Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2005

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report: N/A

Commission file number: 000-51380

Silicon Motion Technology Corporation

(Exact name of Registrant as specified in its charter)

Cayman Islands

(Jurisdiction of incorporation or organization)

No. 20-1, Taiyuan St.,

Jhubei City Hsinchu County 302

Taiwan

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| None | N/A |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

Ordinary shares, par value US$0.01 per share

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 122,612,000 ordinary shares, US$0.01 par value per share.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filed. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ |

Accelerated filer ¨ | Non-accelerated filer þ |

Indicate by check mark which financial statement item the registrant has elected to follow. ¨ Item 17 þ Item 18

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act): Yes ¨ No þ

Table of Contents

i

Table of Contents

CONVENTIONS THAT APPLY TO THIS ANNUAL REPORT

Unless otherwise indicated, references in this annual report to:

| • | “ADRs” are to the American depositary receipts that evidence our ADSs; |

| • | “ADSs” are to our American depositary shares, each of which represents four ordinary shares; |

| • | “CAGR” are to compound annual growth rate; |

| • | “China” or “PRC” are to the People’s Republic of China excluding the special administrative regions of Hong Kong and Macau; |

| • | “Nasdaq” are to the Nasdaq National Market; |

| • | “NT dollar,” “NT dollars” or “NT$” are to New Taiwan dollars, the legal currency of Taiwan; |

| • | “ROC” or “Taiwan” are to Taiwan, the Republic of China, the official name of Taiwan; |

| • | “shares” or “ordinary shares” are to our ordinary shares, with par value US$0.01 per share; |

| • | “U.S. GAAP” are to generally accepted accounting principles in the United States; |

| • | “U.S. dollar,” “U.S. dollars” or “US$” are to United States dollars, the legal currency of the United States; and |

| • | “we,” “us,” “our company,” “our” and “Silicon Motion” are to Silicon Motion Technology Corporation, its predecessor entities and subsidiaries including (i) Silicon Motion, Inc., incorporated in Taiwan, or SMI Taiwan, and formerly known as Feiya Technology Corporation and (ii) Silicon Motion, Inc., a California, USA, corporation, or SMI USA. |

Unless otherwise indicated, our financial information presented in this annual report has been prepared in accordance with U.S. GAAP.

Solely for your convenience, this annual report contains translations of certain NT dollar amounts into U.S. dollars at specified rates. All translations from NT dollar to U.S. dollar amounts are made at the noon buying rate in the City of New York for cable transfers of NT dollars as certified for customs purposes by the Federal Reserve Bank of New York. Unless otherwise stated, the translation from NT dollars into U.S. dollars and from U.S. dollars into NT dollars has been made at the noon buying rate in effect on December 31, 2005, which was NT$32.80 to US$1.00. No representation is made that the NT dollar or U.S. dollar amounts referred to in this annual report could have been or could be converted into U.S. dollar or NT dollar amounts, as the case may be, at any particular rate or at all. See “Risk Factors — If economic conditions in Taiwan deteriorate, our current business and future growth would be adversely affected” for discussions on how fluctuating exchange rates could affect our profitability and your investment in us. On June 27, 2006, the noon buying rate was NT$32.65 to US$1.00.

The “Glossary of Technical Terms” contained in Annex A of this report sets forth the description of certain technical terms and definitions used in this annual report.

This annual report also contains statistical data and forecasted information that we obtained from industry publications and reports generated by Gartner Dataquest, or Gartner, (Forecast: Electronic Equipment Production and Semiconductors by Application, Worldwide, 2002-2010, Gartner Dataquest, May 2006), and International Data Corporation, or IDC (Worldwide and U.S. Portable Compressed Audio Player 2006-2010 Forecast and Analysis: Portable Music and More, IDC, April 2006; Worldwide Smart Handheld Device 2005-2009 Forecast and Analysis: Passing the Torch, IDC, May 2005; Worldwide NAND Flash Demand and Supply 2006-2010 Forecast and Analysis: With 4Q05- 4Q06 Short - Term Forecast, IDC , April 2006; Worldwide Flash Memory Card 2006-2010 Forecast, IDC, May 2006; and Worldwide PC Camera 2006-2010 Forecast and 2005 Vendor Shares, IDC, March 2006). These industry publications generally indicate that they have obtained their information from sources believed to be reliable, but do not guarantee the accuracy and completeness of their information. Although we believe that the publications are reliable, we have not independently verified their data.

ii

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements. These statements relate to future events or our future financial performance, our ability to continue to control our costs and maintain the quality of our products, the expected growth of and change in the semiconductor and multimedia consumer electronics industries worldwide, and involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to differ materially from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. These risks and other factors include those listed under “Risk Factors” and elsewhere in this annual report. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “intend,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” “continue” or the negative of these terms or other comparable terminology. A variety of factors, some of which are outside of our control, may cause our operating results to fluctuate significantly. They include:

| • | unpredictable volume and timing of customer orders, which are not fixed by contract but vary on a purchase order basis; |

| • | the loss of one or more key customers or the significant reduction, postponement, rescheduling or cancellation of orders from these customers; |

| • | general economic conditions or conditions in the semiconductor or multimedia consumer electronics market; |

| • | decreases in the overall average selling prices of our products; |

| • | changes in the relative sales mix of our products; |

| • | changes in our cost of finished goods; |

| • | the availability, pricing and timeliness of delivery of other components and raw materials used in our customers’ products; |

| • | our customers’ sales outlook, purchasing patterns and inventory adjustments based on consumer demands and general economic conditions; |

| • | our ability to successfully develop, introduce and sell new or enhanced products in a timely manner; and |

| • | the timing of new product announcements or introductions by us or by our competitors. |

One or more of these factors could materially and adversely affect our operating results and financial condition in future periods. We cannot assure you that we will attain any estimates or maintain profitability or that the assumptions on which they are based are reliable.

Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise after the date of this annual report. All forward-looking statements contained in this annual report are qualified by reference to this cautionary statement.

iii

Table of Contents

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| ITEM 3. | KEY INFORMATION |

Selected Consolidated Financial Data

You should read the following information with our consolidated financial statements and related notes and “Item 5. Operating and Financial Review and Prospects” included elsewhere in this annual report.

The summary consolidated statements of income and cash flow data for the years ended December 31, 2002, 2003, 2004 and 2005 and the summary consolidated balance sheet data as of December 31, 2003, 2004 and 2005 are derived from our consolidated financial statements included elsewhere in this annual report and should be read in conjunction with, and are qualified in their entirety by reference to, these consolidated financial statements and related notes. These consolidated financial statements are prepared in accordance with U.S. GAAP.

We have omitted the selected consolidated financial data as of and for the year ended December 31, 2001. None of our current senior financial managers and accountants was a member of our financial staff in 2001, and as a result, our current senior financial managers and accountants are unfamiliar with the transactions and activities of the company in these periods. In addition, we implemented a new system of internal control, financial management and accounting record keeping in the second quarter of 2001 and this system does not contain the necessary information, data and records for part of 2001. Therefore, we are unable to prepare selected consolidated financial data as of and for the years ended December 31, 2001 without significant additional effort and expense.

1

Table of Contents

| Year Ended December 31, | ||||||||||||

| 2002 | 2003 | 2004 | 2005 | 2005 | ||||||||

| NT$ | NT$ | NT$ | NT$ | US$ | ||||||||

| (in thousands, except for per share data) | ||||||||||||

| Consolidated Statements of Income Data: |

||||||||||||

| Net sales |

456,874 | 915,070 | 2,166,727 | 2,686,492 | 81,906 | |||||||

| Cost of sales |

366,236 | 424,668 | 1,274,410 | 1,342,749 | 40,937 | |||||||

| Gross profit |

90,638 | 490,402 | 892,317 | 1,343,743 | 40,969 | |||||||

| Operating expenses: |

||||||||||||

| Research and development |

107,504 | 203,646 | 238,485 | 373,548 | 11,389 | |||||||

| Sales and marketing |

52,593 | 125,680 | 141,136 | 157,278 | 4,795 | |||||||

| General and administrative |

38,230 | 69,262 | 103,303 | 129,141 | 3,937 | |||||||

| Amortization of intangible assets |

8,048 | 24,145 | 17,758 | 4,501 | 137 | |||||||

| Impairment of intangible assets (1) |

— | 54,143 | 11,718 | — | — | |||||||

| In-process research and development |

310,813 | — | — | — | — | |||||||

| Restructuring charge |

10,170 | — | — | — | — | |||||||

| Total operating expenses |

527,358 | 476,876 | 512,400 | 664,468 | 20,258 | |||||||

| Operating income (loss) |

(436,720 | ) | 13,526 | 379,917 | 679,275 | 20,711 | ||||||

| Total non-operating income (expenses) |

10,477 | 2,512 | 21,187 | 36,082 | 1,099 | |||||||

| Income (loss) before income taxes |

(426,243 | ) | 16,038 | 401,104 | 715,357 | 21,810 | ||||||

| Income tax (benefit) expense |

9,573 | (94,405 | ) | 133,101 | 42,055 | 1,282 | ||||||

| Net income (loss) |

(435,816 | ) | 110,443 | 268,003 | 673,302 | 20,528 | ||||||

| Weighted average shares outstanding: |

||||||||||||

| Basic |

66,752 | 96,901 | 103,878 | 114,083 | 114,083 | |||||||

| Diluted |

66,752 | 96,901 | 103,878 | 116,015 | 116,015 | |||||||

| Earning (loss) per share: |

||||||||||||

| Basic |

(6.53 | ) | 1.14 | 2.58 | 5.90 | 0.18 | ||||||

| Diluted |

(6.53 | ) | 1.14 | 2.58 | 5.80 | 0.18 | ||||||

| Earning (loss) per ADS(2): |

||||||||||||

| Basic earnings per ADS |

(26.12 | ) | 4.56 | 10.32 | 23.61 | 0.72 | ||||||

| Diluted earnings per ADS |

(26.12 | ) | 4.56 | 10.32 | 23.21 | 0.71 | ||||||

| (1) | In 2003 and 2004 we determined that impairment of our intangible assets occurred as a result of a significant decline in expected net sales from new consumer products such as broadband Internet video phones, car navigation systems, and Tablet PCs. As the development and market for these products did not materialize, the forecasted sales and cash flows were significantly reduced. |

| (2) | Each ADS represents four ordinary shares. |

2

Table of Contents

| As of December 31, | ||||||||

| 2003 | 2004 | 2005 | 2005 | |||||

| NT$ | NT$ | NT$ | US$ | |||||

| (in thousands) | ||||||||

| Consolidated Balance Sheet Data: |

||||||||

| Cash and cash equivalents |

763,545 | 727,165 | 1,581,993 | 48,231 | ||||

| Other current assets |

459,634 | 1,324,343 | 2,341,402 | 71,386 | ||||

| Working capital |

976,767 | 1,339,418 | 3,292,041 | 100,368 | ||||

| Long-term investments |

7,195 | 3,142 | 15,954 | 486 | ||||

| Property and equipment, net |

52,610 | 65,657 | 83,734 | 2,553 | ||||

| Intangible assets, net |

38,080 | 6,843 | — | — | ||||

| Other assets |

41,281 | 39,887 | 65,048 | 1,983 | ||||

| Total assets |

1,362,345 | 2,167,037 | 4,088,131 | 124,639 | ||||

| Total liabilities |

253,754 | 718,804 | 638,346 | 19,462 | ||||

| Total shareholders’ equity |

1,108,591 | 1,448,233 | 3,449,785 | 105,177 | ||||

| Year Ended December 31, | |||||||||||||||

| 2002 | 2003 | 2004 | 2005 | 2005 | |||||||||||

| NT$ | NT$ | NT$ | NT$ | US$ | |||||||||||

| (in thousands) | |||||||||||||||

| Consolidated Cash Flow Data: |

|||||||||||||||

| Net cash provided by (used in) operating activities |

(53,973 | ) | 128,322 | 234,703 | 539,008 | 16,433 | |||||||||

| Net cash provided by (used in) investing activities |

(31,492 | ) | 9,706 | (263,101 | ) | (1,011,935 | ) | (30,852 | ) | ||||||

| Net cash provided by (used in) financing activities |

12,353 | 268,562 | (3,081 | ) | 1,278,868 | 38,990 | |||||||||

| Depreciation and amortization |

19,541 | 28,210 | 21,734 | 23,906 | 729 | ||||||||||

| Capital expenditures |

(3,018 | ) | (13,996 | ) | (36,409 | ) | (42,708 | ) | (1,302 | ) | |||||

Exchange Rate Information

We conduct our business primarily in Taiwan and our revenues and expenses are primarily denominated in NT dollars. This annual report contains translations of NT dollar amounts into U.S. dollar amounts at specific rates solely for the convenience of the reader. The translations of NT dollar amounts into U.S. dollar amounts in this annual report are based on the noon buying rate in the City of New York for cable transfers of the NT dollar as certified for customs purposes by the Federal Reserve Bank of New York. Unless otherwise noted, all translations from NT dollar amounts to U.S. dollar amounts and from U.S. dollar amounts to NT dollar amounts in this annual report were made at a rate of NT$32.80 to US$1.00, the noon buying rate in effect as of December 31, 2005. The noon buying rate as of May 31, 2006 was NT$31.99 to US$1.00. We make no representation that any NT dollar or U.S. dollar amounts could have been, or could be, converted into U.S. dollar or NT dollar amounts, as the case may be, at any particular rate, the rates stated below, or at all.

The following table sets forth information concerning exchange rates between NT dollars and U.S. dollars for the periods indicated. These rates are provided solely for your convenience and are not necessarily the exchange rates that we used in this annual report or will use in the preparation of our periodic reports or any other information to be provided to you. The source of these rates is the Federal Reserve Bank of New York.

| Noon Buying Rate | ||||

| NT$ per US$ | ||||

| High | Low | |||

| December 2005 |

33.56 | 32.80 | ||

| January 2006 |

32.59 | 31.83 | ||

| February 2006 |

32.65 | 31.97 | ||

| March 2006 |

32.62 | 32.28 | ||

| April 2006 |

32.54 | 31.90 | ||

| May 2006 |

32.13 | 31.28 | ||

3

Table of Contents

The following table sets forth the average noon buying rates between NT dollars and U.S. dollars for each of the periods indicated, calculated by averaging the noon buying rates on the last day of each month of the periods shown.

| Average Noon Buying Rate | ||

| NT$ Per US$ | ||

| 2001 |

33.91 | |

| 2002 |

34.53 | |

| 2003 |

34.40 | |

| 2004 |

33.27 | |

| 2005 |

32.16 |

Risk Factors

Risks Related to Our Business

We have sustained losses in the past and cannot guarantee profitability in the future.

Although we have been profitable since the second quarter of 2003, we cannot assure you that we will remain profitable in the future. A variety of factors may cause our operating results to decline and financial condition to worsen, including:

| • | competitors offering comparable products at cheaper prices; |

| • | continuing downward pressure on the average selling prices of our products caused by intense competition in our industry and other reasons; |

| • | decreases in demand for multimedia consumer electronics products into which our semiconductor solutions are incorporated; |

| • | superior product innovations by our competitors; |

| • | rising costs for raw materials; |

| • | changes in our management team and other key personnel; and |

| • | increased operating expenses relating to research and development, sales and marketing efforts and general and administrative expenses as we seek to grow our business. |

As a result of these and other factors, we could fail to achieve our revenue targets or experience higher than expected operating expenses, or both. As a result, we cannot assure you that we will remain profitable in the future.

The loss of a significant customer or a reduction in orders from such a customer could adversely affect our operating results.

We are dependent on a small group of customers for a substantial portion of our sales. Power Digital Card, or PDC, was our largest customer in 2003 and 2004, accounting for approximately 29% and 22% of our net sales in 2003 and 2004, respectively. However, in 2005, PDC became our sixth largest customer and accounted for only 6% of our net sales. Macrotron Systems, our eighth and third largest customers in 2003 and 2004 respectively, accounted for 3% and 13% of our net sales in 2003 and 2004 respectively. In 2005, Macrotron Systems became our eighth largest customer, accounting for only 5% of our net sales. We started direct sales to Lexar Media in 2004, which became our second and fourth largest customer in 2004 and 2005, respectively, and accounted for 14% and 7% of our net sales in 2004 and 2005, respectively. We believe that a substantial portion of our sales to PDC and Macrotron Systems are included in Lexar Media’s products and that such indirect sales

4

Table of Contents

and our direct sales to Lexar Media amounted to between 30% to 35% of our net sales in 2004 and between 20% and 26% of our net sales in 2005. In 2003, 2004 and 2005, our three largest direct customers accounted for approximately 48%, 49% and 26% respectively, of our net sales. We expect that we will continue to depend on a relatively limited number of customers for a substantial portion of our net sales and our ability to maintain good relationships with these customers will be important to the ongoing success of our business. We cannot assure you that the revenue generated from these customers, individually or in the aggregate, will reach or exceed historical levels in any future period. Our failure to meet the demands of these customers could lead to a cancellation or reduction of business from these customers. In addition, loss, cancellation or reduction of business from, significant changes in scheduled deliveries to, or decreases in the prices of products sold to, any of these customers could significantly reduce our revenues and adversely affect our financial condition and operating results. Moreover, any difficulty in collecting outstanding amounts due from our customers particularly customers who place large orders, would harm our financial performance. In addition, if our relationships with our three largest customers are disrupted for any reason, it could have a significant impact on our business.

Our limited operating history may not serve as an adequate basis to judge our future prospects and operating results.

We have a limited operating history with respect to our current business, which may not provide a meaningful basis on which to evaluate our business or future prospects. Although our sales have grown rapidly in recent years, we incurred net losses prior to the second quarter of 2003. We cannot assure you that we will maintain our profitability or that we will not incur net losses in the future. We expect that our operating expenses will increase as we expand. Any significant failure to realize anticipated sales growth could result in significant operating losses. We will continue to encounter risks and difficulties frequently experienced by companies at a similar stage of development, including our potential failure to:

| • | implement our business model and strategy and adapt and modify them as needed; |

| • | maintain our current, and develop new relationships with customers; |

| • | manage our expanding operations and product offerings, including the integration of any future acquisitions; |

| • | maintain adequate control of our expenses; |

| • | attract, retain and motivate qualified personnel; |

| • | protect our reputation and enhance customer loyalty; and |

| • | anticipate and adapt to changing conditions in the semiconductor industry and other markets in which we operate as well as the impact of any changes in government regulation, mergers and acquisitions involving our competitors, technological developments and other significant competitive and market dynamics. |

If we are not successful in addressing any or all of these risks, our business may be materially and adversely affected.

We expect our operating results to fluctuate from quarter to quarter, which may make it difficult to predict our future performance and could cause the market price of our ADSs to fluctuate.

Our quarterly sales and operating results are difficult to predict and have in the past, and will likely in the future, fluctuate from quarter to quarter.

Since our products are primarily used in multimedia consumer electronics products, our business is subject to seasonality, with a tendency toward increased sales in the third and fourth quarters of each year, when our customers place orders in anticipation of year-end demand for consumer electronics products, and lower sales in

5

Table of Contents

the first and second quarters of each year. Moreover, we are also subject to the highly cyclical nature of the semiconductor industry.

Our quarterly operating results could be affected by a number of other factors, including:

| • | unpredictable volume and timing of customer orders, which are not fixed by contract but vary on a purchase order basis; |

| • | the loss of one or more key customers or the significant reduction, postponement, rescheduling or cancellation of orders from these customers; |

| • | decreases in the overall average selling prices of our products; |

| • | changes in the relative sales mix of our products; |

| • | changes in our cost of finished goods; |

| • | the availability, pricing and timeliness of delivery of other components and raw materials used in our customers’ products; |

| • | our customers’ sales outlook, purchasing patterns and inventory adjustments based on consumer demands and general economic conditions; |

| • | our ability to successfully develop, introduce and sell new or enhanced products in a timely manner; and |

| • | the timing of new product announcements or introductions by us or by our competitors. |

These factors, as well as our recent rapid growth, make it difficult for us to assess our future performance. Any variations in our quarter-to-quarter performance may cause the market price of our ADSs to fluctuate. In addition, as a result of these fluctuations, our operating results in the future may be below the expectations of public market analysts or investors, which would likely cause the market price of our ADSs to decline. Accordingly, you should not rely on the results of any prior periods as a reliable indicator of our future operating performance.

We may not be able to sustain our current growth rates, and even if we do maintain them, we are susceptible to many challenges relating to our growth.

We have experienced significant growth in the scope and complexity of our business. Our net sales grew from approximately NT$456.9 million in 2002 to approximately NT$915.1 million in 2003 to approximately NT$2,166.7 million in 2004 and to approximately NT$2,686.5 million (US$81.9 million) in 2005. This growth has placed and will continue to place a strain on our management, personnel, systems and resources. If we are unable to manage our growth effectively, we may not be able to take advantage of market opportunities, develop new products, enhance our technological capabilities, satisfy customer requirements, execute on our business plan or respond to competitive pressures. In particular, the success of our goal to penetrate the MP3 market is highly contingent on the viability of our strategy and the success of our growth plans. To successfully manage our growth, we believe we must effectively:

| • | hire, train, integrate and manage additional qualified engineers, sales and marketing personnel and financial and information technology personnel; |

| • | implement additional and improve existing administrative, financial and operations systems, procedures and controls; |

| • | continue to enhance our manufacturing and customer resource management systems; |

| • | continue to expand and upgrade our core semiconductor design and software development capabilities; |

| • | manage multiple relationships with foundries, distributors, suppliers and certain other third parties; and |

| • | manage our financial condition. |

6

Table of Contents

Our success also depends largely on our ability to anticipate and respond to expected changes in future demand for our products. In the event the timing of our expansion does not match market demand, our business strategy may need to be revised, and there could be delays in our roll-out of new products, which may adversely affect our growth and future prospects. If we over-expand and demand for our products does not increase as we may have projected, our financial results will be materially and adversely affected. However, if we do not expand, and demand for our products increases sharply, our business could be seriously harmed because we may not be as cost-effective as our competitors due to our inability to take advantage of increased economies of scale. In addition, we may not be able to satisfy the needs of our current customers or attract new customers, and we may lose credibility and our relationships with our customers may be negatively affected. Moreover, if we do not properly allocate our resources in line with future demand for particular products, we may miss changing market opportunities and our business and financial results could be materially and adversely affected. We cannot assure you that we will be able to successfully sustain our current growth rate or that we will be able to manage our growth in the future.

Industry standards and demands in the multimedia consumer electronics market are continuously and rapidly evolving, and our success depends on our ability to anticipate and meet these changes and trends.

In order to remain competitive in the future, we must ensure that our products meet continuously evolving industry standards and are compatible with rapidly changing customer requirements. If our products do not keep pace with evolving industry standards or if our products are not in compliance with prevailing industry standards for an extended period of time, we could be required to invest significant time, effort and funds to redesign our products to ensure compatibility with relevant standards. If we are slow to anticipate changing trends and respond to such charges in a timely manner, we could miss opportunities to capture potential customers and we could lose our existing market share or existing customers. Currently, our primary products are controllers used in flash memory devices. If new models for storing digital media are developed that compete with flash memory technology or render it obsolete and if we are not able to shift our product offerings accordingly, demand for our products would likely decline and our business would be materially and adversely affected.

In addition, we may not have sufficient financial resources to fund all of the required research to develop future innovations and meet changing industry standards. Moreover, even if we have adequate financial resources, our future innovations may be outpaced by competing innovations. As a result, we may lose customers and significant sales, and our business and operating results may be materially and adversely affected.

If demand for our products declines in the major end markets that we serve, our selling prices and our overall sales will decrease.

Demand for our products is affected by a number of factors, including the general demand for the products in the end markets that we serve and price attractiveness. A vast majority of our sales revenue is derived from customers who use our semiconductor solutions in portable digital media devices, such as MP3 players, smart phones, digital cameras and PDAs. Any significant decrease in the demand for portable digital media devices may decrease the demand for our semiconductor solutions and may result in a decrease in our revenues and earnings. A variety of factors, including economic, political and social instability, could contribute to a slowdown in the demand for non-essential consumer electronics products as consumers delay purchasing decisions or reduce their discretionary spending. In addition, the historical and continuing trend of declining average selling prices of portable digital media devices places pricing pressure on our semiconductor solutions. As a result, we expect that the average selling prices for many of our semiconductor solutions will continue to decline over the long term. If we are not able to introduce higher margin products, reduce our manufacturing costs to offset expected declines in average selling prices or maintain a high capacity utilization rate, our gross margin will continue to decline, which could have a material and adverse effect on our financial condition and operating results.

7

Table of Contents

The highly cyclical nature of the semiconductor industry has produced significant and sometimes prolonged downturns; future downturns could materially affect our operating results.

The semiconductor industry is highly cyclical. The industry has experienced significant downturns, often in connection with, or in anticipation of, maturing product cycles of both semiconductor companies’ and their customers’ products and declines in general economic conditions. These downturns have been characterized by production overcapacity, high inventory levels and accelerated erosion of average selling prices. For example, the semiconductor industry experienced a downturn beginning in the fourth quarter of 2000 until late 2002. Although the semiconductor industry has been in the process of recovery from the downturn since late 2002, any future downturns could significantly reduce our sales or our profitability for a prolonged period. From time to time, the semiconductor industry also has experienced periods of increased demand and production capacity constraints. As a result, we may experience substantial changes in future operating results due to general semiconductor industry conditions, general economic conditions and other factors.

If the semiconductor industry suffers a shortage of flash memory, which is a key component in many of our customers’ end products, our revenues could be adversely affected.

In 2004 and 2005, some of our customers indicated that they were unable to acquire enough flash memory to meet all of the anticipated demand for their products. Several manufacturers of flash memory have increased manufacturing capacity for flash memory since then. However, we cannot assure you that there will continue to be enough additional capacity to satisfy worldwide demand for flash memory. According to IDC, the demand for flash memory cards is expected to rise rapidly through 2008. Because flash memory is a key component of most of the products manufactured by our customers, if any shortage in the supply of flash memory occurs and is not remedied, our customers may not be able to purchase enough flash memory to manufacture their products and may therefore purchase fewer semiconductor solutions from us than they would have otherwise purchased. Our ability to increase revenues and grow our profits could be materially and adversely affected as a result of any shortage or decrease in the supply of flash memory.

A failure to accurately forecast customer demand may result in excess or insufficient inventory, which may increase our operating costs and harm our business.

To ensure the availability of our products for our customers, in some cases we cause our manufacturers to begin manufacturing our products based on forecasts provided by these customers in advance of receiving purchase orders. However, these forecasts do not represent binding purchase commitments, and we do not recognize revenue from these products until they are shipped to the customer. As a result, we incur inventory and manufacturing costs in advance of anticipated revenue. Because demand for our products may not materialize, manufacturing based on forecasts subjects us to risks of high inventory carrying costs and increased obsolescence and may increase our costs. If we overestimate customer demand for our products or if purchase orders are cancelled or shipments delayed, we may end up with excess inventory that we cannot sell, which could have a material and adverse effect on our financial results. Conversely, if we underestimate demand, we may not have sufficient product inventory and may lose market share and damage customer relationships, which could also harm our business.

The average selling prices of our products could decrease rapidly.

We may experience period-to-period fluctuations in future operating results if our average selling prices decline. We may be forced to reduce the average unit price of our products in response to new product introductions by us or our competitors, competitive pricing pressures and other factors. The semiconductor market is extremely cost sensitive, which may result in declining average selling prices of the components comprising our products. We expect that these factors will create downward pressure on our average selling prices and operating results. To maintain acceptable operating results, we will need to develop and introduce new products and product enhancements on a timely basis and continue to reduce our costs. If we are unable to offset

8

Table of Contents

any reductions in our average selling prices by increasing our sales volumes or reducing corresponding production costs, or if we fail to develop and introduce new products and enhancements on a timely basis, our sales and operating results will be materially and adversely affected.

We rely primarily on a small number of distributors to market and distribute certain of our products, and if we fail to maintain or expand these sales channels, our revenues would likely decline.

Most of our display controllers are sold through independent distributors. Sales of these products to distributors generate a significant amount of our revenues. Our business will depend on our ability to maintain and expand our relationships with distributors, develop additional channels for the distribution and sale of our products and effectively manage these relationships. Because not all of our distributors are required to make a specified minimum level of purchases from us, we cannot be certain that they will sell our products on a priority basis. As we continue to expand our indirect sales capabilities, we will need to manage the potential conflicts that may arise within our indirect sales force. We also rely on our distributors to accurately and timely report to us their sales of our products and to provide certain engineering support services to customers. Our inability to obtain accurate and timely reports and to successfully manage these relationships would have a material and adverse effect on our financial results.

The loss of any of our key personnel or the failure to attract or retain specialized technical and management personnel could impair our ability to grow our business.

We rely heavily on the services of our key employees, including Wallace C. Kou, our President and Chief Executive Officer. In addition, our engineers and other key technical personnel are a significant asset and are the source of our technological and product innovations. We believe our future success will depend upon our ability to retain these key employees and our ability to attract and retain other skilled managerial, engineering, technical and sales and marketing personnel. The competition for such personnel, particularly technical personnel, is intense in our industry. We may not be successful in attracting and retaining sufficient numbers of technical personnel to support our anticipated growth. These technical personnel are required to refine the existing hardware system and application programming interface and to introduce enhancements in future applications. Despite the incentives we provide, our current employees may not continue to work for us, and if additional personnel were required for our operations, we may not be able to obtain the services of additional personnel necessary for our growth. In addition, we do not maintain “key person” life insurance for any of our senior management or other key employees. The loss of any of our key employees or our inability to attract or retain qualified personnel, including engineers, could delay the development and introduction of, and have an adverse effect on our ability to sell, our products as well as our overall growth.

In addition, if any other members of our senior management or any of our other key personnel joins a competitor or forms a competing company, we may not be able to replace them easily and we may lose customers, business partners, key professionals and staff members. Substantially all of our senior executives and key personnel have entered into confidentiality and non-disclosure agreements. In the event of a dispute between any of our senior executives or key personnel and SMI, we cannot assure you the extent, if any, to which these provisions may be enforceable in Taiwan due to uncertainties involving the Taiwan legal system.

We may be unsuccessful in developing and selling new products or in penetrating new markets required to maintain or expand our business.

Our revenue growth has been primarily from sales of our semiconductor solutions. Our future success depends, in part, on our ability to develop successful new semiconductor solutions in a cost-effective and timely manner. We continually evaluate expenditures for planned product developments and choose among alternatives based upon our expectations of future market trends. The development of our semiconductor solutions is highly complex, and successful product development and market acceptance of our products depends on a number of factors, including:

| • | our accurate prediction of the changing requirements of our customers; |

9

Table of Contents

| • | our timely completion and introduction of new designs; |

| • | the availability of third-party manufacturing, assembly and test capacity; |

| • | the ability of our foundries to achieve high manufacturing yields for our products; |

| • | our ability to transition to smaller manufacturing process geometries; |

| • | the quality, price, performance, power efficiency and size of our products and those of our competitors; |

| • | our management of our indirect sales channels; |

| • | our customer service capabilities and responsiveness; |

| • | the success of our relationships with existing and potential customers; and |

| • | changes in industry standards. |

We cannot assure you that we will be able to develop and introduce new or improved products in a timely and cost-effective manner, that the products we introduce will generate significant revenues or that we will be able to accurately anticipate or respond to future market trends.

We may not be able to deliver our products on a timely basis if our relationships with our suppliers, our semiconductor foundries or our assembly and test subcontractors are disrupted or terminated.

We do not own or operate a semiconductor fabrication facility. Instead, we rely on third parties to manufacture our semiconductors. Two outside foundries, UMC, in Taiwan, and SMIC, in China, currently manufacture the majority of our semiconductors. As a result, we face several significant risks, including higher wafer prices, lack of manufacturing capacity, quality assurance, manufacturing yields and production costs, limited control over delivery schedules and product quality, increased exposure to potential misappropriation of our intellectual property, labor shortages or strikes and actions taken by third party contractors that breach our agreements.

The ability of each foundry to provide us with semiconductors is limited by its available capacity. We do not have long-term agreements with any of these foundries and we place orders on a purchase order basis. We place our orders based on our customers’ purchase orders and sales forecasts. However, the foundries can allocate capacity to the production of the products of their other customers and reduce deliveries to our manufacturing logistics partners on short notice or increase the price they charge us. It is possible that other foundry customers that are larger and better financed than we are, or have long-term agreements with these foundries, may induce these foundries to reallocate capacity to them. Any reallocation could impair our ability to secure the supply of semiconductors that we need for our products. In addition, interruptions to the wafer manufacturing processes caused by a natural disaster or human error could result in partial or complete disruption in supply until we are able to shift manufacturing to another fabrication facility. It may not be possible to obtain sufficient capacity or comparable production costs at another foundry. Migrating our design methodology to a new third-party foundry could involve increased costs, resources and development time comparable to a new product development effort. Any reduction in the supply of semiconductors for our products could significantly delay our ability to ship our products and potentially have negative effects on our relationships with existing customers and our results of operations. In addition, if our subcontractors terminate their relationships with us, we would be required to qualify new subcontractors, which could take as long as six months, resulting in unforeseen operations problems, and our operating results may be materially and adversely affected.

If the foundries that provide us with the products for our operations do not achieve satisfactory yield or quality, or if the assembly and testing services fail us in the quality of their output, then our revenue, operating results and customer relationships will be affected.

The manufacture of semiconductors is a highly complex process. Minor deviations in the manufacturing process can cause substantial decreases in yield. In some situations, such deviations may cause production to be

10

Table of Contents

suspended. The foundries that manufacture our semiconductors have from time to time experienced lower than anticipated manufacturing yields, including yields for our semiconductors, typically during the production of new products or architectures or during the installation and start-up and ramp-up of new process technologies or equipment. If the foundries that manufacture our semiconductors do not achieve planned yields, our product costs could increase, and product availability would decrease.

After the wafer fabrication processes, our wafers are shipped to our assembly and testing subcontractors. We have a system to maximize consistent product quality, reliability and yield which involve our quality assurance team working closely with pertinent subcontractors in the various phases of the assembly and testing processes. We also emphasize a strong supplier quality management practice through which our quality assurance team pre-qualifies our manufacturing suppliers and subcontractors. However, despite our efforts to strengthen supplier quality management, if our foundries fail to deliver fabricated silicon wafers of satisfactory quality in the volume and at the price we require, or if our assembly and test subcontractors fail to efficiently and accurately assemble and test our products, we will be unable to meet our customers’ demand for our products or to sell those products at an acceptable profit margin, which would have a material and adverse effect on our sales and margins and damage our customer relationships.

Failure to protect our proprietary technologies or maintain the right to certain technologies may negatively affect our ability to compete.

We believe that the protection of our intellectual property rights will continue to be important to the success of our business. We rely on a combination of patent, copyright, trademark and trade secret laws and restrictions on disclosure to protect our intellectual property rights. We also enter into confidentiality or license agreements with our employees, business partners and other third parties, and have implemented procedures to control access to and distribution of our documentation and other proprietary information. Despite these efforts, we cannot assure you that these measures will provide meaningful protection of our intellectual property rights. Further, these agreements do not prevent others from independently developing technologies that are equivalent to or superior to our technology. In addition, unauthorized parties may attempt to copy or otherwise obtain and use our proprietary technology. Monitoring unauthorized use of our technology is difficult, and we cannot be certain that the steps we have taken will prevent unauthorized use of our technology, particularly in foreign countries, such as China, where the laws may not protect our proprietary rights as fully as do the laws of the United States. In addition, if the foundries that manufacture our semiconductors lose control of our intellectual property, it would be more difficult for us to take remedial measures because our foundries are located in countries that do not have the same protection for intellectual property that is provided in the United States. Also, some of our contracts, including license agreements, are subject to termination upon certain types of change-of-control transactions.

We currently have more than 40 patents. We also have 42 patent applications pending in four countries. We cannot be certain that patents will be issued as a result of our pending applications nor can we be certain that any issued patents would protect or benefit us or give us adequate protection from competing products. For example, issued patents may be circumvented or challenged and declared invalid or unenforceable or provide only limited protection for our technologies. We also cannot be certain that others will not design around our patented technology, independently develop our unpatented proprietary technology or develop effective competing technologies on their own.

Failure to successfully defend against intellectual property lawsuits brought against us may adversely affect our business.

As technology is an integral part of our design and product, we have, in the past, received communications alleging that our products infringe or misappropriate certain intellectual property rights held by others, and may continue to receive such communications in the future. We are currently involved in an intellectual property dispute with O2Micro International Limited. See “Our Business — Legal Proceedings.” If any third party were to make valid intellectual property infringement or misappropriation claims against us, we may be required to:

| • | discontinue using disputed manufacturing process technologies; |

11

Table of Contents

| • | stop selling products that contain allegedly infringing technology; |

| • | pay substantial monetary damages; |

| • | seek to develop non-infringing technologies, which may not be feasible; or |

| • | seek to acquire licenses to the infringed technology, which may not be available on commercially reasonable terms, if at all. |

If our products are found to infringe or misappropriate third-party intellectual property rights, we may be subject to significant liabilities and be required to change our manufacturing processes or products. This could restrict us from making, using, selling or exporting some of our products, which could in turn materially and adversely affect our business and financial condition. Our failure to develop non-infringing technologies or license intellectual property rights in a timely and cost-effective manner could materially and adversely affect our business and financial condition. In addition, any litigation, whether to enforce our patents or other intellectual property rights or to defend ourselves against claims that we have infringed the intellectual property rights of others, could, regardless of the ultimate outcome, materially and adversely affect our operating results by requiring us to incur significant legal expenses and diverting the resources of the company and the attention of management.

Failure to achieve and maintain technological leadership in our various multimedia consumer electronics markets could erode our competitiveness and cause our profits to decrease.

The consumer electronics market and the semiconductor components used in such market are constantly changing with increased demand for improved features such as low power or smaller size. If we do not anticipate these changes in technologies and rapidly develop and introduce new and innovative technologies, we may not be able to provide advanced semiconductor solutions on competitive terms. If we are unable to maintain the ability to provide advanced semiconductor solutions on competitive terms, some of our customers may buy semiconductor solutions from our competitors instead of us. To be competitive, we must anticipate the needs of the market and successfully develop and introduce innovative new products in a timely fashion. We cannot assure you that we will be able to successfully complete the design of our new products, have these products manufactured at acceptable manufacturing yields, or obtain significant purchase orders for these products. Furthermore, if our future innovations are ahead of the then-current technological standards in our industry, customers may be unwilling to purchase our platforms until the multimedia consumer electronics market is ready to accept them. The introduction of new products may adversely affect sales of existing products and contribute to fluctuations in our operating results from quarter to quarter. Our introduction of new products also requires that we carefully manage our inventory to avoid inventory surplus and obsolescence. Our failure to do so could have a material and adverse effect on our operating results. Furthermore, failure to achieve advances in technology or processes or to obtain access to advanced technologies or processes developed by others could erode our competitive position.

Development of new platforms and products may require us to obtain rights to use intellectual property that we currently do not have. If we are unable to obtain or license the necessary intellectual property on reasonable terms or at all, our product development may be delayed, the gross margins on our planned products may be lower than anticipated and our business and operating results would be materially and adversely affected.

Because the markets in which we compete are highly competitive and many of our competitors have greater resources than we have, we cannot be certain that our products will compete favorably in the market place.

We face competition from a large number of competitors in each of our targeted areas. We currently compete with other companies that produce flash card controllers, primarily Cypress, Genesys, Hyperstone AG, Incomm, Panasonic, Phison, Renesas, Samsung, SanDisk, Silicon Storage Technology, Skymedi, Toshiba and

12

Table of Contents

USBest. We may also face competition from some of our customers who may develop products or technologies internally that compete with our solution. For audio, graphics and imaging SoC products, we compete with Actions Semiconductor, ATI, NVIDIA, PortalPlayer, SigmaTel, Sunplus and Telechips. We expect to face increased competition in the future from our current and potential competitors. In addition, some of our customers have developed products and technologies that could replace their need for our products or otherwise reduce their demand for our products.

Many of our current and potential competitors have longer operating histories, greater name recognition, access to larger customer bases and significantly greater financial, sales and marketing, manufacturing, distribution, technical and other resources than we have. As a result, they may be able to respond more quickly to changing customer demands or to devote greater resources to the development, promotion and sales of their products than we can. Our current and potential competitors may develop and introduce new products that will be priced lower, provide superior performance or achieve greater market acceptance than our products. In addition, in the event of a manufacturing capacity shortage, these competitors may be able to obtain capacity when we are unable to do so.

The multimedia consumer electronics market, which is a principal end market for our products, has historically been subject to intense price competition. In many cases, low-cost, high-volume producers have entered the markets and driven down profit margins. If a low-cost, high-volume producer should develop products that compete with our products, our sales and profit margins would suffer.

Our principal subsidiary, Silicon Motion, Inc., is based and operates in Taiwan; we derive a substantial majority of our revenues from direct or indirect sales to non-U.S. customers and have significant foreign operations, which may expose us to foreign exchange risks.

A portion of our capital expenditures for our sales operations are denominated in currencies other than NT dollars, primarily U.S. dollars, but also, to a lesser extent, Japanese Yen, Renminbi and Euros. A significant portion of our sales are denominated in U.S. dollars, in addition to NT dollars. Therefore, we are affected by fluctuations in exchange rates among the U.S. dollar, the Japanese Yen, the NT dollar, the Renminbi and the Euro. In 2004, the U.S. dollar devalued 3% against the NT dollar, based on the average of daily exchange rates. The devaluation in 2004 hypothetically lowered our operating income by approximately 5%-6%. The value of the U.S. dollar increased slightly in 2005 versus the NT dollar, but any significant unfavorable fluctuation in the future could potentially increase our operational costs and may have a material and adverse effect on our financial condition and operating results.

Our products must meet exacting specifications and undetected defects and failures may occur, which may cause customers to return or stop buying our products and may expose us to product liability risk and risks of indemnification against defects in our products.

Our products are complex and may contain undetected hardware or software defects or failures, especially when first introduced or when new versions are released. These errors could cause us to incur significant re-engineering costs, divert the attention of our engineering personnel from product development efforts and materially affect our customer relations and business reputation. If we deliver products with errors or defects, our credibility and the market acceptance and sales of our products could be harmed. Defects could also lead to liability for defective products as a result of lawsuits against us or against our customers. We have agreed to indemnify some of our customers in some circumstances against liability from defects in our products. A successful product liability claim could require us to make significant damage payments.

Our intellectual property indemnification practices may adversely impact our business.

We may be required to indemnify our customers and our third-party intellectual property providers for certain costs and damages of intellectual property infringement in circumstances where our products are a factor

13

Table of Contents

in creating the customer’s or these third-party providers’ infringement exposure. This practice may subject us to significant indemnification claims by our customers and our third-party providers. In some instances, our products are designed for use in devices manufactured by our customers that comply with international standards, such as the MP3 compression standard. These international standards are often covered by patent rights held by third parties, which may include our competitors. The combined costs of identifying and obtaining licenses from all holders of patent rights essential to such international standards could be high and could reduce our profitability or increase our losses. The cost of not obtaining these licenses could also be high if a holder of the patent rights brings a claim for patent infringement. In the contracts under which we distribute semiconductor products, we generally have agreed to indemnify our customers against losses arising out of claims of unauthorized use of intellectual property. In some of our licensing agreements, we have agreed to indemnify the licensor against losses arising out of or related to our conduct or services. We cannot assure you that additional claims for indemnification will not be made or that these claims would not have a material and adverse effect on our business, operating results or financial condition.

Major earthquakes, fires or other natural disasters and resulting systems outages may cause us significant losses.

Our principal executive offices and a significant part of our operations are based in Taiwan. Many of our suppliers, providers of semiconductor manufacturing services for us, including semiconductor foundries and primary subcontractors for the assembly and testing of our products are located in Taiwan.

Taiwan is particularly susceptible to earthquakes. For example, in September 1999, Taiwan experienced a severe earthquake that caused significant property damage and loss of life, particularly in the central part of Taiwan. Although earthquakes and other natural disasters in Taiwan have not caused serious damages to us, if we, our suppliers, providers of semiconductor manufacturing services and primary subcontractors are affected by an earthquake or other natural disasters, such as typhoons, our production schedule could be interrupted or delayed. As a result, a major earthquake, natural disaster or

other disruptive event in Taiwan could severely disrupt the normal operation of business and have a material and adverse effect on our financial condition and operating results.

The manufacturers of our semiconductors use highly flammable materials such as alcohol, acetone, photo resistance, AsHs and pH3, in the manufacturing processes and are therefore subject to the risk of loss arising from explosion and fire. The risk of explosion and fire associated with these materials cannot be completely eliminated. Semiconductor companies experience explosion and fire damage from time to time. If any of their fabs were to be damaged or cease operations as a result of an explosion or fire, it could reduce their manufacturing capacity. Such a reduction in the manufacturing capacity of our manufacturers could disrupt the production schedule of our products thereby causing us to miss orders from our customers, which will in turn have a material and adverse effect on our business and operating results.

The recurrence of a severe acute respiratory syndrome outbreak or an outbreak of avian influenza or other outbreaks could materially and adversely affect our operating results and financial conditions.

In early 2003, China and certain other areas in Asia experienced an outbreak of severe acute respiratory syndrome, or SARS. In addition, in the spring of 2004, China had several reported cases of deaths caused by SARS. A general downturn in most Asian economies accompanied the outbreak.

In 2003, an outbreak of avian influenza affected bird and poultry populations in countries throughout Southeast Asia and other parts of Asia, including China, Hong Kong and Japan. Avian influenza resulted in human deaths in Vietnam and Thailand. Any recurrence of SARS, avian influenza or other outbreak may have a negative effect on our operations. Our operations may be impacted by a number of health-related factors, including, among other things, quarantines or closure of our offices, the sickness or death of our key officers and

14

Table of Contents

employees and a general slowdown in the economies of China, Hong Kong and Taiwan, among other countries where we have operations.

Our inability to achieve and maintain effective internal control over financial reporting could negatively impact our business, our results of operations and the market price of our ADSs.

Beginning next year, SEC rules implementing Section 404 of the Sarbanes-Oxley Act of 2002will require us to include in our Annual Reports on Form 20-F a report by our management on our internal control over financial reporting that contains our management’s assessment of the effectiveness of our internal control over financial reporting. In addition, our independent auditor must attest to and report on management’s assessment. We expect to incur additional costs and use significant management and other resources in an effort to comply with Section 404 of the Sarbanes-Oxley Act and other requirements associated with our public company reporting requirements that we did not incur as a private company.

Our management could potentially conclude that our internal controls over financial reporting are not effective. Even if our management concludes that our internal controls are effective, our independent auditor may disagree with management’s assessment. Alternatively, our independent auditor may decline to attest to our management’s assessment or may issue an adverse opinion if its interpretation of the requirements differs from our or it is otherwise dissatisfied with our internal control over financial reporting or the level at which our internal control over financial reporting is documented, designed, operated or reviewed. Any of these possible scenarios could cause investors to lose confidence in the reliability of our consolidated financial statements, which could result in a decline in the market price of our ADSs. Moreover, if we fail to maintain acceptable internal control over financial reporting, fail to implement required new or improved controls, or experience difficulties in their implementation, our business and operating results could suffer, we could fail to meet our reporting obligations, and the market price of ADSs could decline as a result.

Political, Regulatory and Economic Risks

We face substantial political risks associated with doing business in Taiwan because of the tense political relationship between Taiwan and the People’s Republic of China.

Our principal executive offices, a majority of our employees and a significant amount of our research and development and operations are based in Taiwan. In addition, two of our primary third party manufacturers, UMC and SMIC, are located in Taiwan and China, respectively. Accordingly, our business and results of operations and the market price of our ADSs may be affected by changes in Taiwan governmental policies, taxation, inflation or interest rates and by social instability and diplomatic and social developments in or affecting Taiwan that are outside of our control. Taiwan has a unique international political status. China does not recognize the sovereignty of Taiwan. Although there have been significant economic and cultural ties between the Taiwan and China in recent years, the political relations have often been strained. The

government of China has indicated that it may use military force to gain control over Taiwan, particularly under what it considers as highly provocative circumstances, such as a declaration of independence by Taiwan or the refusal by Taiwan to accept China’s stated “one China” policy. On March 14, 2005, the National Peoples’ Congress of China passed what is widely referred to as the “anti-secession” law, a law authorizing the Chinese military to attack in order to block moves by Taiwan toward formal independence. Past developments in relations between Taiwan and China have on occasion depressed the market prices of the securities of Taiwanese companies. Relations between Taiwan and China and other factors affecting military, political or economic conditions in Taiwan could have a material adverse effect on our financial condition and results of operations, as well as the market price of our ADSs.

The relations between Taiwan and China and other factors affecting military, political or economic conditions in Taiwan could also have a material and adverse effect on the financial condition of the two primary

15

Table of Contents

foundries that manufacture most of our semiconductors. One of the foundries, UMC, is located in Taiwan, and the other, SMIC, is located in China. Such relations between Taiwan and China and other factors could also have a material and adverse effect on the financial condition of SPIL, ASE and King Yuan Electronics Co., Ltd., our primary subcontractors for the assembly and testing of our products, which are also located in Taiwan. In addition, any expansion or development of our research and development team in China could be restricted or jeopardized, and our sales and marketing performance may be affected.

If economic conditions in Taiwan deteriorate, our current business and future growth would be adversely affected.

The currencies of many East Asian countries, including Taiwan, have experienced considerable volatility and depreciation in recent years. The Central Bank of China, which is the central bank of Taiwan, has from time to time intervened in the foreign exchange market to minimize the fluctuation of the U.S. dollar/NT dollar exchange rate and to prevent significant decline in the value of the NT dollar. NT dollars have depreciated against U.S. dollars from US$1.00 = NT$27.52 on January 2, 1997 to US$1.00 = NT$31.99 on May 31, 2006, based on the noon buying rates published by the Federal Reserve Bank of New York. Any change in the value of NT dollars could have a material and adverse effect on the value in foreign currency terms of our ADSs and any dividends payable by us.

In addition, Taiwan’s banking and financial sectors have been seriously affected by the general economic downturn in Asia and Taiwan in recent years, which has caused an increase in the number of companies filing for corporate reorganization and bankruptcy protection. As a result, financial institutions are more cautious in providing credit to businesses in Taiwan. We cannot assure you that we will continue to have access to credit at commercially reasonable rates of interest or at all, should we need additional capital to expand our business.

Our business depends on the support of the Taiwan government, and a decrease in this support may increase our tax liabilities and decrease our net income.

The Taiwan government has been very supportive of technology companies such as ours. In particular, we, like many Taiwanese technology companies, have benefited from tax incentives provided by the Taiwan government. For example, under the Statute for Upgrading Industries of Taiwan, we are granted tax credits by the Taiwan Ministry of Finance at rates set at certain percentages of the amounts utilized in qualifying research and development costs and in qualifying employee training expenses. If such tax credits cannot be utilized in the fiscal year in which the relevant costs or expenses were incurred, they may be carried forward for up to the next four years. In addition, Taiwan law offers preferential tax treatments to industries that are encouraged by the Taiwan government. These preferential tax treatments include 5-year tax exemptions for income attributable to expanded production capacity or newly developed technologies funded in whole or in part by proceeds from initial capital investments made by our shareholders, or subsequent capital increases, or capitalization of our retained earnings. Such tax exemptions may be available either to the shareholders of a company, or, if the shareholders so determine, to the company itself. SMI Taiwan has filed three applications for such tax exemptions as SMI Taiwan had used the proceeds of the new share offerings received in 2002, 2003 and 2004 to fund eligible research and development projects. In the first quarter of 2005, SMI Taiwan received certain requisite consents or approvals for tax exemptions. See “Management’s Discussion and Analysis of Financial Conditions and Results of Operations – Principal Factors Affecting Our Results of Operations – Provision for income taxes” for a more detailed description of our ability to enjoy these preferential tax treatments. If any of our tax credits or our ability to take advantage of these preferential tax treatments are curtailed or eliminated, our net income may decrease materially.

16

Table of Contents

If we are unable to satisfy the conditions set by the Investment Commission of the Taiwan Ministry of Economic Affairs, or the IC, the effectiveness of the share exchange leading to the establishment of our current corporate structure could be challenged by the ROC government authorities.

Our current corporate structure is established as a result of a share exchange between us and the shareholders of SMI Taiwan. Approval from the IC was sought and successfully granted for the share exchange. However the IC granted the approval on condition that SMI Taiwan must firstly, apply for at least five patents in each of 2005, 2006 and 2007, secondly, employ between 15 to 20 research and development engineers in each of 2005, 2006 and 2007, and finally, maintain research and development expenditures in the amount of at least NT$100 million (US$3.0 million) in each of 2005, 2006 and 2007. We are required to submit to the IC SMI Taiwan’s annual financial statements audited by a certified public accountant and other relevant supporting documents in connection with the implementation of those three conditions within four months after the end of each of 2005, 2006 and 2007. To the extent that we are unable to satisfy any of those three conditions, the IC may revoke our rights of repatriation of profits to be distributed by SMI Taiwan or rescind its approval of the share exchange. This would have an adverse effect on our corporate structure and consequently, materially and adversely affect our ability to conduct our business.

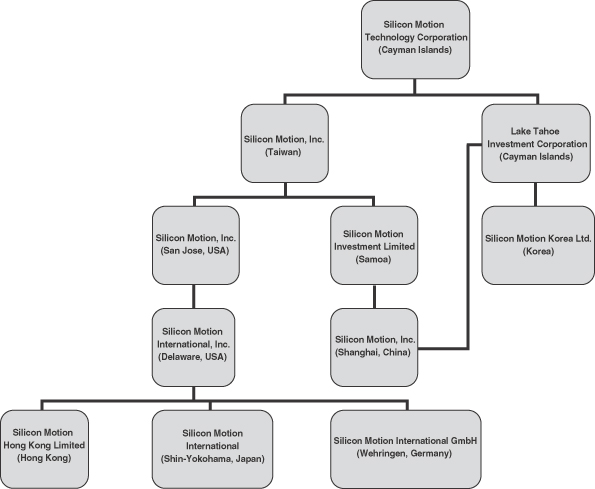

| ITEM 4. | INFORMATION ON THE COMPANY |

History and Development of the Company

SMI Taiwan (formerly Feiya Technology Corporation) was incorporated on April 8, 1997 and its shares were approved for public issue in Taiwan in December 1999.

SMI USA was incorporated in California in November 1995.

In August 2002, Feiya Technology Corporation acquired SMI USA and changed its name from “Feiya Technology Corporation” to “Silicon Motion, Inc.” To facilitate the acquisition:

| • | Crane Technology, Inc., or CTI, a Delaware corporation, was formed to become a holding company for SMI USA; |

| • | one of the then shareholders of Feiya Technology Corporation sold certain shares in Feiya to CTI; |

| • | Crane Acquisition Corporation, or CAC, a California corporation and a wholly-owned subsidiary of CTI then merged with and into SMI USA and in the process the separate corporate existence of CAC ceased and SMI USA continued as the surviving corporation and became a wholly-owned subsidiary of CTI; |

| • | in the merger, the shareholders of SMI USA received cash or shares of CTI and became holders of all outstanding shares of CTI; |

| • | prior to the merger, CTI purchased shares of SMI Taiwan from SMI Taiwan and a then shareholder of SMI Taiwan; and |

| • | subsequent to the merger, SMI Taiwan purchased from CTI all of the outstanding shares of SMI USA held by CTI after the merger. |

The entire transaction was accounted for under the purchase method of accounting with Feiya as the acquirer such that Feiya issued 25.4 million shares of Feiya common stock in exchange for 100% of the outstanding shares of SMI USA preferred stock. As each share of outstanding common stock of SMI USA was repurchased by SMI USA and cancelled prior to the merger, Feiya also issued 18.5 million shares of its common stock to former employees or their designees, directors and former common shareholders of SMI USA. The purchase consideration was NT$610 million (US$18.6 million) and was determined using a per share price of NT$13.7 for Feiya common stock which was determined to be the fair value of the shares at the date of consummation of the merger.

SMI Taiwan’s common shares had been traded on the Emerging Stock Board of the Taiwan GreTai Securities Market (formerly known as the Taiwan Over-the-Counter Securities Exchange), or Taiwan OTC, since

17

Table of Contents

June 27, 2003. Trading of SMI Taiwan’s common shares on the Emerging Stock Board ceased on April 18, 2005. On January 27, 2005, Silicon Motion Technology Corporation was incorporated in the Cayman Islands. On April 25, 2005, SMI Taiwan became a wholly-owned subsidiary of Silicon Motion Technology Corporation through a share exchange, which was approved at a shareholders’ meeting of SMI Taiwan on March 7, 2005, with no dissenting shareholders. According to the resolutions adopted by such shareholders meeting of SMI Taiwan, one common share of SMI Taiwan would be exchanged for one ordinary share of Silicon Motion Technology Corporation. The share exchange was conducted under the Business Mergers and Acquisitions Law of Taiwan. Under such share exchange, the issued shares of SMI Taiwan were acquired by Silicon Motion Technology Corporation, which issued 105,412,000 ordinary shares to the shareholders of SMI Taiwan. The Investment Committee, or IC, of the Ministry of Economic Affairs of Taiwan on April 12, 2005, approved our acquisition of 105,412,000 common shares of SMI Taiwan in the share exchange, and on April 14, 2005, approved the acquisition by Taiwan shareholders of SMI Taiwan of 81,145,807 ordinary shares of Silicon Motion Technology Corporation. Acquisition of ordinary shares of Silicon Motion Technology Corporation by non-Taiwan shareholders of SMI Taiwan is not subject to prior approval of the IC.

On July 5, 2005, we completed an underwritten initial public offering of 4,300,000 ADSs, representing 17,200,000 of our ordinary shares. Our ADSs have been traded on the Nasdaq National Market since June 30, 2005.