Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21780

MFS SERIES TRUST XII

(Exact name of registrant as specified in charter)

111 Huntington Avenue, Boston, Massachusetts 02199

(Address of principal executive offices) (Zip code)

Christopher R. Bohane

Massachusetts Financial Services Company

111 Huntington Avenue

Boston, Massachusetts 02199

(Name and address of agents for service)

Registrant’s telephone number, including area code: (617) 954-5000

Date of fiscal year end: October 31*

Date of reporting period: October 31, 2018

| * | This Form N-CSR pertains to the following series of the Registrant: MFS Equity Opportunities Fund. The remaining series of the Registrant have fiscal year ends of April 30. |

Table of Contents

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

Table of Contents

Annual Report

October 31, 2018

MFS® Equity Opportunities Fund

MSR-ANN

Table of Contents

MFS® Equity Opportunities Fund

The report is prepared for the general information of shareholders.

It is authorized for distribution to prospective investors only when preceded or accompanied by a current prospectus.

NOT FDIC INSURED • MAY LOSE VALUE • NO BANK GUARANTEE

Table of Contents

LETTER FROM THE EXECUTIVE CHAIRMAN

Dear Shareholders:

Rising bond yields, international trade friction, and geopolitical uncertainty have contributed to an uptick in market volatility in recent quarters — a departure from the

low-volatility environment that prevailed for much of 2017. Against this more challenging backdrop, equity markets in the United States have outperformed most international markets on a relative basis, though returns have been modest year to date on an absolute basis. Global economic growth has become less synchronized over the past few months, with Europe, China, and some emerging markets having shown signs of slowing growth while U.S. growth has remained above average.

Although the U.S. Federal Reserve continues to gradually raise interest rates and shrink its balance sheet, monetary policy remains fairly accommodative around the world, with many central banks taking only tentative steps toward tighter policies.

U.S. tax reforms adopted in late 2017 have been welcomed by equity markets while emerging market economies have recently had to contend with tighter financial conditions as a result of firmer U.S. Treasury yields and a stronger dollar. The split result of the U.S. midterm congressional elections suggests meaningful further U.S. fiscal stimulus is less likely than if the Republicans had maintained control of both houses of Congress. Globally, inflation remains largely subdued, but tight labor markets and moderate global demand have investors on the lookout for its potential reappearance. Increased U.S. protectionism is also a growing concern, as investors fear trade disputes could dampen business sentiment, leading to even slower global growth. While there has been progress on this front — NAFTA has been replaced with a new agreement between the U.S., Mexico, and Canada; the free trade pact with Korea has been updated; and a negotiating framework with the European Union has been agreed upon — tensions over trade with China remain quite high.

As a global investment manager with nearly a century of expertise, MFS® firmly believes active risk management offers downside mitigation and may help improve investment outcomes. We built our active investment platform with this belief in mind. Our long-term perspective influences nearly every aspect of our business, ensuring our investment decisions align with the investing time horizons of our clients.

Respectfully,

Robert J. Manning

Executive Chairman

MFS Investment Management

December 14, 2018

The opinions expressed in this letter are subject to change and may not be relied upon for investment advice. No forecasts can be guaranteed.

1

Table of Contents

Cash & Cash Equivalents includes any cash, investments in money market funds, short-term securities, and other assets less liabilities. Please see the Statement of Assets and Liabilities for additional information related to the fund’s cash position and other assets and liabilities.

Percentages are based on net assets as of October 31, 2018.

The portfolio is actively managed and current holdings may be different.

2

Table of Contents

Summary of results

For the twelve months ended October 31, 2018, Class A shares of the MFS Equity Opportunities Fund (“fund”) provided a total return of –3.46%, at net asset value. This compares with a return of 6.98% for the fund’s benchmark, the Russell 1000® Index.

Market Environment

During the reporting period, the US Federal Reserve raised interest rates by 100 basis points, bringing the total number of rate hikes to eight since the central bank began to normalize monetary policy in late 2015. The growth rate in the US, eurozone and Japan remained above trend, although inflation remained contained, particularly outside the US. Late in the period, the European Central Bank announced that it would halt its asset purchase program at the end of 2018, but issued forward guidance that it does not expect to raise interest rates at least until after the summer of 2019. Both the Bank of England and the Bank of Canada raised rates several times during the period. The European political backdrop became a bit more volatile late in the period, spurred by concerns over cohesion in the eurozone after the election of an anti-establishment, Eurosceptic coalition government in Italy.

Bond yields rose in the US during the period but remained low by historical standards, while yields in many developed markets fell. Outside of emerging markets, where spreads and currencies came under pressure, credit spreads remained quite tight, particularly in US high yield corporates. Growing concern over increasing global trade friction appeared to have weighed on business sentiment during the period’s second half, especially outside the US. Tighter financial conditions from rising US rates and a strong dollar combined with trade uncertainty helped expose structural weaknesses in several emerging markets in the second half of the period.

Volatility increased at the end of the period amid signs of slowing global economic growth and increasing trade tensions, which prompted a market setback shortly after US markets set record highs in September. It was the second such equity market decline during the reporting period. The correction came despite a third consecutive quarter of strong growth in US earnings per share. Strong earnings growth, combined with the market decline, brought US equity valuations down from elevated levels, earlier in the period, to multiples more in line with long-term averages. While the US economy maintained its strength, global economic growth became less synchronized during the period, with Europe and China showing signs of a modest slowdown and some emerging markets coming under stress.

Detractors from Performance

Stock selection and, to a lesser extent, an overweight position in the autos & housing sector were primary factors that detracted from performance relative to the Russell 1000® Index. Within this sector, an overweight position in residential and commercial building materials manufacturer Owens Corning, and holdings of suspended ceilings systems distributor GMS (b), held back relative returns. Despite strong sales, the share price of Owens Corning declined, primarily due to rising input cost inflation and weakness in its roofing and composites divisions.

3

Table of Contents

Management Review – continued

Stock selection and an underweight allocation to the technology sector also hampered relative returns. Within this sector, not owning shares of computer and personal electronics maker Apple weighed on relative results after the company reported better-than-expected earnings results, driven by an average sales price increase on iPhones, which resulted in stronger revenues, services acceleration and growth in wearables. Apple’s management also increased its guidance for the year, which further supported the stock price growth. Additionally, the fund’s position in technology products and services provider Tech Data (b) further weighed on relative returns.

Stock selection in both the leisure and financial services sectors further weakened relative performance. Within the leisure sector, an overweight position in video game maker Electronic Arts hindered relative returns. Within the financial services sector, an overweight position in insurance provider Unum Group, and holdings of real estate investment trust Stag Industrial (b)(h), dampened relative performance. The share price of Unum declined following earnings results that came in shy of market expectations and a higher-than-expected long-term care loss ratio that put pressure on the company’s reserves.

Elsewhere, the fund’s position in shares of natural gas transmission company EQM Midstream Partners (b) hindered relative returns after the company missed on earnings expectations, owing to lower-than-expected gathering rates that were the primary driver behind the share price weakness. Additionally, the timing of the fund’s ownership in shares of internet retailer Amazon.com, and an overweight position in food producer Tyson Foods (h), further detracted from relative performance.

Contributors to Performance

Stock selection in the energy sector boosted relative performance, led by an overweight position in independent petroleum products company Marathon Petroleum. The share price of Marathon Petroleum rose after the company reported earnings that were ahead of consensus estimates, driven by volume growth and higher-than-expected gross margins in its refining segment, as well as the increase in the price of crude oil.

Stock selection and an underweight position in the basic materials sector also boosted relative returns. However, there were no individual stocks within this sector that were among the fund’s largest relative contributors during the period.

Elsewhere, the fund’s overweight positions in apparel retailer Urban Outfitters (h) and real estate investment trust Store Capital boosted relative returns. The share price of Urban Outfitters appreciated early in the reporting period following better-than-expected earnings and same-store sales across all divisions. Additionally, holdings of specialty value retailer Five Below (b)(h), and the timing of the fund’s ownership in shares of high-performance laser manufacturer IPG Photonics (h), biotechnology company Biogen, tobacco company Philip Morris International and financial services provider East West Bancorp (h) boosted relative returns. The share price of Five Below benefited from strong earnings results, driven by solid same-store sales growth and better-than-expected guidance. Furthermore, not owning shares of diversified industrial

4

Table of Contents

Management Review – continued

conglomerate General Electric, and an underweight position in tobacco company Altria Group, also supported relative results.

Respectfully,

Portfolio Manager(s)

Jim Fallon, Matt Krummell, Jonathan Sage, and Jed Stocks

| (b) | Security is not a benchmark constituent. |

| (h) | Security was not held in the portfolio at period end. |

The views expressed in this report are those of the portfolio manager(s) only through the end of the period of the report as stated on the cover and do not necessarily reflect the views of MFS or any other person in the MFS organization. These views are subject to change at any time based on market or other conditions, and MFS disclaims any responsibility to update such views. These views may not be relied upon as investment advice or an indication of trading intent on behalf of any MFS portfolio. References to specific securities are not recommendations of such securities, and may not be representative of any MFS portfolio’s current or future investments.

5

Table of Contents

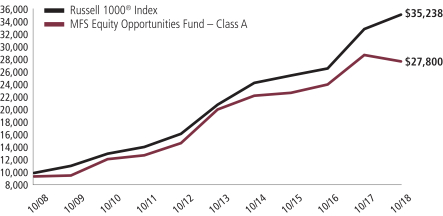

PERFORMANCE SUMMARY THROUGH 10/31/18

The following chart illustrates a representative class of the fund’s historical performance in comparison to its benchmark(s). Performance results include the deduction of the maximum applicable sales charge and reflect the percentage change in net asset value, including reinvestment of dividends and capital gains distributions. The performance of other share classes will be greater than or less than that of the class depicted below. Benchmarks are unmanaged and may not be invested in directly. Benchmark returns do not reflect sales charges, commissions or expenses. (See Notes to Performance Summary.)

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your shares, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. The performance shown does not reflect the deduction of taxes, if any, that a shareholder would pay on fund distributions or the redemption of fund shares.

Growth of a Hypothetical $10,000 Investment

6

Table of Contents

Performance Summary – continued

Total Returns through 10/31/18

Average annual without sales charge

| Share Class | Class Inception Date | 1-yr | 5-yr | 10-yr | Life (t) | |||||||||

| A | 8/30/00 | (3.46)% | 6.69% | 11.42% | N/A | |||||||||

| B | 1/03/07 | (4.18)% | 5.89% | 10.59% | N/A | |||||||||

| C | 3/01/04 | (4.18)% | 5.90% | 10.59% | N/A | |||||||||

| I | 2/28/11 | (3.21)% | 6.96% | N/A | 9.99% | |||||||||

| R1 | 5/01/08 | (4.13)% | 5.90% | 10.60% | N/A | |||||||||

| R2 | 5/01/08 | (3.68)% | 6.43% | 11.15% | N/A | |||||||||

| R3 | 5/01/08 | (3.46)% | 6.69% | 11.42% | N/A | |||||||||

| R4 | 5/01/08 | (3.16)% | 6.97% | 11.71% | N/A | |||||||||

| R6 | 3/03/08 | (3.09)% | 7.06% | 11.74% | N/A | |||||||||

| Comparative benchmark(s) | ||||||||||||||

| Russell 1000® Index (f) | 6.98% | 11.05% | 13.42% | N/A | ||||||||||

| Average annual with sales charge | ||||||||||||||

| A With Initial Sales Charge (5.75%) |

(9.01)% | 5.44% | 10.77% | N/A | ||||||||||

| B With CDSC (Declining over six years from 4% to 0%) (v) |

(7.68)% | 5.57% | 10.59% | N/A | ||||||||||

| C With CDSC (1% for 12 months) (v) |

(5.05)% | 5.90% | 10.59% | N/A | ||||||||||

CDSC – Contingent Deferred Sales Charge.

Class I, R1, R2, R3, R4, and R6 shares do not have a sales charge.

On May 30, 2012, Class W shares were redesignated Class R5 shares. Total returns for Class R5 shares prior to May 30, 2012 reflect the performance history of Class W shares which had different fees and expenses than Class R5 shares. Effective August 26, 2016, Class R5 shares were renamed Class R6 shares.

| (f) | Source: FactSet Research Systems Inc. |

| (t) | For the period from the class inception date through the stated period end (for those share classes with less than 10 years of performance history). No comparative benchmark performance information is provided for “life” periods. (See Notes to Performance Summary.) |

| (v) | Assuming redemption at the end of the applicable period. |

Benchmark Definition(s)

Russell 1000® Index – constructed to provide a comprehensive barometer for the large-cap segment of the U.S. equity universe based on total market capitalization, which represents approximately 92% of the investable U.S. equity market. The Russell 1000® Index is a trademark/service mark of the Frank Russell Company. Russell® is a trademark of the Frank Russell Company.

It is not possible to invest directly in an index.

7

Table of Contents

Performance Summary – continued

Notes to Performance Summary

Performance information for periods prior to February 1, 2010, reflects periods when a sub-adviser was responsible for selecting investments for the fund under different investment strategies. Effective February 1, 2010, MFS assumed responsibility for the day-to-day management of the fund’s portfolio in its capacity as the fund’s investment adviser.

Average annual total return represents the average annual change in value for each share class for the periods presented. Life returns are presented where the share class has less than 10 years of performance history and represent the average annual total return from the class inception date to the stated period end date. As the fund’s share classes may have different inception dates, the life returns may represent different time periods and may not be comparable. As a result, no comparative benchmark performance information is provided for life periods.

Performance results reflect any applicable expense subsidies and waivers in effect during the periods shown. Without such subsidies and waivers the fund’s performance results would be less favorable. Please see the prospectus and financial statements for complete details.

Performance results do not include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles and may differ from amounts reported in the financial highlights.

From time to time the fund may receive proceeds from litigation settlements, without which performance would be lower.

8

Table of Contents

Fund expenses borne by the shareholders during the period, May 1, 2018 through October 31, 2018

As a shareholder of the fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on certain purchase or redemption payments, and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period May 1, 2018 through October 31, 2018.

Actual Expenses

The first line for each share class in the following table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each share class in the following table provides information about hypothetical account values and hypothetical expenses based on the fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line for each share class in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

9

Table of Contents

Expense Table – continued

| Share Class |

Annualized Expense Ratio |

Beginning Account Value 5/01/18 |

Ending Account Value 10/31/18 |

Expenses Paid During Period (p) 5/01/18-10/31/18 |

||||||||||||||

| A | Actual | 1.18% | $1,000.00 | $973.23 | $5.87 | |||||||||||||

| Hypothetical (h) | 1.18% | $1,000.00 | $1,019.26 | $6.01 | ||||||||||||||

| B | Actual | 1.94% | $1,000.00 | $969.77 | $9.63 | |||||||||||||

| Hypothetical (h) | 1.94% | $1,000.00 | $1,015.43 | $9.86 | ||||||||||||||

| C | Actual | 1.94% | $1,000.00 | $969.48 | $9.63 | |||||||||||||

| Hypothetical (h) | 1.94% | $1,000.00 | $1,015.43 | $9.86 | ||||||||||||||

| I | Actual | 0.94% | $1,000.00 | $974.52 | $4.68 | |||||||||||||

| Hypothetical (h) | 0.94% | $1,000.00 | $1,020.47 | $4.79 | ||||||||||||||

| R1 | Actual | 1.94% | $1,000.00 | $970.01 | $9.63 | |||||||||||||

| Hypothetical (h) | 1.94% | $1,000.00 | $1,015.43 | $9.86 | ||||||||||||||

| R2 | Actual | 1.44% | $1,000.00 | $972.13 | $7.16 | |||||||||||||

| Hypothetical (h) | 1.44% | $1,000.00 | $1,017.95 | $7.32 | ||||||||||||||

| R3 | Actual | 1.18% | $1,000.00 | $973.44 | $5.87 | |||||||||||||

| Hypothetical (h) | 1.18% | $1,000.00 | $1,019.26 | $6.01 | ||||||||||||||

| R4 | Actual | 0.94% | $1,000.00 | $974.59 | $4.68 | |||||||||||||

| Hypothetical (h) | 0.94% | $1,000.00 | $1,020.47 | $4.79 | ||||||||||||||

| R6 | Actual | 0.85% | $1,000.00 | $974.97 | $4.23 | |||||||||||||

| Hypothetical (h) | 0.85% | $1,000.00 | $1,020.92 | $4.33 | ||||||||||||||

| (h) | 5% class return per year before expenses. |

| (p) | “Expenses Paid During Period” are equal to each class’s annualized expense ratio, as shown above, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). Expenses paid do not include any applicable sales charges (loads). If these transaction costs had been included, your costs would have been higher. |

Notes to Expense Table

Each class with a Rule 12b-1 service fee is subject to a rebate of a portion of such fee. Such rebates are included in the expense ratios above and are outside of the expense limitation arrangement. For Class A shares, this rebate reduced the expense ratio above by 0.01%. See Note 3 in the Notes to Financial Statements for additional information.

10

Table of Contents

10/31/18

The Portfolio of Investments is a complete list of all securities owned by your fund. It is categorized by broad-based asset classes.

| Common Stocks - 99.5% | ||||||||

| Issuer | Shares/Par | Value ($) | ||||||

| Aerospace - 6.6% | ||||||||

| Boeing Co. | 22,583 | $ | 8,013,803 | |||||

| Leidos Holdings, Inc. | 110,398 | 7,151,582 | ||||||

| Lockheed Martin Corp. | 21,883 | 6,430,320 | ||||||

|

|

|

|||||||

| $ | 21,595,705 | |||||||

| Airlines - 2.4% | ||||||||

| Delta Air Lines, Inc. | 143,820 | $ | 7,871,269 | |||||

| Alcoholic Beverages - 2.0% | ||||||||

| Molson Coors Brewing Co. | 100,410 | $ | 6,426,240 | |||||

| Automotive - 1.7% | ||||||||

| Lear Corp. | 42,482 | $ | 5,645,858 | |||||

| Biotechnology - 2.0% | ||||||||

| Biogen, Inc. (a) | 21,604 | $ | 6,573,449 | |||||

| Business Services - 6.2% | ||||||||

| DXC Technology Co. | 87,231 | $ | 6,353,034 | |||||

| Travelport Worldwide Ltd. | 452,640 | 6,771,494 | ||||||

| WEX, Inc. (a) | 40,356 | 7,101,042 | ||||||

|

|

|

|||||||

| $ | 20,225,570 | |||||||

| Computer Software - 4.7% | ||||||||

| Adobe, Inc. (a) | 29,487 | $ | 7,246,725 | |||||

| Microsoft Corp. | 75,332 | 8,046,211 | ||||||

|

|

|

|||||||

| $ | 15,292,936 | |||||||

| Computer Software - Systems - 1.7% | ||||||||

| Tech Data Corp. (a) | 77,256 | $ | 5,458,909 | |||||

| Construction - 3.4% | ||||||||

| GMS, Inc. (a) | 288,330 | $ | 4,740,145 | |||||

| Owens Corning | 137,633 | 6,505,912 | ||||||

|

|

|

|||||||

| $ | 11,246,057 | |||||||

| Consumer Services - 2.2% | ||||||||

| Planet Fitness, Inc. (a) | 147,520 | $ | 7,241,757 | |||||

11

Table of Contents

Portfolio of Investments – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Common Stocks - continued | ||||||||

| Electrical Equipment - 4.1% | ||||||||

| MSC Industrial Direct Co., Inc., “A” | 90,843 | $ | 7,363,734 | |||||

| WESCO International, Inc. (a) | 121,503 | 6,097,020 | ||||||

|

|

|

|||||||

| $ | 13,460,754 | |||||||

| Electronics - 1.8% | ||||||||

| Marvell Technology Group Ltd. | 361,091 | $ | 5,925,503 | |||||

| Energy - Independent - 5.6% | ||||||||

| Marathon Petroleum Corp. | 135,311 | $ | 9,532,660 | |||||

| Phillips 66 | 85,558 | 8,797,074 | ||||||

|

|

|

|||||||

| $ | 18,329,734 | |||||||

| Food & Beverages - 4.6% | ||||||||

| General Mills, Inc. | 170,411 | $ | 7,464,002 | |||||

| Ingredion, Inc. | 73,485 | 7,435,212 | ||||||

|

|

|

|||||||

| $ | 14,899,214 | |||||||

| Health Maintenance Organizations - 2.2% | ||||||||

| Humana Inc. | 22,878 | $ | 7,330,340 | |||||

| Insurance - 2.9% | ||||||||

| MetLife, Inc. | 76,071 | $ | 3,133,364 | |||||

| Unum Group | 172,287 | 6,247,127 | ||||||

|

|

|

|||||||

| $ | 9,380,491 | |||||||

| Internet - 2.3% | ||||||||

| GoDaddy, Inc. (a) | 100,848 | $ | 7,379,048 | |||||

| Leisure & Toys - 1.6% | ||||||||

| Electronic Arts, Inc. (a) | 58,843 | $ | 5,353,536 | |||||

| Machinery & Tools - 5.9% | ||||||||

| AGCO Corp. | 123,143 | $ | 6,900,934 | |||||

| Eaton Corp. PLC | 97,778 | 7,007,749 | ||||||

| Regal Beloit Corp. | 75,064 | 5,382,089 | ||||||

|

|

|

|||||||

| $ | 19,290,772 | |||||||

| Major Banks - 2.1% | ||||||||

| Bank of America Corp. | 244,222 | $ | 6,716,105 | |||||

| Medical & Health Technology & Services - 1.8% | ||||||||

| McKesson Corp. | 46,425 | $ | 5,791,983 | |||||

12

Table of Contents

Portfolio of Investments – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Common Stocks - continued | ||||||||

| Natural Gas - Pipeline - 3.6% | ||||||||

| Enterprise Products Partners LP | 272,817 | $ | 7,316,952 | |||||

| EQM Midstream Partners LP | 94,578 | 4,342,076 | ||||||

|

|

|

|||||||

| $ | 11,659,028 | |||||||

| Other Banks & Diversified Financials - 2.1% | ||||||||

| Discover Financial Services | 99,906 | $ | 6,960,451 | |||||

| Pharmaceuticals - 1.9% | ||||||||

| Bristol-Myers Squibb Co. | 125,860 | $ | 6,360,964 | |||||

| Real Estate - 12.3% | ||||||||

| EPR Properties, REIT | 114,060 | $ | 7,840,484 | |||||

| Extra Space Storage, Inc., REIT | 85,087 | 7,662,935 | ||||||

| Life Storage, Inc., REIT | 81,316 | 7,656,715 | ||||||

| Store Capital Corp., REIT | 326,752 | 9,485,611 | ||||||

| W.P. Carey, Inc., REIT | 115,921 | 7,651,945 | ||||||

|

|

|

|||||||

| $ | 40,297,690 | |||||||

| Restaurants - 2.2% | ||||||||

| U.S. Foods Holding Corp. (a) | 242,341 | $ | 7,069,087 | |||||

| Specialty Stores - 2.2% | ||||||||

| Amazon.com, Inc. | 4,406 | $ | 7,040,832 | |||||

| Tobacco - 4.9% | ||||||||

| Altria Group, Inc. | 123,450 | $ | 8,029,188 | |||||

| Philip Morris International, Inc. | 88,861 | 7,825,988 | ||||||

|

|

|

|||||||

| $ | 15,855,176 | |||||||

| Utilities - Electric Power - 2.5% | ||||||||

| Exelon Corp. | 187,965 | $ | 8,234,747 | |||||

| Total Common Stocks (Identified Cost, $333,932,012) | $ | 324,913,205 | ||||||

| Investment Companies (h) - 0.8% | ||||||||

| Money Market Funds - 0.8% | ||||||||

| MFS Institutional Money Market Portfolio, 2.21% (v) (Identified Cost, $2,685,071) |

2,685,339 | $ | 2,685,071 | |||||

| Other Assets, Less Liabilities - (0.3)% | (1,055,724 | ) | ||||||

| Net Assets - 100.0% | $ | 326,542,552 | ||||||

13

Table of Contents

Portfolio of Investments – continued

| (a) | Non-income producing security. |

| (h) | An affiliated issuer, which may be considered one in which the fund owns 5% or more of the outstanding voting securities, or a company which is under common control. At period end, the aggregate values of the fund’s investments in affiliated issuers and in unaffiliated issuers were $2,685,071 and $324,913,205, respectively. |

| (v) | Affiliated issuer that is available only to investment companies managed by MFS. The rate quoted for the MFS Institutional Money Market Portfolio is the annualized seven-day yield of the fund at period end. |

The following abbreviations are used in this report and are defined:

| PLC | Public Limited Company |

| REIT | Real Estate Investment Trust |

See Notes to Financial Statements

14

Table of Contents

Financial Statements

STATEMENT OF ASSETS AND LIABILITIES

At 10/31/18

This statement represents your fund’s balance sheet, which details the assets and liabilities comprising the total value of the fund.

| Assets | ||||

| Investments in unaffiliated issuers, at value (identified cost, $333,932,012) |

$324,913,205 | |||

| Investments in affiliated issuers, at value (identified cost, $2,685,071) |

2,685,071 | |||

| Receivables for |

||||

| Fund shares sold |

119,779 | |||

| Dividends |

371,842 | |||

| Total assets |

$328,089,897 | |||

| Liabilities | ||||

| Payables for |

||||

| Fund shares reacquired |

$1,239,920 | |||

| Payable to affiliates |

||||

| Investment adviser |

13,321 | |||

| Shareholder servicing costs |

211,597 | |||

| Distribution and service fees |

5,608 | |||

| Payable for independent Trustees’ compensation |

9 | |||

| Accrued expenses and other liabilities |

76,890 | |||

| Total liabilities |

$1,547,345 | |||

| Net assets |

$326,542,552 | |||

| Net assets consist of | ||||

| Paid-in capital |

$282,134,193 | |||

| Total distributable earnings (loss) |

44,408,359 | |||

| Net assets |

$326,542,552 | |||

| Shares of beneficial interest outstanding |

10,430,556 |

15

Table of Contents

Statement of Assets and Liabilities – continued

| Net assets | Shares outstanding |

Net asset value per share (a) |

||||||||||

| Class A |

$147,126,356 | 4,651,188 | $31.63 | |||||||||

| Class B |

9,291,846 | 311,493 | 29.83 | |||||||||

| Class C |

57,410,290 | 1,922,601 | 29.86 | |||||||||

| Class I |

99,258,510 | 3,127,090 | 31.74 | |||||||||

| Class R1 |

46,428 | 1,560 | 29.76 | |||||||||

| Class R2 |

516,531 | 16,832 | 30.69 | |||||||||

| Class R3 |

862,857 | 27,375 | 31.52 | |||||||||

| Class R4 |

602,147 | 18,920 | 31.83 | |||||||||

| Class R6 |

11,427,587 | 353,497 | 32.33 | |||||||||

| (a) | Maximum offering price per share was equal to the net asset value per share for all share classes, except for Class A, for which the maximum offering price per share was $33.56 [100 / 94.25 x $31.63]. On sales of $50,000 or more, the maximum offering price of Class A shares is reduced. A contingent deferred sales charge may be imposed on redemptions of Class A, Class B, and Class C shares. Redemption price per share was equal to the net asset value per share for Classes I, R1, R2, R3, R4, and R6. |

See Notes to Financial Statements

16

Table of Contents

Financial Statements

Year ended 10/31/18

This statement describes how much your fund earned in investment income and accrued in expenses. It also describes any gains and/or losses generated by fund operations.

| Net investment income (loss) | ||||

| Income |

||||

| Dividends |

$8,183,717 | |||

| Other |

71,720 | |||

| Dividends from affiliated issuers |

46,985 | |||

| Total investment income |

$8,302,422 | |||

| Expenses |

||||

| Management fee |

$3,103,442 | |||

| Distribution and service fees |

1,339,561 | |||

| Shareholder servicing costs |

438,743 | |||

| Administrative services fee |

70,412 | |||

| Independent Trustees’ compensation |

7,532 | |||

| Custodian fee |

24,949 | |||

| Shareholder communications |

32,847 | |||

| Audit and tax fees |

47,647 | |||

| Legal fees |

3,514 | |||

| Miscellaneous |

164,784 | |||

| Total expenses |

$5,233,431 | |||

| Reduction of expenses by investment adviser and distributor |

(48,818 | ) | ||

| Net expenses |

$5,184,613 | |||

| Net investment income (loss) |

$3,117,809 | |||

| Realized and unrealized gain (loss) | ||||

| Realized gain (loss) (identified cost basis) |

||||

| Unaffiliated issuers |

$61,183,024 | |||

| Affiliated issuers |

(818 | ) | ||

| Net realized gain (loss) |

$61,182,206 | |||

| Change in unrealized appreciation or depreciation |

||||

| Unaffiliated issuers |

$(73,955,050) | |||

| Net realized and unrealized gain (loss) |

$(12,772,844) | |||

| Change in net assets from operations |

$(9,655,035) |

See Notes to Financial Statements

17

Table of Contents

Financial Statements

STATEMENTS OF CHANGES IN NET ASSETS

These statements describe the increases and/or decreases in net assets resulting from operations, any distributions, and any shareholder transactions.

| Year ended | ||||||||

| 10/31/18 | 10/31/17 | |||||||

| Change in net assets | ||||||||

| From operations | ||||||||

| Net investment income (loss) |

$3,117,809 | $1,545,127 | ||||||

| Net realized gain (loss) |

61,182,206 | 43,536,292 | ||||||

| Net unrealized gain (loss) |

(73,955,050 | ) | 38,508,362 | |||||

| Change in net assets from operations |

$(9,655,035 | ) | $83,589,781 | |||||

| Total distributions declared to shareholders (a) |

$(39,507,241 | ) | $(6,451,175 | ) | ||||

| Change in net assets from fund share transactions |

$(89,655,411 | ) | $(75,223,638 | ) | ||||

| Total change in net assets |

$(138,817,687 | ) | $1,914,968 | |||||

| Net assets | ||||||||

| At beginning of period |

465,360,239 | 463,445,271 | ||||||

| At end of period (b) |

$326,542,552 | $465,360,239 | ||||||

| (a) | Distributions from net investment income and from net realized gain are no longer required to be separately disclosed. See Note 2. For the year ended October 31, 2017, distributions from net investment income and from net realized gain were $2,350,035 and $4,101,140, respectively. |

| (b) | Parenthetical disclosure of undistributed net investment income is no longer required. See Note 2. For the year ended October 31, 2017, end of period net assets included undistributed net investment income of $835,995. |

See Notes to Financial Statements

18

Table of Contents

Financial Statements

The financial highlights table is intended to help you understand the fund’s financial performance for the past 5 years. Certain information reflects financial results for a single fund share. The total returns in the table represent the rate that an investor would have earned (or lost) on an investment in the fund share class (assuming reinvestment of all distributions) held for the entire period.

| Class A | Year ended | |||||||||||||||||||

| 10/31/18 | 10/31/17 | 10/31/16 | 10/31/15 | 10/31/14 | ||||||||||||||||

| Net asset value, beginning of period |

$35.76 | $30.38 | $28.78 | $28.25 | $25.54 | |||||||||||||||

| Income (loss) from investment operations |

|

|||||||||||||||||||

| Net investment income (loss) (d) |

$0.28 | $0.14 | (c) | $0.19 | $0.12 | $0.09 | ||||||||||||||

| Net realized and unrealized gain (loss) |

(1.36 | ) | 5.69 | 1.50 | 0.49 | 2.69 | ||||||||||||||

| Total from investment operations |

$(1.08 | ) | $5.83 | $1.69 | $0.61 | $2.78 | ||||||||||||||

| Less distributions declared to shareholders |

|

|||||||||||||||||||

| From net investment income |

$(0.08 | ) | $(0.18 | ) | $(0.09 | ) | $(0.08 | ) | $(0.07 | ) | ||||||||||

| From net realized gain |

(2.97 | ) | (0.27 | ) | — | — | — | |||||||||||||

| Total distributions declared to shareholders |

$(3.05 | ) | $(0.45 | ) | $(0.09 | ) | $(0.08 | ) | $(0.07 | ) | ||||||||||

| Net asset value, end of period (x) |

$31.63 | $35.76 | $30.38 | $28.78 | $28.25 | |||||||||||||||

| Total return (%) (r)(s)(t)(x) |

(3.46 | ) | 19.37 | (c) | 5.88 | 2.17 | 10.90 | |||||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

|

|||||||||||||||||||

| Expenses before expense reductions (f) |

1.19 | 1.19 | (c) | 1.20 | 1.21 | 1.19 | ||||||||||||||

| Expenses after expense reductions (f) |

1.18 | 1.18 | (c) | 1.19 | 1.20 | 1.19 | ||||||||||||||

| Net investment income (loss) |

0.83 | 0.43 | (c) | 0.63 | 0.41 | 0.32 | ||||||||||||||

| Portfolio turnover |

119 | 121 | 109 | 119 | 106 | |||||||||||||||

| Net assets at end of period (000 omitted) |

$147,126 | $176,950 | $210,858 | $218,412 | $257,948 | |||||||||||||||

See Notes to Financial Statements

19

Table of Contents

Financial Highlights – continued

| Class B | Year ended | |||||||||||||||||||

| 10/31/18 | 10/31/17 | 10/31/16 | 10/31/15 | 10/31/14 | ||||||||||||||||

| Net asset value, beginning of period |

$34.05 | $28.99 | $27.59 | $27.21 | $24.72 | |||||||||||||||

| Income (loss) from investment operations |

|

|||||||||||||||||||

| Net investment income (loss) (d) |

$0.02 | $(0.10 | )(c) | $(0.03 | ) | $(0.10 | ) | $(0.11 | ) | |||||||||||

| Net realized and unrealized gain (loss) |

(1.27 | ) | 5.43 | 1.43 | 0.48 | 2.60 | ||||||||||||||

| Total from investment operations |

$(1.25 | ) | $5.33 | $1.40 | $0.38 | $2.49 | ||||||||||||||

| Less distributions declared to shareholders |

|

|||||||||||||||||||

| From net investment income |

$— | $— | $— | $— | $— | |||||||||||||||

| From net realized gain |

(2.97 | ) | (0.27 | ) | — | — | — | |||||||||||||

| Total distributions declared to shareholders |

$(2.97 | ) | $(0.27 | ) | $— | $— | $— | |||||||||||||

| Net asset value, end of period (x) |

$29.83 | $34.05 | $28.99 | $27.59 | $27.21 | |||||||||||||||

| Total return (%) (r)(s)(t)(x) |

(4.18 | ) | 18.50 | (c) | 5.07 | 1.40 | 10.07 | |||||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

|

|||||||||||||||||||

| Expenses before expense reductions (f) |

1.94 | 1.94 | (c) | 1.95 | 1.96 | 1.95 | ||||||||||||||

| Expenses after expense reductions (f) |

1.93 | 1.94 | (c) | 1.95 | 1.95 | 1.94 | ||||||||||||||

| Net investment income (loss) |

0.07 | (0.33 | )(c) | (0.11 | ) | (0.35 | ) | (0.43 | ) | |||||||||||

| Portfolio turnover |

119 | 121 | 109 | 119 | 106 | |||||||||||||||

| Net assets at end of period (000 omitted) |

$9,292 | $12,977 | $13,895 | $17,022 | $18,480 | |||||||||||||||

| Class C | Year ended | |||||||||||||||||||

| 10/31/18 | 10/31/17 | 10/31/16 | 10/31/15 | 10/31/14 | ||||||||||||||||

| Net asset value, beginning of period |

$34.08 | $29.02 | $27.62 | $27.23 | $24.74 | |||||||||||||||

| Income (loss) from investment operations |

|

|||||||||||||||||||

| Net investment income (loss) (d) |

$0.02 | $(0.10 | )(c) | $(0.03 | ) | $(0.10 | ) | $(0.12 | ) | |||||||||||

| Net realized and unrealized gain (loss) |

(1.27 | ) | 5.43 | 1.43 | 0.49 | 2.61 | ||||||||||||||

| Total from investment operations |

$(1.25 | ) | $5.33 | $1.40 | $0.39 | $2.49 | ||||||||||||||

| Less distributions declared to shareholders |

|

|||||||||||||||||||

| From net investment income |

$— | $— | $— | $— | $— | |||||||||||||||

| From net realized gain |

(2.97 | ) | (0.27 | ) | — | — | — | |||||||||||||

| Total distributions declared to shareholders |

$(2.97 | ) | $(0.27 | ) | $— | $— | $— | |||||||||||||

| Net asset value, end of period (x) |

$29.86 | $34.08 | $29.02 | $27.62 | $27.23 | |||||||||||||||

| Total return (%) (r)(s)(t)(x) |

(4.18 | ) | 18.48 | (c) | 5.07 | 1.43 | 10.06 | |||||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

|

|||||||||||||||||||

| Expenses before expense reductions (f) |

1.94 | 1.94 | (c) | 1.95 | 1.96 | 1.95 | ||||||||||||||

| Expenses after expense reductions (f) |

1.93 | 1.94 | (c) | 1.95 | 1.95 | 1.94 | ||||||||||||||

| Net investment income (loss) |

0.06 | (0.33 | )(c) | (0.12 | ) | (0.36 | ) | (0.45 | ) | |||||||||||

| Portfolio turnover |

119 | 121 | 109 | 119 | 106 | |||||||||||||||

| Net assets at end of period (000 omitted) |

$57,410 | $95,208 | $105,432 | $108,122 | $106,272 | |||||||||||||||

See Notes to Financial Statements

20

Table of Contents

Financial Highlights – continued

| Class I | Year ended | |||||||||||||||||||

| 10/31/18 | 10/31/17 | 10/31/16 | 10/31/15 | 10/31/14 | ||||||||||||||||

| Net asset value, beginning of period |

$35.88 | $30.49 | $28.88 | $28.35 | $25.61 | |||||||||||||||

| Income (loss) from investment operations |

|

|||||||||||||||||||

| Net investment income (loss) (d) |

$0.36 | $0.22 | (c) | $0.26 | $0.19 | $0.15 | ||||||||||||||

| Net realized and unrealized gain (loss) |

(1.35 | ) | 5.70 | 1.51 | 0.49 | 2.71 | ||||||||||||||

| Total from investment operations |

$(0.99 | ) | $5.92 | $1.77 | $0.68 | $2.86 | ||||||||||||||

| Less distributions declared to shareholders |

|

|||||||||||||||||||

| From net investment income |

$(0.18 | ) | $(0.26 | ) | $(0.16 | ) | $(0.15 | ) | $(0.12 | ) | ||||||||||

| From net realized gain |

(2.97 | ) | (0.27 | ) | — | — | — | |||||||||||||

| Total distributions declared to shareholders |

$(3.15 | ) | $(0.53 | ) | $(0.16 | ) | $(0.15 | ) | $(0.12 | ) | ||||||||||

| Net asset value, end of period (x) |

$31.74 | $35.88 | $30.49 | $28.88 | $28.35 | |||||||||||||||

| Total return (%) (r)(s)(t)(x) |

(3.21 | ) | 19.64 | (c) | 6.17 | 2.42 | 11.19 | |||||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

|

|||||||||||||||||||

| Expenses before expense reductions (f) |

0.94 | 0.95 | (c) | 0.95 | 0.96 | 0.95 | ||||||||||||||

| Expenses after expense reductions (f) |

0.94 | 0.94 | (c) | 0.95 | 0.95 | 0.95 | ||||||||||||||

| Net investment income (loss) |

1.07 | 0.65 | (c) | 0.88 | 0.66 | 0.54 | ||||||||||||||

| Portfolio turnover |

119 | 121 | 109 | 119 | 106 | |||||||||||||||

| Net assets at end of period (000 omitted) |

$99,259 | $156,864 | $112,860 | $110,990 | $146,339 | |||||||||||||||

| Class R1 | Year ended | |||||||||||||||||||

| 10/31/18 | 10/31/17 | 10/31/16 | 10/31/15 | 10/31/14 | ||||||||||||||||

| Net asset value, beginning of period |

$33.97 | $28.93 | $27.53 | $27.14 | $24.66 | |||||||||||||||

| Income (loss) from investment operations |

|

|||||||||||||||||||

| Net investment income (loss) (d) |

$0.01 | $(0.11 | )(c) | $(0.02 | ) | $(0.10 | ) | $(0.13 | ) | |||||||||||

| Net realized and unrealized gain (loss) |

(1.25 | ) | 5.42 | 1.42 | 0.49 | 2.61 | ||||||||||||||

| Total from investment operations |

$(1.24 | ) | $5.31 | $1.40 | $0.39 | $2.48 | ||||||||||||||

| Less distributions declared to shareholders |

|

|||||||||||||||||||

| From net investment income |

$— | $— | $— | $— | $— | |||||||||||||||

| From net realized gain |

(2.97 | ) | (0.27 | ) | — | — | — | |||||||||||||

| Total distributions declared to shareholders |

$(2.97 | ) | $(0.27 | ) | $— | $— | $— | |||||||||||||

| Net asset value, end of period (x) |

$29.76 | $33.97 | $28.93 | $27.53 | $27.14 | |||||||||||||||

| Total return (%) (r)(s)(t)(x) |

(4.16 | ) | 18.47 | (c) | 5.09 | 1.44 | 10.06 | |||||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

|

|||||||||||||||||||

| Expenses before expense reductions (f) |

1.95 | 1.95 | (c) | 1.95 | 1.96 | 1.95 | ||||||||||||||

| Expenses after expense reductions (f) |

1.94 | 1.94 | (c) | 1.95 | 1.96 | 1.95 | ||||||||||||||

| Net investment income (loss) |

0.03 | (0.34 | )(c) | (0.08 | ) | (0.37 | ) | (0.48 | ) | |||||||||||

| Portfolio turnover |

119 | 121 | 109 | 119 | 106 | |||||||||||||||

| Net assets at end of period (000 omitted) |

$46 | $310 | $258 | $1,643 | $1,397 | |||||||||||||||

See Notes to Financial Statements

21

Table of Contents

Financial Highlights – continued

| Class R2 | Year ended | |||||||||||||||||||

| 10/31/18 | 10/31/17 | 10/31/16 | 10/31/15 | 10/31/14 | ||||||||||||||||

| Net asset value, beginning of period |

$34.78 | $29.58 | $28.00 | $27.59 | $24.94 | |||||||||||||||

| Income (loss) from investment operations |

|

|||||||||||||||||||

| Net investment income (loss) (d) |

$0.18 | $0.06 | (c) | $0.11 | $0.04 | $(0.02 | ) | |||||||||||||

| Net realized and unrealized gain (loss) |

(1.30 | ) | 5.53 | 1.47 | 0.48 | 2.68 | ||||||||||||||

| Total from investment operations |

$(1.12 | ) | $5.59 | $1.58 | $0.52 | $2.66 | ||||||||||||||

| Less distributions declared to shareholders |

|

|||||||||||||||||||

| From net investment income |

$— | $(0.12 | ) | $— | $(0.11 | ) | $(0.01 | ) | ||||||||||||

| From net realized gain |

(2.97 | ) | (0.27 | ) | — | — | — | |||||||||||||

| Total distributions declared to shareholders |

$(2.97 | ) | $(0.39 | ) | $— | $(0.11 | ) | $(0.01 | ) | |||||||||||

| Net asset value, end of period (x) |

$30.69 | $34.78 | $29.58 | $28.00 | $27.59 | |||||||||||||||

| Total return (%) (r)(s)(t)(x) |

(3.68 | ) | 19.05 | (c) | 5.64 | 1.89 | 10.66 | |||||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

|

|||||||||||||||||||

| Expenses before expense reductions (f) |

1.44 | 1.45 | (c) | 1.45 | 1.46 | 1.48 | ||||||||||||||

| Expenses after expense reductions (f) |

1.43 | 1.44 | (c) | 1.45 | 1.45 | 1.47 | ||||||||||||||

| Net investment income (loss) |

0.56 | 0.20 | (c) | 0.38 | 0.14 | (0.09 | ) | |||||||||||||

| Portfolio turnover |

119 | 121 | 109 | 119 | 106 | |||||||||||||||

| Net assets at end of period (000 omitted) |

$517 | $1,270 | $1,716 | $1,894 | $1,728 | |||||||||||||||

| Class R3 | Year ended | |||||||||||||||||||

| 10/31/18 | 10/31/17 | 10/31/16 | 10/31/15 | 10/31/14 | ||||||||||||||||

| Net asset value, beginning of period |

$35.64 | $30.28 | $28.68 | $28.19 | $25.49 | |||||||||||||||

| Income (loss) from investment operations |

|

|||||||||||||||||||

| Net investment income (loss) (d) |

$0.28 | $0.15 | (c) | $0.18 | $0.11 | $0.07 | ||||||||||||||

| Net realized and unrealized gain (loss) |

(1.35 | ) | 5.66 | 1.50 | 0.49 | 2.70 | ||||||||||||||

| Total from investment operations |

$(1.07 | ) | $5.81 | $1.68 | $0.60 | $2.77 | ||||||||||||||

| Less distributions declared to shareholders |

|

|||||||||||||||||||

| From net investment income |

$(0.08 | ) | $(0.18 | ) | $(0.08 | ) | $(0.11 | ) | $(0.07 | ) | ||||||||||

| From net realized gain |

(2.97 | ) | (0.27 | ) | — | — | — | |||||||||||||

| Total distributions declared to shareholders |

$(3.05 | ) | $(0.45 | ) | $(0.08 | ) | $(0.11 | ) | $(0.07 | ) | ||||||||||

| Net asset value, end of period (x) |

$31.52 | $35.64 | $30.28 | $28.68 | $28.19 | |||||||||||||||

| Total return (%) (r)(s)(t)(x) |

(3.46 | ) | 19.39 | (c) | 5.87 | 2.17 | 10.90 | |||||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

|

|||||||||||||||||||

| Expenses before expense reductions (f) |

1.19 | 1.19 | (c) | 1.20 | 1.21 | 1.20 | ||||||||||||||

| Expenses after expense reductions (f) |

1.18 | 1.19 | (c) | 1.20 | 1.20 | 1.20 | ||||||||||||||

| Net investment income (loss) |

0.83 | 0.47 | (c) | 0.63 | 0.38 | 0.26 | ||||||||||||||

| Portfolio turnover |

119 | 121 | 109 | 119 | 106 | |||||||||||||||

| Net assets at end of period (000 omitted) |

$863 | $1,210 | $1,593 | $1,677 | $1,492 | |||||||||||||||

See Notes to Financial Statements

22

Table of Contents

Financial Highlights – continued

| Class R4 | Year ended | |||||||||||||||||||

| 10/31/18 | 10/31/17 | 10/31/16 | 10/31/15 | 10/31/14 | ||||||||||||||||

| Net asset value, beginning of period |

$35.93 | $30.52 | $28.90 | $28.37 | $25.62 | |||||||||||||||

| Income (loss) from investment operations |

|

|||||||||||||||||||

| Net investment income (loss) (d) |

$0.40 | $0.23 | (c) | $0.26 | $0.18 | $0.16 | ||||||||||||||

| Net realized and unrealized gain (loss) |

(1.38 | ) | 5.71 | 1.50 | 0.49 | 2.69 | ||||||||||||||

| Total from investment operations |

$(0.98 | ) | $5.94 | $1.76 | $0.67 | $2.85 | ||||||||||||||

| Less distributions declared to shareholders |

|

|||||||||||||||||||

| From net investment income |

$(0.15 | ) | $(0.26 | ) | $(0.14 | ) | $(0.14 | ) | $(0.10 | ) | ||||||||||

| From net realized gain |

(2.97 | ) | (0.27 | ) | — | — | — | |||||||||||||

| Total distributions declared to shareholders |

$(3.12 | ) | $(0.53 | ) | $(0.14 | ) | $(0.14 | ) | $(0.10 | ) | ||||||||||

| Net asset value, end of period (x) |

$31.83 | $35.93 | $30.52 | $28.90 | $28.37 | |||||||||||||||

| Total return (%) (r)(s)(t)(x) |

(3.16 | ) | 19.68 | (c) | 6.11 | 2.41 | 11.18 | |||||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

|

|||||||||||||||||||

| Expenses before expense reductions (f) |

0.94 | 0.95 | (c) | 0.95 | 0.96 | 0.94 | ||||||||||||||

| Expenses after expense reductions (f) |

0.93 | 0.94 | (c) | 0.95 | 0.96 | 0.94 | ||||||||||||||

| Net investment income (loss) |

1.15 | 0.70 | (c) | 0.87 | 0.61 | 0.57 | ||||||||||||||

| Portfolio turnover |

119 | 121 | 109 | 119 | 106 | |||||||||||||||

| Net assets at end of period (000 omitted) |

$602 | $4,199 | $6,656 | $6,322 | $9,664 | |||||||||||||||

| Class R6 | Year ended | |||||||||||||||||||

| 10/31/18 | 10/31/17 | 10/31/16 | 10/31/15 | 10/31/14 | ||||||||||||||||

| Net asset value, beginning of period |

$36.48 | $30.99 | $29.36 | $28.80 | $26.02 | |||||||||||||||

| Income (loss) from investment operations |

|

|||||||||||||||||||

| Net investment income (loss) (d) |

$0.40 | $0.25 | (c) | $0.29 | $0.23 | $0.22 | ||||||||||||||

| Net realized and unrealized gain (loss) |

(1.37 | ) | 5.80 | 1.53 | 0.50 | 2.68 | ||||||||||||||

| Total from investment operations |

$(0.97 | ) | $6.05 | $1.82 | $0.73 | $2.90 | ||||||||||||||

| Less distributions declared to shareholders |

|

|||||||||||||||||||

| From net investment income |

$(0.21 | ) | $(0.29 | ) | $(0.19 | ) | $(0.17 | ) | $(0.12 | ) | ||||||||||

| From net realized gain |

(2.97 | ) | (0.27 | ) | — | — | — | |||||||||||||

| Total distributions declared to shareholders |

$(3.18 | ) | $(0.56 | ) | $(0.19 | ) | $(0.17 | ) | $(0.12 | ) | ||||||||||

| Net asset value, end of period (x) |

$32.33 | $36.48 | $30.99 | $29.36 | $28.80 | |||||||||||||||

| Total return (%) (r)(s)(t)(x) |

(3.09 | ) | 19.75 | (c) | 6.25 | 2.58 | 11.20 | |||||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

|

|||||||||||||||||||

| Expenses before expense reductions (f) |

0.85 | 0.85 | (c) | 0.85 | 0.85 | 0.86 | ||||||||||||||

| Expenses after expense reductions (f) |

0.84 | 0.84 | (c) | 0.85 | 0.85 | 0.86 | ||||||||||||||

| Net investment income (loss) |

1.15 | 0.72 | (c) | 0.95 | 0.81 | 0.79 | ||||||||||||||

| Portfolio turnover |

119 | 121 | 109 | 119 | 106 | |||||||||||||||

| Net assets at end of period (000 omitted) |

$11,428 | $16,373 | $10,178 | $7,115 | $1,647 | |||||||||||||||

See Notes to Financial Statements

23

Table of Contents

Financial Highlights – continued

| (c) | Amount reflects a one-time reimbursement of expenses by the custodian (or former custodian) without which net investment income and performance would be lower and expenses would be higher. |

| (d) | Per share data is based on average shares outstanding. |

| (f) | Ratios do not reflect reductions from fees paid indirectly, if applicable. |

| (r) | Certain expenses have been reduced without which performance would have been lower. |

| (s) | From time to time the fund may receive proceeds from litigation settlements, without which performance would be lower. |

| (t) | Total returns do not include any applicable sales charges. |

| (x) | The net asset values and total returns have been calculated on net assets which include adjustments made in accordance with U.S. generally accepted accounting principles required at period end for financial reporting purposes. |

See Notes to Financial Statements

24

Table of Contents

(1) Business and Organization

MFS Equity Opportunities Fund (the fund) is a diversified series of MFS Series Trust XII (the trust). The trust is organized as a Massachusetts business trust and is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company.

The fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 Financial Services – Investment Companies.

(2) Significant Accounting Policies

General – The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates. In the preparation of these financial statements, management has evaluated subsequent events occurring after the date of the fund’s Statement of Assets and Liabilities through the date that the financial statements were issued.

In August 2018, the FASB issued Accounting Standards Update 2018-13, Fair Value Measurement (Topic 820) – Disclosure Framework – Changes to the Disclosure Requirements for Fair Value Measurement (“ASU 2018-13”) which introduces new fair value disclosure requirements as well as eliminates and modifies certain existing fair value disclosure requirements. ASU 2018-13 would be effective for fiscal years beginning after December 15, 2019, and interim periods within those fiscal years; however, management has elected to early adopt ASU 2018-13 effective with the current reporting period. The impact of the fund’s adoption was limited to changes in the fund’s financial statement disclosures regarding fair value, primarily those disclosures related to transfers between levels of the fair value hierarchy.

In August 2018, the Securities and Exchange Commission (SEC) released its Final Rule on Disclosure Update and Simplification (the “Final Rule”) which is intended to simplify an issuer’s disclosure compliance efforts by removing redundant or outdated disclosure requirements without significantly altering the mix of information provided to investors. Effective with the current reporting period, the fund adopted the Final Rule with the impacts being that the fund is no longer required to present the components of distributable earnings on the Statement of Assets and Liabilities or the sources of distributions to shareholders and the amount of undistributed net investment income on the Statements of Changes in Net Assets.

Balance Sheet Offsetting – The fund’s accounting policy with respect to balance sheet offsetting is that, absent an event of default by the counterparty or a termination of the agreement, the International Swaps and Derivatives Association (ISDA) Master Agreement, or similar agreement, does not result in an offset of reported amounts of financial assets and financial liabilities in the Statement of Assets and Liabilities across

25

Table of Contents

Notes to Financial Statements – continued

transactions between the fund and the applicable counterparty. The fund’s right to setoff may be restricted or prohibited by the bankruptcy or insolvency laws of the particular jurisdiction to which a specific master netting agreement counterparty is subject. Balance sheet offsetting disclosures, to the extent applicable to the fund, have been included in the fund’s Significant Accounting Policies note under the captions for each of the fund’s in-scope financial instruments and transactions.

Investment Valuations – Equity securities, including restricted equity securities, are generally valued at the last sale or official closing price on their primary market or exchange as provided by a third-party pricing service. Equity securities, for which there were no sales reported that day, are generally valued at the last quoted daily bid quotation on their primary market or exchange as provided by a third-party pricing service. Short-term instruments with a maturity at issuance of 60 days or less may be valued at amortized cost, which approximates market value. Open-end investment companies are generally valued at net asset value per share. Securities and other assets generally valued on the basis of information from a third-party pricing service may also be valued at a broker/dealer bid quotation. In determining values, third-party pricing services can utilize both transaction data and market information such as yield, quality, coupon rate, maturity, type of issue, trading characteristics, and other market data.

The Board of Trustees has delegated primary responsibility for determining or causing to be determined the value of the fund’s investments (including any fair valuation) to the adviser pursuant to valuation policies and procedures approved by the Board. If the adviser determines that reliable market quotations are not readily available, investments are valued at fair value as determined in good faith by the adviser in accordance with such procedures under the oversight of the Board of Trustees. Under the fund’s valuation policies and procedures, market quotations are not considered to be readily available for most types of debt instruments and floating rate loans and many types of derivatives. These investments are generally valued at fair value based on information from third-party pricing services. In addition, investments may be valued at fair value if the adviser determines that an investment’s value has been materially affected by events occurring after the close of the exchange or market on which the investment is principally traded (such as foreign exchange or market) and prior to the determination of the fund’s net asset value, or after the halting of trading of a specific security where trading does not resume prior to the close of the exchange or market on which the security is principally traded. Events that occur on a frequent basis after foreign markets close (such as developments in foreign markets and significant movements in the U.S. markets) and prior to the determination of the fund’s net asset value may be deemed to have a material effect on the value of securities traded in foreign markets. Accordingly, the fund’s foreign equity securities may often be valued at fair value. The adviser generally relies on third-party pricing services or other information (such as the correlation with price movements of similar securities in the same or other markets; the type, cost and investment characteristics of the security; the business and financial condition of the issuer; and trading and other market data) to assist in determining whether to fair value and at what value to fair value an investment. The value of an investment for purposes of calculating the fund’s net asset value can differ depending on the source and method used to determine value. When fair valuation is used, the value of an investment used to determine the fund’s net asset value may differ from

26

Table of Contents

Notes to Financial Statements – continued

quoted or published prices for the same investment. There can be no assurance that the fund could obtain the fair value assigned to an investment if it were to sell the investment at the same time at which the fund determines its net asset value per share.

Various inputs are used in determining the value of the fund’s assets or liabilities. These inputs are categorized into three broad levels. In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, an investment’s level within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement. The fund’s assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment, and considers factors specific to the investment. Level 1 includes unadjusted quoted prices in active markets for identical assets or liabilities. Level 2 includes other significant observable market-based inputs (including quoted prices for similar securities, interest rates, prepayment speed, and credit risk). Level 3 includes unobservable inputs, which may include the adviser’s own assumptions in determining the fair value of investments. The following is a summary of the levels used as of October 31, 2018 in valuing the fund’s assets or liabilities:

| Financial Instruments | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Equity Securities | $324,913,205 | $— | $— | $324,913,205 | ||||||||||||

| Mutual Funds | 2,685,071 | — | — | 2,685,071 | ||||||||||||

| Total | $327,598,276 | $— | $— | $327,598,276 | ||||||||||||

For further information regarding security characteristics, see the Portfolio of Investments.

Indemnifications – Under the fund’s organizational documents, its officers and Trustees may be indemnified against certain liabilities and expenses arising out of the performance of their duties to the fund. Additionally, in the normal course of business, the fund enters into agreements with service providers that may contain indemnification clauses. The fund’s maximum exposure under these agreements is unknown as this would involve future claims that may be made against the fund that have not yet occurred.

Investment Transactions and Income – Investment transactions are recorded on the trade date. Dividends received in cash are recorded on the ex-dividend date. Certain dividends from foreign securities will be recorded when the fund is informed of the dividend if such information is obtained subsequent to the ex-dividend date. Dividend payments received in additional securities are recorded on the ex-dividend date in an amount equal to the value of the security on such date.

The fund may receive proceeds from litigation settlements. Any proceeds received from litigation involving portfolio holdings are reflected in the Statement of Operations in realized gain/loss if the security has been disposed of by the fund or in unrealized gain/loss if the security is still held by the fund. Any other proceeds from litigation not related to portfolio holdings are reflected as other income in the Statement of Operations.

Tax Matters and Distributions – The fund intends to qualify as a regulated investment company, as defined under Subchapter M of the Internal Revenue Code, and to distribute all of its taxable income, including realized capital gains. As a result,

27

Table of Contents

Notes to Financial Statements – continued

no provision for federal income tax is required. The fund’s federal tax returns, when filed, will remain subject to examination by the Internal Revenue Service for a three year period. Management has analyzed the fund’s tax positions taken on federal and state tax returns for all open tax years and does not believe that there are any uncertain tax positions that require recognition of a tax liability. Foreign taxes, if any, have been accrued by the fund in the accompanying financial statements in accordance with the applicable foreign tax law. Foreign income taxes may be withheld by certain countries in which the fund invests. Additionally, capital gains realized by the fund on securities issued in or by certain foreign countries may be subject to capital gains tax imposed by those countries.

Distributions to shareholders are recorded on the ex-dividend date. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from U.S. generally accepted accounting principles. Certain capital accounts in the financial statements are periodically adjusted for permanent differences in order to reflect their tax character. These adjustments have no impact on net assets or net asset value per share. Temporary differences which arise from recognizing certain items of income, expense, gain or loss in different periods for financial statement and tax purposes will reverse at some time in the future. Distributions in excess of net investment income or net realized gains are temporary overdistributions for financial statement purposes resulting from differences in the recognition or classification of income or distributions for financial statement and tax purposes.

Book/tax differences primarily relate to wash sale loss deferrals, treating a portion of the proceeds from redemptions as a distribution for tax purposes, and partnership adjustments.

The tax character of distributions declared to shareholders for the last two fiscal years is as follows:

| Year ended 10/31/18 |

Year ended 10/31/17 |

|||||||

| Ordinary income (including any short-term capital gains) | $8,414,148 | $2,350,035 | ||||||

| Long-term capital gains | 31,093,093 | 4,101,140 | ||||||

| Total distributions | $39,507,241 | $6,451,175 | ||||||

The federal tax cost and the tax basis components of distributable earnings were as follows:

| As of 10/31/18 | ||||

| Cost of investments | $336,098,880 | |||

| Gross appreciation | 15,564,085 | |||

| Gross depreciation | (24,064,689 | ) | ||

| Net unrealized appreciation (depreciation) | $(8,500,604 | ) | ||

| Undistributed ordinary income | 26,608,981 | |||

| Undistributed long-term capital gain | 26,761,091 | |||

| Other temporary differences | (461,109 | ) | ||

28

Table of Contents

Notes to Financial Statements – continued

Multiple Classes of Shares of Beneficial Interest – The fund offers multiple classes of shares, which differ in their respective distribution and service fees. The fund’s income, realized and unrealized gain (loss), and common expenses are allocated to shareholders based on the daily net assets of each class. Dividends are declared separately for each class. Differences in per share dividend rates are generally due to differences in separate class expenses. Class B shares will convert to Class A shares approximately eight years after purchase. Effective April 23, 2018, Class C shares will convert to Class A shares approximately ten years after purchase. The fund’s distributions declared to shareholders as reported in the Statements of Changes in Net Assets are presented by class as follows:

| From net investment income |

From net realized gain |

|||||||||||||||

| Year ended 10/31/18 |

Year ended 10/31/17 |

Year ended 10/31/18 |

Year ended 10/31/17 |

|||||||||||||

| Class A | $406,404 | $1,203,331 | $14,397,767 | $1,824,850 | ||||||||||||

| Class B | — | — | 1,102,773 | 126,354 | ||||||||||||

| Class C | — | — | 8,085,856 | 950,683 | ||||||||||||

| Class I | 756,202 | 975,525 | 12,756,323 | 1,016,269 | ||||||||||||

| Class R1 | — | — | 26,534 | 2,216 | ||||||||||||

| Class R2 | — | 6,730 | 108,819 | 15,650 | ||||||||||||

| Class R3 | 2,584 | 9,647 | 102,175 | 14,270 | ||||||||||||

| Class R4 | 17,306 | 56,153 | 340,821 | 58,605 | ||||||||||||

| Class R6 | 92,578 | 98,649 | 1,311,099 | 92,243 | ||||||||||||

| Total | $1,275,074 | $2,350,035 | $38,232,167 | $4,101,140 | ||||||||||||

(3) Transactions with Affiliates

Investment Adviser – The fund has an investment advisory agreement with MFS to provide overall investment management and related administrative services and facilities to the fund. The management fee is computed daily and paid monthly at the following annual rates based on the fund’s average daily net assets:

| Up to $1 billion | 0.75 | % | ||

| In excess of $1 billion and up to $2.5 billion | 0.65 | % | ||

| In excess of $2.5 billion and up to $5 billion | 0.60 | % | ||

| In excess of $5 billion | 0.50 | % |

MFS has agreed in writing to reduce its management fee by a specified amount if certain MFS mutual fund assets exceed thresholds agreed to by MFS and the fund’s Board of Trustees. For the year ended October 31, 2018, this management fee reduction amounted to $38,436, which is included in the reduction of total expenses in the Statement of Operations. The management fee incurred for the year ended October 31, 2018 was equivalent to an annual effective rate of 0.74% of the fund’s average daily net assets.

The investment adviser has agreed in writing to pay a portion of the fund’s total annual operating expenses, excluding interest, taxes, extraordinary expenses, brokerage and

29

Table of Contents

Notes to Financial Statements – continued

transaction costs, and investment-related expenses, such that total fund operating expenses do not exceed the following rates annually of each class’s average daily net assets:

| Classes | ||||||||||||||||||||||||||||||||

| A | B | C | I | R1 | R2 | R3 | R4 | R6 | ||||||||||||||||||||||||

| 1.40% | 2.15% | 2.15% | 1.15% | 2.15% | 1.65% | 1.40% | 1.15% | 1.09% | ||||||||||||||||||||||||

This written agreement will continue until modified by the fund’s Board of Trustees, but such agreement will continue at least until February 29, 2020. For the year ended October 31, 2018, the fund’s actual operating expenses did not exceed the limit and therefore, the investment adviser did not pay any portion of the fund’s expenses related to this agreement.

Distributor – MFS Fund Distributors, Inc. (MFD), a wholly-owned subsidiary of MFS, as distributor, received $21,523 for the year ended October 31, 2018, as its portion of the initial sales charge on sales of Class A shares of the fund.

The Board of Trustees has adopted a distribution plan for certain share classes pursuant to Rule 12b-1 of the Investment Company Act of 1940.

The fund’s distribution plan provides that the fund will pay MFD for services provided by MFD and financial intermediaries in connection with the distribution and servicing of certain share classes. One component of the plan is a distribution fee paid to MFD and another component of the plan is a service fee paid to MFD. MFD may subsequently pay all, or a portion, of the distribution and/or service fees to financial intermediaries.

Distribution Plan Fee Table:

| Distribution Fee Rate (d) |

Service Fee Rate (d) |

Total Distribution Plan (d) |

Annual Effective Rate (e) |

Distribution and Service Fee |

||||||||||||||||

| Class A | — | 0.25% | 0.25% | 0.24% | $418,659 | |||||||||||||||

| Class B | 0.75% | 0.25% | 1.00% | 1.00% | 113,516 | |||||||||||||||

| Class C | 0.75% | 0.25% | 1.00% | 1.00% | 798,284 | |||||||||||||||

| Class R1 | 0.75% | 0.25% | 1.00% | 1.00% | 2,100 | |||||||||||||||

| Class R2 | 0.25% | 0.25% | 0.50% | 0.50% | 4,086 | |||||||||||||||

| Class R3 | — | 0.25% | 0.25% | 0.25% | 2,916 | |||||||||||||||

| Total Distribution and Service Fees |

|

$1,339,561 | ||||||||||||||||||

| (d) | In accordance with the distribution plan for certain classes, the fund pays distribution and/or service fees equal to these annual percentage rates of each class’s average daily net assets. The distribution and service fee rates disclosed by class represent the current rates in effect at the end of the reporting period. Any rate changes, if applicable, are detailed below. |

| (e) | The annual effective rates represent actual fees incurred under the distribution plan for the year ended October 31, 2018 based on each class’s average daily net assets. MFD has voluntarily agreed to rebate a portion of each class’s 0.25% service fee attributable to accounts for which MFD retains the 0.25% service fee except for accounts attributable to MFS or its affiliates’ seed money. For the year ended October 31, 2018, this rebate amounted to $9,916, $45, $386, and $35 for Class A, Class B, Class C, and Class R3, respectively, and is included in the reduction of total expenses in the Statement of Operations. |

Certain Class A shares are subject to a contingent deferred sales charge (CDSC) in the event of a shareholder redemption within 18 months of purchase. Class B shares are subject to a CDSC in the event of a shareholder redemption within six years of

30

Table of Contents

Notes to Financial Statements – continued

purchase. Class C shares are subject to a CDSC in the event of a shareholder redemption within 12 months of purchase. All contingent deferred sales charges are paid to MFD and during the year ended October 31, 2018, were as follows:

| Amount | ||||

| Class A | $1,109 | |||

| Class B | 24,191 | |||

| Class C | 5,346 | |||

Shareholder Servicing Agent – MFS Service Center, Inc. (MFSC), a wholly-owned subsidiary of MFS, receives a fee from the fund for its services as shareholder servicing agent calculated as a percentage of the average daily net assets of the fund as determined periodically under the supervision of the fund’s Board of Trustees. For the year ended October 31, 2018, the fee was $50,396, which equated to 0.0122% annually of the fund’s average daily net assets. MFSC also receives payment from the fund for out-of-pocket expenses, sub-accounting and other shareholder servicing costs which may be paid to affiliated and unaffiliated service providers. Class R6 shares do not incur sub-accounting fees. For the year ended October 31, 2018, these out-of-pocket expenses, sub-accounting and other shareholder servicing costs amounted to $388,347.

Administrator – MFS provides certain financial, legal, shareholder communications, compliance, and other administrative services to the fund. Under an administrative services agreement, the fund reimburses MFS the costs incurred to provide these services. The fund is charged an annual fixed amount of $17,500 plus a fee based on average daily net assets. The administrative services fee incurred for the year ended October 31, 2018 was equivalent to an annual effective rate of 0.0170% of the fund’s average daily net assets.

Trustees’ and Officers’ Compensation – The fund pays compensation to independent Trustees in the form of a retainer, attendance fees, and additional compensation to Board and Committee chairpersons. The fund does not pay compensation directly to Trustees or officers of the fund who are also officers of the investment adviser, all of whom receive remuneration for their services to the fund from MFS. Certain officers and Trustees of the fund are officers or directors of MFS, MFD, and MFSC.

Other – This fund and certain other funds managed by MFS (the funds) have entered into a service agreement (the ISO Agreement) which provides for payment of fees solely by the funds to Tarantino LLC in return for the provision of services of an Independent Senior Officer (ISO) for the funds. Frank L. Tarantino serves as the ISO and is an officer of the funds and the sole member of Tarantino LLC. The funds can terminate the ISO Agreement with Tarantino LLC at any time under the terms of the ISO Agreement. For the year ended October 31, 2018, the fee paid by the fund under this agreement was $696 and is included in “Miscellaneous” expense in the Statement of Operations. MFS has agreed to bear all expenses associated with office space, other administrative support, and supplies provided to the ISO.

The fund invests in the MFS Institutional Money Market Portfolio which is managed by MFS and seeks current income consistent with preservation of capital and liquidity. This money market fund does not pay a management fee to MFS.

31

Table of Contents

Notes to Financial Statements – continued