UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended: June 30, 2015

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______________ to _______________

Commission file number: 000-54303

Li3 Energy, Inc.

(Exact name of registrant as specified in its charter)

| Nevada | 20-3061907 |

| (State or other jurisdiction of | (IRS Employer Identification No.) |

| incorporation or organization) | |

| Matias Cousiño 82 | |

| Oficina 806 | |

| Santiago | |

| Chile | |

| (Address of principal executive offices) | (Zip Code) |

| Registrant’s telephone number, including area code | +(56) 2-2206 5252 |

| Securities registered under Section 12(b) of the Act: | None |

| Securities registered under Section 12(g) of the Act: | Common Stock, $0.001 par value per share |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a smaller reporting company. See the definitions of the “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer ¨ | Accelerated Filer ¨ |

| Non-Accelerated Filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

On December 31, 2014, the last business day of the registrant’s most recently completed second fiscal quarter, 261,272,692 shares of its common stock, par value $0.001 per share (its only class of voting or non-voting common equity), were held by non-affiliates of the registrant. The aggregate market value of such shares was approximately $3,919,090, based on the price at which the registrant’s common stock was last sold at such time (i.e. $0.015 per share on December 31, 2014). For purposes of making this calculation, shares beneficially owned at such time by each executive officer and director of the registrant and by each beneficial owner of greater than 10% of the voting stock of the registrant have been excluded because such persons may be deemed to be affiliates of the registrant. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of November 6, 2015, there were 483,291,849 shares of the registrant's common stock, par value $0.001, issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

TABLE OF CONTENTS

| 2 |

Various statements in this Annual Report, including those that express a belief, expectation or intention, as well as those that are not statements of historical fact, are “forward-looking statements.” The forward-looking statements may include projections and estimates concerning the timing and success of specific projects, revenues, income and capital spending. Forward-looking statements are often (but not always) accompanied by words such as “believe,”“intend,”“expect,”“seek,”“may,”“should,”“anticipate,”“could,”“estimate,”“plan,”“predict,”“project,”“target,”“goal,”“objective” or other similar expressions. These statements are likely to address our growth strategy, financial results and exploration and development programs, among other things.

Forward-looking statements are subject to risks and uncertainties that may change at any time. The forward-looking statements contained in this Annual Report are largely based on our expectations, which reflect many estimates and assumptions made by our management. These estimates and assumptions reflect our best judgment based on currently known market conditions and other factors. Although we believe such estimates and assumptions are reasonable, we caution that it is very difficult to predict the impact of known factors and it is impossible for us to anticipate all factors that could affect our actual results. In addition, management’s assumptions about future events may prove to be inaccurate. Management cautions all readers that the forward-looking statements contained in this Annual Report are not guarantees of future performance, and we cannot assure any reader that such statements will be realized or the forward looking events and circumstances will occur. There are a number of risks, uncertainties and other important factors that could cause our actual results to differ materially from those anticipated or implied in the forward-looking statements, including, but not limited to, those described in the “Risk Factors” section and elsewhere in this Annual Report.

All forward-looking statements are based upon information available to us on the date of this Annual Report. Except as otherwise required by the federal securities laws, we disclaim any obligations or undertaking to publicly release any updates or revisions to any forward-looking statement contained in this Report to reflect any change in our expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based.

| 3 |

| ITEM 1. | BUSINESS |

Corporate Summary

Li3 Energy, Inc., (“Li3,” “Li3 Energy”, “the Company” “we,” “our” or “us”) was incorporated under the laws of the state of Nevada on June 24, 2005. We are an exploration company in the lithium and potassium mining sector, based in South America. Our common stock is currently quoted on the OTCQB. We aim to acquire and develop a unique portfolio of lithium and potassium brine projects in the Americas. We are currently focused on further exploring, developing and commercializing our 49% interest in the Maricunga Project (as defined below), located in the northeast section of the Salar de Maricunga in Region III of Atacama in northern Chile, as well as increasing our portfolio of projects. The “Maricunga Project” refers to a lithium and potassium exploration project consisting of two adjacent properties covering an aggregate of 1,888 hectares: a 60% interest in Sociedades Legales Mineras Litio 1 a 6 de la Sierra Hoyada de Maricunga (“SLM Litio 1-6”), and a 100% interest in a group of exploitation mining concessions named Cocina 19 through 27 (the “Cocina Mining Concessions”). To the best of our knowledge, the Maricunga Project is the only advanced exploration stage lithium and potassium project within the Salar de Maricunga, the second largest lithium-bearing salt brine deposit in Chile. We plan to continue exploring other synergistic opportunities to further augment and strengthen this property and our land portfolio throughout the region. We are seeking to be a low cost producer of lithium, potash and other mineral products.

Our goals are to: a) advance our portfolio of projects to the feasibility study stage; b) support the global implementation of clean and green energy initiatives; c) meet growing lithium market demands; and d) become a mid-tier, low cost secondary supplier of lithium, potassium, and other strategic minerals, serving global clients in the energy, fertilizer and specialty chemical industries.

All of our mineral rights in the Maricunga Project are held by Minera Li Energy SpA (“Minera Li”), of which the Company holds a 49% ownership interest. The controlling interest in Minera Li (51%) is held by a private Chilean company, BBL SpA (“BBL”). Pursuant to the Shareholders Agreement with BBL, BBL has agreed to provide funding for our share of the development of the Maricunga Project until construction permits are in place.

In Chile, the Chilean Organic Law on Mining Concessions (“LOCM”) and the Chilean Mining Code (“CMC”) provide that lithium may not be granted in a mining concession initiated after January 1, 1979. As a result, only mining exploitation concessions initiated before January 1, 1979 are authorized for the exploitation of lithium. For all other cases, the CMC establishes the reserve of lithium to Chile and expressly provides that the exploration or exploitation of “non-concessible” substances (including lithium) can be performed only directly by the State of Chile, or its companies, or by means of administrative concessions or special operation contracts, fulfilling the requirements and conditions set forth by the President of Chile for each case. As a result, Minera Li is currently authorised to exploit lithium from the Cocina Mining Concessions but not from SLM Litio 1-6.

However, in June 2014, Chile´s President and Minister of Mining signed a decree for the establishment of the National Lithium Commission, with the objective of recommending a new state policy for the exploitation of lithium and promotion and development of new projects in Chile. In January 2015, the National Lithium Commission issued its report and, as a result, the Chilean government is to consider working alongside companies from the private sector to develop the country's lithium reserves, increase production and secure the long-term sustainability of Chile's lithium industry. This is a positive step forward in Minera Li´s continued efforts of seeking a permit to exploit lithium from SLM Litio 1-6. Minera Li continues to seek a permit for SLM Litio 1-6, however, if no permit for lithium exploitation is acquired, Minera Li plans to develop and exploit potassium from this property.

The current market environment is showing attractive valuations for advanced lithium projects, and due to our execution of the Maricunga Project and our regional/market knowledge, we believe that we are uniquely positioned to identify and execute on certain of these opportunities. We have been actively reviewing opportunities with low-cost, high-quality deposits in an advanced exploration stage that are located mainly in Chile, Argentina, and North America.

Through our strategic partner, POSCO Canada, Ltd. (“POSCAN”), a wholly-owned subsidiary of POSCO (NYSE: PKX), we have been evaluating the use of advanced process technologies that may further improve upon the economics and shorten the commercial production timeline of Minera Li´s Maricunga Project, of which we retain a 49% interest. These technologies have been evaluated by POSCO in a pilot test facility, proving effective when measured against the conventional lithium and potassium commercialization process.

According to the signumBOX Performance Index published in January 2015, SLM Litio 1-6 is ranked as the fourth best undeveloped lithium project in the world out of 37 other brine salars, subject to obtaining lithium exploitation permits. SLM Litio 1-6 is the highest ranked undeveloped lithium brine project in Chile and after Atacama, the Salar de Maricunga has the second highest quality deposit of lithium in Chile.

| 4 |

During the period from May 2011 to April 2013, our key activities were as follows:

| · | Completed acquisition of 60% Controlling Interest in SLM Litio1-6, which established the Maricunga Project. |

| · | Strategic Partnership with POSCAN, which established, among other things, an $18 million Exploration and Development program for SLM Litio 1-6. |

| · | Completed $8 million funding tranche with POSCAN and launched $8 million Phase One Exploration Plan on SLM Litio 1-6. |

| · | Issued a technical report validating our lithium and potash exploration campaign at SLM Litio 1-6 and recommending the project to advance to the feasibility study stage. |

| · | Completed a $10 million funding tranche from POSCAN. |

| · | Formed a consortium (Li3 Energy, POSCO, Mitsui, Daewoo) to bid on auction for lithium exploitation permit on SLM Litio 1-6. |

| · | Participated in a government auction for a lithium exploitation permit (CEOL) for SLM Litio 1-6, for which we were unsuccessful. The CEOL process was subsequently cancelled by the Chilean government. |

| · | Received approval of Environmental Impact Declaration for SLM Litio 1-6. This approval allows us to advance the development of SLM Litio 1-6 toward a feasibility study. |

| · | Acquired the Cocina Mining Concessions for a purchase price of $6.3 million, which Cocina Mining Concessions do not require a special permit to exploit lithium. |

During January 2014, the Company executed the BBL Transaction pursuant to which BBL SpA acquired 51% of Minera Li, with Li3 retaining 49% ownership.

We believe that if Minera Li is successful in advancing the Maricunga Project through the exploration and feasibility study stage, obtains the necessary Chilean government approvals/licenses, closes and acquires additional land acreage to support further development of the Maricunga Project, achieves a definitive feasibility study, and raises the necessary capital, Minera Li could begin commercial production and generate revenues within the next 5-7 years. However, there can be no assurance that it will achieve its stated objectives.

We are led by a management team with extensive exploration, mining, minerals, finance and commercialization expertise, and a Board of Directors who have advised, led and operated numerous mining entities. They are supported by an experienced technical team, many of whom have worked on other junior lithium projects. The Li3 management team comprises three of the seven Board members advising on the development of the Maricunga Project.

We have never generated revenues from operations and currently do not expect to generate any such revenues in the near term.

Strategic Plan

Our objective is to become an integrated chemical company through the strategic acquisition and development of lithium and potassium assets, as well as other assets that have by-product synergies. Part of our strategic plan is to ensure Minera Li explores and develops the existing Maricunga Project while simultaneously identifying other synergistic opportunities with new projects with production potential that could also be advanced in an accelerated manner, with the goal of becoming a company with valuable lithium, potassium and other industrial minerals properties. Our primary objective is to become a low cost lithium and potash producer utilizing improved technologies for the extraction of lithium and potash from brines.

Some of the actions we have taken in striving to achieve our objective are as follows:

Advancement of the Existing Maricunga Project

Along with our strategic partner BBL, we are fully committed to advancing the Maricunga Project to the stage of full permitting, including environmental, social, and construction permits, and all other studies required on the project, to internationally recognized standards (the "Project Milestone"). To enable this, BBL has committed to financing our share of the exploration expenses until the Project Milestone is achieved.

During the year ended June 30, 2015, a preliminary work program was carried out on the Maricunga Project including preparation of a closure plan and relevant approvals, preparation and permitting of a new Declaration de Impacto Ambiental (“DIA”), geophysical surveys, initiation of baseline monitoring programs and pumping test program on existing production wells. The results of the testing are expected during the last quarter of 2015.

The Company continues to pursue joint venture opportunities within the Salar de Maricunga. BBL has also acquired options to buy additional mining properties within the Salar in order to consolidate its property holdings within the Salar de Maricunga. We also continue to negotiate with the Chilean government regarding permitting for exploitation of lithium and have been part of the discussions with the National Lithium Commission for a joint effort between state and private companies to develop a lithium project within Chile.

| 5 |

In March 2013, POSCO announced that it had developed a chemical lithium extraction technology that reduces recovery time from around 12 months to less than a few days. Testing of this technology showed that it increases the lithium recovery rate from a maximum of 50% using traditional evaporation ponds to more than 80%, and the lithium carbonate produced is more than 99.9% pure. Minera Li plans to assess the use of this technology to gain efficiencies in exploiting lithium from the Maricunga Project.

In January 2015, initial test results from POSCO´s demonstration plant located in the Cauchari-Olaroz salar in Argentina indicated that the Direct Lithium Extraction Process achieved or exceeded all performance targets and that the lithium products subsequently processed were of very high quality. During a one month period, over 20 tonnes of lithium phosphate was produced from the demonstration plant and subsequently exported to POSCO’s facility in Pohang, Korea where it was further processed into battery grade lithium carbonate and lithium hydroxide.

Identifying other opportunities with new projects

The current market environment is showing attractive valuations for advanced lithium projects, and due to our execution of the Maricunga Project and our regional/market knowledge, we believe that we are uniquely positioned to identify and execute on certain of these opportunities. We have been actively reviewing opportunities with low-cost, high quality deposits in an advanced exploration stage that are located mainly in Chile, Argentina and North America.

Strategic Partners

BBL

BBL is a private Chilean Corporation with an objective to advance a business in the production of lithium. BBL is controlled by a Chilean entrepreneur.

On January 27, 2014, the Company entered into the BBL Transaction, pursuant to which BBL acquired 11 of our 60 shares of Minera Li for a cash payment of $1,500,000 and Minera Li issued 40 Additional Shares to BBL in exchange for a cash payment of $5,500,000. As a result of the BBL Transaction, BBL became the majority shareholder of Minera Li with a 51% interest, and the Company retains a 49% interest in Minera Li.

Concurrent with the execution of the BBL Transaction, the Company and BBL also entered into a Shareholders Agreement regarding their joint ownership interest of Minera Li (the “Shareholders Agreement”). Under the Shareholders Agreement, BBL will pay $1,000,000 (the “Additional Payment”) to the Company upon the earlier of (i) its completion of certain Project Milestones relating to the permitting and development of the Maricunga Project and (ii) January 27, 2016.

Under the Shareholders Agreement, BBL agreed to finance the Company’s exploration and development expenses until the Maricunga Project reaches full permitting and is ready for construction, by providing loans due 24 months from receipt at an interest rate of 12% per annum. The loans will be secured by the Company’s ownership interest in Minera Li. Specific limits for these loans have not been established and will be negotiated in good faith between BBL and the Company. To date, the Company has not received any such loans.

In addition to the foregoing financing, BBL also committed to provide the Company with a line of credit (the “BBL Credit Facility”) in the amount of $1,800,000 (the “Maximum Amount”) to be used for the working capital needs of the Company. Each drawdown must be repaid within 18 months of the drawdown date, at 8.5% interest per annum. The BBL Credit Facility is secured by the Company’s ownership interest in Minera Li. As of June 30, 2015 and 2014, the Company has received $1,220,000 and $240,000, respectively, under the BBL Credit Facility, as follows:

| Agreement Date | June 30, 2015 | June 30, 2014 | ||||||

| May 27, 2014 | $ | 100,000 | $ | 100,000 | ||||

| June 11, 2014 | 140,000 | 140,000 | ||||||

| July 23, 2014 | 200,000 | - | ||||||

| August 27, 2014 | 200,000 | - | ||||||

| October 21, 2014 | 200,000 | - | ||||||

| November 25, 2014 | 180,000 | - | ||||||

| February 3, 2015 | 200,000 | - | ||||||

| Total | 1,220,000 | 240,000 | ||||||

| Current-portion of long-term notes payable to BBL | (1,020,000 | ) | - | |||||

| Long-term notes payable to BBL | $ | 200,000 | $ | 240,000 | ||||

The Company has made several requests to BBL for the remaining $580,000 payable under the BBL Credit Facility, however to date these requests have not been honored and the Company continues to negotiate with BBL regarding this matter.

| 6 |

In accordance with the Shareholders Agreement, the board of directors of Minera Li consists of four representatives from BBL and three representatives from Li3, including Li3´s Chairman and CEO. Although financial control of Minera Li lies with BBL, BBL is reliant on Li3´s expertise in the mining and lithium sectors. As such, the technical team previously responsible for the Maricunga Project remains deeply involved in its current development plans and continues to be supervised by Li3´s management and board participants.

POSCO / POSCAN

POSCO (with its subsidiaries) is a diversified company, with operations in energy, chemicals and materials and is one of the largest steel manufacturers in the world. It is publicly-listed on the NYSE and POSCO’s management possesses executive leadership, a world renowned Global Research and Development Center (RIST), a vast knowledge of lithium and other strategic minerals, and a vision to transform the methodology in how lithium is commercialized. We believe that POSCO demonstrates a unique ability to apply both intellectual and financial capital, and that a strategic partnership with POSCO would enable the Company to begin to execute its strategic plan.

On August 24, 2011, we entered into a Securities Purchase Agreement (the “SPA”) and an Investor Rights Agreement (the “IRA” and, together with the SPA, the “POSCAN Agreements”) with POSCAN pursuant to which POSCAN acquired 100,595,238 units of the Company for approximately $18 million, with each unit consisting of one share of common stock and one three-year warrant, each warrant enabling the holder to purchase one share of the Company’s common stock at an exercise price of $0.21 per share. Li3 also agreed to issue POSCAN a two-year warrant to purchase 5,000,000 shares of common stock at an exercise price of $0.15 per share (together with the warrants underlying the units, the POSCAN Warrants). All POSCAN Warrants have expired unexercised and, as of the date of this filing, shares of the Company’s common stock held by POSCAN represent 20.8% of our common stock currently issued and outstanding.

The IRA provides that Li3 will appoint a director nominated by POSCAN to our board of directors, and will continue to nominate a POSCAN-designee at each annual meeting for as long as POSCAN owns not less than 10% of the issued and outstanding shares of common stock. Dr. Uong Chon was appointed as a director on May 23, 2014, and is currently the POSCAN-designee on the Company’s board of directors.

In March 2013, POSCO announced that it had successfully completed testing of its proprietary, patented Direct Lithium Extraction Process. This process addresses the current economics and inefficiencies in the lithium market by significantly improving lithium recovery yields and shortening the time to commercial production. According to POSCO, this process includes the following benefits:

| · | Significantly reduces the use of evaporation ponds, thereby reducing capital requirements, time to market, required land footprint, and variability of production rates and quality; |

| · | Lowers processing times (from an average of 12 months under traditional methods to under 8 hours), thereby reducing working capital requirements and time to market; and |

| · | Higher lithium recoveries (increase from 40-50% under traditional methods to 70-80%), thereby enabling faster and greater recovery of lithium from the same brine resource. |

In January 2015, initial test results from POSCO´s demonstration plant located in the Cauchari-Olaroz salar in Argentina indicated that the Direct Lithium Extraction Process achieved or exceeded all performance targets and that the lithium products subsequently processed were of very high quality. During a one month period, over 20 tonnes of lithium phosphate was produced from the demonstration plant and subsequently exported to POSCO’s facility in Pohang, Korea where it was further processed into battery grade lithium carbonate and lithium hydroxide.

There can be no assurance that any agreement will be reached with POSCAN with respect to a pilot plant, a commercial plant, any further investment by POSCAN, any purchase by POSCAN of our production, or otherwise.

| 7 |

Project Overview

Maricunga Project

Location

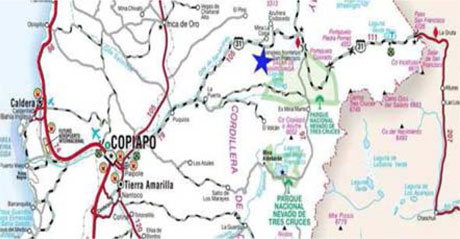

We retain a 49% interest in the Maricunga Project. The Maricunga Project consists of approximately 1,888 hectares, and is located in the northeast section of the Salar de Maricunga, the second largest lithium-bearing salt brine deposit in Chile. It consists of Minera Li´s 60% controlling interest in SLM Litio 1-6 (1,438 hectares - highlighted in blue on the map below) and the Cocina Mining Concessions (450 hectares - highlighted in green on the map below).

The Salar de Maricunga is located in Region III (Atacama region) of northern Chile at an elevation of approximately 3,750m. It is classified as a mixed type of salar of the Na-Cl-Ca/SO4 system. It is located about 180km to the north-east of Copiapo, the capital of the Atacama region, via “Carreteradel Inca” highway. As the properties are both undeveloped, at this stage there is no source of power or material plant and equipment located on the properties. Local infrastructure at the Salar de Maricunga includes National Highway 31 and an electrical power line running parallel to the highway.

Location of the Salar de Maricunga

Maricunga Project within the Salar

|

|

The area of each mining concession is:

| (a) | Litio 1- 1/29 - 130 hectares. |

| (b) | Litio 2- 1/29 - 143 hectares. |

| (c) | Litio 3- 1/58 - 286 hectares. |

| (d) | Litio 4- 1/60 - 297 hectares. |

| (e) | Litio 5- 1/60 - 300 hectares. |

| (f) | Litio 6- 1/60 - 282 hectares. |

| (g) | Cocina 19-27 - 450 hectares. |

| 8 |

SLM Litio 1-6

On May 20, 2011, Minera Li acquired 60% of SLM Litio 1-6, comprising six exploitation mining concessions granted by the Chilean government, each held by one of a group of six private companies (the “Maricunga Companies”) as follows:

| 1. | Sociedades Legales Mineras Litio 1 de la Sierra Hoyada de Maricunga |

| 2. | Sociedades Legales Mineras Litio 2 de la Sierra Hoyada de Maricunga |

| 3. | Sociedades Legales Mineras Litio 3 de la Sierra Hoyada de Maricunga |

| 4. | Sociedades Legales Mineras Litio 4 de la Sierra Hoyada de Maricunga |

| 5. | Sociedades Legales Mineras Litio 5 de la Sierra Hoyada de Maricunga |

| 6. | Sociedades Legales Mineras Litio 6 de la Sierra Hoyada de Maricunga |

The purchase price was $6,370,000 in cash, including amounts paid to agents, and 127,500,000 restricted shares of our common stock. Each mining concession grants the owner the right to explore and commercially develop any mineral deposits located at SLM Litio 1-6, with the exception of lithium. SLM Litio 1-6 were constituted subsequent to the 1979 Lithium Exploitation Restrictions. Consequently, under the current Chilean state policy, their holder is not authorized to exploit lithium in the area covered by those concessions. In June 2014, Chile´s President and Minister of Mining signed a decree for the establishment of the National Lithium Commission, with the objective of recommending a new state policy for the exploitation of lithium and promotion and development of new projects in Chile. In January 2015, the National Lithium Commission issued its report and, as a result, the Chilean government is to consider working alongside private companies in the lithium sector to develop the country's lithium reserves, increase production and secure the long term sustainability of Chile's lithium industry.

SLM Litio 1-6 are not subject to royalties or other agreements. However, Minera Li must pay annual licenses in March of each year, aggregating approximately $15,000 per year for exploration and exploitation concessions.

Cocina Mining Concessions

On April 16, 2013, Minera Li entered into an agreement to acquire the Cocina Mining Concessions. Minera Li paid $6.6 million (including a $300,000 late penalty payment) to acquire the Cocina Mining Concessions.

The Cocina Mining Concessions were constituted prior to the 1979 Lithium Exploitation Restrictions. Consequently, their holder has a constitutionally protected ownership right to exploit lithium in the area covered by those concessions. All requisite permits must be obtained prior to receipt of authorization for exploitation. Refer to the section ‘Lithium Exploitation Permitting in Chile’ below for more details about the rights to exploit lithium in Chile.

Exploration Work Performed

In December 2011, we effected a timely completion of the $8 million Phase One of our Exploration and Development Program, on our SLM Litio 1-6 concessions. We reported the initial results from brine samples taken during the sonic and reverse circulation well drilling program that was initiated in October 2011. We carried out sonic drilling for the collection of undisturbed samples from continuous core for porosity determinations and brine samples for laboratory chemical analyses. Six sonic boreholes, for a total of 900 meters, were drilled and completed to a depth of 150 meters each. We carried out reverse circulation well drilling with isolated brine sampling. A total of 884 meters of 6-inch monitoring wells were drilled and a total of 300 meters of 17 inch production wells were drilled. A total of 431 samples were taken during the drilling and were submitted to the University of Antofagasta in Antofagasta, Chile for analysis.

In May 2012, we reported the completion of a technical report on SLM Litio 1-6 prepared by Donald H. Hains, Principal of Hains Technology and Associates. The technical report demonstrates that SLM Litio 1-6 has high grades of lithium and potassium and recommended the project to advance to the feasibility study stage. The report included the following conclusions and recommendations:

| - | Results of airlift testing and pumping tests on test trenches indicate that future brine production can be achieved through a combination of production wells and open trenches. |

| - | The analyses of brine chemistry indicate that the brine is amenable to lithium and potash recovery through conventional technology. |

| - | It is believed that through the application of proprietary technology developed by Li3’s strategic partners, lithium recovery from the brine can be significantly enhanced and may range from 45 percent to more than 70 percent. |

| - | It is the recommendation of the authors that a full feasibility study be completed for the Project. |

In March 2013, we received approval of the Environmental Impact Declaration for SLM Litio 1-6 from the Chilean Environmental Authority. This approval allows us to advance the development of SLM Litio 1-6 toward a feasibility study.

During the year ended June 30, 2015, a preliminary work program was carried out on the Maricunga Project including preparation of a closure plan and relevant approvals, preparation and permitting of a new DIA, geophysical surveys, initiation of baseline monitoring programs and a pumping test program on existing production wells. The results of the testing are expected during the last quarter of 2015.

| 9 |

Short-Term Goals for the Maricunga Project

The Minera Li Board has formed an Operations and Finance Committee which will oversee the technical work required to advance the Maricunga Project along with the financial aspects of Minera Li.

The Operations and Finance Committee has identified the short term goals to continue the program of exploration on the Maricunga Project as follows:

Stage 1 – Complete an updated technical report to include both SLM Litio 1-6 and the Cocina Mining Concessions. Works required include core drilling and pumping tests, monitoring well installations and geophysical, stratigraphic and topographic survey.

Stage 2 – Complete a Prefeasibility Study (“PFS”).

Minera Li´s technical teams have developed a work program targeted to complete stage 1, with an estimated cost of $1.8 - $2 million, of which Li3´s share will be approximately $0.9 - $1 million. As part of the work program, data will be collected for the Environmental Impact Assessment. Once the PFS is completed, Minera Li will carry out further works towards a feasibility study.

The timeline to complete this technical work on the Maricunga Project will depend on the outcome of the ongoing developments on the legislation over the exploitation of lithium in Chile. The developments have been positive with the recommendations of the National Lithium Commission in January 2015 calling for a joint effort between state and private companies to develop a lithium project within Chile. We have been in discussions to be part of this joint effort and if an agreement is reached, we will be in a position to move ahead with the final exploration and permitting on the Maricunga Project.

Lithium Exploitation Permitting in Chile

In Chile, the Chilean Organic Law on Mining Concessions (“LOCM”) and the Chilean Mining Code (“CMC”) provide that lithium may not be granted in a mining concession initiated after January 1, 1979. As a result, only mining exploitation concessions initiated before January 1, 1979 are authorized for the exploitation of lithium. For all other cases, the CMC establishes the reserve of lithium to Chile and expressly provides that the exploration or exploitation of “non-concessible” substances (including lithium) can be performed only directly by the State of Chile, or its companies, or by means of administrative concessions or special operation contracts, fulfilling the requirements and conditions set forth by the President of Chile for each case. Additionally, Law 16,319, which created the Chilean Nuclear Energy Commission (the “NEC”), provides in its Article 8 that, for reasons of national interest, any act or contract in connection with lithium will require the previous authorization of NEC (or have NEC as a party thereto). Once any such authorization is granted to an applicant, NEC is not authorized to amend it or terminate it, nor the applicant to resign it, for reasons other than those set forth in the resolution granting it.

As the constitution process of the Cocina Mining Concessions was initiated in 1937, lithium exploitation is authorized in the area covered by the Cocina Mining Concessions. However, as the constitution process of SLM Litio 1-6 was initiated in 2000, lithium exploitation is not authorized in the area covered by such concessions. All other minerals on the property are concessible and, as with any mineral exploitation in Chile, all requisite permits must be obtained.

In June 2012, the Chilean Government’s Ministry of Mining established its first ever auction for the award of lithium, production quotas and licenses (Special Lithium Operations Contracts, or “CEOL”) which would permit the exploitation of an aggregate of 100,000 tons of lithium metal (approximately 530,000 tons of lithium carbonate equivalent) over a 20 year period, subject to a 7% royalty. In September 2012, we formed a consortium consisting of Li3, POSCO, Daewoo International Corp, and Mitsui & Co. (the “Consortium”) for the purpose of participating in such CEOL auction. As required under the rules established by the Ministry of Mining, the Consortium submitted its bid for the CEOLs and in September 2012, the Company was informed that the Consortium’s bid was not the winning bid.

The Chilean government subsequently decided to invalidate the CEOL process due to an administrative error, as well as rescinding the CEOL Basis, which defined the regulations of the CEOL process. The Company submitted several appeals to the Chilean government requesting it to reconsider the invalidation and award the CEOL to the second highest bidder - the Consortium. The appeals have been rejected by the Chilean government. In June 2014, Chile´s President and Minister of Mining signed a decree for the establishment of the National Lithium Commission, tasked with recommending a new state policy for the exploitation of lithium in Chile. The recommendation was issued in January 2015, following which the Chilean government is to consider working alongside private companies in the lithium sector to develop the country’s lithium reserves, increase production and secure the long term sustainability of Chile’s lithium industry. We believe this is a positive step forward in Minera Li´s continued efforts of seeking a permit to exploit lithium from SLM Litio 1-6.

While Minera Li´s current plan for the Maricunga Project is to exploit lithium and potash from both SLM Litio 1-6 and the Cocina Mining Concessions, if no permit for lithium exploitation is obtained for SLM Litio 1-6, Minera Li plans to produce lithium carbonate and potash from the Cocina Mining Concessions in conjunction with producing potash only from SLM Litio 1-6. The technical report shows that potassium resources are available in these properties. The majority of the past and current technical work performed on the project is applicable to the production of lithium and/or potassium. Potassium exploitation does not require special permits and it is exploitable via regular mining concessions, according to the CMC. Initial estimations suggest that a potash project may be economically feasible. However, there can be no assurance that Minera Li will be able to obtain the permits necessary to exploit any minerals that it discovers in a timely manner or at all.

| 10 |

Other Permits

Our operations, and that of Minera Li, are subject to numerous Chilean and international laws and regulations governing the operation and maintenance of our facilities and the discharge of materials into the environment or otherwise relating to environmental protection. These laws and regulations may:

| · | Require that we acquire the relevant permits before commencing extraction operations; |

| · | Restrict the substances that can be released into the environment in connection with mining and extraction activities; |

| · | Limit or prohibit mining activities on protected areas such as wetland or wilderness areas; and |

| · | Require remedial measures to mitigate pollution from former operations, such as dismantling abandoned production facilities. |

Companies must meet, maintain and abide by strict environmental regulations in accordance with Chilean and international laws and regulations. We will also have to abide and comply with national labor laws that protect and govern our employees. We believe that between our management team, our consultants and the experts we have hired, we will be able to satisfy any and all regulatory and compliance requirements. We are unable to assess the cost of complying with all of the regularity requirements at this stage, however, non-compliance may result in us or Minera Li being unable to continue exploration, construction or operation of a mine.

Competition

We are a junior mineral resource exploration company that competes with other mineral resource exploration companies for financing, personnel and equipment and for the acquisition of mineral properties. Many of the mineral resource exploration companies with whom we compete have greater financial and technical resources than those available to us. Accordingly, these competitors may be able to spend greater amounts on acquisitions of mineral properties of merit, on exploration of their mineral properties and on development of their mineral properties and on exploration and development. This competition could result in competitors having mineral properties of greater quality and interest to prospective investors who may finance additional exploration and/or development. This competition could adversely impact on our ability to finance further exploration and to achieve the financing necessary for us to develop our mineral properties. Our competition includes companies such as Pure Energy Minerals, Western Lithium and Lithium Americas.

Compliance with Government Regulation

We are committed to complying with and are, to our knowledge, in compliance with, all governmental and environmental regulations applicable to our company and our properties. Permits from a variety of regulatory authorities are required for many aspects of mine operation and reclamation. We cannot predict the extent to which these requirements will affect our company or our properties if we identify the existence of minerals in commercially exploitable quantities. In addition, future legislation and regulation could cause additional expense, capital expenditure, restrictions and delays in the exploration of our properties.

Employees

At June 30, 2015, we had three full-time employees, including our Chief Executive Officer and Chief Financial Officer, and one contract employee. In addition, we engage several advisors and consultants.

We engage contractors from time to time to consult with us on specific corporate affairs or to perform specific tasks in connection with our exploration programs.

Subsidiaries

We currently have three wholly owned subsidiaries:

| 1. | Li3 Energy Peru SRL, a private limited company organized under the laws of Peru; |

| 2. | Alfredo Holdings, Ltd., an exempted limited company incorporated under the laws of the Cayman Islands; |

| 3. | Li3 Energy Copiapó, SA, a Chilean corporation which is a subsidiary of Alfredo Holdings, Ltd.; and |

On October 22, 2014, the Company sold 60% of its shares in Noto Energy SA (“Noto”, an Argentinean corporation and a previously 100% owned subsidiary) to its CEO for proceeds of $4,245.

| 11 |

Following the BBL Transaction on January 27, 2014, we retain 49% ownership of Minera Li (previously a 100% owned subsidiary). Minera Li holds 60% ownership of SLM Litio 1-6, a group of six private companies (the “Maricunga Companies”).

Intellectual Property

We do not own, either legally or beneficially, any patent or trademark nor any material intellectual license, and are not dependent on any such rights. We have trademarked Li3 Energy, its logo and registered the domain name www.li3energy.com. We consider many of our lithium mining site evaluation, exploration and development techniques to be proprietary, and periodically evaluate whether to seek protection for any such techniques.

Lithium and Lithium Mining

Lithium is the lightest metal in the periodic table of elements. It is a soft, silver white metal and belongs to the alkali group of elements, which includes sodium, potassium, rubidium, cesium and francium. The chemical symbol for lithium is “Li,” and its atomic number is 3. Like the other alkali metals, lithium has a single valence electron that is easily given up to form a cation (positively charged ion). Because of this, it is a good conductor of both heat and electricity and highly reactive, though it is the least reactive of the alkali metals. Lithium possesses a low coefficient of thermal expansion (which describes how the size of an object changes with a change in temperature) and the highest specific heat capacity (a measure of the heat, or thermal energy, required to increase the temperature of a given quantity of a substance by one unit of temperature) of any solid element.

These properties make lithium an excellent material for manufacturing batteries (lithium-ion batteries). According to the U.S. Geological Survey’s (“USGS”) “Mineral Commodity Summaries 2014”, issued in February 2014, batteries accounted for 29% of lithium end-usage globally, and we expect demand for lithium from the battery segment to grow along with demand for such batteries. Although lithium markets vary by location, global end-usage was estimated by the USGS as follows: ceramics and glass, 35%; batteries, 29%; lubricating greases, 9%; continuous casting mold flux powders, 6%; air treatment, 5%; polymer production, 5%; primary aluminum production, 1%; and other uses, 10%. Lithium use in batteries has increased significantly in recent years because rechargeable lithium batteries are used extensively in portable electronic devices, and have been used increasingly in electric tools, electric vehicles, and grid storage applications. Lithium is extracted from solutions called brines, which are associated with evaporate deposits, as well as from spodumene (a lithium aluminum silicate), which occurs in a rock called pegmatite.

Historically, especially during the period leading up to and during World War II, lithium was designated a strategic metal, heavily used in the aircraft industry because it is light and strong. During this period, the mineral spodumene (a lithium aluminum silicate) was mined by open pit hard rock mining methods and processed to recover the lithium. During the post-war period, lithium production from the higher cost hard rock mines was replaced by the lower cost extraction of lithium from the mineral rich brines associated with evaporite deposits. Evaporite deposits occur in environments characterized by arid conditions with extremely high evaporation rates. This environment typically occurs at high altitudes, greater than 3,000 meters above sea level, so evaporite deposits occur in only a very few locations in the world, including China (the province of Qinghai and the Autonomous Region of Tibet); the Puna Plateau, a high altitude plateau covering part of Argentina, Chile, Bolivia and the southern portion of Peru; and in a small region in Nevada, which is the core of what is called the Great Basin of the western United States.

Brine extraction (mining) and the recovery of lithium and other economic compounds is analogous to pumping water from an aquifer, but instead of fresh water, the water contains a variety of mineral salts in solution, including lithium, potassium (K), magnesium (Mg) and sodium (Na). This form of “mining” is much more efficient, cost effective and environmentally friendly than open pit mining. However, the processing cost of brine extraction can vary by a wide range, depending largely on:

| · | lithium concentration in the particular brine; |

| · | evaporation rates at the site, which determine how quickly the brine can be concentrated; and |

| · | the balance of other minerals in the brine, which affects the degree of processing needed to remove impurities. |

Ideal Brine Conditions

The most important metrics when evaluating lithium brine resources are:

| 1) | lithium content; |

| 2) | evaporation rate; |

| 3) | magnesium to lithium ratio; |

| 4) | potassium content; and |

| 5) | sulphate to lithium ratio. |

The lithium concentration in the brines is typically measured in parts per million (ppm) or weight percentages. A high lithium concentration is most desirable. However, high local evaporation rates can compensate for lower lithium concentrations.

| 12 |

Providing that lithium contents are high enough, the magnesium to lithium (Mg:Li) ratio is another important chemical feature in assessing favorable brine chemistry and the ultimate economic viability of a site at an early stage. The lower the ratio the better, as a high ratio means that, during the evaporation process, an increasing amount of lithium will be trapped (“entrained”) in the magnesium salts when they crystallize early. This will ultimately lead to a lower lithium recovery rate and thus less profitability. High Mg:Li ratios also generally mean that more soda ash (Na 2 CO 3) reagent is required during the processing of the brine and, therefore, may add significantly to costs.

The potassium (K) concentration in the brines is typically measured as a weight percentage.

The lower the sulphate (SO4) to lithium ratio in the final lithium brine pond, the more the brine will be amenable to lithium extraction via the conventional solar evaporation process. This is because lithium sulphate (Li 2 SO 4) is highly soluble and so, to the extent that it is able to form, the lithium recovery will suffer.

Brine Exploration Phases

The life cycle of a brine mining operation can be divided into five phases:

| · | Mining activity begins with the “exploration phase,” in which one seeks to define the type, extent, location and value of deposits and to estimate the grade and size of the deposits; |

| · | The “feasibility phase” then ensues to address the financial viability of the project (including any permitting requirements) and to determine whether or not to proceed to development - the end of the feasibility stage is marked by the conclusion of a feasibility study; |

| · | If the decision is made to move forward after the feasibility stage, then the “development phase” follows, in which the infrastructure needed to begin operations is constructed; |

| · | Upon completion of such infrastructure, a project enters the “production phase,” during which the applicable minerals are extracted, produced and sold; |

| · | Once all economically extractable minerals have been produced, a mine is closed and it enters the “reclamation phase,” in which the area is made suitable for future uses. |

The Maricunga Project is currently in the exploration phase, seeking to define the type, extent, location and value of deposits.

Key Stages of Lithium Recovery

Currently the most economical way to recover lithium from a salar (a dry lake or salt flat) is by solar evaporation. However, the process is subject to natural conditions, and the evaporation rate, relative humidity, wind velocity, temperature and brine composition have a tremendous influence on the solar pond requirements and in turn on pumping and settling rates to meet production quotas.

Each lithium recovery process has a unique design based on the concentrations of Li, Na, K, Mg, calcium (Ca) and SO4 in the brine, and, although there may be some similarities, each salar has its own customized methodology for optimum recovery due to the varying ionic concentrations. Wells are drilled, and the mineral rich brine is pumped to the surface into a series of large shallow ponds of increasing concentration. As water evaporates, the concentration of minerals in solution increases. Typically the brine evaporates over an 18-24 month period until it has a sufficient concentration of lithium salts. At that point, the concentrate is shipped by truck or pipelined to processing plants where it is converted to usable salt products. In the plant, sodium carbonate (soda ash) is added to precipitate lithium carbonate, which is dried and shipped to end users to be further processed into pure lithium metal. The by-products such as potassium chloride (potash), sodium borate (borax) and other salts may also be recovered and sold to end users.

The primary reagents used to produce lithium from brine are lime and soda ash. Both substances are natural materials, commonly used in many processes and have no detrimental environmental effect when used properly. Other than solar energy, only minor amounts of fuels are consumed in the production process (pumping the brines into the ponds, etc.).

Global Market

Based on the most recent available information from the United States Geological Survey (“USGS”) issued in January 2015, worldwide lithium production increased by about 6% in 2014. According to the report, production from Argentina and Chile increased approximately 15%, each in response to increased lithium demand for battery applications, and lithium production in Australia and China increased by approximately 2.5%. Major lithium producers expected worldwide consumption of lithium in 2014 to be approximately 33,000 tons, an increase of 10% from that of 2013. Lithium prices, on average, remained flat owing to the near balanced increase in worldwide lithium consumption and supply. Several brine operations were under development in Argentina, Bolivia, and Chile; spodumene mining operations were under development in Australia, Canada, China, and Finland; and a jadarite mining operation was under development in Serbia. Additional exploration for lithium continued, with numerous claims having been leased or staked worldwide.

| 13 |

Subsurface brines have become the leading raw material for lithium carbonate production worldwide because of lower production costs compared with the mining and processing costs for hard-rock ores. Owing to growing lithium demand from China in the past several years, however, mineral-sourced lithium regained market share and was estimated to account for one-half of the world’s lithium supply in 2014. Two brine operations in Chile and a spodumene operation in Australia accounted for the majority of world production. Argentina produced lithium carbonate and lithium chloride from brines. China produced lithium carbonate, lithium chloride, and lithium hydroxide from domestic brines and, increasingly, domestic and imported spodumene. In the United States, the brine operation in Nevada doubled production capacity in 2013. A new brine operation in Argentina was expected to be commissioned by year end 2014. Lithium minerals were used directly as ore concentrates in ceramics and glass applications worldwide,

Recent years have seen consolidation among the handful of major lithium producers. In 2013, China’s leading lithium chemical producer acquired Australia’s leading spodumene producing facility, having a capacity of 110,000 tons per year of lithium carbonate equivalent. In 2014, the United States-based parent company of one of Chile’s brine operations acquired 49% of the Australian spodumene operation from the Chinese chemical producer, and effectively became the world’s leading lithium producer. Later in 2014, a U.S. bromine products manufacturer agreed to purchase the U.S. lithium producer for $6.2 billion to create one of the world’s largest specialty chemicals businesses.

Rechargeable batteries were the largest potential growth area for lithium compounds. Demand for rechargeable lithium batteries exceeds that of other rechargeable batteries. Automobile companies were developing lithium batteries for electric and hybrid electric vehicles. A leading electric car manufacturer announced plans to construct an immense lithium-ion battery plant in the United States capable of producing up to 500,000 lithium-ion vehicle batteries per year by 2020. The plant was expected to be vertically integrated, capable of producing finished battery packs directly from raw materials.

According to the USGS, Australia and Chile are the leading lithium producers in the world. China, Argentina and the United States are also major producers. The 2015 edition of the USGS Mineral Commodity Summaries gives the following estimated world lithium mine production (in metric tons of lithium content):

| Mine production | ||||||||

| 2014 (est.) | 2013 | |||||||

| Australia | 13,000 | 12,700 | ||||||

| Chile | 12,900 | 11,200 | ||||||

| China | 5,000 | 4,700 | ||||||

| Argentina | 2,900 | 2,500 | ||||||

| Zimbabwe | 1,000 | 1,000 | ||||||

| Portugal | 570 | 570 | ||||||

| Brazil | 400 | 400 | ||||||

| United States (1) | Withheld | 870 | ||||||

| World total (rounded) | 36,000 | 1 | 34,000 | 1 | ||||

| (1) | Excludes U.S. production. |

Substitution for lithium compounds is possible in batteries, ceramics, greases, and manufactured glass. Examples are calcium and aluminum soaps as substitutes for stearates in greases; calcium, magnesium, mercury, and zinc as anode material in primary batteries; and sodic and potassic fluxes in ceramics and glass manufacture. Lithium carbonate is not considered to be an essential ingredient in aluminum potlines. Substitutes for aluminum-lithium alloys in structural materials are composite materials consisting of boron, glass, or polymer fibers in engineering resins.

Demand for Lithium

According to the January 2015 signumBOX Performance Index, Global lithium demand is expected to grow at a base rate of 13% in 2015 from 2014 rates. The increase in the growth rate is due primarily to an increase in demand from the battery industry. signumBOX forecast that lithium demand in the following five years will grow at an average rate of about 7.6% annually, and then will start to grow faster as the developments of hybrid and electric vehicles allow them to be more affordable.

Additional Information

The Company files annual, quarterly and current reports, proxy statements and other information with the SEC. The public may inspect or copy these materials at the Public Reference Room at the SEC at 100 F Street, N.E., Washington, D.C. 20549, and can obtain information of the operation of the Public Reference Room by calling the Commission at 1-800-SEC-0330. Our public filings are also available from the SEC’s website at www.sec.gov.

| 14 |

| ITEM 1A. | RISK FACTORS |

THIS ANNUAL REPORT ON FORM 10-K CONTAINS CERTAIN FORWARD-LOOKING STATEMENTS. YOU ARE CAUTIONED THAT SUCH STATEMENTS ARE ONLY PREDICTIONS AND ARE SUBJECT TO VARIOUS RISKS AND UNCERTAINTIES, MANY OF WHICH WE CANNOT CONTROL OR PREDICT. ACTUAL EVENTS OR RESULTS MAY DIFFER MATERIALLY FROM THOSE EXPRESSED OR IMPLIED BY FORWARD-LOOKING STATEMENTS. IN EVALUATING SUCH STATEMENTS, YOU SHOULD SPECIFICALLY CONSIDER, AMONG OTHER THINGS, THE VARIOUS FACTORS IDENTIFIED IN THIS ANNUAL REPORT ON FORM 10-K, INCLUDING THE MATTERS SET FORTH BELOW. IF ANY OF THE FOLLOWING RISKS ACTUALLY OCCURS, THEN OUR BUSINESS, PROSPECTS, FINANCIAL CONDITION AND RESULTS OF OPERATIONS COULD BE MATERIALLY ADVERSELY AFFECTED.

RISKS RELATED TO OUR BUSINESS AND FINANCIAL CONDITION

We are in the exploration stage and our planned principal operations have not commenced. Currently we have no revenues. Our business plan depends on our ability to explore for and develop mineral reserves and place any such reserves into extraction. Because we have a limited operating history, it is difficult to predict our future performance.

Although we were formed in June 2005, we continue to be in the exploration stage. Therefore, we have limited operating and financial history available to help potential investors evaluate our past performance and the risks of investing in us. Moreover, our limited historical financial results may not accurately predict our future performance. Companies in their initial stages of development present substantial business and financial risks and may suffer significant losses. As a result of the risks specific to our new business and those associated with new companies in general, it is possible that we may not be successful in implementing our business strategy.

We have generated no revenues to date and do not anticipate generating any revenues in the near term. Our activities to date have been limited to capital formation, organization, acquisition of interests in mining properties and limited exploration on the Maricunga Project, of which we currently hold a minority interest. We have yet to generate positive earnings and there can be no assurance that we will ever operate profitably. Our success is significantly dependent on a successful exploration, mining and production program. Our operations will be subject to all the risks inherent in the establishment of a developing enterprise and the uncertainties arising from the absence of a significant operating history. We may be unable to locate exploitable quantities of mineral resources or operate on a profitable basis. We are in the exploration stage and potential investors should be aware of the difficulties normally encountered by enterprises in the exploration stage. If our business plan is not successful, and we are not able to operate profitably, investors may lose some or all of their investment in our Company.

There is doubt about our ability to continue as a going concern.

The consolidated financial statements contained herein have been prepared assuming we will continue as a going concern. At June 30, 2015, we had no source of current revenue, had a cash balance of $6,217 and negative working capital of $881,467.

Pursuant to the terms of the BBL Transaction and the Shareholders Agreement with BBL, the Company has access to the following sources of funding:

| · | Li3 Energy will receive $1,000,000 upon the earlier of completion of certain Maricunga Project milestones, or January 27, 2016. |

| · | BBL has provided the Company with the BBL Credit Facility of $1,800,000 for working capital. The loans are secured by the Company’s ownership interest in Minera Li. Repayment of each drawdown is 18 months from the drawdown date, at 8.5% interest per annum. As of the date of this filing, the Company has received $1,220,000 under the BBL Credit Facility. The Company has made several requests to BBL for the remaining $580,000 payable under the BBL Credit Facility, however to date these requests have not been honored and the Company continues to negotiate with BBL regarding this matter. |

| · | BBL will finance Li3 Energy´s share of exploration expenses on the Maricunga Project to the stage of full permitting including environmental, social, and construction, and all studies related to the Maricunga Project to internationally recognized standards. The loans will be due 24 months from receipt and interest will be charged at 12% per annum. Specific limits for these loans have not been established and will be negotiated in good faith between the Company and BBL. |

The Company’s current negative working capital position is not sufficient to maintain its basic operations for at least the next 12 months.

We have sustained and continue to sustain losses as a result of our operations and cannot predict if and when we may generate profits. In the event we identify commercial reserves of lithium or other minerals, it will require substantial additional capital to develop those reserves. We expect to finance our operations primarily through future equity or debt financing. However, as discussed in the notes to our consolidated financial statements included elsewhere in this Report, there exists substantial doubt about our ability to continue as a going concern because there is no assurance that we will be able to obtain such capital, through equity or debt financing, or any combination thereof, on satisfactory terms or at all. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Mineral operations are subject to applicable law and government regulation, which could restrict or prohibit the exploitation of that mineral resource.

Both mineral exploration and extraction in Chile require obtaining mining concessions as well as permits from various foreign, federal, state, provincial and local governmental authorities, as the case may be, and are governed by laws and regulations, including those with respect to prospecting, mine development, mineral production, transport, export, taxation, labor standards, occupational health, waste disposal, toxic substances, land use, environmental protection, mine safety and other matters. There can be no assurance that we will be able to obtain or maintain any of the mining rights and permits required for the continued exploration of mineral properties or for the construction and operation of a mine on its properties (especially but not limited to extracting lithium) nor that it will be able to obtain or maintain any of such rights and permits at economically viable costs.

| 15 |

In Chile, the Chilean Organic Law on Mining Concessions (“LOCM”) and the Chilean Mining Code (“CMC”) provide that lithium may not be granted in a mining concession initiated after January 1, 1979. As a result, only mining exploitation concessions initiated before January 1, 1979 are authorized for the exploitation of lithium. For all other cases, the CMC establishes the reserve of lithium to Chile and expressly provides that the exploration or exploitation of “non-concessible” substances (including lithium) can be performed only directly by the State of Chile, or its companies, or by means of administrative concessions or special operation contracts, fulfilling the requirements and conditions set forth by the President of Chile for each case. Additionally, Law 16,319, which created the Chilean Nuclear Energy Commission (the “NEC”), provides in its article 8 that, for reasons of national interest, any act or contract in connection with lithium will require the previous authorization of NEC (or have NEC as a party thereto). Once any such authorization is granted to an applicant, NEC is not authorized to amend it or terminate it, nor the applicant to resign it, for reasons other than those set forth in the resolution granting it. The Chilean government is currently reviewing this law to allow private companies to exploit lithium.

As the constitution process of the Cocina Mining Concessions was initiated in 1937, Minera Li, as the owner of the Cocina Mining Concessions, is authorized to exploit lithium in the area covered by the Cocina Mining Concessions. However, as the constitution process of SLM Litio 1-6 was initiated in 2000, the Maricunga Companies are not authorized to exploit lithium in the area covered by such concessions, unless they also obtain a CEOL authorizing such exploitation. At the date of this report there is no assurance that the Chilean Government will begin another CEOL process.

Our option on the Alfredo Property has expired, and we may have a continuing obligation in the event we develop future iodine nitrate properties in Chile.

On August 3, 2010, we signed an agreement to acquire Alfredo Holdings, Ltd. which held an option to acquire six mining concessions in Pozo Almonte, Chile. We allowed the option to expire because we determined that the project was not economically viable. Pursuant to an amendment to our agreement with the Alfredo Sellers, if and when certain milestones are achieved with respect to any future Li3 Energy iodine nitrate project in Chile, we must make additional payments to the Alfredo Sellers in an aggregate amount of up to $5.5 million. There can be no assurance that financing sufficient to make such payments will be available to us when needed. We are not currently planning to explore, exploit or develop any iodine nitrate project in Chile.

All of the properties in which we retain an ownership interest are in the exploration stage. Investment in exploration projects increases the risks inherent in our mining activities. There is no assurance that the existence of any mineral resource can be established on any of the properties in commercially exploitable quantities, and mining operations may not be successful.

We have not established that any of the mineral properties in which we retain an ownership interest contain any meaningful levels of mineral reserves. There can be no assurance that future exploration and mining activities will be successful.

A mineral reserve is defined by the SEC in its Industry Guide 7 (which can be viewed at http://www.sec.gov/divisions/corpfin/forms/industry.html.secguide7) as that part of a mineral deposit which could be economically and legally extracted or produced at the time of the reserve determination. There can be no assurance that we will ever establish any mineral reserves.

Even if a meaningful mineral reserve is eventually discovered on one or more of the properties, there can be no assurance that the properties will be able to be developed into producing mines and that resources will be able to be extracted from those properties. Both mineral exploration and development involve a high degree of risk and few properties which are explored are ultimately developed into producing mines. Furthermore, we cannot be sure that an overall exploration success rate or extraction operations within a particular area will ever come to fruition and, in any event, production rates inevitably decline over time. The commercial viability of an established mineral deposit will depend on a number of factors including, by way of example, the size, grade and other attributes of the mineral deposit, the proximity of the resource to infrastructure such as a smelter, roads and a point for shipping, government regulation and market prices. Most of these factors will be beyond our control, and any of them could increase costs and make extraction of any identified mineral resource unprofitable.

We have limited financial resources and may not be able to fund our anticipated exploration activities. If we are unable to fund our exploration activities, our potential profitability will be adversely affected.

Our anticipated exploration activities will require financial resources substantially in excess of our current working capital. If we are not able to finance our exploration activities, then we will be unable to identify commercially exploitable resources even if present on our properties. If we fail to adequately support our exploration activities, it could have a material adverse effect on our results of operations and the market price of our shares. There can be no assurance that capital will be available to us when needed, on favorable terms or at all.

| 16 |

If the existence of a mineral resource is established in a commercially exploitable quantity on any of the properties in which we retain an ownership interest, we will require additional capital in order to finance the development of the property into a producing mine. If we are unable to obtain additional funding, our business operations will be harmed and if we do obtain additional financing, existing shareholders may suffer substantial dilution.

If mineral resources are discovered in commercially exploitable quantities on any of the properties in which we retain an ownership interest, we will be required to expend substantial sums of money to establish the extent of the resource, develop processes to extract it and develop extraction and processing facilities and infrastructure. Although we may derive substantial benefits from the discovery of a major deposit, there can be no assurance that such a resource will be large enough to justify commercial operations, nor can there be any assurance that we will be able to raise the funds required for development on a timely basis.

Pursuant to the Shareholders Agreement, BBL has agreed to provide funding for our share of the development of the Maricunga Project until construction permits are in place. To continue developing the property from that stage into a producing mine, we will need to fund our 49% share of the development costs or risk dilution of our 49% ownership interest. We currently do not have any contracts or firm commitments for additional financing. There can be no assurance that additional financing will be available in amounts or on terms acceptable to us, if at all. An inability to obtain additional capital would restrict our ability to grow and could diminish our ability to continue to conduct our business operations. If we are unable to obtain additional financing, we will likely be required to curtail exploration and development plans and possibly cease operations. Any additional equity financing may involve substantial dilution to then existing shareholders.

Newer battery and/or fuel cell technologies could decrease demand for lithium over time, which could significantly impact our prospects and future revenues.

Many materials and technologies are being researched and developed with the goal of making batteries lighter, more efficient, faster charging and less expensive. Some of these technologies could be successful and could impact demand for lithium batteries in personal electronics, electric and hybrid vehicles and other applications. Advances in nanotechnology, in particular, offer the prospect of significantly better batteries in the future. For example, researchers at Stanford University have recently demonstrated ultra-lightweight, bendable batteries and super capacitors made from paper coated with ink made of carbon nanotubes and silver nanowires; the material charges and discharges very quickly, making it potentially useful in hybrid and electric vehicles, which need rapid power for acceleration and would benefit from quicker charging than is available with current technologies. We cannot predict which new technologies may ultimately prove to be commercializable and on what time horizon. While lithium battery technology is currently among the best available for electronics, vehicles and other applications, commercialized battery technologies that offer superior weight, capacity, charging time and/or cost could significantly adversely affect the demand for lithium in the future and thus could significantly adversely impact our prospects and future revenues.

Mineral exploration and development is subject to extraordinary operating risks. We do not currently insure against these risks. In the event of a cave-in or similar occurrence, our liability may exceed our resources, which could have an adverse impact on us.

Mineral exploration, development and production involve many risks which even a combination of experience, knowledge and careful evaluation may not be able to overcome. Our operations will be subject to all the hazards and risks inherent in the exploration for mineral resources and, if we discover a mineral resource in commercially exploitable quantity, our operations could be subject to all of the hazards and risks inherent in the development and production of resources, including liability for pollution, cave-ins or similar hazards against which we cannot insure or against which we may elect not to insure. Any such event could result in work stoppages and damage to property, including damage to the environment. We do not currently maintain any insurance coverage against these operating hazards. The payment of any liabilities that arise from any such occurrence would have a material adverse impact on us.

Lithium and potash prices are subject to unpredictable fluctuations, making it difficult to predict the economic viability of the exploration properties and projects that we retain an ownership interest in.

We may derive revenues, if any, from income or loss from our equity investment in Minera Li or from the sale of our equity interest in Minera Li. Minera Li will derive its revenues, if any, either from the extraction and sale of lithium and potash, as well as other potentially economic salts produced from the lithium salar brines, or from the sale of its mineral resource properties. The price of these commodities may fluctuate widely, and is affected by numerous factors beyond our control, including international, economic and political trends, expectations of inflation, currency exchange fluctuations, interest rates, global or regional consumptive patterns, speculative activities, increased production due to new extraction developments and improved extraction and production methods and technological changes in the markets for the end products. The effect of these factors on the price of these minerals, and therefore the economic viability of any of Minera Li´s exploration properties and projects, cannot accurately be predicted.

The mining industry is highly competitive, and we face competition from many established global companies. We may not be able to compete effectively with these companies which may adversely affect our prospects.

The markets in which we operate are highly competitive. The mineral exploration, development, and production industry is largely un-integrated. We compete against numerous well-established national and foreign companies in every aspect of the mineral mining industry. Some of our competitors have longer operating histories and greater technical facilities, and significantly greater recognition in the market and financial and other resources, than we. We may not compete effectively with other exploration companies in locating and acquiring mineral resource properties, and customers may not buy any or all of the mineral products that we expect to produce.

| 17 |

Because we are small and have limited capital, we may have to limit our exploration and developmental mining activity which may adversely affect our prospects.

Because we are a small exploration stage company and have limited capital, we may have to limit our exploration and production activity. As such, we may not be able to complete an exploration program that is as thorough as we would like. In that event, existing reserves may go undiscovered. Without finding reserves, our ability to generate revenues and our business prospects will be adversely affected.

Compliance with environmental and other government regulations could be costly and could negatively impact production and adversely affect our operating results.