Exhibit 4.32

General Agreement 2013

between

Fresenius Medical Care AG & Co. KGaA

Else-Kröner-Straße 1

D-61352 Bad Homburg

(„FME”)

and

Fresenius Netcare GmbH

Else-Kröner-Straße 1

D-61352 Bad Homburg

(„NETCARE”)

|

Current status |

: |

|

18.02.2013 |

|

Last printed |

: |

|

18.2.2013 |

|

Version |

: |

|

1.0 |

Index

|

Preamble |

3 |

|

|

|

|

1. |

Contractual Structure and Scope of Application |

5 |

|

|

|

|

|

2. |

NETCARE’s Duties |

8 |

|

|

|

|

|

3. |

Use of Subcontractors |

9 |

|

|

|

|

|

4. |

FME’s duties |

10 |

|

|

|

|

|

5. |

Cooperation |

11 |

|

|

|

|

|

6. |

Prices, Invoice, Payments |

11 |

|

|

|

|

|

7. |

Governance Structure and Change Request Procedure |

12 |

|

|

|

|

|

8. |

Confidentiality |

14 |

|

|

|

|

|

9. |

Privacy Law/Safety/Compliance with GxP/Order-Data Processing |

15 |

|

|

|

|

|

10. |

Order-Data Processing (Auftragsdatenverarbeitung) |

17 |

|

|

|

|

|

11. |

Rights of Use and Intellectual Property RIGHTS |

20 |

|

|

|

|

|

12. |

Defects AND Warranty |

22 |

|

|

|

|

|

13. |

Liability |

22 |

|

|

|

|

|

14. |

Penalties |

24 |

|

|

|

|

|

15. |

Term and Termination |

24 |

|

|

|

|

|

16. |

Effect of Termination/Expiration |

25 |

|

|

|

|

|

17. |

Governing Law, Arbitration |

27 |

|

|

|

|

|

18. |

Miscellaneous |

28 |

2

GENERAL AGREEMENT

This agreement is made and entered into on 01.01.2013 by and among Fresenius Medical Care AG & Co. KGaA, Else-Kröner-Straße 1, 61352 Bad Homburg v. d. H. (“FME”) and Fresenius Netcare GmbH, Else-Kröner-Straße 1, 61352 Bad Homburg v. d. H. (“NETCARE” and together with FME, the “Parties” and each a “Party”).

PREAMBLE

(A) FME is the parent company of a group that manufactures and distributes dialysisrelated products and provides dialysis services.

(B) NETCARE is a provider of IT services.

(C) The Parties entered into a General Agreement dated 8 December 2003 to provide for a legal framework under which NETCARE provided IT services to FME. The term of such General Agreement will expire on 31 December 2012.

(D) The Parties intend to continue the existing contractual relationship by entering into this General Agreement (hereinafter referred to as the “General Agreement”).

(E) FME, in its own name and on behalf of its current and future affiliates (as listed in Attachment 1 to this Agreement, as amended once a year in accordance with the procedure defined in the MSD), for each limited to users located in the Territory (“Territory” exclusively meaning: FME regions Europe, Africa, Middle East and Latin America, the “FME EMEALA”) and NETCARE intend to agree upon the parameters of their cooperation with respect to services in the field of information technology. This General Agreement and its Annexes and Service Agreements shall describe the services to be provided by NETCARE to FME and the terms and conditions under which the services will be provided and of the cooperation between the Parties with the intention to continue the long term business relationship in the same manner as under the expired General Agreement.

(F) NETCARE has the expertise, knowledge and capacity to provide the IT services under this General Agreement. Based on its previous role as service provider to FME, NETCARE is prepared to assume and render the services, functions and projects described in the Set of Contracts (as defined below) to FME.

(G) Such cooperation shall be governed by the following principles both Parties have accepted:

(i) Information Technology to support the FME business

(ii) Partnership

3

(iii) Transparency

(iv) Competitiveness

(v) Economic benefits and

(vi) Safety

(vii) Compliance

(H) Information Technology to Support FME business. The maxim of the FME EMEALA IT-strategy is to support the business units of FME through the use of information technologies efficiently. According to such maxim, technology is a method serving such purpose consequently and must not become an end in itself. Subject to the terms and conditions of this General Agreement, the Annexes and Service Agreements thereto, “Efficiently” in this context means the use of software close to the standard, the avoidance of custom-developments and, in given cases and subject to written -agreement thereon, the repatriation of uneconomic modifications deviating from the standard.

(I) Partnership. Reliable and high performing information technology may be achieved only in close collaboration between the Parties. Amicable collaboration in this context shall mean frequent communication through established channels of communication as defined in this General Agreement and a common pursuit for achieving goals. Cases of controversy shall be discussed openly and settled amicable. When using their discretion, both Parties shall in no instance disregard the other Party’s interests involved.

(J) Transparency. Either Party shall inform the respective other Party of projects which may affect the collaboration under this General Agreement in due time via the established communication channels as described within this General Agreement. Parties shall undertake to provide data for plausibility analysis if required by the General Agreement, Annexes or Service Agreements thereto.

(K) Competitiveness. Both prices and services or goods rendered shall be competitive to market prices. NETCARE shall be responsible for keeping its compensation scheme proportionate to the costs incurred. Savings earned through joint projects shall be allocated fairly. Pricing and price changes shall be discussed between the Parties and shall be jointly settled. FME may commission benchmark opinions by third Parties. NETCARE shall undertake to assists in such benchmark projects.

(L) Economic effects. It is understood that FME desires to save costs by means of information technology. It shall be a continuous task of both Parties to determine and to realize possible cost saving potentials made available by the use and operation of information

4

technology. However, cost saving measures shall not adversely affect the scope and quality of services rendered under the terms and conditions of any Annex or Service Agreement. (Both Parties are aware, that although the prices per user are envisioned to be decreasing the total cost may increase due to an increasing number of users and additional functionality). The goal of performing cost saving measures shall be a common one even though the intent of NETCARE to make profits contradicts FME’s desire to lower cost at first sight.

(M) Safety. FME shall have unhindered access to its proprietary data. However, unauthorized access by third Parties and employees shall be prevented. NETCARE may not misuse data security rationale for denying FME access to data, e. g. preventing FME to undertake additional data analysis with IT technology which is not covered by this General Agreement.

(N) Compliance. The Parties acknowledge that FME as a company with its business in the medical and pharmaceutical industry operates in a regulated market and is subject to certain legal and regulatory requirements, including, but not limited to GxP, SOX and data protection. NETCARE shall provide the services in a manner required by FME to ensure compliance of FME with such legal requirements and NETCARE shall reasonably assist FME upon request in complying with such legal requirements as far as the legal requirements impose requirements on the IT services and FME has notified NETCARE of the relevant requirements.

(O) Third Party comparison. Furthermore, this General Agreement and the Set of Contracts (as defined below) shall be drafted and construed without taking into account that the Parties are affiliated companies. Therefore, this General Agreement and modules attached hereto shall be in accordance with arm’s length principles and stand third Party comparison. In order to achieve this purpose, FME and NETCARE have commissioned Ernst & Young GmbH Wirtschaftsprüfungsgesellschaft to issue a fairness opinion on the comparability of the terms and conditions of this present Set of Contracts with third Party agreements. The fairness opinion is attached hereto as Attachment 2.

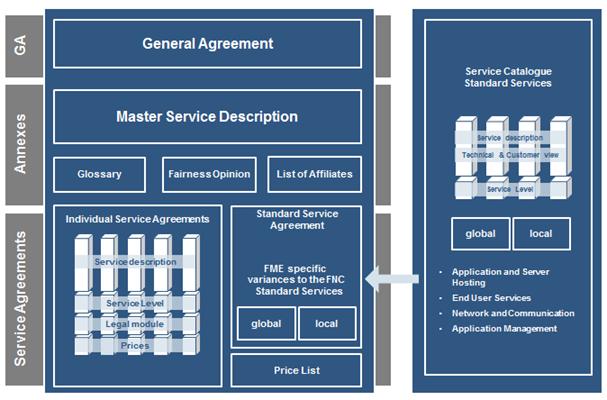

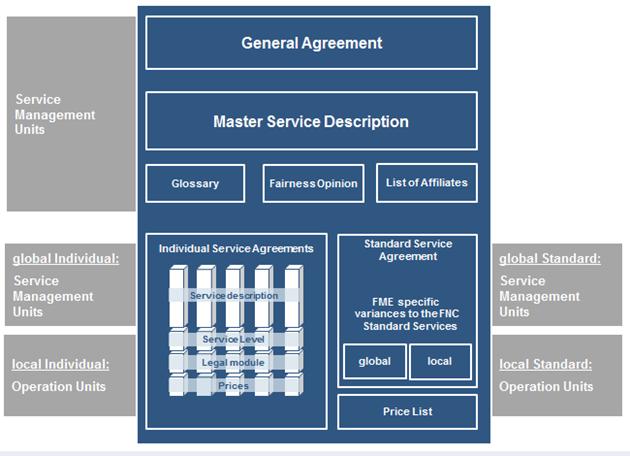

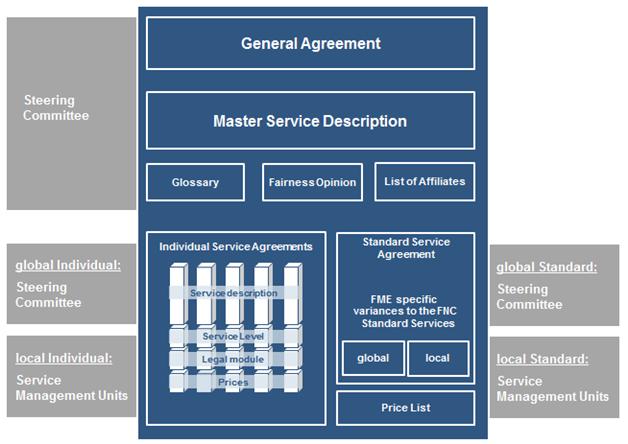

1. CONTRACTUAL STRUCTURE AND SCOPE OF APPLICATION

1.1 The complete agreement between the Parties and the contractual structure defined as “Set of Contracts” consists of:

a) this General Agreement; and

b) related documents (the Annexes) such as:

(i) Master Service Description;

5

(ii) Glossary

(iii) Fairness Opinion

c) Service Agreements

(i) Standard Service Agreements

(ii) Individual Service Agreements;

1.2 The Set of Contracts is structured in a modular basis:

a) This General Agreement provides the legal framework that shall govern the cooperation between, and the overall relationship and general obligations of, the Parties. The provisions in this General Agreement shall apply as a general agreement to all Annexes and Service Agreements hereto between FME and NETCARE on services provided in the area of information technology.

b) The Service Agreements, as mutually agreed, will define specific Services and provide detailed provisions on individual Services.

1.3 The following details shall be provided at a minimum:

6

a) Master Service Description (MSD)

(i) The MSD defines general processes, requirements and conditions for each Service or qualities for the Services.

(ii) MSD defines testing and acceptance procedures as well as general acceptance criteria for the Services.

(iii) MSD shall define the extent, type and purpose of the intended collection, processing or use of personal data, the type of data and categories of data subjects, if applicable to the type of services.

b) Service Agreements

(i) a specified description of the scope and the subject of the Services to be performed by NETCARE.

(ii) time and location of performance of Services.

(iii) tasks to be performed by FME and FME’s assistance.

(iv) reimbursements and service fees.

(v) definition of service levels and measure procedure.

1.4 Existing contracts already created as Annexes under the former General Agreement as of 8th December 2003 and not terminated until 31.12.2012 shall become an integral part of the Set of Contracts and shall remain in effect subject to the terms of this General Agreement without amendment under this General Agreement until their regular termination.

1.5 In cases of contradictions, clauses in Annexes shall supersede the clauses in this General Agreement, and clauses in Individual Service Agreements or Standard Service Agreements shall supersede the clauses in the General Agreement and the Annexes.

1.6 The individual Services to be provided by NETCARE may qualify as service, work, rent or similar type of contract under civil law or a combination of various types of contracts defined under civil law. The Parties shall mutually agree and define the relevant obligations and the type of contract in a Service Agreement, as far as possible, in order to clarify the applicable legal regulations and obligations of the Parties;

1.7 For the avoidance of doubt, the contractual provisions and principles set forth in the General Agreement, including but not limited to regulatory, data protection, shall only be subject to change in accordance with the change request procedure pursuant to

7

Section 7.

1.8 This General Agreement shall govern all future Services ordered by FME or any of FME EMEALA’s affiliates and rendered by NETCARE to FME or any of FME EMEALA’s affiliates, even where no explicit reference is made hereto, unless the applicability of the General Agreement has been explicitly excluded.

2. NETCARE’S DUTIES

2.1 NETCARE will provide Services in the area of information technology to FME. Individual Services and details are specified in the Annexes and Service Agreements.

2.2 NETCARE shall

a) render the Services in accordance with the provisions defined in the Set of Contracts and, where applicable and where defined, at the place/location defined in a specific service description in a Service Agreement or, if not defined, at the location mutually agreed by both Parties;

b) render its Services in compliance with applicable statutory accident prevention regulations, applying to NETCARE and FME, if notified by FME of the relevant regulations, as well as applicable statutory health and safety regulations;

c) deliver services in compliance with the current state of the art, as applicable from time to time, according to best practice, and free of material Defects with respect to specifications for the Services.

d) comply, and procure that any of its sub-contractors complies, with FME’s security and control regulations and systems provided that NETCARE has been notified hereof at a reasonable time before the commencement of NETCARE’s performance.

e) procure licenses as agreed in Section 11.

f) provide and use appropriate verification tools to monitor and measure compliance with any service levels agreed in a Service Agreement, whereas such verification tool shall be appropriate if it measures the items to be measured according to the verification method agreed between the Parties in connection with such service level; whether non-compliance with agreed service levels results in legal consequences shall be agreed in the relevant Annex or Service Agreement.

g) be obliged to comply with the license terms of the third party licensor and not use the software in violation of such license. In particular, NETCARE shall notify

8

FME of any violations of such license agreement and terms defined therein.

h) allow FME or an agent of FME to audit whether NETCARE’s use of the software is consistent with the rights granted to NETCARE herein upon request by FME and provided there is a legitimate interest therein and to give full cooperation to FME or its agent carrying out such audit. In case of an audit by the licensor with respect to compliance of FME with the licensing conditions, NETCARE shall reasonably assist FME in providing the information reasonably requested by the licensor in connection with such audit.

2.3 Unless explicitly agreed otherwise between the Parties, NETCARE shall not be obliged to consult with FME when modifying or changing any hardor software, or amending any system, used for rendering a Service, unless the modification or change adversely affects the performance of NETCARE or the compliance with any service levels agreed or the compliance with privacy law;

2.4 NETCARE is not obliged to deliver the source code unless such obligation is agreed upon in the Service Agreements.

3. USE OF SUBCONTRACTORS

3.1 NETCARE may use subcontractors for rendering the services in its own discretion. In no event will NETCARE be relieved of its obligations under this General Agreement as a result of its use of any subcontractors. NETCARE shall inform FME of any subcontractors used upon written request of FME.

3.2 NETCARE’s obligations for imposing duties of secrecy and compliance with an obligation towards FME on subcontractors shall be governed by Section 8 and 9 and NETCARE shall ensure that all subcontractors are subject to and comply with the same obligations as are imposed on NETCARE under the terms agreed in the Set of Contracts.

3.3 If FME determines that a subcontractor has to be replaced for good reasons, FME shall notify NETCARE explaining the reasons for such a replacement. Following receipt of this notification, NETCARE will promptly, or within such period of time reasonably agreed by the Parties, replace such a subcontractor by another third party or by NETCARE’s personnel. A good reason exists, in particular, if

a) a supervisory authority objects to or prohibits the engagement of a specific subcontractor or the subcontracting with respect to the services rendered by the subcontractor;

9

b) any rights or interests of FME or any of its affiliates with respect to confidentiality, data protection or data security are at risk;

c) a subcontractor engaged in data processing relocates its activities or the data processing or parts thereof to a country outside of the EU;

d) a competitor of FME holds or acquires more than 25% of the interests or voting rights in the subcontractor.

4. FME’S DUTIES

4.1 FME shall

a) provide all required reasonable assistance and co-operate with NETCARE including

· the assignment of competent staff to a reasonable extent for problem solution.

· the assignment, supervision and control of FME staff and capacities.

· the assurance that FME employees will comply with FME´s guidelines implemented for the use of the services, data and applications.

b) provide to NETCARE all relevant information and documentation reasonably required by NETCARE for the provision of the Services under the Set of Contracts, including any (internal) guidelines or regulations NETCARE shall comply with when providing the Services.

c) if required, grant NETCARE and its agents and subcontractors access to FME’s premises and equipment free of charge for the time reasonably expectable for an appropriate performance under this Set of Contracts, at least during FME’s regular business hours.

d) assist and cooperate with NETCARE in implementing any changes or system requirements, i.e. by allowing NETCARE to train FME personnel.

e) be obliged to comply with the license terms of the third party licensor and not use the software in violation of such license. In particular, FME shall notify NETCARE of any violations of such license agreement and terms defined therein.

f) allow NETCARE or an agent of NETCARE to audit whether FME’s use of the software is consistent with the rights granted to FME herein upon request by

10

NETCARE and provided there is a legitimate interest therein and to give full co-operation to NETCARE or its agent carrying out such audit. In case of an audit by the licensor with respect to compliance of NETCARE with the licensing conditions, FME shall reasonably assist NETCARE in providing the information reasonably requested by the licensor in connection with such audit.

4.2 The Parties shall agree on the specifications of any required assistance and cooperation in connection with a service and an Annex or Service Agreement.

5. COOPERATION

5.1 The Parties shall

a) co-operate in good faith;

b) appoint relevant key personnel with respect to the overall management of the Set of Contracts and the cooperation between the Parties and shall ensure that such key personnel will only be replaced for good cause;

c) appoint responsible personnel and contact persons for the coordination and general management of the Services under this General Agreement, the MSD, other Annexes and Service Agreements;

d) inform the other Party of any circumstances that may have an impact on the provision of the services and result in a default with respect to the services as well as any actual default or remedy of defaults;

e) agree on and comply with a defined communication and escalation process which shall leave the obligations of the Parties under the Set of Contracts unaffected, in particular any retention rights or rights to non-performance shall be excluded;

f) co-operate and provide reasonable assistance for transition and migration of the relevant services after termination of any Annex, Service Agreement or this General Agreement.

g) agree on the performance of license management for FME.

6. PRICES, INVOICE, PAYMENTS

6.1 All prices, conditions of payment, and schedules are subject to written agreements, and shall be as defined in the MSD and the Service Agreements, if Individual Services are concerned. As regards Standard Services, fees shall be equal to the up-to-

11

date prices listed in the price list for standard services of NETCARE, published, updated and agreed with FME each year.

6.2 Services, where no fees have been agreed, shall be rendered according to the hourly or daily rate in accordance with latest price list as per 6.1.

6.3 Prices shall be renegotiated and reasonably be modified if a Service Agreement is modified or amended.

6.4 A price adjustment clause may be incorporated if applicable in any individual Service Agreement.

6.5 Prices are net prices plus the applicable VAT (value added tax, in Germany currently 19%) and as determined in the specific Service Agreement.

6.6 Payments hereunder shall be made in EURO.

6.7 The payment terms should be agreed between NETCARE and the respective affiliate invoiced in a separate or the relevant Service Agreement. For Germany payment terms shall be according to the applicable Fresenius group procedures. A written invoice shall be provided to the respective affiliate even though the booking is done by EDI. Outside Germany, a payment range between 30 —60 days shall be applied.

6.8 Overall NETCARE shall offer to FME competitive prices in the average for a Group of Services, based on the costs for the individual Services. FME shall be entitled to request a review of the prices for a Group of Services. Upon such request, the Parties shall make a benchmarking evaluation. If NETCARE’s prices are out of market range after such benchmarking evaluation, FME shall have the right to request an alternative offer from NETCARE within a period of one month after the benchmarking results. NETCARE shall have a period of three month to prepare such an offer. If FME accepts the alternative offer, acceptance may not be unreasonably withheld, adjusted pricing shall apply with retrospective effect from the date of receipt of FME’s request for an alternative offer. The same procedure shall apply as far as NETCARE’s prices are below market prices whereas NETCARE shall be entitled to submit the alternative offer to FME without request from FME and FME shall be obliged to reasonably accept the alternative offer. If a benchmark of the prices for a Group of Services has been conducted, FME shall not request another review for the next three years after completion of the benchmarking process. Upon request, the Parties shall make a benchmarking evaluation.

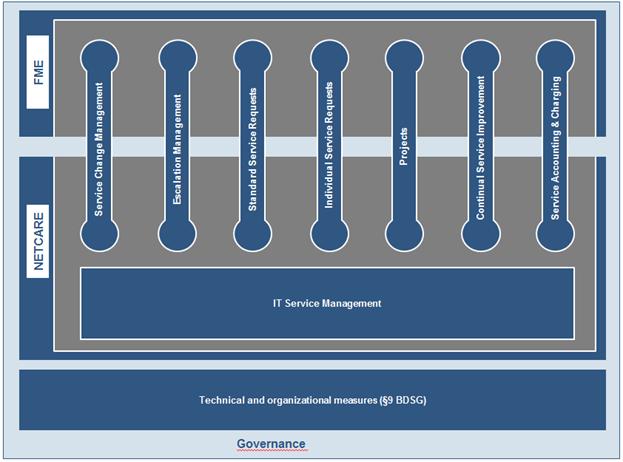

7. GOVERNANCE STRUCTURE AND CHANGE REQUEST PROCEDURE

7.1 The Parties agree to implement and appoint certain committees and boards for the

12

coordination of the cooperation between the Parties. The governance structure shall have the following three levels:

a) Management Board: strategic level

b) Steering Committee: tactical level

c) Operation Units: operational level.

7.2 Obligations and tasks of each level, the constitution and composition of each level as well as escalation procedures shall be governed by and defined in the MSD.

7.3 Each Party shall have the right to request in writing a change to the contractual arrangements between the Parties, as agreed in the Set of Contracts, including the processes defined in the MSD, the Services or specifications.

a) Changes with an impact on the specifications or scope of the Services shall be subject to the change procedures defined in the MSD. The following provisions shall apply to any changes to the contractual provisions of this General Agreement or any processes defined in the MSD, the Attachments or any general provisions in the Annexes or Service Agreements that are meant to provide a deviation from the provisions in this General Agreement or the MSD and that do not have an impact on the content or scope of a Service, the service fees or alike (“Contractual Change”).Subject to the terms and conditions of this General Agreement, NETCARE shall undertake to comply with FME’s reasonable requests for a Contractual Change provided that the Parties have agreed in writing on the effects of any Contractual Change on this General Agreement or its Annexes.

b) If provisions in the Set of Contracts are erroneous, incomplete, ambiguous, or impossible to fulfill for anybody, the Parties shall upon request of one Party decide without undue delay on modifying and completing such provisions.

c) If changes in applicable laws, orders of authorities or courts have an impact on the Services or the Set of Contract or make changes to the Services or Set of Contract necessary, NETCARE shall implement such changes upon request of FME or in its own discretion provided that NETCARE will inform FME of such change. The Parties will mutually and reasonably agree on the relevant contractual changes necessary.

d) Neither Party shall unreasonably withhold or delay its consent to a Contractual Change. Any Contractual Change agreed between the Parties shall be made in writing and signed by the Parties.

13

e) Contractual Changes shall be discussed and agreed on the level of the Steering Committee.

8. CONFIDENTIALITY

8.1 Each Party shall keep strictly confidential

a) all documents, information, and data, and

b) all trade secrets or confidential information proprietary to one of the Parties or a third Party disclosed to her or obtained by her incidental to the cooperation under the Set of Contracts (Confidential Information). Confidential Information shall include without limitation know-how, details of orders, contractual provisions and prices.

8.2 The Parties shall disclose Confidential Information as defined in Section 8.1 to third Parties only upon prior written consent of the other Party. The Parties shall put all third Parties or companies who may receive Confidential Information or who are retained under this General Agreement under the same obligations as the respective Party has entered into.

8.3 Subcontractors obtained by NETCARE shall not qualify as third parties under Section 8.2, provided that such subcontractors are under an obligation to keep information confidential at least as protective as the confidentiality provisions under this General Agreement and that the breach of such obligation shall be punishable by an adequate penalty. Confidential Information shall only be disclosed to subcontractors on a need to know basis.

8.4 This obligation to keep confidential does not include

a) information which is now or hereafter becomes part of the public domain in other ways than by faults, acts or omissions of the Receiving Party;

b) information which hereafter lawfully comes into the Receiving Party’s possession from an independent third source without any obligation of secrecy;

c) information which the Receiving Party can show by sufficient evidence was in the Receiving Party’s possession prior to the time of receipt from the Disclosing Party, or information or knowledge which was independently developed by or for the Receiving Party without access to any of the Confidential Information disclosed hereunder.

d) information which the Receiving Party has an obligation or duty to disclose under applicable law or by order issued by the competent courts, provided

14

Disclosing Party is given a reasonable opportunity to review the planned disclosure and discuss the need for such with Receiving Party prior to the actual disclosure;

8.5 FME shall ensure that any user names and passwords are kept confidential and that only authorized users use the Services and licenses rendered by NETCARE. User names and passwords shall not be disclosed to an third Party and shall be kept confidential in order to prevent access of not authorized third Parties.

9. PRIVACY LAW/SAFETY/COMPLIANCE WITH GXP/ORDER-DATA PROCESSING

9.1 NETCARE shall comply with the data protection, data safety and security obligations imposed on FME by the applicable laws and regulations and the provisions of the Network Security Guideline of Fresenius Medical Care AG & Co. KGaA provided to NETCARE by FME.

9.2 For that reason and according to requirements imposed on FME by law, regulations and safety aspects, FME has to insist on the obedience of the following terms and conditions. NETCARE acknowledges these terms and conditions as being mandatory for FME to comply with laws, regulations and safety aspects and for the fulfillment of FME’s business.

9.3 NETCARE shall be liable to FME that

a) NETCARE follows FME’s instructions with regard to the creation and implementation of user profiles; and

b) system architecture shall maintain the security and consistency of the data, and access by FME officers, employees and agents shall be according to the user profiles; and

c) each of FME’s employees shall have unhindered access to FME’s proprietary data unless such access is restricted by the user profile and/or FME’s other instructions; and

d) no third Party (including employees or representatives of further companies of the Fresenius SE & Co. KGaA group of companies) shall, at any time, have access to FME’s data.

9.4 FME shall be entitled to audit and/or qualify NETCARE with respect to the current quality management system and the quality management system envisioned to be implemented under section 9.5, the internal control system prescribed by FME’s corporate governance regulations, and/or, at FME’s choice, to let have an external auditor audit and/or qualify NETCARE once a year, or as deemed necessary, but reasonably

15

acceptable for NETCARE, in order to assure that NETCARE complies with its contractual obligations. Prior to such FME or third Party audit, FME shall give NETCARE timely prior written notice and FME or third Party access shall be limited to NETCARE’s normal business hours.

9.5 NETCARE shall be obliged to maintain a quality management system meeting the requirements agreed in a separate quality assurance agreement. The quality assurance agreement shall define responsibilities, scope, regulatory requirements, validation and documentation requirements, among others.

9.6 In general Netcare shall ensure that FME’s GxP-critical applications and data, as expressly defined by FME, are maintained and archived in a GxP-compliant way. Netcare shall ensure that all FME GxP-critical systems, applications and data will be operated GxP-compliant in accordance to the specifications as set forth in the applicable Service Agreement and instructions of FME. Further requirements concerning archiving and disaster recovery as well as how FME and Netcare work in GxPcritical projects shall be defined in the quality assurance agreement.

9.7 Whenever FME shall be obligated by the applicable laws, regulations or requirements imposed on FME by the competent authorities or agencies to change, amend or modify its quality as well as corporate governance standards in order to fulfill the regulatory requirements for FME’s business, NETCARE shall be obligated to follow any of such FME’s requests in order to comply with any such changes, amendments or modifications. Any changes shall be made by applying the change procedures defined in this General Agreement or the MSD, as applicable.

9.8 FME’s business is strongly regulated by governmental authorities. Due to regulation changes FME may be forced to changed business processes that may also affect NETCARE’s duties and may require NETCARE to exceed any cur r ent st andards, i. e.the requirements defined in the qualit y assur ance. As f ar as t he im plem ent at ion of such changes tr igg er s any m at er ial cost s NETCARE shall inform FME before implementation of such changes or requirements. Both Parties shall agree in accordance with the change procedures defined in this General Agreement or the MSD, as applicable, on the implementation of such changes and document in writing such changes and related costs. FME shall compensate NETCARE for any costs related to such changes based on the related effort and expenses.

Any measures and related costs in connection with the implementation, application and maintenance of any internal control system required by FME or FME’s corporate governance regulations shall be agreed in a separate Annex or Service Agreement.

16

10. ORDER-DATA PROCESSING (AUFTRAGSDATENVERARBEITUNG)

10.1 The Parties acknowledge that NETCARE (as the processor) will provide services to FME (as the controller) on basis of order-data processing (Auftragsdatenverarbeitung). The following rules apply to all activities in which the staff of NETCARE or a third party acting on behalf of NETCARE may come into contact with Personal Data of FME. Personal Data means any individual element of information concerning the personal or material circumstances of an identified or identifiable natural person (individual).

10.2 Duration (term) and subject of the order-data processing shall be defined in the Master Service Description, the Standard Service Agreement or the Individual Service Agreement — whichever is applicable.

10.3 The extent, type and purpose of the intended collection, processing or use of personal data, the type of data and categories of data subjects are stipulated in Section 1 of this General Agreement.

10.4 NETCARE shall take the appropriate technical and organizational measures to adequately protect FME’s Personal Data against misuse und loss in accordance with requirements of section 9 of the German Federal Data Protection Law (Bundesdatenschutzgesetz; hereinafter: BDSG). The measures are defined in the Master Service Description and may be expanded in Standard Service Agreements or Individual Service Agreements.

10.5 The technical and organizational measures are subject to technical progress and development, and NETCARE may implement adequate alternative measures in accordance with Section 7.3 of this General Agreement. These must not however fall short of the level of security provided by the specified measures. Any material changes must be documented.

10.6 FME and NETCARE are aware of the fact that, at present, NETCARE operates its services under the Set of Contracts through a “one-client-system”, i. e. FME and further companies of the Fresenius SE & Co. KGaA group of companies are within the same “client-system”.

10.7 NETCARE is obliged to rectify, erase or block the Personal Data processed in accordance with the reasonable instructions of FME. NETCARE shall take the necessary precautions to ensure that Personal Data can be rectified, erased or blocked in its systems.

10.8 If a data subject (individual person) should apply directly to NETCARE to request the correction or deletion of his Personal Data, NETCARE must forward this request to

17

FME without delay, unless the correction or deletion is part of the specific service.

10.9 NETCARE shall collect, process and use Personal Data only within the Set of Contracts. NETCARE may not use Personal Data for any other purposes, including its own purposes.

10.10 NETCARE shall ensure that any personnel entrusted with processing FME’s Personal Data have undertaken to comply with the principle of data secrecy in accordance with section 5 of the BDSG and have been duly instructed on the obligations of NETCARE to protect Personal Data. The obligation of confidentiality shall continue after their employment ends.

10.11 NETCARE shall monitor compliance with the provision of this section by means of regular tests.

10.12 Where stipulated by law, NETCARE shall appoint a data protection officer, able to discharge his duties as set out in sections 4f and 4g of the BDSG. The officer’s contact details must be supplied to FME to enable direct contact to be made.

10.13 Upon FME’s request, NETCARE shall provide all information necessary for compiling the overview defined by section 4g (2) sentence 1 of the BDSG.

10.14 NETCARE may use sub-contractors according to Section 3 of this General Agreement.

10.15 FME must be granted the right to monitor and inspect the sub-contractor in all cases of order-data processing.

10.16 In addition to Section 10.7 of this General Agreement, FME may carry out the job control stipulated in No. 6 of the annex to the BDSG, or appoint auditors to do so.

10.17 NETCARE shall provide FME with the information required to meet its job control obligation, and shall make the necessary documentation available.

10.18 With regard to the monitoring obligations of FME under section 11 (2) sentence 4 BDSG before the start of data processing and throughout the term of the commission, NETCARE must ensure that FME can confirm adherence to the technical and organizational measures taken. For this purpose, NETCARE must provide FME upon request with evidence of the implementation of the technical and organizational measures pursuant to section 9 of the BDSG and the annex thereto. Evidence of the implementation of any measures that do not only affect the specific commission may also be presented in the form of up-to-date attestations, reports or extracts thereof from independent bodies (e.g. external auditors, internal audit, the data protection officer, the IT security department or quality auditors) or suitable certification by way of

18

an IT security or data protection audit.

10.19 In addition to Section 5 of this General Agreement, NETCARE shall notify FME in all cases of violations of data protection provisions.

10.20 Where FME’s Personal Data becomes subject to search and seizure, an attachment order, confiscation during bankruptcy or insolvency proceedings, or similar events or measures by third parties while being processed, NETCARE shall inform FME without undue delay. NETCARE also shall, without undue delay, notify to all pertinent parties in such action, that any Personal Data affected thereby is in FME’s sole property and area of responsibility, that Personal Data is at FME’s sole disposition, and that FME is the responsible body in the sense of the BDSG.

10.21 The Parties are aware that section 42a of the BDSG may impose a duty to inform in the event of the loss or unlawful disclosure of Personal Data or access to it. Such incidents should therefore be notified by NETCARE to FME immediately, regardless of their origin. This also applies to serious operational faults or where there is any suspicion of an infringement of provisions relating to the protection of Personal Data or other irregularities in the handling of Personal Data belonging to FME. In consultation with FME, NETCARE must take appropriate measures to secure the data and limit any possible detrimental effect on the data subjects. Where obligations are placed in FME under section 42a of the BDSG, NETCARE must assist in meeting them.

10.22 FME is responsible for compliance with the BDSG and other relevant regulations on data protection, and retains control over the extent of the data to be processed.

10.23 FME shall have the right to give NETCARE reasonable instructions as to the nature, scope and method of data processing. The proceeding of FME’s authority to issue instructions is stipulated in Section 7 of this General Agreement.

10.24 Any changes to the subject-matter of the processing must be agreed in writing by the Parties and documented together.

10.25 NETCARE shall inform FME immediately if NETCARE believes that an instruction violates privacy laws. NETCARE may then postpone the execution of the relevant instruction until it is confirmed or changed by FME.

10.26 After the termination of a commission under this General Agreement NETCARE must return to FME all of FME’s Personal Data in NETCARE’s possession and all Personal Data collected and produced in connection with the commission, or delete them with the prior written consent of FME. The deletion log must be presented upon request.

10.27 Documentation intended as proof of proper data processing must be kept by NETCARE beyond the end of the Set of Contracts in accordance with relevant retention

19

periods. NETCARE may hand such documentation over to FME after expiry of this General Agreement or its Annexes.

11. RIGHTS OF USE AND INTELLECTUAL PROPERTY RIGHTS

11.1 NETCARE shall procure, operate and maintain any software, licenses and rights needed by NETCARE for the provision of the Services.

11.2 As a matter of principle, NETCARE shall procure and acquire licenses and rights in connection with the Services in its own name and sublicense such licenses or grant to FME the rights of use for software or other deliverables to the extent required by FME in connection with, or as a result of, the relevant Service Agreement for the use of the Services under the Set of Contracts in accordance with the provisions defined in this Section 11, unless otherwise agreed in a Service Agreement.

11.3 Any rights granted by NETCARE to FME under this Agreement shall not entitle FME, without NETCARE’s prior consent, to modify, decompile, translate, decrypt, decompose, or copy the deliverable, unless otherwise expressly agreed herein or in a Service Agreement.

11.4 With respect to third party standard software or NETCARE’s own software, not specifically and exclusively developed for FME, which is used by NETCARE to provide the Services (“Standard Software”), NETCARE shall grant FME the non-exclusive, nontransferable right to use without limitation in time, scope or place subject to the terms of this General Agreement and the relevant Service Agreement, in particular limited to the purpose described in the relevant Service Agreement. The scope of the right of use of FME shall be in accordance with the license and right of use granted by the third party licensor to NETCARE. NETCARE shall ensure that it will obtain all required rights and licenses to sub-license or transfer the license to FME for the required purposes.

11.5 To the extent that any rights derive from software or other deliverables expressly developed for and on behalf of FME by NETCARE, including new developments of interfaces, platforms, changes, etc., provided that NETCARE has not used any proprietary software of NETCARE or any third party, any intellectual property rights shall vest in FME and FME shall be the owner of any intellectual property rights in connection with such deliverable. FME grants to NETCARE the non-exclusive, transferable right to use, to copy, to revise and to decompile the deliverables without limitation in time, scope or place subject to the terms of the Set of Contracts. The right to use is limited to the purposes described in the Service Agreement applicable to the relevant deliverable. The right to copy, revise and decompile the deliverable shall be limited, however, to the maintenance or reinstatement of the agreed functionality of the deliverable.

20

11.6 As far as NETCARE develops any deliverable only partly for and on behalf of FME or FME only partly reimburses the costs associated with a deliverable, NETCARE and FME shall be co-owners of such deliverable in the proportion of the relevant contribution to the development of the deliverable. FME shall have the non-exclusive, transferable right to use the deliverable for the purpose of this General Agreement. NETCARE shall have the non-exclusive, transferable right to use, to copy, to revise and to decompile the deliverables without limitation in time, scope or place subject to the terms of the Set of Contracts. The right to use is limited to the purposes described in the Service Agreement applicable to the relevant deliverable. The right to copy, revise and decompile the deliverable shall be limited, however, to the maintenance or reinstatement of the agreed functionality of the deliverable. NETCARE shall have the right to sublicense such rights to affiliated companies and to provide maintenance, update and upgrade services with respect to the deliverables to such affiliated companies as agreed between the Parties in a Service Agreement.

11.7 In case of developments, updates, upgrades and changes to Standard Software or NETCARE’s proprietary software, provided that such updates and upgrades are not available on the market, including customizing and adjustments to general structures, systems, configurations, scripts and other customizing, NETCARE shall grant FME the non-exclusive, transferable right for the term of this General Agreement to use the developments in connection with the basis software without additional charges.

11.8 Own developments of NETCARE shall be solely in the property of NETCARE. Any rights of use of FME shall be granted in accordance with Section 11.4.

11.9 As far as FME has acquired licenses or rights in connection with a Service from a third party, that are required for the use of the Services, or FME is obliged in connection with a Service to provide standard software or other individual software developed for FME, FME shall grant to NETCARE the non-exclusive, non-transferable right to use the software or deliverables for the purposes and as far as necessary for the provision of the Services to FME under the Set of Contracts. As far as necessary for the provision of the Services FME shall also grant NETCARE the right to copy, revise and decompile the software, whereas such right shall be limited to the maintenance or reinstatement of the agreed functionality of the software. The Parties shall agree on the specific rights in the relevant Service Agreement. The scope of the right of use of NETCARE shall be in accordance with the license and right of use granted by the third party licensor to FME. FME shall be obliged to ensure that any relevant license permits NETCARE’s use of any licensed rights granted hereunder to NETCARE for the required purpose and FME shall inform NETCARE of any license terms applicalble. NETCARE shall be obliged to comply with the license terms of the third party licensor and not use or revise the software in violation of such license. In particular, NETCARE shall notify FME of any violations of such license agreement and terms

21

defined therein.

12. DEFECTS AND WARRANTY

12.1 NETCARE shall render its Services in accordance with the service levels defined, if any, or any specifications defined in the relevant Service Agreement and the Services shall be free of defects of priority 1, 2 and 3. Services rendered by NETCARE or its subcontractors not complying with the aforementioned standards shall be deemed “Defects”.

12.2 In the event of Defects of an agreed product or works that shall be supplied, FME’s claims shall expire twenty four months after delivery of the respective product or works. FME shall notify NETCARE of any Defects immediately upon delivery, or in case of hidden Non-Conformities upon discovery, at the latest within 10 business days.

12.3 NETCARE shall have opportunity to cure all Defects free of charge and within reasonable time. NETCARE may choose to remedy by repair or redelivery within its discretion. NETCARE shall have two attempts to remedy a Defects. If NETCARE fails to cure before an appropriate dead-line set by FME expires FME may appropriately reduce the price. If said Defect that has not been remedied by NETCARE does not affect economically reasonable uses of the remaining parts of services or goods which NETCARE has delivered or shall deliver and FME makes such use thereof, FME’s rights shall be limited to the defect service or part of NETCARE’s performance. Save for the provisions in Section 15 FME shall have no right to terminate the relevant Service Agreement or this General Agreement due to a Defect.

12.4 Unless otherwise agreed between the Parties in this Section 12 any Defects shall be regulated by the relevant warranty provisions defined by statutory law, as applicable to the Service.

13. LIABILITY

13.1 Either Party shall be liable without limitation for all damages caused by intent or gross negligence of the Party or its vicarious agents as well as Defects fraudulently concealed and all mandatory statutory liability.

13.2 Parties shall be liable for all personal injuries up to an amount of Euro 500,000 (five hundred thousand Euros) for each incident, in a total for all such damages up to an amount of Euro 5,000,000 (five million Euros), provided that such liability is not covered by section 13.1. For all other civil liability arising out of slight negligence by the Parties and their relevant vicarious agents not covered by section 13.1 or 13.2 the following applies:

22

a) for all damages to material objects (Eigentumsverletzungen) in the property of or leased by FME which are caused as a direct consequence of the services performed under the Set of Contracts, such as but not limited to excess of voltage, damages to hard and software due to services rendered under the Set of Contracts the injured Party may recover the amount necessary for repair or for compensation of such damages up to an amount of Euro 2,000,000 (two million Euro) for each incident.

b) For all damages caused by negligent breach of contract, such as but not limited to system break-downs and which FME has to incur in accordance with claims of third contractors which cannot be solved amicably, FME is to be held harmless by NETCARE by a calendar-year compensation cap up to 15% (Fifteen percent) of the contractual value of the respective Service Agreement reduced by the penalty, if any, as defined in the respective Service Agreement. NETCARE shall be informed about the facts underlying such case in a maximum transparent manner. FME shall use best efforts to defend such cases.

c) No Party shall be liable for lost profits, potential savings, consequential or indirect damages.

13.3 Should NETCARE be held liable for a breach of contract or other liability, FME’s contributory fault shall be reasonably considered. NETCARE shall not be liable for damages caused by instructions, information, documents, materials, or contributions or support provided by FME to NETCARE.

13.4 NETCARE shall in no instance be liable for deficiencies of software, assistance or other appliances that FME has ordered from third parties or that FME has provided. NETCARE shall support FME by problem solving with best effort against compensation, if not agreed otherwise within the specific Service Agreement. NETCARE shall in no event be liable under this Section 13 if FME (without NETCARE’s written approval) or a third party has modified Services delivered by NETCARE, FME has used the Service in breach of the Set of Contracts (handling error), FME has not provided its cooperation obligations in a proper or timely manner, the Defect arises from instructions of FME provided that NETCARE has notified FME of the associated risks that lead to the Defect.

13.5 In the event that NETCARE retained a subcontractor upon FME’s sole and specific request to use such subcontractor, NETCARE hereby assigns all its claims and rights vis-á-vis such subcontractor under the relevant contract with the subcontractor to FME. To the extent of such assignment, FME’s claim against NETCARE shall be fulfilled and NETCARE shall not be liable for any damages, losses or claims of FME or any third party resulting from the services of such subcontractor. FME authorizes NETCARE to make any claims and enforce any claims against such subcontractor.

23

NETCARE shall reasonably enforce any claims out of or in courts and FME will assist NETCARE in any actions. NETCARE shall in any event consult and coordinate any actions with FME and follow instructions of FME in connection with the enforcement of a claim. The aforementioned shall also apply in case NETCARE has integrated or used a certain product or software or procured such product or software from a designated subcontractor upon FME’s request.

13.6 NETCARE shall be responsible for the services and contractual deliverables rendered by its own subcontractors to the same extent NETCARE itself is liable for the Services. Contractual partner of subcontractors shall solely be NETCARE and the scope of services to be rendered by NETCARE to FME shall not be affected by the use of subcontractors.

13.7 The aforementioned provisions shall apply to the personal liability of all statutory representatives, senior management, agents, subcontractors and employees as far as these qualify as vicarious agents of the relevant Party.

13.8 NETCARE shall be excused from performance of its obligations and the Services under this General Agreement, any Annex and Service Agrement affected and shall not be held liable for any losses, damages or delays, including consequential damages, resulting from any event or cause beyond its reasonable control, including earthquake, fire, flood, explosion, war, embargo, transportation shortage or delay, breakage of machinery or electric power outage.

14. PENALTIES

14.1 The sum of any penalties accrued under the Set of Contracts for the period of one year shall not exceed 5 % of the total remuneration under the Set of Contract, excluding remuneration for Projects, for the previous year. For the purposes of this section the yearly remuneration and sum of penalties shall not be calculated on the basis of the calendar year but on a rolling basis, i.e. the 12 months prior to the event triggering the penalty.

15. TERM AND TERMINATION

15.1 The term of this General Agreement shall commence on January 1, 2013 and shall extend to December 31, 2017. Thereafter, the General Agreement shall automatically renew by another period of five years unless one Party terminates the agreement by giving six months prior written notice to the end of the term. From then on the General Agreement will be extended automatically for successive one year periods unless one of the parties terminates this General Agreement by giving 6 months prior written notice to the expiration of the then current term.

24

15.2 The Parties shall be entitled to terminate individual Service Agreements by giving 6 months written notice prior to the end of the agreed term unless otherwise agreed under applicable termination clauses in the Service Agreements.

15.3 Each Party shall be entitled to terminate this General Agreement and the Set of Contracts in whole or in part with immediate effect by giving written notice if (a) the other Party becomes insolvent, (b) the other Party is the subject of any winding up, dissolution, insolvency or liquidation proceedings, or makes any assignment of materially all assets for the benefit of creditors, (c) the other Party terminates its business in whole or in substantial part, or (d) in case of a merger or acquisition, whereby the common shareholder Fresenius SE & Co. KGaA transfers its controlling interest, be it by transfer of assets or by transfers of shares or dilution of the interest of Fresenius SE & Co. KGaA, in the non-terminating Party to a third Party which is not under the control of Fresenius SE & Co. KGaA.

15.4 Furthermore, FME shall be entitled to terminate the Set of Contracts upon giving reasonable notice, if NETCARE (i) unreasonably restricts FME from accessing data for processing in other systems; (ii) breaches the terms and conditions of Sections 9.1, 9.3, 9.5, 9.6 or 9.7 above and/or (iii) after discussion in the Steering Committee, will not be able to comply with the terms and conditions as outlined under Sections 9.1, 9.3, 9.5, 9.6 or 9.7 above.

16. EFFECT OF TERMINATION/EXPIRATION

16.1 The termination of this General Agreement shall not affect the term of its Service Agreements or any Annex and no such Service Agreement or Annex shall be terminated unless expressly and separately terminated by the terminating Party. In case of a termination of this General Agreement the terminating Party shall have a special termination right with respect to each Annex and Service Agreement being part of the Set of Contracts.

16.2 The termination of a Service Agreement or Annex shall not affect this General Agreement or any other Annex or document of this Set of Contracts unless expressly agreed for certain cases in Section 16.

16.3 After termination or expiration of the contractual relationship the Parties shall undertake to modify the remainder of the Set of Contracts as economically indicated and according to the factual situation. Furthermore, they shall return all documents and other information which they have received from the other Party because of or incidental to the cooperation upon first request. The correspondence between the Parties and all documents and papers that have to be kept available as required by laws or

25

regulations or papers and documents that are destined to remain with the respective Party.

16.4 After termination of the General Agreement or Service Agreement hereto, NETCARE shall be obliged to deliver the services agreed upon hereunder to FME upon FME’s request for such period which is required by FME to retain an alternative service provider. FME’s obligations defined under Section 4 shall remain in effect for such transition period. However, FME shall not be required to buy these services from NETCARE. In case that FME decides to discontinue individual services or parts thereof NETCARE shall not be responsible for the remainder of the services to be delivered to FME, provided, that the discontinued services were required for rendering the remainder of the services. Furthermore, NETCARE shall reasonably cooperate with FME on the transfer of any services or system operated or maintained under this Set of Contracts to an alternative service provider. Remuneration for services rendered and other terms and conditions for this transition period shall be analogous to the terms of this General Agreement or any Service Agreement referred to of the year of termination. Additional services required for the transition or migration of services to an alternative service provider shall be agreed separately and shall be compensated by FME in accordance with the agreed prices in the relevant up-to-date price list of NETCARE or as separately agreed.

16.5 Details regarding the services and transfer of data shall be agreed upon in the Steering Committee. As far as an agreement about the reintegration and continuation of the services has not been achieved within 3 months after written notice, an external Party shall be commissioned for defining the scope of services to be rendered by NETCARE and FME’s or any third Parties responsibilities and assistance. The external Party shall be nominated by FME and NETCARE in mutual agreement, however, if such consensus cannot be reached by FME and NETCARE, the arbitrator under Section 17.3 shall nominate the external Party.

16.6 NETCARE shall grant to FME upon termination/expiration of the contractual relationship a license for the use of all intellectual property rights owned by NETCARE at the time of termination/expiration of the contractual relationship, with respect to NETCARE’s own developments, including modifications, add-ons, developments, required to operate and run the system governed by and arising out of the Set of Contracts. Such license shall be non-exclusive, unlimited, unrestricted and shall include the right to grant sublicenses to re-outsourcers for the purposes of providing services to FME, however, the right to grant further sublicenses shall not be included. Such license shall be granted free of charge and shall enable FME for further development for internal purposes.

16.7 Upon termination of this Set of Contracts, neither tangible nor intangible assets shall be transferred from NETCARE to FME and neither claim for such transfer shall vest in

26

FME except for those where FME is the owner of such tangible or intangible assets. Additionally, FME shall in no event actively pursue employment of employees of NETCARE during the term of the General Agreement and for the period of two years thereafter.

16.8 Upon termination of this General Agreement and/or its applicable Annexes and Service Agreements under the Set of Contracts FME shall neither be entitled without the prior written consent of NETCARE nor shall FME be contractually obligated to take over any employee of NETCARE. In the event FME is obligated to take over such employees or employment contracts according to the respective law, NETCARE shall be obligated to compensate FME any costs and expenses which FME might incur thereby for employees FME is not willing to take over provided that FME is not actively deploying such employees.

16.9 The following provisions shall survive a termination of this General Agreement and shall remain in effect upon a termination for a period of at least five years or applicable storage and documentation obligations, whichever is longer: Sections 5, 8, 9, 13, 16, 17, 18.

17. GOVERNING LAW, ARBITRATION

17.1 The Set of Contracts shall be governed by the laws of Germany (excluding UN-CISG and the rules and principles on the conflict of laws).

17.2 Any dispute, controversy or claim, arising out of or in connection with the Set of Contracts, or the breach, termination or invalidity thereof (the “Controversies”), shall be governed by the following dispute resolution mechanism:

17.3 Controversies shall be settled amicably between the Parties on operational level and according to the escalation procedure as defined in the MSD. If the Parties are unable to reach a mutual consensus, the Parties shall be entitled to file for arbitration complaints in the arbitration panel of the Deutsche Gesellschaft für Recht and Informatik e.V. (“DGRI”), according to its Rules of Arbitration. The place of arbitration shall be in Frankfurt am Main, Germany. The numbers of arbitrators shall be [3]. English shall be used in the arbitrational proceedings.

17.4 In order to allow the arbitration to proceed the Parties waive the defense of expiration of statute of limitation for all claims arising in the disputed matter, starting with the request for arbitration filed with the DGRI and until one month after the end of the arbitration process. The expiration of statute of examination shall be suspended for the time of the arbitration proceeding.

17.5 The decision of the arbitration panel shall be binding.

27

18. MISCELLANEOUS

18.1 All Annexes, the Attachments, and the Preamble are incorporated into this General Agreement. The Preamble shall reflect the intentions of the Parties as of the effective date of the General Agreement and shall have legal effect, however, only insofar as it may be used for interpretative purposes in case of controversy over the interpretation of certain clauses in the General Agreement, Annexes or the Attachments or if Section 17 is applicable.

18.2 Neither Party’s general terms and conditions (Allgemeine Geschäftsbedingungen) shall be incorporated in this Set of Contracts.

18.3 The rights inuring to the benefits of the Parties under the Set of Contracts shall be non-transferable unless the other Party has agreed to the transfer in writing. Such consent shall not be unreasonably withheld if the rights are transferred to Parties under common control of Fresenius SE & Co. KGaA or Fresenius Medical Care AG & Co. KGaA.

18.4 No action or inaction of one of the Parties shall be construed as a waiver of rights or shall affect such rights, unless this General Agreement does provide to the contrary.

18.5 Alterations of and amendments to the Set of Contracts must be made in writing. This applies also to this requirement of writing.

18.6 If any provision of the General Agreement is held to be invalid or unenforceable, the validity of the remaining provisions shall not be affected. The Parties shall replace the invalid or unenforceable provision by a valid and enforceable provision closest to the intention of the Parties when signing the General Agreement.

18.7 Same shall apply to all contractual provisions that the Parties may have omitted to include in this General Agreement.

18.8 As far as the language of Set of Contracts uses the name under which a software is marketed all later releases shall be included.

18.9 FME may execute rights to hold back or to set off only upon claims uncontested by NETCARE, or sums finally awarded by DGRI under Section 17 of this General Agreement.

28

|

Bad Homburg, |

|

|

Bad Homburg, 08.05.2013 |

|

|

|

|

|

|

|

|

|

|

|

|

Fresenius Medical Care AG & Co. KGaA |

|

Fresenius Netcare GmbH |

|

|

represented by its General Partner |

|

represented by |

|

|

Fresenius Medical Care Management AG, |

|

|

|

|

represented by |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

By: |

/s/ Rice Powell |

|

By: |

/s/ Klaus Kieren |

|

|

|

Rice Powell |

|

|

Klaus Kieren |

|

|

|

Global Chief Executive Officer and |

|

|

Chairman |

|

|

|

Chairman of Management Board |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

By: |

/s/ Dr. Emanuele Gatti |

|

By: |

/s/ Jurgen Kunze |

|

|

|

Dr. Emanuele Gatti |

|

|

Jürgen Kunze |

|

|

|

CEO Europe, Latin America, |

|

|

Vice Chairman |

|

|

|

Middle East and Africa |

|

|

|

|

|

|

Global Chief Strategist |

|

|

|

|

|

Attachment 1: |

List of Affiliates |

|

Attachment 2: |

Fairness Opinion |

|

Attachment 3: |

Glossary |

|

Attachment 4: |

Master Service Description |

29

Attachment 1 to the General Agreement

List of Affiliates based on FNC’s customer master data

Attachment 1 to the General Agreement

List of Affiliates

|

Branch |

|

Debitor |

|

Affiliate |

|

Unit |

|

Location |

|

Country

code |

|

N210 |

|

60000252 |

|

FMC D GmbH |

|

-Zahler- |

|

Bad Homburg |

|

DE |

|

N210 |

|

60000295 |

|

FMC D GmbH |

|

GB ZE Overhead/Key Turn Proj. |

|

Bad Homburg |

|

DE |

|

N210 |

|

60000296 |

|

FMC D GmbH |

|

Projektierung |

|

Bad Homburg |

|

DE |

|

N210 |

|

60000300 |

|

FMC D GmbH |

|

Marketing Technik |

|

Bad Homburg |

|

DE |

|

N210 |

|

60000305 |

|

FMC D GmbH |

|

IT-Projektierung |

|

Bad Homburg |

|

DE |

|

N210 |

|

60000306 |

|

FMC D GmbH |

|

GB ZE Production |

|

Bad Homburg |

|

DE |

|

N210 |

|

60000388 |

|

GFI - Deltronix |

|

Ges. für Informationssysteme mbH |

|

Fürth / Bayern |

|

DE |

|

N210 |

|

60000728 |

|

FMC D GmbH |

|

GB ZE OVH Technics /Training & Educ |

|

Bad Homburg |

|

DE |

|

N210 |

|

60000729 |

|

FMC D GmbH |

|

GB ZE Technical Service Internation |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000128 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - Overhead EMEA +Comme |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000130 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - Controlling |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000134 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - SCE Distribution |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000267 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - NESEE Overhead |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000268 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - Supply Network Plann |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000269 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - SC OVH&SCPI |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000270 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - EEMEA BG/PL/RO |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000271 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - Clinical Governance |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000394 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - CS Latin America |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000395 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - SCE CDC |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000592 |

|

FMC D GmbH |

|

International Marketing & Medicine |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000618 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEALA - POI |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000619 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - Overhead EEMEA + Pro |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000620 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - Russian Speaking |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000621 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - Middle East Overhead |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000622 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - W Africa Overhead |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000623 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - SE Africa Overhead |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000753 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - Supply Chain F&D |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000759 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - Supply Chain Executi |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000760 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - System & Demand Plan |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000761 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - Business Operation |

|

Bad Homburg |

|

DE |

1

|

N211 |

|

60000762 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - Medical Reporting & |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000763 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - Clinical Research |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000764 |

|

Fresenius Medical Care Deutschland |

|

Bereich EMEA - Nephrocare Coordinat |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000871 |

|

Fresenius Medical Care Deutsch. - G |

|

Bereich EMEA - |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000878 |

|

Fresenius Medical Care Deutschland |

|

WE OVH |

|

Bad Homburg |

|

DE |

|

N211 |

|

60000879 |

|

Fresenius Medical Care Deutschland |

|

TME |

|

Bad Homburg |

|

DE |

|

N213 |

|

60000132 |

|

FMC GmbH |

|

Sales Region |

|

Bad Homburg |

|

DE |

|

N213 |

|

60000297 |

|

FMC GmbH |

|

Marketing Deutschland |

|

Bad Homburg |

|

DE |

|

N213 |

|

60000298 |

|

FMC GmbH |

|

Technical Service National |

|

Bad Homburg |

|

DE |

|

N213 |

|

60000299 |

|

FMC GmbH |

|

Stammdaten & Projektmanagement |

|

Bad Homburg |

|

DE |

|

N213 |

|

60000301 |

|

FMC GmbH |

|

Commercial Department OVH |

|

Bad Homburg |

|

DE |

|

N213 |

|

60000302 |

|

FMC GmbH |

|

Material Planning |

|

Bad Homburg |

|

DE |

|

N213 |

|

60000303 |

|

FMC GmbH |

|

Logistics |

|

Bad Homburg |

|

DE |

|

N213 |

|

60000304 |

|

FMC GmbH |

|

Congresses |

|

Bad Homburg |

|

DE |

|

N213 |

|

60000727 |

|

FMC GmbH |

|

Overhead |

|

Bad Homburg |

|

DE |

|

N213 |

|

60000730 |

|

FMC GmbH |

|

Application Service |

|

Bad Homburg |

|

DE |

|

N213 |

|

60000742 |

|

FMC GmbH |

|

-Zahler- |

|

Bad Homburg |

|

DE |

|

N213 |

|

60000777 |

|

FMC GmbH |

|

Provider Deutschland |

|

Bad Homburg |

|

DE |

|

N219 |

|

60000137 |

|

FMC D GmbH |

|

Executive Medical Consulting |

|

Bad Homburg |

|

DE |

|

N219 |

|

60000138 |

|

FMC D GmbH |

|

Renal Pharma |

|

Bad Homburg |

|

DE |

|

N219 |

|

60000141 |

|

FMC D GmbH |

|

IBD Corp. Finance |

|

Bad Homburg |

|

DE |

|

N219 |

|

60000143 |

|

FMC D GmbH |

|

Human Resources |

|

Bad Homburg |

|

DE |

|

N219 |

|

60000144 |

|

FMC D GmbH |

|

Quality/Regulatory/Environment |

|

Bad Homburg |

|

DE |

|

N219 |

|

60000147 |

|

FMC D GmbH |

|

R&D (HG) |

|

Bad Homburg |

|

DE |

|

N219 |

|

60000148 |

|

FMC D GmbH |

|

Vorstand |

|

Bad Homburg |

|

DE |

|

N219 |

|

60000487 |

|

FMC D GmbH |

|

R&D (SW) |

|

Schweinfurt |

|

DE |

|

N219 |

|

60000635 |

|

FMC D GmbH |

|

Business Development |

|

Bad Homburg |

|

DE |

|

N219 |

|

60000858 |

|

FMC D GmbH |

|

International Strategic Development |

|

Bad Homburg |

|

DE |

|

N219 |

|

60000882 |

|

FMC D GmbH |

|

R&D (WND) |

|

Bad Homburg |

|

DE |

|

N220 |

|

60000005 |

|

FMC Nederland B.V. |

|

Administratie |

|

VLIJMEN |

|

NL |

|

N220 |

|

60000006 |

|

Fresenius Medical Care (Schweiz) AG |

|

|

|

Oberdorf |

|

CH |

|

N220 |

|

60000011 |

|

FMC AUSTRIA GmbH |

|

|

|

WIEN |

|

AT |

2

|

N220 |

|

60000021 |

|

FMC Belgium NV |

|

|

|

ANTWERPEN - WILRIJK |

|

BE |

|

N220 |

|

60000389 |

|

Fresenius Medical Care |

|

Slovenija d.o.o. |

|

Zrece |

|

SI |

|

N220 |

|

60000773 |

|

Fresenius Medical Care |

|

Servizi Logistici SA |

|

Manno |

|

CH |

|

N221 |

|

60000003 |

|

FMC Ltda., Portugal |

|

|

|

Moreira - Maia |

|

PT |

|

N221 |

|

60000004 |

|

FMC ITALIA S.P.A |

|

|

|

PALAZZO PIGNANO(CREMONA) |

|

IT |

|

N221 |

|

60000007 |

|

FMC Magyarország Egészségügyi Kft |

|

|

|

BUDAPEST |

|

HU |

|

N221 |

|

60000015 |

|

FMC FRANCE SAS |

|

|

|

FRESNES Cedex |

|

FR |

|

N221 |

|

60000017 |

|