Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO THE CONSOLIDATED FINANCIAL STATEMENTS OF AMEC

INDEX TO THE CONSOLIDATED FINANCIAL STATEMENTS OF FOSTER WHEELER

INDEX TO THE RECONCILIATION OF FOSTER WHEELER'S FINANCIAL INFORMATION

As filed with the Securities and Exchange Commission on 28 April 2014

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form F-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

AMEC plc

(Exact name of registrant as specified in its charter)

Not Applicable

(Translation of registrant name into English)

| United Kingdom (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

Not Applicable (I.R.S. Employer Identification Number) |

Alison Yapp

General Counsel & Company Secretary

Old Change House

128 Queen Victoria Street

London EC4V 4BJ

United Kingdom

+44 (0) 20 7429 7500

(Address, including zip code, and telephone number, including

area code, of Registrant's principal executive offices)

(Name, address, including zip code, and telephone number, including

area code, of agent of service)

| Copies to: | ||||||

Thomas B. Shropshire, Jr. Linklaters LLP One Silk Street London EC2Y 8HQ United Kingdom +44 (0) 20 7456 2000 |

Scott Sonnenblick Peter Cohen-Millstein Linklaters LLP 1345 Avenue of the Americas New York, NY 10105 United States +1 (212) 903 9000 |

Doug Smith Freshfields Bruckhaus Deringer LLP 65 Fleet Street London EC4Y 1HT United Kingdom +44 (0) 20 7936 4000 |

Matthew F. Herman Freshfields Bruckhaus Deringer US LLP 601 Lexington Avenue New York, NY 10022 United States +1 (212) 277 4000 |

|||

Approximate date of commencement of proposed sale of the securities to the public:

As soon as practicable after this Registration Statement becomes effective and all other conditions to the consummation of the transaction described in this prospectus have been satisfied or waived.

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) o

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) o

CALCULATION OF REGISTRATION FEE

|

||||||||

| Title of each class of securities to be registered(1) |

Amount to be registered(2) |

Proposed maximum offering price per unit |

Proposed maximum aggregate offering price(3) |

Amount of registration fee(4) |

||||

|---|---|---|---|---|---|---|---|---|

Ordinary shares, nominal value £0.50 per share |

90,917,043 | N/A | 1,733,703,270 | 223,301.11 | ||||

|

||||||||

Notes:

- (1)

- American

depositary shares issuable on deposit of the AMEC shares registered hereby are being registered pursuant to a separate Registration Statement on

Form F-6.

- (2)

- Represents

the maximum number of AMEC shares estimated to be issuable upon the completion of the Offer for Foster Wheeler shares described herein.

- (3)

- Pursuant

to Rule 457(c) and Rule 457(f), and solely for the purpose of calculating the registration fee, the market value of the securities to

be offered was calculated as the sum of (a) the product of (i) 99,713,289 Foster Wheeler shares, par value CHF3.00 per share and (ii) the average of the high and low sales prices

of Foster Wheeler registered shares reported on NASDAQ on 21 April 2014 equal to $33.60, less $1,616,662,240, the estimated maximum aggregate amount of cash to be paid in the offer in exchange

for such securities.

- (4)

- Calculated in accordance with Rule 457(f) under the Securities Act as the product of the maximum aggregate offering price and $128.80 per $1,000,000 of securities registered.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus may change. AMEC may not complete the exchange offer and issue these securities until the registration statement filed with the US Securities and Exchange Commission, referred to as the SEC, is effective. This prospectus is not an offer to sell or a solicitation to sell these securities in any jurisdiction where such offer, sale or solicitation is not permitted.

![]()

Offer to Exchange

Each

Registered Share

of

![]()

For

$16.00 Cash and 0.8998 Securities in AMEC plc

(at the election of Foster Wheeler shareholders, $32.00 Cash or 1.7996 Securities)

by

AMEC INTERNATIONAL INVESTMENTS BV

a wholly-owned subsidiary of

AMEC PLC

AMEC International Investments BV, a company organised under the laws of the Netherlands and a direct wholly-owned subsidiary of AMEC plc, a company organised under the laws of England and Wales, is offering to acquire all of the issued and to be issued registered shares, par value CHF3.00 per share, or Foster Wheeler shares, of Foster Wheeler AG, a company organised under the laws of Switzerland, upon the terms and subject to the conditions set forth in this prospectus and in the related letter of transmittal, which are referred to in this prospectus together, as each may be amended or supplemented from time to time, as the Offer. Pursuant to the implementation agreement, dated 13 February 2014 and amended by the Deed of Amendment dated 2014, between AMEC and Foster Wheeler, which is referred to as the Implementation Agreement, AMEC International Investments BV will pay up to $1,616,662,240 in cash and will offer up to 90,917,043 new AMEC securities, or AMEC securities, which, at the election of Foster Wheeler shareholders, will be issued in the form of ordinary shares, nominal value £0.50 per share, or AMEC shares, or American depositary shares each representing one (1) AMEC share, or AMEC ADSs.

You may elect to receive either cash or AMEC securities with respect to each Foster Wheeler share you hold, subject in each case to proration as set forth in the Implementation Agreement and described in this prospectus. See "The Offer—Terms of the Offer—Mix and Match Election and Proration" for a detailed description of the proration procedures.

If, following completion of the exchange offer, AMEC, directly or indirectly, has acquired or controls at least 90 per cent. of the issued Foster Wheeler voting rights, no actions or proceedings are pending with respect to the exercisability of those voting rights and no other legal impediment to a Squeeze-Out Merger under Swiss law exists, AMEC will, indirectly through a wholly-owned subsidiary, initiate a Squeeze-Out Merger under Swiss law whereby any remaining holders of Foster Wheeler shares will be compensated (in cash or otherwise) as required pursuant to Swiss law. Pursuant to the Swiss Merger Act, the amount or value of such compensation must be adequate, but such amount may be different in form and/or value from the consideration received in the Offer.

As at 22 April 2014, the latest practicable date prior to the date of this document, the total value of the consideration being offered by AMEC was $3,459,816,179, based on the closing price of £12.05 for the AMEC shares on the London Stock Exchange, or the LSE, on that date and an exchange rate of $1.6824 per pound sterling, as published in The Financial Times on 23 April 2014.

FOSTER WHEELER'S BOARD HAS UNANIMOUSLY RESOLVED THAT THE IMPLEMENTATION AGREEMENT AND THE OFFER ARE IN THE BEST INTERESTS OF FOSTER WHEELER AND FAIR TO THE HOLDERS OF FOSTER WHEELER SHARES, HAS APPROVED THE IMPLEMENTATION AGREEMENT AND HAS RESOLVED TO RECOMMEND THAT HOLDERS OF FOSTER WHEELER SHARES TENDER THEIR FOSTER WHEELER SHARES INTO THE OFFER.

The completion of the Offer is subject to certain conditions, including that at least 80 per cent. of the Foster Wheeler shares are tendered in the Offer, subject to the right by AMEC to waive the minimum tender condition down to 662/3 per cent. A detailed description of the terms and conditions of this Offer appears under "The Offer—Terms of the Offer" and "The Offer—Conditions to the Offer" in this prospectus.

THIS OFFER WILL COMMENCE AT NEW YORK CITY TIME ( LONDON TIME; ZUG TIME) ON 2014. THIS OFFER, AND YOUR RIGHT TO WITHDRAW FOSTER WHEELER SHARES YOU TENDER IN THIS OFFER, WILL EXPIRE AT 11:59 P.M., NEW YORK CITY TIME ( LONDON TIME; ZUG TIME) ON 2014, UNLESS THE EXPIRATION TIME OF THIS OFFER IS EXTENDED.

Foster Wheeler shares are listed on NASDAQ Stock Market. AMEC's shares are listed and admitted to trading on the London Stock Exchange's main market for listed securities. Prior to completion of the Offer, AMEC will apply to the UK Financial Conduct Authority for the new AMEC shares to be admitted to the premium listing segment of the Official List of the UK Listing Authority and to the London Stock Exchange for the new AMEC shares to be admitted to trading on the LSE, respectively. AMEC intends to apply for the AMEC ADSs to be listed on the New York Stock Exchange.

FOR A DISCUSSION OF RISK FACTORS THAT YOU SHOULD CAREFULLY CONSIDER IN EVALUATING THE OFFER, SEE "RISK FACTORS" BEGINNING ON PAGE 36.

THIS PROSPECTUS CONTAINS DETAILED INFORMATION CONCERNING THE OFFER FOR FOSTER WHEELER SHARES AND THE PROPOSED ACQUISITION OF FOSTER WHEELER. AMEC RECOMMENDS THAT YOU READ THIS PROSPECTUS CAREFULLY.

THIS PROSPECTUS IS NOT AN OFFER TO SELL SECURITIES AND IS NOT A SOLICITATION OF AN OFFER TO BUY SECURITIES, NOR SHALL THERE BE ANY SALE OR PURCHASE OF SECURITIES PURSUANT HERETO, IN ANY JURISDICTION IN WHICH SUCH OFFER, SALE OR SOLICITATION IS NOT PERMITTED OR WOULD BE UNLAWFUL PRIOR TO REGISTRATION OR QUALIFICATION UNDER THE LAWS OF ANY SUCH JURISDICTION.

NEITHER THE SEC NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THE SECURITIES TO BE ISSUED IN CONNECTION WITH THE OFFER OR HAS PASSED UPON THE ADEQUACY OR ACCURACY OF THE DISCLOSURE IN THIS PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE IN THE UNITED STATES.

THIS IS NOT A PROSPECTUS PUBLISHED IN ACCORDANCE WITH THE PROSPECTUS RULES MADE UNDER PART VI OF THE UNITED KINGDOM FINANCIAL SERVICES AND MARKETS ACT 2000 (AS SET OUT IN THE FINANCIAL CONDUCT AUTHORITY HANDBOOK), OR THE UK PROSPECTUS RULES. AMEC INTENDS TO PUBLISH A PROSPECTUS UNDER THE UK PROSPECTUS RULES IN CONNECTION WITH ITS APPLICATION FOR ADMISSION OF AMEC ORDINARY SHARES TO LISTING ON THE PREMIUM SEGMENT OF THE OFFICIAL LIST OF THE UNITED KINGDOM LISTING AUTHORITY AND TO TRADING ON THE MAIN MARKET OF THE LONDON STOCK EXCHANGE. A COPY OF SUCH PROSPECTUS MAY BE OBTAINED AT AMEC'S WEBSITE (WWW.AMEC.COM) FOLLOWING APPROVAL BY THE FINANCIAL CONDUCT AUTHORITY OF THE UNITED KINGDOM.

The date of this prospectus is 2014.

This prospectus is not an offer to sell securities and it is not a solicitation of an offer to buy securities, nor shall there be any sale or purchase of securities pursuant hereto, in any jurisdiction in which such offer, solicitation or sale is not permitted or would be unlawful prior to registration or qualification under the laws of any such jurisdiction. If you are in any doubt as to your eligibility to participate in the Offer, you should contact your professional adviser immediately.

This prospectus has not been, and will not be, lodged with the Australian Securities and Investments Commission, which is referred to as ASIC, as a disclosure document for the purposes of the Corporations Act of Australia 2001, referred to as the Corporations Act. This prospectus does not purport to include the information required of a disclosure document under Chapter 6D of the Corporations Act. Any securities received in the Offer may not be offered for sale (or transferred, assigned or otherwise alienated) to investors in Australia for at least 12 months after issuance, except in circumstances where disclosure to investors is not required under Chapter 6D of the Corporations Act or unless a disclosure document that complies with the Corporations Act is lodged with ASIC. Each investor acknowledges the above and, by applying for shares in the Offer under this prospectus, gives an undertaking not to sell those shares (except in the circumstances referred to above) for 12 months after issuance.

This document, which forms part of a registration statement on Form F-4 filed with the SEC by AMEC, constitutes a prospectus of AMEC under Section 5 of the US Securities Act of 1933, as amended, with respect to the shares of AMEC, which are referred to as the AMEC shares, underlying the American Depositary Shares representing the AMEC shares, which are referred to as AMEC ADSs, to be delivered to Foster Wheeler shareholders pursuant to the Offer.

In this prospectus, unless otherwise specified or the context otherwise requires:

- •

- "CHF" and "Swiss Franc" each refer to the lawful currency of the Swiss Confederation;

- •

- "£" and "pound sterling" each refer to the lawful currency of the United Kingdom of Great Britain and Northern

Ireland; and

- •

- "$" and "US dollar" each refer to the US dollar.

REFERENCE TO ADDITIONAL INFORMATION

Foster Wheeler files annual, quarterly and other reports, proxy statements and other information with the SEC. AMEC has filed a registration statement on Form F-4 with the SEC. You can obtain documents related to AMEC and Foster Wheeler, without charge, by requesting them in writing or by telephone from the appropriate company.

| AMEC | Foster Wheeler | Foster Wheeler | ||

| Old Change House | 53 Frontage Road | Lindenstrasse 10 | ||

| 128 Queen Victoria Street | P.O. Box 9000 | 6340 Baar, Switzerland | ||

| London EC4V 4BJ | Hampton, NJ 08827-9000 | +41 41 748 4320 | ||

| United Kingdom | United States | www.fwc.com | ||

| +44 (0) 20 7429 7500 | +1 (908) 730 4000 | |||

| Attention: Investor Relations | Attention: Corporate Secretary | |||

| www.amec.com | www.fwc.com |

You may also obtain copies of these documents, without charge, from the website maintained by the SEC at www.sec.gov.

See "Additional Information for Security Holders—Where You Can Find More Information" beginning on page 417.

QUESTIONS AND ANSWERS ABOUT THE OFFER

The following are some of the questions that you, as a Foster Wheeler shareholder, may have regarding the Offer along with answers to those questions. These questions and answers, as well as the following summary, are not meant to be a substitute for the information contained in the remainder of this prospectus or the appendices to this prospectus, and this information is qualified in its entirety by the more detailed descriptions and explanations contained therein. AMEC urges you to carefully read this prospectus in its entirety prior to making any decision as to your Foster Wheeler shares.

Q. Who is making the Offer?

A. AMEC is making the Offer to purchase all of the issued and to be issued Foster Wheeler shares through its direct wholly-owned subsidiary, AMEC International Investments BV. Pursuant to the Implementation Agreement, AMEC has agreed to cause all members of its group, including AMEC International Investments BV, to comply with all of its obligations in connection with the Offer.

Q. Who is AMEC?

A. AMEC is a focused supplier of consultancy, engineering and project management services to its customers in the world's oil and gas, mining, clean energy, environment and infrastructure markets. AMEC provides support for assets, such as upstream oil and gas production facilities, mines and nuclear power stations, throughout their lifecycle, from inception to decommissioning. For the year ended 31 December 2013, AMEC's revenue was £3,974 million, its trading profit was £343 million and it employed an average of 28,867 people. See "Presentation of Certain Financial and Other Information—Non-IFRS and Non-US GAAP Financial Measures" for a reconciliation of trading profit to the nearest IFRS measure, profit before net financing income.

AMEC is incorporated and registered in England and Wales. AMEC is headquartered at Old Change House, 128 Queen Victoria Street, London EC4V 4BJ, United Kingdom, its registered office is at Booths Park, Chelford Road, Knutsford, Cheshire WA16 8QZ, United Kingdom and its main telephone number is +44 (0) 20 7429 7500. AMEC's shares are listed on the Official List of the UK Financial Conduct Authority, or FCA, and admitted to trading on the main market of the London Stock Exchange under the symbol "AMEC". The AMEC ADSs will be traded on the New York Stock Exchange on a "when issued" basis, subject to the issuance of AMEC ADSs upon completion of the Offer.

Q. Who is AMEC International Investments BV?

A. AMEC International Investments BV is a direct wholly-owned subsidiary of AMEC. All outstanding shares of AMEC International Investments BV are owned by AMEC. AMEC International Investments BV's principal executive offices are located at Facility Point, Meander 251, 6825 MC Arnhem, the Netherlands, and its telephone number is +31 (0) 88 2174 111.

Q. Why is AMEC seeking to acquire all of the issued and to be issued Foster Wheeler shares?

A. AMEC, through AMEC International Investments BV, is offering to acquire all of the issued and to be issued Foster Wheeler shares in order to acquire 100 per cent. of the issued share capital of Foster Wheeler, which is referred to as the Acquisition. AMEC believes that the Acquisition will provide a number of strategic opportunities, including enabling AMEC to expand its operations across the entire oil and gas value chain, and increasing AMEC's presence in regions where it currently has less exposure and which it considers to offer higher growth opportunities, such as the Middle East and Latin America.

3

Q. What consideration is being offered for my Foster Wheeler shares?

A. Foster Wheeler shareholders are being offered $16.00 in cash and 0.8998 in AMEC securities (in the form of AMEC shares or AMEC ADSs, at the election of Foster Wheeler shareholders) for each Foster Wheeler share held, which tendering Foster Wheeler shareholders may elect to receive as (i) $32.00 in cash or (ii) 1.7996 in AMEC securities (in the form of AMEC shares or AMEC ADSs, at the election of the Foster Wheeler shareholders), subject in each case to proration as described in the section entitled "The Offer—Terms of the Offer—Mix and Match Election and Proration".

This represents approximately $3.3 billion in aggregate, calculated using the closing AMEC share price on the LSE of £10.92 and an exchange rate of $1.658 per pound sterling as at 12 February 2014. This represents a premium of approximately 12.4 per cent. to Foster Wheeler's closing share price on NASDAQ of $28.73 on 26 November 2013, the last trading day prior to initial public reports about a potential business combination involving AMEC and Foster Wheeler, and a premium of approximately 18.9 per cent. to the three-month volume weighted average price of Foster Wheeler's shares (measured for the three-month period ending on 26 November 2013) of approximately $27.15.

Q. What will I receive if I accept the Offer?

A. The aggregate amount of cash and the total number of AMEC securities (in the form of AMEC shares or AMEC ADSs, at the election of the Foster Wheeler shareholder) to be paid and issued pursuant to the Offer, respectively, is fixed. Therefore, the actual amount of cash or number of AMEC securities that Foster Wheeler shareholders will be entitled to receive for each Foster Wheeler share cannot be determined before the end of the Offer period or, in the case of any subsequent offering period, on each day of payment. The Offer will allow for a "mix and match" election, whereby tendering Foster Wheeler shareholders may elect, subject in each case to proration, to receive either (i) $32.00 in cash or (ii) 1.7996 AMEC securities, which, at the election of Foster Wheeler shareholders, will be issued in the form of AMEC shares or AMEC ADSs, in exchange for each Foster Wheeler share held.

As noted above, the aggregate amount of cash to be paid (on the one hand) and the aggregate number of AMEC securities to be issued (on the other hand) are both fixed. Depending on the elections made by other Foster Wheeler shareholders, you may receive a proportion of cash and/or AMEC securities that is different from what you elected. If the elections result in an oversubscription of the pool of cash or AMEC securities available to be paid or issued pursuant to the Offer, certain proration procedures (as agreed by the parties in the Implementation Agreement) for allocating cash and AMEC securities among tendering Foster Wheeler shareholders will be followed by the exchange agent. Shareholders who make no election will receive cash and AMEC shares in proportion to the amount of each type of consideration that remains after payment to tendering Foster Wheeler shareholders who have made valid elections.

The exchange ratio in relation to the securities portion of the Offer consideration is fixed and will not vary, regardless of any fluctuations in the market price of either AMEC securities or Foster Wheeler shares. Therefore, the dollar value of the AMEC securities that holders of Foster Wheeler shares will receive upon completion of the Offer will depend on the market value of AMEC shares and the exchange rate of pounds sterling to US dollars at the time of completion.

See "The Offer—Terms of the Offer—Mix and Match Election and Proration" for more information about the mix and match election.

Q. How will the cash component of the Offer be financed?

A. The cash component of the Offer (approximately $1.6 billion) will be financed through a combination of AMEC's existing cash resources and new debt financing. The new debt financing has

4

been arranged through a combination of new bank facilities from Bank of America Merrill Lynch International Limited, Bank of Tokyo Mitsubishi UFJ, Ltd., Barclays Bank plc and The Royal Bank of Scotland plc, or the Lenders, including a bridging facility and an additional revolving credit facility.

Q. What are the most significant conditions to the Offer?

A. The Offer is conditioned upon a number of things, including having received valid acceptance of the Offer from Foster Wheeler shareholders holding a minimum of 80 per cent. of Foster Wheeler's total issued share capital, anti-trust and other regulatory approvals having been obtained, AMEC shareholders having approved the transaction and the listing of the new AMEC securities to be issued in the Offer. In addition, the Offer is conditioned upon the absence of a material adverse effect on Foster Wheeler.

AMEC, through AMEC International Investments BV, reserves the right to waive, in whole or in part, subject to certain exceptions, any condition to the Offer. AMEC, through AMEC International Investments BV, may waive the minimum tender condition down to 662/3 per cent.

The Offer is not subject to any financing condition.

See "The Offer—Conditions to the Offer" for additional information.

Q. Is AMEC's financial condition relevant to my decision to tender into the Offer?

A. Yes. Foster Wheeler shares validly tendered and accepted for payment in the Offer will be exchanged for cash and/or AMEC securities, which, at the election of Foster Wheeler shareholders, will be issued in the form of AMEC shares or AMEC ADSs. You should consider AMEC's financial condition before you decide to become a holder of AMEC's shares (whether in the form of AMEC shares or AMEC ADSs) through the Offer.

Q. Does AMEC's Board support the Offer?

A. Yes. AMEC's Board has:

- •

- unanimously determined that the Implementation Agreement and the Offer are in the best interests of AMEC and fair to the

holders of AMEC shares; and

- •

- approved the Implementation Agreement.

Q. Does Foster Wheeler's Board support the Offer?

A. Yes. Foster Wheeler's Board has:

- •

- unanimously resolved that the Implementation Agreement and the Offer are in the best interests of Foster Wheeler and fair

to the holders of Foster Wheeler shares;

- •

- approved the Implementation Agreement; and

- •

- resolved to recommend that holders of Foster Wheeler shares tender their Foster Wheeler shares into the Offer.

Q. Will Foster Wheeler's executive officers and directors participate in the Offer?

A. Yes. To Foster Wheeler's knowledge, after making reasonable inquiry, all of its directors and executive officers currently intend to tender, or cause to be tendered, all Foster Wheeler shares held of record or beneficially owned by such persons pursuant to the Offer (other than Foster Wheeler shares as to which such holder does not have discretionary authority).

5

Q. What will happen to my outstanding Foster Wheeler stock options, or Foster Wheeler options, my Foster Wheeler restricted share units, or Foster Wheeler RSUs, or my Foster Wheeler restricted share units with performance goals, or Foster Wheeler PRSUs, in the Offer?

A. The Offer does not extend to Foster Wheeler options, Foster Wheeler RSUs or Foster Wheeler PRSUs. All outstanding unvested Foster Wheeler options and Foster Wheeler RSUs granted on or before 8 November 2012 will vest in full on the closing of the Offer. Outstanding Foster Wheeler PRSUs granted on or before 8 November 2012 will vest on the closing of the Offer, to the extent that Foster Wheeler's Compensation and Executive Development Committee determines that the applicable performance condition has been met as at the latest practicable measurement date prior to the closing of the Offer, and shall lapse as to the balance. Holders of such Foster Wheeler options, Foster Wheeler RSUs and Foster Wheeler PRSUs will, following the closing of the Offer, receive (at the election of Foster Wheeler) the relevant number of Foster Wheeler shares or a cash sum calculated by multiplying the number of vested Foster Wheeler shares under the applicable award by the closing price on NASDAQ of a Foster Wheeler share on the last trading day prior to the closing of the Offer, less, in the case of Foster Wheeler options only, any exercise price payable to exercise the option. Any cash sum will be paid no later than 10 Business Days after closing of the Offer and will be subject to applicable withholding taxes.

All outstanding Foster Wheeler options, Foster Wheeler RSUs and Foster Wheeler PRSUs granted after 8 November 2012 which have not vested in the ordinary course prior to the closing of the Offer will not vest and instead holders of such awards will receive equivalent, replacement awards of AMEC shares. The number of AMEC shares subject to replacement awards, in the case of Foster Wheeler options and Foster Wheeler RSUs, will be calculated by multiplying the number of Foster Wheeler shares subject to the outstanding award by 1.7996 and rounding down to the nearest whole number. In the case of a Foster Wheeler option, the total exercise price payable to exercise the replacement award will, to the greatest extent possible, be the same as the corresponding total exercise price for the Foster Wheeler option which it replaces. The number of AMEC shares subject to replacement awards, in the case of Foster Wheeler PRSUs, will be calculated by multiplying 50 per cent. of the maximum number of Foster Wheeler shares subject to the outstanding award by 1.7996 and rounding down to the nearest whole number. The terms and conditions of the replacement awards will be equivalent in all material respects to those applicable to the Foster Wheeler awards immediately prior to closing of the Offer, except that no performance conditions will apply to the replacement award in respect of Foster Wheeler PRSUs.

Foster Wheeler awards of approximately 105,728 Foster Wheeler shares will vest in the ordinary course in May, July, August and September 2014. Foster Wheeler RSUs and Foster Wheeler PRSUs will be settled in Foster Wheeler shares shortly after vesting and Foster Wheeler options, if exercised, will be settled in Foster Wheeler shares upon exercise. AMEC will extend the Offer to holders of any Foster Wheeler shares obtained under Foster Wheeler RSUs and Foster Wheeler PRSUs that vest prior to the closing of the Offer and Foster Wheeler options that are exercised prior to the closing of the Offer.

Q. How do I accept the Offer?

A. The steps you must take to validly tender into the Offer will depend on whether you hold your Foster Wheeler shares directly, or indirectly through a financial intermediary, broker, dealer, commercial bank, trust company or other entity.

- •

- If you hold your Foster Wheeler shares in registered form, you may tender your Foster Wheeler shares to the exchange agent

by delivering to the exchange agent a properly completed and duly executed letter of transmittal.

- •

- If you hold your Foster Wheeler shares through a financial intermediary, you should instruct your financial intermediary through which you hold your Foster Wheeler shares to tender your Foster

6

Wheeler shares to the exchange agent by means of delivery through the book-entry confirmation facilities of The Depository Trust Company, or DTC, before the expiration of the Offer.

Q. When does the Offer expire, and under what circumstances will the Offer be extended?

A. The Offer will expire at 11:59 p.m. New York City time ( London time; Zug time) on 2014, unless the expiration time of the Offer is extended.

If one or more of the conditions to the Offer set out in the Implementation Agreement and described in this prospectus under "The Offer—Conditions to the Offer" is not satisfied or, to the extent legally permitted, waived, AMEC will cause AMEC International Investments BV to extend the period of time for which the Offer is open, in consecutive periods of up to 10 Business Days, until all the conditions set forth in "The Offer—Conditions to the Offer" have been satisfied or waived, except that neither AMEC nor AMEC International Investments BV will be required to extend the Offer beyond 31 October 2014 except in limited circumstances, as provided for in the Implementation Agreement. For purposes of the Offer, a "Business Day" means any day other than a Saturday or Sunday on which banks in the City of London, New York and Zurich are generally open for business.

Following the first date on which all conditions to the Offer, other than the minimum tender condition, have been satisfied or, to the extent legally permitted, waived, AMEC will cause AMEC International Investments BV to extend the Offer for a single, five Business Day period.

During any extension, any Foster Wheeler shares validly tendered and not properly withdrawn will remain subject to purchase in the Offer, subject to the right of each Foster Wheeler shareholder to withdraw the Foster Wheeler shares that such holder has previously tendered.

Q. How will I know if the Offer is extended?

A. AMEC and/or AMEC International Investments BV will announce any extension of the Offer by issuing a press release including on the Dow Jones News Service and the Regulatory News Service of the LSE, or RNS, by no later than 9:00 a.m. New York City time on the next US Business Day after the previously scheduled expiration date. For purposes of the Offer, a "US Business Day" means any day other than a Saturday, Sunday or US federal holiday and consists of the time period from 12:01 a.m. through 12:00 midnight, New York City time.

In the event that AMEC intends to waive the minimum tender condition down to 662/3 per cent., it will announce such waiver by issuing a press release including on the Dow Jones News Service and the RNS, as promptly as practicable thereafter, and will extend the Offer by 10 US Business Days in a manner consistent with the requirements of the US tender offer rules. Subject to the requirements of the US tender offer rules (including US tender offer rules that require that any material changes to an Offer be promptly disseminated to shareholders in a manner reasonably designed to inform them of such change) and without limiting the manner in which AMEC and/or AMEC International Investments BV may choose to make any public announcement, it will have no obligation to communicate any public announcement other than as described above.

Q. When will I be notified of the results of the Offer?

A. Unless the Offer period is extended, within three US business days after the scheduled expiration date of the Offer, AMEC and/or AMEC International Investments BV will make a public announcement stating whether (i) the conditions to the Offer have been satisfied or waived or (ii) the Offer is terminated, as a result of any of the conditions to the Offer not having been satisfied or waived.

In accordance with the US tender offer rules, any extension of the Offer period will be announced by no later than 9:00 a.m. New York City time on the next US business day after the scheduled expiration

7

date. AMEC and/or AMEC International Investments BV will announce the final results of the Offer, including whether all of the conditions to the Offer have been satisfied or waived and whether AMEC will cause AMEC International Investments BV to accept the tendered Foster Wheeler shares for exchange, as promptly as practicable following the scheduled expiration date of the Offer.

Q. Under what circumstances will there be a subsequent offering period?

A. AMEC and AMEC International Investments BV reserve the right to, or, upon the reasonable request of Foster Wheeler, shall be obligated to, in each case subject to applicable US tender offer rules, provide a "subsequent offering period" following the close of the Offer period, including any extension thereof. A subsequent offering period is an additional period of time during which Foster Wheeler shareholders may tender, but not withdraw, Foster Wheeler shares and receive the Offer consideration. Such subsequent offering period will be for a reasonable period of time, in accordance with Rule 14d-11 of the Exchange Act, as determined by AMEC and AMEC International Investments BV or reasonably requested by Foster Wheeler. If AMEC and AMEC International Investments BV provide a subsequent offering period, they will publicly disclose that a subsequent offering period will occur and that such subsequent offering period will commence immediately after the closing of the Offer. However, there is no assurance that there will be a subsequent offering period, or the length of time of such subsequent offering period, if one is provided.

During any subsequent offering period, AMEC will cause AMEC International Investments BV to accept for exchange and pay for such Foster Wheeler shares tendered promptly, and in any event, within three US business days of such Foster Wheeler shares being tendered.

Q. Will I receive the same consideration if I tender in the subsequent offering period, if any, that I would have received in the initial offering period?

A. Yes, subject to proration. The consideration that Foster Wheeler shareholders will be entitled to receive for any Foster Wheeler shares tendered during any subsequent offering period will be the same as the consideration offered in the initial offering period subject to proration. However, as a result of proration in connection with the tender of Foster Wheeler shares in the initial offering period, the total aggregate amount of cash and the total number of AMEC securities (in the form of AMEC shares or AMEC ADSs, at the election of Foster Wheeler shareholders) available to be paid and issued in the subsequent offering period will be less than in the initial offering period. Foster Wheeler shareholders who tender during any subsequent offering period will have the opportunity to elect to receive cash or AMEC securities (in the form of AMEC shares or AMEC ADSs, at the election of Foster Wheeler shareholders). The calculation of the allocation of rights to receive either cash or share/ADS consideration (as applicable) in the subsequent offering period will occur on each day of the subsequent offering period in the same manner as in the initial offering period, based on a fixed amount of cash to be paid and fixed number of AMEC securities to be issued that will depend on the total number of Foster Wheeler shares tendered on such day. Therefore, the pools of each form of consideration available at the time of payment, in addition to being smaller as a result of the payment of the offer consideration to tendering shareholders during the initial offering period, will be subject to the elections of other Foster Wheeler shareholders on each day of payment during the subsequent offering period.

Q. After I tender my Foster Wheeler shares, may I change my mind and withdraw them?

A. Yes. You may withdraw your Foster Wheeler shares at any time before the expiration of the Offer and at any time after the expiration of the Offer until AMEC International Investments BV accepts the Foster Wheeler shares for exchange. Once AMEC International Investments BV accepts Foster Wheeler shares for exchange pursuant to the Offer, all withdrawal rights will terminate and you will not be able to withdraw any tendered Foster Wheeler shares. During any subsequent offering period, no

8

withdrawal rights will apply to Foster Wheeler shares tendered during such subsequent offering period, in accordance with Rule 14d-7(a)(2) under the Exchange Act.

Q. How do I withdraw previously tendered Foster Wheeler shares?

A. If you tendered Foster Wheeler shares directly to the exchange agent by delivering a letter of transmittal, you may withdraw your Foster Wheeler shares by delivering to the exchange agent a properly completed and duly executed notice of withdrawal, guaranteed by an eligible guarantor institution (if the letter of transmittal required a signature guarantee) before the expiration of the Offer or before AMEC International Investments BV accepts the Foster Wheeler shares for exchange.

If you tendered Foster Wheeler shares by means of the book-entry confirmation facilities of DTC, you may withdraw your Foster Wheeler shares by instructing your financial intermediary through which you hold your Foster Wheeler shares to cause the DTC participant through which your Foster Wheeler shares were tendered to deliver a notice of withdrawal to the exchange agent through the book-entry confirmation facilities of DTC before the expiration of the Offer or before AMEC International Investments BV accepts the Foster Wheeler shares for exchange.

During any subsequent offering period, no withdrawal rights will apply to Foster Wheeler shares tendered during such subsequent offering period, in accordance with Rule 14d-7(a)(2) under the Exchange Act.

See "The Offer—Withdrawal Rights" for more information about the procedures for withdrawing your previously tendered Foster Wheeler shares.

Q. Do I need to do anything if I want to retain my Foster Wheeler shares?

A. No. If you want to retain your Foster Wheeler shares, you do not need to take any action.

Q. If I decide not to tender, what will happen to my Foster Wheeler shares?

A. If you decide not to tender, you will continue to own your Foster Wheeler shares in their current form. However, if the Offer is completed, the number of publicly held Foster Wheeler shares may be so small that there may no longer be an active trading market for Foster Wheeler shares. The absence of an active trading market, and corresponding lack of analyst coverage, could reduce the liquidity and, consequently, the market value of your Foster Wheeler shares. In addition, Foster Wheeler shares may no longer meet the requirements for continued listing and may be delisted from NASDAQ.

In the event that AMEC, through AMEC International Investments BV, acquires control of Foster Wheeler, to the extent permitted under applicable law and stock exchange regulations, it intends to request that Foster Wheeler seek the delisting of the Foster Wheeler shares from NASDAQ. Following delisting of the Foster Wheeler shares from NASDAQ and provided that the criteria for deregistration are met, AMEC intends to cause Foster Wheeler to make a filing with the SEC requesting that Foster Wheeler's reporting obligations under the Exchange Act be terminated. Deregistration would substantially reduce the information required to be furnished by Foster Wheeler to its shareholders and to the SEC and would make certain provisions of the Exchange Act no longer applicable to Foster Wheeler. In addition, if the Foster Wheeler shares are delisted and/or deregistered, they would cease to be "margin securities", which would likely have an adverse impact on the value of your Foster Wheeler shares.

Further, following completion of the Offer, in the event that delisting from NASDAQ does not occur, AMEC may cause Foster Wheeler to take all actions necessary to be treated as a "controlled company", which would mean that Foster Wheeler would be exempt from certain NASDAQ corporate governance requirements.

9

In addition, if, following completion of the Offer, AMEC has acquired or controls at least 90 per cent. of the issued Foster Wheeler voting rights, no actions or proceedings are pending with respect to the exercisability of those voting rights and no other legal impediment to a Squeeze-Out Merger under Swiss law exists, it will, indirectly through a wholly-owned subsidiary, initiate a Squeeze-Out Merger under Swiss law whereby any remaining holders of Foster Wheeler shares would be compensated (in cash or otherwise) as required pursuant to Swiss law. Pursuant to the Swiss Merger Act, the amount or value of such compensation must be adequate, but such amount may be different in form and/or value from the consideration received in the Offer. Upon completion of the Squeeze-Out Merger, all Foster Wheeler shares not owned, directly or indirectly, by AMEC will be cancelled.

For a description of AMEC's plans and proposals for Foster Wheeler, the potential effects of the Offer and the associated risks, see "Plans and Proposals for Foster Wheeler" and "Risk Factors—Risks related to the Offer—The Offer may adversely affect the liquidity and value of non-tendered Foster Wheeler shares".

Q. What is an AMEC ADS?

A. An ADS is a security that allows shareholders in the United States to hold and trade interests in foreign-based companies more easily. ADSs are often evidenced by certificates known as American depositary receipts, or ADRs. Each AMEC ADS represents one AMEC share.

Q. What if I want to hold the AMEC shares in the form of AMEC ADSs?

A. Under the Offer, you may elect to receive AMEC shares or AMEC ADSs as part of the consideration in exchange for your Foster Wheeler shares. AMEC has established an ADS facility in the United States, and AMEC ADSs issued thereunder will be registered with the SEC and AMEC intends to apply for the AMEC ADSs to be listed on the NYSE. AMEC ADSs will commence trading on the NYSE on a conditional "when issued" basis on 2014. "When issued" trading refers to a sale or purchase of a security that is made conditionally because the security has been authorised but not yet issued or delivered. Foster Wheeler shareholders will be able to elect to receive AMEC shares in the form of AMEC ADSs under the terms of the Offer. AMEC ADSs will be issued under the facility operated by Deutsche Bank Trust Company Americas, as depositary for the AMEC ADSs, or the AMEC depositary, at the ratio of one AMEC ADS for every one AMEC share. The rights of holders of AMEC ADSs will be governed by the terms of a deposit agreement among the AMEC depositary, AMEC and the owners and beneficial owners of AMEC ADSs. See "Description of AMEC American Depositary Shares".

You may direct any questions related to the AMEC ADS facility to at .

Q. What are the advantages and disadvantages of receiving AMEC ADSs instead of AMEC shares?

A. Foster Wheeler shareholders may prefer to hold AMEC ADSs instead of AMEC shares for the following reasons: (i) AMEC ADSs will trade on the NYSE, whereas AMEC shares trade on the LSE and do not trade on any US national securities exchange; (ii) you will be able to receive dividends in US dollars whereas holders of AMEC shares are unable to elect to receive dividends in US dollars; (iii) unlike AMEC shares, trading of AMEC ADSs in the United States is not subject to UK stamp tax; and (iv) the settlement cycle in the United States is different from that in the United Kingdom. However, there are certain disadvantages to holding AMEC ADSs instead of AMEC shares. In certain limited circumstances, it may not be possible, for certain reasons outlined in "Description of AMEC American Depositary Shares", for the AMEC depositary to make cash, share or other distributions to holders of AMEC ADSs. In addition, holders of AMEC ADSs will not be entitled to attend AMEC's shareholders' meetings and will only be able to vote by giving timely instructions to the AMEC

10

depositary in advance of the meeting, unless, in each case, a proxy by the AMEC depositary is furnished to them.

Q. If my Foster Wheeler shares are acquired in the Offer, how will my rights as a Foster Wheeler shareholder change?

A. The rights of Foster Wheeler shareholders are governed by Swiss law. If your Foster Wheeler shares are acquired in the Offer, you will become a holder of AMEC securities, either in the form of AMEC shares or AMEC ADSs. Your rights as a holder of AMEC shares will be governed by English law and by AMEC's Articles of Association. Your rights as a holder of AMEC ADSs will be governed by the deposit agreement among the AMEC depositary, AMEC and the owners and beneficial owners of AMEC ADSs. For a discussion of the differences in such rights of holders, see "Comparison of Shareholders' Rights" and "Description of AMEC American Depositary Shares".

Q. Do I have appraisal rights under the Offer with respect to the Foster Wheeler shares?

A. Holders of Foster Wheeler shares are not entitled under Swiss law or otherwise to appraisal rights with respect to the Offer. However, if AMEC has acquired or controls, directly or indirectly, at least 90 per cent. of the issued Foster Wheeler voting rights, no actions or proceedings are pending with respect to the exercisability of those voting rights and no other legal impediment to a Squeeze-Out Merger under Swiss law exists, it will, indirectly through a wholly-owned subsidiary, initiate a Squeeze-Out Merger under Swiss law. In connection with such Squeeze-Out Merger, Foster Wheeler shareholders can exercise appraisal rights under Article 105 of the Swiss Merger Act by filing a suit against the surviving company with the competent Swiss civil court at the corporate seat of the surviving company or of Foster Wheeler. The suit must be filed by non-tendering Foster Wheeler shareholders within two months after the merger has been published in the Swiss Official Gazette of Commerce. Foster Wheeler shareholders who tender all of their shares in the Offer will not be able to file a suit to exercise appraisal rights. If such a suit is filed by non-tendering Foster Wheeler shareholders, the court will determine whether the compensation determined in the Squeeze-Out Merger was inadequate and the amount of compensation due to the relevant shareholder, if any, and such court's determination will benefit remaining non-tendering Foster Wheeler shareholders. The filing of an appraisal suit will not prevent completion of the Squeeze-Out Merger.

If, after completion of the Offer, AMEC, directly or indirectly, has acquired and controls less than 90 per cent. of the issued Foster Wheeler voting rights, it may not be able to unilaterally effect a Squeeze-Out Merger under the Swiss Merger Act immediately following completion of the Offer. However, AMEC may pursue any legally available method to acquire the remaining outstanding Foster Wheeler shares. For a description of these methods, see the section entitled "Plans and Proposals for Foster Wheeler". It is possible that any of these transactions may constitute a "going private" transaction within the meaning of Rule 13e-3 under the US Securities Exchange Act of 1934.

Q. What happens if the Offer is not completed?

A. If the Offer is not completed:

- •

- and you tendered your Foster Wheeler shares by delivering a letter of transmittal, your Foster Wheeler shares will be

returned to you promptly following the announcement that the Offer has not been completed; or

- •

- you tendered your Foster Wheeler shares by book-entry transfer, such Foster Wheeler shares will be credited to an account maintained at the original book-entry transfer facility to which the Foster Wheeler shares were tendered.

11

Under no circumstances shall AMEC or AMEC International Investments BV pay, or otherwise agree to be responsible for the payment of, interest or other fees, expenses or other costs of holders of Foster Wheeler shares if the Offer is not completed.

Q. What percentage of AMEC shares will be owned by the former holders of Foster Wheeler shares after the Offer is completed?

A. If all of the issued and to be issued Foster Wheeler shares on a fully-diluted basis are exchanged pursuant to the Offer, immediately after the completion of the Offer, the former Foster Wheeler shareholders will own approximately 23 per cent. of the enlarged AMEC share capital, and the current AMEC shareholders will own approximately 77 per cent. of the enlarged AMEC share capital.

Q. Will I have to pay any transaction fees or brokerage commissions?

A. You will not have to pay any transaction fees or brokerage commissions if:

- •

- your Foster Wheeler shares are registered in your name and you tender them to the exchange agent; or

- •

- you instruct your financial intermediary to tender your Foster Wheeler shares, subject to the policies of such financial intermediary.

Q. What are the tax consequences if I participate or do not participate in the Offer?

A. For more information on the Swiss, UK and US tax consequences of the Offer, see the "Material Tax Consequences" section of this prospectus. You should consult your own tax adviser on the tax consequences to you of tendering your Foster Wheeler shares in the Offer.

Q. What is the market value of the Foster Wheeler shares as of a recent date?

A. On 2014, the last trading day before commencement of the Offer, the closing price of the Foster Wheeler shares reported on NASDAQ was $ per Foster Wheeler share.

Q. Where can I find more information about AMEC and Foster Wheeler?

A. You can find more information about AMEC and Foster Wheeler by reading this prospectus and from various sources described in the section of this prospectus entitled "Additional Information for Security Holders—Where You Can Find More Information".

Q. Who can answer my questions?

A. If you have any questions about the Offer, or if you need to request additional copies of this prospectus or other documents, you should contact the information agent:

12

The following summary highlights material information contained in this prospectus. It does not contain all of the information that may be important to you. In particular, you should read the documents attached to this prospectus which are made part of this prospectus. This summary and the balance of this prospectus contain forward-looking statements about events that are not certain to occur as described, or at all, and you should not place undue reliance on those statements. Please carefully read the section entitled "Cautionary Statement Regarding Forward-Looking Statements". You are urged to read carefully this entire document (including the annexes) and other documents that are referred to in this prospectus in order to fully understand the transactions contemplated by the Implementation Agreement. See "Additional Information for Security Holders—Where You Can Find More Information". Most items in this summary include a page reference directing you to a more complete description of those items.

The Companies

AMEC International Investments BV (see page 158)

AMEC International Investments BV is a direct wholly-owned subsidiary of AMEC. All outstanding shares of AMEC International Investments BV are owned by AMEC. AMEC International Investments BV's principal executive offices are located at Facility Point, Meander 251, 6825 MC Arnhem, the Netherlands, and its telephone number is +31 (0) 88 2174 111.

AMEC (see page 159)

AMEC is a focused supplier of consultancy, engineering and project management services to its customers in the world's oil and gas, mining, clean energy, environment and infrastructure markets. AMEC provides support for assets such as upstream oil and gas production facilities, mines and nuclear power stations throughout their lifecycle from inception to decommissioning.

AMEC operates in around 40 countries worldwide through three business units: the Americas, Europe and Growth Regions (which includes Africa, the Middle East and Australasia). AMEC's geographical structure is designed to promote collaboration across services and markets and between people, which AMEC believes improves its service offering to customers and enhances its growth opportunities.

AMEC provides the following services by markets:

- •

- Oil & Gas, comprising a broad range of services, including

engineering, project management and asset support to onshore and offshore projects for the conventional oil and gas market, as well as unconventional oil and gas projects, in particular oil sands;

- •

- Mining, comprising consultancy, design, design/supply, and project and

construction management services for mining companies worldwide;

- •

- Clean Energy, comprising engineering, procurement, construction and

decommissioning services for nuclear energy, renewable energy (in the form of wind, solar, biomass and biofuel projects), transmission and distribution, and power; and

- •

- Environment & Infrastructure, or E&I, which offers environmental consulting and other services in the water, transportation/infrastructure, government services and industrial/commercial sectors.

For the year ended 31 December 2013, AMEC employed an average of 28,687 people. AMEC is headquartered at Old Change House, 128 Queen Victoria Street, London EC4V 4BJ, United Kingdom, its registered office is at Booths Park, Chelford Road, Knutsford, Cheshire WA16 8QZ, United Kingdom and its main telephone number is +44 (0) 20 7429 7500. AMEC's internet website is http://www.amec.com. The information provided on AMEC's website is not part of this prospectus and is not incorporated herein by reference.

13

AMEC shares are traded on the LSE under the symbol "AMEC" and the AMEC ADSs will be listed and traded on the NYSE under the symbol " ". AMEC ADSs will be traded on the NYSE on a "when issued" basis, subject to the issuance of AMEC ADSs upon completion of the Offer.

Foster Wheeler (see page 216)

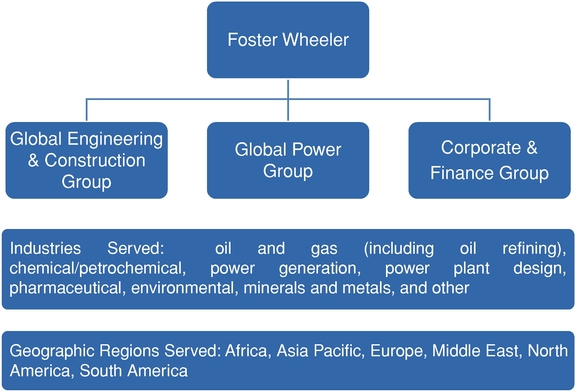

Foster Wheeler is a leading international engineering, construction and project management contractor and power equipment supplier with operations in over 30 countries worldwide.

Foster Wheeler operates through two business groups:

- •

- The Global Engineering and Construction Group, or the Global E&C Group, designs, engineers and constructs onshore and

offshore upstream oil and gas processing facilities, natural gas liquefaction facilities and receiving terminals, gas-to-liquids facilities, oil refining, chemical and petrochemical, pharmaceutical

and biotechnology facilities and related infrastructure, including power generation facilities, distribution facilities, gasification facilities and processing facilities associated with the minerals

and metals sector, and is also involved in the design of facilities in developing market sectors, including carbon capture and storage, solid fuel-fired integrated gasification combined-cycle power

plants, coal-to-liquids, coal-to-chemicals and biofuels.

- •

- The Global Power Group designs, manufactures and installs steam generators and auxiliary equipment for electric power generating stations, district heating and power plants and industrial facilities worldwide and also provides a wide range of aftermarket services.

As at 31 December 2013, Foster Wheeler had 13,311 employees. Foster Wheeler is incorporated under the laws of Switzerland with its registered office in Baar, Canton of Zug, Switzerland. The principal executive office of Foster Wheeler is located at Shinfield Park, Reading, Berkshire RG2 9FW, United Kingdom and its main telephone number is +44 (0) 118 913 1234. Foster Wheeler's internet website is http://www.fwc.com. The information provided on Foster Wheeler's website is not part of this prospectus and is not incorporated herein by reference.

Foster Wheeler shares are traded on NASDAQ under the symbol "FWLT".

Risk Factors (see page 36)

In deciding whether to tender your Foster Wheeler shares, you should carefully consider the risks described under "Risk Factors".

Background to and Reasons for the Offer (see page 76)

AMEC's Reasons for the Transaction (see page 83)

AMEC believes that the Acquisition complements its stated growth strategy and business model, and that the AMEC group as enlarged by the Acquisition, will be well positioned to take advantage of, and create, new growth opportunities. Specifically, by acquiring Foster Wheeler, AMEC expects to be able to strengthen its Oil & Gas business as it believes the Acquisition positions the Enlarged Group to serve the entire Oil & Gas value chain, expand its geographic footprint, particularly in the Growth Regions, where it expects to more than double its revenues, and benefit from a strong profitable power equipment business. AMEC believes that each of these benefits will be underpinned by the combination of AMEC's and Foster Wheeler's customer-oriented, collaborative and skilled workforces and by continued adherence to AMEC's existing low-risk, cash generative business model. AMEC also believes that the Enlarged Group will benefit from annualised cost synergies of at least $75 million per year, and there may be additional tax synergies depending on the ultimate operational and financial structure of the Enlarged Group post-Acquisition.

14

Foster Wheeler's Reasons for the Transaction; Recommendation of Foster Wheeler's Board (see page 90)

In evaluating the Implementation Agreement, the Offer and the other transactions contemplated by the Implementation Agreement, Foster Wheeler's Board consulted with its senior management and its Special Projects Committee, and with Freshfields Bruckhaus Deringer LLP, or Freshfields (its legal adviser), Goldman, Sachs & Co., or Goldman Sachs, and J.P. Morgan Securities LLC, or J.P. Morgan (its financial advisers), and considered a number of factors in recommending by unanimous vote that Foster Wheeler's shareholders accept the Offer and tender their Foster Wheeler shares pursuant to the Offer.

After careful consideration, including a thorough review of the Offer with its Special Projects Committee and its legal and financial advisers, Foster Wheeler's Board unanimously resolved: (i) that the Implementation Agreement and the Offer are in the best interests of Foster Wheeler and fair to Foster Wheeler's shareholders; (ii) to approve the Implementation Agreement in all respects; and (iii) to recommend that Foster Wheeler shareholders accept the Offer.

Opinion of the Financial Advisers to Foster Wheeler's Board (see page 95)

In connection with the Offer, Foster Wheeler's Board received the following opinions from its financial advisers, each described in further detail below under "Background to and Reasons for the Offer—Opinions of Foster Wheeler's Financial Advisers":

- •

- The opinion of Goldman Sachs that, as of the date of such written opinion and based upon and subject to the factors and

assumptions set forth therein, the aggregate consideration to be paid to the shareholders of Foster Wheeler (other than AMEC and its affiliates) in the Offer pursuant to the Implementation Agreement

was fair, from a financial point of view, to such shareholders. The full text of the written opinion of Goldman Sachs, dated 13 February 2014, which sets forth

assumptions made, procedures followed, matters considered and limitations on the review undertaken in connection with the opinion, is attached as Annex A to this prospectus. Goldman Sachs

provided its opinion for the information and assistance of Foster Wheeler's Board in connection with its consideration of the Offer. The Goldman Sachs opinion is not a recommendation as to whether or

not any holder of Foster Wheeler shares should tender such Foster Wheeler shares in the Offer or how any holder of Foster Wheeler shares should vote or make any election in connection with the

transactions contemplated by the Implementation Agreement or any other matter.

- •

- On 13 February 2014, Foster Wheeler's Board received a written opinion, dated 13 February 2014, from J.P. Morgan that, as of such date and based upon and subject to the factors and assumptions set forth in its opinion, the consideration per share and the $0.40 cash dividend, collectively referred to as the total per share payments, to be paid to the holders of Foster Wheeler shares in the proposed Offer and Squeeze-Out Merger was fair, from a financial point of view, to such holders. The full text of the written opinion of J.P. Morgan, dated 13 February 2014, which sets forth, among other things, the assumptions made, procedures followed, matters considered and limitations on the review undertaken by J.P. Morgan in rendering its opinion, is attached as Annex B to this prospectus. Foster Wheeler shareholders are urged to read the opinion in its entirety. J.P. Morgan's written opinion is addressed to Foster Wheeler's Board, is directed only to the fairness from a financial point of view of the total per share payments to be paid to the holders of Foster Wheeler shares in the proposed Offer and Squeeze-Out Merger as of the date of the opinion and does not constitute a recommendation to any Foster Wheeler shareholder as to whether such shareholder should tender its shares into the Offer or how such shareholder should vote with respect to the Offer and Squeeze-Out Merger or any other matter. The summary of the opinion of J.P. Morgan set forth in this prospectus is qualified in its entirety by reference to the full text of such opinion.

15

- •

- At a meeting of Foster Wheeler's Board held on the evening of 12 February 2014, IFBC AG, or IFBC, delivered its oral opinion to the Board, confirmed by delivery of a written opinion, dated 13 February 2014, to the effect that, as of 13 February 2014, and based on and subject to various assumptions, matters considered and limitations described in its written opinion, the aggregate consideration to be received by Foster Wheeler shareholders in the Offer was fair, from a financial point of view, to such holders. IFBC acted as an independent fairness opinion provider and prepared its opinion according to the standards typically applied to fairness opinions in tender offers governed by Swiss takeover law. The full text of the written opinion of IFBC, dated 13 February 2014, is attached as Annex C to this prospectus. IFBC's opinion was provided for the benefit of Foster Wheeler's Board in connection with, and for the purpose of, its evaluation of the consideration to be received by the holders of Foster Wheeler shares to the Offer. The IFBC opinion does not address the relative merits of the Offer as compared to other business strategies or transactions that might be available with respect to Foster Wheeler or Foster Wheeler's underlying business decision to effect the transaction contemplated by the Offer. The IFBC opinion does not constitute a recommendation to any holders of Foster Wheeler shares as to how such holder should vote or act with respect to the Offer or any other matter, including any election a holder of Foster Wheeler shares should make with respect to the consideration to be received in the Offer. Holders of Foster Wheeler shares are encouraged to read this opinion carefully in its entirety. The summary of IFBC's opinion set forth in this prospectus is qualified in its entirety by reference to the full text of its opinion.

Plans and Proposals for Foster Wheeler (see page 121)

If, following completion of the Offer (including any subsequent offering period), AMEC has, directly or indirectly, acquired or controls at least 90 per cent. of the issued Foster Wheeler voting rights, no actions or proceedings are pending with respect to the exercisability of those voting rights and no other legal impediment to a Squeeze-Out Merger under Swiss law exists, it will, indirectly through a wholly-owned Swiss subsidiary, initiate a Squeeze-Out Merger under Swiss law whereby any remaining holders of Foster Wheeler shares would be compensated (in cash or otherwise) as required pursuant to Swiss law. Pursuant to the Swiss Merger Act, the amount or value of such compensation must be adequate, but such amount may be different in form and/or value from the consideration received in the Offer.

AMEC reserves the right to waive the 80 per cent. minimum tender condition down to 662/3 per cent. Therefore, Foster Wheeler shareholders will not know at the time they make their decision to tender their shares the exact percentage of the Foster Wheeler shares AMEC, directly or indirectly, will own after the expiration of the Offer, but they will know that such percentage will be at least 662/3 per cent. of the Foster Wheeler shares.

If the minimum tender condition is satisfied but less than 90 per cent. of the issued Foster Wheeler voting rights are controlled, directly or indirectly, by AMEC after completion of the Offer, it will not be able to unilaterally initiate a Squeeze-Out Merger immediately following completion of the Offer. However, it may use all legally permitted means to obtain the remaining outstanding Foster Wheeler voting rights after the Offer, including engaging in one or more corporate restructuring transactions, such as a contribution of assets, businesses or shareholdings into Foster Wheeler in connection with a capital increase of Foster Wheeler by contribution in kind, whereby the pre-emptive rights of the remaining shareholders would be withdrawn and new Foster Wheeler shares would be issued to AMEC (or its contributing affiliate), or purchases of Foster Wheeler shares from minority Foster Wheeler shareholders. For any such transaction, the form and amount of the consideration to be paid could be different from the consideration offered pursuant to the Offer. It is possible that any of these transactions may be considered a "going private" transaction within the meaning of Rule 13e-3 under the Exchange Act, in which case AMEC would be required to file a Schedule 13E-3 with the SEC that would describe, among other things, the reasons for the "going private" transaction, the relationship of

16

the parties involved, the source(s) of financing and the process used to determine the valuation or price paid to minority shareholders and detailed disclosures as to the fairness of any such transaction to minority shareholders.

AMEC has not yet determined which method or methods it would use to acquire the remaining outstanding Foster Wheeler shares if, after completion of the Offer, it has not acquired or does not control 90 per cent. of the issued Foster Wheeler voting rights. However, in making such a determination, AMEC will consider a number of factors, including the number of Foster Wheeler shares tendered into the Offer, the size and identity of the minority shareholders (including the means legally available in a particular jurisdiction to enable AMEC to acquire all of the outstanding Foster Wheeler shares in that jurisdiction), additional due diligence in respect of Foster Wheeler and any applicable law.

Delisting and Deregistration (see page 128)

If the Offer is consummated, but not all of the Foster Wheeler shares are tendered in the Offer, the shareholders and the number of Foster Wheeler shares held by individual holders will be greatly reduced. In these circumstances, the liquidity of, and market for, those remaining publicly held Foster Wheeler shares could be adversely affected by the lack of active trading market and lack of analyst coverage.

Depending on the number of Foster Wheeler shares that AMEC, through AMEC International Investments BV, acquires in the Offer, AMEC intends to request that Foster Wheeler seek the delisting of the Foster Wheeler shares from NASDAQ. Following delisting of the Foster Wheeler shares from NASDAQ and provided that the criteria for deregistration are met, AMEC intends to cause Foster Wheeler to make a filing with the SEC to request that Foster Wheeler's reporting obligations under the Exchange Act be terminated. This would substantially reduce the information required to be furnished by Foster Wheeler to its shareholders and to the SEC and would make certain provisions of the Exchange Act no longer applicable. In addition, if the Foster Wheeler shares are delisted and/or deregistered, they would cease to be "margin securities", which would likely have an adverse impact on the value of the Foster Wheeler shares.

Following completion of the Offer, in the event that delisting from NASDAQ does not occur, AMEC may cause Foster Wheeler to take all actions necessary to be treated as a "controlled company", which would mean that Foster Wheeler would be exempt from certain NASDAQ corporate governance requirements.

The Offer (see page 130)

AMEC, through AMEC International Investments BV, is offering to acquire all of the Foster Wheeler shares pursuant to an offer to exchange made to all Foster Wheeler shareholders. Foster Wheeler shareholders may elect to receive cash or AMEC securities (in the form of AMEC shares or AMEC ADSs, at the election of the Foster Wheeler shareholder).

Each Foster Wheeler shareholder is entitled to receive $16.00 in cash and 0.8998 AMEC securities (in the form of AMEC shares or AMEC ADSs, at the election of Foster Wheeler shareholders) for each Foster Wheeler share held, which tendering Foster Wheeler shareholders may elect to receive as (i) $32.00 in cash or (ii) 1.7996 in AMEC securities (in the form of AMEC shares or AMEC ADSs, at the election of Foster Wheeler shareholders). The exchange ratio is fixed and will not vary regardless of any fluctuations in the market price of either AMEC securities or Foster Wheeler shares. Therefore, the dollar value of the shares of AMEC securities that holders of Foster Wheeler shares will receive upon completion of the Offer will depend on the market value of AMEC shares and the exchange rate of pounds sterling to US dollars at the time of completion.

17

As a result of the "mix and match" election, the actual amount of cash and the actual number of AMEC securities to be delivered to each Foster Wheeler shareholder who has validly tendered and made a valid election cannot be determined before the end of the Offer period, or the relevant cycle during the subsequent offering period, if any.

Mix and Match Election and Proration (see page 130)

For each Foster Wheeler share, tendering Foster Wheeler shareholders may elect to receive (i) $32.00 in cash or (ii) 1.7996 AMEC securities, which, at the election of Foster Wheeler shareholders, will be issued in the form of AMEC shares or AMEC ADSs. However, since there is a fixed number of AMEC securities and a fixed amount of cash, Foster Wheeler shareholders cannot be certain of receiving the form of consideration that they elect with respect to all of their Foster Wheeler shares. If the elections result in an oversubscription of the pool of cash or AMEC securities available to be paid or issued pursuant to the Offer, certain proration procedures as agreed by the parties in the Implementation Agreement for allocating cash and AMEC securities among tendering Foster Wheeler shareholders will be followed by the exchange agent. The exchange ratio in relation to the securities portion of the Offer consideration is fixed and will not vary, regardless of any fluctuations in the market price of either AMEC securities or Foster Wheeler shares. Therefore, the dollar value of the AMEC securities that holders of Foster Wheeler shares will receive upon completion of the Offer will depend on the market value of AMEC shares and the exchange rate of pounds sterling to US dollars at the time of completion.

Timing of the Offer (see page 131)

The Offer will commence at New York City time ( London time; Zug time) on 2014 and will expire at 11:59 p.m. New York City time ( London time; Zug time) on 2014. If one or more of the conditions to the Offer are not satisfied or, to the extent legally permitted, waived, AMEC will cause AMEC International Investments BV to, in consecutive periods of up to 10 Business Days, extend the period of time for which the Offer is open until all the conditions set forth in "The Offer—Conditions to the Offer" have been satisfied or waived. However, neither AMEC nor AMEC International Investments BV will be required to extend the Offer beyond 31 October 2014, except in limited circumstances, as provided for in the Implementation Agreement.

Following the first date on which all conditions to the Offer, other than the minimum tender condition, have been satisfied or, to the extent legally permitted, waived, AMEC will cause AMEC International Investments BV to extend the Offer for a single, five Business Day period.

Withdrawal Rights (see page 133)

Foster Wheeler shareholders may withdraw their Foster Wheeler shares at any time before the expiration of the Offer and at any time before AMEC International Investments BV accepts Foster Wheeler shares for exchange pursuant to the Offer. During a subsequent offering period, if any, no withdrawal rights will apply to Foster Wheeler shares tendered during such subsequent offering period.

Conditions to the Offer (see page 133)

AMEC's obligation through AMEC International Investments BV to accept for payment or pay for any Foster Wheeler shares tendered pursuant to the Offer is subject to the satisfaction or, to the extent permitted by law, waiver of the following conditions:

- •

- the approval by AMEC shareholders of the Acquisition and any such resolutions as may be required for the purposes of the listing rules of the UK Listing Authority, or UKLA, and as may be required by applicable law or regulation to issue the AMEC securities;

18

- •

- (i) the expiration or termination of any applicable waiting period under the Hart-Scott-Rodino Antitrust Improvements Act

of 1976, or the HSR Act; (ii) the issuance of a decision by the European Commission clearing the Acquisition under the relevant European competition regulations; (iii) the receipt of

antitrust clearance in certain other jurisdictions; and (iv) the receipt of approval from the Committee on Foreign Investment in the United States, or CFIUS;

- •

- the receipt of valid acceptances for at least 80 per cent. of the Foster Wheeler shares by the expiration of the

Offer, referred to as the minimum tender condition, which may be waived down by AMEC to 662/3 per cent.;

- •

- the absence of a material adverse effect on Foster Wheeler;

- •

- the approval by Foster Wheeler shareholders of amendments to the 10 per cent. transfer restriction and the

10 per cent. voting limitation contained in Foster Wheeler's Articles of Association to remove such restriction and limitation with respect to any shareholder who, together with its affiliates,

acquires more than two-thirds of Foster Wheeler's issued and outstanding shares in a successful public tender offer; and either (i) the registration of the approved amendments of Foster

Wheeler's Articles of Association with the competent commercial register; or (ii) the granting of an exception by Foster Wheeler's Board with the agreement of Foster Wheeler and AMEC from the

transfer restrictions and voting limitations in relation to the Foster Wheeler shares acquired by AMEC or its direct wholly-owned subsidiary in the Offer and in the case of either (i) or

(ii) no other transfer restrictions or voting limitations having been introduced or resolved to be introduced in the Articles of Association of Foster Wheeler;

- •

- Foster Wheeler's Board having passed resolutions to register AMEC and its affiliates in the Foster Wheeler share register

as a shareholder with voting rights in respect of all Foster Wheeler shares acquired or to be acquired in the Offer with effect from the closing of the Offer (or, if applicable, to register, or

maintain the registration of, the clearing nominees in the Foster Wheeler share register as shareholders with voting rights in respect of all Foster Wheeler shares such clearing nominees hold on

behalf of AMEC and/or its affiliates with effect from the closing of the Offer), subject to (i) the amendments of Foster Wheeler's Articles of Association being approved by Foster Wheeler's

shareholders and the amendment being registered in the commercial register; (ii) AMEC and/or its affiliates (or, if applicable, the clearing nominees) being exempt from the transfer restriction and