Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21780

MFS SERIES TRUST XII

(Exact name of registrant as specified in charter)

500 Boylston Street, Boston, Massachusetts 02116

(Address of principal executive offices) (Zip code)

Susan S. Newton

Massachusetts Financial Services Company

500 Boylston Street

Boston, Massachusetts 02116

(Name and address of agents for service)

Registrant’s telephone number, including area code: (617) 954-5000

Date of fiscal year end: October 31

Date of reporting period: October 31, 2011*

| * | This Form N-CSR pertains to the following series of the Registrant, MFS Equity Opportunities Fund (formerly MFS Sector Rotational Fund). The remaining series of the Registrant, MFS Lifetime Retirement Income Fund, MFS Lifetime 2010 Fund, MFS Lifetime 2020 Fund, MFS Lifetime 2030 Fund, MFS Lifetime 2040 Fund, and MFS Lifetime 2050 Fund have fiscal year ends of April 30. |

Table of Contents

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

Table of Contents

MFS® Equity Opportunities Fund

(formerly MFS® Sector Rotational Fund)

ANNUAL REPORT

October 31, 2011

MSR-ANN

Table of Contents

MFS® EQUITY OPPORTUNITIES FUND

(formerly MFS® Sector Rotational Fund)

SIPC Contact Information: You may obtain information about the Securities Investor Protection Corporation (“SIPC”), including the SIPC Brochure, by contacting SIPC either by telephone (1-202-371-8300) or by accessing SIPC’s web site address (www.sipc.org).

The report is prepared for the general information of shareholders. It is authorized for distribution to prospective investors only when preceded or accompanied by a current prospectus.

NOT FDIC INSURED Ÿ MAY LOSE VALUE Ÿ NO BANK GUARANTEE

Table of Contents

LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholders:

We are indeed living through some volatile times. Economic uncertainty is everywhere, as it seems no place in the world has been unmoved by crisis this year. We have seen a devastating earthquake and tsunami that have led to disruptions in the Japanese markets and supply chains. Protests have changed the face of the Middle East and left in their wake lingering tensions and resultant higher oil prices. We have seen debt limits tested in Europe and the United States and policymakers grappling to craft often unpopular monetary and fiscal responses at a time when consumers and businesses struggle with what appears to be a slowing global economy. On top of all of that, we have seen long-term U.S. debt lose its Standard & Poor’s AAA rating.

When markets become volatile, managing risk becomes a top priority for investors and their advisors. At MFS® risk management is foremost in our minds in all market climates. Our analysts and portfolio managers keep risks firmly in mind when evaluating securities. Additionally, we have a team of quantitative analysts that measures and assesses the risk profiles of our portfolios and securities on an ongoing basis. The chief investment risk officer, who oversees the team, reports directly to the firm’s president and chief investment officer so the risk associated with each portfolio can be assessed objectively and independently of the portfolio management team.

As always, we continue to be mindful of the many economic challenges faced at the local, national, and international levels. It is in times such as these that we want to remind investors of the merits of maintaining a long-term view, adhering to basic investing principles such as asset allocation and diversification, and working closely with their advisors to research and identify appropriate investment opportunities.

Respectfully,

Robert J. Manning

Chairman and Chief Executive Officer

MFS Investment Management®

December 16, 2011

The opinions expressed in this letter are subject to change, may not be relied upon for investment advice, and no forecasts can be guaranteed.

1

Table of Contents

Portfolio structure

| Top ten holdings | ||||

| Cliffs Natural Resources, Inc. | 2.8% | |||

| Macy’s, Inc. | 2.8% | |||

| Gilead Sciences, Inc. | 2.7% | |||

| Philip Morris International, Inc. | 2.7% | |||

| Aetna, Inc. | 2.7% | |||

| Reynolds American, Inc. | 2.7% | |||

| Chevron Corp. | 2.6% | |||

| Oracle Corp. | 2.5% | |||

| TIBCO Software, Inc. | 2.5% | |||

| Discover Financial Services | 2.5% |

| Equity sectors | ||||

| Financial Services | 18.3% | |||

| Health Care | 16.5% | |||

| Consumer Staples | 12.5% | |||

| Technology | 11.8% | |||

| Retailing | 7.6% | |||

| Utilities & Communications | 7.0% | |||

| Industrial Goods & Services | 6.9% | |||

| Basic Materials | 5.3% | |||

| Autos & Housing | 4.6% | |||

| Leisure | 4.6% | |||

| Energy | 2.6% | |||

| Transportation | 0.8% |

Percentages are based on net assets as of 10/31/11.

The portfolio is actively managed and current holdings may be different.

2

Table of Contents

Summary of Results

For the twelve months ended October 31, 2011, Class A shares of the MFS Equity Opportunities Fund (formerly the MFS Sector Rotational Fund) (the “fund”) provided a total return of 4.88%, at net asset value. This compares with a return of 8.01% for the fund’s benchmark, the Russell 1000 Index.

Market Environment

Early in the period, the U.S. Federal Reserve (the Fed) indicated that further monetary loosening would be forthcoming if macroeconomic activity did not show signs of improvement. The prospects for, and subsequent implementation of, more easing by the Fed improved market sentiment and drove risk-asset prices markedly higher. The December agreement on a surprisingly large (relative to expectations) expansionary U.S. fiscal package also boosted sentiment. During the subsequent several months, the renewed positive market sentiment, coupled with better indications of global macroeconomic activity, pushed many asset valuations to post-crisis highs. At the same time, global sovereign bond yields rose amidst the more “risk-seeking” environment.

However, towards the middle of the period, a weakening macroeconomic backdrop and renewed concerns over Greek debt sustainability began to challenge equity valuations and pushed high-quality sovereign bond yields lower. Towards the end of the reporting period, uncertainty in financial markets continued to increase. European policy makers debated and disagreed over elements of a new Greek bailout package, while Spanish and Italian bond yields increased markedly signaling a widening European crisis. In the U.S., concerns about sovereign debt default and the long-term sustainability of the trend in U.S. fiscal policy resulted in one agency downgrading U.S. credit quality. Amidst this turmoil, global equity markets declined sharply. As a result of these developments, global consumer and producer sentiment indicators fell precipitously, highly-rated sovereign bond yields hit multi-decade lows and, despite a more mixed picture emanating from the “hard” data, markets grew increasingly worried about a return to global recession.

Detractors from Performance

Stock selection in the transportation sector dampened performance relative to the Russell 1000 Index. Holdings of air transportation services company United Continental (h) and air cargo and aircraft operation solutions provider Atlas Air Worldwide Holdings (b) held back relative results as both stocks underperformed the benchmark over the reporting period. Shares of Atlas Air declined as the company reported lower profits due to higher maintenance and aircraft fuel expenses, while revenue growth missed analysts’ expectations.

3

Table of Contents

Management Review – continued

Stock selection and an underweight position in the technology sector was another negative factor for relative performance. The fund’s timing of ownership in shares of strong-performing computer and personal electronics maker Apple and automatic test equipment supplier Teradyne (h) hindered relative results. Holdings of network appliances company F5 Networks (h) also hurt. Shares of F5 Networks declined after reported earnings came in lower-than-consensus expectations. Investor concerns that future growth is slowing also appeared to have contributed to the loss.

Stock selection in the financial services sector held back relative performance. Holdings of insurance companies Genworth Financial and Aflac were among the fund’s top relative detractors over the reporting period.

Elsewhere, holdings of casino resorts operator Las Vegas Sands (h), cruise operator Royal Caribbean Cruises (h), and battery company Energizer Holdings (h) dampened relative performance. Shares of Las Vegas Sands declined as the company reported weaker-than-expected profits and revenue in the company’s Macau operations. Reports that Las Vegas Sands faces an investigation from the U.S. Securities and Exchange Commission and the Justice Department relating to its Macau operations’ compliance with the Foreign Corrupt Practices Act also negatively impacted its shares.

Contributors to Performance

Stock selection and an overweight position in the retailing sector were positive factors for relative performance. Within this sector, retailer Abercrombie & Fitch (h) was among the fund’s top relative contributors. Shares of Abercrombie & Fitch rose after the teen clothing retailer announced that it would open stores in China. The company also benefited, along with other retailers, from better-than-expected industry-wide retail sales. The fund’s holdings of retail farm and ranch stores operator Tractor Supply (h) and department stores operator Macy’s also bolstered relative results. Shares of Macy’s, one of the largest U.S. department store chains, traded higher after the company raised its 2011 profit outlook and doubled its dividend amid surging on-line sales.

Top relative contributors from other sectors included media company CBS (h) and tobacco manufacturer Reynolds American. Shares of Reynolds American rose as investors appeared to have continued to favor the characteristics of tobacco companies (e.g., strong pricing power, returning cash to shareholders) in the current uncertain economic environment. The fund’s timing of ownership in specialty chemicals company Rockwood Holdings (h), global integrated energy company Hess (h), wide area network optimization product designer and manufacturer Riverbed Technology (h), and biotech firm Gilead Sciences also aided relative performance. Not holding financial services firm

4

Table of Contents

Management Review – continued

Bank of America benefited relative returns as this stock significantly underperformed the benchmark over the reporting period.

Respectfully,

Matthew Krummell

Portfolio Manager

Note to Shareholders: Effective August 1, 2011, the fund’s name changed from MFS® Sector Rotational Fund to MFS® Equity Opportunities Fund.

| (b) | Security is not a benchmark constituent. |

| (h) | Security was not held in the portfolio at period end. |

The views expressed in this report are those of the portfolio manager only through the end of the period of the report as stated on the cover and do not necessarily reflect the views of MFS or any other person in the MFS organization. These views are subject to change at any time based on market or other conditions, and MFS disclaims any responsibility to update such views. These views may not be relied upon as investment advice or an indication of trading intent on behalf of any MFS portfolio. References to specific securities are not recommendations of such securities, and may not be representative of any MFS portfolio’s current or future investments.

5

Table of Contents

PERFORMANCE SUMMARY THROUGH 10/31/11

The following chart illustrates a representative class of the fund’s historical performance in comparison to its benchmark(s). Performance results include the deduction of the maximum applicable sales charge and reflect the percentage change in net asset value, including reinvestment of dividends and capital gains distributions. The performance of other share classes will be greater than or less than that of the class depicted below. Benchmarks are unmanaged and may not be invested in directly. Benchmark returns do not reflect sales charges, commissions or expenses. (See Notes to Performance Summary.)

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your shares, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. The performance shown does not reflect the deduction of taxes, if any, that a shareholder would pay on fund distributions or the redemption of fund shares.

Growth of a Hypothetical $10,000 Investment

6

Table of Contents

Performance Summary – continued

Total Returns through 10/31/11

Average annual without sales charge

| Share class | Class inception date | 1-yr | 5-yr | 10-yr | Life (t) | |||||||||

| A | 8/30/00 | 4.88% | 0.34% | 6.32% | N/A | |||||||||

| B | 1/03/07 | 4.14% | N/A | N/A | (1.10)% | |||||||||

| C | 3/01/04 | 4.09% | (0.35)% | N/A | 3.39% | |||||||||

| I | 2/28/11 | N/A | N/A | N/A | (6.01)% | |||||||||

| W | 3/03/08 | 5.10% | N/A | N/A | (1.55)% | |||||||||

| R1 | 5/01/08 | 4.08% | N/A | N/A | (3.55)% | |||||||||

| R2 | 5/01/08 | 4.67% | N/A | N/A | (3.05)% | |||||||||

| R3 | 5/01/08 | 4.92% | N/A | N/A | (2.82)% | |||||||||

| R4 | 5/01/08 | 5.12% | N/A | N/A | (2.57)% | |||||||||

| Comparative benchmark | ||||||||||||||

| Russell 1000 Index (f) | 8.01% | 0.54% | 4.17% | N/A | ||||||||||

| Average annual with sales charge | ||||||||||||||

| A With Initial Sales Charge (5.75%) |

(1.15)% | (0.84)% | 5.70% | N/A | ||||||||||

| B With CDSC (Declining over six years from 4% to 0%) (x) |

0.14% | N/A | N/A | (1.51)% | ||||||||||

| C With CDSC (1% for 12 months) (x) |

3.09% | (0.35)% | N/A | 3.39% | ||||||||||

Class I, W, R1, R2, R3, and R4 shares do not have a sales charge.

CDSC – Contingent Deferred Sales Charge.

| (f) | Source: FactSet Research Systems Inc. |

| (t) | For the period from the class inception date through the stated period end (for those share classes with less than 10 years of performance history). No comparative benchmark performance information is provided for “life” periods. (See Notes to Performance Summary.) |

| (x) | Assuming redemption at the end of the applicable period. |

Benchmark Definition

Russell 1000 Index – constructed to provide a comprehensive barometer for the large-cap segment of the U.S. equity universe based on total market capitalization, which represents approximately 92% of the investable U.S. equity market.

It is not possible to invest directly in an index.

7

Table of Contents

Performance Summary – continued

Notes to Performance Summary

Performance information in the chart and tables for periods prior to January 3, 2007, reflect performance information of the Penn Street Advisors Sector Rotational Portfolio, the fund’s predecessor (the “Predecessor Fund”). On January 3, 2007, the fund acquired all of the assets of the Predecessor Fund pursuant to an agreement and plan of reorganization, in exchange for Class A and Class C shares of the fund. The dates in the table are the inception dates for the predecessor fund’s Class A and C shares.

Prior to February 1, 2010, Valley Forge Capital Advisors, Inc. (“Valley Forge”) served as the sub-adviser for the fund. Effective February 1, 2010, Valley Forge no longer served as the sub-adviser of the fund and MFS assumed responsibility for the day-to-day management of the fund’s portfolio in its capacity as the fund’s investment adviser.

Average annual total return represents the average annual change in value for each share class for the periods presented. Life returns are presented where the share class has less than 10 years of performance history and represent the average annual total return from the class inception date to the stated period end date. As the fund’s share classes may have different inception dates, the life returns may represent different time periods and may not be comparable. As a result, no comparative benchmark performance information is provided for life periods.

Performance results reflect any applicable expense subsidies and waivers in effect during the periods shown. Without such subsidies and waivers the fund’s performance results would be less favorable. Please see the prospectus and financial statements for complete details.

Performance results do not include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles and may differ from amounts reported in the financial highlights.

From time to time the fund may receive proceeds from litigation settlements, without which performance would be lower.

8

Table of Contents

Fund expenses borne by the shareholders during the period,

May 1, 2011 through October 31, 2011

As a shareholder of the fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on certain purchase or redemption payments, and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period May 1, 2011 through October 31, 2011.

Actual Expenses

The first line for each share class in the following table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each share class in the following table provides information about hypothetical account values and hypothetical expenses based on the fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line for each share class in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

9

Table of Contents

Expense Table – continued

| Share Class |

Annualized Expense Ratio |

Beginning Account Value 5/01/11 |

Ending Account Value 10/31/11 |

Expenses Paid During Period (p) 5/01/11-10/31/11 |

||||||||||||||

| A | Actual | 1.29% | $1,000.00 | $906.42 | $6.20 | |||||||||||||

| Hypothetical (h) | 1.29% | $1,000.00 | $1,018.70 | $6.56 | ||||||||||||||

| B | Actual | 2.04% | $1,000.00 | $903.08 | $9.79 | |||||||||||||

| Hypothetical (h) | 2.04% | $1,000.00 | $1,014.92 | $10.36 | ||||||||||||||

| C | Actual | 2.04% | $1,000.00 | $902.63 | $9.78 | |||||||||||||

| Hypothetical (h) | 2.04% | $1,000.00 | $1,014.92 | $10.36 | ||||||||||||||

| I | Actual | 0.98% | $1,000.00 | $907.22 | $4.71 | |||||||||||||

| Hypothetical (h) | 0.98% | $1,000.00 | $1,020.27 | $4.99 | ||||||||||||||

| W | Actual | 1.14% | $1,000.00 | $907.61 | $5.48 | |||||||||||||

| Hypothetical (h) | 1.14% | $1,000.00 | $1,019.46 | $5.80 | ||||||||||||||

| R1 | Actual | 2.04% | $1,000.00 | $903.03 | $9.79 | |||||||||||||

| Hypothetical (h) | 2.04% | $1,000.00 | $1,014.92 | $10.36 | ||||||||||||||

| R2 | Actual | 1.54% | $1,000.00 | $905.56 | $7.40 | |||||||||||||

| Hypothetical (h) | 1.54% | $1,000.00 | $1,017.44 | $7.83 | ||||||||||||||

| R3 | Actual | 1.29% | $1,000.00 | $906.32 | $6.20 | |||||||||||||

| Hypothetical (h) | 1.29% | $1,000.00 | $1,018.70 | $6.56 | ||||||||||||||

| R4 | Actual | 1.04% | $1,000.00 | $907.22 | $5.00 | |||||||||||||

| Hypothetical (h) | 1.04% | $1,000.00 | $1,019.96 | $5.30 | ||||||||||||||

| (h) | 5% class return per year before expenses. |

| (p) | Expenses paid is equal to each class’ annualized expense ratio, as shown above, multiplied by the average account value over the period, multiplied by the number of days in the period, divided by the number of days in the year. Expenses paid do not include any applicable sales charges (loads). If these transaction costs had been included, your costs would have been higher. |

10

Table of Contents

10/31/11

The Portfolio of Investments is a complete list of all securities owned by your fund. It is categorized by broad-based asset classes.

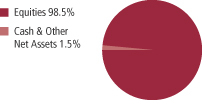

| Common Stocks - 98.5% | ||||||||

| Issuer | Shares/Par | Value ($) | ||||||

| Aerospace - 2.2% | ||||||||

| Lockheed Martin Corp. | 43,480 | $ | 3,300,129 | |||||

| Apparel Manufacturers - 0.8% | ||||||||

| Jones Group, Inc. | 114,045 | $ | 1,273,883 | |||||

| Automotive - 4.6% | ||||||||

| General Motors Co. (a) | 124,480 | $ | 3,217,808 | |||||

| Lear Corp. | 80,730 | 3,787,044 | ||||||

|

|

|

|||||||

| $ | 7,004,852 | |||||||

| Biotechnology - 5.0% | ||||||||

| Amgen, Inc. | 61,800 | $ | 3,539,286 | |||||

| Gilead Sciences, Inc. (a) | 99,470 | 4,143,920 | ||||||

|

|

|

|||||||

| $ | 7,683,206 | |||||||

| Brokerage & Asset Managers - 2.3% | ||||||||

| NASDAQ OMX Group, Inc. (a) | 137,700 | $ | 3,449,385 | |||||

| Cable TV - 4.6% | ||||||||

| Time Warner Cable, Inc. | 54,850 | $ | 3,493,397 | |||||

| Virgin Media, Inc. | 142,520 | 3,474,638 | ||||||

|

|

|

|||||||

| $ | 6,968,035 | |||||||

| Chemicals - 2.5% | ||||||||

| PPG Industries, Inc. | 43,950 | $ | 3,797,720 | |||||

| Computer Software - 5.0% | ||||||||

| Oracle Corp. | 117,230 | $ | 3,841,627 | |||||

| TIBCO Software, Inc. (a) | 132,850 | 3,838,037 | ||||||

|

|

|

|||||||

| $ | 7,679,664 | |||||||

| Computer Software - Systems - 4.5% | ||||||||

| Apple, Inc. (a) | 8,100 | $ | 3,278,718 | |||||

| BroadSoft, Inc. (a) | 101,510 | 3,654,360 | ||||||

|

|

|

|||||||

| $ | 6,933,078 | |||||||

| Energy - Integrated - 2.6% | ||||||||

| Chevron Corp. | 37,050 | $ | 3,892,103 | |||||

11

Table of Contents

Portfolio of Investments – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Common Stocks - continued | ||||||||

| Engineering - Construction - 2.4% | ||||||||

| Fluor Corp. | 63,630 | $ | 3,617,366 | |||||

| Food & Beverages - 2.2% | ||||||||

| Coca-Cola Enterprises, Inc. | 126,490 | $ | 3,392,462 | |||||

| Food & Drug Stores - 2.3% | ||||||||

| Kroger Co. | 153,360 | $ | 3,554,885 | |||||

| General Merchandise - 2.8% | ||||||||

| Macy’s, Inc. | 137,760 | $ | 4,205,813 | |||||

| Health Maintenance Organizations - 5.0% | ||||||||

| Aetna, Inc. | 102,940 | $ | 4,092,894 | |||||

| WellPoint, Inc. | 50,890 | 3,506,321 | ||||||

|

|

|

|||||||

| $ | 7,599,215 | |||||||

| Insurance - 11.5% | ||||||||

| Aflac, Inc. | 55,370 | $ | 2,496,633 | |||||

| Allied World Assurance Co. | 62,920 | 3,655,652 | ||||||

| Genworth Financial, Inc. (a) | 369,690 | 2,358,622 | ||||||

| Hartford Financial Services Group, Inc. | 161,870 | 3,115,998 | ||||||

| MetLife, Inc. | 86,450 | 3,039,582 | ||||||

| Prudential Financial, Inc. | 53,170 | 2,881,814 | ||||||

|

|

|

|||||||

| $ | 17,548,301 | |||||||

| Internet - 2.3% | ||||||||

| Google, Inc., “A” (a) | 5,900 | $ | 3,496,576 | |||||

| Major Banks - 2.0% | ||||||||

| JPMorgan Chase & Co. | 87,230 | $ | 3,032,115 | |||||

| Medical & Health Technology & Services - 2.3% | ||||||||

| DaVita, Inc. (a) | 50,130 | $ | 3,509,100 | |||||

| Metals & Mining - 2.8% | ||||||||

| Cliffs Natural Resources, Inc. | 63,190 | $ | 4,310,822 | |||||

| Other Banks & Diversified Financials - 2.5% | ||||||||

| Discover Financial Services | 161,820 | $ | 3,812,479 | |||||

12

Table of Contents

Portfolio of Investments – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Common Stocks - continued | ||||||||

| Pharmaceuticals - 4.2% | ||||||||

| Abbott Laboratories | 51,030 | $ | 2,748,986 | |||||

| Pfizer, Inc. | 193,590 | 3,728,543 | ||||||

|

|

|

|||||||

| $ | 6,477,529 | |||||||

| Pollution Control - 2.3% | ||||||||

| Republic Services, Inc. | 122,000 | $ | 3,472,120 | |||||

| Specialty Stores - 1.7% | ||||||||

| TJX Cos., Inc. | 43,410 | $ | 2,558,151 | |||||

| Tobacco - 10.3% | ||||||||

| Altria Group, Inc. | 135,970 | $ | 3,745,974 | |||||

| Lorillard, Inc. | 34,350 | 3,801,171 | ||||||

| Philip Morris International, Inc. | 58,870 | 4,113,247 | ||||||

| Reynolds American, Inc. | 105,500 | 4,080,740 | ||||||

|

|

|

|||||||

| $ | 15,741,132 | |||||||

| Trucking - 0.8% | ||||||||

| Atlas Air Worldwide Holdings, Inc. (a) | 32,180 | $ | 1,239,574 | |||||

| Utilities - Electric Power - 7.0% | ||||||||

| AES Corp. (a) | 309,990 | $ | 3,478,088 | |||||

| Alliant Energy Corp. | 86,930 | 3,545,005 | ||||||

| CenterPoint Energy, Inc. | 171,450 | 3,573,018 | ||||||

|

|

|

|||||||

| $ | 10,596,111 | |||||||

| Total Common Stocks (Identified Cost, $146,843,208) | $ | 150,145,806 | ||||||

| Money Market Funds (v) - 0.1% | ||||||||

| MFS Institutional Money Market Portfolio, 0.07%, at Cost and Net Asset Value |

174,611 | $ | 174,611 | |||||

| Total Investments (Identified Cost, $147,017,819) | $ | 150,320,417 | ||||||

| Other Assets, Less Liabilities - 1.4% | 2,154,224 | |||||||

| Net Assets - 100.0% | $ | 152,474,641 | ||||||

| (a) | Non-income producing security. |

| (v) | Underlying affiliated fund that is available only to investment companies managed by MFS. The rate quoted is the annualized seven-day yield of the fund at period end. |

See Notes to Financial Statements

13

Table of Contents

Financial Statements

STATEMENT OF ASSETS AND LIABILITIES

At 10/31/11

This statement represents your fund’s balance sheet, which details the assets and liabilities comprising the total value of the fund.

| Assets | ||||

| Investments- |

||||

| Non-affiliated issuers, at value (identified cost, $146,843,208) |

$150,145,806 | |||

| Underlying affiliated funds, at cost and value |

174,611 | |||

| Total investments, at value (identified cost, $147,017,819) |

$150,320,417 | |||

| Receivables for |

||||

| Investments sold |

16,748,707 | |||

| Fund shares sold |

223,000 | |||

| Dividends |

69,526 | |||

| Total assets |

$167,361,650 | |||

| Liabilities | ||||

| Payables for |

||||

| Investments purchased |

$14,059,643 | |||

| Fund shares reacquired |

659,811 | |||

| Payable to affiliates |

||||

| Investment adviser |

13,252 | |||

| Shareholder servicing costs |

87,387 | |||

| Distribution and service fees |

7,454 | |||

| Payable for independent Trustees’ compensation |

43 | |||

| Accrued expenses and other liabilities |

59,419 | |||

| Total liabilities |

$14,887,009 | |||

| Net assets |

$152,474,641 | |||

| Net assets consist of | ||||

| Paid-in capital |

$265,819,112 | |||

| Unrealized appreciation (depreciation) on investments |

3,302,598 | |||

| Accumulated net realized gain (loss) on investments |

(118,135,824 | ) | ||

| Undistributed net investment income |

1,488,755 | |||

| Net assets |

$152,474,641 | |||

| Shares of beneficial interest outstanding |

9,231,088 |

14

Table of Contents

Statement of Assets and Liabilities – continued

| Net assets | Shares outstanding |

Net asset value per share (a) |

||||||||||

| Class A | $91,777,842 | 5,507,544 | $16.66 | |||||||||

| Class B | 10,418,540 | 646,388 | 16.12 | |||||||||

| Class C | 32,004,882 | 1,983,608 | 16.13 | |||||||||

| Class I | 7,440,476 | 444,955 | 16.72 | |||||||||

| Class W | 5,555,544 | 332,701 | 16.70 | |||||||||

| Class R1 | 91,723 | 5,692 | 16.11 | |||||||||

| Class R2 | 99,118 | 6,081 | 16.30 | |||||||||

| Class R3 | 101,853 | 6,119 | 16.65 | |||||||||

| Class R4 | 4,984,663 | 298,000 | 16.73 | |||||||||

| (a) | Maximum offering price per share was equal to the net asset value per share for all share classes, except for Class A, for which the maximum offering price per share was $17.68 [100 / 94.25 x $16.66]. On sales of $50,000 or more, the maximum offering price of Class A shares is reduced. A contingent deferred sales charge may be imposed on redemptions of Class A, Class B, and Class C shares. Redemption price per share was equal to the net asset value per share for Classes I, W, R1, R2, R3, and R4. |

See Notes to Financial Statements

15

Table of Contents

Financial Statements

Year ended 10/31/11

This statement describes how much your fund earned in investment income and accrued in expenses.

It also describes any gains and/or losses generated by fund operations.

| Net investment income | ||||

| Income |

||||

| Dividends |

$4,539,789 | |||

| Dividends from underlying affiliated funds |

2,931 | |||

| Total investment income |

$4,542,720 | |||

| Expenses |

||||

| Management fee |

$1,341,484 | |||

| Distribution and service fees |

768,498 | |||

| Shareholder servicing costs |

263,357 | |||

| Administrative services fee |

35,505 | |||

| Independent Trustees’ compensation |

6,295 | |||

| Custodian fee |

26,151 | |||

| Shareholder communications |

26,232 | |||

| Auditing fees |

42,590 | |||

| Legal fees |

2,634 | |||

| Miscellaneous |

161,628 | |||

| Total expenses |

$2,674,374 | |||

| Fees paid indirectly |

(71 | ) | ||

| Reduction of expenses by investment adviser |

(777 | ) | ||

| Net expenses |

$2,673,526 | |||

| Net investment income |

$1,869,194 | |||

| Realized and unrealized gain (loss) on investments | ||||

| Realized gain (loss) on investment transactions (identified cost basis) |

$27,025,101 | |||

| Change in unrealized appreciation (depreciation) on investments |

$(23,293,015 | ) | ||

| Net realized and unrealized gain (loss) on investments |

$3,732,086 | |||

| Change in net assets from operations |

$5,601,280 |

See Notes to Financial Statements

16

Table of Contents

Financial Statements

STATEMENTS OF CHANGES IN NET ASSETS

These statements describe the increases and/or decreases in net assets resulting from operations, any distributions, and any shareholder transactions.

| Years ended 10/31 | ||||||||

| 2011 | 2010 | |||||||

| Change in net assets | ||||||||

| From operations | ||||||||

| Net investment income |

$1,869,194 | $657,055 | ||||||

| Net realized gain (loss) on investments |

27,025,101 | 26,028,537 | ||||||

| Net unrealized gain (loss) on investments |

(23,293,015 | ) | 14,120,916 | |||||

| Change in net assets from operations |

$5,601,280 | $40,806,508 | ||||||

| Distributions declared to shareholders | ||||||||

| From net investment income |

$(1,050,009 | ) | $(400,097 | ) | ||||

| Change in net assets from fund share transactions |

$(6,965,918 | ) | $(98,449,195 | ) | ||||

| Total change in net assets |

$(2,414,647 | ) | $(58,042,784 | ) | ||||

| Net assets | ||||||||

| At beginning of period |

154,889,288 | 212,932,072 | ||||||

| At end of period (including undistributed net investment |

$152,474,641 | $154,889,288 | ||||||

See Notes to Financial Statements

17

Table of Contents

Financial Statements

The financial highlights table is intended to help you understand the fund’s financial performance for the past 5 years (or life of a particular share class, if shorter). Certain information reflects financial results for a single fund share. The total returns in the table represent the rate by which an investor would have earned (or lost) on an investment in the fund share class (assuming reinvestment of all distributions) held for the entire period.

| Class A | Years ended 10/31 | |||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| Net asset value, beginning of period |

$16.01 | $12.62 | $12.40 | $20.02 | $17.50 | |||||||||||||||

| Income (loss) from investment operations | ||||||||||||||||||||

| Net investment income (loss) (d) |

$0.21 | $0.08 | $0.04 | $0.02 | $(0.03 | ) | ||||||||||||||

| Net realized and unrealized gain (loss) |

0.57 | 3.34 | 0.18 | (7.64 | ) | 3.55 | ||||||||||||||

| Total from investment operations |

$0.78 | $3.42 | $0.22 | $(7.62 | ) | $3.52 | ||||||||||||||

| Less distributions declared to shareholders | ||||||||||||||||||||

| From net investment income |

$(0.13 | ) | $(0.03 | ) | $— | $— | $— | |||||||||||||

| From net realized gain on investments |

— | — | — | — | (1.00 | ) | ||||||||||||||

| Total distributions declared to shareholders |

$(0.13 | ) | $(0.03 | ) | $— | $– | $(1.00 | ) | ||||||||||||

| Net asset value, end of period |

$16.66 | $16.01 | $12.62 | $12.40 | $20.02 | |||||||||||||||

| Total return (%) (r)(s)(t)(x) |

4.88 | 27.15 | 1.77 | (38.06 | ) | 20.99 | ||||||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

||||||||||||||||||||

| Expenses before expense reductions (f) |

1.32 | 1.37 | 1.41 | 1.38 | 1.38 | |||||||||||||||

| Expenses after expense reductions (f) |

1.32 | 1.37 | 1.39 | 1.38 | 1.37 | |||||||||||||||

| Net investment income (loss) |

1.23 | 0.59 | 0.34 | 0.13 | (0.14 | ) | ||||||||||||||

| Portfolio turnover |

154 | 191 | 211 | 196 | 141 | |||||||||||||||

| Net assets at end of period (000 omitted) |

$91,778 | $90,409 | $137,360 | $236,816 | $210,954 | |||||||||||||||

See Notes to Financial Statements

18

Table of Contents

Financial Highlights – continued

| Class B | Years ended 10/31 | |||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 (i) | ||||||||||||||||

| Net asset value, beginning of period |

$15.50 | $12.28 | $12.16 | $19.75 | $17.03 | |||||||||||||||

| Income (loss) from investment operations | ||||||||||||||||||||

| Net investment income (loss) (d) |

$0.08 | $(0.02 | ) | $(0.04 | ) | $(0.09 | ) | $(0.12 | ) | |||||||||||

| Net realized and unrealized gain (loss) |

0.56 | 3.24 | 0.16 | (7.50 | ) | 2.84 | (g) | |||||||||||||

| Total from investment operations |

$0.64 | $3.22 | $0.12 | $(7.59 | ) | $2.72 | ||||||||||||||

| Less distributions declared to shareholders | ||||||||||||||||||||

| From net investment income |

$(0.02 | ) | $— | $— | $— | $— | ||||||||||||||

| Net asset value, end of period |

$16.12 | $15.50 | $12.28 | $12.16 | $19.75 | |||||||||||||||

| Total return (%) (r)(s)(t)(x) |

4.14 | 26.22 | 0.99 | (38.43 | ) | 15.97 | (n) | |||||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

||||||||||||||||||||

| Expenses before expense reductions (f) |

2.07 | 2.12 | 2.12 | 2.03 | 1.98 | (a) | ||||||||||||||

| Expenses after expense reductions (f) |

2.07 | 2.12 | 2.10 | 2.03 | 1.98 | (a) | ||||||||||||||

| Net investment income (loss) |

0.51 | (0.16 | ) | (0.39 | ) | (0.53 | ) | (0.85 | )(a) | |||||||||||

| Portfolio turnover |

154 | 191 | 211 | 196 | 141 | |||||||||||||||

| Net assets at end of period (000 omitted) |

$10,419 | $11,825 | $12,028 | $15,029 | $13,484 | |||||||||||||||

| Class C | Years ended 10/31 | |||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| Net asset value, beginning of period |

$15.51 | $12.29 | $12.16 | $19.76 | $17.38 | |||||||||||||||

| Income (loss) from investment operations | ||||||||||||||||||||

| Net investment income (loss) (d) |

$0.08 | $(0.02 | ) | $(0.04 | ) | $(0.09 | ) | $(0.15 | ) | |||||||||||

| Net realized and unrealized gain (loss) |

0.55 | 3.24 | 0.17 | (7.51 | ) | 3.53 | ||||||||||||||

| Total from investment operations |

$0.63 | $3.22 | $0.13 | $(7.60 | ) | $3.38 | ||||||||||||||

| Less distributions declared to shareholders | ||||||||||||||||||||

| From net investment income |

$(0.01 | ) | $— | $— | $— | $— | ||||||||||||||

| From net realized gain on investments |

— | — | — | — | (1.00 | ) | ||||||||||||||

| Total distributions declared to shareholders |

$(0.01 | ) | $— | $— | $— | $(1.00 | ) | |||||||||||||

| Net asset value, end of period |

$16.13 | $15.51 | $12.29 | $12.16 | $19.76 | |||||||||||||||

| Total return (%) (r)(s)(t)(x) |

4.09 | 26.20 | 1.07 | (38.46 | ) | 20.30 | ||||||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

||||||||||||||||||||

| Expenses before expense reductions (f) |

2.07 | 2.12 | 2.12 | 2.03 | 1.98 | |||||||||||||||

| Expenses after expense reductions (f) |

2.07 | 2.12 | 2.10 | 2.03 | 1.98 | |||||||||||||||

| Net investment income (loss) |

0.49 | (0.16 | ) | (0.39 | ) | (0.53 | ) | (0.85 | ) | |||||||||||

| Portfolio turnover |

154 | 191 | 211 | 196 | 141 | |||||||||||||||

| Net assets at end of period (000 omitted) |

$32,005 | $34,189 | $46,261 | $61,857 | $51,831 | |||||||||||||||

See Notes to Financial Statements

19

Table of Contents

Financial Highlights – continued

| Class I | Period ended 10/31/11 (i) |

|||

| Net asset value, beginning of period |

$17.79 | |||

| Income (loss) from investment operations | ||||

| Net investment income (d) |

$0.05 | |||

| Net realized and unrealized gain (loss) |

(1.12 | )(g) | ||

| Total from investment operations |

$(1.07 | ) | ||

| Net asset value, end of period |

$16.72 | |||

| Total return (%) (r)(s)(x) |

(6.01 | )(n) | ||

| Ratios (%) (to average net assets) and Supplemental data: |

||||

| Expenses before expense reductions (f) |

0.99 | (a) | ||

| Expenses after expense reductions (f) |

0.99 | (a) | ||

| Net investment income |

0.46 | (a) | ||

| Portfolio turnover |

154 | |||

| Net assets at end of period (000 omitted) |

$7,440 | |||

| Class W | Years ended 10/31 | |||||||||||||||

| 2011 | 2010 | 2009 | 2008 (i) | |||||||||||||

| Net asset value, beginning of period |

$16.04 | $12.67 | $12.42 | $17.96 | ||||||||||||

| Income (loss) from investment operations | ||||||||||||||||

| Net investment income (d) |

$0.23 | $0.10 | $0.05 | $0.03 | ||||||||||||

| Net realized and unrealized gain (loss) |

0.59 | 3.35 | 0.20 | (5.57 | )(g) | |||||||||||

| Total from investment operations |

$0.82 | $3.45 | $0.25 | $(5.54 | ) | |||||||||||

| Less distributions declared to shareholders | ||||||||||||||||

| From net investment income |

$(0.16 | ) | $(0.08 | ) | $— | $— | ||||||||||

| Net asset value, end of period |

$16.70 | $16.04 | $12.67 | $12.42 | ||||||||||||

| Total return (%) (r)(s)(x) |

5.10 | 27.34 | 2.01 | (30.85 | )(n) | |||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

||||||||||||||||

| Expenses before expense reductions (f) |

1.16 | 1.22 | 1.20 | 1.13 | (a) | |||||||||||

| Expenses after expense reductions (f) |

1.16 | 1.22 | 1.19 | 1.12 | (a) | |||||||||||

| Net investment income |

1.32 | 0.72 | 0.36 | 0.30 | (a) | |||||||||||

| Portfolio turnover |

154 | 191 | 211 | 196 | ||||||||||||

| Net assets at end of period (000 omitted) |

$5,556 | $13,324 | $15,824 | $1,430 | ||||||||||||

See Notes to Financial Statements

20

Table of Contents

Financial Highlights – continued

| Class R1 | Years ended 10/31 | |||||||||||||||

| 2011 | 2010 | 2009 | 2008 (i) | |||||||||||||

| Net asset value, beginning of period |

$15.51 | $12.29 | $12.16 | $18.32 | ||||||||||||

| Income (loss) from investment operations | ||||||||||||||||

| Net investment income (loss) (d) |

$0.08 | $(0.02 | ) | $(0.05 | ) | $(0.04 | ) | |||||||||

| Net realized and unrealized gain (loss) |

0.55 | 3.24 | 0.18 | (6.12 | )(g) | |||||||||||

| Total from investment operations |

$0.63 | $3.22 | $0.13 | $(6.16 | ) | |||||||||||

| Less distributions declared to shareholders | ||||||||||||||||

| From net investment income |

$(0.03 | ) | $— | $— | $— | |||||||||||

| Net asset value, end of period |

$16.11 | $15.51 | $12.29 | $12.16 | ||||||||||||

| Total return (%) (r)(s)(x) |

4.08 | 26.20 | 1.07 | (33.62 | )(n) | |||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

||||||||||||||||

| Expenses before expense reductions (f) |

2.06 | 2.12 | 2.12 | 2.03 | (a) | |||||||||||

| Expenses after expense reductions (f) |

2.06 | 2.12 | 2.10 | 2.03 | (a) | |||||||||||

| Net investment income (loss) |

0.47 | (0.15 | ) | (0.41 | ) | (0.48 | )(a) | |||||||||

| Portfolio turnover |

154 | 191 | 211 | 196 | ||||||||||||

| Net assets at end of period (000 omitted) |

$92 | $85 | $67 | $66 | ||||||||||||

| Class R2 | Years ended 10/31 | |||||||||||||||

| 2011 | 2010 | 2009 | 2008 (i) | |||||||||||||

| Net asset value, beginning of period |

$15.67 | $12.38 | $12.19 | $18.32 | ||||||||||||

| Income (loss) from investment operations | ||||||||||||||||

| Net investment income (d) |

$0.16 | $0.05 | $0.01 | $0.00 | (w) | |||||||||||

| Net realized and unrealized gain (loss) |

0.57 | 3.27 | 0.18 | (6.13 | )(g) | |||||||||||

| Total from investment operations |

$0.73 | $3.32 | $0.19 | $(6.13 | ) | |||||||||||

| Less distributions declared to shareholders | ||||||||||||||||

| From net investment income |

$(0.10 | ) | $(0.03 | ) | $— | $— | ||||||||||

| Net asset value, end of period |

$16.30 | $15.67 | $12.38 | $12.19 | ||||||||||||

| Total return (%) (r)(s)(x) |

4.67 | 26.82 | 1.56 | (33.46 | )(n) | |||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

||||||||||||||||

| Expenses before expense reductions (f) |

1.56 | 1.62 | 1.62 | 1.53 | (a) | |||||||||||

| Expenses after expense reductions (f) |

1.56 | 1.62 | 1.60 | 1.52 | (a) | |||||||||||

| Net investment income |

0.94 | 0.35 | 0.08 | 0.02 | (a) | |||||||||||

| Portfolio turnover |

154 | 191 | 211 | 196 | ||||||||||||

| Net assets at end of period (000 omitted) |

$99 | $86 | $68 | $67 | ||||||||||||

See Notes to Financial Statements

21

Table of Contents

Financial Highlights – continued

| Class R3 | Years ended 10/31 | |||||||||||||||

| 2011 | 2010 | 2009 | 2008 (i) | |||||||||||||

| Net asset value, beginning of period |

$15.99 | $12.63 | $12.41 | $18.62 | ||||||||||||

| Income (loss) from investment operations | ||||||||||||||||

| Net investment income (d) |

$0.20 | $0.08 | $0.04 | $0.02 | ||||||||||||

| Net realized and unrealized gain (loss) |

0.60 | 3.33 | 0.18 | (6.23 | )(g) | |||||||||||

| Total from investment operations |

$0.80 | $3.41 | $0.22 | $(6.21 | ) | |||||||||||

| Less distributions declared to shareholders | ||||||||||||||||

| From net investment income |

$(0.14 | ) | $(0.05 | ) | $— | $— | ||||||||||

| Net asset value, end of period |

$16.65 | $15.99 | $12.63 | $12.41 | ||||||||||||

| Total return (%) (r)(s)(x) |

4.98 | 27.11 | 1.77 | (33.35 | )(n) | |||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

||||||||||||||||

| Expenses before expense reductions (f) |

1.31 | 1.37 | 1.37 | 1.27 | (a) | |||||||||||

| Expenses after expense reductions (f) |

1.31 | 1.37 | 1.35 | 1.27 | (a) | |||||||||||

| Net investment income |

1.20 | 0.60 | 0.33 | 0.28 | (a) | |||||||||||

| Portfolio turnover |

154 | 191 | 211 | 196 | ||||||||||||

| Net assets at end of period (000 omitted) |

$102 | $86 | $68 | $67 | ||||||||||||

See Notes to Financial Statements

22

Table of Contents

Financial Highlights – continued

| Class R4 | Years ended 10/31 | |||||||||||||||

| 2011 | 2010 | 2009 | 2008 (i) | |||||||||||||

| Net asset value, beginning of period |

$16.07 | $12.68 | $12.43 | $18.62 | ||||||||||||

| Income (loss) from investment operations | ||||||||||||||||

| Net investment income (d) |

$0.25 | $0.10 | $0.07 | $0.04 | ||||||||||||

| Net realized and unrealized gain (loss) |

0.58 | 3.37 | 0.18 | (6.23 | )(g) | |||||||||||

| Total from investment operations |

$0.83 | $3.47 | $0.25 | $(6.19 | ) | |||||||||||

| Less distributions declared to shareholders | ||||||||||||||||

| From net investment income |

$(0.17 | ) | $(0.08 | ) | $— | $— | ||||||||||

| Net asset value, end of period |

$16.73 | $16.07 | $12.68 | $12.43 | ||||||||||||

| Total return (%) (r)(s)(x) |

5.18 | 27.52 | 2.01 | (33.24 | )(n) | |||||||||||

| Ratios (%) (to average net assets) and Supplemental data: |

||||||||||||||||

| Expenses before expense reductions (f) |

1.07 | 1.10 | 1.12 | 1.03 | (a) | |||||||||||

| Expenses after expense reductions (f) |

1.07 | 1.10 | 1.11 | 1.03 | (a) | |||||||||||

| Net investment income |

1.48 | 0.73 | 0.57 | 0.57 | (a) | |||||||||||

| Portfolio turnover |

154 | 191 | 211 | 196 | ||||||||||||

| Net assets at end of period (000 omitted) |

$4,985 | $4,886 | $1,258 | $1,069 | ||||||||||||

| (a) | Annualized. |

| (d) | Per share data is based on average shares outstanding. |

| (f) | Ratios do not reflect reductions from fees paid indirectly, if applicable. |

| (g) | The per share amount varies from the net realized and unrealized gain/loss for the period because of the timing of sales of fund shares and the per share amount of realized and unrealized gains and losses at such time. |

| (i) | For the period from the class’ inception, January 3, 2007 (Class B), February 28, 2011 (Class I), March 3, 2008 (Class W), and May 1, 2008, (Classes R1, R2, R3 and R4) through the stated period end. |

| (n) | Not annualized. |

| (r) | Certain expenses have been reduced without which performance would have been lower. |

| (s) | From time to time the fund may receive proceeds from litigation settlements, without which performance would be lower. |

| (t) | Total returns do not include any applicable sales charges. |

| (w) | Per share amount was less than $0.01. |

| (x) | Total returns have been calculated on net asset values which include adjustments made in accordance with U.S. generally accepted accounting principles required at period end for financial reporting purposes. |

See Notes to Financial Statements

23

Table of Contents

| (1) | Business and Organization |

MFS Equity Opportunities Fund (formerly MFS Sector Rotational Fund) (the fund) is a series of MFS Series Trust XII (the trust). The trust is organized as a Massachusetts business trust and is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company.

| (2) | Significant Accounting Policies |

General – The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. In the preparation of these financial statements, management has evaluated subsequent events occurring after the date of the fund’s Statement of Assets and Liabilities through the date that the financial statements were issued.

Investment Valuations – Equity securities, including restricted equity securities, are generally valued at the last sale or official closing price as provided by a third-party pricing service on the market or exchange on which they are primarily traded. Equity securities, for which there were no sales reported that day, are generally valued at the last quoted daily bid quotation as provided by a third-party pricing service on the market or exchange on which such securities are primarily traded. Equity securities held short, for which there were no sales reported for that day, are generally valued at the last quoted daily ask quotation as provided by a third-party pricing service on the market or exchange on which such securities are primarily traded. Short-term instruments with a maturity at issuance of 60 days or less generally are valued at amortized cost, which approximates market value. Open-end investment companies are generally valued at net asset value per share. Securities and other assets generally valued on the basis of information from a third-party pricing service may also be valued at a broker/dealer bid quotation. Values obtained from third-party pricing services can utilize both transaction data and market information such as yield, quality, coupon rate, maturity, type of issue, trading characteristics, and other market data.

The Board of Trustees has delegated primary responsibility for determining or causing to be determined the value of the fund’s investments (including any fair valuation) to the adviser pursuant to valuation policies and procedures approved by the Board. If the adviser determines that reliable market quotations are not readily available, investments are valued at fair value as determined in good faith by the adviser in accordance with such procedures

24

Table of Contents

Notes to Financial Statements – continued

under the oversight of the Board of Trustees. Under the fund’s valuation policies and procedures, market quotations are not considered to be readily available for most types of debt instruments and floating rate loans and many types of derivatives. These investments are generally valued at fair value based on information from third-party pricing services. In addition, investments may be valued at fair value if the adviser determines that an investment’s value has been materially affected by events occurring after the close of the exchange or market on which the investment is principally traded (such as foreign exchange or market) and prior to the determination of the fund’s net asset value, or after the halting of trading of a specific security where trading does not resume prior to the close of the exchange or market on which the security is principally traded. Events that occur on a frequent basis after foreign markets close (such as developments in foreign markets and significant movements in the U.S. markets) and prior to the determination of the fund’s net asset value may be deemed to have a material effect on the value of securities traded in foreign markets. Accordingly, the fund’s foreign equity securities may often be valued at fair value. The adviser generally relies on third-party pricing services or other information (such as the correlation with price movements of similar securities in the same or other markets; the type, cost and investment characteristics of the security; the business and financial condition of the issuer; and trading and other market data) to assist in determining whether to fair value and at what value to fair value an investment. The value of an investment for purposes of calculating the fund’s net asset value can differ depending on the source and method used to determine value. When fair valuation is used, the value of an investment used to determine the fund’s net asset value may differ from quoted or published prices for the same investment. There can be no assurance that the fund could obtain the fair value assigned to an investment if it were to sell the investment at the same time at which the fund determines its net asset value per share.

Various inputs are used in determining the value of the fund’s assets or liabilities. These inputs are categorized into three broad levels. In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, an investment’s level within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement. The fund’s assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment, and considers factors specific to the investment. Level 1 includes unadjusted quoted prices in active markets for identical assets or liabilities. Level 2 includes other significant observable market-based inputs (including quoted prices for similar securities, interest rates, prepayment speed, and credit risk). Level 3 includes unobservable inputs, which may include the adviser’s own

25

Table of Contents

Notes to Financial Statements – continued

assumptions in determining the fair value of investments. The following is a summary of the levels used as of October 31, 2011 in valuing the fund’s assets or liabilities:

| Investments at Value | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Equity Securities | $150,145,806 | $— | $— | $150,145,806 | ||||||||||||

| Mutual Funds | 174,611 | — | — | 174,611 | ||||||||||||

| Total Investments | $150,320,417 | $— | $— | $150,320,417 | ||||||||||||

For further information regarding security characteristics, see the Portfolio of Investments.

Indemnifications – Under the fund’s organizational documents, its officers and Trustees may be indemnified against certain liabilities and expenses arising out of the performance of their duties to the fund. Additionally, in the normal course of business, the fund enters into agreements with service providers that may contain indemnification clauses. The fund’s maximum exposure under these agreements is unknown as this would involve future claims that may be made against the fund that have not yet occurred.

Investment Transactions and Income – Investment transactions are recorded on the trade date. Dividends received in cash are recorded on the ex-dividend date. Certain dividends from foreign securities will be recorded when the fund is informed of the dividend if such information is obtained subsequent to the ex-dividend date. Dividend and interest payments received in additional securities are recorded on the ex-dividend or ex-interest date in an amount equal to the value of the security on such date.

The fund may receive proceeds from litigation settlements. Any proceeds received from litigation involving portfolio holdings are reflected in the Statement of Operations in realized gain/loss if the security has been disposed of by the fund or in unrealized gain/loss if the security is still held by the fund. Any other proceeds from litigation not related to portfolio holdings are reflected as other income in the Statement of Operations.

Fees Paid Indirectly – The fund’s custody fee may be reduced according to an arrangement that measures the value of cash deposited with the custodian by the fund. This amount, for the year ended October 31, 2011, is shown as a reduction of total expenses on the Statement of Operations.

Tax Matters and Distributions – The fund intends to qualify as a regulated investment company, as defined under Subchapter M of the Internal Revenue Code, and to distribute all of its taxable income, including realized capital gains. As a result, no provision for federal income tax is required. The fund’s federal tax returns for the prior three fiscal years remain subject to examination by the Internal Revenue Service.

26

Table of Contents

Notes to Financial Statements – continued

Distributions to shareholders are recorded on the ex-dividend date. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from U.S. generally accepted accounting principles. Certain capital accounts in the financial statements are periodically adjusted for permanent differences in order to reflect their tax character. These adjustments have no impact on net assets or net asset value per share. Temporary differences which arise from recognizing certain items of income, expense, gain or loss in different periods for financial statement and tax purposes will reverse at some time in the future. Distributions in excess of net investment income or net realized gains are temporary overdistributions for financial statement purposes resulting from differences in the recognition or classification of income or distributions for financial statement and tax purposes.

Book/tax differences primarily relate to wash sale loss deferrals.

The tax character of distributions declared to shareholders for the last two fiscal years is as follows:

| 10/31/11 | 10/31/10 | |||||||

| Ordinary income (including any short-term capital gains) | $1,050,009 | $400,097 | ||||||

The federal tax cost and the tax basis components of distributable earnings were as follows:

| As of 10/31/11 | ||||

| Cost of investments | $147,064,563 | |||

| Gross appreciation | 11,143,963 | |||

| Gross depreciation | (7,888,109 | ) | ||

| Net unrealized appreciation (depreciation) | $3,255,854 | |||

| Undistributed ordinary income | 1,488,755 | |||

| Capital loss carryforwards | (118,089,080 | ) | ||

As of October 31, 2011, the fund had capital loss carryforwards available to offset future realized gains. Such losses expire as follows:

| 10/31/16 | $(44,778,203 | ) | ||

| 10/31/17 | (73,310,877 | ) | ||

| Total | $(118,089,080 | ) |

Multiple Classes of Shares of Beneficial Interest – The fund offers multiple classes of shares, which differ in their respective distribution and service fees. The fund’s income, realized and unrealized gain (loss), and common expenses are allocated to shareholders based on the daily net assets of each class. Dividends are declared separately for each class. Differences in per share dividend rates are generally due to differences in separate class expenses. Class B shares will convert to Class A shares approximately eight years after

27

Table of Contents

Notes to Financial Statements – continued

purchase. The fund’s distributions declared to shareholders as reported on the Statements of Changes in Net Assets are presented by class as follows:

| From net investment income |

||||||||

| Year ended 10/31/11 |

Year ended 10/31/10 |

|||||||

| Class A | $799,464 | $299,651 | ||||||

| Class B | 16,704 | — | ||||||

| Class C | 31,156 | — | ||||||

| Class W | 141,324 | 92,049 | ||||||

| Class R1 | 179 | — | ||||||

| Class R2 | 561 | 137 | ||||||

| Class R3 | 741 | 285 | ||||||

| Class R4 | 59,880 | 7,975 | ||||||

| Total | $1,050,009 | $400,097 | ||||||

| (3) | Transactions with Affiliates |

Investment Adviser – The fund has an investment advisory agreement with MFS to provide overall investment management and related administrative services and facilities to the fund.

The management fee is computed daily and paid monthly at the following annual rates:

| First $1 billion of average daily net assets | 0.75 | % | ||

| Next $1.5 billion of average daily net assets | 0.65 | % | ||

| Next $2.5 billion of average daily net assets | 0.60 | % | ||

| Average daily net assets in excess of $5 billion | 0.50 | % |

The management fee incurred for the year ended October 31, 2011 was equivalent to an annual effective rate of 0.75% of the fund’s average daily net assets.

The investment adviser has agreed in writing to pay a portion of the fund’s total annual operating expenses, exclusive of interest, taxes, extraordinary expenses, brokerage and transaction costs, and investment-related expenses, such that total annual fund operating expenses do not exceed the following rates annually of each class’ average daily net assets.

| Class A | Class B | Class C | Class I | Class W | Class R1 | Class R2 | Class R3 | Class R4 | ||||||||||||||||||||||||

| 1.40% | 2.15% | 2.15% | 1.15% | 1.25% | 2.15% | 1.65% | 1.40% | 1.15% | ||||||||||||||||||||||||

This written agreement will continue until modified by the fund’s Board of Trustees, but such agreement will continue at least until February 28, 2013. For the year ended October 31, 2011, the fund’s actual operating expenses did not exceed the limit and therefore, the investment adviser did not pay any portion of the fund’s expenses related to this agreement.

28

Table of Contents

Notes to Financial Statements – continued

Distributor – MFS Fund Distributors, Inc. (MFD), a wholly-owned subsidiary of MFS, as distributor, received $40,480 for the year ended October 31, 2011, as its portion of the initial sales charge on sales of Class A shares of the fund.

The Board of Trustees has adopted a distribution plan for certain class shares pursuant to Rule 12b-1 of the Investment Company Act of 1940.

The fund’s distribution plan provides that the fund will pay MFD for services provided by MFD and financial intermediaries in connection with the distribution and servicing of certain share classes. One component of the plan is a distribution fee paid to MFD and another component of the plan is a service fee paid to MFD. MFD may subsequently pay all, or a portion, of the distribution and/or service fees to financial intermediaries.

Distribution Plan Fee Table:

| Distribution Fee Rate (d) |

Service Fee Rate (d) |

Total Distribution Plan (d) |

Annual Effective Rate (e) |

Distribution and Service Fee |

||||||||||||||||

| Class A | — | 0.25% | 0.25% | 0.25% | $265,262 | |||||||||||||||

| Class B | 0.75% | 0.25% | 1.00% | 1.00% | 121,294 | |||||||||||||||

| Class C | 0.75% | 0.25% | 1.00% | 1.00% | 362,348 | |||||||||||||||

| Class W | 0.10% | — | 0.10% | 0.10% | 17,925 | |||||||||||||||

| Class R1 | 0.75% | 0.25% | 1.00% | 1.00% | 933 | |||||||||||||||

| Class R2 | 0.25% | 0.25% | 0.50% | 0.50% | 494 | |||||||||||||||

| Class R3 | — | 0.25% | 0.25% | 0.25% | 242 | |||||||||||||||

| Total Distribution and Service Fees | $768,498 | |||||||||||||||||||

| (d) | In accordance with the distribution plan for certain classes, the fund pays distribution and/or service fees equal to these annual percentage rates of each class’ average daily net assets. The distribution and service fee rates disclosed by class represent the current rates in effect at the end of the reporting period. |

| (e) | The annual effective rates represent actual fees incurred under the distribution plan for the year ended October 31, 2011 based on each class’ average daily net assets. |

Certain Class A shares are subject to a contingent deferred sales charge (CDSC) in the event of a shareholder redemption within 24 months of purchase. Class C shares are subject to a CDSC in the event of a shareholder redemption within 12 months of purchase. Class B shares are subject to a CDSC in the event of a shareholder redemption within six years of purchase. All contingent deferred sales charges are paid to MFD and during the year ended October 31, 2011, were as follows:

| Amount | ||||

| Class A | $4,201 | |||

| Class B | 40,596 | |||

| Class C | 3,465 | |||

Shareholder Servicing Agent – MFS Service Center, Inc. (MFSC), a wholly-owned subsidiary of MFS, receives a fee from the fund for its services as shareholder servicing agent calculated as a percentage of the average daily net

29

Table of Contents

Notes to Financial Statements – continued

assets of the fund as determined periodically under the supervision of the fund’s Board of Trustees. For the year ended October 31, 2011, the fee was $68,203, which equated to 0.0381% annually of the fund’s average daily net assets. MFSC also receives payment from the fund for out-of-pocket expenses, sub-accounting and other shareholder servicing costs which may be paid to affiliated and unaffiliated service providers. For the year ended October 31, 2011, these out-of-pocket expenses, sub-accounting and other shareholder servicing costs amounted to $195,154.

Administrator – MFS provides certain financial, legal, shareholder communications, compliance, and other administrative services to the fund. Under an administrative services agreement, the fund partially reimburses MFS the costs incurred to provide these services. The fund is charged an annual fixed amount of $17,500 plus a fee based on average daily net assets. The administrative services fee incurred for the year ended October 31, 2011 was equivalent to an annual effective rate of 0.0198% of the fund’s average daily net assets.

Trustees’ and Officers’ Compensation – The fund pays compensation to independent Trustees in the form of a retainer, attendance fees, and additional compensation to Board and Committee chairpersons. The fund does not pay compensation directly to Trustees or officers of the fund who are also officers of the investment adviser, all of whom receive remuneration for their services to the fund from MFS. Certain officers and Trustees of the fund are officers or directors of MFS, MFD, and MFSC.

Other – This fund and certain other funds managed by MFS (the funds) have entered into services agreements (the Agreements) which provide for payment of fees by the funds to Tarantino LLC and Griffin Compliance LLC in return for the provision of services of an Independent Chief Compliance Officer (ICCO) and Assistant ICCO, respectively, for the funds. The ICCO and Assistant ICCO are officers of the funds and the sole members of Tarantino LLC and Griffin Compliance LLC, respectively. The funds can terminate the Agreements with Tarantino LLC and Griffin Compliance LLC at any time under the terms of the Agreements. For the year ended October 31, 2011, the aggregate fees paid by the fund to Tarantino LLC and Griffin Compliance LLC were $1,615 and are included in miscellaneous expense on the Statement of Operations. MFS has agreed to reimburse the fund for a portion of the payments made by the fund in the amount of $777, which is shown as a reduction of total expenses in the Statement of Operations. Additionally, MFS has agreed to bear all expenses associated with office space, other administrative support, and supplies provided to the ICCO and Assistant ICCO.

The fund invests in the MFS Institutional Money Market Portfolio which is managed by MFS and seeks a high level of current income consistent with

30

Table of Contents

Notes to Financial Statements – continued

preservation of capital and liquidity. Income earned on this investment is included in dividends from underlying affiliated funds on the Statement of Operations. This money market fund does not pay a management fee to MFS.

| (4) | Portfolio Securities |

Purchases and sales of investments, other than U.S. Government securities, purchased option transactions, and short-term obligations, aggregated $270,904,759 and $279,050,032, respectively.

| (5) | Shares of Beneficial Interest |

The fund’s Declaration of Trust permits the Trustees to issue an unlimited number of full and fractional shares of beneficial interest. Transactions in fund shares were as follows:

| Year ended 10/31/11 |

Year ended 10/31/10 |

|||||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||||

| Shares sold | ||||||||||||||||

| Class A |

2,464,718 | $41,847,783 | 707,085 | $9,893,030 | ||||||||||||

| Class B |

110,139 | 1,847,652 | 93,758 | 1,293,145 | ||||||||||||

| Class C |

439,963 | 7,362,604 | 149,364 | 2,066,429 | ||||||||||||

| Class I (i) |

481,667 | 8,015,820 | — | — | ||||||||||||

| Class W |

1,096,469 | 19,455,681 | 358,713 | 5,227,493 | ||||||||||||

| Class R1 |

224 | 3,656 | — | — | ||||||||||||

| Class R2 |

583 | 9,655 | — | — | ||||||||||||

| Class R3 |

683 | 12,444 | — | — | ||||||||||||

| Class R4 |

91,957 | 1,574,093 | 258,418 | 3,844,717 | ||||||||||||

| 4,686,403 | $80,129,388 | 1,567,338 | $22,324,814 | |||||||||||||

| Shares issued to shareholders in reinvestment of distributions | ||||||||||||||||

| Class A |

39,046 | $ 657,545 | 20,054 | $ 266,724 | ||||||||||||

| Class B |

781 | 12,799 | — | — | ||||||||||||

| Class C |

1,339 | 21,968 | — | — | ||||||||||||

| Class W |

3,058 | 51,525 | 496 | 6,602 | ||||||||||||

| Class R1 |

11 | 179 | — | — | ||||||||||||

| Class R2 |

34 | 561 | 11 | 137 | ||||||||||||

| Class R3 |

44 | 741 | 21 | 285 | ||||||||||||

| Class R4 |

3,552 | 59,880 | 599 | 7,975 | ||||||||||||

| 47,865 | $805,198 | 21,181 | $281,723 | |||||||||||||

31

Table of Contents

Notes to Financial Statements – continued

| Year ended 10/31/11 |

Year ended 10/31/10 |

|||||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||||

| Shares reacquired | ||||||||||||||||

| Class A |

(2,644,252 | ) | $ (44,574,000 | ) | (5,963,882 | ) | $ (82,395,036 | ) | ||||||||

| Class B |

(227,468 | ) | (3,744,297 | ) | (310,027 | ) | (4,194,463 | ) | ||||||||

| Class C |

(662,405 | ) | (10,857,614 | ) | (1,708,978 | ) | (22,864,423 | ) | ||||||||

| Class I (i) |

(36,712 | ) | (611,547 | ) | — | — | ||||||||||

| Class W |

(1,597,587 | ) | (26,412,005 | ) | (777,231 | ) | (10,856,035 | ) | ||||||||

| Class R1 |

(1 | ) | (22 | ) | — | — | ||||||||||

| Class R2 |

(5 | ) | (83 | ) | — | — | ||||||||||

| Class R4 |

(101,606 | ) | (1,700,936 | ) | (54,074 | ) | (745,775 | ) | ||||||||

| (5,270,036 | ) | $(87,900,504 | ) | (8,814,192 | ) | $(121,055,732 | ) | |||||||||

| Net change | ||||||||||||||||

| Class A |

(140,488 | ) | $ (2,068,672 | ) | (5,236,743 | ) | $ (72,235,282 | ) | ||||||||

| Class B |

(116,548 | ) | (1,883,846 | ) | (216,269 | ) | (2,901,318 | ) | ||||||||

| Class C |

(221,103 | ) | (3,473,042 | ) | (1,559,614 | ) | (20,797,994 | ) | ||||||||

| Class I (i) |

444,955 | 7,404,273 | — | — | ||||||||||||

| Class W |

(498,060 | ) | (6,904,799 | ) | (418,022 | ) | (5,621,940 | ) | ||||||||

| Class R1 |

234 | 3,813 | — | — | ||||||||||||

| Class R2 |

612 | 10,133 | 11 | 137 | ||||||||||||

| Class R3 |

727 | 13,185 | 21 | 285 | ||||||||||||

| Class R4 |

(6,097 | ) | (66,963 | ) | 204,943 | 3,106,917 | ||||||||||

| (535,768 | ) | $(6,965,918 | ) | (7,225,673 | ) | $(98,449,195 | ) | |||||||||

| (i) | For the period from the Class I inception, February 28, 2011, through the stated period end. |

| (6) | Line of Credit |

The fund and certain other funds managed by MFS participate in a $1.1 billion unsecured committed line of credit, subject to a $1 billion sublimit, provided by a syndication of banks under a credit agreement. Borrowings may be made for temporary financing needs. Interest is charged to each fund, based on its borrowings, generally at a rate equal to the higher of the Federal Reserve funds rate or one month LIBOR plus an agreed upon spread. A commitment fee, based on the average daily, unused portion of the committed line of credit, is allocated among the participating funds at the end of each calendar quarter. In addition, the fund and other funds managed by MFS have established unsecured uncommitted borrowing arrangements with certain banks for temporary financing needs. Interest is charged to each fund, based on its borrowings, at a rate equal to the Federal Reserve funds rate plus an agreed upon spread. For the year ended October 31, 2011, the fund’s commitment fee and interest expense were $1,478 and $0, respectively, and are included in miscellaneous expense on the Statement of Operations.

32

Table of Contents

Notes to Financial Statements – continued

| (7) | Transactions in Underlying Affiliated Funds-Affiliated Issuers |

An affiliated issuer may be considered one in which the fund owns 5% or more of the outstanding voting securities, or a company which is under common control. For the purposes of this report, the fund assumes the following to be affiliated issuers:

| Underlying Affiliated Funds | Beginning Shares/Par Amount |

Acquisitions Shares/Par Amount |

Dispositions Shares/Par Amount |

Ending Shares/Par Amount |

||||||||||||

| MFS Institutional Money Market Portfolio |

548,426 | 50,901,261 | (51,275,076 | ) | 174,611 | |||||||||||

| Underlying Affiliated Funds | Realized Gain (Loss) |

Capital Gain Distributions |

Dividend Income |

Ending Value |

||||||||||||

| MFS Institutional Money Market Portfolio |

$— | $— | $2,931 | $174,611 | ||||||||||||

33

Table of Contents

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Trustees of MFS Series Trust XII and Shareholders of MFS Equity Opportunities Fund:

We have audited the accompanying statement of assets and liabilities of MFS Equity Opportunities Fund (formerly MFS Sector Rotational Fund, one of the portfolios comprising the MFS Series Trust XII), (the “Fund”), including the portfolio of investments, as of October 31, 2011, the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended and the financial highlights for each of the periods indicated therein. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of October 31, 2011, by correspondence with the Fund’s custodian and brokers or by other appropriate auditing procedures where replies from brokers were not received. We believe that our audits provide a reasonable basis for our opinion.