false2023Q1000132611012-31http://fasb.org/us-gaap/2022#FairValueAdjustmentOfWarrantshttp://fasb.org/us-gaap/2022#FairValueAdjustmentOfWarrantsP2YP1Yhttp://fasb.org/us-gaap/2022#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2022#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2022#AccountsPayableAndOtherAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2022#AccountsPayableAndOtherAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2022#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2022#OtherLiabilitiesNoncurrent0000013261102023-01-012023-03-3100013261102023-05-05xbrli:shares00013261102023-03-31iso4217:USD00013261102022-12-310001326110ibrx:PromissoryNotesPayableMember2023-03-310001326110ibrx:PromissoryNotesPayableMember2022-12-310001326110us-gaap:ConvertibleNotesPayableMember2023-03-310001326110us-gaap:ConvertibleNotesPayableMember2022-12-31iso4217:USDxbrli:shares00013261102022-01-012022-03-310001326110us-gaap:CommonStockMember2022-12-310001326110us-gaap:AdditionalPaidInCapitalMember2022-12-310001326110us-gaap:RetainedEarningsMember2022-12-310001326110us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001326110us-gaap:AociIncludingPortionAttributableToNoncontrollingInterestMember2022-12-310001326110us-gaap:NoncontrollingInterestMember2022-12-310001326110us-gaap:PrivatePlacementMember2023-01-012023-03-310001326110us-gaap:CommonStockMemberus-gaap:PrivatePlacementMember2023-01-012023-03-310001326110us-gaap:AdditionalPaidInCapitalMemberus-gaap:PrivatePlacementMember2023-01-012023-03-310001326110us-gaap:PrivatePlacementMemberus-gaap:AociIncludingPortionAttributableToNoncontrollingInterestMember2023-01-012023-03-310001326110us-gaap:AdditionalPaidInCapitalMember2023-01-012023-03-310001326110us-gaap:AociIncludingPortionAttributableToNoncontrollingInterestMember2023-01-012023-03-310001326110us-gaap:CommonStockMember2023-01-012023-03-310001326110us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-03-310001326110us-gaap:RetainedEarningsMember2023-01-012023-03-310001326110us-gaap:NoncontrollingInterestMember2023-01-012023-03-310001326110us-gaap:CommonStockMember2023-03-310001326110us-gaap:AdditionalPaidInCapitalMember2023-03-310001326110us-gaap:RetainedEarningsMember2023-03-310001326110us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-03-310001326110us-gaap:AociIncludingPortionAttributableToNoncontrollingInterestMember2023-03-310001326110us-gaap:NoncontrollingInterestMember2023-03-310001326110us-gaap:CommonStockMember2021-12-310001326110us-gaap:AdditionalPaidInCapitalMember2021-12-310001326110us-gaap:RetainedEarningsMember2021-12-310001326110us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001326110us-gaap:AociIncludingPortionAttributableToNoncontrollingInterestMember2021-12-310001326110us-gaap:NoncontrollingInterestMember2021-12-3100013261102021-12-310001326110us-gaap:AdditionalPaidInCapitalMember2022-01-012022-03-310001326110us-gaap:AociIncludingPortionAttributableToNoncontrollingInterestMember2022-01-012022-03-310001326110us-gaap:CommonStockMember2022-01-012022-03-310001326110us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-03-310001326110us-gaap:RetainedEarningsMember2022-01-012022-03-310001326110us-gaap:NoncontrollingInterestMember2022-01-012022-03-310001326110us-gaap:CommonStockMember2022-03-310001326110us-gaap:AdditionalPaidInCapitalMember2022-03-310001326110us-gaap:RetainedEarningsMember2022-03-310001326110us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-03-310001326110us-gaap:AociIncludingPortionAttributableToNoncontrollingInterestMember2022-03-310001326110us-gaap:NoncontrollingInterestMember2022-03-3100013261102022-03-310001326110ibrx:AtTheMarketOfferingProgramMember2023-03-310001326110ibrx:February2023ShelfRegistrationStatementMember2023-03-310001326110ibrx:RelatedPartyConvertibleNotesMember2023-01-012023-03-310001326110ibrx:RelatedPartyConvertibleNotesMember2022-01-012022-03-310001326110us-gaap:WarrantMember2023-01-012023-03-310001326110us-gaap:WarrantMember2022-01-012022-03-310001326110us-gaap:EmployeeStockOptionMember2023-01-012023-03-310001326110us-gaap:EmployeeStockOptionMember2022-01-012022-03-310001326110us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-03-310001326110us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-03-310001326110ibrx:RelatedPartyWarrantsMember2023-01-012023-03-310001326110ibrx:RelatedPartyWarrantsMember2022-01-012022-03-310001326110us-gaap:ConvertibleNotesPayableMemberibrx:NantCapitalIssued33123Member2023-03-310001326110us-gaap:LeaseholdImprovementsMember2023-03-310001326110us-gaap:LeaseholdImprovementsMember2022-12-310001326110us-gaap:EquipmentMember2023-03-310001326110us-gaap:EquipmentMember2022-12-310001326110us-gaap:ConstructionInProgressMember2023-03-310001326110us-gaap:ConstructionInProgressMember2022-12-310001326110us-gaap:FurnitureAndFixturesMember2023-03-310001326110us-gaap:FurnitureAndFixturesMember2022-12-310001326110us-gaap:SoftwareAndSoftwareDevelopmentCostsMember2023-03-310001326110us-gaap:SoftwareAndSoftwareDevelopmentCostsMember2022-12-310001326110us-gaap:OffMarketFavorableLeaseMember2023-01-012023-03-310001326110us-gaap:OffMarketFavorableLeaseMember2023-03-310001326110us-gaap:OffMarketFavorableLeaseMember2022-01-012022-12-310001326110us-gaap:OffMarketFavorableLeaseMember2022-12-310001326110ibrx:OrganizedWorkforceMember2022-12-310001326110ibrx:CurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2023-01-012023-03-310001326110ibrx:CurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2023-03-310001326110ibrx:CurrentAssetsMemberus-gaap:MutualFundMember2023-03-310001326110ibrx:CurrentAssetsMember2023-03-310001326110ibrx:NoncurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2023-01-012023-03-310001326110ibrx:NoncurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2023-03-310001326110ibrx:CurrentAssetsMemberus-gaap:MutualFundMember2022-12-310001326110ibrx:NoncurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2022-01-012022-12-310001326110ibrx:NoncurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2022-12-31ibrx:Security0001326110us-gaap:MutualFundMember2023-03-310001326110us-gaap:ForeignGovernmentDebtMember2023-03-310001326110us-gaap:MutualFundMember2022-12-310001326110us-gaap:ForeignGovernmentDebtMember2022-12-310001326110us-gaap:EquitySecuritiesMember2023-03-310001326110us-gaap:EquitySecuritiesMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:CashAndCashEquivalentsMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberibrx:CurrentAssetsMemberus-gaap:CashAndCashEquivalentsMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:CashAndCashEquivalentsMember2023-03-310001326110us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:CashAndCashEquivalentsMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:EquitySecuritiesMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberibrx:CurrentAssetsMemberus-gaap:EquitySecuritiesMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:EquitySecuritiesMember2023-03-310001326110us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:EquitySecuritiesMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberibrx:CurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:ForeignGovernmentDebtMember2023-03-310001326110us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:MutualFundMemberibrx:CurrentAssetsMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberus-gaap:MutualFundMemberibrx:CurrentAssetsMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:MutualFundMemberibrx:CurrentAssetsMemberus-gaap:FairValueInputsLevel2Member2023-03-310001326110us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:MutualFundMemberibrx:CurrentAssetsMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:NoncurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberibrx:NoncurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Memberibrx:NoncurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2023-03-310001326110us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberibrx:NoncurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2023-03-310001326110us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:RelatedPartyConvertibleNotesMemberibrx:CurrentLiabilitiesMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberibrx:RelatedPartyConvertibleNotesMemberibrx:CurrentLiabilitiesMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:RelatedPartyConvertibleNotesMemberus-gaap:FairValueInputsLevel2Memberibrx:CurrentLiabilitiesMember2023-03-310001326110us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberibrx:RelatedPartyConvertibleNotesMemberibrx:CurrentLiabilitiesMember2023-03-310001326110ibrx:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentLiabilitiesMember2023-03-310001326110ibrx:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberibrx:CurrentLiabilitiesMember2023-03-310001326110ibrx:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Memberibrx:CurrentLiabilitiesMember2023-03-310001326110ibrx:ContingentConsiderationMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentLiabilitiesMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMemberibrx:NoncurrentLiabilitiesMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMemberibrx:NoncurrentLiabilitiesMemberus-gaap:FairValueInputsLevel1Member2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMemberibrx:NoncurrentLiabilitiesMemberus-gaap:FairValueInputsLevel2Member2023-03-310001326110us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMemberibrx:NoncurrentLiabilitiesMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:CashAndCashEquivalentsMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberibrx:CurrentAssetsMemberus-gaap:CashAndCashEquivalentsMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:CashAndCashEquivalentsMember2022-12-310001326110us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:CashAndCashEquivalentsMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:EquitySecuritiesMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberibrx:CurrentAssetsMemberus-gaap:EquitySecuritiesMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:EquitySecuritiesMember2022-12-310001326110us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:EquitySecuritiesMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:MutualFundMemberibrx:CurrentAssetsMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberus-gaap:MutualFundMemberibrx:CurrentAssetsMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:MutualFundMemberibrx:CurrentAssetsMemberus-gaap:FairValueInputsLevel2Member2022-12-310001326110us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:MutualFundMemberibrx:CurrentAssetsMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:NoncurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberibrx:NoncurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Memberibrx:NoncurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2022-12-310001326110us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberibrx:NoncurrentAssetsMemberus-gaap:ForeignGovernmentDebtMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2022-12-310001326110us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001326110ibrx:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentLiabilitiesMember2022-12-310001326110ibrx:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberibrx:CurrentLiabilitiesMember2022-12-310001326110ibrx:ContingentConsiderationMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Memberibrx:CurrentLiabilitiesMember2022-12-310001326110ibrx:ContingentConsiderationMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentLiabilitiesMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMemberibrx:NoncurrentLiabilitiesMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMemberibrx:NoncurrentLiabilitiesMemberus-gaap:FairValueInputsLevel1Member2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMemberibrx:NoncurrentLiabilitiesMemberus-gaap:FairValueInputsLevel2Member2022-12-310001326110us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMemberibrx:NoncurrentLiabilitiesMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:AgencySecuritiesMemberus-gaap:CashAndCashEquivalentsMember2023-03-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:AgencySecuritiesMemberus-gaap:CashAndCashEquivalentsMember2022-12-310001326110us-gaap:FairValueMeasurementsRecurringMemberibrx:CurrentAssetsMemberus-gaap:CorporateDebtSecuritiesMemberus-gaap:CashAndCashEquivalentsMember2022-12-310001326110us-gaap:ConvertibleNotesPayableMemberibrx:MeasurementInputExpectedMarketYieldMember2023-03-31xbrli:pure0001326110us-gaap:ConvertibleNotesPayableMemberibrx:MeasurementInputDiscountPeriodMember2023-03-31utr:Y0001326110us-gaap:ConvertibleNotesPayableMemberus-gaap:MeasurementInputDiscountRateMember2023-03-310001326110ibrx:December2022WarrantsMemberus-gaap:PrivatePlacementMember2023-03-310001326110ibrx:December2022WarrantsMemberus-gaap:MeasurementInputExercisePriceMember2023-03-310001326110ibrx:December2022WarrantsMemberus-gaap:MeasurementInputExpectedTermMember2023-03-310001326110us-gaap:MeasurementInputPriceVolatilityMemberibrx:December2022WarrantsMember2023-03-310001326110ibrx:December2022WarrantsMemberus-gaap:MeasurementInputExpectedDividendRateMember2023-03-310001326110ibrx:December2022WarrantsMemberus-gaap:MeasurementInputRiskFreeInterestRateMember2023-03-310001326110ibrx:December2022WarrantsMember2022-12-310001326110ibrx:December2022WarrantsMember2023-01-012023-03-310001326110ibrx:December2022WarrantsMember2023-03-310001326110us-gaap:PrivatePlacementMemberibrx:February2023WarrantsMember2023-03-310001326110us-gaap:MeasurementInputExercisePriceMemberibrx:February2023WarrantsMember2023-03-310001326110us-gaap:MeasurementInputExercisePriceMemberibrx:February2023WarrantsMember2023-02-150001326110us-gaap:MeasurementInputExpectedTermMemberibrx:February2023WarrantsMember2023-03-310001326110us-gaap:MeasurementInputExpectedTermMemberibrx:February2023WarrantsMember2023-02-150001326110us-gaap:MeasurementInputPriceVolatilityMemberibrx:February2023WarrantsMember2023-03-310001326110us-gaap:MeasurementInputPriceVolatilityMemberibrx:February2023WarrantsMember2023-02-150001326110us-gaap:MeasurementInputExpectedDividendRateMemberibrx:February2023WarrantsMember2023-03-310001326110us-gaap:MeasurementInputExpectedDividendRateMemberibrx:February2023WarrantsMember2023-02-150001326110us-gaap:MeasurementInputRiskFreeInterestRateMemberibrx:February2023WarrantsMember2023-03-310001326110us-gaap:MeasurementInputRiskFreeInterestRateMemberibrx:February2023WarrantsMember2023-02-150001326110ibrx:February2023WarrantsMember2023-02-150001326110ibrx:February2023WarrantsMember2023-01-012023-03-310001326110ibrx:February2023WarrantsMember2023-03-310001326110ibrx:AmyrisJointVentureMemberibrx:AmyrisIncMember2021-12-310001326110ibrx:AmyrisJointVentureMember2021-12-310001326110ibrx:AmyrisJointVentureMember2022-02-012022-02-280001326110ibrx:AmyrisJointVentureMember2023-03-310001326110ibrx:AmyrisJointVentureMember2023-01-012023-03-310001326110ibrx:AmyrisJointVentureMember2022-01-012022-03-310001326110us-gaap:LicenseAgreementTermsMemberibrx:A3MIPCAndAccessToAdvancedHealthInstituteLicenseAgreementMemberibrx:CollaborativeArrangementAndArrangementOtherThanCollaborativeFeeOneMember2023-01-012023-03-310001326110us-gaap:LicenseAgreementTermsMemberibrx:A3MIPCAndAccessToAdvancedHealthInstituteLicenseAgreementMemberibrx:CollaborativeArrangementAndArrangementOtherThanCollaborativeFeeOneMember2021-11-012021-11-300001326110us-gaap:LicenseAgreementTermsMemberibrx:A3MIPCAndAccessToAdvancedHealthInstituteLicenseAgreementMemberibrx:CollaborativeArrangementAndArrangementOtherThanCollaborativeFeeOneMember2022-06-300001326110ibrx:AccessToAdvancedHealthInstituteAAHIMember2021-05-012021-05-310001326110ibrx:AccessToAdvancedHealthInstituteAAHIMember2022-05-010001326110ibrx:AccessToAdvancedHealthInstituteAAHIMember2023-01-012023-03-310001326110ibrx:AccessToAdvancedHealthInstituteAAHIMemberus-gaap:LicenseAgreementTermsMember2021-09-012021-09-300001326110ibrx:AccessToAdvancedHealthInstituteAAHIMemberus-gaap:LicenseAgreementTermsMemberibrx:CollaborativeArrangementAndArrangementOtherThanCollaborativeFeeOneMember2022-06-300001326110ibrx:AccessToAdvancedHealthInstituteAAHIMemberus-gaap:LicenseAgreementTermsMemberibrx:CollaborativeArrangementAndArrangementOtherThanCollaborativeFeeTrancheTwoMember2023-03-310001326110ibrx:AccessToAdvancedHealthInstituteAAHIMemberus-gaap:LicenseAgreementTermsMember2023-03-310001326110ibrx:AccessToAdvancedHealthInstituteAAHIMemberus-gaap:LicenseAgreementTermsMember2021-09-300001326110ibrx:AccessToAdvancedHealthInstituteAAHIMemberus-gaap:LicenseAgreementTermsMemberibrx:CollaborativeArrangementAndArrangementOtherThanCollaborativeFeeOneMember2023-01-012023-03-310001326110srt:MinimumMemberibrx:AccessToAdvancedHealthInstituteAAHIMemberibrx:SponsoredResearchAgreementMember2023-01-012023-03-310001326110ibrx:AccessToAdvancedHealthInstituteAAHIMemberibrx:SponsoredResearchAgreementMember2023-01-012023-03-310001326110ibrx:DunkirkFacilityMember2022-02-14utr:sqft0001326110ibrx:DunkirkFacilityMember2022-02-142022-02-14ibrx:employee0001326110ibrx:DunkirkFacilityMembersrt:MinimumMemberibrx:StateOfNewYorkMember2023-03-310001326110ibrx:DunkirkFacilityMembersrt:MaximumMemberibrx:StateOfNewYorkMember2023-03-310001326110ibrx:VivaBioCellMember2015-04-300001326110ibrx:VivaBioCellMember2015-04-012015-04-300001326110ibrx:VivaBioCellMember2021-01-012021-12-310001326110ibrx:VivaBioCellMember2022-09-012022-09-300001326110ibrx:VivaBioCellMember2023-01-012023-03-310001326110ibrx:AltorBioScienceCorporationMemberibrx:ContingentValueRightsObligationRegulatoryMilestoneMember2017-12-310001326110ibrx:ContingentValueRightsObligationSalesMilestoneMemberibrx:AltorBioScienceCorporationMember2017-12-310001326110ibrx:ContingentValueRightsObligationSalesMilestoneMemberibrx:AltorBioScienceCorporationMember2017-01-012017-12-310001326110ibrx:DrSoonShiongAndRelatedPartyMemberibrx:ContingentValueRightsObligationSalesMilestoneMemberibrx:AltorBioScienceCorporationMember2023-03-310001326110ibrx:ContingentValueRightsObligationSalesMilestoneMemberibrx:AltorBioScienceCorporationMemberibrx:AltorStockholdersMember2023-03-310001326110ibrx:AltorBioScienceLLCMember2022-03-310001326110us-gaap:PrivatePlacementMember2022-07-090001326110us-gaap:PrivatePlacementMember2022-07-092022-07-090001326110ibrx:AltorBioScienceLLCMember2022-04-300001326110ibrx:AltorBioScienceLLCMember2022-12-082022-12-080001326110ibrx:SorrentoTherapeuticsIncLitigationMemberibrx:NantCellIncMember2022-12-022022-12-020001326110ibrx:SorrentoTherapeuticsIncLitigationMemberibrx:NANTibodyLLCMember2022-12-022022-12-020001326110ibrx:SorrentoTherapeuticsIncLitigationMember2023-02-072023-02-070001326110ibrx:SorrentoTherapeuticsIncLitigationMemberibrx:NantCellIncMember2023-02-072023-02-070001326110srt:MinimumMember2023-03-310001326110srt:MaximumMember2023-03-310001326110ibrx:SecuredOvernightFinancingRateSOFRMemberibrx:NantCapitalIssued33123Member2023-01-012023-03-310001326110us-gaap:ConvertibleNotesPayableMemberibrx:NantCapitalIssued33123Member2023-01-012023-03-310001326110us-gaap:ConvertibleNotesPayableMemberibrx:NantCapitalNantWorksLLCNantCancerStemCellLLCAndNantMobileLLCMember2022-08-310001326110srt:MinimumMemberus-gaap:ConvertibleNotesPayableMemberibrx:NantCapitalNantWorksLLCNantCancerStemCellLLCAndNantMobileLLCMember2022-01-012022-07-310001326110us-gaap:ConvertibleNotesPayableMemberibrx:NantCapitalNantWorksLLCNantCancerStemCellLLCAndNantMobileLLCMembersrt:MaximumMember2022-01-012022-07-310001326110us-gaap:ConvertibleNotesPayableMemberibrx:NantCapitalNantCancerStemCellLLCAndNantMobileLLCMember2023-03-310001326110us-gaap:ConvertibleNotesPayableMemberibrx:NantCapitalNantCancerStemCellLLCAndNantMobileLLCMember2022-12-310001326110us-gaap:ConvertibleNotesPayableMemberibrx:NantCapitalTwoMember2023-01-012023-03-310001326110us-gaap:ConvertibleNotesPayableMemberibrx:NantCapitalTwoMember2022-01-012022-03-310001326110us-gaap:ConvertibleNotesPayableMemberibrx:NantCapitalTwoMember2023-03-310001326110ibrx:PromissoryNotesPayableMemberibrx:NantCapital3Member2023-03-310001326110ibrx:NantCapital3Memberibrx:SecuredOvernightFinancingRateSOFRMember2022-01-012022-12-310001326110ibrx:NantCapital3Member2022-08-312022-08-310001326110ibrx:PromissoryNotesPayableMemberibrx:NantCapital3Member2023-01-012023-03-310001326110ibrx:PromissoryNotesPayableMemberibrx:NantCapital3Member2022-01-012022-03-310001326110ibrx:PromissoryNotesPayableMemberibrx:NantCapital4Member2023-03-310001326110ibrx:NantCapital4Memberibrx:SecuredOvernightFinancingRateSOFRMember2023-01-012023-03-310001326110ibrx:PromissoryNotesPayableMemberibrx:NantCapital4Member2023-01-012023-03-310001326110ibrx:PromissoryNotesPayableMemberibrx:NantCapital6Member2023-03-310001326110ibrx:NantCapital6Memberibrx:SecuredOvernightFinancingRateSOFRMember2023-01-012023-03-310001326110ibrx:PromissoryNotesPayableMemberibrx:NantCapital6Member2023-01-012023-03-310001326110ibrx:NantCapitalMember2023-01-012023-03-310001326110ibrx:NantCapitalMemberus-gaap:ConvertibleNotesPayableMember2023-03-310001326110ibrx:NantCapitalOneMember2023-01-012023-03-310001326110ibrx:NantCapitalOneMemberus-gaap:ConvertibleNotesPayableMember2023-03-310001326110ibrx:NantCapitalTwoMember2023-01-012023-03-310001326110ibrx:NantMobileMember2023-01-012023-03-310001326110ibrx:NantMobileMemberus-gaap:ConvertibleNotesPayableMember2023-03-310001326110ibrx:NCSCMember2023-01-012023-03-310001326110ibrx:NCSCMemberus-gaap:ConvertibleNotesPayableMember2023-03-310001326110ibrx:NantCapital3Member2023-01-012023-03-310001326110ibrx:NantCapitalMember2022-01-012022-12-310001326110ibrx:NantCapitalMemberus-gaap:ConvertibleNotesPayableMember2022-12-310001326110ibrx:NantCapitalOneMember2022-01-012022-12-310001326110ibrx:NantCapitalOneMemberus-gaap:ConvertibleNotesPayableMember2022-12-310001326110ibrx:NantCapitalTwoMember2022-01-012022-12-310001326110us-gaap:ConvertibleNotesPayableMemberibrx:NantCapitalTwoMember2022-12-310001326110ibrx:NantMobileMember2022-01-012022-12-310001326110ibrx:NantMobileMemberus-gaap:ConvertibleNotesPayableMember2022-12-310001326110ibrx:NCSCMember2022-01-012022-12-310001326110ibrx:NCSCMemberus-gaap:ConvertibleNotesPayableMember2022-12-310001326110ibrx:NantCapital3Member2022-01-012022-12-310001326110us-gaap:ConvertibleNotesPayableMemberibrx:RelatedPartyNotesPrincipalMembersrt:AffiliatedEntityMember2023-03-310001326110ibrx:PromissoryNotesPayableMemberibrx:RelatedPartyNotesPrincipalMembersrt:AffiliatedEntityMember2023-03-310001326110ibrx:RelatedPartyNotesInterestMemberus-gaap:ConvertibleNotesPayableMembersrt:AffiliatedEntityMember2023-03-310001326110ibrx:PromissoryNotesPayableMemberibrx:RelatedPartyNotesInterestMembersrt:AffiliatedEntityMember2023-03-310001326110ibrx:RelatedPartyNotesMembersrt:AffiliatedEntityMember2023-03-310001326110ibrx:NantBioIncMember2023-03-310001326110ibrx:NantBioIncMember2022-12-310001326110ibrx:BrinkBiologicsIncMember2023-03-310001326110ibrx:BrinkBiologicsIncMember2022-12-310001326110ibrx:VariousMember2023-03-310001326110ibrx:VariousMember2022-12-310001326110ibrx:DuleyRoadMember2023-03-310001326110ibrx:DuleyRoadMember2022-12-310001326110ibrx:NantWorksMember2023-03-310001326110ibrx:NantWorksMember2022-12-310001326110ibrx:ImmunoOncologyClinicMember2023-03-310001326110ibrx:ImmunoOncologyClinicMember2022-12-310001326110ibrx:NantWorksMemberibrx:SharedServicesAgreementMember2023-01-012023-03-310001326110ibrx:NantWorksMemberibrx:SharedServicesAgreementMember2022-01-012022-03-310001326110ibrx:ReimbursementsMemberibrx:NantWorksMemberibrx:SharedServicesAgreementMember2023-01-012023-03-310001326110ibrx:ReimbursementsMemberibrx:NantWorksMemberibrx:SharedServicesAgreementMember2023-03-310001326110ibrx:ReimbursementsMemberibrx:NantWorksMemberibrx:SharedServicesAgreementMember2022-12-310001326110ibrx:NantWorksMemberibrx:SharedServicesAgreementMember2023-03-310001326110ibrx:NantWorksMemberibrx:SharedServicesAgreementMember2022-12-310001326110ibrx:NantWorksMember2015-12-310001326110ibrx:NantWorksMember2022-01-012022-01-010001326110ibrx:NantWorksMember2022-05-010001326110ibrx:NantWorksMember2022-05-012022-05-010001326110ibrx:NantWorksMemberus-gaap:ResearchAndDevelopmentExpenseMember2023-01-012023-03-310001326110ibrx:NantWorksMemberus-gaap:ResearchAndDevelopmentExpenseMember2022-01-012022-03-310001326110ibrx:ConsiderationForFutureServicesMemberibrx:ImmunoOncologyClinicIncMember2019-01-012019-12-310001326110ibrx:ImmunoOncologyClinicIncMemberus-gaap:ResearchAndDevelopmentExpenseMember2021-01-012021-12-310001326110ibrx:ImmunoOncologyClinicIncMember2023-01-012023-03-310001326110ibrx:ImmunoOncologyClinicIncMember2022-01-012022-03-310001326110ibrx:ImmunoOncologyClinicIncMember2022-12-310001326110ibrx:NCSCMember2018-08-310001326110ibrx:NCSCMember2018-08-012018-08-310001326110ibrx:NCSCMember2022-01-012022-03-310001326110ibrx:NCSCMember2023-03-310001326110ibrx:NCSCMember2022-12-310001326110ibrx:NantBioIncMember2023-03-310001326110ibrx:NantBioIncMember2022-12-310001326110ibrx:SixZeroFiveDougStLLCMember2016-09-300001326110ibrx:SixZeroFiveDougStLLCMember2016-09-012016-09-30ibrx:Term0001326110us-gaap:ResearchAndDevelopmentExpenseMemberibrx:SixZeroFiveDougStLLCMember2023-01-012023-03-310001326110us-gaap:ResearchAndDevelopmentExpenseMemberibrx:SixZeroFiveDougStLLCMember2022-01-012022-03-310001326110ibrx:DuleyRoadLLCMember2017-02-280001326110ibrx:DuleyRoadLLCMember2017-02-012017-02-280001326110ibrx:SeptemberTwentyNineteenLeaseMemberibrx:DuleyRoadLLCMember2019-01-010001326110ibrx:JulyTwentyNineteenLeaseMemberibrx:DuleyRoadLLCMember2019-01-010001326110ibrx:DuleyRoadLLCMember2019-01-012019-01-31ibrx:lease0001326110ibrx:DueToRelatedPartiesMemberibrx:DuleyRoadLLCMember2023-03-310001326110ibrx:DueToRelatedPartiesMemberibrx:DuleyRoadLLCMember2022-12-310001326110ibrx:DuleyRoadLLCMember2023-01-012023-03-310001326110ibrx:DuleyRoadLLCMember2022-01-012022-03-310001326110ibrx:InitialPremisesMemberibrx:SixZeroFiveNashLLCMember2021-01-010001326110ibrx:InitialPremisesMemberibrx:SixZeroFiveNashLLCMember2021-01-012021-01-010001326110ibrx:ExpansionPremisesMemberibrx:SixZeroFiveNashLLCMember2021-04-010001326110ibrx:ExpansionPremisesMemberibrx:SixZeroFiveNashLLCMember2021-04-012021-04-010001326110us-gaap:ResearchAndDevelopmentExpenseMemberibrx:InitialAndExpansionPremisesMemberibrx:SixZeroFiveNashLLCMember2023-01-012023-03-310001326110us-gaap:ResearchAndDevelopmentExpenseMemberibrx:InitialAndExpansionPremisesMemberibrx:SixZeroFiveNashLLCMember2022-01-012022-03-310001326110ibrx:FourTwoZeroNashLLCMember2021-10-010001326110ibrx:FourTwoZeroNashLLCMember2021-10-012021-10-010001326110us-gaap:ResearchAndDevelopmentExpenseMemberibrx:FourTwoZeroNashLLCMember2023-01-012023-03-310001326110us-gaap:ResearchAndDevelopmentExpenseMemberibrx:FourTwoZeroNashLLCMember2022-01-012022-03-310001326110ibrx:A23AlaskaLLCMember2022-05-010001326110ibrx:A23AlaskaLLCMember2022-05-012022-05-010001326110us-gaap:ResearchAndDevelopmentExpenseMemberibrx:A23AlaskaLLCMember2023-01-012023-03-310001326110ibrx:ReimbursementsMemberibrx:NantWorksMemberibrx:SharedServicesAgreementMember2022-01-012022-03-310001326110ibrx:ImmunoOncologyClinicIncMember2023-03-310001326110us-gaap:PrivatePlacementMember2022-12-122022-12-120001326110ibrx:December2022WarrantsMember2022-12-120001326110ibrx:December2022WarrantsMember2022-12-122022-12-120001326110us-gaap:PrivatePlacementMember2022-12-120001326110ibrx:December2022WarrantsMember2022-01-012022-12-310001326110us-gaap:PrivatePlacementMember2023-02-152023-02-150001326110us-gaap:PrivatePlacementMember2023-02-150001326110ibrx:TwoThousandFifteenShareRepurchasePlanMember2022-01-012022-03-310001326110ibrx:TwoThousandFifteenShareRepurchasePlanMember2023-01-012023-03-310001326110ibrx:TwoThousandFifteenShareRepurchasePlanMember2023-03-310001326110ibrx:February2023ShelfRegistrationStatementMember2023-02-280001326110ibrx:February2023ShelfRegistrationStatementMember2023-02-152023-02-150001326110srt:MaximumMemberibrx:AtTheMarketOfferingProgramMember2021-04-302021-04-300001326110us-gaap:PrivatePlacementMember2022-01-012022-12-3100013261102022-12-1200013261102023-02-170001326110ibrx:TwoThousandFifteenEquityIncentivePlanMember2023-03-310001326110us-gaap:StockOptionMember2023-01-012023-03-310001326110us-gaap:StockOptionMember2022-01-012022-03-310001326110us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-03-310001326110us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-03-310001326110us-gaap:ResearchAndDevelopmentExpenseMember2023-01-012023-03-310001326110us-gaap:ResearchAndDevelopmentExpenseMember2022-01-012022-03-310001326110us-gaap:SellingGeneralAndAdministrativeExpensesMember2023-01-012023-03-310001326110us-gaap:SellingGeneralAndAdministrativeExpensesMember2022-01-012022-03-3100013261102022-01-012022-12-310001326110us-gaap:EmployeeStockOptionMember2023-03-310001326110us-gaap:EmployeeStockOptionMember2023-01-012023-03-310001326110us-gaap:EmployeeStockOptionMember2022-01-012022-03-310001326110us-gaap:RestrictedStockUnitsRSUMember2022-12-310001326110us-gaap:RestrictedStockUnitsRSUMember2023-03-310001326110us-gaap:RestrictedStockUnitsRSUMemberibrx:NantWorksMember2021-03-042021-03-040001326110us-gaap:AdditionalPaidInCapitalMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-012023-03-310001326110us-gaap:AdditionalPaidInCapitalMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-012022-03-310001326110ibrx:WarrantsMember2023-03-310001326110country:US2023-01-012023-03-310001326110country:KR2023-01-012023-03-310001326110country:IT2023-01-012023-03-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| | | | | |

| þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2023

or

| | | | | |

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-37507

_____________________________________

IMMUNITYBIO, INC.

(Exact name of registrant as specified in its charter)

_____________________________________

| | | | | |

| Delaware | 43-1979754 |

(State or other jurisdiction of

incorporation or organization) | (I.R.S. Employer

Identification No.) |

| |

3530 John Hopkins Court San Diego, California | 92121 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (844) 696-5235

_____________________________________

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common Stock, par value $0.0001 per share | | IBRX | | The Nasdaq Global Select Market |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

| Large accelerated filer | ¨ | | Accelerated filer | ¨ |

| Non-accelerated filer | þ | | Smaller reporting company | þ |

| | | Emerging growth company | ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The number of shares of the Registrant’s common stock outstanding as of May 5, 2023 was 435,984,529 (excluding 163,800 shares held by a majority owned subsidiary of ours which are treated as treasury shares for accounting purposes).

TABLE OF CONTENTS

PART I—FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS.

ImmunityBio, Inc. and Subsidiaries

Condensed Consolidated Balance Sheets

(in thousands, except share and per share amounts)

| | | | | | | | | | | |

| March 31,

2023 | | December 31,

2022 |

| (Unaudited) | | |

| ASSETS | | | |

| Current assets: | | | |

| Cash and cash equivalents | $ | 88,481 | | | $ | 104,641 | |

| Marketable securities | 2,787 | | | 2,543 | |

| Due from related parties | 1,464 | | | 1,890 | |

| Prepaid expenses and other current assets (including amounts with related parties) | 20,754 | | | 31,503 | |

| Total current assets | 113,486 | | | 140,577 | |

| Marketable securities, noncurrent | 820 | | | 840 | |

| Property, plant and equipment, net | 154,165 | | | 143,659 | |

| | | |

| Intangible assets, net | 19,502 | | | 20,003 | |

| Convertible note receivable | 6,691 | | | 6,629 | |

| Operating lease right-of-use assets, net (including amounts with related parties) | 44,191 | | | 45,788 | |

| Other assets (including amounts with related parties) | 4,545 | | | 4,860 | |

| Total assets | $ | 343,400 | | | $ | 362,356 | |

| LIABILITIES AND STOCKHOLDERS’ DEFICIT | | | |

| Current liabilities: | | | |

| Accounts payable | $ | 33,573 | | | $ | 21,016 | |

| Accrued expenses and other liabilities | 54,118 | | | 41,825 | |

Related-party promissory notes, net of discounts and deferred issuance costs (Note 9) | 441,628 | | | 431,901 | |

Related-party convertible note at fair value (Note 5 and Note 9) | 29,850 | | | — | |

| Due to related parties | 2,932 | | | 3,469 | |

| Operating lease liabilities (including amounts with related parties) | 2,844 | | | 2,650 | |

| Total current liabilities | 564,945 | | | 500,861 | |

| | | |

Related-party convertible notes and accrued interest, net of discount (Note 9) | 245,640 | | | 241,271 | |

| Operating lease liabilities, less current portion (including amounts with related parties) | 46,289 | | | 47,951 | |

| Warrant liabilities | 17,780 | | | 21,636 | |

| | | |

| Other liabilities | 462 | | | 457 | |

| Total liabilities | 875,116 | | | 812,176 | |

Commitments and contingencies (Note 7) | | | |

| Stockholders’ deficit: | | | |

Common stock, $0.0001 par value; 900,000,000 shares authorized as of March 31, 2023 and December 31, 2022, respectively; 435,923,104 and 421,569,115 shares issued and outstanding as of March 31, 2023 and December 31, 2022, respectively; excluding treasury stock, 163,800 shares outstanding as of March 31, 2023 and December 31, 2022, respectively | 43 | | | 42 | |

| Additional paid-in capital | 1,965,838 | | | 1,930,936 | |

| Accumulated deficit | (2,494,831) | | | (2,378,488) | |

| Accumulated other comprehensive (loss) income | (33) | | | 183 | |

| Total ImmunityBio stockholders’ deficit | (528,983) | | | (447,327) | |

| Noncontrolling interests | (2,733) | | | (2,493) | |

| Total stockholders’ deficit | (531,716) | | | (449,820) | |

| Total liabilities and stockholders’ deficit | $ | 343,400 | | | $ | 362,356 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

ImmunityBio, Inc. and Subsidiaries

Condensed Consolidated Statements of Operations

(in thousands, except share and per share amounts)

(Unaudited)

| | | | | | | | | | | | | | | |

| Three Months Ended

March 31, | | |

| 2023 | | 2022 | | | | |

| | | | | | | |

| Revenue | $ | 360 | | | $ | 14 | | | | | |

| Operating expenses: | | | | | | | |

Research and development (including amounts with related parties) | 79,264 | | | 55,378 | | | | | |

Selling, general and administrative (including amounts with related parties) | 32,676 | | | 40,608 | | | | | |

| | | | | | | |

| Total operating expenses | 111,940 | | | 95,986 | | | | | |

| Loss from operations | (111,580) | | | (95,972) | | | | | |

| Other income (expense), net: | | | | | | | |

| Interest and investment income, net | 673 | | | 1,666 | | | | | |

| Interest expense (including amounts with related parties) | (29,816) | | | (8,491) | | | | | |

| Loss on equity method investment | (2,337) | | | (197) | | | | | |

| Change in fair value of warrant liabilities | 27,554 | | — | | | | |

| | | | | | | |

Other expense, net (including amounts

with related parties) | (1,077) | | | (4) | | | | | |

| Total other expense, net | (5,003) | | | (7,026) | | | | | |

| Loss before income taxes and noncontrolling interests | (116,583) | | | (102,998) | | | | | |

| Income tax expense | — | | | — | | | | | |

| Net loss | (116,583) | | | (102,998) | | | | | |

| Net loss attributable to noncontrolling interests, net of tax | (240) | | | (172) | | | | | |

| Net loss attributable to ImmunityBio common stockholders | $ | (116,343) | | | $ | (102,826) | | | | | |

| | | | | | | |

| Net loss per ImmunityBio common share – basic and diluted | $ | (0.27) | | | $ | (0.26) | | | | | |

| | | | | | | |

Weighted-average number of common shares used in computing net loss per share – basic and diluted | 428,381,485 | | | 397,882,441 | | | | | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

ImmunityBio, Inc. and Subsidiaries

Condensed Consolidated Statements of Comprehensive Loss

(in thousands)

(Unaudited)

| | | | | | | | | | | | | | |

| | Three Months Ended

March 31, |

| | | | 2023 | | 2022 |

| | | | | | |

| Net loss | | | | $ | (116,583) | | | $ | (102,998) | |

| Other comprehensive income (loss), net of income taxes: | | | | | | |

| Net unrealized gains (losses) on available-for-sale securities | | | | 4 | | | (310) | |

Reclassification of net realized gains on available-for-sale securities included in net loss | | | | 6 | | | — | |

| Foreign currency translation adjustments | | | | (226) | | | (61) | |

| Total other comprehensive loss | | | | (216) | | | (371) | |

| Comprehensive loss | | | | (116,799) | | | (103,369) | |

| Less: Comprehensive loss attributable to noncontrolling interests | | | | (240) | | | (172) | |

Comprehensive loss attributable to ImmunityBio common stockholders | | | | $ | (116,559) | | | $ | (103,197) | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

ImmunityBio, Inc. and Subsidiaries

Condensed Consolidated Statements of Stockholders’ Deficit

(in thousands, except share amounts)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended March 31, 2023 |

| | Common Stock | | Additional Paid-in Capital | | Accumulated

Deficit | | Accumulated Other Comprehensive Income (Loss) | | Total ImmunityBio Stockholders’ Deficit | | Noncontrolling

Interests | | Total Stockholders’ Deficit |

| Shares | | Amount | | | | | | |

| | | | | | | | | | | | | | | | |

Balance as of December 31, 2022 | | 421,569,115 | | | $ | 42 | | | $ | 1,930,936 | | | $ | (2,378,488) | | | $ | 183 | | | $ | (447,327) | | | $ | (2,493) | | | $ | (449,820) | |

Issuance of shares in a registered direct offering, net of discount and offering costs of $2,046 and value ascribed to associated warrants (Note 11) | | 14,072,615 | | | 1 | | | 24,255 | | | — | | | — | | | 24,256 | | | — | | | 24,256 | |

Stock-based compensation expense | | — | | | — | | | 10,878 | | | — | | | — | | | 10,878 | | | — | | | 10,878 | |

| Exercise of stock options | | 81,037 | | | — | | | 126 | | | — | | | — | | | 126 | | | — | | | 126 | |

Vesting of restricted stock units (RSUs) | | 313,975 | | | — | | | — | | | — | | | — | | | — | | | — | | | — | |

Net share settlement for RSUs vesting | | (113,638) | | | — | | | (357) | | | — | | | — | | | (357) | | | — | | | (357) | |

Other comprehensive (loss) income, net of tax | | — | | | — | | | — | | | — | | | (216) | | | (216) | | | — | | | (216) | |

| Net loss | | — | | | — | | | — | | | (116,343) | | | — | | | (116,343) | | | (240) | | | (116,583) | |

Balance as of March 31, 2023 | | 435,923,104 | | | $ | 43 | | | $ | 1,965,838 | | | $ | (2,494,831) | | | $ | (33) | | | $ | (528,983) | | | $ | (2,733) | | | $ | (531,716) | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

ImmunityBio, Inc. and Subsidiaries

Condensed Consolidated Statements of Stockholders’ Deficit

(in thousands, except share amounts)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended March 31, 2022 |

| | Common Stock | | Additional Paid-in Capital | | Accumulated

Deficit | | Accumulated Other Comprehensive Income (Loss) | | Total ImmunityBio Stockholders’ Deficit | | Noncontrolling

Interests | | Total Stockholders’ Deficit |

| Shares | | Amount | | | | | | |

| | | | | | | | | | | | | | | | |

Balance as of December 31, 2021 | | 397,830,044 | | | $ | 40 | | | $ | 1,719,704 | | | $ | (1,961,921) | | | $ | 4 | | | $ | (242,173) | | | $ | (1,740) | | | $ | (243,913) | |

| Stock-based compensation expense | | — | | | — | | | 10,024 | | | — | | | — | | | 10,024 | | | — | | | 10,024 | |

| Exercise of stock options | | 14,767 | | | — | | | 74 | | | — | | | — | | | 74 | | | — | | | 74 | |

| Vesting of RSUs | | 177,783 | | | — | | | — | | | — | | | — | | | — | | | — | | | — | |

| Net share settlement for RSUs vesting | | (65,832) | | | — | | | (372) | | | — | | | — | | | (372) | | | — | | | (372) | |

| Other comprehensive (loss) income, net of tax | | — | | | — | | | — | | | — | | | (371) | | | (371) | | | — | | | (371) | |

| Net loss | | — | | | — | | | — | | | (102,826) | | | — | | | (102,826) | | | (172) | | | (102,998) | |

Balance as of March 31, 2022 | | 397,956,762 | | | $ | 40 | | | $ | 1,729,430 | | | $ | (2,064,747) | | | $ | (367) | | | $ | (335,644) | | | $ | (1,912) | | | $ | (337,556) | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

ImmunityBio, Inc. and Subsidiaries

Condensed Consolidated Statements of Cash Flows

(in thousands)

(Unaudited)

| | | | | | | | | | | |

| | Three Months Ended

March 31, |

| | 2023 | | 2022 |

| Operating activities: | | | |

| Net loss | $ | (116,583) | | | $ | (102,998) | |

| Adjustments to reconcile net loss to net cash used in operating activities: | | | |

| Stock-based compensation expense | 10,878 | | | 10,024 | |

| Change in fair value of warrant liabilities | (27,554) | | | — | |

| Transaction costs allocated to warrant liabilities | 984 | | | — | |

| Non-cash interest items, net (including amounts with related parties) | 2,505 | | | 3,028 | |

| Amortization of related-party notes discounts | 11,536 | | | 370 | |

| Depreciation and amortization | 4,681 | | | 4,090 | |

| | | |

| Non-cash lease expense related to operating lease right-of-use assets | 1,597 | | | 1,318 | |

| | | |

| | | |

| | | |

| Unrealized (gains) on equity securities | (135) | | | (1,419) | |

| | | |

| | | |

| Other | 111 | | | 1,045 | |

| Changes in operating assets and liabilities: | | | |

| Prepaid expenses and other current assets | 9,689 | | | (218) | |

| Other assets | 295 | | | 101 | |

| Accounts payable | 668 | | | 795 | |

| Accrued expenses and other liabilities | 18,590 | | | 10,891 | |

| Related parties | (61) | | | (1,618) | |

| Operating lease liabilities | (1,511) | | | (339) | |

Net cash used in operating activities | (84,310) | | | (74,930) | |

| Investing activities: | | | |

| Purchases of property, plant and equipment | (8,428) | | | (27,347) | |

| Purchase of intangible assets | — | | | (21,229) | |

| | | |

| Purchases of marketable debt securities, available-for-sale | (158) | | | (34,082) | |

| Maturities of marketable debt securities, available for sale | — | | | 14,345 | |

| Proceeds from sales of marketable debt and equity securities | 102 | | | — | |

| Investment in joint venture – an equity method investment | — | | | (1,000) | |

Net cash used in investing activities | (8,484) | | | (69,313) | |

| Financing activities: | | | |

Proceeds from equity offerings,

net of discounts and issuance costs | 47,288 | | | — | |

| | | |

Proceeds from issuance of related-party convertible promissory notes,

net of issuance costs paid | 29,850 | | | — | |

| Proceeds from exercises of stock options | 126 | | | 74 | |

| | | |

| Net share settlement for RSUs vesting | (357) | | | (372) | |

| Principal payments of finance leases | (19) | | | — | |

| | | |

Net cash provided by (used in) financing activities | 76,888 | | | (298) | |

| Effect of exchange rate changes on cash, cash equivalents, and restricted cash | (254) | | | (175) | |

| Net change in cash, cash equivalents, and restricted cash | (16,160) | | | (144,716) | |

| Cash, cash equivalents, and restricted cash, beginning of period | 104,965 | | | 181,280 | |

| Cash, cash equivalents, and restricted cash, end of period | $ | 88,805 | | | $ | 36,564 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

ImmunityBio, Inc. and Subsidiaries

Condensed Consolidated Statements of Cash Flows (Continued)

(in thousands)

(Unaudited)

| | | | | | | | | | | |

| | Three Months Ended

March 31, |

| | 2023 | | 2022 |

| | | |

| Reconciliation of cash, cash equivalents, and restricted cash, end of period: | | | |

| Cash and cash equivalents | $ | 88,481 | | | $ | 36,385 | |

| Restricted cash | 324 | | | 179 | |

| Cash, cash equivalents, and restricted cash, end of period | $ | 88,805 | | | $ | 36,564 | |

| | | |

| Supplemental disclosure of cash flow information: | | | |

| Cash paid during the period for: | | | |

| Interest | $ | 15,515 | | | $ | 5,036 | |

| Income taxes | — | | | — | |

| | | |

| Supplemental disclosure of non-cash activities: | | | |

| | | |

Initial measurement of warrants issued in connection with the registered direct offering accounted for as liabilities | $ | 23,698 | | | $ | — | |

Property and equipment purchases included in accounts payable, accrued expenses and due to related parties | 19,033 | | | 1,061 | |

| Unpaid offering costs included in accounts payable and accrued expenses | 318 | | | — | |

| | | |

| | | |

| Unrealized gains (losses) on marketable debt securities, net | 10 | | | (310) | |

| Right-of-use assets obtained in exchange for operating lease liabilities | — | | | 911 | |

| | | |

| | | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

ImmunityBio, Inc. and Subsidiaries

Notes to Unaudited Condensed Consolidated Financial Statements

1. Description of Business

In these notes to unaudited condensed consolidated financial statements, the terms “ImmunityBio,” “the company,” “we,” “us,” and “our” refer to ImmunityBio, Inc. and its subsidiaries.

Our Business

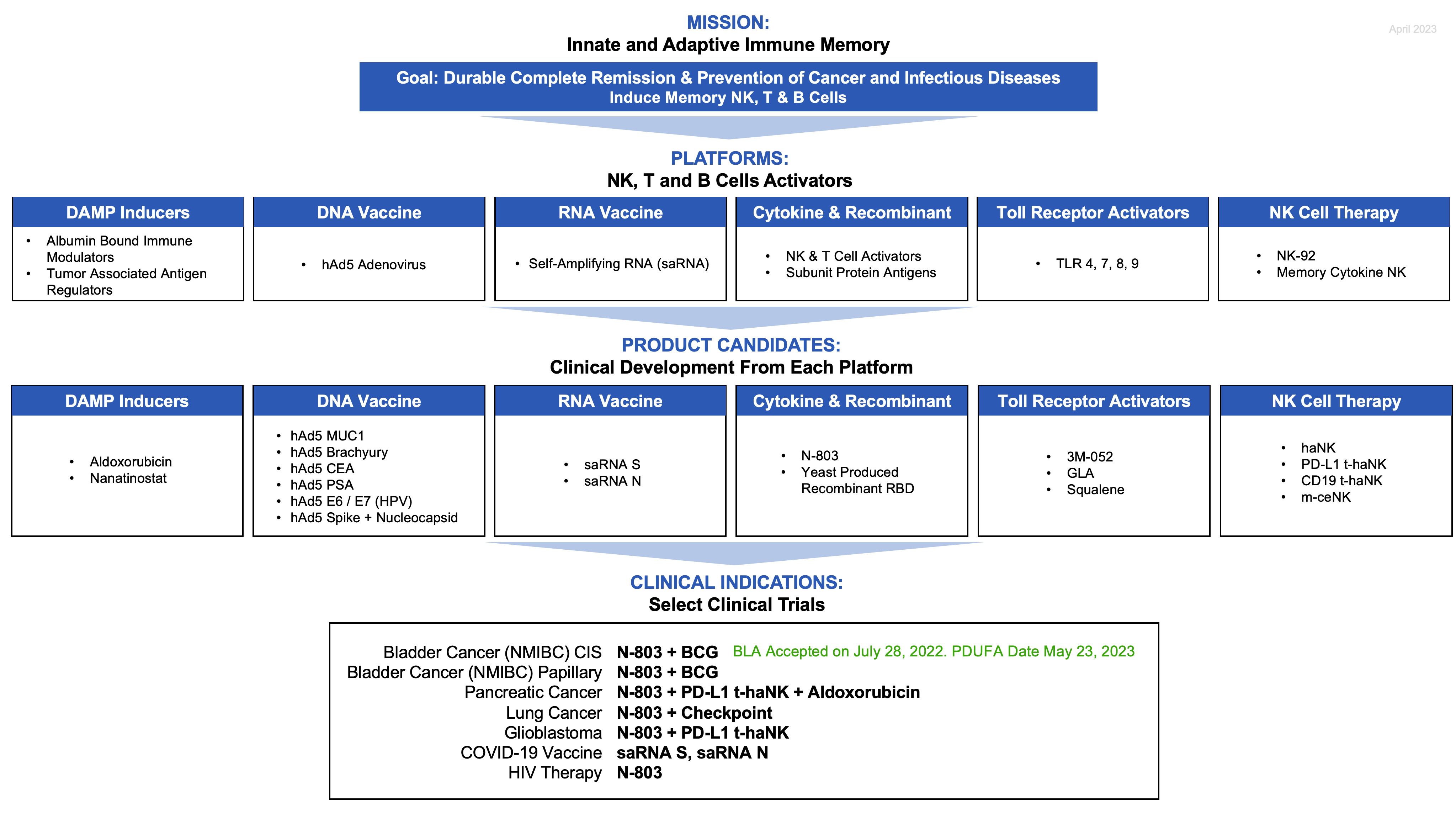

ImmunityBio, Inc. is a clinical-stage biotechnology company developing next-generation therapies and vaccines that complement, harness, and amplify the immune system to defeat cancers and infectious diseases. We strive to be a vertically-integrated immunotherapy company designing and manufacturing our products so they are more effective, accessible, more conveniently stored, and more easily administered to patients.

Our broad immunotherapy and cell therapy platforms are designed to attack cancer and infectious pathogens by activating both the innate immune system—natural killer (NK) cells, dendritic cells, and macrophages—and the adaptive immune system—B cells and T cells—in an orchestrated manner. The goal of this potentially best-in-class approach is to generate immunogenic cell death thereby eliminating rogue cells from the body whether they are cancerous or virally infected. Our ultimate goal is to employ this approach to establish an “immunological memory” that confers long-term benefit for the patient.

Although such designations may not lead to a faster development process or regulatory review and may not increase the likelihood that a product candidate will receive approval, Anktiva™ (N-803), our novel antibody cytokine fusion protein, has received Breakthrough Therapy and Fast Track designations in combination with bacillus Calmette-Guérin (BCG) from the United States (U.S.) Food and Drug Administration (FDA) for BCG-unresponsive non-muscle invasive bladder cancer (NMIBC) with carcinoma in situ (CIS). In May 2022, we announced the submission of a Biologics License Application (BLA) to the FDA for our product candidate, Anktiva in combination with BCG for the treatment of patients with BCG-unresponsive NMIBC with CIS with or without Ta or T1 disease. In July 2022, we announced the FDA had accepted our BLA for review and set a target Prescription Drug User Fee Act (PDUFA) action date of May 23, 2023. On May 9, 2023, the FDA delivered a complete response letter to us regarding the BLA. The company plans to request a meeting with the FDA as soon as possible to address the subject matter of the letter and a response timeline, and plans to diligently address and resolve the issues identified and seek approval as expeditiously as possible. It is unclear when the FDA will approve our BLA, if at all.

Our platforms include 13 novel therapeutic agents either in clinical trials or for which we are developing protocols. We are currently engaged in 15 active clinical trials involving 10 of these agents. Seven of these trials are being sponsored by ImmunityBio while the remaining eight are investigator-led studies. Twelve of these trials are in Phase 2 or 3 development across eleven indications in liquid and solid tumors. These include bladder, pancreatic, and lung cancers, which are among the most frequent and lethal cancer types, and where there are high failure rates for existing standards of care or no available effective treatment. In infectious diseases, our pipeline currently targets such pathogens as the novel strain of the coronavirus (SARS-CoV-2) and human immunodeficiency virus (HIV).

We have established Good Manufacturing Practice (GMP) manufacturing capacity at scale with cutting-edge cell manufacturing expertise and ready-to-scale facilities, as well as extensive and seasoned research and development (R&D), clinical trial, and regulatory operations, and development teams.

2. Summary of Significant Accounting Policies

Basis of Presentation

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (U.S. GAAP) and pursuant to the rules and regulations of the U.S. Securities and Exchange Commission (SEC). The unaudited condensed consolidated financial statements reflect all adjustments which are, in the opinion of management, necessary for a fair presentation of our financial position and results of operations. The unaudited condensed consolidated financial statements do not include all information and notes required by U.S. GAAP for annual reports and therefore should be read in conjunction with our consolidated financial statements and the notes thereto contained in our Annual Report on Form 10-K for the year ended December 31, 2022 filed with the SEC on March 1, 2023. These interim financials are not necessarily indicative of results expected for the full fiscal year.

Principles of Consolidation

The accompanying unaudited condensed consolidated financial statements include the accounts of the company, its wholly-owned subsidiaries, and a variable interest entity (VIE) for which the company is the primary beneficiary. Any material intercompany transactions and balances have been eliminated upon consolidation. For consolidated entities where we have less than 100% of ownership, we record net loss attributable to noncontrolling interest on the unaudited condensed consolidated statements of operations equal to the percentage of the ownership interest retained in such entities by the respective noncontrolling parties.

We assess whether we are the primary beneficiary of a VIE at the inception of the arrangement and at each reporting date. This assessment is based on our power to direct the activities of the VIE that most significantly impact the VIE’s economic performance and our obligation to absorb losses or the right to receive benefits from the VIE that could potentially be significant to the VIE.

Liquidity

As of March 31, 2023, the company had an accumulated deficit of $2.5 billion. We also had negative cash flows from operations of $84.3 million for the three months ended March 31, 2023. The company will likely need additional capital to further fund the development of, and to seek regulatory approvals for, our product candidates, and to begin to commercialize any approved products.

The condensed consolidated financial statements have been prepared assuming the company will continue as a going concern, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business, and do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or amounts and classification of liabilities that may result from the outcome of the uncertainty of our ability to continue as a going concern. As a result of continuing anticipated operating cash outflows, we believe that substantial doubt exists regarding our ability to continue as a going concern without additional funding or financial support. However, we believe our existing cash, cash equivalents, and investments in marketable securities, together with capital to be raised through equity offerings (including but not limited to the offering, issuance and sale by us of our common stock that may be issued and sold under an “at-the-market” sales agreement (the Sale Agreement) with our sales agent (the ATM), of which we had $225.4 million available for future issuance as of March 31, 2023, and a February 2023 shelf registration statement, of which we had $640.0 million available for future offerings as of March 31, 2023), and our potential ability to borrow from affiliated entities, will be sufficient to fund our operations through at least the next 12 months following the issuance date of the condensed consolidated financial statements based primarily upon our Executive Chairman and Global Chief Scientific and Medical Officer’s intent and ability to support our operations with additional funds, including loans from affiliated entities, as required, which we believe alleviates such doubt. See Note 12, Stockholders’ Deficit, for information regarding the ATM and the shelf registration statement. We may also seek to sell additional equity, through one or more follow-on offerings, or in separate financings, or obtain a credit facility. However, we may not be able to secure such external financing in a timely manner or on favorable terms. Without additional funds, we may choose to delay or reduce our operating or investment expenditures. Further, because of the risk and uncertainties associated with the potential commercialization of our product candidates in development, we may need additional funds to meet our needs sooner than planned.

Use of Estimates

The preparation of condensed consolidated financial statements in conformity with U.S. GAAP requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the condensed consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. On an ongoing basis, we evaluate our estimates, including those related to the valuation of equity-based awards, deferred income taxes and related valuation allowances, preclinical and clinical trial accruals, impairment assessments, contingent value right measurement and assessments, the measurement of right-of-use assets and lease liabilities, useful lives of long-lived assets, loss contingencies, fair value calculation of warrants and convertible promissory notes, fair value measurements, and the assessment of our ability to fund our operations for at least the next 12 months from the date of issuance of these condensed consolidated financial statements. We base our estimates on historical experience and on various other market-specific and relevant assumptions that we believe to be reasonable under the circumstances. Estimates are assessed each period and updated to reflect current information, such as the economic considerations related to the impact that the ongoing coronavirus pandemic could have on our significant accounting estimates. Actual results could differ from those estimates.

Significant Accounting Policies

There have been no material changes to our significant accounting policies from those described in Note 2, Summary of Significant Accounting Policies, of the “Notes to Consolidated Financial Statements” that appears in Part II, Item 8. “Financial Statements and Supplementary Data” of our Annual Report on Form 10-K filed with the SEC on March 1, 2023.

Warrants

The company accounts for warrants as either equity-classified or liability-classified instruments based on an assessment of the warrant’s specific terms and applicable authoritative guidance in Accounting Standards Codification (ASC) Topic 480, Distinguishing Liabilities from Equity (ASC 480), and ASC Topic 815, Derivatives and Hedging (ASC 815). The assessment considers whether the warrants are freestanding financial instruments pursuant to ASC 480, meet the definition of a liability pursuant to ASC 480, and whether the warrants meet all of the requirements for equity classification under ASC 815, including whether the warrants are indexed to the company’s own stock and whether the warrant holders could potentially require “net cash settlement” in a circumstance outside of the company’s control, among other conditions for equity classification. This assessment, which requires the use of professional judgment, is conducted at the time of warrant issuance and as of each subsequent quarterly period end date while the warrants are outstanding.

For warrants that meet all criteria for equity classification, the warrants are required to be recorded as a component of additional paid-in capital at the time of issuance. For warrants that do not meet all the criteria for equity classification, the warrants are required to be recorded at their initial fair value on the date of issuance, and on each balance sheet date thereafter. Changes in the estimated fair value of the warrants are recognized as a non-cash change in fair value of warrant liabilities in other income (expense), net, on the condensed consolidated statements of operations. The fair value of the warrants was estimated using the Black-Scholes option pricing model.

Fair Value Option (FVO) Election

The company accounts for certain convertible notes issued during the three months ended March 31, 2023 under the fair value option (FVO) election of ASC 825, Financial Instruments (ASC 825), as discussed below.

The convertible notes accounted for under the FVO election are each debt host financial instruments containing embedded features wherein the entire financial instrument is initially measured at its issue-date estimated fair value and then subsequently remeasured at estimated fair value on a recurring basis at each reporting period date.

Changes in the estimated fair value of the convertible notes are recorded as other income (expense), net on the condensed consolidated statements of operations, except that the change in estimated fair value attributable to a change in the instrument-specific credit risks is recognized as a component of other comprehensive income. Since the underlying financial instrument was issued on March 31, 2023, we did not recognize any change in estimated fair values during the three months ended March 31, 2023.

Basic and Diluted Net Loss per Share of Common Stock

Basic net loss per share is calculated by dividing the net loss attributable to ImmunityBio common stockholders by the weighted-average number of common shares outstanding for the period. Diluted loss per share is computed by dividing net loss attributable to ImmunityBio common stockholders by the weighted-average number of common shares, including the number of additional shares that would have been outstanding if the potential common shares had been issued and if the additional common shares were dilutive.

For all periods presented, potentially dilutive securities are excluded from the computation of fully diluted loss per share as their effect is anti-dilutive. The following table details those securities that have been excluded from the computation of potentially dilutive securities:

| | | | | | | | | | | |

| As of March 31, |

| 2023 | | 2022 |

| (Unaudited) |

| | | |

| Related-party convertible notes (1) | 46,726,407 | | | — | |

| Outstanding third-party warrants | 23,163,524 | | | — | |

| Outstanding stock options | 9,159,665 | | | 8,819,466 | |

| Outstanding RSUs | 6,188,292 | | | 6,149,411 | |

| Outstanding related-party warrants | 1,638,000 | | | 1,638,000 | |

| Total | 86,875,888 | | | 16,606,877 | |

_______________

| | | | | |

| (1) | Amount excludes the shares related to the related-party convertible note with a principal amount of $30.0 million issued on March 31, 2023 as the conversion price has not yet been determined. See Note 9, Related-Party Debt, for further information. |

Recent Accounting Pronouncements

Application of New or Revised Accounting Standards – Not Yet Adopted

In June 2022, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2022-03, Fair Value Measurement (Topic 820): Fair Value Measurement of Equity Securities Subject to Contractual Sale Restrictions, which amends the guidance in Topic 820, Fair Value Measurement, to clarify that a contractual restriction on the sale of an equity security is not considered part of the unit of account of the equity security and, therefore, is not considered in measuring fair value. The amendments also clarify that an entity cannot, as a separate unit of account, recognize and measure a contractual sale restriction. In addition, ASU 2022-03 introduces new disclosure requirements for equity securities subject to contractual sale restrictions that are measured at fair value. ASU 2022-03 is effective for fiscal years beginning after December 15, 2023, including interim periods within those fiscal years. We are currently evaluating the impact of this standard on our condensed consolidated financial statements.

In March 2023, the FASB issued ASU 2023-01, Leases (Topic 842): Common Control Arrangements, which requires that leasehold improvements associated with common control leases be amortized over the useful life of the leasehold improvements to the common control group, regardless of the lease term. ASU 2023-01 is effective for fiscal years beginning after December 15, 2023, including interim periods within those fiscal years. We are currently evaluating the impact of this standard on our condensed consolidated financial statements and related disclosures.

Other recent authoritative guidance issued by the FASB (including technical corrections to the ASC), the American Institute of Certified Public Accountants, and the SEC during the three months ended March 31, 2023 did not, or are not expected to, have a material effect on our condensed consolidated financial statements.

3. Financial Statement Details

Prepaid Expenses and Other Current Assets

Prepaid expenses and other current assets consist of the following (in thousands):

| | | | | | | | | | | |

| March 31,

2023 | | December 31,

2022 |

| (Unaudited) | | |

| | | |

| Prepaid research and development costs | $ | 6,741 | | | $ | 11,704 | |

| Prepaid services | 3,246 | | | 8,013 | |

| Prepaid supplies | 2,160 | | | 2,160 | |

| | | |

| Prepaid insurance | 2,150 | | | 2,282 | |

| Prepaid software license fees | 1,672 | | | 2,195 | |

| Insurance premium financing asset | 357 | | | 1,417 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Other | 4,428 | | | 3,732 | |

| Prepaid expenses and other current assets | $ | 20,754 | | | $ | 31,503 | |

Property, Plant and Equipment, Net

Property, plant and equipment, net, consist of the following (in thousands):

| | | | | | | | | | | |

| March 31,

2023 | | December 31,

2022 |

| (Unaudited) | | |

| | | |

| Leasehold improvements | $ | 73,078 | | | $ | 68,710 | |

| Equipment | 68,973 | | | 67,945 | |

| Construction in progress | 81,941 | | | 72,693 | |

| Furniture & fixtures | 1,931 | | | 1,906 | |

| Software | 1,657 | | | 1,657 | |

| | | |

| Gross property, plant and equipment | 227,580 | | | 212,911 | |

| Less: Accumulated depreciation and amortization | 73,415 | | | 69,252 | |

| Property, plant and equipment, net | $ | 154,165 | | | $ | 143,659 | |

Depreciation expense related to property, plant and equipment totaled $4.2 million and $3.8 million for the three months ended March 31, 2023 and 2022, respectively.

Intangible Assets, Net

The gross carrying amounts and accumulated amortization of intangible assets are as follows at the dates indicated (in thousands):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | March 31, 2023 |

| Weighted-

Average

Life

(in years) | | Gross Carrying

Amount | | Accumulated

Amortization | | Impairment | | Net Carrying

Amount |

| | | | | | | | | |

| Finite-lived: Favorable leasehold rights | 8.9 | | $ | 20,398 | | | $ | (2,295) | | | $ | — | | | $ | 18,103 | |

Indefinite-lived: In-process research and development (IPR&D) | | | 1,399 | | | — | | | — | | | 1,399 | |

| Total intangible assets | | | $ | 21,797 | | | $ | (2,295) | | | $ | — | | | $ | 19,502 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | December 31, 2022 |

| Weighted-

Average

Life

(in years) | | Gross Carrying

Amount | | Accumulated

Amortization | | Impairment | | Net Carrying

Amount |

| | | | | | | | | |

| Finite-lived: Favorable leasehold rights | 9.1 | | $ | 20,398 | | | $ | (1,785) | | | $ | — | | | $ | 18,613 | |

| Finite-lived: Organized workforce | | | 831 | | | (150) | | | (681) | | | — | |

| Total finite-lived intangible assets | | | 21,229 | | | (1,935) | | | (681) | | | 18,613 | |

| Indefinite-lived: IPR&D | | | 1,390 | | | — | | | — | | | 1,390 | |

| Total intangible assets | | | $ | 22,619 | | | $ | (1,935) | | | $ | (681) | | | $ | 20,003 | |

In connection with the acquisition of the Dunkirk facility in 2022, we acquired finite-lived intangibles consisting of favorable leasehold rights and an organized workforce. We recorded amortization expense of our finite-lived intangibles totaling $0.5 million and $0.3 million in research and development expense, on the condensed consolidated statements of operations for the three months ended March 31, 2023 and 2022, respectively.

Future amortization expense associated with our finite-lived intangible assets is as follows (in thousands):

| | | | | | | | |

| Years ending December 31: | | Finite-lived Intangible Assets |

| | |

2023 (excluding the three months ended March 31, 2023) | | $ | 1,530 | |

| 2024 | | 2,040 | |

| 2025 | | 2,040 | |

| 2026 | | 2,040 | |

| 2027 | | 2,040 | |

| Thereafter | | 8,413 | |

| Total | | $ | 18,103 | |

Accrued Expenses and Other Liabilities

Accrued expenses and other liabilities consist of the following (in thousands):

| | | | | | | | | | | |

| March 31,

2023 | | December 31,

2022 |

| (Unaudited) | | |

| | | |

| Accrued research and development costs | $ | 15,916 | | | $ | 1,930 | |

| Accrued bonus | 14,642 | | | 12,068 | |

| Accrued professional and service fees | 9,229 | | | 6,685 | |

| Accrued preclinical and clinical trial costs | 5,523 | | | 4,985 | |

| Accrued compensation | 5,327 | | | 6,040 | |

| | | |

| Accrued construction costs | 2,136 | | | 7,072 | |

| Financing obligation – current portion | 357 | | | 1,417 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Other | 988 | | | 1,628 | |

| Accrued expenses and other liabilities | $ | 54,118 | | | $ | 41,825 | |

Interest and Investment Income, Net

Interest and investment income, net consists of the following (in thousands):

| | | | | | | | | | | | | | | |

| Three Months Ended

March 31, | | |

| 2023 | | 2022 | | | | |

| (Unaudited) | | |

| | | | | | | |

| Unrealized gains from equity securities | $ | 135 | | | $ | 1,419 | | | | | |

| Interest income | 284 | | | 1,296 | | | | | |

| Investment amortization expense, net | 260 | | | (1,049) | | | | | |

| Net realized losses on investments | (6) | | | — | | | | | |

| Interest and investment income, net | $ | 673 | | | $ | 1,666 | | | | | |

Interest income includes interest from marketable securities, convertible notes receivable, other assets, and on bank deposits.

Interest expense

Interest expense consists of the following (in thousands):

| | | | | | | | | | | | | | | |

| Three Months Ended

March 31, | | |

| 2023 | | 2022 | | | | |

| (Unaudited) | | |

| | | | | | | |

| Interest expense on related-party notes | $ | (18,260) | | | $ | (8,101) | | | | | |

| Amortization of related-party notes discounts | (11,536) | | | (370) | | | | | |

| Other interest expense | (20) | | | (20) | | | | | |

| Interest expense | $ | (29,816) | | | $ | (8,491) | | | | | |

4. Financial Instruments

Investments in Marketable Debt Securities

As of March 31, 2023, the weighted-average remaining contractual life, amortized cost, gross unrealized gains, gross unrealized losses and fair value of marketable debt securities, which were considered as available-for-sale, by type of security were as follows (in thousands):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | March 31, 2023 |

| | (Unaudited) |

| Weighted-

Average

Remaining

Contractual Life

(in years) | | Amortized

Cost | | Gross

Unrealized

Gains | | Gross

Unrealized

Losses | | Fair

Value |

| | | | | | | | | |

| Current: | | | | | | | | | |

| | | | | | | | | |

| Foreign bonds | 2.0 | | $ | 107 | | | $ | — | | | $ | — | | | $ | 107 | |

| Mutual funds | | | 39 | | | — | | | (2) | | | 37 | |

| Current portion | | | 146 | | | — | | | (2) | | | 144 | |

| Noncurrent: | | | | | | | | | |

| Foreign bonds | 0.3 | | 902 | | | — | | | (82) | | | 820 | |

| | | | | | | | | |

| Total | | | $ | 1,048 | | | $ | — | | | $ | (84) | | | $ | 964 | |

As of December 31, 2022, the weighted-average remaining contractual life, amortized cost, gross unrealized gains, gross unrealized losses and fair value of marketable debt securities, which were considered as available-for-sale, by type of security were as follows (in thousands):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| December 31, 2022 |

| Weighted-

Average

Remaining

Contractual Life

(in years) | | Amortized

Cost | | Gross

Unrealized

Gains | | Gross

Unrealized

Losses | | Fair

Value |

| | | | | | | | | |

| Current: | | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| Mutual funds | | | $ | 38 | | | $ | — | | | $ | (2) | | | $ | 36 | |

| | | | | | | | | |

| Noncurrent: | | | | | | | | | |

| Foreign bonds | 4.5 | | 932 | | | — | | | (92) | | | 840 | |

| | | | | | | | | |

| Total | | | $ | 970 | | | $ | — | | | $ | (94) | | | $ | 876 | |

At March 31, 2023, 14 of the securities were in an unrealized loss position. Accumulated unrealized losses on marketable debt securities that have been in a continuous loss position for less than 12 months and more than 12 months were as follows (in thousands):

| | | | | | | | | | | | | | | | | | | | | | | |

| March 31, 2023 |

| (Unaudited) |

| Less than 12 months | | More than 12 months |

| Estimated

Fair

Value | | Gross

Unrealized

Losses | | Estimated

Fair

Value | | Gross

Unrealized

Losses |

| | | | | | | |

| | | | | | | |

| Mutual funds | $ | — | | | $ | — | | | $ | 37 | | | $ | (2) | |