Exhibit 99.1

PENN WEST PETROLEUM LTD.

Annual Information Form

for the year ended December 31, 2013

March 6, 2014

TABLE OF CONTENTS

| Page | ||||

| GLOSSARY OF TERMS |

3 | |||

| CONVENTIONS |

4 | |||

| ABBREVIATIONS |

5 | |||

| OIL AND GAS INFORMATION ADVISORIES |

5 | |||

| CONVERSIONS |

6 | |||

| EFFECTIVE DATE OF INFORMATION |

6 | |||

| GENERAL AND ORGANIZATIONAL STRUCTURE |

9 | |||

| DESCRIPTION OF OUR BUSINESS |

10 | |||

| CAPITALIZATION OF PENN WEST |

14 | |||

| DIRECTORS AND EXECUTIVE OFFICERS OF PENN WEST |

17 | |||

| AUDIT COMMITTEE DISCLOSURES |

20 | |||

| DIVIDENDS AND DIVIDEND POLICY |

22 | |||

| MARKET FOR SECURITIES |

24 | |||

| INDUSTRY CONDITIONS |

25 | |||

| RISK FACTORS |

39 | |||

| MATERIAL CONTRACTS |

56 | |||

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS |

57 | |||

| TRANSFER AGENTS AND REGISTRARS |

57 | |||

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS |

57 | |||

| INTERESTS OF EXPERTS |

57 | |||

| ADDITIONAL INFORMATION |

58 | |||

| APPENDIX A – RESERVES DATA AND OTHER OIL AND GAS INFORMATION

|

||

| Appendix A-1 – Report of Management and Directors on Reserves Data and Other Information |

||

| Appendix A-2 – Report on Reserves Data |

||

| Appendix A-3 – Statement of Reserves Data and Other Oil and Gas Information |

||

| APPENDIX B – MANDATE OF THE AUDIT COMMITTEE | ||

2

GLOSSARY OF TERMS

The following is a glossary of certain terms used in this Annual Information Form.

“ABCA” means the Business Corporations Act (Alberta), R.S.A. 2000, C. B-9, as amended, including the regulations promulgated thereunder.

“Board” or “Board of Directors” means the board of directors of Penn West.

“Common Shares” means common shares in the capital of Penn West.

“Corporate Conversion” means the reorganization of Penn West Trust from a trust to a publicly traded exploration and production corporation, being Penn West, pursuant to a plan of arrangement completed under the ABCA effective January 1, 2011.

“Engineering Report” means the report prepared by Sproule dated January 30, 2014 evaluating approximately 75 percent and auditing approximately 25 percent of the crude oil, natural gas and natural gas liquids reserves of Penn West and the net present value of future net revenue attributable to those reserves effective as at December 31, 2013.

“Form 40-F” means our Annual Report on Form 40-F for the fiscal year ended December 31, 2013 filed with the SEC.

“Gross” or “gross” means:

| (a) | in relation to our interest in production or reserves, our “company gross reserves”, which are our working interest (operating or non-operating) share before deduction of royalties and without including any royalty interests of ours; |

| (b) | in relation to wells, the total number of wells in which we have an interest; and |

| (c) | in relation to properties, the total area of properties in which we have an interest. |

“Handbook” means the Chartered Professional Accountant Canada Handbook, as amended from time to time.

“IFRS” means International Financial Reporting Standards, being the standards and interpretations issued by the International Accounting Standards Board, as amended from time to time. The changeover date to IFRS was January 1, 2011 with retrospective adoption from January 1, 2010 onwards. For periods relating to financial years beginning on or after January 1, 2011, Canadian generally accepted accounting principles applicable to publicly accountable enterprises is determined with reference to Part I of the Handbook, which is IFRS.

“Net” or “net” means:

| (a) | in relation to our interest in production or reserves, our working interest (operating or non-operating) share after deduction of royalty obligations, plus our royalty interests in production or reserves; |

| (b) | in relation to our interest in wells, the number of wells obtained by aggregating our working interest in each of our gross wells; and |

| (c) | in relation to our interest in a property, the total area in which we have an interest multiplied by the working interest we own. |

“NI 51-101” means National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities.

“Non-Resident” means: (i) a person who is not a resident of Canada for the purposes of the Tax Act; or (ii) a partnership that is not a Canadian partnership for the purposes of the Tax Act.

3

“NYSE” means the New York Stock Exchange.

“Penn West”, “we”, “us” or “our” means: (i) subsequent to the completion of the Corporate Conversion, Penn West Petroleum Ltd., a corporation existing under the ABCA and the successor to Penn West Trust; and (ii) prior to the completion of the Corporate Conversion, Penn West Trust. Where the context requires, these terms also include all of Penn West’s Subsidiaries on a consolidated basis.

“Penn West Trust” means Penn West Energy Trust, which trust was reorganized into Penn West and terminated pursuant to the Corporate Conversion.

“SEC” means the United States Securities and Exchange Commission.

“Senior Notes” means our guaranteed, unsecured senior notes consisting of US$1,629 million principal amount of notes, Cdn$175 million principal amount of notes, £77 million principal amount of notes and €10 million principal amount of notes, all as described under the heading “Capitalization of Penn West – Debt Capital – Senior Notes”.

“Shareholders” means holders of our Common Shares.

“Sproule” means Sproule Associates Limited, independent petroleum consultants of Calgary, Alberta.

“Subsidiaries” has the meaning ascribed thereto in the Securities Act (Ontario) and, for greater certainty, includes all corporations and partnerships owned, controlled or directed, directly or indirectly, by Penn West or Penn West Trust, as the case may be.

“Tax Act” means the Income Tax Act (Canada), R.S.C. 1985, C. 1 (5th Supp.), as amended, including the regulations promulgated thereunder, as amended from time to time.

“Trust Unit” means a trust unit of Penn West Trust, all of which were exchanged for Common Shares on a one-for-one basis pursuant to the Corporate Conversion.

“TSX” means the Toronto Stock Exchange.

“undeveloped land” and “unproved property” each mean a property or part of a property to which no reserves have been specifically attributed.

“United States” or “U.S.” means the United States of America.

CONVENTIONS

Certain terms used herein are defined in the “Glossary of Terms”. Certain other terms used herein but not defined herein are defined in NI 51-101 and, unless the context otherwise requires, shall have the same meanings herein as in NI 51-101.

All dollar amounts in this document are expressed in Canadian dollars, except where otherwise indicated. References to “$” or “Cdn$” are to Canadian dollars, references to “US$” are to United States dollars, references to “£” are to pounds sterling, and references to “€” are to Euros. On March 6, 2014, the exchange rate based on the noon rate as reported by the Bank of Canada, was Cdn$1.00 equals US$0.9119.

All financial information herein has been presented in Canadian dollars in accordance with IFRS.

4

ABBREVIATIONS

| Oil and Natural Gas Liquids |

Natural Gas | |||||

| bbl | barrel or barrels | GJ | gigajoule | |||

| bbl/d | barrels per day | GJ/d | gigajoules per day | |||

| Mbbl | thousand barrels | Mcf | thousand cubic feet | |||

| MMbbl | million barrels | MMcf | million cubic feet | |||

| NGLs | natural gas liquids | Bcf | billion cubic feet | |||

| MMboe | million barrels of oil equivalent | Mcf/d | thousand cubic feet per day | |||

| Mboe | thousand barrels of oil equivalent | MMcf/d | million cubic feet per day | |||

| boe/d | barrels of oil equivalent per day | m3 MMbtu |

cubic metres million British thermal units | |||

| Other |

||||||

| BOE or boe | barrel of oil equivalent, using the conversion factor of 6 Mcf of natural gas being equivalent to one barrel of oil. | |||||

| WTI | West Texas Intermediate, the reference price paid in United States dollars at Cushing, Oklahoma for crude oil of standard grade. | |||||

| API | American Petroleum Institute. | |||||

| °API | the measure of the density or gravity of liquid petroleum products derived from a specific gravity. | |||||

| psi | pounds per square inch. | |||||

| MM$ | million dollars. | |||||

| MW | megawatt. | |||||

| MWh | megawatt hour. | |||||

| CO2 | carbon dioxide. | |||||

OIL AND GAS INFORMATION ADVISORIES

Where any disclosure of reserves data is made in this Annual Information Form (including the Appendices hereto) that does not reflect all of the reserves of Penn West, the reader should note that the estimates of reserves and future net revenue for individual properties may not reflect the same confidence level as estimates of reserves and future net revenue for all properties, due to the effects of aggregation.

All production and reserves quantities included in this Annual Information Form (including the Appendices hereto) have been prepared in accordance with Canadian practices and specifically in accordance with NI 51-101. These practices are different from the practices used to report production and to estimate reserves in reports and other materials filed with the SEC by United States companies. Nevertheless, as part of Penn West’s Annual Report on Form 40-F for the year ended December 31, 2013 filed with the SEC, Penn West has disclosed proved reserves quantities using the standards contained in SEC Regulation S-X, and the standardized measure of discounted future net cash flows relating to proved oil and gas reserves determined in accordance with the U.S. Financial Accounting Standards Board, “Disclosures About Oil and Gas Producing Activities”, which disclosure complies with the SEC’s rules for disclosing oil and gas reserves.

References in this Annual Information Form to land and properties held, owned, acquired or disposed by us, or in respect of which we have an interest, refer to land or properties in respect of which we have a lease or other contractual right to explore for, develop, exploit and produce hydrocarbons underlying such land or properties.

BOEs may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf: 1 bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. Given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency conversion ratio of 6:1, utilizing a conversion on a 6:1 basis is misleading as an indication of value.

5

CONVERSIONS

The following table sets forth certain conversions between Standard Imperial Units and the International System of Units (or metric units).

| To Convert From |

To | Multiply By | ||||

| Mcf |

cubic metres | 28.174 | ||||

| cubic metres |

cubic feet | 35.494 | ||||

| bbl |

cubic metres | 0.159 | ||||

| cubic metres |

bbl | 6.293 | ||||

| feet |

metres | 0.305 | ||||

| metres |

feet | 3.281 | ||||

| miles |

kilometres | 1.609 | ||||

| kilometres |

miles | 0.621 | ||||

| acres |

hectares | 0.405 | ||||

| hectares |

acres | 2.500 | ||||

| gigajoules (at standard) |

MMbtu | 0.948 | ||||

| MMbtu (at standard) |

gigajoules | 1.055 | ||||

| gigajoules (at standard) |

Mcf | 1.055 | ||||

EFFECTIVE DATE OF INFORMATION

Except where otherwise indicated, the information in this Annual Information Form is presented as at the end of Penn West’s most recently completed financial year, being December 31, 2013.

6

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

In the interest of providing our securityholders and potential investors with information regarding Penn West, including management’s assessment of Penn West’s future plans and operations, certain statements contained and incorporated by reference in this document constitute forward-looking statements or information (collectively “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “budget”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “objective”, “aim”, “potential”, “target” and similar words suggesting future events or future performance. In addition, statements relating to “reserves” or “resources” are deemed to be forward-looking statements as they involve the implied assessment, based on certain estimates and assumptions, that the reserves and resources described exist in the quantities predicted or estimated and can be profitably produced in the future. In particular, this document and the documents incorporated by reference herein contain, without limitation, forward-looking statements pertaining to the following: our focus on profitability and goals of growing production per share, cash flow per share and strengthening our balance sheet position; our commitment to maximizing the efficiency of our capital programs and the reliability of our production base while growing the oil and liquids weighting of our total production; our belief that our long-term plan to deleverage our balance sheet, continue operational and cost control improvements, and focus on light oil development integrated with waterflood programs concentrated in our Cardium, Slave Point and Viking plays is the best strategy available to maximize Shareholder value; the objective of our long-term plan to provide Shareholders with compound annual per share growth in oil production and funds flow subsequent to a deleveraging period and provide Shareholders with a return through a sustainable dividend; our intention to sell $1.5 to 2.0 billion of non-core assets before 2015 in order to deleverage our balance sheet; the details of the proposed disposition expected to close in mid-March 2014, including the anticipated sale proceeds, the nature of the assets and liabilities to be sold and the closing timing; the details of our 2014 exploration and development capital budget, including the amount thereof and our intention that the majority of the development capital budget will be allocated to light-oil development in the Cardium, Viking and Slave Point plays; our intention that our capital spending program will be more balanced during 2014 than in previous years, resulting in production additions weighted to the second half of 2014; our forecast average daily production for 2014 and the liquids weighting thereof; the details of our ongoing acquisition, disposition, farm-out and financing strategy; our dividend policy, including the amount of dividends that we intend to pay, the proposed timing of such payments, the factors that may affect the amount of dividends that we pay and the anticipated timing of the Board’s review of our dividend policy; the effect on the market value of the Common Share should we reduce or suspend the amount of cash dividends that we pay in the future; our expectations regarding the operational and financial impact that climate change regulations in the jurisdictions in which we operate will have on us; our belief that the trend towards heightened and additional standards in environmental legislation and regulation will continue and our expectation that we will be making increased expenditures as a result of the expansion of our operations and the adoption of new legislation relating to the protection of the environment; our assessment of the operational and financial impacts that certain risks factors could have on us and on our dividend policy and the value of our Common Shares should such risk factors materialize; the quantity of our oil, natural gas liquids and natural gas reserves, the recoverability thereof, and the net present values of future net revenue to be derived from our reserves using forecast prices and costs, including the disclosure set forth in Appendix A-3 under “Statement of Reserves Data and Other Oil and Gas Information – Reserves Data”; the amount of royalties, operating costs, development costs, abandonment and reclamation costs and income taxes that we will incur in connection with the production of our reserves; our outlook for oil, natural gas liquids and natural gas prices; our expectations regarding future currency exchange rates and inflation rates; our expectations regarding how we will fund the development costs of our reserves; our expectation that interest and other funding costs will not make the development of any of our properties uneconomic; our expectations regarding the timing for developing our proved undeveloped reserves and probable undeveloped reserves and the amount of future capital expenditures required to develop such reserves; our expectations regarding the significant economic factors and other significant uncertainties that could affect our reserves data; the number of net well bores and facilities and the length of pipeline in respect of which we expect to incur abandonment and reclamation costs and the total amount of such costs that we expect to incur and the timing thereof; the details of our exploration and development plans in each of our Cardium, Slave Point and Viking resource plays in 2014, including our key focus areas within each resource play, the details of our ongoing and proposed waterflood programs, and our pursuit of down spacing opportunities; our belief that recent results in our key plays and continuing advancements in drilling, completions and other technologies will enable us to pursue various enhanced recovery techniques aimed at increasing oil recovery rates in several of our large plays; our plans to continue to expand our existing waterflood projects and initiate others in most of our key areas; the details of our 2014 capital budget, including the amount thereof, our focus on improving capital efficiencies and profitability over short-term production, the total budget for development capital and base infrastructure improvement, the amount of the budget allocated to light-oil development, including the budgets for each of the Cardium, Viking and Slave Point plays, the allocations to longer lead time production projects, including drilling

7

wells in the Cardium and Slave Point areas and making significant investments in waterflood programs in our key areas, and the number of net wells we expect to drill; our expectation regarding when we will be required to pay income taxes; our production volume estimates for 2014; and the nature of, effectiveness of, and benefits to be derived from, our future marketing arrangements and risk management strategies.

With respect to forward-looking statements contained or incorporated by reference in this document, we have made assumptions regarding, among other things: the terms and timing of asset sales completed under our ongoing program to sell between $1.5 billion and $2.0 billion of non-core assets, including the asset sale anticipated to close in the first quarter of 2014; our ability to execute or long-term plan as described herein and the impact that the successful execution of such plan will have on us and our shareholders; the economic returns anticipated from expenditures on our assets; future crude oil, natural gas liquids and natural gas prices and differentials between light, medium and heavy oil prices and Canadian, WTI and world oil and natural gas prices; future capital expenditure levels and capital programs; future crude oil, natural gas liquids and natural gas production levels; the laws and regulations that we will be required to comply with, including laws and regulations relating to taxation, royalty regimes and environmental protection, and the continuance of those laws and regulations; that we will have sufficient cash flow, debt or equity sources or other financial resources required to fund our capital and operating expenditures and requirements as needed; drilling results and the recoverability of our reserves; the estimates of our reserves volumes and the assumptions related thereto (including commodity prices and development costs) are accurate in all material respects; the amount of royalties, operating costs, development costs, abandonment and reclamation costs and income taxes that we will incur in connection with the production of our reserves; future exchange rates, inflation rates and interest rates; future income tax rates; the amount of tax pools available to us; the amount of future cash dividends that we intend to pay and the level of participation in our dividend reinvestment plan; the cost of expanding our property holdings; our ability to execute our capital programs as planned without significant adverse impacts from various factors beyond our control, including weather, infrastructure access and delays in obtaining regulatory approvals and third party consents; our ability to obtain equipment in a timely manner to carry out development activities and the costs thereof; our ability to market our oil and natural gas successfully to current and new customers; our ability to reduce our exposure to commodity price fluctuations and counterparty risks through our risk management programs; the impact of increasing competition; our ability to obtain financing on acceptable terms, including our ability to renew or replace our credit facility and our ability to finance the repayment of our senior unsecured notes on maturity; that our conduct and results of operations will be consistent with expectations; our ability to add production and reserves through our development and exploitation activities; and that we will have the ability to develop our oil and gas properties in the manner currently contemplated. In addition, many of the forward-looking statements contained or incorporated by reference in this document are located proximate to assumptions that are specific to those forward-looking statements, and such assumptions should be taken into account when reading such forward-looking statements: see in particular the assumptions identified in Appendix A-3 under “Statement of Reserves Data and Other Oil and Gas Information – Reserves Data” and “Statement of Reserves Data and Other Oil and Gas Information – Notes to Reserves Data Tables”.

Although Penn West believes that the expectations reflected in the forward-looking statements contained or incorporated by reference in this document, and the assumptions on which such forward-looking statements are made, are reasonable, there can be no assurance that such expectations will prove to be correct. Readers are cautioned not to place undue reliance on forward-looking statements included or incorporated by reference in this document, as there can be no assurance that the plans, intentions or expectations upon which the forward-looking statements are based will occur. By their nature, forward-looking statements involve numerous assumptions, known and unknown risks and uncertainties that contribute to the possibility that the predictions, forecasts, projections and other forward-looking statements will not occur, which may cause our actual performance and financial results in future periods to differ materially from any estimates or projections of future performance or results expressed or implied by such forward-looking statements. These risks and uncertainties include, among other things: the possibility that we are unable to execute some or all of our ongoing non-core asset disposition program on favourable terms or at all, including the disposition discussed herein that is scheduled to close in the first quarter of 2014, whether due to the failure to receive requisite regulatory approvals or satisfy applicable closing conditions or for other reasons that we cannot anticipate; the possibility that we will not be able to successfully execute our long-term plan in part or in full, and the possibility that some or all of the benefits that we anticipate will accrue to us and our securityholders as a result of the successful execution of such plan do not materialize; the impact of weather conditions on seasonal demand; the impact of weather conditions on our ability to execute capital programs; the risk that we will be unable to execute our capital programs as planned without significant adverse impacts from various factors beyond our control, including weather, infrastructure access and delays in obtaining regulatory approvals and third party consents; risks inherent in oil and natural gas operations; uncertainties associated with estimating reserves and resources; competition for, among other things, capital, acquisitions of reserves, resources, undeveloped lands and skilled personnel; incorrect assessments of the value of

8

acquisitions, including the historical acquisitions discussed herein; geological, technical, drilling and processing problems; general economic and political conditions in Canada, the U.S., Europe and globally, and in particular, the effect that those conditions have on commodity prices and our access to capital; industry conditions, including fluctuations in the price of oil and natural gas, price differentials for crude oil and natural gas produced in Canada as compared to other markets and transportation restrictions, including pipeline and railway capacity constraints; royalties payable in respect of our oil and natural gas production and changes to government royalty frameworks in jurisdictions in which we operate and the impact that such changes may have on us; changes in government regulation of the oil and natural gas industry, including environmental regulation; fluctuations in foreign exchange or interest rates; unanticipated operating events or environmental events that can reduce production or cause production to be shut-in or delayed, including extreme cold during winter months, wild fires and flooding; failure to obtain regulatory, industry partner and other third-party consents and approvals when required, including for acquisitions, dispositions, joint ventures, partnerships and mergers; failure to realize the anticipated benefits of dispositions, acquisitions, joint ventures and partnerships, including the historical dispositions, acquisitions, joint ventures and partnerships discussed herein; changes in taxation and other laws and regulations that affect us and our securityholders; the potential failure of counterparties to honour their contractual obligations; stock market volatility and market valuations; the ability of the Organization of the Petroleum Exporting Countries (“OPEC”) to control production and balance global supply and demand of crude oil at desired price levels; political uncertainty, including the risks of hostilities, in the petroleum producing regions of the world; delays in exploration and development activities if drilling and related equipment is unavailable or if access to drilling locations is restricted; the impact of pipeline interruptions and apportionments and the actions or inactions of third party operators; and the other factors described under “Risk Factors” in this document and in Penn West’s public filings available in Canada at www.sedar.com and in the United States at www.sec.gov. Readers are cautioned that this list of risk factors should not be construed as exhaustive.

The forward-looking statements contained and incorporated by reference in this document speak only as of the date of this document. Except as expressly required by applicable securities laws, Penn West does not undertake any obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. The forward-looking statements contained and incorporated by reference in this document are expressly qualified by this cautionary statement.

GENERAL AND ORGANIZATIONAL STRUCTURE

General

Penn West is a corporation amalgamated under the ABCA. It is the successor to Penn West Trust and commenced operations as such on January 1, 2011. It operates under the trade names “Penn West” and “Penn West Exploration”. Penn West’s head and registered office is located at Suite 200, 207 – 9th Avenue S.W., Calgary, Alberta, T2P 1K3.

Corporate Conversion

The Corporate Conversion was completed on January 1, 2011 and resulted in the reorganization of Penn West Trust (an income trust) into Penn West (a corporation) and the unitholders of Penn West Trust becoming the Shareholders of Penn West. Penn West and its Subsidiaries now carry on the business formerly carried on by Penn West Trust and its Subsidiaries.

In accordance with the terms of the Corporate Conversion, all of the outstanding Trust Units were exchanged for Common Shares on a one-for-one basis. In addition, as part of the Corporate Conversion, Penn West Trust was dissolved and, through a series of steps, Penn West acquired all of the assets and assumed all of the liabilities of Penn West Trust.

Penn West’s Common Shares commenced trading on the TSX under the trading symbol “PWT” on January 10, 2011 and on the NYSE under the trading symbol “PWE” on January 3, 2011.

9

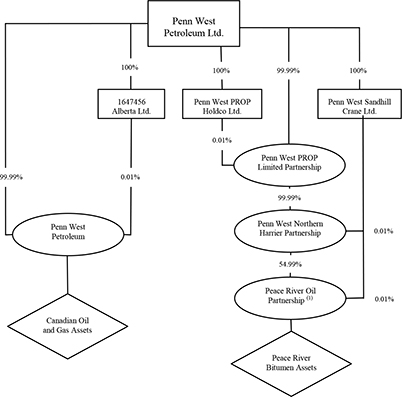

Our Organizational Structure

The following diagram sets forth the organizational structure of Penn West and its material Subsidiaries as at the date hereof.

Notes:

| (1) | The remaining 45% interest in Peace River Oil Partnership is owned by Winter Spark Resources, Inc., an affiliate of China Investment Corporation. |

| (2) | Each of the entities identified in the diagram was incorporated, continued, formed or organized, as the case may be, under the laws of the Province of Alberta. |

DESCRIPTION OF OUR BUSINESS

Overview

Penn West is one of the largest conventional oil and natural gas producers in Canada. Penn West operates a significant portfolio of opportunities with a dominant position in light oil in Canada. Based in Calgary, Alberta, Penn West operates throughout western Canada on a land base encompassing approximately five million acres. Penn West is a development and production company focused on profitability with goals of growing production per share, cash flow per share and strengthening its balance sheet position. We are committed to maximizing the efficiency of our capital programs and the reliability of our production base while growing the oil and liquids weighting of our total production. As at December 31, 2013, Penn West had approximately 1,415 employees.

Reserves Data

See Appendices A-1, A-2 and A-3 for complete NI 51-101 oil and gas reserves disclosure for Penn West as at December 31, 2013.

General Development of the Business

The following is a description of the general development of Penn West’s business over the last three completed financial years.

10

Year Ended December 31, 2011

Corporate Conversion

The Corporate Conversion was completed on January 1, 2011 and resulted in the reorganization of Penn West Trust (an income trust) into Penn West (a corporation) and the unitholders of Penn West Trust becoming the Shareholders of Penn West. Penn West’s Common Shares commenced trading on the TSX under the trading symbol “PWT” on January 10, 2011 and on the NYSE under the trading symbol “PWE” on January 3, 2011.

Convertible Debenture Maturities

On May 31, 2011, Penn West’s 7.2% convertible, unsecured, subordinated debentures matured and were settled in cash for a total of approximately $24 million.

On December 31, 2011, Penn West’s 6.5% convertible, extendible, unsecured, subordinated debentures matured and were settled in cash for a total of approximately $224 million.

Renewal of Credit Facilities

On June 27, 2011, Penn West renewed its unsecured, revolving credit facility for a four-year term ending June 26, 2015 with a syndicate of Canadian and international banks. The credit facility had an aggregate borrowing limit of $2.25 billion at that time.

Executive Appointments

On August 9, 2011, Bill Andrew retired as Chief Executive Officer and assumed the role of Vice-Chairman of Penn West. Murray Nunns, the President and Chief Operating Officer of Penn West, was appointed President and Chief Executive Officer.

Increase in Borrowing Limit on Credit Facilities

On October 27, 2011, Penn West exercised the “accordion” feature of its credit facility, thereby increasing the borrowing limit on its unsecured, revolving credit facility by $500 million. The credit facility then had an aggregate borrowing limit of $2.75 billion. No other terms of the credit facility, including the rates, terms and maturity date of the additional capacity, were changed.

Private Placement of Notes

On November 30, 2011, Penn West completed the private placement of its Series CC, Series DD, Series EE and Series FF Senior Notes, which consisted of the issuance of US$25 million principal amount of 3.64 percent notes due in 2016, US$12 million principal amount of 4.23 percent notes due in 2018, US$68 million principal amount of 4.79 percent notes due in 2021 and Cdn$30 million principal amount of 4.63 percent notes due in 2018. Each of these Series of Senior Notes are guaranteed, unsecured and rank equally with Penn West’s bank credit facilities and its other Senior Notes. The proceeds of the private placement were used to repay a portion of the indebtedness outstanding under Penn West’s bank credit facilities.

Aggregate Acquisition and Disposition Activity

Penn West completed non-core property dispositions, net of acquisitions, of approximately $266 million in 2011.

Year Ended December 31, 2012

Renewal of Credit Facilities

On June 15, 2012, Penn West renewed its unsecured, revolving credit facility for a four-year term ending June 30, 2016 with a syndicate of Canadian and international banks. The credit facility now has an aggregate borrowing limit of $3.0 billion.

11

Aggregate Acquisition and Disposition Activity

Penn West completed non-core property dispositions, net of acquisitions, of approximately $1,615 million in 2012. Total production associated with the combined divestments was approximately 16,500 boe per day. Production was weighted toward oil and liquids. Divested assets were located primarily in Eastern Alberta and Southeast Saskatchewan and represented mature, base assets in Penn West’s asset portfolio. The net proceeds of the dispositions were used to repay a portion of the indebtedness outstanding under our bank credit facilities.

Year Ended December 31, 2013

Board, Management and Staffing Changes

The Board underwent a renewal process in May 2013 that resulted in John Brussa (Chairman), William Andrew (Vice-Chairman) and Shirley McClellan retiring from the Board and Rick George (Chairman), Allan Markin (Vice-Chairman) and Jay Thornton joining the Board. James Allard, George Brookman, Gillian Denham, Daryl Gilbert, Frank Potter, Jack Schanck and James Smith were re-elected as directors at Penn West’s annual general meeting and continued as directors.

In June 2013, Murray Nunns (President and Chief Executive Officer) retired from both his Board and management positions. David Roberts joined Penn West in June 2013 as President and Chief Executive Officer and was added to the Board.

In July 2013, Allan Markin (Vice-Chairman) resigned from the Board.

Penn West streamlined its management structure in July 2013 which resulted in management changes. This led to David Middleton (Executive Vice-President, Operations Engineering and Managing Director, Peace River Oil Partnership), Bob Shepherd (Senior Vice-President, Enhanced Oil Recovery and Cordova Joint Venture) and Rob Wollmann (Senior Vice President, Exploration) leaving Penn West. The new senior management structure consists of David Roberts (President and Chief Executive Officer), Todd Takeyasu (Executive Vice-President and Chief Financial Officer), Mark Fitzgerald (Senior Vice-President, Development), Gregg Gegunde (Senior Vice-President, Production), and Keith Luft (General Counsel and Senior Vice-President, Corporate Services).

In 2013, in an effort to operate in a more efficient manner Penn West reduced its staffing levels by over 25 percent.

Change to Dividend Amount

In June 2013, Penn West announced a change to its dividend amount. Effective for the 2013 third quarter dividend, Penn West reduced its quarterly dividend amount from $0.27 per Common Share to $0.14 per Common Share.

Strategic Alternatives Review

In June 2013, the Board formed a special committee (the “Special Committee”) to review strategic alternatives to increase Shareholder value. In November 2013, Penn West announced that the review was complete and that the Board, based on recommendations from management, the Special Committee and its financial advisor, had determined that Penn West’s long-term plan to deleverage its balance sheet, continue operational and cost control improvements, and focus on light oil development integrated with waterflood programs concentrated in its Cardium, Slave Point and Viking plays was the best strategy available to maximize Shareholder value. Penn West announced that the objective of the long-term plan was to provide Shareholders with compound annual per share growth in oil production and funds flow subsequent to a deleveraging period and provide Shareholders with a return through a sustainable dividend. In furtherance of the plan, Penn West announced its intention to sell $1.5 to 2.0 billion of non-core assets before 2015 in order to deleverage its balance sheet of which $486 million had purchase and sale agreements in place and closed in December 2013.

12

Aggregate Acquisition and Disposition Activity

Penn West completed non-core property dispositions, net of acquisitions, of approximately $525 million in 2013. Total production associated with the combined divestments was approximately 11,000 boe per day. Divested assets were located primarily in the East Central, North West and Southern areas of Alberta and represented mature, base assets in Penn West’s asset portfolio which had minimal capital allocated to them in the long-term plan. The net proceeds of the dispositions were used to repay a portion of the indebtedness outstanding under our bank credit facilities.

2014 Developments

Pending Disposition

In January 2014, Penn West announced that it had entered into an agreement to dispose of non-core assets in the central and southwestern areas of Alberta for total proceeds of $175 million. Average production on these assets was 6,700 boe per day and weighted 58 percent to natural gas and included approximately 1,800 producing or suspended wellbores. The assets do not have any development capital allocated to them in Penn West’s long-term plan. The disposition is expected to close in mid-March 2014.

2014 Capital Expenditure Budget and Production Guidance

Penn West announced in November 2013 that its Board had approved a 2014 exploration and development capital budget of $900 million. The majority of Penn West’s development capital budget is allocated to light-oil development in the Cardium, Viking and Slave Point plays.

Penn West’s capital spending program is anticipated to be more balanced during 2014 than in previous years, resulting in production additions weighted to the second half of 2014. This change in spending profile combined with the dispositions that closed in December 2013 and the disposition described above that is scheduled to close in mid-March 2014 resulted in Penn West forecasting average production for 2014 of between 101,000 and 106,000 boe per day weighted approximately 66 percent to crude oil and NGLs.

Ongoing Acquisition, Disposition, Farm-Out and Financing Activities

Potential Acquisitions

Penn West continues to evaluate potential acquisitions of all types of petroleum and natural gas and other energy-related assets as part of its ongoing asset portfolio management program. At times, Penn West could be in the process of evaluating several potential acquisitions which individually or in the aggregate could be material. As of the date hereof, Penn West has not reached agreement on the price or terms of any potential material acquisitions. Penn West cannot predict whether any current or future opportunities will result in one or more acquisitions for Penn West.

Potential Dispositions and Farm-Outs

Penn West continues to evaluate potential dispositions of its petroleum and natural gas assets as part of its ongoing portfolio asset management program. In particular, Penn West has announced its intention to sell $1.5 to 2.0 billion of non-core assets before 2015. In late 2013, Penn West completed the first phase of its disposition program which resulted in proceeds of $486 million. The second phase of its disposition program began in 2014 with the announcement of a $175 million disposition expected to close in mid-March 2014. In addition, Penn West continues to consider potential farm-out opportunities with other industry participants in respect of its petroleum and natural gas assets in circumstances where Penn West believes it is prudent to do so based on, among other things, its capital program, development plan timelines and the risk profile of such assets. Penn West is normally in the process of evaluating several potential dispositions of its assets and farm-out opportunities at any one time, which individually or in the aggregate could be material. As of the date hereof, Penn West has not reached agreement on the price or terms of any potential material dispositions or farm-outs. Penn West cannot predict whether any current or future opportunities will result in one or more dispositions or farm-outs for Penn West.

13

Potential Financings

Penn West continuously evaluates its capital structure, liquidity and capital resources, and financing opportunities that arise from time to time. Penn West may in the future complete financings of Common Shares or debt (including debt which may be convertible into Common Shares) for purposes that may include the financing of acquisitions, the financing of Penn West’s operations and capital expenditures, and the repayment of indebtedness. As of the date hereof, Penn West has not reached agreement on the pricing or terms of any potential material financing. Penn West cannot predict whether any current or future financing opportunity will result in one or more material financings being completed.

Significant Acquisitions

Penn West did not complete an acquisition during its most recently completed financial year that was a significant acquisition for the purposes of Part 8 of National Instrument 51-102.

CAPITALIZATION OF PENN WEST

Share Capital

The authorized capital of Penn West consists of an unlimited number of Common Shares without nominal or par value and 90,000,000 preferred shares without nominal or par value. A description of the share capital of Penn West is set forth below. This description is a summary only. Shareholders are encouraged to read the full text of such share provisions, which are available on SEDAR at www.sedar.com.

Common Shares

Shareholders are entitled to notice of, to attend and to one vote per Common Share held at any meeting of the shareholders of Penn West (other than meetings of a class or series of shares of Penn West other than the Common Shares).

Shareholders are entitled to receive dividends as and when declared by the Board of Directors on the Common Shares as a class, subject to prior satisfaction of all preferential rights to dividends attached to shares of other classes of shares of Penn West ranking in priority to the Common Shares in respect of dividends.

The holders of Common Shares are entitled in the event of any liquidation, dissolution or winding-up of Penn West, whether voluntary or involuntary, or any other distribution of the assets of Penn West among its Shareholders for the purpose of winding-up its affairs, and subject to prior satisfaction of all preferential rights to return of capital on dissolution attached to all shares of other classes of shares of Penn West ranking in priority to the Common Shares in respect of return of capital on dissolution, to share rateably, together with the holders of shares of any other class of shares of Penn West ranking equally with the Common Shares in respect of return of capital on dissolution, in such assets of Penn West as are available for distribution.

As at March 6, 2014, 490,688,948 Common Shares were issued and outstanding.

Preferred Shares

Preferred shares of Penn West may at any time or from time to time be issued in one or more series. Before any shares of a particular series are issued, the Board shall, by resolution, fix the number of shares that will form such series and shall, subject to the limitations set out in Penn West’s articles, by resolution fix the designation, rights, privileges, restrictions and conditions to be attached to the preferred shares of such series, including, but without in any way limiting or restricting the generality of the foregoing, the rate, amount or method of calculation of dividends thereon, the time and place of payment of dividends, the consideration for and the terms and conditions of any purchase for cancellation, retraction or redemption thereof, conversion or exchange rights (if any), and whether into or for securities of Penn West or otherwise, voting rights attached thereto (if any), the terms and conditions of any share purchase or retirement plan or sinking fund, and restrictions on the payment of dividends on any shares other than preferred shares or payment in respect of capital on any shares in the capital of Penn West or creation or issue of debt or equity securities; the whole subject to filing of Articles of Amendment setting forth a description of such series, including the designation, rights, privileges, restrictions and conditions attached to

14

the shares of such series. Notwithstanding the foregoing, other than in the case of a failure to declare or pay dividends specified in any series of preferred shares, the voting rights attached to the preferred shares shall be limited to one vote per preferred share at any meeting where the preferred shares and Common Shares vote together as a single class.

As at the date hereof, no preferred shares are issued and outstanding.

Debt Capital

Penn West has issued the Senior Notes and has a syndicated credit facility. A description of the debt capital of Penn West is set forth below. This description is a summary only. Shareholders are encouraged to read the full text of the agreements governing Penn West’s Senior Notes and credit facility, which are available on SEDAR at www.sedar.com.

Senior Notes

Penn West has issued the Senior Notes, which consist of US$1,629 million principal amount of notes, Cdn$175 million principal amount of notes, £77 million principal amount of notes and €10 million principal amount of notes. The Senior Notes are guaranteed by Penn West’s material subsidiaries, are unsecured and rank equally with our bank credit facilities. The following is a brief summary of certain of the material terms of each series of our Senior Notes.

| Series |

Currency / Principal Amount |

Interest Rate | Issue Date | Maturity Date | ||||||||

| Series A |

US$ | 160 million | 5.68 | % | May 31, 2007 | May 31, 2015 | ||||||

| Series B |

US$ | 155 million | 5.80 | % | May 31, 2007 | May 31, 2017 | ||||||

| Series C |

US$ | 140 million | 5.90 | % | May 31, 2007 | May 31, 2019 | ||||||

| Series D |

US$ | 20 million | 6.05 | % | May 31, 2007 | May 31, 2022 | ||||||

| Series E |

US$ | 152.5 million | 6.12 | % | May 29, 2008 | May 29, 2016 | ||||||

| Series F |

US$ | 278 million | 6.30 | % | May 29, 2008 | May 29, 2018 | ||||||

| Series G |

US$ | 49.5 million | 6.40 | % | May 29, 2008 | May 29, 2020 | ||||||

| Series H |

Cdn$ | 30 million | 6.16 | % | May 29, 2008 | May 29, 2018 | ||||||

| Series I |

£ | 57 million | (1) | 7.78 | %(1) | July 31, 2008 | July 31, 2018 | |||||

| Series J |

US$ | 50 million | 8.29 | % | May 5, 2009 | May 5, 2014 | ||||||

| Series K |

US$ | 35 million | 8.89 | % | May 5, 2009 | May 5, 2016 | ||||||

| Series L |

US$ | 34 million | 9.32 | % | May 5, 2009 | May 5, 2019 | ||||||

| Series M |

US$ | 30 million | 8.89 | % | May 5, 2009 | May 5, 2019(2) | ||||||

| Series N |

£ | 20 million | (3) | 9.49 | %(3) | May 5, 2009 | May 5, 2019 | |||||

| Series O |

€ | 10 million | (4) | 9.52 | %(4) | May 5, 2009 | May 5, 2019 | |||||

| Series P |

Cdn$ | 5 million | 7.58 | % | May 5, 2009 | May 5, 2014 | ||||||

15

| Series |

Currency /Principal Amount |

Interest Rate | Issue Date | Maturity Date | ||||||||

| Series Q |

US$ | 27.5 million | 4.53 | % | March 16, 2010 | March 16, 2015 | ||||||

| Series R |

US$ | 65 million | 5.29 | % | March 16, 2010 | March 16, 2017 | ||||||

| Series S |

US$ | 112.5 million | 5.85 | % | March 16, 2010 | March 16, 2020 | ||||||

| Series T |

US$ | 25 million | 5.95 | % | March 16, 2010 | March 16, 2022 | ||||||

| Series U |

US$ | 20 million | 6.10 | % | March 16, 2010 | March 16, 2025 | ||||||

| Series V |

Cdn$ | 50 million | 4.88 | % | March 16, 2010 | March 16, 2015 | ||||||

| Series W |

US$ | 18 million | 4.17 | % | December 2, 2010 | December 2, 2017 | ||||||

| Series X |

US$ | 84 million | 4.88 | % | December 2, 2010 and January 4, 2011 |

December 2, 2020 | ||||||

| Series Y |

US$ | 18 million | 4.98 | % | December 2, 2010 | December 2, 2022 | ||||||

| Series Z |

US$ | 50 million | 5.23 | % | December 2, 2010 and January 4, 2011 |

December 2, 2025 | ||||||

| Series AA |

Cdn$ | 10 million | 4.44 | % | December 2, 2010 | December 2, 2015 | ||||||

| Series BB |

Cdn$ | 50 million | 5.38 | % | December 2, 2010 | December 2, 2020 | ||||||

| Series CC |

US$ | 25 million | 3.64 | % | November 30, 2011 | November 30, 2016 | ||||||

| Series DD |

US$ | 12 million | 4.23 | % | November 30, 2011 | November 30, 2018 | ||||||

| Series EE |

US$ | 68 million | 4.79 | % | November 30, 2011 | November 30, 2021 | ||||||

| Series FF |

Cdn$ | 30 million | 4.63 | % | November 30, 2011 | November 30, 2018 | ||||||

Notes:

| (1) | Penn West has entered into contracts to fix the interest rate of the Series I Senior Notes at 6.95% in Canadian dollars and to fix the exchange rate on repayment. |

| (2) | Penn West is obligated to repay US$5 million of the total US$30 million principal amount of the Series M notes outstanding on May 5 of each year ending in 2019. |

| (3) | Penn West has entered into contracts to fix the interest rate of the Series N Senior Notes at 9.15% and to fix the exchange rate on repayment. |

| (4) | Penn West has entered into contracts to fix the interest rate of the Series O Senior Notes at 9.22% and to fix the exchange rate on repayment. |

Credit Facility

Penn West has an unsecured, revolving credit facility with a four-year term ending June 30, 2016 with a syndicate of Canadian and international banks. The credit facility has an aggregate borrowing limit of $3.0 billion. As at March 6, 2014, approximately $0.4 billion had been borrowed under the credit facility.

16

Additional Information

For additional information regarding our Senior Notes and our credit facility, see Notes 9 and 18 (collectively, the “Financial Statement Disclosure”) to our audited consolidated financial statements for the year ended December 31, 2013, and “Financing” and “Liquidity and Capital Resources” (collectively, the “MD&A Disclosure”) in our related management’s discussion and analysis, both of which are available on SEDAR at www.sedar.com. The Financial Statement Disclosure and the MD&A Disclosure and are both incorporated by reference into this Annual Information Form.

DIRECTORS AND EXECUTIVE OFFICERS OF PENN WEST

The following table sets forth, as at March 6, 2014, the name, province and country of residence and positions and offices held for each of the directors and executive officers of Penn West, together with their principal occupations during the last five years. The directors of Penn West will hold office until the next annual meeting of Shareholders or until their respective successors have been duly elected or appointed.

| Name, Province and Country of Residence |

Positions and Offices Held with Penn West |

Principal Occupations | ||

| James E. Allard(2)(5) Alberta, Canada |

Director since June 30, 2006 | Independent director and business advisor. | ||

| George H. Brookman(2)(4) Alberta, Canada |

Director since August 3, 2005 | Chief Executive Officer of West Canadian Industries Group Inc. (a digital printing and document management company). | ||

| Gillian H. Denham(1)(2)(4) Ontario, Canada |

Director since June 13, 2012 | Corporate director. | ||

| Richard L. George Alberta, Canada |

Chairman of the Board and director since May 3, 2013 | Partner of Novo Investment Group Ltd. (a Calgary-based investment management company). Chief Executive Officer of Suncor Energy Inc. (“Suncor”) (an integrated energy company) prior to May 2012 and President and Chief Executive Officer of Suncor prior to December 2011. | ||

| Daryl H. Gilbert(3)(4)(5) Alberta, Canada |

Director since January 11, 2008 | Independent businessman since 2005. | ||

| Frank Potter(1)(4) Ontario, Canada |

Director since June 30, 2006 | Independent director for a number of public, private and not-for-profit corporations. | ||

| David E. Roberts Alberta, Canada |

Director since June 19, 2013 President and Chief Executive Officer |

President and Chief Executive Officer of Penn West since June 2013. Prior thereto, Executive Vice-President and Chief Operating Officer of Marathon Oil Corporation (“Marathon”) (an independent energy company) from July 2011 to December 2012. Executive Vice-President Upstream of Marathon from April 2008 to July 2011. Prior thereto, Senior Vice-President Business Development of Marathon. | ||

17

| Name, Province and Country of Residence |

Positions and Offices Held with Penn West |

Principal Occupations | ||

| Jack Schanck(2)(3)(5) Alberta, Canada |

Director since June 2, 2008 | Independent director and businessman since June 2013. Prior thereto, President, Chief Executive Officer and director of Sonde Resources Corp., a public oil and natural gas company, since December 2010. Prior thereto, an independent businessman from January 2010 to December 2010. Prior thereto, Managing Partner of Tecton Energy, LLC, a private oil and natural gas company. | ||

| James C. Smith(1)(3) Alberta, Canada |

Director since May 31, 2005 | Independent director and consultant to a number of public and private oil and gas companies. | ||

| Jay W. Thornton(1)(3) Alberta, Canada |

Director since June 5, 2013 | Partner of Novo Investment Group Ltd. (a Calgary-based investment management company). Prior thereto, various operating and corporate executive positions with Suncor. | ||

| Mark P. Fitzgerald Alberta, Canada |

Senior Vice President, Development | Senior Vice President, Development of Penn West since August 2011. Prior thereto, Senior Vice President, Production of Penn West from November 2008 to July 2011. | ||

| Gregg Gegunde Alberta, Canada |

Senior Vice President, Production | Senior Vice President, Production of Penn West since February 2012. Prior thereto, Vice President, Production of Penn West from July 2011 to February 2012. Prior thereto, various Vice President roles in the development area and production engineering with Penn West. | ||

| S. Keith Luft Alberta, Canada |

General Counsel and Senior Vice President, Corporate Services | General Counsel and Senior Vice-President, Corporate Services of Penn West since July 2013. Prior thereto, General Counsel and Senior Vice President, Stakeholder Relations of Penn West. | ||

| Todd H. Takeyasu Alberta, Canada |

Executive Vice President and Chief Financial Officer | Executive Vice President and Chief Financial Officer of Penn West. | ||

Notes:

| (1) | Member of the Audit Committee. |

| (2) | Member of the Human Resources and Compensation Committee. |

| (3) | Member of the Reserves and Acquisitions and Divestitures Committee. |

| (4) | Member of the Governance Committee. |

| (5) | Member of the Health, Safety, Environment and Regulatory Committee. |

As at March 6, 2014, the directors and executive officers of Penn West, as a group, beneficially owned, or controlled or directed, directly or indirectly, approximately one million Common Shares, or less than one percent of the issued and outstanding Common Shares.

Cease Trade Orders, Bankruptcies, Penalties or Sanctions

To the knowledge of Penn West, except as otherwise set forth herein, no director or executive officer of Penn West (nor any personal holding company of any of such persons) is, as of the date of this Annual Information Form, or was within ten years before the date of this Annual Information Form, a director, Chief Executive Officer or Chief Financial Officer of any company (including Penn West), that:

18

| (a) | was subject to a cease trade order (including a management cease trade order), an order similar to a cease trade order or an order that denied the relevant company access to any exemption under securities legislation, in each case that was in effect for a period of more than 30 consecutive days (collectively, an “Order”) that was issued while the director or executive officer was acting in the capacity as director, Chief Executive Officer or Chief Financial Officer; or |

| (b) | was subject to an Order that was issued after the director or executive officer ceased to be a director, Chief Executive Officer or Chief Financial Officer and which resulted from an event that occurred while that person was acting in the capacity as director, Chief Executive Officer or Chief Financial Officer. |

To the knowledge of Penn West, except as otherwise disclosed herein, no director or executive officer of Penn West or shareholder holding a sufficient number of securities of Penn West to affect materially the control of Penn West (nor any personal holding company of any of such persons):

| (a) | is, as of the date of this Annual Information Form, or has been within the ten years before the date of this Annual Information Form, a director or executive officer of any company (including Penn West) that, while that person was acting in that capacity, or within a year of that person ceasing to act in that capacity, became bankrupt, made a proposal under any legislation relating to bankruptcy or insolvency or was subject to or instituted any proceedings, arrangement or compromise with creditors or had a receiver, receiver manager or trustee appointed to hold its assets; or |

| (b) | has, within the ten years before the date of this Annual Information Form, become bankrupt, made a proposal under any legislation relating to bankruptcy or insolvency, or become subject to or instituted any proceedings, arrangement or compromise with creditors, or had a receiver, receiver manager or trustee appointed to hold the assets of the director, executive officer or shareholder. |

Daryl Gilbert was a director of Globel Direct, Inc. The company sought and received protection under the Companies’ Creditors Arrangement Act (Canada) in June 2007, and after a failed restructuring effort a receiver was appointed by one of the company’s lenders in December 2007. Cease trade orders dated September 24, 2008 and September 30, 2008 were issued by the Alberta Securities Commission and the British Columbia Securities Commission, respectively, for failure to file financial statements. The cease trade orders were issued following the appointment of the receiver and, as at the date hereof, have not been revoked. The company has since ceased operations and is delisted.

To the knowledge of Penn West, no director or executive officer of Penn West or shareholder holding a sufficient number of securities of Penn West to affect materially the control of Penn West (nor any personal holding company of any of such persons), has been subject to:

| (a) | any penalties or sanctions imposed by a court relating to securities legislation or by a securities regulatory authority or has entered into a settlement agreement with a securities regulatory authority; or |

| (b) | any other penalties or sanctions imposed by a court or regulatory body that would likely be considered important to a reasonable investor in making an investment decision; |

provided that for the purposes of the foregoing, a late filing fee, such as a filing fee that applies to the late filing of an insider report, is not considered to be a “penalty or sanction”.

Conflicts of Interest

The Board of Directors has adopted a Code of Business Conduct and Ethics (the “Code”) and a Code of Ethics for Directors, Officers and Senior Financial Management (the “Oversight Code” and together with the Code, the “Codes”). In general, the private investment activities of employees, directors and officers are not prohibited; however, should an existing investment pose a potential conflict of interest, the potential conflict is required by the Code to be disclosed to an officer or a member of Penn West’s legal department and by the Oversight Code to be disclosed to the Board of Directors. Any other activities posing a potential conflict of interest are also required by the Codes to be disclosed to an officer or to a member of Penn West’s legal department. Any such potential conflicts of interests will be dealt with openly with full disclosure of the nature and extent of the potential conflicts of interests with Penn West.

19

It is acknowledged in the Codes that the directors may be directors or officers of other entities engaged in the oil and gas business, and that such entities may compete directly or indirectly with Penn West. Passive investments in public or private entities of less than one per cent of the outstanding shares will not be viewed as “competing” with Penn West. No executive officer or employee of Penn West should be a director, employee, contractor, consultant or officer of any entity that is or may be in competition with Penn West unless expressly authorized by an executive officer or the Board of Directors. Any director of Penn West who is a director or officer of, or who is otherwise actively engaged in the management of, or who owns an investment of one per cent or more of the outstanding shares, in public or private entities shall disclose such holding to the Board of Directors. In the event that any circumstance should arise as a result of such positions or investments being held or otherwise which in the opinion of the Board of Directors constitutes a conflict of interest which reasonably affects such person’s ability to act with a view to the best interests of Penn West, the Board of Directors will take such actions as are reasonably required to resolve such matters with a view to the best interests of Penn West. Such actions, without limitation, may include excluding such directors, officers or employees from certain information or activities of Penn West.

The ABCA provides that in the event that an officer or director is a party to, or is a director or an officer of, or has a material interest in any person who is a party to, a material contract or material transaction or proposed material contract or proposed material transaction, such officer or director shall disclose the nature and extent of his or her interest and shall refrain from voting to approve such contract or transaction.

As of the date hereof, Penn West is not aware of any existing or potential material conflicts of interest between Penn West or a Subsidiary of Penn West and any director or officer of Penn West or of any Subsidiary of Penn West.

Promoters

No person or company has been, within the two most recently completed financial years or during the current financial year, a “promoter” (as defined in the Securities Act (Ontario)) of Penn West or of a Subsidiary of Penn West.

AUDIT COMMITTEE DISCLOSURES

National Instrument 52-110 (“NI 52-110”) relating to audit committees has mandated certain disclosures for inclusion in this Annual Information Form. The text of the Audit Committee’s mandate is attached as Appendix B to this Annual Information Form.

Composition of the Audit Committee and Relevant Education and Experience

As of March 6, 2014, the members of the Audit Committee are James C. Smith (Chairman), Gillian H. Denham, Frank Potter and Jay W. Thornton, each of whom is independent and financially literate within the meaning of NI 52-110. The following comprises a brief summary of each member’s education and experience that is relevant to the performance of his or her responsibilities as an Audit Committee member.

James C. Smith (Chairman)

Mr. Smith is a Chartered Accountant with over 40 years of experience in public accounting and industry. Since 1998, he has been a business consultant and independent director to a number of public and private companies operating in the oil and natural gas industry. From February 2002 to June 2006, he served as the Vice-President and Chief Financial Officer of Mercury Energy Corporation, a private oil and natural gas company. Mr. Smith also held the position of Chief Financial Officer of Segue Energy Corporation, a private oil and natural gas company, from January 2001 to August 2003. From 1999 to 2000, Mr. Smith was the Vice-President and Chief Financial Officer of Probe Exploration Inc., a publicly traded oil and natural gas company. Mr. Smith served as the Vice-President and Chief Financial Officer of Crestar Energy Inc. from its inception in 1992 until 1998, during which time the company completed an initial public offering, was listed on the TSX and completed several major debt and equity financing transactions.

20

Gillian H. Denham

Ms. Denham, a Corporate Director, sits on the board of Morneau Shepell Inc., a provider of human resource consulting and outsourcing services, and the board of National Bank of Canada. From 2001 to 2005, she was Vice Chair, Retail Markets at Canadian Imperial Bank of Commerce (“CIBC”). Ms. Denham joined Wood Gundy in 1983, subsequently acquired by CIBC, as an Assistant Vice-President in Corporate Finance. Throughout her career at CIBC, she held progressively more senior roles. From 2006 to 2010, she was a member of the board of directors and Chair of the Human Resources and Compensation Committee of the Ontario Teachers’ Pension Plan. Ms. Denham is a member of the board of governors and the audit committee of Upper Canada College. She holds an Honours Business Administration from University of Western Ontario School of Business and an MBA from Harvard Business School.

Frank Potter

Mr. Potter has a background in international banking in Europe, the Middle East and the United States. He managed the international business of one of Canada’s principal banks before being appointed to the executive board of the World Bank in Washington where he served for nine years, including as lead director and Chairman of the bank’s Steering Committee. Mr. Potter subsequently served as a Senior Advisor at the Department of Finance for the Canadian government. He is formerly the Chairman of Emerging Markets Advisors, Inc., a Toronto based consultancy that assists corporations in making and managing direct investments internationally. Mr. Potter serves on a number of boards, including Canadian Tire Corporation and the Royal Ontario Museum, where he is a former Chairman of the board of governors. Mr. Potter has experience serving on audit committees for several public issuers.

Jay W. Thornton

Mr. Thornton is a partner of Novo Investment Group Ltd., a Calgary-based investment management company. Mr. Thornton has over 27 years of oil and gas experience. He spent the first part of his career in various management positions with Shell. From 2000 to 2012, he held various operating and corporate executive positions with Suncor. He spent four years in Fort McMurray at Suncor’s oil sands mining operations. His most recent position with Suncor was Executive Vice-President of Supply, Trading and Development. He has held previous board positions with both the Canadian Association of Petroleum Producers (CAAP) and the Canadian Petroleum Products Institute (CPPI). He was a past board member of the YMCA Fort McMurray and is currently a member of the board of North American Energy Partners Inc., US-based mining company Xinergy Ltd. and a private Calgary-based oil and gas company. Mr. Thornton is a graduate of McMaster University with an Honours degree in Economics. He is also a graduate of the Institute of Corporate Directors’ (ICD) Directors Education Program.

Pre-Approval Policies and Procedures for Audit and Non-Audit Services

The terms of the engagement of Penn West’s external auditors to provide audit services, including the budgeted fees for such audit services and the representations and disclaimer relating thereto, must be pre-approved by the entire Audit Committee.

With respect to any engagements of Penn West’s external auditors for non-audit services, Penn West must obtain the approval of the Audit Committee or the Chairman of the Audit Committee prior to retaining the external auditors to complete such engagement. If such pre-approval is provided by the Chairman of the Audit Committee, the Chairman must report to the Audit Committee on any non-audit service engagement pre-approved by him at the Audit Committee’s first scheduled meeting following such pre-approval.

If, after using its reasonable best efforts, Penn West is unable to contact the Chairman of the Audit Committee on a timely basis to obtain the pre-approval contemplated by the preceding paragraph, Penn West may obtain the required pre-approval from any other member of the Audit Committee, provided that any such Audit Committee member shall report to the Audit Committee on any non-audit service engagement pre-approved by him or her at the Audit Committee’s first scheduled meeting following such pre-approval.

21

External Auditor Service Fees

The following table summarizes the fees billed to Penn West by KPMG LLP for external audit and other services during the periods indicated

| Year |

Audit Fees(1) ($) |

Audit-Related Fees(2) ($) |

Tax Fees(3) ($) |

All Other Fees ($) |

||||||||||||

| 2013 |

1,340,000 | 145,700 | — | — | ||||||||||||

| 2012 |

1,120,000 | 146,000 | 38,000 | — | ||||||||||||

Notes:

| (1) | The aggregate fees billed by our external auditor in each of the last two fiscal years for audit services, including fees for the integrated audit of Penn West’s annual financial statements or services that are normally provided in connection with statutory and regulatory filings or engagements, reviews in connection with acquisitions and Sarbanes-Oxley Act related services, long-form comfort letters related to the public offering of securities and review procedures on the unaudited interim consolidated financial statements. |

| (2) | The aggregate fees billed in each of the last two fiscal years by our external auditor for assurance and related services that are reasonably related to the performance of the audit or review of our financial statements (and not included in audit services fees in note (1)). The services comprising the fees disclosed under this category principally consisted of Penn West’s portion of fees for the Peace River Oil Partnership audit and French translation services. |

| (3) | The aggregate fees billed in each of the last two fiscal years by our external auditor for professional services for tax compliance, tax advice and tax planning. The services comprising the fees disclosed under this category principally relate to general tax compliance and planning services. |

Reliance on Exemptions

At no time since the commencement of Penn West’s most recently completed financial year has Penn West relied on any of the exemptions contained in Sections 2.4, 3.2, 3.4 or 3.5 of NI 52-110, or an exemption from NI 52-110, in whole or in part, granted under Part 8 thereof. In addition, at no time since the commencement of Penn West’s most recently completed financial year has Penn West relied upon the exemptions in Subsection 3.3(2) or Section 3.6 of NI 52-110. Furthermore, at no time since the commencement of Penn West’s most recently completed financial year has Penn West relied upon Section 3.8 of NI 52-110.

Audit Committee Oversight

At no time since the commencement of Penn West’s most recently completed financial year has a recommendation of the Audit Committee to nominate or compensate an external auditor not been adopted by the Board of Directors.

DIVIDENDS AND DIVIDEND POLICY

Dividend Policy

The Board of Directors has adopted a quarterly dividend policy with a current dividend amount of Cdn$0.14 per Common Share. The quarterly dividend is paid on or about the 15th day of the month following the end of each quarter to Shareholders of record at the end of such quarter.

Notwithstanding the foregoing, the amount of future cash dividends, if any, will be subject to the discretion of the Board and may vary depending on a variety of factors and conditions existing from time to time, including fluctuations in commodity prices, production levels, capital expenditure requirements, debt service requirements, operating costs, royalty burdens, foreign exchange rates, compliance with any restrictions on the declaration and payment of dividends contained in any agreement to which Penn West is a party from time to time (including, without limitation, the agreements governing Penn West’s credit facilities and Senior Notes), and the satisfaction of liquidity and solvency tests imposed by the ABCA for the declaration and payment of dividends.

22

The Board intends to review Penn West’s dividend policy on a quarterly basis. Depending on the foregoing factors and any other factors that the Board deems relevant from time to time, many of which are beyond the control of our Board and management team, the Board may change our dividend policy following any such quarterly review or at any other time that the Board deems appropriate, and as a result, future cash dividends could be reduced or suspended entirely. The market value of our Common Shares may deteriorate if we reduce or suspend the amount of cash dividends that we pay in the future and such deterioration may be material. See “Risk Factors”. As at the date hereof, the Board does not have any intention to change Penn West’s dividend policy.

Effective from January 1, 2011, all dividends paid on our Common Shares to shareholders residing in Canada have been and will continue to be designated as “eligible dividends” for Canadian income tax purposes. This designation will apply until we notify Shareholders otherwise. Shareholders seeking further information regarding the taxation of “eligible dividends” should contact their Canadian tax advisor.

The credit agreement governing our syndicated credit facility and each of the note purchase agreements governing our Senior Notes contain provisions which restrict our ability to pay dividends to Shareholders in the event of the occurrence of certain events of default. The full text of the agreements governing our credit facility and our Senior Notes is available on SEDAR at www.sedar.com. For additional information regarding our credit facility and our Senior Notes, see “Capitalization of Penn West – Debt Capital”.

Dividend Reinvestment and Optional Common Share Purchase Plan

Our Dividend Reinvestment and Optional Common Share Purchase Plan (the “DRIP”) provides eligible Shareholders with the advantage of acquiring additional Common Shares by reinvesting their dividends. At our discretion, Common Shares will be acquired with dividends either on the TSX at prevailing market rates or from treasury at 95% of the “average market price” (as defined in the DRIP). Generally, we expect to issue Common Shares from treasury at a discount to satisfy the dividend reinvestment component of the DRIP.

Eligible Shareholders may also make optional cash payments of a minimum of $500 up to a maximum of $15,000 per quarter to purchase additional Common Shares. Common Shares purchased with optional cash payments will be acquired either on the TSX at prevailing market rates or from treasury at the average market price (without a discount).

We will determine prior to each dividend payment date the number of Common Shares, if any, that will be made available from treasury under the DRIP on such payment date. No assurances can be made that Common Shares will be made available from treasury on a regular basis, or at all.

Shareholders who are residents of Canada are eligible to participate in the dividend reinvestment component of the DRIP and to purchase new Common Shares with optional cash payments. Shareholders who are resident in the United States are eligible to participate in the dividend reinvestment component of the DRIP. United States residents are not eligible to make optional cash payments to purchase additional Common Shares pursuant to the DRIP. With the exception of the foregoing, unless otherwise announced by us, Shareholders who are not residents of Canada are not entitled to participate, directly or indirectly, in the DRIP.

Dividends Declared Payable to Shareholders of Penn West

During the financial years ended December 31, 2011, 2012 and 2013, Penn West declared payable the following amount of cash dividends per Common Share:

| Quarter |

2013 Dividends Declared Payable ($) |

2012 Dividends Declared Payable ($) |

2011 Dividends Declared Payable ($) |

|||||||||