

SandRidge

|

6.9%

|

7.8%

|

|||

|

Apache

|

2.3%

|

1.7%

|

|||

|

Chesapeake

|

5.7%

|

5.1%

|

|||

|

Devon

|

2.7%

|

3.1%

|

|||

|

EnCana

|

3.0%

|

2.6%

|

|||

|

Range Resources

|

4.5%

|

1.8%

|

|||

|

Shell

|

1.9%

|

0.8%

|

|||

|

Source: Bloomberg

|

|||||||

|

1 Interest rate based on YTM of benchmark 8-10 year senior notes

|

|||||||

|

2.G&A based on YTD 2012 annualized selling, general and administrative expenses. Shell based on Upstream only.

|

|||||||

Staggering overhead costs: Even more than the high cost of capital, the most significant structural challenge facing shareholders is the extraordinarily high level of corporate overhead. Compared to competitors, SandRidge ought to have G&A expenses that are low - after all, the company operations and assets are dramatically more concentrated than many competitors. Many other energy companies have assets scattered across many continents, whereas SandRidge assets are all in a few hundred mile radius of each other. Instead, corporate overhead is over $200 million per year, and is projected (by the company) to rise! This figure is more than double the company’s total net income, and represents a staggering 8% of the entire market capitalization of the company, spent each year on overhead. By comparison, most other E&P companies have overhead levels that represent 1 – 3% of their market capitalization – therefore, SandRidge shareholders are paying 3 to 5 times more than other companies for the privilege of management. This level of inefficiency and waste is a massive ‘tax’ on shareholders that is simply unsustainable. No company can survive over time, if it suffers such handicaps relative to competitors.

In our previous letter, we noted the outrageous levels of compensation for Mr Ward – $150 million in direct payments over the past five years (not including the indirect payments outlined below, or lease payments on his land), despite an almost 80% collapse in the stock. However, the extraordinary level of overhead is not just a function of Mr Ward’s compensation. Rather, it is a function of a culture of cronyism and waste that permeates the company, and Mr Ward’s compensation must be viewed in the context of the additional expenses that enable it, and accompany it. The company provides little detail on how it spends such extraordinary amounts. How can a company, this size, possibly spend over $200 million per year on top management and related expenses? Through careful examination, we have uncovered some details.

|

●

|

Senior management compensation: As we noted in our previous letter, Mr Ward’s compensation is shocking, relative to his performance and the size of the company (total payments to Mr Ward over the past five years represent 6% of the total current market capitalization of the company). However, the ridiculous levels of compensation extend to other senior managers as well. Compensation for the company’s Chief Financial Officer has quadrupled since 2007, from $1.8 million to $6.8 million, making him one of the highest paid CFO’s in corporate America. Similarly, compensation for the company’s Chief Operating Officer more than doubled in the past five years, from $3.2 million to $7.7 million, making him one of the highest paid Chief Operating Officers in corporate America. In aggregate, compensation for the top few executives of SandRidge has doubled over the past five years, to $45 million (just under 2% of the market capitalization of the company – per year!). Obviously, these levels of compensation are remarkable for any company in America, but are simply unfathomable in the context of a company that has been the worst performing company in its sector over the past five years, and one of the worst performing companies in all of corporate America.

|

|

●

|

Director Compensation: Why have the directors of the company approved such outrageous compensation, particularly in light of the abysmal performance of the company? Perhaps because most have few credentials as directors and fiduciaries of publicly listed companies, and appear to have personal ties to Mr Ward. Or, perhaps because their compensation has also tripled over the past five years. SandRidge directors are paid annual fees of $360,000 each; a level that is among the highest of any company in the country. To put this figure in context, directors of Exxon Mobil (the largest energy company in the world, whose market value is 150 times that of SandRidge), are paid ‘only’ $285,000 per year. In addition, we believe directors have been provided enormously valuable perks – private jet usage, use of luxury suites, etc. Unfortunately, value has been steadily drained from shareholders by a vicious and corrupt circle – Mr Ward selects directors of the company, who are then paid extraordinary sums and given remarkable perks, and then reciprocate by approving shocking levels of compensation and payments for Mr Ward and other top executives.

|

|

●

|

Management and Director Perks: Even from the few details disclosed by the company, it is clear that the perks for management and directors are truly extraordinary by any standard. The company pays almost $1 million year to provide personal accounting services to Mr Ward. The company spends millions of dollars each year sponsoring the Oklahoma City Thunder (of which Mr. Ward is a co-owner), and pays for luxury suites for the basketball team. One of the largest perks is private jet usage. Many companies provide some degree of private jet usage for work travel for senior executives, but few have the ‘air force’ that SandRidge does. Prior to the IPO in 2007 (when expenses were actually borne by Mr Ward), the company owned one old and small jet and two old propeller airplanes to transport executives and workers. Once shareholders were bearing the cost, Mr Ward decided to upgrade – now the company has four jets (two of which are large size intercontinental jets, and one of which is one of the most expensive jets in the market), and over 15 full time employees dedicated to maintaining and flying these jets. Most companies require executives to use jets only for work, and to compensate the company for personal usage. SandRidge provides unlimited personal usage for Mr Ward – last year that included dozens of personal flights to Scottsdale (Mr Ward’s vacation home), and numerous weekend trips to Las Vegas, Los Angeles, the Bahamas, etc…all paid for by shareholders. It is extraordinary that a company that has needed to issue equity 5 times in 5 years, has the highest cost of debt of any comparable company, and has faced bankruptcy, has chosen to invest tens of millions of dollars in private aircraft ownership, and then spend many millions each year in expenses…and for personal use, not just company needs!

|

|

●

|

‘Other’ Expenses: Despite the fact that the company does not provide details on its massive overhead spending, it is clear to us that enormous sums are being spent on wasteful or vanity expenses. The company spends many millions each year on television advertising – other than ego gratification, why does a small E&P company need to heavily advertise on TV? The company spends massive amounts of money on real estate in Oklahoma City – far in excess of what would be sensibly needed (and including many fully-owned buildings, and real estate development projects). We cannot explain the enormous number of employees the company has at headquarters (almost 700), and it is remarkable that the company has doubled the number of general employees at its Oklahoma City headquarters over the past five years. Yet, the company appears to have real estate assets and investments far in excess of what would be needed even by this number of employees. In addition, the co-mingling of business and personal matters is present in the company’s real estate expenses and investments as well – for example, SandRidge provides real estate for many of Mr Ward’s personal interests, and pays one Director over $500,000 per year in real estate lease payments.

|

We provide these details, not to be salacious, but to provide examples of the numerous items that aggregate into overhead that is extraordinary in any context. One might sensibly think that SandRidge would have a lean and efficient level of overhead, given its narrow and dense nature of operations. Instead, most of the $200 + million that is spent appear to be in excessive compensation, perks, and extraneous activities. These expenses are a massive drain on the company. When one combines the extraordinary cost of debt capital with the even more extraordinary level of overhead expenses, it becomes clear why the stock has performed as poorly as it has. No company, in any industry, can survive when 10 – 15% of the total market capitalization is siphoned off each year, leaving the company with a massive handicap relative to competitors.

To put these sums in another context, I suspect your shareholders would never invest in a mutual fund that charged 10 – 15% management fees and expenses, each and every year, especially if the fund had disastrous performance. After all, that would be an obvious recipe for disastrous net returns over time. Yet, that is exactly what is happening at SandRidge. And, it appears that things are getting worse, not better. In response to the immense challenges the company has faced this year (collapse in the stock price, issuing equity, significant downgrades in cashflow projections, etc.) the company response has been to spend even more money on compensation and perks. In the recent 3rd quarter conference call, management had the nerve to announce that they would be increasing corporate overhead by 10% in the coming year! And, despite the challenges this year, the company decided (this spring) that Mr Ward needed a better plane, and purchased a Falcon 900EX for his exclusive business and personal use. For reference, the Falcon 900EX is one of the most expensive private business jets made, with new list price of over $35 million, and flying range of almost 6,000 miles. Given that every employee and asset of the company is within a 500 mile radius of headquarters, it seems obvious that a $35 million plane with 6,000 flying mile range is for CEO gratification, not business necessity.

THE PATH AHEAD

Ultimately, we believe the time has come for change, and that shareholders must assess whether value will be maximized by a radical restructuring, or by a sale of the company. Under the current structure, the company will simply not be able to create value for shareholders. Cost of capital, and expenses, are too high, and funding needs are too great. The ‘leakage’ of value each year to creditors and management will simply destroy shareholder value over the long run, particularly given the extensive funding needs the company will have for years to come. Recent events and actions highlight the paradox for the company – it must sell assets to provide funding for capital expenditure plans, and yet those asset sales shrink the asset base and result in amplification of already outrageous levels of costs and expenses…therefore, attempts to reduce cost of capital only serve to increase the burden of overhead.

How should the company restructure? We believe the company would need to take significant steps to reduce cost of capital AND expenses AND funding needs. Addressing only a portion of the problem will simply shift the burden, rather than reduce it.

Therefore, we believe the following steps would have to be taken:

|

●

|

Restructure both the Board of Directors and Management team: Without dramatic changes at the top, the company cannot restore the confidence of capital markets (necessary to reduce cost of capital) or seriously address profligacy in expenses.

|

|

●

|

Drastically reduce overhead and waste: The company should dramatically reduce the extravagance and waste that has led to extraordinary levels of overhead for the company. We believe it would be not just possible, but necessary, to reduce overhead by 75%. Unless this is done, the ‘tax’ on shareholders will simply be too great over time, and value will continue to be destroyed. Compensation for remaining employees should be reduced to sensible levels. Extraneous assets (planes, buildings, etc.) should be sold. Extraneous expenses should be terminated (personal payments, advertising, luxury suites, etc.). Overall, the company should seek to emerge as one of the leanest and most efficient companies in the industry, in keeping with the focused and concentrated nature of its assets.

|

|

●

|

Sell extraneous assets: The Company should both unlock value, and improve balance sheet and funding needs, by selling assets. The first priority should be to sell the offshore assets. The Dynamic Offshore assets were a mistake to have acquired, and make little sense for the company to keep. Sadly, while we do not believe the company can recover what it paid for the assets, it is best to recover what is possible from these assets, and move on. In addition, we would then recommend proceeding with the sale of the Permian assets (and even explore whether it could be possible to sell the 20% of the Permian assets encumbered by the royalty trust agreements.) Overall, assuming a full sale of both assets, we believe the company could realize proceeds from these sales of $3.5 to $5 billion, which would be enough to fully retire all existing debt (approximately $3.5 billion) and even leave additional funds for future needs. We would note that there is genuine debate among shareholders regarding whether the Permian assets should be retained or sold. We would certainly agree that it would be best to sell the Offshore assets and keep the Permian, rather than the other way around. However, ultimately we think the benefits of reducing cost of capital, and the ability to truly maximize efficiency by simplifying assets, outweigh the positives of keeping the Permian assets.

|

|

●

|

Reduce future funding needs: The remaining assets would be the Mississippian producing wells, vast amounts (1.8 million acres) of Mississippian acreage, and the significant amount of infrastructure (particularly water disposal) that the company has built in the Mississippian. For example, we believe the water disposal system could be worth as much as $1 billion, and should be monetized over time. Overall, the Mississippian acreage the company controls is simply too vast for the company to develop by itself, even net of the joint venture deals the company has already struck (Repsol and Atinum). We believe the company should seek to monetize (either through a sale or additional joint ventures) a significant portion (1/2 or more) of the undeveloped Mississippian acreage, so that the remaining interest will be of a size that the company can develop economically and efficiently using its own balance sheet and cashflow.

|

If all of these steps are taken, the company may dramatically reduce its cost of future capital, unlock significant value for shareholders, and be left with valuable remaining assets that can be developed to their full potential. In our previous letter, we noted that asset value (NAV) of the company was $12 to $14 per share. Unfortunately, we do believe the updated information regarding the Mississippian wells (type curves, gas/oil mix) should reduce NAV somewhat – we believe a more conservative assessment, with updated information, would be $1 ½ to $2 lower than before – therefore $10 to $12 is perhaps the best range for current SandRidge NAV. However, that value is a near-term value, and would grow dramatically over time, as confidence in the company increased, and the Mississippian assets are developed successfully.

However, ultimately we believe shareholders must ask whether the radical restructuring and simplification of the company is really a better route than a sale of the full company (whether in one package or in various packages as a sum of the parts). A restructuring of the company can deliver dramatic value for shareholders – we think 50 to 100% upside from current stock levels is realistic over the next 6 – 12 months. However, there are two factors that lead us to believe that a sale of the company is best:

Ultimately, the value of the Mississippian assets is extraordinary, but so is the investment and time required to develop those assets. As a result, there is a compelling argument that the assets will be worth the most to a company with the cheapest cost of capital, and the most need for massive reserve replacement in coming years. It may be that a joint venture could address this issue, but we believe shareholders should consider the full range of options for the Mississippian assets.

In addition, it is likely that there will be some leakage of value from sales of the ‘other’ assets (Offshore Gulf of Mexico, Permian, etc.). Our estimates of value and proceeds already incorporate this risk. However, it is likely that value will be maximized if in fact there is a buyer who wants (and can extract synergies from) all of the SandRidge assets. Fortunately, there are a number of companies that have assets and operations adjacent to all of SandRidge’s assets – Offshore Gulf of Mexico, the Permian, and the Mississippian – and therefore might be willing to acquire all of the assets. This would simplify the process, minimize transaction costs and ‘leakage’ of value, and maximize overall value. In addition, most buyers of the overall company would be able to eliminate almost all overhead expenses, and achieve operational cost savings as well. Therefore, value achieved in a full sale ought to be well in excess of stand-alone values.

In conclusion, we would emphasize and re-iterate that the time has come for dramatic change, and for a focus on delivering shareholder value. We continue to believe that SandRidge stock is dramatically undervalued, and that a sensible restructuring or sale of the company could provide enormous upside for shareholders. It is our hope that the Board and management will take steps necessary to restructure the company and explore all options to maximize value for shareholders. However, in the event that is not the case, we remain determined and prepared to take actions necessary to ensure that the right steps are taken.

We remain hopeful that management will focus on delivering value, and not on defending themselves. In that instance, we remain open to constructive dialogue. In the alternative, we will proceed steadily to exercise the rights to which we are entitled by the company charter and bylaws, and by common sense, and sensible corporate governance.

Sincerely,

Founder and CEO

TPG-Axon Capital

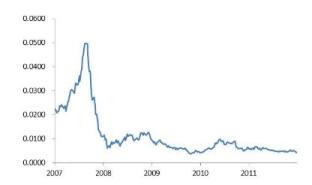

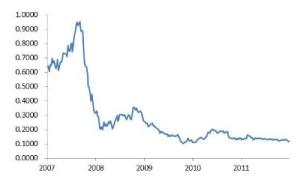

Appendix 1: Stock Performance since IPO

Absolute Stock Price Performance

Relative Stock Price Performance vs. S&P 500

Relative Stock Price Performance vs. Peers (XOP Equity)

Source: Bloomberg

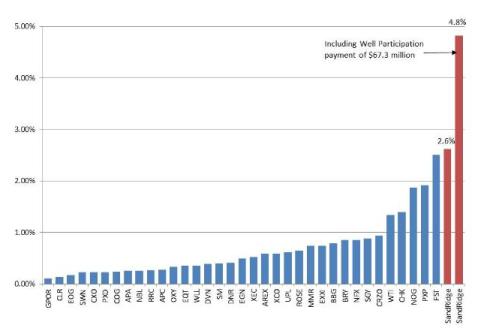

Appendix 2: CEO Compensation

2008-2011 CEO Compensation, as percentage of current market cap

Source: Bloomberg

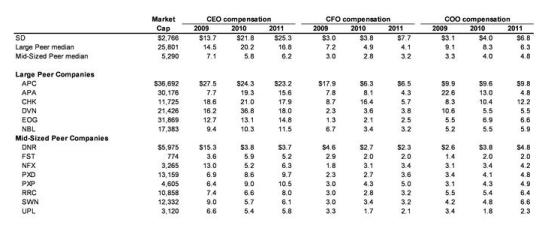

Appendix 3: Management Compensation

Source: Bloomberg